risk and asset allocation: value at risk, · pdf filerisk and asset allocation: value at risk,...

TRANSCRIPT

RISK AND ASSET ALLOCATION:

Value at Risk, Conditional-VaR and Copula Modelling

Dean Fantazzini

July 8-12th, 2007, Meielisalp, (Switzerland)

Overview of the Presentation

1st Introduction

1st International R/Rmetrics User and Developer Workshop 2

Overview of the Presentation

1st Introduction

2nd Risk Measures: VaR and C-VaR

1st International R/Rmetrics User and Developer Workshop 2-a

Overview of the Presentation

1st Introduction

2nd Risk Measures: VaR and C-VaR

3rd Advanced Multivariate Modelling: The Theory of Copulas

1st International R/Rmetrics User and Developer Workshop 2-b

Overview of the Presentation

1st Introduction

2nd Risk Measures: VaR and C-VaR

3rd Advanced Multivariate Modelling: The Theory of Copulas

4th Empirical Applications: Market Risk Management for Bivariate

Portfolios

1st International R/Rmetrics User and Developer Workshop 2-c

Overview of the Presentation

1st Introduction

2nd Risk Measures: VaR and C-VaR

3rd Advanced Multivariate Modelling: The Theory of Copulas

4th Empirical Applications: Market Risk Management for Bivariate

Portfolios

5th Empirical Applications: Market Risk Management for

Multivariate Portfolios (Dynamic Grouped-T and T-copulas)

1st International R/Rmetrics User and Developer Workshop 2-d

Overview of the Presentation

1st Introduction

2nd Risk Measures: VaR and C-VaR

3rd Advanced Multivariate Modelling: The Theory of Copulas

4th Empirical Applications: Market Risk Management for Bivariate

Portfolios

5th Empirical Applications: Market Risk Management for

Multivariate Portfolios (Dynamic Grouped-T and T-copulas)

6th Empirical Applications: C-VaR and VaR for Portfolio

Management

1st International R/Rmetrics User and Developer Workshop 2-e

Introduction

In the Mean-Variance model, the risk of a portfolio measured by the

variance takes into account the covariances among the returns of all

investments.

However, this approach is appropriate when dealing with multivariate

Elliptic distributions only, like the multivariate Normal or the multivariate

Student’s T joint distribution.

→ Only if the joint distribution function is elliptical the Markowitz

Mean-Variance approach can give efficient portfolios.

Therefore, more general risk measures have been proposed: the Value at

Risk and (more recently) the Conditional Value at Risk.

1st International R/Rmetrics User and Developer Workshop 3

Introduction

The increasing complexity of financial markets has pointed out the need

for advanced dependence modelling in finance. Why?

• Multivariate models with more flexibility than the multivariate normal

distribution are needed;

• When constructing a model for risk management, the study of both

marginals and the dependence structure is crucial for the analysis. A

wrong choice may lead to severe underestimation of financial risks.

Recent developments in financial studies have tried to tackle these issues

by using the theory of Copulas: see Cherubini et al. (2004) for a general

review of copula methods in finance.

1st International R/Rmetrics User and Developer Workshop 4

Coherent Risk Measures

Artzner, Delbaen, Eber and Heath (1999) examined the issue of setting out

the axioms that a coherent risk measure ought to satisfy. They then looked

for measures that satisfy these properties.

If X and Y are the random variables representing the future values of two

risky investments, a risk measure ρ(·) is said to be coherent if it satisfies

the following properties:

1. Sub-additivity : ρ(X + Y ) ≤ ρ(X) + ρ(Y ) (diversification effect).

2. Monotonicity : ρ(X) ≤ ρ(Y ) whenever X ≤ Y (the bigger the loss the

bigger the risk).

3. Homogeneity : ρ(λX) = λρ(X) for λ > 0 (the risk scales in proportion

to a scaled loss).

4. Translation invariance: ρ(X + rn) = ρ(X) − n (reduction of risk by

investing in the risk-free payoff r).

1st International R/Rmetrics User and Developer Workshop 5

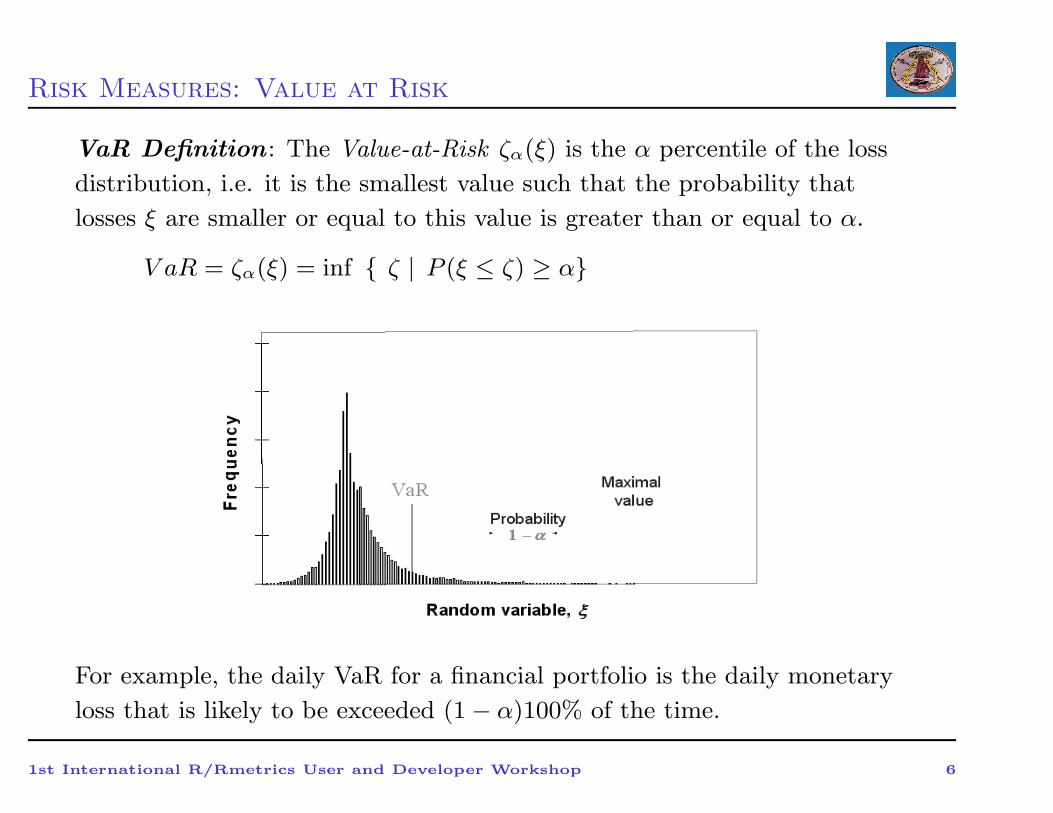

Risk Measures: Value at Risk

VaR Definition : The Value-at-Risk ζα(ξ) is the α percentile of the loss

distribution, i.e. it is the smallest value such that the probability that

losses ξ are smaller or equal to this value is greater than or equal to α.

V aR = ζα(ξ) = inf { ζ | P (ξ ≤ ζ) ≥ α}

For example, the daily VaR for a financial portfolio is the daily monetary

loss that is likely to be exceeded (1 − α)100% of the time.

1st International R/Rmetrics User and Developer Workshop 6

Risk Measures: Value at Risk

• VaR Properties:

• Simple convenient representation of risks (one number);

• Measures downside risk (compared to variance which is impacted by

high returns);

• applicable to nonlinear instruments, such as options, with non-

symmetric (non-normal) loss distributions;

• Does not measure losses exceeding VaR (e.g., excluding or doubling of

big losses in November 1987 may not impact VaR historical estimates)

• Reduction of VaR may lead to stretch of tail exceeding VaR (Yamai

and Yoshiba, 2002)

• Since VaR does not take into account risks exceeding VaR, it may

provide conflicting results at different confidence levels;

• Non-sub-additive and non-convex (portfolio diversification may

increase the risk - Difficult to optimize for non-normal distribution);

1st International R/Rmetrics User and Developer Workshop 7

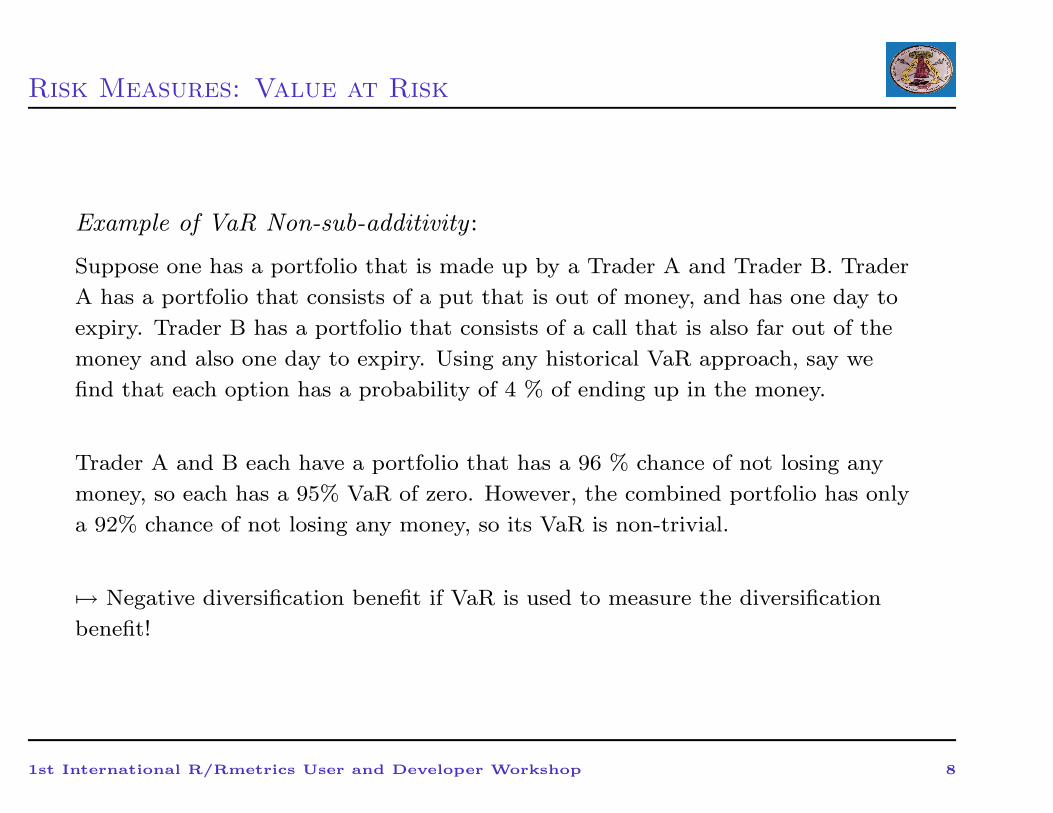

Risk Measures: Value at Risk

Example of VaR Non-sub-additivity :

Suppose one has a portfolio that is made up by a Trader A and Trader B. Trader

A has a portfolio that consists of a put that is out of money, and has one day to

expiry. Trader B has a portfolio that consists of a call that is also far out of the

money and also one day to expiry. Using any historical VaR approach, say we

find that each option has a probability of 4 % of ending up in the money.

Trader A and B each have a portfolio that has a 96 % chance of not losing any

money, so each has a 95% VaR of zero. However, the combined portfolio has only

a 92% chance of not losing any money, so its VaR is non-trivial.

7→ Negative diversification benefit if VaR is used to measure the diversification

benefit!

1st International R/Rmetrics User and Developer Workshop 8

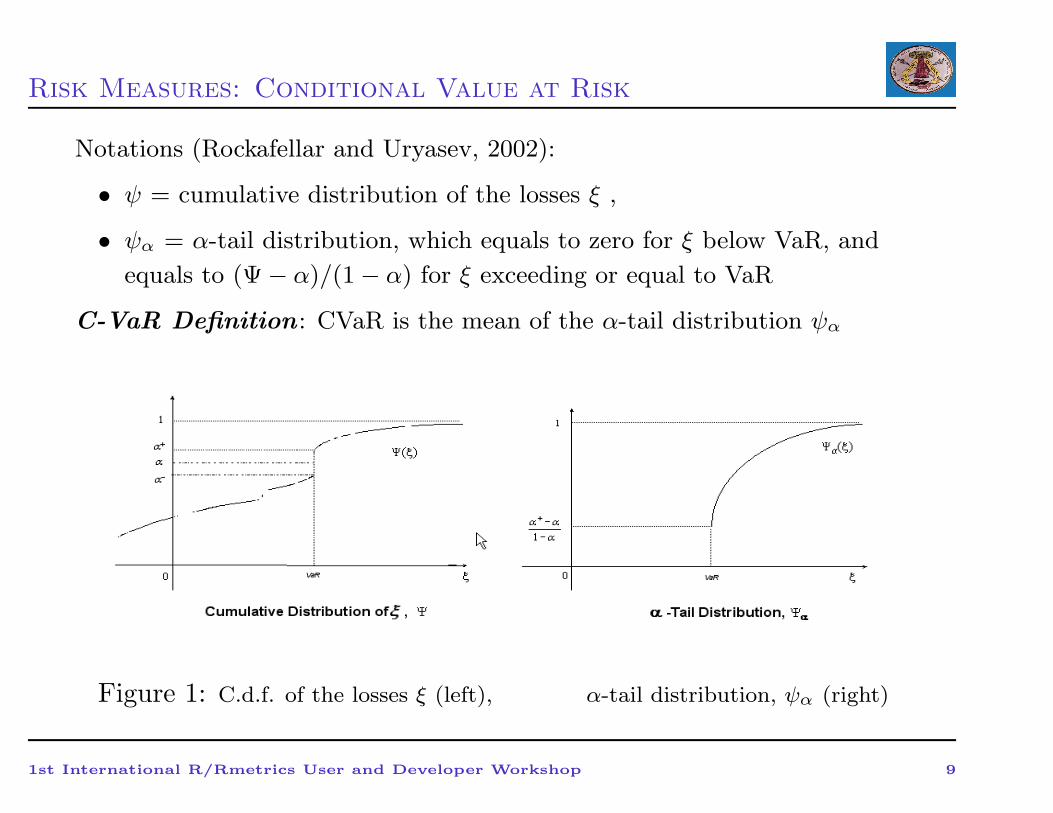

Risk Measures: Conditional Value at Risk

Notations (Rockafellar and Uryasev, 2002):

• ψ = cumulative distribution of the losses ξ ,

• ψα = α-tail distribution, which equals to zero for ξ below VaR, and

equals to (Ψ − α)/(1 − α) for ξ exceeding or equal to VaR

C-VaR Definition : CVaR is the mean of the α-tail distribution ψα

Figure 1: C.d.f. of the losses ξ (left), α-tail distribution, ψα (right)

1st International R/Rmetrics User and Developer Workshop 9

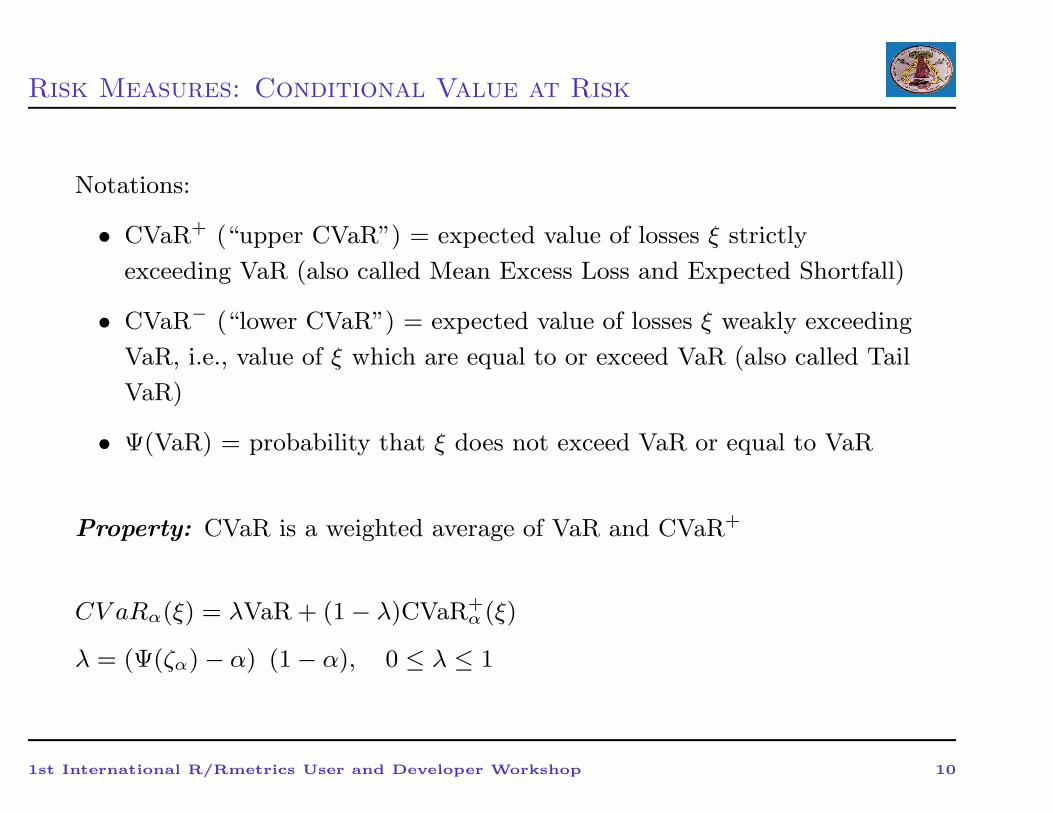

Risk Measures: Conditional Value at Risk

Notations:

• CVaR+ (“upper CVaR”) = expected value of losses ξ strictly

exceeding VaR (also called Mean Excess Loss and Expected Shortfall)

• CVaR− (“lower CVaR”) = expected value of losses ξ weakly exceeding

VaR, i.e., value of ξ which are equal to or exceed VaR (also called Tail

VaR)

• Ψ(VaR) = probability that ξ does not exceed VaR or equal to VaR

Property: CVaR is a weighted average of VaR and CVaR+

CV aRα(ξ) = λVaR + (1 − λ)CVaR+α (ξ)

λ = (Ψ(ζα) − α) (1 − α), 0 ≤ λ ≤ 1

1st International R/Rmetrics User and Developer Workshop 10

Risk Measures: Conditional Value at Risk

1st International R/Rmetrics User and Developer Workshop 11

Risk Measures: Conditional Value at Risk

• C-VaR Properties:

• Simple convenient representation of risks (one number);

• Measures downside risk applicable to non-symmetric loss distributions

CVaR accounts for risks beyond VaR (more conservative than VaR);

• CVaR is convex with respect to control variables;

• VaR ≤ CVaR− ≤ CVaR ≤ CVaR+

• CVaR is continuous with respect to confidence level alpha, consistent

at different confidence levels compared to VaR;

• Consistency with mean-variance approach: for normal loss

distributions optimal variance and CVaR portfolios coincide;

• Easy to control/optimize for non-normal distributions; linear

programming (LP): can be used for optimization of very large

problems.

1st International R/Rmetrics User and Developer Workshop 12

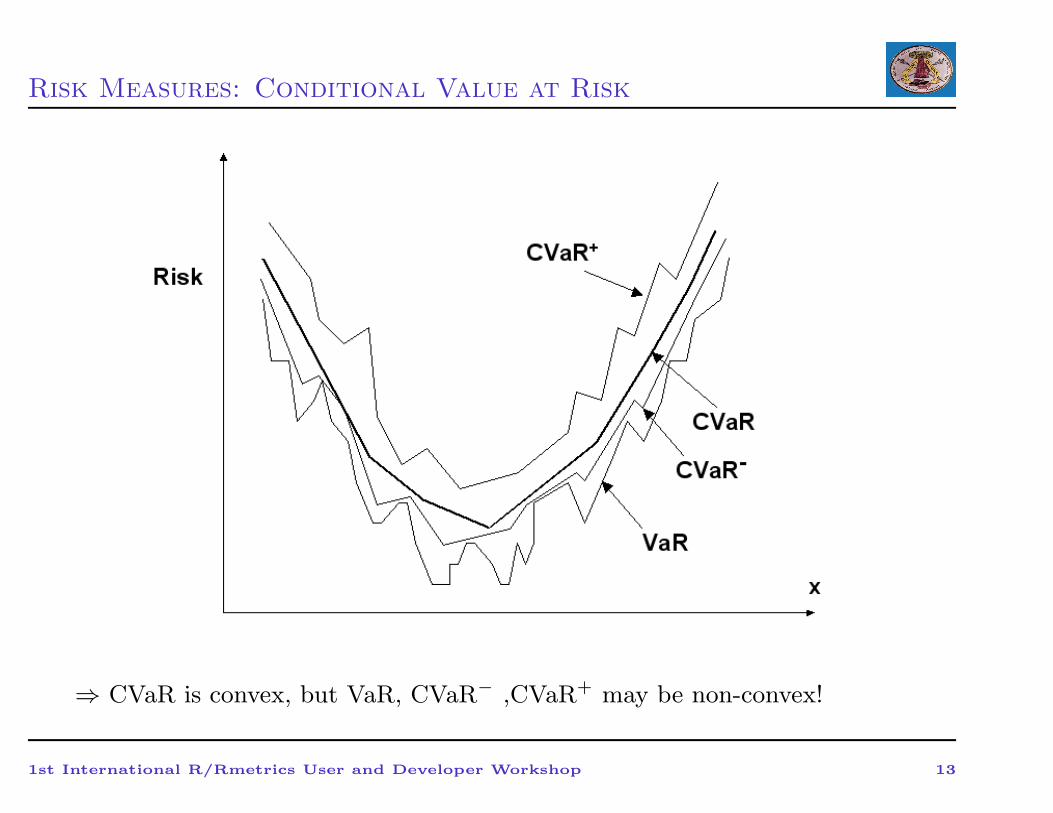

Risk Measures: Conditional Value at Risk

⇒ CVaR is convex, but VaR, CVaR− ,CVaR+ may be non-convex!

