reliance life insurance

DESCRIPTION

reliancTRANSCRIPT

A TRAINING REPORT

ON

RELIANCE HEALTH INSURANCE PLAN

For fulfillment and the requirement of the award for the degree of BBA/MBA .

Subject: TPP(IMS-506)

Under the supervision of

Sanjeev Verma(Executive Manager)

SUBMITTED TO :- SUBMITTED BY :-

DR. M.k.Jain Lovely Kumar Verma

Director MBA(5-year) , 5th Sem.

IMS, KUK Roll No. :- 20

Reg. No. :- 11UD3043

Institute Of Management Studies

Kurukshetra University, Kurukshetra

(Sept. 2013)

DECLARATIONI LOVELY KUMAR VERMA OF MBA(5-year) 5th Sem. of “Institute Of

Management Studies” hereby declare that the summer training report

entitled “HEALTH INSURANCE PLAN” IN RELIANCE LIFE INSURACNE is

an original word and the same has not been submitted to any other

institute for the award of any other degree.

Lovely Kumar Verma

2

ACKNOWLEDGEMENT

I would like to thank my project guide Mr. Sanjeev Verma , Excecutive

Branch Manager, RELIANCE Life Insurance, Kurukshetra for guiding me

through my summer internship and research project. His encouragement,

time and effort are greatly appreciated.

I would like to thank Pankaj Sharma, for supporting me during this

project and providing me an opportunity to learn outside the class room.

It was a truly wonderful learning experience.

I would like to dedicate this project to my parents. Without their help and

constant support this project would not have been possible.

Lastly I would like to thank all the respondents who offered their opinions

and suggestions through the survey that was conducted by me in

Kurukshetra.

Once again my gratitude to the RELIANCE Life insurance, for their kind

co-operation.

3

CONTENTS

CHAPTER

NO.

TITLE PAGE

NO.

1. INTRODUCTION

.SECTOR

.MAJOR PLAYER IN SECTOR

2. RELIANCE LIFE INSURANCE

. INTRODUCTION

. PRODUCT & SERVICES

. RELIANCE HEALTH PLAN

3. RESEARCH METHODOLOGY

ANALYSIS AND DISCUSSION

4.

5.

SWOT ANALYSIS

SUGGESTIONS

CONCLUSION

LEARNING FROM THE REPORT

ANNEXURES

BIBLOGRAPHY

4

CHAPTER 1

INSURANCE INDUSTRY

“AN OVERVIEW”

5

Introduction

Insurance is a contract between two parties whereby one party called insurer undertakes in

exchange for a fixed sum called premiums, to pay the other party called insured a fixed amount of money on

the happening of a certain event."Insurance is a protection against financial loss arising on the happening of

an unexpected event. Insurance companies collect premiums to provide for this protection. A loss is paid out

of the premiums collected from the insuring public and the Insurance Companies act as trustees to the

amount collected. For Example, in a Life Policy, by paying a premium to the Insurer, the family of the

insured person receives a fixed compensation on the death of the insured. Similarly, in a car insurance, in

the event of the car meeting with an accident, the insured receives the compensation to the extent of

damage. It is a system by which the losses suffered by a few are spread over many, exposed to similar risks.

Logic of insurance

It is a system by which the losses suffered by a few are spread over many, exposed to similar risks.

Insurance is a protection against financial loss arising on the happening of an unexpected event. Insurance

companies collect premiums to provide for this protection. A loss is paid out of the amount premiums

collected from the insuring public and the Insurance Companies act as trustees to the collected.

Need of insurance

Insurance is desired to safeguard oneself and one's family against possible losses on account of risks and

perils. It provides financial compensation for the losses suffered due to the happening of any unforeseen

events. By taking life insurance a person can have peace of mind and need not worry about the financial

consequences in case of any untimely death. Certain Insurance contracts are also made compulsory by

legislation. For example, Motor Vehicles Act 1988, stipulates that a person driving a vehicle in a public

place should hold a valid insurance policy covering “Act" risks. Another example of compulsory insurance

6

pertains the Environmental Protection Act, wherein a person using or to carrying hazardous substances (as

defined in the Act) must hold a valid public liability (Act) policy.

Insurance in India

Insurance is a federal subject in India and has a history dating back to 1818. Life and general insurance in

India is still a nascent sector with huge potential for various global players with the life insurance premiums

accounting to 2.5% of the country's GDP while general insurance premiums to 0.65% of India's GDP. The

Insurance sector in India has gone through a number of phases and changes, particularly in the recent years

when the Govt. of India in 1999 opened up the insurance sector by allowing private companies to solicit

insurance and also allowing FDI up to 26%. Ever since, the Indian insurance sector is considered as a

booming market with every other global insurance company wanting to have a lion's share. Currently, the

largest life insurance company in India is still owned by the government.

History of Insurance in India

Insurance in India has its history dating back till 1818, when Oriental Life Insurance Company was

started by Europeans in Kolkata to cater to the needs of European community. Pre-independent

era in India saw discrimination among the life of foreigners and Indians with higher premiums being

charged for the latter. It was only in the year 1870, Bombay Mutual Life Assurance Society, the

first Indian insurance company covered Indian lives at normal rates.At the dawn of the twentieth century,

insurance companies started mushrooming up. In the year 1912, the Life Insurance Companies Act, and the

Provident Fund Act were passed to regulate the insurance business. The Life Insurance Companies Act,

1912 made it necessary that the premium rate tables and periodical valuations of companies should be

7

certified by an actuary. However, the disparage still existed as discrimination between Indian and foreign

companies. The oldest existing insurance company in India is National Insurance Company Ltd, which was

founded in 1906 and is doing business even today. The Insurance industry earlier consisted of only two state

insurers: Life Insurers i.e. Life Insurance Corporation of India (LIC) and General Insurers i.e. General

Insurance Corporation of India (GIC). GIC had four subsidiary companies.With effect from December

2000, these subsidiaries have been de-linked from parent company and made as independent insurance

companies: Oriental Insurance Company Limited, New India Assurance Company Limited, National

Insurance Company Limited and United India Insurance Company Limited.

Life Insurance Corporation Act, 1956

Even though the first legislation was enacted in 1938, it was only in 19 January 1956, that life insurance in

India was completely nationalized, through a Government ordinance; the Life Insurance Corporation Act,

1956 effective from 1.9.1956 was enacted in the same year to, inter-alia, form LIFE INSURANCE

CORPORATION after nationalization of the 245 companies into one entity. There were 245 insurance

companies of both Indian and foreign origin in 1956. Nationalization was accomplished by the govt.

acquisition of the management of the companies. The Life Insurance Corporation of India was created on 1

September, 1956, as a result and has grown to be the largest insurance company in India as of 2006 .

General Insurance Business (Nationalization) Act, 1972

The General Insurance Business (Nationalization) Act, 1972 was enacted to nationalize the 100 odd general

insurance companies and subsequently merging them into four companies. All the companies were

amalgamated into National Insurance, New India Assurance, Oriental Insurance, and United India Insurance

which were headquartered in each of the four metropolitan cities.

8

Insurance Regulatory and Development Authority (IRDA) Act, 1999

Till 1999, there were not any private insurance companies in Indian insurance sector. The Govt. of India

then introduced the Insurance Regulatory and Development Authority Act in 1999, thereby de-regulating

the insurance sector and allowing private companies into the insurance. Further, foreign investment was

also allowed and capped at 26% holding in the Indian insurance companies. In recent years many private

players entered in the Insurance sector of India. Companies with equal strength started competing in the

Indian insurance market. Currently, in India only 2 million people (0.2 % of total population of 1 billion),

are covered under Medi claim, whereas in developed nations like USA about 75 % of the total population

are covered under some insurance scheme. With more and more private players in the sector this scenario

may change at a rapid pace

1.2. Major Players in Insurance Sector

Insurance is an upcoming sector, in India the year 2000 was a landmark year for life insurance industry, in

this year the life insurance industry was liberalized after more than fifty years. Insurance sector was once a

monopoly, with LIC as the only company, a public sector enterprise. But nowadays the market opened up

and there are many private players competing in the market. There are fifteen private life insurance

companies has entered the industry. After the entry of these private players, the market share of LIC has

been considerably reduced. In the last five years the private players is able to expand the market (growing at

30% per annum) and also has improved their market share to 18%.For the past five years private players

have launched many innovations in the industry in terms of products, market channels and

advertisement of products, agent training and customer services etc.The various life insurers entered India:-

9

1. Bajaj Allianz Life Insurance Company Limited

2. Birla Sun Life Insurance Co. Ltd

3. HDFC Standard life Insurance Co. Ltd

4. ICICI Prudential Life Insurance Co. Ltd.

5. ING Vysya Life Insurance Company Ltd.

6. Max New York Life Insurance Co. Ltd

7. Met Life India Insurance Company Ltd.

8. Kotak Mahindra Old Mutual Life Insurance Limited

9. SBI Life Insurance Co. Ltd

10. Tata AIG Life Insurance Company Limited

11. Reliance Life Insurance Company Limited.

12. Aviva Life Insurance Co. India Pvt. Ltd.

13. Sahara India Life Insurance Co, Ltd.

14. Shriram Life Insurance Co, Ltd.

15. Bharti AXA Life Insurance Company Ltd.

1.2.1 TOP 10 LIFE INSURANCE COMPANIES IN INDIA

1. Life Insurance Corporation of India

LIC (Life Insurance Corporation of India) still remains the largest life insurance company accounting for

64% market share. Its share, however, has dropped from 74% a year before ,mainly owing to entry of

private players with innovative products and better sales force.

2. ICICI Prudential Life Insurance Company Ltd.

The largest player in the private life insurance industry ICICI Prudential Life Insurance, the life insurance

arm of ICICI Bank posted a 8.09% rise in profit after tax for the full year ended March 2013. The private

life insurer posted net profit of Rs 1,496 crore compared to Rs 1,384 crore for full year ended March 2012.

In terms of premiums, ICICI Life’s annualised premium equivalent (APE) increased by 13% to Rs 3,532

10

crore in FY2013 from Rs 3,118 crore in FY2012. The assets under management at March 31, 2013 were

Rs 74,164 crore (US$ 13.7 billion).

3.Bajaj Allianz Life Insurance Company Ltd.

Bajaj Allianz Life Insurance Company Limited is a joint venture between Bajaj Finserv Limited

(recently demerged from Bajaj Auto Limited) and Allianz. Bajaj Allianz Life Insurance offers a range of

insurance products for financial planning and life insurance. Bajaj Allianz Life Insurance Co Ltd has

reported a growth of 52% and its market share went upto 6.98% in 2009-10 form 5.66% in 2011-12.

4. SBI Life Insurance Company Ltd.

SBI Life Insurance is a joint venture life insurance company between State Bank of India (SBI), the

largest state-owned banking and financial services company in India, and BNP Paribas Assurance. SBI

owns 74% of the total capital and BNP Paribas Assurance the remaining 26% of the capital. SBI Life

Insurance has an authorized capital of 2000 crore (US$310 million)and a paid up capital of 1000 crore

(US$150 million).

