rich dad-poor-dad-presentation

TRANSCRIPT

GETTING STARTED

Represented by,• BINDU• LOHIT• SUJIT

Rich Dad, Poor Dad

“Study hard, get good grades and find a high paying job with good benefits” is advice from a previous era.

“Network Marketing is the Perfect Business…

The richest people in the world look for and build networks everyone else looks for work”

Robert Kiyosaki,

Author Rich Dad Poor Dad

Introduction

Robert Kiyosaki, is a multi billionaire by all standards

The book basically is about what people must learn and practice in order to become financially independent. The book talks about two different points of view about attaining financial independence (Rich dad Vs. Poor dad)

His poor dad (his biological father), was a PhD holder who worked for Government, but never really attained financial independence, while his rich dad (his friend’s father) did not graduate from high school, but later became a very rich man

Parents’ advice of getting good grades and jobs will not necessarily lead to financial independence, because schools do not equip kids with the information needed to ensure financial independence

Lesson 1 – The rich don’t work for money

Don’t work for money i.e. don’t depend on your boss to make you rich

Learn how to make money work for you by cutting your expenses moderately, investing wisely and creating opportunities to earn passive incomes outside of salaries

Seek to be a business owner and/or an investor, rather than an employee

Lesson 1 – The rich don’t work for money

Avoiding the trap– fear and greed– The rat race - work to spend and spend to have– a job is a short term solution to a long term

problem– The poor and middle class believe that money

is real and that the company or government will look after them.

