sa freight coun.infra bklet2012 sa freight coun.infra bklet06 reports... · port adelaide sa 5015...

TRANSCRIPT

Moving Freight

Version 3

South Australia’sFreight Transport

Infrastructure

November 2012

South Australian Freight Council Inc

Level 1, 296 St Vincent St

Port Adelaide SA 5015

Tel: (08) 8447 0635

Fax: 908) 8447 0606

Email: [email protected]

The South Australian Freight Council Inc(SAFC) is the State’s peak, multi-modal freightand logistics industry group that advises boththe Federal and State governments on industryrelated issues. SAFC represents road, rail, seaand air freight modes and operations, freightservice users, and assists the industry onissues relating to freight logistics across allmodes. SAFC is funded by grants from boththe State and Commonwealth Governments(through the Agency of the State Minister forTransport and Infrastructure and theCommonwealth Minister for Infrastructure andTransport) as well as industry.

1

The South Australian Freight Council (SAFC) believes that an efficient,effective, internationally competitive, multi-modal, state-wide freightsystem is essential in enabling the State to achieve the social andeconomic future it demands. A fundamental objective is the provision of relevant, timely and accessible infrastructure.

Major infrastructure such as ports, airports and key road and railroutes are important to the movement of products and resourcesproduced and consumed in the South Australian economy and haveundergone hundreds of millions of dollars in improvements under public and private regimes. However, whilst evidence exists thataccess is improving, there are still areas for further enhancement.

As an adviser to State and Commonwealth Governments on all aspects of South Australia’sfreight and logistics-related needs, the SAFC’s Moving Freight report aims to provide thedecision-makers of this State with assistance in recognising the importance and priorityneed for efficient, cost effective, and cohesively planned transport infrastructure over thenext 20 plus years.

In the six years since the publication of the previous edition of the SAFC’s Moving Freight:Infrastructure Principles and Project Priorities report, there has been significant improvement to the access and egress to Port Adelaide and some progress on the development of Adelaide’s vital North-South Corridor. However, the North-South corridor has not yet progressed to completion, and a plan for the entire corridor has notyet been released.

This latest edition of Moving Freight is the result of a collaborative effort amongst majorstakeholders in the South Australian transport and logistics community to identify andprioritise the projects that we are confident will create a major positive economic impactfor the state. Moving Freight takes a critical look at some of the more pressing challengesfacing South Australia’s transport industry, including the rapid growth of minerals exploration and its implications for major freight corridors and port facilities. It alsoaddresses potential sources of funding for future transport infrastructure – withoutincreasing the tax burden on an already overburdened industry.

The document does not attempt to quantify the economic, social or environmental benefitsthat particular projects may deliver to the South Australian and national community butdoes allude to the general areas where benefits will accrue. Quantifying the benefits isbeyond the resources of SAFC and is best left to Governments and industry proponents.However, SAFC’s Economic Impact Assessment & Strategic Analysis: South Australia’sTransport and Logistics Industry paper (July 2010) provides a broad overview of socio-economic benefits.

This report is complemented by other freight and logistics policy documents that explorethe myriad of challenges facing our freight transport industry.

As South Australia moves to play an even greater role in the national economy, with ablossoming minerals industry and strong prospects in defence, technology, aquaculture,education and other industries, the time has come for both State and CommonwealthGovernments, and where appropriate the private sector, to increase their investment inthis State’s freight and logistics infrastructure – creating jobs during the constructionphase and longer-term wealth creation and sustainability for businesses and the community.

Tony GrantSouth Australian Freight Council ChairmanNovember 2012

Chairman’s Statement

Executive Summary

2

SAFC members and the South Australian transport and logistics community have identifiedthe projects that they consider to be crucial to lifting South Australia’s transport infrastructure to a level that is comparable and competitive nationally. These projectshave been assessed and prioritised in terms of their adherence to the Core InfrastructureCriteria (page 5), and the contribution that SAFC believes they can make to the achieve-ment of economic, social and environmental objectives. Of the identified projects, four wereconsidered “Urgent”, requiring immediate attention. The top four priority projects are:

1. A free-flowing North-South Corridor ($2.5 billion-$4 billion +), as the backbone of Adelaide’s transport system, was the number one priority in our 2006 paper, and retains this position in 2012 as it remains a critical component of South Australia’s long-term economic prosperity;

2. An accelerated road maintenance program for our State roads to alleviate a maintenance deficit that has exponentially increased from the State Government’s estimate of $160 million in 2003 (not including roads under the care and control of Local Government);

3. Transport infrastructure to support the expanding mining industry, including the development of key deep water ports and road and rail links to service the mining sector across the State; and

4. Addressing “Last Mile” road access issues through critical upgrades and access improvements, and creating more rest facilities on High Productivity Vehicle routes for heavy vehicles across the State ($220 million + over a 20 year period).

In addition, the SAFC also makes the following recommendations:

1. Anticipate the need to expand capacity on key roads leading to and from mines – higher capacity routes able to accommodate high productivity vehicles such as Double and Triple Road Trains, B-Triples, and new innovative road combinations which will be a necessary prerequisite for mine sustainability and will improve environmental and safety outcomes for the community and service providers to these communities. These routes will also be required to handle over-dimensional loads of specialised mining equipment, particularly during their establishment phase;

2. Plan for population growth which will increase the demand for goods and services, and anticipate the impacts of price signalling through road pricing levers and the carbon tax by encouraging the use of larger, and more economical, safer and environmentally friendly heavy vehicles in our community; and

3. Mandate that all Structure Plans adjacent to key freight corridors and facilities incorporate design details for appropriate policies which ensure the free flowing nature of freight corridors and insulates the community against negative environmental outcomes (noise, odour etc.).

SAFC believes that it is now necessary for the State to develop a statewide, integratedmulti-modal Transport Plan to guide transport network and system development.

SAFC also acknowledges that the funding available to Governments for transport infrastructure spending is presently constrained by falling revenues and competingdemands from other sectors (e.g. health and education). In addition, many key transportinfrastructure facilities are increasingly shifting towards private sector control and consequently, the need to invest is now a shared demand and, in some cases, responsibilitywill fall to the private sector alone.

Nonetheless, Governments at all three levels have a responsibility to facilitate investmentin transport infrastructure and to set the appropriate investment environment which encourages private sector involvement where appropriate.

The Organisation for Economic Co-operation and Development (OECD) InternationalFutures Programme recently predicted world Gross Domestic Product (GDP) to growstrongly, possibly double over the period to 2030, meaning air passenger traffic coulddouble in 15 years; air freight could triple in 20 years; and port handling of maritime containers worldwide could quadruple by 20301.

Infrastructure Australia states that between 2010 and 2030 truck traffic is predicted toincrease by 50% and rail freight is expected to jump 90%2.

Moreover, forecasts produced by IBISWorld for Infrastructure Partnerships Australia suggest that the freight task in Australia will increase from 503 billion tonne kilometres in2008 to 1,540 tonne kilometres in 20503.

The provision and maintenance of effective and integrated freight transport infrastructureto meet this challenge is a core responsibility of governments. Achieving a regime thatstrikes the best balance of air, sea, rail and road transport use throughout the State, interstate and overseas remains a fundamental prerequisite for the long-term economicand social viability of South Australia.

Since the South Australian Freight Council released its last Moving Freight: InfrastructurePrinciples and Project Priorities paper in March 2006 much has changed. The global economy has moved into a period of volatility, and Australia has experienced a change inCommonwealth Government – together with a corresponding change in national focusand priorities.

Prices of some commodities have fallen, and ship charter rates for bulk cargo vesselshave only recently begun to recover from unsustainable levels. Vessels were scrappedand aircraft taken out of service as profit margins drastically declined.

Restructuring has also taken place within the intermodal sector, with competition for taskproviding significant benefits to consumers.

Government taxation revenues have dropped against this backdrop of dwindling businessactivity. While the Commonwealth Government increased infrastructure expenditurethrough debt funding, some State governments continue to tighten their spending.

However, a well-performing transport network requires substantial resources to maintainthe quality and condition of the infrastructure, and to meet future needs for expansion.The impacts from any lack of investment are tangible and economic: the construction-costinflation associated with deferred investments can be greater than the borrowing andfinancing costs involved in earlier funding. We should also be mindful that the losses ineconomic and societal benefits are likely to be greater still.

Infrastructure is a smart investment for governments and the community: it is an assetthat increases the productivity of the economy, both now and into the future – making usmore competitive internationally. It also provides a demand for construction, keepingthese businesses (and the businesses that supply them) healthy and providing theiremployees with income that is distributed throughout the economy as they spend.Thirdly, Government taxation revenues expand through company tax, payroll tax, incometax and GST.

While there are ways in which we could better use existing infrastructure (includingreviewing access regimes, traffic light management, and incorporating technologies suchas the Australian Rail Track Corporation Ltd (ARTC) Advanced Train Management Systeminto the supply chain), there is no doubt that measured additional spending on SouthAustralia’s transport infrastructure network during tough economic times will have bothan immediate positive benefit on the economy, and a long-term benefit on our productivity.

1 IBISworld, Road Freight Transport in Australia: Market Research Report. August 2012, accessed 26September 2012, www.ibisworld.com.au<http://www.ibisworld.com.au><http://www.ibisworld.com.au>2 Australasian Transports News, Australasian Transport News Media Kit, 2012-13. Accessed 26 September2012, http://www.fullyloaded.com.au/3 Infrastructure Partnerships Australia, Meeting the 2050 Freight Challenge. 2009. 3

Introduction

Core Principles and Policy Issues:

4

Freight transport underpins the community: Freight infrastructure and the freight transportindustry exist to serve the interests and daily needs of business and the community.

