redefining competitiveness and growth unlocking … business summit report 2016 redefining...

TRANSCRIPT

European Business Summit Report 2016

Redefining competitiveness and growth

Unlocking the digital potential of industries across Europe

Research carried out by

2 European Business Summit Report 2016

Foreword 04

Introduction 06

| From recovery to opportunity 07Europe still lags behind

The growth opportunity

Competing in a digital economy

| Boosting economic output 15Optimising investments

The value influencers

| Growing industry potential 19

| Unlocking industry growth 23 Generating new value for industry

| Redefining competitiveness 30The fuel for growth

Workforce of the future

Bold moves with digital

| Making Europe ready for business 35Accelerators for growth

Steps to success

The final word

About the research 40

Contents

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 3

4 European Business Summit Report 2016

Foreword

Jo DeblaereChief Operating Officer & Chief Executive–EuropeAccenture

Digital disruption is no longer an event; it is on a fast track to be embedded into every business culture.

Few European companies have avoided the powerful influence of digital technologies. And why would they want to? There are so many benefits from being a digital business: creative ways to incentivise customers, an ability to attract digitally savvy talent with fresh ideas, and the birth of digital ecosystems that enable open innovation. It is a path to progress that I believe can help Europe realise an important new phase of growth and competitiveness.

We address many of these opportunities in the following European Business Summit Report 2016. We explore Europe’s current challenges and illustrate where digital can offer real value—and how to achieve that value—to help Europe rejoin the leaders on the global stage.

European businesses must play their part in optimising the potential of digital technologies. And it helps to know where they stand today. Our research shows not only what digital looks like in their industry now, but also suggests that any industry with the right combination of digital skills, technologies and accelerators can drive greater productivity and growth.

It is time for business and governments in Europe to embrace risk and experimentation. We must be bold. And we must act now.

I would like take this opportunity on behalf of Accenture to thank BUSINESSEUROPE and the EBS for their support and involvement with this vital research. Working together, we aim to show how Europe can prepare for business success—making the most of industry investments and unlocking the digital potential that redefines competitiveness and growth.

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 5

Can Europe be successful without the efforts of industry? Clearly, the answer is no. Due to its beneficial effect on other sectors, industry is often underestimated in terms of its importance to the overall economy, significantly contributing to economic growth, employment and innovation activities.

The context in which industry operates has dramatically changed. Industry and services have become interlinked, modifying traditional value chains. Furthermore, the economy is now on a rapid path to digitalisation, creating another industrial revolution and initiating transformation on an immense scale.

We need to speed up the digitalisation of the European Union economy. If Europe cannot leverage the potential of digital revolution, the EU will not be able to increase its manufacturing base. In particular, medium-sized enterprises need to catch up.

Europe must develop a coherent approach to industrial policy, building on existing strengths like the single market, a skilled workforce or our potential for innovation, while eliminating restrictions, to bring our continent back on track.

The Accenture study for EBS 2016 highlights how unlocking the digital potential of industries across Europe can redefine competitiveness and growth.

Harnessing the digital economy today means examining its potential future growth. Industries that are making the most of digital technologies can drive greater productivity and growth. We believe there is unprecedented potential for Europe. By exploiting digital, we can not only regain competitiveness, but also speed up the journey to economic prosperity.

Emma MarcegagliaPresidentBUSINESSEUROPE

6 European Business Summit Report 2016

Introduction

Despite cautious forecasts, Europe will not be a laggard on the world stage forever. Digital disruption can act as a growth multiplier and is poised to be instrumental in helping Europe regain lost competitiveness. According to our research, the size of Europe’s digital economy is 24.5 percent of European Union GDP, equivalent to €3.6 trillion.1 And by 2020 we estimate there will be 27.3 percent of European Union GDP, which equates to €4.4 trillion.2 A sizable opportunity that could mean Europe is a force to be reckoned with.

So what are the steps to get us there? As part of an ambitious program of research over the past three years, we evaluate the digital profile of today’s economies and look at how Europe can focus investments and initiatives to succeed. We identify three value levers—digital skills, technologies and accelerators—that can make a difference to how European economies enhance their overall productivity and growth. And we show how, with small adjustments, those levers can better exploit digital disruption. We also discuss the changes required for governments and policy makers and offer insights into what actions they need to take to provide high-quality, citizen centric, digital services.

This year’s European Business Summit 2016 intends to share with participants the ways in which Europe can redefine competitiveness and growth. Our report, produced in in collaboration with BUSINESSEUROPE and the European Business Summit (EBS), goes some way toward illustrating the practical steps that can help it do so. I look forward to discussing the ideas further with industry leaders and policy makers alike—and exploring how to unlock their digital potential.

Bruno BerthonManaging Director, Accenture Strategy, Europe and Global Lead, Digital Strategy

While global economies remain cautious, uncertainties in Europe mean it is continuing to lag behind other major economies. To improve the European outlook, leaders and policy makers must seek out new opportunities to enhance productivity, growth and competitiveness.

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 7

From recovery to opportunity

Europe still lags behind

Europe has a number of advanced economies which can compete with the best. Germany and the Netherlands are in the top five most competitive countries globally with Finland, Sweden and the United Kingdom ranked in the top ten.3 This positioning is built on a heritage of world-class science, business, education, entrepreneurship and innovation. Unfortunately, these northern powerhouses are in sharp contrast to some of the other regions of Europe which, when looked at collectively, reflect a much gloomier outlook for overall competitiveness.

Although forecasts show the world economy is expected to grow by 3.1 percent in 2016 and 3.4 percent in 2017, growth outside the European Union (EU) in the last year has been far from buoyant.4 Following the lessening pace of emerging markets, global growth fell to its lowest levels since 2009 (3.2 percent in 2015), with an equally bleak outlook—global gross domestic product (GDP) growth has weakened as major advanced economies also slowed. The potential for even a modest pick-up seems slim.

Since the 1990s, Europe has not kept pace with other leading economies, and its ability to compete has declined.5

Despite EU forecasts for euro area growth of 1.6 percent and EU growth of 1.8 percent in 2016, economic growth in Europe is likely to remain even more tentative. Factors such as poor key trading partners' performance, the pace of structural reforms and monetary policy potentially reaching its limits are adding to Europe’s challenges.

Even cautious optimism may be at risk from uncertainties. Growth could be negatively influenced by vagaries in emerging markets, particularly China, or geopolitical tensions. European growth has been hampered, too, by the shockwaves of fluctuations in oil prices and the ups-and-downs of the financial markets.

