rotman international trading competition 2011tradingteam/ritc2011-case-package... · rotman...

TRANSCRIPT

Rotman

International

Trading

Competition

2011

Ca

se P

ack

ag

e

2

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Table of Contents

11 Interest Rates Case

32 CIBC Algorithmic HFT Case

6 Case Summaries

29 Thomson Reuters QED

23 BP Canada Commodities

14 Alpha ATS S&T Case

18 Quantitative Outcry

3 About RITC

35 Appendix

4 Important Information

8 Social Outcry

3

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

About RITC The Rotman International Trading Competition is a one-of-a-kind event hosted annually at the University of Toronto. Now entering its 8th year, the three day competition brings together over 300 participants representing approximately 50 different top universities and corporations across the world. Despite the technological improvements and continued shift towards remote electronic trading, the event continues to draw ever larger interest as our competitors and sponsors demonstrate that they value the face-to-face interaction encouraged by our conference format. The competition is predominantly structured around the Rotman Interactive Trader platform, a software simulation that creates an electronic market which participants use to trade with each other. The platform is designed to run simulation cases that are designed to test traders’ ability to handle a magnitude of market scenarios. The following case package provides an overview of the content presented at the 2011 Rotman International Trading Competition. Each case has been specifically tailored to be linked to topics taught in university level classes and real-life trading situations. We hope you enjoy your experience at the competition.

See You in Toronto

4

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Important Information Practice Servers Practice servers will be online as of Monday, January 31st, 2010 and will operate 24 hours a day 7 days a week until the start of the competition. You will need to update your client to RIT version 1.75 in order to trade. The release of 1.75 will occur shortly before January 31st and can be downloaded from rit.rotman.utoronto.ca or the RITC website. If you are unfamiliar with the RIT platform and environment, it is essential that you spend some time running the demonstration Microstructure 2 (MM2) case (and read the associated help file) located at the RIT website above. The documentation is available in the Tour/Demo section. The follow table details the server IP & ports for the RITC practice environments.

Case Name Server IP Port

Interest Rate Case flserver.rotman.utoronto.ca 16500

Alpha ATS S&T Case Server 1 flserver.rotman.utoronto.ca 16510

Alpha ATS S&T Case Server 2 flserver.rotman.utoronto.ca 16520

BP Canada Commodities Case flserver.rotman.utoronto.ca 16530

Thomson Reuters QED Case flserver.rotman.utoronto.ca 16540

CIBC Algorithmic HFT Case Server 1 flserver.rotman.utoronto.ca 16550

CIBC Algorithmic HFT Case Server 2 flserver.rotman.utoronto.ca 16560

CIBC Algorithmic HFT Case Server 3 flserver.rotman.utoronto.ca 16570

CIBC Algorithmic HFT Case Server 4 flserver.rotman.utoronto.ca 16580 To login to any server, you can type in any username and password and it will automatically create an account if it does not exist. If you have forgotten your password or the username appears to be taken, simply choose a new username and password to create a new account. Multiple server ports have been provided for the CIBC Algorithmic HFT Case and the Alpha ATS S&T Case to allow teams to trade in either populated or unpopulated environments. For example, if you are testing your algorithm and there are 7 other algorithms running, you may want to move to a different port where less trading is occurring. The Interest Rate Case, BP Canada Commodities Case, and Thomson Reuters QED Case will be updated with a different set of news on Saturday, February 5th at 10AM EST and Saturday, and February 12th at 10AM EST. Teams wishing to trade against other participants are encouraged to login at this time. At each update, a new case file with different news items will be uploaded and will continue to run until the next update. As such, teams that continue to practice from the start of the practice server up to the competition will have traded 3 different iterations of each of the aforementioned cases. The Alpha ATS and CIBC HFT cases have no news drivers and randomize a new set of security paths each time they are run.

5

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Additional Servers 3 additional servers will be running the MM2, ALGO1, and ALGO2 RIT cases. This is so that participants working through the MM2, ALGO1, and ALGO2 case tutorials have a server to practice with. Competitors will not be trading these cases during the competition but they do provide a good place to start for individuals seeking to learn RIT, VBA and the Rotman API.

Case Name Server IP Port

Market Microstructure 2 (MM2) Case flserver.rotman.utoronto.ca 10000

ALGO1 RIT Case flserver.rotman.utoronto.ca 14980

ALGO2 RIT Case flserver.rotman.utoronto.ca 14990

Additional Support Files Additional support files including the CIBC Algorithmic HFT Case Base Algorithm, the Thomson Reuters QED Data Set, and other relevant support and documentation files will be provided on RITC website prior to launch of the Practice Servers. A brief description of the documentation files can be found in the Appendix.

Scoring and Ranking Methodology The Scoring and Ranking Methodology document will be released prior to the start of the competition on the RITC website. An announcement will be sent out to competitors once the document becomes available.

Competition Schedule This schedule is subject to change prior to the competition. Competitors can check on the RITC website for the most up-to-date schedule. Each competitor will also receive a personalized schedule when they arrive at the competition.

6

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Case Summaries

Social Outcry The opening event of the competition gives you your first opportunity to make an impression on the sponsors, faculty members, and other teams in this fun introduction to the Rotman International Trading Competition. Trade against experienced professionals from the industry, try to make your case against the professors, and show everyone your outcry skills by making fast and loud trading decisions. The Social Outcry case was introduced at RITC 2004.

Interest Rates This case will test students’ abilities to trade interest rate derivatives in response to the ever changing macro-economic landscape. Students will trade interest rate yield futures which represent direct exposure to changes in different benchmark yields. In addition students may use combinations of these futures, or specialized yield spread futures, to express a view on the slope of the yield curve. The Interest Rates case is new to RITC.

Alpha ATS Sales and Trader This is our premier electronic trading case on the Rotman Interactive Trader platform. With six different trading scenarios, this simulated market environment will put your critical thinking and analytical skills to the test. Whether you make a market, trade institutional orders or a combination of the two, participants will have to think fast and logically in order to get the highest return. In addition, traders will be able to execute their trades on two different marketplaces each featuring different cost structures. The Alpha ATS: Sales and Trader case was introduced at RITC 2010.

Quantitative Outcry Building on the experience of the Social Open Outcry, this case combines trading, analytical, and communication skills to make it even more demanding. With the use of complex financial analysis models made in Excel, participants will use news releases that give quantitative economic forecasts, instead of qualitative micro and macro data, to predict the futures market. Analyzing macroeconomic indicators, participants should be able to gain an understanding of the sensitivity of the index to each of the factors and be able to effectively model it. The Quantitative Outcry case was introduced at RITC 2005.

BP Canada Commodity Trading The BP Canada Commodity Trading case will place competitors into a three-month trading simulation where they can transact Natural Gas futures contracts in an attempt to generate entrepreneurial trading profits. Traders will be provided with both qualitative and quantitative news updates impacting the supply and demand of the energy marketplace in North America and will be able to forecast commodities prices based on this information. The BP Canada Commodity Trading Case was introduced at RITC 2007

7

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Thomson Reuters Quantitative and Event Driven (QED) The Thomson Reuters Quantitative and Event Driven (QED) case introduces competitors to the cutting-edge environment of machine-readable news. Participants will be responsible for reviewing a historic Reuters QED dataset and determining the relationships between news and stock price movements. Based on this analysis, traders will be able to model the expected effects of future news events that are released during the trading cases. The Thomson Reuters QED case is new to RITC.

CIBC Algorithmic High Frequency Trading (HFT) The CIBC Algorithmic High Frequency Trading (HFT) case is designed to challenge competitor’s logic and programming skills as they attempt to design the most effective algorithm to generate trading profits. Competitors lacking knowledge in programming can follow step-by-step guides and use trading templates to design their algorithm, while more ambitious traders can design an algorithm from the ground up. The CIBC Algorithmic HFT case was introduced at RITC 2010.

8

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Social Outcry Overview The objective of the social outcry case is to allow competition participants to interact (“to break the ice”) and to understand the progression of market technology. This segment of the competition is not included in the cumulative team score as scores are based on individual performance. This Social Outcry will be an exciting way for you to introduce yourself to the participants at RITC as well as great preparation for the Quantitative Outcry. You will be ranked based on your Net Liquidation Value at the end of the case.

Description Each participant will start the session with $1,000,000 cash and a neutral position in the futures. Participants are allowed to go long (buy) or go short (sell). Contracts in hand at the end of trading will be marked-to-market at the closing price.

Market Dynamics Participants will trade futures contracts on an index, the RT100. The futures price will be determined by the market’s transactions while the spot price will follow a stochastic path subject to influence from qualitative news announcements which will be displayed on the ticker. One news announcement will be displayed at a time, and each news release will have a random length and effect. Favourable news will result in an increase in the spot price while unfavourable news will cause a decrease in the spot price. These reactions may occur instantly or with lags. Participants are expected to trade based on how they interpret the news and their anticipation of the market reaction.

Margin Requirements and Trading Costs There is no margin limit and each contract will be charged a trading commission of $1/contract.

Rules and Responsibilities The following rules apply throughout the social outcry case:

Market agents are RITC staff members at the front of the outcry pit collecting tickets.

Maximum 5 contracts per trade/ticket.

All tickets must be filled out completely and legibly and verified by both parties with no portion of the ticket left blank. Illegible tickets may be ignored by the market agents!

Both transacting parties are responsible to make sure that the white portion of the ticket is received by the market agent. The transaction will not be processed if the white portion is not handed in. Both trading parties must walk the ticket up to the market agent.

Only the white portion of the ticket will be accepted by the market agent; trading receipts (pink and yellow) are for the team’s records only.

Once parties have verbally committed to a trade, they are required to transact.

RITC staff reserve the right to break any unreasonable trades.

Any breaches of the above stated rules and responsibilities are to be reported to the market agent or floor governors immediately.