5. Reliance Life Insurance Company Ltd.

Reliance Life Insurance Company (RLIC) is amongst the leading private sector life insurance companies

in terms of new business premium with a market share of 5% of the private sector life insurance industry.

The company has over 7 million policy holders with a strong distribution network of close to 1,230 branches

with over 124,000 agents as of March 31, 2013. Reliance Life offers life insurance products targeted at

individuals and groups, catering to four distinct segments: protection, children, retirement and investment

plans

6. HDFC Standard Life Insurance Company Ltd.

HDFC Life, one of India's leading private life insurance companies, offers a range of individual and group

insurance solutions. It is a joint venture between Housing Development Finance Corporation Limited

11

(HDFC), India's leading housing finance institution and Standard Life plc, the leading provider of financial

services in the United Kingdom. HDFC Ltd. holds 72.37% and Standard Life (Mauritius Holding) Ltd.

holds 26.00% of equity in the joint venture, while the rest is held by others.

HDFC Life has seen a 66.5% growth in net profit and posted net profit of Rs 451 crore in financial year

2012-13. The company recorded 16% positive growth in new business premium income (Individual

business) and 11% growth in total premium income.

7. Birla Sun Life Insurance Company Ltd .

Birla Sun Life Insurance Company Limited (BSLI) is a joint venture between the Aditya Birla Group, a well

known Indian conglomerate and Sun Life Financial Inc, one of the leading international financial services

organizations from Canada. With an experience of over a decade, BSLI has contributed to the growth and

development of the Indian life insurance industry and currently is one of the leading life insurance

companies in the country. Birla Sun Life Insurance Co Ltd market share of the company increased from

1.22% to 3.17% in 2012-13.

8. Max New York Life Insurance Company Ltd.Max Life Insurance, one of the leading

life insurers, is a joint venture between Max India Ltd. and Mitsui Sumitomo Insurance Co. Ltd. Max Life

Insurance has partnered with 50 companies, so that our products are available at 1453 locations ensuring

ease of reach for you. Max Life Insurance Company Limited reported a 17% increase in profit before tax

(PBT) for the fiscal 2013 at INR 8,600 million. Gross written premium for 2012-13 increased by 4% to INR

66,390 million.

9. Kotak Mahindra Old Mutual Life Insurance Ltd.

Kotak Mahindra Old Mutual Life Insurance Ltd is a 74:26 joint venture between Kotak Mahindra Bank

Ltd., its affiliates and Old Mutual plc. The company started operations in 2001, and strives to offer its

customers outstanding value through high customer empathy, consistent and benchmarked service and a

12

suite of products that leverage the combined prowess of protection and long term savings. The company

covers over 4 million lives and is one of the fastest growing insurance companies in India. The consolidated

balance sheet of Kotak Mahindra group is over Rs. 1.17 lakh crore and the consolidated net worth of the

Group stands at Rs. 17,228 crore (approx US$ 2.9 billion) as on June 30, 2013.

10. Aviva Life Insurance Company India Ltd .

Aviva India is an Indian life assurance firm, and a joint venture between Aviva plc, a British assurance

company, and Dabur Group, an Indian conglomerate. Aviva began operations in July 2002 as a joint

venture with Dabur Group, one of India’s oldest business houses. As per the Indian insurance sector

regulations, Aviva plc has a 26% stake and Dabur has a 74% stake in the JV partnership It has presence in

more than 3,000 locations across India via 221 branches and close to40 banc assurance partnerships. Aviva

Life Insurance plans to increase its capital base by Rs 344 crore.

Market Shares of insurance companies

13

14

CHAPTER 2

RELIANCE LIFE INSURANCE

“Profile organization”

15

2.1 Profile of organization

Reliance life insurance company ltd.

FOUNDER

Few men in history have made as dramatic a contribution to their country’s economic fortunes as did the

founder of Reliance, Sh. Dhirubhai H Ambani. Fewer still have left behind a legacy that is more enduring

and timeless.

•As with all great pioneers, there is more than one unique way of describing the true genius of Dhirubhai:

The corporate visionary, the unmatched strategist, the proud patriot, the leader of men, the architect of

India’s capital markets, the champion of shareholder interest.

•But the role Dhirubhai cherished most was perhaps that of India’s greatest wealth creator. In one lifetime,

he built, starting from the proverbial scratch, India’s largest private sector enterprise.

•When Dhirubhai embarked on his first business venture, he had a seed capital of barely US$ 300 (around

Rs 14,000). Over the next three and a half decades, he converted this fledgling enterprise into a Rs 60,000

crore colossus—an achievement which earned Reliance a place on the global Fortune 500 list, the first ever

Indian private company to do so.

•Dhirubhai is widely regarded as the father of India’s capital markets. In 1977, when Reliance Textile

Industries Limited first went public, the Indian stock market was a place patronised by a small club of elite

investors which dabbled in a handful of stocks.

•Undaunted, Dhirubhai managed to convince a large number of first-time retail investors to participate in

the unfolding Reliance story and put their hard-earned money in the Reliance Textile IPO, promising them,

in exchange for their trust, substantial return on their investments. It was to be the start of one of great

stories of mutual respect and reciprocal gain in the Indian markets.

•Under Dhirubhai’s extraordinary vision and leadership, Reliance scripted one of the greatest growth stories

in corporate history anywhere in the world, and went on to become India’s largest private sector enterprise.

•Through out this amazing journey, Dhirubhai always kept the interests of the ordinary shareholder

uppermost in mind, in the process making millionaires out of many of the initial investors in the Reliance

stock, and creating one of the world’s largest shareholder families.

2.1.1. ABOUT RELIANCE

16

R.L.I. Company Limited is a part of Reliance Capital Ltd. of the Reliance – Anil Dhirubhai Ambani Group.

Reliance Capital is one of India’s leading private sector financial services companies, and ranks among the

top 3 private sector financial services and banking companies, in terms of net worth. Reliance Capital has

interests in asset management and mutual funds, stock broking, and general insurance, proprietary

investments, private equity and other activities in financial services.

•Reliance Capital Limited (RCL) is a Non-Banking Financial Company (NBFC) registered with the Reserve

Bank of India under section 45IA of the Reserve Bank of India Act, 1934.

•Reliance Capital sees immense potential in the rapidly growing financial services sector in India and aims

to become a dominant player in this industry and offer fully integrated financial services.

•R.L.I. is another step forward for Reliance Capital Limited to offer need based Insurance solutions to

individuals and Corporates.

2.1.2. CORPORATE OBJECTIVE

At R.L.I. we strongly believe that as is different at every stage, insurance must offer flexibility and choice to

go with that stage. We are fully prepared and committed to guide you on insurance products and services

through our well-trained advisors, backed by competent marketing and customer services, in the best

possible way.

•It is our aim to become one of the top private insurance companies in India and to

become a cornerstone of RLI integrated financial services business in India.

2.1.3. CORPORATE MISSION

•“To set the standard in helping our customers manage their financial future”.

BELOW ARE FEW OF THE PLANS THAT ARE OFFERED BY R.L.I. INSURANCE

PLANS AVAILABLE

1. Products (Individual Plans) Savings (Endowment)

2.Reliance Endowment Plan (formerly Divya Shree)

3. Reliance Cash Flow Plan (formerly Dhana Shree)

4.. Reliance Child Plan (formerly Yuva Shree)

5. Reliance Whole Plan (formerly Nithya Shree) Pensions

6. Risk / Protection

7. Reliance Term Plan (formerly Raksha Shree) Products (Group / Corporate Plans)

17

Tax Benefits

It is one kind on benefit from life insurance policy . Maximum people buy insurance because they want

deduction in their income tax.

Premiums paid for Life insurance - Deduction under Section 80C

1. Category of assesses allowed deduction: Individual assessee and Hindu Undivided Family assessee.

2. Eligible Savings: Premiums paid or deposited by assessee to effect or to keep in force insurance on the

life of following persons:

In case of individual assessee – Himself/Herself, spouse, children of such individual

In case of HUF assesses – any member

3. 20% limit: If the amount of premium paid in a financial year for a policy is in excess of 20% of the

actual capital sum assured, then deduction will be allowed only for premiums upto 20% of the sum assured.

4. Limit on amount of deduction: Deduction will be restricted to investments upto Rs 100,000 in savings

specified under Section 80C (including life insurance premiums). The limit of deduction under Section 80C

will be part of the overall limit prescribed under Section 80C.

5. Disallowance: This benefit will be reversed if the policy is terminated/cease to be inforce within 2 years

after the date of commencement of policy.

Premiums paid for Pension plans - Section 80C

1. Permitted Deduction: Section 80C allows for deduction of premiums paid under a pension scheme. As

per this Section, the whole of amount paid or deposited (excluding interest or bonus accrued or credited to

the assessee’s account, if any) as does not exceed the amount of Rs 100,000 is eligible for deduction from

the total income.

2. Receipt under Policy: Amounts received on surrender (whole/part) of annuity plan, amounts received as

Pension is taxed as income.

3. Limit: The limit of deduction under Section 80C will be part of the overall limit prescribed under Section

80C.

Overall deduction limit - Section 80C.

As per this section, the maximum amount of deduction that an assessee can claim under Sections 80C and

80D will be limited to Rs 100,000.

Premiums paid for medical insurance - Section 80D

18

1. Category of assesses allowed deduction: Individual assessee and Hindu Undivided Family assessee.

2. Eligible premiums: Premiums paid by assessee by any mode other than cash out of his taxable income to

effect or to keep in force an insurance on the health of following persons:

o In case of individual assessee – Himself/Herself, spouse, dependent children and parent or parents. The

condition of dependency of parent has been removed from FY 2008-09. In other words, even if the parent is

independent, the individual can pay the premium and claim the deduction.

o In case of HUF assessee – any member of HUF

3. Deduction and upper limit: The qualifying amounts under Section 80D for self, spouse and

dependent children is upto Rs. 15,000/- and additional deduction upto Rs. 15,000/- for the parents.

However, a higher amount of upto Rs 20,000/- is permitted if the person, for whose health insurance the

premium was paid, was aged 65 years or more at any time during the financial year in which the premium

was paid. Such amounts of premium paid would be allowed as deduction from the total income of the

assessee.

Benefits under insurance policy - Section 10(10D)

As per Section 10(10D) of Income tax Act, 1961, any sum received under a life insurance policy, including

the sum allocated by way of bonus on such policy is exempt from tax. However, this rule does not apply to

following amounts:

sum received under Section 80D D(3), or

any sum received under a Keyman Insurance Policy, or

any sum received other than as death benefit under an insurance policy which has been issued on or after

April 1 2003 and if the premium paid in any of the years during the term of the policy is more than 20% of

the sum assured.