Of course, Europe is not one amorphous whole. Distinct countries, often with their own language and economic challenges, mean domestic EU developments present their own risks. For instance, the forthcoming EU referendum in the United Kingdom is raising questions nationally and internationally about the country’s future growth.

8 European Business Summit Report 2016

On a more positive note, the impact from structural reforms in Europe could turn out to be stronger than expected and the transfer of benefits from current monetary policy into the real economy have the potential to be larger than anticipated. So are there ways in which Europe can regain some of the ground lost to its global competitors?

"The economic recovery in Europe continues but the global context is less conducive than it was. Future growth will increasingly depend on the opportunities we create for ourselves.”6

Valdis Dombrovskis, Vice-President for the Euro and Social Dialogue.

Figure 1. Compound Annual Growth Rate (CAGR) Forecast 2015 to 2020

Italy

4.0%

3.5%

3.0%

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

FinlandGermany

BelgiumFrance

AustriaNetherlands

SwedenSpain

UnitedKingdom

Global average 3.0%

United States 2.6%

EU average 1.8%

As Figure 1 shows, the Compound Annual Growth Rate (CAGR) for Europe is only just over one-half of the global rate, and one-third that of emerging markets, China and India—a situation that has serious implications for European competitiveness. Going forward, industries and economies in Europe must focus their investments on high-level growth opportunities to improve productivity and reinvigorate their competitive position.

Source: Oxford Economics

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 9

The growth opportunity

Forecasts aside, there are opportunities for European economies to accelerate growth, boost output and better compete, at both industry and national levels. A first step is to evaluate the current profile of each economy by comparing traditional elements with the impact of the digital economy (see sidebar below). Addressing the digital economy requires a new approach that goes beyond the limitations of standard measures and methods.

What is the digital economy?The digital economy is the share of total economic output derived from a number of broad “digital” inputs. These digital inputs include digital skills, digital equipment (hardware, software and communications equipment) and the intermediate digital goods and services used in production. Such broad measures reflect the foundations of the digital economy.7

Traditional measures of the digital economy have focused largely on technology infrastructure, IT and communications sector investment, eCommerce, and broadband penetration rates. Using this approach has derived relatively small estimates of digital output in the economy of around 5.2 percent for mature market economies. But this fails to account for the whole scope of digital.

Using a ground-breaking model that assesses how digital is adding value throughout the entire economy—by tracing the use of digital skills, equipment and intermediate goods and services in the production of all goods and services—we can derive a more comprehensive and rounded view of what constitutes a digital economy (see About the research, page 40).

10 European Business Summit Report 2016

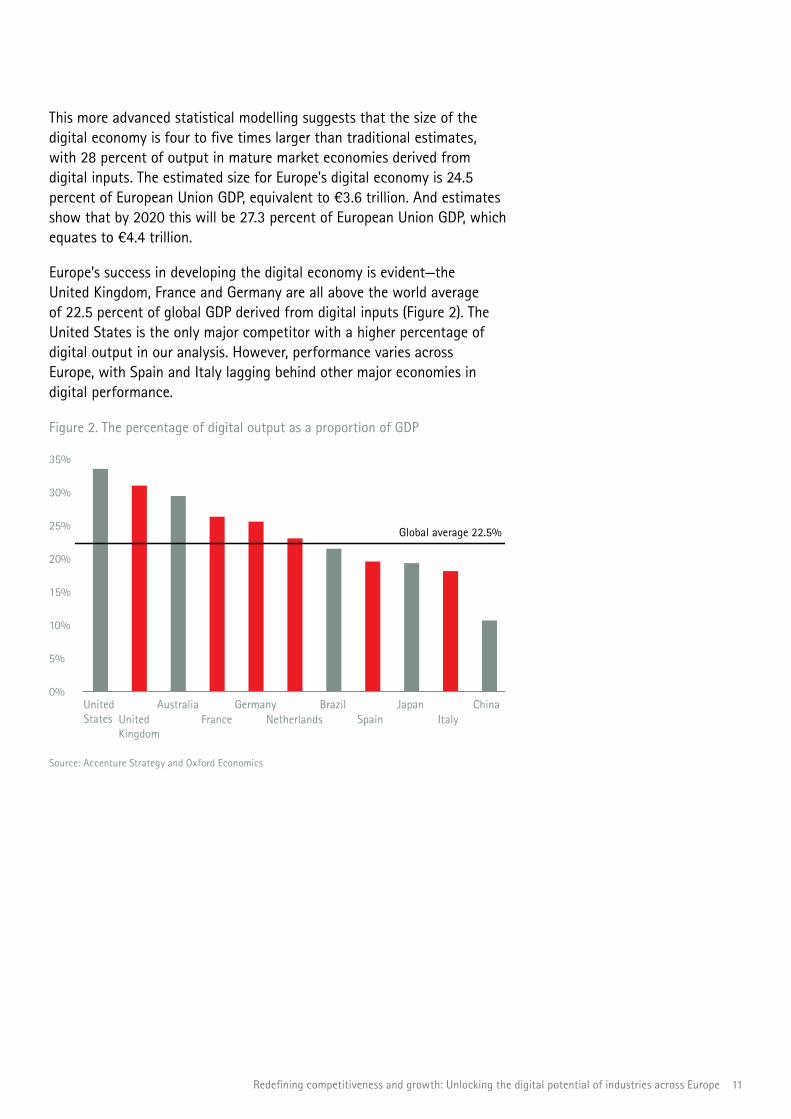

This more advanced statistical modelling suggests that the size of the digital economy is four to five times larger than traditional estimates, with 28 percent of output in mature market economies derived from digital inputs. The estimated size for Europe's digital economy is 24.5 percent of European Union GDP, equivalent to €3.6 trillion. And estimates show that by 2020 this will be 27.3 percent of European Union GDP, which equates to €4.4 trillion.

Europe’s success in developing the digital economy is evident—the United Kingdom, France and Germany are all above the world average of 22.5 percent of global GDP derived from digital inputs (Figure 2). The United States is the only major competitor with a higher percentage of digital output in our analysis. However, performance varies across Europe, with Spain and Italy lagging behind other major economies in digital performance.

