risks and perspectives in european energy markets · risks and perspectives in european energy...

TRANSCRIPT

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

Risks and perspectives in European Energy Markets

Christoph Weber

Essen, March 23, 2015

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

• What has gone wrong for power producers in Germany and elsewhere between 2007 and 2014?

• What is happening with fossil fuel prices?

• What are the perspectives for carbon pricing?

Key questions for European Energy Markets

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3

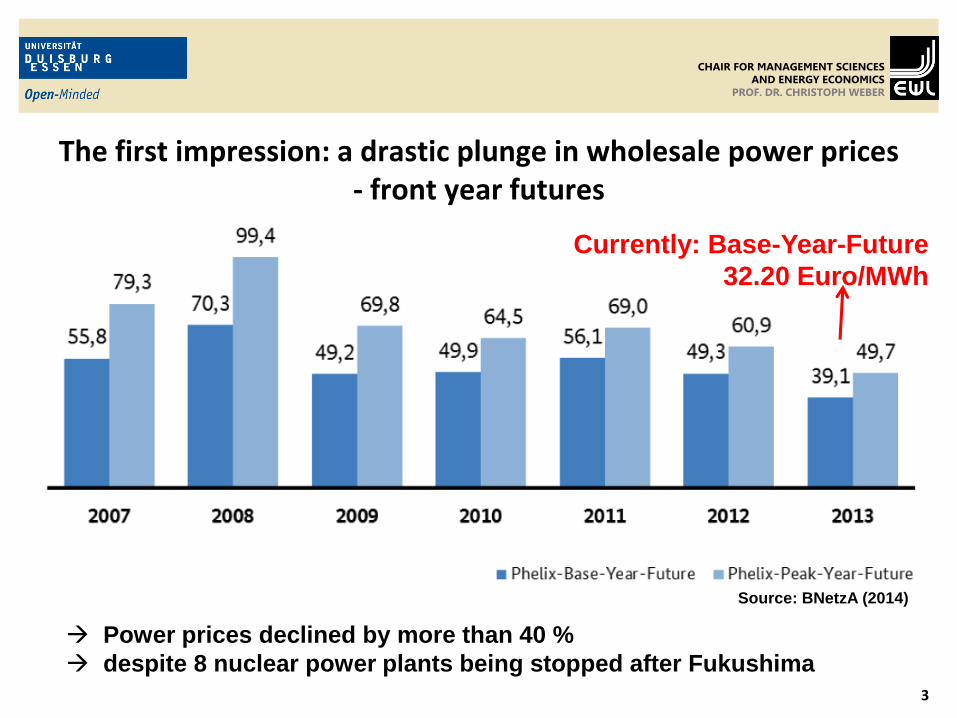

The first impression: a drastic plunge in wholesale power prices- front year futures

Source: BNetzA (2014)

Currently: Base-Year-Future

32.20 Euro/MWh

Power prices declined by more than 40 %

despite 8 nuclear power plants being stopped after Fukushima

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 4www.ewl.wiwi.uni-due.de/en

