regulatory challenges and islamic banking in the cross ... · the islamic banking is facing often...

TRANSCRIPT

Prepared by

Dr. Abul Bashar Bhuiyan

Regulatory Challenges and Islamic

Banking in the Cross Border

Operations

In the era of high-growth Islamic banking:Islamic mode of finances have identified the best-fit alternative and trusted financialmethods over the world.

With the increasing demand :The Islamic mode of financing from the cross countries customers, the Islamic Bank is

offering cross border opportunity of transaction in the global market .(Brown & Skully, 2007).

Even:There are many more conventional banks who are offering to provide the Islamicbanking products to their Muslim customers within the national and internationalperspective.

On the other hand:They are opening an Islamic banking window or Islamic banking section(Mohammad Kabir Hassan & Mehmet F. Dicle, 2005).

In the same way:In such situation cross border banking activities are playing vital roles for meeting

up raising demand of global customers.

Introduction

Introduction

Due to changing features of banking in the global market:The Islamic banking is facing often challenges to make appropriate rules andregulations to cope up with present coming demand for their customer

with Conventional counterparts base on the Islamic Shariah principles. (Gavin,

Gibson, McCrum, & Summers, 2010; Mamun, Hassan, & Isik, 2011).

Because of :It is merely easy to operate the Islamic Banking activities in the cross bordercountries within the umbrella of Conventional banking operation in thedifferent traditional rules, custom and regulation (Amihud, DeLong, & Saunders, 2002; Mohamad,

Hassan, & Bader, 2008).

Thus:Islamic Banking are facing strong regulatory challenges in the

cross border activities.

Shariah is the main sources for Islamic economy and finance. It

comes from the Arabic word as meaning of Islamic Law.

Shariah covers not only religious rituals, but many aspects of day-to-day life,

politics, economics, banking, business or contract law, andsocial issues.

The main sources of Islamic law:

The Holly QuranThe Hadith or directions of the prophet Muhammad (PBH).

Ijma is the drawing analogy from the essence of divine principles.

Qiyas is the various forms of reasoning, including by analogy are used

by the law scholars to deal with situations where the sources provided noconcrete rules.

REGULATORY SOURCES OF ISLAMIC LAW

Cross Border Issues and Islamic Bank

The competitions of Islamic and conventional banks are increasing day by dayin the cross border transaction due to globalization (Brown and Skully, 2007).

Due to the globalization the world banking are rapidly converging into asingle marketplace.

On the other hand,The liberalization of foreign exchange markets it has further reinforced inthis trend.

Further more:Technological innovations are also playing an important part in financialintegration and globalization (Amuda, Ariss and Sarieddine, 2007).

The Islamic Banking perspectives:It is a prime challenges to introduce new Shariah-compatible products on thebasis of the Shariah laws that can be meet the demand of investors, financialintermediaries, and entrepreneurs for liquidity and safety (Hassan and Dicle, 2005, Iqbal,

2007, Tahir and Bakar, 2009).

Moreover:It is not so easy to operate the Islamic banking activities in the cross border

countries within the umbrella of Conventional banking operation in thedifferent traditional rules, custom and regulation .

Thus:Islamic banking is facing strong regulatory challenges in the cross borderactivities:Financial engineeringUnique Shariah AuthorityHarmonization of Shariah RulingsLack of Profit and Loss Sharing FinancingLack of proper institutional frameworkLack of appropriate legal frameworkLack of equity institutionsMaintaining of proper accounting standardsCost and competitiveness of cross-jurisdictionsLack of equal field for Islamic and Conventional bankingRisk management and diversificationDevelop of the capital marketRisk of contracting and documentationChallenges for Deposit InsurersIntervention and Resolution Mechanisms:

Cross Border Issues and Islamic Bank

Contemporary Issues:Financial innovations are the main challenges in the Banking sectores, to cope

up with the rising demand from the rapidly changing of the world financialtrends.

They are facing big challenges to process of:

New design.Development and implementation of innovative financial instruments andproducts.Formulation of creative solutions to corporate financial problems.

In the Islamic banking perspectives:It is also a prime challenge of Islamic Bank’s for offering a new products with

different risk-return profiles that meet the demand of: Investors Financial intermediaries and

Entrepreneurs

for ensure liquidity and safety on basis of shariyah rules and regulations.

