rural - urban water inter-dependence mike young the university of adelaide

TRANSCRIPT

Rural - Urban Water Inter-DependenceMike Young

The University of Adelaide

Main conclusions

• Consequences of urban rural inconsistencies not well studied

• Policy choices have important implications at the regional and national level– Urban-Rural trading barriers remain– Price discipline is lacking from urban markets– Subsidies (grants) inconsistent with the NWI

objectives– Cost reflective infrastructure pricing needed– Urban water market could be expanded

Main challenges

• Changing Demand and Supply– Increasing population– Drier regime where we live and grow food– Significant over-allocation in some systems– Decreasing Peri-Urban supply opportunity– Increasing Peri-Urban development & demand

(dams)

• Need for adjustment away from existing allocation base

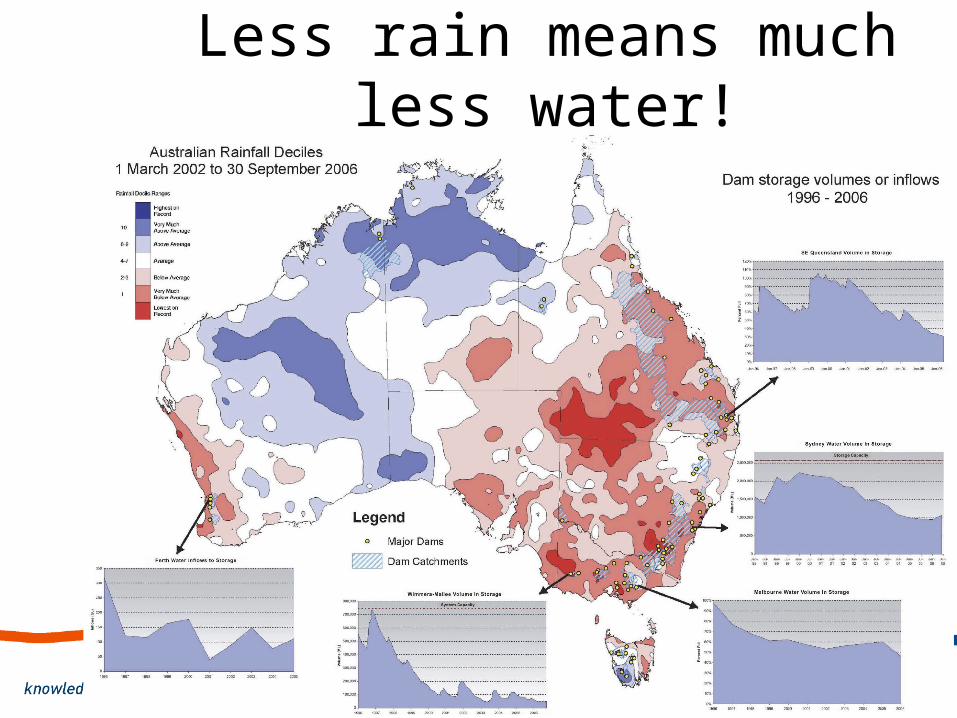

Less rain means much less water!