1st International R/Rmetrics User and Developer Workshop 13

Risk Measures: Some Examples

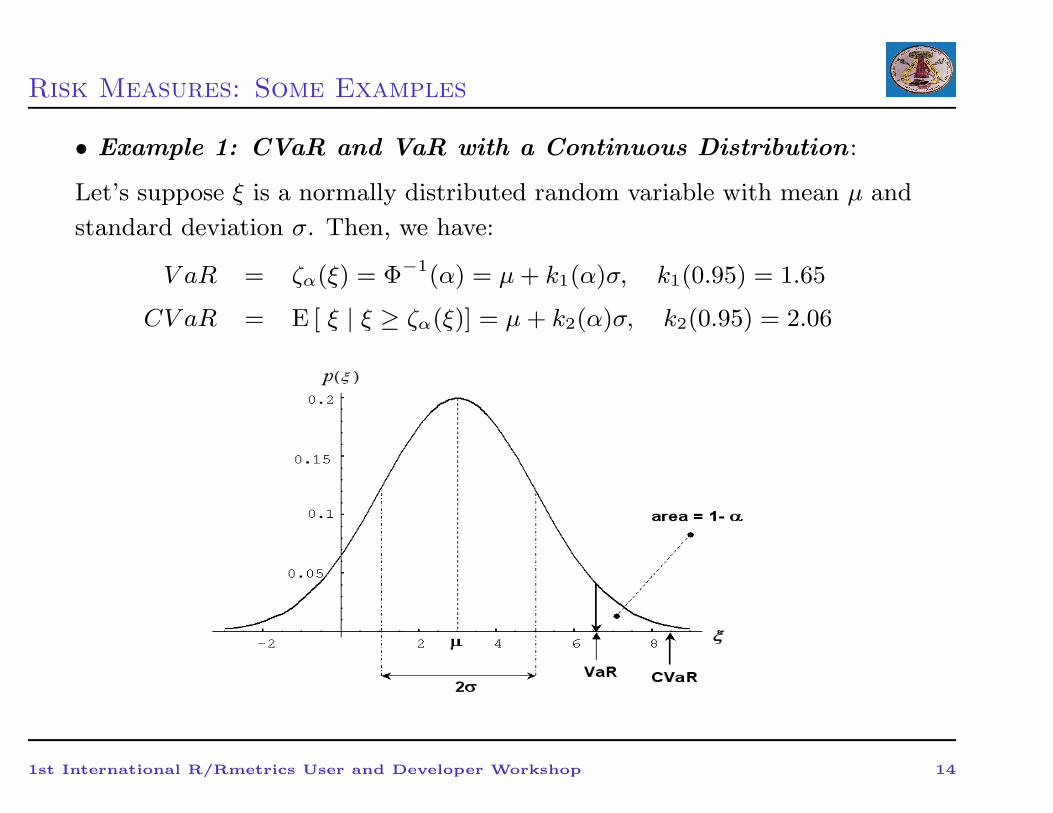

• Example 1: CVaR and VaR with a Continuous Distribution :

Let’s suppose ξ is a normally distributed random variable with mean µ and

standard deviation σ. Then, we have:

V aR = ζα(ξ) = Φ−1(α) = µ+ k1(α)σ, k1(0.95) = 1.65

CV aR = E [ ξ | ξ ≥ ζα(ξ)] = µ+ k2(α)σ, k2(0.95) = 2.06

1st International R/Rmetrics User and Developer Workshop 14

Risk Measures: Some Examples

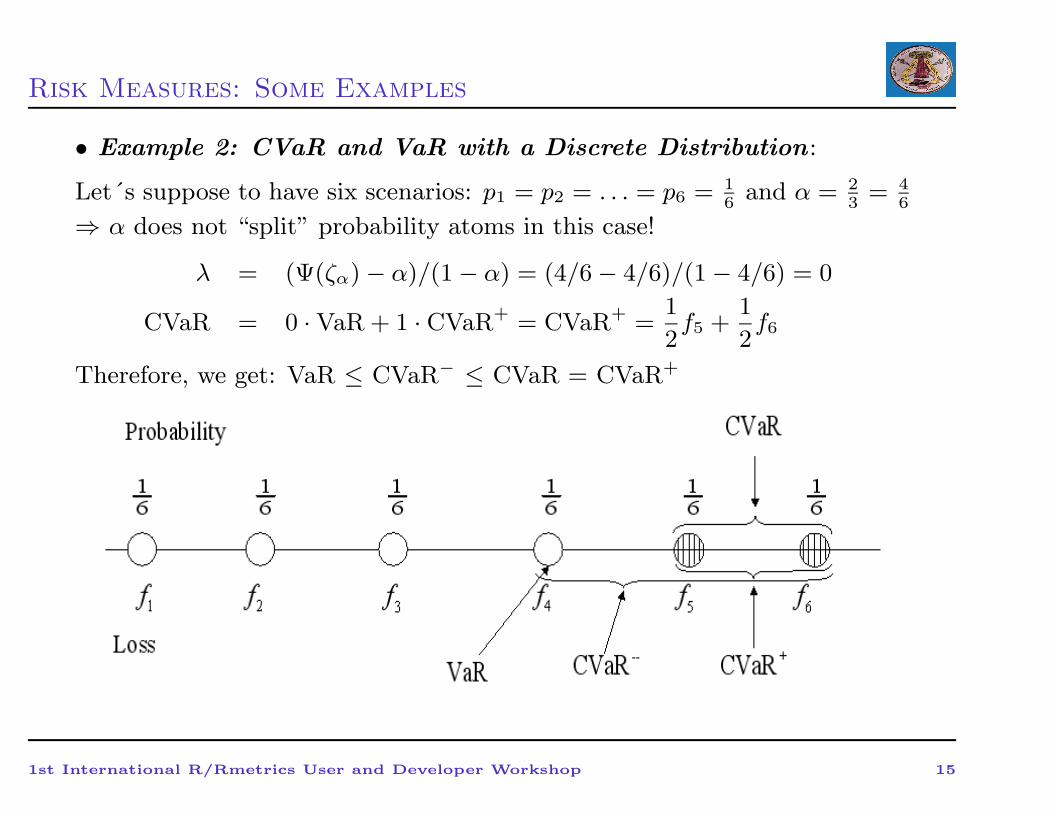

• Example 2: CVaR and VaR with a Discrete Distribution :

Let´s suppose to have six scenarios: p1 = p2 = . . . = p6 = 16

and α = 23

= 46

⇒ α does not “split” probability atoms in this case!

λ = (Ψ(ζα) − α)/(1 − α) = (4/6 − 4/6)/(1 − 4/6) = 0

CVaR = 0 · VaR + 1 · CVaR+ = CVaR+ =1

2f5 +

1

2f6

Therefore, we get: VaR ≤ CVaR− ≤ CVaR = CVaR+

1st International R/Rmetrics User and Developer Workshop 15

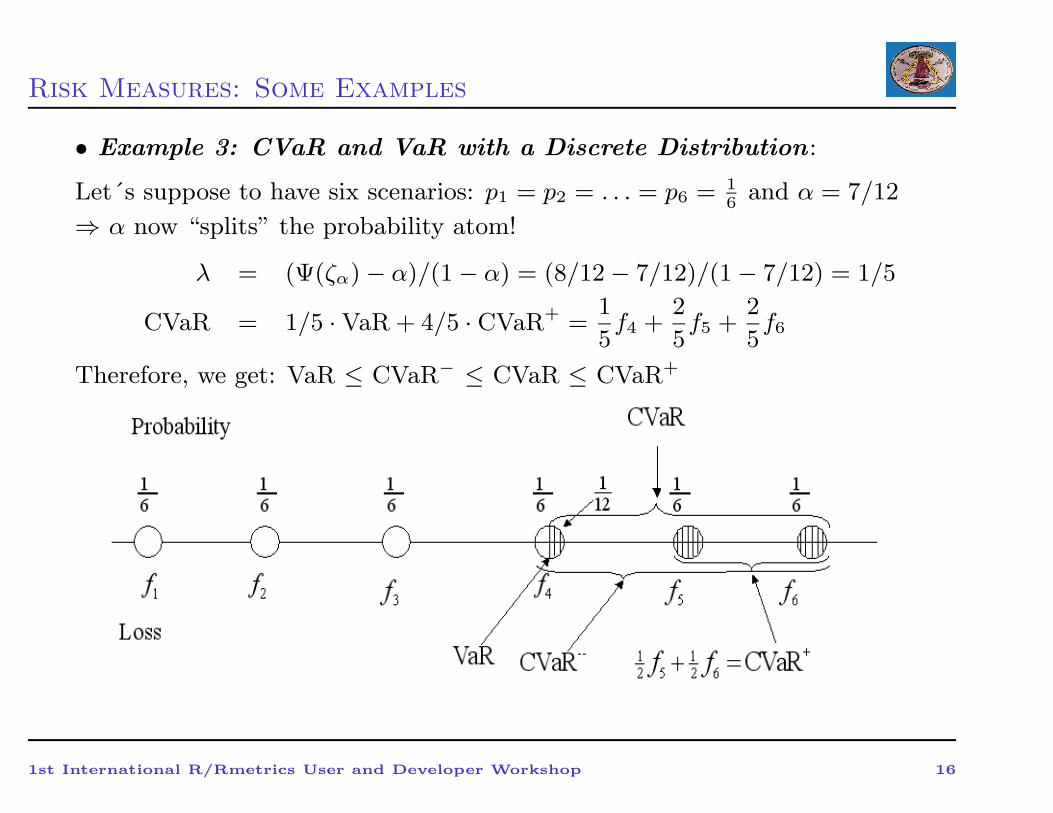

Risk Measures: Some Examples

• Example 3: CVaR and VaR with a Discrete Distribution :

Let´s suppose to have six scenarios: p1 = p2 = . . . = p6 = 16

and α = 7/12

⇒ α now “splits” the probability atom!

λ = (Ψ(ζα) − α)/(1 − α) = (8/12 − 7/12)/(1 − 7/12) = 1/5

CVaR = 1/5 · VaR + 4/5 · CVaR+ =1

5f4 +

2

5f5 +

2

5f6

Therefore, we get: VaR ≤ CVaR− ≤ CVaR ≤ CVaR+

1st International R/Rmetrics User and Developer Workshop 16

Advanced Multivariate Modelling: The Theory of Copulas

→ A copula is a multivariate distribution function H of random variables

X1 . . . Xn with standard uniform marginal distributions F1, . . . , Fn,

defined on the unit n-cube [0,1]n with the following properties:

1. The range of C (u1, u2, ..., un) is the unit interval [0,1];

2. C (u1, u2, ..., un) = 0 if any ui = 0, for i = 1, 2, ..., n.

3. C (1, ..., 1, ui, 1, ..., 1) = ui , for all ui ∈ [0, 1]

The previous three conditions provides the lower bound on the distribution

function and ensures that the marginal distributions are uniform.

The Sklar’s theorem justifies the role of copulas as dependence functions...

1st International R/Rmetrics User and Developer Workshop 17

Advanced Multivariate Modelling: The Theory of Copulas

(Sklar’s theorem): Let H denote a n-dimensional distribution function

with margins F1. . .Fn . Then there exists a n-copula C such that for all

real (x1,. . . , xn)

H(x1, . . . , xn) = C(F1(x1), . . . , Fn(xn)) (1)

If all the margins are continuous, then the copula is unique. Conversely, if

C is a copula and F1, . . . Fn are distribution functions, then the function H

defined in (1) is a joint distribution function with margins F1, . . . Fn.

→ A copula is a function that links univariate marginal distributions of

two or more variables to their multivariate distribution.

→ F1 and Fn need not to be identical or even to belong to the same

distribution family.

1st International R/Rmetrics User and Developer Workshop 18

Advanced Multivariate Modelling: The Theory of Copulas

Main consequences:

• For continuous multivariate distributions, the univariate margins and

the multivariate dependence can be separated;

• Copula is invariant under strictly increasing and continuous

transformations: no matter whether we work with price series or with

log-prices.

Example. Independent copula: C(u, v) = u · v

What is the probability that both returns in market A and B are in their

lowest 10th percentiles?

C(0.1; 0.1) = 0.1 · 0.1 = 0.01

1st International R/Rmetrics User and Developer Workshop 19

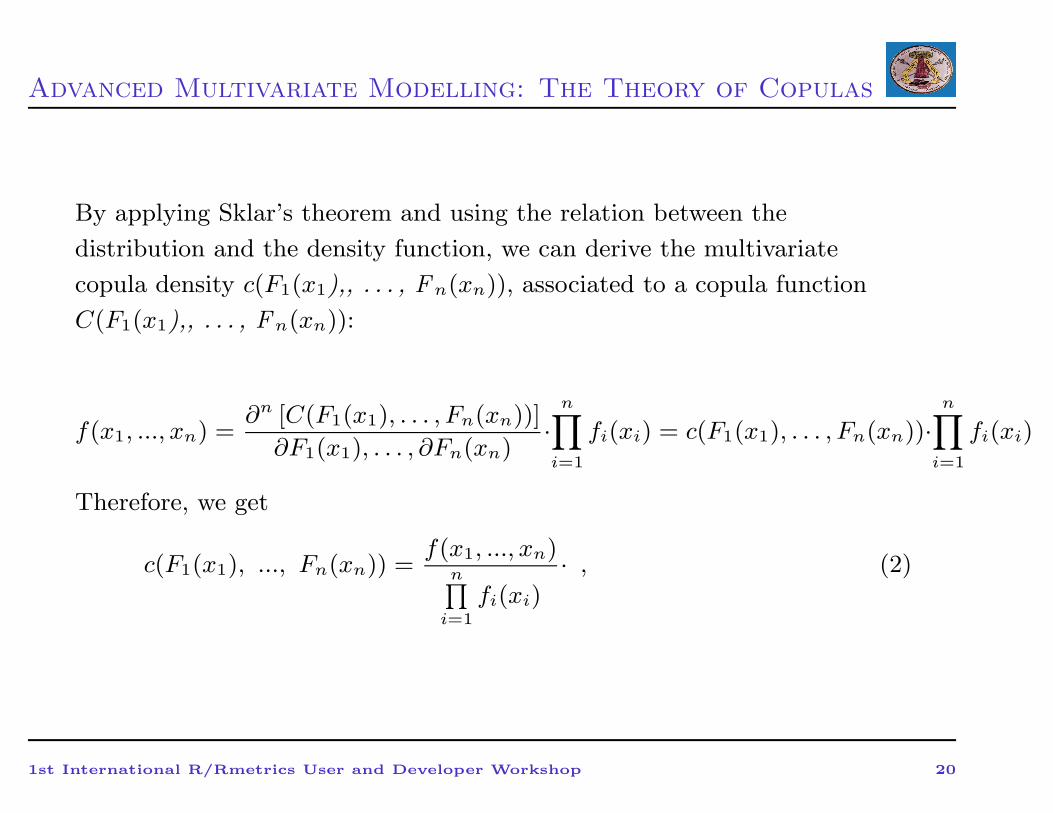

Advanced Multivariate Modelling: The Theory of Copulas

By applying Sklar’s theorem and using the relation between the

distribution and the density function, we can derive the multivariate

copula density c(F1(x1),, . . . , Fn(xn)), associated to a copula function

C(F1(x1),, . . . , Fn(xn)):

f(x1, ..., xn) =∂n [C(F1(x1), . . . , Fn(xn))]

∂F1(x1), . . . , ∂Fn(xn)·

n∏

i=1

fi(xi) = c(F1(x1), . . . , Fn(xn))·n∏

i=1

fi(xi)

Therefore, we get

c(F1(x1), ..., Fn(xn)) =f(x1, ..., xn)

n∏

i=1

fi(xi)· , (2)

1st International R/Rmetrics User and Developer Workshop 20

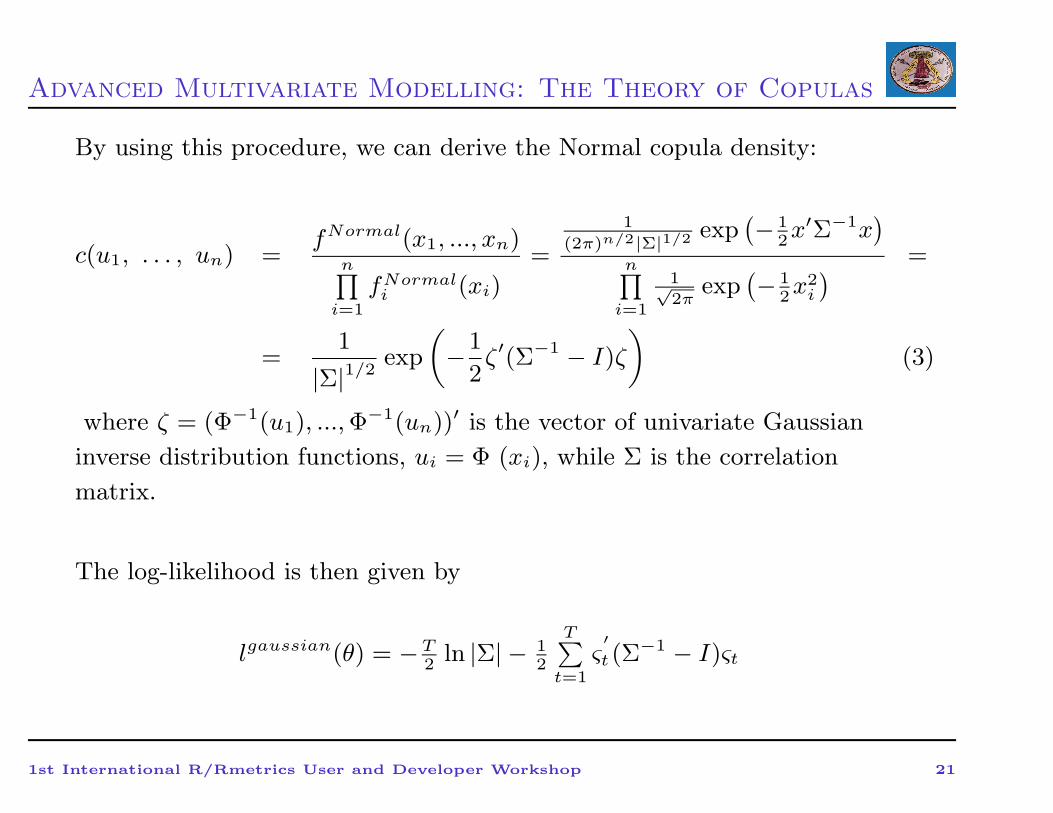

Advanced Multivariate Modelling: The Theory of Copulas

By using this procedure, we can derive the Normal copula density:

c(u1, . . . , un) =fNormal(x1, ..., xn)

n∏

i=1

fNormali (xi)

=

1

(2π)n/2|Σ|1/2 exp(

− 12x′Σ−1x

)

n∏

i=1

1√2π

exp(

− 12x2

i

)

=

=1

|Σ|1/2exp

(

−1

2ζ′(Σ−1 − I)ζ

)

(3)

where ζ = (Φ−1(u1), ...,Φ−1(un))′ is the vector of univariate Gaussian

inverse distribution functions, ui = Φ (xi), while Σ is the correlation

matrix.

The log-likelihood is then given by

lgaussian(θ) = −T2

ln |Σ| − 12

T∑

t=1

ς′

t(Σ−1 − I)ςt

1st International R/Rmetrics User and Developer Workshop 21

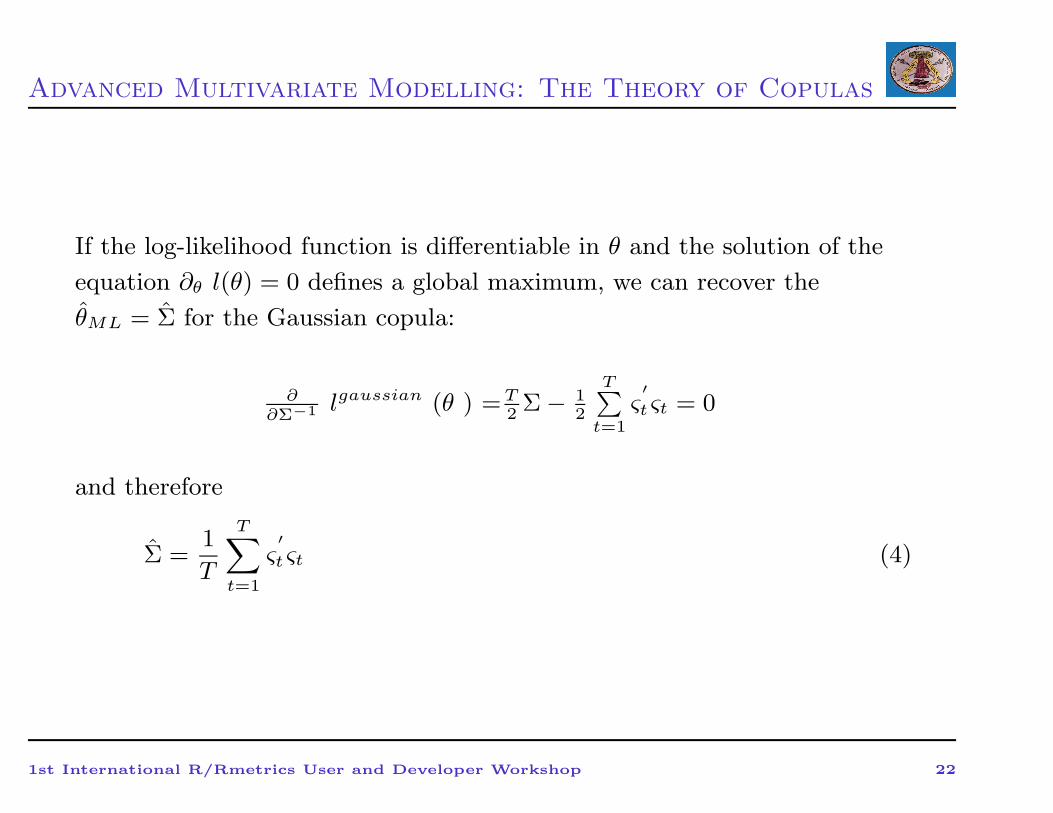

Advanced Multivariate Modelling: The Theory of Copulas

If the log-likelihood function is differentiable in θ and the solution of the

equation ∂θ l(θ) = 0 defines a global maximum, we can recover the

θML = Σ for the Gaussian copula:

∂∂Σ−1 lgaussian (θ ) =T

2Σ − 1

2

T∑

t=1

ς′

t ςt = 0

and therefore

Σ =1

T

T∑

t=1

ς′

t ςt (4)

1st International R/Rmetrics User and Developer Workshop 22

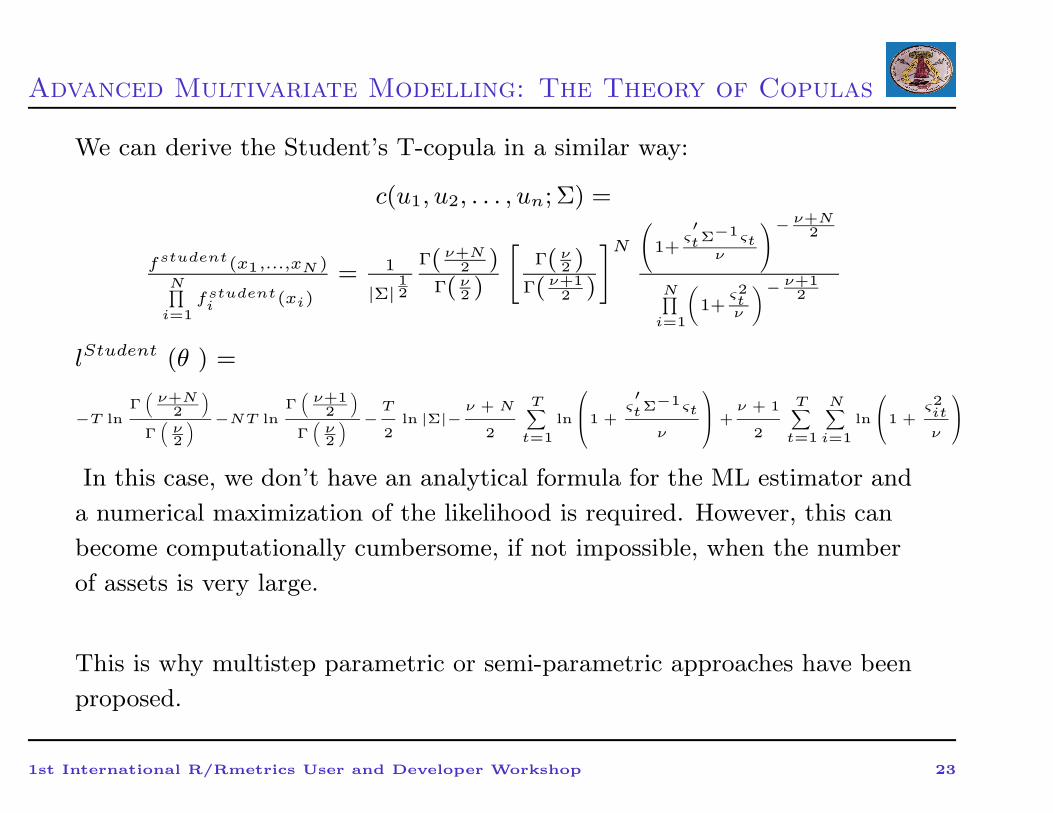

Advanced Multivariate Modelling: The Theory of Copulas

We can derive the Student’s T-copula in a similar way:

c(u1, u2, . . . , un; Σ) =

fstudent(x1,...,xN )N∏

i=1fstudent

i (xi)

= 1

|Σ|12

Γ( ν+N2 )

Γ( ν2 )

[

Γ( ν2 )

Γ( ν+12 )

]N

(

1+ς′tΣ−1ςt

ν

)− ν+N2

N∏

i=1

(

1+ς2tν

)− ν+12

lStudent (θ ) =

−T lnΓ(

ν+N2

)

Γ(

ν2

) −NT lnΓ(

ν+12

)

Γ(

ν2

) −T

2ln |Σ|−

ν + N

2

T∑

t=1

ln

1 +

ς′tΣ−1ςt

ν

+

ν + 1

2

T∑

t=1

N∑

i=1

ln

1 +ς2it

ν

In this case, we don’t have an analytical formula for the ML estimator and

a numerical maximization of the likelihood is required. However, this can

become computationally cumbersome, if not impossible, when the number

of assets is very large.

This is why multistep parametric or semi-parametric approaches have been

proposed.

1st International R/Rmetrics User and Developer Workshop 23

Empirical Applications: Market Risk Management:

Overview of the Presentation

• Aim: Build flexible multivariate distribution, without the

constraints of the traditional joint normal distribution.

• Aim 2 : Evaluate what are the main determinants when doing

VaR forecasts for a portfolio of assets.

• Contribution: Copulae capture those properties of the joint

distribution which are invariant under strictly increasing

transformation and do not depend on marginals and allow for

time dependency

• Benefit : More precise portfolio Value at Risk estimates

1st International R/Rmetrics User and Developer Workshop 24

Empirical Applications: Market Risk Management:

Copula: Definitions and Estimation method

Sklar’s theorem for conditional distributions: Let Ft be the

conditional distribution of x|Ft−1, Gt be the conditional distribution of

y|Ft−1, and Ht be the joint conditional bivariate distribution of

(x, y|Ft−1). Assume that Ft and Gt are continuous in x and y. Then there

exists a unique conditional copula Ct such that

Ht(x, y|Ft−1) = Ct(Ft(x|Ft−1), Gt(y|Ft−1)|Ft−1), (5)

7→ A copula is a function that links univariate marginal distributions of

two or more variables to their multivariate distribution.