• Freight transport is a derived demand – it arises from the original demand from businesses and the community for specific products and their transport and handling.People demand the product, the freight transport sector moves it to them, and it alsoremoves the by-products and waste of the community and manufacturing.

Core government responsibility and community acceptance: Governments at all threelevels have a core responsibility to ensure the provision and proper maintenance of thetransport infrastructure network to meet the needs of the community and the commercialsector today and for future generations.

• Full funding of the transport infrastructure network, for new projects and maintenance,must be a first-order priority for all governments. Funding may be through government,private sector and/or public private partnerships (PPP), or other funding mechanisms.

• Governments and businesses must raise the community’s awareness and acceptanceof the necessity of the transport infrastructure network to support the community’sneeds. In turn, the community must acknowledge, rather than ignore, the need to allocate substantial government funding for transport infrastructure as a high orderpriority.

Long-term confidence and certainty: Freight infrastructure network planning and development must be managed in a manner that provides the community and the business sector with the necessary certainty and confidence to undertake sound commercialdecisions and the long-term investments required for the State to be nationally and internationally competitive.

• Governments and industry partners must deliver the infrastructure network asplanned, and on time, and the network must perform reliably, to the desired standard,on a consistent and sustainable basis.

• Freight corridors, infrastructure and precincts must not subsequently be encroachedupon or be downgraded by urban sprawl and inappropriate adjacent developments.

Facilitate multi-modal balance: The infrastructure assets, policies and regimes implementedby governments must facilitate genuine and effective modal choice and a sound balance inthe use of the various modes – air, sea, rail and road.

• SAFC represents all freight transport modes and therefore has no underlying preferencefor any given mode. We support the utilisation of the most appropriate mode/s for anygiven freight task and region.

• Governments should not artificially manipulate modal choice, through subsidies or othermeans, as this will likely result in inefficient outcomes, which can only be counter-productive for the economy, society and the environment.

• Where Government does exercise its powers in influencing modal choice, it should onlydo so on a basis that is genuinely commercially sustainable in the medium to long term,in so far as freight rates, services and the infrastructure network are concerned.

• SAFC acknowledges that it is not necessary to make all competitive modes available tocustomers in all instances. There will be situations where the provision of an efficientand effective network for one mode (say rail) will negate the need to upgrade modalalternatives (say road).

Core Infrastructure Criteria

5

Given these principles, the aim must be to ensure that South Australia has a freight transport infrastructure network that meets the following criteria:

• Is efficient and effective; An efficient and effective freight infrastructure network advantages the entire community by reducing costs and increasing economic viabilitythrough:

• Improving the free flow of freight;• Decreasing congestion which, in turn:

– Decreases safety risks, and – Decreases the adverse environmental impacts of fuel and noise

emissions.

• Is fit for the purpose; it is able to accommodate the desired current and future tasksand reliably perform at the levels of safety, efficiency and effectiveness demanded byindustry and the community.

• Facilitates internationally competitive transport outcomes including:– Access – meeting the accessibility requirements of industry, including connectivity;– Accommodating the vehicles, trains, vessels and aircraft that industry requires

now, and in the future, to remain competitive in its markets;– Competitiveness / pricing - freight logistics costs are a significant component of

overall manufacturing and commodity costs and, as such, the marketability of theproducts is very sensitive to increased freight transport costs. Freight transportcosts must be kept to an absolute minimum to avoid any negative impact upon thecompetitiveness of South Australian (and Australian) products in their respectivemarkets;

– Attractiveness to business and potential investors in the State; and– Delivering a competitive advantage to South Australian businesses by being efficient

and effective in international markets.

• Is genuinely multi-modal and provides for efficient modal-interchange.

• Is state-wide and supports connectivity - facilitating seamless intrastate linkages, aswell as to interstate and international markets with appropriate linkages.

• Provides the capacity to meet ongoing and projected freight demands of the communityand the economy;

• Provides the flexibility to facilitate a responsive freight transport system capable ofmeeting emerging needs and trends.

• Optimises the balance between freight transport logistics and appropriate and sustainable environmental and social outcomes.

• Supports economic development so that industry can, as a minimum, compete on a level playing field in its markets.

• Is funded for the life of the project and the asset - both new infrastructure and, importantly, the maintenance of existing infrastructure for its effective working life,must be fully funded.

• Is sustainable in economic, social and environmental terms, as well as for individuals.

6

SA Priority Projects Map

HIGHPrinces Highway duplicationincluding bypass of PortWakefield

URGENTTarcoola-Crystal Brook Rail including Whyalla SpurUrgent/High as volumes warrant

HIGHStuart Highway

URGENTPort Augusta Triangle

MediumSwanport Bridgeduplication

Renmark •

HIGHAdelaide to Melbourne raildoublestack and1800m trains(including double loops)

HIGHSturt Hwy, Port Wakefield to PortAugusta Rd wider shoulders,more passing lanes to accomodate PBS3 vehicles

MEDIUMDukes Highway duplicationTailem Bend Victorian border

MEDIUMYorkey’s Crossing(Add to National NetworkUpgrade as Mines expand)

MEDIUMDuplication of these highways

HIGHRenmark bypass andParinga Bridgereplacement

Myponie Point Area •• Port Spencer

• Swanport Bridge

• Lucky Bay

• Port Bonython

• Port Augusta

URGENTPort Bonython(Port rail and associated facilities)

STATEWIDE PROJECTS n URGENT: Accelerated Road Maintenance, High Productivity Vehicle Access and Facilitation;

n HIGH PRIORITY: Statewide Highway PassingLanes and Shoulder Improvements Program;

n MEDIUM PRIORITY: Rail Intermodal Terminal Development .

HIGHNorthern Connector andNorthern Expressway

HIGHAdelaide Melbourne RailDoublestack and 1,800m trainsincluding passing loops

MEDIUMAddition to National Networkwhen North-South upgradecomplete

MEDIUMOuter ring route Gepps CrossGrade Separation

HIGHAirport connection and Freight Facilities

URGENTPrimary North South CorridorSouth Road

HIGHAdelaide Airport Access

7

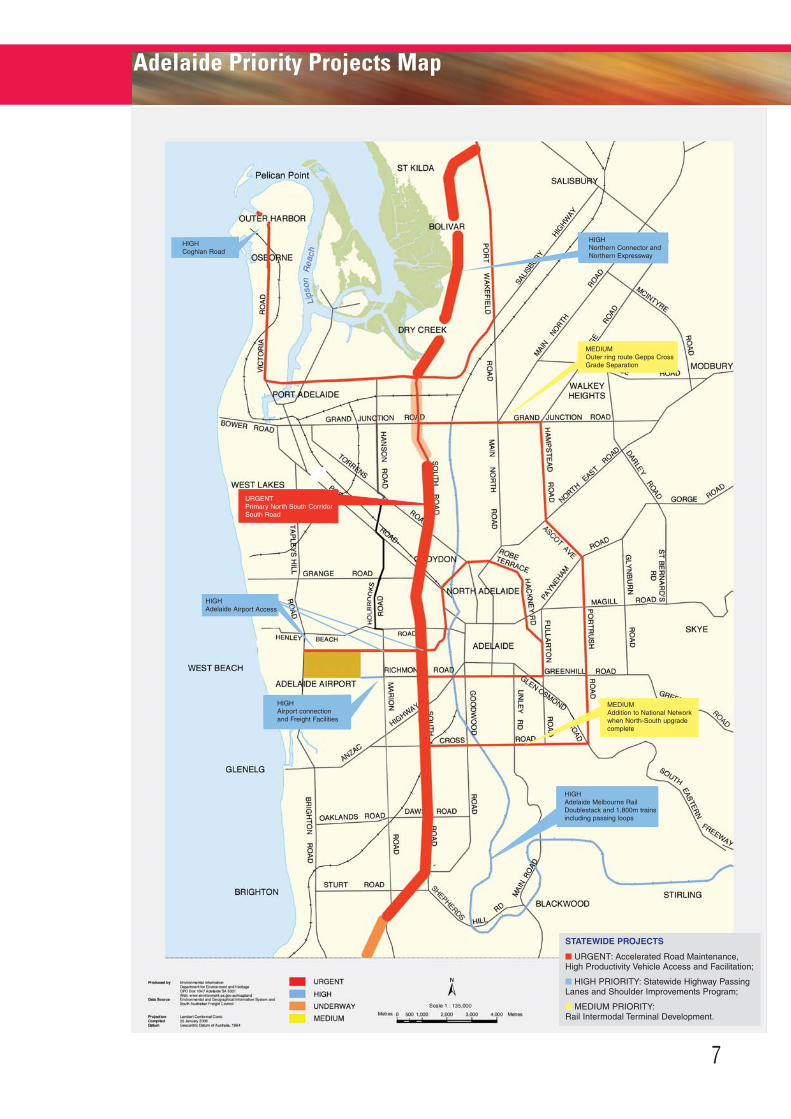

Adelaide Priority Projects Map

HIGHCoghlan Road

STATEWIDE PROJECTS n URGENT: Accelerated Road Maintenance, High Productivity Vehicle Access and Facilitation;

n HIGH PRIORITY: Statewide Highway PassingLanes and Shoulder Improvements Program;

n MEDIUM PRIORITY: Rail Intermodal Terminal Development .

An Introduction to the Four Modes

8

The four modes of transport – road, rail, sea and air4 – play a crucial role in supporting thenational, state and local economies and ultimately, the community as it goes about its dailyactivities.

Each mode plays its part, be that pick-up and delivery to homes, key facilities and manufacturing precincts, haulage from mines to ports and airports for subsequent export,the rapid movement of perishable products to national and international markets, or longhauls between capital cities.

In 2010 in South Australia the Transport and Logistics (T&L) industry had turnover of $8.4 billion, representing 6.9% of Gross State Product, employed 29,000 people (about31,000 Full Time Equivalents- FTE’s), and paid an estimated $355 million of direct taxes(excl. income tax).