Figure 2. The percentage of digital output as a proportion of GDP

United States

35%

30%

25%

20%

15%

10%

5%

0%Australia

FranceGermany

NetherlandsBrazil

SpainJapan

ItalyChina

Global average 22.5%

UnitedKingdom

Source: Accenture Strategy and Oxford Economics

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 11

Competing in a digital economy

As we can see from the model’s findings, the digital economy is important both for individual countries, and Europe as a whole. But the impact is even greater when we consider the growth rates of the digital economy over the next five years compared with the rest of the economy. The growth in digital output from 2015 to 2020 is forecast to be 2.7 times to 8.5 times the growth expected from the rest of the economies’ output for the European countries illustrated (Figure 3).

Figure 3. Percentage increase in output of digital economy, 2015 to 2020

In our analysis, the growth rates for European countries compare favourably with all major economies globally, with the exception of China which is growing from a smaller base (only 10.5 percent of output in China is currently related to digital inputs). Italy, with only 18.1 percent of current output related to digital, shows the greatest potential for growth, with the digital economy forecasted to grow at 8.5 times the rest of the economy. Germany, with 25.1 percent of its economy related to digital, also shows a large potential growth spurt, with the digital economy forecasted to grow at eight times the rest of the economy. Even in the United Kingdom, with the largest domestic share of the digital economy at 30.7 percent, digital output shows accelerated growth of 2.7 times the rest of the economy.

Economies, whether in Europe or beyond, can gain from the digital economy—even without any additional measures in place. But our analysis reveals that there are even greater levels of growth to be found by optimising the digital conditions within each economy.

12 European Business Summit Report 2016

United States

60%

50%

40%

30%

20%

10%

0%AustraliaFrance

Germany Netherlands BrazilSpain

JapanItaly China

UnitedKingdom

Percentage increase in output of digital economyPercentage increase in output of non-digital economy

Source: Accenture Strategy and Oxford Economics

“One of the keys to effectively capitalizing on the potential of digital technologies to accelerate competitiveness and growth in the EU is to understand current performance and the opportunity for improvement from a business, industry and policy-making perspective.”

European Business Summit report, Accelerating Europe’s comeback: Digital opportunities for competitiveness and growth, 2014.8

What are the underlying factors that can drive greater economic growth in the digital economy? In 2014, our European Business Summit report highlighted the need to measure the progress and impact of digital adoption in Europe. Accenture developed the Digital Economic Opportunity Index to capture the extent to which digital technologies have penetrated economic activity in a country or industry. Assessing whether an economy is digital goes beyond utilising digital technologies and processes, to understanding the degree to which “digital” is enabled in the surrounding business, institutional and economic environment.

In this way, the Digital Economic Opportunity Index is an interactive tool that enables us to explore the digital profile of an economy. The tool can be used to identify which economies are at the digital frontier and which have most room for digital progress. The industry level scorecard is focused on eleven industry groupings across the EU (see About the research, page 40).

Part of the Digital Economic Opportunity Index model included the identification of three value levers—digital skills, technologies and accelerators—that can make a difference to how European economies enhance their productivity and growth.

• Digital skills: the digital nature of occupations and the skills and knowledge required of people to perform their jobs.

• Digital technologies: the productive assets related to digital technologies (hardware, software and communications equipment).

• Digital accelerators: the environmental, cultural and behavioural aspects of digital components of the economy that support digital entrepreneurship or activities.

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 13

Figure 4. Country ranking 2014 to 2016

Our analysis reveals some interesting developments over the three years we have been tracking performance. For example, the United Kingdom is ranked top of the countries in our analysis but its skills score has dropped 10 percent since 2014, meaning it will lose its lead eventually if this continues. Italy may rank bottom of the list but it is the fastest digitiser due to rapid improvements in digital skills and in accelerators. France is another country, like Italy, to experience a rapid growth in their accelerator score—a direct result of measurable improvements in the government's prioritisation of digital.

Europe has an opportunity to focus investment and other initiatives to not only regain some of the ground lost to competitors in recent years but, more importantly, to take advantage of the opportunity to take the lead in the digital economy.

5 10 15 20 25 30 35 50

Digital Economic Opportunity scores 2014, 2015 and 2016

0

Percentage improvements in DEO score 2014 to 2016

UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

40 45

2016 2015 2014

-5% 5% 10% 15% 20%0%

Source: Accenture Strategy and Oxford Economics

14 European Business Summit Report 2016

As with any strategic decision making, harnessing the digital economy means understanding today’s position in the context of potential future growth. Economies, industries and governments must create the right environment to drive success.

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 15

Boosting economic output

Assessing the digital economy offers insight into its size and scope. But while it is vitally important to the overall well-being of European economies to calculate how much has been spent on information, communications and technology or account for the number of digital jobs, there is more to achieving a high-performing economy than accumulating digital assets and skills.

Even when organisations understand the size of their digital economy and the opportunities from their digital efforts, they often lack the ability to influence or change their digital outcomes on the global stage. As our Digital Economic Opportunity Index has shown, being digital is not just a question of size—it is the degree to which digital practices and capabilities are embedded into the fabric of European economies. In short, digital can act as a growth multiplier for economies.

Optimising investments

Looking at the global study of national Digital Economic Opportunity Index scores, there is a clear link between the three value levers—digital skills, digital technologies and digital accelerators—and total factor productivity. Allocating each economy a hypothetical “budget” of 10-points to invest in improvements to economies’ digital capabilities, one point at a time, we modelled the optimal combination to make the greatest 10-point impact. In this way, each country can find new and untapped value that goes beyond the gains from maintaining “business as usual” (Figure 6).

Figure 5. Three levers to optimise a 10-point Digital Economic Opportunity improvement per country

Country Skills Technologies Accelerators

France 3 6 1

Germany 5 4 1

Italy 0 6 4

Netherlands 5 4 1

Spain 2 3 5

United Kingdom 1 5 4

Australia 3 3 4

Brazil 0 7 3

China 4 4 2

Japan 6 0 4

United States 4 1 5

16 European Business Summit Report 2016

By finding the optimum combination of these specific levers, high-performing economies can realise a dramatic improvement in their country’s gross domestic product growth rates. For example, in our national level Digital Economic Opportunity Index, the United Kingdom had relatively high scores in the digital technologies and digital accelerators levers, but a particularly strong score in digital skills. Using its 10-point increase to allocate five points to technology, one point to digital skills and four points to digital accelerators, it has the potential to gain the equivalent of €77 billion (US$84 billion) by 2020.

It is important to note that the categories marked zero (Figure 5) indicate where countries need to maintain their current levels of activity, rather than take no action. For example, we found Italy needed to make additional effort in its digital technologies to improve it by 6 points, maintain current activities with digital skills and improve its digital accelerators by four points. In other words, the country should have invested 60 percent of its efforts in a smarter use of digital technologies and 40 percent in digital accelerators to realise the maximum gains.