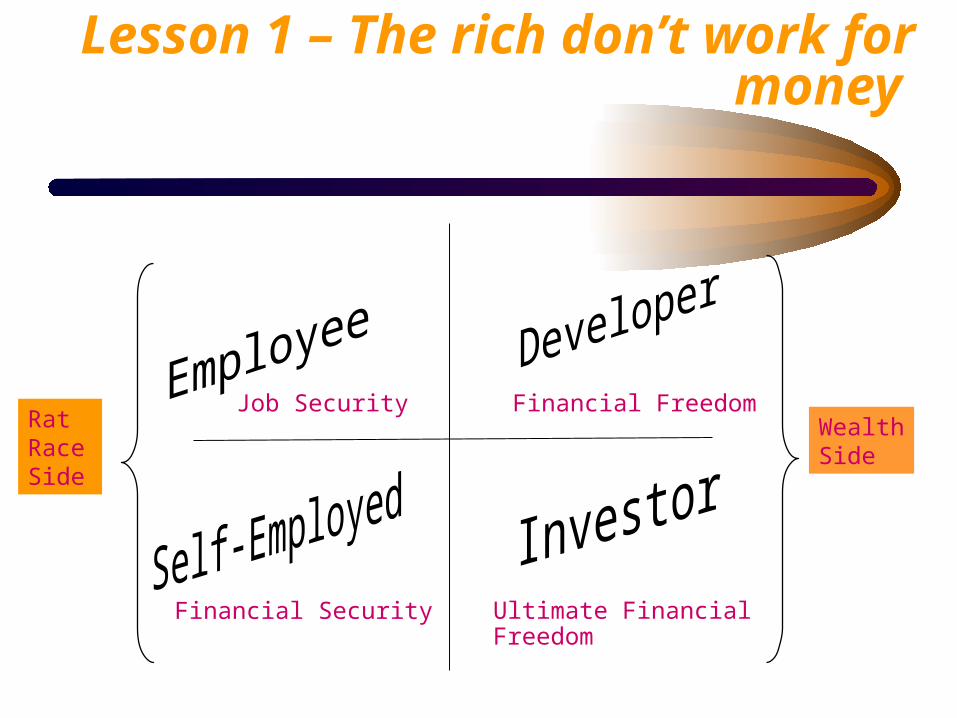

Lesson 1 – The rich don’t work for money

Job Security

Financial Security

Financial Freedom

Ultimate Financial Freedom

WealthSide

RatRaceSide

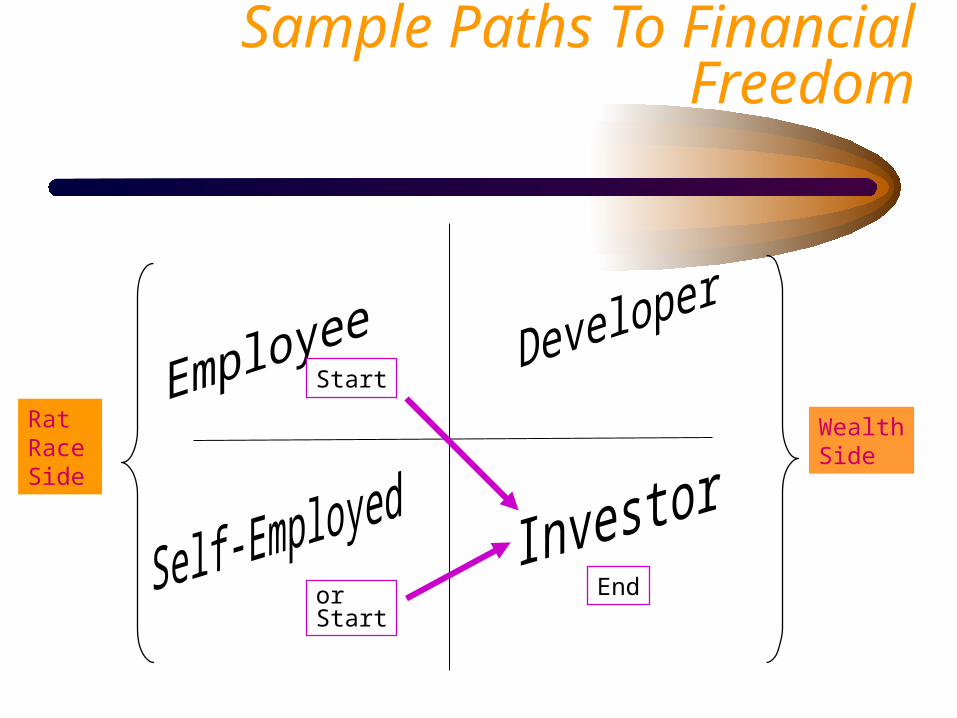

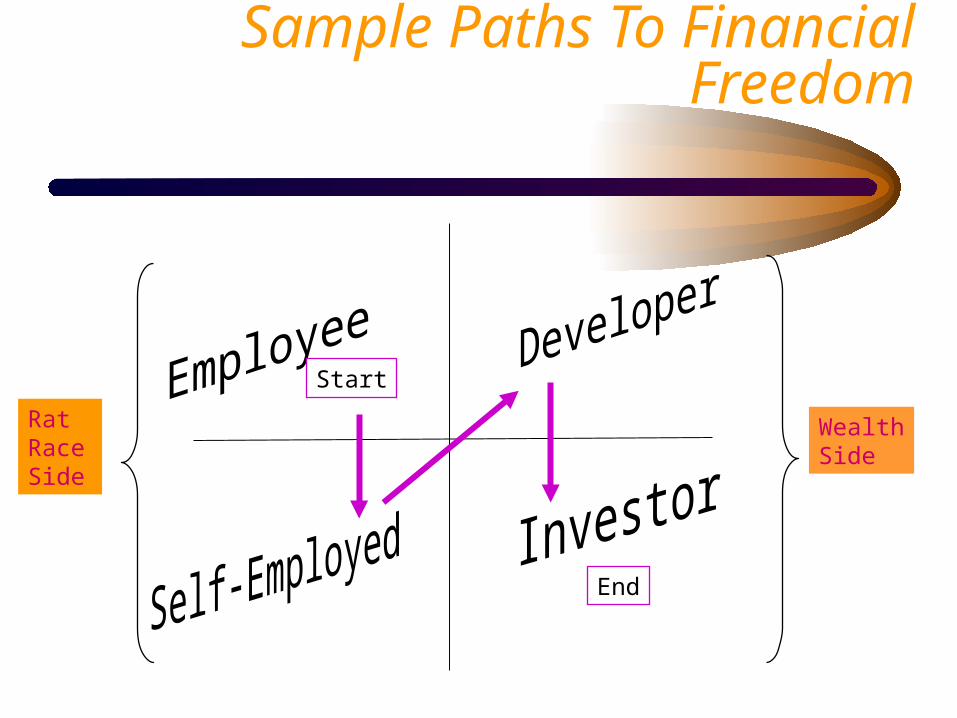

Sample Paths To Financial Freedom

WealthSide

RatRaceSide

Start

EndorStart

Sample Paths To Financial Freedom

WealthSide

RatRaceSide

Start

End

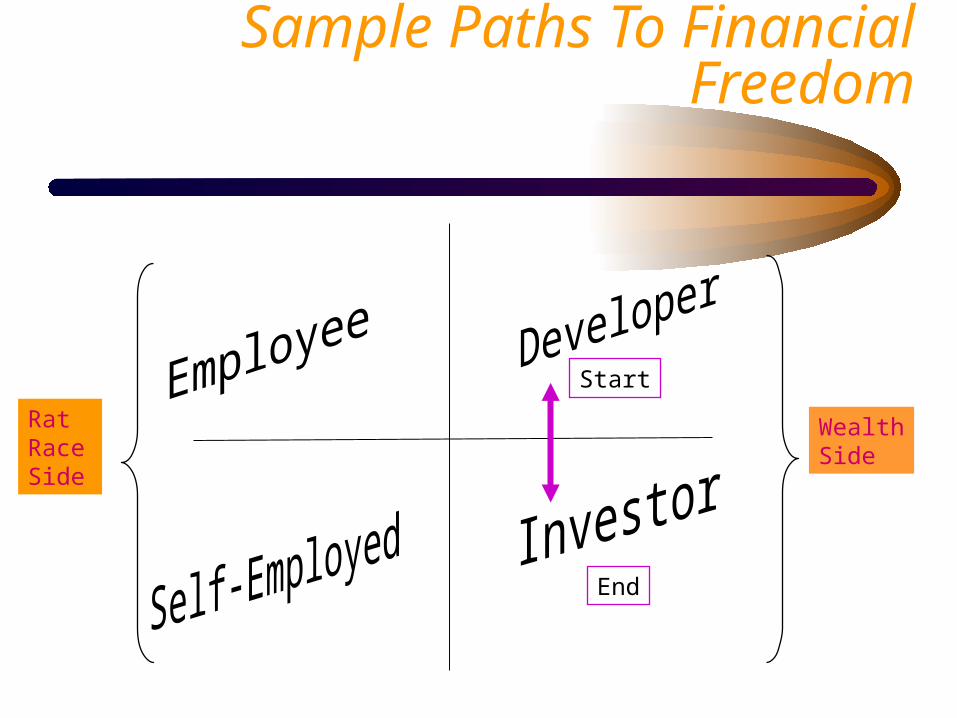

Sample Paths To Financial Freedom

WealthSide

RatRaceSide

Start

End

Lesson 2 – Master Financial Literacy

Financial intelligence equips you with the what is required to make money that will last for generations, while money without financial intelligence is soon gone

Financial literacy teaches that it does not matter how much money you make, but how much money you keep

It also teaches that Investments can be made at each income level and if you invest today you will guarantee your financial future

Differentiate between an asset and liability, and invest in assets

Assets generate income, while liabilities generate expenses; i.e. your GSM mobile phone could be an asset or liability depending on what it is used for

Financial IntelligenceRich Dad. Poor Dad’s Basic Philosophy

• Know the difference between an ASSET and a LIABILITY, and only buy assets.– A True Asset gives a positive cash flow each and

every month.• Live below your means, while constantly

increasing your means.• Make your PASSIVE INCOME cover your

Lifestyle Expenses forever.

Financial Literacy

• Sadly, most of us have been taught to read words and books, but not numbers and financial statements.

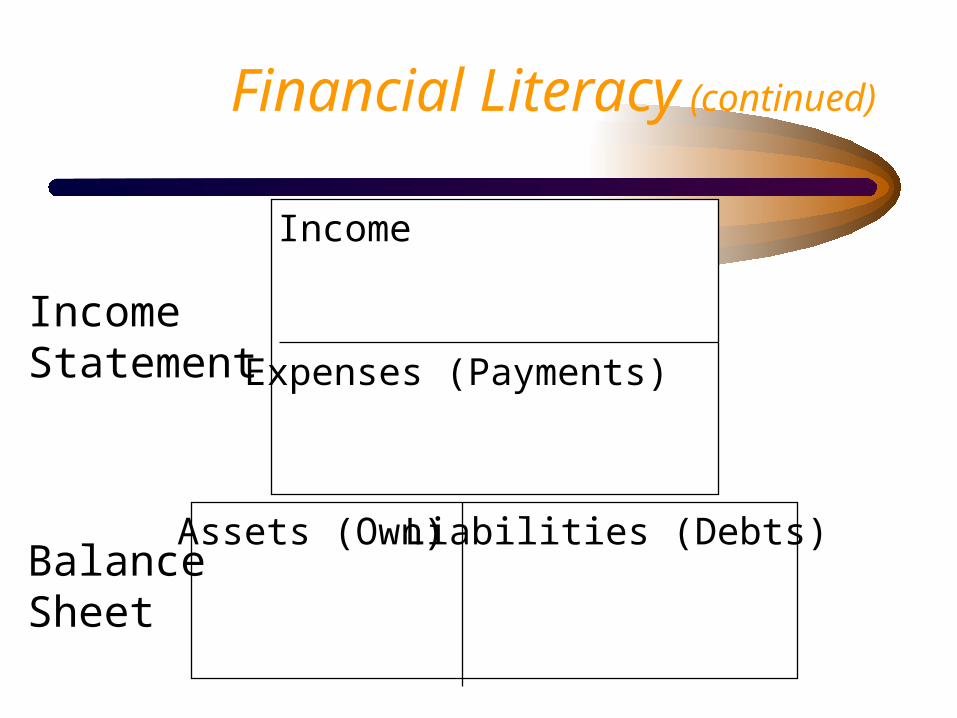

• Two key personal and business financial statements we all must be able to read.– The Income Statement shows the amount of

money coming in and going out.– The Balance Sheet shows the balance of what

you own and what you owe.

