risk aggregation under dependence uncertaintyembrecht/ftp/ra_du.pdfframework var and es bounds...

TRANSCRIPT

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Risk Aggregation under Dependence

UncertaintyChallenges in Theory and Practice

Paul Embrechts

RiskLab, Department of Mathematics, ETH Zurich

Senior SFI Professor

www.math.ethz.ch/˜embrechts/

Paul Embrechts Risk Aggregation 1/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Outline

1 Framework

2 VaR and ES Bounds

3 Asymptotic Equivalence

4 Challenges

5 References

Paul Embrechts Risk Aggregation 2/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Fundamental problem in Finance/Insurance

Risk factors: X = (X1, . . . ,Xd)

Model assumption: Xi ∼ Fi, Fi known, i = 1, . . . , d

A financial position Ψ(X)

A risk measure/pricing function: ρ(Ψ(X))

Calculate ρ(Ψ(X))

Paul Embrechts Risk Aggregation 3/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Calculating ρ(Ψ(X))

Example:

Ψ(X) =∑d

i=1 Xi

ρ = VaRp or ρ = ESp

Challenge:

We need a joint model for the random vector X

Joint models are hard to get by

We will focus on the above special choices of Ψ and ρ.

Paul Embrechts Risk Aggregation 4/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

VaR and ES

VaRp(X)

For p ∈ (0, 1),

VaRp(X) = F−1X (p) = inf{x ∈ R : FX(x) ≥ p}

ESp(X)

For p ∈ (0, 1),

ESp(X) =1

1− p

∫ 1

pVaRq(X)dq =

(F cont.)E[X|X > VaRp(X)

]

Paul Embrechts Risk Aggregation 5/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

VaR and ES

A related quantity Left-tail-ES:

LESp(X)

For p ∈ (0, 1),

LESp(X) =1p

∫ p

0VaRq(X)dq = −ES1−p(−X)

Paul Embrechts Risk Aggregation 6/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Frechet problem

Denote

Sd = Sd(F1, . . . ,Fd) =

{d∑

i=1

Xi : Xi ∼ Fi, i = 1, . . . , d

}

Every element in Sd is a possible risk position.

Determination of Sd: very challenging.

Think about S2(U[0, 1],U[0, 1]) ... open question!

Paul Embrechts Risk Aggregation 7/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Worst- and best-values of VaR and ES

The Frechet (unconstrained) problems for VaRp

VaRp(Sd) = sup{VaRp(S) : S ∈ Sd(F1, . . . ,Fd)},

VaRp(Sd) = inf{VaRp(S) : S ∈ Sd(F1, . . . ,Fd)}.

Same notation for ESp and LESp.

Paul Embrechts Risk Aggregation 8/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Worst- and best-values of VaR and ES

ES is subadditive:

ESp(Sd) =

d∑i=1

ESp(Xi).

Similarly LESp(Sd) =∑d

i=1 LESp(Xi).

VaRp(Sd), VaRp(Sd) and ESp(Sd): generally open questions

Challenge for ESp(Sd)

To calculate ESp(Sd) one naturally seeks a safest risk in Sd.

Paul Embrechts Risk Aggregation 9/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Mathematical difficulty

Common understanding of the most dangerous scenario:

Comonotonicity - well accepted notion

Understanding concerning the safest scenario:

d = 2: counter-monotonicity

d ≥ 3: question mark! (?!)

Calls for notions of extremal negative dependence.

Paul Embrechts Risk Aggregation 10/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Mathematical difficulty

ES respects convex order: the natural order of risk preference.

Convex orderWe write X ≤cx Y if E[f (X)] ≤ E[f (Y)] for all convex functions fsuch that the two expectations exist.

Finding ESp(Sd)

Search for a smallest element in Sd with respect to convex

order, if it exists.

Paul Embrechts Risk Aggregation 11/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Mathematical difficulty

VaR does not respect convex order: more tricky

Good news: the questions for VaRp(Sd), VaRp(Sd) and

ESp(Sd) are mathematically similar.