By focusing on the optimised potential for the unique country profiles, GDP growth in 2020 can be enhanced by between 1.6 percent and 4.2 percent across the European countries studied. This equates to an uplift in 2020 GDP of €356 billion across the six EU economies from our analysis.

Figure 6. The gross domestic product impact from Digital Economic Opportunity optimisation

Country Change in 2020 gross domestic product (Euros billion, 2015 prices)

Change in 2020 gross domestic product (%)

France 73.0 3.1%

Germany 81.4 2.5%

Italy 73.2 4.2%

Netherlands 12.1 1.6%

Spain 39.4 3.2%

United Kingdom 76.5 2.5%

Australia 30.9 2.4%

Brazil 109.3 6.6%

China 478.8 3.7%

Japan 132.7 3.3%

United States 382.5 2.1%

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 17

The value influencers

To optimise their digital opportunity, European countries need to be aware of two key influencers of undiscovered value.

The impact of digital accelerators on total factor productivity: Even though each of the three digital levers can positively impact productivity growth in their own right, we found that the interaction of digital accelerators and digital skills and technology levers has an additional effect. When the digital accelerator score is higher, the impact of any given change in skills or technology is higher, too. Whereas some countries are merely maintaining their digital skills and technologies, all countries in our sample rely on at least some investment in the area of digital accelerators to find their optimal combination of levers—with Spain among those standing to gain the most from investing in digital accelerators by 2020.

The importance of digital “catch up”: We found that there was an extra productivity boost for those countries that rank lowest on the economic opportunity scale, enabling them to “catch up” with the leaders. A one-point increase in any of the three levers delivered a greater increase in gross domestic product growth for the country ranked lowest, than that same one-point impact for a country at the top of the table. Take France, where a one-point movement on the digital technologies lever would be associated with a 0.09 percentage point boost to annual gross domestic product growth, compared to a 0.05 percentage point boost in the higher-ranking Australia.

The implications for economies are compelling, but to make a difference a further layer of granularity needs to be considered. Individual industries are subject to the same variations in digital intensity as the countries to which they belong. Let us examine the industry picture in more detail and better understand what actions can be taken to enhance their economies’ growth and competitiveness.

18 European Business Summit Report 2016

The search for economic growth potential in each economy would not be complete without a reconciliation of the underlying dynamics of individual industries’ activities. Our research includes a series of industry analyses to better understand this relationship and how greater productivity gains are within their grasp.

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 19

Growing industry potential

By tracing the use of digital skills, equipment and intermediate goods and services in the production of all goods and services, we can derive a more comprehensive and rounded view of industries’ contribution to economic growth. Our advanced statistical modelling suggests the scales of industry output related to digital from the sectors in our analysis is four to five times larger than traditional estimates, ranging from 52 percent in Insurance to 15 percent in Chemicals and Refined Petroleum (Figure 7).

Figure 7. Percentage of industry gross value add (GVA) related to digital output

50%

40%

30%

20%

10%

0%

Automotive, industrial, infrastructure and travel

Businessservices

Insurance Electronics and high tech

Retail Utilities

Naturalresources

CommunicationsBanking

Chemicals and refined petroleum

Consumer goods and services

60%% of GVA

% growth

40%

20%

10%

0%

Automotive, industrial, infrastructure and travel

Businessservices

Insurance Electronics and high tech

Retail Utilities

Naturalresources

Communications

Growth in Digital GVA

30%

Banking

Growth in non-digital GVA

Chemicals and refined petroleum

Consumer goods and services

-5%

5%

35%

15%

25%

Source: Accenture Strategy and Oxford Economics

Source: Accenture Strategy and Oxford Economics

Figure 8. Percentage increase in gross value add (GVA) related to digital output 2015 to 2020

20 European Business Summit Report 2016

In our analysis, the growth rates in gross value add (GVA) for European industries illustrate the future potential to boost growth in EU economies. Natural resources, although growing from one of the smallest bases of digital output (15.3 percent), shows the greatest potential for growth with the digital share of GVA forecasted to grow at 7.4 times the non-digital output. The Automotive, Industrial, Infrastructure and Travel sector, with 19.3 percent of its output related to digital, also shows a large potential growth spurt, with the digital component of GVA forecasted to grow at 7.2 times the non-digital output. Even the Communications sector, with a large proportion of digital output (41.0 percent), shows accelerated growth of 3.2 times the growth of non-digital output.

To further understand the dynamics of industry growth, we constructed a composite index, based on the three value levers, to look at a broad spectrum of characteristics, including the intangible qualities that have been shown to translate investments in digital into productivity gains. We measured the readiness of the marketplace, the agility of the organisational structure, the sophistication of production processes, the flexibility and quality of the factors of production and the institutional environment in which a firm operates—factors that determine the effectiveness of digital investments.

The aggregate Digital Economic Opportunity industry analysis scores for the EU are shown in Figure 9. The Insurance, Banking and Communications sectors have a clear lead over the rest, with Electronics and High Tech and Business Services further behind.

Figure 9. Industry Digital Economic Opportunity scores (0-100), 2014 to 2016

50

40

20

10

0

Automotive, industrial, infrastructure and travel

Businessservices

Insurance

Electronics and high tech

Retail

Utilities

Naturalresources

Communications

2016

30

Banking

2015 2014

Chemicals and refined petroleum

Consumer goods and services

Source: Accenture Strategy and Oxford Economics

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 21

Figure 10. Percentage improvements in Digital Economic Opportunity scores (percent change), 2014 to 2016

Chemicalsand refined petroleum

10%

8%

6%

4%

2%

0%

Consumer goods and services

Electronics and high tech

Banking

Business services

Utilities

Automotive, industrial, infrastructure and travel

Communications Naturalresources

Insurance Retail

Our three-year timeline shows us that certain industries have a way to go to keep pace with the industry leaders. But they should take heart: by taking a closer look at the skills, technologies and accelerators that affect their digital output, they can address areas of weakness and more closely align with their more successful peers.

Source: Accenture Strategy and Oxford Economics

22 European Business Summit Report 2016

Some industries are more attuned than others to making the most of digital technologies. But the fact remains that any industry, with the right combination of skills, technologies and accelerators, can drive greater productivity and growth.

