rupert melsom april 2010 analysis of the microfinance sector · pdf fileanalysis of the...

TRANSCRIPT

3iG

Analysis of the Microfinance SectorFaith Institutions and Impact Investing

RUPERT MELSOM APRIL 2010

International Interfaith Investment Group

₩

₡₱

₳

₩

₡₱

₳

3iG International Interfaith Investment Group Impact Investing: Microfinance2

“Rupert Melsom’s analysis of the microfinance market for the faith community’s investment managers is a must-read for leaders throughout the development sector. His recommendation to invest in deposit schemes, to counter volatility of commercial funding and to increase local sustainabi-lity, demonstrates the depth of his analysis of the sector and his understan-ding of sustainable solutions that are required in the developing world.”Rev Séamus Finn OMI, executive board member of 3iG, is a consultant to a number of investment committees in his own institution, the Oblates of Mary Immaculate 1, and for other religious congregations.

“Rupert’s microfinance investor paper gives Faith investors food for thought on how to allocate their impact investment funds best. Parties with a primary aim to alleviate poverty should take note of the strategic changes in the funding of the microfinance sector in order to achieve their goals effectively.”Fanny Ruighaver, Manager Institutional Investors, Oikocredit 2

“3iG is delighted to offer the Faith community this microfinance review as part of the series of impact investing papers. By combining 13 years of finance sector expertise with a passion for business development in emer-ging markets, Rupert has provided a remarkable account of the strategic challenges that face the industry and its investors. We are very pleased to share with you the strategic insights and in-depth knowledge to better achieve one’s impact investing charter goals.”Katinka van Cranenburgh, Secretary General, 3iG – International Interfaith Investment Group 3

“At Five Talents we recognise the positive effects of deposit schemes in Africa. It is with great pleasure to see that Rupert’s microfinance report for 3iG identifies the importance of local funding. Although many different deposit schemes are operating in different cultures, the common feature is that they all provide sustainable and locally expandable solutions for pover-ty alleviation. Based on Rupert’s strong finance and business development background this report helps the investor in the development to assess the strategic direction of the industry.”Tom Sanderson, UK Director, Five Talents 4

1 The Oblates are a Roman Catholic religious congregation with members in 65 countries and a long history of Faith Consistent Investing.2 Oikocredit is one of the world’s largest sources of private funding to the microfinance sector.3 3iG is a non-profit, multi-faith philanthropic foundation, whose mission is to contribute to a just and sustainable society through responsible investment in a spirit of genuine interfaith dialogue and co-operation.4 Five Talents is the microfinance development initiative of the worldwide Anglican Church. The church provides a ready made infrastructure – a physical presence of people and premises at the heart of even the remotest communities.

Recommendations

33iG International Interfaith Investment Group Impact Investing: Microfinance

3iG is proud to present the first report from the series of Faith Institutions and Impact Investing. Impact investments are investments that explicitly aim to respond to social or environmental challenges while generating financial returns. The first report is dedicated to microfinance and faith institutions.

Historically, religious institutions have been at the forefront of the microfinance market – offering small loans to the poor in the undeveloped world – resulting in positive social impact and community development, as well as generating financial returns. Many of the currently existing microfinance institutions have their origins in the faith communities.

This report defines microfinance and the microfinance industry’s present parameters, highlighting both risks and trends in a comprehensive approach. In addition, the report makes recommendations about the different ways that faith institutions can participate in the changing reality.

Whilst the report is primarily written for religious institutional investors, one should not underestimate the cascade effect that the initiatives of religious institutions have on their members and the civil society. While faith institutions may struggle to invest part of their portfolio in microfinance, the exemplary role of a church, synagogue or temple might have a significant influence on its members. Individual religious investors may often be less hesitant to change the mix of their portfolios and therefore microfinance can readily be considered as a potential alternative.

Follow-up reports on clean technology, sustainable agriculture and other types of impact investment are envisaged to be published by 3iG in the upcoming years to complete the series on Faith Institutions and Impact Investing. By doing so, 3iG hopes to capitalize more religious money into the impact investment market.

I hope you enjoy reading this report and find it valuable.

Katinka C. Van CranenburghSecretary General 3iG

Disclaimer: 3iG is not responsible for any investment decisions made by religious investors. All best practises mentioned in this report are based on a qualitative selection. 3iG does not necessarily promote one above others but just showcases them as examples of faith institutions’ investing with impact.

Foreword

43iG International Interfaith Investment Group Impact Investing: Microfinance

This research has been conducted for 3iG as part of an MBA project at Ashridge Business School in the UK. The detail of this document would not have been achievable without Katinka van Cranenburgh’s support and vast network within the faith and microfinance investor community. I would like to thank her for her contribution.

There are also a number of people I would like to thank at Ashridge Business School. Eve Poole has provided much direction and input regarding faiths and their relationship with usury and investments. Furthermore a token of appreciation should go to Erik Heinen of Oikocredit and Tom Sanderson of the UK based Christian charity Five Talents. By giving up their time from daily activities they shared important sector expertise, experiences and insights. Their offer to provide such wealth of experience with fellow faith institution investors and microfinance institutions, benefits the industry and the people for who poverty remains a daily reality.

Rupert Melsom April 2010

©copyright International Interfaith Investment Group 3iG, 2010

Acknowledgements

3iG International Interfaith Investment Group Impact Investing: Microfinance5

Microfinance has proven to be a valuable tool in alleviating poverty. In the years from 2000 to 2009 the industry introduced more transparency through standardised reporting and benchmarking. The performance generally demonstrated to be healthy in the sense of risk/return. The availability of comparable data, the performance track record and a general in-crease in loan origination volumes led to an increased interest from commercial investors.

Historically the microfinance sector has been predominantly funded by non-commercial investors, such as faith institutions and NGOs. The entrance of an increasing number of commercial investors has led to an increase in competition, particularly for funding of well performing microfinance institutions. Commercial investors are driven by profitability, therefore tend to compete for the most lucrative investments first and then move down the value curve. Non-commercial investors are driven by (sustainable) investment to alleviate poverty, opposed to purely profitability. The entrance of commercial investors is forcing non-commercial investors to make choices to protect their investment portfolios and charter objectives by learning from, and competing with, commercial investors. If no active management is undertaken, they risk having to scale down their investments, or even exit the microfinance market, which is contrary to their poverty alleviation objectives.

Non-commercial investors, who have funded a diverse portfolio of high and low margin microfinance institutions, find that the balance of their investment portfolio is shifting to the low margin end. Due to the loss of high margin investment areas, the portfolio returns are reduced and cannot be redeployed in support of more socially orientated low margin investments. In other words, although an increase in commercial investment is benefi-cial for the high margin market, it has an adverse effect on the less profitable part of the microfinance market. Commercially it makes sense to cease profit redeployment to lower yielding investments; therefore profits are repatriated to commercial investors by means of dividend or redeployed in other high margin areas. As an effect the non-commercial inves-tor has less high margin returns to cross-subsidise its low margin section of the portfolio. Leaving the most socially in need, subject to rising funding costs an overall lack of funding availability.

The commercialisation of the sector has resulted in a number of positive trends, but also some undesirable effects. • Commercialinvestorshaveaccesstocapitalmarkets.Thisprovidesrelativelyshort term capital at a competitive price. Therefore local microfinance borrowers have access to lower interest rates. Although this seems beneficial, there is another side to the coin. Short term capital markets funding is more volatile than long term funding. Market conditions such as in 2007-08 result in a reduction of available funding to local microfinance institutions. This means that local borrowers suddenly have no access to loans and slip back into poverty again. Such confron- tation of basic needs funded by market dynamics is reduced by non-commercial investors who continue to provide long term capital at sub-market rates, but their reach is limited.

Executive summary

3iG International Interfaith Investment Group Impact Investing: Microfinance6

• Theentranceofthecommercialinvestorshasresultedinaprofessionalizationof the industry. Loan origination procedures and reporting standards are introduced. The microfinance institutions tend to be forced to adhere to international quality standards in order to pitch for any commercial funding. This has a positive effect on their efficiency. • Thecommercialisationoftheindustryhasincreasedtheleveloffinancialservices expertise. The need for other financial services has also been evaluated, resulting in an increase of insurance, trade finance and depositing services. • Theconvergenceofmobiletelephonyandfinancialservicesisfaraheadofthe developed world. It is foreseeable that telecom operators could be a key player in microfinance. If consumer credit score trends in the developed world are to be taken into account, then telecom operators are probably the best positioned to register financial services transactions. Commercial investors of microfinance are taking such trend parallels with the Western financial services market into account when investing in microfinance institutions. The value in this industry is far greater than simply the interest margin on microfinance loans.

Any commercial investments are likely to result in the profits being repatriated to their (mainly Western) shareholders. In which case, it is uncertain that any proceeds shall be redeployed in the developing world. Local communities would benefit most from keeping an equity stake in their microfinance institutions. This would most likely be in the form of a co-operative (like the German Sparkassen and British Building Societies). Any (future) value generation due to interest margin, consumer credit data and product cross-sell opportunity would be returned to the microfinance client (member of co-operative) upon an acquisition or de-mutualisation of their entity. It is quite possible that the emerging markets would see a consolidation of microfinance institutions within the next 10 to 20 years. This would be driven by internal cost cutting and efficiency generation as well as the desire of financial firms to get a greater retail distribution network. One should not forget that today’s microfinance clients are tomorrow’s banking and insurance clients.

Commercial investors, such as private equity funds could benefit from launching and acquiring local microfinance institutions, in order to build up a substantial retail distri-bution network. The client data and relationship network could be of substantial value in markets where there is practically no consumer, credit or even census data. Their exit strategy would be to sell to a strategic buyer, such as a financial services, telecoms or retail company.

Faith institutions should be aware of these trends and consider whether local borrowers benefit from the entrance of commercial investors in the long term. Faith investment charters regarding microfinance might require a review in order to align investment poli-cies with the changing (more commercialised) market. Faith institutions may also wish to consider whether strategic long term equity5 opposed to debt investments or the launch of local co-operative and / or deposit funded schemes provide a more sustainable and beneficial solution for alleviating poverty.

73iG International Interfaith Investment Group Impact Investing: Microfinance

Lastly, it might be beneficial to take into account whether faith institutions should pool their resources and knowledge in order to protect and grow their market share whilst safeguarding the true drivers of microfinance – to alleviate world poverty. Otherwise they might find that this sector is “lost” to commercial investors and global poverty is not actually eradicated.

5 It is important to stress the long term nature of equity investments, as marginally profitable microfinance institutions might seem a less attractive investment to the equity investor, whereas for a debt investor it might have been acceptable. There are examples in the industry whereby microfinance institutions have become much more short term oriented in order to deliver shareholder value. Venture capital inspired incentive schemes like carried interests are not necessarily aligned to the social drivers of non-commercial investors. Hence long term strategic stakes are to be considered, whereas short term horizons should probably be reviewed only with significant diligence.