This makes the T&L industry 40% larger than the wine industry, 40% bigger than the motorvehicle industry and 70% the size of the agricultural and mining sectors. The economic multiplier effect adds an additional $5.5 billion to the economic impact of the industry5.

Source: Economic Impact Assessment & Strategic Analysis: South Australia’s Transport and LogisticsIndustry, July 2010 (Hudson Howells for SAFC – see http://www.safreightcouncil.com.au/)

RoadRoad transport is an essential element of the Australian transport network. Due toAustralia’s large land area and low population density, Australia relies heavily on roadtransport to move goods across the nation, for pick-up and delivery to intermodal rail terminals, airports and ports, delivery of consumer goods to retail outlets and homes, andthe removal of waste products.

For the 2012/13 Year trucking industry revenue is estimated to be worth $48 billion to theAustralian economy, and employs almost 250,000 staff across 47,000 businesses.

In 2010 in South Australia, the road transport sector had turnover of almost $3.9 billion,including generating $1.7 billion of value add and employed over 19,000 persons (FTE’s).The road sector paid an estimated $180 million in direct taxes7.

SeaShipping represents an industry that makes a massive contribution to the Australian economy, moving the vast majority of the nation’s international imports and exports, aswell as performing a vital role in moving predominantly bulk products around theAustralian coast.

Shipping in Australia carries more than $200 billion worth of cargo in and out of the countryeach year and employs more than 14,000 people either at sea or onshore8;

4 Some companies may consider using slurry pipelines, particularly where high volumes are involved and available transport network capacity may not be able to accommodate it. This document does not consider these potential slurrypipelines, concentrating instead on the four “traditional” modes.5 Economic Impact Assessment & Strategic Analysis: South Australia’s Transport and Logistics Industry, July 2010 (HudsonHowells for SAFC – see http://www.safreightcouncil.com.au/). Incorporates direct employment only and does not includeancillary employment (those working in traditional T&L roles for other industries)6 www.ibisworld.com.au7 Hudson Howells 2010, loc cit8 Stronger Shipping for a Stronger Australia, Speech to the Maritime Industry, Sydney, 9 September 2011, the Hon AnthonyAlbanese, MP, Minister for Infrastructure and Transport, http://www.minister.infrastructure.gov.au/aa/speeches/2011/AS26_2011.aspx

An Introduction to the Four Modes Continued

9

In 2010 in South Australia the ‘water transport’ industry had turnover of almost $145m andemployed an estimated 430 persons9. This does not include turnover or employment oninternational vessels visiting South Australian ports.

RailRail is a significant contributor to Australia’s rural and regional economies, producing economic benefits worth around $7.7 billion each year10. Grain and mineral products aremoved from up-country silos and aggregation points to ports for export, and intermodalservices carrying containers and other freight travel between Australia’s capital cities andkey regional centres on a daily basis.

The volume of freight moved by rail in Australia, measured in billion tonne kilometres hasbeen growing strongly over recent years from around 136.9 billion tonne kilometres in2000-01 to around 198.7 billion tonne kilometres in 2006-07, accounting for around 39% oftotal freight transported in 2006-0711. This represents an average growth rate of around5.8% a year.

In 2010 in South Australia the rail industry (including pipeline and other transport)employed almost 2000 persons with turnover of almost $730 million and growing strongly12.

AviationAir transport enables rapid access to markets and expands links between businesses andcommunities. It is particularly significant for the movement of perishable produce, high-value items, and time sensitive freight. Greater aviation connectivity can increase acountry's international competitiveness and lead to improvements in productivity and economic growth.

Aviation contributes greatly to our economic strength as a nation, including as a majoremployer. The annual gross value added by the air and space industry to the Australianeconomy is nearly $6.3 billion. In August 2009, nearly 50,000 Australians were directlyemployed in the air and space industries, over 80 per cent of them full-time employees13.

In 2010 in South Australia the air and space transport industry employed over 1800 personswith turnover exceeding $758 million14.

9 Hudson Howells 2010, loc cit10 Australasian Rail Association, ‘Careers’. Accessed 26 September 2012, <http://www.ara.net.au/careers>http://www.ara.net.au/careers<http://www.ara.net.au/careers'>11 Deloitte Access Economics for Australasian Railway Association, The True Value of Rail Report, August 2011. p. 21.http://www.ara.net.au12 Hudson Howells 2010, loc cit13The Australian Government, Department of Infrastructure and Transport, National Aviation Policy White Paper, 2009.http://www.infrastructure.gov.au/aviation/nap/14 Hudson Howells 2010, loc cit

Government Transport Policies

10

The Transport and Logistics industry in South Australia deserves attention as a significantprovider of economic activity – it supports a great number of jobs and generates substantial income and wealth for the community. It is therefore important to have effectivepolicies in place to maximise opportunities in the sector.

State transport planning frameworks need to highlight the importance of a strategic infrastructure network. There must be a focus on strategic, multimodal core networks thatare funded for the life of the asset, and are able to handle the major share of the future economic growth and resultant transport and logistics tasks.

The South Australian Government has released a variety of critical policies developed toguide South Australia’s future. These include:

• The South Australian Strategic PlanThe plan reflects the input of communities throughout the State, and their aspirations forhow the State can best continue to grow and prosper by effectively balancing our econom-ic, social and environmental aspirations in a way that improves our overall wellbeing whilealso creating greater opportunities.

• The 30 Year Plan for Greater AdelaideThe 30 Year Plan is a long-term vision for the State, bringing together all the elements thatneed to be planned so that Greater Adelaide continues to be one of the best places to live inthe world. Transport corridors, including the importance of major freight corridors as strategic transport routes, are acknowledged in the document. The 30 Year Plan is one volume of the Planning Strategy, and there are seven other volumes covering regional aresof the State.

• Strategic Transport Routes – Overlay 2 (South Australian Planning Policy Library – Technical Information Sheet 7)

The purpose of the “overlay” is to distinguish between strategic routes (such as key freightroutes) and other transport routes along corridors. Specific policies about protecting thestrategic importance of the road as a strategic transport route have been included.

• The Strategic Infrastructure Plan for South Australia The South Australian Government has commenced a process to update the StrategicInfrastructure Plan for South Australia 2004/5-2014/15 (released in 2005) to map out infrastructure priorities for the next 10 to 15 years. The 2005 Plan provides an overview ofprogress in infrastructure development and the key challenges and opportunities to be con-sidered in future planning for 15 infrastructure sectors, including transport infrastructure. It also identifies the long term strategic directions or priorities to guide decisions on infrastructure planning and development over the next 10 to 15 years andbeyond.

SAFC welcomes the State Government’s announcement that they will develop a StateFreight Strategy and a State Ports Strategy but these have not been released for consulta-tion at this stage.

All of these Strategies sit within a broader national framework that presently incorporatesthe National Transport Policy Framework, a national urban infrastructure policy (Our Cities:Building a productive, sustainable and liveable future), a National Ports Strategy (Nationalports strategy: Infrastructure for an economically, socially, and environmentally sustainablefuture under consideration by the Standing Committee on Transport and Infrastructure(SCOTI)) and a National Land Freight Network Strategy Update. There are also a variety of smaller regional plans (eg: Green Triangle Region Freight ActionPlan) aimed at addressing issues for a specific local area.

The SAFC supports these Plans in principle, and believes these documents to be a usefulfirst step towards providing an environment in which the transport and logistics industry inthis State and nation can plan it’s future, grow and prosper and continue to service the community at large.

Government Transport Policies Continued

11

However, SAFC contends that South Australia would benefit from the development of aState-wide, Integrated Multi-Modal Transport Plan aimed at guiding freight and logisticsnetwork and system development and to highlight emerging opportunities for all industrysectors, including the freight and logistics industry, across the board.

It is anticipated that such a transport plan would address issues currently not addressed inthe various plans listed previously. These issues include:

• An overall assessment of the aggregate impacts that expanding industry sectors (eg:mining, defence industries) will have on the State’s transport infrastructure network andlogistics systems as well as the proposed infrastructure and regulatory adjustments thatwill be necessary to facilitate achievement of the community’s goals for economic development.

• The interaction of various users of the transport network (eg: freight users, cyclists,pedestrians, commuters and the like) and how their sometimes competing needs will beaccommodated.

• The projected population increase forecast within the 30 Year Plan will result in a corresponding increase in economic activity, both in terms of direct employment, as well as in relation to servicing the needs of the community. This expanded populationwill require a well-planned freight network that caters for both industry and the community (including workers) and is efficient and effective, so as to both encourageinvestment that leads to jobs, and to ensure the free flow of consumer goods to anexpanding population that will continue to demand delivery of goods such as food andhousehold items. Of critical importance will be the need to ensure the free flowingmovement of heavy freight vehicles to and from key facilities and between facilities and precincts.

• With the increased dwelling density proposed for some key transit corridors it is imperative that we include the linking transport corridors, both road and rail, into ourstate policy frameworks, including reservation of land for gateway expansion, funding of the new corridors, and increasing capacity on existing corridors when needed. Givencompeting demands and sometimes conflicting uses for our transport networks, it isappropriate for all Structure Plans to incorporate design details for appropriate buffers.This will be a particular issue for the proposed Transit Oriented Developments (TODs),especially where the adjacent transport corridor has a shared and pre-existing freightusage.

• Increased housing density may create difficulties for heavy vehicle access to key centres, as well as delivery vehicle access to private homes. Without a collaborativestrategy issues of access, noise and pollution will be compounded.