Unlocking industry growth

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 23

Productivity is critical to economic growth. Economists agree that in the long run, it is the principal source of improvements to living standards. In the short and medium term too, productivity enhancements can engineer significant improvements in economic performance.

Productivity growth can be defined as expanding output for a fixed level of input. This is most commonly achieved with advancements in technology or technique and it is within this space that digital innovations have the most impact on economic performance.

The Digital Economic Opportunity Index measures the “digitalness” of an industry, as captured by the three levers previously referenced: digital skills, digital technologies and digital accelerators. The skills and technologies scores are driven from the bottom up, capturing the behaviours demonstrated by companies. The accelerators scores are broadly determined from the top down, capturing the enabling environment in which the industry operates. The digitalness within each is represented by four key aspects, which are measured using a series of indicators from primary and secondary data sources, and incorporates Accenture insights.

Using the Digital Economic Opportunity Index we are able to analyse the rate of digitisation of Europe’s industries, identify the industry leaders and draw lessons from their approach that may be applied to other organisations within that sector. There are also cross-industry lessons to be learned by analysing those industries in certain European economies that are choosing the right combination of skills, technologies and accelerators to deliver greater value.

High scores in the Digital Economic Opportunity Index mean that countries or industries have, for example, a strong emphasis on digital skills development, committed investments in digital enablers such as the Internet of Things, or a positive attitude toward digital in their governments.

Generating new value for industry

Taking a sector snapshot across Europe, we can see which regions are behaving more digitally than others. For example, in the retail sector, Sweden stands out as making the most of digital, whereas Spain, Austria, Italy could benefit from making further adjustments.

24 European Business Summit Report 2016

The path to productivityDigital technology has effectively established itself as a general purpose technology, like electrification or steam power before it.

But this process has not unravelled uniformly across all sectors and regions of the world economy. The impact of digital innovations on productivity depends on the degree to which purchases of new equipment are complemented by a host of other, often intangible factors. These are factors that enable firms to make productive use of digital innovations and their quality differs wildly across industries and geographical regions.

The extensive literature on the disparity between the United States and EU productivity levels identifies a range of characteristics that set the United States apart as a global leader in digital innovation and the application of that innovation to the wider economy. Variables are as diverse as the strength of competition, the regulatory environment, access to risk capital, the quality of the labour force and managerial structures. There is general consensus in wider literature, too, that for digital innovations to effectively translate into wider productivity gains, they must be accompanied by other supporting features.9 This has been the underlying principle adopted in the Accenture Strategy Digital Economic Opportunity Index.

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 25

The Digital Economic Opportunity Index also offers useful insights around which sectors are more digitally competitive than others in certain countries. For instance, France is lagging behind in Business Services but has the third highest score in the Electronics and High Tech sector.

As the following charts show, the United Kingdom is in the lead for digital capabilities across Europe, with the Netherlands following closely behind. Both countries are characterised by strong digital accelerators scores, which should be considered a foundation for all industries. In addition, both countries excel consistently across all three digital levers.

26 European Business Summit Report 2016

10 20 30 40 50 60 70 80

Digital Economic Opportunity scores by country

0 20% 40% 60% 80% 100%

Digital value levers: proportion of digital output related to skills, technology and accelerators

0%UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

Digital Skills Digital Technology Digital Accelerators

Automotive, industrial, infrastructure and travel

Source: Accenture Strategy and Oxford Economics

Digital Economic Opportunity scores by country

20% 40% 60% 80% 100%

Digital value levers: proportion of digital output related to skills, technology and accelerators

0%UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

Digital Skills Digital Technology Digital Accelerators

10 20 30 40 50 60 70 800

Banking

Source: Accenture Strategy and Oxford Economics

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 27

10 20 30 40 50 60 70 80

Digital Economic Opportunity scores by country

0 20% 40% 60% 80% 100%

Digital value levers: proportion of digital output related to skills, technology and accelerators

0%UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

Digital Skills Digital Technology Digital Accelerators

Business Services

Source: Accenture Strategy and Oxford Economics

Digital Economic Opportunity scores by country

20% 40% 60% 80% 100%

Digital value levers: proportion of digital output related to skills, technology and accelerators

0%UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

Digital Skills Digital Technology Digital Accelerators

10 20 30 40 50 60 70 800

Chemicals and Refined Petroleum

Source: Accenture Strategy and Oxford Economics

10 20 30 40 50 60 70 80

Digital Economic Opportunity scores by country

0 20% 40% 60% 80% 100%

Digital value levers: proportion of digital output related to skills, technology and accelerators

0%UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

Digital Skills Digital Technology Digital Accelerators

Communications

Source: Accenture Strategy and Oxford Economics

Digital Economic Opportunity scores by country

20% 40% 60% 80% 100%

Digital value levers: proportion of digital output related to skills, technology and accelerators

0%UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

Digital Skills Digital Technology Digital Accelerators

10 20 30 40 50 60 70 800

Consumer goods and services

Source: Accenture Strategy and Oxford Economics

Digital Economic Opportunity scores by country

20% 40% 60% 80% 100%

Digital value levers: proportion of digital output related to skills, technology and accelerators

0%UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

Digital Skills Digital Technology Digital Accelerators

10 20 30 40 50 60 70 800

Electronics and High Tech

Source: Accenture Strategy and Oxford Economics

Digital Economic Opportunity scores by country

20% 40% 60% 80% 100%

Digital value levers: proportion of digital output related to skills, technology and accelerators

0%UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

Digital Skills Digital Technology Digital Accelerators

10 20 30 40 50 60 70 800

Insurance

Source: Accenture Strategy and Oxford Economics

28 European Business Summit Report 2016

Digital Economic Opportunity scores by country

20% 40% 60% 80% 100%

Digital value levers: proportion of digital output related to skills, technology and accelerators

0%UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

Digital Skills Digital Technology Digital Accelerators

10 20 30 40 50 60 70 800

Natural Resources

Source: Accenture Strategy and Oxford Economics

10 20 30 40 50 60 70 80

Digital Economic Opportunity scores by country

0 20% 40% 60% 80% 100%

Digital value levers: proportion of digital output related to skills, technology and accelerators

0%UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

Digital Skills Digital Technology Digital Accelerators

Retail

Source: Accenture Strategy and Oxford Economics

Digital Economic Opportunity scores by country

20% 40% 60% 80% 100%

Digital value levers: proportion of digital output related to skills, technology and accelerators

0%UnitedKingdom

Netherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

UnitedKingdomNetherlands

France

Sweden

Germany

Belgium

Austria

Spain

Italy

Digital Skills Digital Technology Digital Accelerators

10 20 30 40 50 60 70 800

Utilities

Source: Accenture Strategy and Oxford Economics

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 29

The rules of competitiveness are changing and European businesses must proactively accelerate their efforts to keep pace with the unprecedented demands for speed, scale and flexibility in today’s global marketplace.