83iG International Interfaith Investment Group Impact Investing: Microfinance

1. Introduction 10

2. Microfinance 12

2.1. What is microfinance? 13

2.2. For who is microfinance suitable? 14

2.3. Who are the providers of microfinance? 15

2.4. Who are the key funders of microfinance? 16

3. Background information on the microfinance market and parties 17

3.1. Microfinance market 18

3.2. Parties offering microfinance services 22

3.2.1. Microfinance Investment Vehicles (“MIVs”) 22

3.2.2. Microfinance Institutions (“MFIs”) 23

3.2.3. Peer-to-peer lenders 24

3.2.4. Service providers 27

3.3. Types of borrowers to lend to 28

4. Background to the risks associated with investing in microfinance 29

4.1. Risks of microfinance investments 30

4.1.1. Risk levels by microfinance investment type 31

5. Current microfinance trends 33

5.1. Local funding through deposit schemes 34

5.2. Increase in commercial investors taking equity stakes in MFIs 35

5.3. The emergence of short term capital markets funding 36

5.4. Effect of above market trends on faith investors’ market share 37

6. Recommendations 39

6.1. Invest in microfinance 40

6.2. Offer deposit schemes 41

6.3. Lobby for regulation to safeguard minimum poverty alleviation 42

6.4. Compete with commercial investors and acquire equity stakes in MFIs 43

6.5. Regulate long term investor commitment 44

7. References 45

8. Glossary 47

Table of Contents

3iG International Interfaith Investment Group Impact Investing: Microfinance9

Appendices 49

Appendix I Case studies of faith related microfinance business cases 50

Default risk (FiveTalents) 50

Why deposit schemes improve lending opportunities and resolve social disputes (FiveTalents) 51

Understanding at grassroots level (ECLOF) 52

Microfinance initiatives can involve state of the art technologies (ECLOF) 52

Conducting sufficient due diligence and investment selection criteria (Oikocredit) 53

The implementation of ancillary services and the effect on obtaining funding 56

Appendix II Overview of largest global and African MFI’s 57

Appendix III Examples of Microfinance Investment Funds (MIVs) 61

Appendix IV What is Impact Investing 62

Appendix V Types of microfinance risks 63

Executive summary

3iG International Interfaith Investment Group Impact Investing: Microfinance10

This report looks at the investment opportunities and trends in the microfinance sector. Microfinance is one of the Impact Investment areas that provides sustainable improve-ments for relieving poverty. Microfinance, in its original form, provides people living in poverty access to very small amounts of credit to invest in (micro-) enterprise in order to climb out of poverty. Historically the financial services sector did not serve this market as it was considered not commercially viable. As the market matured, it became more commo-ditised and actual returns demonstrated commercial viability.

The research explains the difference between narrow and broad definitions of microfi-nance and details the different service providers that operate in the sector as well as the tar-get market. For readers new to the industry, there is background information on the market and the risks associated with the investment class. The global poverty market is touched upon to gauge the size and compilation of the potential microfinance market. Some of the key microfinance investors and local microfinance organisations are named. This offers newcomers to the industry, the possibility to research potential partners further and get a better understanding of where and how they operate in the business column.

The key element of the research is the identification of the key industry trends and their potential effect on faith institutions’ investment charter objectives. The trends deal with faith institutions’ financial as well as non-financial drivers (such as eradication of global poverty). A number of recommendations are made based on the market requirements, investment risks, faith institutions’ commercial and non-commercial drivers and industry trends.

The key message from the recommendations is that faith institutions should take note of the commercialisation of the sector as it has an adverse effect to their commercial and non-commercial investment charter objectives. They may wish to consider: • takingnoteoftheprofessionalrigour,basedonincreasedtransparency,efficiency and corporate governance that commercial investors introduced; • bundlingtheirinvestorresourcestoinfluencethedirectionandspeedofpoverty alleviation; • makingtheirvoicemoreactivelyheardinordertobenefitthepoorestintheworld by safe guarding acceptable investment methodology regulation over full free market commercialism.

The findings upon which the key message and proposed considerations are founded are related to the market trends that are having an adverse effect on faith institutions’ (non-)financial investment returns. • 1.Thepotentiallosstocommercialinvestorsofvaluablemarketshareatthehigh margin end of the microfinance market. This is due to commercial investors’ cherry picking of the more profitable investments from the market. Priority of

1. Introduction

3iG International Interfaith Investment Group Impact Investing: Microfinance11

investment objectives are not aligned between commercial and non-commercial investors. Commercial investors are driven first by profit and secondly by social return, whereas for non-commercial investors the priorities are vice-versa. In addition the volume of commercial investment to the sector increased due to low yields in Western markets in the years preceding the 2007-08 market correction.

A search for higher returns was found in emerging markets. In addition to margin drivers, social and sustainable investments have become more acceptable amongst the private investment community. This is possibly due to the Western public’s ove rindulgence of the early “noughties” (2000-2007), which has resulted in increased interest in social returns. The faith institutions’ loss of the well yielding parts of the microfinance market to commercial investors, could reduce the overall level of investment to lower margin opportunities. It is particularly those areas that are most in need of microfinance investment. • 2.Theeffectofvolatileshorttermfundingonlongtermpovertyalleviation.The entrance of commercial investors grew the overall market, but also increased cost of capital volatility due to the reliance on short term funding. One should take into consideration that the volatility of short term funding may have a more negative effect on poverty alleviation in declining markets than long term funding.

As faith institution investors tend to be asset rich, they generally hold long term funds and are not (as) reliant on capital markets as commercial investors. They serve the microfinance market sustainably, irrespective of economic trends. As we saw in 2007-08, commercial investors (needed to) retract from funding in declining markets. As a result, borrowers, in the process of rising out of poverty, are denied funding and slip back into poverty.

However, commercial investors have helped alleviate poverty substantially. The influx of capital has increased the reach of microfinance hugely and the lower cost of capital has helped many local borrowers rise from poverty more quickly. In addition, commercial investors have enhanced corporate governance, transparency and standardised investor reporting and operating procedures. This has made many microfinance institutions more efficient and effective.

The topic of this paper is to share current and potential industry trends, so that faith institutions can consider how best to achieve their financial and non-financial investment charter objectives. Based on the recommendations provided, it also aims to initiate an inter-faith discussion on the following topic:Considering that in the emerging markets, contrary to in the developed world, there is no minimum social security in place: Should faith institutions use their influence in the industry, to safeguard availability of sustainable poverty alleviation methodologies – like funding liquidity for microfinance, or let capitalism driven markets operate freely across the entire spectrum of the market?

3iG International Interfaith Investment Group Impact Investing: Microfinance1212

3iG International Interfaith Investment Group Impact Investing: Microfinance

2. Microfinance

133iG International Interfaith Investment Group Impact Investing: Microfinance

Microfinance is often associated with lending money to the poor. As the interest in microfinance has expanded, so has the extent of the definition. According to one of the UK’s largest microfinance charities it has a broad definition: “Microfinance is the provision of a broad range of financial services and products such as credit, savings and insurance designed to assist poor people who lack access to financial services in the mainstream banking sector to develop their small businesses, save their earnings, and guard against risks”.(Opportunity International, 2009)

Most local microfinance operators, also known as microfinance institutions (“MFIs”), have started with one element: providing small loans to local entrepreneurs. In this paper the more narrow “microcredit” definition is adopted: “Microcredit refers to very small loans for unsalaried borrowers with little or no collateral, provided by legally registered institutions”.(Microfinance Gateway, 2009)

Irrespective of the adoption of the broad or narrow definition of microfinance, the services have the aim to alleviate poverty in a sustainable way for the local population. By providing access to financial services the poor can break the poverty cycle and achieve an improved business return as source of income.Based on the poverty alleviation driver, microfinance has strong roots in the faith commu-nity. Faiths have applied social investment for many years and have been at the forefront of investing in microfinance initiatives.The United Nations designated 2005 as the year of microcredit. Its objectives included promotion of the industry, public awareness and inclusive financial sectors. The increa-sed visibility of microfinance had a strong effect on the increase of funding for the sector. The increased awareness and endorsement by the UN of microfinance as a tool to alleviate poverty has a positive effect on the industry.

2.1. What is microfinance?

3iG International Interfaith Investment Group Impact Investing: Microfinance14

Microfinance loans generally serve unsalaried workers and entrepreneurs who live in poverty. In line with the microfinance background of this paper, poverty is defined as:Poverty is a condition in which people lack satisfactory material resources (food, shelter, clothing, housing), are unable to access basic services (health, education, water, sanita-tion), and are constrained in their ability to exercise rights, share power and lend their voices to the institutions and processes which affect the social, economic and political environments in which they live and work. (Vandenberg, 2006)

Many new borrowers of microfinance loans live in poverty. Whether this means they live off more or less than the much cited “$1 per day” is not relevant. The core issue is that they do not have access to (financial) means to lift them to a minimum living standard that is deemed acceptable by more fortunate people, predominantly living in the Western world. By providing access to financial products an improvement of living standards can be reached. According to Jonathan Morduch’s 2002 working paper on “Analysis of the Effects of Microfinance on Poverty Reduction”, there is...:...ample evidence to support the positive impact of microfinance on poverty reduction as it relates to fully six out of seven of the Millennium Goals. In particular, there is overwhelming evidence substantiating a beneficial effect on income smoothing and increases to income. There is less evidence to support a positive impact on health, nutritional status and increases to primary schooling attendance. Nevertheless, the evidence that does exist is largely positive.” (Morduch, 2002)

Morduch concludes further that “microfinance, if used under the right conditions, fits the needs for a broad selection of the population”. However, microfinance lending practices are not suitable for the poorest of the poor – the destitute. Condition for a loan is a reasonable likelihood that the borrower repays capital plus interest6. This requires a prospect of(regular) income. Microfinance tends to be offered to the “top end” of the poor; people with access to shelter, clothing, regular food and income. The destitute are defined as people who do not have a stable source of income and who require shelter, clothing, access to regular food and medical care. The destitute must rely on aid and charity to improve their living standards.

SKS Foundation, the non-profit arm of SKS Microfinance (SKS Foundation, 2009), is a good example of an aid provider distinguishing between potential microfinance borrowers and the destitute. Its aim is to serve the destitute in a way to lift them to microfinance eligibility status. It does this by providing an 18 month training program in India to help economic, health and social development areas. By providing an asset (like a cow or a goat) the destitute train how to get a stable income and become independent. At the end of the 18 month program they should have moved out of the poorest of the poor category and be eligible for microfinance.

6 Capital plus interest or for Sharia loans the repayment amount

2.2. For who is microfinance suitable?

3iG International Interfaith Investment Group Impact Investing: Microfinance15

Microfinance loans to borrowers are generally provided by MFIs. MFIs range from single, voluntary staffed locations, to global, professionally staffed operations. Some MFIs rely on direct donations from individuals, foundations, faith institutions and NGOs. Such donations are used to provide lending capital, whereas interest received often contributes to cover defaults and ongoing operating expenses. Other than through donation, many MFIs are funded commercially through debt or equity participations from commercial investors, faiths institutions and NGOs.

As local growth potential is high, MFIs funded solely by faith institutions and NGOs may seek 3rd party commercial funding to expand. Additional funding boosts their ability to grow their loan portfolio and alleviate more people from poverty. Any attracted (debt) funding must however, be repaid. This is either done through refinancing or by winding down the loan portfolio.