• Implied increase in gross state product (GSP) forecast in the State’s various plans andstrategies suggests that there will be productivity improvements across all sectors,including transport and logistics. Consequently plans are needed for expanded access tothe transport network by larger vehicle combinations, especially B-Doubles, B-Triples and Double Road Trains, as well as other innovative vehicles gaining access tothe network through the Performance Based Standards (PBS) process.

South Australia’s future is bright but we will need to be proactive and have access to a suitable transport infrastructure network if we are to achieve our goals for economic, environmental and social development.

Project Priority #1: The North-South Corridor

12

The North-South Corridor is currently defined by the State Government as the 78kmstretch of road running between Gawler and Old Noarlunga15. This incorporates theNorthern Expressway, proposed Northern Connector, South Road and SouthernExpressway.

Hemmed in by the ocean to the west and the Mount Lofty Ranges to the east, Adelaidehas always been a north-south oriented city. The primary port, the airport and major railterminals are concentrated in the central-west area, with major industrial and employmentareas located throughout the metropolitan area, all feeding onto the North-South corridor.

The net effect of Adelaide’s geographical limitations is a large volume of road vehiclesrequiring north-south transport movements – whether travelling to and from work, toexport ports and airports, or for other commercial, private and recreational reasons.

Each segment of the North-South Corridor along South Road handles between 22,700 and72,50016 vehicle movements each day, with key intersections handling higher volumes due to cross traffic and turning vehicles. It should be noted that east-west transport is also enhanced by grade separated, north-south oriented cross routes, reducinglong waiting periods at intersections. This route is currently close to capacity.

Since the 2006 edition of Moving Freight, the Commonwealth Government has includedthe full length of the North-South Corridor (to Darlington) on the national network, andhas allocated $940 million for projects.

These funds have now been spent or committed on projects such as the NorthernExpressway, South Road Superway and planning for the section between Regency Roadand Gallipoli Underpass. Funding allocations however remain inadequate for a full routeupgrade.

The State Government funded grade separation at ANZAC Highway (Gallipoli Underpass)and the Glenelg Tram Overpass project have been completed, and the current constructionof the jointly funded South Road Superway elevated road bridge has been welcomeprogress on this corridor.

However, the absence of an integrated corridor plan sees elements such as at-gradepedestrian crossings delaying traffic and negating the good work undertaken to date.

Construction of the proposed tunnel under Port Road, Grange Road and the Outer Harbortrain line has not commenced, and the much touted widening of South Road betweenPort Road and Torrens Road has not progressed, although they form part of the currentplanning study for the corridor.

Construction of the $445m Southern Expressway Duplication project has commenced but,while the project is significant for various communities, it is of relatively minor significanceto the freight industry. A plan for the Darlington Precinct was released in 2010 but has notprogressed to the construction phase and compounds the Darlington bottle-neck.

15 The Government of South Australia, Department of Planning, Transport and Infrastructure, Adelaide’sNorth-South Corridor. Accessed 30 July 2012, http://www.infrastructure.sa.gov.au/south_road_upgrade16 The Government of South Australia, Department of Planning, Transport and Infrastructure, Annual AverageDaily Traffic Estimates: 24 hour two-way traffic flows. Accessed 30 July, 2012.http://www.transport.sa.gov.au/transport_network/facts_figures/traffic_pdfs/aadt_mt11_colour.pdf

Project Priority #1: The North-South Corridor Continued

13

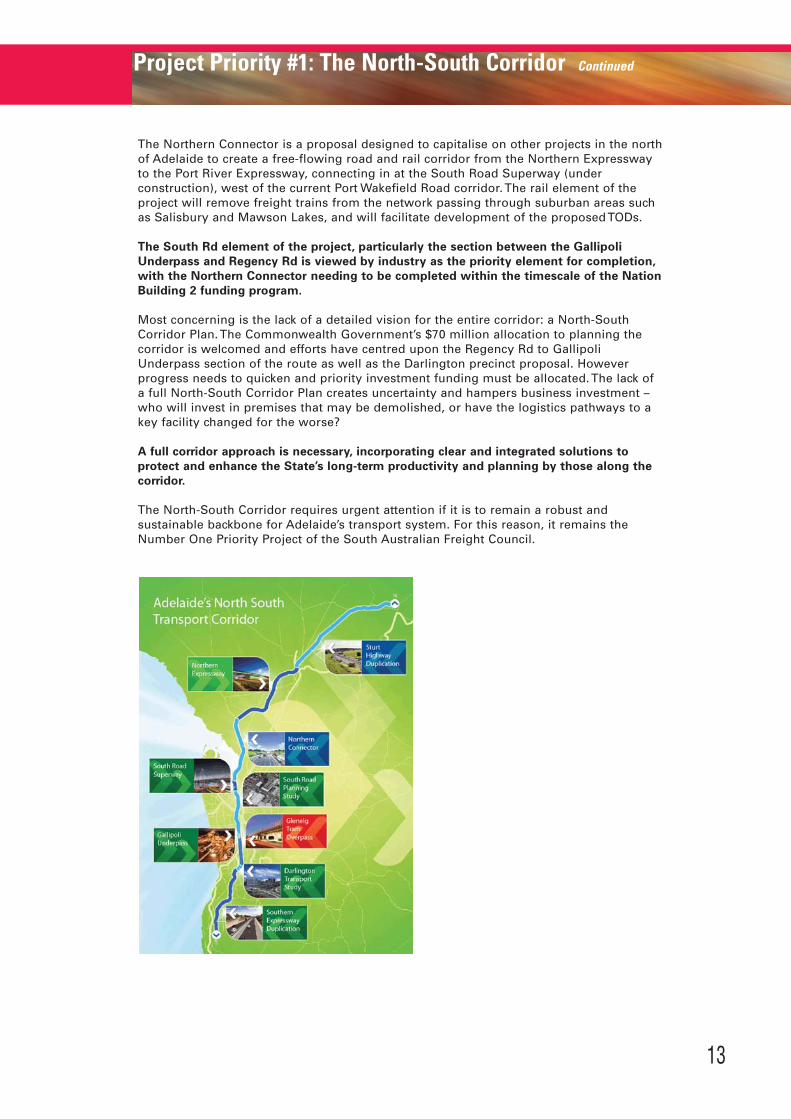

The Northern Connector is a proposal designed to capitalise on other projects in the northof Adelaide to create a free-flowing road and rail corridor from the Northern Expresswayto the Port River Expressway, connecting in at the South Road Superway (under construction), west of the current Port Wakefield Road corridor. The rail element of theproject will remove freight trains from the network passing through suburban areas suchas Salisbury and Mawson Lakes, and will facilitate development of the proposed TODs.

The South Rd element of the project, particularly the section between the GallipoliUnderpass and Regency Rd is viewed by industry as the priority element for completion,with the Northern Connector needing to be completed within the timescale of the NationBuilding 2 funding program.

Most concerning is the lack of a detailed vision for the entire corridor: a North-SouthCorridor Plan. The Commonwealth Government’s $70 million allocation to planning thecorridor is welcomed and efforts have centred upon the Regency Rd to GallipoliUnderpass section of the route as well as the Darlington precinct proposal. Howeverprogress needs to quicken and priority investment funding must be allocated. The lack ofa full North-South Corridor Plan creates uncertainty and hampers business investment –who will invest in premises that may be demolished, or have the logistics pathways to akey facility changed for the worse?

A full corridor approach is necessary, incorporating clear and integrated solutions to protect and enhance the State’s long-term productivity and planning by those along thecorridor.

The North-South Corridor requires urgent attention if it is to remain a robust and sustainable backbone for Adelaide’s transport system. For this reason, it remains theNumber One Priority Project of the South Australian Freight Council.

Project Priority #2: Accelerated Maintenance

14

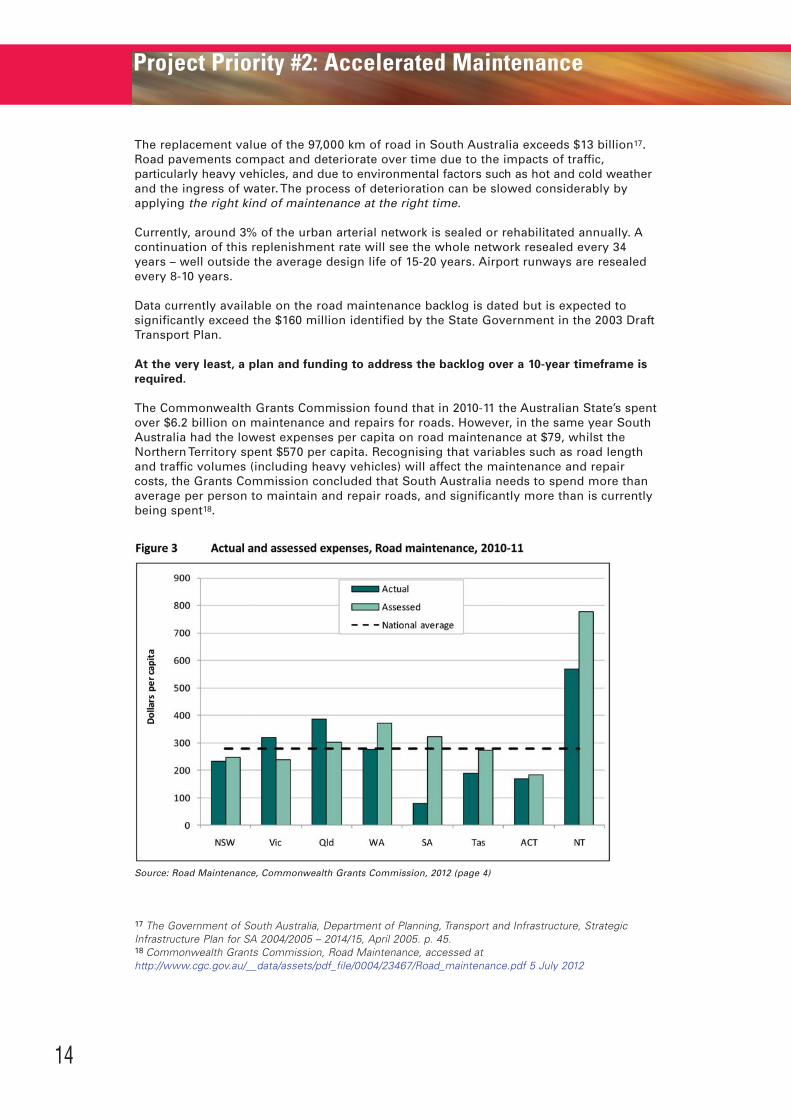

The replacement value of the 97,000 km of road in South Australia exceeds $13 billion17.Road pavements compact and deteriorate over time due to the impacts of traffic, particularly heavy vehicles, and due to environmental factors such as hot and cold weatherand the ingress of water. The process of deterioration can be slowed considerably byapplying the right kind of maintenance at the right time.