Redefining competitiveness

30 European Business Summit Report 2016

To drive competitiveness and grow profitably, winning company cultures will adopt a strategic approach around investing funds from cost reduction initiatives, build a more flexible operating model and be prepared for the future of work. What is more, European businesses and governments need to consider the bold moves they can take to make the most of a digital world.

The fuel for growth

Cost reduction is key to unlocking funds that can be reinvested in growth. But without a cohesive, strategic plan—and the right people to support the plan—those efforts will fail. To better connect cost reduction efforts with their growth strategy, European business leaders must first understand where growth is coming from and where they are going to place their bets in the future. Then, they need to understand which activities, processes and spends create value for the business—and which do not. Identifying non-working spend is critical to create a cost reduction program that will free up large amounts of cash, assets and capital that can be reinvested to meet the needs of the growth strategy. Connecting cost reduction and growth strategies—in line with the business strategy—makes cost savings sustainable.

Second, a rigid operating model and a lack of clear visibility into what creates value for an organisation will dilute growth efforts.10 Only one in four companies have a flexible operating model that can adapt to consistently deliver on strategy and execute activities that drive value for the organisation. European business leaders must ensure that their operating models align with how their business wants to profitably grow—and ensure that the C-suite is aligned with that strategy.

Finally, digital business models and strategies help increase organisational agility, flexibility and sustainable growth. European businesses that commit to building digital capabilities and digitising traditional processes will be better positioned to manage disruption, grow sustainably and create competitive advantage. And by taking advantage of digital to cost-effectively experiment at speed and scale, businesses can solve customers' problems and bring new products to market faster.

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 31

Workforce of the future

While understanding changing customer needs and behaviours is hugely important, the deciding factor in the digital era will be an ability to evolve a new, digital corporate culture. European businesses must focus on people first—consumers, employees and ecosystem partners—and enable them to do more with technology so that they can continuously adapt, learn, create new solutions, drive relentless change, and disrupt the status quo.

In the early days of digital, technological advances were associated primarily with efficiency. Removing human intervention and replacing it with automation to change the how work is performed. Now, with advances in collaboration and social media, digital is transforming working practices; democratising how work is conducted is reinventing how organisations are run. Workplaces will rely on skills that are more tailored to individual strengths, more flexible and portable, more collaborative and more meaningful for employees throughout the organisation.

Humanising the workforce through digital takes a conscious effort. Intelligent machines—information systems that sense, comprehend, act and learn—inform better, faster decisions. They enable managers to shift their focus to activities that call for decidedly human traits such as complex thinking and higher-order reasoning. Providing guidance and recommendations, machines complement managers' expertise, experience and ethics, as well as their ability to experiment and innovate. In all these ways, intelligent machines open the door to “judgment work,” which values intuition as much as, if not more than, know-how.

To take full advantage of what the cognitive computing revolution has to offer, European business leaders must ensure that their organisations have the capacity to change. By creating a culture of experimentation and trust among leaders at all levels, organisations can unlock the potential of the workforce of the future.

32 European Business Summit Report 2016

Bold moves with digital

With start-ups relentlessly pursuing market share, traditional European business leaders need to fight back through the power of reinvention. Yet, many are slow to do so. Our research showed that 43 percent of European business leaders preferred to be a “fast follower” when it comes to implementing a digital business strategy, with 18 percent comfortable with taking a “wait and see” approach. Only 19 percent of European business leaders described their organisation as being a “digital business.”11

Many European business leaders are stuck in a state of “disruption paralysis.” When fed a constant diet of disruption, where risk and change are presented as the only feasible strategic options, many leaders and their Board of directors become paralysed by the options available and struggle to identify, agree on, and navigate the best path forward. European organisations need to fundamentally challenge their existing definition of digital, and embed it into every element of their mind-set, culture and operations.

European business leaders must look beyond the traditional realms of their own business model or market confines to identify new areas of growth and have the confidence to open up their business and do things differently. The creation of new business structures and services, the rise of partnerships with digital start-ups, creative ways of incentivising customers, new approaches to attracting digitally savvy talent, and the development of digital ecosystems for open innovation can all help organisations become inherently digital.

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 33

34 European Business Summit Report 2016

Governments and policy makers have a key role to play in a digitally enabled future. Working with European businesses, they need to create the right environment to help optimise investment and maximise the potential for growth.

Making Europe ready for business

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 35

36 European Business Summit Report 2016

Accelerators for growth

Our analysis has shown a wide variation across European economies in their ability to nurture growth from the digital economy. Leading digital economies have the right fundamentals, with conditions in place that generally make it easier to do business. These conditions include policies that minimise red tape, enable access to finance, provide tax incentives for entrepreneurs and innovators and encourage business and education partnerships to develop a skilled workforce.12 To maximise the potential for growth in a digitally enabled future, governments need to build on these fundamentals by first, putting in place a regulatory environment that supports investment in digital infrastructure, technology and new digitally enabled business models and services; second, making strategic investments, including in skills, that leverage national economic strengths and the industrial base—for example, manufacturing, services, technology sectors—and finally, embracing digital disruption in how they themselves work, provide services and interact with citizens.

Establish a regulatory environment that supports investment in a digitally enabled future

In Europe, the consistent implementation of EU rules by member states is vital for a fully functioning Digital Single Market that can provide the scale to incentivise private sector investment in digital infrastructure, forming the backbone of the digital economy and enabling business and consumers to fully benefit from digital technologies and services at a lower cost.

Traditional approaches to regulation are being challenged, as technology and new digitally enabled business models outpace the regulatory response. A strategic approach to future regulation is required to enable experimentation with new technologies and the development of new business models. In this way, the risk of investment is reduced, for the benefit of traditional companies, in addition to digital innovators, entrepreneurs and consumers who seek to participate in the sharing economy.

As traditional business models are disrupted and greater collaboration across industries and borders takes place, careful review of the existing regulatory framework, or consideration of how industry standards can effectively address consumer and market issues, needs to be undertaken before new regulation is introduced.

In addition, there needs to be recognition of the fact that the digital economy is global, and the interoperability of standards and mutual recognition of other countries’ regulatory frameworks, to better serve companies and consumers, must be considered.