Commercial MFIs sometimes have a social charter, but lend “sustainably”. In essence this means lending commercially, to retain continuity of operations. The commerciality brings more pressure to return an acceptable margin and parties tend to operate in a structured business like and efficient way. Training, financial reporting and collection procedures tend to be centrally prescribed, as investors maintain those as minimum quality requi-rements. When capital is available in the capital markets or through the participation in investment funds, then credit lines are made available to MFIs. In which case, the MFI can continue to make loans available to local borrowers.

2.3. Who are the providers of microfinance?

3iG International Interfaith Investment Group Impact Investing: Microfinance16

MFIs are either funded though donation, debt or equity. Funding is available from com-mercial and non-commercial (e.g. faith and NGO) investors. With the launch of peer-to-peer lending platforms, MFI funding is also sourced directly from private investors. Com-mercial and non-commercial investors tend to launch funds, also known as microfinance investment vehicles (“MIVs”). MIVs either have access to long term investor capital (faith institutions, NGOs and asset managers), or short term investor capital (capital markets). Investors either lend money to a fund (i.e. debt) or buy a unit or share in the fund (i.e. equity participation). Capital raised by the fund is invested in MFIs according to predefined terms (investment charter) and the fund manager’s investment decisions. There are various alternatives to investment funds: •InvestorscaninvestinanMFIonabi-lateralbasis.Thismeansthattheysource and manage their investments in-house. Various faith institutions and NGOs conduct their investments this way, as they might have a sister organisation that operates locally. The downside is that one might be the only investor in such MFI, which makes the MFI very reliant on the funder. Furthermore there is no risk diversification such as investing in funds. •Securitisation.Thisworksinasimilarwayasamortgagebackedsecuritisation. With (very) short term funding a portfolio is built up and then subsequently refinanced for the mid-term by means of a securitisation structure. In essence, the forecast loan portfolio receivables are bought by a separate legal entity. The periodic cash flow receivables (capital and interest from local borrowers) are used to pay interest and repayments to the investors. The investor group is tranched into low risk and high risk investors. The low risk investors have first access to any receivables, but receive a low interest rate for their investment. The high risk investors have last access to the receivables, but receive a high interest rate. If defaults are higher than expected the high risk investors will probably lose out, but if defaults are less than expected their risk taking yields them a high return. •Peer-to-peerlending.Thismethodisdesignedtocutoutany“middle-men”,i.e. MIVs. Consumers and institutional investors can become a member of a lending platform that matches borrower loan requests with available investment funds. This method is generally used by consumers, whereby screened MFIs upload a borrowing request. The consumer can then bid for (a part of) the loan. The cheapest interest rates then form part of the winning bid and the funds are allocated to the borrower. The peer-to-peer lending platform manages all allocation of funds and receivables as well as the investor administration. The screened MFI manages the local financial reporting and collections and receives a fee for this that forms part of the grossing up of the interest rate actually provided to the borrower. MyC4.com and Kiva.org are examples of peer-to-peer lending platforms.

In the next chapter an overview of the microfinance market is given. As part of that a more detailed account is provided of the above types of microfinance funders.

2.4. Who are the key funders of microfinance?

3iG International Interfaith Investment Group Impact Investing: Microfinance1717

3iG International Interfaith Investment Group Impact Investing: Microfinance

3. Background information on the microfinance market and parties

3iG International Interfaith Investment Group Impact Investing: Microfinance18

World Bank affiliate CGAP8, publishes a global progress indicator detailing barrier le-vels to traditional banking. The CGAP 2009 Financial Access Report has benchmarked financial services against those of the developed world. Policy makers and regulators in 139 countries have identified global indicators that demonstrate the barriers of traditional banking. Such restrictions result in only the wealthiest people having access to financial services. People in emerging markets hold only one quarter of deposits and loans compared to people in developed countries. Hence the poor have no significant tools to invest in their economies.

Note: Estimates for countries that did not report the number of accounts in commercial banks were generated from a statistical model that uses income per capita and various features of the financial system—such as the number of bank branches per 100,000 adults and the value of deposits per adult—to predict the number of commercial bank accounts. Where the number of accounts in nonbanks was not reported, an attempt was made to fill in data from other sources. The estimates for bank and nonbank categories were summed by country to estimate the total number of deposit accountsin each country. See the methodology appendix for more details.Source: Financial Access database.

Figure 1. The number of bank loans per 1,000 adults is correlated with economic developmentSource: (CGAP - Consultative Group to Assist the Poor / World Bank, 2009)

8 Consultative Group to Assist the Poor

3.1. Microfinance market

Least bank loans per capita. Sub-Saharan Africa most underserved

3iG International Interfaith Investment Group Impact Investing: Microfinance19

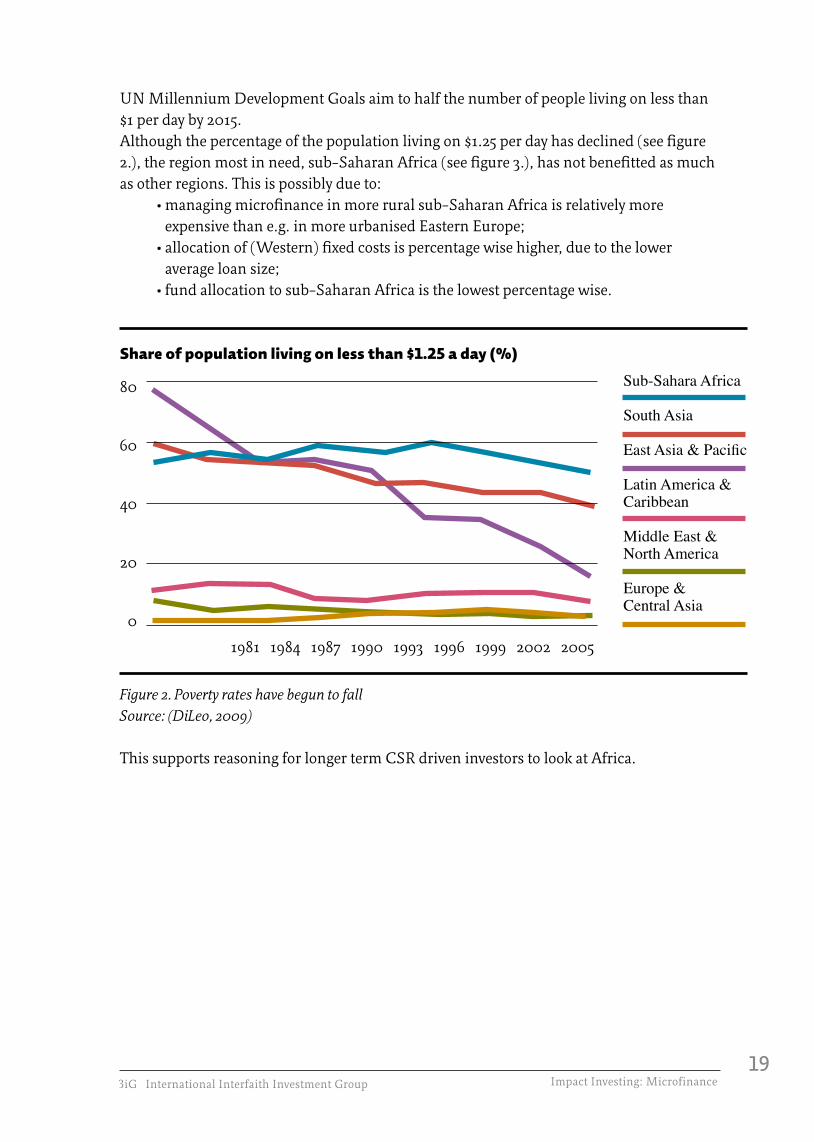

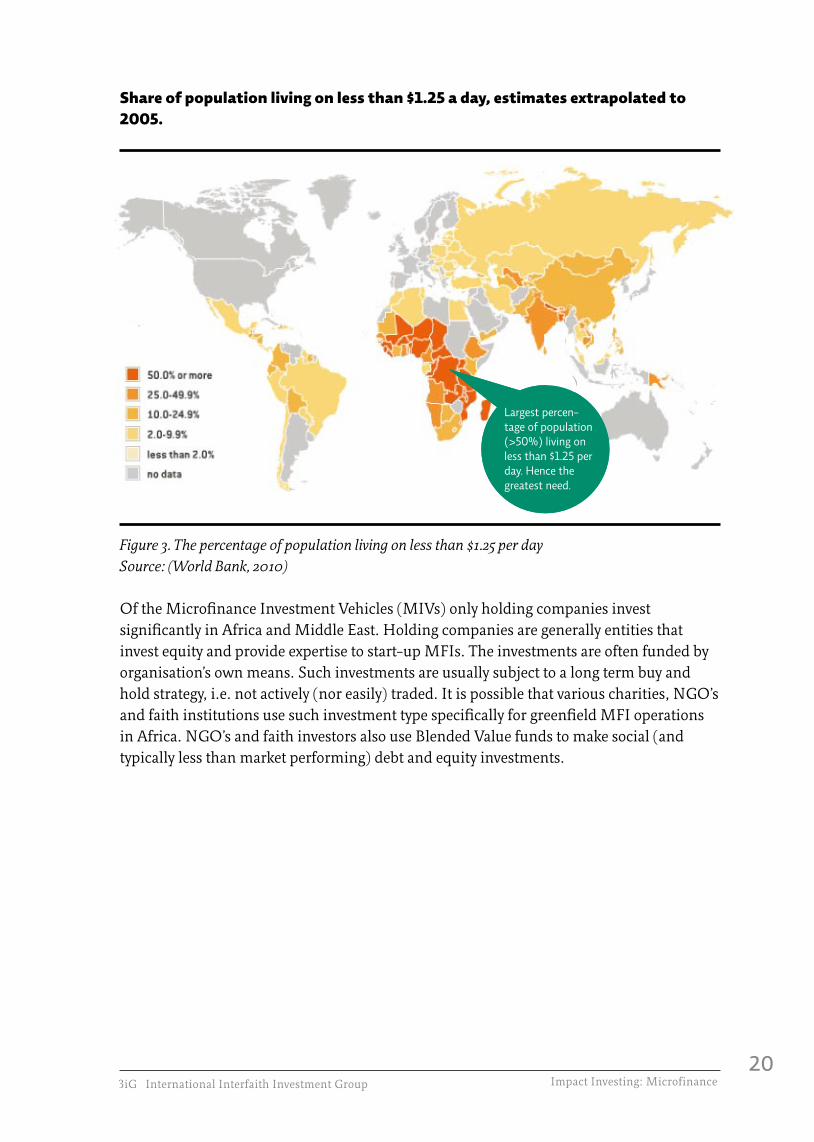

UN Millennium Development Goals aim to half the number of people living on less than $1 per day by 2015. Although the percentage of the population living on $1.25 per day has declined (see figure 2.), the region most in need, sub-Saharan Africa (see figure 3.), has not benefitted as much as other regions. This is possibly due to: •managingmicrofinanceinmoreruralsub-SaharanAfricaisrelativelymore expensive than e.g. in more urbanised Eastern Europe; •allocationof(Western)fixedcostsispercentagewisehigher,duetothelower average loan size; •fundallocationtosub-SaharanAfricaisthelowestpercentagewise.