Currently, around 3% of the urban arterial network is sealed or rehabilitated annually. Acontinuation of this replenishment rate will see the whole network resealed every 34years – well outside the average design life of 15-20 years. Airport runways are resealedevery 8-10 years.

Data currently available on the road maintenance backlog is dated but is expected to significantly exceed the $160 million identified by the State Government in the 2003 DraftTransport Plan.

At the very least, a plan and funding to address the backlog over a 10-year timeframe isrequired.

The Commonwealth Grants Commission found that in 2010-11 the Australian State’s spentover $6.2 billion on maintenance and repairs for roads. However, in the same year SouthAustralia had the lowest expenses per capita on road maintenance at $79, whilst theNorthern Territory spent $570 per capita. Recognising that variables such as road lengthand traffic volumes (including heavy vehicles) will affect the maintenance and repaircosts, the Grants Commission concluded that South Australia needs to spend more thanaverage per person to maintain and repair roads, and significantly more than is currentlybeing spent18.

Source: Road Maintenance, Commonwealth Grants Commission, 2012 (page 4)

17 The Government of South Australia, Department of Planning, Transport and Infrastructure, StrategicInfrastructure Plan for SA 2004/2005 – 2014/15, April 2005. p. 45.18 Commonwealth Grants Commission, Road Maintenance, accessed athttp://www.cgc.gov.au/__data/assets/pdf_file/0004/23467/Road_maintenance.pdf 5 July 2012

Project Priority #2: Accelerated Maintenance Continued

15

Local Government in South Australia maintains approximately 75,000 kms of the State’sroads, 15,000 kms of which are sealed. On average Councils in South Australia spend$162 million p.a on road construction and maintenance. The Local GovernmentAssociation’s 2001 "Wealth of Opportunities Study", whilst 11 years old is still relevant,and found that South Australian Councils needed to increase their spending on maintaining their road assets from $42 million to $147 million per annum just to maintaintheir existing condition and stop further deterioration19. They have insufficient availablefunds to do so.

Poorly maintained transport networks have economic, social and environmental costs.They can:

1. Increase vehicle operating costs and travel timesPoorly maintained roads result in higher fuel consumption, increased vehicle maintenance, increased tyre wear and vehicle depreciation. Poorly maintained roads also impact on travel speeds. Vehicle operating costs and increased travel times directly impact the cost of all goods and services transported by road.

2. Increase road maintenance expenditure.Failure to carry out maintenance when it is needed can lead to increased damage to the road pavement, reducing the wearing surface life. In turn this results in major expenditure to keep the asset in service and ultimately, the need to replace the asset arrives earlier than would normally be the case.

3. Reduce safety.Poorly maintained roads result in greater risk of road accidents, through poor wet weather traction, and bitumen binder “bleeding” or “flushing”resulting in a very smooth surface. Either of these problems can increase braking distances or contribute to loss of vehicle control.

Deterioration of the wearing surface can also lead to poor surface drainage increasing the risk of wet weather crashes.

Inadequate maintenance of the roadside can also impact on road safety. Guardrailsplay an important role in reducing the severity of accidents and preventing rollovers but they also require regular maintenance and repair. Roadside signage and traffic control devices are also important and roadside trees and vegetation, if not cut and maintained, can reduce sight lines and make curves more dangerous. Road shoulders must be graded and kept free of water and loose debris so that vehicles pulling off the road are not at risk.

4. Reduce user satisfaction with ride qualityThe community expects to be able to travel safely and with comfort. Road users expect their roads to be smooth and any increase in roughness is easily discernibleby road users.

5. Reduce trade and tourismPoorly maintained roads can also impact on trade. Sensitive commodities such as fruit and vegetables can suffer damage and loss of value. Poor access to tourist attractions can discourage visitors.

6. Intensify vehicle impacts on the community and the environmentPoorly maintained road surfaces can lead to increased noise and dust levels and vehicle emissions which in turn impacts on nearby residences and local communities. Similarly, rough roads result in higher vehicle emissions and increased levels of greenhouse gases.

19 Local Government Association of South Australia, Wealth of Opportunities – A Study into InfrastructureAsset Conditions in South Australia, http://www.lga.sa.gov.au/site/page.cfm?u=252. Accessed 14 June,2012.

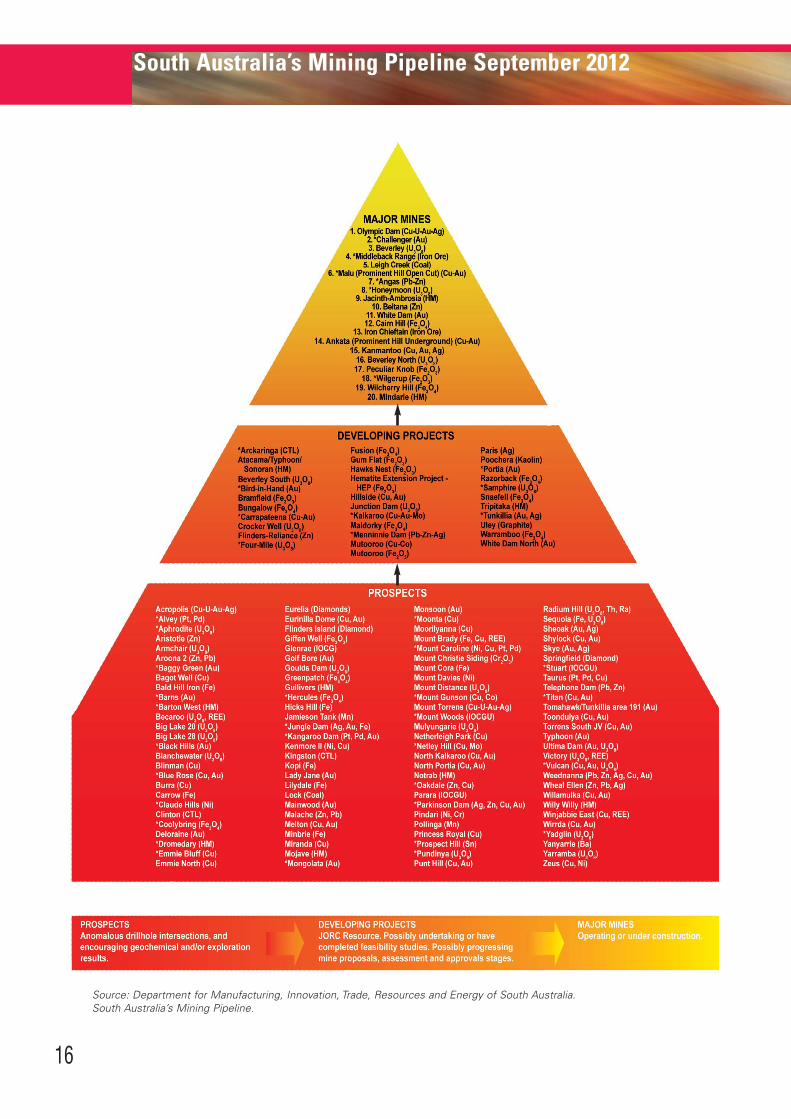

South Australia’s Mining Pipeline September 2012

16

Source: Department for Manufacturing, Innovation, Trade, Resources and Energy of South Australia.South Australia’s Mining Pipeline.

Project Priority #3: Mining Infrastructure and Development

17

The Minerals Boom: South Australia’s New Freight Challenge

The Mining Pipeline “pyramid” graphic indicates that South Australia is on the brink of amajor resources boom, with several new mines and mining projects coming on streamover the next decade.

Exploration activity in South Australia continues to boom, with the state enjoying highstatus in terms of mineral potential (14th of 93 mining jurisdictions surveyed worldwide)20,and private exploration expenditure increasing from $167.9 million in 2009-10 to $328.4million in 2011-1221.

New and existing mines will require significant road and rail transport infrastructureinvestment in order to move outputs to ports and processing facilities, and supplies (fuel,food and mining inputs) back to the mine efficiently. It is understood that some proponents of new mines are also considering the use of slurry pipelines.

Infrastructure funding can be provided by either the private sector when it is the main“direct” beneficiary from the investment, or the three levels of Government, whilst inmany cases, a partnership approach involving the public and private sectors will be necessary.

Three new ports, located at Port Bonython, Port Spencer and somewhere on the westernside of Yorke Peninsula (perhaps in the Wallaroo/Myponie Point area) will be required toexport and import materials and resources from a variety of mines, big and small.Existing ports will likely need to expand so as to facilitate interim solutions for junior miners to assist them to access their markets. Lucky Bay will develop as an interim solution for miners that are expected to shift to direct out-load through deep water portsas volumes grow. Ore exports through Whyalla and Port Pirie continue to grow and areexpected to increase significantly as new mines come on stream. In some instances withvery large developments, new or upgraded airports may also be needed to handle “fly in-fly out” workers and urgent freight (such as replacement machinery parts).