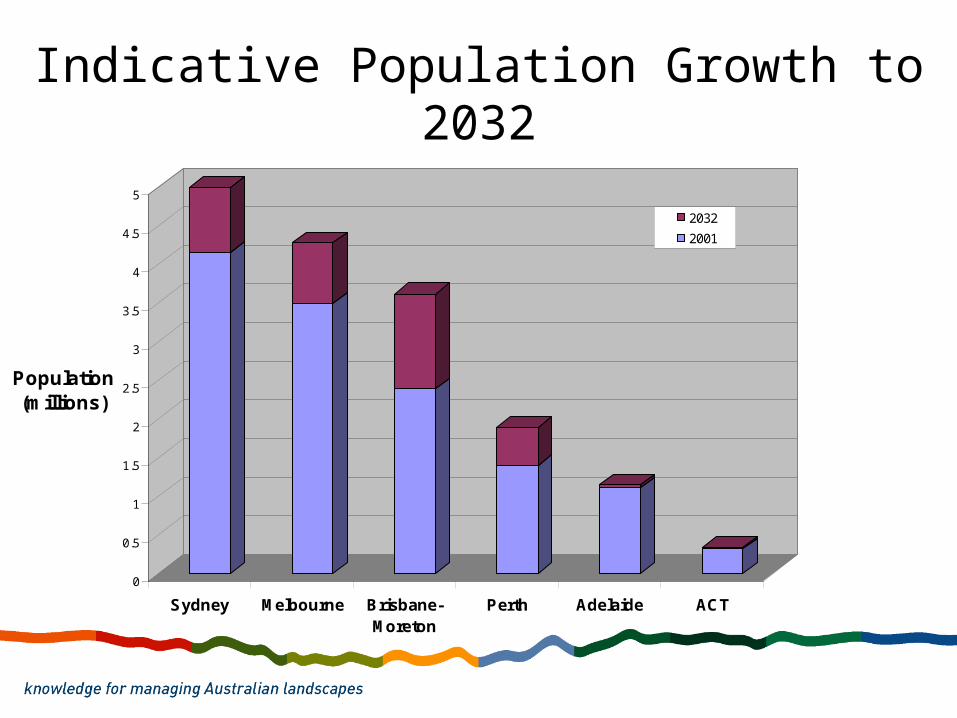

Indicative Population Growth to 2032

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

Population (millions)

Sydney Melbourne Brisbane-Moreton

Perth Adelaide ACT

2032

200120%

22%

52%

35%4%

6%

Paper’s Methodology

• Few papers on the urban rural interaction

• Two simple policy tests– Efficiency of policy– Consistency of policy approach

• Leave detail about water accounting and management of externalities to others

National Water Initiative

• History gave 100% supply security to urban users at price – often a fn (land value)– More recently metered

• NWI signals policy shift from an “urban prior right” to – full cost pricing– trading – new source development (when it pays)

• s.64 … “facilitate the efficient functioning of water markets, including inter-jurisdictional water markets, and in both rural and urban settings”

Facilitation v’s implementation

• Entitlements– Many urban entitlements normally still

defined as a separate pool that is inaccessible to rural water users• SA Urban (Adelaide) = moving average non-

tradeable allocation• NSW towns entitlement => fn(population)

– Regular two way allocation trade is rare

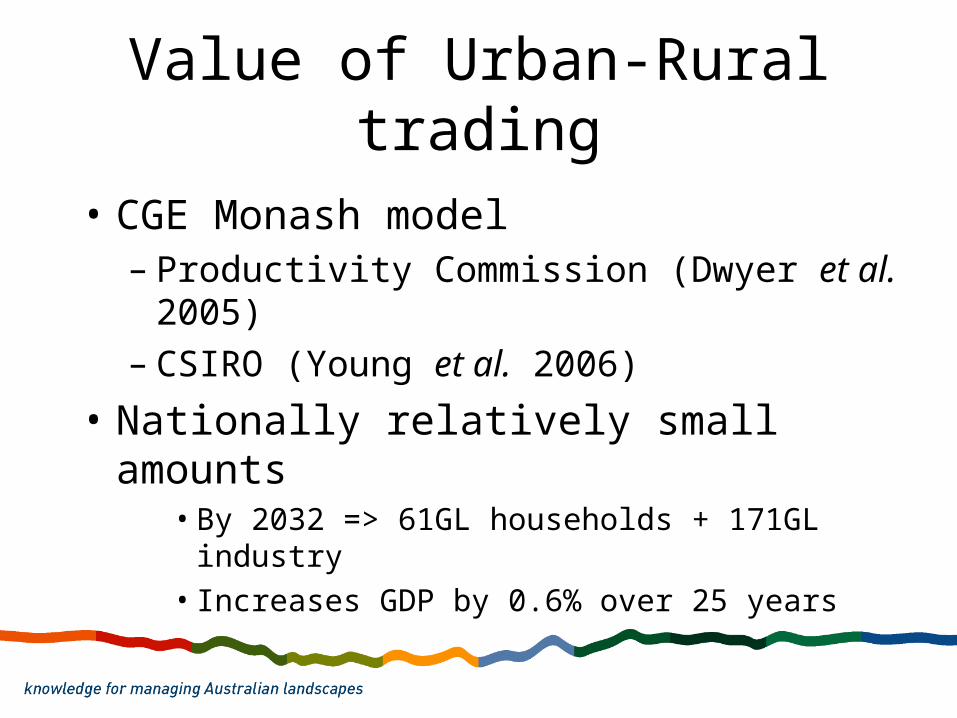

Value of Urban-Rural trading

• CGE Monash model– Productivity Commission (Dwyer et al.