19

2.3 Reliance Products

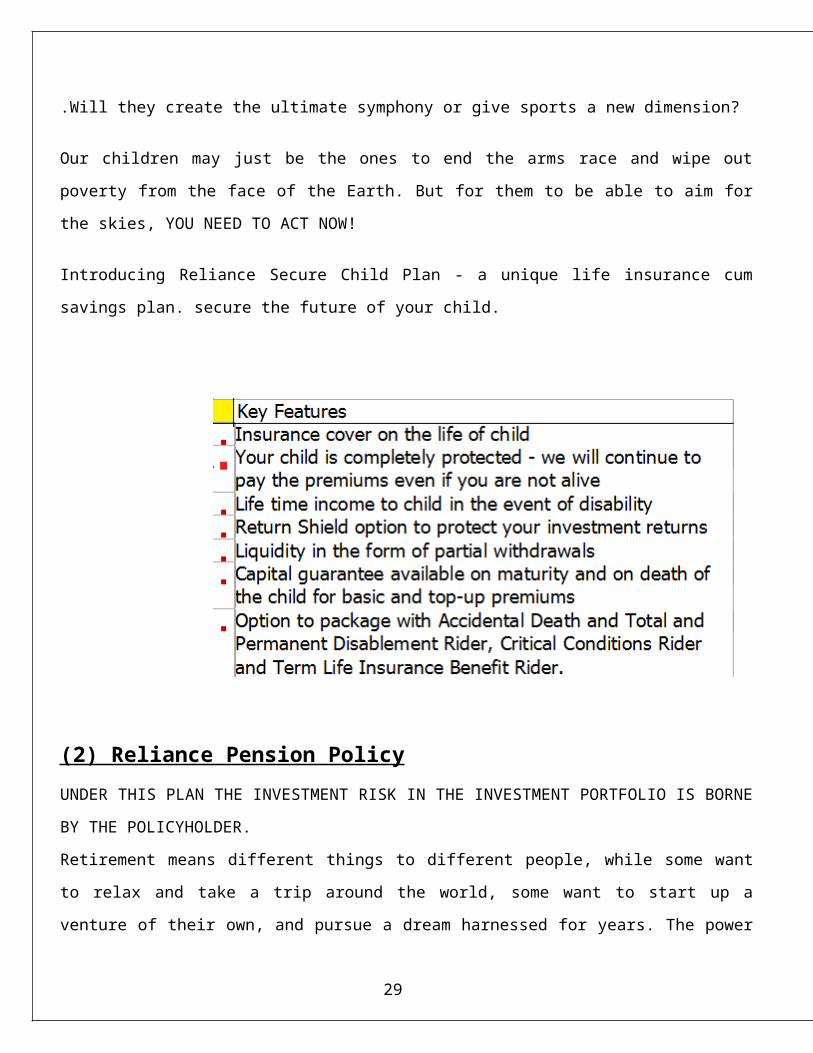

(1) Reliance Child Plans

What could make you happier than knowing, that your child's future is secure? Nothing, we suppose. Which

is why, Reliance Life Insurance brings to you Reliance Secure Child Plan, a unit-linked Insurance Plan, that

gives you the freedom to enjoy today with your child, because his tomorrow is in safe hands.

.Do you see your child becoming a trailblazer?

.Will they create the ultimate symphony or give sports a new dimension?

Our children may just be the ones to end the arms race and wipe out poverty from the face of the Earth. But

for them to be able to aim for the skies, YOU NEED TO ACT NOW!

Introducing Reliance Secure Child Plan - a unique life insurance cum savings plan. secure the future of your

child.

20

(2) Reliance Pension Policy

UNDER THIS PLAN THE INVESTMENT RISK IN THE INVESTMENT PORTFOLIO IS BORNE BY

THE POLICYHOLDER.

Retirement means different things to different people, while some want to relax and take a trip around the

world, some want to start up a venture of their own, and pursue a dream harnessed for years. The power to

make your autumn years special lies only with you. The Reliance Super Golden Years Plan gives you the

power and the right kind of solution - A retirement plan that allows you to save systematically and generate

the much-needed corpus to make your olden years look golden.

21

(3) Reliance Whole life insurance policy

You’ve always loved your family. As a loving person you want to be rest assured that they will be happy,

even if something were to happen to you. With Reliance Whole Life Plan you can be sure that your family

will receive that timely financial support they need. Go ahead, live your today to the fullest, without a worry

about tomorrow.

22

RELIANCE HEALTH INSURANCE PLAN

23

What this plan brings for you?

Key Features and Benefits

Reimbursement of all admissible medical expenses when you are in hospital

Maternity Benefit (available under family floater cover)

Pre existing illness covered after 4 continuous years of membership

150 Day Care Treatment covered

Pre & Post hospitalization expenses are covered

Ambulance charges payable

Income Tax benefit under section 80(D)

Entire family covered under a single umbrella of protection

Cover your Parents & parents-in-law

Guaranteed Renewability

Cashless facility at 4000 hospitals across the country

Sum Insured is increased by 5% without paying any extra premium, for every claim free year.

Guaranteed fixed rate of premium for 3 years

Renewal discount of 15% on premium at the time of term renewal as a token of appreciation for your

continued faith in us

Wide range of Sum Insured ranging from ` 2 lacs to` 10 lacs

How does the plan work?

This is regular premium, non-participating, non unit linked,

hospitalization benefit plan based on Individual and Family

Floater basis. The plan will be offered to individuals or a family which includes the primary insured, spouse,

eldest four eligible children, dependent parents and parents in law. Addition of parents in law under the

policy will be subject to production of certificate regarding financial dependency on the primary life. The

premiums are paid on annual basis or monthly (only if premiums are paid electronically) basis. Member

with the highest age among husband and wife will be referred as Primary Insured and all the other members

of the family covered under the plan will be referred as Secondary Insured. On death of the Primary Insured

during the policy term, the insured spouse becomes the Primary Insured. If both Primary Insured and

Insured Spouse die, the policy will be terminated from the policy anniversary following the death of the

second life. Children are covered , provided the children are economically dependent on parent(s) and are

not married at the time of commencement of policy or on any subsequent renewal date.

24

What does your plan cover?

The plan covers reasonable and customary medical expenses incurred towards hospitalisation during the

policy term for the disease, illness, medical condition or injury contracted or sustained by the member(s)

subject to terms, conditions, limitations, waiting period and exclusions as mentioned below:

1. In a policy year, the total liability of the company under this policy is limited to the sum assured, without

making any reference to what the company has reimbursed or are liable to reimburse for the claimsmade in

the previous policy year. Where sum assured means the sum shown in your policy document

whichrepresents Our maximum liability in relation to all claims made by You and all of Your Dependents, if

any during the Policy Year.

Hospital Expenses

Reliance Life Care For You plan will reimburse all admissible medical expenses in case of an unfortunate

event of Hospitalisation:

Room, boarding and nursing expenses.

Surgeon, Anaesthetists, Medical Practitioner Consultants, Specialists fee

Operation theatre charges

Anaesthesia, blood, oxygen, medicines and drugs etc.

Diagnostics and laboratory tests.

Day Care Treatment

We cover 150 listed day care treatment and procedure as given in Annexure A, wherein even 24 continuous

hours of hospitalisation is not required.

Maternity Benefit

Maternity benefit is available only with Family Floater coverage and is not available under Individual

coverage. Maternity expenses up to a maximum of ` 15,000/- will be reimbursed if the member stays with us

for a continuous period of 3 years without break.

25

Pre & Post hospitalisation Benefit

A flat benefit of 5% of the admissible hospitalization expenses, subject to a maximum of ` 5000 will be paid

on each hospitalisation claim towards Pre and Post hospitalisation expenses.

Ambulance Charges

Ambulance charges will be reimbursed by us subject to a maximum of ` 1,000 in a policy year provided the

member is hospitalised for more than 24 continuous hours.

Death Benefit

No benefit is payable on death of the insured members.

Maturity Benefit

No benefit is payable on maturity of the policy

Surrender Benefit

No benefit is payable on surrender of the policy

What are the other offerings under this plan?

Single sum insured covers the entire family under family floater coverage

This means, you and your family members (spouse, eldest four eligible children, dependent parents and

parents-in-law) together can utilize up to a maximum of sum insured opted for in a policy year for

hospitalisation benefit. Thus, your entire family is covered under the single umbrella of protection.

Guaranteed Renewability

Once you choose to hold our hands we will protect you from any unforeseen contingencies. You and your

family members will enjoy a guaranteed renewability upto the age of 75 years for adults and 21 years for the

children, irrespective of claim experience and change in your health condition.

Fixed Premium

Your Premium will remain constant for a period of 3 years irrespective of increase in your age and claim

experience.

26

Renewal Discount

As a token of appreciation for your loyalty towards our company, a discount of 15% on the renewal

premium will be given at the time of term renewal i.e. at the end of third year, which may change in future

subject to regulatory guidelines.

Enhancement of Sum Insured

We shall reward you for staying fit. If you have not claimed during a policy year, the sum assured under the

policy will be increased by an amount equivalent to 5% of the basic sum assured in the subsequent policy

year without any corresponding increase in premium subject to a maximum increase of 30% of the basic

sum assured over the duration of the policy including term renewals, where the basic sum assured is the sum

assured chosen as on policy commencement date.

If a claim is made by the member after this provision has come into force, then the sum assured under the

policy will be reduced back to basic sum assured at commencement in the subsequent policy year

Cashless facility

You have access to over 4000 empanelled hospitals across India where you can avail of cashless

hospitalisation facility by showing your Reliance Life Insurance health card. This relives you from paying

hospital bills at the crucial moment of medical emergency. The cashless & reimbursement claim will be

facilitated by the Third Party Administrator (TPA) of the company. You will be provided with a health card

and a guide book containing the list of empanelled hospital and details on the claim process. A 24X7

helpline number (number available in the guide book) is maintained by the TPA to assist you in resolving

your queries.

What are the options available under the policy?

Term Renewal of policy (after expiry of the policy term of 3 years)

You have the option to renew the policy within 30 days after the expiry of the previous policy term at the

premium rates, terms and conditions prevailing at the time of renewal of the policy. Coverage ceases on the

expiry of the previous policy term and no cover exists during this period of 30 days.

If the sum assured after renewal is more than the sum assured on commencement of the previous policy,

the renewal of policy would be subject to the Primary Insured and the Secondary Insured member satisfying

the financial and medical underwriting requirements of the company. The company shall have the right to

refuse the increase in sum assured on renewal.

On renewal, the waiting period would be reduced by the number of continuous years the member has

been insured with company under this plan or any other plan of the company of similar nature.

27

Alteration of Premium Payment Frequency

The premium payment frequency may be changed at any policy anniversary.

Option to increase the SA

The Sum assured chosen at the commencement of the policy can be changed on any renewal date of the

policy (where renewal occurs after the end of each policy term of 3 years) subject to underwriting, if

required by company.

Option to include other members

The Primary Insured can include secondary members (upto 4 eldest children, Spouse, father, mother, father

in-law, mother in-law) from commencement of the policy or from any subsequent policy anniversary.