Finding VaRp(Sd)

Search for a smallest element in Sd(F1, . . . , Fd) with respect to

convex order, where Fi is the p-tail-conditional distribution of

Fi.

VaRp(Sd) is symmetric to VaRp(Sd).

Paul Embrechts Risk Aggregation 12/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Summary of existing results

d = 2:

fully solved analytically

d ≥ 3:

Homogeneous model (F1 = · · · = Fd)

ESp(Sd) solved analytically for decreasing densities, e.g.Pareto, ExponentialVaRp(Sd) solved analytically for tail-decreasing densities,e.g. Pareto, Gamma, Log-normal

Inhomogeneous model

Few analytical results: current research

Numerical methods available: Rearrangement Algorithm

Paul Embrechts Risk Aggregation 13/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

VaR bounds

d = 2, Makarov (1981) and Ruschendorf (1982)

For any p ∈ (0, 1),

VaRp(S2) = infx∈[0,1−p]

{F−11 (p + x) + F−1

2 (1− x)},

and

VaRp(S2) = supx∈[0,p]

{F−11 (x) + F−1

2 (p− x)}.

A large outcome is coupled with a small outcome.

Paul Embrechts Risk Aggregation 14/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

VaR bounds - homogeneous model

Sharp VaR bounds (Wang, Peng and Yang, 2013)

Suppose that the density function of F is decreasing on [b,∞)

for some b ∈ R. Then, for p ∈ [F(b), 1), and X d∼ F,

VaRp(Sd) = dE[X|X ∈ [F−1(p + (d− 1)c),F−1(1− c)]],

where c is the smallest number in [0, 1d(1− p)] such that

∫ 1−cp+(d−1)c F−1(t)dt ≥ 1−p−dc

d ((d− 1)F−1(p + (d− 1)c) + F−1(1− c)).

Red part clearly has an ES-type form.

c = 0: VaRp(Sd) = ESp(Sd).

Paul Embrechts Risk Aggregation 15/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

VaR bounds - homogeneous model

Sharp VaR bounds II

Suppose that the density function of F is decreasing on its

support. Then for p ∈ (0, 1) and X d∼ F,

VaRp(Sd) = max{(d− 1)F−1(0) + F−1(p), dE[X|X ≤ F−1(p)]}.

Red part has an LES form.

Paul Embrechts Risk Aggregation 16/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

ES bounds - homogeneous model

Sharp ES bounds (Bernard, Jiang and Wang, 2014)

Suppose that the density function of F is decreasing on its

support. Then for p ∈ (1− dc, 1), q = (1− p)/d and X d∼ F,

ESp(Sd) =1q

∫ q

0

((d− 1)F−1((d− 1)t) + F−1(1− t)

)dt,

= (d− 1)2LES(d−1)q(X) + ES1−q(X),

where c is the smallest number in [0, 1d ] such that

∫ 1−c(d−1)c F−1(t)dt ≥ 1−dc

d ((d− 1)F−1((d− 1)c) + F−1(1− c)).

One large outcome is coupled with d− 1 small outcomes.

Paul Embrechts Risk Aggregation 17/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Complete mixability

The homogeneous VaR and ES bounds are based on the notion

of complete mixability:

Complete mixability, Wang and Wang (2011)

A distribution function F on R is called d-completely mixable

(d-CM) if there exist d random variables X1, . . . ,Xd ∼ F such

that

P(X1 + · · ·+ Xd = dk) = 1,

for some k ∈ R.

Equivalently, Sd(F, . . . ,F) contains a constant.

Paul Embrechts Risk Aggregation 18/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Complete mixability

Some examples of d-CM distributions for all d ≥ 2:

Normal, Student t, Cauchy, Uniform.

Most relevant result: F has a monotone density on a finiteinterval with a mean condition (depends on d) is d-CM.

Examples: (truncated) Pareto, Gamma, Log-normal.

Inhomogeneous version called joint mixability.

A full characterization of these classses is at the moment is

widely open.