Share of population living on less than $1.25 a day (%)

Figure 2. Poverty rates have begun to fallSource: (DiLeo, 2009)

This supports reasoning for longer term CSR driven investors to look at Africa.

80

60

40

20

0

1981 1984 1987 1990 1993 1996 1999 2002 2005

Sub-Sahara Africa

South Asia

East Asia & Pacific

Latin America &Caribbean

Middle East & North America

Europe &Central Asia

3iG International Interfaith Investment Group Impact Investing: Microfinance20

Share of population living on less than $1.25 a day, estimates extrapolated to 2005.

Figure 3. The percentage of population living on less than $1.25 per daySource: (World Bank, 2010)

Of the Microfinance Investment Vehicles (MIVs) only holding companies invest significantly in Africa and Middle East. Holding companies are generally entities that invest equity and provide expertise to start-up MFIs. The investments are often funded by organisation’s own means. Such investments are usually subject to a long term buy and hold strategy, i.e. not actively (nor easily) traded. It is possible that various charities, NGO’s and faith institutions use such investment type specifically for greenfield MFI operations in Africa. NGO’s and faith investors also use Blended Value funds to make social (and typically less than market performing) debt and equity investments.

Largest percen-tage of population (>50%) living on less than $1.25 per day. Hence the greatest need.

Largest percen-tage of population (>50%) living on less than $1.25 per day. Hence the greatest need.

3iG International Interfaith Investment Group Impact Investing: Microfinance21

An alternative to holding companies is a fund based structure as mentioned in the previous chapter. In such structures the fund manager is generally under pressure to achieve a target return. This could be the reason that fund structured MIVs tend to seek investment oppor-tunities in more mature and profitable microfinance geographies, such as Eastern Europe, Central Asia and Latin America (see figure 4 below).

Microfinance Portfolio, Main regions

Figure 4. Geographic allocation of funds by MIV typeSource: (DiLeo, 2009) It is difficult to gage the extent the emerging markets are underserved regarding financial services. Market size estimates range from USD 50bn (DiLeo, 2009) to USD300bn9 (Bo-chatay, 2009), whereas total MIV investments are estimated at $10.4bn (DiLeo, 2009).

9 Based on 1.5bn people (population on less than $2 per day and working), and multiplied by a conservative9 average loan size of $200

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Eastern Europe &Central Asia

Latin America Asia Africa & Middle East

Other

All MIV’s RegisteredMutualFunds

CommercialInvestment

Funds

StructuredFinanceVehiclesactively

managed

StructuredFinanceVehiclespassively managed

BlendedValueFunds

HoldingCompanies

PrivateEquityFunds

Only holding company MIV’s are major investors in Africa.

3iG International Interfaith Investment Group Impact Investing: Microfinance22

Of 500 million active microfinance clients, 150m have credit, 300m saving and 50m insurance products. Geographically the client group is split 70% in Asia, 20% Latin Ame-rica and 10% in other geographies (Bochatay, 2009). The substantial sub-Sahara African market is therefore largely underserved.The microfinance market can be split into various direct and indirect investors:

3.2. Parties offering microfinance services

There were 91 MIVs in the world as at 31-12-2008. Top five MIVs held a 52% market share and represented a total of USD 5.4bn of assets under management (as at 31-12-2007) (DiLeo, 2009).

The top five MIVs were: •ProCreditHolding •BlueOrchardFinance •CreditSuisseMFFundManagementCompany–responsibility •Oikocredit •OppenheimAssetManagementServices(EFSE)(DiLeo, 2009).

ProCredit Holding is a German based company that has built up 22 banks/organisations in Middle and South America, Eastern Europe and Africa. It is a social sustainability orien-tated organisation, but believes that commercial terms have to be adhered to as well. Key shareholders and funders are: IPC, KfW, FMO, IFC, TIAA-CREF, DOEN foundation and the Omidyar-Tufts Microfinance Fund (founder of eBay).

Blue Orchard Finance is a Swiss based commercial microfinance investor. Through the launch of investment funds and equity participations they attract capital, which is lent to, or invested in, MFIs. Credit Suisse and Oppenheim are global financial services players. They follow a social sustainability driven investment charter for the fund and business unit mentioned, but also aim to work on commercial terms.

Oikocredit is the only faith related (ecumenical) MIV in the top five. They drive a social sustainability investment charter, aiming in particular at underserved MFIs (smaller and more rural-based MFIs) with a clear social mission as well as financial sustainability. Their loan pricing policy is set as the higher of a. Local market price; and b. Internally calculated cost price. Not all investors might be aware that the loan pricing is at market standard.

3.2.1. Microfinance Investment Vehicles (“MIVs”)

3iG International Interfaith Investment Group Impact Investing: Microfinance23

DiLeo et al. have defined six key groupings of MIVs depending on: • thewaythefundsinvestinMFIs(provisionofdebt,equity,guaranteesora mixture), • thedriversofthefund(socialdevelopmentorcommercialdrivers),or • theownershipofthefund(mutualorshareholderstructure).An overview of these main types of funds and names of some of the key players are listed in Appendix III.

There are about 10,000 MFIs world-wide (Bochatay, 2009). The MIVs’ main challenge as a fund manager is to identify the right MFI to invest in. For MFIs on the other hand, it is often a challenge to know which MIV could be interested in their way of operating, their corporate/NGO values and beliefs. The required skill set at an MFI is wide as one might be teaching an illiterate client money and repayment concepts one day and negotiating finan-cial and legal terms with investors and lawyers the next.

Many not-for-profit organisations are related to certain focus areas, values and beliefs. This can be a certain region or village, an ethnicity or a faith. Some institutions have a policy that they lend only for proposals that meet certain borrowing criteria (white listed sectors such as agriculture and handicraft, or do not lend to blacklisted sectors such as tobacco, arms and child labour). Further acceptance criteria can involve alignment of the borrower’s faith with that of the provider of credit; certain faith institutions provide loans only to borrowers, who share the faith of the institution (Steve, 2009). Fortunately there are also faith institutions who lend indiscriminately.

As MFIs are the organisations on the ground, they have the local infrastructure and resources to train people and monitor loan proposals and collections. As many MFIs are linked to NGO’s they work with frequently changing Western volunteers and local emplo-yees. The commercial success of an MFI is often determined by the quality of the training, monitoring and procedures the organisation has in place. It is essential to run the MFI in a professional way to maximise efficient use of capital. Since the entrance of specialist data providers, such as MixMarket in 2002, comparison of the performance of MFIs has become easier. In addition specialist MFI rating agencies have launched that monitor the MFIs. MIVs rely more and more on external views when allocating investment funds to MFIs.