Addition of parents in law under the policy will be subject to production of certificate regarding financial

dependency on the primary life. If the secondary member is not included on commencement of policy and is

added from a subsequent policy anniversary, then there will be a 3 months waiting period during which no

claims will be admitted.

Tax Benefit

Tax benefits under the policy will be as per the prevailing Income Tax laws. Service tax and education cess

will be charged extra as per applicable rates. Tax laws are subject to amendments from time to time and

interpretations. You are advised to consult a tax expert.

28

What are the Eligibility Criteria?

29

Minimumum

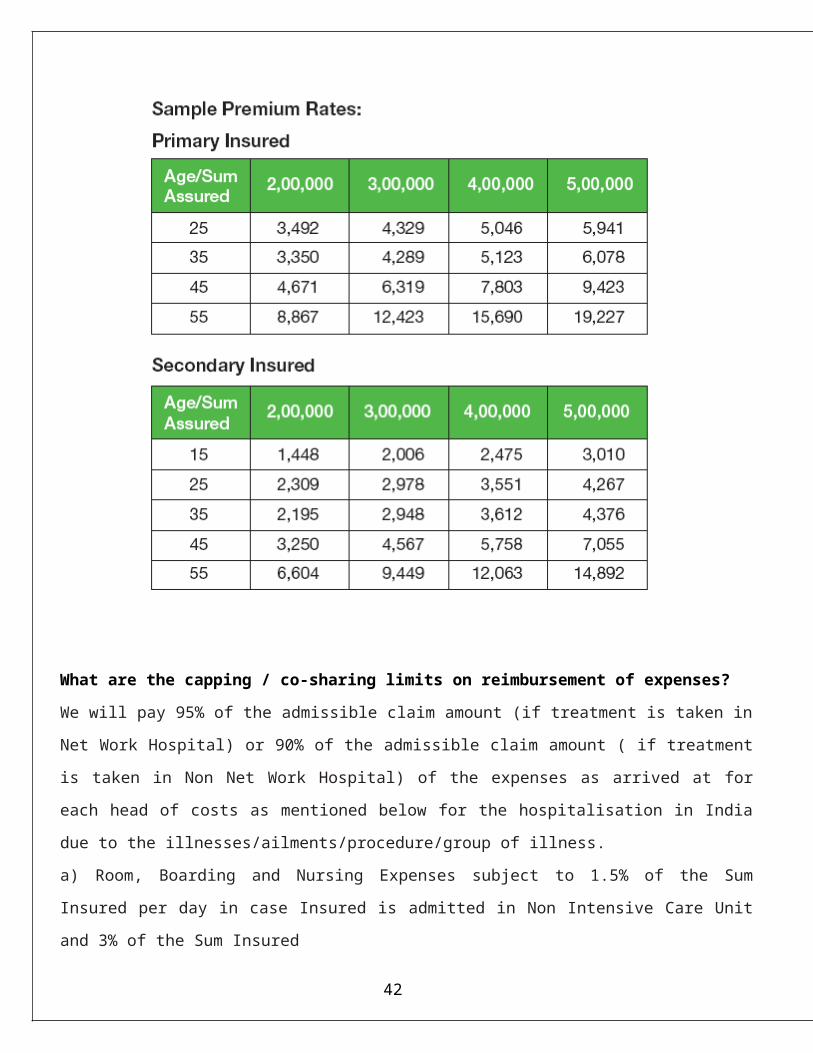

What are the capping / co-sharing limits on reimbursement of expenses?

We will pay 95% of the admissible claim amount (if treatment is taken in Net Work Hospital) or 90% of the

admissible claim amount ( if treatment is taken in Non Net Work Hospital) of the expenses as arrived at for

each head of costs as mentioned below for the hospitalisation in India due to the

illnesses/ailments/procedure/group of illness.

a) Room, Boarding and Nursing Expenses subject to 1.5% of the Sum Insured per day in case Insured is

admitted in Non Intensive Care Unit and 3% of the Sum Insured

per day in case insured is admitted in Intensive Care Unit. Room rent and boarding expenses would include

Registered Medical Officer charges, administration charges for Fluids/Blood Transfusion/Injections/Nursing

Care Charges.

b) Operation theatre charges.

30

c) Special Nursing expenses incurred for deployment of qualified nurse will be reimbursed, subject to the

treating Doctor's advice and submission of receipt from the registered nurse's Association

d) Surgeon, Anaesthetists, Medical Practitioner, Consultants, Specialists fee subject to a maximum limit of

25% of the total admissible medical expenses incurred

e) Anaesthesia, blood, oxygen, medicines and drugs, diagnostic materials, x-ray, surgical appliances, any

disposable surgical consumables, dialysis, radiotherapy, Cardiac Pacemaker, Artificial limbs, stents and

implants.In respect of above under point no. i & ii we will make payment only for those days of treatment as

an in-Patient, falling within the policy term.

f) 150 day care procedures as mentioned in list.

g) If Hospitalisation is due to one of the following illnesses/ procedures/ailments/group of illnesses, then we

will reimburse 95% of the medical expenses if the treatment is taken in Net Work Hospital or 90% of the

medical expenses treatment is taken in Non Net Work Hospital, subject to a maximum reimbursement limit

per member in a policy year, as described in the table below:

h) If at the time when any claim arises under this policy there is in existence any other insurance (other than

Cancer Insurance Policy in collaboration with Indian Cancer Society/Cancer Patient Aid Association),

whether it be affected by or on behalf of any insured person in respect of whom the claim may have arisen

31

covering the same loss, liability, compensation, cost or expenses, the company shall not be liable to pay or

contribute more than its rateable proportion of any loss, liability, compensation, cost or expenses. The

benefits under this policy shall be in excess of the benefits available under cancer insurance policy as

indicated above.

What your plan does not cover?

"Pre-Existing Medical Condition" means any Medical Condition or related condition (s) for which the

Member(s) had any signs or symptoms, whether or not they received medical advice, in the 48 months

immediately prior to the Policy Commencement date or any condition, signs or symptoms which occurred in

the same 48 month period which would have caused any ordinary prudent person to seek treatment,

diagnosis, care, medical advice or treatment. The exclusion shall cease to apply if you have maintained the

Policy with the company for a continuous period of 4 years without break from the date of the first Policy

with the company

Hospitalisation/Medical expenses not directly related to the specific illness or injury for which

hospitalization took place and the expenses which are not recommended by the attending doctor.

Any treatment not performed by a doctor or any treatment of a purely experimental nature.

Expenses which are not for actual, necessary and reasonable expenses incurred in the treatment of the

Illness or Physical Injury, or any elective surgery or treatment which is not medically necessary.

Any diagnosis or treatment arising from or traceable to pregnancy, childbirth including caesarean section,

medical termination of pregnancy and/or any treatment related to pre and post natal care of the mother or the

new born ( excepting ectopic pregnancy ) for Individual Coverage. This is not applicable if the member has

been insured under Family Floater Plan and has renewed the policy continuously for a period of 3 years with

the Company. However, the expenses related to new born baby are not reimbursable.

Sterility, treatment whether to effect or to treat infertility, any fertility, sub fertility or assisted conception

procedure, surrogate or vicarious pregnancy, birth control, contraceptive supplies or services including

complication arising due to supplying services.

Hospitalization for correction of birth defects or external congenital anomaly /internal congenital

anomaly.

Any sexually transmitted diseases or any condition directly or indirectly caused to or associated with

Human Immune Deficiency Virus (HIV) or any Syndrome or condition of a similar kind commonly referred

to as AIDS (Acquired Immune Deficiency Syndrome}

Dental treatment or surgery of any kind unless necessitated by accidental bodily injury.

32

Cost of spectacles contact lenses hearing aids and the cost of treatment for vision correction.

Self affected injuries or conditions (attempted suicide) and or the treatment directly or indirectly arising

from alcoholism or drug abuse and any Illness or Physical Injury which may be suffered after consumption

of intoxication liquors or drugs.

Non-allopathic methods of surgery and treatment.

Hospitalisation and surgery for donation of an organ.

Medical or surgical treatment for weight reduction or weight improvement regardless of whether the

same is caused (directly or indirectly) by a medical condition.

Psychiatric, mental disorders (including mental health treatments and, sleep-apnoea), Parkinson and

Alzheimer's disease, general debility or exhaustion ("run-down conditions"): congenital internal or external

diseases, defects or anomalies, generic disorders: stem cell implantation or surgery, or growth hormone

therapy.

Medical expenses relating to any Hospitalisation primarily for diagnostic, X-ray or any other

investigations.

Any experimental or unproven procedures or treatments, devices or pharmacological regimens of any

description (not recognized by Indian Medical Council).

Stay in Hospital for domestic reason where no active regular treatment is given by a Doctor.

Charges for services received in convalescent home and nursing homes, nature cure clinics and similar

establishments.

Circumcision unless necessary for treatment due to an accident.

Plastic surgery or cosmetic surgery unless necessary as a part of medically necessary treatment certified

by the attending Medical Practitioner for reconstruction following an Accident or illness.

Any treatment related to sleep disorder or sleep Apnoea syndrome.

Medical Expenses incurred due to Ventral/Incisional Hernia unless the Company has paid the first

operation.

Expenses for any routine or prescribed medical check up or examination, external and or durable Medical

Non medical equipment of any kind used for diagnosis and/or treatment and/or treatment and/or monitoring

and/or maintenance and/ or support including CPAP,CAPD,Infusion pump, oxygen concentrator etc,

ambulatory devices that is walker, crutches, belts, collars, caps, splints, stings, braces, stockings, gloves,

hand soaps etc. of any kind, Diabetic footwear, glucometer/ thermometer and similar related items and also

any medical equipment, which are subsequently used at home.

33

Any kind of service charges, surcharges, admission fees, registration charges etc. levied by the Hospital.

Any natural peril (including but not limited to avalanche, earthquake, volcanic irruptions, or any kind of

natural hazard). Nuclear disaster, radioactive contamination and/or release of nuclear or atomic energy,

War, invasion, acts of foreign enemies, hostilities (whether war be declared or not), civil war, terrorism,

rebellion, active participation in strikes, riots or civil commotion, revolution, insurrection or military or

usurped power, and full-time service in any of the armed forces.

Naval or military operations ( including duties of peace time ) of the armed forces or air force and

participation in operation requiring the use of arms or which are ordered by military authorities for

combating terrorists, rebels and the like.

Participation in any hazardous activity or sports including but not limited to racing scuba dividing, aerial

sports, bungee jumping or mountaineering, activities such as hang-gliding, ballooning, and any other

hazardous activities or sports unless agreed by special endorsement.

Expenses incurred for procurement of a replacement organ, transportation costs of the replacement organ

and associated administration costs and all costs incurred by the donor.

Any insured person committing or attempting to commit a criminal or illegal act, or intentional self injury

or attempted suicide while sane or insane.