Income Statement

BalanceSheet

Income

Expenses (Payments)

Assets (Own) Liabilities (Debts)

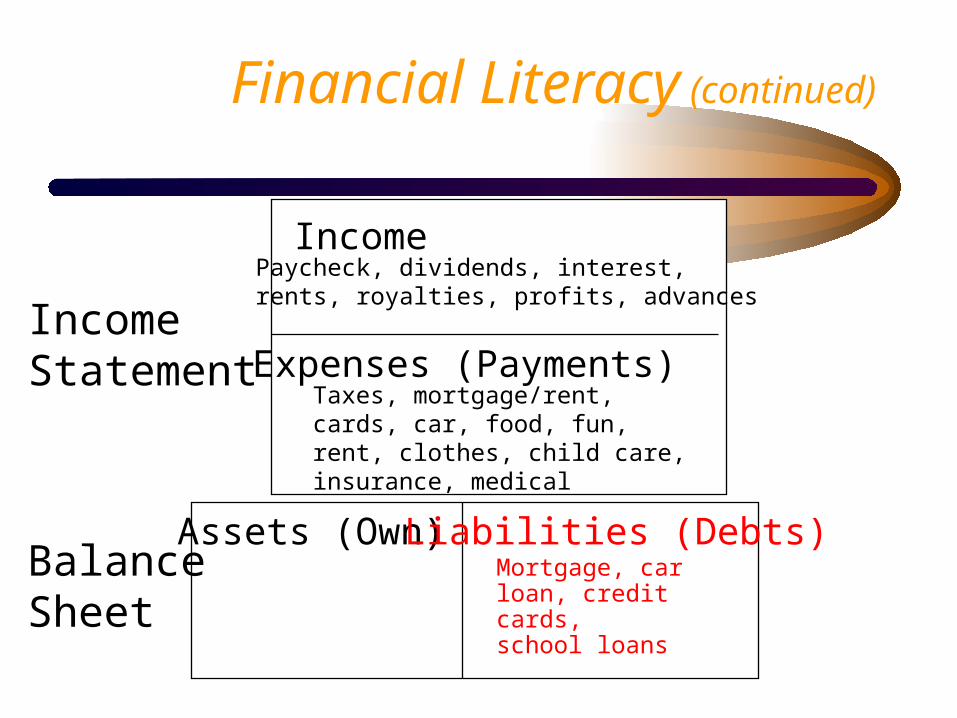

Financial Literacy (continued)

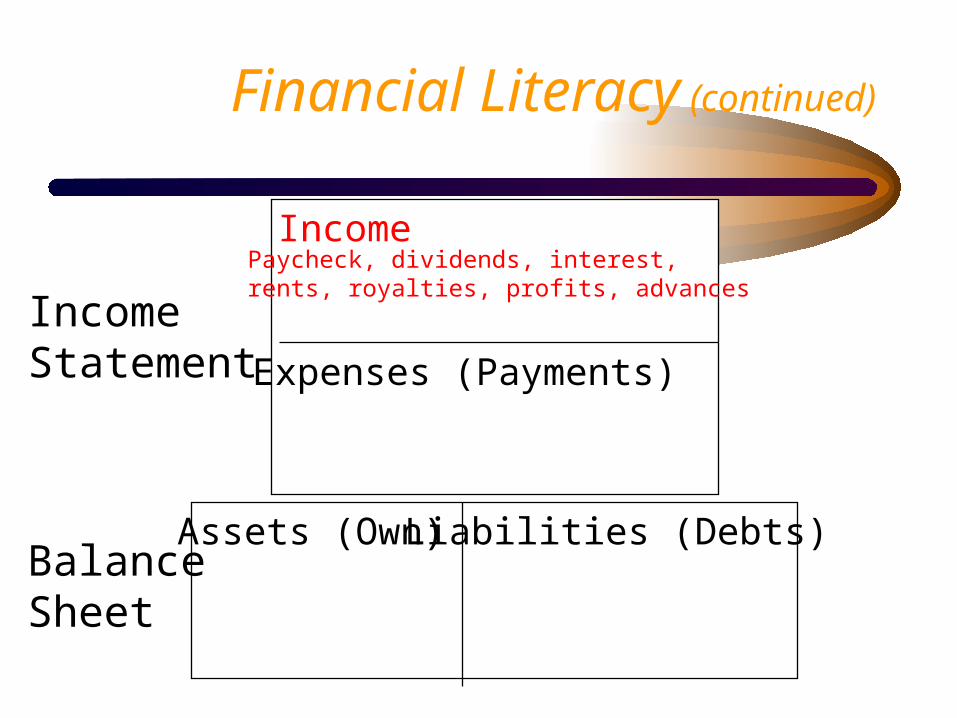

Income Statement

BalanceSheet

Income

Expenses (Payments)

Assets (Own) Liabilities (Debts)

Paycheck, dividends, interest,rents, royalties, profits, advances

Financial Literacy (continued)