In some cases, investment in one mode may negate the need to invest in an alternative(and competing) mode.

Many of the priorities listed within this report have been included, or have grown in priority in part/wholly, due to the growing prospects of mining industry projects. Thesepriority projects include:

• Port Bonython Expansion & Rail Link – the building of new bulk port facilities, a 23km rail connection to the interstate main line, and possibly, a rail link from the isolated narrow gauge networks on Eyre Peninsula to the national network. Connections may also be justified to link sustainable mines to the rail network and ultimately the port.(Port Spencer and Wallaroo/Myponie Point are expected to initially develop to service specific company requirements and are likely to develop into multi-user ports as development progresses).

• Tarcoola - Crystal Brook Rail Capacity, including the Whyalla spur expansion – this portion of the interstate main line network will be key to logistics for many mines in the region, and is already close to capacity. Implementation of ARTC’s ATMS, new crossing loops and potentially eventual duplication may be required to facilitate rail movement if and when needed, including the interaction of trains moving at different speeds. A rail bypass of Port Augusta may be necessary to improve amenity in the Port Augusta township, and a new connection to the Port Augusta-Whyalla rail spur (commonly referred to as the “Port Augusta Triangle”) will improve rail access from the west and north of the State.

20 Cervantes, M., McMahon, F. Survey of Mining Companies: 2011/2012. The Fraser Institute, February 2012.21 Hon. Tom Koutsantonis, Minister for Mineral Resources and Energy, Media Release: Mineral explorationhits post GFC-high, 3 September, 2012. http://www.pir.sa.gov.au/minerals/press_and_events/news_releas-es/mineral_exploration_hits_post_gfc-high

Project Priority #3: Mining Infrastructure and DevelopmentContinued

18

• Intermodal Terminal Development – mines generally require goods in large quantities, and often rail is the most efficient way to deliver them. Intermodal terminals, where volumes are sufficient to support a business case, are necessary to facilitate the transferof freight to/from road and sea to rail. Terminal developments may also alleviate the demand for road investment to accommodate High Productivity Vehicles.

• Princes Highway Upgrade: Port Wakefield to Port Augusta – this is the key road link from Adelaide and its facilities (such as the container terminal) to the prospective mining regions in the north and west of the State which will see an increasing volume of trucks as new mines develop.

• Yorkey’s Crossing – this road requires an upgrade to firmly establish it as an alternativeroute to Highway 1 around Port Augusta. While both the State Government and the Port Augusta City Council currently share responsibility for the road, there is a strong argument for the Commonwealth Government to fund an upgrade to this alternative route to Highway 1 in the event that the Port Augusta causeway is disabled. This corridoris also the over-dimensional route around the Port Augusta township and facilitates the movement of large equipment items to the mines, and therefore should be upgraded to facilitate all weather usage (notwithstanding that the high cost associatedwith this project will mean that proving viability will be difficult).

Ultimately rail capacity is dependent on crossing loops and therefore additional, longerloops are required to cope with longer trains, an expected increase in traffic, and to facilitate the interaction of trains travelling at different speeds. Axle loads may also presentlimitations to train capacity in the future. ARTC’s current investment in the Advanced TrainManagement System (ATMS) may improve network capacity, reliability, transit times andon-time performance in the short term.

IMX's Cairn Hill Iron Ore Project which commenced in 2010 has added several rail servicesin each direction to the network each week, and there are many other potential minesassessing rail based logistics options which, if proven viable, will significantly increasethe demand for train paths.

Project Priority #4: High Productivity Vehicle Access and Facilitation

19

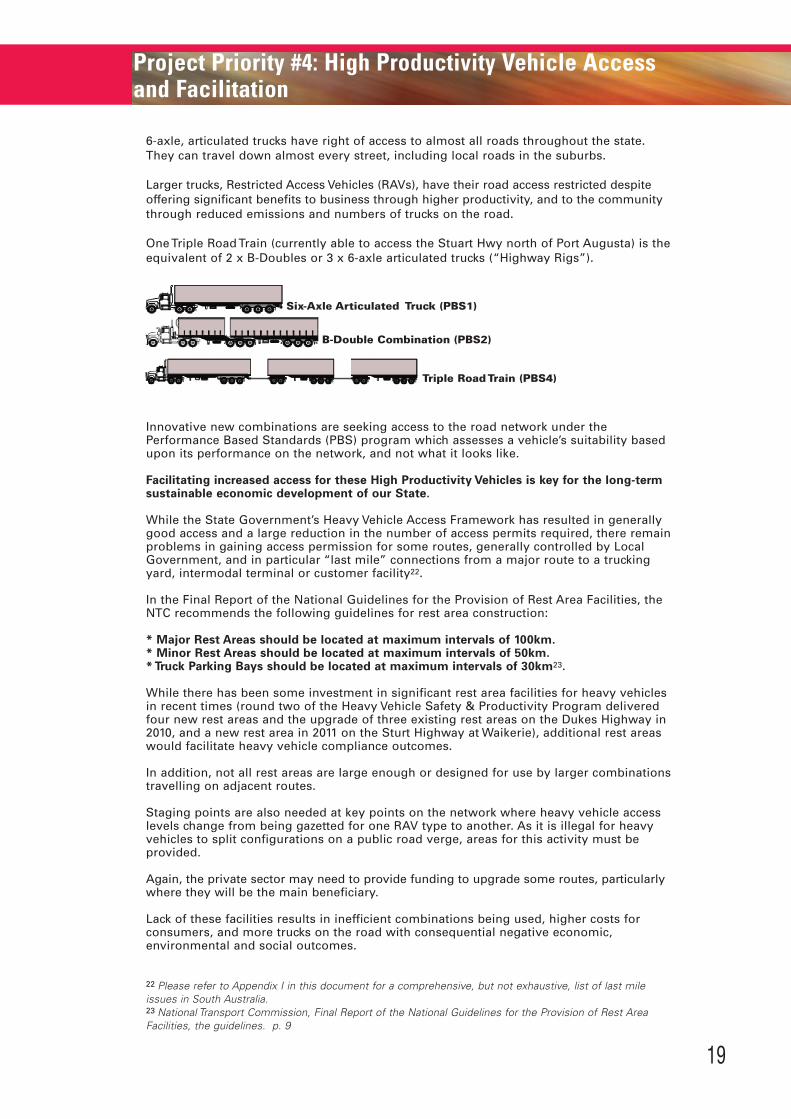

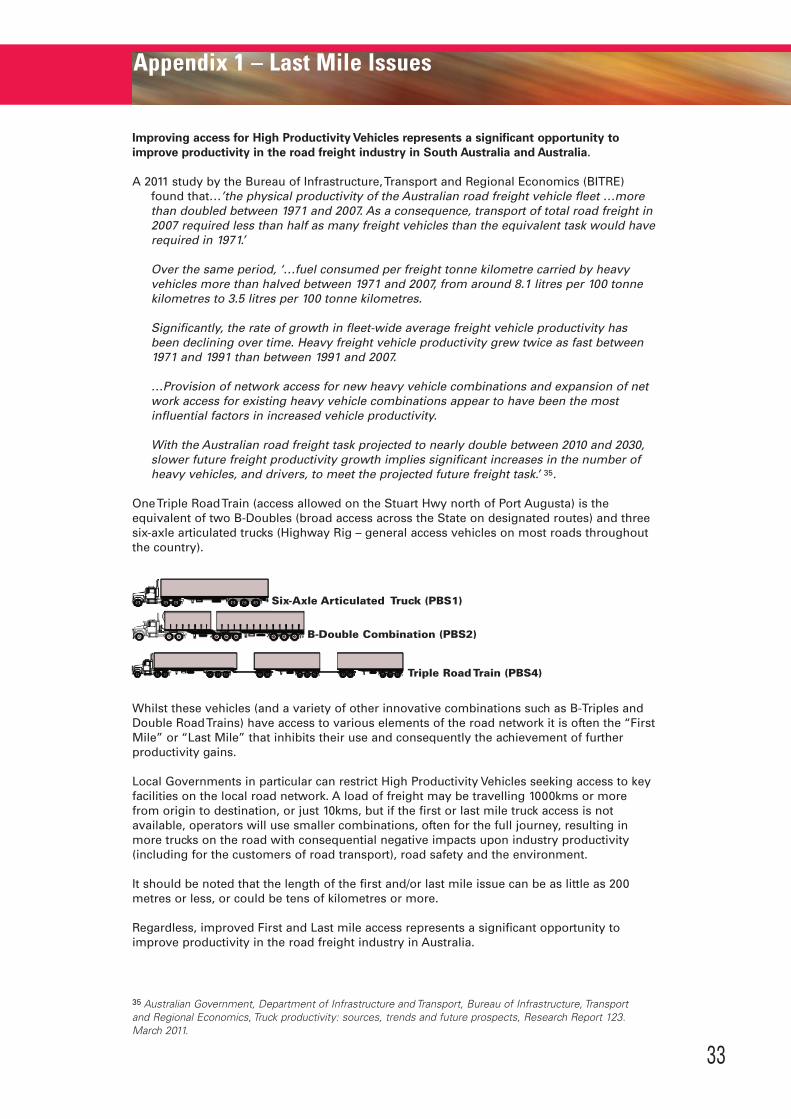

6-axle, articulated trucks have right of access to almost all roads throughout the state.They can travel down almost every street, including local roads in the suburbs.

Larger trucks, Restricted Access Vehicles (RAVs), have their road access restricted despiteoffering significant benefits to business through higher productivity, and to the communitythrough reduced emissions and numbers of trucks on the road.