2005)– CSIRO (Young et al. 2006)

• Nationally relatively small amounts• By 2032 => 61GL households + 171GL

industry• Increases GDP by 0.6% over 25 years

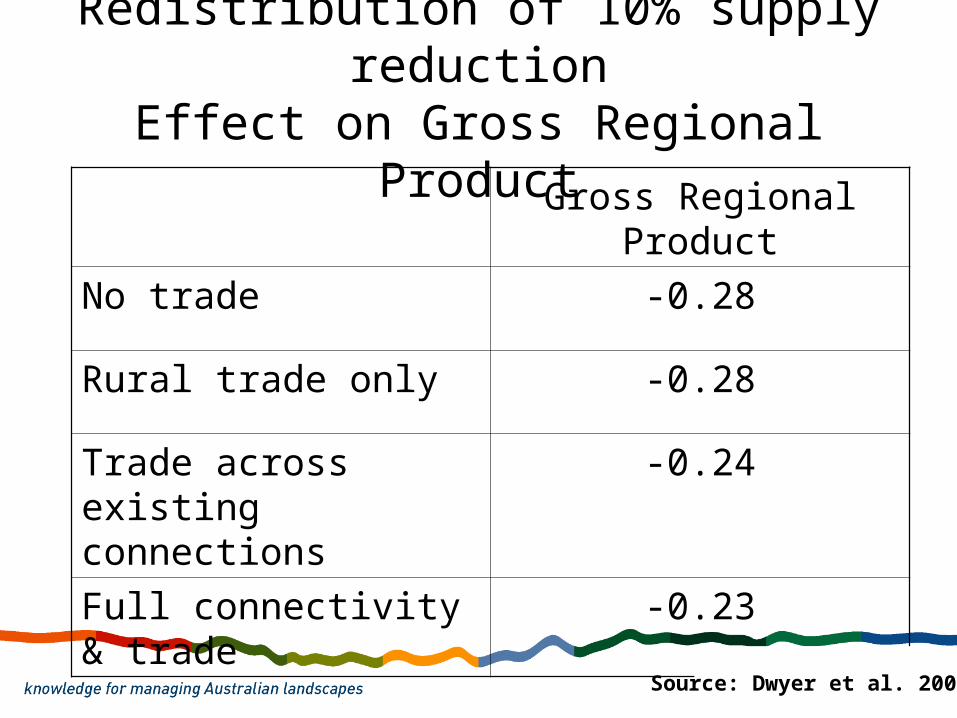

Redistribution of 10% supply reduction

Effect on Gross Regional ProductGross Regional

Product

No trade -0.28

Rural trade only -0.28

Trade across existing connections

-0.24

Full connectivity & trade

-0.23

Source: Dwyer et al. 2006

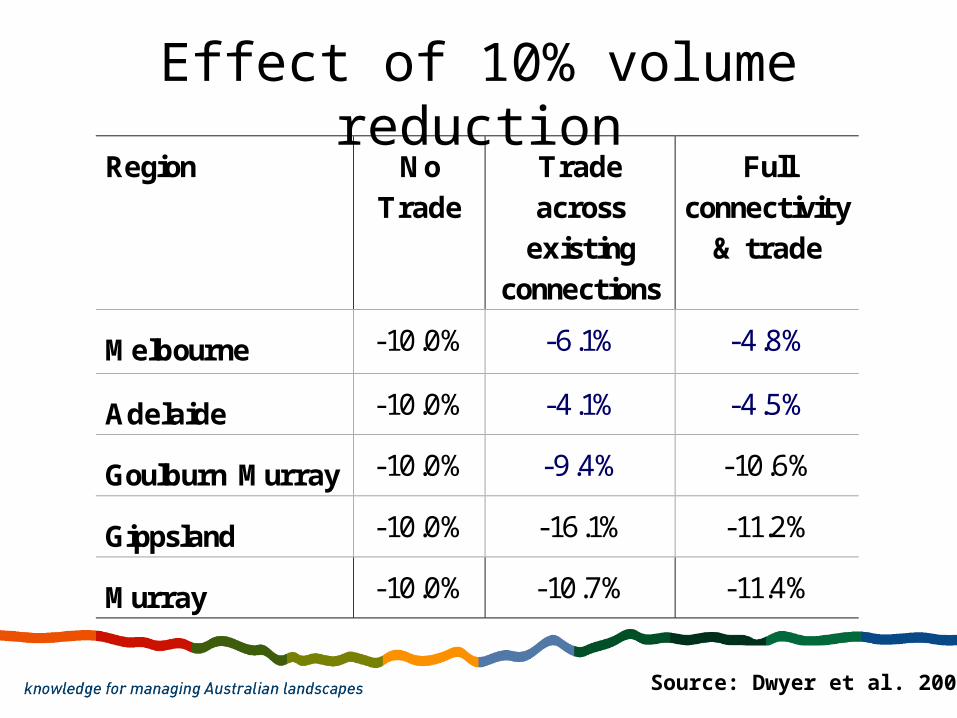

Effect of 10% volume reductionRegion No

Trade Trade across existing

connections

Full connectivity

& trade

Melbourne -10.0% -6.1% -4.8%

Adelaide -10.0% -4.1% -4.5%

Goulburn Murray -10.0% -9.4% -10.6%

Gippsland -10.0% -16.1% -11.2%

Murray -10.0% -10.7% -11.4%

Source: Dwyer et al. 2006

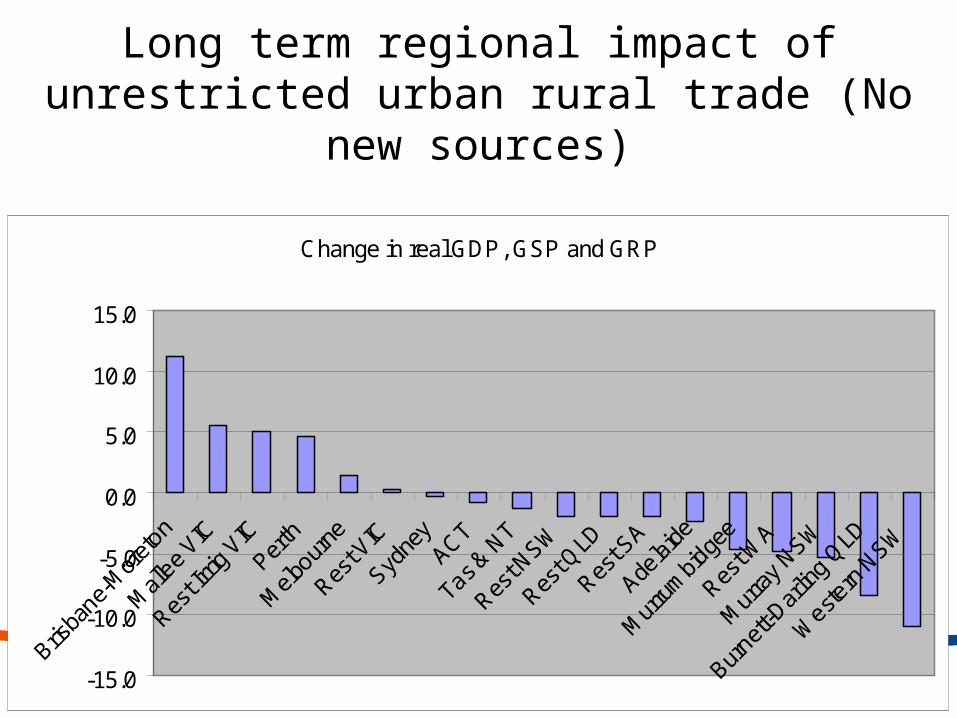

Long term regional impact of unrestricted urban rural trade (No new

sources)

Change in real GDP, GSP and GRP

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

NWI aim

Create policy settings which facilitate water use efficiency and innovation in urban and rural areas– Remove administrative impediments to

trade– Subject all water users and all water

suppliers to the same price disciplines

SA Trading Experience

SA Trading Experience

• 15,000 GL pa recycled sewage water to North Adelaide Plains

• Mannum-Adelaide pipeline used to supply water to Barossa Infrastructure Ltd off-season

• Purchase 25 GL from Lower Murray Swamps for Adelaide & 10 GL for environment

Other urban rural trading experience

• Harvey Water Infrastructure saving with Perth

• Proposals in Victoria – Coliban Water considering purchases

from Campaspe– Bendigo and Ballarat

• USA transfers are common• Arizona requires suburban developers

to prove water availability

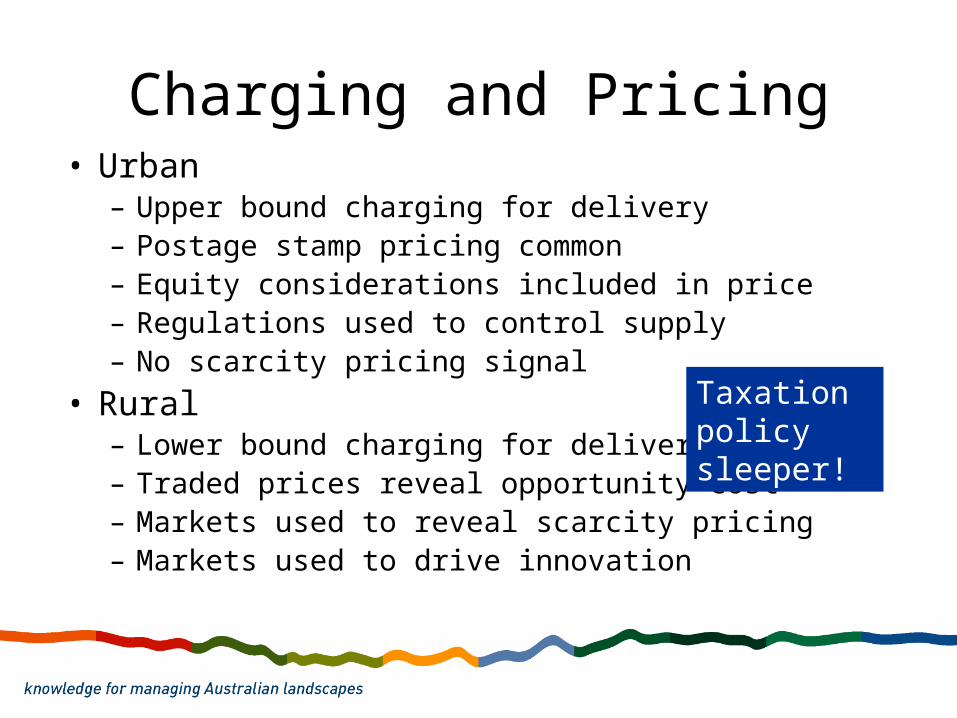

Charging and Pricing• Urban

– Upper bound charging for delivery– Postage stamp pricing common– Equity considerations included in price– Regulations used to control supply– No scarcity pricing signal

• Rural– Lower bound charging for delivery– Traded prices reveal opportunity cost– Markets used to reveal scarcity pricing– Markets used to drive innovation

Taxation policy sleeper!

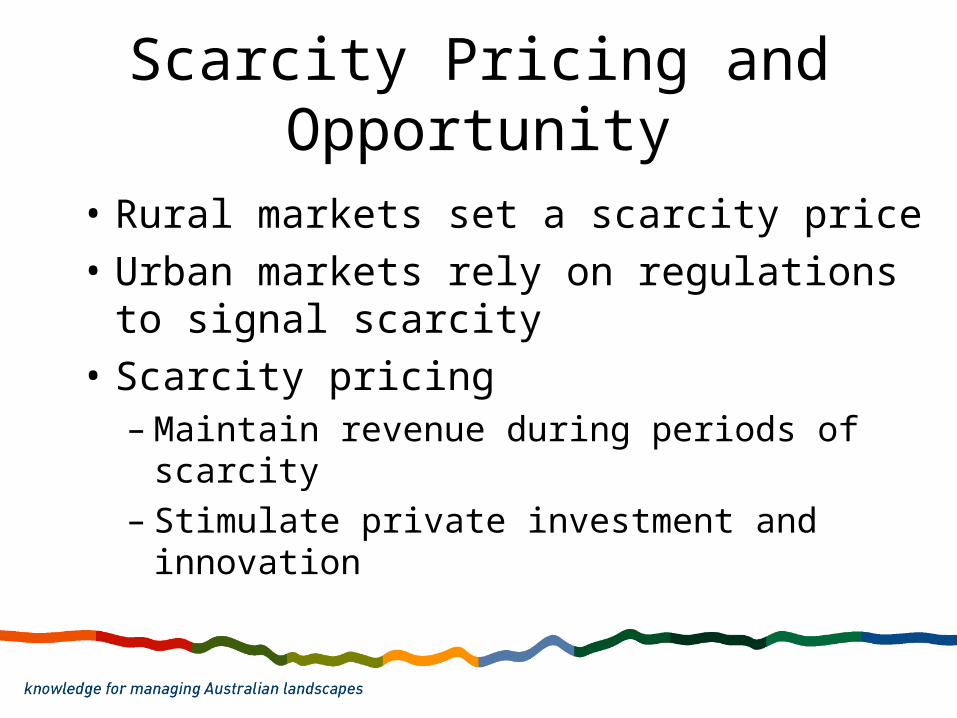

Scarcity Pricing and Opportunity

• Rural markets set a scarcity price• Urban markets rely on regulations to

signal scarcity• Scarcity pricing

– Maintain revenue during periods of scarcity

– Stimulate private investment and innovation

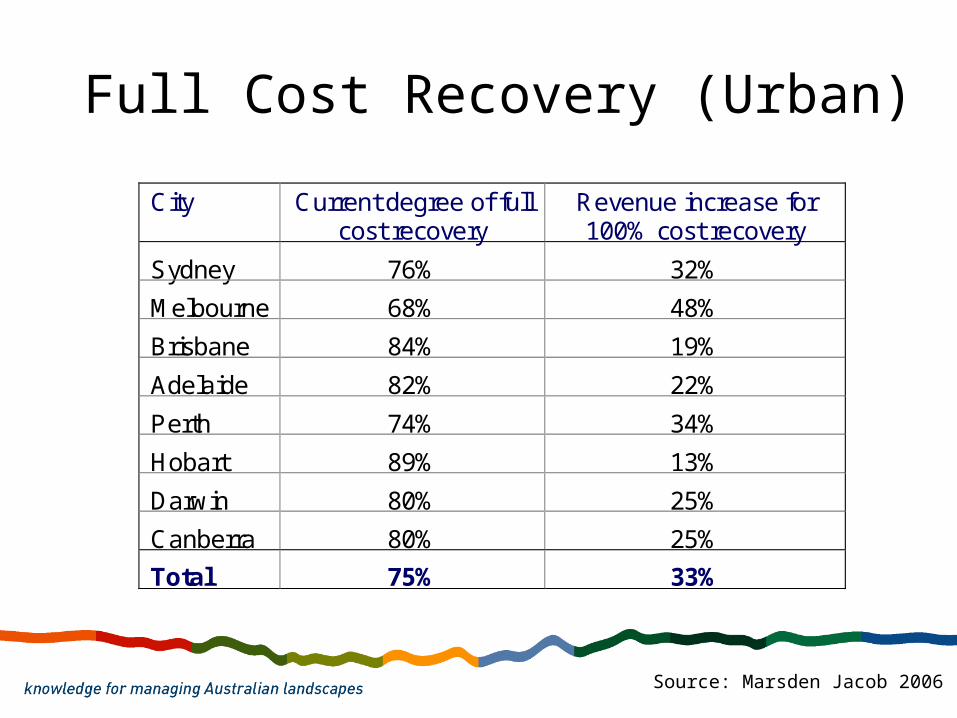

Full Cost Recovery (Urban)

City Current degree of full cost recovery

Revenue increase for 100% cost recovery

Sydney 76% 32%

Melbourne 68% 48%

Brisbane 84% 19%

Adelaide 82% 22%

Perth 74% 34%

Hobart 89% 13%

Darwin 80% 25%

Canberra 80% 25%

Total 75% 33%

Source: Marsden Jacob 2006

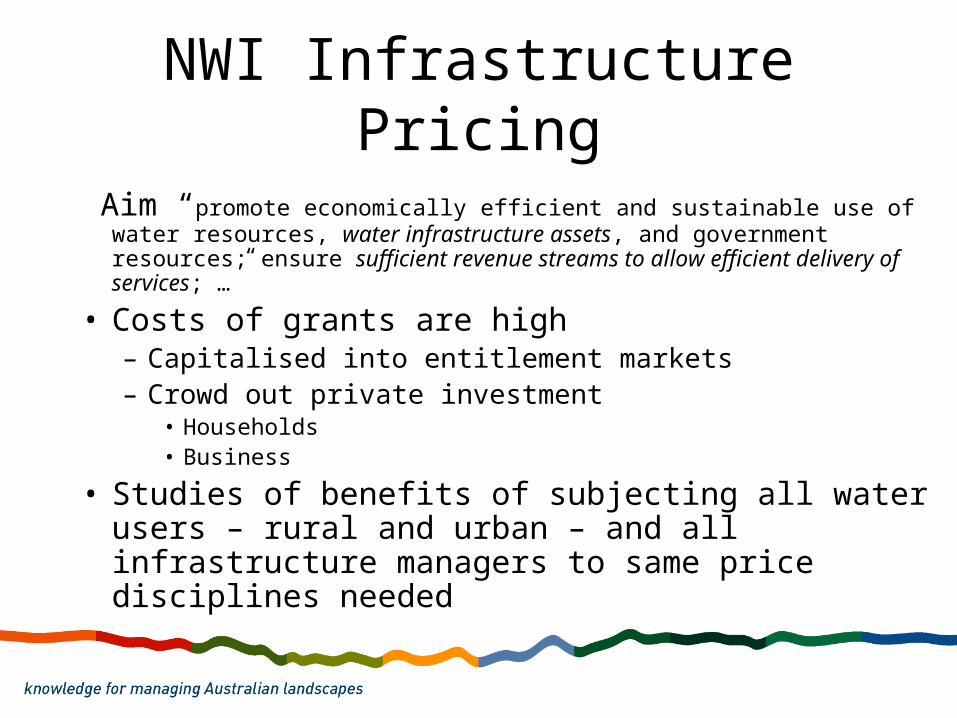

NWI Infrastructure Pricing

Aim “promote economically efficient and sustainable use of water resources, water infrastructure assets, and government resources; ensure sufficient revenue streams to allow efficient delivery of services; …”

