retail inventory method & lcm - pondering the classroom · solution to problem 68 retail...

TRANSCRIPT

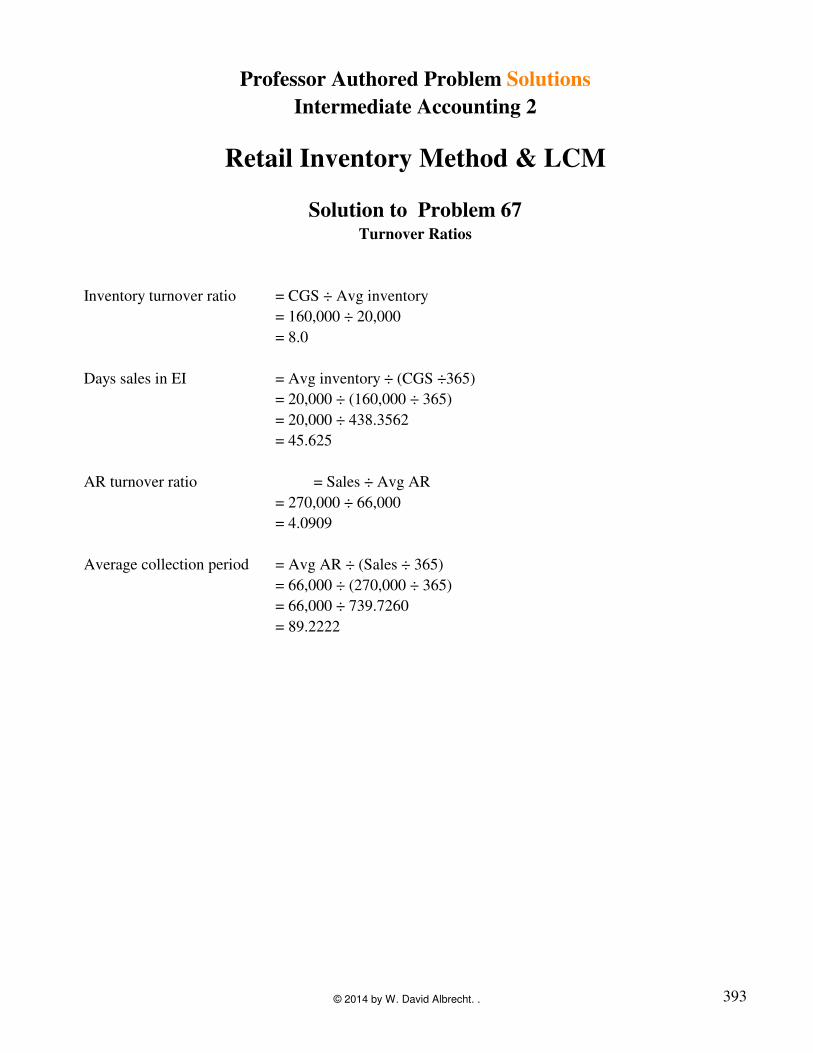

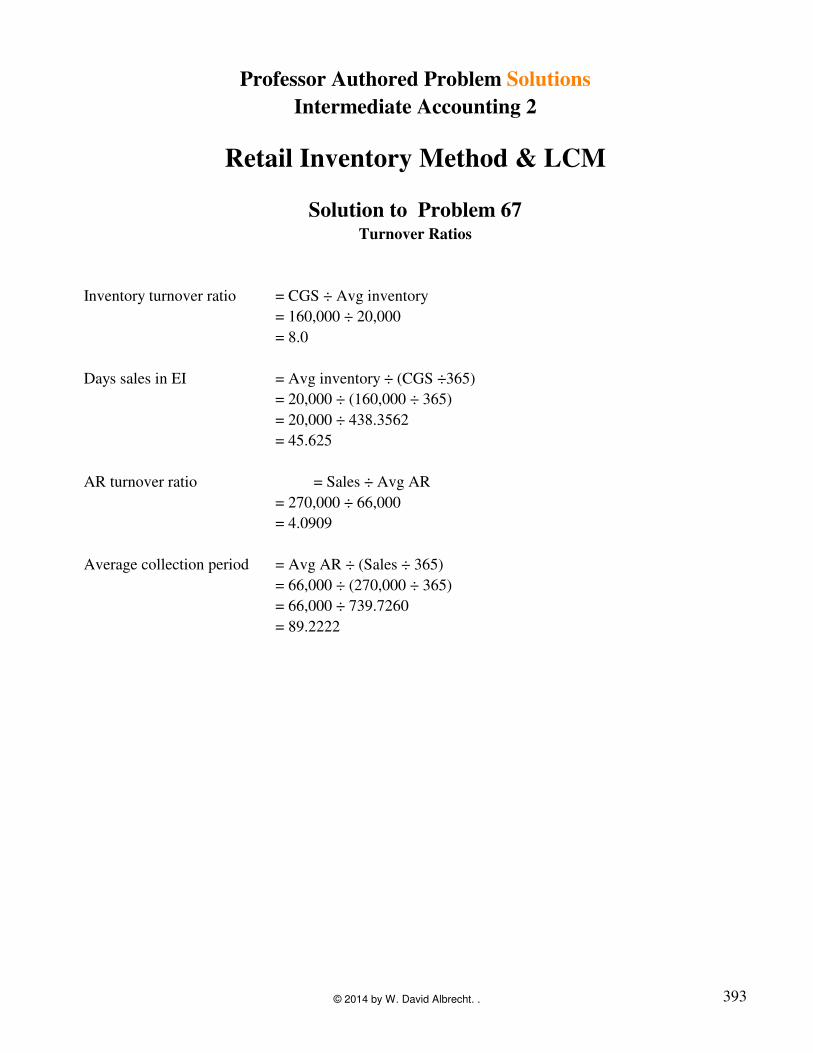

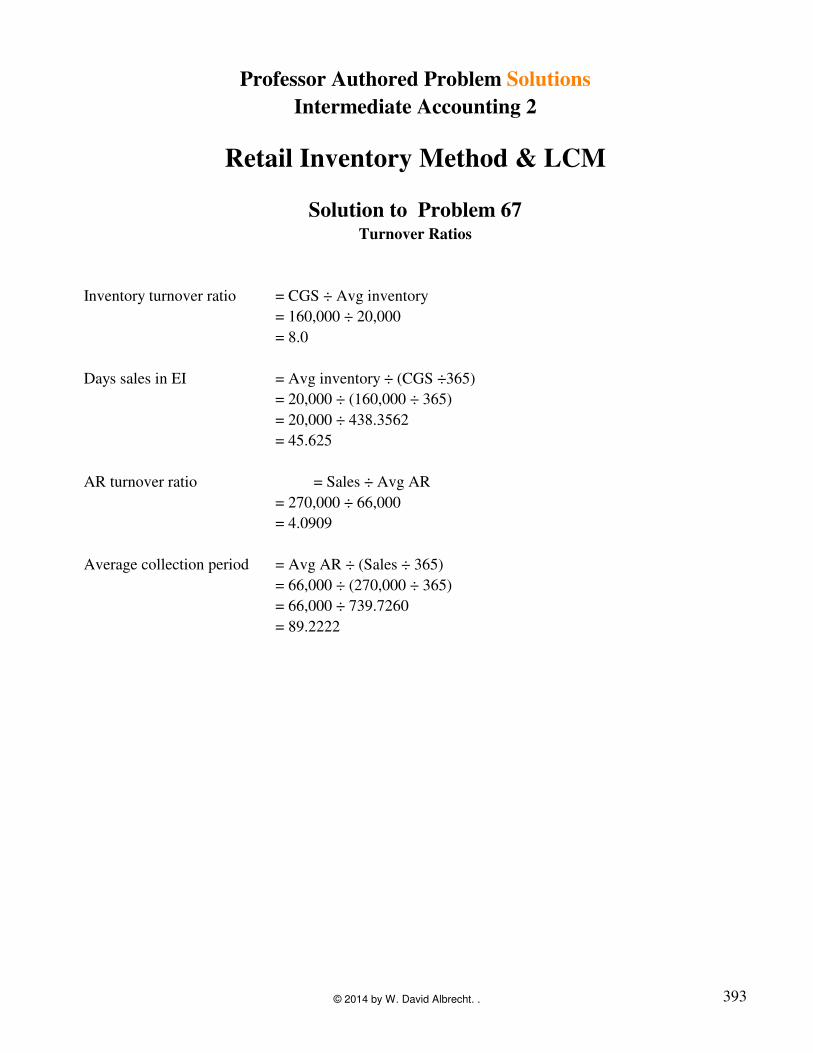

Professor Authored Problem Solutions

Intermediate Accounting 2

Retail Inventory Method & LCM

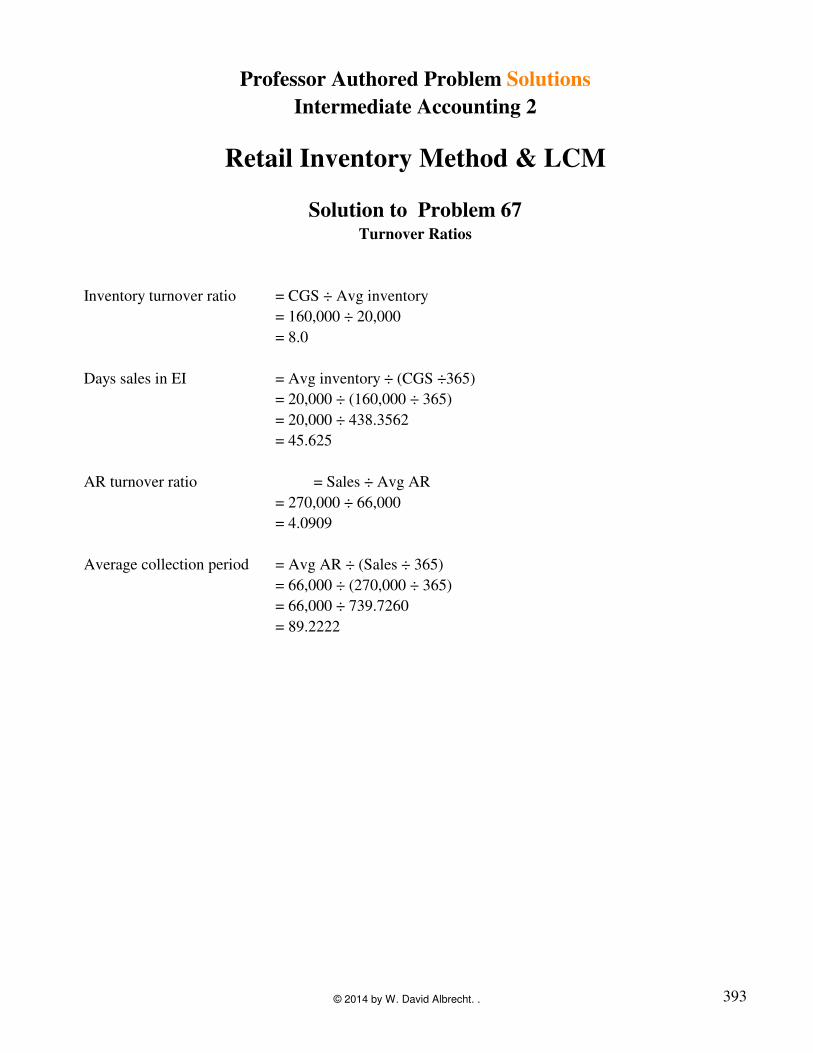

Solution to Problem 67Turnover Ratios

Inventory turnover ratio = CGS ÷ Avg inventory

= 160,000 ÷ 20,000

= 8.0

Days sales in EI = Avg inventory ÷ (CGS ÷365)

= 20,000 ÷ (160,000 ÷ 365)

= 20,000 ÷ 438.3562

= 45.625

AR turnover ratio = Sales ÷ Avg AR

= 270,000 ÷ 66,000

= 4.0909

Average collection period = Avg AR ÷ (Sales ÷ 365)

= 66,000 ÷ (270,000 ÷ 365)

= 66,000 ÷ 739.7260

= 89.2222

393© 2014 by W. David Albrecht. .

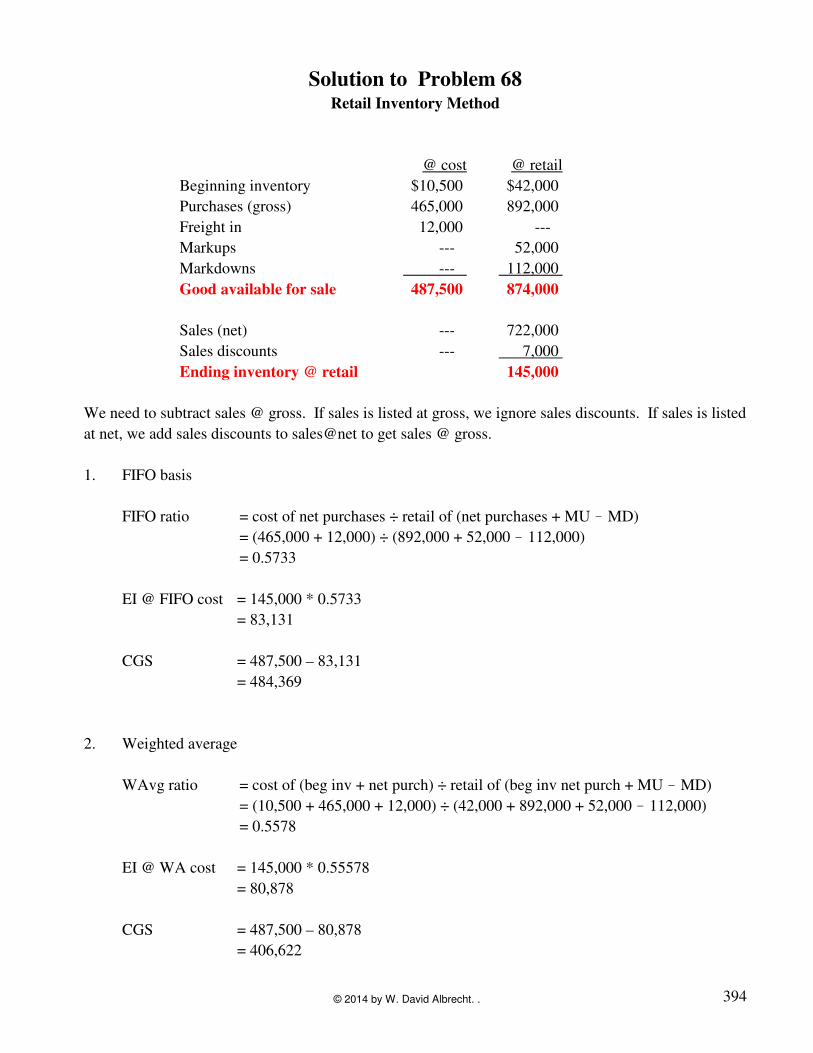

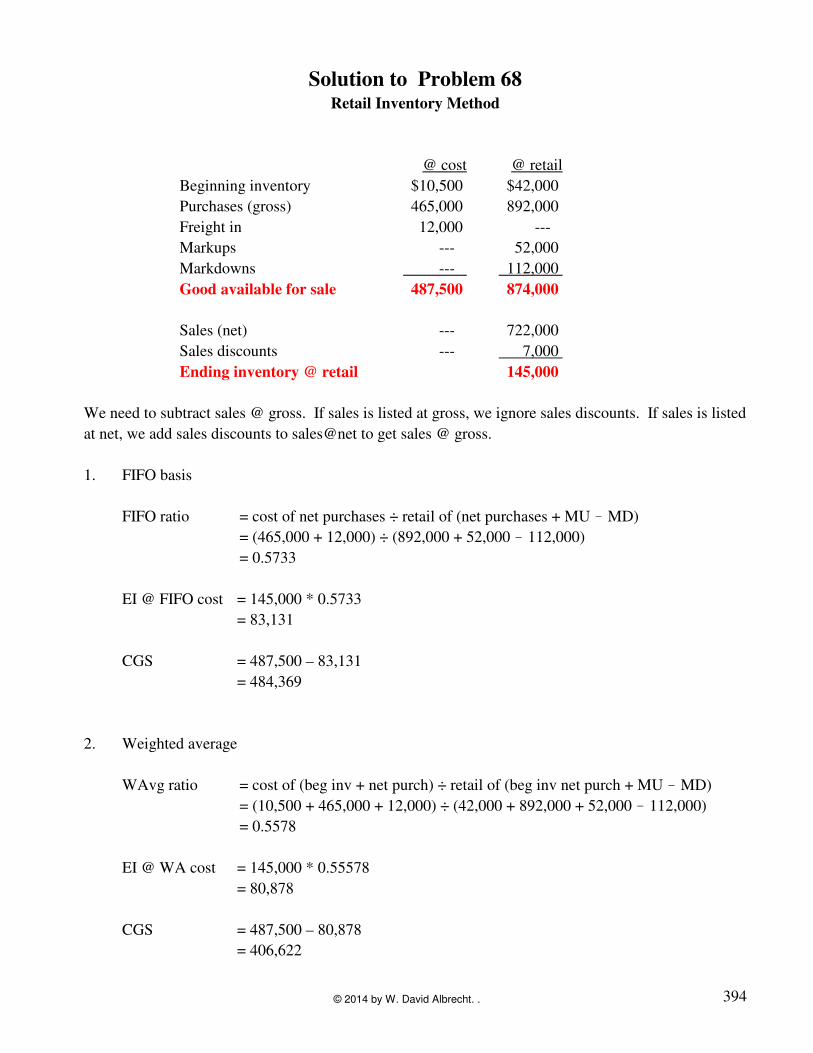

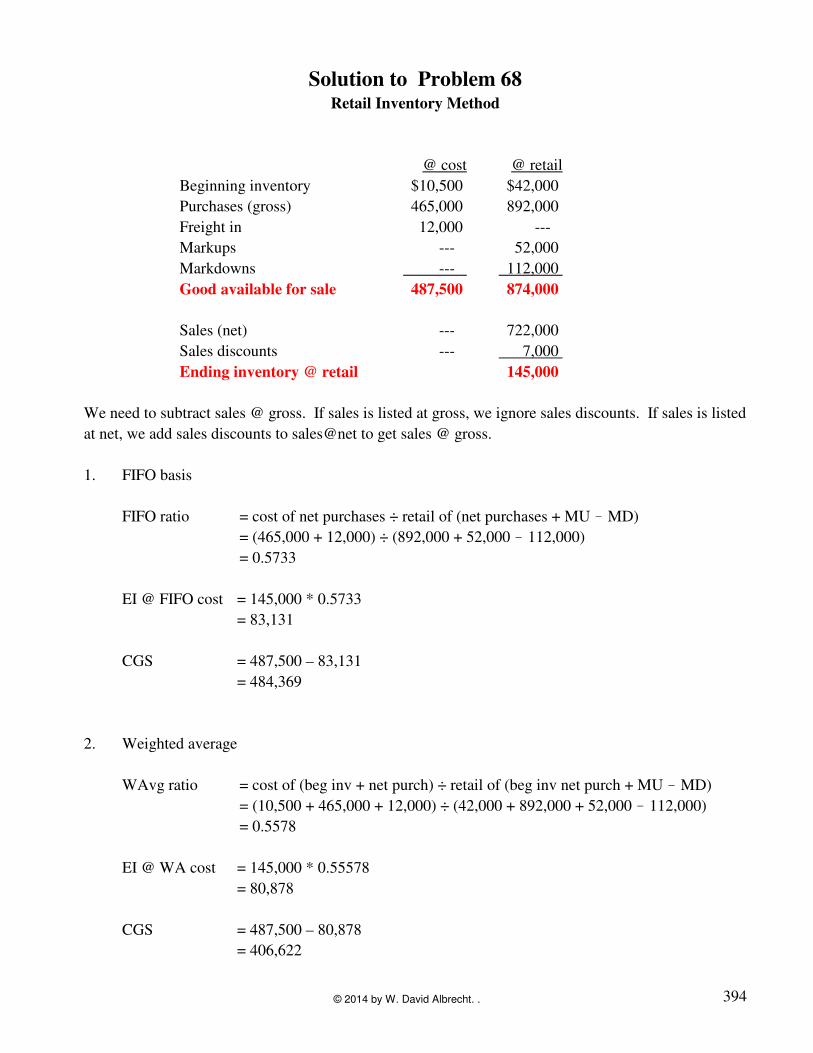

Solution to Problem 68Retail Inventory Method

@ cost @ retail

Beginning inventory $10,500 $42,000

Purchases (gross) 465,000 892,000

Freight in 12,000 ---

Markups --- 52,000

Markdowns --- 112,000

Good available for sale 487,500 874,000

Sales (net) --- 722,000

Sales discounts --- 7,000

Ending inventory @ retail 145,000

We need to subtract sales @ gross. If sales is listed at gross, we ignore sales discounts. If sales is listed

at net, we add sales discounts to sales@net to get sales @ gross.