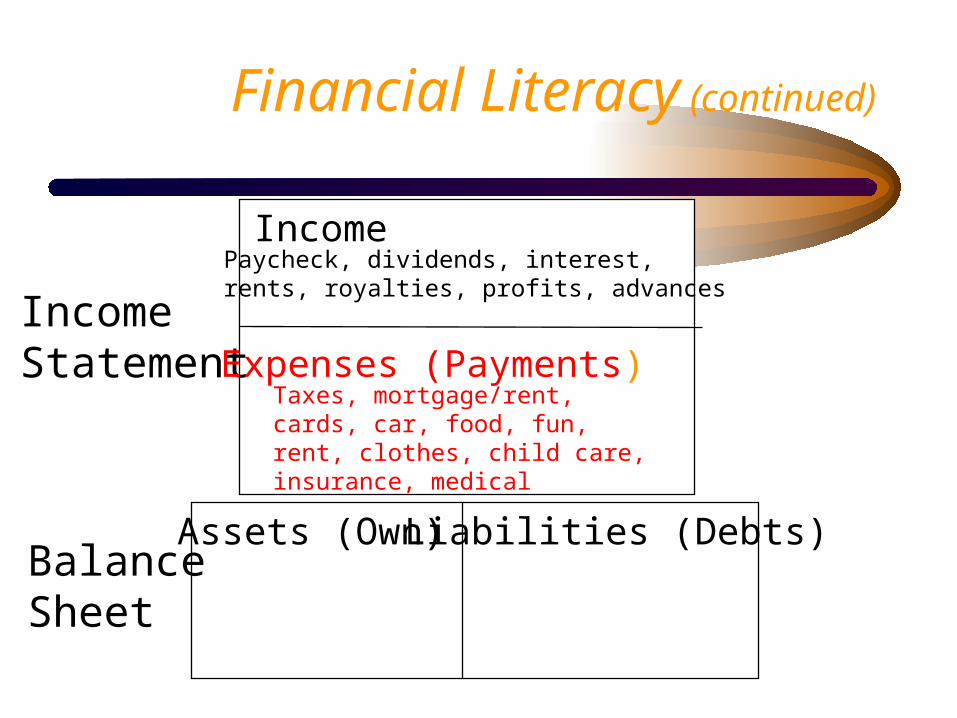

Income Statement

BalanceSheet

Income

Expenses (Payments)

Assets (Own) Liabilities (Debts)

Taxes, mortgage/rent, cards, car, food, fun, rent, clothes, child care, insurance, medical

Paycheck, dividends, interest,rents, royalties, profits, advances

Financial Literacy (continued)

Income Statement

BalanceSheet

Income

Expenses (Payments)

Assets (Own) Liabilities (Debts)

Taxes, mortgage/rent, cards, car, food, fun, rent, clothes, child care, insurance, medical

Paycheck, dividends, interest,rents, royalties, profits, advances

Mortgage, car loan, credit cards, school loans

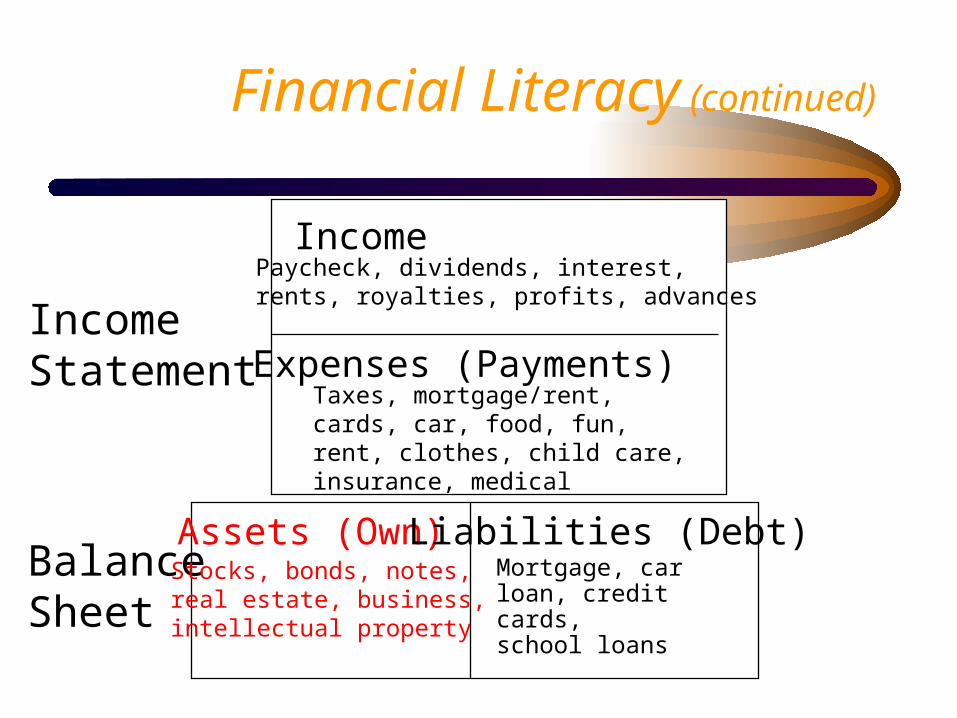

Financial Literacy (continued)

Income Statement

BalanceSheet

Income

Expenses (Payments)

Assets (Own) Liabilities (Debt)

Taxes, mortgage/rent, cards, car, food, fun, rent, clothes, child care, insurance, medical

Paycheck, dividends, interest,rents, royalties, profits, advances

Mortgage, car loan, credit cards, school loans

Stocks, bonds, notes,real estate, business, intellectual property

Financial Literacy (continued)