7→ F1 and F2 need not to be identical or even to belong to the same

distribution family.

1st International R/Rmetrics User and Developer Workshop 25

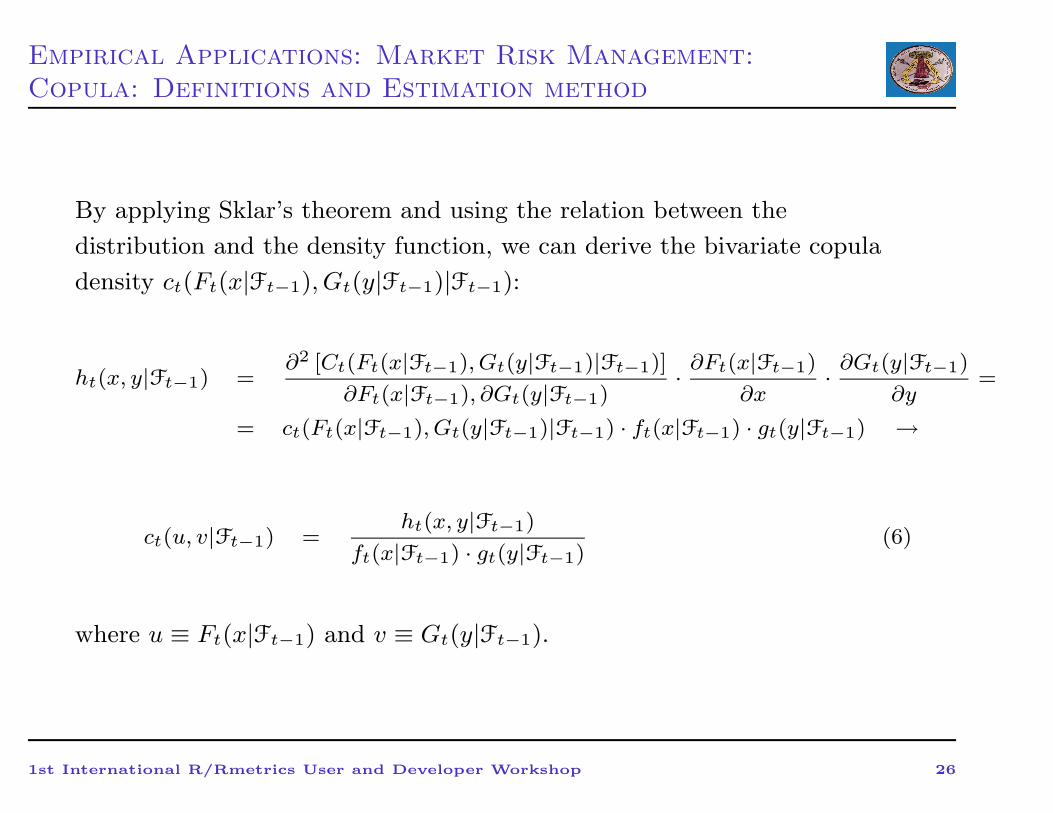

Empirical Applications: Market Risk Management:

Copula: Definitions and Estimation method

By applying Sklar’s theorem and using the relation between the

distribution and the density function, we can derive the bivariate copula

density ct(Ft(x|Ft−1), Gt(y|Ft−1)|Ft−1):

ht(x, y|Ft−1) =∂2 [Ct(Ft(x|Ft−1), Gt(y|Ft−1)|Ft−1)]

∂Ft(x|Ft−1), ∂Gt(y|Ft−1)· ∂Ft(x|Ft−1)

∂x· ∂Gt(y|Ft−1)

∂y=

= ct(Ft(x|Ft−1), Gt(y|Ft−1)|Ft−1) · ft(x|Ft−1) · gt(y|Ft−1) →

ct(u, v|Ft−1) =ht(x, y|Ft−1)

ft(x|Ft−1) · gt(y|Ft−1)(6)

where u ≡ Ft(x|Ft−1) and v ≡ Gt(y|Ft−1).

1st International R/Rmetrics User and Developer Workshop 26

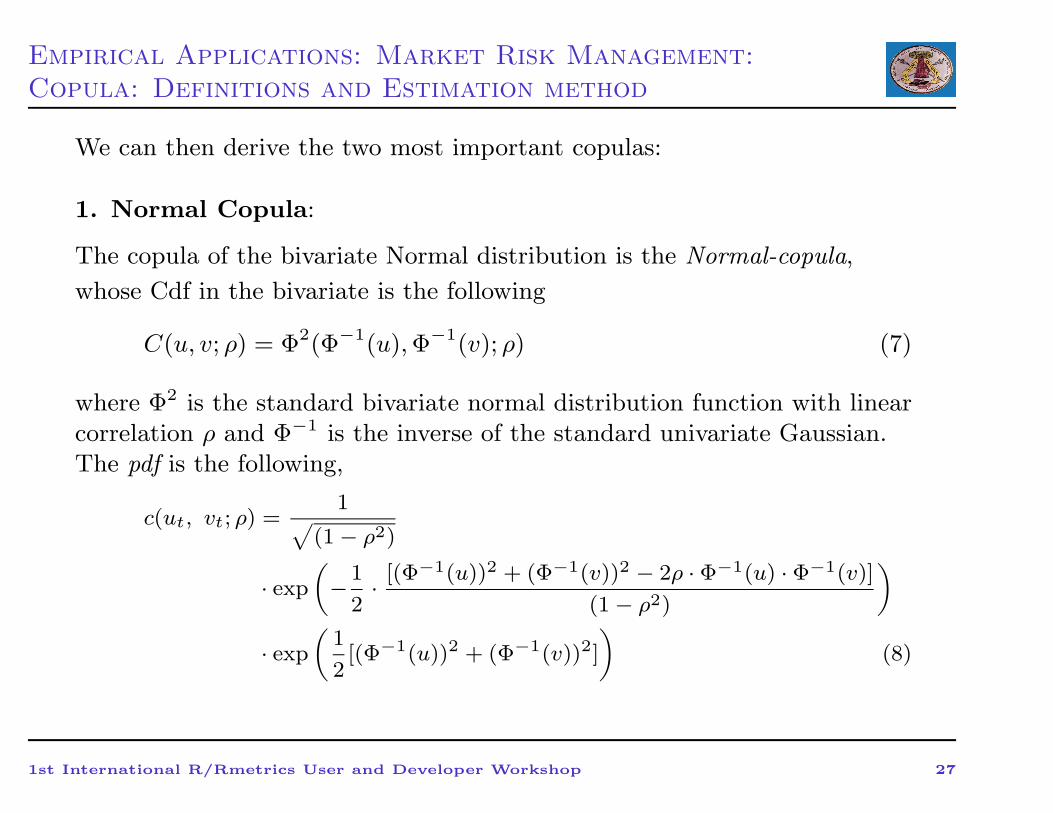

Empirical Applications: Market Risk Management:

Copula: Definitions and Estimation method

We can then derive the two most important copulas:

1. Normal Copula:

The copula of the bivariate Normal distribution is the Normal-copula,

whose Cdf in the bivariate is the following

C(u, v; ρ) = Φ2(Φ−1(u),Φ−1(v); ρ) (7)

where Φ2 is the standard bivariate normal distribution function with linearcorrelation ρ and Φ−1 is the inverse of the standard univariate Gaussian.The pdf is the following,

c(ut, vt; ρ) =1

√

(1 − ρ2)

· exp

(

−1

2· [(Φ−1(u))2 + (Φ−1(v))2 − 2ρ · Φ−1(u) · Φ−1(v)]

(1 − ρ2)

)

· exp

(

1

2[(Φ−1(u))2 + (Φ−1(v))2]

)

(8)

1st International R/Rmetrics User and Developer Workshop 27

Empirical Applications: Market Risk Management:

Copula: Definitions and Estimation method

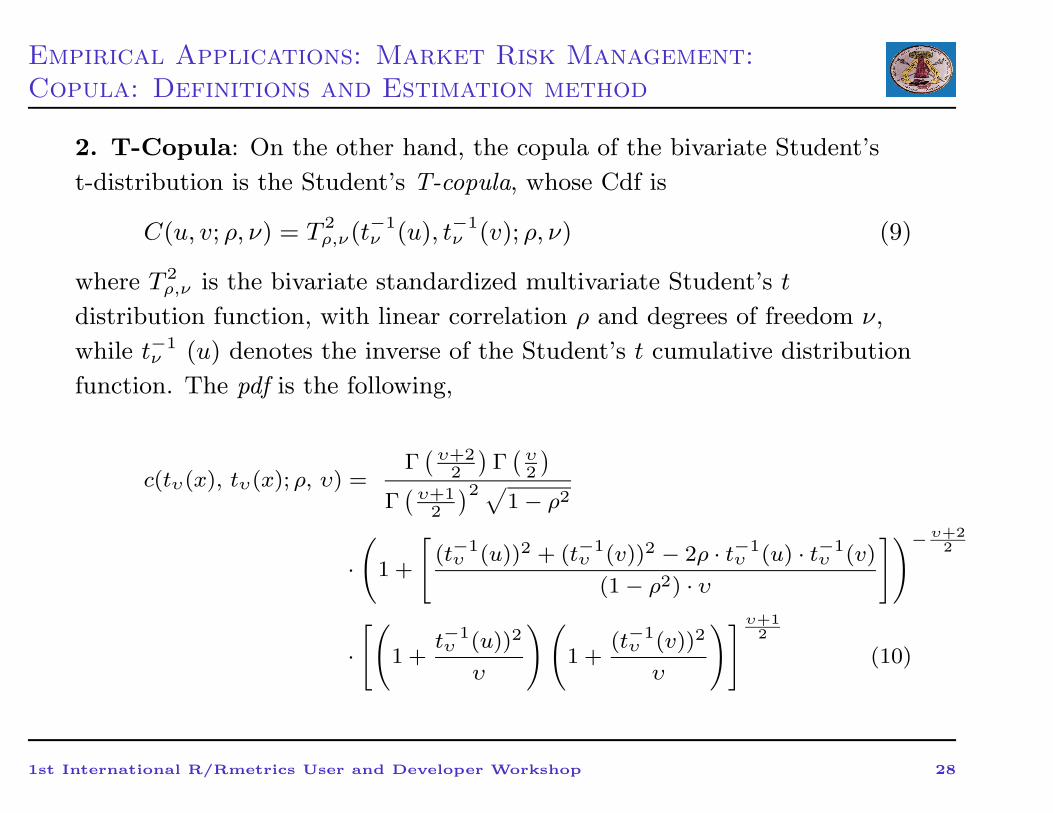

2. T-Copula: On the other hand, the copula of the bivariate Student’s

t-distribution is the Student’s T-copula, whose Cdf is

C(u, v; ρ, ν) = T 2ρ,ν(t−1

ν (u), t−1ν (v); ρ, ν) (9)

where T 2ρ,ν is the bivariate standardized multivariate Student’s t

distribution function, with linear correlation ρ and degrees of freedom ν,

while t−1ν (u) denotes the inverse of the Student’s t cumulative distribution

function. The pdf is the following,

c(tυ(x), tυ(x); ρ, υ) =Γ(

υ+22

)

Γ(

υ2

)

Γ(

υ+12

)2√1 − ρ2

·(

1 +

[

(t−1υ (u))2 + (t−1

υ (v))2 − 2ρ · t−1υ (u) · t−1

υ (v)

(1 − ρ2) · υ

])− υ+22

·[(

1 +t−1υ (u))2

υ

)(

1 +(t−1

υ (v))2

υ

)]υ+12

(10)

1st International R/Rmetrics User and Developer Workshop 28

Empirical Applications: Market Risk Management:

Copula: Definitions and Estimation method

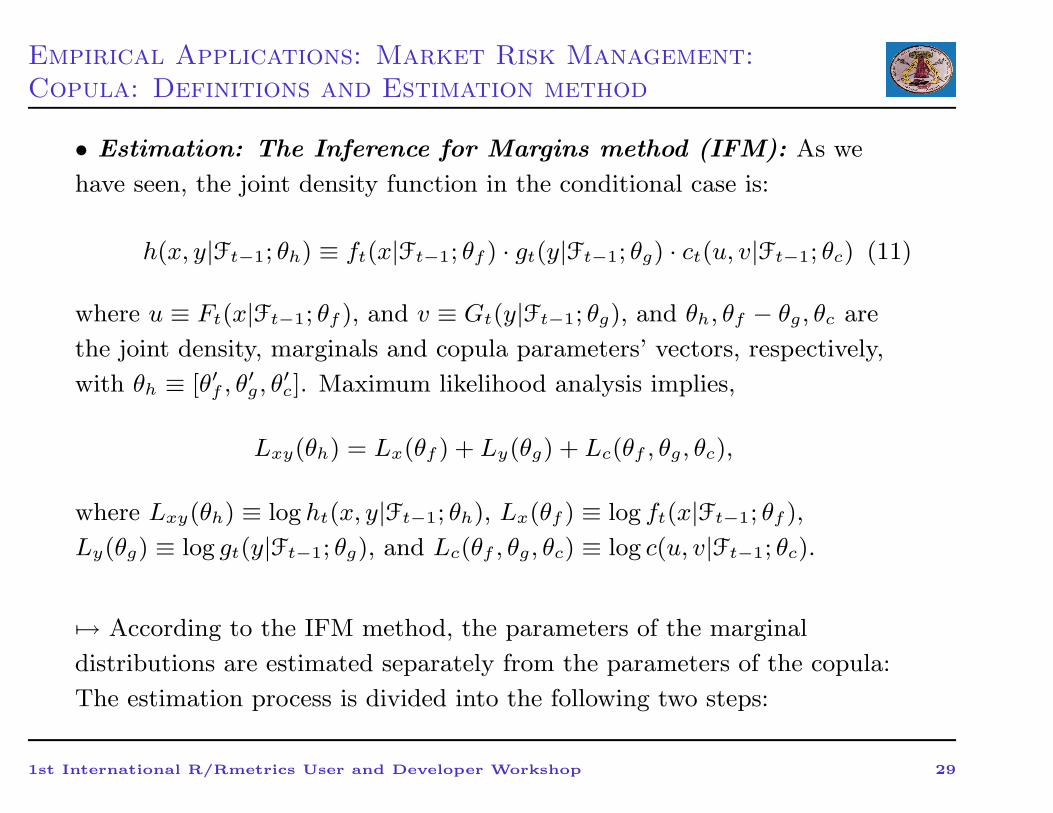

• Estimation: The Inference for Margins method (IFM): As we

have seen, the joint density function in the conditional case is:

h(x, y|Ft−1; θh) ≡ ft(x|Ft−1; θf ) · gt(y|Ft−1; θg) · ct(u, v|Ft−1; θc) (11)

where u ≡ Ft(x|Ft−1; θf ), and v ≡ Gt(y|Ft−1; θg), and θh, θf − θg, θc are

the joint density, marginals and copula parameters’ vectors, respectively,

with θh ≡ [θ′f , θ′g, θ

′c]. Maximum likelihood analysis implies,

Lxy(θh) = Lx(θf ) + Ly(θg) + Lc(θf , θg, θc),

where Lxy(θh) ≡ log ht(x, y|Ft−1; θh), Lx(θf ) ≡ log ft(x|Ft−1; θf ),

Ly(θg) ≡ log gt(y|Ft−1; θg), and Lc(θf , θg, θc) ≡ log c(u, v|Ft−1; θc).

7→ According to the IFM method, the parameters of the marginal

distributions are estimated separately from the parameters of the copula:

The estimation process is divided into the following two steps:

1st International R/Rmetrics User and Developer Workshop 29

Empirical Applications: Market Risk Management:

Copula: Definitions and Estimation method

1. Estimating the parameters θf and θg of the marginal distributions Ft

and Gt using the ML method:

θf , = arg maxL(θf ) = arg max

T∑

t=1

log ft(xt; θf )

θg , = arg maxL(θg) = arg max

T∑

t=1

log gt(yt; θg) (12)

2. Estimating the copula parameters θc , given step 1):

θc = arg maxL(θc) = arg max

T∑

t=1

log[ct(Ft(xt; θf ), Gt(yt; θg); θc)] (13)

The estimator asymptotic distribution is (Joe 1997, Patton 2003):√T (θh − θ0) → N(0, V −1(θ0)) (14)

where V (θ0) = D−1M (D−1)⊤ is the Godambe Information Matrix (or

“sandwich estimator”), where D = E[∂g(θ)⊤/∂ θ] , M = E [g(θ)⊤ g(θ)],

and g(θ) = (∂Lx/∂θf , ∂Ly/∂θg, ∂Lc/∂θθ) is the score function.

1st International R/Rmetrics User and Developer Workshop 30

Empirical Applications: Market Risk Management:

Copula: Definitions and Estimation method

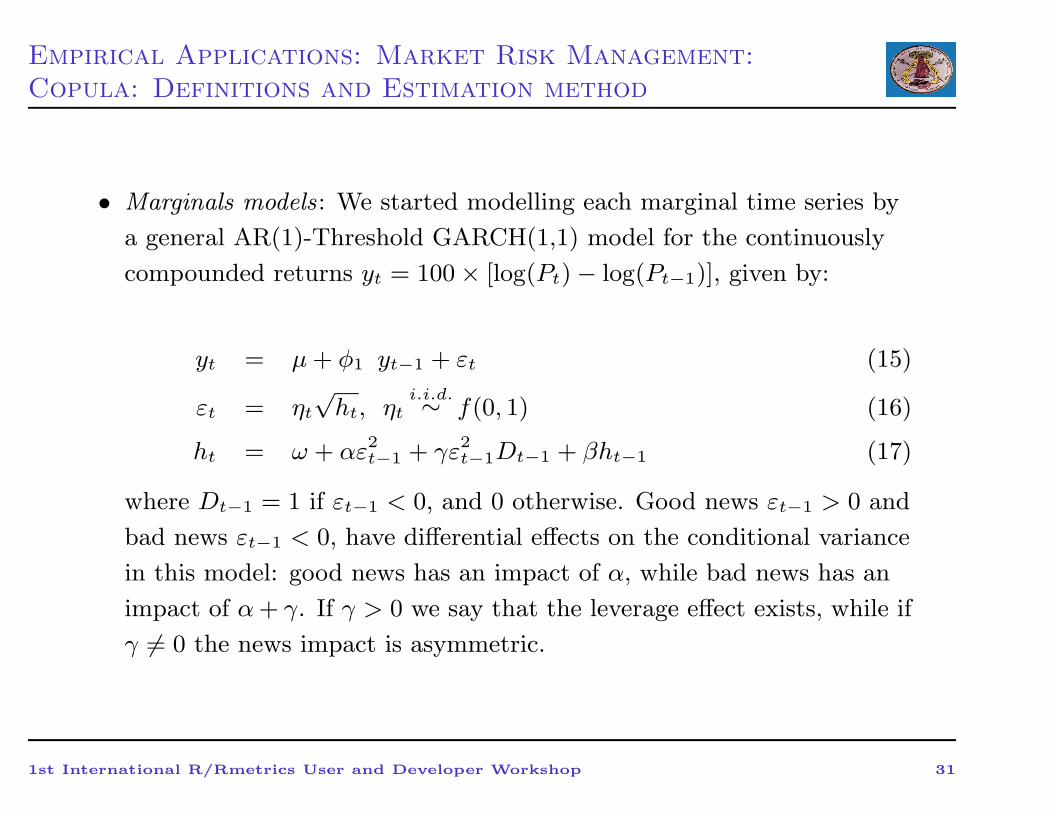

• Marginals models: We started modelling each marginal time series by

a general AR(1)-Threshold GARCH(1,1) model for the continuously

compounded returns yt = 100 × [log(Pt) − log(Pt−1)], given by:

yt = µ+ φ1 yt−1 + εt (15)

εt = ηt

√ht, ηt

i.i.d.∼ f(0, 1) (16)

ht = ω + αε2t−1 + γε2t−1Dt−1 + βht−1 (17)

where Dt−1 = 1 if εt−1 < 0, and 0 otherwise. Good news εt−1 > 0 and

bad news εt−1 < 0, have differential effects on the conditional variance

in this model: good news has an impact of α, while bad news has an

impact of α+ γ. If γ > 0 we say that the leverage effect exists, while if

γ 6= 0 the news impact is asymmetric.

1st International R/Rmetrics User and Developer Workshop 31

Empirical Applications: Market Risk Management:

Copula: Definitions and Estimation method

We estimate the AR(1)-TGARCH(1,1) model assuming four different

density functions f(0, 1) for ηt: the Normal, the Skew-Normal, the

Student’s-T and the Skew-T.

When working with the latter three distributions, we have to specify a

dynamic model for the conditional skewness parameter and/or the

conditional degrees of freedom, as well.

λt = Λ (ζ + δ · εt−1) (18)

νt = Γ (θ + τ · εt−1) (19)

where Λ(·) is a modified logistic transformation designed to keep the

conditional skewness parameter λt in (-1, 1) at all times, while Γ(·) is

a logistic transformation designed to keep the conditional degrees of

freedom in (2, 30) at all times

1st International R/Rmetrics User and Developer Workshop 32

Empirical Applications: Market Risk Management:

Copula: Definitions and Estimation method

• Copula models:

We fitted the Normal and T-copula to our financial asset pairs, by

using the cumulative distribution function of the standardized

residuals ηt estimated from the marginal models:(

Xt − µxt

√

hxt

,Yt − µy

t√

hyt

)

∼ CNormal−copula (Ft(ηxt ), Gt(η

yt ); ρt|Ft−1)

(

Xt − µxt

√

hxt

,Yt − µy

t√

hyt

)

∼ CT−copula (Ft(ηxt ), Gt(η

yt ); ρt, νt|Ft−1)

(20)

where [ρt, νt] are the conditional correlation and conditional degrees

of freedom, respectively, [µt, ht] the conditional means and variances,

while {Ft, Gt} can be Normal / Skew-Normal / Student’s T / Skew T.

1st International R/Rmetrics User and Developer Workshop 33

Empirical Applications: Market Risk Management:

Value at Risk Applications

Let xt and yt denote the assets log-returns at time t and be β ∈ (0, 1) the

allocation weight, so that the portfolio return is given by

zt = βxt + (1− β)yt. By using Sklar’s theorem, the cumulative distribution

functions for the portfolio return Z is given by:

ζ(z) = Pr(Z ≤ zt) = Pr(βX + (1 − β)Y ≤ zt) =

=

+∞∫

−∞

1β

zt−1−β

βyt

∫

−∞

ct(Ft(x|Ft−1), Gt(y|Ft−1)|Ft−1) · ft(x|Ft−1)dx

· gt(y|Ft−1)dy

(21)

The one-step-ahead VaR computed in t− 1 for the portfolio at a

confidence level p is the solution z∗ of the equation ζ(z∗) = p, times the

value of the financial position at t− 1.

1st International R/Rmetrics User and Developer Workshop 34

Empirical Applications: Market Risk Management:

Value at Risk Applications

⇒ The computation of the one-step-ahead VaR requires the solution of the

previous double integral: However, while this solution is feasible in the

bivariate case, it becomes computationally problematic when the number

of assets is much higher than two.

⇒ This is why we prefer to compute the VaR using a simple Monte Carlo

simulation as widely used in quantitative finance and option pricing. See

Jorion (2000) for a discussion of Monte Carlo techniques in VaR

applications.

⇒ Following this solution, we generate a large number of one-day-ahead

returns {xt, yt} for the two assets, by simulating 100,000 random returns

with the conditional distribution function (21) and we revaluate the

portfolio at time t. We then determine the Value at Risk at a given

confidence level p, by simply taking the empirical quantile at p of the

simulated portfolio profit and loss distribution.

1st International R/Rmetrics User and Developer Workshop 35

Empirical Applications: Market Risk Management:

Value at Risk Applications

The detailed steps of the procedure for estimating the 95%, 99% VaR over

a one-day holding period are the following:

1. Let consider the portfolio z which contains one position for each of the

2 risk factors (or assets), whose value at time t− 1 is:

Pz,t−1 = Px,t−1 + Py,t−1

where Px,t−1, Py,t−1 are the market prices of the two assets at time

t− 1.

2. We simulate j = 100,000 MC scenarios for each asset log-returns,

{xj,t , yj,t}, over the time horizon [t− 1, t], using the conditional joint

distributional function (3.1).

(a) First, we have to simulate a j random variate (uj,x, uj,y)′ from the

copula Ct(·). See Cherubini et al. (2004), for a discussion about

copula simulation.