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 37

To this end governments, policy makers and regulators must encourage the free and secure flow of data in Europe and globally, while maintaining an adequate level of protection for personal data. Unnecessary restrictions, including data localisation requirements, drive up costs and limit consumer choice.

Invest in skills and initiatives to take advantage of national strengths

With increasing competition for people with digital skills, not only from technology companies but across all industries, governments need to work with businesses and educators to invest in and attract the right talent. Developing the digital economy relies on increasing the volume of digitally equipped graduates. Investments must be made in the development of these skills from primary school through the education cycle, including adding computer science to the curriculum from the earliest stage possible, adequately training teachers and educating parents about careers in a digitally enabled economy. The existing workforce needs to be upskilled through targeted, relevant technical and vocational training in digital skills, in partnership with business. Policies will be necessary to enhance the mobility of qualified talent within, and into, the EU—which is part of the solution.

To maximise the potential for growth, governments need to consider how they can support digital innovation and experimentation by drawing on national economic and industry strengths. Governments can consider funding innovation programmes and pilots that support cross-industry collaboration and experimentation with new technologies; for example, test beds for new technologies and innovation hubs that bring together traditional industries with digital disruptors, multinationals and start-ups, universities, educational and research institutes to develop, test and bring to market new technology solutions and business models.

Embrace digital disruption

Digital disruption is changing the way governments themselves work and interact with citizens, offering an opportunity to improve the quality and delivery of public services. The public sector represents, on average, one-half of GDP across EU economies, meaning governments and policy makers have a significant role to play in creating the conditions for improved competitiveness and growth in Europe.

38 European Business Summit Report 2016

Governments can contribute by nurturing a digital mind-set through investment in digital and entrepreneurial skills for public servants, the creation of pilot programmes to support digital innovation and leveraging best practices across public sector agencies. Government also has a role as a partner, enabler and facilitator rather than purely a public-service provider. Indeed, the greater opportunity is for government to become an open platform, enabling people inside and outside government to collaborate and innovate in the provision of high quality, citizen-centric, digital services.

Steps to success

Actions governments can take today13:

• Strategic actions: Strategic actions need to be implemented at various governmental levels—from the EU to individual municipalities—to govern for success. Build public trust and create a system of transparency, public participation and collaboration, showcase best practice and launch impactful exemplary projects. Reengineer internal administrative processes and apply capabilities across organisational silos. Prepare the digitally-savvy public service workforce for an empowered and inclusive society.

• Regulatory actions: Policy-makers need to put in place an enabling regulatory framework that contributes to the extensive roll out of digital public services and connects public administrations across Europe. Develop a regulatory framework for reliable electronic identification (eID), a critical pre-condition for effective digital government. Put in place a framework that supports pan-European cloud computing solutions for government and big data analytics.

• Technical actions: Open, platform-based thinking about the public sector provides a powerful means to underpin the technological aspects of modern, digital public services. Develop common standards for Government platforms. Explore the potential of blockchain and other groundbreaking peer-to-peer technologies.

In a shift to government-as-a-platform, government will be more a broker or facilitator to other sectors and stakeholders and become far more embedded in the community it serves.

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 39

Actions businesses can take today:

• Organise for growth: Identify activities that realise value, eliminate non-value adding costs and reinvest savings into growth initiatives that improve competitiveness. The journey to growth must be mapped out to prioritise the scope of the effort and split it into manageable phases.

• Experiment and be creative: Explore and introduce new ideas. The process of pushing the company forward is as equally disruptive as the ideas themselves. Be comfortable with trial and error—some initiatives will work, others will not—digital success requires a degree of failure so see it as a “test-bed.”

• Establish digital partnerships: Join forces, particularly with digital start-ups, to draw on each other’s expertise to create innovative or complementary products and services, and extend these offerings to reach broader audiences and markets. Such partnerships enable businesses to orient themselves around the customer and deliver new experiences and value.

• Cultivate the workforce of the future: Introduce fresh perspectives. Individuals from outside the business or industry come unencumbered by traditional legacy thinking. Implementing initiatives to share and crowdsource ideas can spark new energy and thinking.

• Nurture a digital mind-set: Digital culture starts at the top. To achieve digital transformation on the inside—operations, culture, practices, and workforce—as well as on the outside—company image and employee appeal—execution relies on the clear commitment and direction of leadership.

The final word

According to Valdis Dombrovskis, Vice-President for the Euro and Social Dialogue: "The economic recovery in Europe continues but the global context is less conducive than it was. Future growth will increasingly depend on the opportunities we create for ourselves.”14

As we enter an era of “living services”, driven by automation and even more digital presence in our everyday lives, Europe has an opportunity to seize competitiveness and grow. For businesses and for governments, a world that is personalised, data and insight-driven, and context-aware requires a new kind of collaboration and understanding. Founded on a strong combination of digital skills, technologies and accelerators, Europe can fulfil its powerhouse potential.

Today, operating a digital strategy is no longer enough. European businesses need a series of strategies to flex and grow in a digital era.

The Accenture Strategy Digital Economic Value Index uses an entirely new approach to traditional examination of the digital economy. Our basic premise is that the value of digital technologies is not confined to any particular sectors, but pervades the entire economy. Our model recognises digital goods and services add value not just at the point of production, but all the way through the supply chain. For the first time, we have developed an internationally comparable, replicable and scalable framework to measure this economic snapshot.

In assessing the impact of the digital levers, we cross-referenced previous analysis on economic opportunity. The earlier study, launched in October 2015, estimated the effect of changes in total factor productivity on gross domestic product. Working with Oxford Economics, we used internationally comparable observations across a large pool of measures of digital technology and related indicators from public and private sources.

We constructed the Accenture Strategy Digital Economic Opportunity Index for 33 major economies and undertook multivariate regression analysis to estimate equations that explain variation in countries total factor productivity by references to their Digital Economic Opportunity scores.

We found a 10-point boost in economic opportunity is associated with an approximately 0.4 percentage point increase in total factor productivity for advanced economies, and a 0.65 percentage point increase in total factor productivity for high-growth emerging markets. Now, in calculating the optimum value of economic opportunity, we effectively allocate each economy a hypothetical “budget” of 10-points to invest in improvements to their digital capabilities. By thoroughly testing where the points are best allocated, one point at a time, our model is able to evaluate which combination of the three levers has the greatest impact.

It is important to note that the optimal combination is a purely statistical result, based on available data. It does not incorporate qualitative judgment, which could influence the outcome.

40 European Business Summit Report 2016

About the research

Industry alignment

Digital Economic Opportunity Industry

IO Sectors

Automotive, industrial, infrastructure and travel (AIIT)

Air Transport

Construction

Inland Transport

Machinery, Nec

Other Supporting and Auxiliary Transport Activities; Activities of Travel Agencies

Sale, Maintenance and Repair of Motor Vehicles and Motorcycles; Retail Sale of Fuel

Transport Equipment

Water Transport

Banking Banking

Business Services Renting of M&Eq and Other Business Activities

Chemicals & Refined Petroleum

Chemicals and Chemical Products

Coke, Refined Petroleum and Nuclear Fuel

Rubber and Plastics

Communications Post and Telecommunications

Consumer Goods and Services

Education

Food, Beverages and Tobacco

Hotels and Restaurants

Leather, Leather and Footwear

Manufacturing, Nec; Recycling

Other Community, Social and Personal Services

Textiles and Textile Products

Electronics and High-tech Electrical and Optical Equipment

Government Public Admin and Defense; Compulsory Social Security

Health Health and Social Work

Insurance Insurance

Natural Resources Agriculture, Hunting, Forestry and Fishing

Basic Metals and Fabricated Metal

Mining and Quarrying

Other Non-Metallic Mineral

Pulp, Paper, Paper , Printing and Publishing

Wood and Products of Wood and Cork

Real Estate Real Estate Activities

Retail Retail Trade, Except of Motor Vehicles and Motorcycles; Repair of Household Goods

Wholesale Trade and Commission Trade, Except of Motor Vehicles and Motorcycles

Utilities Electricity, Gas and Water Supply

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 41

42 European Business Summit Report 2016

1 Oxford Economics, 2015 EU GDP, Nominal Euro Bns

2 Oxford Economics, Euro, 2015 prices

3 The Global Competitiveness Report 2015-2016, World Economic Forum, http://reports.weforum.org/global-competitiveness-report-2015-2016/

4 European Commission - Spring 2016 Economic Forecast: Staying the course amid high risks, http://ec.europa.eu/economy_finance/eu/forecasts/2016_spring_forecast_en.htm

5 Restoring EU competitiveness (2016 updated version), European Investment Bank, January 2016, http://www.eib.org/attachments/efs/restoring_eu_competitiveness_en.pdf

6 European Commission - Press release, Spring 2016 Economic Forecast: Staying the course amid high risks, Brussels, 3 May 2016. http://europa.eu/rapid/press-release_IP-16-1613_en.htm

7 Digital disruption: The growth multiplier, Accenture Strategy 2016

8 http://click-accenture.com/accelerating-europes-comeback-digital/#.V0Q81nnmouU

9 Black, S, Lynch, L. “What’s Driving the New Economy: Understanding the Role of Workplace Practices” Economic Journal, February 2004. 114 (493); Brynjolfsson, E, Hitt, L. M., “Computing Productivity: Firm Level Evidence” Review of Economics and Statistics, 2003, 85 (4); Jorgenson, D. W., Ho, M. S., Stiroh, K, J. “A Retrospective Look at the US Productivity Growth Resurgence” Journal of Economic Perspectives – Volume 22, Number 1 – Winter 2008

10 The broken link: Why cost reduction efforts fail to fuel growth, Accenture Strategy, 2016

11 Being digital: Remaking business for a digital Europe, Accenture Strategy 2015

References

Redefining competitiveness and growth: Unlocking the digital potential of industries across Europe 43

12 Digital density index: Guiding digital transformation, Accenture, 2015

13 Government of the Future: How Digital Technology Will Change the Way We Live, Work and Govern, European Digital Forum, 2015

14 European Commission - Press release, Spring 2016 Economic Forecast: Staying the course amid high risks, Brussels, 3 May 2016. http://europa.eu/rapid/press-release_IP-16-1613_en.htm

Our grateful thanks to Oxford Economics for its contribution to this research program.

Oxford Economics is one of the world’s foremost independent global advisory firms, providing reports, forecast and analytical tools on 200 countries, 100 industrial sectors and over 3,000 cities. Headquartered in Oxford, England, with regional centres in London, New York and Singapore, Oxford Economics has more than 100 economists and analysts—one of the largest economics teams in the private sector. For more information, visit www.oxfordeconomics.com.

The views and opinions expressed in this document are meant to stimulate thought and discussion. As each business has unique requirements and objectives, these ideas should not be viewed as professional advice with respect to your business.

This document makes descriptive reference to trademarks that may be owned by others. The use of such trademarks herein is not an assertion of ownership of such trademarks by Accenture and is not intended to represent or imply the existence of an association between Accenture and the lawful owners of such trademarks.

About the European Business SummitThe European Business Summit (EBS) is Europe’s key meeting place for business leaders and decision makers, where business and politics shape the future. Every year, the EBS attracts more than 2,000 participants from over 60 countries, including: European Commissioners, Prime Ministers, high-ranking individuals and about 200 journalists. The European Business Summit is an initiative of BUSINESSEUROPE and the Federation of Enterprises in Belgium.

About BUSINESSEUROPEBUSINESSEUROPE is the leading advocate for growth and competitiveness at European level, standing up for companies across the continent and campaigning on the issues that most influence their performance. A recognised social partner, BUSINESSEUROPE speaks for all-sized enterprises in 34 European countries whose national business federations are our direct members.

About AccentureAccenture is a leading global professional services company, providing a broad range of services and solutions in strategy, consulting, digital, technology and operations. Combining unmatched experience and specialized skills across more than 40 industries and all business functions—underpinned by the world’s largest delivery network—Accenture works at the intersection of business and technology to help clients improve their performance and create sustainable value for their stakeholders. With approximately 373,000 people serving clients in more than 120 countries, Accenture drives innovation to improve the way the world works and lives. Visit us at www.accenture.com.

About Accenture StrategyAccenture Strategy operates at the intersection of business and technology. We bring together our capabilities in business, technology, operations and function strategy to help our clients envision and execute industry-specific strategies that support enterprise wide transformation. Our focus on issues related to digital disruption, competitiveness, global operating models, talent and leadership help drive both efficiencies and growth. For more information, follow @AccentureStrat or visit www.accenture.com/strategy.

Copyright © 2016 Accenture All rights reserved.

Accenture, its logo, and High Performance Delivered are trademarks of Accenture.