Expenses for services or treatment which are paid for by any other party or which are claimable under

workmen's compensation insurance. In such case, the Company will reimburse the difference between the

expenses that would have been reimbursable by the Company had there been no other insurer or workmen's

compensation insurance involved and the amount already reimbursed or reimbursable by other party or by

workmen's compensation insurance.

Non Medical expenses including Personal comfort and convenience items or services such as telephone,

television, personal attendant or barber or beauty services, diet charges, food, cosmetics, napkins, toiletry

items, guest services and similar incidental expenses or services.

Any hospitalisation outside India

Waiting Period

30 days waiting Period:

Hospitalisation or Medical Expenses incurred for any illness/diseases diagnosed during first 30 days of the

Policy commencement date or date of revival, whichever is later will not be reimbursed except accidental

injuries.

34

90 days waiting period:

This is applicable if any of the secondary insured members is not included on commencement of the policy

but added from a subsequent policy anniversary. Hospitalisation due to illness/treatment within 90 day from

the date of inclusion of member will be excluded.

One year waiting Period:

The following ailments/procedures are not covered during the first year of the policy from commencement

date or revival date. Tonsillectomy, Cancer of any kind.

Two years waiting Period:

The following ailments/procedures are not covered during the first two years of the policy from

commencement date or revival date. Kidney Stone/ Ureteric Stone / Lithotripsy, Cataract, Hysterectomy,

Cholelithiasis, Choledocholithiasis, surgery of Gall bladder and Bile ducts excluding Malignancy, surgery

of Benign Prostatic Hypertrophy, Hernia (Inguinal), Hemorrhoids, Anal Fissure, Fistula-in-anus,

Exploratory Laparotomy, Lapchole, diagnostic Laparoscopy, any gynaecological disease, Hydrocoele,

Fibroids,

Three years waiting Period:

The following ailments/procedures are not covered during the first three years of the policy from

commencement date or revival date. Tympanoplasty, Valve Replacement, Valvotomy, Cerebral

Haemorrhage; Angiographies, Angioplasty (with or without stent), Coronary Artery Bypass Graft, unless

post Accident.

Cost of treatment payable after completion of 1 year from the 1st term renewal:

On completion of one year after the first term renewal of the policy from commencement date or revival

date if the following diseases are diagnosed or Hospitalisation or Medical Expenses incurred are payable:

Total Knee Replacement, Total Hip Replacement, Diskectomy, Arthroscopy, unless post Accident for each

of these treatments/surgeries/procedures, Pelvic Inflammatory Disease, Varicose Veins; Diabetes with or

without high blood pressure and its complications, direct results of or accompanied by it; Chronic Renal

Failure, no matter when detected.

Grace period, Lapse & Revival (Reinstatement)

The grace period will be 30 days from the due date for payment of regular premiums under annual modes

and 15 days from the due date for payment of regular premiums under monthly mode. If premium is not

received within the grace period then the policy will lapse. The policy can be revived within 90 days from

the due date of first unpaid premium, by paying the arrears of premiums with interest at the prevailing rate

35

of interest. The current rate of interest is 9.0% p.a. This will be subject to satisfactory medical and financial

underwriting. If the lapsed policy is not revived within 90 days of the due date of the first unpaid premium

then the policy will be terminated The company will not be liable to make any payments if claims are made

due to any treatment of illness/ailment/ disease diagnosed or hospitalization taking place during the period

when the policy lapsed.

Suicide Exclusion

Self affected injuries or conditions (attempted suicide) and or the treatment directly or indirectly arising

from alcoholism or drug abuse and any Illness or Physical Injury which may be suffered after consumption

of intoxication liquors or drugs.

Claim information & role of the TPA

You have the option to avail of cash less service facility at network hospitals as identified and empanelled

by the company / Third Party Administrator (TPA). In case of a planned hospitalisation, you have to take

pre-authorization from the Third Party Administrator (TPA) prior to taking admission at any network

hospital. In case of emergency hospitalisation, you have to notify the TPA in writing within 24 hours of the

hospitalisation on medical emergency. You will be provided with a photo identity card with a unique

membership number by the TPA which will entitle you and your enrolled family members to avail of cash

less hospitalisation services. However, if you do not wish to avail of cash less facility or you are hospitalised

in any hospital other than the specified network hospitals, the company/ TPA will reimburse the admissible

medical expenses within 7 working days from the date of receipt of all relevant documents and subject to

your fulfillment of terms and conditions of the policy.

36

Simple stepwise Claim process flow:

CASH M

Free Look Period

In case you disagree with any of the terms and conditions o the policy, you may return the policy to the

Company within 15 days of its receipt for cancellation, stating your objections in which case the Company

will refund an amount equal to the premium paid less the expenses incurred by the Company on medical

examination and stamp duty charges.

Nomination

Nominations will be allowed under this plan as per Section 39 of the Insurance Act, 1938.

37

CHAPTER 3(a) RESEARCH METHODOLOGY

(b) DATA ANALYSIS

(c) DATA INTERPRETATION

38

RESEARCH METHODOLOGY

TITLE:

To determine customer-buying behavior with a focus on market segmentation for Reliance Life Insurance.

TITLE JUSTIFICATION:

The above title is self explanatory. The study deals mainly with studying the buying pattern in the

insurance industry with a special focus on Reliance life Insurance. The various segments of the markets

divided in terms of Insurance Needs, Age groups , Satisfaction levels etc will also studied.

OBJECTIVE

Objective One

.To determine reasons behind opting for an insurance.

.To provide the company with information of customer's Insurance policy if they have any and reasons for

opting for that particular policies.

.To know the most preferred policy.

Objective Two

.To determine customers perception towards private insurance companies and their expectation form private

insurance companies.

.To determine the feedback on services provided by any other insurance agent.

.To study the types of benefits provided by insurance services.

.To determine the use of Internet for valuable information and decision-making process.

SCOPE OF THE STUDY

A big boom has been witnessed in Insurance Industry in recent times. A large number of new players have

entered the market and are vying to gain market share in this rapidly improving market. The study deals

39

with Reliance in focus and the various segments that it caters to. The study then goes on to evaluate and

analyse the findings so as to present a clear picture of trends in the Insurance sector.

SIGNIFICANCE OF THE STUDY

SIGNIFICANCE TO THE INDUSTRY :

This is a limited study which takes into consideration the responses of 100 people. This data can be

explorated to take in the trends across the industry. The significance for the industry lies in studying these

trends that emerge from the study. It is a rapiddly changing and evolving sector. People are only beginning

to wake up to it’s vast possibilities. A study like this can attempt to guide the future of the industry based on

current trends.

SIGNIFICANE FOR THE RESEARCHER :

To facilitate and provide all the useful informtaion of the studt, the company, the insurance industry and

also provide marketing ways, methods of reliance life insurance.

RESEARCH DESIGN

.NON-PROBABILITY

.EXPLORATORY & DISCRIPTIVE EXPERIMENTAL RESEARCH

The research is primarily both exploratory as well as descriptive in nature. The sources of information are

both primary & secondary.

A well-structured questionnaire was prepared and personal interviews were conducted to collect the

customer’s perception and buying behavior, through this questionnaire.

SAMPLING METHODOLOGY

SamplingTechnique:

Initially, a rough draft was prepared keeping in mind the objective of the research. A pilot study was done in

order to know the accuracy of the Questionnaire. The final Questionnaire was arrived only after certain

important changes were done. Thus my sampling came out to be judemental and convinent

Sampling Unit:

40

The respondants who were asked to fill out questionnaires are the sampling units. These comprise of

employees of MNCs, Govt. Employees, Self Employeds etc.

Sample size:

The sample size was restricted to only 100, which comprised of mainly peoples from different regions due

to time constraints.

Sampling Area :

The area of the research was Pehowa, India.

MARKETING STRATREGIES OF THE COMPANY

. SOME OF THE STRATEGIES ADOPTED BY RELIANCE LIFE INSURANCE COMPANY.

Reliance Life Insurance plans to tap Reliance Communications' 2.5-crore telephony subscriber base to

market its products. The company is considering a series of options to leverage its relationship with

Reliance Communications.

However, a joint product or a co-branded solution would require approval from the Insurance Regulatory

and Development Authority

Customers of R World, the information and entertainment portal of Reliance Communications, would also

be able to pay premiums through a bank account, provided the bank is listed on the network.

Reliance Life Insurance officials, however, offered no comment when asked whether there would be an

arrangement for payment of commission to Reliance Communications. As an alternative channel for

distribution, insurance companies usually tie up with banks. In the case of bank assurance, where there is a

corporate agency tie-up, the commission

41

DATA ANALYSIS & INTERPRETATION

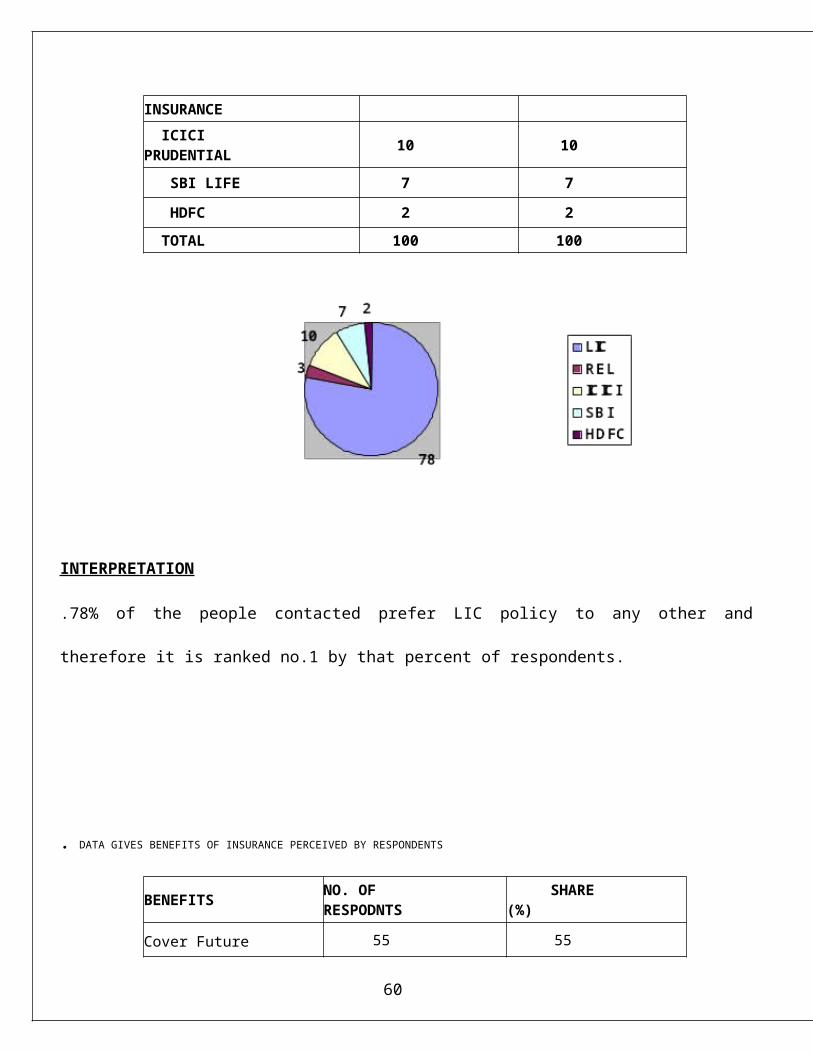

. DATA GIVES PREFERENCE OF RESPONDENTS OF INSURANCE COMPANIES

COMPANY’S NAMENO.OF RESPONDENT

SHARE (%)

L.I.C. 78 78

RELIANCE LIFE INSURANCE

3 3

ICICI PRUDENTIAL 10 10

SBI LIFE 7 7

HDFC 2 2

TOTAL 100 100

INTERPRETATION

42

.78% of the people contacted prefer LIC policy to any other and therefore it is ranked no.1 by that percent of

respondents.

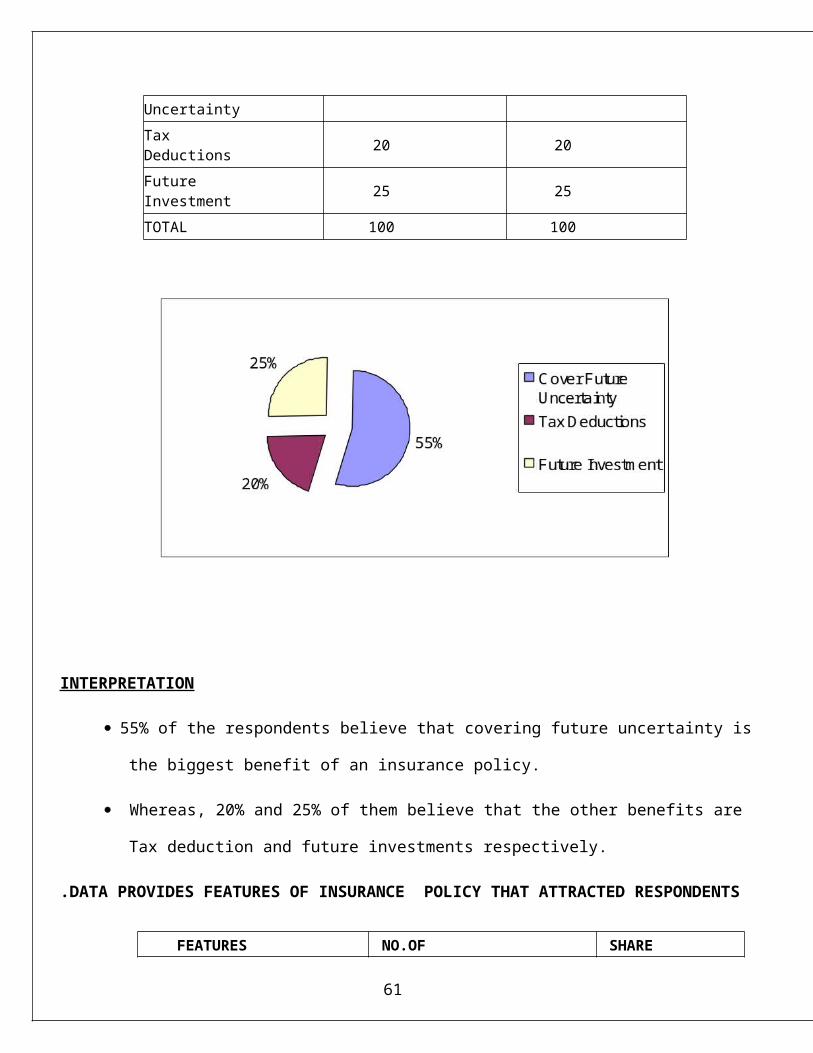

. DATA GIVES BENEFITS OF INSURANCE PERCEIVED BY RESPONDENTS

BENEFITSNO. OF RESPODNTS

SHARE (%)

Cover Future Uncertainty

55 55

Tax Deductions 20 20

Future Investment 25 25

TOTAL 100 100

INTERPRETATION

43

55% of the respondents believe that covering future uncertainty is the biggest benefit of an

insurance policy.

Whereas, 20% and 25% of them believe that the other benefits are Tax deduction and future

investments respectively.

.DATA PROVIDES FEATURES OF INSURANCE POLICY THAT ATTRACTED

RESPONDENTS

FEATURES NO.OF RESPONDENTS SHARE (%)

Money Back Guarantee 15 15

Larger Risk Coverance 37 37

Easy Access to Agents 7 7

Low Premium 30 30

Company’s Reputation 11 11

TOTAL 100 100

INTERPRETATION

44

. Majority of the respondent (37%) found Larger risk coverance as the most attracted feature of the all.

45

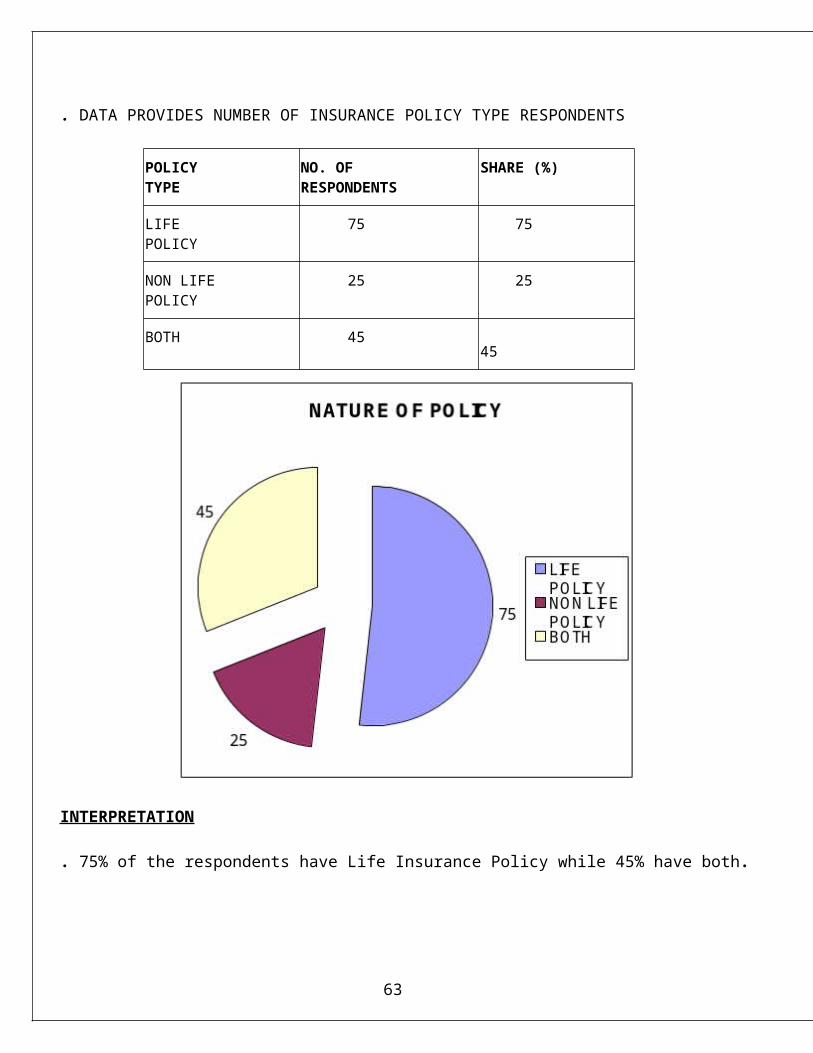

. DATA PROVIDES NUMBER OF INSURANCE POLICY TYPE RESPONDENTS

POLICY TYPE

NO. OF RESPONDENTS

SHARE (%)

LIFE POLICY 75 75

NON LIFE POLICY

25 25

BOTH 45 45

INTERPRETATION

. 75% of the respondents have Life Insurance Policy while 45% have both.

46

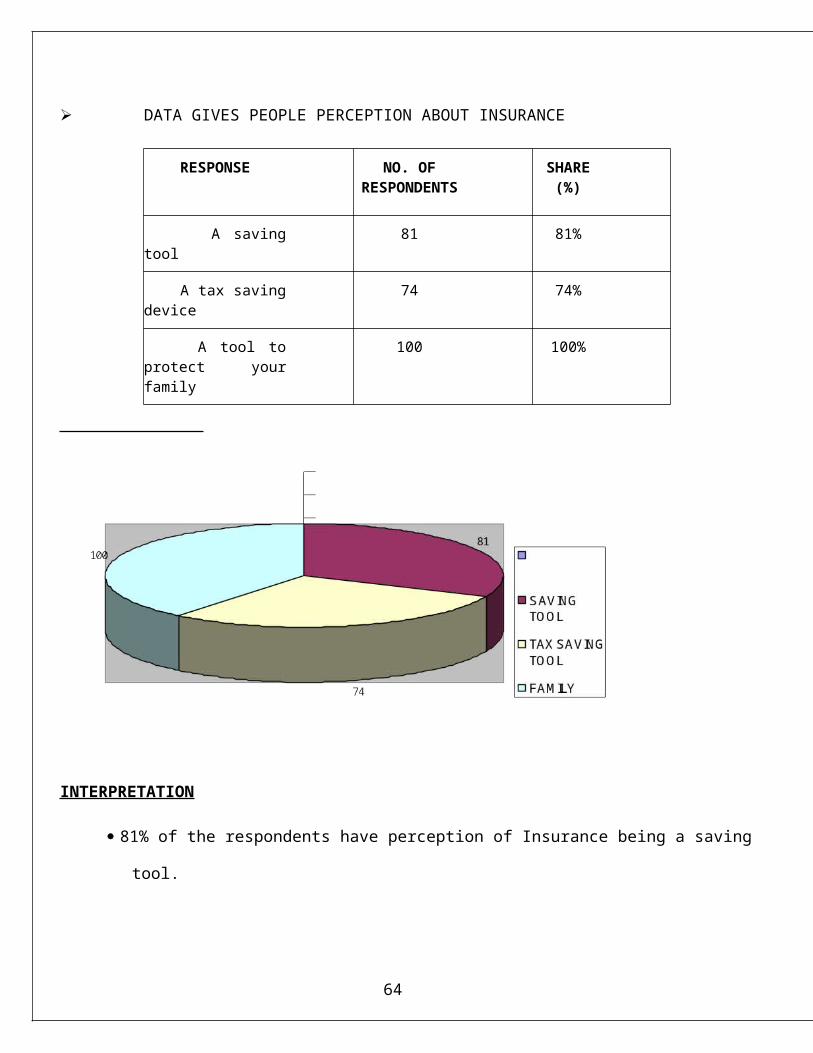

DATA GIVES PEOPLE PERCEPTION ABOUT INSURANCE

RESPONSE NO. OF RESPONDENTS

SHARE (%)

A saving tool 81 81%

A tax saving device 74 74%

A tool to protect your family

100 100%

INTERPRETATION

81% of the respondents have perception of Insurance being a saving tool.