Financial Engineering

Financial Engineering

In the cross border context:The global transactions have been increased and as well as increased difficulties lackof integrated capital market.

Thus:It is beggest regulatory threat of Islamic Banking activities to produces new butuniqe financial innovations in the cross border countries within the umbrellaof Conventional banking operation in the different traditional rules, customand regulations.

Way of Solutions:Conducting basic research and development collectively on the market trend andpossible shariah obligations.

Islamic bank has to focus on the development of new products that foster marketintegration and attract investors and entrepreneurs.

Making joint efforts to develop the basic infrastructure for introducing newproducts.

Contemporary Issues:

The the Shariah board is the main regulatory council of the Islamicbanking who controls the whole banking system on the basis ofIslamic Shariah.

But it is very prety for Islamic Banking there is no Unique Shariah Authorityover the Islamic World:

Even every bank have a separate Shariah council to examine and evaluateseach new product but there are merely coordinating with other banks withinthe boundary or cross boundary.

Because of:Differents particular schools of thought.Diversity of Shariah explanations on the practices or products.Diversity of local customs, traditions, norms etc.

Unique Shariah Authority and Harmonization of Shariah Rulings: :

In the cross border arena:Lack of proper standardization of common product for all schools ofthought; it has faced challenges in the cross border arena and there is merelycoordinating with other banks within the boundary or cross boundary.

Thus:The harmonization of Shariah rulings through unique Shariah authority is

essential to make a smooth operation of Islamic banking activities in the crossborder arena.

To solve these issues integrated and unique Shariah decision can be minimizedTime Effort and

Confusion for innovation a new product.

In such situations:

Islamic scholars agreed to develop common Shariah standardsorganizations as similar as:

The Islamic Financial Services Board (IFSB) andThe Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI).

Unique Shariah Authority and Harmonization of Shariah Rulings: :

Islamic mode of finances are based on:The fixed charge on the capital investment and sharing profit from lendingmoney and both of types provide financing through the purchase and sale ofreal commodities.

On the other hand:The Conventional Banking financial transactions are based on lending and borrowingof money for a fixed charge (interest).

In the context of cross border transactions:Islamic banking are facing conflicts with Conventional parts due to interest basedmentality rather profit and loss sharing financing.

In some cases:Islamic bank being used fixed-return mode of financing such as Murabahah andleasing that’s been clearly distinguishable from the Conventional mode of financesince the transaction with these modes are always on the basis of real.

Furthermore:

For safe of cross border activities, the Islamic banks can be encouraged toprovide more profit-sharing finance products to conventional counterparts.

Lack of Profit and Loss Sharing Financing

Contemporary Issues:The legal supervisory entity is an important issues in thecompetitive global cross border transaction for both of Islamicbanking and Conventional one.

Operate by Same Act:The most of the country central bank has supervised all types ofbanking activities and Islamic banks are also controlled by thesame act of the central bank as like as Conventional bank.

Although:Some countries issue a special Islamic Banking Act to govern theoperations of specific Islamic banks and their relationship withthe central bank.

Regulatory Issues of Islamic Bank:

It is big difficulties for Islamic bank to adjust within sameregulation with traditional interest based convention banking.