1st International R/Rmetrics User and Developer Workshop 36

Empirical Applications: Market Risk Management:

Value at Risk Applications

(b) Second, we get the standardized asset log-returns by using the

inverse functions of the estimated marginals, which can be Normal

/ Skew-Normal / T-Student / Skew-T, as described in section 2.2

and Appendix A:

Qj = (qj,x, qj,y)′ = (Ft−1

(uj,x); Gt−1

(uj,y))

(c) Third, we rescale the standardized assets log-returns by using the

forecasted means and variances, estimated with AR-GARCH

models as described in section 2.3.2:

{xj,t, yj,t} =

(

µx,t + qj,x ·√

hx,t, µy,t + qj,y ·√

hy,t

)

(d) Finally, we repeat this procedure for j = 100, 000 times.

3. By using these 100,000 scenarios, the portfolio is being revaluated at

time t, that is:

P jz,t = Px,t−1 · exp(xj,t) + Py,t−1 · exp(yj,t), j = 1...100, 000

1st International R/Rmetrics User and Developer Workshop 37

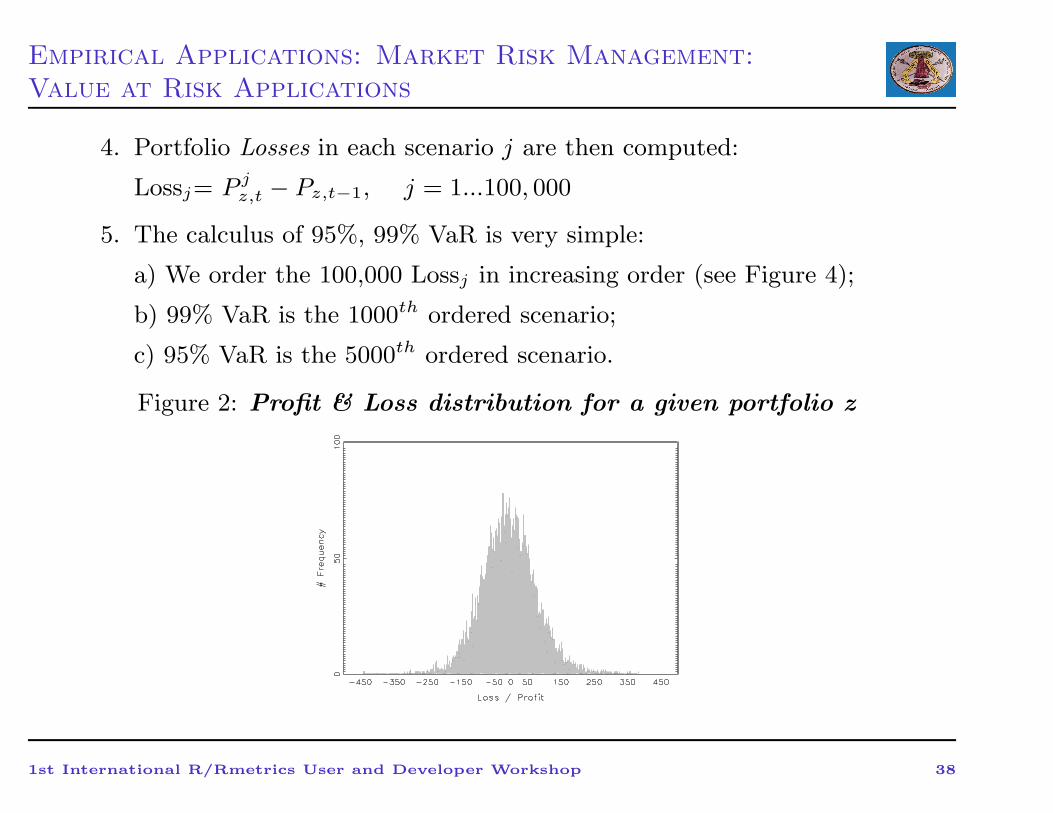

Empirical Applications: Market Risk Management:

Value at Risk Applications

4. Portfolio Losses in each scenario j are then computed:

Lossj= P jz,t − Pz,t−1, j = 1...100, 000

5. The calculus of 95%, 99% VaR is very simple:

a) We order the 100,000 Lossj in increasing order (see Figure 4);

b) 99% VaR is the 1000th ordered scenario;

c) 95% VaR is the 5000th ordered scenario.

Figure 2: Profit & Loss distribution for a given portfolio z

1st International R/Rmetrics User and Developer Workshop 38

Empirical Applications: Market Risk Management:

Value at Risk Applications

Traditional risk measurement models assume that the risk factors are

multivariate normal: empirical evidence shows the importance of skewness,

kurtosis, dynamic dependence (Tsay, 2002).

→ Starting from these stylized facts and theoretical background, I

introduced a model to generate scenarios for portfolio risk factors from

different conditional multivariate distributions.

Four elements were considered:

1. The choice of the marginals distribution;

2. The specification of the conditional moments of the marginals;

3. The choice of the copula to link the marginals into a proper

multivariate distribution;

4. The specification of the conditional copula parameters

1st International R/Rmetrics User and Developer Workshop 39

Empirical Applications: Market Risk Management:

Value at Risk Applications

To evaluate how important these four elements are, I generate out-of-

sample VaR forecasts for three portfolios (SP500-DAX, SP500-NIKKEI225,

NIKKEI225-DAX), by simulating 100.000 MC scenarios out of the

conditional joint density (11) with these different possible choices:

1. marginals distribution: Normal, Skew-Normal, Student´s T, Skew-T;

2. conditional moments Specification:

• Constant Mean / AR(1) process;

• Constant Variance / GARCH(1,1) process / T-GARCH(1,1)

• Constant / Dynamic Degrees of Freedom;

• Constant / Dynamic Skewness parameters;

3. Normal copula / T - copula;

4. Constant / Dynamic copula parameters

1st International R/Rmetrics User and Developer Workshop 40

Empirical Applications: Market Risk Management:

Empirical analysis

→ I generate portfolio Value at Risk forecasts at the 95 % - 99 %

confidence levels. The predicted one-step-ahead VaR forecasts are then

compared with the observed portfolio losses.

→ The initialization sample is given by the first 700 observations.

→ Recursive estimation from the 700th to the 1699th observation (for a

total of 1000 observations).

→ The performance of the competing models over these 1000 observations

is assessed using the following back-testing techniques:

• Kupiec’s unconditional coverage test;

• Christoffersen’s conditional coverage test;

• Loss functions to evaluate VaR forecasts accuracy.

1st International R/Rmetrics User and Developer Workshop 41

Empirical Applications: Market Risk Management:

Empirical analysis

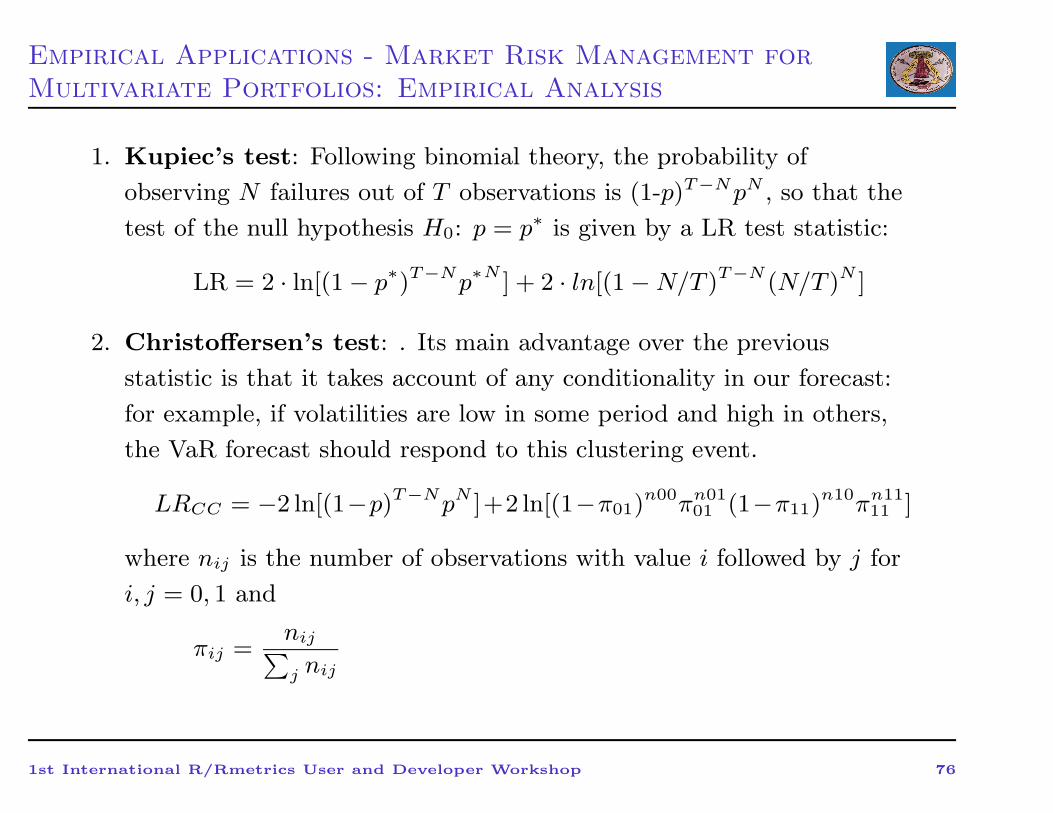

• Diagnostics for real VaR exceedances

1. Kupiec’s test: Following binomial theory, the probability of

observing N failures out of T observations is (1-p)T−NpN , so that the

test of the null hypothesis H0: p = p∗ is given by a LR test statistic:

LR = 2 · ln[(1 − p∗)T−Np∗N

] + 2 · ln[(1 −N/T )T−N (N/T )N ]

2. Christoffersen’s test: . Its main advantage over the previous

statistic is that it takes account of any conditionality in our forecast:

for example, if volatilities are low in some period and high in others,

the VaR forecast should respond to this clustering event.

LRCC = −2 ln[(1−p)T−NpN ]+2 ln[(1−π01)n00πn01

01 (1−π11)n10πn11

11 ]

where nij is the number of observations with value i followed by j for

i, j = 0, 1 and

πij =nij

∑

j nij

1st International R/Rmetrics User and Developer Workshop 42

Empirical Applications: Market Risk Management:

Empirical analysis

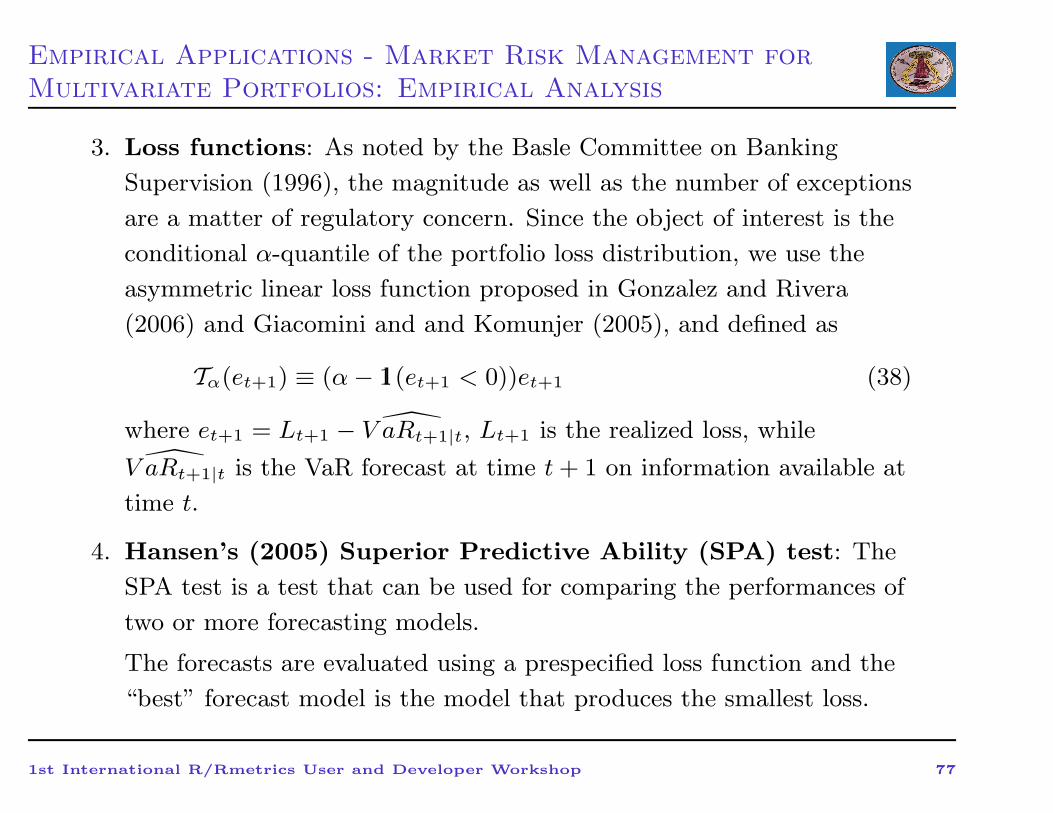

3. Loss functions: As noted by the Basle Committee on Banking

Supervision (1996), the magnitude as well as the number of exceptions

are a matter of regulatory concern. We used two different kind of loss

functions recently proposed:

(a) Lopez (1998):

Ct+1 =

1 + (Lt+1 − V ARt+1)2 if Lt+1 > V ARt+1

0 if Lt+1 ≤ V ARt+1

(b) Blanco and Ihle (1999):

Ct+1 =

Lt+1−V ARt+1

V ARt+1if Lt+1 < V ARt+1

0 if Lt+1 ≥ V ARt+1

1st International R/Rmetrics User and Developer Workshop 43

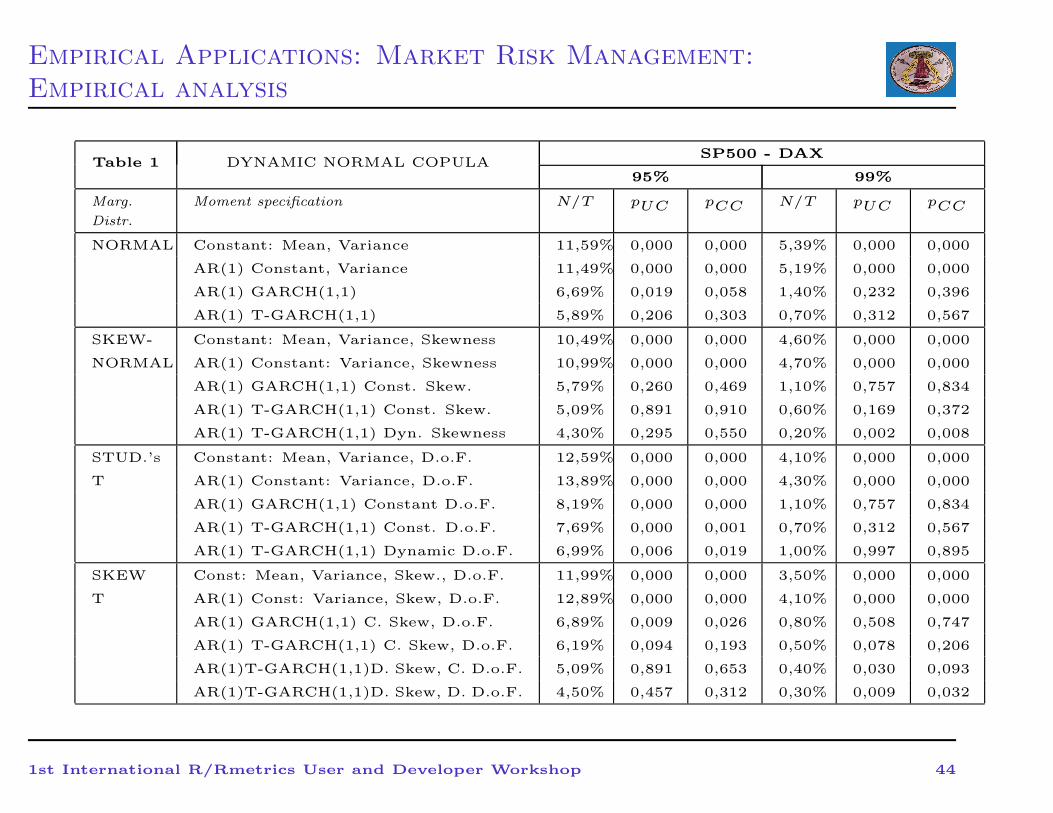

Empirical Applications: Market Risk Management:

Empirical analysis

Table 1 DYNAMIC NORMAL COPULASP500 - DAX

95% 99%

Marg.

Distr.

Moment specification N/T pUC pCC N/T pUC pCC

NORMAL Constant: Mean, Variance 11,59% 0,000 0,000 5,39% 0,000 0,000

AR(1) Constant, Variance 11,49% 0,000 0,000 5,19% 0,000 0,000

AR(1) GARCH(1,1) 6,69% 0,019 0,058 1,40% 0,232 0,396

AR(1) T-GARCH(1,1) 5,89% 0,206 0,303 0,70% 0,312 0,567

SKEW- Constant: Mean, Variance, Skewness 10,49% 0,000 0,000 4,60% 0,000 0,000

NORMAL AR(1) Constant: Variance, Skewness 10,99% 0,000 0,000 4,70% 0,000 0,000

AR(1) GARCH(1,1) Const. Skew. 5,79% 0,260 0,469 1,10% 0,757 0,834

AR(1) T-GARCH(1,1) Const. Skew. 5,09% 0,891 0,910 0,60% 0,169 0,372

AR(1) T-GARCH(1,1) Dyn. Skewness 4,30% 0,295 0,550 0,20% 0,002 0,008

STUD.’s Constant: Mean, Variance, D.o.F. 12,59% 0,000 0,000 4,10% 0,000 0,000

T AR(1) Constant: Variance, D.o.F. 13,89% 0,000 0,000 4,30% 0,000 0,000

AR(1) GARCH(1,1) Constant D.o.F. 8,19% 0,000 0,000 1,10% 0,757 0,834

AR(1) T-GARCH(1,1) Const. D.o.F. 7,69% 0,000 0,001 0,70% 0,312 0,567

AR(1) T-GARCH(1,1) Dynamic D.o.F. 6,99% 0,006 0,019 1,00% 0,997 0,895

SKEW Const: Mean, Variance, Skew., D.o.F. 11,99% 0,000 0,000 3,50% 0,000 0,000

T AR(1) Const: Variance, Skew, D.o.F. 12,89% 0,000 0,000 4,10% 0,000 0,000

AR(1) GARCH(1,1) C. Skew, D.o.F. 6,89% 0,009 0,026 0,80% 0,508 0,747

AR(1) T-GARCH(1,1) C. Skew, D.o.F. 6,19% 0,094 0,193 0,50% 0,078 0,206

AR(1)T-GARCH(1,1)D. Skew, C. D.o.F. 5,09% 0,891 0,653 0,40% 0,030 0,093

AR(1)T-GARCH(1,1)D. Skew, D. D.o.F. 4,50% 0,457 0,312 0,30% 0,009 0,032

1st International R/Rmetrics User and Developer Workshop 44

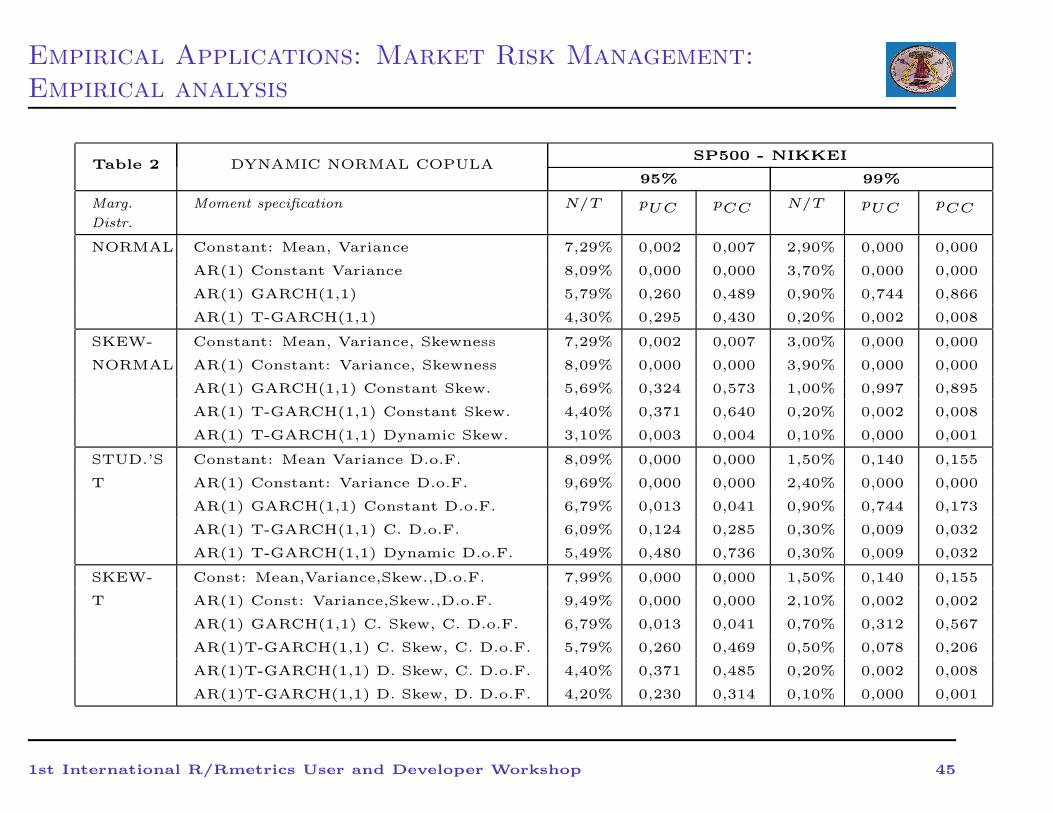

Empirical Applications: Market Risk Management:

Empirical analysis

Table 2 DYNAMIC NORMAL COPULASP500 - NIKKEI

95% 99%

Marg.

Distr.