Paul Embrechts Risk Aggregation 19/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Numerical calculation

Rearrangement Algorithm (RA): Embrecths, Puccetti and

Ruschendorf (2013).

A fast numerical procedure

Based on the CM-idea

Discretization of relevant quantile regions

d possibly large

Applicable to VaRp, VaRp and ESp

Paul Embrechts Risk Aggregation 20/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

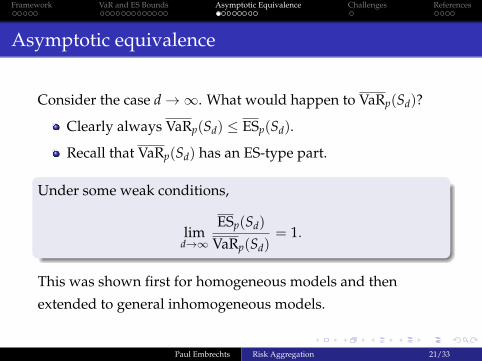

Asymptotic equivalence

Consider the case d→∞. What would happen to VaRp(Sd)?

Clearly always VaRp(Sd) ≤ ESp(Sd).

Recall that VaRp(Sd) has an ES-type part.

Under some weak conditions,

limd→∞

ESp(Sd)

VaRp(Sd)= 1.

This was shown first for homogeneous models and then

extended to general inhomogeneous models.

Paul Embrechts Risk Aggregation 21/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Asymptotic equivalence - homogeneous model

Theorem 1In the homogeneous model, F1 = F2 = · · · = F, for p ∈ (0, 1) andX ∼ F, we have that

limd→∞

1d

VaRp(Sd) = ESp(X).

Similar limits hold for a large class of risk measures

Paul Embrechts Risk Aggregation 22/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Asymptotic equivalence - worst-cases

Theorem 2 (Embrechts, Wang and Wang, 2014)

Suppose the continuous distributions Fi, i ∈ N satisfy that forXi ∼ Fi and some p ∈ (0, 1),

(i) E[|Xi − E[Xi]|k] is uniformly bounded for some k > 1;

(ii) lim infd→∞

1d

d∑i=1

ESp(Xi) > 0.

Then as d→∞,

ESp(Sd)

VaRp(Sd)= 1 + O(d1/k−1).

Paul Embrechts Risk Aggregation 23/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Asymptotic equivalence - best-cases

Similar results holds for VaRp and ESp: assume (i) and

(iii) lim infd→∞

1d

d∑i=1

LESp(Xi) > 0,

then

limd→∞

VaRp(Sd)

LESp(Sd)= 1,

limd→∞

ESp(Sd)∑di=1 E[Xi]

= 1,

andVaRp(Sd)

ESp(Sd)≈∑d

i=1 LESp(Xi)∑di=1 E[Xi]

≤ 1, d→∞.

Paul Embrechts Risk Aggregation 24/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Example: Pareto(2) risks

Bounds on VaR and ES for the sum of d Pareto(2) distributed rvs forp = 0.999; VaR+

p corresponds to the comonotonic case.

d = 8 d = 56

VaRp 31 53

ESp 178 472

VaR+p 245 1715

VaRp 465 3454

ESp 498 3486

VaRp/VaR+p 1.898 2.014

ESp/VaRp 1.071 1.009

Paul Embrechts Risk Aggregation 25/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Example: Pareto(θ) risks

Bounds on the VaR and ES for the sum of d = 8

Pareto(θ)-distributed rvs for p = 0.999.

θ = 1.5 θ = 2 θ = 3 θ = 5 θ = 10

VaRp 1897 465 110 31.65 9.72

ESp 2392 498 112 31.81 9.73

ESp/VaRp 1.261 1.071 1.018 1.005 1.001

Paul Embrechts Risk Aggregation 26/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Dependence-uncertainty spread

Theorem 3 (Embrechts, Wang and Wang, 2014)

Take 1 > q ≥ p > 0. Suppose that the continuous distributionsFi, i ∈ N, satisfy (i) and (iii), and lim supd→∞

∑di=1 E[Xi]∑d

i=1 ESp(Xi)< 1, then

lim infd→∞

VaRq(Sd)− VaRq(Sd)

ESp(Sd)− ESp(Sd)≥ 1.