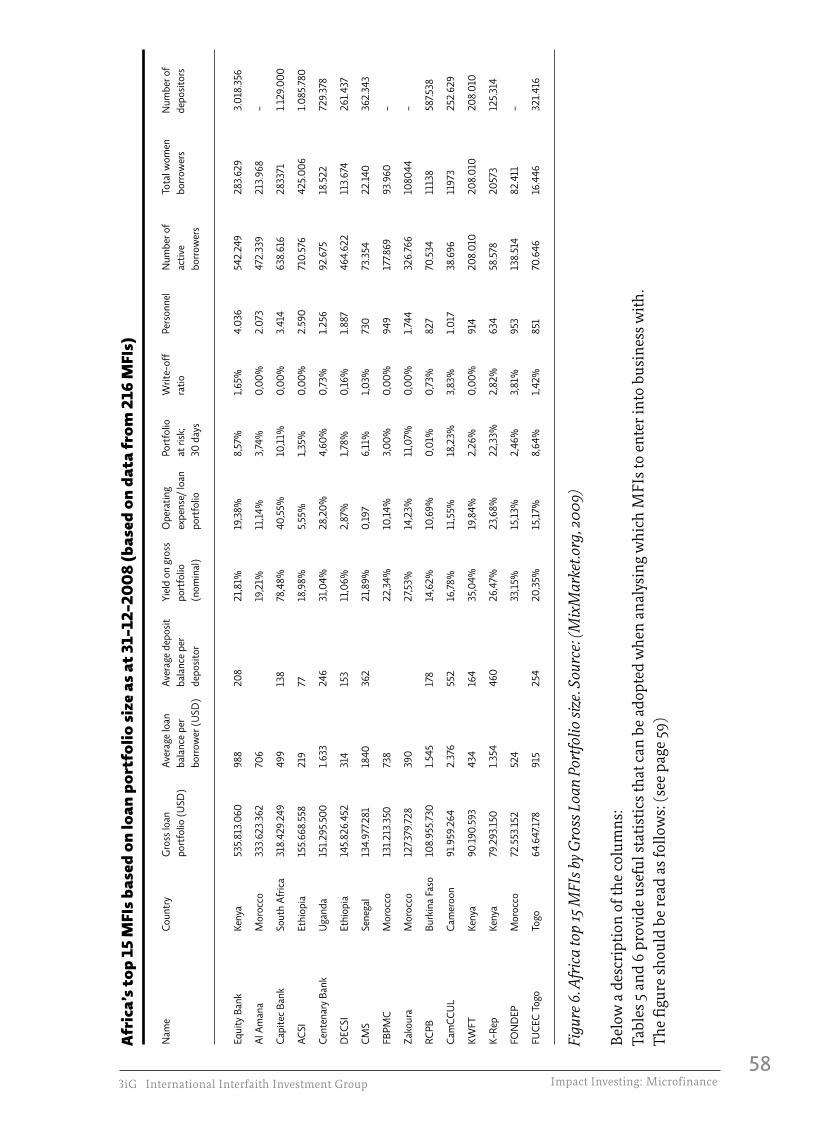

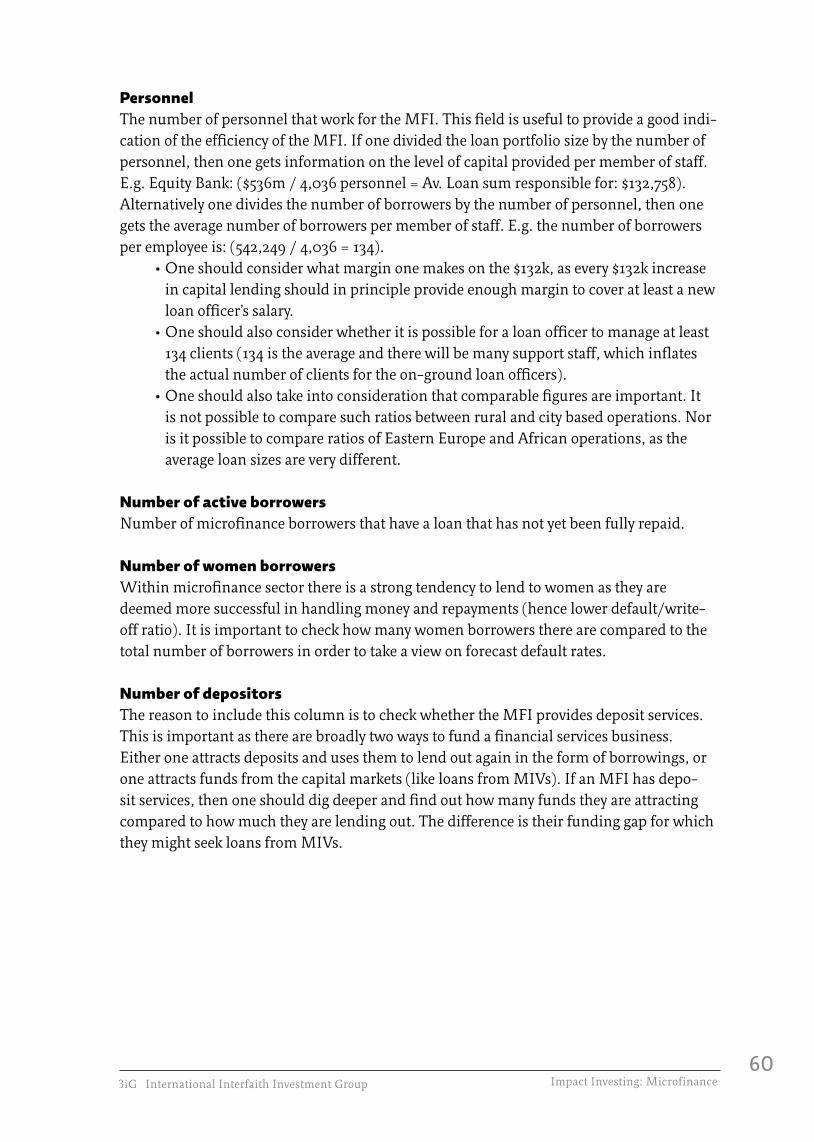

In Appendix II global and Africa focused data tables are listed, detailing the 15 largest MFIs, their portfolios and performance. The data presented is typically what a MIV fund manager would form investment decisions on. As a (potential) microfinance investor, it is advisable to analyse the presented data, as this is what one is actually investing in directly

3.2.2. Microfinance Institutions (“MFIs”)

3iG International Interfaith Investment Group Impact Investing: Microfinance24

or indirectly. Understanding of the performance measures is also helpful to verify the fund manager’s decisions and asset allocation.

As indicated there are thousands of MFIs. Some are funded exclusively; others operate through donation and/or multiple funding lines. For a better understanding of the activi-ties of MFIs one could review information from prominent global organisations that operate own or partner with third party local MFIs. Examples of such global organisations are FINCA, Grameen, Opportunity International, Shared-interest, Women’s World Banking and ACCION.

Peer-to-peer (“P2P”) lenders are parties who provide a matching facility to investors and MFIs/borrowers. Although the name might suggest a form of lending, they do not take any lending risk. An online broker infrastructure is provided to match investors directly with microfinance borrowers or MFI’s and take a commission for doing so. Different P2P players operate differently:

MyC4.com is a Danish based co-operative company that provides a service to African en-trepreneurs to submit a preset application form with their borrowing requirements and ca-pital allocation reason. Members of MyC4.com submit bids for a loan proposal, detailing capital amount and interest rate. The most competitive bids get selected and the “winning” lenders form part of a syndicate to the respective borrower. Each investor receives their pro-rata share of interest and repayment and MyC4.com takes care of the investor admi-nistration. Any defaults are also split pro-rata the investor capital contributions. Upon repayment of the loan the investor receives their capital back and can choose to re-invest in a new loan proposal. Since launch, over 16,000 investors have lent almost Euro 10.5m. According to user experiences on blogs, MyC4 is not fully transparent in calculating the interest rate. Users are confronted with local withholding taxes and (deemed) unreasona-ble exchange rates as all loans are made in local currency. However, the latter is disclosed clearly and investors simply have to price such risks and rates in, if they want to invest in different jurisdictions with little traded local currencies. It is not believed that MyC4 is making any gain/loss on the currency risk; simply small loan sizes have less favourable ex-change rates. Such risks also occur for MIV investors, although with such fund structures the FX exposure is pooled and swapped on a total portfolio basis.

MyC4 has encountered some unfortunate MFI selection choices, which has resulted in high default rates in the past (Costa, 2009). Despite some negative blogs and press, MyC4 is probably one of the best organised and presented P2P service providers. They are also leading from a social and sustainability point of view as the entity is a co-operative.Kiva.org is a non-profit US based P2P provider that operates in a similar way to MyC4, except that the “philanthropic” lenders (usually people in the global north) do not receive any interest on their loan. It also has pre-selected MFIs who upload the entrepreneur’s

3.2.3. Peer-to-peer lenders

3iG International Interfaith Investment Group Impact Investing: Microfinance25

borrowing request. But opposed to investors bidding for loans, they simply allocate a loan amount (minimum $25). It is in essence almost a donation, which upon repayment of the loan, is returned to the lender for withdrawal (but with a request for it to be donated in full to Kiva, for re-lending by Kiva itself).

Although Kiva is one of the largest P2P providers and is endorsed by many respectable foundations and MIVs, it has had some negative press (Microfinance Gateway, 2008). This was based on the procedure that Kiva goes through when allocating funds through MFIs. The investor is led to believe that they are investing in a certain entrepreneur and business case, whereas in reality the MFI receives the funds from Kiva and can allocate accordingly to current business propositions. Kiva now clearly states on its website that the MFIs pre-lend to the borrowers and then submit funding requests to Kiva lenders. Hence the

Peer-to-peer (“P2P”) lenders are parties who provide a matching facility to investors and MFIs/borrowers. Although the name might suggest a form of lending, they do not take any lending risk. An online broker infrastructure is provided to match investors directly with microfinance borrowers or MFI’s and take a commission for doing so. Different P2P players operate differently:

MyC4.com is a Danish based co-operative company that provides a service to African en-trepreneurs to submit a preset application form with their borrowing requirements and ca-pital allocation reason. Members of MyC4.com submit bids for a loan proposal, detailing capital amount and interest rate. The most competitive bids get selected and the “winning” lenders form part of a syndicate to the respective borrower. Each investor receives their pro-rata share of interest and repayment and MyC4.com takes care of the investor admi-nistration. Any defaults are also split pro-rata the investor capital contributions. Upon repayment of the loan the investor receives their capital back and can choose to re-invest in a new loan proposal. Since launch, over 16,000 investors have lent almost Euro 10.5m. According to user experiences on blogs, MyC4 is not fully transparent in calculating the interest rate. Users are confronted with local withholding taxes and (deemed) unreasona-ble exchange rates as all loans are made in local currency. However, the latter is disclosed clearly and investors simply have to price such risks and rates in, if they want to invest in different jurisdictions with little traded local currencies. It is not believed that MyC4 is making any gain/loss on the currency risk; simply small loan sizes have less favourable ex-change rates. Such risks also occur for MIV investors, although with such fund structures the FX exposure is pooled and swapped on a total portfolio basis.

MyC4 has encountered some unfortunate MFI selection choices, which has resulted in high default rates in the past (Costa, 2009). Despite some negative blogs and press, MyC4 is probably one of the best organised and presented P2P service providers. They are also leading from a social and sustainability point of view as the entity is a co-operative.Kiva.org is a non-profit US based P2P provider that operates in a similar way to MyC4, except that the “philanthropic” lenders (usually people in the global north) do not receive any interest on their loan. It also has pre-selected MFIs who upload the entrepreneur’s borrowing request. But opposed to investors bidding for loans, they simply allocate a loan

3iG International Interfaith Investment Group Impact Investing: Microfinance26

amount (minimum $25). It is in essence almost a donation, which upon repayment of the loan, is returned to the lender for withdrawal (but with a request for it to be donated in full to Kiva, for re-lending by Kiva itself).

Although Kiva is one of the largest P2P providers and is endorsed by many respectable foundations and MIVs, it has had some negative press (Microfinance Gateway, 2008). This was based on the procedure that Kiva goes through when allocating funds through MFIs. The investor is led to believe that they are investing in a certain entrepreneur and business case, whereas in reality the MFI receives the funds from Kiva and can allocate accordingly to current business propositions. Kiva now clearly states on its website that the MFIs pre-lend to the borrowers and then submit funding requests to Kiva lenders. Hence the perception of a lender funding a specific borrower is somewhat reduced. In November 2009, four years after its trading practices started, Kiva exceeded a cumulative loan origina-tion value of $100m. Throughout the four years they had brought together 573,000 lenders and 239,000 local entrepreneurs. (Techcrunch, 2009)

MicroPlace is a for-profit P2P provider in the US. It was bought by eBay in 2008, a year after its launch. This platform does not provide access to local borrowers, but to MIVs and MFIs. The investor can choose what MFIs they would like to lend money to, or participate by subscribing to a MIV equity offering or investment fund. The MIV then loans the funds on to the MFI under their own conditions.

Two MIVs that use MicroPlace to offer their funds to consumers are Calvert and Oiko-credit. This is a convenient way to tap the individual investor market (opposed to institu-tional investors and members (e.g. churches with Oikocredit).

MicroPlace investors receive a return of about 1.25% - 3% p.a., but is only accessible for US citizens. The average loan term is 27 months, in comparison to Kiva’s average loan term of approximately 10 months. The difference is that one invests in multiple loans, whereas with Kiva funds are returned at the end of each local loan. (Microfinance Gateway, 2008)Veecus is a French based limited liability company that operates in a similar way to Kiva. One lends the money for 0% interest, but the MFI is the counterparty and takes any default risk. The funds are allocated to individual borrowers that the investor has selected. Veecus makes a return by receiving a one-off new investor fee and a kick-back from MFIs for bringing in loans (the cost of which is obviously added to the borrower’s rate).OptINnow is a platform run by Opportunity International. It operates from a donation perspective opposed to an investor lending platform.

3iG International Interfaith Investment Group Impact Investing: Microfinance27

Service providers are in principle all other parties who provide ancillary services to micro-finance clients, MFIs, MIVs and investors. Examples are: •specialistMFIratingagencies(e.g.PlanetFinance); •MFIdatacollectorswhoofferperformancereportsandstatistics (e.g. mixmarket.org); • researchproviders(e.g.CGAP,MicrocapitalandMicrofinance-gateway) • tradebodiesofprofessionals(e.g.intheUKMicrofinanceAssociationand MicrofinanceClubUK) •advisoryserviceproviderslikeconsultancies(M2iandGFA) •otherssuchassupportingacademic,government,aid,accountancy,legaland faith organisationsWith the sector becoming more mature and the increased interest of commercial investors, the need for service providers has increased. It is difficult to collect and generate timely and comparable data as the sector is relatively young, fragmented and subject to many different local disclosure laws and regulations. The research houses and rating agencies rely on local MFIs to process data in a predetermined way. Key challenges obtaining data are often local as MFIs are staffed by volunteers and local loan officers. They might be unaware of the context and importance of certain Q&A’s. Communication and distances are also contribu-tors. Data is often logged by hand and then typed up when back at the MFI base. If infor-mation is unclear or missing, it might be a week/month before the loan officer can visit a specific region again.