Moment specification N/T pUC pCC N/T pUC pCC

NORMAL Constant: Mean, Variance 7,29% 0,002 0,007 2,90% 0,000 0,000

AR(1) Constant Variance 8,09% 0,000 0,000 3,70% 0,000 0,000

AR(1) GARCH(1,1) 5,79% 0,260 0,489 0,90% 0,744 0,866

AR(1) T-GARCH(1,1) 4,30% 0,295 0,430 0,20% 0,002 0,008

SKEW- Constant: Mean, Variance, Skewness 7,29% 0,002 0,007 3,00% 0,000 0,000

NORMAL AR(1) Constant: Variance, Skewness 8,09% 0,000 0,000 3,90% 0,000 0,000

AR(1) GARCH(1,1) Constant Skew. 5,69% 0,324 0,573 1,00% 0,997 0,895

AR(1) T-GARCH(1,1) Constant Skew. 4,40% 0,371 0,640 0,20% 0,002 0,008

AR(1) T-GARCH(1,1) Dynamic Skew. 3,10% 0,003 0,004 0,10% 0,000 0,001

STUD.’S Constant: Mean Variance D.o.F. 8,09% 0,000 0,000 1,50% 0,140 0,155

T AR(1) Constant: Variance D.o.F. 9,69% 0,000 0,000 2,40% 0,000 0,000

AR(1) GARCH(1,1) Constant D.o.F. 6,79% 0,013 0,041 0,90% 0,744 0,173

AR(1) T-GARCH(1,1) C. D.o.F. 6,09% 0,124 0,285 0,30% 0,009 0,032

AR(1) T-GARCH(1,1) Dynamic D.o.F. 5,49% 0,480 0,736 0,30% 0,009 0,032

SKEW- Const: Mean,Variance,Skew.,D.o.F. 7,99% 0,000 0,000 1,50% 0,140 0,155

T AR(1) Const: Variance,Skew.,D.o.F. 9,49% 0,000 0,000 2,10% 0,002 0,002

AR(1) GARCH(1,1) C. Skew, C. D.o.F. 6,79% 0,013 0,041 0,70% 0,312 0,567

AR(1)T-GARCH(1,1) C. Skew, C. D.o.F. 5,79% 0,260 0,469 0,50% 0,078 0,206

AR(1)T-GARCH(1,1) D. Skew, C. D.o.F. 4,40% 0,371 0,485 0,20% 0,002 0,008

AR(1)T-GARCH(1,1) D. Skew, D. D.o.F. 4,20% 0,230 0,314 0,10% 0,000 0,001

1st International R/Rmetrics User and Developer Workshop 45

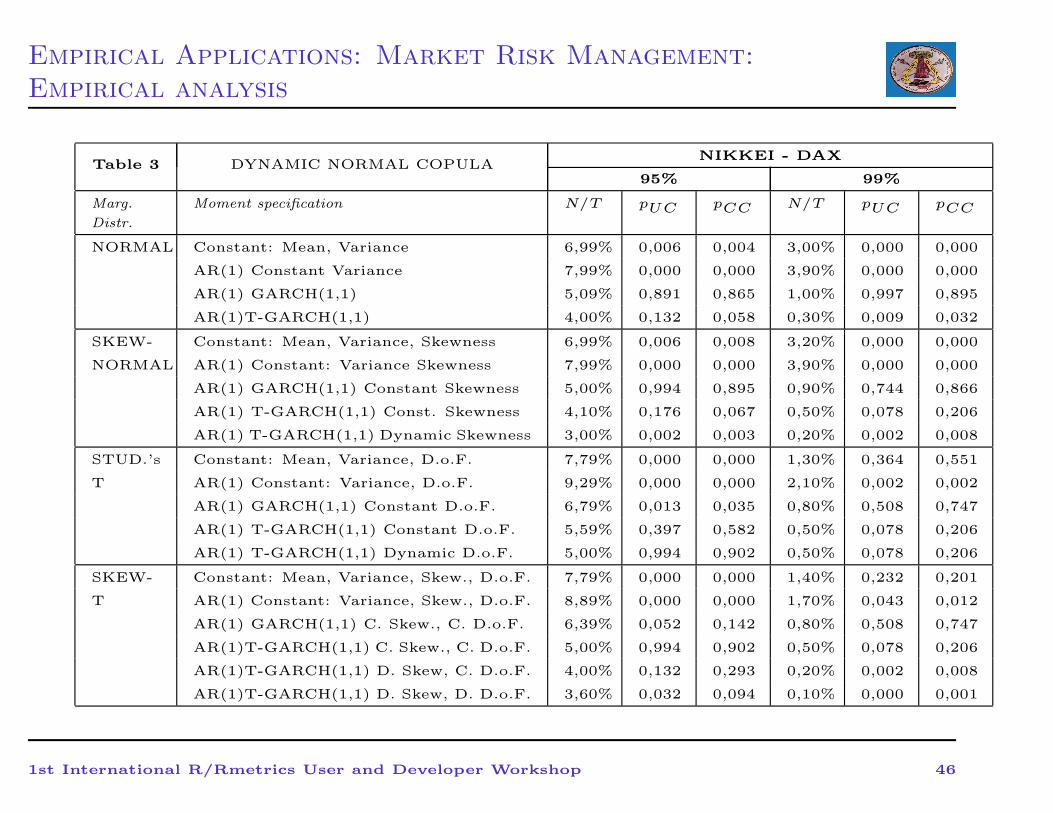

Empirical Applications: Market Risk Management:

Empirical analysis

Table 3 DYNAMIC NORMAL COPULANIKKEI - DAX

95% 99%

Marg.

Distr.

Moment specification N/T pUC pCC N/T pUC pCC

NORMAL Constant: Mean, Variance 6,99% 0,006 0,004 3,00% 0,000 0,000

AR(1) Constant Variance 7,99% 0,000 0,000 3,90% 0,000 0,000

AR(1) GARCH(1,1) 5,09% 0,891 0,865 1,00% 0,997 0,895

AR(1)T-GARCH(1,1) 4,00% 0,132 0,058 0,30% 0,009 0,032

SKEW- Constant: Mean, Variance, Skewness 6,99% 0,006 0,008 3,20% 0,000 0,000

NORMAL AR(1) Constant: Variance Skewness 7,99% 0,000 0,000 3,90% 0,000 0,000

AR(1) GARCH(1,1) Constant Skewness 5,00% 0,994 0,895 0,90% 0,744 0,866

AR(1) T-GARCH(1,1) Const. Skewness 4,10% 0,176 0,067 0,50% 0,078 0,206

AR(1) T-GARCH(1,1) Dynamic Skewness 3,00% 0,002 0,003 0,20% 0,002 0,008

STUD.’s Constant: Mean, Variance, D.o.F. 7,79% 0,000 0,000 1,30% 0,364 0,551

T AR(1) Constant: Variance, D.o.F. 9,29% 0,000 0,000 2,10% 0,002 0,002

AR(1) GARCH(1,1) Constant D.o.F. 6,79% 0,013 0,035 0,80% 0,508 0,747

AR(1) T-GARCH(1,1) Constant D.o.F. 5,59% 0,397 0,582 0,50% 0,078 0,206

AR(1) T-GARCH(1,1) Dynamic D.o.F. 5,00% 0,994 0,902 0,50% 0,078 0,206

SKEW- Constant: Mean, Variance, Skew., D.o.F. 7,79% 0,000 0,000 1,40% 0,232 0,201

T AR(1) Constant: Variance, Skew., D.o.F. 8,89% 0,000 0,000 1,70% 0,043 0,012

AR(1) GARCH(1,1) C. Skew., C. D.o.F. 6,39% 0,052 0,142 0,80% 0,508 0,747

AR(1)T-GARCH(1,1) C. Skew., C. D.o.F. 5,00% 0,994 0,902 0,50% 0,078 0,206

AR(1)T-GARCH(1,1) D. Skew, C. D.o.F. 4,00% 0,132 0,293 0,20% 0,002 0,008

AR(1)T-GARCH(1,1) D. Skew, D. D.o.F. 3,60% 0,032 0,094 0,10% 0,000 0,001

1st International R/Rmetrics User and Developer Workshop 46

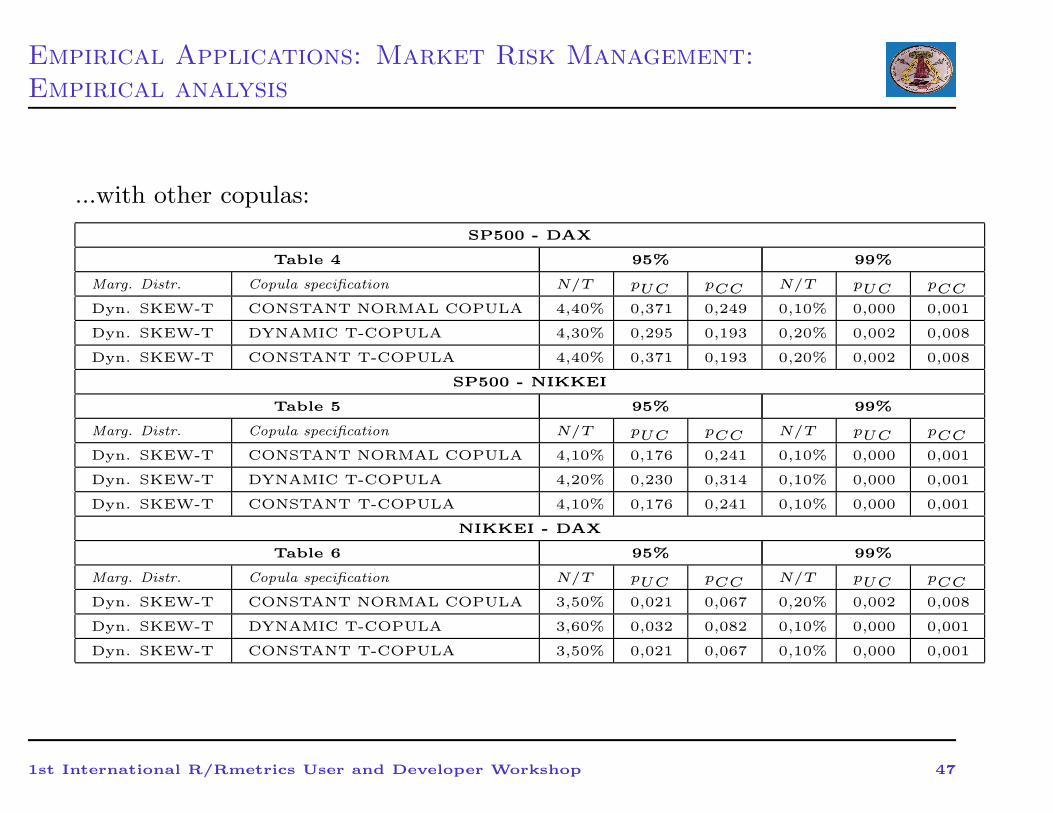

Empirical Applications: Market Risk Management:

Empirical analysis

...with other copulas:

SP500 - DAX

Table 4 95% 99%

Marg. Distr. Copula specification N/T pUC pCC N/T pUC pCC

Dyn. SKEW-T CONSTANT NORMAL COPULA 4,40% 0,371 0,249 0,10% 0,000 0,001

Dyn. SKEW-T DYNAMIC T-COPULA 4,30% 0,295 0,193 0,20% 0,002 0,008

Dyn. SKEW-T CONSTANT T-COPULA 4,40% 0,371 0,193 0,20% 0,002 0,008

SP500 - NIKKEI

Table 5 95% 99%

Marg. Distr. Copula specification N/T pUC pCC N/T pUC pCC

Dyn. SKEW-T CONSTANT NORMAL COPULA 4,10% 0,176 0,241 0,10% 0,000 0,001

Dyn. SKEW-T DYNAMIC T-COPULA 4,20% 0,230 0,314 0,10% 0,000 0,001

Dyn. SKEW-T CONSTANT T-COPULA 4,10% 0,176 0,241 0,10% 0,000 0,001

NIKKEI - DAX

Table 6 95% 99%

Marg. Distr. Copula specification N/T pUC pCC N/T pUC pCC

Dyn. SKEW-T CONSTANT NORMAL COPULA 3,50% 0,021 0,067 0,20% 0,002 0,008

Dyn. SKEW-T DYNAMIC T-COPULA 3,60% 0,032 0,082 0,10% 0,000 0,001

Dyn. SKEW-T CONSTANT T-COPULA 3,50% 0,021 0,067 0,10% 0,000 0,001

1st International R/Rmetrics User and Developer Workshop 47

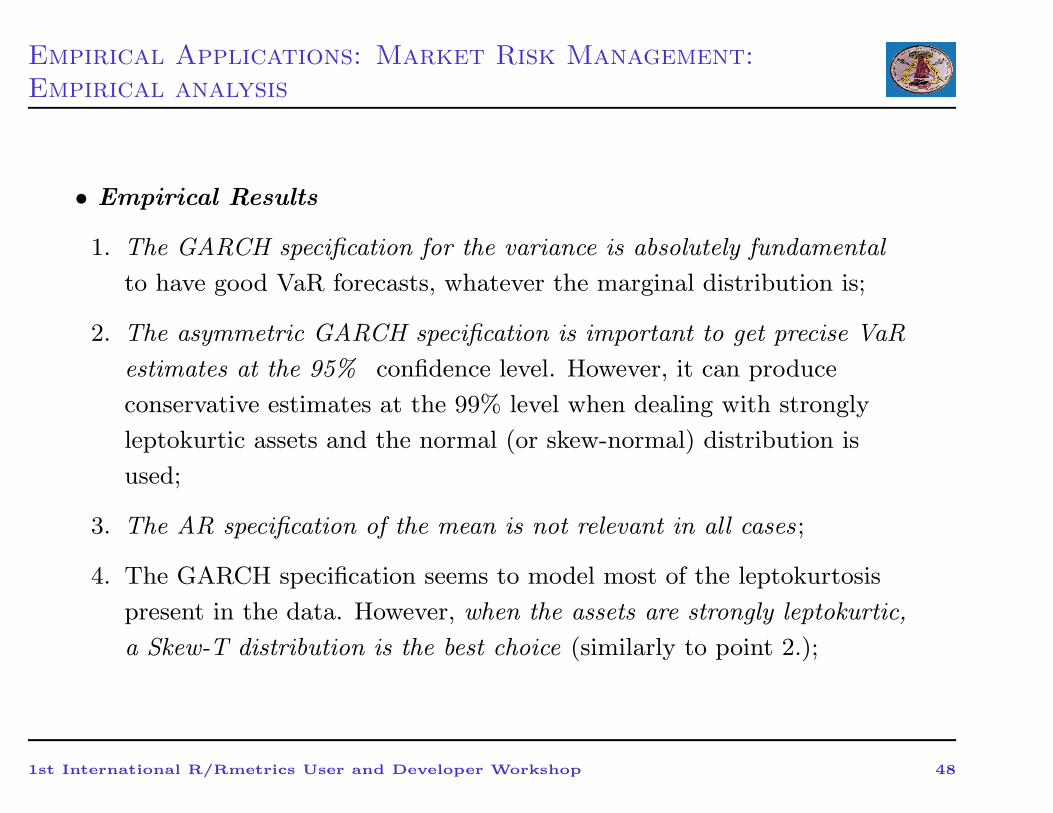

Empirical Applications: Market Risk Management:

Empirical analysis

• Empirical Results

1. The GARCH specification for the variance is absolutely fundamental

to have good VaR forecasts, whatever the marginal distribution is;

2. The asymmetric GARCH specification is important to get precise VaR

estimates at the 95% confidence level. However, it can produce

conservative estimates at the 99% level when dealing with strongly

leptokurtic assets and the normal (or skew-normal) distribution is

used;

3. The AR specification of the mean is not relevant in all cases;

4. The GARCH specification seems to model most of the leptokurtosis

present in the data. However, when the assets are strongly leptokurtic,

a Skew-T distribution is the best choice (similarly to point 2.);

1st International R/Rmetrics User and Developer Workshop 48

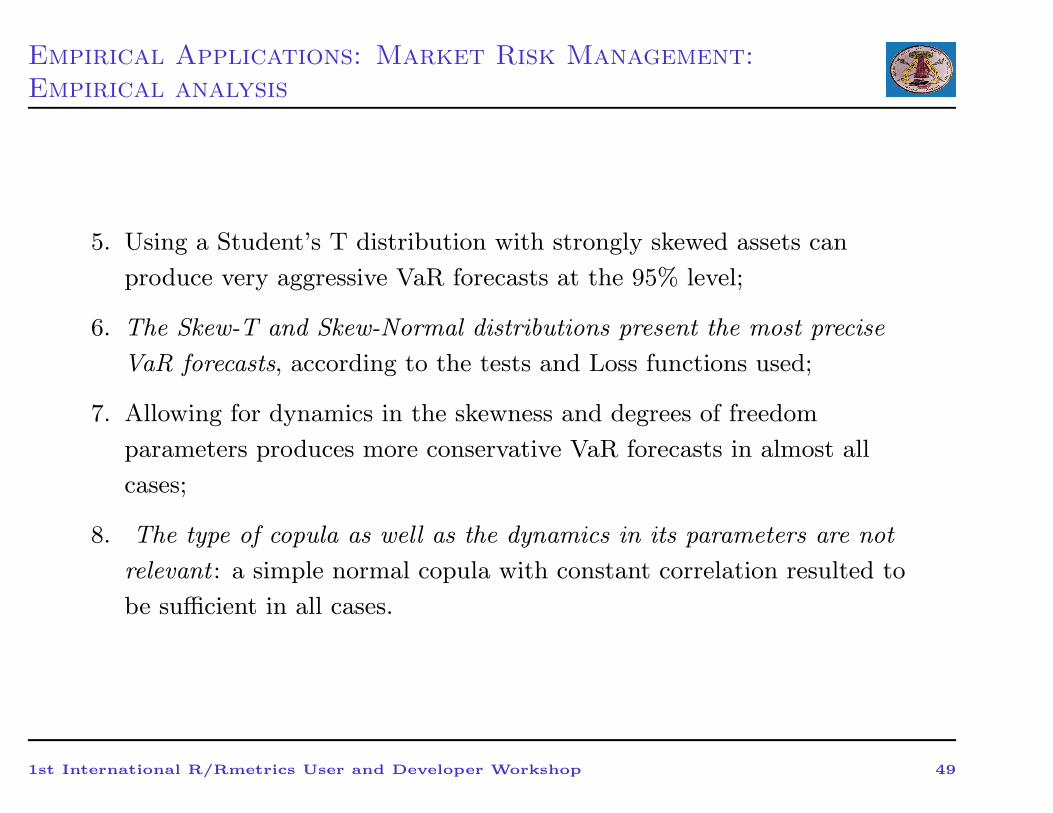

Empirical Applications: Market Risk Management:

Empirical analysis

5. Using a Student’s T distribution with strongly skewed assets can

produce very aggressive VaR forecasts at the 95% level;

6. The Skew-T and Skew-Normal distributions present the most precise

VaR forecasts, according to the tests and Loss functions used;

7. Allowing for dynamics in the skewness and degrees of freedom

parameters produces more conservative VaR forecasts in almost all

cases;

8. The type of copula as well as the dynamics in its parameters are not

relevant : a simple normal copula with constant correlation resulted to

be sufficient in all cases.

1st International R/Rmetrics User and Developer Workshop 49

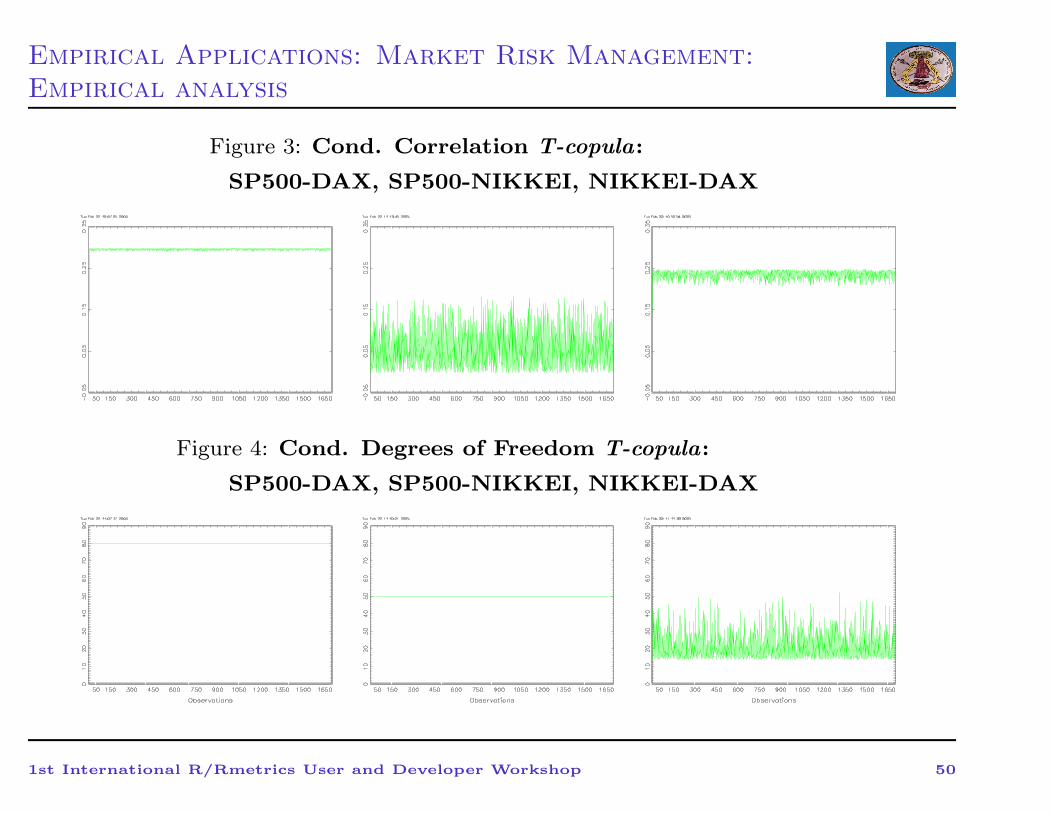

Empirical Applications: Market Risk Management:

Empirical analysis

Figure 3: Cond. Correlation T-copula:

SP500-DAX, SP500-NIKKEI, NIKKEI-DAX

Figure 4: Cond. Degrees of Freedom T-copula:

SP500-DAX, SP500-NIKKEI, NIKKEI-DAX

1st International R/Rmetrics User and Developer Workshop 50

Empirical Applications: Market Risk Management:

Conclusions and extensions

• Joint conditional normal distribution can give poor VaR

forecasts.

• Copulae proved to be a good solution for modeling dependence .

• ...but the choice of marginals is still the most important decision!

→ Skew - Normal or Skew - T

• Extend this framework to the Multivariate case, where copula’s

conditional correlation matrix is modelled with a DCC model

(Patton et al, 2004), or by using decomposition models like

Rydberg and Shephard (2003)

1st International R/Rmetrics User and Developer Workshop 51

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Introduction

Daul, Giorgi, Lindskog, and McNeil (2003), Demarta and McNeil (2005)

and Mc-Neil, Frey, and Embrechts (2005) underlined the ability of the

grouped t-copula to model the dependence present in a large set of

financial assets into account.

We extend their methodology by allowing the copula dependence structure

to be time-varying and we show how to estimate its parameters.

Furthermore, we prove the consistency and asymptotic normality of this

estimator under some special cases and we examine its finite samples

properties via simulations.

Finally, we apply this methodology for the estimation of the VaR of a

portfolio composed of thirty assets.

1st International R/Rmetrics User and Developer Workshop 52

Market Risk Management for Multivariate Portfolios: Dynamic

Grouped-T Copula Modelling: Definition and Estimation

Let Z|Ft−1 ∼ Nn(0,Rt), t = 1, . . . T , given the conditioning set Ft−1,

where Rt is the n× n conditional linear correlation matrix which follows a

DCC model, and R is the unconditional correlation matrix. Furthermore

let U ∼ Uniform(0, 1) be independent of Z .

Let Gν denote the distribution function of√

ν/χν , where χν is a chi

square distribution with ν degrees of freedom, and partition 1, . . . , n into

m subsets of sizes s1, . . . , sm. Set Wk = G−1νk

(U) for k = 1, . . . ,m and then

Y|Ft−1 = (W1Z1, . . . ,W1Zs1 ,W2Zs1+1, . . . ,W2Zs1+s2 , . . . ,WmZn), so

that Y has a so-called grouped t distribution. Finally, define

U|Ft−1 = (tν1(Y1), . . . , tν1(Ys1), tν2(Ys1+1), . . . , tν2(Ys1+s2), . . . , tνm(Yn))

(22)

U has a distribution on [0, 1]n with components uniformly distributed on

[0, 1]. We call its distribution function the dynamic grouped t-copula.

1st International R/Rmetrics User and Developer Workshop 53

Market Risk Management for Multivariate Portfolios: Dynamic

Grouped-T Copula Modelling: Definition and Estimation

Note that (Y1, . . . , Ys1) has a t distribution with ν1 degrees of freedom, and

in general for k = 1, . . . ,m− 1, (Ys1+...+sk+1, . . . , Ys1+...+sk+1) has a t

distribution with νk+1 degrees of freedom. Similarly, subvectors of U have

a t-copula with νk+1 degrees of freedom, for k = 0, . . . ,m− 1.

In this case no elementary density has been given.

However, there is a very useful correlation approximation, obtained by

Daul et al. (2003) for the constant correlation case:

ρi,j(zi, zj) ≈ sin(πτij(ui, uj)/2) (23)

where i and j belong to different groups and τij is the pairwise Kendall’s

tau. This approximation then allows for Maximum Likelihood estimation

for each subgroup separately.

1st International R/Rmetrics User and Developer Workshop 54

Market Risk Management for Multivariate Portfolios: Dynamic

Grouped-T Copula Modelling: Definition and Estimation

Definition 0.1 (Dynamic Grouped-T copula estimation).

1. Transform the standardized residuals (η1t, η2t, . . . , ηnt) obtained from a

univariate GARCH estimation, for example, into uniform variates

(u1t, u2t, . . . unt), using either a parametric cumulative distribution

function (c.d.f.) or an empirical c.d.f..

2. Collect all pairwise estimates of the unconditional sample Kendall’s

tau given by

ˆτi,j(uj , uk) =

T

2

−1∑

1≤t<s<T

sign(

(ui,t − ˜ui,s)(uj,t − ˜uj,s))

(24)

in an empirical Kendall’s tau matrix ˆΣτ

defined by ˆΣτ

jk = ˆτ(uj , uk),

and then construct the unconditional correlation matrix using this

relationship ˆRj,k = sin(π2ˆΣ

τ

j,k), where the estimated parameters are the

q = n · (n− 1)/2 unconditional correlations [ρ1, . . . , ρq]′.