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (465,000 + 12,000) ÷ (892,000 + 52,000 ! 112,000)

= 0.5733

EI @ FIFO cost = 145,000 * 0.5733

= 83,131

CGS = 487,500 – 83,131

= 484,369

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000 ! 112,000)

= 0.5578

EI @ WA cost = 145,000 * 0.55578

= 80,878

CGS = 487,500 – 80,878

= 406,622

394© 2014 by W. David Albrecht. .

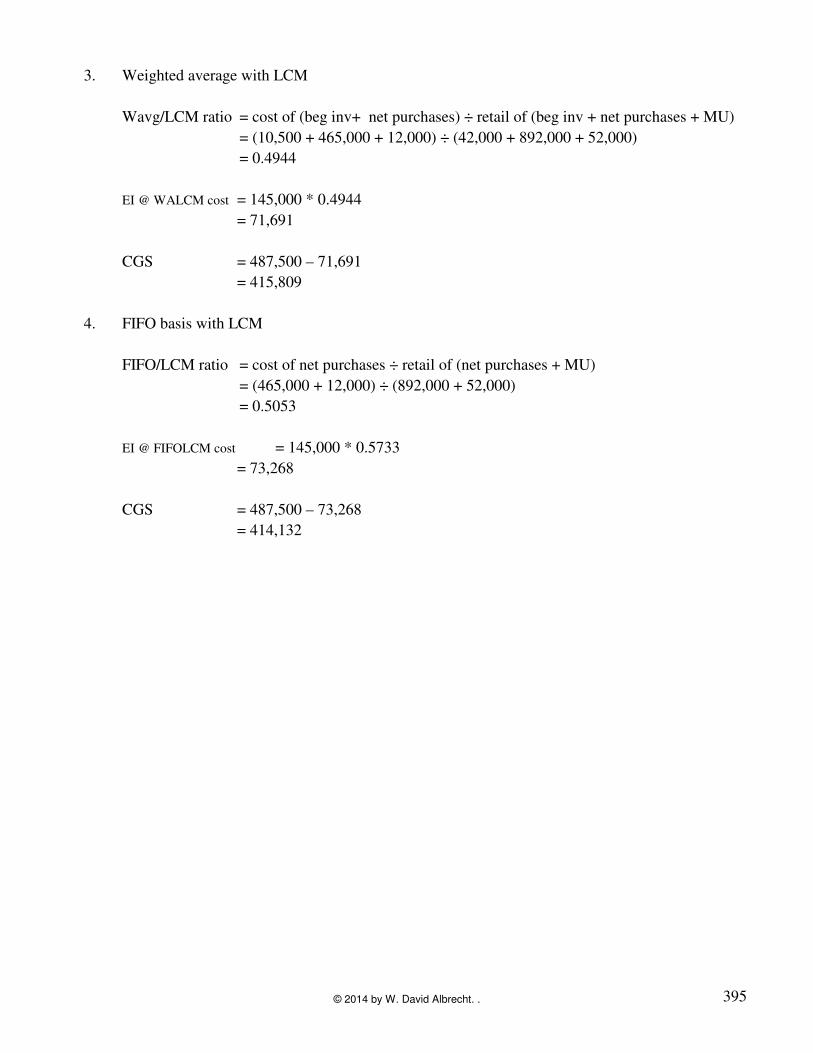

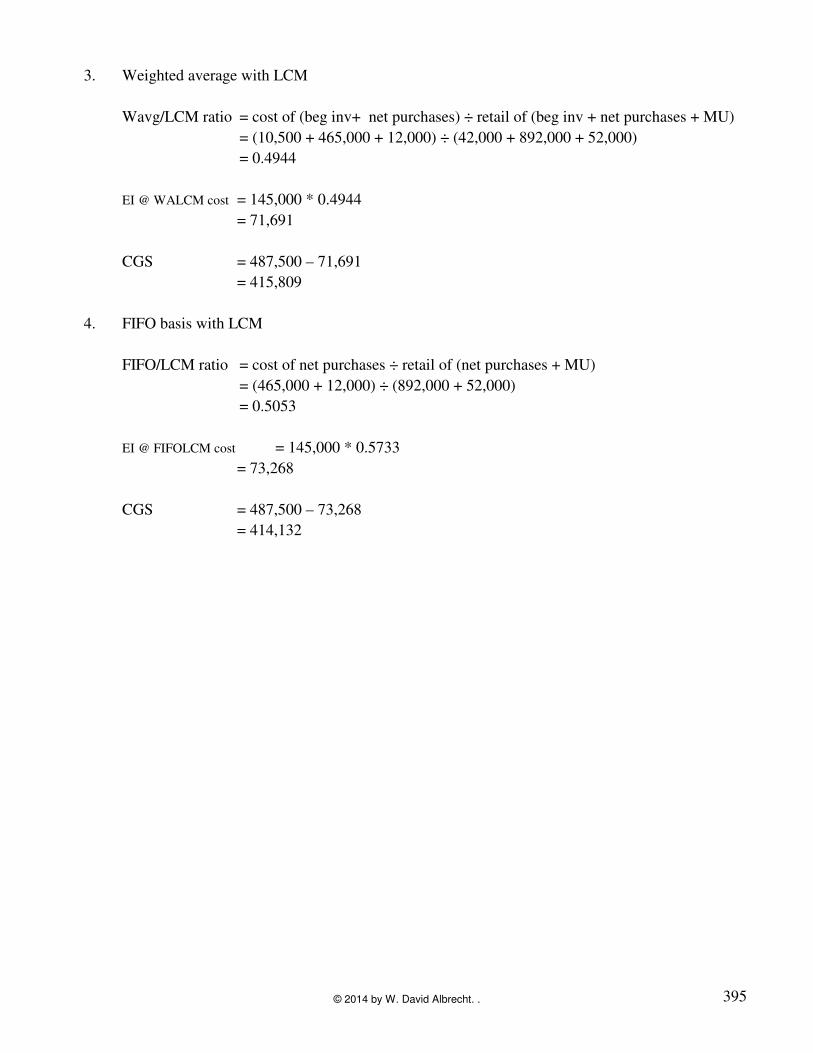

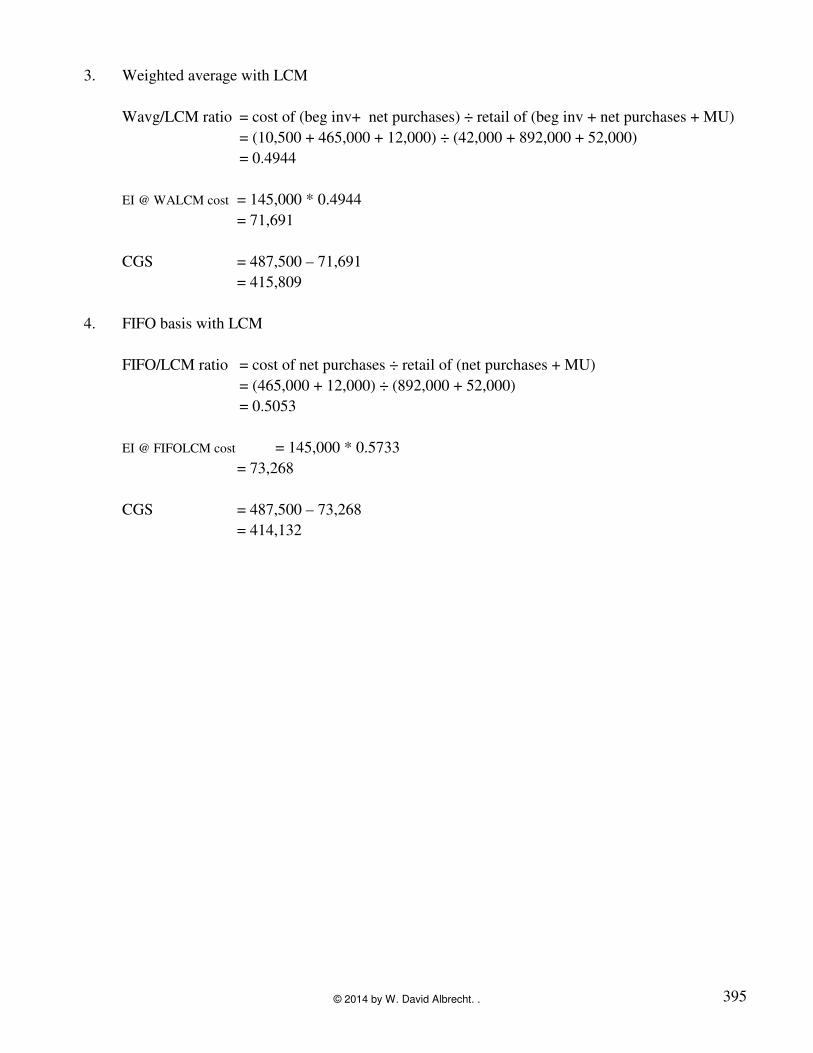

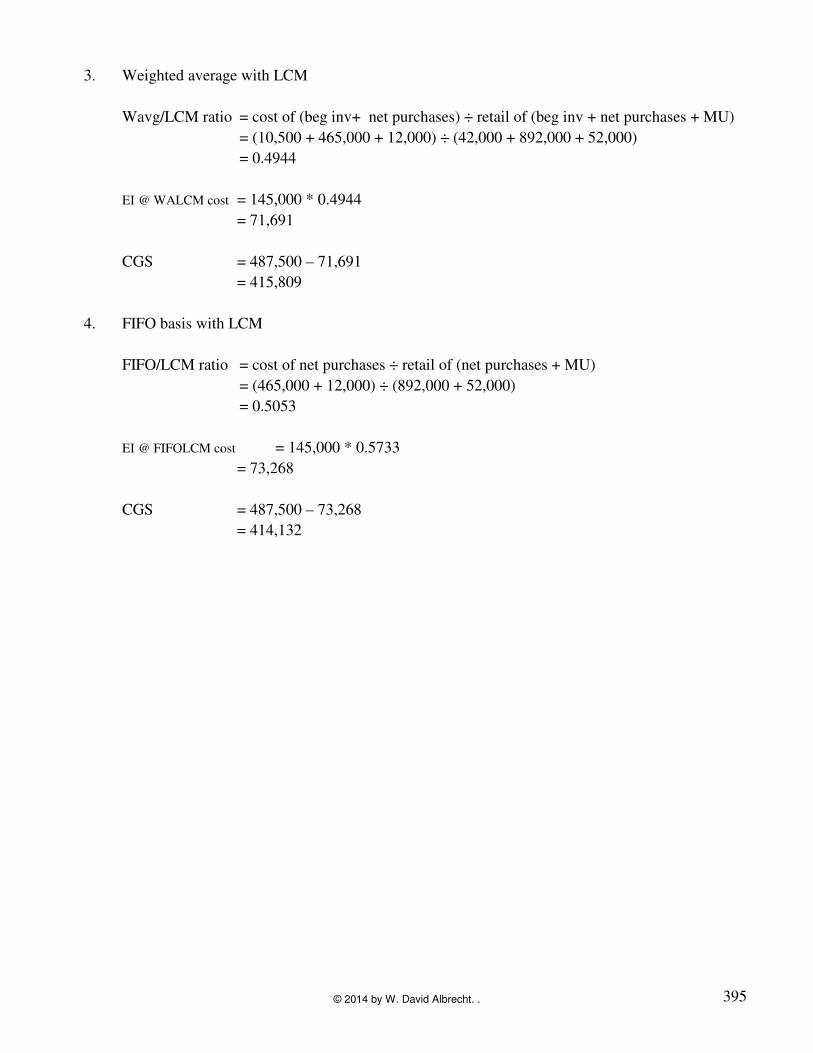

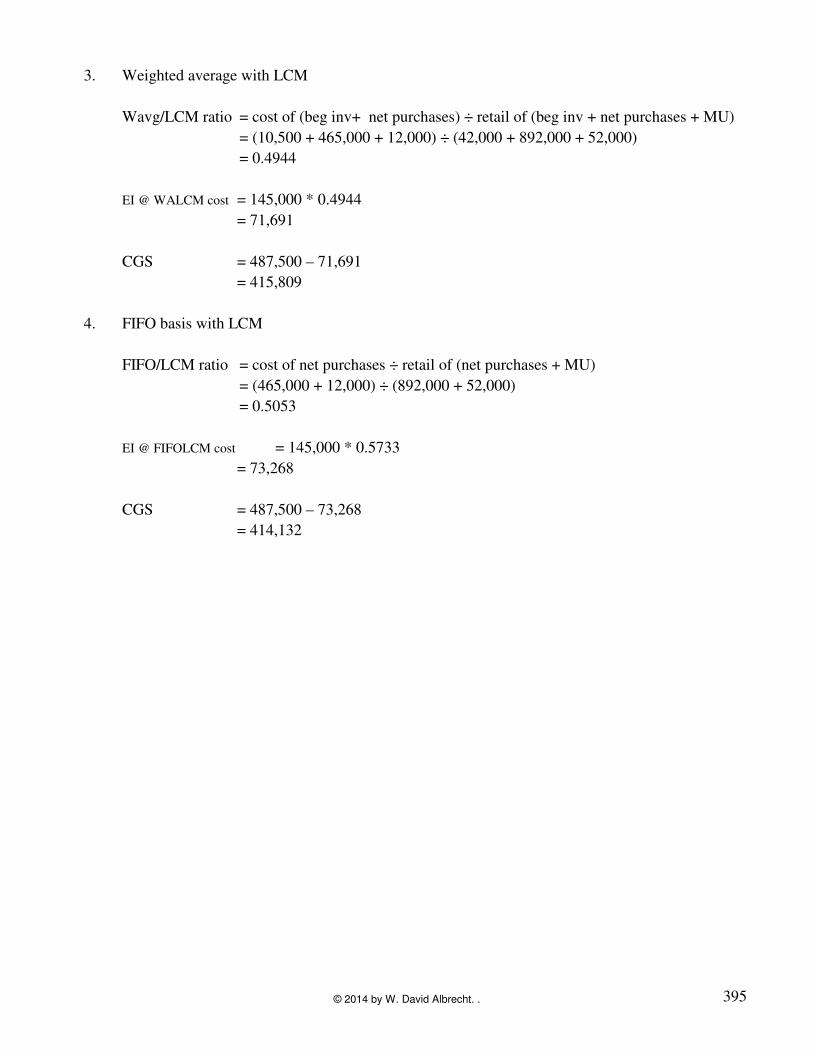

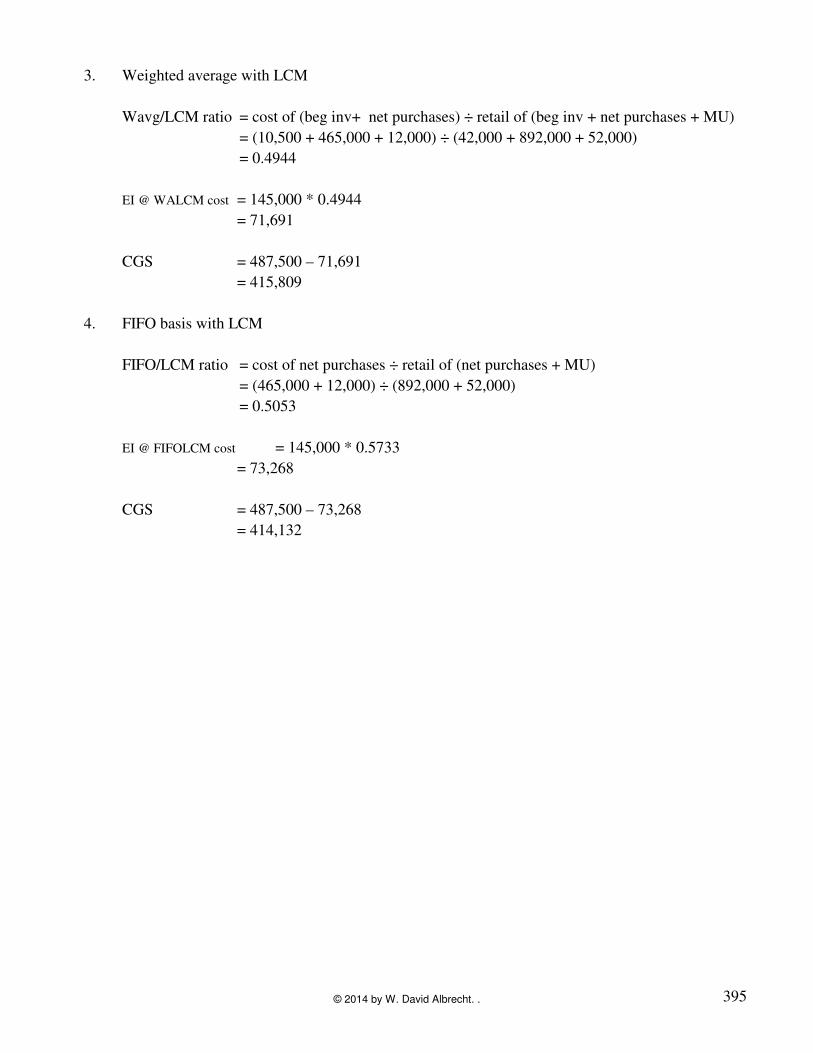

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000)

= 0.4944

EI @ WALCM cost = 145,000 * 0.4944

= 71,691

CGS = 487,500 – 71,691

= 415,809

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (465,000 + 12,000) ÷ (892,000 + 52,000)

= 0.5053

EI @ FIFOLCM cost = 145,000 * 0.5733

= 73,268

CGS = 487,500 – 73,268

= 414,132

395© 2014 by W. David Albrecht. .

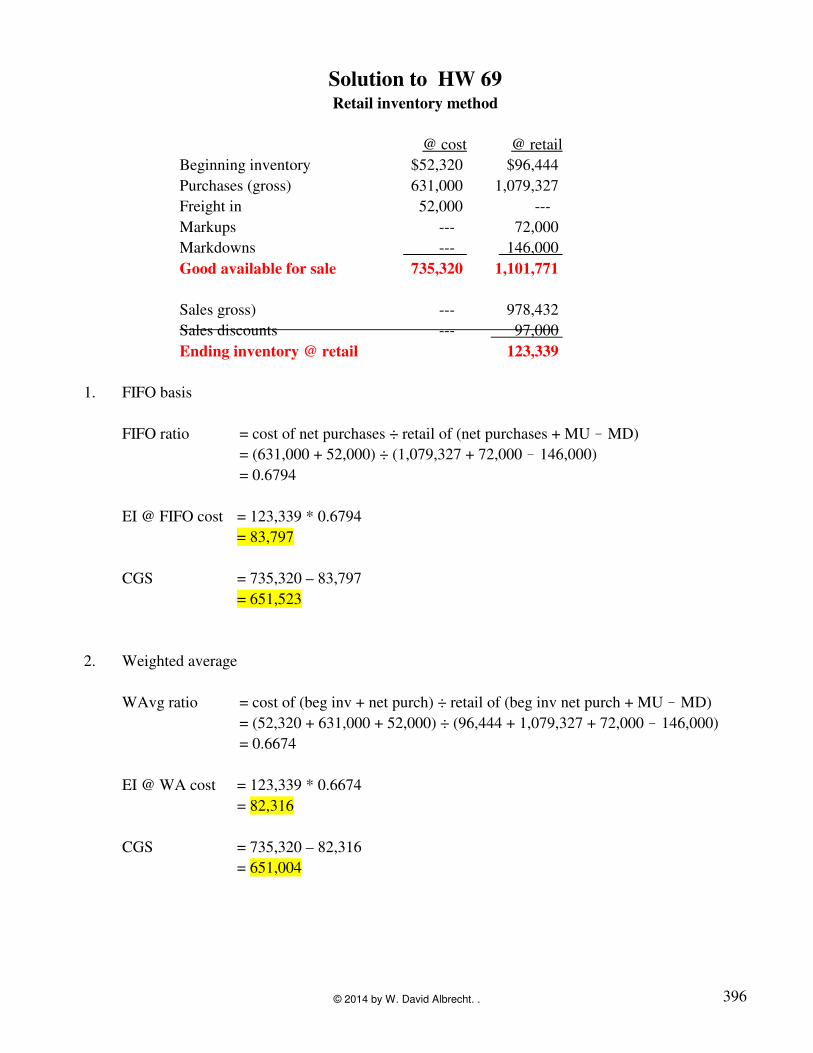

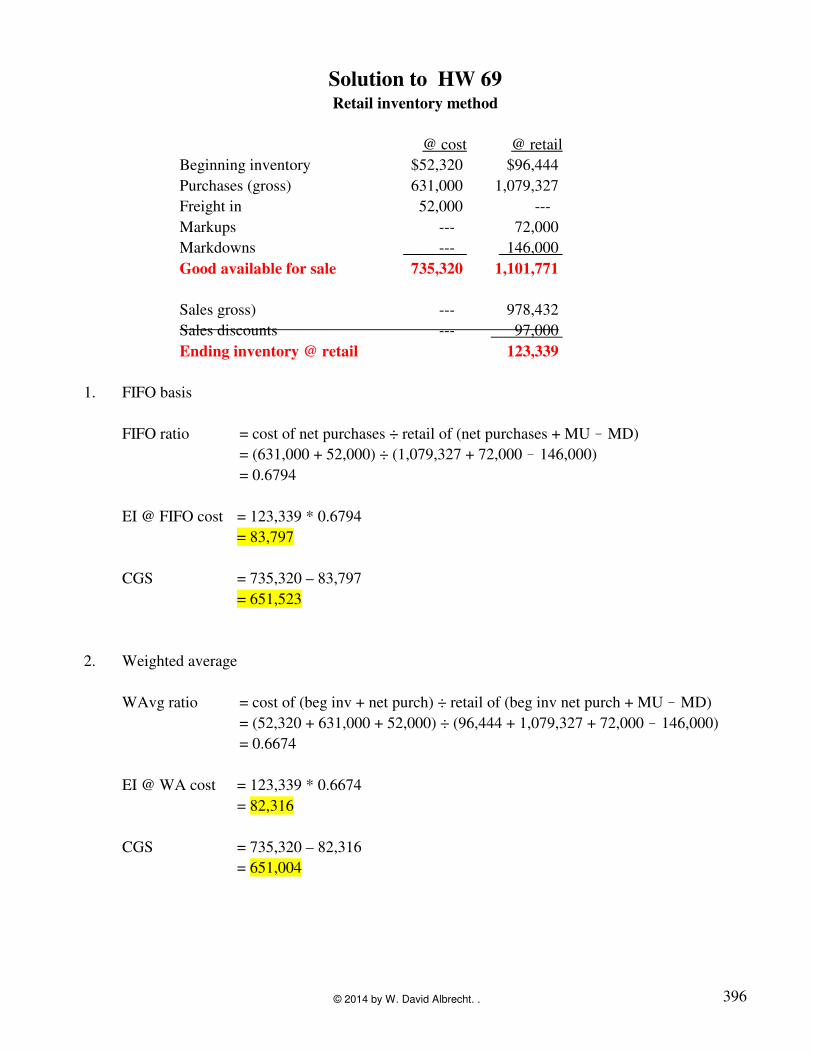

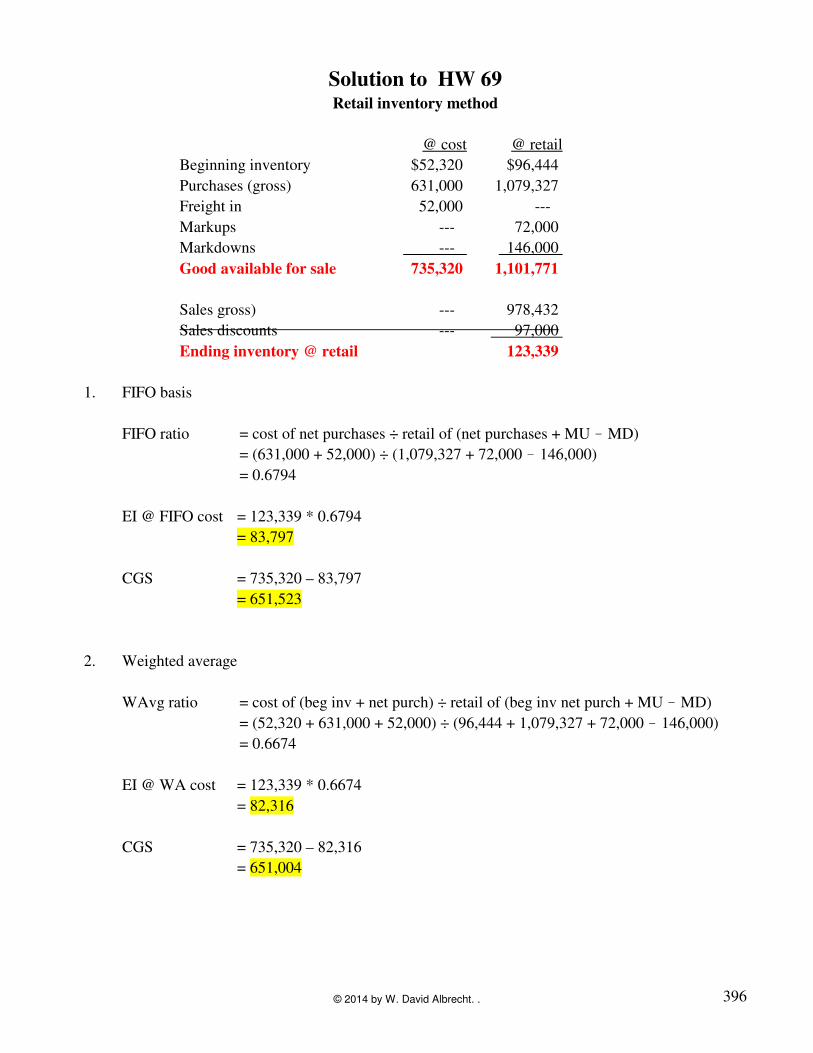

Solution to HW 69Retail inventory method

@ cost @ retail

Beginning inventory $52,320 $96,444

Purchases (gross) 631,000 1,079,327

Freight in 52,000 ---

Markups --- 72,000

Markdowns --- 146,000

Good available for sale 735,320 1,101,771

Sales gross) --- 978,432

Sales discounts --- 97,000

Ending inventory @ retail 123,339

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000 ! 146,000)

= 0.6794

EI @ FIFO cost = 123,339 * 0.6794

= 83,797

CGS = 735,320 – 83,797

= 651,523

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000 ! 146,000)

= 0.6674

EI @ WA cost = 123,339 * 0.6674

= 82,316

CGS = 735,320 – 82,316

= 651,004

396© 2014 by W. David Albrecht. .

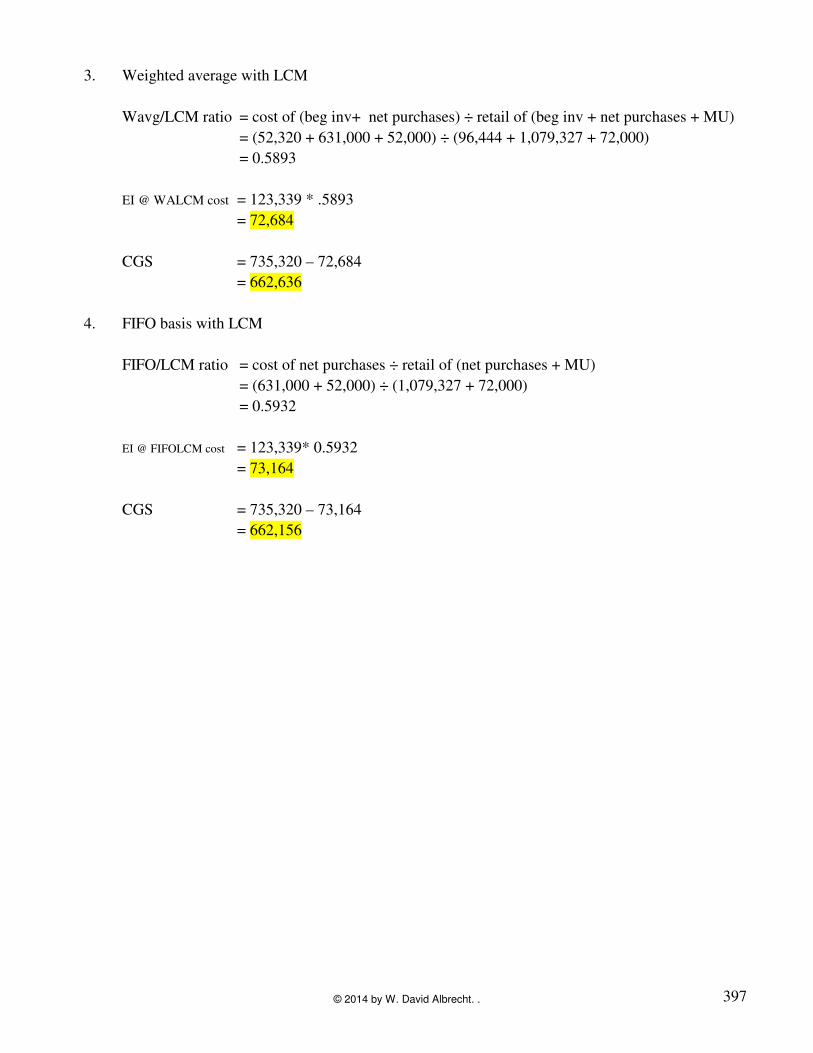

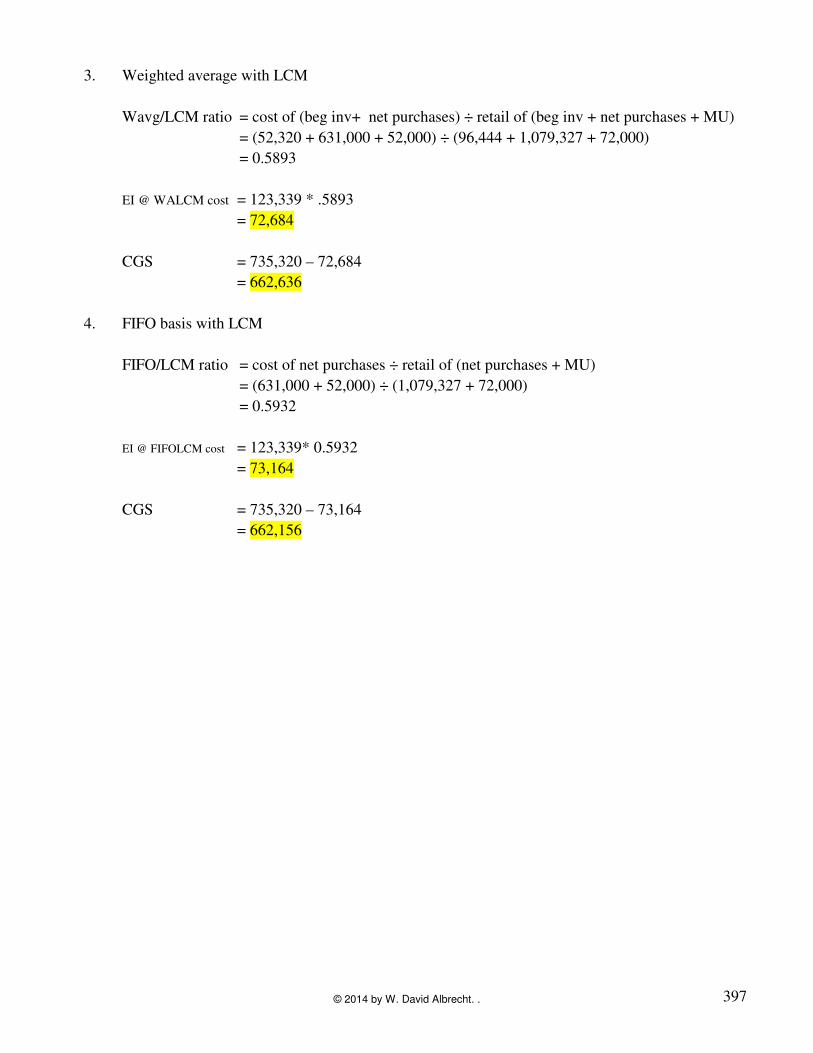

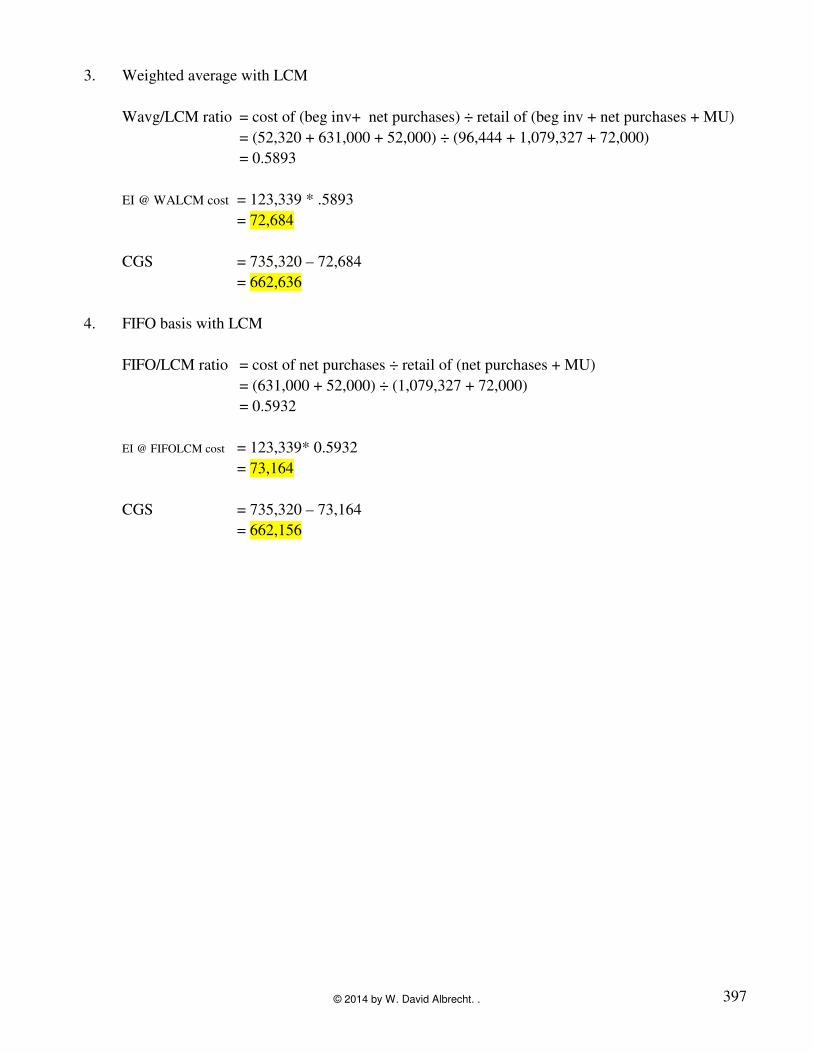

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000)

= 0.5893

EI @ WALCM cost = 123,339 * .5893

= 72,684

CGS = 735,320 – 72,684

= 662,636

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000)

= 0.5932

EI @ FIFOLCM cost = 123,339* 0.5932

= 73,164

CGS = 735,320 – 73,164

= 662,156

397© 2014 by W. David Albrecht. .

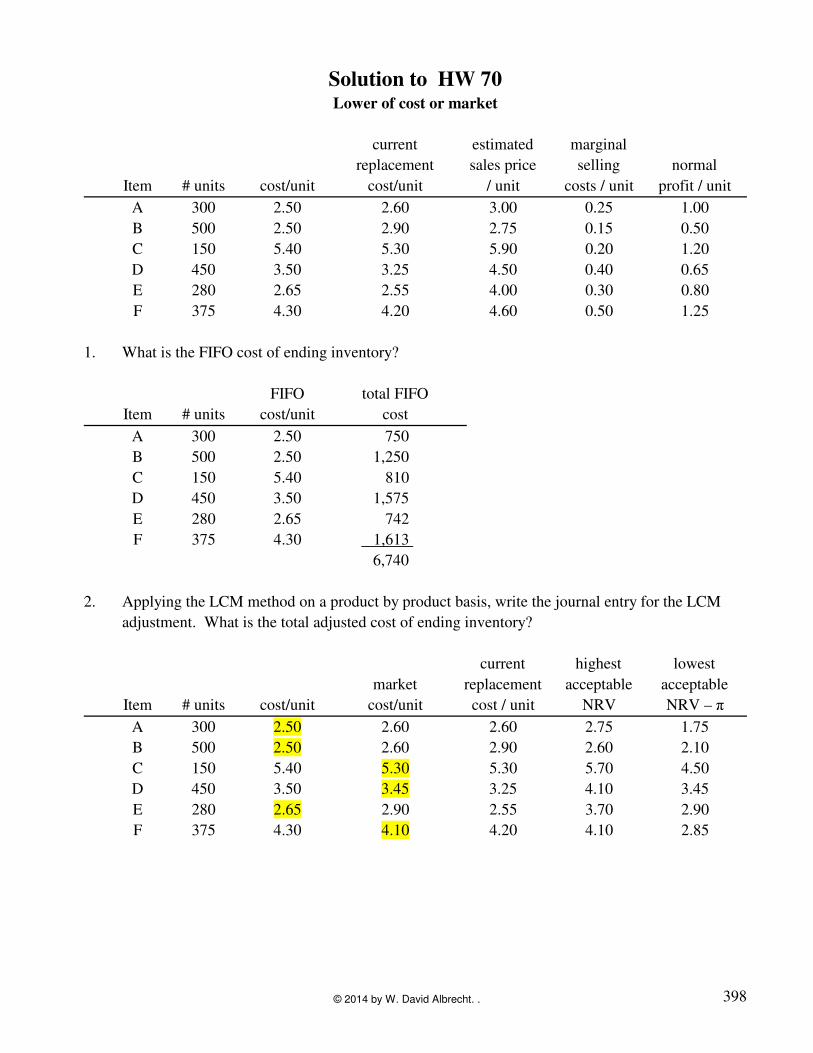

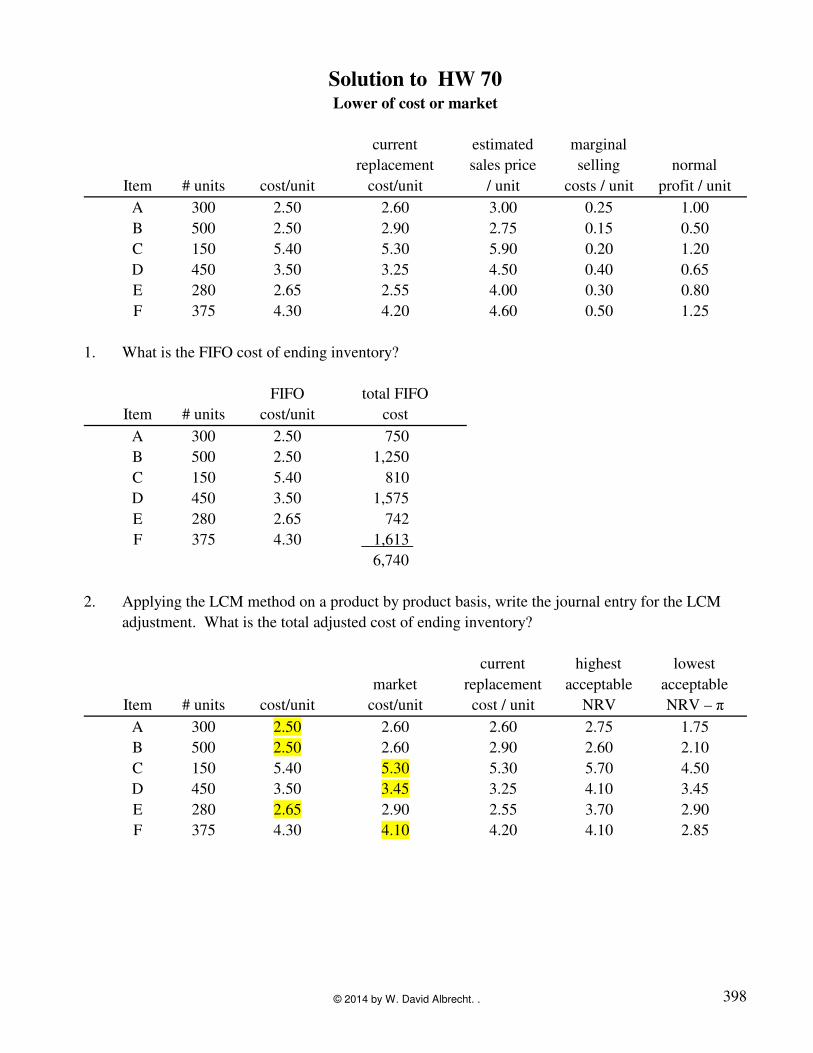

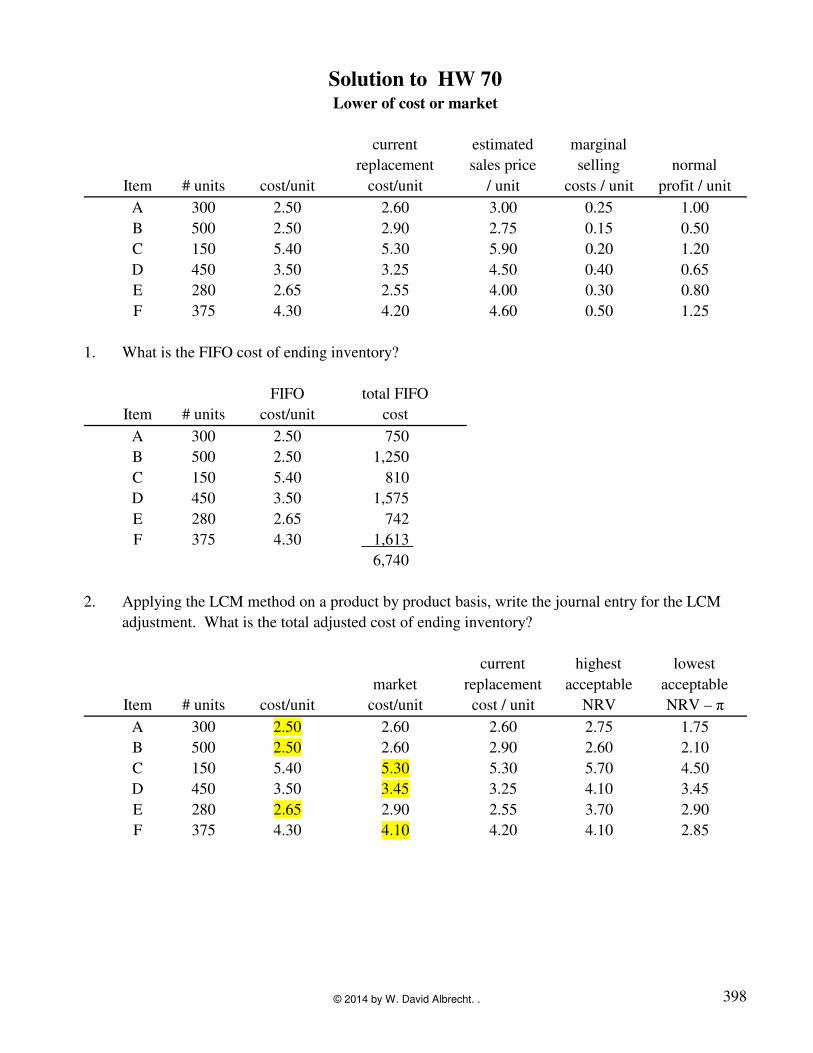

Solution to HW 70Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 300 2.50 2.60 3.00 0.25 1.00

B 500 2.50 2.90 2.75 0.15 0.50

C 150 5.40 5.30 5.90 0.20 1.20

D 450 3.50 3.25 4.50 0.40 0.65

E 280 2.65 2.55 4.00 0.30 0.80

F 375 4.30 4.20 4.60 0.50 1.25

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 300 2.50 750

B 500 2.50 1,250

C 150 5.40 810

D 450 3.50 1,575

E 280 2.65 742

F 375 4.30 1,613

6,740

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

market replacement acceptable acceptable

Item # units cost/unit cost/unit cost / unit NRV NRV – π

A 300 2.50 2.60 2.60 2.75 1.75

B 500 2.50 2.60 2.90 2.60 2.10

C 150 5.40 5.30 5.30 5.70 4.50

D 450 3.50 3.45 3.25 4.10 3.45

E 280 2.65 2.90 2.55 3.70 2.90

F 375 4.30 4.10 4.20 4.10 2.85

398© 2014 by W. David Albrecht. .

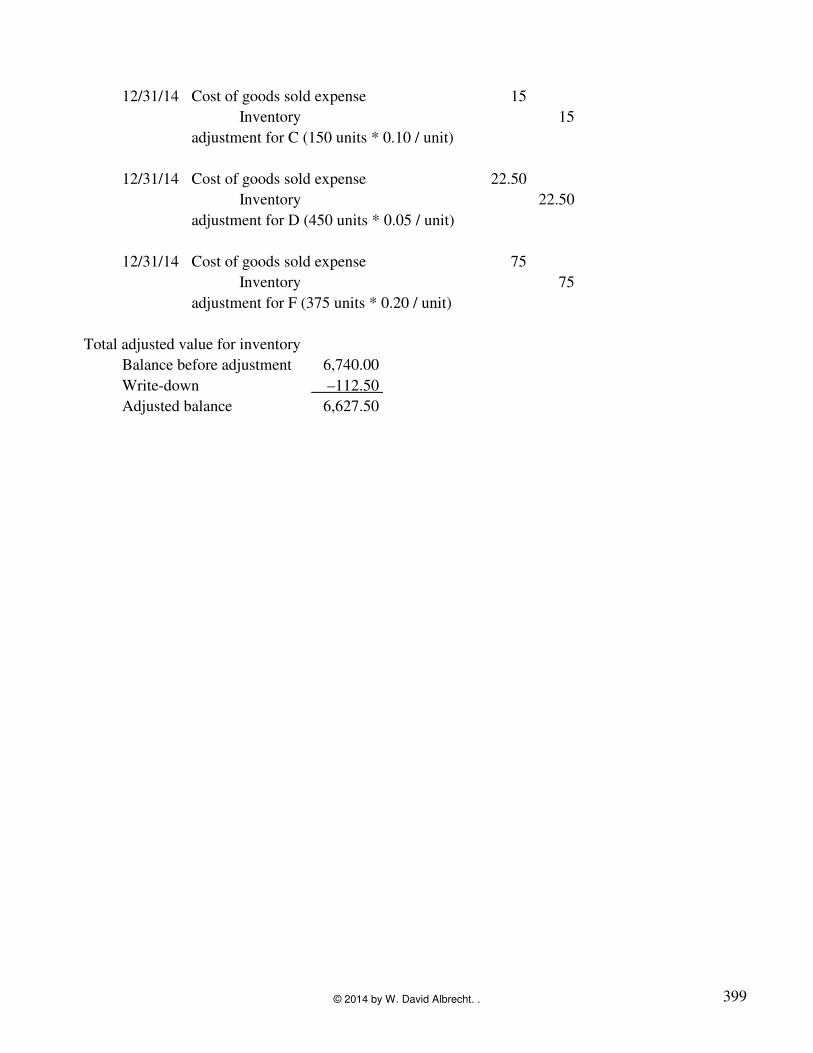

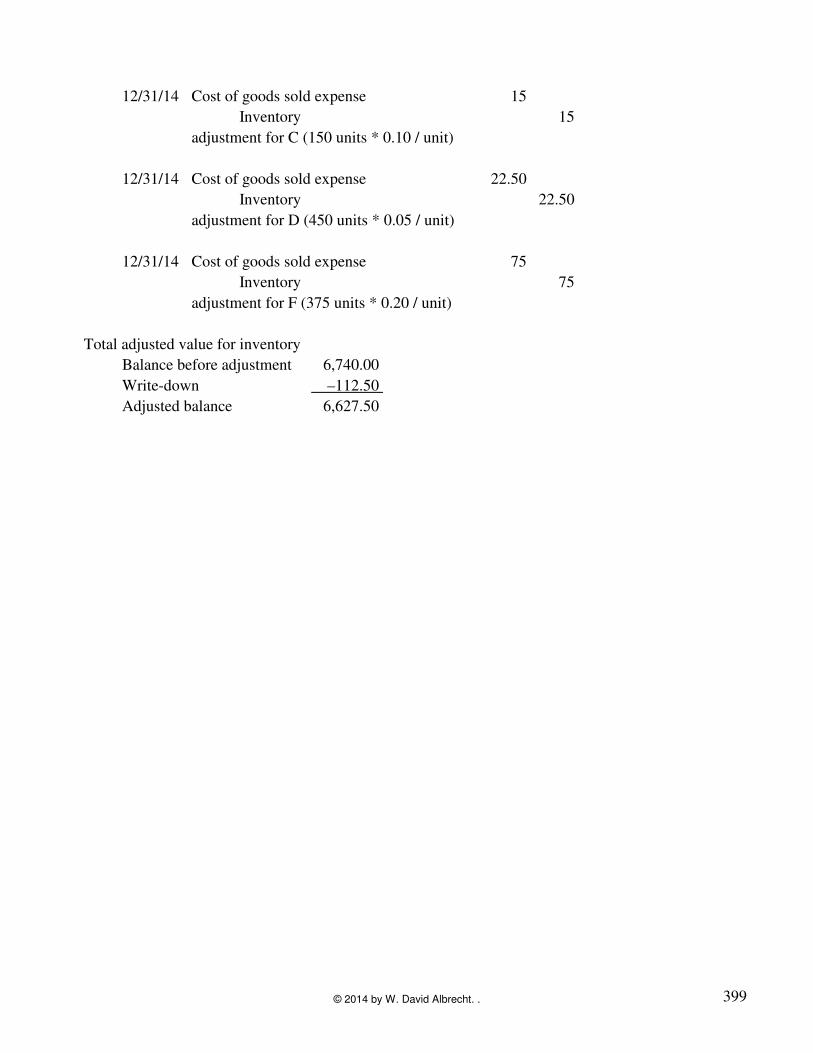

12/31/14 Cost of goods sold expense 15

Inventory 15

adjustment for C (150 units * 0.10 / unit)

12/31/14 Cost of goods sold expense 22.50

Inventory 22.50

adjustment for D (450 units * 0.05 / unit)

12/31/14 Cost of goods sold expense 75

Inventory 75

adjustment for F (375 units * 0.20 / unit)

Total adjusted value for inventory

Balance before adjustment 6,740.00

Write-down –112.50

Adjusted balance 6,627.50

399© 2014 by W. David Albrecht. .

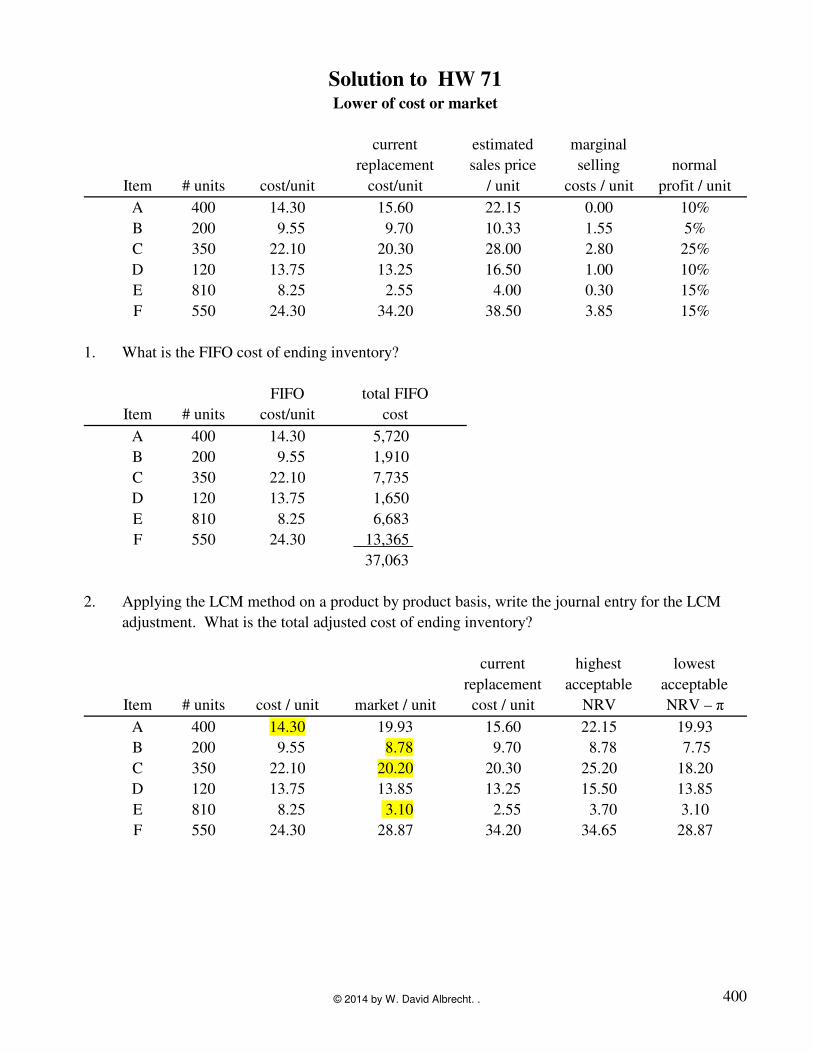

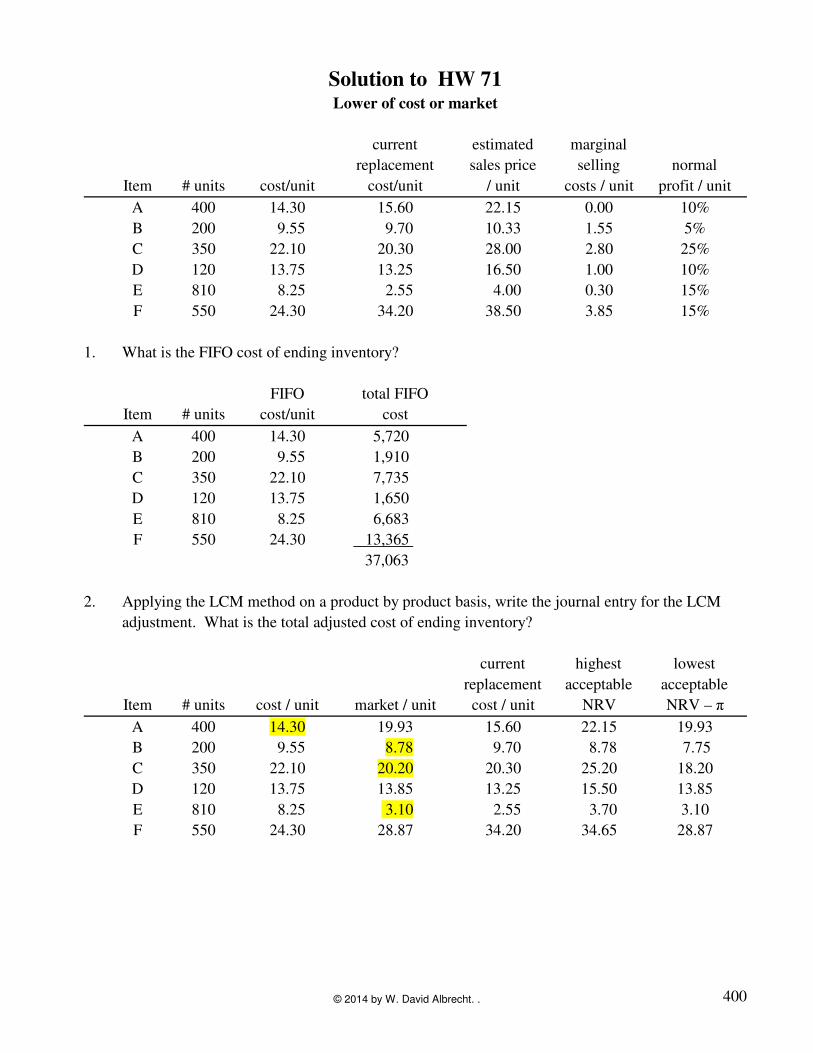

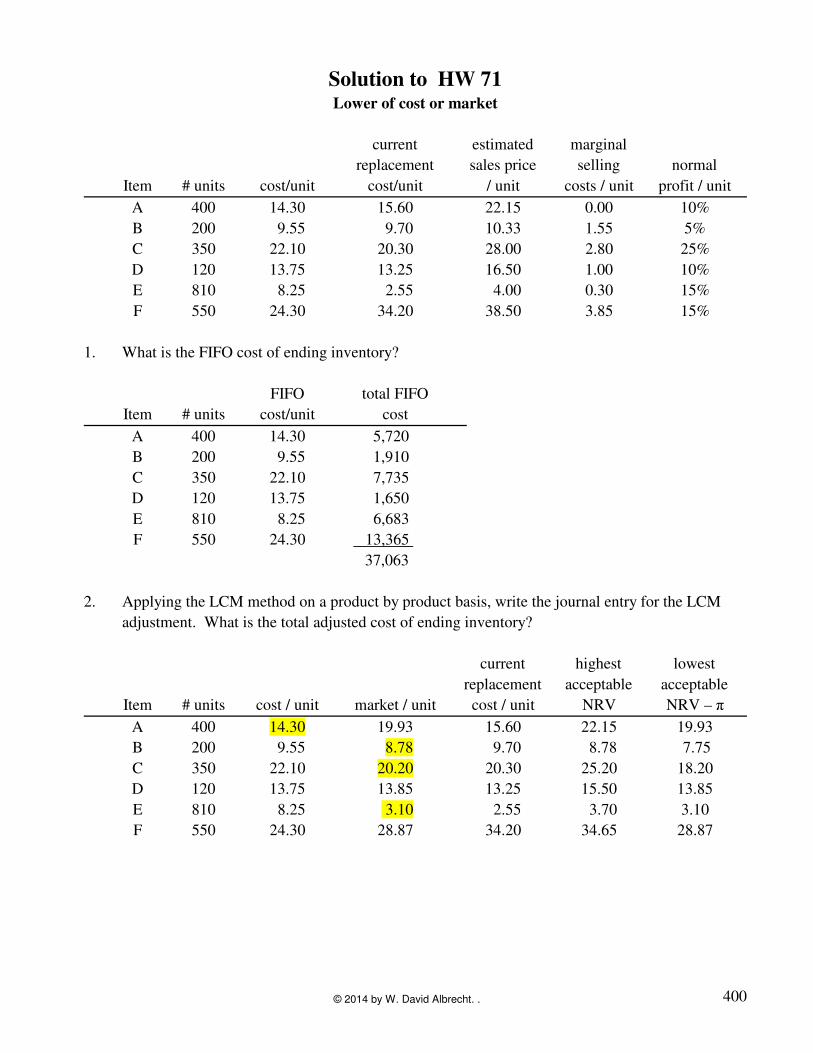

Solution to HW 71Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 400 14.30 15.60 22.15 0.00 10%

B 200 9.55 9.70 10.33 1.55 5%

C 350 22.10 20.30 28.00 2.80 25%

D 120 13.75 13.25 16.50 1.00 10%

E 810 8.25 2.55 4.00 0.30 15%

F 550 24.30 34.20 38.50 3.85 15%

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 400 14.30 5,720

B 200 9.55 1,910

C 350 22.10 7,735

D 120 13.75 1,650

E 810 8.25 6,683

F 550 24.30 13,365

37,063

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

replacement acceptable acceptable

Item # units cost / unit market / unit cost / unit NRV NRV – π

A 400 14.30 19.93 15.60 22.15 19.93

B 200 9.55 8.78 9.70 8.78 7.75

C 350 22.10 20.20 20.30 25.20 18.20

D 120 13.75 13.85 13.25 15.50 13.85

E 810 8.25 3.10 2.55 3.70 3.10

F 550 24.30 28.87 34.20 34.65 28.87

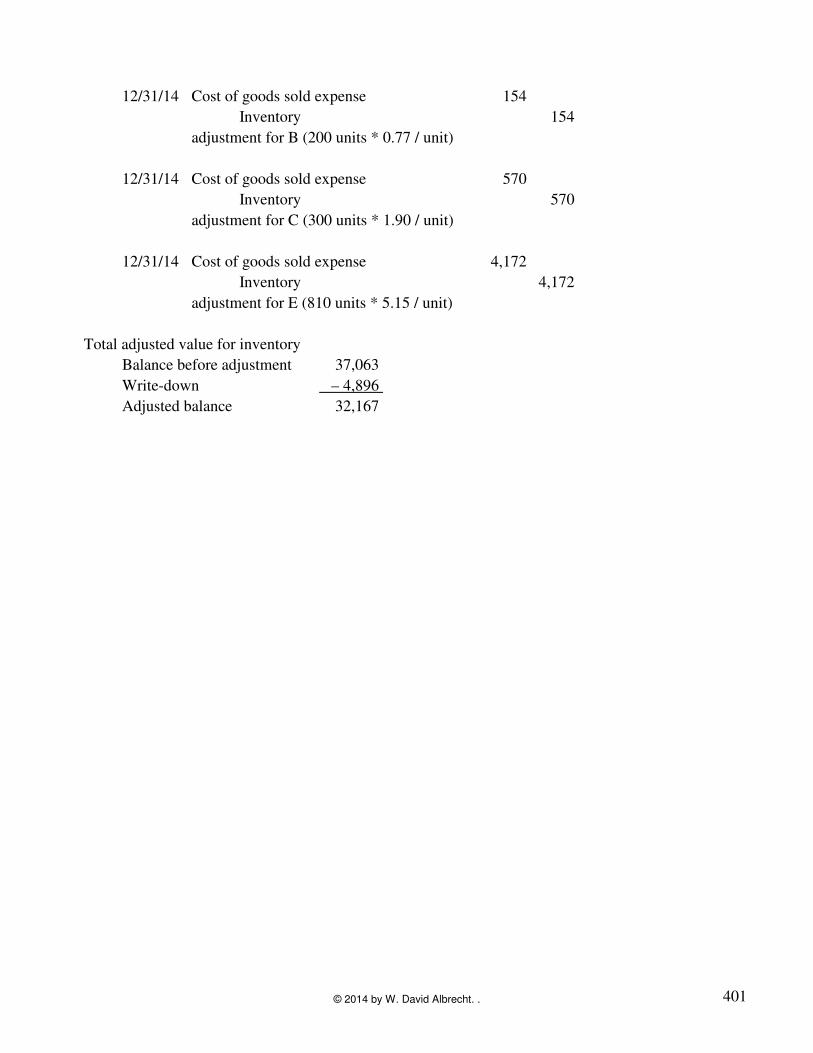

400© 2014 by W. David Albrecht. .

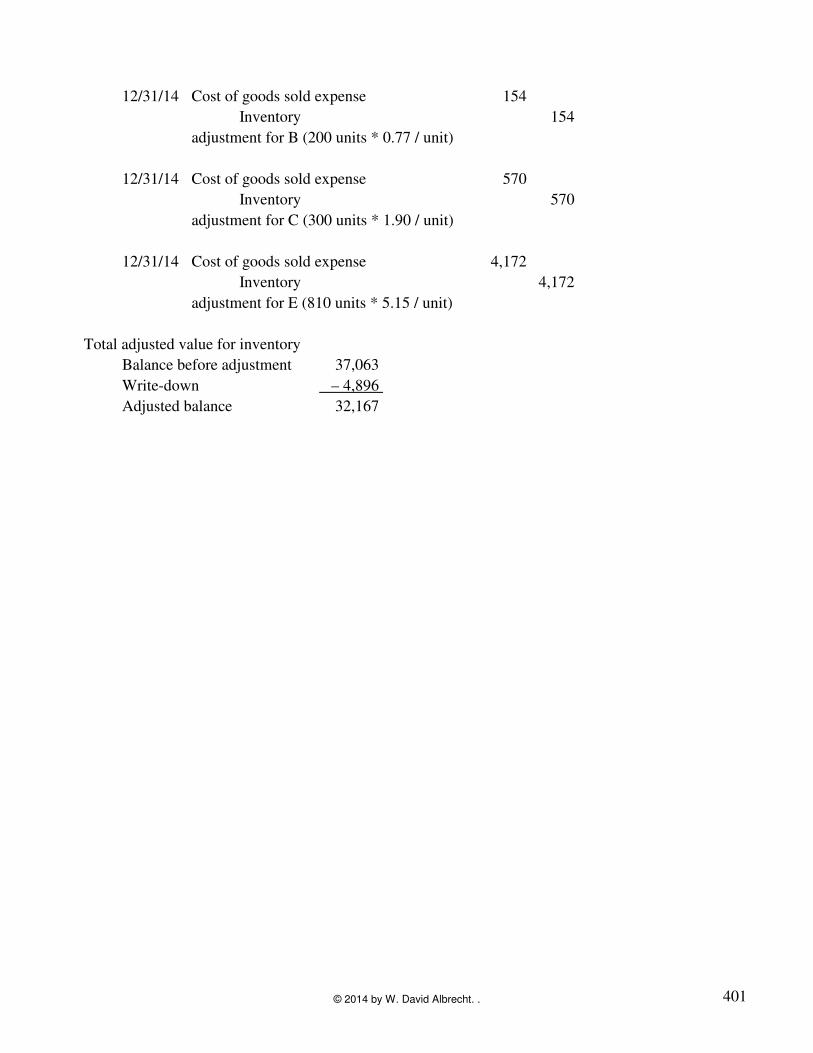

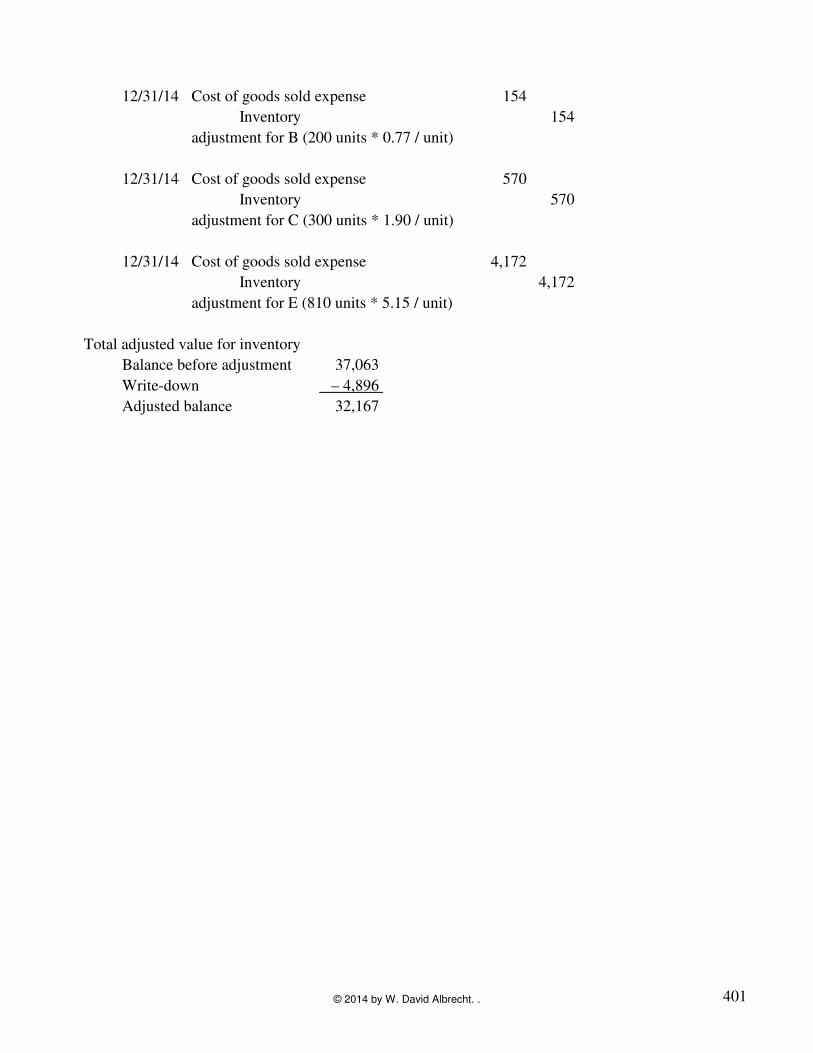

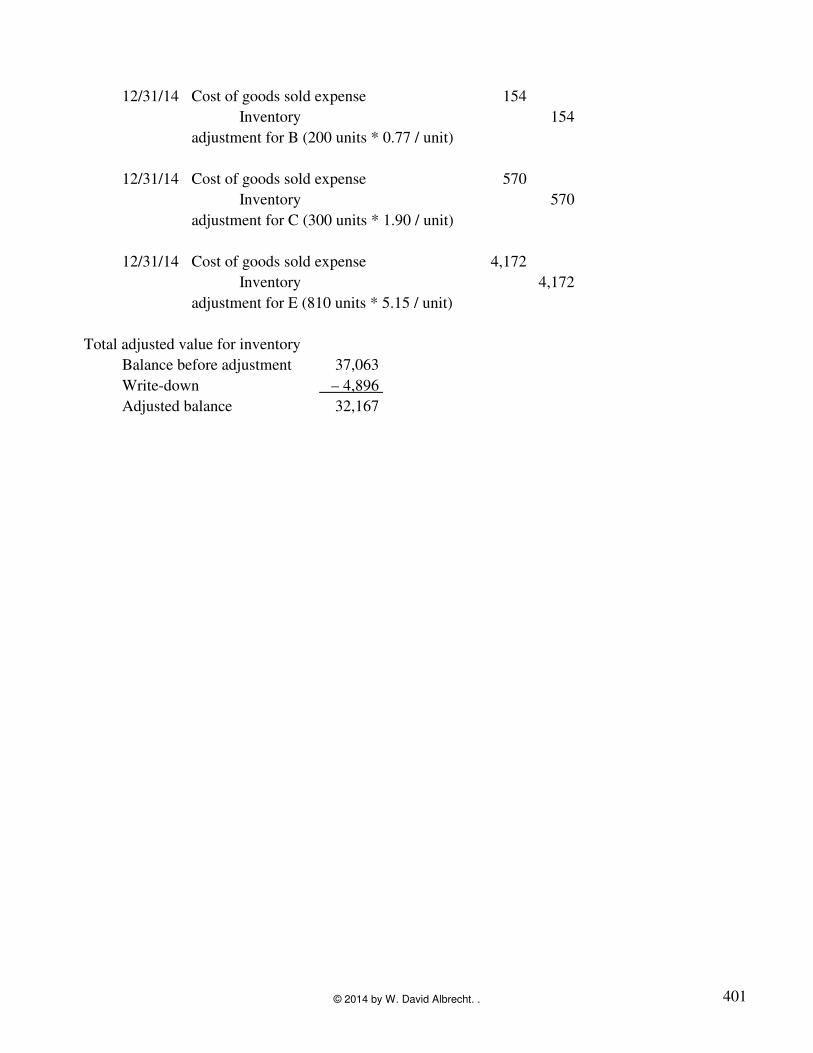

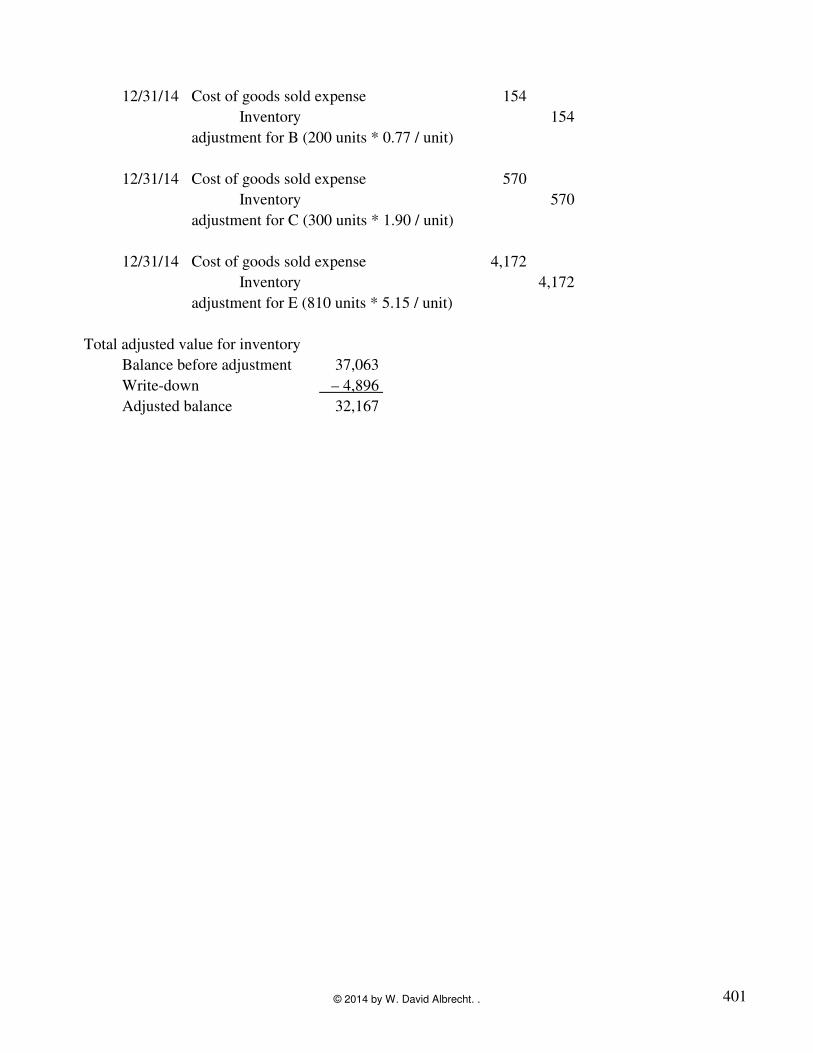

12/31/14 Cost of goods sold expense 154

Inventory 154

adjustment for B (200 units * 0.77 / unit)

12/31/14 Cost of goods sold expense 570

Inventory 570

adjustment for C (300 units * 1.90 / unit)

12/31/14 Cost of goods sold expense 4,172

Inventory 4,172

adjustment for E (810 units * 5.15 / unit)

Total adjusted value for inventory

Balance before adjustment 37,063

Write-down – 4,896

Adjusted balance 32,167

401© 2014 by W. David Albrecht. .

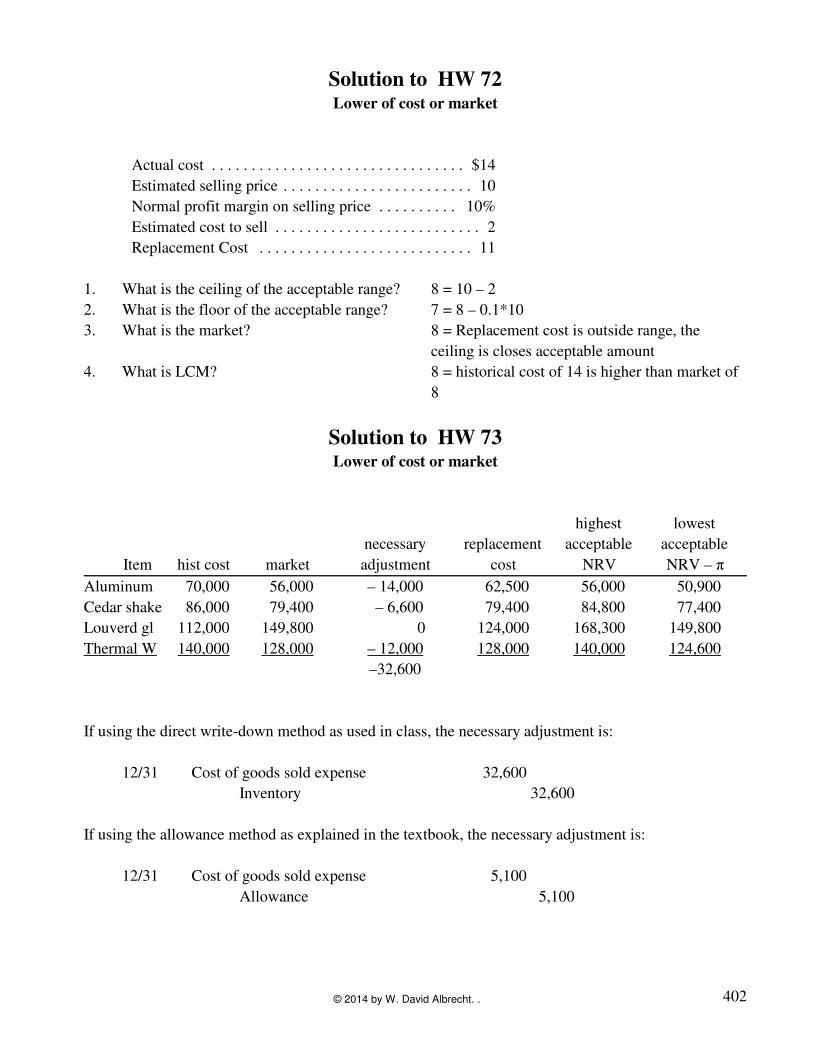

Solution to HW 72Lower of cost or market

Actual cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $14

Estimated selling price . . . . . . . . . . . . . . . . . . . . . . . . 10

Normal profit margin on selling price . . . . . . . . . . 10%

Estimated cost to sell . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Replacement Cost . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1. What is the ceiling of the acceptable range? 8 = 10 – 2

2. What is the floor of the acceptable range? 7 = 8 – 0.1*10

3. What is the market? 8 = Replacement cost is outside range, the

ceiling is closes acceptable amount

4. What is LCM? 8 = historical cost of 14 is higher than market of

8

Solution to HW 73Lower of cost or market

highest lowest

necessary replacement acceptable acceptable

Item hist cost market adjustment cost NRV NRV – π

Aluminum 70,000 56,000 – 14,000 62,500 56,000 50,900

Cedar shake 86,000 79,400 – 6,600 79,400 84,800 77,400

Louverd gl 112,000 149,800 0 124,000 168,300 149,800

Thermal W 140,000 128,000 – 12,000 128,000 140,000 124,600

–32,600

If using the direct write-down method as used in class, the necessary adjustment is:

12/31 Cost of goods sold expense 32,600

Inventory 32,600

If using the allowance method as explained in the textbook, the necessary adjustment is:

12/31 Cost of goods sold expense 5,100

Allowance 5,100

402© 2014 by W. David Albrecht. .

Professor Authored Problem Solutions

Intermediate Accounting 2

Retail Inventory Method & LCM

Solution to Problem 67Turnover Ratios

Inventory turnover ratio = CGS ÷ Avg inventory

= 160,000 ÷ 20,000

= 8.0

Days sales in EI = Avg inventory ÷ (CGS ÷365)

= 20,000 ÷ (160,000 ÷ 365)

= 20,000 ÷ 438.3562

= 45.625

AR turnover ratio = Sales ÷ Avg AR

= 270,000 ÷ 66,000

= 4.0909

Average collection period = Avg AR ÷ (Sales ÷ 365)

= 66,000 ÷ (270,000 ÷ 365)

= 66,000 ÷ 739.7260

= 89.2222

393© 2014 by W. David Albrecht. .

Solution to Problem 68Retail Inventory Method

@ cost @ retail

Beginning inventory $10,500 $42,000

Purchases (gross) 465,000 892,000

Freight in 12,000 ---

Markups --- 52,000

Markdowns --- 112,000

Good available for sale 487,500 874,000

Sales (net) --- 722,000

Sales discounts --- 7,000

Ending inventory @ retail 145,000

We need to subtract sales @ gross. If sales is listed at gross, we ignore sales discounts. If sales is listed

at net, we add sales discounts to sales@net to get sales @ gross.

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (465,000 + 12,000) ÷ (892,000 + 52,000 ! 112,000)

= 0.5733

EI @ FIFO cost = 145,000 * 0.5733

= 83,131

CGS = 487,500 – 83,131

= 484,369

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000 ! 112,000)

= 0.5578

EI @ WA cost = 145,000 * 0.55578

= 80,878

CGS = 487,500 – 80,878

= 406,622

394© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000)

= 0.4944

EI @ WALCM cost = 145,000 * 0.4944

= 71,691

CGS = 487,500 – 71,691

= 415,809

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (465,000 + 12,000) ÷ (892,000 + 52,000)

= 0.5053

EI @ FIFOLCM cost = 145,000 * 0.5733

= 73,268

CGS = 487,500 – 73,268

= 414,132

395© 2014 by W. David Albrecht. .

Solution to HW 69Retail inventory method

@ cost @ retail

Beginning inventory $52,320 $96,444

Purchases (gross) 631,000 1,079,327

Freight in 52,000 ---

Markups --- 72,000

Markdowns --- 146,000

Good available for sale 735,320 1,101,771

Sales gross) --- 978,432

Sales discounts --- 97,000

Ending inventory @ retail 123,339

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000 ! 146,000)

= 0.6794

EI @ FIFO cost = 123,339 * 0.6794

= 83,797

CGS = 735,320 – 83,797

= 651,523

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000 ! 146,000)

= 0.6674

EI @ WA cost = 123,339 * 0.6674

= 82,316

CGS = 735,320 – 82,316

= 651,004

396© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000)

= 0.5893

EI @ WALCM cost = 123,339 * .5893

= 72,684

CGS = 735,320 – 72,684

= 662,636

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000)

= 0.5932

EI @ FIFOLCM cost = 123,339* 0.5932

= 73,164

CGS = 735,320 – 73,164

= 662,156

397© 2014 by W. David Albrecht. .

Solution to HW 70Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 300 2.50 2.60 3.00 0.25 1.00

B 500 2.50 2.90 2.75 0.15 0.50

C 150 5.40 5.30 5.90 0.20 1.20

D 450 3.50 3.25 4.50 0.40 0.65

E 280 2.65 2.55 4.00 0.30 0.80

F 375 4.30 4.20 4.60 0.50 1.25

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 300 2.50 750

B 500 2.50 1,250

C 150 5.40 810

D 450 3.50 1,575

E 280 2.65 742

F 375 4.30 1,613

6,740

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

market replacement acceptable acceptable

Item # units cost/unit cost/unit cost / unit NRV NRV – π

A 300 2.50 2.60 2.60 2.75 1.75

B 500 2.50 2.60 2.90 2.60 2.10

C 150 5.40 5.30 5.30 5.70 4.50

D 450 3.50 3.45 3.25 4.10 3.45

E 280 2.65 2.90 2.55 3.70 2.90

F 375 4.30 4.10 4.20 4.10 2.85

398© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 15

Inventory 15

adjustment for C (150 units * 0.10 / unit)

12/31/14 Cost of goods sold expense 22.50

Inventory 22.50

adjustment for D (450 units * 0.05 / unit)

12/31/14 Cost of goods sold expense 75

Inventory 75

adjustment for F (375 units * 0.20 / unit)

Total adjusted value for inventory

Balance before adjustment 6,740.00

Write-down –112.50

Adjusted balance 6,627.50

399© 2014 by W. David Albrecht. .

Solution to HW 71Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 400 14.30 15.60 22.15 0.00 10%

B 200 9.55 9.70 10.33 1.55 5%

C 350 22.10 20.30 28.00 2.80 25%

D 120 13.75 13.25 16.50 1.00 10%

E 810 8.25 2.55 4.00 0.30 15%

F 550 24.30 34.20 38.50 3.85 15%

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 400 14.30 5,720

B 200 9.55 1,910

C 350 22.10 7,735

D 120 13.75 1,650

E 810 8.25 6,683

F 550 24.30 13,365

37,063

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

replacement acceptable acceptable

Item # units cost / unit market / unit cost / unit NRV NRV – π

A 400 14.30 19.93 15.60 22.15 19.93

B 200 9.55 8.78 9.70 8.78 7.75

C 350 22.10 20.20 20.30 25.20 18.20

D 120 13.75 13.85 13.25 15.50 13.85

E 810 8.25 3.10 2.55 3.70 3.10

F 550 24.30 28.87 34.20 34.65 28.87

400© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 154

Inventory 154

adjustment for B (200 units * 0.77 / unit)

12/31/14 Cost of goods sold expense 570

Inventory 570

adjustment for C (300 units * 1.90 / unit)

12/31/14 Cost of goods sold expense 4,172

Inventory 4,172

adjustment for E (810 units * 5.15 / unit)

Total adjusted value for inventory

Balance before adjustment 37,063

Write-down – 4,896

Adjusted balance 32,167

401© 2014 by W. David Albrecht. .

Solution to HW 72Lower of cost or market

Actual cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $14

Estimated selling price . . . . . . . . . . . . . . . . . . . . . . . . 10

Normal profit margin on selling price . . . . . . . . . . 10%

Estimated cost to sell . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Replacement Cost . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1. What is the ceiling of the acceptable range? 8 = 10 – 2

2. What is the floor of the acceptable range? 7 = 8 – 0.1*10

3. What is the market? 8 = Replacement cost is outside range, the

ceiling is closes acceptable amount

4. What is LCM? 8 = historical cost of 14 is higher than market of

8

Solution to HW 73Lower of cost or market

highest lowest

necessary replacement acceptable acceptable

Item hist cost market adjustment cost NRV NRV – π

Aluminum 70,000 56,000 – 14,000 62,500 56,000 50,900

Cedar shake 86,000 79,400 – 6,600 79,400 84,800 77,400

Louverd gl 112,000 149,800 0 124,000 168,300 149,800

Thermal W 140,000 128,000 – 12,000 128,000 140,000 124,600

–32,600

If using the direct write-down method as used in class, the necessary adjustment is:

12/31 Cost of goods sold expense 32,600

Inventory 32,600

If using the allowance method as explained in the textbook, the necessary adjustment is:

12/31 Cost of goods sold expense 5,100

Allowance 5,100

402© 2014 by W. David Albrecht. .

Professor Authored Problem Solutions

Intermediate Accounting 2

Retail Inventory Method & LCM

Solution to Problem 67Turnover Ratios

Inventory turnover ratio = CGS ÷ Avg inventory

= 160,000 ÷ 20,000

= 8.0

Days sales in EI = Avg inventory ÷ (CGS ÷365)

= 20,000 ÷ (160,000 ÷ 365)

= 20,000 ÷ 438.3562

= 45.625

AR turnover ratio = Sales ÷ Avg AR

= 270,000 ÷ 66,000

= 4.0909

Average collection period = Avg AR ÷ (Sales ÷ 365)

= 66,000 ÷ (270,000 ÷ 365)

= 66,000 ÷ 739.7260

= 89.2222

393© 2014 by W. David Albrecht. .

Solution to Problem 68Retail Inventory Method

@ cost @ retail

Beginning inventory $10,500 $42,000

Purchases (gross) 465,000 892,000

Freight in 12,000 ---

Markups --- 52,000

Markdowns --- 112,000

Good available for sale 487,500 874,000

Sales (net) --- 722,000

Sales discounts --- 7,000

Ending inventory @ retail 145,000

We need to subtract sales @ gross. If sales is listed at gross, we ignore sales discounts. If sales is listed

at net, we add sales discounts to sales@net to get sales @ gross.

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (465,000 + 12,000) ÷ (892,000 + 52,000 ! 112,000)

= 0.5733

EI @ FIFO cost = 145,000 * 0.5733

= 83,131

CGS = 487,500 – 83,131

= 484,369

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000 ! 112,000)

= 0.5578

EI @ WA cost = 145,000 * 0.55578

= 80,878

CGS = 487,500 – 80,878

= 406,622

394© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000)

= 0.4944

EI @ WALCM cost = 145,000 * 0.4944

= 71,691

CGS = 487,500 – 71,691

= 415,809

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (465,000 + 12,000) ÷ (892,000 + 52,000)

= 0.5053

EI @ FIFOLCM cost = 145,000 * 0.5733

= 73,268

CGS = 487,500 – 73,268

= 414,132

395© 2014 by W. David Albrecht. .

Solution to HW 69Retail inventory method

@ cost @ retail

Beginning inventory $52,320 $96,444

Purchases (gross) 631,000 1,079,327

Freight in 52,000 ---

Markups --- 72,000

Markdowns --- 146,000

Good available for sale 735,320 1,101,771

Sales gross) --- 978,432

Sales discounts --- 97,000

Ending inventory @ retail 123,339

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000 ! 146,000)

= 0.6794

EI @ FIFO cost = 123,339 * 0.6794

= 83,797

CGS = 735,320 – 83,797

= 651,523

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000 ! 146,000)

= 0.6674

EI @ WA cost = 123,339 * 0.6674

= 82,316

CGS = 735,320 – 82,316

= 651,004

396© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000)

= 0.5893

EI @ WALCM cost = 123,339 * .5893

= 72,684

CGS = 735,320 – 72,684

= 662,636

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000)

= 0.5932

EI @ FIFOLCM cost = 123,339* 0.5932

= 73,164

CGS = 735,320 – 73,164

= 662,156

397© 2014 by W. David Albrecht. .

Solution to HW 70Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 300 2.50 2.60 3.00 0.25 1.00

B 500 2.50 2.90 2.75 0.15 0.50

C 150 5.40 5.30 5.90 0.20 1.20

D 450 3.50 3.25 4.50 0.40 0.65

E 280 2.65 2.55 4.00 0.30 0.80

F 375 4.30 4.20 4.60 0.50 1.25

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 300 2.50 750

B 500 2.50 1,250

C 150 5.40 810

D 450 3.50 1,575

E 280 2.65 742

F 375 4.30 1,613

6,740

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

market replacement acceptable acceptable

Item # units cost/unit cost/unit cost / unit NRV NRV – π

A 300 2.50 2.60 2.60 2.75 1.75

B 500 2.50 2.60 2.90 2.60 2.10

C 150 5.40 5.30 5.30 5.70 4.50

D 450 3.50 3.45 3.25 4.10 3.45

E 280 2.65 2.90 2.55 3.70 2.90

F 375 4.30 4.10 4.20 4.10 2.85

398© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 15

Inventory 15

adjustment for C (150 units * 0.10 / unit)

12/31/14 Cost of goods sold expense 22.50

Inventory 22.50

adjustment for D (450 units * 0.05 / unit)

12/31/14 Cost of goods sold expense 75

Inventory 75

adjustment for F (375 units * 0.20 / unit)

Total adjusted value for inventory

Balance before adjustment 6,740.00

Write-down –112.50

Adjusted balance 6,627.50

399© 2014 by W. David Albrecht. .

Solution to HW 71Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 400 14.30 15.60 22.15 0.00 10%

B 200 9.55 9.70 10.33 1.55 5%

C 350 22.10 20.30 28.00 2.80 25%

D 120 13.75 13.25 16.50 1.00 10%

E 810 8.25 2.55 4.00 0.30 15%

F 550 24.30 34.20 38.50 3.85 15%

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 400 14.30 5,720

B 200 9.55 1,910

C 350 22.10 7,735

D 120 13.75 1,650

E 810 8.25 6,683

F 550 24.30 13,365

37,063

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

replacement acceptable acceptable

Item # units cost / unit market / unit cost / unit NRV NRV – π

A 400 14.30 19.93 15.60 22.15 19.93

B 200 9.55 8.78 9.70 8.78 7.75

C 350 22.10 20.20 20.30 25.20 18.20

D 120 13.75 13.85 13.25 15.50 13.85

E 810 8.25 3.10 2.55 3.70 3.10

F 550 24.30 28.87 34.20 34.65 28.87

400© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 154

Inventory 154

adjustment for B (200 units * 0.77 / unit)

12/31/14 Cost of goods sold expense 570

Inventory 570

adjustment for C (300 units * 1.90 / unit)

12/31/14 Cost of goods sold expense 4,172

Inventory 4,172

adjustment for E (810 units * 5.15 / unit)

Total adjusted value for inventory

Balance before adjustment 37,063

Write-down – 4,896

Adjusted balance 32,167

401© 2014 by W. David Albrecht. .

Solution to HW 72Lower of cost or market

Actual cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $14

Estimated selling price . . . . . . . . . . . . . . . . . . . . . . . . 10

Normal profit margin on selling price . . . . . . . . . . 10%

Estimated cost to sell . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Replacement Cost . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1. What is the ceiling of the acceptable range? 8 = 10 – 2

2. What is the floor of the acceptable range? 7 = 8 – 0.1*10

3. What is the market? 8 = Replacement cost is outside range, the

ceiling is closes acceptable amount

4. What is LCM? 8 = historical cost of 14 is higher than market of

8

Solution to HW 73Lower of cost or market

highest lowest

necessary replacement acceptable acceptable

Item hist cost market adjustment cost NRV NRV – π

Aluminum 70,000 56,000 – 14,000 62,500 56,000 50,900

Cedar shake 86,000 79,400 – 6,600 79,400 84,800 77,400

Louverd gl 112,000 149,800 0 124,000 168,300 149,800

Thermal W 140,000 128,000 – 12,000 128,000 140,000 124,600

–32,600

If using the direct write-down method as used in class, the necessary adjustment is:

12/31 Cost of goods sold expense 32,600

Inventory 32,600

If using the allowance method as explained in the textbook, the necessary adjustment is:

12/31 Cost of goods sold expense 5,100

Allowance 5,100

402© 2014 by W. David Albrecht. .

Professor Authored Problem Solutions

Intermediate Accounting 2

Retail Inventory Method & LCM

Solution to Problem 67Turnover Ratios

Inventory turnover ratio = CGS ÷ Avg inventory

= 160,000 ÷ 20,000

= 8.0

Days sales in EI = Avg inventory ÷ (CGS ÷365)

= 20,000 ÷ (160,000 ÷ 365)

= 20,000 ÷ 438.3562

= 45.625

AR turnover ratio = Sales ÷ Avg AR

= 270,000 ÷ 66,000

= 4.0909

Average collection period = Avg AR ÷ (Sales ÷ 365)

= 66,000 ÷ (270,000 ÷ 365)

= 66,000 ÷ 739.7260

= 89.2222

393© 2014 by W. David Albrecht. .

Solution to Problem 68Retail Inventory Method

@ cost @ retail

Beginning inventory $10,500 $42,000

Purchases (gross) 465,000 892,000

Freight in 12,000 ---

Markups --- 52,000

Markdowns --- 112,000

Good available for sale 487,500 874,000

Sales (net) --- 722,000

Sales discounts --- 7,000

Ending inventory @ retail 145,000

We need to subtract sales @ gross. If sales is listed at gross, we ignore sales discounts. If sales is listed

at net, we add sales discounts to sales@net to get sales @ gross.

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (465,000 + 12,000) ÷ (892,000 + 52,000 ! 112,000)

= 0.5733

EI @ FIFO cost = 145,000 * 0.5733

= 83,131

CGS = 487,500 – 83,131

= 484,369

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000 ! 112,000)

= 0.5578

EI @ WA cost = 145,000 * 0.55578

= 80,878

CGS = 487,500 – 80,878

= 406,622

394© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000)

= 0.4944

EI @ WALCM cost = 145,000 * 0.4944

= 71,691

CGS = 487,500 – 71,691

= 415,809

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (465,000 + 12,000) ÷ (892,000 + 52,000)

= 0.5053

EI @ FIFOLCM cost = 145,000 * 0.5733

= 73,268

CGS = 487,500 – 73,268

= 414,132

395© 2014 by W. David Albrecht. .

Solution to HW 69Retail inventory method

@ cost @ retail

Beginning inventory $52,320 $96,444

Purchases (gross) 631,000 1,079,327

Freight in 52,000 ---

Markups --- 72,000

Markdowns --- 146,000

Good available for sale 735,320 1,101,771

Sales gross) --- 978,432

Sales discounts --- 97,000

Ending inventory @ retail 123,339

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000 ! 146,000)

= 0.6794

EI @ FIFO cost = 123,339 * 0.6794

= 83,797

CGS = 735,320 – 83,797

= 651,523

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000 ! 146,000)

= 0.6674

EI @ WA cost = 123,339 * 0.6674

= 82,316

CGS = 735,320 – 82,316

= 651,004

396© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000)

= 0.5893

EI @ WALCM cost = 123,339 * .5893

= 72,684

CGS = 735,320 – 72,684

= 662,636

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000)

= 0.5932

EI @ FIFOLCM cost = 123,339* 0.5932

= 73,164

CGS = 735,320 – 73,164

= 662,156

397© 2014 by W. David Albrecht. .

Solution to HW 70Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 300 2.50 2.60 3.00 0.25 1.00

B 500 2.50 2.90 2.75 0.15 0.50

C 150 5.40 5.30 5.90 0.20 1.20

D 450 3.50 3.25 4.50 0.40 0.65

E 280 2.65 2.55 4.00 0.30 0.80

F 375 4.30 4.20 4.60 0.50 1.25

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 300 2.50 750

B 500 2.50 1,250

C 150 5.40 810

D 450 3.50 1,575

E 280 2.65 742

F 375 4.30 1,613

6,740

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

market replacement acceptable acceptable

Item # units cost/unit cost/unit cost / unit NRV NRV – π

A 300 2.50 2.60 2.60 2.75 1.75

B 500 2.50 2.60 2.90 2.60 2.10

C 150 5.40 5.30 5.30 5.70 4.50

D 450 3.50 3.45 3.25 4.10 3.45

E 280 2.65 2.90 2.55 3.70 2.90

F 375 4.30 4.10 4.20 4.10 2.85

398© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 15

Inventory 15

adjustment for C (150 units * 0.10 / unit)

12/31/14 Cost of goods sold expense 22.50

Inventory 22.50

adjustment for D (450 units * 0.05 / unit)

12/31/14 Cost of goods sold expense 75

Inventory 75

adjustment for F (375 units * 0.20 / unit)

Total adjusted value for inventory

Balance before adjustment 6,740.00

Write-down –112.50

Adjusted balance 6,627.50

399© 2014 by W. David Albrecht. .

Solution to HW 71Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 400 14.30 15.60 22.15 0.00 10%

B 200 9.55 9.70 10.33 1.55 5%

C 350 22.10 20.30 28.00 2.80 25%

D 120 13.75 13.25 16.50 1.00 10%

E 810 8.25 2.55 4.00 0.30 15%

F 550 24.30 34.20 38.50 3.85 15%

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 400 14.30 5,720

B 200 9.55 1,910

C 350 22.10 7,735

D 120 13.75 1,650

E 810 8.25 6,683

F 550 24.30 13,365

37,063

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

replacement acceptable acceptable

Item # units cost / unit market / unit cost / unit NRV NRV – π

A 400 14.30 19.93 15.60 22.15 19.93

B 200 9.55 8.78 9.70 8.78 7.75

C 350 22.10 20.20 20.30 25.20 18.20

D 120 13.75 13.85 13.25 15.50 13.85

E 810 8.25 3.10 2.55 3.70 3.10

F 550 24.30 28.87 34.20 34.65 28.87

400© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 154

Inventory 154

adjustment for B (200 units * 0.77 / unit)

12/31/14 Cost of goods sold expense 570

Inventory 570

adjustment for C (300 units * 1.90 / unit)

12/31/14 Cost of goods sold expense 4,172

Inventory 4,172

adjustment for E (810 units * 5.15 / unit)

Total adjusted value for inventory

Balance before adjustment 37,063

Write-down – 4,896

Adjusted balance 32,167

401© 2014 by W. David Albrecht. .

Solution to HW 72Lower of cost or market

Actual cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $14

Estimated selling price . . . . . . . . . . . . . . . . . . . . . . . . 10

Normal profit margin on selling price . . . . . . . . . . 10%

Estimated cost to sell . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Replacement Cost . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1. What is the ceiling of the acceptable range? 8 = 10 – 2

2. What is the floor of the acceptable range? 7 = 8 – 0.1*10

3. What is the market? 8 = Replacement cost is outside range, the

ceiling is closes acceptable amount

4. What is LCM? 8 = historical cost of 14 is higher than market of

8

Solution to HW 73Lower of cost or market

highest lowest

necessary replacement acceptable acceptable

Item hist cost market adjustment cost NRV NRV – π

Aluminum 70,000 56,000 – 14,000 62,500 56,000 50,900

Cedar shake 86,000 79,400 – 6,600 79,400 84,800 77,400

Louverd gl 112,000 149,800 0 124,000 168,300 149,800

Thermal W 140,000 128,000 – 12,000 128,000 140,000 124,600

–32,600

If using the direct write-down method as used in class, the necessary adjustment is:

12/31 Cost of goods sold expense 32,600

Inventory 32,600

If using the allowance method as explained in the textbook, the necessary adjustment is:

12/31 Cost of goods sold expense 5,100

Allowance 5,100

402© 2014 by W. David Albrecht. .

Professor Authored Problem Solutions

Intermediate Accounting 2

Retail Inventory Method & LCM

Solution to Problem 67Turnover Ratios

Inventory turnover ratio = CGS ÷ Avg inventory

= 160,000 ÷ 20,000

= 8.0

Days sales in EI = Avg inventory ÷ (CGS ÷365)

= 20,000 ÷ (160,000 ÷ 365)

= 20,000 ÷ 438.3562

= 45.625

AR turnover ratio = Sales ÷ Avg AR

= 270,000 ÷ 66,000

= 4.0909

Average collection period = Avg AR ÷ (Sales ÷ 365)

= 66,000 ÷ (270,000 ÷ 365)

= 66,000 ÷ 739.7260

= 89.2222

393© 2014 by W. David Albrecht. .

Solution to Problem 68Retail Inventory Method

@ cost @ retail

Beginning inventory $10,500 $42,000

Purchases (gross) 465,000 892,000

Freight in 12,000 ---

Markups --- 52,000

Markdowns --- 112,000

Good available for sale 487,500 874,000

Sales (net) --- 722,000

Sales discounts --- 7,000

Ending inventory @ retail 145,000

We need to subtract sales @ gross. If sales is listed at gross, we ignore sales discounts. If sales is listed

at net, we add sales discounts to sales@net to get sales @ gross.

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (465,000 + 12,000) ÷ (892,000 + 52,000 ! 112,000)

= 0.5733

EI @ FIFO cost = 145,000 * 0.5733

= 83,131

CGS = 487,500 – 83,131

= 484,369

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000 ! 112,000)

= 0.5578

EI @ WA cost = 145,000 * 0.55578

= 80,878

CGS = 487,500 – 80,878

= 406,622

394© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000)

= 0.4944

EI @ WALCM cost = 145,000 * 0.4944

= 71,691

CGS = 487,500 – 71,691

= 415,809

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (465,000 + 12,000) ÷ (892,000 + 52,000)

= 0.5053

EI @ FIFOLCM cost = 145,000 * 0.5733

= 73,268

CGS = 487,500 – 73,268

= 414,132

395© 2014 by W. David Albrecht. .

Solution to HW 69Retail inventory method

@ cost @ retail

Beginning inventory $52,320 $96,444

Purchases (gross) 631,000 1,079,327

Freight in 52,000 ---

Markups --- 72,000

Markdowns --- 146,000

Good available for sale 735,320 1,101,771

Sales gross) --- 978,432

Sales discounts --- 97,000

Ending inventory @ retail 123,339

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000 ! 146,000)

= 0.6794

EI @ FIFO cost = 123,339 * 0.6794

= 83,797

CGS = 735,320 – 83,797

= 651,523

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000 ! 146,000)

= 0.6674

EI @ WA cost = 123,339 * 0.6674

= 82,316

CGS = 735,320 – 82,316

= 651,004

396© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000)

= 0.5893

EI @ WALCM cost = 123,339 * .5893

= 72,684

CGS = 735,320 – 72,684

= 662,636

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000)

= 0.5932

EI @ FIFOLCM cost = 123,339* 0.5932

= 73,164

CGS = 735,320 – 73,164

= 662,156

397© 2014 by W. David Albrecht. .

Solution to HW 70Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 300 2.50 2.60 3.00 0.25 1.00

B 500 2.50 2.90 2.75 0.15 0.50

C 150 5.40 5.30 5.90 0.20 1.20

D 450 3.50 3.25 4.50 0.40 0.65

E 280 2.65 2.55 4.00 0.30 0.80

F 375 4.30 4.20 4.60 0.50 1.25

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 300 2.50 750

B 500 2.50 1,250

C 150 5.40 810

D 450 3.50 1,575

E 280 2.65 742

F 375 4.30 1,613

6,740

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

market replacement acceptable acceptable

Item # units cost/unit cost/unit cost / unit NRV NRV – π

A 300 2.50 2.60 2.60 2.75 1.75

B 500 2.50 2.60 2.90 2.60 2.10

C 150 5.40 5.30 5.30 5.70 4.50

D 450 3.50 3.45 3.25 4.10 3.45

E 280 2.65 2.90 2.55 3.70 2.90

F 375 4.30 4.10 4.20 4.10 2.85

398© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 15

Inventory 15

adjustment for C (150 units * 0.10 / unit)

12/31/14 Cost of goods sold expense 22.50

Inventory 22.50

adjustment for D (450 units * 0.05 / unit)

12/31/14 Cost of goods sold expense 75

Inventory 75

adjustment for F (375 units * 0.20 / unit)

Total adjusted value for inventory

Balance before adjustment 6,740.00

Write-down –112.50

Adjusted balance 6,627.50

399© 2014 by W. David Albrecht. .

Solution to HW 71Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 400 14.30 15.60 22.15 0.00 10%

B 200 9.55 9.70 10.33 1.55 5%

C 350 22.10 20.30 28.00 2.80 25%

D 120 13.75 13.25 16.50 1.00 10%

E 810 8.25 2.55 4.00 0.30 15%

F 550 24.30 34.20 38.50 3.85 15%

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 400 14.30 5,720

B 200 9.55 1,910

C 350 22.10 7,735

D 120 13.75 1,650

E 810 8.25 6,683

F 550 24.30 13,365

37,063

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

replacement acceptable acceptable

Item # units cost / unit market / unit cost / unit NRV NRV – π

A 400 14.30 19.93 15.60 22.15 19.93

B 200 9.55 8.78 9.70 8.78 7.75

C 350 22.10 20.20 20.30 25.20 18.20

D 120 13.75 13.85 13.25 15.50 13.85

E 810 8.25 3.10 2.55 3.70 3.10

F 550 24.30 28.87 34.20 34.65 28.87

400© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 154

Inventory 154

adjustment for B (200 units * 0.77 / unit)

12/31/14 Cost of goods sold expense 570

Inventory 570

adjustment for C (300 units * 1.90 / unit)

12/31/14 Cost of goods sold expense 4,172

Inventory 4,172

adjustment for E (810 units * 5.15 / unit)

Total adjusted value for inventory

Balance before adjustment 37,063

Write-down – 4,896

Adjusted balance 32,167

401© 2014 by W. David Albrecht. .

Solution to HW 72Lower of cost or market

Actual cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $14

Estimated selling price . . . . . . . . . . . . . . . . . . . . . . . . 10

Normal profit margin on selling price . . . . . . . . . . 10%

Estimated cost to sell . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Replacement Cost . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1. What is the ceiling of the acceptable range? 8 = 10 – 2

2. What is the floor of the acceptable range? 7 = 8 – 0.1*10

3. What is the market? 8 = Replacement cost is outside range, the

ceiling is closes acceptable amount

4. What is LCM? 8 = historical cost of 14 is higher than market of

8

Solution to HW 73Lower of cost or market

highest lowest

necessary replacement acceptable acceptable

Item hist cost market adjustment cost NRV NRV – π

Aluminum 70,000 56,000 – 14,000 62,500 56,000 50,900

Cedar shake 86,000 79,400 – 6,600 79,400 84,800 77,400

Louverd gl 112,000 149,800 0 124,000 168,300 149,800

Thermal W 140,000 128,000 – 12,000 128,000 140,000 124,600

–32,600

If using the direct write-down method as used in class, the necessary adjustment is:

12/31 Cost of goods sold expense 32,600

Inventory 32,600

If using the allowance method as explained in the textbook, the necessary adjustment is:

12/31 Cost of goods sold expense 5,100

Allowance 5,100

402© 2014 by W. David Albrecht. .

Professor Authored Problem Solutions

Intermediate Accounting 2

Retail Inventory Method & LCM

Solution to Problem 67Turnover Ratios

Inventory turnover ratio = CGS ÷ Avg inventory

= 160,000 ÷ 20,000

= 8.0

Days sales in EI = Avg inventory ÷ (CGS ÷365)

= 20,000 ÷ (160,000 ÷ 365)

= 20,000 ÷ 438.3562

= 45.625

AR turnover ratio = Sales ÷ Avg AR

= 270,000 ÷ 66,000

= 4.0909

Average collection period = Avg AR ÷ (Sales ÷ 365)

= 66,000 ÷ (270,000 ÷ 365)

= 66,000 ÷ 739.7260

= 89.2222

393© 2014 by W. David Albrecht. .

Solution to Problem 68Retail Inventory Method

@ cost @ retail

Beginning inventory $10,500 $42,000

Purchases (gross) 465,000 892,000

Freight in 12,000 ---

Markups --- 52,000

Markdowns --- 112,000

Good available for sale 487,500 874,000

Sales (net) --- 722,000

Sales discounts --- 7,000

Ending inventory @ retail 145,000

We need to subtract sales @ gross. If sales is listed at gross, we ignore sales discounts. If sales is listed

at net, we add sales discounts to sales@net to get sales @ gross.

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (465,000 + 12,000) ÷ (892,000 + 52,000 ! 112,000)

= 0.5733

EI @ FIFO cost = 145,000 * 0.5733

= 83,131

CGS = 487,500 – 83,131

= 484,369

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000 ! 112,000)

= 0.5578

EI @ WA cost = 145,000 * 0.55578

= 80,878

CGS = 487,500 – 80,878

= 406,622

394© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000)

= 0.4944

EI @ WALCM cost = 145,000 * 0.4944

= 71,691

CGS = 487,500 – 71,691

= 415,809

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (465,000 + 12,000) ÷ (892,000 + 52,000)

= 0.5053

EI @ FIFOLCM cost = 145,000 * 0.5733

= 73,268

CGS = 487,500 – 73,268

= 414,132

395© 2014 by W. David Albrecht. .

Solution to HW 69Retail inventory method

@ cost @ retail

Beginning inventory $52,320 $96,444

Purchases (gross) 631,000 1,079,327

Freight in 52,000 ---

Markups --- 72,000

Markdowns --- 146,000

Good available for sale 735,320 1,101,771

Sales gross) --- 978,432

Sales discounts --- 97,000

Ending inventory @ retail 123,339

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000 ! 146,000)

= 0.6794

EI @ FIFO cost = 123,339 * 0.6794

= 83,797

CGS = 735,320 – 83,797

= 651,523

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000 ! 146,000)

= 0.6674

EI @ WA cost = 123,339 * 0.6674

= 82,316

CGS = 735,320 – 82,316

= 651,004

396© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000)

= 0.5893

EI @ WALCM cost = 123,339 * .5893

= 72,684

CGS = 735,320 – 72,684

= 662,636

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000)

= 0.5932

EI @ FIFOLCM cost = 123,339* 0.5932

= 73,164

CGS = 735,320 – 73,164

= 662,156

397© 2014 by W. David Albrecht. .

Solution to HW 70Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 300 2.50 2.60 3.00 0.25 1.00

B 500 2.50 2.90 2.75 0.15 0.50

C 150 5.40 5.30 5.90 0.20 1.20

D 450 3.50 3.25 4.50 0.40 0.65

E 280 2.65 2.55 4.00 0.30 0.80

F 375 4.30 4.20 4.60 0.50 1.25

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 300 2.50 750

B 500 2.50 1,250

C 150 5.40 810

D 450 3.50 1,575

E 280 2.65 742

F 375 4.30 1,613

6,740

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

market replacement acceptable acceptable

Item # units cost/unit cost/unit cost / unit NRV NRV – π

A 300 2.50 2.60 2.60 2.75 1.75

B 500 2.50 2.60 2.90 2.60 2.10

C 150 5.40 5.30 5.30 5.70 4.50

D 450 3.50 3.45 3.25 4.10 3.45

E 280 2.65 2.90 2.55 3.70 2.90

F 375 4.30 4.10 4.20 4.10 2.85

398© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 15

Inventory 15

adjustment for C (150 units * 0.10 / unit)

12/31/14 Cost of goods sold expense 22.50

Inventory 22.50

adjustment for D (450 units * 0.05 / unit)

12/31/14 Cost of goods sold expense 75

Inventory 75

adjustment for F (375 units * 0.20 / unit)

Total adjusted value for inventory

Balance before adjustment 6,740.00

Write-down –112.50

Adjusted balance 6,627.50

399© 2014 by W. David Albrecht. .

Solution to HW 71Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 400 14.30 15.60 22.15 0.00 10%

B 200 9.55 9.70 10.33 1.55 5%

C 350 22.10 20.30 28.00 2.80 25%

D 120 13.75 13.25 16.50 1.00 10%

E 810 8.25 2.55 4.00 0.30 15%

F 550 24.30 34.20 38.50 3.85 15%

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 400 14.30 5,720

B 200 9.55 1,910

C 350 22.10 7,735

D 120 13.75 1,650

E 810 8.25 6,683

F 550 24.30 13,365

37,063

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

replacement acceptable acceptable

Item # units cost / unit market / unit cost / unit NRV NRV – π

A 400 14.30 19.93 15.60 22.15 19.93

B 200 9.55 8.78 9.70 8.78 7.75

C 350 22.10 20.20 20.30 25.20 18.20

D 120 13.75 13.85 13.25 15.50 13.85

E 810 8.25 3.10 2.55 3.70 3.10

F 550 24.30 28.87 34.20 34.65 28.87

400© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 154

Inventory 154

adjustment for B (200 units * 0.77 / unit)

12/31/14 Cost of goods sold expense 570

Inventory 570

adjustment for C (300 units * 1.90 / unit)

12/31/14 Cost of goods sold expense 4,172

Inventory 4,172

adjustment for E (810 units * 5.15 / unit)

Total adjusted value for inventory

Balance before adjustment 37,063

Write-down – 4,896

Adjusted balance 32,167

401© 2014 by W. David Albrecht. .

Solution to HW 72Lower of cost or market

Actual cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $14

Estimated selling price . . . . . . . . . . . . . . . . . . . . . . . . 10

Normal profit margin on selling price . . . . . . . . . . 10%

Estimated cost to sell . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Replacement Cost . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1. What is the ceiling of the acceptable range? 8 = 10 – 2

2. What is the floor of the acceptable range? 7 = 8 – 0.1*10

3. What is the market? 8 = Replacement cost is outside range, the

ceiling is closes acceptable amount

4. What is LCM? 8 = historical cost of 14 is higher than market of

8

Solution to HW 73Lower of cost or market

highest lowest

necessary replacement acceptable acceptable

Item hist cost market adjustment cost NRV NRV – π

Aluminum 70,000 56,000 – 14,000 62,500 56,000 50,900

Cedar shake 86,000 79,400 – 6,600 79,400 84,800 77,400

Louverd gl 112,000 149,800 0 124,000 168,300 149,800

Thermal W 140,000 128,000 – 12,000 128,000 140,000 124,600

–32,600

If using the direct write-down method as used in class, the necessary adjustment is:

12/31 Cost of goods sold expense 32,600

Inventory 32,600

If using the allowance method as explained in the textbook, the necessary adjustment is:

12/31 Cost of goods sold expense 5,100

Allowance 5,100

402© 2014 by W. David Albrecht. .

Professor Authored Problem Solutions

Intermediate Accounting 2

Retail Inventory Method & LCM

Solution to Problem 67Turnover Ratios

Inventory turnover ratio = CGS ÷ Avg inventory

= 160,000 ÷ 20,000

= 8.0

Days sales in EI = Avg inventory ÷ (CGS ÷365)

= 20,000 ÷ (160,000 ÷ 365)

= 20,000 ÷ 438.3562

= 45.625

AR turnover ratio = Sales ÷ Avg AR

= 270,000 ÷ 66,000

= 4.0909

Average collection period = Avg AR ÷ (Sales ÷ 365)

= 66,000 ÷ (270,000 ÷ 365)

= 66,000 ÷ 739.7260

= 89.2222

393© 2014 by W. David Albrecht. .

Solution to Problem 68Retail Inventory Method

@ cost @ retail

Beginning inventory $10,500 $42,000

Purchases (gross) 465,000 892,000

Freight in 12,000 ---

Markups --- 52,000

Markdowns --- 112,000

Good available for sale 487,500 874,000

Sales (net) --- 722,000

Sales discounts --- 7,000

Ending inventory @ retail 145,000

We need to subtract sales @ gross. If sales is listed at gross, we ignore sales discounts. If sales is listed

at net, we add sales discounts to sales@net to get sales @ gross.

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (465,000 + 12,000) ÷ (892,000 + 52,000 ! 112,000)

= 0.5733

EI @ FIFO cost = 145,000 * 0.5733

= 83,131

CGS = 487,500 – 83,131

= 484,369

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000 ! 112,000)

= 0.5578

EI @ WA cost = 145,000 * 0.55578

= 80,878

CGS = 487,500 – 80,878

= 406,622

394© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000)

= 0.4944

EI @ WALCM cost = 145,000 * 0.4944

= 71,691

CGS = 487,500 – 71,691

= 415,809

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (465,000 + 12,000) ÷ (892,000 + 52,000)

= 0.5053

EI @ FIFOLCM cost = 145,000 * 0.5733

= 73,268

CGS = 487,500 – 73,268

= 414,132

395© 2014 by W. David Albrecht. .

Solution to HW 69Retail inventory method

@ cost @ retail

Beginning inventory $52,320 $96,444

Purchases (gross) 631,000 1,079,327

Freight in 52,000 ---

Markups --- 72,000

Markdowns --- 146,000

Good available for sale 735,320 1,101,771

Sales gross) --- 978,432

Sales discounts --- 97,000

Ending inventory @ retail 123,339

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000 ! 146,000)

= 0.6794

EI @ FIFO cost = 123,339 * 0.6794

= 83,797

CGS = 735,320 – 83,797

= 651,523

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000 ! 146,000)

= 0.6674

EI @ WA cost = 123,339 * 0.6674

= 82,316

CGS = 735,320 – 82,316

= 651,004

396© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000)

= 0.5893

EI @ WALCM cost = 123,339 * .5893

= 72,684

CGS = 735,320 – 72,684

= 662,636

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000)

= 0.5932

EI @ FIFOLCM cost = 123,339* 0.5932

= 73,164

CGS = 735,320 – 73,164

= 662,156

397© 2014 by W. David Albrecht. .

Solution to HW 70Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 300 2.50 2.60 3.00 0.25 1.00

B 500 2.50 2.90 2.75 0.15 0.50

C 150 5.40 5.30 5.90 0.20 1.20

D 450 3.50 3.25 4.50 0.40 0.65

E 280 2.65 2.55 4.00 0.30 0.80

F 375 4.30 4.20 4.60 0.50 1.25

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 300 2.50 750

B 500 2.50 1,250

C 150 5.40 810

D 450 3.50 1,575

E 280 2.65 742

F 375 4.30 1,613

6,740

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

market replacement acceptable acceptable

Item # units cost/unit cost/unit cost / unit NRV NRV – π

A 300 2.50 2.60 2.60 2.75 1.75

B 500 2.50 2.60 2.90 2.60 2.10

C 150 5.40 5.30 5.30 5.70 4.50

D 450 3.50 3.45 3.25 4.10 3.45

E 280 2.65 2.90 2.55 3.70 2.90

F 375 4.30 4.10 4.20 4.10 2.85

398© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 15

Inventory 15

adjustment for C (150 units * 0.10 / unit)

12/31/14 Cost of goods sold expense 22.50

Inventory 22.50

adjustment for D (450 units * 0.05 / unit)

12/31/14 Cost of goods sold expense 75

Inventory 75

adjustment for F (375 units * 0.20 / unit)

Total adjusted value for inventory

Balance before adjustment 6,740.00

Write-down –112.50

Adjusted balance 6,627.50

399© 2014 by W. David Albrecht. .

Solution to HW 71Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 400 14.30 15.60 22.15 0.00 10%

B 200 9.55 9.70 10.33 1.55 5%

C 350 22.10 20.30 28.00 2.80 25%

D 120 13.75 13.25 16.50 1.00 10%

E 810 8.25 2.55 4.00 0.30 15%

F 550 24.30 34.20 38.50 3.85 15%

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 400 14.30 5,720

B 200 9.55 1,910

C 350 22.10 7,735

D 120 13.75 1,650

E 810 8.25 6,683

F 550 24.30 13,365

37,063

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

replacement acceptable acceptable

Item # units cost / unit market / unit cost / unit NRV NRV – π

A 400 14.30 19.93 15.60 22.15 19.93

B 200 9.55 8.78 9.70 8.78 7.75

C 350 22.10 20.20 20.30 25.20 18.20

D 120 13.75 13.85 13.25 15.50 13.85

E 810 8.25 3.10 2.55 3.70 3.10

F 550 24.30 28.87 34.20 34.65 28.87

400© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 154

Inventory 154

adjustment for B (200 units * 0.77 / unit)

12/31/14 Cost of goods sold expense 570

Inventory 570

adjustment for C (300 units * 1.90 / unit)

12/31/14 Cost of goods sold expense 4,172

Inventory 4,172

adjustment for E (810 units * 5.15 / unit)

Total adjusted value for inventory

Balance before adjustment 37,063

Write-down – 4,896

Adjusted balance 32,167

401© 2014 by W. David Albrecht. .

Solution to HW 72Lower of cost or market

Actual cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $14

Estimated selling price . . . . . . . . . . . . . . . . . . . . . . . . 10

Normal profit margin on selling price . . . . . . . . . . 10%

Estimated cost to sell . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Replacement Cost . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1. What is the ceiling of the acceptable range? 8 = 10 – 2

2. What is the floor of the acceptable range? 7 = 8 – 0.1*10

3. What is the market? 8 = Replacement cost is outside range, the

ceiling is closes acceptable amount

4. What is LCM? 8 = historical cost of 14 is higher than market of

8

Solution to HW 73Lower of cost or market

highest lowest

necessary replacement acceptable acceptable

Item hist cost market adjustment cost NRV NRV – π

Aluminum 70,000 56,000 – 14,000 62,500 56,000 50,900

Cedar shake 86,000 79,400 – 6,600 79,400 84,800 77,400

Louverd gl 112,000 149,800 0 124,000 168,300 149,800

Thermal W 140,000 128,000 – 12,000 128,000 140,000 124,600

–32,600

If using the direct write-down method as used in class, the necessary adjustment is:

12/31 Cost of goods sold expense 32,600

Inventory 32,600

If using the allowance method as explained in the textbook, the necessary adjustment is:

12/31 Cost of goods sold expense 5,100

Allowance 5,100

402© 2014 by W. David Albrecht. .

Professor Authored Problem Solutions

Intermediate Accounting 2

Retail Inventory Method & LCM

Solution to Problem 67Turnover Ratios

Inventory turnover ratio = CGS ÷ Avg inventory

= 160,000 ÷ 20,000

= 8.0

Days sales in EI = Avg inventory ÷ (CGS ÷365)

= 20,000 ÷ (160,000 ÷ 365)

= 20,000 ÷ 438.3562

= 45.625

AR turnover ratio = Sales ÷ Avg AR

= 270,000 ÷ 66,000

= 4.0909

Average collection period = Avg AR ÷ (Sales ÷ 365)

= 66,000 ÷ (270,000 ÷ 365)

= 66,000 ÷ 739.7260

= 89.2222

393© 2014 by W. David Albrecht. .

Solution to Problem 68Retail Inventory Method

@ cost @ retail

Beginning inventory $10,500 $42,000

Purchases (gross) 465,000 892,000

Freight in 12,000 ---

Markups --- 52,000

Markdowns --- 112,000

Good available for sale 487,500 874,000

Sales (net) --- 722,000

Sales discounts --- 7,000

Ending inventory @ retail 145,000

We need to subtract sales @ gross. If sales is listed at gross, we ignore sales discounts. If sales is listed

at net, we add sales discounts to sales@net to get sales @ gross.

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (465,000 + 12,000) ÷ (892,000 + 52,000 ! 112,000)

= 0.5733

EI @ FIFO cost = 145,000 * 0.5733

= 83,131

CGS = 487,500 – 83,131

= 484,369

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000 ! 112,000)

= 0.5578

EI @ WA cost = 145,000 * 0.55578

= 80,878

CGS = 487,500 – 80,878

= 406,622

394© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000)

= 0.4944

EI @ WALCM cost = 145,000 * 0.4944

= 71,691

CGS = 487,500 – 71,691

= 415,809

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (465,000 + 12,000) ÷ (892,000 + 52,000)

= 0.5053

EI @ FIFOLCM cost = 145,000 * 0.5733

= 73,268

CGS = 487,500 – 73,268

= 414,132

395© 2014 by W. David Albrecht. .

Solution to HW 69Retail inventory method

@ cost @ retail

Beginning inventory $52,320 $96,444

Purchases (gross) 631,000 1,079,327

Freight in 52,000 ---

Markups --- 72,000

Markdowns --- 146,000

Good available for sale 735,320 1,101,771

Sales gross) --- 978,432

Sales discounts --- 97,000

Ending inventory @ retail 123,339

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000 ! 146,000)

= 0.6794

EI @ FIFO cost = 123,339 * 0.6794

= 83,797

CGS = 735,320 – 83,797

= 651,523

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000 ! 146,000)

= 0.6674

EI @ WA cost = 123,339 * 0.6674

= 82,316

CGS = 735,320 – 82,316

= 651,004

396© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000)

= 0.5893

EI @ WALCM cost = 123,339 * .5893

= 72,684

CGS = 735,320 – 72,684

= 662,636

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000)

= 0.5932

EI @ FIFOLCM cost = 123,339* 0.5932

= 73,164

CGS = 735,320 – 73,164

= 662,156

397© 2014 by W. David Albrecht. .

Solution to HW 70Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 300 2.50 2.60 3.00 0.25 1.00

B 500 2.50 2.90 2.75 0.15 0.50

C 150 5.40 5.30 5.90 0.20 1.20

D 450 3.50 3.25 4.50 0.40 0.65

E 280 2.65 2.55 4.00 0.30 0.80

F 375 4.30 4.20 4.60 0.50 1.25

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 300 2.50 750

B 500 2.50 1,250

C 150 5.40 810

D 450 3.50 1,575

E 280 2.65 742

F 375 4.30 1,613

6,740

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

market replacement acceptable acceptable

Item # units cost/unit cost/unit cost / unit NRV NRV – π

A 300 2.50 2.60 2.60 2.75 1.75

B 500 2.50 2.60 2.90 2.60 2.10

C 150 5.40 5.30 5.30 5.70 4.50

D 450 3.50 3.45 3.25 4.10 3.45

E 280 2.65 2.90 2.55 3.70 2.90

F 375 4.30 4.10 4.20 4.10 2.85

398© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 15

Inventory 15

adjustment for C (150 units * 0.10 / unit)

12/31/14 Cost of goods sold expense 22.50

Inventory 22.50

adjustment for D (450 units * 0.05 / unit)

12/31/14 Cost of goods sold expense 75

Inventory 75

adjustment for F (375 units * 0.20 / unit)

Total adjusted value for inventory

Balance before adjustment 6,740.00

Write-down –112.50

Adjusted balance 6,627.50

399© 2014 by W. David Albrecht. .

Solution to HW 71Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 400 14.30 15.60 22.15 0.00 10%

B 200 9.55 9.70 10.33 1.55 5%

C 350 22.10 20.30 28.00 2.80 25%

D 120 13.75 13.25 16.50 1.00 10%

E 810 8.25 2.55 4.00 0.30 15%

F 550 24.30 34.20 38.50 3.85 15%

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 400 14.30 5,720

B 200 9.55 1,910

C 350 22.10 7,735

D 120 13.75 1,650

E 810 8.25 6,683

F 550 24.30 13,365

37,063

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

replacement acceptable acceptable

Item # units cost / unit market / unit cost / unit NRV NRV – π

A 400 14.30 19.93 15.60 22.15 19.93

B 200 9.55 8.78 9.70 8.78 7.75

C 350 22.10 20.20 20.30 25.20 18.20

D 120 13.75 13.85 13.25 15.50 13.85

E 810 8.25 3.10 2.55 3.70 3.10

F 550 24.30 28.87 34.20 34.65 28.87

400© 2014 by W. David Albrecht. .

12/31/14 Cost of goods sold expense 154

Inventory 154

adjustment for B (200 units * 0.77 / unit)

12/31/14 Cost of goods sold expense 570

Inventory 570

adjustment for C (300 units * 1.90 / unit)

12/31/14 Cost of goods sold expense 4,172

Inventory 4,172

adjustment for E (810 units * 5.15 / unit)

Total adjusted value for inventory

Balance before adjustment 37,063

Write-down – 4,896

Adjusted balance 32,167

401© 2014 by W. David Albrecht. .

Solution to HW 72Lower of cost or market

Actual cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $14

Estimated selling price . . . . . . . . . . . . . . . . . . . . . . . . 10

Normal profit margin on selling price . . . . . . . . . . 10%

Estimated cost to sell . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Replacement Cost . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

1. What is the ceiling of the acceptable range? 8 = 10 – 2

2. What is the floor of the acceptable range? 7 = 8 – 0.1*10

3. What is the market? 8 = Replacement cost is outside range, the

ceiling is closes acceptable amount

4. What is LCM? 8 = historical cost of 14 is higher than market of

8

Solution to HW 73Lower of cost or market

highest lowest

necessary replacement acceptable acceptable

Item hist cost market adjustment cost NRV NRV – π

Aluminum 70,000 56,000 – 14,000 62,500 56,000 50,900

Cedar shake 86,000 79,400 – 6,600 79,400 84,800 77,400

Louverd gl 112,000 149,800 0 124,000 168,300 149,800

Thermal W 140,000 128,000 – 12,000 128,000 140,000 124,600

–32,600

If using the direct write-down method as used in class, the necessary adjustment is:

12/31 Cost of goods sold expense 32,600

Inventory 32,600

If using the allowance method as explained in the textbook, the necessary adjustment is:

12/31 Cost of goods sold expense 5,100

Allowance 5,100

402© 2014 by W. David Albrecht. .

Professor Authored Problem Solutions

Intermediate Accounting 2

Retail Inventory Method & LCM

Solution to Problem 67Turnover Ratios

Inventory turnover ratio = CGS ÷ Avg inventory

= 160,000 ÷ 20,000

= 8.0

Days sales in EI = Avg inventory ÷ (CGS ÷365)

= 20,000 ÷ (160,000 ÷ 365)

= 20,000 ÷ 438.3562

= 45.625

AR turnover ratio = Sales ÷ Avg AR

= 270,000 ÷ 66,000

= 4.0909

Average collection period = Avg AR ÷ (Sales ÷ 365)

= 66,000 ÷ (270,000 ÷ 365)

= 66,000 ÷ 739.7260

= 89.2222

393© 2014 by W. David Albrecht. .

Solution to Problem 68Retail Inventory Method

@ cost @ retail

Beginning inventory $10,500 $42,000

Purchases (gross) 465,000 892,000

Freight in 12,000 ---

Markups --- 52,000

Markdowns --- 112,000

Good available for sale 487,500 874,000

Sales (net) --- 722,000

Sales discounts --- 7,000

Ending inventory @ retail 145,000

We need to subtract sales @ gross. If sales is listed at gross, we ignore sales discounts. If sales is listed

at net, we add sales discounts to sales@net to get sales @ gross.

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (465,000 + 12,000) ÷ (892,000 + 52,000 ! 112,000)

= 0.5733

EI @ FIFO cost = 145,000 * 0.5733

= 83,131

CGS = 487,500 – 83,131

= 484,369

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000 ! 112,000)

= 0.5578

EI @ WA cost = 145,000 * 0.55578

= 80,878

CGS = 487,500 – 80,878

= 406,622

394© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (10,500 + 465,000 + 12,000) ÷ (42,000 + 892,000 + 52,000)

= 0.4944

EI @ WALCM cost = 145,000 * 0.4944

= 71,691

CGS = 487,500 – 71,691

= 415,809

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (465,000 + 12,000) ÷ (892,000 + 52,000)

= 0.5053

EI @ FIFOLCM cost = 145,000 * 0.5733

= 73,268

CGS = 487,500 – 73,268

= 414,132

395© 2014 by W. David Albrecht. .

Solution to HW 69Retail inventory method

@ cost @ retail

Beginning inventory $52,320 $96,444

Purchases (gross) 631,000 1,079,327

Freight in 52,000 ---

Markups --- 72,000

Markdowns --- 146,000

Good available for sale 735,320 1,101,771

Sales gross) --- 978,432

Sales discounts --- 97,000

Ending inventory @ retail 123,339

1. FIFO basis

FIFO ratio = cost of net purchases ÷ retail of (net purchases + MU ! MD)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000 ! 146,000)

= 0.6794

EI @ FIFO cost = 123,339 * 0.6794

= 83,797

CGS = 735,320 – 83,797

= 651,523

2. Weighted average

WAvg ratio = cost of (beg inv + net purch) ÷ retail of (beg inv net purch + MU ! MD)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000 ! 146,000)

= 0.6674

EI @ WA cost = 123,339 * 0.6674

= 82,316

CGS = 735,320 – 82,316

= 651,004

396© 2014 by W. David Albrecht. .

3. Weighted average with LCM

Wavg/LCM ratio = cost of (beg inv+ net purchases) ÷ retail of (beg inv + net purchases + MU)

= (52,320 + 631,000 + 52,000) ÷ (96,444 + 1,079,327 + 72,000)

= 0.5893

EI @ WALCM cost = 123,339 * .5893

= 72,684

CGS = 735,320 – 72,684

= 662,636

4. FIFO basis with LCM

FIFO/LCM ratio = cost of net purchases ÷ retail of (net purchases + MU)

= (631,000 + 52,000) ÷ (1,079,327 + 72,000)

= 0.5932

EI @ FIFOLCM cost = 123,339* 0.5932

= 73,164

CGS = 735,320 – 73,164

= 662,156

397© 2014 by W. David Albrecht. .

Solution to HW 70Lower of cost or market

current estimated marginal

replacement sales price selling normal

Item # units cost/unit cost/unit / unit costs / unit profit / unit

A 300 2.50 2.60 3.00 0.25 1.00

B 500 2.50 2.90 2.75 0.15 0.50

C 150 5.40 5.30 5.90 0.20 1.20

D 450 3.50 3.25 4.50 0.40 0.65

E 280 2.65 2.55 4.00 0.30 0.80

F 375 4.30 4.20 4.60 0.50 1.25

1. What is the FIFO cost of ending inventory?

FIFO total FIFO

Item # units cost/unit cost

A 300 2.50 750

B 500 2.50 1,250

C 150 5.40 810

D 450 3.50 1,575

E 280 2.65 742

F 375 4.30 1,613

6,740

2. Applying the LCM method on a product by product basis, write the journal entry for the LCM

adjustment. What is the total adjusted cost of ending inventory?

current highest lowest

market replacement acceptable acceptable

Item # units cost/unit cost/unit cost / unit NRV NRV – π

A 300 2.50 2.60 2.60 2.75 1.75

B 500 2.50 2.60 2.90 2.60 2.10

C 150 5.40 5.30 5.30 5.70 4.50

D 450 3.50 3.45 3.25 4.10 3.45