And 74% of the respondents have perception of Insurance being a tax saving device.

But 100% of the respondents are with the view that Insurance is a tool to protect your family.

47

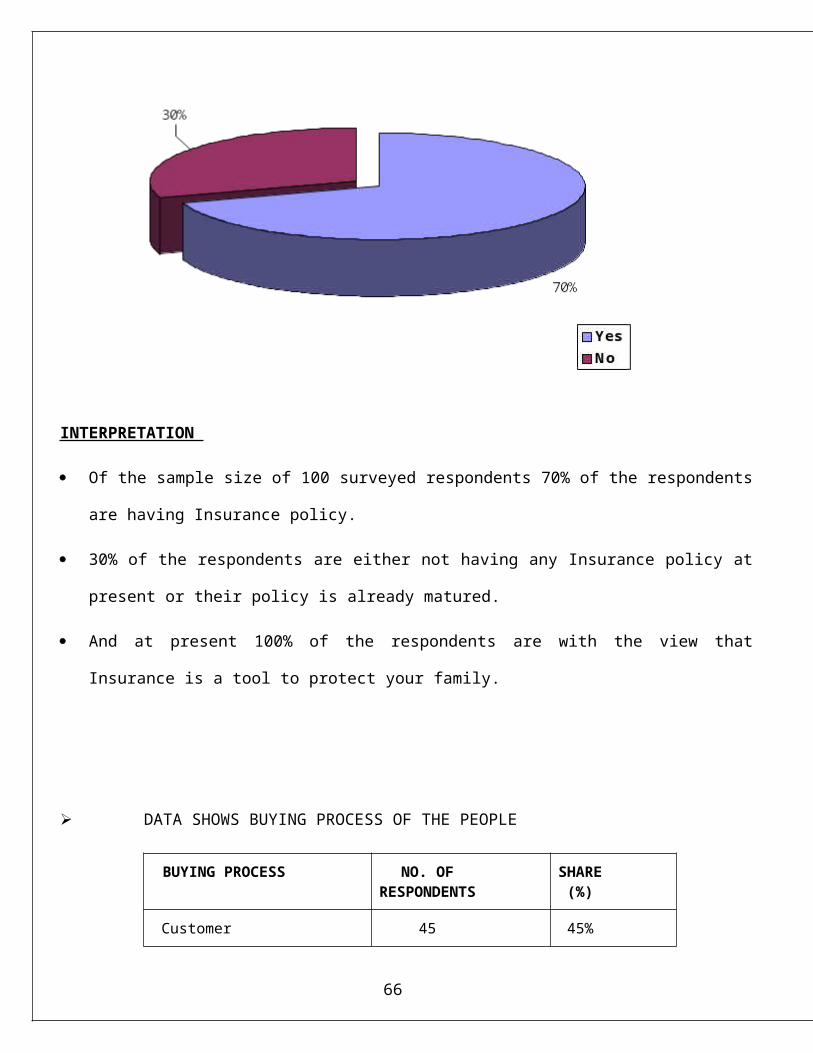

DATA SHOWS PEOPLES HAVING INSURANCE

RESPONSE NO. OF RESPONDENTS

SHARE (%)

Yes 70 70%

No 30 30%

100 100%

INTERPRETATION

Of the sample size of 100 surveyed respondents 70% of the respondents are having Insurance policy.

30% of the respondents are either not having any Insurance policy at present or their policy is already

matured.

And at present 100% of the respondents are with the view that Insurance is a tool to protect your

family.

48

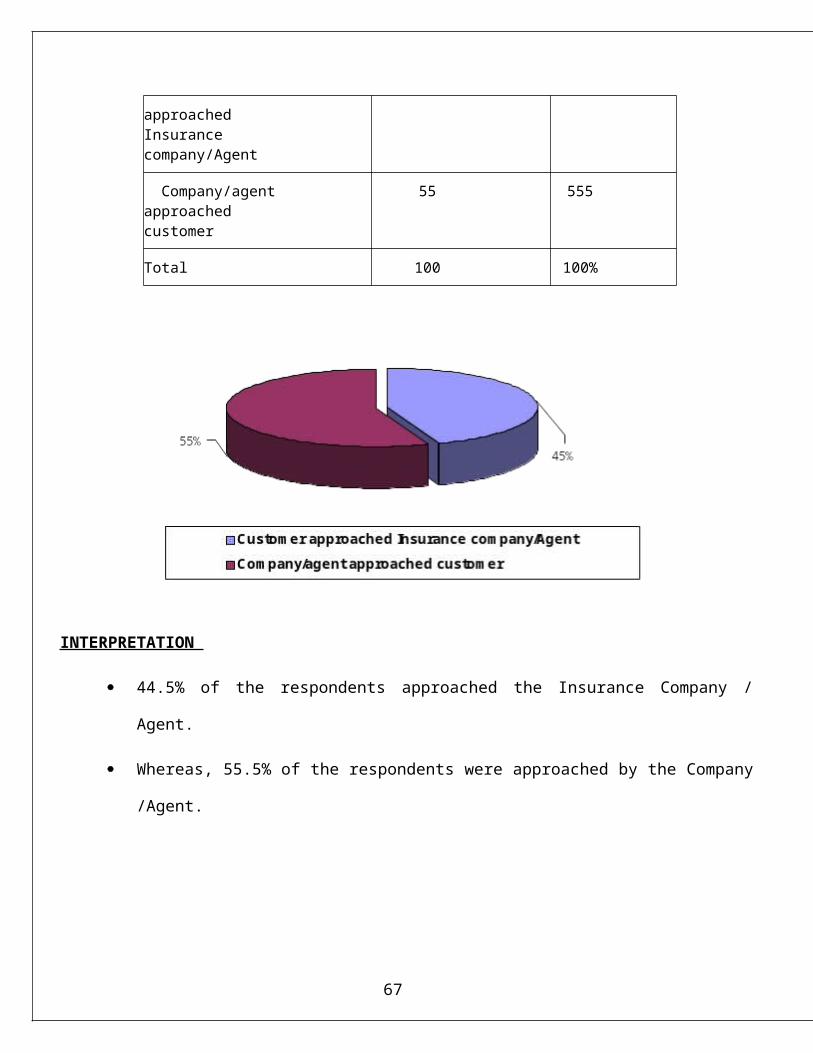

DATA SHOWS BUYING PROCESS OF THE PEOPLE

BUYING PROCESS NO. OF RESPONDENTS

SHARE (%)

Customer approached Insurance company/Agent

45 45%

Company/agent approached customer

55 555

Total 100 100%

INTERPRETATION

44.5% of the respondents approached the Insurance Company / Agent.

Whereas, 55.5% of the respondents were approached by the Company /Agent.

49

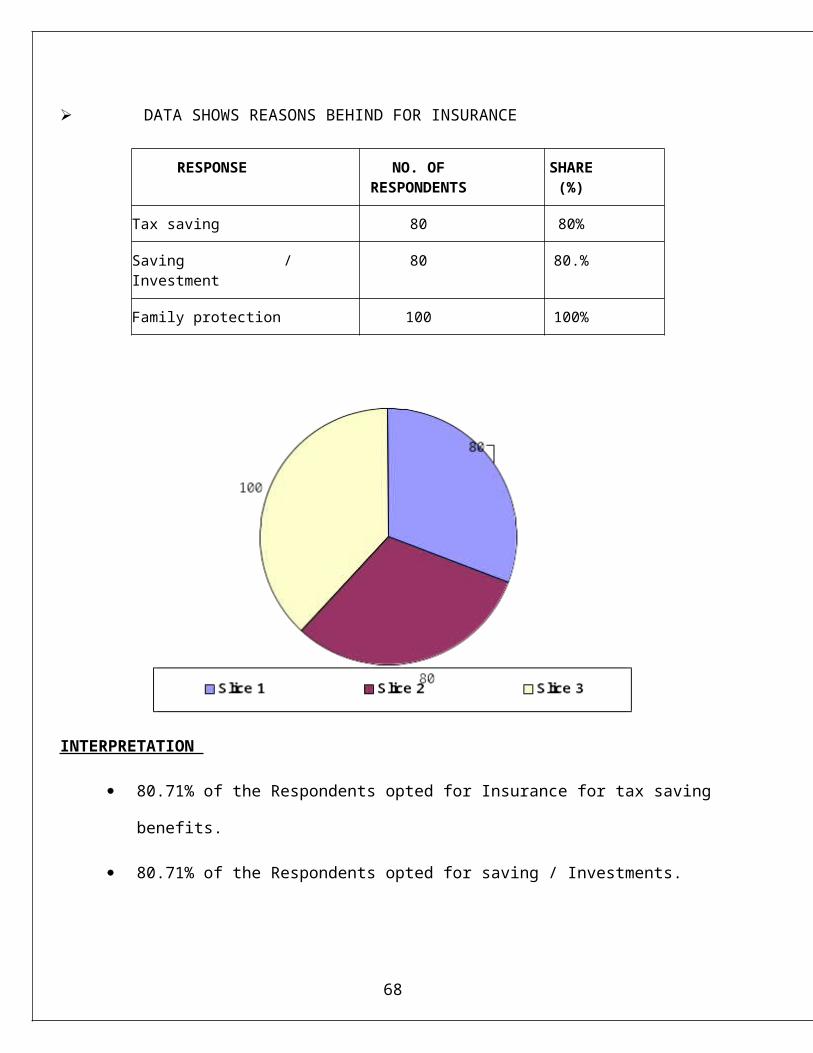

DATA SHOWS REASONS BEHIND FOR INSURANCE

RESPONSE NO. OF RESPONDENTS

SHARE (%)

Tax saving 80 80%

Saving / Investment 80 80.%

Family protection 100 100%

INTERPRETATION

80.71% of the Respondents opted for Insurance for tax saving benefits.

80.71% of the Respondents opted for saving / Investments.

But all of them, i.e. 100% of the respondents have opted for insurance for their family

protection.

50

DATA SHOWS SATISFACTION OF RESPONDENTS WITH RESPECT TO POLICY

RESPONSE NO. OF RESPONDENTS

SHARE (%)

Satisfied 60 60%

Not satisfied 40 40%

Not Responded 0 0.0%

Total 100 100%

INTERPRETATION

60% of the respondents are more or less satisfied with their existing policy.

40% of the respondents are not satisfied with their existing policy.

In this case all of those who have taken a policy have responded.

51

DATA SHOWS SATISFACTION OF +RESPONDENTS WITH RESPECT TO SERVICE

AGENT

RESPONSE NO. OF RESPONDENTS

SHARE (%)

Satisfied 45 45%

Not satisfied 55 55%

Not Responded 0 0.0%

Total 100 100%

INTERPRETATION

45% of the respondents are satisfied with their existing service agent.

55% of the respondents are not satisfied with their existing insurance agent.

All of those who have taken a policy have responded.

52

DATA SHOWS NUMBER OF RESPONDENTS PAYING TAX

RESPONSE NO. OF RESPONDENTS

SHARE (%)

Paying tax 100 100%

Not paying tax - 0%

Total 100 100%

INTERPRETATION

Of the sample size of 400 respondents, all the respondents are paying tax.

53

DATA SHOWS RESPONDENT’S INVESTMENTS FOR TAX SAVING

INVESTMENTS NO. OF RESPONDENTS

SHARE (%)

LIC 51 51%

NSC 33 33%

Bonds 32 32%

PPF 25 25%

PF 21 21%

EPF 11 11%

INTERPRETATION

51% of the respondents save their tax by investing in LIC, which is the highest among all Investment.

This shows that most people for getting taxes benefits invest in LIC.

33.25% of the respondents do their tax saving by investing in NSC.

32.25% of the respondents to their tax saving by investing in bonds.

DATA SHOWS RESPONDENTS PERCEPTION ABOUT BEST FORM OF INVESTMENT

FOR SECURING THEIR FUTURE

PARTICULARS NO. OF RESPONDENT

SHARE (%)

Fixed Assets 75 75%

Bank deposits 11 11%

Jewellery 25 25%

Securities i.e. bonds, MFs 40. 40%

Shares 10 10%

Insurance 70 70%

54

INTERPRETATION

75.25% of the respondents as with the view that Fixed Assets is the best form of investment for

securing their future.

70.5% of the respondents are with the perception that Insurance is the best form of investment

for securing their future, which is one of the highest and this shows that insurance is an

important key for securing your future.

DATA SHOWS WHAT PEOPLE INTENT TO GAIN FROM THEIR INVESTMENT

RESPONSE NO. OF RESPONDENTS

SHARE (%)

Saving & Returns

100 100%

Security 90 90%

Tax benefits 71. 71.%

55

INTERPRETATION

100% of the respondents intent to gain saving and returns from their investment.

90% of the respondent’s intent to gain security from their investments.

Whereas, 71.75% of the respondent’s intent to gain tax benefits from their investments.

DATA GIVES PEOPLE’S PERCEPTION ON APPROPRIATE AGE FOR BUYING

INSURANCE

RESPONSE NO. OF RESPONDENTS

SHARE (%)

After 25 years 29 29%

After 35 years 10 10%

After 45 years 0 0%

Anytime 60 60%

56

INTERPRETATION

29% of the respondents are with the view that insurance should be bought after the age of 25

years.

10.5% of the respondents are with the view that insurance should be buyed after the age of 35

years.

Whereas, 60.5% of the respondents are with the view that buying of insurance do not have any

thing to do with age i.e. there is no age limitations. It can be purchased any time according to

the need.

57

DATA SHOWS PEOPLE OPINION ABOUT INDIAN INSURANCE COMPANIES

RESPONSE NO. OF RESPONDENT

SHARE (%)

Rigid plans 67 67%

Non user friendly 29 29%

Unsatisfactory services 26 26%

Non Aggressive 35 35%

Satisfactory 24 24%

Good 10 10%

Very good 0 0%

INTERPRETATION

67% of the respondents have the opinion that Indian Insurance Companies have Rigid plans.

29.5% feel that Indian Insurance companies are Non-user friendly.

58

26.5% feel that services of Indian Insurance companies are Unsatisfactory.

35.75% of the respondents are with the view that Indian Insurance companies are Non-

aggressive.

24% of the respondents feel that products and services of Indian Insurance companies is

Satisfactory.

Whereas only 10.25% feel that it is Good enough.

And according to the data, no single person has felt that it is very good.

DATA SHOWS WHAT PEOPLE WOULD LOOK FOR IN AN INSURANCE COMPANY

RESPONSE NO. OF RESPONDENTS

SHARE (%)

A trusted name 82 82%

Friendly service & responsiveness

71 71%

Good plans 81 81%

Accessibility 49 49%

59

INTERPRETATION

82% customers look for a Trusted name in a company for insurance.

81.5% customers look for a good plan in a company for insurance.

Friendly service & responsiveness and Accessibility are also important factors looked by

customers in a company.

. DATA SHOWS PEOPLE PLANNING FOR NEW INVESTMENTS

RESPONSE NO. OF RESPONDENTS

SHARE (%)

Planning 87 87%

Not planning 13 13%

Total 100 100%

INTERPRETATION

Only 12.5% of the customers contacted are not planning for new investments presently.

Whereas, 87.5% of the customers are still planning for new investments this can be a great

potential for Reliance Life Insurance to take them on their favor.

. DATA SHOWS PEOPLE INTERESTED IN GOING FOR INSURANCE IF A SERVICE

PROVIDER AWAY FROM THE CITY OFFERS BETTER SERVICE & PRODUCTS

RESPONSE NO. OF RESPONDENTS

SHARE (%)

Yes 43 43%

60

No 44 44%

Uncertain 13 13%

Total 100 100%

INTERPRETATION

The interested customers i.e. 43% are ready to go for insurance even away from a city if services and

products are worthwhile, which again is a good prospect (potential) for Reliance Life Insurance to take them

on their favor.

CHAPTER 4

61

(a) SWOT ANALYSIS

(b) CONCLUSION

(c) SUGGESTION

4.1 SWOT ANALYSIS of Reliance life Insurance

62

4.2. Suggestions and recommendation

63

✔ People are not aware of the life insurance. Most of them know only one company which provides life

insurance i.e. LIC. So awareness campaign should be run so that people are aware of different life insurance

companies in India.

✔ People should be educated about the different types of products or plans offered by the life insurance

companies. Most of them don’t know much of the different types of plan or products.

✔ It was felt that most of the people took life for tax savings or just to cover up their life, not as an

investment avenue. Life Insurance companies need to advertise in such a manner that people start investing

in life insurance like the way they invest in the stock market

✔ Now at the time of global turmoil insurance company had to hold on to the policyholders trust which

might lead the company to the path of success

✔ Insurance companies should try to adopt different strategies to market their products or plan. Companies

should not primarily focus on the agents for their business.

4.3. Conclusion

64

Insurance is one sector that witnessed continuous growth owing to the reforms in 2000. The insurance sector

is likely to attain a size of Rs. 2,00,000 crore ($ 51.2 billion) in 2012-13. In life insurance, the business

grew by 23.3% to Rs. 93,000 crore in 2010-11 (Source:Assocham). The sector alone employs close to 30

lakh people (including agents and direct employees).A well-functioning insurance market plays an

important role in economic development and financial stability of developing economies such as India’s.

First, it inculcates and encourages the habit of saving. Second, it provides a safety net to rural and urban

enterprise and productive individuals The life insurance market in India is on a growth path. In spite of this,

the country lags far behind the others in awareness about life insurance. The challenge is to spread

awareness about life insurance and it true benefits. The industry has to convince people to park their hard

earned money in long-term insurance and not just look at it as a tax saving instrument.

Learning From The Report

65

From this report I had learned that what is insurance , why do we need insurance, why insurance is

nessacery for every person, how much it is beneficial for business, how it is helpful in investment and how

it is beneficial for family.

And also learned that how about the life insurance sectors in india , especially about the Reliance Life

Insurance, how does they work , how many policies it contains and how these policies are benfecial to us

and for our family.

66

ANNEXURE

QUESTIONNAIRE

1. ARE YOU EMPLOYED?

YES NO

If YES, only then proceed

2. DO YOU HAVE ANY INSURANCE POLICY?

YES NO

3. WHICH INSURANCE POLICY DO YOU HAVE?

LIFE NON-LIFE BOTH

4, WHICH CO’S INSURANCE POLICY YOU PREFER THE MOST? (RANK THEM)

a) LIC

b) ICICIPRUDENTIAL

c) SBI LIFE INSURANCE

d) ING VYSYA LIFE

e) RELIANCE LIFE INSURANCE

67

f) TATA AIG LIFE

g) ANY OTHER ________( Specify)

5. FOR HOW MANY YEARS DO YOU HAVE INSURANCE POLICY? (Please Tick)

a) <5Yrs b) 5-10 Yrs c) 10-15 Yrs d) Any Other______

(Specify)

6. WHAT DO YOU THINK ARE THE BENEFITS OF INSURANCE COVER? (RANK THEM)

a) COVER FUTURE UNCERTAINITY

b) TAX DEDUCTIONS

c) FUTURE INVESTMENT

d) ANY OTHER _________ (Specify)

7. WHICH FEATURE OF YOUR POLICY ATTRACTED YOU TO BUY IT? (RANK THEM)

a) LOW PREMIUM

b) LARGER RISK COVERANCE

c) MONEY BACK GUARNTEE

d) REPUTATION OF COMPANY

e) EASY ACCESS TO AGENTS

68

f) ANY OTHER _________ (Specify)

8. YOUR MONTHLY INCOME?

a)<4k b)4k-8k c)8k-12k d)12k-16k e)Other_____(Specify)

9. DO YOU REALLY THINK INSURANCE POLICY COVER IN TODAY’S SCENARIO IS NOT

ESSENTIAL?

10. WHAT’S YOUR PERCEPTION ABOUT INSURANCE? (RANK THEM)

a) A SAVING TOOL

b) A TAX SAVING DEVICE

c) A TOOL TO PROTECT FUTURE

11. HOW HAS/WOULD YOU BOUGHT/BUY AN INSURANCE?

a) CUSTOMER APPROCHED INSURANCE COs

b) INSURANCE COs APPROCHED CUSTOMER

12. ARE YOU SATISFIED WITH THE POLICY?

69

a) SATISFIED SAVING TOOL

b) NOT SATISFIED

c) NOT RESPONDING

13. ARE YOU SATISFIED WITH THE SERVICE AGENT?

a) SATISFIED SAVING TOOL

b) NOT SATISFIED

c) NOT RESPONDING

14. WHERE HAVE YOU INVESTED FOR TAX SAVING?

(RANK THEM)

a) LIC

b) NSC

c) BONDS

d) PPF

e) PF

f) EPF

70

15.WHICH IS THE BEST FORM OF INVESTMENTS?

(RANK THEM)

a) FIXED ASSETS

b) BANK DEPOSITS

c) JEWELLERY

d) SECURITIES, i.e. Bonds, MFs

e) SHARES

f) INSURANCE

71

BIBLIOGRAPHY

1.BOOKS/MAGAZINES REFFERED:

STUDY GUIDE- PRINCILES & PRACTICES OF LIFE / GENERALINSURANCE, by AIMA.

Books published by INSURANCE INSTITUTE OF INDIA

LIFE-INSURANCE, by Mc GILL

INSURANCEWATCH.

MONEYOUTLOOK.

2. WEBSITES REFFERED:

www.reliancelife.co.in

WWW.CIFAINSURANCE.COM

WWW.MONEYOUTLOOK.COM

WWW.INSURANCE.IND.COM

72