1st International R/Rmetrics User and Developer Workshop 55

Market Risk Management for Multivariate Portfolios: Dynamic

Grouped-T Copula Modelling: Definition and Estimation

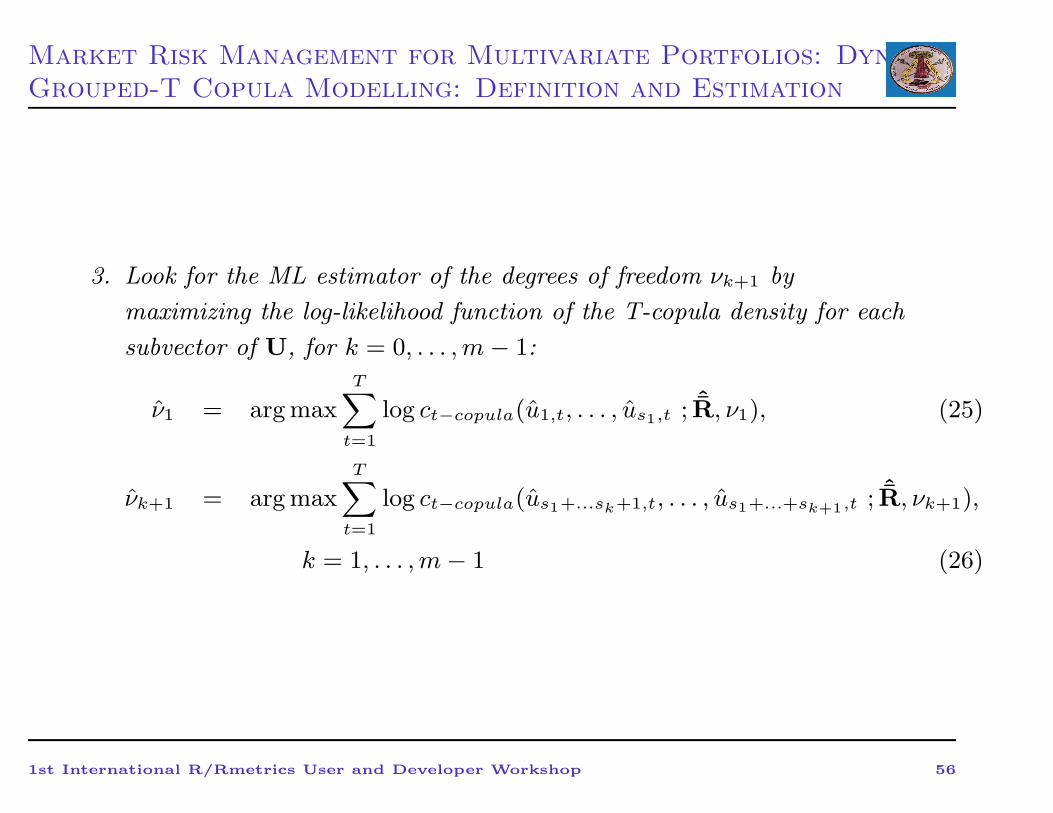

3. Look for the ML estimator of the degrees of freedom νk+1 by

maximizing the log-likelihood function of the T-copula density for each

subvector of U, for k = 0, . . . ,m− 1:

ν1 = arg max

T∑

t=1

log ct−copula(u1,t, . . . , us1,t ; ˆR, ν1), (25)

νk+1 = arg max

T∑

t=1

log ct−copula(us1+...sk+1,t, . . . , us1+...+sk+1,t ; ˆR, νk+1),

k = 1, . . . ,m− 1 (26)

1st International R/Rmetrics User and Developer Workshop 56

Market Risk Management for Multivariate Portfolios: Dynamic

Grouped-T Copula Modelling: Definition and Estimation

4. Estimate a DCC(1,1) model for the conditional correlation matrix Rt,

by using QML estimation with the normal copula density:

α, β = arg max

T∑

t=1

log cnormal(u1,t, . . . , un,t;ˆR,Rt) = (27)

= arg max

T∑

t=1

1

|Rt|1/2exp

(

−1

2ζ′(R−1

t − I)ζ

)

(28)

where ζ = (Φ−1(u1,t), . . . ,Φ−1(un,t))

′ is the vector of univariate

normal inverse distribution functions, and where we assume the

following DCC(1,1) model for the correlation matrix Rt

Rt = (diagQt)−1/2Qt(diagQt)

−1/2 (29)

Qt =

(

1 −L∑

l=1

αl −S∑

s=1

βs

)

Q+

L∑

l=1

αlut−lu′t−l +

S∑

s=1

βsQt−s

where Q is the n× n unconditional correlation matrix of ut, αl (≥ 0)

and βs (≥ 0) are scalar parameters satisfying∑L

l=1 αl +∑S

s=1 βs < 1.

1st International R/Rmetrics User and Developer Workshop 57

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Asymptotic Properties

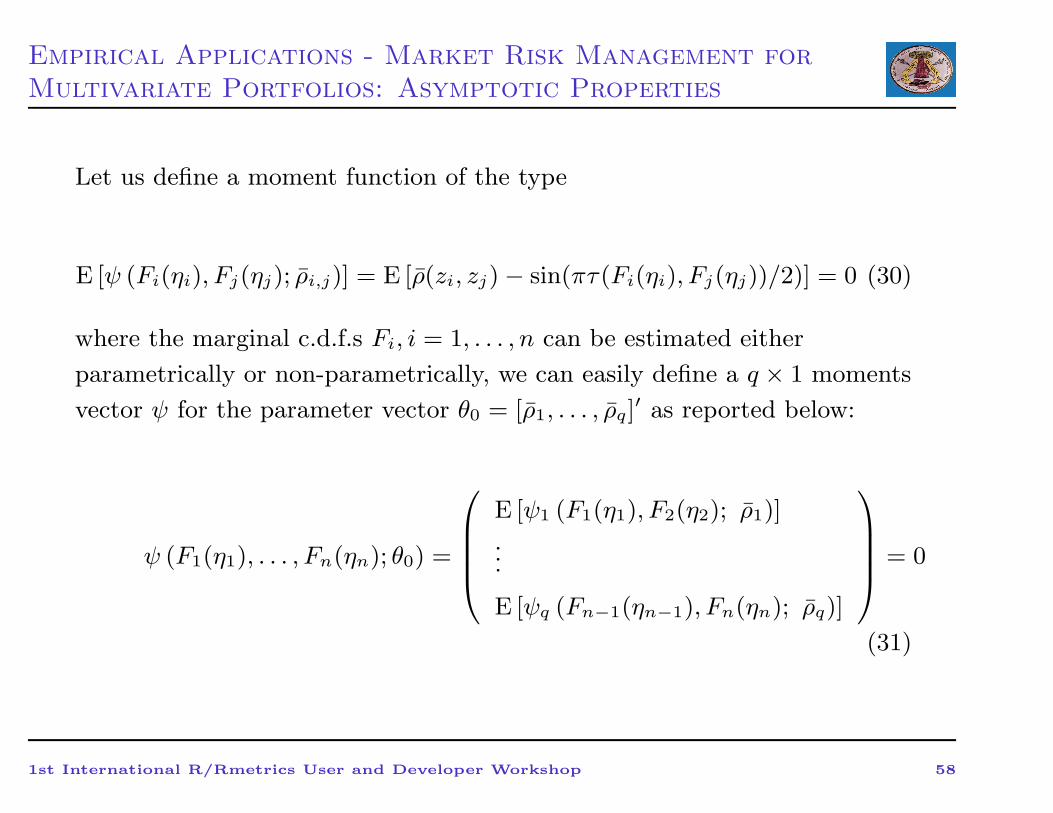

Let us define a moment function of the type

E [ψ (Fi(ηi), Fj(ηj); ρi,j)] = E [ρ(zi, zj) − sin(πτ(Fi(ηi), Fj(ηj))/2)] = 0 (30)

where the marginal c.d.f.s Fi, i = 1, . . . , n can be estimated either

parametrically or non-parametrically, we can easily define a q × 1 moments

vector ψ for the parameter vector θ0 = [ρ1, . . . , ρq]′ as reported below:

ψ (F1(η1), . . . , Fn(ηn); θ0) =

E [ψ1 (F1(η1), F2(η2); ρ1)]

...

E [ψq (Fn−1(ηn−1), Fn(ηn); ρq)]

= 0

(31)

1st International R/Rmetrics User and Developer Workshop 58

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Asymptotic Properties

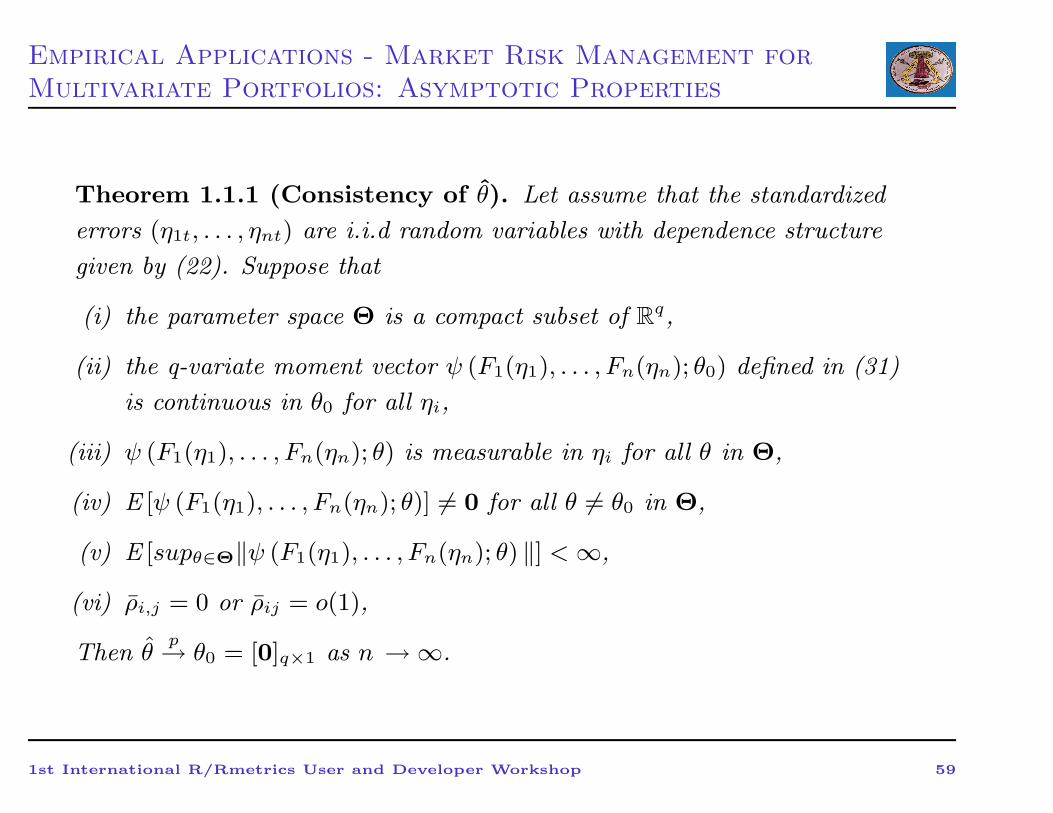

Theorem 1.1.1 (Consistency of θ). Let assume that the standardized

errors (η1t, . . . , ηnt) are i.i.d random variables with dependence structure

given by (22). Suppose that

(i) the parameter space Θ is a compact subset of Rq,

(ii) the q-variate moment vector ψ (F1(η1), . . . , Fn(ηn); θ0) defined in (31)

is continuous in θ0 for all ηi,

(iii) ψ (F1(η1), . . . , Fn(ηn); θ) is measurable in ηi for all θ in Θ,

(iv) E [ψ (F1(η1), . . . , Fn(ηn); θ)] 6= 0 for all θ 6= θ0 in Θ,

(v) E [supθ∈Θ‖ψ (F1(η1), . . . , Fn(ηn); θ) ‖] <∞,

(vi) ρi,j = 0 or ρij = o(1),

Then θp→ θ0 = [0]q×1 as n → ∞.

1st International R/Rmetrics User and Developer Workshop 59

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Asymptotic Properties

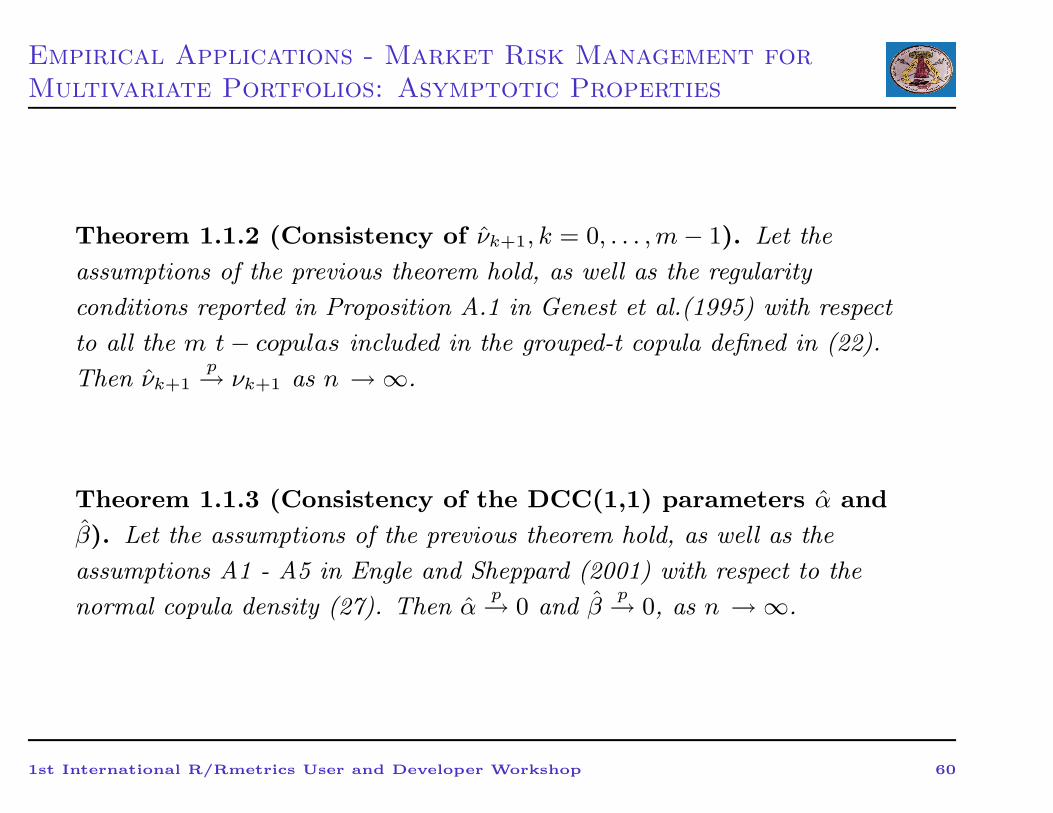

Theorem 1.1.2 (Consistency of νk+1, k = 0, . . . ,m− 1). Let the

assumptions of the previous theorem hold, as well as the regularity

conditions reported in Proposition A.1 in Genest et al.(1995) with respect

to all the m t− copulas included in the grouped-t copula defined in (22).

Then νk+1p→ νk+1 as n → ∞.

Theorem 1.1.3 (Consistency of the DCC(1,1) parameters α and

β). Let the assumptions of the previous theorem hold, as well as the

assumptions A1 - A5 in Engle and Sheppard (2001) with respect to the

normal copula density (27). Then αp→ 0 and β

p→ 0, as n → ∞.

1st International R/Rmetrics User and Developer Workshop 60

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Asymptotic Properties

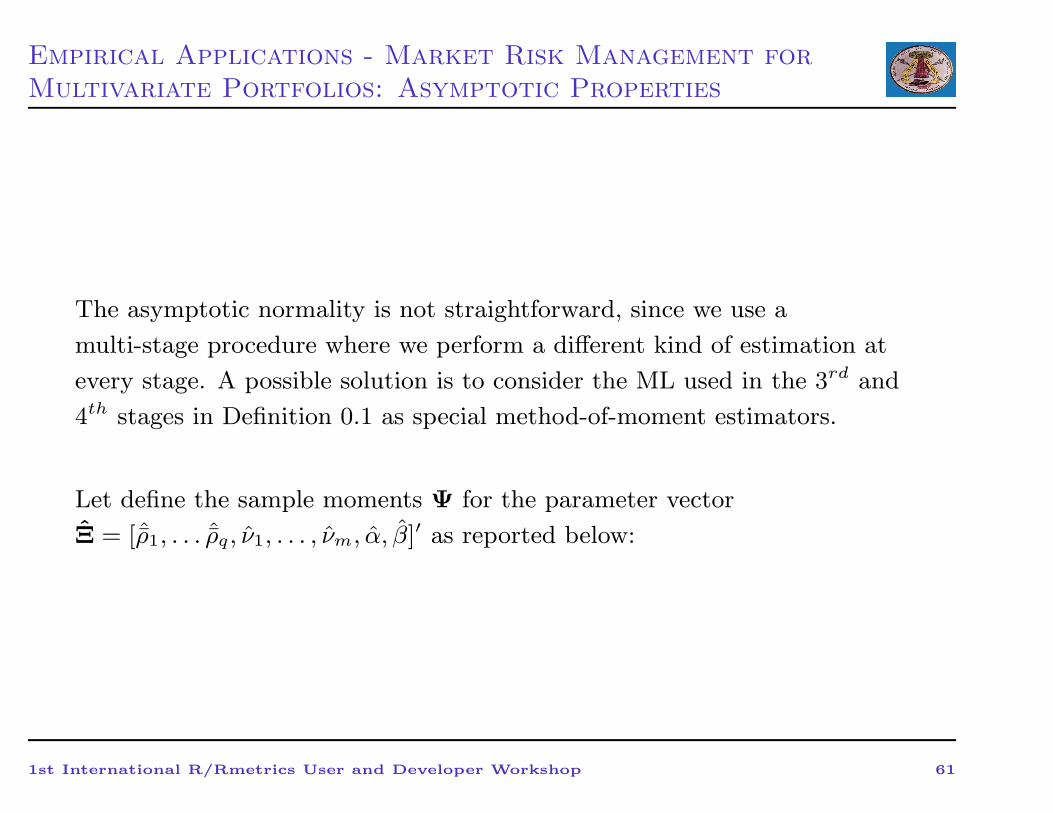

The asymptotic normality is not straightforward, since we use a

multi-stage procedure where we perform a different kind of estimation at

every stage. A possible solution is to consider the ML used in the 3rd and

4th stages in Definition 0.1 as special method-of-moment estimators.

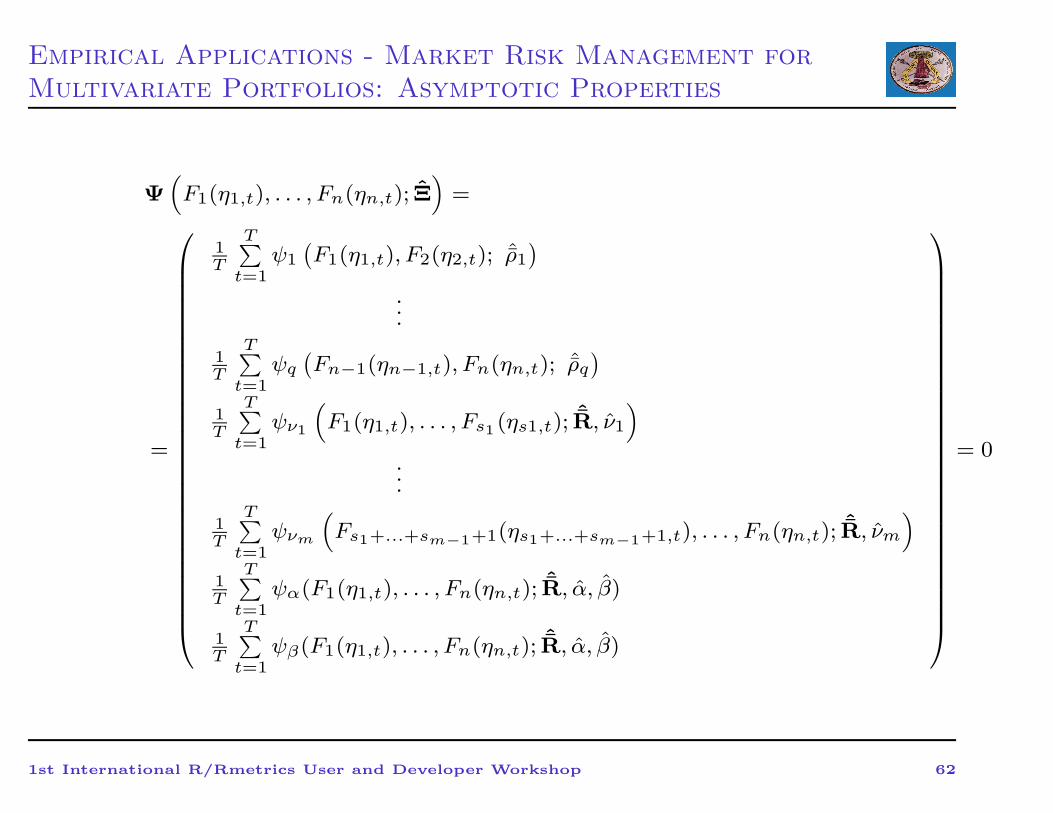

Let define the sample moments Ψ for the parameter vector

Ξ = [ˆρ1, . . . ˆρq, ν1, . . . , νm, α, β]′ as reported below:

1st International R/Rmetrics User and Developer Workshop 61

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Asymptotic Properties

Ψ(

F1(η1,t), . . . , Fn(ηn,t); Ξ)

=

=

1T

T∑

t=1ψ1

(

F1(η1,t), F2(η2,t); ˆρ1)

...

1T

T∑

t=1ψq(

Fn−1(ηn−1,t), Fn(ηn,t); ˆρq)

1T

T∑

t=1ψν1

(

F1(η1,t), . . . , Fs1 (ηs1,t);ˆR, ν1

)

..

.

1T

T∑

t=1ψνm

(

Fs1+...+sm−1+1(ηs1+...+sm−1+1,t), . . . , Fn(ηn,t);ˆR, νm

)

1T

T∑

t=1ψα(F1(η1,t), . . . , Fn(ηn,t);

ˆR, α, β)

1T

T∑

t=1ψβ(F1(η1,t), . . . , Fn(ηn,t);

ˆR, α, β)

= 0

1st International R/Rmetrics User and Developer Workshop 62

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Asymptotic Properties

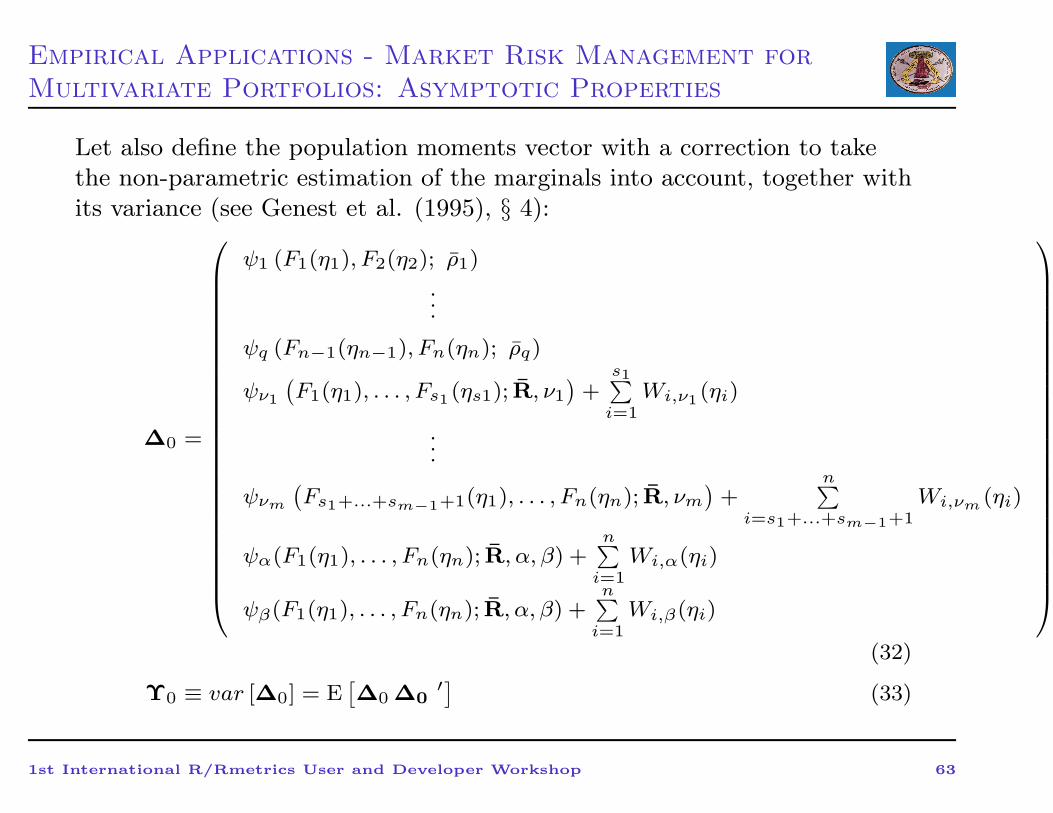

Let also define the population moments vector with a correction to takethe non-parametric estimation of the marginals into account, together withits variance (see Genest et al. (1995), § 4):

∆0 =

ψ1 (F1(η1), F2(η2); ρ1)

.