One Triple Road Train (currently able to access the Stuart Hwy north of Port Augusta) is theequivalent of 2 x B-Doubles or 3 x 6-axle articulated trucks (“Highway Rigs”).

Innovative new combinations are seeking access to the road network under thePerformance Based Standards (PBS) program which assesses a vehicle’s suitability basedupon its performance on the network, and not what it looks like.

Facilitating increased access for these High Productivity Vehicles is key for the long-termsustainable economic development of our State.

While the State Government’s Heavy Vehicle Access Framework has resulted in generallygood access and a large reduction in the number of access permits required, there remainproblems in gaining access permission for some routes, generally controlled by LocalGovernment, and in particular “last mile” connections from a major route to a truckingyard, intermodal terminal or customer facility22.

In the Final Report of the National Guidelines for the Provision of Rest Area Facilities, theNTC recommends the following guidelines for rest area construction:

* Major Rest Areas should be located at maximum intervals of 100km.* Minor Rest Areas should be located at maximum intervals of 50km.* Truck Parking Bays should be located at maximum intervals of 30km23.

While there has been some investment in significant rest area facilities for heavy vehiclesin recent times (round two of the Heavy Vehicle Safety & Productivity Program deliveredfour new rest areas and the upgrade of three existing rest areas on the Dukes Highway in2010, and a new rest area in 2011 on the Sturt Highway at Waikerie), additional rest areaswould facilitate heavy vehicle compliance outcomes.

In addition, not all rest areas are large enough or designed for use by larger combinationstravelling on adjacent routes.

Staging points are also needed at key points on the network where heavy vehicle accesslevels change from being gazetted for one RAV type to another. As it is illegal for heavyvehicles to split configurations on a public road verge, areas for this activity must be provided.

Again, the private sector may need to provide funding to upgrade some routes, particularlywhere they will be the main beneficiary.

Lack of these facilities results in inefficient combinations being used, higher costs for consumers, and more trucks on the road with consequential negative economic, environmental and social outcomes.

22 Please refer to Appendix I in this document for a comprehensive, but not exhaustive, list of last mileissues in South Australia.23 National Transport Commission, Final Report of the National Guidelines for the Provision of Rest AreaFacilities, the guidelines. p. 9

Six-Axle Articulated Truck (PBS1)

B-Double Combination (PBS2)

Triple Road Train (PBS4)

Urg

ent P

roje

cts

Lifti

ng S

outh

Aus

tral

ia’s

tran

spor

t inf

rast

ruct

ure

netw

ork

com

petit

iven

ess

20

Pro

ject

nam

e W

hy?

Fun

din

g/c

ost

Tim

efra

me

1.N

ort

h-S

ou

th C

orr

ido

r

(So

uth

Ro

ad U

pg

rad

e an

d

No

rth

ern

Co

nn

ecto

r)

Th

e N

ort

h-S

ou

th C

orr

ido

r is

th

esp

ine

of

the

Ad

elai

de

Met

rop

olit

an R

oad

Net

wo

rkan

d r

un

s fo

r 78

kms

fro

mN

oar

lun

ga t

o G

awle

r in

corp

ora

tin

g t

he

So

uth

ern

Exp

ress

way

, S

ou

th R

d,

No

rth

ern

Co

nn

ecto

r (r

epla

cin

gel

emen

ts o

f th

e Po

rt R

iver

Exp

ress

way

an

d P

ort

Wak

efie

ldR

d a

s w

ell

as t

he

Inte

rsta

teM

ain

line

Rai

l N

etw

ork

) an

d t

he

No

rth

ern

Exp

ress

way

.

So

uth

Rd

Up

gra

de:

Co

mm

onw

ealt

h &

Sta

teG

ove

rnm

ents

, $2

.5 -

$4.

0 b

illio

n

No

rth

ern

Co

nn

ecto

r:C

om

mo

nwea

lth

(in

cl A

RT

C)

&S

tate

Go

vern

men

t $1

.2 b

illio

n +

So

uth

ern

Exp

ress

way

Du

plic

atio

n:

$445

mill

ion

(u

nd

erw

ay)

Sta

teG

ove

rnm

ent

fun

ded

, is

of

less

sig

nif

ican

ce t

o t

he

frei

gh

tin

du

stry

an

d i

s th

eref

ore

no

tin

corp

ora

ted

in

th

e fi

gu

res

abo

ve.

(Po

ten

tial

To

ll R

oad

Can

did

ates

)

Sig

nif

ican

t p

rog

ress

wit

hin

th

ep

aram

eter

s o

f th

e N

atio

nB

uild

ing

2 f

un

din

g p

rog

ram

(201

3/14

– 2

018/

19)

Sta

gg

ered

del

iver

y o

f co

rrid

or

pro

ject

s ta

rget

ing

co

mp

leti

on

of

the

wh

ole

co

rrid

or

in 2

022.

Ele

men

ts o

f th

e p

roje

cts

are

Un

der

way

(Gal

lipo

li U

nd

erp

ass

and

Gle

nel

g T

ram

Cro

ssin

g G

rad

eS

eper

atio

n c

om

ple

ted

.N

ort

her

n E

xpre

ssw

ay

com

ple

ted

. S

ou

th R

d S

up

erw

ayu

nd

erw

ay.

Pla

nn

ing

of

sect

ion

bet

wee

n G

allip

oli

Un

der

pas

san

d R

egen

cy R

d u

nd

erw

ay,

Dar

ling

ton

pre

cin

ct c

on

cep

tp

lan

co

mp

lete

d b

ut

curr

entl

y is

no

t a

pri

ori

ty p

roje

ct,

So

uth

ern

Exp

ress

way

Du

plic

atio

n

un

der

way

)

Exe

cuti

on

of

a fu

ll vi

sio

n o

r p

lan

fo

r th

e co

rrid

or

inco

rpo

rati

ng

ro

ad w

iden

ing

, el

evat

ed r

oad

s, a

nd

tun

nel

s fo

r th

e en

tire

co

rrid

or

to f

acili

tate

fre

igh

t an

dp

asse

ng

er m

ove

men

ts.

Th

e N

ort

h-S

ou

th c

orr

ido

r re

pre

sen

ts t

he

spin

e o

f th

eA

del

aid

e tr

ansp

ort

net

wo

rk a

nd

is

ther

efo

re f

un

da-

men

tal

to t

he

effi

cien

t m

ove

men

t o

f p

eop

le a

nd

frei

gh

t w

ith

in,

acro

ss a

nd

th

rou

gh

th

e m

etro

po

litan

area

.

The

corr

idor

car

ries

fre

ight

of

all k

inds

to/

from

fac

ilitie

san

d w

areh

ou

ses,

po

rts,

air

po

rts

and

ter

min

als

as w

ell

as r

etai

l o

utl

ets

and

pri

vate

ho

mes

.

Th

e S

ou

th R

d e

lem

ent

of

the

pro

ject

, p

arti

cula

rly

the

sect

ion

bet

wee

n t

he

Gal

lipo

li U

nd

erp

ass

and

Reg

ency

Rd

is

view

ed b

y in

du

stry

as

the

pri

ori

ty

elem

ent

wit

h t

he

No

rth

ern

Co

nn

ecto

r al

so n

eed

ing

to

be

com

ple

ted

wit

hin

th

e ti

mes

cale

of

the

Nat

ion

Bu

ildin

g 2

fu

nd

ing

pro

gra

m.

Th

e N

ort

her

n C

on

nec

tor

is a

pro

ject

des

ign

ed t

o

cap

ital

ise

on

oth

er p

roje

cts

in t

he

no

rth

of

Ad

elai

de

to c

reat

e a

free

-flo

win

g r

oad

an

d r

ail

corr

ido

r fr

om

the

Nor

ther

n Ex

pres

sway

to

the

Port

Riv

er E

xpre

ssw

ay(r

ecen

tly

com

ple

ted

), c

on

nec

tin

g i

n a

t th

e S

ou

thR

oad

Su

per

way

(u

nd

er c

on

stru

ctio

n)

to t

he

wes

t o

fth

e cu

rren

t co

rrid

or

alo

ng

Po

rt W

akef

ield

Ro

ad.

Th

e ra

il p

ort

ion

of

the

pro

ject

will

rem

ove

fre

igh

ttr

ain

s fr

om

th

e p

ort

ion

of

the

net

wo

rk p

assi

ng

thro

ug

h s

ub

urb

an a

reas

su

ch a

s S

alis

bu

ry a

nd

Maw

son

Lak

es a

nd

wo

uld

fac

ilita

te d

evel

op

men

t o

fth

e p

rop

ose

d T

OD

s.

21

Urg

ent P

roje

cts

Cont

inue

d

Lifti

ng S

outh

Aus

tral

ia’s

tran

spor

t inf

rast

ruct

ure

netw

ork

com

petit

iven

ess

Pro

ject

nam

e W

hy?

Fun

din

g/c

ost

Tim

efra

me

2.A

ccel

erat

ed R

oad

M

ain

ten

ance

An

ass

et n

ot

mai

nta

ined

is

anas

set

lost

!

3.M

inin

g R

elat

ed

Infr

astr

uct

ure

an

d

Dev

elo

pm

ent

So

uth

Au

stra

lia i

s o

n t

he

cusp

of

a m

inin

g b

oo

m w

ith

po

ten

tial

new

min

es b

ein

g i

nves

tiga

ted

acro

ss t

he

Sta

te.

Min

es a

re o

fva

ryin

g s

izes

– l

arg

e an

d

rela

tive

ly s

mal

l (a

lbei

t st

ill

pro

du

cin

g h

igh

vo

lum

es o

f co

nce

ntr

ates

an

d o

res)

– a

cro

ssa

bro

ad r

ang

e o

f m

iner

al

pro

du

cts

– co

nce

ntr

ates

an

do

res,

iro

n,

cop

per

, g

old

, si

lver

,u

ran

ium

, n

icke

l an

d m

iner

alsa

nd

s to

nam

e a

few

.