Income Statement

BalanceSheet

Income

Expenses

Assets = Zero Liabilities = Zero

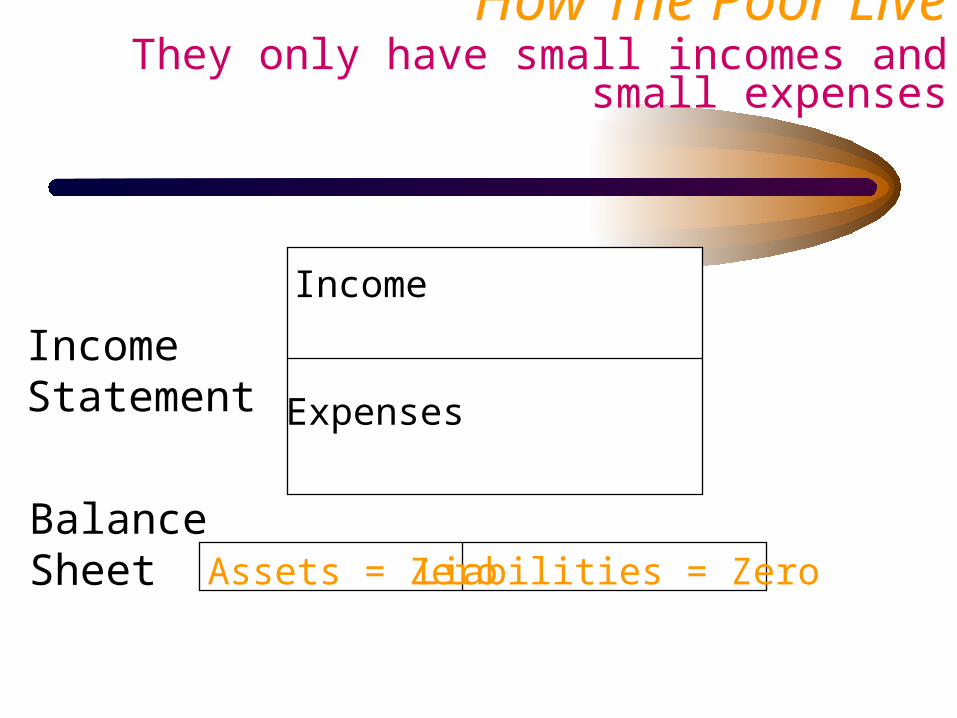

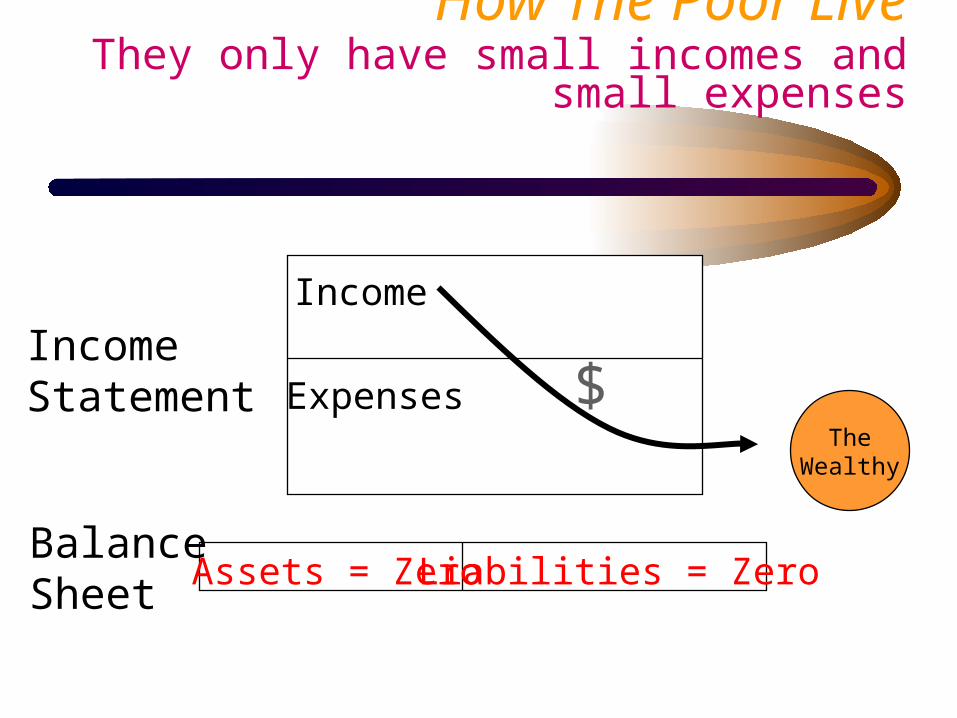

How The Poor Live They only have small incomes and small expenses

Income Statement

BalanceSheet

Income

Expenses

Assets = Zero Liabilities = Zero

How The Poor Live They only have small incomes and small expenses

$The

Wealthy

Income Statement

BalanceSheet

Income

Expenses

Assets

Liabilities

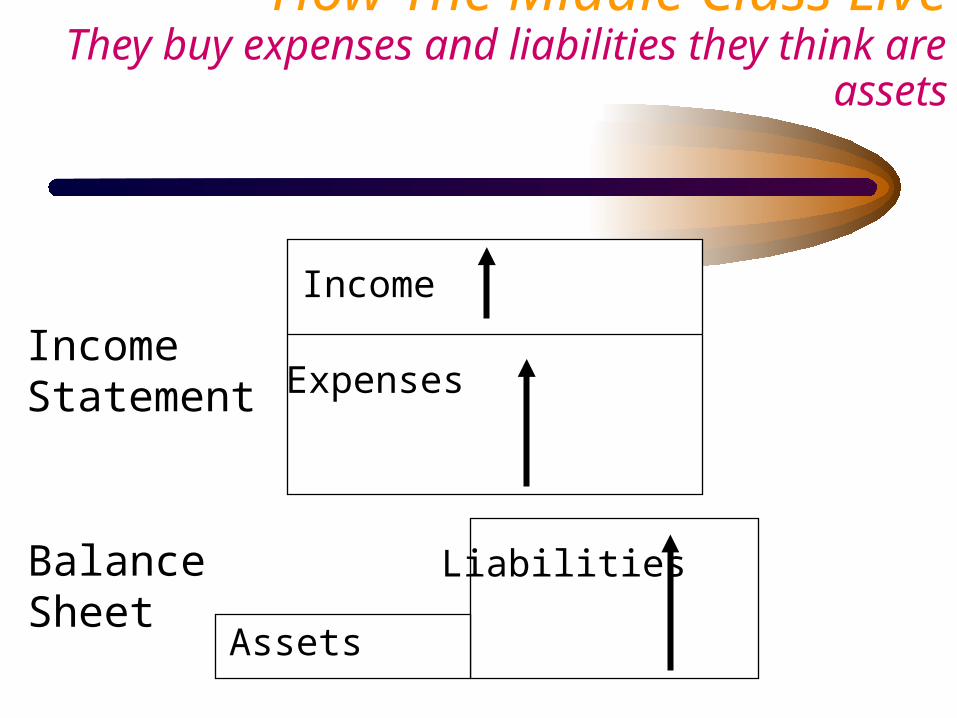

How The Middle Class LiveThey buy expenses and liabilities they think are assets

Assets

Income Statement

BalanceSheet

Income

Expenses

Assets

Liabilities

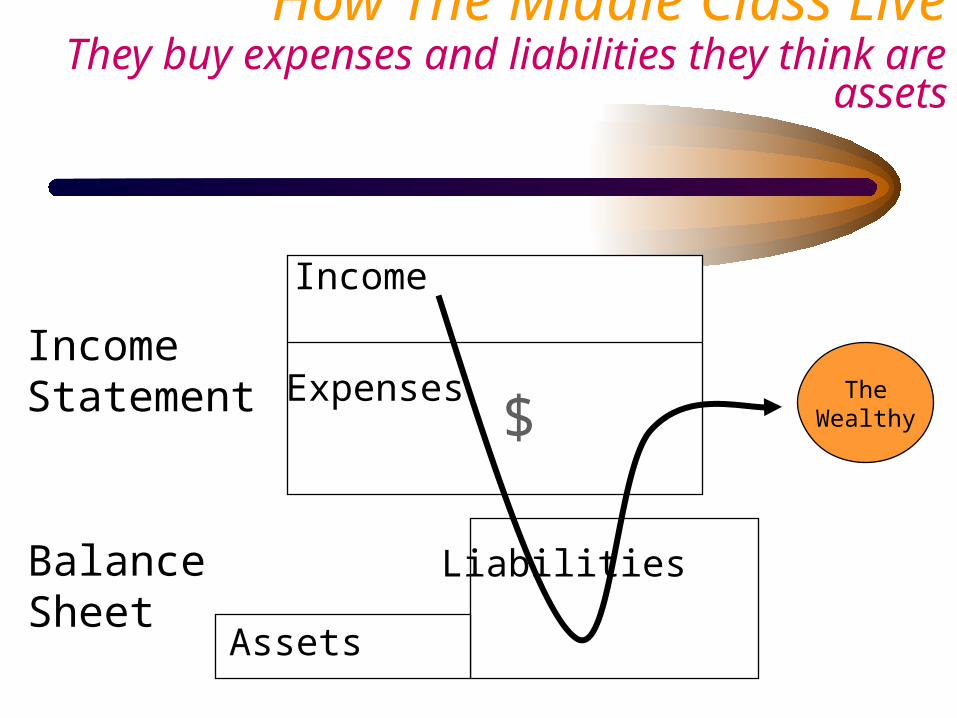

How The Middle Class Live They buy expenses and liabilities they think are assets

Assets

$The

Wealthy

Income Statement

BalanceSheet

Income

Expenses

Assets

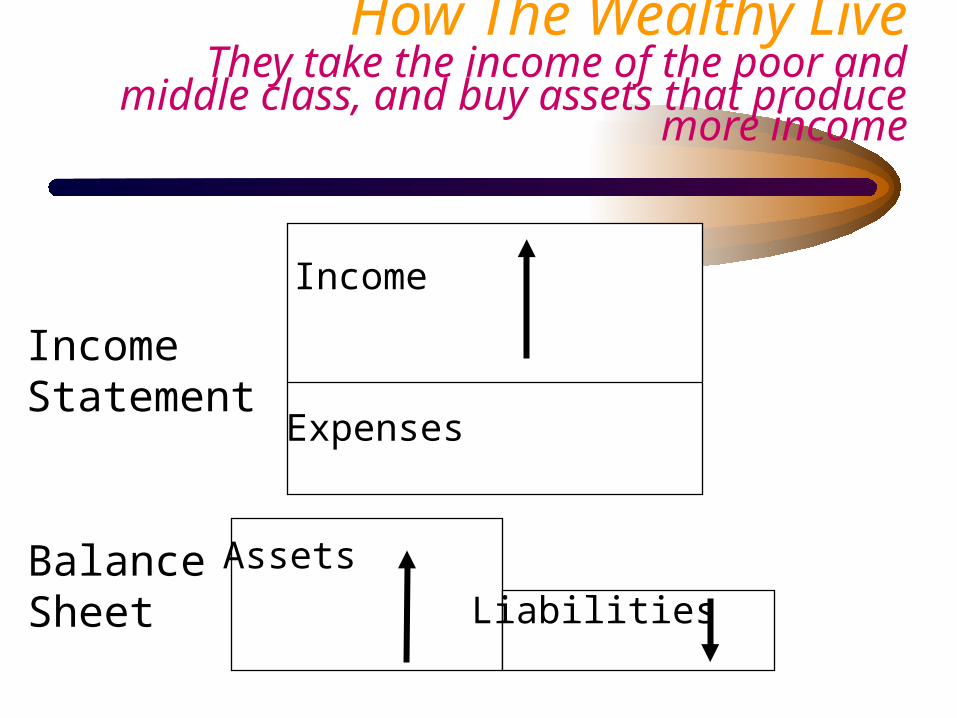

How The Wealthy Live They take the income of the poor and middle

class, and buy assets that produce more income

Liabilities

Income Statement

BalanceSheet

Income

Expenses

Assets

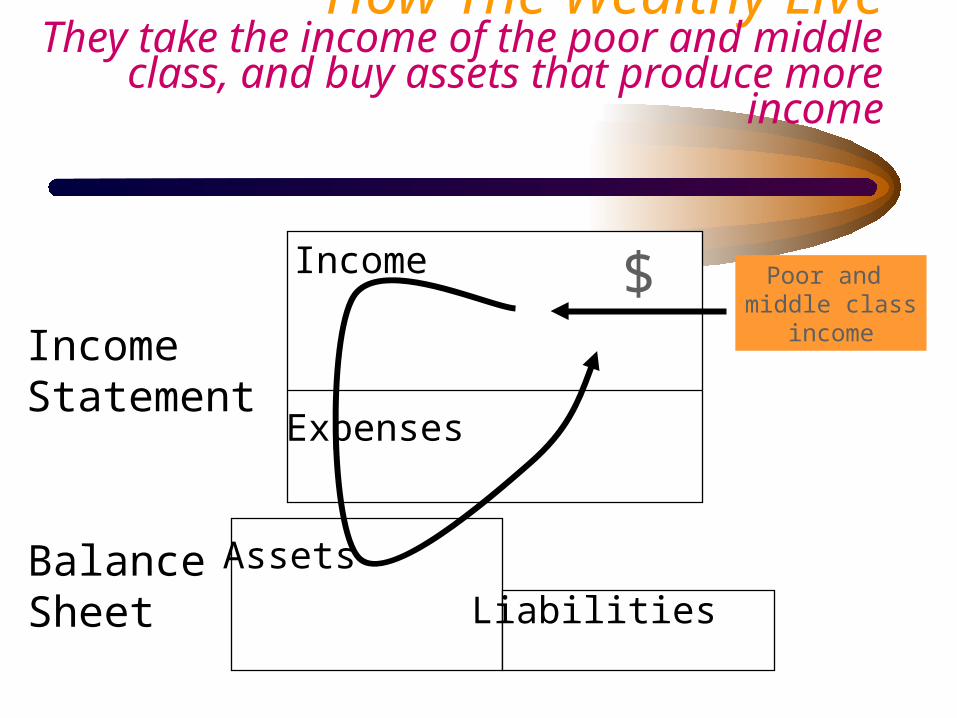

How The Wealthy LiveThey take the income of the poor and middle class,

and buy assets that produce more income

Liabilities

$ Poor and middle class

income

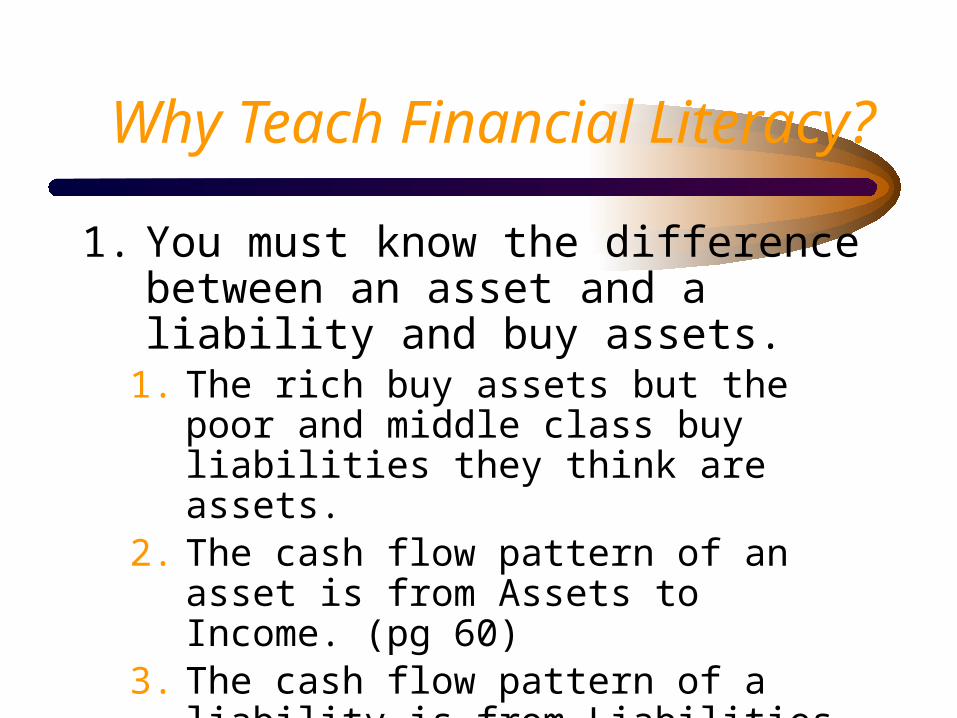

Why Teach Financial Literacy?

1. You must know the difference between an asset and a liability and buy assets.

1. The rich buy assets but the poor and middle class buy liabilities they think are assets.

2. The cash flow pattern of an asset is from Assets to Income. (pg 60)

3. The cash flow pattern of a liability is from Liabilities to Expense.

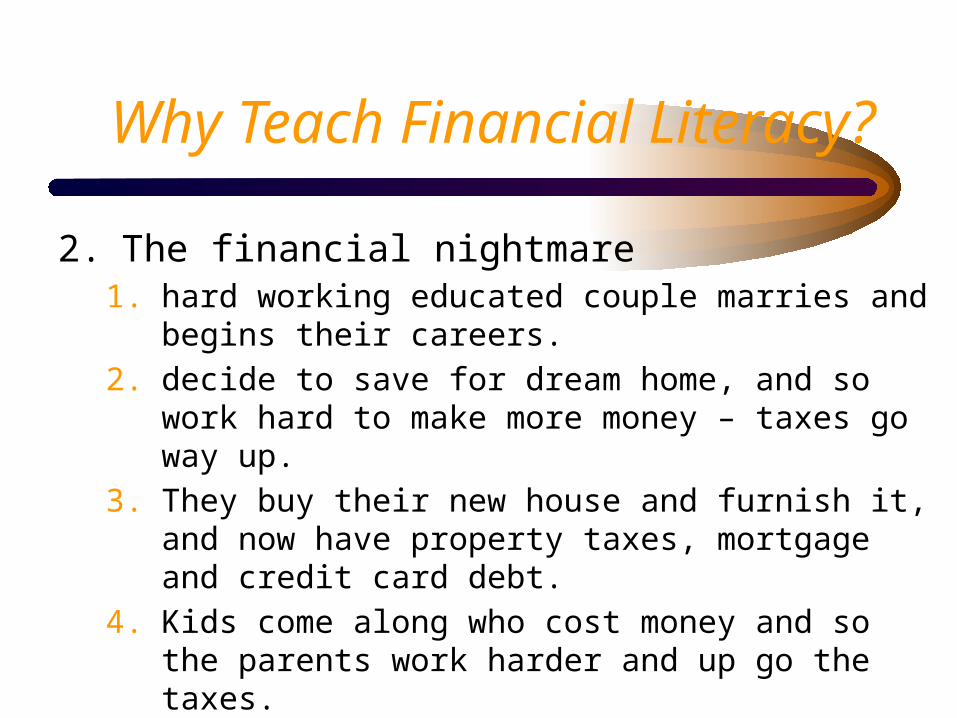

Why Teach Financial Literacy?

2. The financial nightmare1. hard working educated couple marries and begins their

careers.

2. decide to save for dream home, and so work hard to make more money – taxes go way up.

3. They buy their new house and furnish it, and now have property taxes, mortgage and credit card debt.

4. Kids come along who cost money and so the parents work harder and up go the taxes.

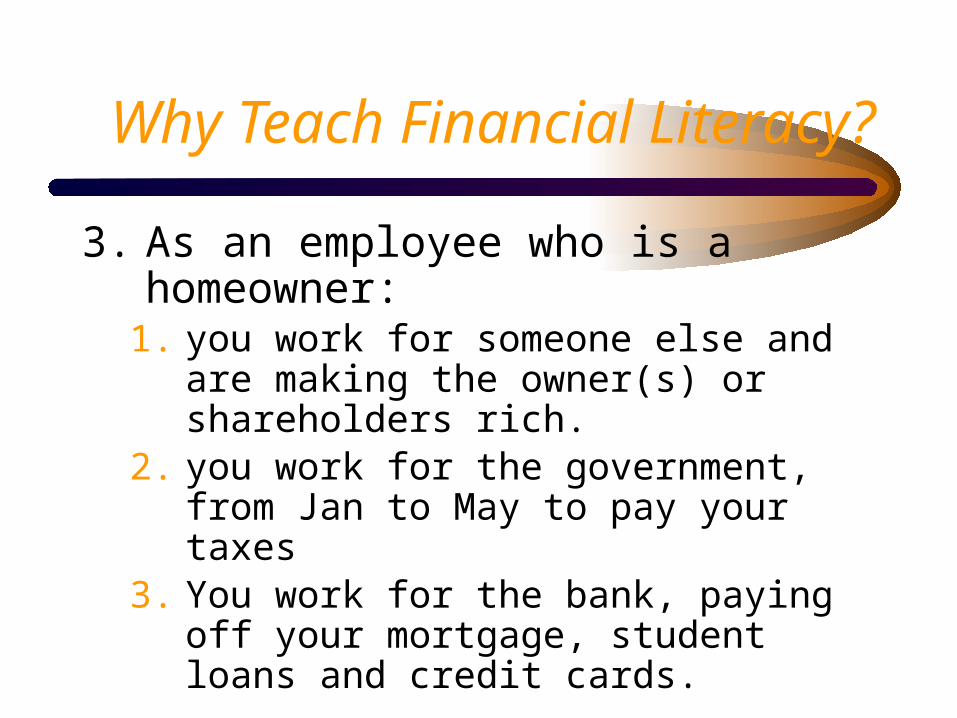

Why Teach Financial Literacy?

3. As an employee who is a homeowner:1. you work for someone else and are making

the owner(s) or shareholders rich.2. you work for the government, from Jan to

May to pay your taxes3. You work for the bank, paying off your

mortgage, student loans and credit cards.

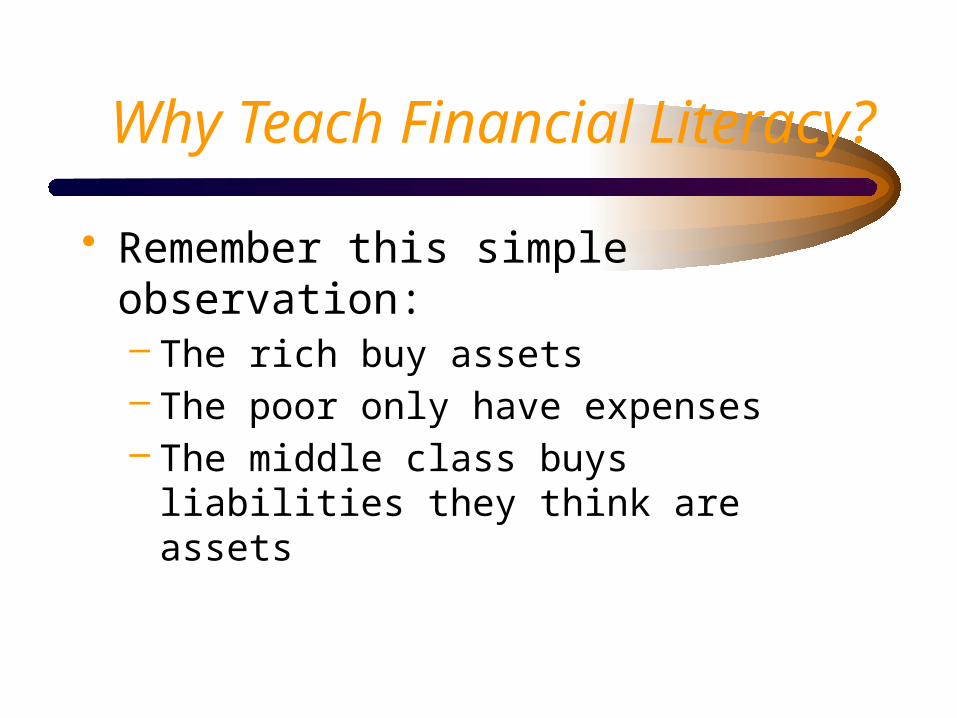

Why Teach Financial Literacy?

• Remember this simple observation:– The rich buy assets– The poor only have expenses– The middle class buys liabilities they think are

assets

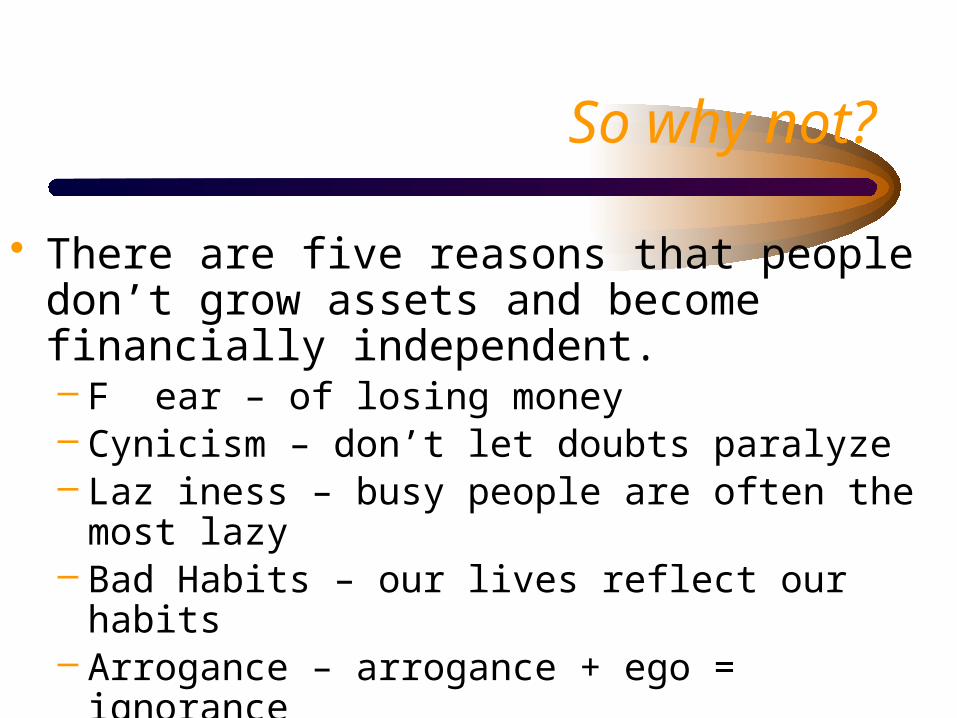

So why not?

• There are five reasons that people don’t grow assets and become financially independent.– F ear – of losing money– Cynicism – don’t let doubts paralyze – Laz iness – busy people are often the most lazy– Bad Habits – our lives reflect our habits– Arrogance – arrogance + ego = ignorance

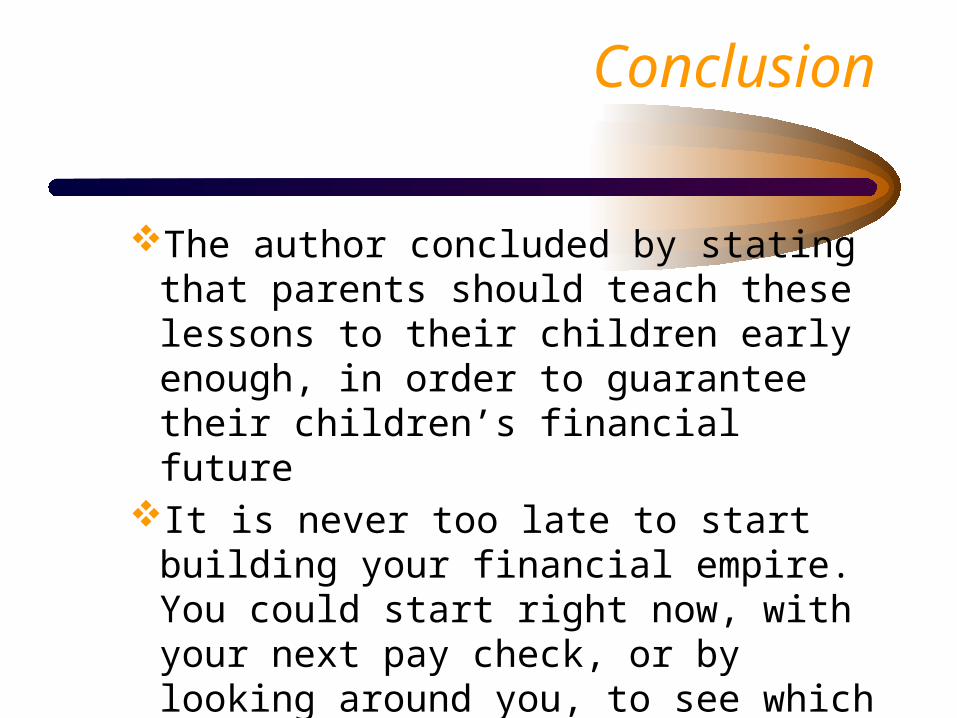

Conclusion

The author concluded by stating that parents should teach these lessons to their children early enough, in order to guarantee their children’s financial future

It is never too late to start building your financial empire. You could start right now, with your next pay check, or by looking around you, to see which need you can fulfill

THANK YOU