30

40

50

60

70

80

90

20

07

_Q

4

20

08

_Q

1

20

08

_Q

2

20

08

_Q

3

20

08

_Q

4

20

09

_Q

1

20

09

_Q

2

20

09

_Q

3

20

09

_Q

4

20

10

_Q

1

20

10

_Q

2

20

10

_Q

3

20

10

_Q

4

20

11

_Q

1

20

11

_Q

2

20

11

_Q

3

20

11

_Q

4

20

12

_Q

1

20

12

_Q

2

20

12

_Q

3

20

12

_Q

4

20

13

_Q

1

20

13

_Q

2

20

13

_Q

3

20

13

_Q

4

EU

R/M

Wh

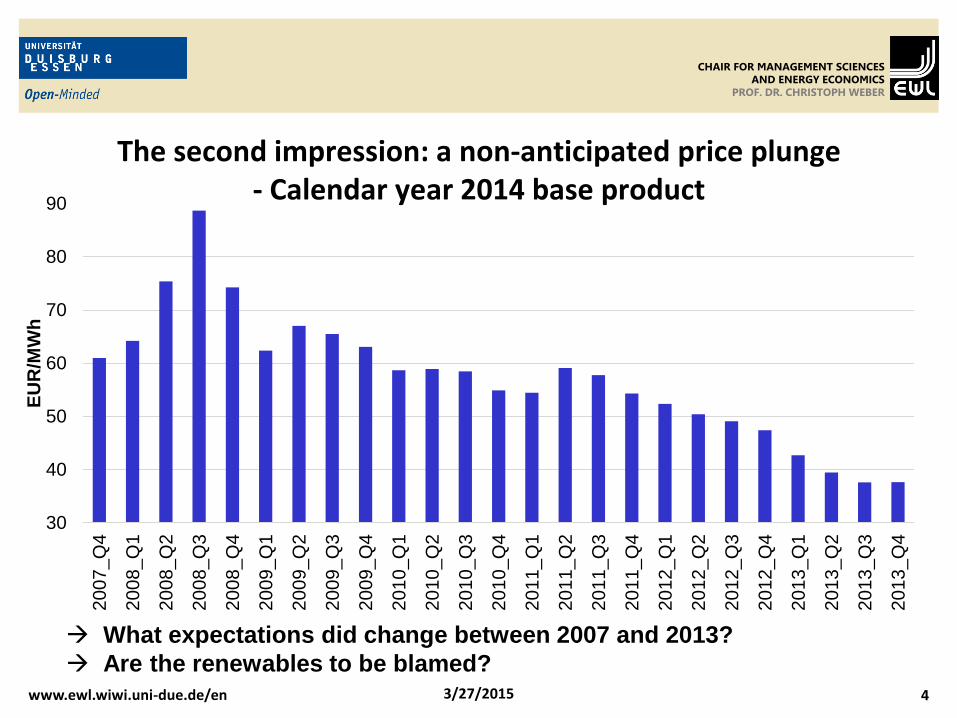

What expectations did change between 2007 and 2013?

Are the renewables to be blamed?

The second impression: a non-anticipated price plunge- Calendar year 2014 base product