Co

mm

onw

ealt

h &

Sta

teG

ove

rnm

ents

.

$160

mill

ion

bac

klo

g o

n S

tate

mai

nta

ined

ro

ads

in 2

003

.S

ign

ific

antl

y h

igh

er i

n 2

012.

$26-

38 m

illio

n (

esti

mat

e) p

erye

ar a

dd

itio

nal

exp

end

itu

re w

illb

e re

qu

ired

fo

r 10

yea

rs t

o t

ake

up

th

e cu

rren

t b

ackl

og

).

$10

0 m

illio

n+

(est

imat

e)

add

itio

nal

an

nu

al f

un

din

g j

ust

to m

ain

tain

lo

cal

road

s in

th

eir

exis

tin

g c

on

dit

ion

. Fu

rth

erfu

nd

ing

will

be

req

uir

ed t

ota

ke-u

p a

ny b

ackl

og

24.

Pub

lic s

ecto

r (S

tate

,C

om

mo

nwea

lth

an

d L

oca

lG

ove

rnm

ents

) an

d t

he

pri

vate

sect

or

sep

arat

ely

and

in

p

artn

ersh

ip

Sp

ence

r G

ulf

Po

rt L

ink

(Flin

der

sPo

rts

Ho

ldin

gs,

Lei

gh

ton

Co

ntr

acto

rs,

Mac

qu

arie

Cap

ital

,B

IS I

nd

ust

rial

Lo

gis

tics

an

dA

RT

C),

$65

0 m

illio

nC

om

mo

nwea

lth

, S

tate

an

dLo

cal

Go

vern

men

ts (

acce

ss

corr

ido

rs)

An

im

med

iate

in

crea

se i

n

fun

din

g a

lloca

ted

fo

r m

ain

ten

ance

of

road

s u

nd

erth

e ca

re a

nd

co

ntr

ol

of

bo

th t

he

Sta

te a

nd

Lo

cal

Go

vern

men

ts.

Sta

gg

ered

del

iver

y o

f m

ain

ten

ance

pro

ject

s to

202

2to

ad

dre

ss c

urr

ent

bac

klo

g.

Del

iver

y o

f p

roje

cts

imm

edia

tely

pri

or

to t

he

nee

d.

2017

(p

ort

exp

ecte

d t

o b

e o

per

atio

nal

at

this

tim

e)

Up

gra

de

the

exis

tin

g r

oad

tra

nsp

ort

net

wo

rk t

ore

mo

ve t

he

exis

tin

g m

ain

ten

ance

bac

klo

g a

nd

bri

ng

the

syst

em u

p t

o a

su

itab

le s

tan

dar

d.

Poo

rly

mai

nta

ined

ro

ad t

ran

spo

rt n

etw

ork

s in

crea

seve

hic

le o

per

atin

g c

ost

s, d

isco

ura

ge

bu

sin

ess

inve

stm

ent,

red

uce

saf

ety,

red

uce

rid

e q

ual

ity

and

use

r sa

tisf

acti

on

an

d c

an i

ncr

ease

to

tal

mai

nte

nan

ceco

sts

ove

r th

e lo

ng

er t

erm

.

If t

his

un

pre

ced

ente

d e

con

om

ic o

pp

ort

un

ity

is t

o b

ere

alis

ed t

hen

th

e in

du

stry

will

nee

d a

cces

s to

a v

ast

arra

y o

f b

oth

maj

or

and

rel

ativ

ely

min

or

tran

spo

rtin

fras

tru

ctu

re p

roje

cts.

No

t al

l o

f th

e re

qu

ired

new

in

fras

tru

ctu

re

dev

elo

pm

ents

hav

e b

een

fu

lly s

cop

ed a

t th

is t

ime,

and

new

pro

po

sals

will

dev

elo

p a

s m

inin

g v

entu

res

mo

ve t

ow

ard

s im

ple

men

tati

on

. S

om

e o

f th

e p

roje

cts

curr

entl

y to

ute

d i

ncl

ud

e:

New

Po

rt F

acili

ties

Co

nst

ruct

ion

of

new

po

rt f

acili

ties

at

Port

Bo

nyth

on

(3km

jet

ty,

load

ers,

en

clo

sed

co

nvey

or,

sh

edd

ing

etc

.)ca

pab

le o

f h

and

ling

Cap

esiz

e b

ulk

ves

sels

, an

din

clu

din

g t

he

esta

blis

hm

ent

of

a 23

km r

ail

spu

r an

db

allo

on

lo

op

fro

m t

he

inte

rsta

te m

ain

lin

e n

ear

Why

alla

to

th

e p

ort

. S

om

e ro

ad u

pg

rad

es m

ay a

lso

be

req

uir

ed t

o f

acili

tate

acc

ess

by

Hig

h P

rod

uct

ivit

yVe

hic

les.

24 Lo

cal G

over

nmen

t A

ssoc

iatio

n of

Sou

th A

ustr

alia

, R

oads

& T

rans

port

, ht

tp://

ww

w.lg

a.sa

.gov

.au/

site

/pag

e.cf

m?u

=25

2A

cces

sed

19/0

3/20

12

22

3.M

inin

g R

elat

ed

Infr

astr

uct

ure

an

d

Dev

elo

pm

ent

(co

nt)

Priv

ate

sect

or

po

rt p

rop

on

ents

Co

mm

onw

ealt

h,

Sta

te a

nd

Loca

l G

ove

rnm

ents

(ac

cess

co

rrid

ors

)

AR

TC

$5-

10 m

illio

n (

esti

mat

e)

AR

TC

$3

- 4m

illio

n p

er C

ross

ing

Loo

p (

do

es n

ot

incl

ud

e si

gn

allin

g c

ost

s)

Co

mm

onw

ealt

h G

ove

rnm

ent

toad

d t

o t

he

nat

ion

al n

etw

ork

an

db

oth

th

e S

tate

an

dC

om

mo

nwea

lth

Go

vern

men

tsto

fu

nd

up

gra

de

$40+

mill

ion

(es

tim

ated

) It

sh

ou

ld b

e n

ote

d t

hat

a

rela

tive

ly h

igh

co

st,

wh

ich

dim

inis

hes

th

e p

roje

ct’s

vi

abili

ty,

is a

sso

ciat

ed w

ith

th

isp

roje

ct.

As

req

uir

ed

2017

(to

co

inci

de

wit

h P

ort

Bo

nyth

on

Dev

elo

pm

ent)

or

ear-

lier

if r

equ

ired

fo

r o

ther

dev

el-

op

men

ts (

eg:

the

So

uth

ern

Iro

nd

evel

op

men

t o

f A

rriu

m M

inin

g)

Exp

ansi

on

as

volu

mes

war

ran

t

2017

(o

r ea

rlie

r to

co

inci

de

wit

hm

ine

dev

elo

pm

ent)

Ad

dit

ion

al p

ort

fac

iliti

es a

re t

ou

ted

fo

r Po

rt S

pen

cer

(nea

r Po

rt N

eill)

, Lu

cky

Bay

an

d t

he

wes

tern

sid

e o

fYo

rke

Pen

insu

la (

Wal

laro

o/M

ypo

nie

Po

int)

.

Exi

stin

g p

ort

s m

ay a

lso

nee

d t

o e

xpan

d c

apac

ity

toac

com

mo

dat

e n

ew b

ulk

exp

ort

s.

Co

nst

ruct

ion

of

a ra

il sp

ur

in t

he

“Po

rt A

ug

ust

aTr

ian

gle

”to

allo

w t

rain

s to

byp

ass

the

raily

ard

s in

Port

Au

gu

sta

to d

irec

tly

acce

ss t

he

Why

alla

lin

e fr

om

the

Wes

t an

d N

ort

h o

f th

e S

tate

.

Th

is p

roje

ct w

ill r

emo

ve t

he

inef

fici

ent

nee

d f

or

shu

nti

ng

op

erat

ion

s in

th

e to

wn

ship

Incr

ease

cap

acit

y o

n t

he

Tarc

oo

la -

Cry

stal

Bro

ok

Rai

lse

ctio

n o

f th

e In

ters

tate

Mai

n L

ine

(in

clu

din

g t

he

Why

alla

sp

ur)

by

intr

od

uci

ng

th

e A

TM

S,

and

co

nst

ruct

ing

ad

dit

ion

al,

lon

ger

cro

ssin

g l

oo

ps

toac

com

mo

dat

e lo

ng

er t

rain

s, a

nd

an

exp

ecte

din

crea

se i

n t

raff

ic.

Ad

dit

ion

al i

nves

tmen

t in

oth

er e

lem

ents

of

the

rail

net

wo

rk (

eg: T

arco

ola

-Dar

win

lin

e an

d C

ryst

al B

roo

k-B

roke

n H

ill l

ine)

may

als

o b

e n

eces

sary

to

ac

com

mo

dat

e n

ew t

raff

ics.

York

ey’s

Cro

ssin

gis

th

e d

esig

nat

ed o

ver

dim

ensi

on

alro

ute

fo

r th

e m

inin

g s

ecto

r m

ovi

ng

aro

un

d P

ort

Au

gu

sta

(bet

wee

n H

igh

way

1 a

nd

Stu

art

Hw

y) a

nd

is

ther

efo

re l

ikel

y to

exp

erie

nce

in

crea

sed

tra

ffic

flo

ws

as t

he

min

ing

in

du

stry

dev

elo

ps.

All

wea

ther

acc

ess

is n

eces

sary

(ev

en r

elat

ivel

y lo

w r

ain

fal

l ev

ents

can

flo

od

th

e ro