The uncertainty spread of VaR is generally bigger than that

of ES.

In recent Consultative Documents of the Basel Committee,

VaR0.99 is compared with ES0.975: p = 0.975 and q = 0.99.

Paul Embrechts Risk Aggregation 27/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

Dependence-uncertainty spread

ES and VaR of Sd = X1 + · · ·+ Xd, where

Xi ∼ Pareto(2 + 0.1i), i = 1, . . . , 5;

Xi ∼ Exp(i− 5), i = 6, . . . , 10;

Xi ∼ Log–Normal(0, (0.1(i− 10))2), i = 11, . . . , 20.

d = 5 d = 20best worst spread best worst spread

ES0.975 22.48 44.88 22.40 29.15 102.35 73.20VaR0.975 9.79 41.46 31.67 21.44 100.65 79.21VaR0.9875 12.06 56.21 44.16 22.12 126.63 104.51VaR0.99 12.96 62.01 49.05 22.29 136.30 114.01

ES0.975

VaR0.9751.08 1.02

Paul Embrechts Risk Aggregation 28/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

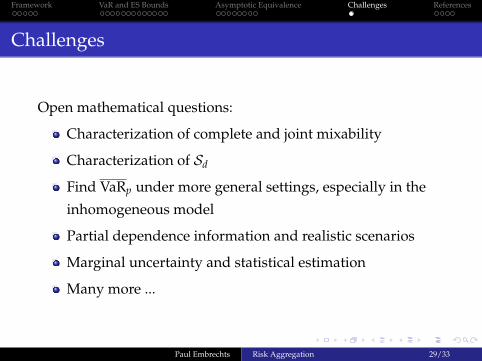

Challenges

Open mathematical questions:

Characterization of complete and joint mixability

Characterization of Sd

Find VaRp under more general settings, especially in the

inhomogeneous model

Partial dependence information and realistic scenarios

Marginal uncertainty and statistical estimation

Many more ...

Paul Embrechts Risk Aggregation 29/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

References I

Bernard, C., X. Jiang, and R. Wang (2014). Risk aggregation

with dependence uncertainty. Insurance: Mathematics andEconomics, 54(1), 93–108.

Embrechts, P., G. Puccetti, and L. Ruschendorf (2013).

Model uncertainty and VaR aggregation. Journal of Bankingand Finance, 37(8), 2750–2764.

Embrechts, P., G. Puccetti, L. Ruschendorf, R. Wang, and A.

Beleraj (2014). An academic response to Basel 3.5. Risks,

2(1), 25–48.

Paul Embrechts Risk Aggregation 30/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

References II

Embrechts, P., B. Wang, and R. Wang (2014).

Aggregation-robustness and model uncertainty of

regulatory risk measures. Preprint, ETH Zurich.

Makarov, G.D. (1981). Estimates for the distribution

function of the sum of two random variables with given

marginal distributions. Theory of Probability and itsApplications, 26, 803–806.

Ruschendorf, L. (1982). Random variables with maximum

sums. Advances in Applied Probability, 14(3), 623–632.

Paul Embrechts Risk Aggregation 31/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

References III

Wang, B. and R. Wang (2011). The complete mixability and

convex minimization problems with monotone marginal

densities. Journal of Multivariate Analysis 102(10), 1344–1360.

Wang, R., L. Peng, and J. Yang (2013). Bounds for the sum

of dependent risks and worst value-at-risk with monotone

marginal densities. Finance and Stochastics 17(2), 395–417.

Paul Embrechts Risk Aggregation 32/33

Framework VaR and ES Bounds Asymptotic Equivalence Challenges References

THANK YOU!

Paul Embrechts Risk Aggregation 33/33