• Costs of grants are high– Capitalised into entitlement markets– Crowd out private investment

• Households• Business

• Studies of benefits of subjecting all water users – rural and urban – and all infrastructure managers to same price disciplines needed

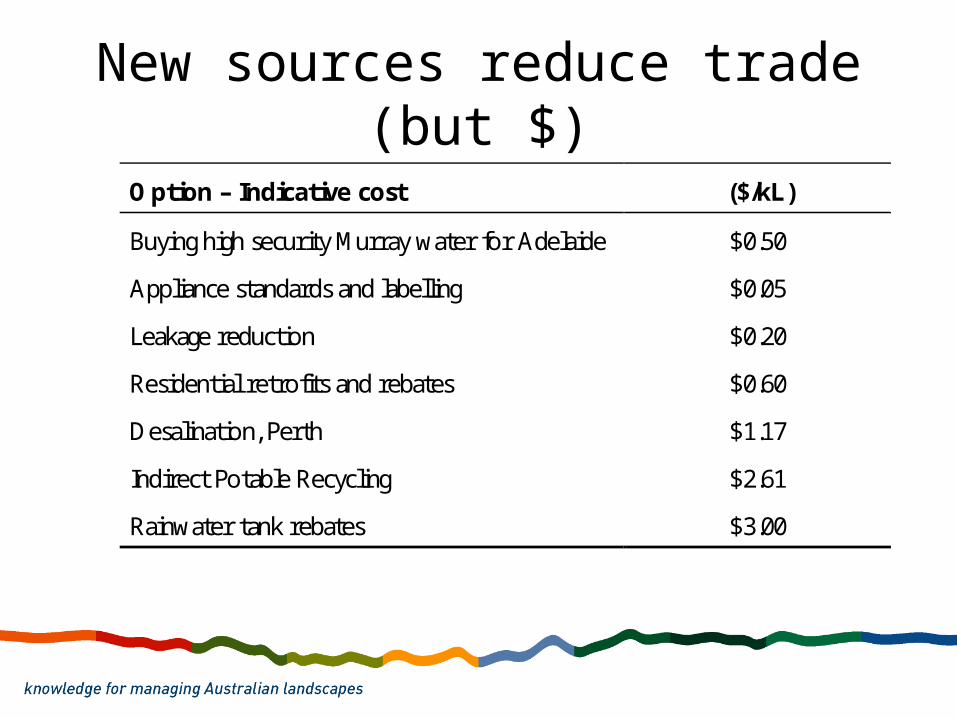

New sources reduce trade (but $)

Option – Indicative cost ($/kL)