..

ψq (Fn−1(ηn−1), Fn(ηn); ρq)

ψν1

(

F1(η1), . . . , Fs1 (ηs1); R, ν1)

+s1∑

i=1Wi,ν1 (ηi)

...

ψνm

(

Fs1+...+sm−1+1(η1), . . . , Fn(ηn); R, νm)

+n∑

i=s1+...+sm−1+1Wi,νm (ηi)

ψα(F1(η1), . . . , Fn(ηn); R, α, β) +n∑

i=1Wi,α(ηi)

ψβ(F1(η1), . . . , Fn(ηn); R, α, β) +n∑

i=1Wi,β(ηi)

(32)

Υ0 ≡ var [∆0] = E[

∆0 ∆0′] (33)

1st International R/Rmetrics User and Developer Workshop 63

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Asymptotic Properties

where

Wi,ν1 (ηi) =

∫

1l Fi(ηi)≤ui

∂2

∂ν1∂uilog c(u1, . . . us1 ; R, ν1)dC(u1, . . . , us1 )

... (34)

Wi,νm (ηi) =

∫

1l Fi(ηi)≤ui

∂2

∂νm∂uilog c(ui=s1+...+sm−1+1, . . . un; R, νm)

dC(ui=s1+...+sm−1+1, . . . , un)

(35)

Wi,α(ηi) =

∫

1l Fi(ηi)≤ui

∂2

∂α∂uilog c(u1, . . . un; R, α, β)dC(u1, . . . , un)

Wi,β(ηi) =

∫

1l Fi(ηi)≤ui

∂2

∂β∂uilog c(u1, . . . un; R, α, β)dC(u1, . . . , un)

(36)

1st International R/Rmetrics User and Developer Workshop 64

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Asymptotic Properties

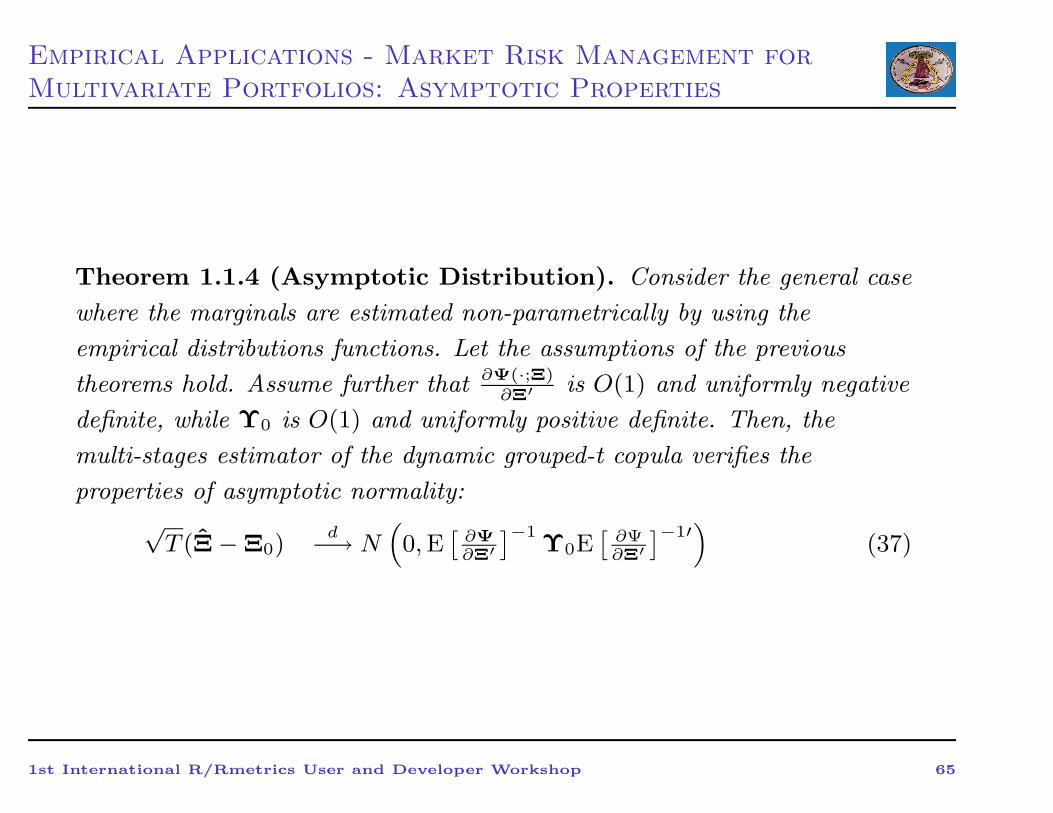

Theorem 1.1.4 (Asymptotic Distribution). Consider the general case

where the marginals are estimated non-parametrically by using the

empirical distributions functions. Let the assumptions of the previous

theorems hold. Assume further that ∂Ψ(·;Ξ)∂Ξ′ is O(1) and uniformly negative

definite, while Υ0 is O(1) and uniformly positive definite. Then, the

multi-stages estimator of the dynamic grouped-t copula verifies the

properties of asymptotic normality:√T (Ξ − Ξ0)

d−→ N(

0,E[

∂Ψ∂Ξ′

]−1Υ0E

[

∂Ψ∂Ξ′

]−1′)

(37)

1st International R/Rmetrics User and Developer Workshop 65

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Simulation Study

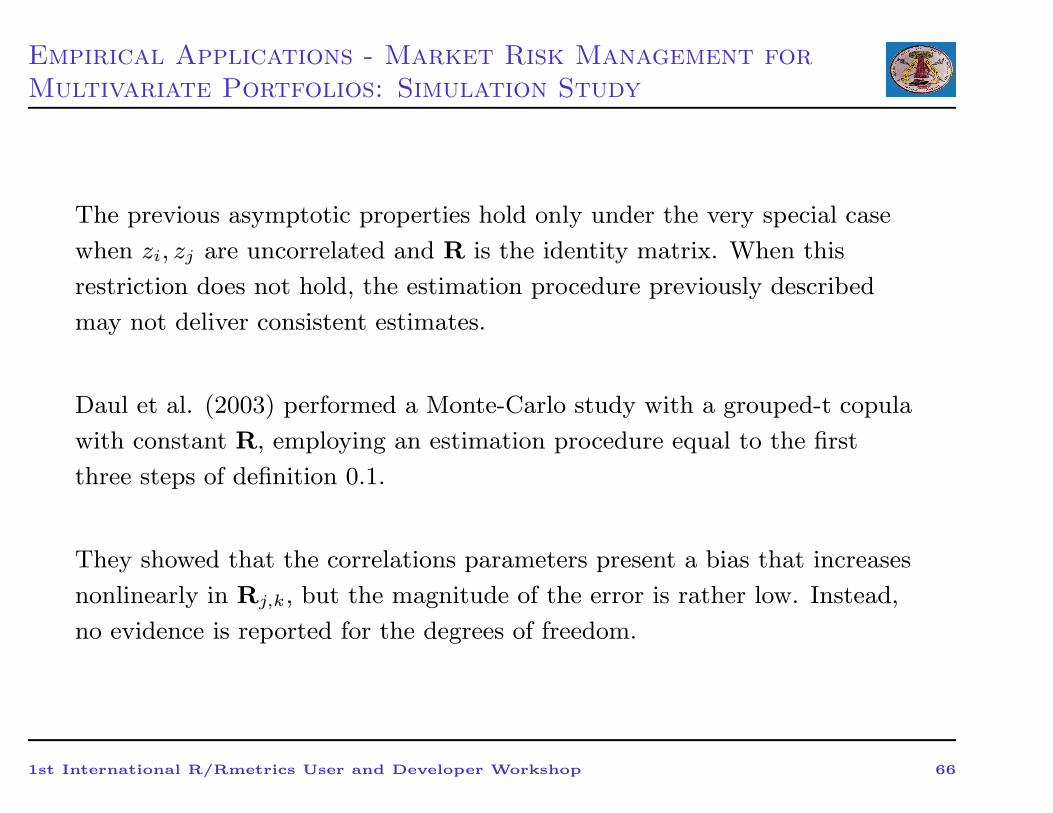

The previous asymptotic properties hold only under the very special case

when zi, zj are uncorrelated and R is the identity matrix. When this

restriction does not hold, the estimation procedure previously described

may not deliver consistent estimates.

Daul et al. (2003) performed a Monte-Carlo study with a grouped-t copula

with constant R, employing an estimation procedure equal to the first

three steps of definition 0.1.

They showed that the correlations parameters present a bias that increases

nonlinearly in Rj,k, but the magnitude of the error is rather low. Instead,

no evidence is reported for the degrees of freedom.

1st International R/Rmetrics User and Developer Workshop 66

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Simulation Study

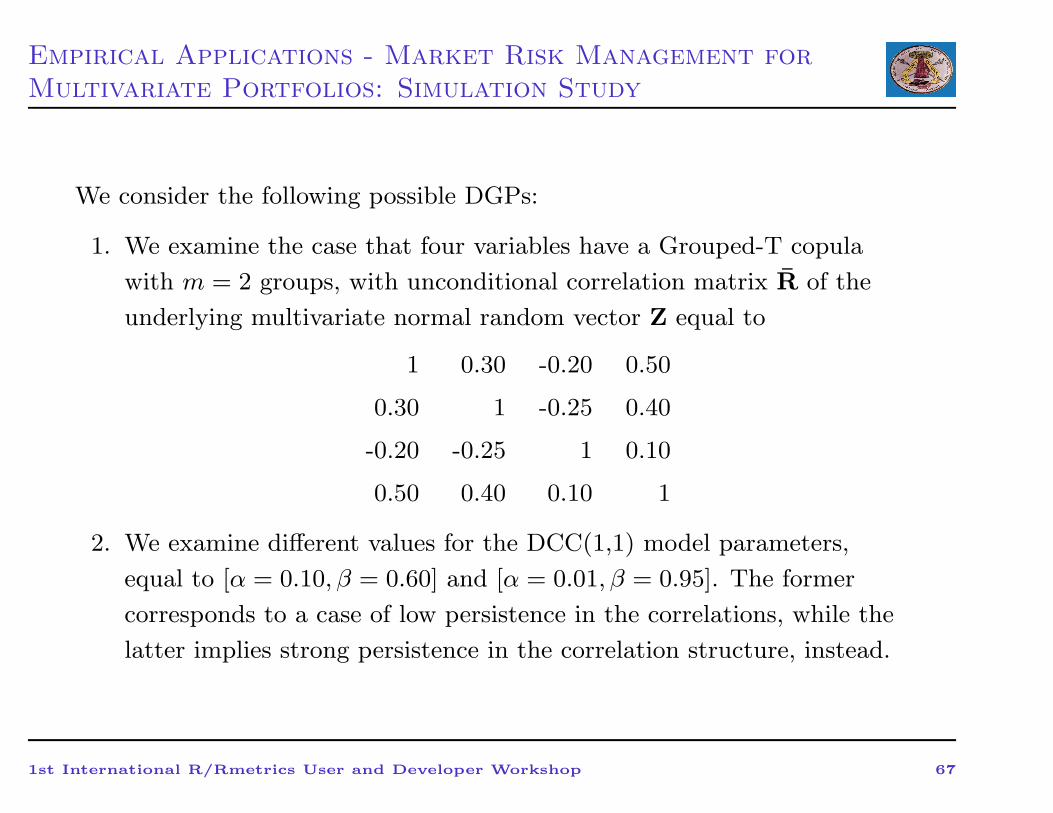

We consider the following possible DGPs:

1. We examine the case that four variables have a Grouped-T copula

with m = 2 groups, with unconditional correlation matrix R of the

underlying multivariate normal random vector Z equal to

1 0.30 -0.20 0.50

0.30 1 -0.25 0.40

-0.20 -0.25 1 0.10

0.50 0.40 0.10 1

2. We examine different values for the DCC(1,1) model parameters,

equal to [α = 0.10, β = 0.60] and [α = 0.01, β = 0.95]. The former

corresponds to a case of low persistence in the correlations, while the

latter implies strong persistence in the correlation structure, instead.

1st International R/Rmetrics User and Developer Workshop 67

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Simulation Study

3. We examine two cases for the degrees of freedom νk for the m = 2

groups:

• ν1 = 3 and ν2 = 4;

• ν1 = 6 and ν2 = 15;

The first case corresponds to a situation of strong tail dependence, that

is there is a high probability to observe an extremely large observation

on one variable, given that the other variable has yielded an extremely

large observation. The last exhibit low tail dependence, instead.

4. We consider three possible data situations: n = 500, n = 1000 and

n = 10000.

1st International R/Rmetrics User and Developer Workshop 68

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Simulation Study

• Unconditional correlation parameters Rj,k: there is a general negative

bias that stabilize after n = 1000. However, this bias is quite high

when there is strong tail dependence among variables (νk are low),

while it is much lower when the tail dependence is rather weak (νk are

high). Besides, it almost disappears when correlations are lower than

0.10, thus confirming the previous asymptotics results. The effects of

different dynamic structure in the correlations are negligible, instead.

• DCC(1,1) parameters (α, β): the higher is the persistence in the

correlations structure (high β), the quicker β converges to the true

values. In general, the effects of different DGPs on β are almost

negligible. The parameter α describing the effect of past shocks shows

positive biases, instead, that are higher in magnitude when high tail

dependence and high persistence in the correlations are considered.

1st International R/Rmetrics User and Developer Workshop 69

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Simulation Study

• Degrees of freedom νk: the speed of convergence towards the true

values is, in general, very low and changes substantially according to

the magnitude of νk and the dynamic structure in the correlations.

Particularly, when there is high tail dependence (νk are low) the

convergence is much quicker than when there is low tail dependence

(νk are high). Furthermore, the convergence is quicker when there is

strong persistence in the correlations structure (β is high), rather than

the persistence is weak (β is low).

This is good news since financial assets usually show high tail

dependence and high persistence in the correlations (see Mcneil et al.

(2005) and references therein). Besides, it is interesting to note that

the biases are negative for all the considered DGPs, i.e. the estimated

νk are lower than the true values νk.

1st International R/Rmetrics User and Developer Workshop 70

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Simulation Study

We explore the consequences of our multi-step estimation procedure of the

dynamic grouped-t copula on Value at Risk (VaR) estimation, by using

the same DGPs previously discussed.

As we want to study only the effects of the estimated dependence

structure, we consider the same marginals for all DGPs, as well as the

same past shocks ut−1. For sake of simplicity, we suppose to invest an

amount Mi = 1$, i = 1, . . . , n = 4 in every asset.

We consider eight different quantiles to better highlight the overall effects

of the estimated copula parameters on the joint distribution of the losses:

0.25%, 0.50%, 1.00%, 5.00%, 95.00%, 99.00%, 99.50%, 99.75%.

1st International R/Rmetrics User and Developer Workshop 71

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Simulation Study

In general, the estimated quantiles show a very small underestimation,

which can range between 0 and 3%. Particularly, we can observe that

• the error in the approximation of the quantiles is lower the lower the

tail dependence between assets is, i.e. when νk are high, ceteris

paribus. As a consequence, when estimating the quantile they tend to

offset the effect of lower correlations, which would decrease the

computed quantile, instead.

• the error in the approximation of the quantiles is lower the higher is

the persistence in the correlations, ceteris paribus. This result is due to

the much smaller biases of the parameters α, β when the true DGPs

are characterized by high persistence in the correlations.

1st International R/Rmetrics User and Developer Workshop 72

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Simulation Study

• the error in the approximation of the quantiles tend to slightly increase

as long as the sample dimension increases. Such a result can be

explained considering that the computed degrees of freedom νk slowly

converge to the true values when the dimension of the dataset

increases, while the negative biases in the correlations tend to

stabilize. As a consequence, the computed νk do not offset any more

the effect of lower correlations, and therefore the underestimation in

the VaR increases.

• the approximations of the extreme quantiles are much better than those

of the central quantiles, while the analysis reveals no major difference

between left tail and right tail.

• It is interesting to note that up to medium-sized datasets consisting of

n = 1000 observations, the effects of the biases in the degrees of

freedom and the biases in the correlations tend to offset each other and

the error in approximating the quantile is close to zero.

1st International R/Rmetrics User and Developer Workshop 73

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Empirical Analysis

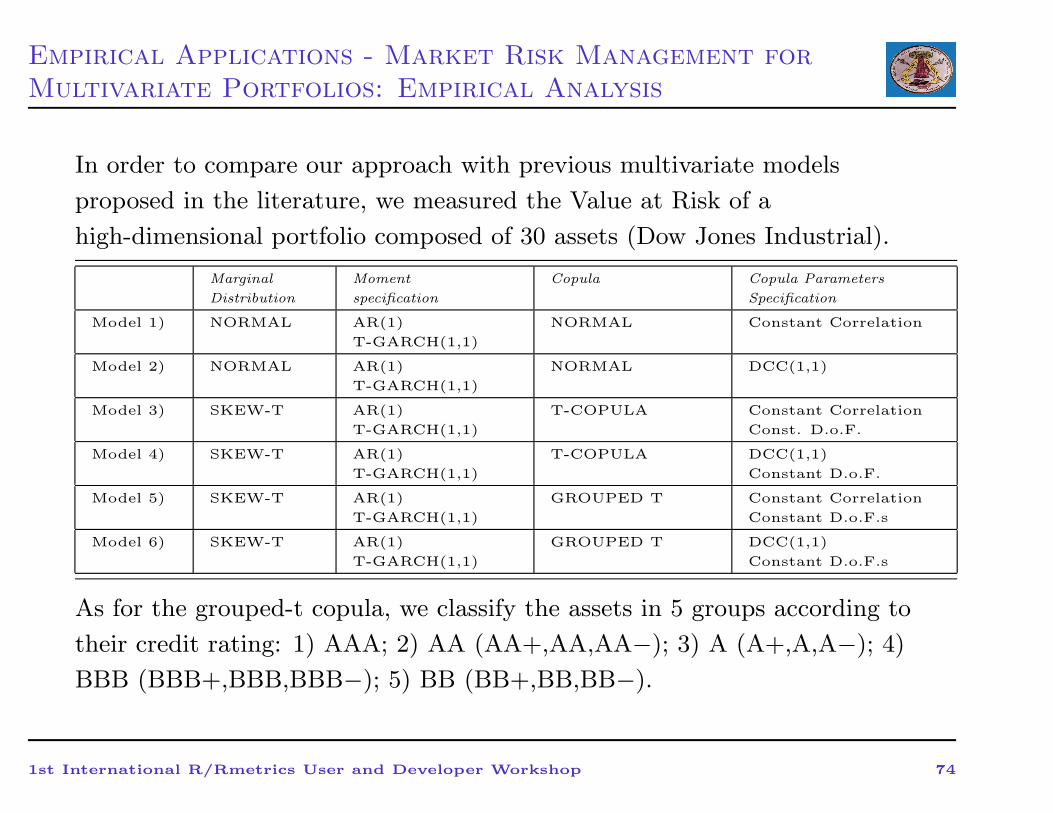

In order to compare our approach with previous multivariate models

proposed in the literature, we measured the Value at Risk of a

high-dimensional portfolio composed of 30 assets (Dow Jones Industrial).

Marginal

Distribution

Moment

specification

Copula Copula Parameters

Specification

Model 1) NORMAL AR(1)

T-GARCH(1,1)

NORMAL Constant Correlation

Model 2) NORMAL AR(1)

T-GARCH(1,1)

NORMAL DCC(1,1)

Model 3) SKEW-T AR(1)

T-GARCH(1,1)

T-COPULA Constant Correlation

Const. D.o.F.

Model 4) SKEW-T AR(1)

T-GARCH(1,1)

T-COPULA DCC(1,1)

Constant D.o.F.

Model 5) SKEW-T AR(1)

T-GARCH(1,1)

GROUPED T Constant Correlation

Constant D.o.F.s

Model 6) SKEW-T AR(1)

T-GARCH(1,1)

GROUPED T DCC(1,1)

Constant D.o.F.s

As for the grouped-t copula, we classify the assets in 5 groups according to

their credit rating: 1) AAA; 2) AA (AA+,AA,AA−); 3) A (A+,A,A−); 4)

BBB (BBB+,BBB,BBB−); 5) BB (BB+,BB,BB−).

1st International R/Rmetrics User and Developer Workshop 74

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Empirical Analysis

We will assess the performance of the competing multivariate models using

the following back-testing techniques

• Kupiec (1995) unconditional coverage test;

• Christoffersen (1998) conditional coverage test;

• Loss functions to evaluate VaR forecast accuracy;

• Hansen and Lunde (2005) and Hansen’s (2005) Superior Predictive

Ability (SPA) test.

1st International R/Rmetrics User and Developer Workshop 75

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Empirical Analysis

1. Kupiec’s test: Following binomial theory, the probability of

observing N failures out of T observations is (1-p)T−NpN , so that the

test of the null hypothesis H0: p = p∗ is given by a LR test statistic:

LR = 2 · ln[(1 − p∗)T−Np∗N

] + 2 · ln[(1 −N/T )T−N (N/T )N ]

2. Christoffersen’s test: . Its main advantage over the previous

statistic is that it takes account of any conditionality in our forecast:

for example, if volatilities are low in some period and high in others,

the VaR forecast should respond to this clustering event.

LRCC = −2 ln[(1−p)T−NpN ]+2 ln[(1−π01)n00πn01

01 (1−π11)n10πn11

11 ]

where nij is the number of observations with value i followed by j for

i, j = 0, 1 and

πij =nij

∑

j nij

1st International R/Rmetrics User and Developer Workshop 76

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Empirical Analysis

3. Loss functions: As noted by the Basle Committee on Banking

Supervision (1996), the magnitude as well as the number of exceptions

are a matter of regulatory concern. Since the object of interest is the

conditional α-quantile of the portfolio loss distribution, we use the

asymmetric linear loss function proposed in Gonzalez and Rivera

(2006) and Giacomini and and Komunjer (2005), and defined as

Tα(et+1) ≡ (α− 1l (et+1 < 0))et+1 (38)

where et+1 = Lt+1 − V aRt+1|t, Lt+1 is the realized loss, while

V aRt+1|t is the VaR forecast at time t+ 1 on information available at

time t.

4. Hansen’s (2005) Superior Predictive Ability (SPA) test: The

SPA test is a test that can be used for comparing the performances of

two or more forecasting models.

The forecasts are evaluated using a prespecified loss function and the

“best” forecast model is the model that produces the smallest loss.

1st International R/Rmetrics User and Developer Workshop 77

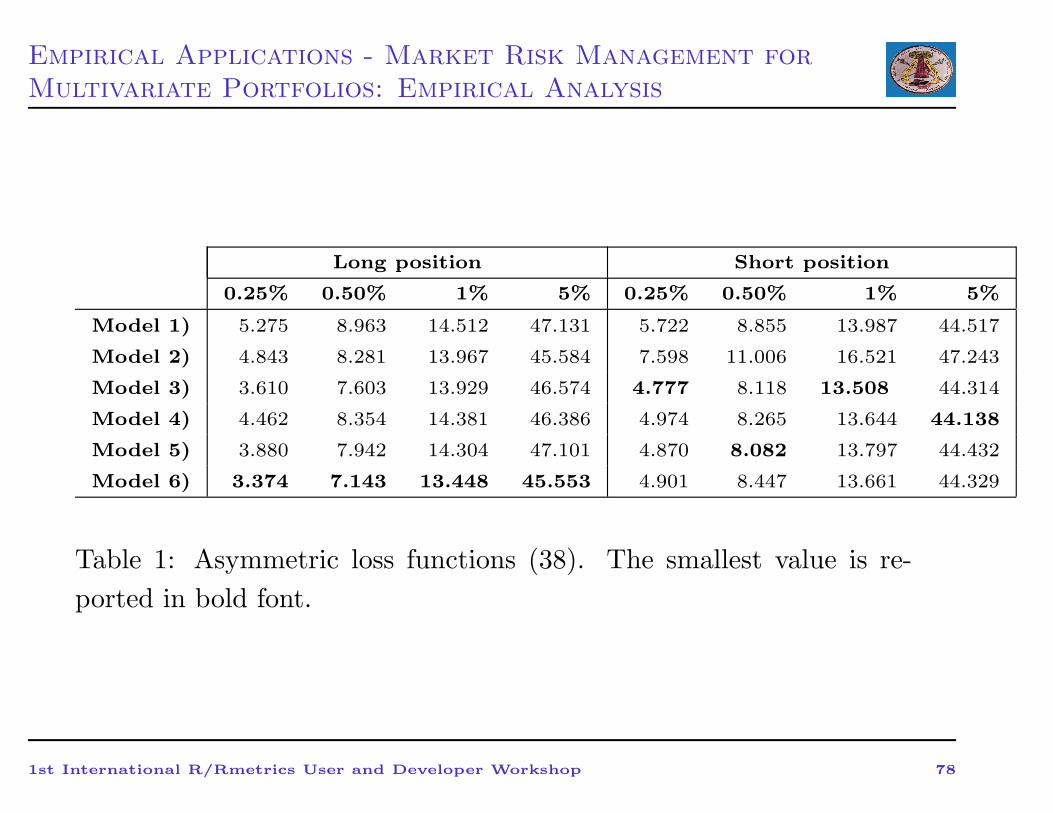

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Empirical Analysis

Long position Short position

0.25% 0.50% 1% 5% 0.25% 0.50% 1% 5%

Model 1) 5.275 8.963 14.512 47.131 5.722 8.855 13.987 44.517

Model 2) 4.843 8.281 13.967 45.584 7.598 11.006 16.521 47.243

Model 3) 3.610 7.603 13.929 46.574 4.777 8.118 13.508 44.314

Model 4) 4.462 8.354 14.381 46.386 4.974 8.265 13.644 44.138

Model 5) 3.880 7.942 14.304 47.101 4.870 8.082 13.797 44.432

Model 6) 3.374 7.143 13.448 45.553 4.901 8.447 13.661 44.329

Table 1: Asymmetric loss functions (38). The smallest value is re-

ported in bold font.