So

cial O

utcry

Ca

se B

rief

9

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

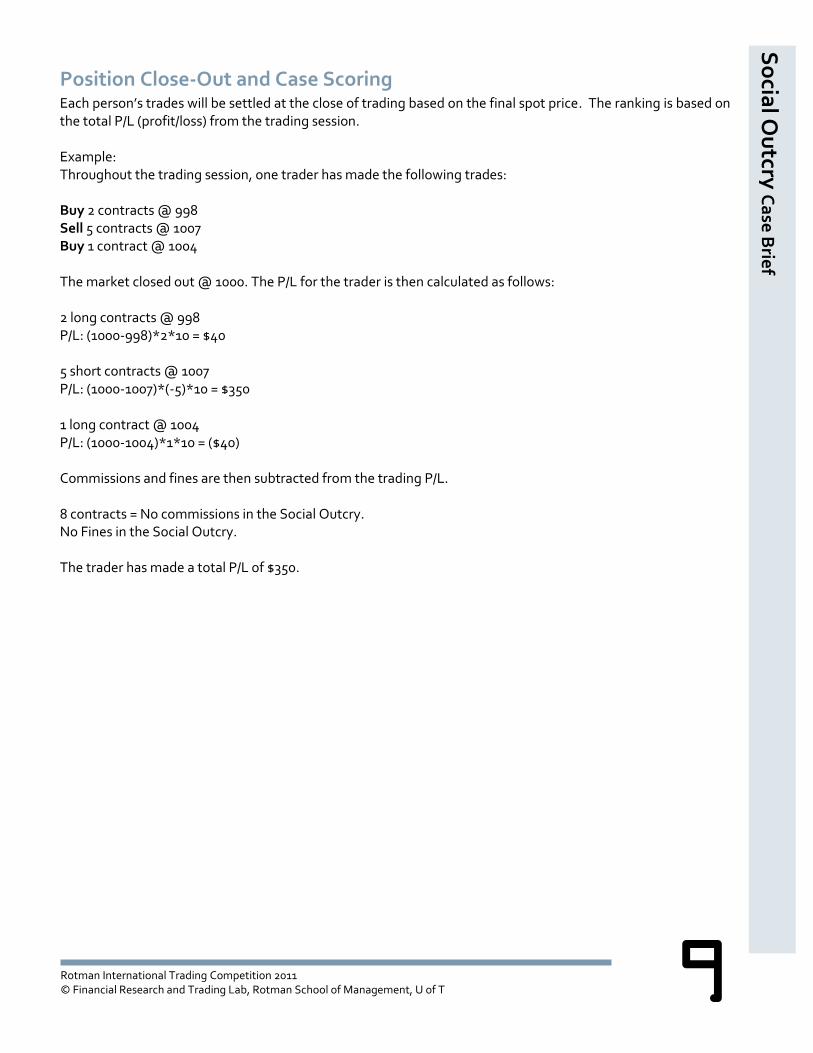

Position Close-Out and Case Scoring Each person’s trades will be settled at the close of trading based on the final spot price. The ranking is based on the total P/L (profit/loss) from the trading session. Example: Throughout the trading session, one trader has made the following trades: Buy 2 contracts @ 998 Sell 5 contracts @ 1007 Buy 1 contract @ 1004 The market closed out @ 1000. The P/L for the trader is then calculated as follows: 2 long contracts @ 998 P/L: (1000-998)*2*10 = $40 5 short contracts @ 1007 P/L: (1000-1007)*(-5)*10 = $350 1 long contract @ 1004 P/L: (1000-1004)*1*10 = ($40) Commissions and fines are then subtracted from the trading P/L. 8 contracts = No commissions in the Social Outcry. No Fines in the Social Outcry. The trader has made a total P/L of $350.

So

cial O

utcry

Ca

se B

rief

10

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Complete Transaction and Social Outcry Language Example To find the market, traders simply yell “What’s the market?” If someone wants to make the market on the bid side, he/she can answer “50 bid” meaning they want to buy at a price ending with 50 (1050, 1150) whichever is closest to the last trade. If someone wants to make the market on the ask side, he/she will yell “at 51” meaning he/she wants to sell at a price ending with 51 (1051, 1151) closest to the last price. Note that so far, no quantity has been declared. Only two digits are required when calling the bid or ask. To complete a trade, someone willing to take the market can simply say “Bought two” to the person selling. The seller’s response must then be: “Sold two” (or any other quantity below 2, but not 0, at the seller’s discretion). After the seller and the buyer fill out the trade ticket and submit the white part to the ticket taker, the trade is complete. Please note that the market maker (trader announcing the price) gets to decide the quantity traded up to a maximum of the quantity requested by the market taker. A complete transaction could run as follows:

Trader1 “What’s the market?” Trader2 “70 bid, at 72” or “70 at 72”, (bid 1070, ask 1072, this trader wants to buy and sell) Trader3 “at 71” (the new market is 1070 to 1071) Trader 1 to trader 3 “Bought 5” (he/she wants to buy 5 contracts at 1071) Trader 3 to trader 1 “Sold 3” (Although trader 1 wanted to buy 5 contracts, trader 3 only wants to sell 3

contracts, trader 1 must accept the three contracts). Trader 1 or trader 3 He/she fills out the trade ticket with initials from both Trader 1 and Trader 3. The white

portion of the ticket is submitted to the market agent by both traders (both traders walk the one ticket up to the front of the trading floor). Trader 1(Buyer) keeps the yellow portion of the ticket and Trader 3(Seller) keeps the pink (red) portion of the ticket.

There will be a brief outcry practice before the Social Outcry on the day of competition

So

cial O

utcry

Ca

se B

rief

11

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Interest Rates Case Overview The Interest Rates Case challenges participants to consider economic news and its impact on U.S. Benchmark yields. In this case, traders will analyze various news releases and determine the direction and degree of the effects. In response, traders can buy and sell yield futures, which represent yields on different benchmark maturities. In addition, traders will be able to trade spread futures, which represent the differences in the yields of different benchmark maturities. This can also be thought of as the difference between the values of the Yield Futures.

Description There will be 2 heats with 2 team members competing per heat. Each heat will consist of five 13-minute independent sub-heats representing 6 months of calendar time. Traders will start with an endowment of $1,000,000 and will be able to trade six securities: three yield futures and three spread futures. In addition, there are three non-tradable benchmark yields that will drive the value of the futures. Each tradable contract will have a contract size of 50,000 and will expire at the end of each sub-heat. The price of the yield future contract represents the expected yield of the underlying benchmark maturity at the end of the period with each $0.01 representing 1 bp. Therefore, if the final yield of the 2-year benchmark is 2.45%, the 2TNY futures contract will close at a price of $2.45.1 Similarly, the spread futures trade based on the yield differential and are also priced at $0.01 per 1bp.

Parameter Value

Number of trading sub-heats 5

Starting endowment $1,000,000

Trading time per sub-heat 780 seconds

Calendar time per sub-heat 6 months (26 weeks)

Interest rate on cash 0% per annum

Maximum single order 25 contracts

Mark-to-market frequency 1 week (30 seconds)

Macroeconomic news will be released at random intervals. Trading from excel using the Rotman API will be disabled.

1 Given the fact that these contracts trade based on the yield of the underlying notes, the returns of the security are linear with respect

to yield. This is in contrast with trading physical bonds which are convex with respect to yield as the price of the bond falls less per 1% increase in yield as yield increases. This is intended as a simplification so that traders do not need make complex duration calculations.

Inte

rest R

ate

s Ca

se B

rief

12

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

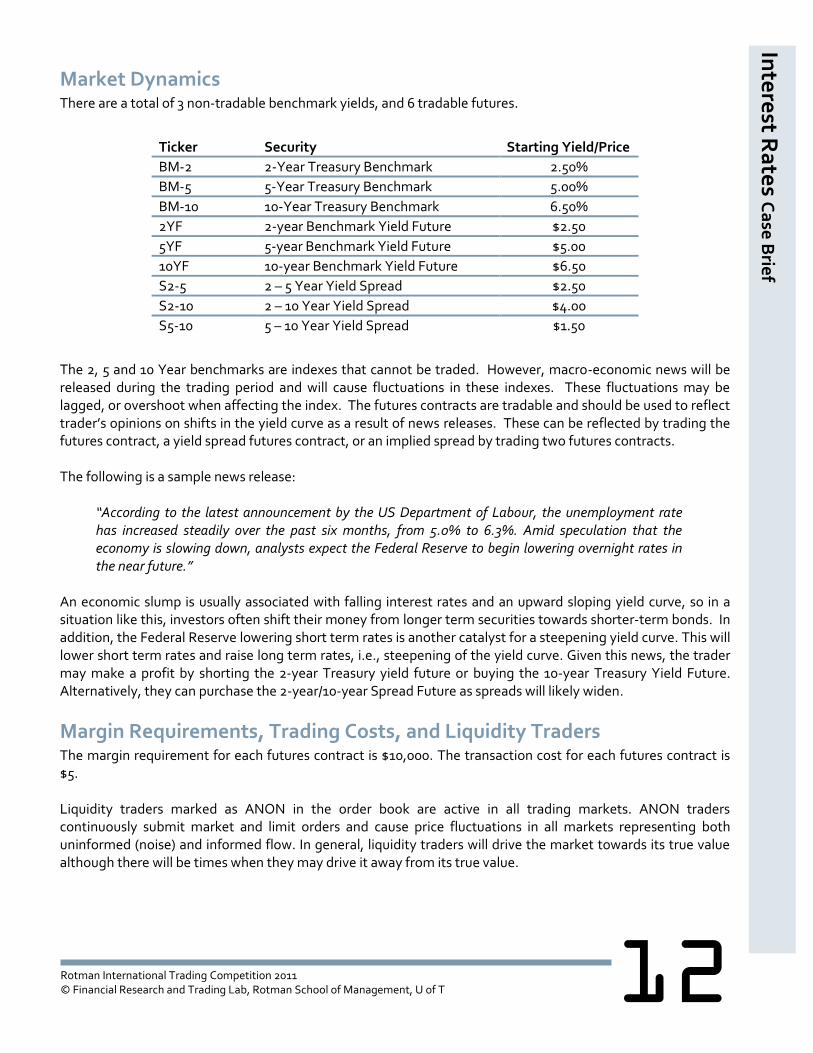

Market Dynamics There are a total of 3 non-tradable benchmark yields, and 6 tradable futures.

Ticker Security Starting Yield/Price

BM-2 2-Year Treasury Benchmark 2.50%

BM-5 5-Year Treasury Benchmark 5.00%

BM-10 10-Year Treasury Benchmark 6.50%

2YF 2-year Benchmark Yield Future $2.50

5YF 5-year Benchmark Yield Future $5.00

10YF 10-year Benchmark Yield Future $6.50

S2-5 2 – 5 Year Yield Spread $2.50

S2-10 2 – 10 Year Yield Spread $4.00

S5-10 5 – 10 Year Yield Spread $1.50

The 2, 5 and 10 Year benchmarks are indexes that cannot be traded. However, macro-economic news will be released during the trading period and will cause fluctuations in these indexes. These fluctuations may be lagged, or overshoot when affecting the index. The futures contracts are tradable and should be used to reflect trader’s opinions on shifts in the yield curve as a result of news releases. These can be reflected by trading the futures contract, a yield spread futures contract, or an implied spread by trading two futures contracts. The following is a sample news release:

“According to the latest announcement by the US Department of Labour, the unemployment rate has increased steadily over the past six months, from 5.0% to 6.3%. Amid speculation that the economy is slowing down, analysts expect the Federal Reserve to begin lowering overnight rates in the near future.”

An economic slump is usually associated with falling interest rates and an upward sloping yield curve, so in a situation like this, investors often shift their money from longer term securities towards shorter-term bonds. In addition, the Federal Reserve lowering short term rates is another catalyst for a steepening yield curve. This will lower short term rates and raise long term rates, i.e., steepening of the yield curve. Given this news, the trader may make a profit by shorting the 2-year Treasury yield future or buying the 10-year Treasury Yield Future. Alternatively, they can purchase the 2-year/10-year Spread Future as spreads will likely widen.

Margin Requirements, Trading Costs, and Liquidity Traders The margin requirement for each futures contract is $10,000. The transaction cost for each futures contract is $5. Liquidity traders marked as ANON in the order book are active in all trading markets. ANON traders continuously submit market and limit orders and cause price fluctuations in all markets representing both uninformed (noise) and informed flow. In general, liquidity traders will drive the market towards its true value although there will be times when they may drive it away from its true value.

Inte

rest R

ate

s Ca

se B

rief

13

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Position Close-Out and Case Scoring All positions will be marked-to-market every 30 seconds with any profits and losses reflected in the traders’ cash balance by the mark-to-market operation. Open positions in the yield futures at the end of the period will be settled at the level of the benchmark rate (The two-year yield future closes out at the level of the two-year benchmark, etc.). Open positions in the spread futures will settle at the final yield spreads of the corresponding benchmarks. Each team will be given a heat rank based on sub-heat ranks calculated from the combined ending NLV of the two traders. For more information please refer to the Scoring and Ranking Methodology document that will be released.

Putting It All Together to Trade the Interest Rates Case There are many different concepts that are introduced by this case. The most fundamentally simple strategy that traders can use is arbitrage. There is an absolute link between the individual futures contracts and the spread futures and that link can be exploited to generate risk-free profit whenever it presents itself.

A more complicated strategy involves taking views on how the yield curve should react in relation to economic news. As an introductory case, a quantitative model cannot be used to forecast the adjustments in the yield curve, rather, traders are expected to use a basic level of economic analysis to anticipate movements in the yield curve as a result of economic news.

For example a news release may occur where the trader expects the entire curve to shift upwards. In this case, to profit off of the increase in interest rates, the trader may want to purchase 5 contracts of the 2 year Yield Future when the value is trading at 2%. If the interest rate then increases to 2.3%, the trader earns 0.3 on their investment of 5 contracts. This is equivalent to 5 contracts multiplied by a profit of 0.3 multiplied by a contract size of 50,000 for a total profit of $75,000.

Keep in mind that the news’ effect may not be fully reflected in the market immediately following its release. As such, the yield differential between two Yield Futures may not equal to the corresponding Yield Spread. When this occurs, an arbitrage opportunity arises.

We advise all traders to closely evaluate the different securities and consider splitting the workload. Since there are two traders from your team active in the market, it might make sense to focus and specialize rather than trading all of the securities at the same time.

Inte

rest R

ate

s Ca

se B

rief

14

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Alpha ATS Sales and Trader Case Overview The Alpha ATS Sales and Trader Case challenges participants to put their critical thinking and analytical abilities to the test in an environment that allows traders to have significant flexibility on the trading strategy they choose to use. Faced with institutional orders, multiple exchanges, and multiple securities, participants must think fast and act fast to take advantage of pricing discrepancies, large block orders, and market making opportunities. Each exchange will also have a different cost structure and exhibit different liquidity properties.

Description There will be 2 heats with 2 team members competing per heat. Each heat will consist of six independent sub-heats of roughly 10 minutes in length representing 12 months of calendar time. Each sub-heat will involve up to three securities with different volatility and liquidity characteristics. Each security will be tradable on two exchanges with one representing the main exchange and one representing the alternative trading venue. As well, the interest rate will differ for each sub-heat but interest will always be compounded weekly (11 seconds).

Parameter Value

Number of trading sub-heats 6

Starting endowment $1,000,000

Trading time per sub-heat 572 seconds

Calendar time per sub-heat 12 months (52 weeks)

Interest rate on cash i % per annum (varied)

Compounding interval 1 week (11 seconds)

Per interval interest rate on cash [(1+i)1/52 – 1]*100% per week

Institutional orders will be generated by computerized traders and distributed at random intervals to random participants. Trading from Excel using the Rotman API will be disabled.

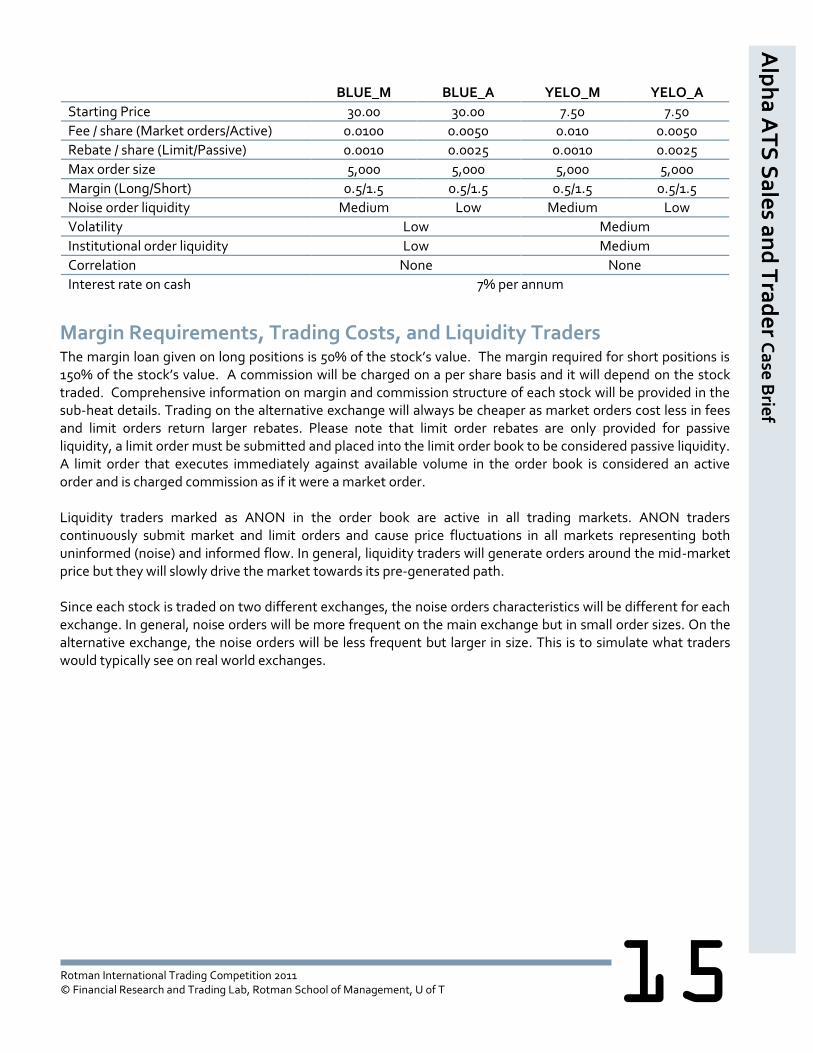

Market Dynamics The market dynamics of each sub-heat will vary in each case due to the varying number and nature of securities as well as the changing interest rate. At the competition, all competitors will receive the details regarding the trading environments of each of the six sub-heats. Participants will then be able to plan their trading strategy based on the sub-heat details. Please be aware that all securities will be tradeable on two exchanges for all sub-heats. Trading on either exchange for a given security is aggregated to form an overall position for that security. However, the overall fees and liquidity characteristics will vary between exchanges. Furthermore, the prevailing price for the same security may not always be the same which may provide opportunites for price discrepancies which traders may take advantage of. Finally, the securities may be correlated positively or negatively with one another; a property traders may take advantage of to manage their overall risk. An example of a sub-heat detail sample is provided below as an illustration.

Alp

ha

AT

S S

ale

s an

d T

rad

er C

ase

Brie

f A

lph

a A

TS

Sa

les a

nd

Tra

de

r Ca

se B

rief

15

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

BLUE_M BLUE_A YELO_M YELO_A

Starting Price 30.00 30.00 7.50 7.50

Fee / share (Market orders/Active) 0.0100 0.0050 0.010 0.0050

Rebate / share (Limit/Passive) 0.0010 0.0025 0.0010 0.0025

Max order size 5,000 5,000 5,000 5,000

Margin (Long/Short) 0.5/1.5 0.5/1.5 0.5/1.5 0.5/1.5

Noise order liquidity Medium Low Medium Low

Volatility Low Medium

Institutional order liquidity Low Medium

Correlation None None

Interest rate on cash 7% per annum

Margin Requirements, Trading Costs, and Liquidity Traders The margin loan given on long positions is 50% of the stock’s value. The margin required for short positions is 150% of the stock’s value. A commission will be charged on a per share basis and it will depend on the stock traded. Comprehensive information on margin and commission structure of each stock will be provided in the sub-heat details. Trading on the alternative exchange will always be cheaper as market orders cost less in fees and limit orders return larger rebates. Please note that limit order rebates are only provided for passive liquidity, a limit order must be submitted and placed into the limit order book to be considered passive liquidity. A limit order that executes immediately against available volume in the order book is considered an active order and is charged commission as if it were a market order. Liquidity traders marked as ANON in the order book are active in all trading markets. ANON traders continuously submit market and limit orders and cause price fluctuations in all markets representing both uninformed (noise) and informed flow. In general, liquidity traders will generate orders around the mid-market price but they will slowly drive the market towards its pre-generated path. Since each stock is traded on two different exchanges, the noise orders characteristics will be different for each exchange. In general, noise orders will be more frequent on the main exchange but in small order sizes. On the alternative exchange, the noise orders will be less frequent but larger in size. This is to simulate what traders would typically see on real world exchanges.

Alp

ha

AT

S S

ale

s an

d T

rad

er C

ase

Brie

f

16

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Institutional Orders Institutional orders are generated by the server and randomly routed to traders in the market. They are influenced by the same pre-generated path that the liquidity traders follow and therefore will also attempt to drive the market price towards that path. Institutional orders will give a spread based on the mid-market price when the order was generated (if the mid-market price is $10, and the spread was 1-2%, an institutional order will offer to buy shares for an amount between $10.10 and $10.20). A random trading commission per share traded will also be added to the trade and paid to the trader who accepts the order. The order will be randomly routed to a trader who then has 15 seconds to accept or decline the order. If the order is accepted, the order is instantly filled out of the trader’s inventory at the advertised price (fills will result in a short position in the stock if the trader does not have a sufficient inventory to cover the size of the trade). Commissions are paid to the trader. Orders that are not accepted or declined within 15 seconds will automatically be rerouted. Orders will be rerouted up to 3 times at which point they will expire. Institutional orders are subject to the same margin restrictions as regular orders. In relation to the two different exchanges, all of the institutional orders are on the main exchange. However, the positions can be traded o the main either the main exchange or the alternative exchange. For example, if you purchase 50,000 shares through an institutional block, selling 15,000 shares on the main exchange and 35,000 shares on the ATS exchange, the result will be a position of zero. Your trade-routing decisions (whether to send your order to the main exchange or Alpha) would be based on commissions, liquidity, and market prices.

Position Close-Out and Case Scoring Any non-zero position in either stock will be closed out at the end of trading based on the Random Price Closeout (RPC) algorithm. For each stock, a price is randomly picked from the sample of all trades in that stock which occurred in the last minute of the case. All long and short positions will then be closed out based on that price. It is strongly suggested that traders close out their positions prior to the end of trading period. Each team will be given a heat rank based on sub-heat ranks calculated from the combined ending NLV of the two traders. For more information please refer to the Scoring and Ranking Methodology document that will be released.

Alp

ha

AT

S S

ale

s an

d T

rad

er C

ase

Brie

f

17

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Putting It All Together to Trade the Alpha ATS Sales and Trader Case The premise of the Alpha ATS: Sales and Trader trading case is relatively simple. There are multiple stocks that have random unpredictable price movement. Since you cannot predict or forecast the direction of the stocks, attempting to make money by speculating on the price movement is generally an unprofitable strategy due to transaction costs. However, the case has many generous institutions that are quite willing to pay you for taking some risk that they would rather avoid. Taking on this risk should generate profits for you, the trader. Typically, you should wait until you receive your first institutional order. Upon receiving the order, you should compare the price that the institution wants to trade at with the price in the current market. You have 15 seconds to make your decision as to whether to accept or decline the order. Keep in mind that if the institution wants to buy shares, you are agreeing to sell shares to them at the block trade price. Since you are agreeing to sell the shares, you will want to be selling the shares only if they are willing to pay more than the current market price (ask). Likewise, if the institution wants to sell shares, you are agreeing to buy shares from them at the block trade price. You will want to be buying shares only if they will sell them for less than the market price (bid). The fact that the institution is buying, which means you are selling, or vice versa, often confuses inexperienced traders. Evaluating the size of the spread is the fastest and easiest level of analysis that you can do when you receive an institutional order. The next step is to look at the limit order book (via the Market Depth View) for the stock that you are analyzing and quickly calculate (generally you would just estimate) what the volume weighted average price would be if you were to buy or sell this entire block of shares at the market. Suppose the institution is willing to pay $26.50 for 25,000 shares. When reviewing the market depth for the stock, you realize that you can place a market order to buy 25,000 shares and realize an average price of $26.25 per share. In this situation the trade is definitely profitable because there is nearly a guaranteed profit of $6250 from the trade, plus commissions (($26.50 - $26.25) x 25,000 = $6250). In reality, you will most likely realize that your VWAP calculation of a market order is often extremely close to the institutional order price, or it shows a loss. Just because there isn’t a guaranteed profit in the trade, does not mean it isn’t a lucrative trade. There are still two other issues to consider. First of all, the trading commission can often be large enough to offset the calculated losses. Second, and more importantly, large market orders are typically an inefficient way to trade large volumes of shares. Remember that the market order for the entire block volume will guarantee you the profit that you have calculated. However, it is usually more efficient to break the block into smaller sizes, and trade those as a combination of market and limit orders. This will often result in a smaller market impact and you will realize a price that is better than just trading the entire block at the market. The decision of whether to use one market order to sell 25,000 shares or 5 limit orders to sell 5000 shares (submit one order, wait for it to complete, then submit another, and then another) is quite subjective and beyond the confines of this document to answer. The concept is that sometimes when a market is very liquid, large market orders are effective ways to trade large amounts of stock. However, when markets are not very liquid, limit orders may be more effective. The key idea is to use this trading case to try different strategies and to see what works for you in different scenarios.

Alp

ha

AT

S S

ale

s an

d T

rad

er C

ase

Brie

f

18

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Quantitative Outcry Case Overview The Quantitative Outcry case challenges participants to understand the effect of macroeconomic indicators on the spot price of the Rotman index (RT100). Competitors are expected to construct a factor sensitivity model that they can use to support their trading decisions during the case. Teams will also be able to make a limited amount of spot transactions to generate arbitrage profits between the spot and futures markets.

Description Each team consists of two traders and two analysts. The two traders will be in the trading pit located in the Rotman Atrium. The two analysts will be in the trading lab using one desktop computer to analyze information. Throughout the case, news items regarding economist estimates, realized values, and factor sensitivities will be released. All of these factors are important in order to model the value of the RT100 Index.

Analysts will receive all news releases while traders will be given a subset of those releases. More specifically, traders will only get realized economic announcements (actual data), while analysts will get the actual data, economist’s estimates, and updated factor sensitivities. With this mechanism, it is up to the analysts in the trading lab to communicate the missing information and their analysis to the traders in the Rotman Atrium using signals (i.e. hands signs) to relay the news. No verbal or electronic communication is allowed between the analysts and traders. It is recommended that you develop the signals/hand signs before you begin the case. The trading mechanics of the Quantitative Outcry will be similar to that of the Social Outcry. For details on the outcry trading, please refer to the Social Outcry Case Description and Tutorial section. The case will comprise of two sub-heats of 30 minutes each, and each heat will represent 6 months.

Aside from the transactions done by traders in the Rotman Atrium, analysts in the trading lab are allowed to make up to three spot trades during each heat, with up to 100 contacts in each trade. The spot trades will be executed at the current spot price of the RT100 index posted on the screen. This trade will allow each team to have an opportunity to close out their positions quicker. Moreover, since the futures market will be driven by trader activity while the spot market is based on the actual economic indicators realized, there may be slight inefficiencies in the spot market and the futures market enabling arbitrage profits. These trades are added to the aggregate futures position of the team and are charged regular trading commissions. The soft and hard trading restriction limits discussed below will apply to trades made by analysts in the trading lab.

Market Dynamics There are four economic factors that affect the value of the RT100 Index. An expected reading of each indicator will be released at the beginning of each month (5 minutes of trading time) to the analysts in the trading lab. A realized reading of each indicator will be released at the middle or at the end of each month to both traders and analysts. Both releases can be considered credible with no errors or outliers. In addition to the release of economic indicators, the traders and the analysts will also be given qualitative news releases that show economists’ expectations of the RT100 index volatility in the following month. Lastly, analysts and traders will be able to see the spot market of the index in real time.

Since the futures market will be settled at the end of the trading case based at the spot market, the futures market should remain relatively close to the spot market. If there is a divergence, teams may generate arbitrage profits by having their analysts transact futures (at the spot price) and then having their traders close out the position on the floor (at the futures price). A week prior to the competition, a sample trading heat of

Qu

an

titative

Ou

tcry C

ase

Brie

f

19

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

data will be released and available on the RITC outcry website so that participates can review how the case works. The four economic factors that affect the value of the RT100 Index are Gross Domestic Product (GDP), Non Farm Payroll (NFP), Home Builders’ Index (HBI) and Manufacturing Inventories/Purchases (INV) Index. Traders will be trading futures contracts on the RT100 Index based on their expectations about the future spot prices of the RT100 Index. The following model should be used to predict the change (based on index points) in the RT100 Index:

( ) ( ) ( )

( )

Let us suppose that the initial estimate given for NFP is 66000, the given sensitivity is 0.0001, and the RT100 index starts at 1000. If the data released at the end of the month shows that NFP increased by 70000, then there is a differential between the estimate and actual figure of 4000. This would cause an increase of (4000 * 0.001 = 4 points) in the RT100 Index from its previous level. Therefore, if the RT100 Index was at 1000 just before the news release of realized economic data the 4000 differential in NFP would make the RT100 index go up to 1004, assuming no other news has been released. During the competition, news will be released regularly and there will be many more shocks to the RT index before the final settlement. It is important to remember that changes in the RT100 index, at the time when realized data are released, will only be caused by unanticipated events. So in the above example, the 66000 growth assumption for NFP was already priced into the RT100 index, and the 70000 growth actually released includes an unexpected component of 4000. Therefore, only the additional 4000 will be reflected in the new value of the RT100 Index, until further news about other realized or expected indicators is released. Based on the data constructed for this case, the starting sensitivities and factor levels are given below.

Economic Indicator Factor

Sensitivity Initial Level Estimate for Month 1 End

Gross Domestic Product (GDP) 100 2.6% 2.7%

Non-Farm Payroll (NFP) 0.001 60,000 66,000

Home Builders’ Index (HBI) 15 52.00 54.60

Manufacturing Inventories Index (INV) -10 49.00 49.49

Each time the actual value of economic factor is released, there will be a resulting effect on the spot price based on the differential between the economic estimate and the actual figure, multiplied by the sensitivity as demonstrated earlier. The final value of the spot market will be the sum of all of these effects.

Qu

an

titative

Ou

tcry C

ase

Brie

f Q

ua

ntita

tive O

utcry

Ca

se B

rief

20

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Information Release Schedule

Time Indicator Released to

Pre-case Month 1 Estimates (Provided Above) Everyone

1 minute Month 1 Actual GDP & INV Everyone

3 minutes Month 1 Actual HBI & NFP Everyone

5 minutes Month 2 Estimates Analysts Only

6 minutes Month 2 Actual GDP & INV Everyone

8 minutes Month 2 Actual HBI & NFP Everyone

10 minutes Month 3 Estimates Analysts Only

11 minutes Month 3 Actual GDP & INV Everyone

13 minutes Month 3 Actual HBI & NFP Everyone

15 minutes Month 4 Estimates Analysts Only

16 minutes Month 4 Actual GDP & INV Everyone

18 minutes Month 4 Actual HBI & NFP Everyone

20 minutes Month 5 Estimates Analysts Only

21 minutes Month 5 Actual GDP & INV Everyone

23 minutes Month 5 Actual HBI & NFP Everyone

25 minutes Month 6 Estimates Analysts Only

26 minutes Month 6 Actual GDP & INV Everyone

28 minutes Month 6 Actual HBI & NFP Everyone

30 minutes End of Heat

Random times Index Volatility Forecast Everyone

Random times Factor Sensitivity Change Analysts Only

Margin Requirements and Trading Costs Each team has a starting position of 0 contracts, a soft margin limit of 200 contracts, and a fixed hard margin limit of 500 contracts on their net positions. Teams will be notified as they approach their soft limit and hard limits on a best efforts basis. If a team exceeds its soft limit, it will be charged a fee proportional to how much they exceed the soft limit. The amount by which a team exceeds the initial soft limit of 200 will become their new soft limit. The fee per contract above the soft limit is $250.

For example, if Team A’s net position is at 230, they will be charged a fee of $250 * 30 = $7500 (they have exceeded their soft limit of 200 by 30 contracts). For Team A, 230 is now the new soft limit. As long as Team A’s position remains below 230, there will be no additional fees. If Team A bought more and had a new net position of 280, then they would be charged an additional fee of $250 * 50 (Difference between the new net position and new soft limit). If a team does not exceed its soft limit, it will not be charged any margin fees.

Each contract will be charged a brokerage commission of $1 per contract and a contract multiplier of 10. For example, a purchase of 1 contract at 1000 that is subsequently sold at 1010 would generate $100 profits minus $2 of trading commissions for a net of $98.

Any team that exceeds the hard limit of 500 will be automatically disqualified from the session. They will be given a rank equal to that of the last place for that session. In addition, there is a zero tolerance policy in regards to electronic communication. Any trader or analyst seen (by an RITC staff member) using or holding a

21

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

cell phone during the trading heats will be immediately disqualified. RITC staff will be positioned throughout the pit and the trading lab to police this.

Position Close-Out and Case Scoring Each team’s position will be settled at the end of the trading session by closing out their remaining positions at the final spot price. Analysts will not be graded based on their estimates; however accurate estimates should generate higher trading profits. Teams will be scored based on their ending Net Liquidation Value over the two sub-heats. For more information please refer to the Scoring and Ranking Methodology document that will be released.

Putting It All Together to Trade the Quantitative Outcry Case It is highly recommended that your team prepare a model to help forecast the value of the RT100 Index prior to the session. In your trading model, you should forecast the returns of RT100 Index based on the difference between the economic estimates and actual data. You should also remember to update the estimates, actual realized indicators and factor sensitivities as they are announced. Successful teams in the past have prepared and tested communication systems (hand signals, confirmation signals, etc.) so that information can properly be communicated from the analysts to the traders.

Prior to the beginning of the market, the two analysts will have access to one desktop in the trading lab. They should proceed to set up their model as well as log into the Rotman Trader Portal to access the news releases as well as the Rotman Index. Remember, only the analysts will be able to see the expected figures of the economic factors, whereas both the traders and the analysts will receive the realized figures and the expected volatility. Meanwhile, all traders for the first heat will assemble in the atrium “trading pit”.

Once trading commences, news updates will begin to flow to the analysts. Generally, analysts’ forecast the value of the RT100 Index using the estimates, realized data and factor sensitivities. Analysts will then convey this information to their partners in the trading pit.

For traders, it is highly recommended that your team practice quoting markets and trading with each other beforehand as clear pit trading terminology will make you a desired counterparty during trading. Traders should then utilize the information conveyed from their Analysts to make trades with other Traders. It is suggested that Traders actively look for new information from their Analysts. Furthermore, the two Traders should keep track of their net position as well as any trading strategies. The most counter-productive thing a team can do is trade with each other, or make opposing trades at disadvantageous prices (for example, member A buys at 1000 while member B on the other side of the pit sells for 990). To be successful at this case, we recommend traders dividing up the following roles:

Qu

an

titative

Ou

tcry C

ase

Brie

f Q

ua

ntita

tive O

utcry

Ca

se B

rief

22

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

• Market maker – responsible for quoting a 2-way market during trading in the Atrium to try to generate profits off the bid/ask spread

• Analyst Lookout – responsible for obtaining new information from analysts on a regular basis

• Book Manager – responsible for keeping track of the team’s aggregate position

• Runner – responsible for running trade tickets in to be reported to the RITC staff, watching compliance of other Traders

As new news is released, traders should be willing to change their position (net long or short) quickly in response to directions from their analyst. All analysts will see the same news simultaneously. Therefore, speed and accuracy in interpreting and relaying that news will also be essential to your team’s success. The half hour outcry sessions are extremely frantic. Six month’s worth of index volatility is being compressed into a thirty minute trading session. You can expect the markets to move in fast and sometimes unpredictable directions. Your team’s ability to adapt to the changing market conditions and stay organized will be essential to your success.

Qu

an

titative

Ou

tcry C

ase

Brie

f

23

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

BP Canada Commodity Trading Case Overview The BP Canada Commodity Trading Case challenges the traders’ ability to respond to the highly dynamic world of commodity trading. In this case, traders will analyze various news releases affecting the supply and demand of natural gas. In response, traders will buy and sell futures contracts for different natural gas delivery months. Traders earn profits by correctly forecasting future supply and usage of natural gas and consequently its closing value. Traders will be ranked based on their profits after marking-to-market at the end of the case.

Description There will be two heats with two team members competing per heat. Each sub-heat will consist of two 30-minute independent sub-heats representing 3 months of the calendar year. Traders will start with an endowment of $1,000,000 and will be able to trade 3 different futures contracts. Each futures contract represents 4,000 mmBtu of natural gas settled/delivered at the end of July, August or September. Prices are quoted based on dollars and cents per mmBtu. All contracts will be marked to market every 30 seconds based on the last traded price. Contracts will be settled at the end of their respective months based on the calculated market price (explained in the Market Dynamics section on the next page). There is a maximum order size of 25 futures contracts in a single order.

Parameter Value

Number of trading sub-heats 2

Starting endowment $1,000,000

Number of periods per sub-heat 3

Trading time per period 600 seconds (30 minutes in total)

Calendar time per period 1 month (3 months in total)

Interest rate on cash 2% per annum

Compounding interval 1 day (30 seconds)

Per interval interest rate on cash [(1.02)1/240 – 1]*100% = 0.00825% per week

Maximum single order 25 contracts

Mark-to-market frequency 1 week (30 seconds)

Trading from excel using the Rotman API will be disabled.

BP

Ca

na

da

Co

mm

od

ity T

rad

ing

Ca

se B

rief

24

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

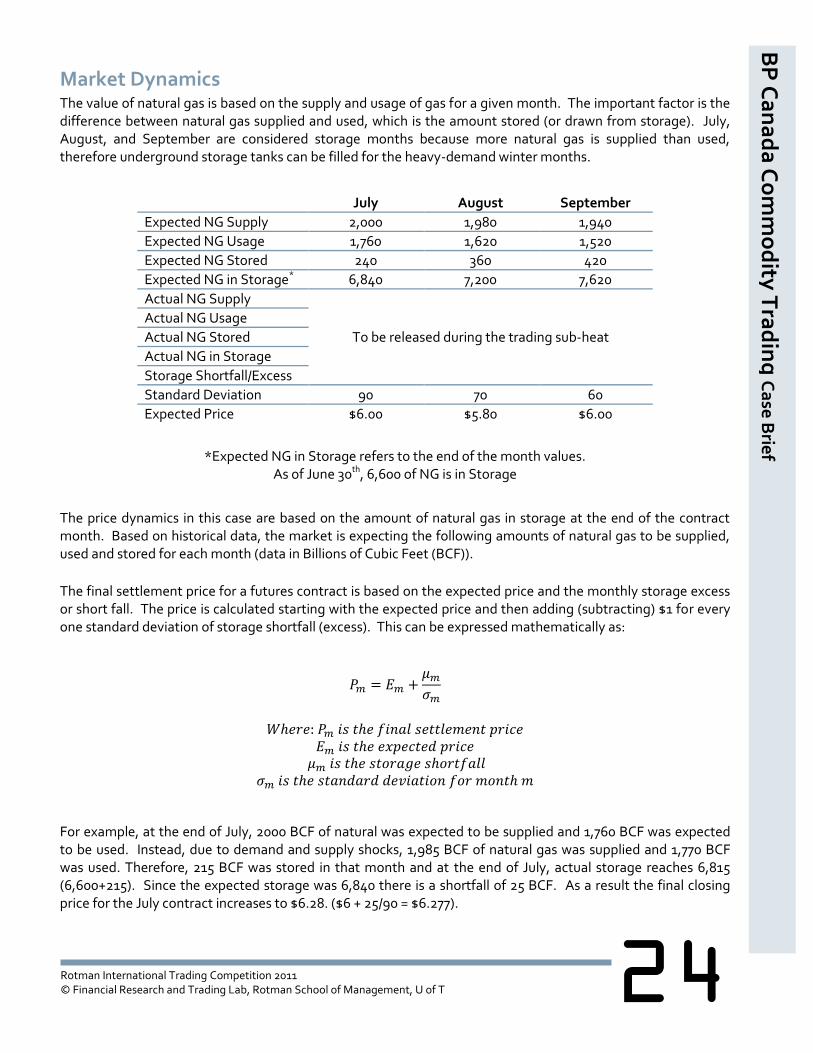

Market Dynamics The value of natural gas is based on the supply and usage of gas for a given month. The important factor is the difference between natural gas supplied and used, which is the amount stored (or drawn from storage). July, August, and September are considered storage months because more natural gas is supplied than used, therefore underground storage tanks can be filled for the heavy-demand winter months.

July August September

Expected NG Supply 2,000 1,980 1,940

Expected NG Usage 1,760 1,620 1,520

Expected NG Stored 240 360 420

Expected NG in Storage* 6,840 7,200 7,620

Actual NG Supply

To be released during the trading sub-heat

Actual NG Usage

Actual NG Stored

Actual NG in Storage

Storage Shortfall/Excess

Standard Deviation 90 70 60

Expected Price $6.00 $5.80 $6.00

*Expected NG in Storage refers to the end of the month values. As of June 30th, 6,600 of NG is in Storage

The price dynamics in this case are based on the amount of natural gas in storage at the end of the contract month. Based on historical data, the market is expecting the following amounts of natural gas to be supplied, used and stored for each month (data in Billions of Cubic Feet (BCF)).

The final settlement price for a futures contract is based on the expected price and the monthly storage excess or short fall. The price is calculated starting with the expected price and then adding (subtracting) $1 for every one standard deviation of storage shortfall (excess). This can be expressed mathematically as:

For example, at the end of July, 2000 BCF of natural was expected to be supplied and 1,760 BCF was expected to be used. Instead, due to demand and supply shocks, 1,985 BCF of natural gas was supplied and 1,770 BCF was used. Therefore, 215 BCF was stored in that month and at the end of July, actual storage reaches 6,815 (6,600+215). Since the expected storage was 6,840 there is a shortfall of 25 BCF. As a result the final closing price for the July contract increases to $6.28. ($6 + 25/90 = $6.277).

BP

Ca

na

da

Co

mm

od

ity T

rad

ing

Ca

se B

rief

25

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

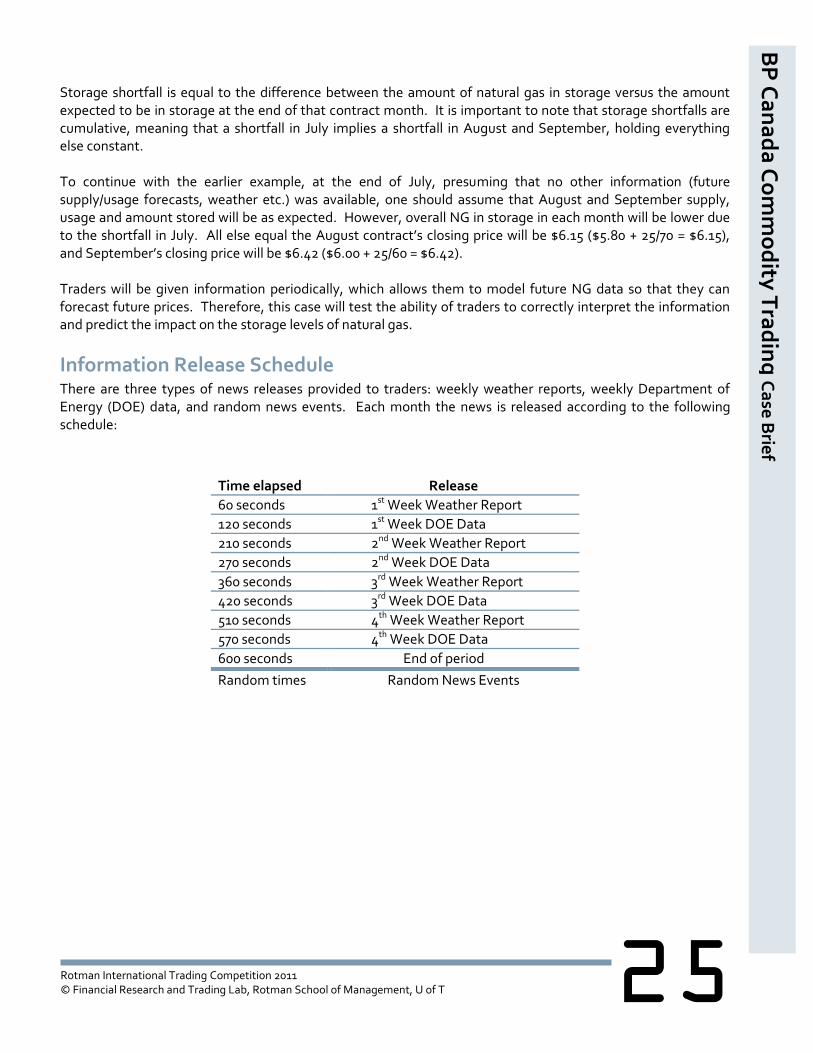

Storage shortfall is equal to the difference between the amount of natural gas in storage versus the amount expected to be in storage at the end of that contract month. It is important to note that storage shortfalls are cumulative, meaning that a shortfall in July implies a shortfall in August and September, holding everything else constant. To continue with the earlier example, at the end of July, presuming that no other information (future supply/usage forecasts, weather etc.) was available, one should assume that August and September supply, usage and amount stored will be as expected. However, overall NG in storage in each month will be lower due to the shortfall in July. All else equal the August contract’s closing price will be $6.15 ($5.80 + 25/70 = $6.15), and September’s closing price will be $6.42 ($6.00 + 25/60 = $6.42). Traders will be given information periodically, which allows them to model future NG data so that they can forecast future prices. Therefore, this case will test the ability of traders to correctly interpret the information and predict the impact on the storage levels of natural gas.

Information Release Schedule There are three types of news releases provided to traders: weekly weather reports, weekly Department of Energy (DOE) data, and random news events. Each month the news is released according to the following schedule:

Time elapsed Release

60 seconds 1st Week Weather Report

120 seconds 1st Week DOE Data

210 seconds 2nd Week Weather Report

270 seconds 2nd Week DOE Data

360 seconds 3rd Week Weather Report

420 seconds 3rd Week DOE Data

510 seconds 4th Week Weather Report

570 seconds 4th Week DOE Data

600 seconds End of period

Random times Random News Events

BP

Ca

na

da

Co

mm

od

ity T

rad

ing

Ca

se B

rief

26

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

Margin Requirements, Trading Costs, and Liquidity Traders The margin requirement for each futures contract is $10,000. The transaction cost for each futures contract is $5. Liquidity traders marked as ANON in the order book are active in all trading markets. ANON traders continuously submit market and limit orders and cause price fluctuations in all markets representing both uninformed (noise) and informed flow. In general, liquidity traders will drive the market towards its true value although there will be times when they may drive it away from its true value.

Position Close-Out and Case Scoring All positions will be marked-to-market every 30 seconds with any profits and losses reflected in the traders’ cash balance by the mark-to-market operation. Futures positions that remain open at the end of the period will be marked-to-market at the last traded price. For contracts that expire at the end of the period, the contract will be marked-to-market at the final fair value calculated based on the natural gas storage shortfall/excess formula described prior. Each team will be given a heat rank based on sub-heat ranks calculated from the combined ending NLV of the two traders. For more information please refer to the Scoring and Ranking Methodology document that will be released.

Additional Notes Traders will be provided with a basic RIT-linked Excel model which will allow them to enter their BCF

expectations and provide them with buy/sell signals. However, this is a very simple model meant to help students get started. It is highly recommended that traders enhance this basic model or build a model from scratch to get a better understanding of the case.

Do not worry about BCF/MM BTU conversion ratios. They have no relevance in this case. BCF is simply the way supply/usage/storage is expressed, while mmBtu is the unit of trade.

There is no intra-month seasonality - that is, if the expected supply of the month is 2,000 BCF, you can assume that 500 BCF are supplied per week. However, shocks may cause individual weeks to deviate.

This case takes place at the end of the summer. Warmer temperatures cause more air conditioning use, which causes more electricity usage. This, in turn, causes more natural gas to be burned to create electricity.

Temperatures will generally cause BCF fluctuations between -12 and 12 additional BCF per region. A reading of 12 would be caused by extremely warm conditions (compared to usual) and -12 would be caused by extremely cold conditions (compared to usual).

BP

Ca

na

da

Co

mm

od

ity T

rad

ing

Ca

se B

rief

27

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

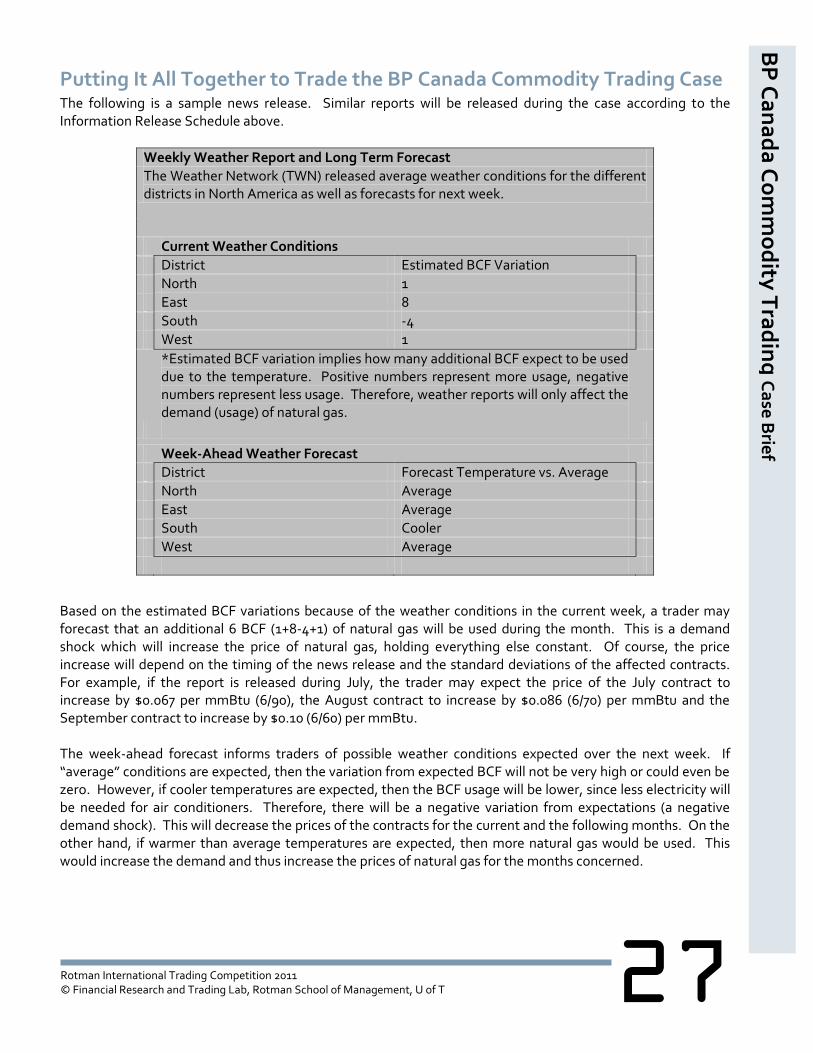

Putting It All Together to Trade the BP Canada Commodity Trading Case The following is a sample news release. Similar reports will be released during the case according to the Information Release Schedule above.

Weekly Weather Report and Long Term Forecast

The Weather Network (TWN) released average weather conditions for the different districts in North America as well as forecasts for next week.

Current Weather Conditions

District Estimated BCF Variation

North 1

East 8

South -4

West 1

*Estimated BCF variation implies how many additional BCF expect to be used due to the temperature. Positive numbers represent more usage, negative numbers represent less usage. Therefore, weather reports will only affect the demand (usage) of natural gas.

Week-Ahead Weather Forecast

District Forecast Temperature vs. Average

North Average

East Average

South Cooler

West Average

Based on the estimated BCF variations because of the weather conditions in the current week, a trader may forecast that an additional 6 BCF (1+8-4+1) of natural gas will be used during the month. This is a demand shock which will increase the price of natural gas, holding everything else constant. Of course, the price increase will depend on the timing of the news release and the standard deviations of the affected contracts. For example, if the report is released during July, the trader may expect the price of the July contract to increase by $0.067 per mmBtu (6/90), the August contract to increase by $0.086 (6/70) per mmBtu and the September contract to increase by $0.10 (6/60) per mmBtu. The week-ahead forecast informs traders of possible weather conditions expected over the next week. If “average” conditions are expected, then the variation from expected BCF will not be very high or could even be zero. However, if cooler temperatures are expected, then the BCF usage will be lower, since less electricity will be needed for air conditioners. Therefore, there will be a negative variation from expectations (a negative demand shock). This will decrease the prices of the contracts for the current and the following months. On the other hand, if warmer than average temperatures are expected, then more natural gas would be used. This would increase the demand and thus increase the prices of natural gas for the months concerned.

BP

Ca

na

da

Co

mm

od

ity T

rad

ing

Ca

se B

rief

28

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

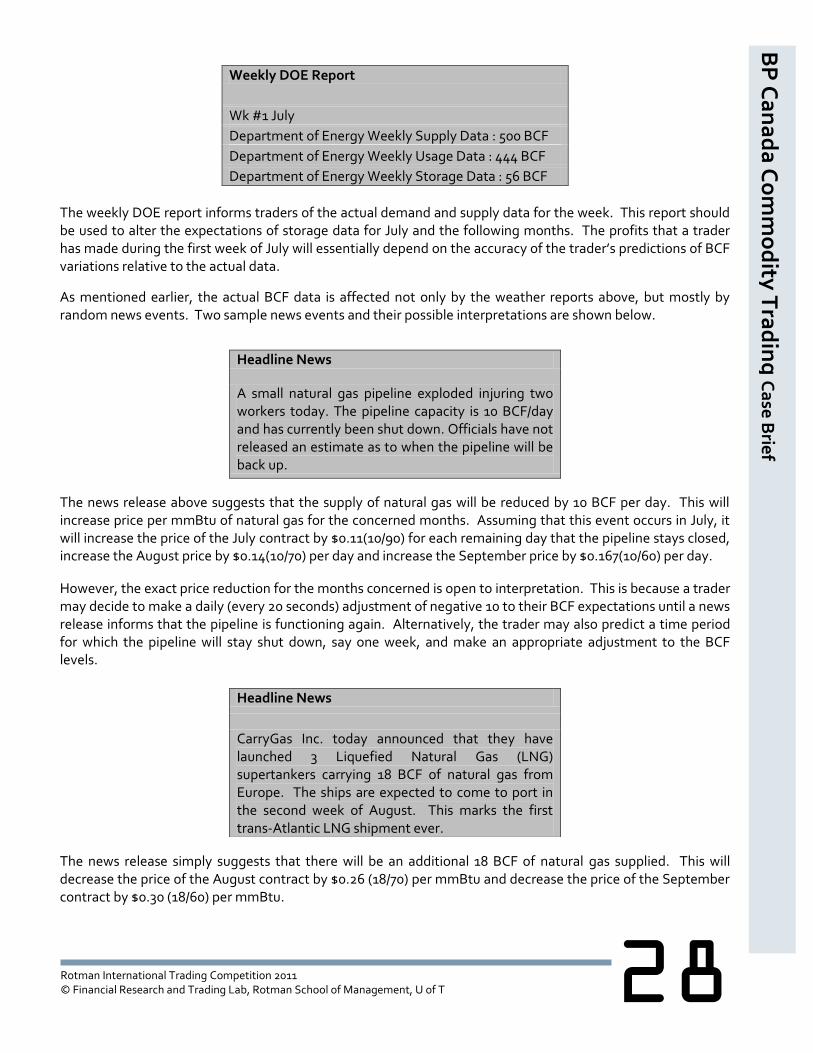

Weekly DOE Report

Wk #1 July

Department of Energy Weekly Supply Data : 500 BCF

Department of Energy Weekly Usage Data : 444 BCF

Department of Energy Weekly Storage Data : 56 BCF

The weekly DOE report informs traders of the actual demand and supply data for the week. This report should be used to alter the expectations of storage data for July and the following months. The profits that a trader has made during the first week of July will essentially depend on the accuracy of the trader’s predictions of BCF variations relative to the actual data.

As mentioned earlier, the actual BCF data is affected not only by the weather reports above, but mostly by random news events. Two sample news events and their possible interpretations are shown below.

Headline News

A small natural gas pipeline exploded injuring two workers today. The pipeline capacity is 10 BCF/day and has currently been shut down. Officials have not released an estimate as to when the pipeline will be back up.

The news release above suggests that the supply of natural gas will be reduced by 10 BCF per day. This will increase price per mmBtu of natural gas for the concerned months. Assuming that this event occurs in July, it will increase the price of the July contract by $0.11(10/90) for each remaining day that the pipeline stays closed, increase the August price by $0.14(10/70) per day and increase the September price by $0.167(10/60) per day.

However, the exact price reduction for the months concerned is open to interpretation. This is because a trader may decide to make a daily (every 20 seconds) adjustment of negative 10 to their BCF expectations until a news release informs that the pipeline is functioning again. Alternatively, the trader may also predict a time period for which the pipeline will stay shut down, say one week, and make an appropriate adjustment to the BCF levels.

The news release simply suggests that there will be an additional 18 BCF of natural gas supplied. This will decrease the price of the August contract by $0.26 (18/70) per mmBtu and decrease the price of the September contract by $0.30 (18/60) per mmBtu.

Headline News

CarryGas Inc. today announced that they have launched 3 Liquefied Natural Gas (LNG) supertankers carrying 18 BCF of natural gas from Europe. The ships are expected to come to port in the second week of August. This marks the first trans-Atlantic LNG shipment ever.

BP

Ca

na

da

Co

mm

od

ity T

rad

ing

Ca

se B

rief

29

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

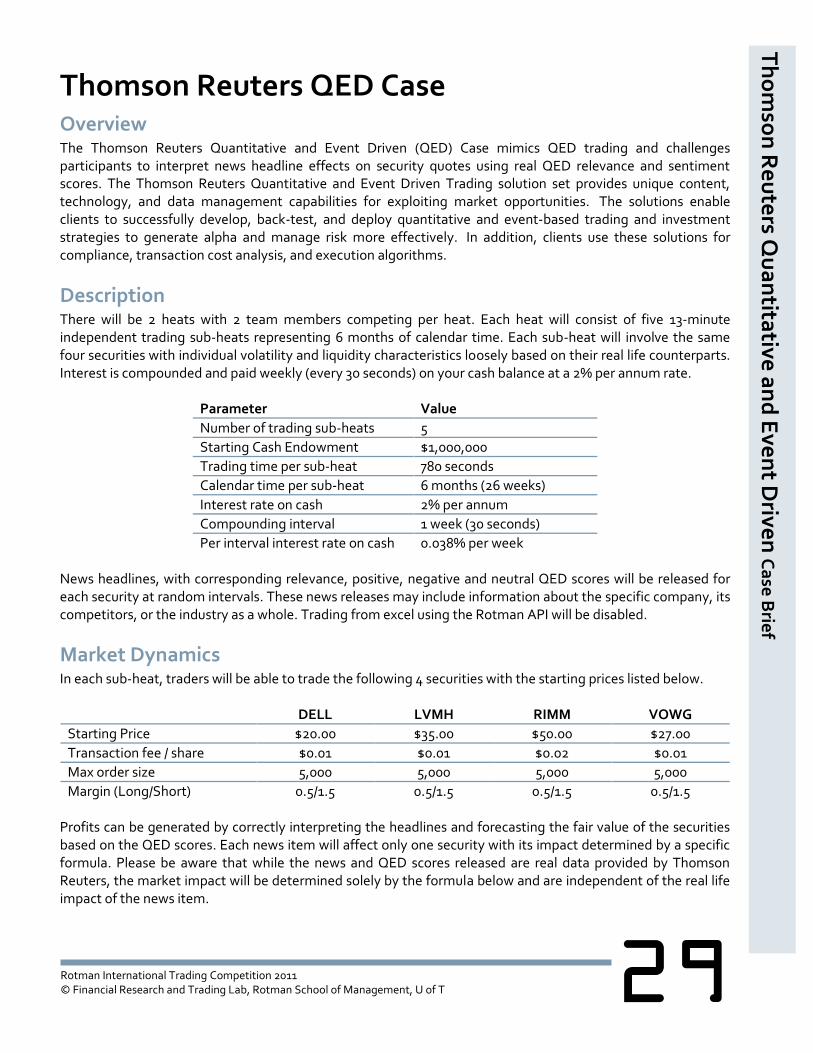

Thomson Reuters QED Case Overview The Thomson Reuters Quantitative and Event Driven (QED) Case mimics QED trading and challenges participants to interpret news headline effects on security quotes using real QED relevance and sentiment scores. The Thomson Reuters Quantitative and Event Driven Trading solution set provides unique content, technology, and data management capabilities for exploiting market opportunities. The solutions enable clients to successfully develop, back-test, and deploy quantitative and event-based trading and investment strategies to generate alpha and manage risk more effectively. In addition, clients use these solutions for compliance, transaction cost analysis, and execution algorithms.

Description There will be 2 heats with 2 team members competing per heat. Each heat will consist of five 13-minute independent trading sub-heats representing 6 months of calendar time. Each sub-heat will involve the same four securities with individual volatility and liquidity characteristics loosely based on their real life counterparts. Interest is compounded and paid weekly (every 30 seconds) on your cash balance at a 2% per annum rate.

Parameter Value

Number of trading sub-heats 5

Starting Cash Endowment $1,000,000

Trading time per sub-heat 780 seconds

Calendar time per sub-heat 6 months (26 weeks)

Interest rate on cash 2% per annum

Compounding interval 1 week (30 seconds)

Per interval interest rate on cash 0.038% per week News headlines, with corresponding relevance, positive, negative and neutral QED scores will be released for each security at random intervals. These news releases may include information about the specific company, its competitors, or the industry as a whole. Trading from excel using the Rotman API will be disabled.

Market Dynamics In each sub-heat, traders will be able to trade the following 4 securities with the starting prices listed below.

DELL LVMH RIMM VOWG

Starting Price $20.00 $35.00 $50.00 $27.00

Transaction fee / share $0.01 $0.01 $0.02 $0.01

Max order size 5,000 5,000 5,000 5,000

Margin (Long/Short) 0.5/1.5 0.5/1.5 0.5/1.5 0.5/1.5 Profits can be generated by correctly interpreting the headlines and forecasting the fair value of the securities based on the QED scores. Each news item will affect only one security with its impact determined by a specific formula. Please be aware that while the news and QED scores released are real data provided by Thomson Reuters, the market impact will be determined solely by the formula below and are independent of the real life impact of the news item.

Th

om

son

Re

ute

rs Qu

an

titative

an

d E

ven

t Drive

n C

ase

Brie

f

30

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

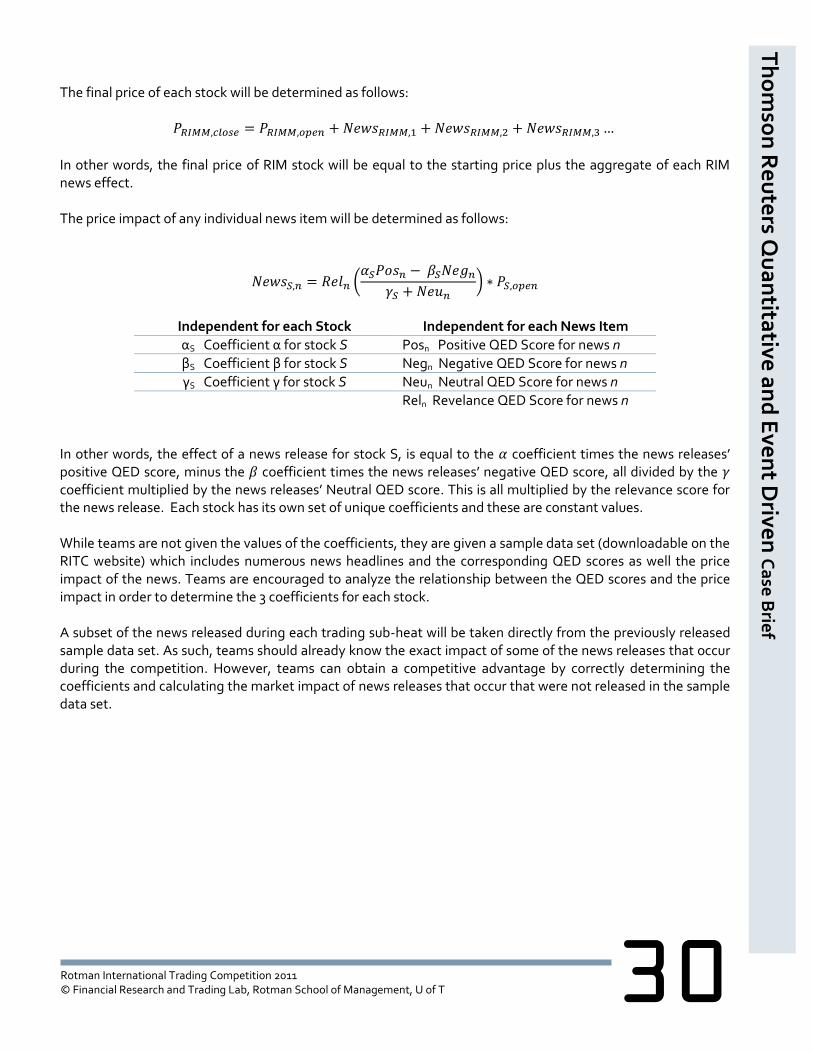

The final price of each stock will be determined as follows:

In other words, the final price of RIM stock will be equal to the starting price plus the aggregate of each RIM news effect. The price impact of any individual news item will be determined as follows:

(

)

Independent for each Stock Independent for each News Item

αS Coefficient α for stock S Posn Positive QED Score for news n

βS Coefficient β for stock S Negn Negative QED Score for news n

γS Coefficient γ for stock S Neun Neutral QED Score for news n

Reln Revelance QED Score for news n In other words, the effect of a news release for stock S, is equal to the coefficient times the news releases’ positive QED score, minus the coefficient times the news releases’ negative QED score, all divided by the coefficient multiplied by the news releases’ Neutral QED score. This is all multiplied by the relevance score for the news release. Each stock has its own set of unique coefficients and these are constant values. While teams are not given the values of the coefficients, they are given a sample data set (downloadable on the RITC website) which includes numerous news headlines and the corresponding QED scores as well the price impact of the news. Teams are encouraged to analyze the relationship between the QED scores and the price impact in order to determine the 3 coefficients for each stock. A subset of the news released during each trading sub-heat will be taken directly from the previously released sample data set. As such, teams should already know the exact impact of some of the news releases that occur during the competition. However, teams can obtain a competitive advantage by correctly determining the coefficients and calculating the market impact of news releases that occur that were not released in the sample data set.

Th

om

son

Re

ute

rs Qu

an

titative

an

d E

ven

t Drive

n C

ase

Brie

f

31

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

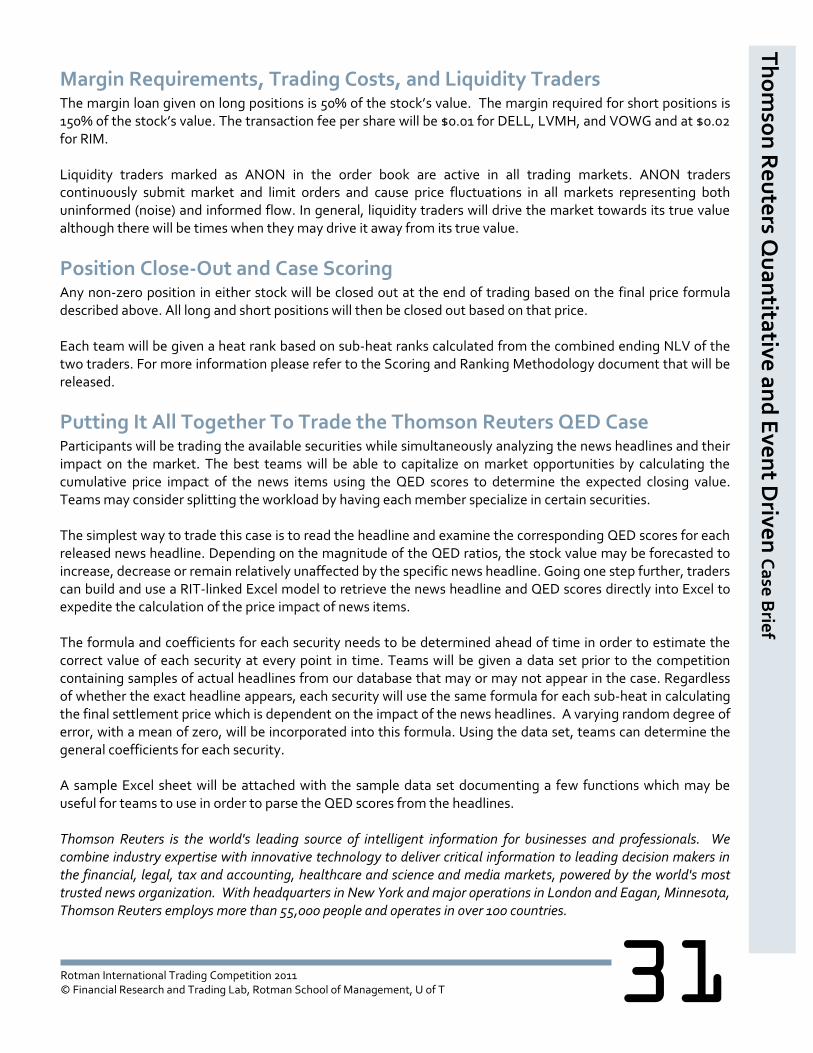

Margin Requirements, Trading Costs, and Liquidity Traders The margin loan given on long positions is 50% of the stock’s value. The margin required for short positions is 150% of the stock’s value. The transaction fee per share will be $0.01 for DELL, LVMH, and VOWG and at $0.02 for RIM. Liquidity traders marked as ANON in the order book are active in all trading markets. ANON traders continuously submit market and limit orders and cause price fluctuations in all markets representing both uninformed (noise) and informed flow. In general, liquidity traders will drive the market towards its true value although there will be times when they may drive it away from its true value.

Position Close-Out and Case Scoring Any non-zero position in either stock will be closed out at the end of trading based on the final price formula described above. All long and short positions will then be closed out based on that price. Each team will be given a heat rank based on sub-heat ranks calculated from the combined ending NLV of the two traders. For more information please refer to the Scoring and Ranking Methodology document that will be released.

Putting It All Together To Trade the Thomson Reuters QED Case Participants will be trading the available securities while simultaneously analyzing the news headlines and their impact on the market. The best teams will be able to capitalize on market opportunities by calculating the cumulative price impact of the news items using the QED scores to determine the expected closing value. Teams may consider splitting the workload by having each member specialize in certain securities. The simplest way to trade this case is to read the headline and examine the corresponding QED scores for each released news headline. Depending on the magnitude of the QED ratios, the stock value may be forecasted to increase, decrease or remain relatively unaffected by the specific news headline. Going one step further, traders can build and use a RIT-linked Excel model to retrieve the news headline and QED scores directly into Excel to expedite the calculation of the price impact of news items. The formula and coefficients for each security needs to be determined ahead of time in order to estimate the correct value of each security at every point in time. Teams will be given a data set prior to the competition containing samples of actual headlines from our database that may or may not appear in the case. Regardless of whether the exact headline appears, each security will use the same formula for each sub-heat in calculating the final settlement price which is dependent on the impact of the news headlines. A varying random degree of error, with a mean of zero, will be incorporated into this formula. Using the data set, teams can determine the general coefficients for each security. A sample Excel sheet will be attached with the sample data set documenting a few functions which may be useful for teams to use in order to parse the QED scores from the headlines. Thomson Reuters is the world's leading source of intelligent information for businesses and professionals. We combine industry expertise with innovative technology to deliver critical information to leading decision makers in the financial, legal, tax and accounting, healthcare and science and media markets, powered by the world's most trusted news organization. With headquarters in New York and major operations in London and Eagan, Minnesota, Thomson Reuters employs more than 55,000 people and operates in over 100 countries.

Th

om

son

Re

ute

rs Qu

an

titative

an

d E

ven

t Drive

n C

ase

Brie

f

32

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

CIBC Algorithmic HFT Case Overview Algorithmic trading is a method used to both manage the market impact of trades as well as automate market making operations. This is achieved by dividing larger volume orders into smaller trades and submitting them electronically. The Algorithmic Trading Case allows competitors to explore these applications of automated trading through the development of their own algorithm. Throughout the design and implementation process, competitors are challenged to strategically think and apply their knowledge of risk management and market making. Furthermore, competitors will experience the role of adjusting their algorithm on the fly in response to both changing market conditions and competition from other algorithms.

Description There will be 4 rounds with 1 team member competing per round. Each team member must compete in one and only one round that will be assigned prior to the start of the competition. Each round will consist of three 5-minute sub-heats representing one hour of trading. Each team will be trading with up to 12 additional teams at a time within one market.

Parameter Value

Number of trading rounds 4 preliminary rounds + 1 final round

Number of trading sub-heats 3

Trading time per sub-heat 300 seconds

Calendar time per sub-heat 1 hour

Trading days per year 252 Days (6.5 hours per trading day)

Interest rate on cash 0% per annum

All trades must be automatically executed by a trading algorithm. Traders will not be allowed to interact with the RIT Client once the case begins. However, traders are allowed to and encouraged to use and modify their Excel spreadsheets in response to prevailing market conditions and competition from the algorithms of other teams. In addition, they will have 3 minutes in between each sub-heat to alter their algorithm. A base template algorithm will be provided for traders and can be directly modified for use in the competition. Alternatively, traders can create their own algorithm using Excel VBA.

Market Dynamics Each trader will be able to trade four securities of which the details are shown below.

ALGO FRTL RITC RTHM

Starting Price 20 20 20 20

Fee / share (Market orders) 0.0050 0.0050 0.0050 0.0050

Rebate / share (Limit/Passive orders) 0.0025 0.0025 0.0025 0.0025

Max order size 5,000 5,000 5,000 5,000

Margin (Long/Short) 0.5/1.5 0.5/1.5 0.5/1.5 0.5/1.5

Annualized volatility 18% 18% 18% 18%

CIB

C A

lgo

rithm

ic Hig

h F

req

ue

ncy

Tra

din

g C

ase

Brie

f

33

Rotman International Trading Competition 2011 © Financial Research and Trading Lab, Rotman School of Management, U of T

The starting positions for each sub-heat will vary and is outlined below.

Starting Amt/Pos. Cash ALGO FRTL RITC RTHM

Sub-heat 1 $75,000 12,500 8,000 5,000 0

Sub-heat 2 $75,000 0 5,000 8,000 12,500

Sub-heat 3 $975,000 0 -10,000 -10,000 0

There will be no information provided that will allow teams to predict the future price or direction of any security. In addition, all teams will start with the same initial positions at the beginning of each sub-heat. While unwinding their positions, teams may choose to simultaneously have their algorithm automatically generate and execute orders in other markets. A fee-rebate structure will be instituted to compensate traders for the addition of liquidity through limit orders. As such, traders will have the opportunity to generate returns by market making.