3.2.4. Service providers

3iG International Interfaith Investment Group Impact Investing: Microfinance28

When one thinks of microfinance borrowers, one often thinks of individuals. In reality many loans are made to groups of borrowers, cooperatives, companies and schools. Individual borrowers: The Grameen model is generally adopted when dealing with indi-viduals: a group of (5-20) individuals present themselves as borrower group and enrol on financial training. Each individual is responsible for interest and repayments of any group member loan. This creates a high degree of social control and low default rates. It also creates a high degree of transparency and due diligence of new lending proposals. Cooperatives: Cooperatives are businesses in which the workers and/or other stakeholders have an equity share. Examples are microfinance loans to agrarian businesses, whereby the workers receive a profit share or a local bank/MFI, whereby the borrowers and depositors have an equity share, based on the custom they contribute (like Sparkassen in Germany and Building Societies in the UK).Company loans: Typical examples are loans to exporters of fair trade goods and SME’s (“small and medium sized enterprises”). Loans to very small companies (drink or telecom booths) are usually structured as a loan to an individual. Schools: Loans to schools are often made by charities opposed to by commercial microfi-nance investors. However, with the increase in sustainability benchmarks, ever more MFIs need to measure and demonstrate what social benefits their operations are delivering to local communities. This has resulted in an increase in social projects by MFIs as it influences their chances to attract funding. Funders might wish to reconsider whether MFIs are best positioned and skilled to launch and deliver on social projects (like schools and medical care).

3.3. Types of borrowers to lend to

3iG International Interfaith Investment Group Impact Investing: Microfinance2929

3iG International Interfaith Investment Group Impact Investing: Microfinance

4. Background to the risks associated with investing in microfinance

3iG International Interfaith Investment Group Impact Investing: Microfinance30

In the West we are used to warnings related to financial products. “Shares can go up or down”, “Do not invest more than you can lose”, “Your home might be at risk if you do not keep up mortgage payments”, etc, etc. Unlike financial services companies, the micro-finance market is lightly regulated and if regulated done so according to many different standards and jurisdictions. Although most investors are institutional, hence of professional nature, there are also consumers that seek to invest or donate. Irrespective of one’s experience in investment markets, it is wise to take note of the encountered risks when investing through certain investment vehicles.

4.1. Risks of microfinance investments

3iG International Interfaith Investment Group Impact Investing: Microfinance31

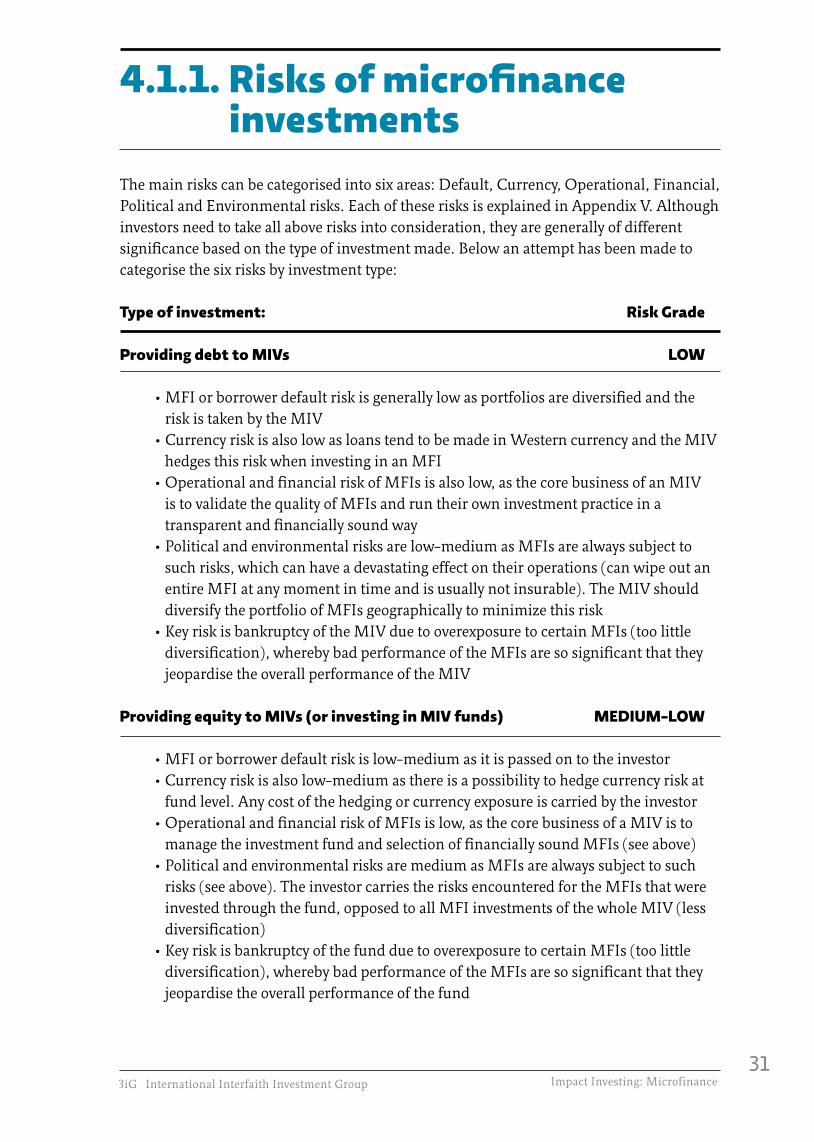

The main risks can be categorised into six areas: Default, Currency, Operational, Financial, Political and Environmental risks. Each of these risks is explained in Appendix V. Although investors need to take all above risks into consideration, they are generally of different significance based on the type of investment made. Below an attempt has been made to categorise the six risks by investment type:

Type of investment: Risk Grade

Providing debt to MIVs LOW •MFIorborrowerdefaultriskisgenerallylowasportfoliosarediversifiedandthe risk is taken by the MIV •CurrencyriskisalsolowasloanstendtobemadeinWesterncurrencyandtheMIV hedges this risk when investing in an MFI •OperationalandfinancialriskofMFIsisalsolow,asthecorebusinessofanMIV is to validate the quality of MFIs and run their own investment practice in a transparent and financially sound way •Politicalandenvironmentalrisksarelow-mediumasMFIsarealwayssubjectto such risks, which can have a devastating effect on their operations (can wipe out an entire MFI at any moment in time and is usually not insurable). The MIV should diversify the portfolio of MFIs geographically to minimize this risk •KeyriskisbankruptcyoftheMIVduetooverexposuretocertainMFIs(toolittle diversification), whereby bad performance of the MFIs are so significant that they jeopardise the overall performance of the MIV

Providing equity to MIVs (or investing in MIV funds) MEDIUM-LOW •MFIorborrowerdefaultriskislow-mediumasitispassedontotheinvestor •Currencyriskisalsolow-mediumasthereisapossibilitytohedgecurrencyriskat fund level. Any cost of the hedging or currency exposure is carried by the investor •OperationalandfinancialriskofMFIsislow,asthecorebusinessofaMIVisto manage the investment fund and selection of financially sound MFIs (see above) •PoliticalandenvironmentalrisksaremediumasMFIsarealwayssubjecttosuch risks (see above). The investor carries the risks encountered for the MFIs that were invested through the fund, opposed to all MFI investments of the whole MIV (less diversification) •KeyriskisbankruptcyofthefundduetooverexposuretocertainMFIs(toolittle diversification), whereby bad performance of the MFIs are so significant that they jeopardise the overall performance of the fund

4.1.1. Risks of microfinance investments

3iG International Interfaith Investment Group Impact Investing: Microfinance32

Type of investment: Risk Grade

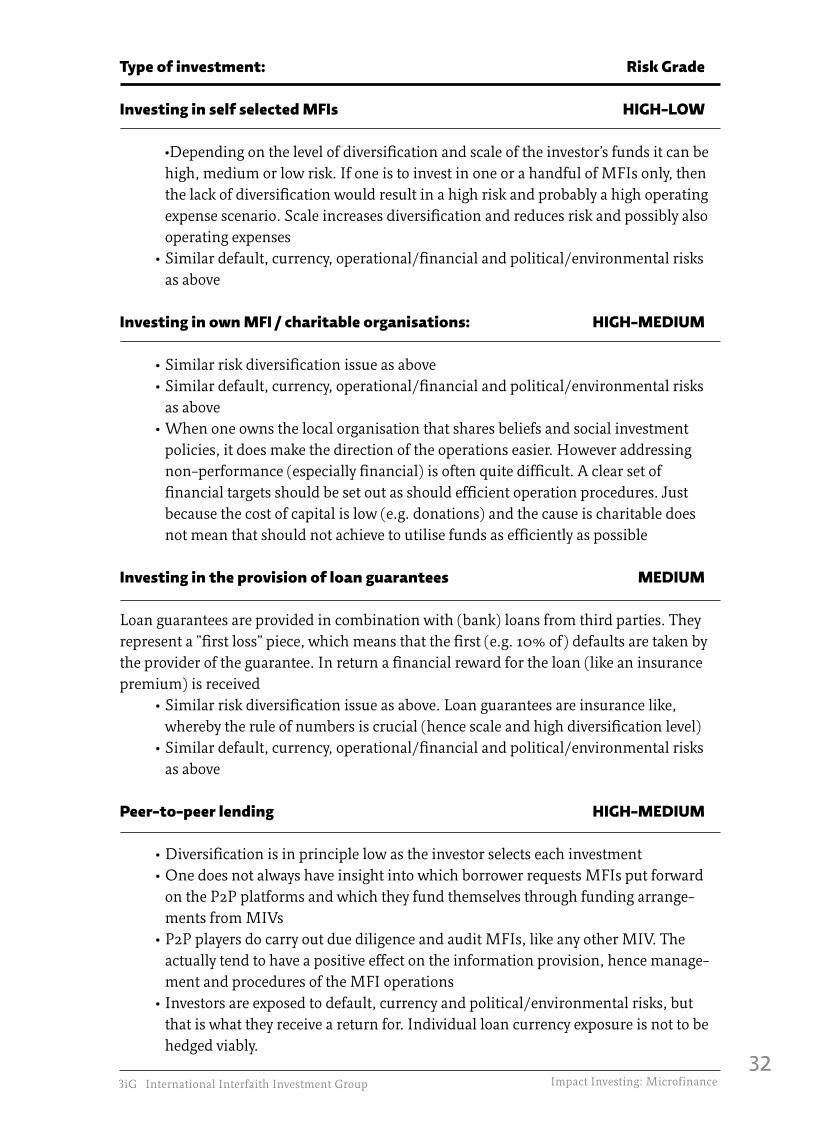

Investing in self selected MFIs HIGH-LOW •Dependingonthelevelofdiversificationandscaleoftheinvestor’sfundsitcanbe high, medium or low risk. If one is to invest in one or a handful of MFIs only, then the lack of diversification would result in a high risk and probably a high operating expense scenario. Scale increases diversification and reduces risk and possibly also operating expenses •Similardefault,currency,operational/financialandpolitical/environmentalrisks as above

Investing in own MFI / charitable organisations: HIGH-MEDIUM

•Similarriskdiversificationissueasabove •Similardefault,currency,operational/financialandpolitical/environmentalrisks as above •Whenoneownsthelocalorganisationthatsharesbeliefsandsocialinvestment policies, it does make the direction of the operations easier. However addressing non-performance (especially financial) is often quite difficult. A clear set of financial targets should be set out as should efficient operation procedures. Just because the cost of capital is low (e.g. donations) and the cause is charitable does not mean that should not achieve to utilise funds as efficiently as possible

Investing in the provision of loan guarantees MEDIUM Loan guarantees are provided in combination with (bank) loans from third parties. They represent a “first loss” piece, which means that the first (e.g. 10% of) defaults are taken by the provider of the guarantee. In return a financial reward for the loan (like an insurance premium) is received •Similarriskdiversificationissueasabove.Loanguaranteesareinsurancelike, whereby the rule of numbers is crucial (hence scale and high diversification level) •Similardefault,currency,operational/financialandpolitical/environmentalrisks as above

Peer-to-peer lending HIGH-MEDIUM •Diversificationisinprinciplelowastheinvestorselectseachinvestment •OnedoesnotalwayshaveinsightintowhichborrowerrequestsMFIsputforward on the P2P platforms and which they fund themselves through funding arrange- ments from MIVs •P2PplayersdocarryoutduediligenceandauditMFIs,likeanyotherMIV.The actually tend to have a positive effect on the information provision, hence manage- ment and procedures of the MFI operations • Investorsareexposedtodefault,currencyandpolitical/environmentalrisks,but that is what they receive a return for. Individual loan currency exposure is not to be hedged viably.

3iG International Interfaith Investment Group Impact Investing: Microfinance3333

3iG International Interfaith Investment Group Impact Investing: Microfinance

5. Current microfinance trends

3iG International Interfaith Investment Group Impact Investing: Microfinance34

A successful and sustainable funding methodology is that of attracting local deposits. Intuitively one would consider that people living in poverty have no savings, but quite the contrary is true. Lack of banking services has resulted in many people holding cash for e.g. medical emergencies and family member funerals. Holding cash is a significant risk due to criminality. It is not uncommon to pay deposit takers to take care of one’s (non-interest bearing) cash. In the developed world it is standard practice to receive interest on depo-sited funds. In emerging markets people often pay to have their funds safe guarded. This creates an interesting commercial business opportunity as deposited funds can be lent out as microfinance loans.

Deposit schemes are not only commercially interesting from an interest margin point of view. From a default risk perspective on microfinance loans, they are also interesting. Local communities have started using terms like “hot money” and “cold money” to distinguish between microfinance funding from local sources (hot) and developed world sources (cold). The incentive to repay any loan financed locally (hot money) is higher than one financed with cold money. A default on a hot money loan might lead to one’s neighbour or village elder knocking on one’s door.

The deposit scheme trend is also important as it contributes to a sustainable long term source of funding for microfinance loans. Funding through local deposits makes borrowers less reliant on external funding. This means they are less likely to attract volatile capital markets funding. The local community also remains shareholder of the local microfinance lending entity, which means that any profits are redeployed locally.

5.1. Local funding through deposit schemes

3iG International Interfaith Investment Group Impact Investing: Microfinance35

In the run up to the credit crunch of 2007-08 MFIs streamlined their operations by imple-menting standardised procedures and reporting. Due to the decline in the capital markets most MFIs found it difficult secure refinancing of their portfolios, let alone meet local borrower demand. With markets recovering private equity investors are returning to seek out “bargains” in the microfinance investment arena. The MFIs that have survived are likely to have sound operating standards and healthy loan portfolios.

If one is to apply the same key valuation drivers to microfinance operations in emerging markets to those of financial services companies in the developed world, then one can con-clude that the opportunity value is much more than simply the return on the loan portfolio. Financial firms in the developed world build up client portfolios and information on their clients. The ownership of the client and their purchase behaviour, gives the firm the opportunity to cross-sell more products. The consumer credit data and purchase behaviour is valuable in itself. Some firms choose to sell this data to third parties in the form of leads. In emerging markets there is very little data on consumer purchase behaviour. Most countries don’t even have basic census data. Investors that own and monitor client portfolios should consider the value, as microfinance clients of today, shall be bank clients of tomorrow.

Private equity investors could benefit substantially by taking equity shares in MFIs with the aim to achieve a substantial retail distribution network. The exit would be to sell such network to a financial services company or retail/telecoms company offering financial services and other cross-sell opportunities.

With regard to this point, faith institution investors may consider two elements: •whethertoletcommercialinvestorscreamoffthetopoftheMFImarket,asthe loss of the well yielding MFIs shall jeopardise the sustainability of their overall investment portfolio; and •whetherlettingprivateequityinvestorstakingequitystakesinMFIsismore beneficial to local communities in the long term, than offering local communities the services and earn-out opportunities in the form of co-operative structures.

The crux of the above is whether any future profits to third party investors are repatriated to the existing shareholders or redeployed in local communities in order to speed up poverty alleviation. Furthermore, to what extent are investments in MFIs purely related to com-mercial financial services vs. alleviation of poverty and provision of basic human needs?

5.2. Increase in commercial investors taking equity stakes in MFIs

3iG International Interfaith Investment Group Impact Investing: Microfinance36

Commercial investors’ initial entrance to the market introduced standardisation of opera-ting procedures and reporting. This brought a greater transparency and improved corpora-te governance. The microfinance market was booming and poverty alleviation was ramping up. Due to the economic downturn in 2007-08, underperforming MFIs were confronted with difficulty to attract funding. Commercial investors became more selective in funding and extending credit lines to MFIs throughout 2008-09.

Although the positive of the initial increased investor appetite was largely welcomed, nobody expected the backlash of them leaving so abruptly. Having funded the industry due to the low cost of capital from the debt capital markets, the MFIs found themselves having to turn down credit requests from local borrowers. Undoubtedly some of those borrowers had been teased with escaping poverty by the provision of previous loans, only to be dropped back into poverty due to the combination of market conditions and the way MFIs had sourced funding.

Although the microfinance market benefits from increased competition in the short run, it can have a damaging effect in the long term. Commercial investors tend to have access to relatively short term capital markets funding (less than 5 years), whereas true sustainability comes from cash rich non-commercial investors, who can bridge market downturns.

One should take into consideration that, unlike in the developed world, microfinance based financial services are a substitute for a non-existent social welfare system. Taking something away that one has previously enjoyed is much more painful than missing the same level of service when one has never experienced it. Let alone, when it involves basic human needs11.

Short term based capital markets funding contributes an undesirable volatility that can jeopardise the sustainable provision of basic human needs. In order to counter this, the microfinance industry should consider only long term funding commitments (20-30 years) to be acceptable, thereby safeguarding sustainability of serving (the lower end of) the industry.

11 This issue has not been highlighted much in the press. Possibly as it encompasses multiple facets of the microfinance and financial services industries and because the entrance of short term funded investors has highlighted and expanded the success of microfinance. The volatility and liquidity issues of short term funding are however particularly negative, possibly even immoral. One could compare it with a donor physically offering food to a nation subject to starvation and then before they could consume it taking it away again. According to today’s moral standards, such behaviour would be widely deemed cruel and unjust.

5.3. The emergence of short term capital markets funding

3iG International Interfaith Investment Group Impact Investing: Microfinance37

Based on Porter’s Five forces framework (Porter, 1979) and a PESTEL analysis the potential shift in market positioning of investors is summarised in a directional policy matrix (Robinson, 1978).

Source: (Porter, 1979)

PEST(EL) analysis

Factor

Political

Economic

Socio-cultural

Technological

Environmental

Legal

Impact

Regulatory landscape is increasinglytransparent and homogeneous

Demand > Supply and recent downturn exposed difference professionality amongst MFIs

Microfinance becoming more known and accepted locally. Initiatives by locals also increasing

Increased transparency, which resulted in efficiency and lower rates

Increased wealth has a negative effect on environment

Microfinance is locally and internationally

Response

Acceleration of commercial investors as entry barriers decrease

Private equity firms funding and acquiring financial sector retail operations

Sector must be educated (people & MFI staff) on concept of profit. Otherwise it will turn into a hard lesson when commercial investors have control of the sector

Has made sector more attractive, calculable, hence investable. Entry barriers have reduced

None, as global wealth parity has higher importance

Legal costs declining. Entry barriers reduced

5.4. Effect of above market trends on faith investors’ market share

Threat of new entrants (High risk)• High due to low capital markets funding• High due to funder appetite for Impact Investments

Internal rivalryCurrent market places shall undergo significant changes due to new entrants and commercialisation

Suppliers (High risk)Faith Investment Funds are long term. Whereas capital markets funds are cheaper, but short term and more volatile

Customers (Low risk)Demand > Supply

Threat of substitute (Medium risk)• Low as charity donations are stable• High if local deposit schemes become the new funding mechanism

3iG International Interfaith Investment Group Impact Investing: Microfinance38

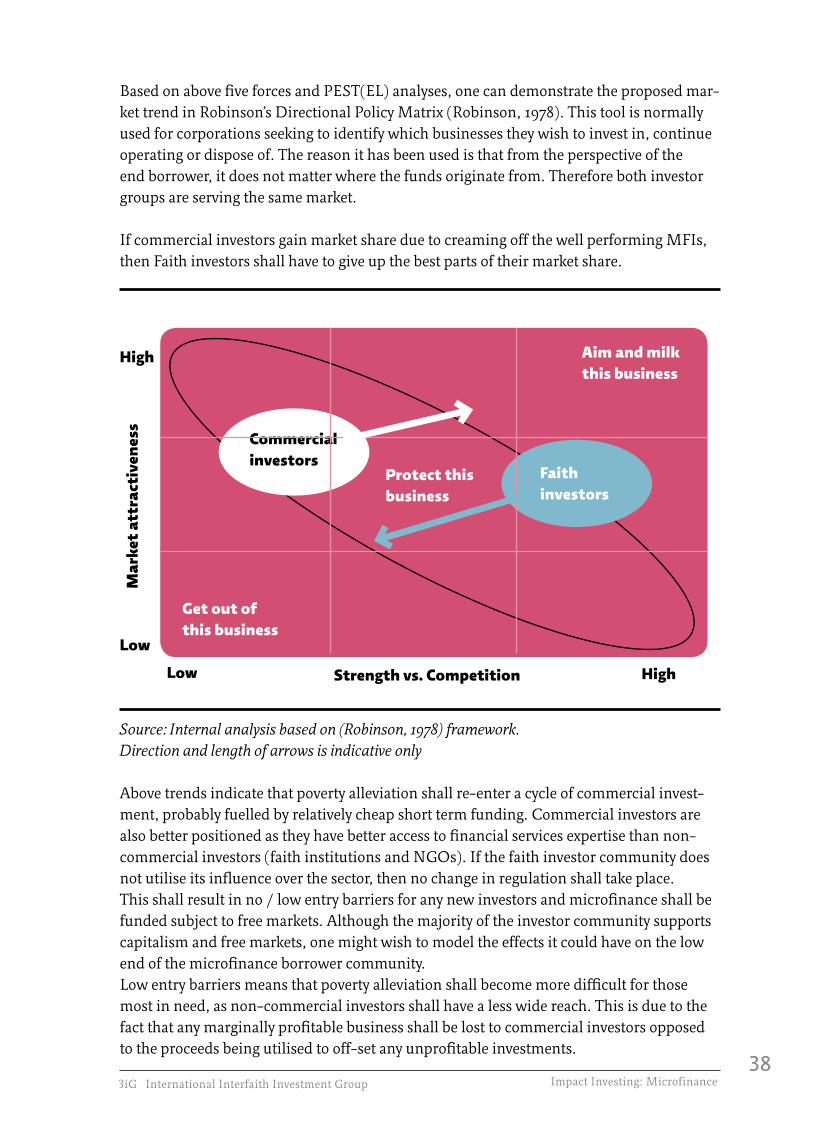

Based on above five forces and PEST(EL) analyses, one can demonstrate the proposed mar-ket trend in Robinson’s Directional Policy Matrix (Robinson, 1978). This tool is normally used for corporations seeking to identify which businesses they wish to invest in, continue operating or dispose of. The reason it has been used is that from the perspective of the end borrower, it does not matter where the funds originate from. Therefore both investor groups are serving the same market.