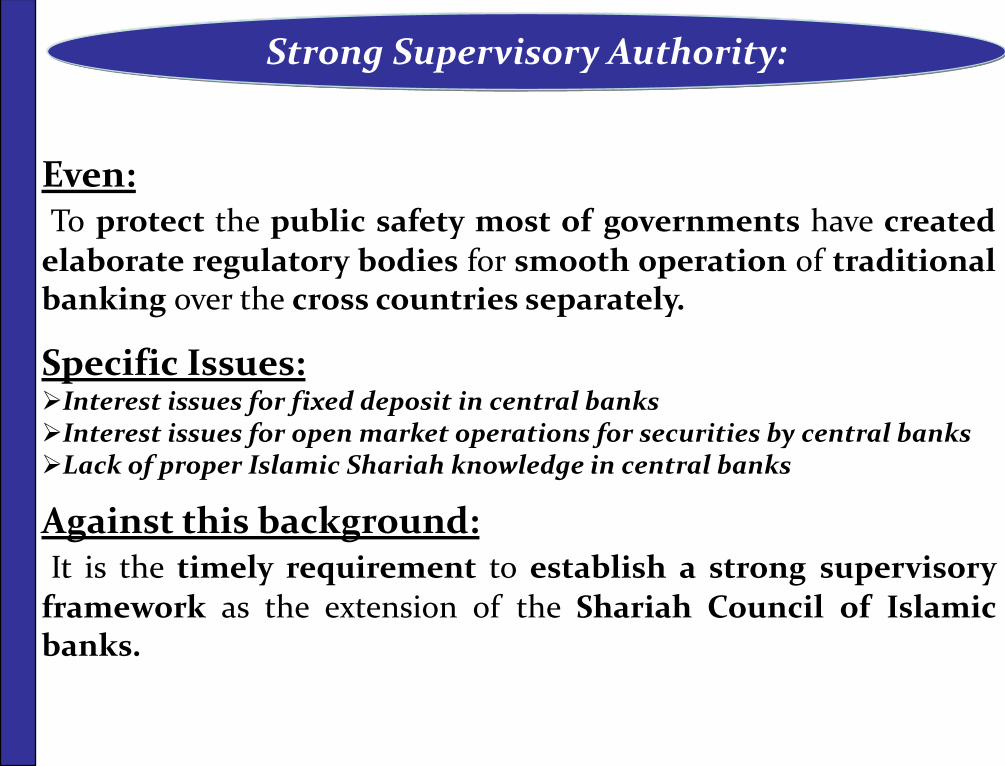

Strong Supervisory Authority:

Strong Supervisory Authority:

Even:To protect the public safety most of governments have created

elaborate regulatory bodies for smooth operation of traditionalbanking over the cross countries separately.

Specific Issues:Interest issues for fixed deposit in central banksInterest issues for open market operations for securities by central banksLack of proper Islamic Shariah knowledge in central banks

Against this background:It is the timely requirement to establish a strong supervisory

framework as the extension of the Shariah Council of Islamicbanks.

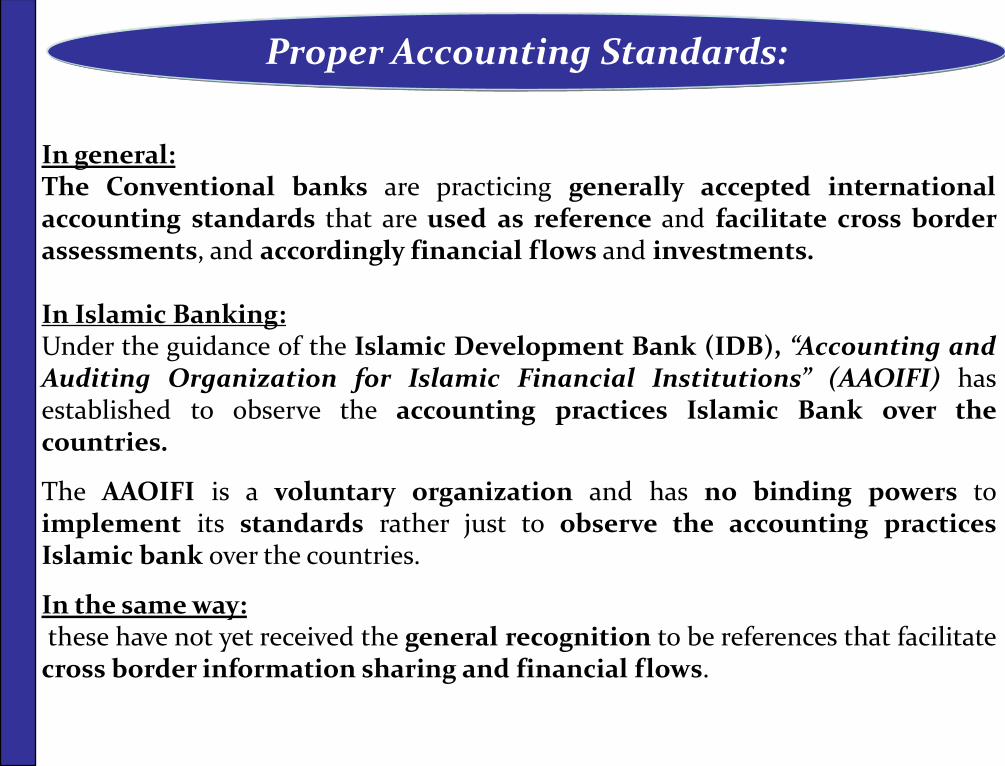

In general:The Conventional banks are practicing generally accepted internationalaccounting standards that are used as reference and facilitate cross borderassessments, and accordingly financial flows and investments.