Buying high security Murray water for Adelaide $0.50

Appliance standards and labelling $0.05

Leakage reduction $0.20

Residential retrofits and rebates $0.60

Desalination, Perth $1.17

Indirect Potable Recycling $2.61

Rainwater tank rebates $3.00

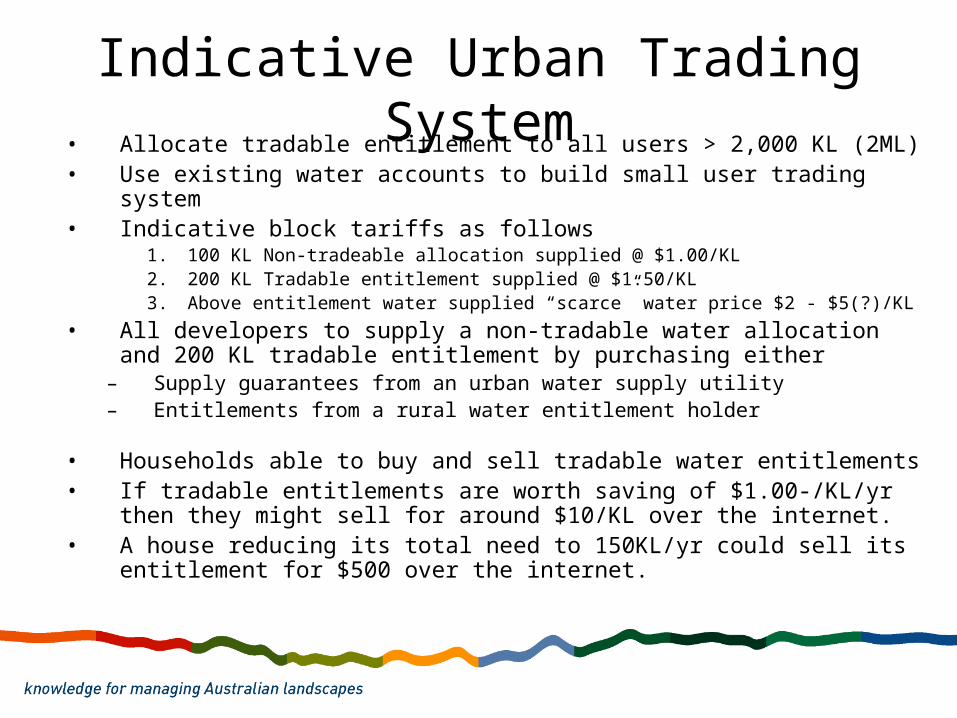

Indicative Urban Trading System• Allocate tradable entitlement to all users > 2,000 KL (2ML)• Use existing water accounts to build small user trading

system• Indicative block tariffs as follows

1. 100 KL Non-tradeable allocation supplied @ $1.00/KL2. 200 KL Tradable entitlement supplied @ $1.50/KL3. Above entitlement water supplied “scarce” water price $2 - $5(?)/KL

• All developers to supply a non-tradable water allocation and 200 KL tradable entitlement by purchasing either

– Supply guarantees from an urban water supply utility– Entitlements from a rural water entitlement holder

• Households able to buy and sell tradable water entitlements• If tradable entitlements are worth saving of $1.00-/KL/yr then

they might sell for around $10/KL over the internet. • A house reducing its total need to 150KL/yr could sell its

entitlement for $500 over the internet.

Urban-Rural Planning

• Allocation planning– Rural moving to statutory role to

manage scarcity– Urban focus on infrastructure planning

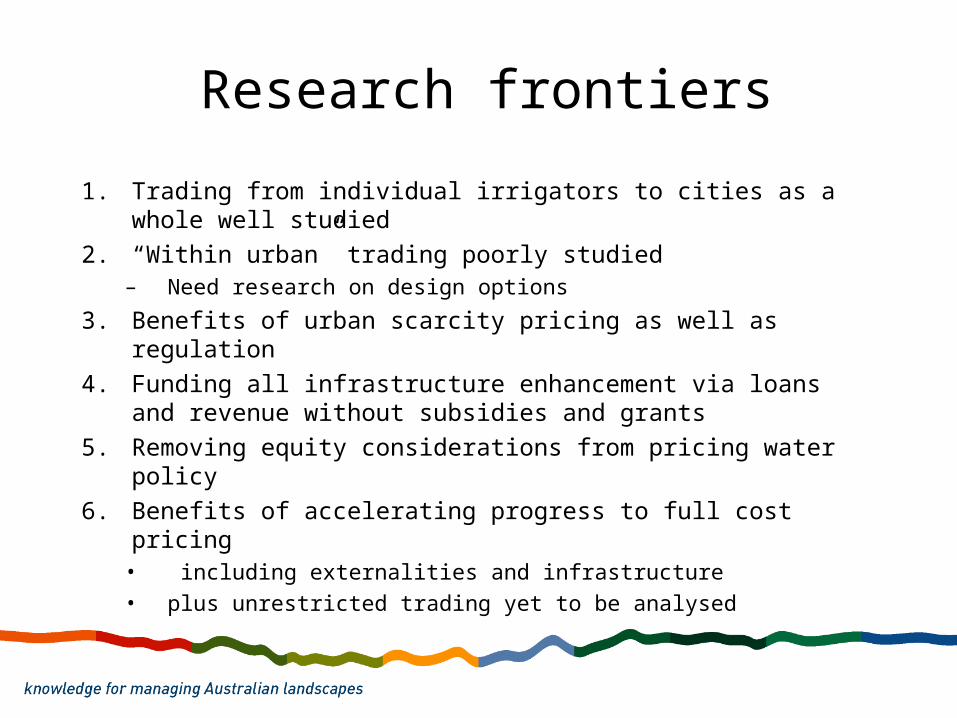

Research frontiers

1. Trading from individual irrigators to cities as a whole well studied

2. “Within urban” trading poorly studied– Need research on design options

3. Benefits of urban scarcity pricing as well as regulation4. Funding all infrastructure enhancement via loans and

revenue without subsidies and grants5. Removing equity considerations from pricing water

policy6. Benefits of accelerating progress to full cost pricing

• including externalities and infrastructure • plus unrestricted trading yet to be analysed