If commercial investors gain market share due to creaming off the well performing MFIs, then Faith investors shall have to give up the best parts of their market share.

Source: Internal analysis based on (Robinson, 1978) framework.Direction and length of arrows is indicative only

Above trends indicate that poverty alleviation shall re-enter a cycle of commercial invest-ment, probably fuelled by relatively cheap short term funding. Commercial investors are also better positioned as they have better access to financial services expertise than non-commercial investors (faith institutions and NGOs). If the faith investor community does not utilise its influence over the sector, then no change in regulation shall take place. This shall result in no / low entry barriers for any new investors and microfinance shall be funded subject to free markets. Although the majority of the investor community supports capitalism and free markets, one might wish to model the effects it could have on the low end of the microfinance borrower community.Low entry barriers means that poverty alleviation shall become more difficult for those most in need, as non-commercial investors shall have a less wide reach. This is due to the fact that any marginally profitable business shall be lost to commercial investors opposed to the proceeds being utilised to off-set any unprofitable investments.

High

Mar

ket

attr

acti

vene

ss

Strength vs. Competition

Low

Low

Get out ofthis business

Aim and milkthis business

Protect thisbusiness

High

Faithinvestors

Commercialinvestors

3iG International Interfaith Investment Group Impact Investing: Microfinance3939

3iG International Interfaith Investment Group Impact Investing: Microfinance

6. Recommendations

3iG International Interfaith Investment Group Impact Investing: Microfinance40

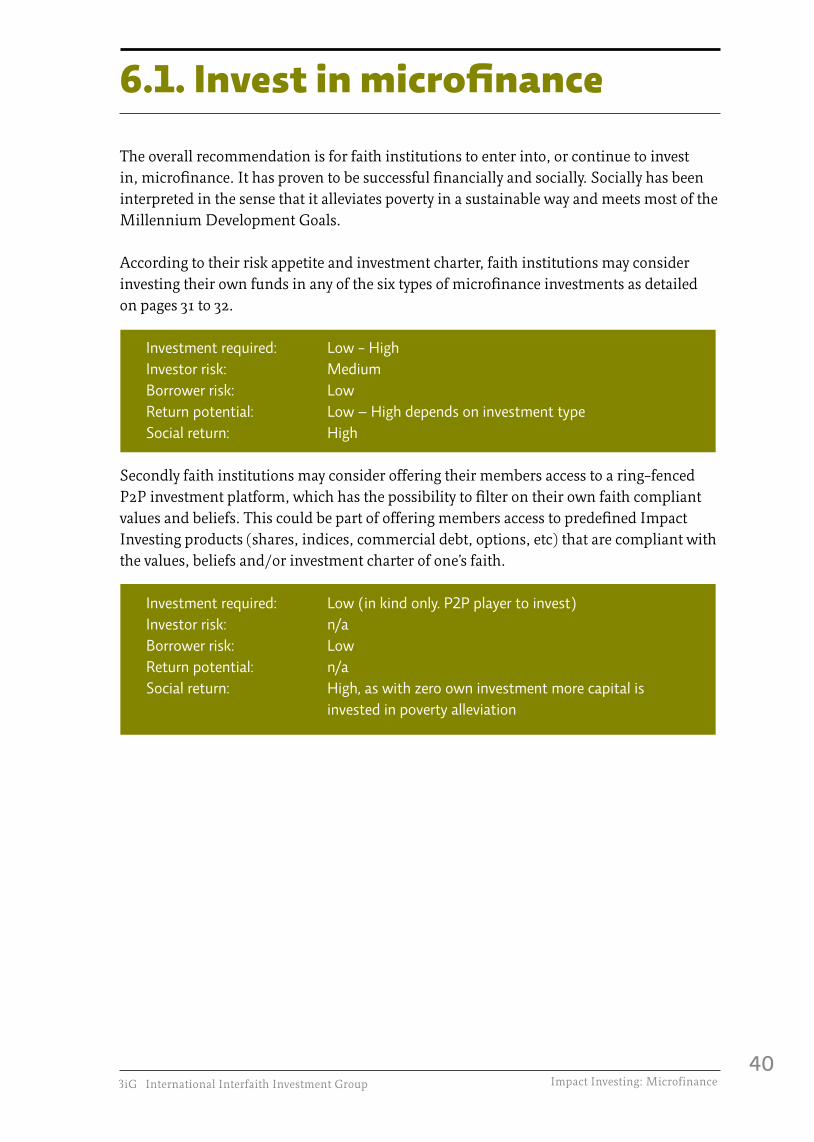

The overall recommendation is for faith institutions to enter into, or continue to invest in, microfinance. It has proven to be successful financially and socially. Socially has been interpreted in the sense that it alleviates poverty in a sustainable way and meets most of the Millennium Development Goals.

According to their risk appetite and investment charter, faith institutions may consider investing their own funds in any of the six types of microfinance investments as detailed on pages 31 to 32.

Investment required: Low - High Investor risk: Medium Borrower risk: Low Return potential: Low – High depends on investment type Social return: High

Secondly faith institutions may consider offering their members access to a ring-fenced P2P investment platform, which has the possibility to filter on their own faith compliant values and beliefs. This could be part of offering members access to predefined Impact Investing products (shares, indices, commercial debt, options, etc) that are compliant with the values, beliefs and/or investment charter of one’s faith.

Investment required: Low (in kind only. P2P player to invest) Investor risk: n/a Borrower risk: Low Return potential: n/a Social return: High, as with zero own investment more capital is invested in poverty alleviation

6.1. Invest in microfinance

3iG International Interfaith Investment Group Impact Investing: Microfinance41

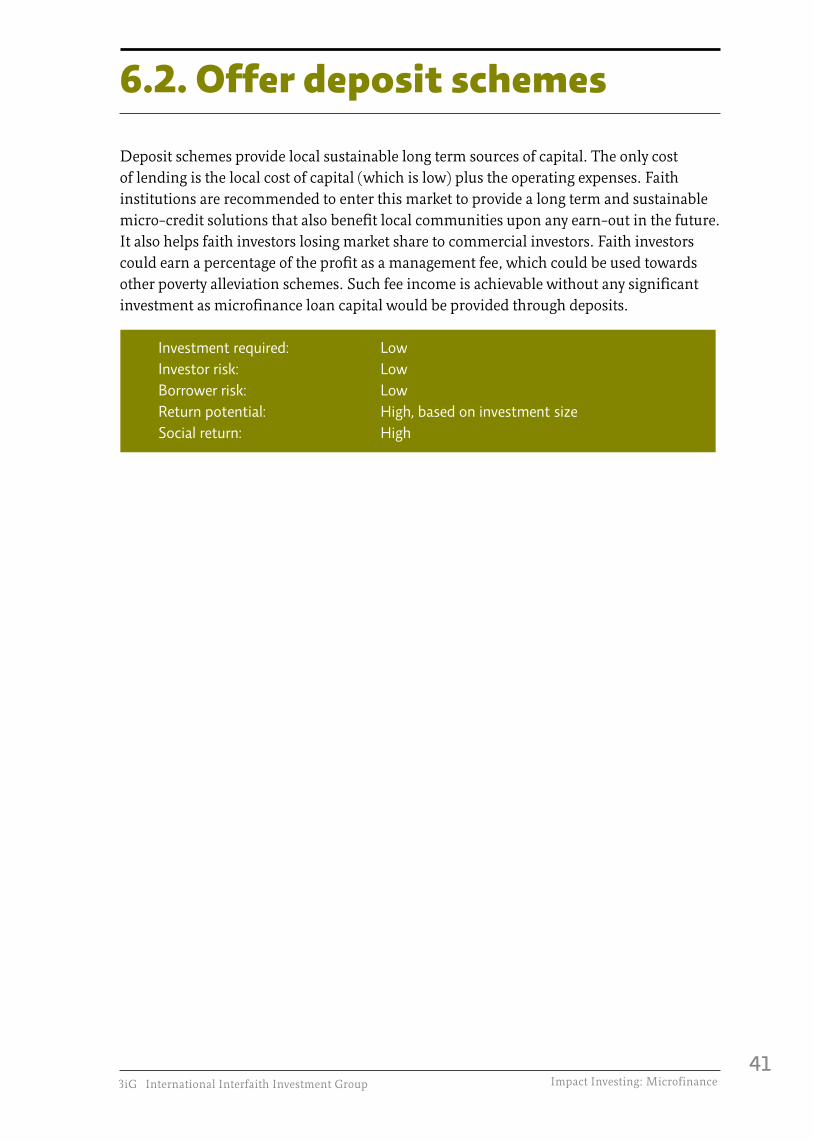

Deposit schemes provide local sustainable long term sources of capital. The only cost of lending is the local cost of capital (which is low) plus the operating expenses. Faith institutions are recommended to enter this market to provide a long term and sustainable micro-credit solutions that also benefit local communities upon any earn-out in the future. It also helps faith investors losing market share to commercial investors. Faith investors could earn a percentage of the profit as a management fee, which could be used towards other poverty alleviation schemes. Such fee income is achievable without any significant investment as microfinance loan capital would be provided through deposits.

Investment required: Low Investor risk: Low Borrower risk: Low Return potential: High, based on investment size Social return: High

Investment required: Low (in kind only. P2P player to invest) Investor risk: n/a Borrower risk: Low Return potential: n/a Social return: High, as with zero own investment more capital is invested in poverty alleviation

6.2. Offer deposit schemes

3iG International Interfaith Investment Group Impact Investing: Microfinance42

If commercial investors only seek to invest in the profitable side of microfinance, then non-commercial investors are driven out of the market. The result is that the size of the non-profitable investment portfolio shall shrink as it is not funded by the proceeds of the profitable side.