In Islamic Banking:Under the guidance of the Islamic Development Bank (IDB), “Accounting andAuditing Organization for Islamic Financial Institutions” (AAOIFI) hasestablished to observe the accounting practices Islamic Bank over thecountries.

The AAOIFI is a voluntary organization and has no binding powers toimplement its standards rather just to observe the accounting practicesIslamic bank over the countries.

In the same way:these have not yet received the general recognition to be references that facilitate

cross border information sharing and financial flows.

Proper Accounting Standards:

Accordingly:Diversity without a set of common references is likely tocompound the challenges of cross border comparisons and mayput Islamic banking services at a competitive disadvantage.

In such situation to address the above issues:All the Islamic banks over the world should maintain commonaccounting standards which are provided by (AAOIFI).

The AAOIFI should also work to find out the way of solution forthe conflict between the accounting standard Conventionalbank and Islamic bank based on the Shariah principles.

Proper Accounting Standards:

Contemporary Issues:The competitions of Islamic and Conventional banks are increasing day by day in thecross border transaction due to globalization. The world markets are rapidlyconverging into a single marketplace.

Technological innovations:

Technological innovations are also playing an important part in financial integrationand globalization.

Electronic correspondence:The discovery of easy communication wave through electronic correspondence thecustomers in many countries can navigate on the Internet banking, unit trusts,mutual funds and even business firms.

Islamic banks in cross border markets:The Islamic banks have to increase the size of their operations as well as form strategicalliances with other banks through the adopted modern technological inventionscarefully.

It will also be useful to build bridges between existing Islamic banks and those

Conventional banks that are interested to do banking on Islamic Principles.

Level Playing Field for Islamic and Conventional Banking

Contemporary Issues:In general, while the market is expanding as well as enhancing riskmanagement practices and their related skill and information requirementsis another challenge facing Islamic banking in the cross countrytransactions.

The current wave of capital market liberalization and globalization isprompting the need for enhanced risk management measures, especiallyfor the developing economies and emerging markets.

Risk categories in Islamic banking cross border transactions :

Due to the absence of shariah compliant instruments, the main of riskcategories are liquidity risks are substantial because of the inability to manageassets and liability maturity mismatches.

Proper Risk Management

Proper Risk Management

In such condition:Islamic banks are often unable to facilitate the high-cost management information systems or right thetechnology to assess and monitor risk in the sphere oforganizational area.

Even:The risk exposure of Islamic banks is high due to weakmanagement and lack of proper risk-monitoringsystems.

Furthermore:The Islamic banks need to adopt the appropriate risk

management system not only for their own portfoliobut also for that of their clients.

To construct a rich Islamic capital market is the one of regulatorychallenges of smoothly expanding Islamic banking activities inthe cross border boundary.

Well formed Islamic capital markets will provide :Available access of loan to the borrowersBenefit to institutional investors to certain investmentEnhance the stability of islamic banksImproved portfolioImproved Liquidity andImproved Risk management tools.

But there are certain obstacles must be faced to establish goodstructure Islamic capital market.

Especially host country government has to take the responsibilityto support in the legal and regulatory issues for further marketdevelopment.

Development of Islamic Capital Market:

A well structured and effective deposit insurers ensure to buildpublic confidence through well governed and well managed.

It must be transparent in their operation to the depositors forincreasing awareness of deposit insurance benefits andlimitations to help mitigate bank runs during bad times.

The Islamic banking is the amazing sectors in the worldeconomy with facing many folds of challenges withcounterparts.

Because of; they have to follow the Shariah guidelines to offer anytypes new investments

•Lack of guidelines and regulatory documents•Issues of Contacts•Issues of Disposal Assets•The lack of skilled human capital.