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 5

• Reconstruction of price expectations in 2007 for 2014

• Use of a parsimonious fundamental model

• Decomposition of price impacts due to changes in

– Renewable penetration

– Conventional capacities

– Fuel prices

– CO2 prices

– Demand

Research approach

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

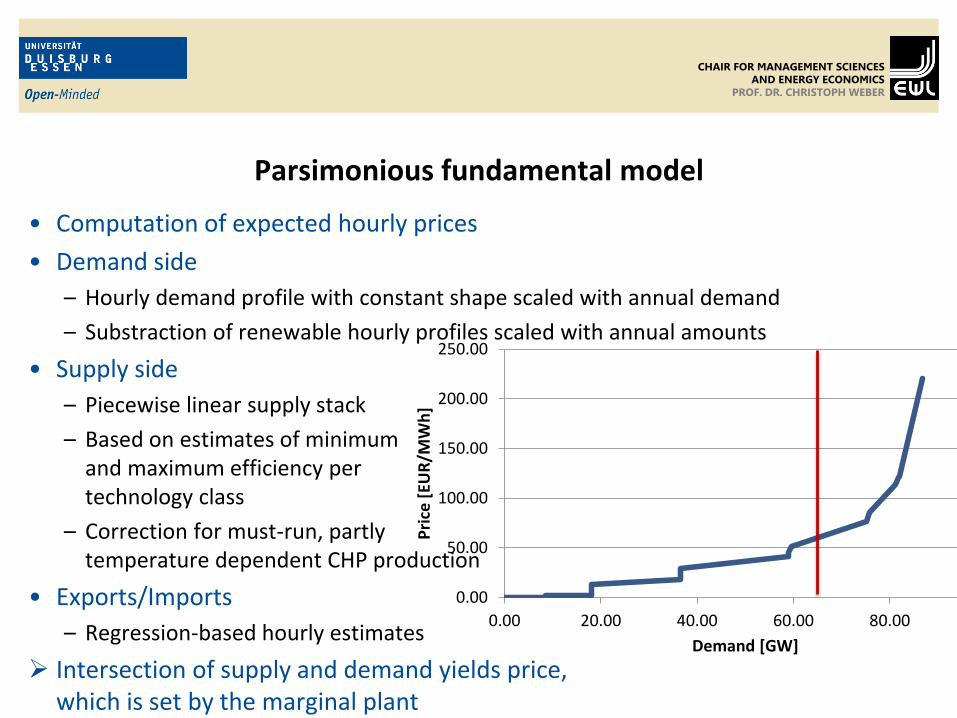

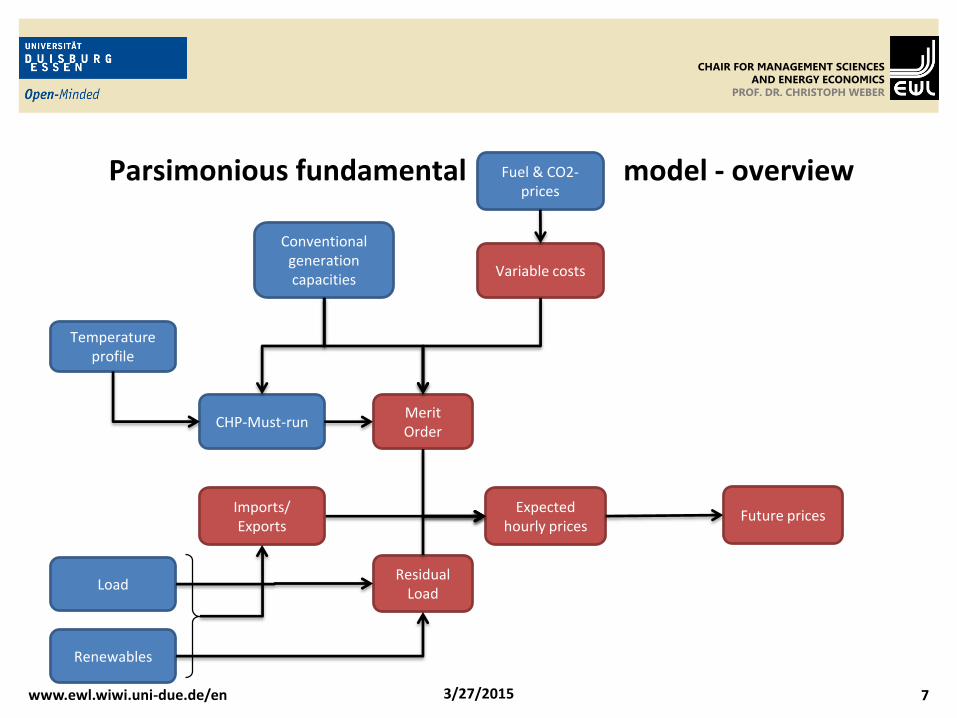

• Computation of expected hourly prices

• Demand side

– Hourly demand profile with constant shape scaled with annual demand

– Substraction of renewable hourly profiles scaled with annual amounts

• Supply side

– Piecewise linear supply stack

– Based on estimates of minimum and maximum efficiency per technology class

– Correction for must-run, partly temperature dependent CHP production

• Exports/Imports

– Regression-based hourly estimates

Intersection of supply and demand yields price, which is set by the marginal plant

Parsimonious fundamental model

0.00

50.00

100.00

150.00

200.00

250.00

0.00 20.00 40.00 60.00 80.00 100.00

Pri

ce [

EUR

/MW

h]

Demand [GW]

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 7

Parsimonious fundamental model - overview

www.ewl.wiwi.uni-due.de/en

Fuel & CO2-prices

Variable costs

Conventional generation capacities

Merit Order

Residual Load

Expected hourly prices

Renewables

CHP-Must-run

Imports/ Exports

Temperatureprofile

Load

Future prices

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 8

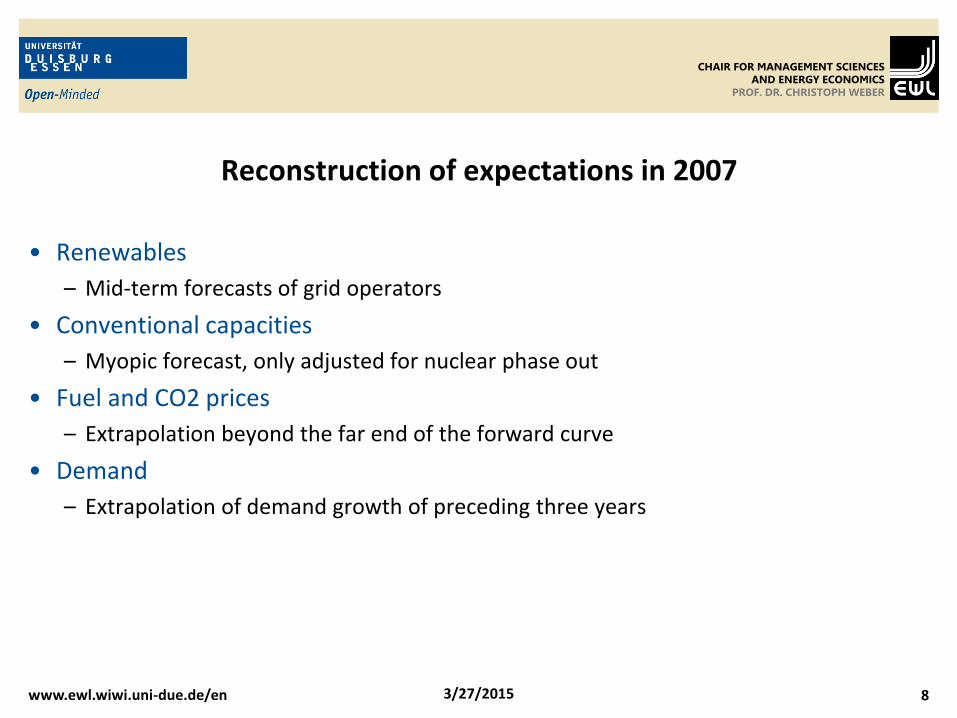

• Renewables

– Mid-term forecasts of grid operators

• Conventional capacities

– Myopic forecast, only adjusted for nuclear phase out

• Fuel and CO2 prices

– Extrapolation beyond the far end of the forward curve

• Demand

– Extrapolation of demand growth of preceding three years

Reconstruction of expectations in 2007

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 9

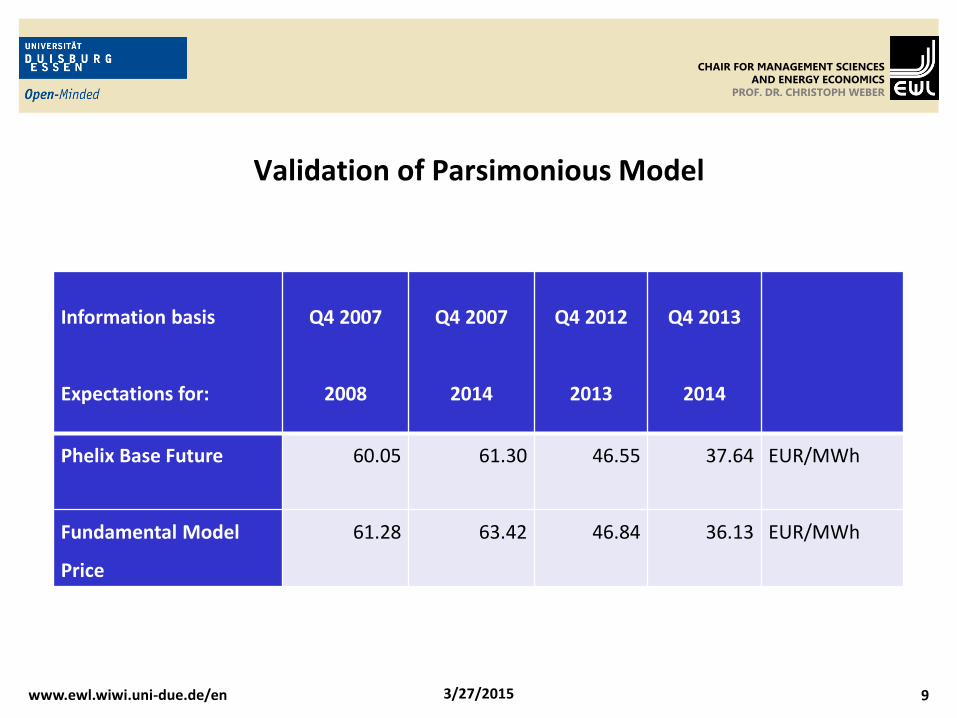

Information basis

Expectations for:

Q4 2007

2008

Q4 2007

2014

Q4 2012

2013

Q4 2013

2014

Phelix Base Future 60.05 61.30 46.55 37.64 EUR/MWh

Fundamental Model

Price

61.28 63.42 46.84 36.13 EUR/MWh

Validation of Parsimonious Model

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 10

Year2014

AbsoluteChanges

RelativeChanges

Unit

Phelix Base Future in Q4 2007 61.30 EUR/MWh

Fundamental Price (Expt. Q4 2007) 63.42 EUR/MWh

Updated Expectations to Q4 2013

Load 59.19 -4.23 -6.7% EUR/MWh

RES 60.39 -3.03 -4.8% EUR/MWh

Fuel Prices 60.63 -2.79 -4.4% EUR/MWh

CO2 Price 49.16 -14.26 -22.5% EUR/MWh

Capacities 63.89 -0.47 +0.7% EUR/MWh

All = Fund. Price (Expt. Q4 2013) 36.13 -27.29 -43.0% EUR/MWh

Phelix Base Future in Q4 2013 37.64 -23.66 -38.6% EUR/MWh

Impact of Expectation Changes on Base Price

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 11

• Strongest price impact through plunge in CO2 price

• RES impact less than 5 %

• Load impact stronger than RES impact

• Impact of fuel prices inhomogenous: coal prices decreased, gas prices increased

CO2 certificates and fuels are input factors for power plants

– impact on profitability possibly different

Impact of Expectation Changes on Base Price

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 12

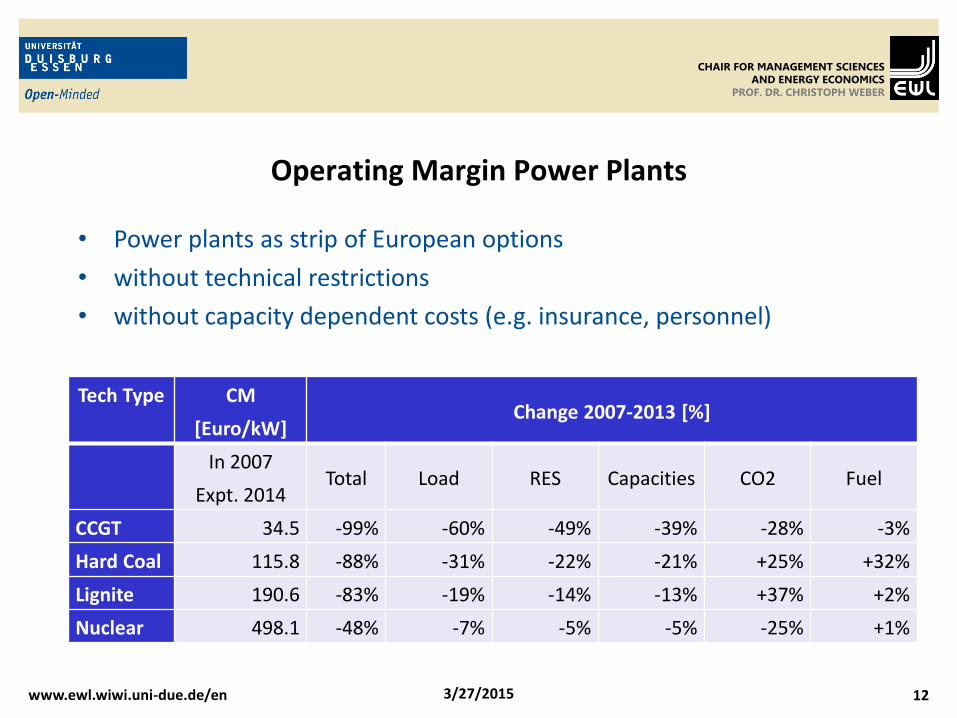

Tech Type CM

[Euro/kW]Change 2007-2013 [%]

In 2007

Expt. 2014Total Load RES Capacities CO2 Fuel

CCGT 34.5 -99% -60% -49% -39% -28% -3%

Hard Coal 115.8 -88% -31% -22% -21% +25% +32%

Lignite 190.6 -83% -19% -14% -13% +37% +2%

Nuclear 498.1 -48% -7% -5% -5% -25% +1%

Operating Margin Power Plants

www.ewl.wiwi.uni-due.de/en

• Power plants as strip of European options

• without technical restrictions

• without capacity dependent costs (e.g. insurance, personnel)

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 13

• More than 80 % drop in operating margins for all plants except nuclear

• Load has single most important impact on all plants except nuclear

• CO2 price plunge has positive impact on lignite and hard coal plants

– With 2007 expectations where gas is rather frequently price setting

– With 2013 expectations much less given that gas is hardly price setting

Strong non-linear superposition effects

Operating Margin Power Plants

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

• What has gone wrong for power producers in Germany and elsewhere between 2007 and 2014?

• What is happening with fossil fuel prices?

• What are the perspectives for carbon pricing?

Key questions for European Energy Markets

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 15

• No crystal ball

• Yet structural modelling of fuel markets possible

Econometric estimation of expected developments and stochastic uncertainty

possible

Learning from the past

Fuel prices of the future

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 16

Oil demand

Oil supply capacity OPEC

Oil supply capacity NOPEC

Structural model of oil prices (C. March 2011) I

www.ewl.wiwi.uni-due.de/en

)log()log()log()log( 1312110 tttt GDPpDD

tDtt GDPp ,21 )log()log(

)log()log()log()log( 13121,10, tttOPECtOPEC KADKK

tKOPECt

i

iti KAD ,2

3

0

,1 )log()log(

))log()(log()log()log()log( 443121,10, ttttNOPECtNOPEC cpDKK

tKNOPECttt cpD ,33211 ))log()(log()log(

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 17

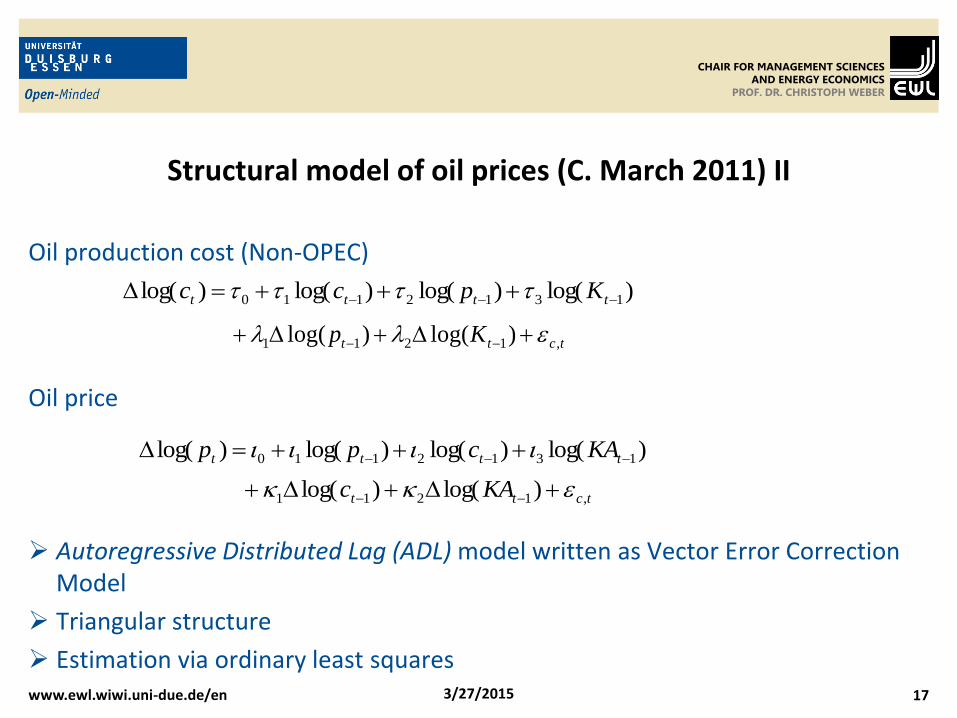

Oil production cost (Non-OPEC)

Oil price

Autoregressive Distributed Lag (ADL) model written as Vector Error CorrectionModel

Triangular structure

Estimation via ordinary least squares

Structural model of oil prices (C. March 2011) II

www.ewl.wiwi.uni-due.de/en

)log()log()log()log( 1312110 tttt Kpcc

tctt Kp ,1211 )log()log(

)log()log()log()log( 1312110 tttt KAcpp

tctt KAc ,1211 )log()log(

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 18

Stochastic oil price forecast (C. March 2011)

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 19

Distribution of oil prices in 2030 (C. March 2011)

www.ewl.wiwi.uni-due.de/en

Prices

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 20

• Large fundamental uncertainty about future price developments

• Key factors

– Economic growth

– Political developments

– Technological improvements

• Price fluctuations amplified by long lead times for new production capacities

– E.g. low price phase from 1986 until approx. 2005

Prices likely to remain below 2008/2011 levels for at least 10 years

Tight oil in the US as marginal producer, lower lead times due to higher production decline rates

Prices below 60 $ not very likely

Fossil fuel perspectives

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

• What has gone wrong for power producers in Germany and elsewhere between 2007 and 2014?

• What is happening with fossil fuel prices?

• What are the perspectives for carbon pricing?

Key questions for European Energy Markets

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 22

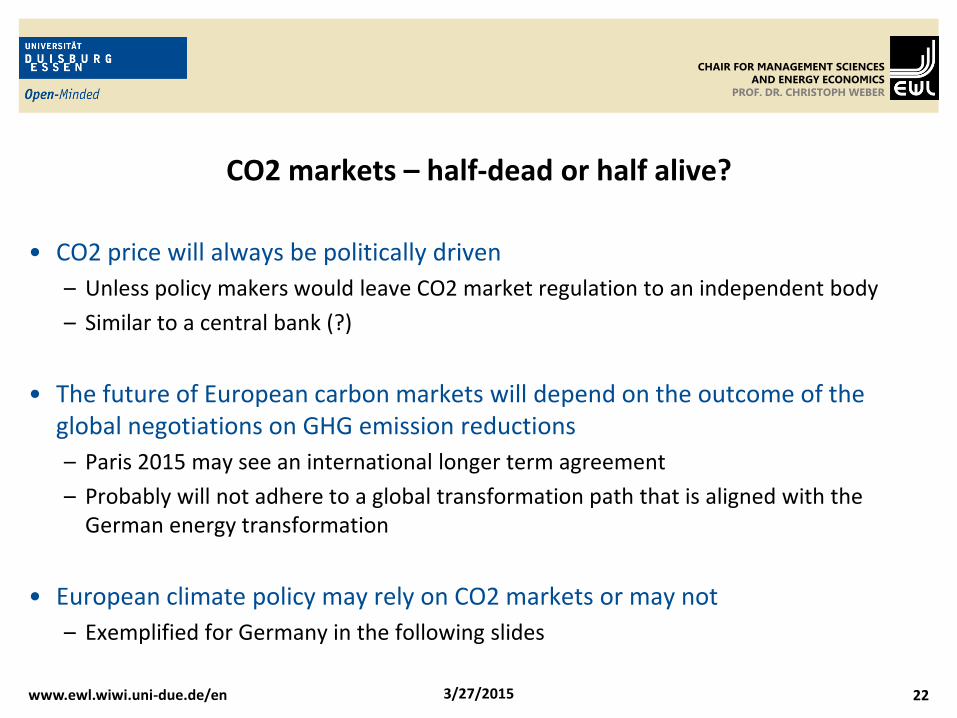

• CO2 price will always be politically driven

– Unless policy makers would leave CO2 market regulation to an independent body

– Similar to a central bank (?)

• The future of European carbon markets will depend on the outcome of the global negotiations on GHG emission reductions

– Paris 2015 may see an international longer term agreement

– Probably will not adhere to a global transformation path that is aligned with the German energy transformation

• European climate policy may rely on CO2 markets or may not

– Exemplified for Germany in the following slides

CO2 markets – half-dead or half alive?

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

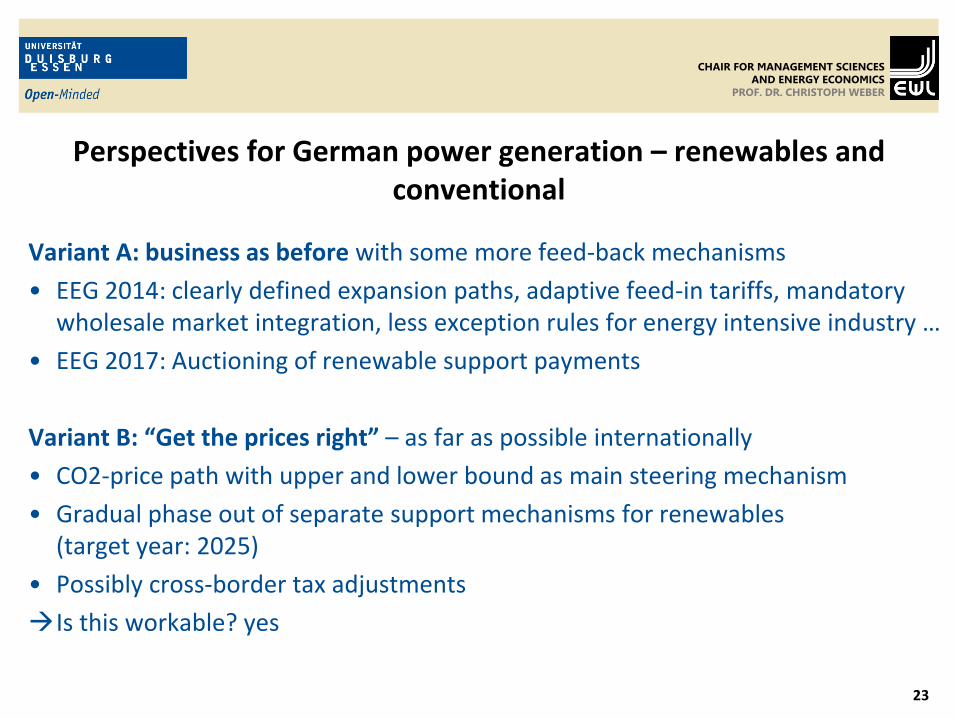

23

Variant A: business as before with some more feed-back mechanisms

• EEG 2014: clearly defined expansion paths, adaptive feed-in tariffs, mandatory wholesale market integration, less exception rules for energy intensive industry …

• EEG 2017: Auctioning of renewable support payments

Variant B: “Get the prices right” – as far as possible internationally

• CO2-price path with upper and lower bound as main steering mechanism

• Gradual phase out of separate support mechanisms for renewables (target year: 2025)

• Possibly cross-border tax adjustments

Is this workable? yes

Perspectives for German power generation – renewables and conventional

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

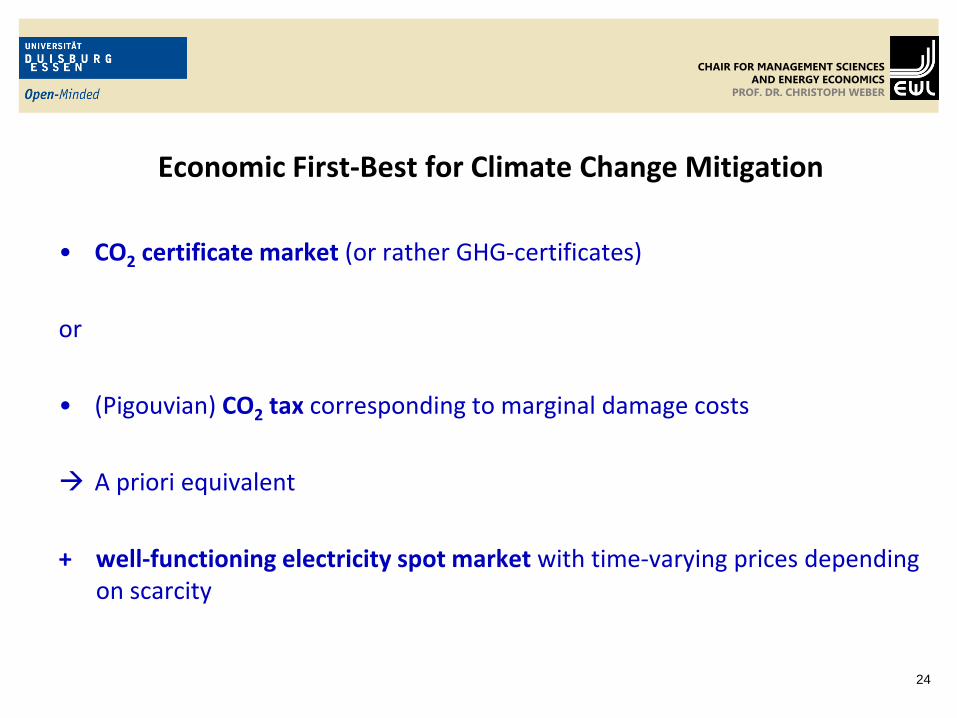

Economic First-Best for Climate Change Mitigation

• CO2 certificate market (or rather GHG-certificates)

or

• (Pigouvian) CO2 tax corresponding to marginal damage costs

A priori equivalent

+ well-functioning electricity spot market with time-varying prices dependingon scarcity

24

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

Exemplary application for Germany– target year 2050 of the Energiewende

• Basis „BMU Leitstudie 2010/2011“ (Environmental ministry foresight study)

• „long term“ – all plant capacities may be chosen flexibly

• Focus on 9 technologies for investment

– Lignite power plant

– Hard coal power plant

– CCGT

– OCGT

– Biogas motor engine (500 kW)

– Biomass power plant (10 MW)

– Wind onshore (5,5 MW)

– Wind offshore (12 MW)

– PV small scale (5 kW)

• CO2 reduction target: -85 % compared to 1990 27

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

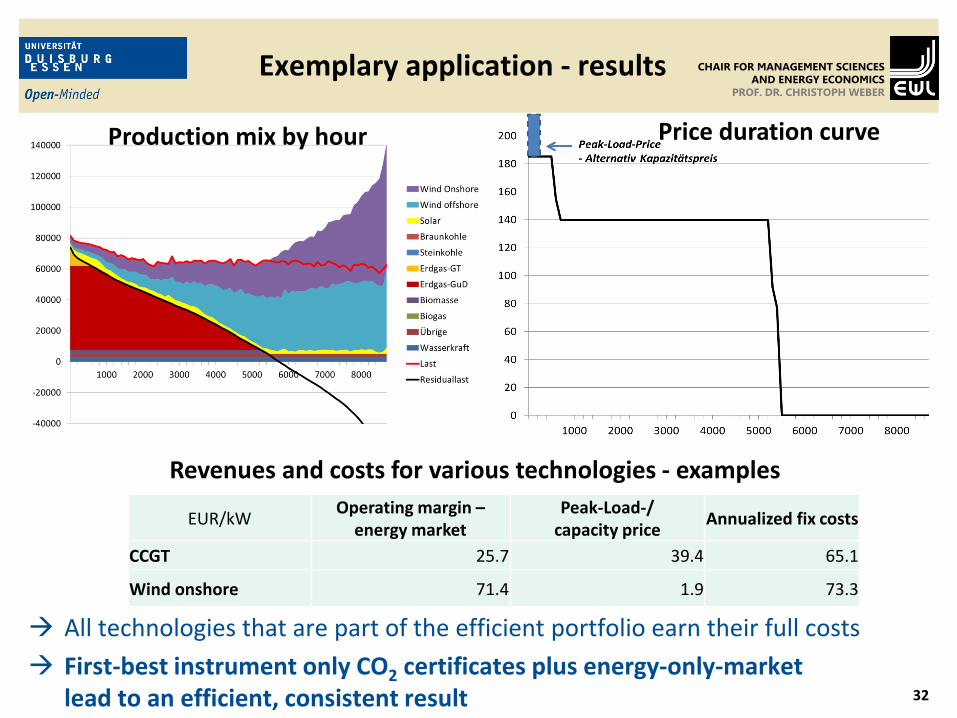

Exemplary Application - results

• CO2 price 67 EUR/t

• Capacity mix (in GW)

• about 3000 hours with zero prices

Results sensitive with respect to cost assumptions 28

Lignite 0

Hard coal 0

CCGT 60.5

OCGT 21.9

Biomass 2.8

Biogas 0.0

Solar 27.0

Wind onshore 80.7

Wind offshore 56.5

Hydro 5.2

Others 3.0

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

32

All technologies that are part of the efficient portfolio earn their full costs

First-best instrument only CO2 certificates plus energy-only-marketlead to an efficient, consistent result

Exemplary application - results

EUR/kWOperating margin –

energy marketPeak-Load-/

capacity priceAnnualized fix costs

CCGT 25.7 39.4 65.1

Wind onshore 71.4 1.9 73.3

Revenues and costs for various technologies - examples

Production mix by hour Price duration curve

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

• Appropriate incentives for storages and load management

– High price differences between hours with production excess and scarcity

– No arbitrary incentives which are possibly not aligned on actual scarcities

• Adequate costs and prices for power plants with CO2 emissions

– Price-based and not administrative phase out of coal power plants

– Fears of supply interruptions for natural gas may be countered by imposing storage requirements in the gas market

• Incentives for a mix of renewables

– Technology mix between wind and solar is economically advantageous

– Diversification of locations is supported, also diversification in orientation of solar panels or construction of low-wind plants

– Incentives for controllable RES like Biomass

Advantages of the economic first-best solution

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

34

• Grid as monopolistic bottleneck is not adequately incentivised

• Supply security has (so far) characteristics of a collective good

• Appropriateness of market prices for societal risks

• International inconsistencies

• Distributional effects

Problems of the market-based solution

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 35

• Energy markets are undergoing a period of disequilibria and uncertainties

• Market-based solutions have been under attackyet non-market-based solutions have also proven weaknesses

• Mathematical modelling and quantification of risks remains a challenging issue

• Identification and handling of societal risks another key challenge

We here in Essen want to contribute to the analysis of these market transformations – through our new House of Energy Markets and Finance

Conclusions

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

3/27/2015 36

• Research Institute in the Department of Economics of the University Duisburg-Essen

• Founding Members:

Prof. Rüdiger Kiesel, Chair for Energy Trading and Financial Services

Prof. Ansgar Belke, Chair for Macroeconomics

Prof. Rainer Elschen, Chair for Finance and Banking

Prof. Christoph Weber, Chair for Management Sciences and Energy Economics

• Key objective:

Combining economic, finance and engineering competences for the analysis of the on-going transformation of energy markets

House of Energy Markets and Finance

www.ewl.wiwi.uni-due.de/en

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

CHAIR FOR MANAGEMENT SCIENCESAND ENERGY ECONOMICS

PROF. DR. CHRISTOPH WEBER

Thank you for your attention

Contact: Christoph Weber

E-Mail: [email protected]

Phone.: +49 201/183-2966