1st International R/Rmetrics User and Developer Workshop 78

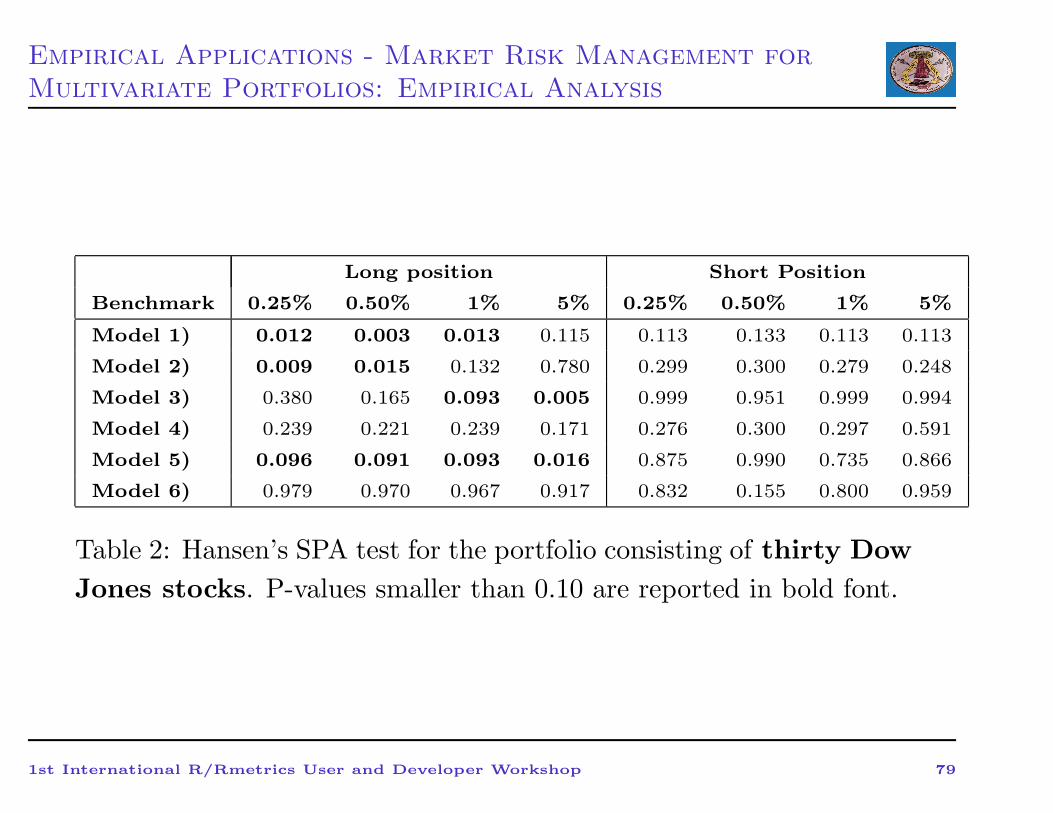

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Empirical Analysis

Long position Short Position

Benchmark 0.25% 0.50% 1% 5% 0.25% 0.50% 1% 5%

Model 1) 0.012 0.003 0.013 0.115 0.113 0.133 0.113 0.113

Model 2) 0.009 0.015 0.132 0.780 0.299 0.300 0.279 0.248

Model 3) 0.380 0.165 0.093 0.005 0.999 0.951 0.999 0.994

Model 4) 0.239 0.221 0.239 0.171 0.276 0.300 0.297 0.591

Model 5) 0.096 0.091 0.093 0.016 0.875 0.990 0.735 0.866

Model 6) 0.979 0.970 0.967 0.917 0.832 0.155 0.800 0.959

Table 2: Hansen’s SPA test for the portfolio consisting of thirty Dow

Jones stocks. P-values smaller than 0.10 are reported in bold font.

1st International R/Rmetrics User and Developer Workshop 79

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Empirical Analysis

Long positions

0.25% 0.50% 1% 5%

M. N/T pUC pCC N/T pUC pCC N/T pUC pCC N/T pUC pCC

1) 1.40% 0.00 0.00 1.90% 0.00 0.00 2.30% 0.00 0.00 6.30% 0.07 0.19

2) 1.30% 0.00 0.00 1.60% 0.00 0.00 1.90% 0.01 0.03 5.80% 0.26 0.49

3) 0.90% 0.00 0.01 1.40% 0.00 0.00 2.00% 0.01 0.01 6.60% 0.03 0.08

4) 0.60% 0.06 0.17 1.40% 0.00 0.00 1.90% 0.01 0.03 6.20% 0.09 0.24

5) 0.80% 0.01 0.02 1.30% 0.00 0.00 1.90% 0.01 0.03 6.10% 0.12 0.18

6) 0.50% 0.16 0.37 1.10% 0.02 0.02 1.80% 0.02 0.05 6.00% 0.16 0.35

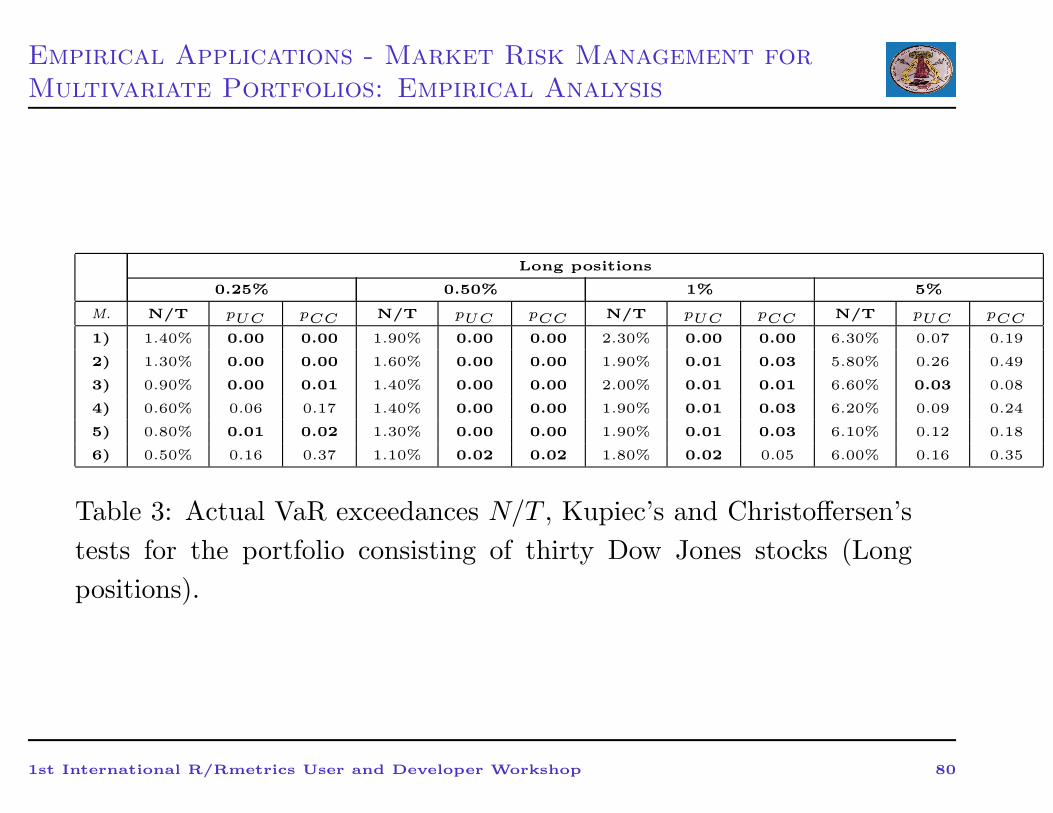

Table 3: Actual VaR exceedances N/T , Kupiec’s and Christoffersen’s

tests for the portfolio consisting of thirty Dow Jones stocks (Long

positions).

1st International R/Rmetrics User and Developer Workshop 80

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Empirical Analysis

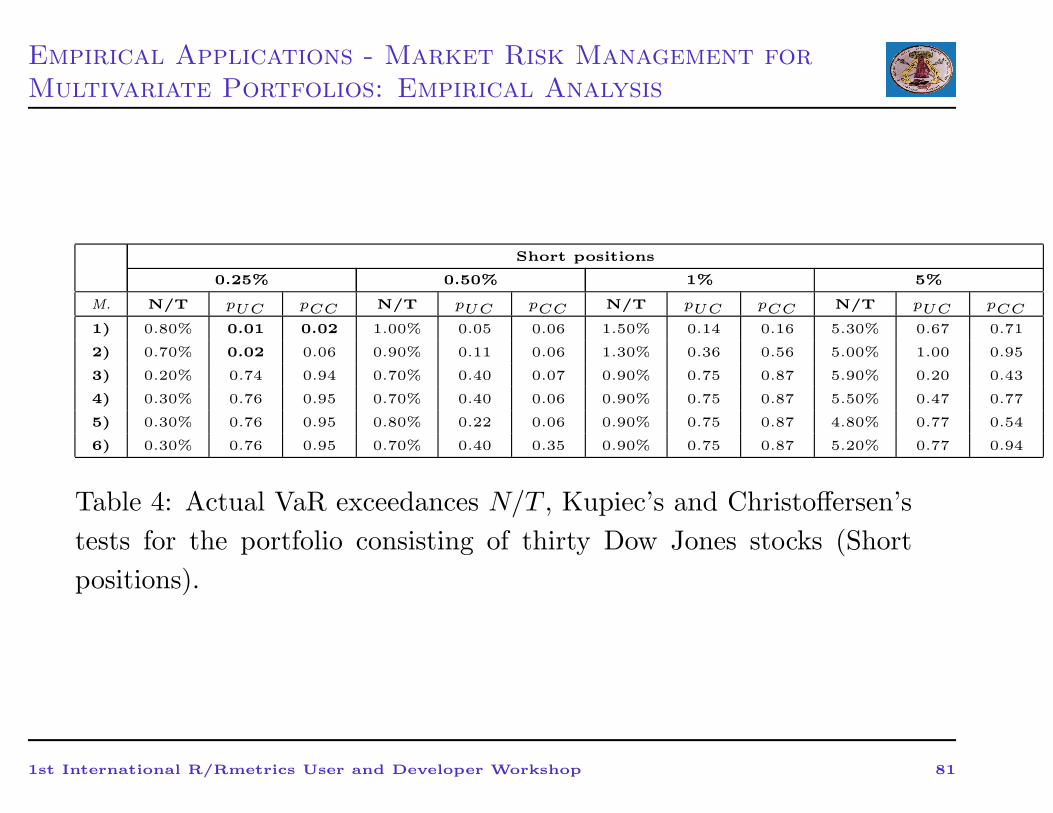

Short positions

0.25% 0.50% 1% 5%

M. N/T pUC pCC N/T pUC pCC N/T pUC pCC N/T pUC pCC

1) 0.80% 0.01 0.02 1.00% 0.05 0.06 1.50% 0.14 0.16 5.30% 0.67 0.71

2) 0.70% 0.02 0.06 0.90% 0.11 0.06 1.30% 0.36 0.56 5.00% 1.00 0.95

3) 0.20% 0.74 0.94 0.70% 0.40 0.07 0.90% 0.75 0.87 5.90% 0.20 0.43

4) 0.30% 0.76 0.95 0.70% 0.40 0.06 0.90% 0.75 0.87 5.50% 0.47 0.77

5) 0.30% 0.76 0.95 0.80% 0.22 0.06 0.90% 0.75 0.87 4.80% 0.77 0.54

6) 0.30% 0.76 0.95 0.70% 0.40 0.35 0.90% 0.75 0.87 5.20% 0.77 0.94

Table 4: Actual VaR exceedances N/T , Kupiec’s and Christoffersen’s

tests for the portfolio consisting of thirty Dow Jones stocks (Short

positions).

1st International R/Rmetrics User and Developer Workshop 81

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Conclusions

• Introduction of the dynamic grouped-t copula for the joint

modelling of high-dimensional portfolios, where we use the DCC

model to specify the time evolution of the correlation matrix of

the grouped-t copula.

• Consistency and asymptotic normality of the estimator under the

special case of a correlation matrix equal to the identity matrix.

• Monte Carlo simulations to study the properties of this estimator

under different data generating processes where such a strong

restriction on the correlation matrix does not hold.

• We investigated the effects of such biases and finite sample

properties on conditional quantile estimation, given the

increasing importance of the Value-at-Risk as risk measure. We

found that the error in the approximation of the quantile can

range between 0 and 3%.

1st International R/Rmetrics User and Developer Workshop 82

Empirical Applications - Market Risk Management for

Multivariate Portfolios: Conclusions

• Empirical analysis 1: When long positions were of concern, we

found that the dynamic grouped-T copula (together with

skewed-t marginals) outperformed both the constant grouped-t

copula and the dynamic student’s T copula as well as the

dynamic multivariate normal model proposed in Engle (2002).

• Empirical analysis 2: As for short positions, we found out that a

multivariate normal model with dynamic normal marginals and

constant normal copula was already a proper choice. This last

result confirms previous evidence in Junker and May (2005) and

Fantazzini (2007) for bivariate portfolios.

• Avenue for future research 1: more sophisticated methods to

separate the assets into homogenous groups when using the

grouped-t copula.

• Avenue for future research 2: look for alternatives to DCC

modelling

1st International R/Rmetrics User and Developer Workshop 83

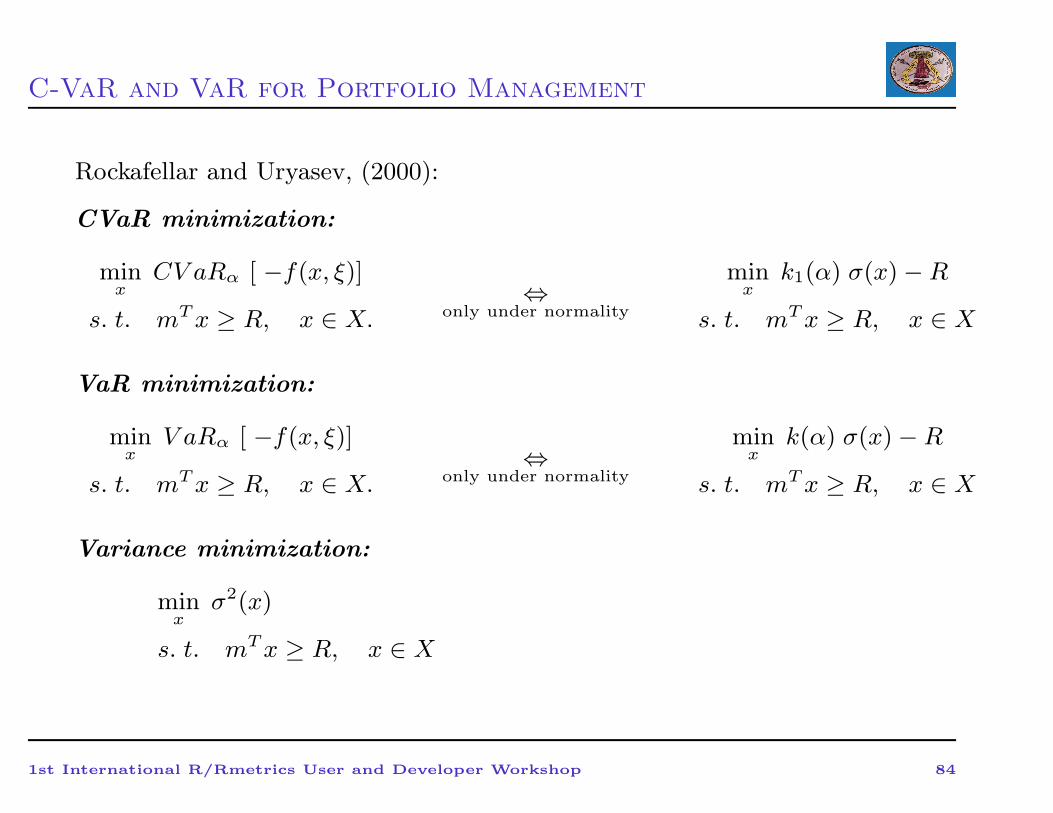

C-VaR and VaR for Portfolio Management

Rockafellar and Uryasev, (2000):

CVaR minimization:

minx

CV aRα [ −f(x, ξ)]

s. t. mTx ≥ R, x ∈ X.⇔

only under normality

minx

k1(α) σ(x) −R

s. t. mTx ≥ R, x ∈ X

VaR minimization:

minx

V aRα [ −f(x, ξ)]

s. t. mTx ≥ R, x ∈ X.⇔

only under normality

minx

k(α) σ(x) −R

s. t. mTx ≥ R, x ∈ X

Variance minimization:

minx

σ2(x)

s. t. mTx ≥ R, x ∈ X

1st International R/Rmetrics User and Developer Workshop 84

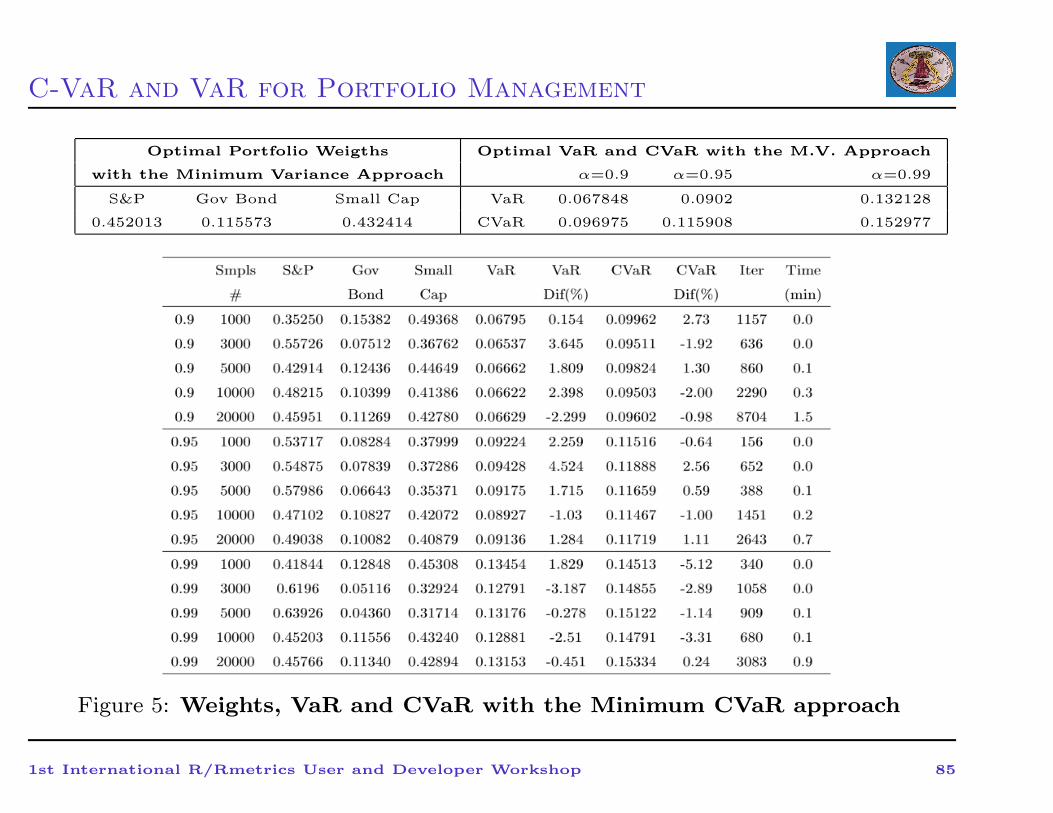

C-VaR and VaR for Portfolio Management

Optimal Portfolio Weigths Optimal VaR and CVaR with the M.V. Approach

with the Minimum Variance Approach α=0.9 α=0.95 α=0.99

S&P Gov Bond Small Cap VaR 0.067848 0.0902 0.132128

0.452013 0.115573 0.432414 CVaR 0.096975 0.115908 0.152977

Figure 5: Weights, VaR and CVaR with the Minimum CVaR approach

1st International R/Rmetrics User and Developer Workshop 85

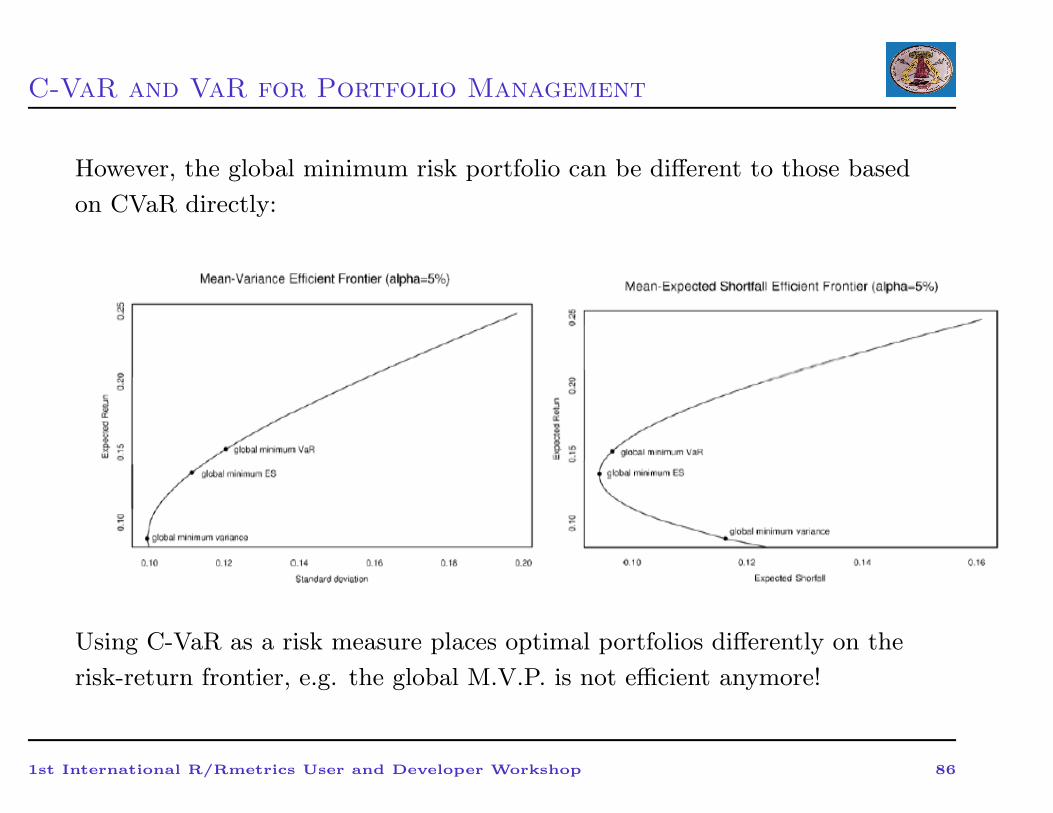

C-VaR and VaR for Portfolio Management

However, the global minimum risk portfolio can be different to those based

on CVaR directly:

Using C-VaR as a risk measure places optimal portfolios differently on the

risk-return frontier, e.g. the global M.V.P. is not efficient anymore!

1st International R/Rmetrics User and Developer Workshop 86