Regulatory Challenges for Deposit Insurers:

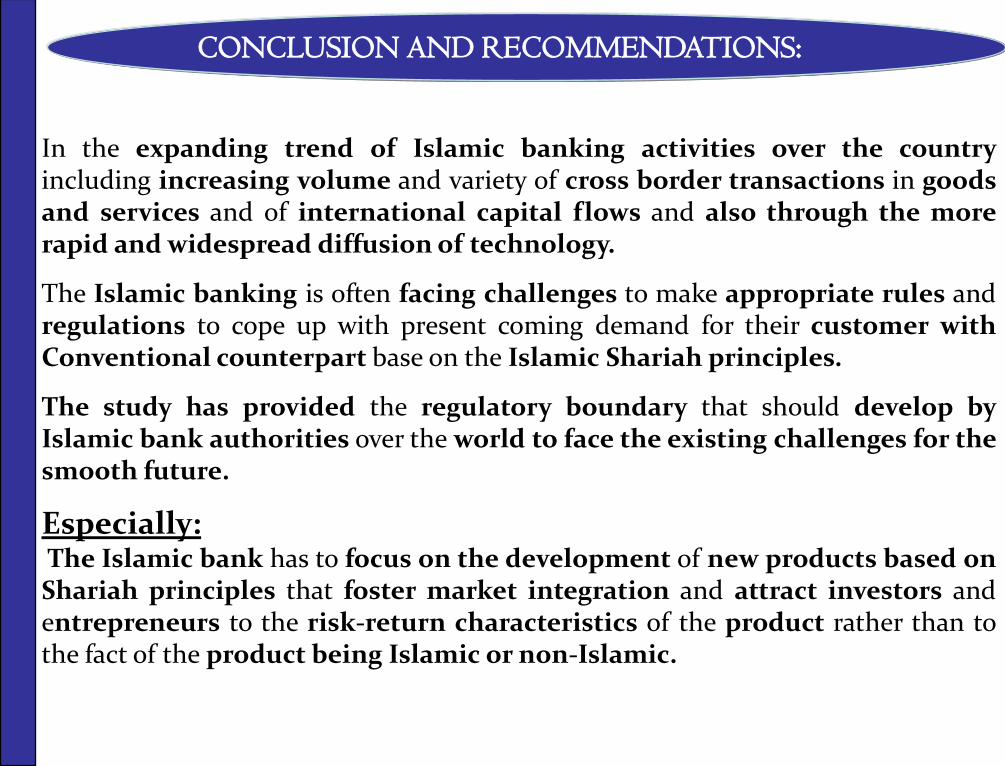

In the expanding trend of Islamic banking activities over the countryincluding increasing volume and variety of cross border transactions in goodsand services and of international capital flows and also through the morerapid and widespread diffusion of technology.

The Islamic banking is often facing challenges to make appropriate rules andregulations to cope up with present coming demand for their customer withConventional counterpart base on the Islamic Shariah principles.

The study has provided the regulatory boundary that should develop byIslamic bank authorities over the world to face the existing challenges for thesmooth future.

Especially:The Islamic bank has to focus on the development of new products based onShariah principles that foster market integration and attract investors andentrepreneurs to the risk-return characteristics of the product rather than tothe fact of the product being Islamic or non-Islamic.

CONCLUSION AND RECOMMENDATIONS:

In considering the importance of financial engineering, Islamic financialinstitutions should seriously consider making joint efforts to develop the basicinfrastructure for introducing new products.

In the same way:It is a regulatory challenge for Islamic banking activities to solve these issues integratedand unique Shariah decision can be minimize time, effort, and confusion forinnovation a new product.

In such situations:

Islamic scholars agreed to develop common Shariah standards organizations.

Furthermore:For encouraging more and safe cross border activities, The Islamic banks can beencouraged to provide more profit-sharing finance through reducing of operatingcosts by institutional appropriate arrangements as well as financial engineeringconsistent with the preferences of fund users.

CONCLUSION AND RECOMMENDATIONS:

It is a timely requirement to establish a strong supervisory framework as the extension of the Shariah Council of Islamic banks. It would be provided right observation for all the regulatory obligations with central bank and Islamic bank.

Then it will help to find the safe and smooth way of opportunity for Islamic banking activities from the existing rules and regulations of central bank respectively.

In such situations:All the Islamic banks over the world should maintain common accounting standards which are provided by Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI).

The AAOIFI should also work to find out the way of solution for the conflict between the accounting standard Conventional bank and Islamic bank based on the Shariah principles.

Moreover:It will also be useful to build bridges between existing Islamic banks and those Conventional banks that are interested to do banking on Islamic Principles.

Finally the Islamic banks need to adopt an appropriate risk management system not only for their own portfolio but also for that of their clients.

CONCLUSION AND RECOMMENDATIONS: