recent developments in as/ ifrs and ind as global … developments in as/ ifrs and ind as – global...

TRANSCRIPT

December 07, 2011

Recent developments in AS/ IFRS and IND AS –Global and India.

Presented by:

CA P.R.Ramesh

Bombay Chartered Accountants Society

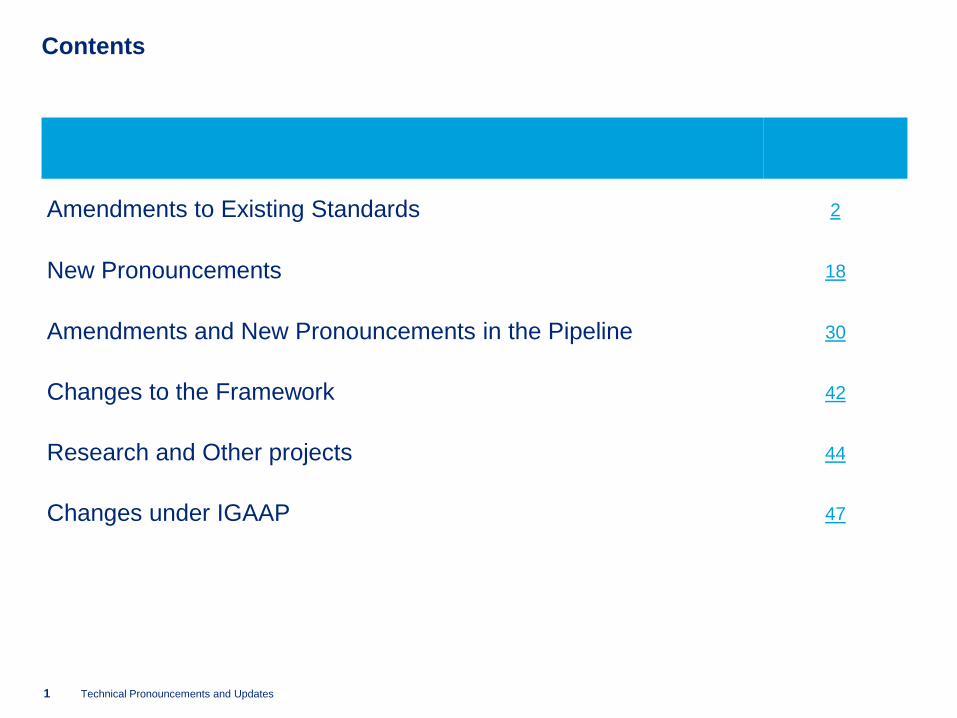

Amendments to Existing Standards 2

New Pronouncements 18

Amendments and New Pronouncements in the Pipeline 30

Changes to the Framework 42

Research and Other projects 44

Changes under IGAAP 47

Contents

1 Technical Pronouncements and Updates

2 Deloitte PowerPoint timesaver – August 2011

Recent Amendments to Existing Standards

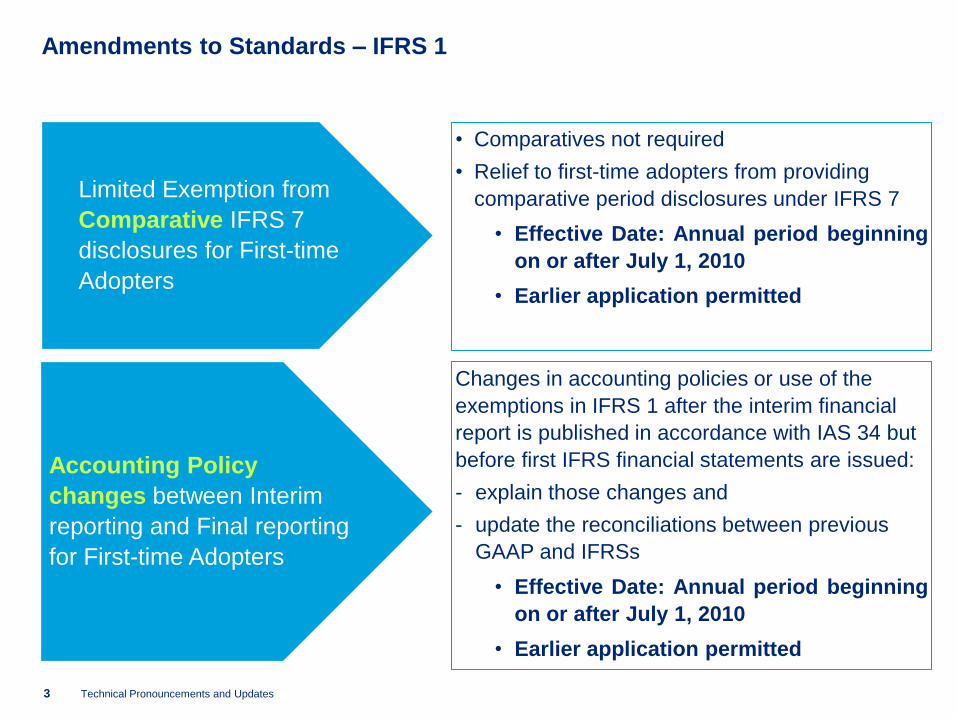

Amendments to Standards – IFRS 1

3 Technical Pronouncements and Updates

Limited Exemption from

Comparative IFRS 7

disclosures for First-time

Adopters

Accounting Policy

changes between Interim

reporting and Final reporting

for First-time Adopters

• Comparatives not required

• Relief to first-time adopters from providing

comparative period disclosures under IFRS 7

• Effective Date: Annual period beginning

on or after July 1, 2010

• Earlier application permitted

Changes in accounting policies or use of the

exemptions in IFRS 1 after the interim financial

report is published in accordance with IAS 34 but

before first IFRS financial statements are issued:

- explain those changes and

- update the reconciliations between previous

GAAP and IFRSs

• Effective Date: Annual period beginning

on or after July 1, 2010

• Earlier application permitted

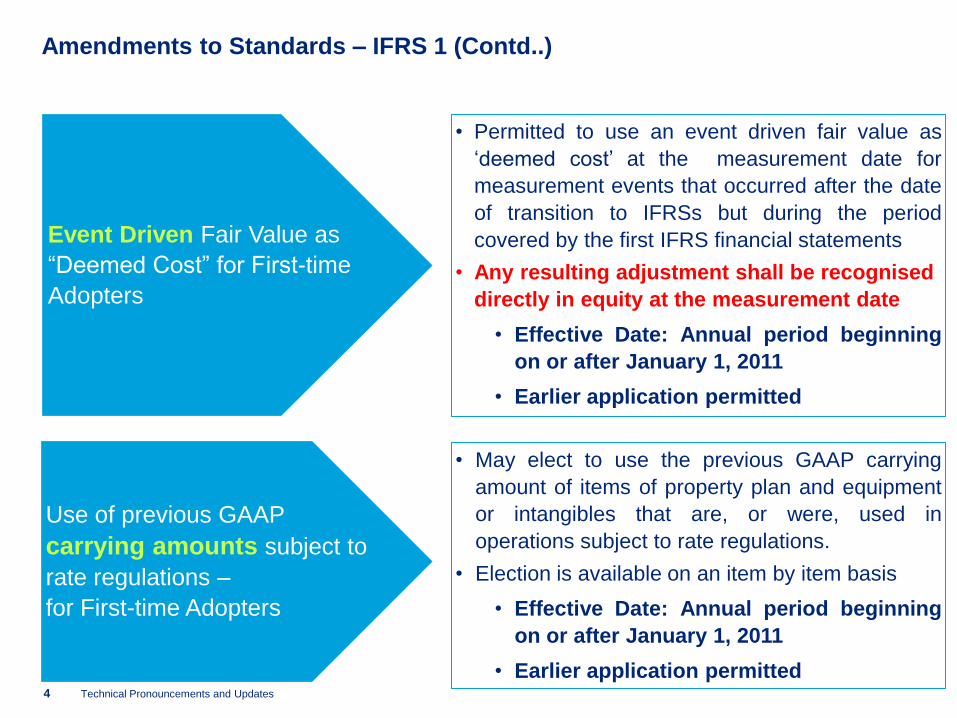

Amendments to Standards – IFRS 1 (Contd..)

4 Technical Pronouncements and Updates

Event Driven Fair Value as

“Deemed Cost” for First-time

Adopters

Use of previous GAAP

carrying amounts subject to

rate regulations –

for First-time Adopters

• Permitted to use an event driven fair value as

„deemed cost‟ at the measurement date for

measurement events that occurred after the date

of transition to IFRSs but during the period

covered by the first IFRS financial statements

• Any resulting adjustment shall be recognised

directly in equity at the measurement date

• Effective Date: Annual period beginning

on or after January 1, 2011

• Earlier application permitted

• May elect to use the previous GAAP carrying

amount of items of property plan and equipment

or intangibles that are, or were, used in

operations subject to rate regulations.

• Election is available on an item by item basis

• Effective Date: Annual period beginning

on or after January 1, 2011

• Earlier application permitted

Amendments to Standards – IFRS 1 (Contd..)

5 Technical Pronouncements and Updates

Removal of Fixed Dates

for First-time Adopters

• Replacing the date of prospective application of

the derecognition of financial assets and financial

liabilities of „1 January 2004‟ with „the date of

transition to IFRSs‟ so that first-time adopters of

IFRSs do not have to apply the derecognition

requirements in IAS 39 retrospectively from an

earlier date

• Relieving first-time adopters from recalculating

„day 1‟ gains and losses on transactions

occurring before the date of transition to IFRSs

• Effective Date: Annual period beginning

on or after July 1, 2011

• Earlier application permitted

Amendments to Standards – IFRS 1 (Contd..)

6 Technical Pronouncements and Updates

Entities emerging out of

severe Hyperinflation –

either resumption or

First-time Adopters

• when an entity‟s date of transition to IFRSs is on

or after the functional currency normalisation

date, the entity may elect to measure all assets

and liabilities held before the functional currency

normalisation date at fair value on the date of

transition to IFRSs and use that fair value as

deemed cost of those assets and liabilities in the

opening IFRS statement of financial position

• When the functional currency normalisation date

falls within a 12-month comparative period, the

comparative period may be less than 12 months,

provided that a complete set of financial

statements is provided for that shorter period

• Adjustments arising from this election must be

recognised directly in equity at the date of

transition to IFRSs and must be accompanied by

an explanation of how, and why, the entity had,

and then ceased to have, a functional currency

that was subject to severe hyperinflation

• Effective Date: Annual period beginning

on or after July 1, 2011

• Earlier application permitted

Amendments to Standards – IFRS 3

7 Technical Pronouncements and Updates

Valuation of

Non-Controlling Interests –

in Financial Statements

• the option to measure NCI either at fair value or

at the proportionate share of the acquiree‟s net

identifiable assets at the acquisition date under

IFRS 3(2008) applies only to NCI that are

present ownership interests and entitle their

holders to a proportionate share of the acquiree‟s

net assets in the event of liquidation

• All other components of NCI should be measured

at their acquisition date fair value, unless another

measurement basis is required by IFRSs

• The current requirement in accordance with IFRS

2 at the acquisition date („market-based

measure‟) applies also to share-based payment

transactions of the acquiree that are not

replaced.

• Effective Date: Annual period beginning

on or after July 1, 2010

• Earlier application permitted

Measurement of

Stock Awards of acquirer

which replace acquiree

awards

Amendments to Standards – IFRS 3 (Contd..)

8 Technical Pronouncements and Updates

Contingent Consideration

arising from business

combinations

• IAS 32 Financial Instruments: Presentation, IAS

39 Financial Instruments: Recognition and

Measurement and IFRS 7 Financial Instruments:

Disclosures do not apply to contingent

consideration that arose from business

combinations whose acquisition dates

preceded the application of IFRS 3(2008).

• Effective Date: Annual period beginning

on or after July 1, 2010

• Earlier application permitted

Amendments to Standards – IFRS 7

9 Technical Pronouncements and Updates

Qualitative Disclosures

in the context of

quantitative disclosures

• encourages qualitative disclosures in the

context of quantitative disclosures required

to help users to form an overall picture of the

nature and extent of risks arising from

financial instruments

• Clarifies the required level of disclosure

around credit risk and collateral held and

provides relief from disclosure of

renegotiated loans.

• Examples:

‒ description of collateral held as security and of

other credit enhancements, and their financial

effect .

‒ the amount that best represents its maximum

exposure to credit risk at the end of the

reporting period without taking account of any

collateral held or other credit enhancements

‒ an analysis of the age of financial assets that

are past due as at the end of the reporting

period but not impaired

• Effective Date: Annual period beginning

on or after January 1, 2011

• Earlier application permitted

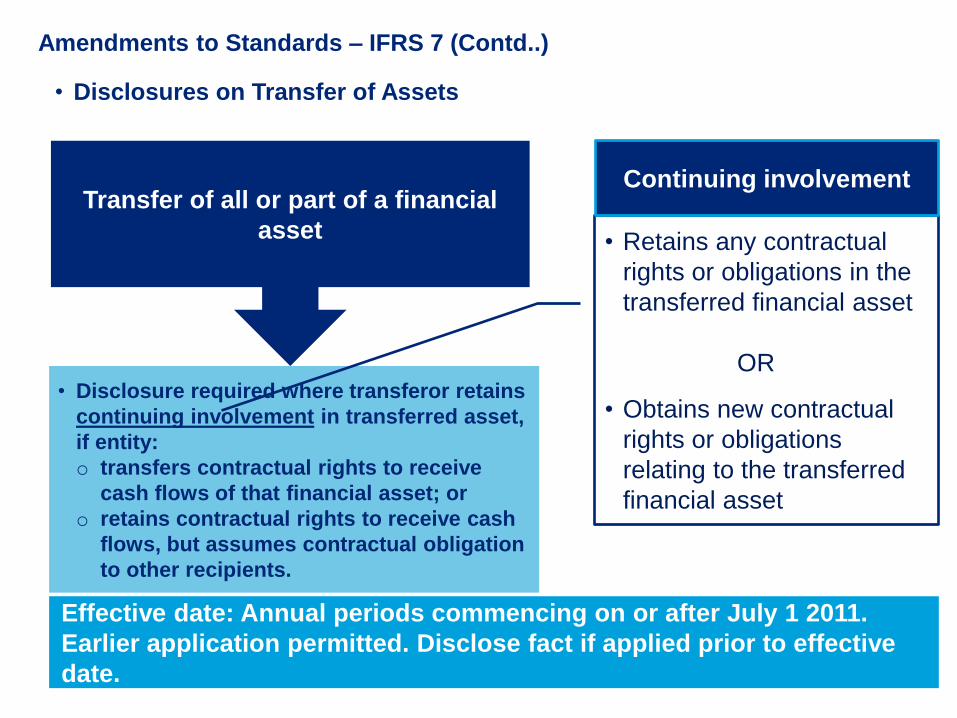

Amendments to Standards – IFRS 7 (Contd..)

Transfer of all or part of a financial

asset

• Disclosure required where transferor retains

continuing involvement in transferred asset,

if entity:

o transfers contractual rights to receive

cash flows of that financial asset; or

o retains contractual rights to receive cash

flows, but assumes contractual obligation

to other recipients.

• Retains any contractual

rights or obligations in the

transferred financial asset

OR

• Obtains new contractual

rights or obligations

relating to the transferred

financial asset

Continuing involvement

Effective date: Annual periods commencing on or after July 1 2011.

Earlier application permitted. Disclose fact if applied prior to effective

date.

• Disclosures on Transfer of Assets

Amendments to Standards – IFRS 9

11 Technical Pronouncements and Updates

Classification and

Recognition – as per

IFRS 9

• The classification criteria for financial liabilities

contained in IAS 39 move to IFRS 9 unchanged

and the IAS 39 classification categories of

amortised cost and fair value through profit or

loss are retained.

• Financial liability designated as at FVTPL using

the fair value option, the change in the liability‟s

fair value attributable to changes in the liability‟s

credit risk is recognised directly in other

comprehensive income, unless it creates or

increases an accounting mismatch

• The amount that is recognised in other

comprehensive income is not recycled when

the liability is settled or extinguished .

• Credit Risk distinguished from asset-specific

performance

• Cost exemption in IAS 39 for derivative liabilities

to be settled by delivery of unquoted equity

instruments is eliminated

• Effective Date: Annual period beginning on or

after January 1, 2013

• Earlier application permitted provided portion

relating to financial assets is also applied early

Amendments to Standards – IAS 12

12 Technical Pronouncements and Updates

Deferred Tax: Recovery

of Underlying Assets

• Exception to the general principles of IAS 12 for

investment property measured using the fair

value model in IAS 40 Investment Property

including those acquired in a business

combination if the acquirer applies the fair value

model in IAS 40 subsequent to the business

combination

• Measurement: introduce a rebuttable

presumption that the carrying amount of such an

asset will be recovered entirely through sale

• The amendments also incorporate that deferred

tax arising on a non-depreciable asset measured

using the revaluation model in IAS 16 should be

based on the sale rate

• Effective Date: Annual period beginning

on or after January 1, 2012

• Earlier application permitted

Amendments to Standards – IAS 19

13 Technical Pronouncements and Updates

Employee Benefits

• Basic Principle - Recognition of changes in the

defined benefit obligation and in plan assets

when those changes occur, eliminating the

corridor approach and accelerating the

recognition of past service costs

• Presentation - Changes in the defined benefit

obligation and plan assets are disaggregated into

three components: service costs, net interest on

the net defined benefit liabilities (assets) and

remeasurements of the net defined benefit

liabilities (assets).

• Net interest is calculated using a high quality

corporate bond yield. This may be lower than the

rate currently used to calculate expected return

on plan assets, resulting in a decrease in net

income.

• Remeasurements are never reclassified to

profit or loss.

• Effective Date: Annual period beginning

on or after January 1, 2013

• Earlier application permitted

Amendments to Standards – IAS 1

14 Technical Pronouncements and Updates

Presentation of Items of

Other Comprehensive

Income

• Change in Title - The „Statement of

Comprehensive Income‟ is changed as

„Statement of Profit or Loss and Other

Comprehensive Income‟. This is not mandatory.

The existing title „can still be used

• The amendments retain the option to present

profit or loss and other comprehensive income in

either a single continuous statement or in two

separate but consecutive statements.

• Items of OCI are required to be grouped into

those that will and those that will not

subsequently be reclassified to profit or loss.

• Tax on items of OCI is required to be allocated to

the above groups of OCI.

• The measurement and recognition of items of

profit or loss and OCI are not affected by the

amendments.

• Effective Date: Annual period beginning

on or after January 1, 2012

• Earlier application permitted

Amendments to Standards – Other Standards

15 Technical Pronouncements and Updates

IAS 1 – OCI presentation

IAS 27 – Consequential

changes

• Clarification issued that an entity may present

the analysis of OCI by item either in the

statement of changes in equity or in the notes to

the financial statements

• Effective Date: Annual period beginning

on or after January 1, 2011

• Earlier application permitted

• Consequential amendments to IAS 21, IAS 28

and IAS 31 as a result of IAS 27(2008) should

be applied prospectively (with the exception of

paragraph 35 of IAS 28 and paragraph 46 of

IAS 31, which should be applied retrospectively)

• Effective Date: Annual period beginning

on or after July 1, 2010

• Earlier application permitted

Amendments to Standards – Other Standards (Contd..)

16 Technical Pronouncements and Updates

IAS 34 – Interim Financial

Reporting

IFRIC 13 – Customer Loyalty

Programmes

‒ Emphasises the principle that the disclosure

about significant events and transactions in

interim periods should update the relevant

information presented in the most recent

annual financial report and Clarifies how to

apply this principle in respect of financial

instruments and their fair values.

‒ Clarifies that the „fair value‟ of award credits

should take into account: (i) the amount of

discounts or incentives that would otherwise

be offered to customers who have not earned

award credits from an initial sale; and (ii) any

expected forfeitures.

• Effective Date: Annual period beginning

on or after January 1, 2011

• Earlier application permitted

17 Deloitte PowerPoint timesaver – August 2011

New Accounting Standards and Interpretations

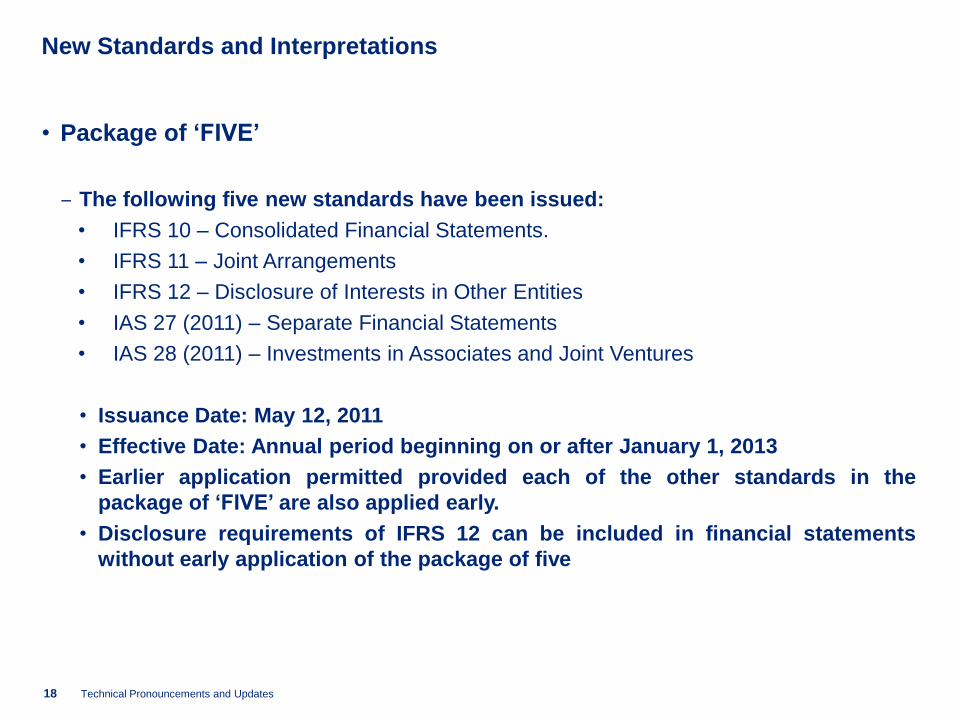

New Standards and Interpretations

• Package of „FIVE‟

‒ The following five new standards have been issued:

• IFRS 10 – Consolidated Financial Statements.

• IFRS 11 – Joint Arrangements

• IFRS 12 – Disclosure of Interests in Other Entities

• IAS 27 (2011) – Separate Financial Statements

• IAS 28 (2011) – Investments in Associates and Joint Ventures

• Issuance Date: May 12, 2011

• Effective Date: Annual period beginning on or after January 1, 2013

• Earlier application permitted provided each of the other standards in the

package of „FIVE‟ are also applied early.

• Disclosure requirements of IFRS 12 can be included in financial statements

without early application of the package of five

18 Technical Pronouncements and Updates

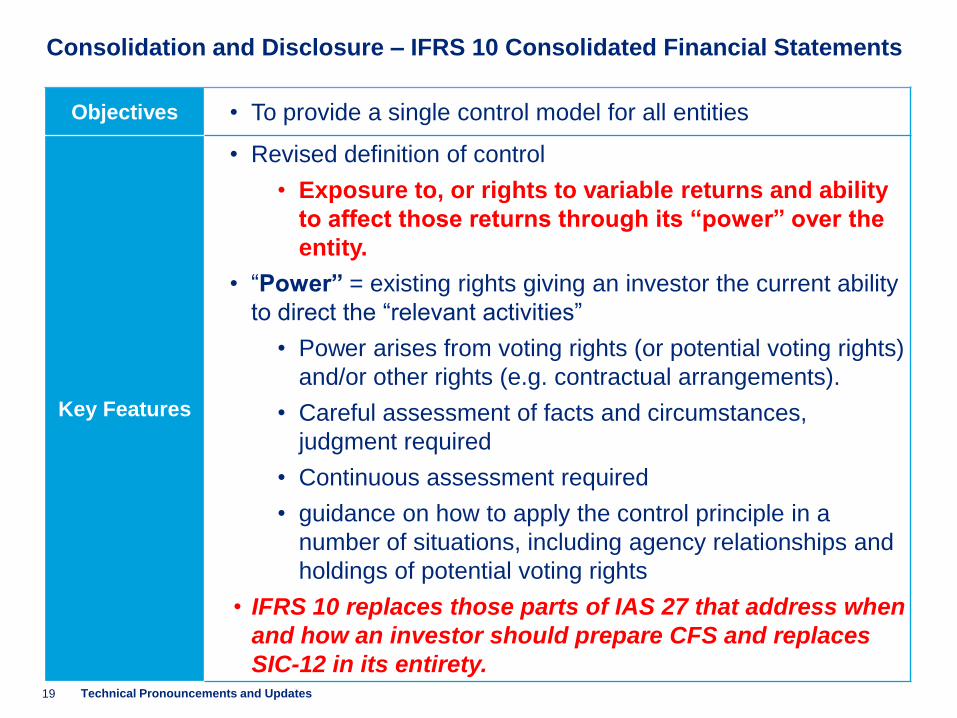

Consolidation and Disclosure – IFRS 10 Consolidated Financial Statements

Objectives • To provide a single control model for all entities

Key Features

• Revised definition of control

• Exposure to, or rights to variable returns and ability

to affect those returns through its “power” over the

entity.

• “Power” = existing rights giving an investor the current ability

to direct the “relevant activities”

• Power arises from voting rights (or potential voting rights)

and/or other rights (e.g. contractual arrangements).

• Careful assessment of facts and circumstances,

judgment required

• Continuous assessment required

• guidance on how to apply the control principle in a

number of situations, including agency relationships and

holdings of potential voting rights

• IFRS 10 replaces those parts of IAS 27 that address when

and how an investor should prepare CFS and replaces

SIC-12 in its entirety.19 Technical Pronouncements and Updates

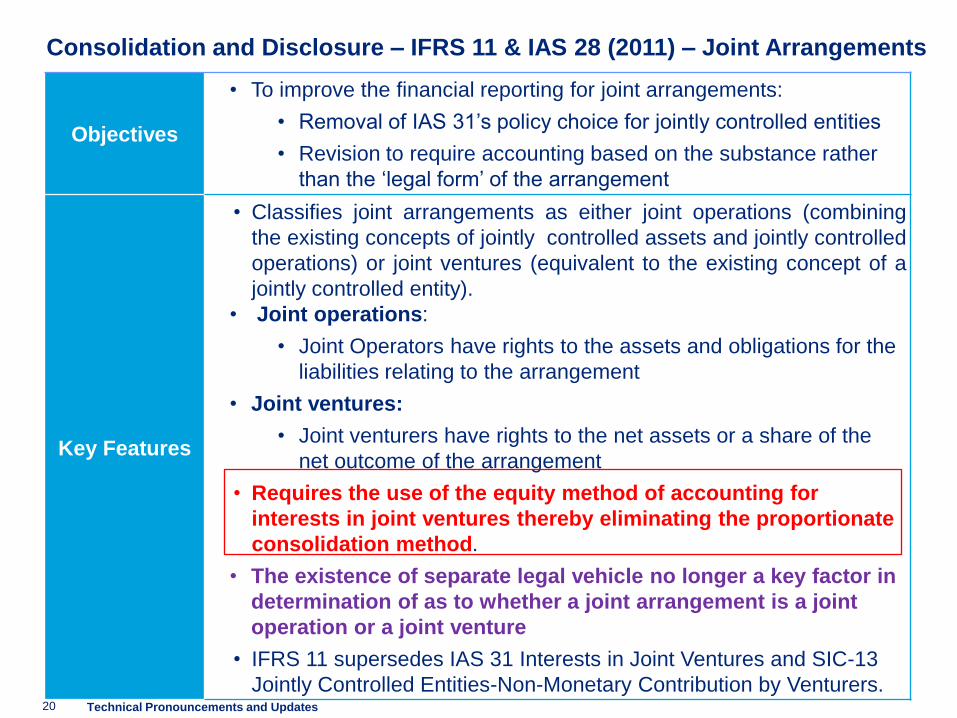

Consolidation and Disclosure – IFRS 11 & IAS 28 (2011) – Joint Arrangements

Objectives

• To improve the financial reporting for joint arrangements:

• Removal of IAS 31‟s policy choice for jointly controlled entities

• Revision to require accounting based on the substance rather

than the „legal form‟ of the arrangement

Key Features

• Classifies joint arrangements as either joint operations (combining

the existing concepts of jointly controlled assets and jointly controlled

operations) or joint ventures (equivalent to the existing concept of a

jointly controlled entity).

• Joint operations:

• Joint Operators have rights to the assets and obligations for the

liabilities relating to the arrangement

• Joint ventures:

• Joint venturers have rights to the net assets or a share of the

net outcome of the arrangement

• Requires the use of the equity method of accounting for

interests in joint ventures thereby eliminating the proportionate

consolidation method.

• The existence of separate legal vehicle no longer a key factor in

determination of as to whether a joint arrangement is a joint

operation or a joint venture

• IFRS 11 supersedes IAS 31 Interests in Joint Ventures and SIC-13

Jointly Controlled Entities-Non-Monetary Contribution by Venturers.20 Technical Pronouncements and Updates

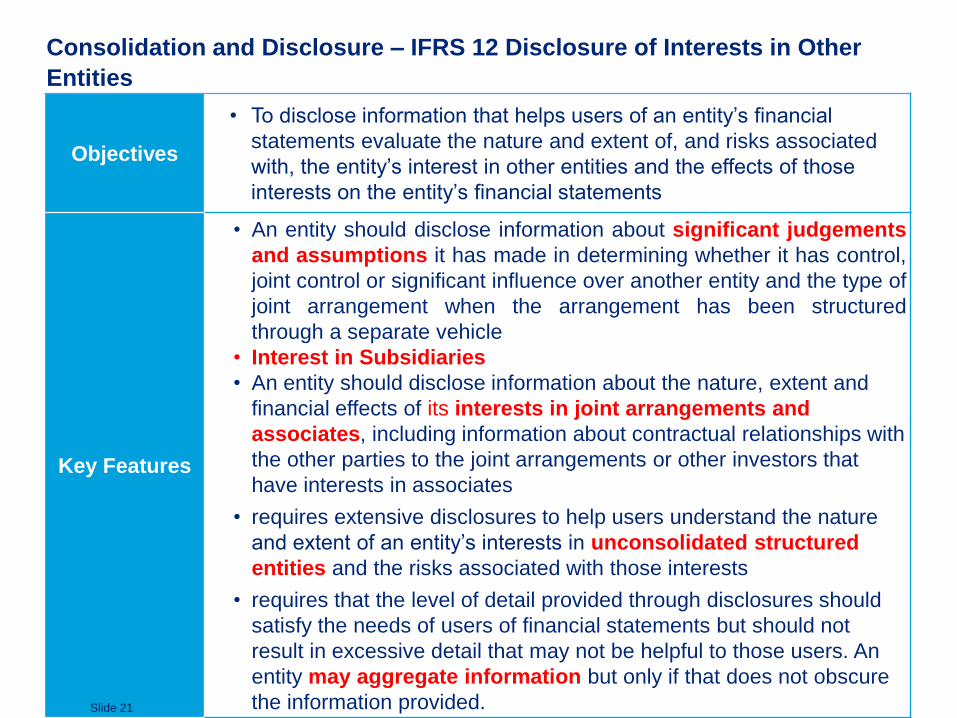

Consolidation and Disclosure – IFRS 12 Disclosure of Interests in Other

Entities

Objectives

• To disclose information that helps users of an entity‟s financial

statements evaluate the nature and extent of, and risks associated

with, the entity‟s interest in other entities and the effects of those

interests on the entity‟s financial statements

Key Features

• An entity should disclose information about significant judgements

and assumptions it has made in determining whether it has control,

joint control or significant influence over another entity and the type of

joint arrangement when the arrangement has been structured

through a separate vehicle

• Interest in Subsidiaries

• An entity should disclose information about the nature, extent and

financial effects of its interests in joint arrangements and

associates, including information about contractual relationships with

the other parties to the joint arrangements or other investors that

have interests in associates

• requires extensive disclosures to help users understand the nature

and extent of an entity‟s interests in unconsolidated structured

entities and the risks associated with those interests

• requires that the level of detail provided through disclosures should

satisfy the needs of users of financial statements but should not

result in excessive detail that may not be helpful to those users. An

entity may aggregate information but only if that does not obscure

the information provided.Slide 21

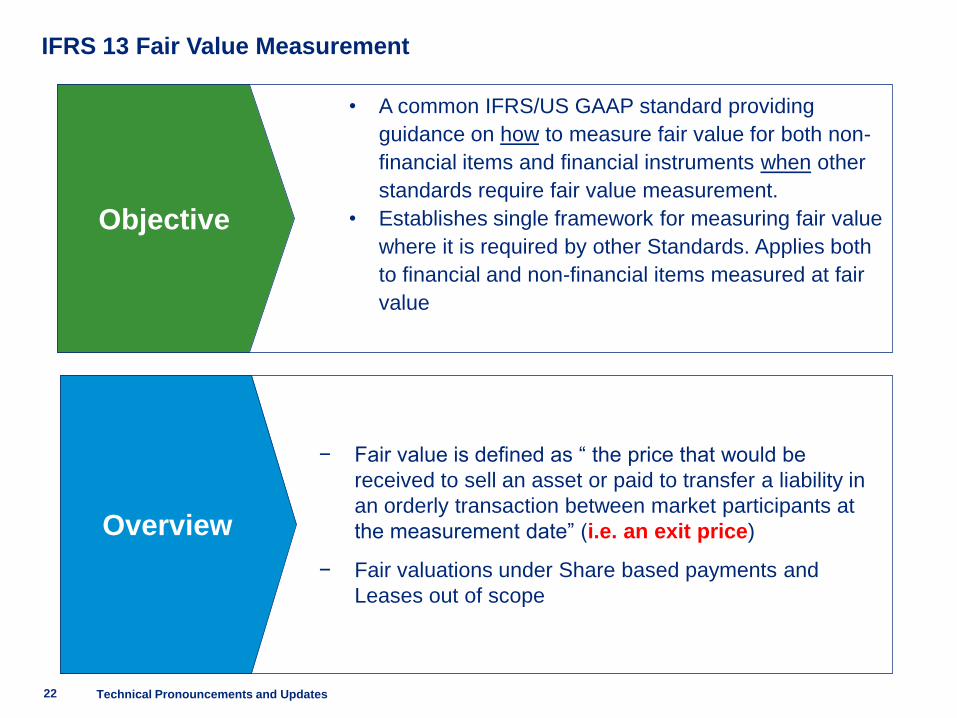

IFRS 13 Fair Value Measurement

22

• A common IFRS/US GAAP standard providing

guidance on how to measure fair value for both non-

financial items and financial instruments when other

standards require fair value measurement.

• Establishes single framework for measuring fair value

where it is required by other Standards. Applies both

to financial and non-financial items measured at fair

value

Objective

− Fair value is defined as “ the price that would be

received to sell an asset or paid to transfer a liability in

an orderly transaction between market participants at

the measurement date” (i.e. an exit price)

− Fair valuations under Share based payments and

Leases out of scope

Overview

Technical Pronouncements and Updates

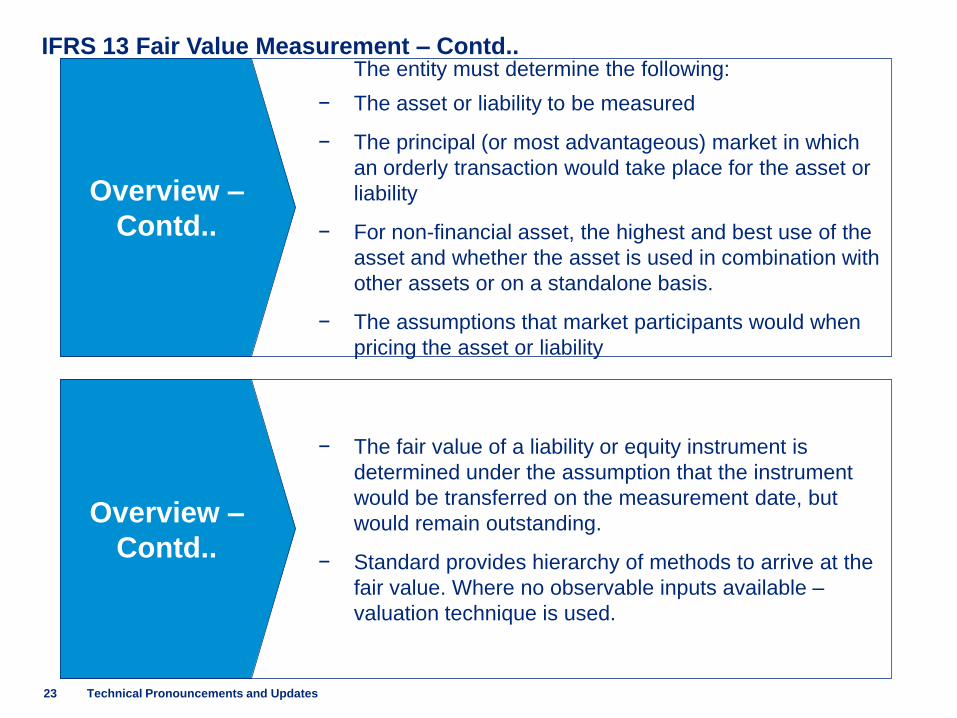

IFRS 13 Fair Value Measurement – Contd..

23 Technical Pronouncements and Updates

The entity must determine the following:

− The asset or liability to be measured

− The principal (or most advantageous) market in which

an orderly transaction would take place for the asset or

liability

− For non-financial asset, the highest and best use of the

asset and whether the asset is used in combination with

other assets or on a standalone basis.

− The assumptions that market participants would when

pricing the asset or liability

Overview –

Contd..

− The fair value of a liability or equity instrument is

determined under the assumption that the instrument

would be transferred on the measurement date, but

would remain outstanding.

− Standard provides hierarchy of methods to arrive at the

fair value. Where no observable inputs available –

valuation technique is used.

Overview –

Contd..

IFRS 13 Fair Value Measurement – Contd..

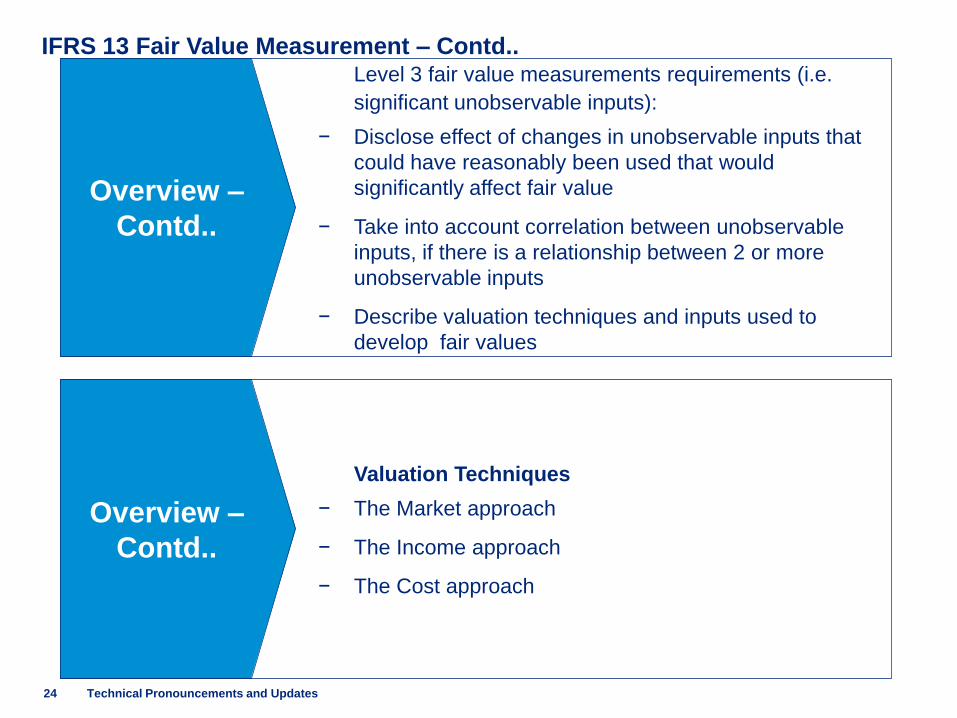

24 Technical Pronouncements and Updates

Level 3 fair value measurements requirements (i.e.

significant unobservable inputs):

− Disclose effect of changes in unobservable inputs that

could have reasonably been used that would

significantly affect fair value

− Take into account correlation between unobservable

inputs, if there is a relationship between 2 or more

unobservable inputs

− Describe valuation techniques and inputs used to

develop fair values

Overview –

Contd..

Valuation Techniques

− The Market approach

− The Income approach

− The Cost approach

Overview –

Contd..

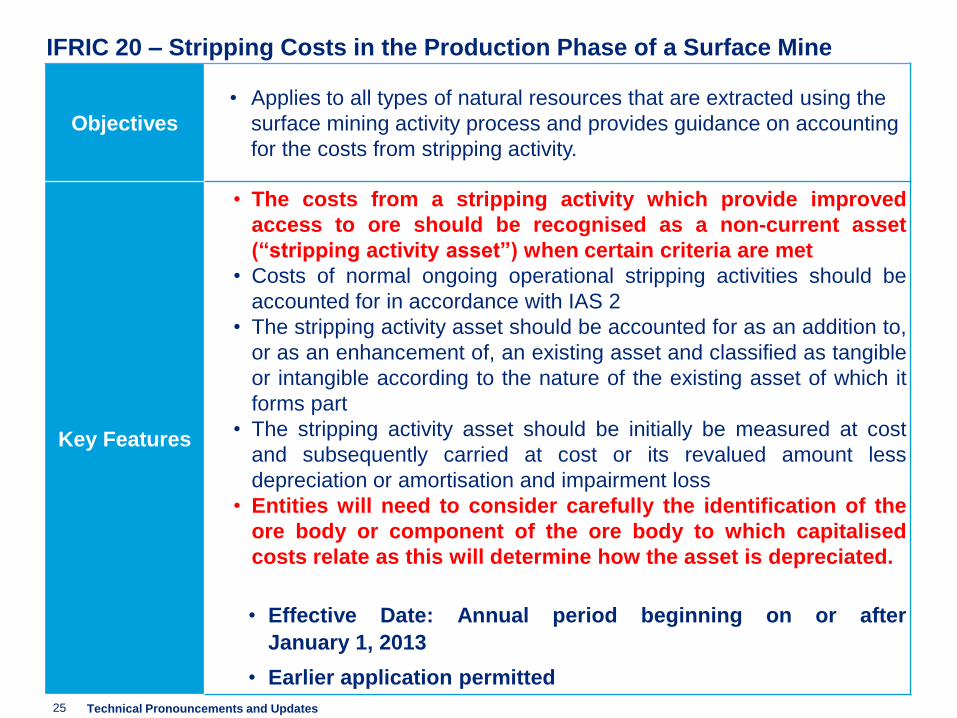

IFRIC 20 – Stripping Costs in the Production Phase of a Surface Mine

Objectives

• Applies to all types of natural resources that are extracted using the

surface mining activity process and provides guidance on accounting

for the costs from stripping activity.

Key Features

• The costs from a stripping activity which provide improved

access to ore should be recognised as a non-current asset

(“stripping activity asset”) when certain criteria are met

• Costs of normal ongoing operational stripping activities should be

accounted for in accordance with IAS 2

• The stripping activity asset should be accounted for as an addition to,

or as an enhancement of, an existing asset and classified as tangible

or intangible according to the nature of the existing asset of which it

forms part

• The stripping activity asset should be initially be measured at cost

and subsequently carried at cost or its revalued amount less

depreciation or amortisation and impairment loss

• Entities will need to consider carefully the identification of the

ore body or component of the ore body to which capitalised

costs relate as this will determine how the asset is depreciated.

• Effective Date: Annual period beginning on or after

January 1, 2013

• Earlier application permitted

25 Technical Pronouncements and Updates

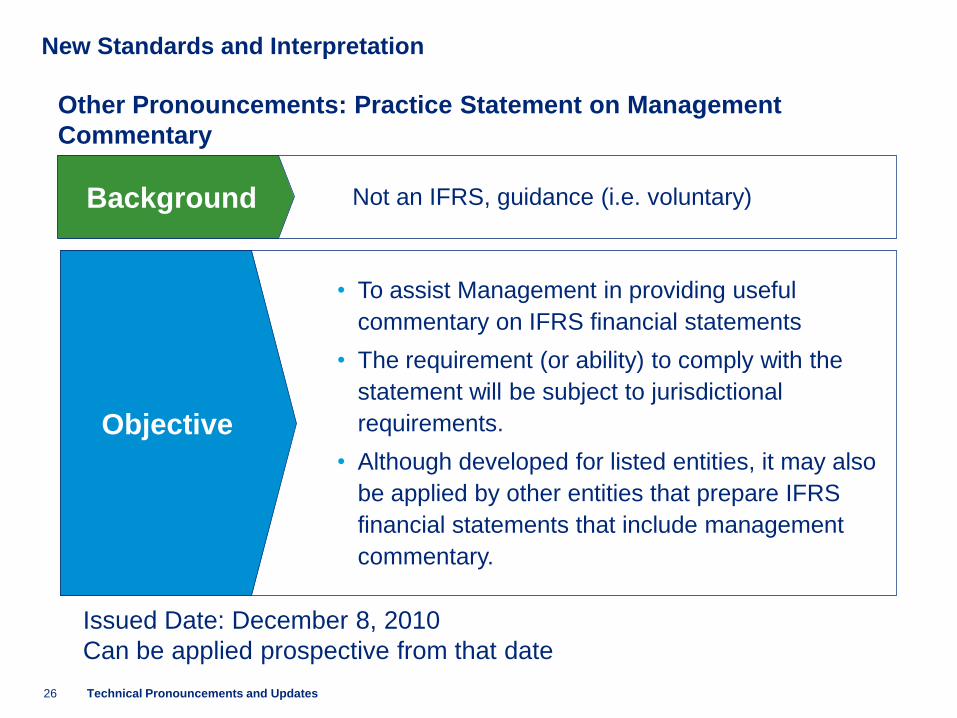

New Standards and Interpretation

26

Not an IFRS, guidance (i.e. voluntary)Background

• To assist Management in providing useful

commentary on IFRS financial statements

• The requirement (or ability) to comply with the

statement will be subject to jurisdictional

requirements.

• Although developed for listed entities, it may also

be applied by other entities that prepare IFRS

financial statements that include management

commentary.

Objective

Other Pronouncements: Practice Statement on Management

Commentary

Issued Date: December 8, 2010

Can be applied prospective from that date

Technical Pronouncements and Updates

27 Deloitte PowerPoint timesaver – August 2011

Amendments/ New Pronouncements in the pipeline

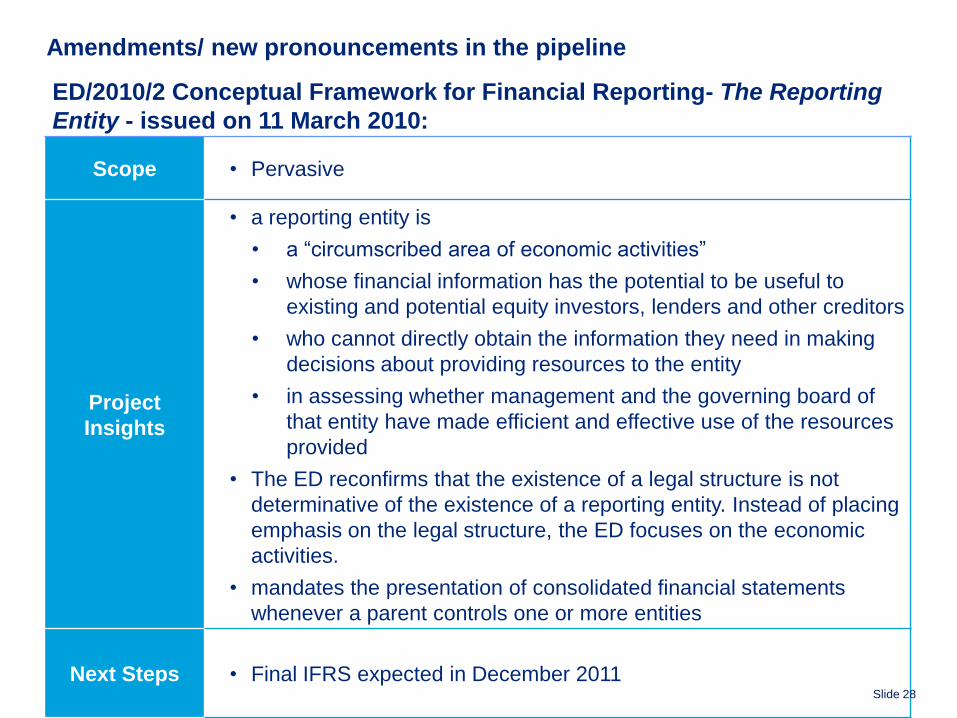

Amendments/ new pronouncements in the pipeline

Scope • Pervasive

Project

Insights

• a reporting entity is

• a “circumscribed area of economic activities”

• whose financial information has the potential to be useful to

existing and potential equity investors, lenders and other creditors

• who cannot directly obtain the information they need in making

decisions about providing resources to the entity

• in assessing whether management and the governing board of

that entity have made efficient and effective use of the resources

provided

• The ED reconfirms that the existence of a legal structure is not

determinative of the existence of a reporting entity. Instead of placing

emphasis on the legal structure, the ED focuses on the economic

activities.

• mandates the presentation of consolidated financial statements

whenever a parent controls one or more entities

Next Steps • Final IFRS expected in December 2011Slide 28

ED/2010/2 Conceptual Framework for Financial Reporting- The Reporting

Entity - issued on 11 March 2010:

Amendments/ new pronouncements in the pipeline

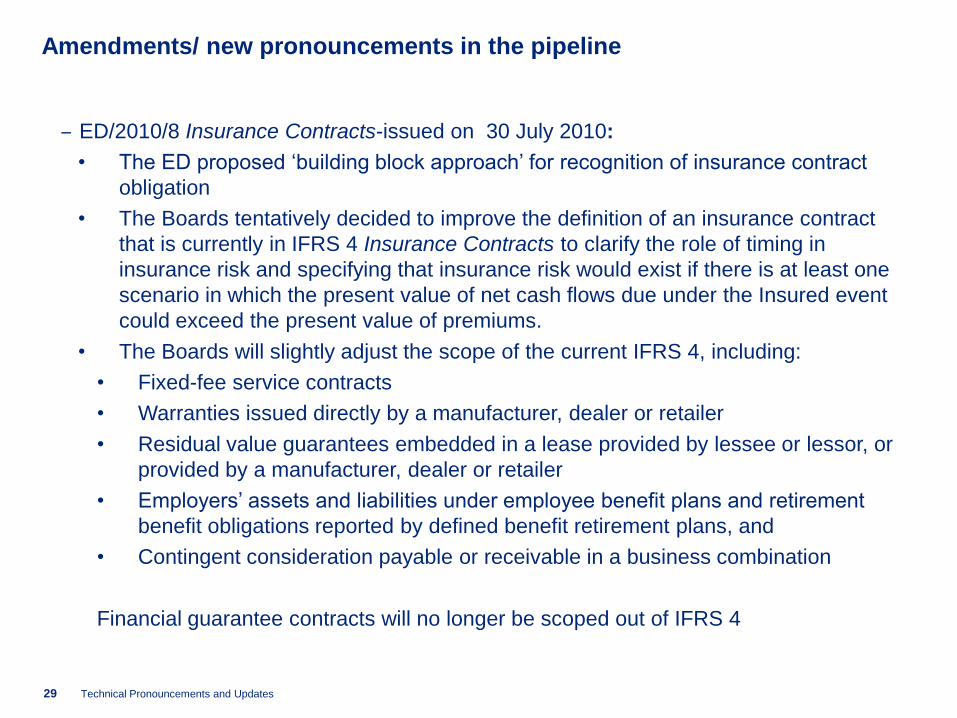

‒ ED/2010/8 Insurance Contracts-issued on 30 July 2010:

• The ED proposed „building block approach‟ for recognition of insurance contract

obligation

• The Boards tentatively decided to improve the definition of an insurance contract

that is currently in IFRS 4 Insurance Contracts to clarify the role of timing in

insurance risk and specifying that insurance risk would exist if there is at least one

scenario in which the present value of net cash flows due under the Insured event

could exceed the present value of premiums.

• The Boards will slightly adjust the scope of the current IFRS 4, including:

• Fixed-fee service contracts

• Warranties issued directly by a manufacturer, dealer or retailer

• Residual value guarantees embedded in a lease provided by lessee or lessor, or

provided by a manufacturer, dealer or retailer

• Employers‟ assets and liabilities under employee benefit plans and retirement

benefit obligations reported by defined benefit retirement plans, and

• Contingent consideration payable or receivable in a business combination

Financial guarantee contracts will no longer be scoped out of IFRS 4

29 Technical Pronouncements and Updates

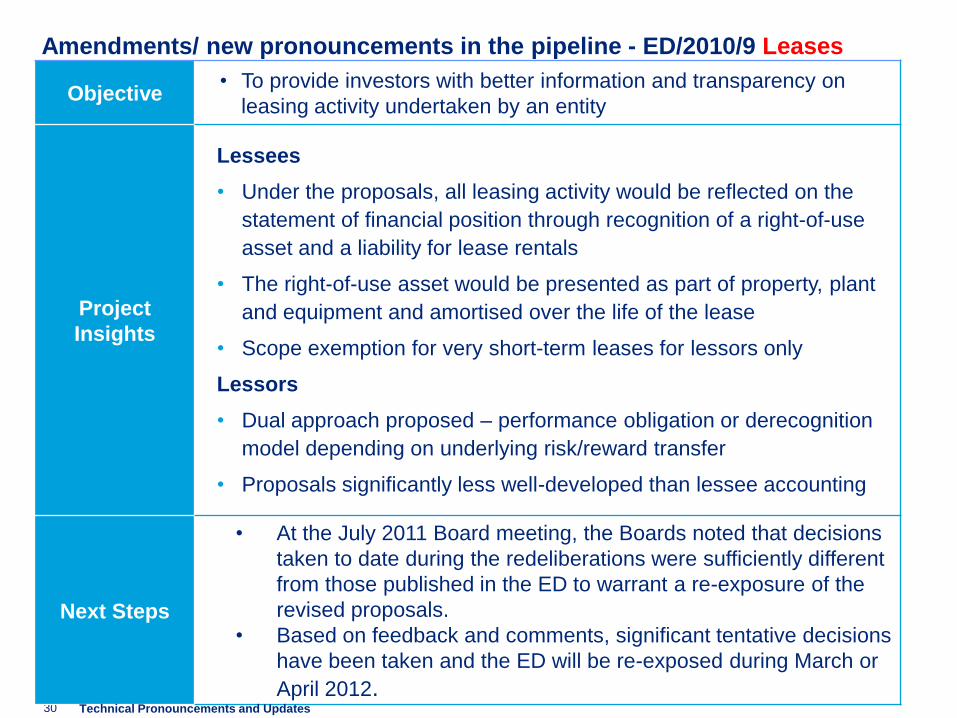

Amendments/ new pronouncements in the pipeline - ED/2010/9 Leases

Slide

30

Objective• To provide investors with better information and transparency on

leasing activity undertaken by an entity

Project

Insights

Lessees

• Under the proposals, all leasing activity would be reflected on the

statement of financial position through recognition of a right-of-use

asset and a liability for lease rentals

• The right-of-use asset would be presented as part of property, plant

and equipment and amortised over the life of the lease

• Scope exemption for very short-term leases for lessors only

Lessors

• Dual approach proposed – performance obligation or derecognition

model depending on underlying risk/reward transfer

• Proposals significantly less well-developed than lessee accounting

Next Steps

• At the July 2011 Board meeting, the Boards noted that decisions

taken to date during the redeliberations were sufficiently different

from those published in the ED to warrant a re-exposure of the

revised proposals.

• Based on feedback and comments, significant tentative decisions

have been taken and the ED will be re-exposed during March or

April 2012.Technical Pronouncements and Updates

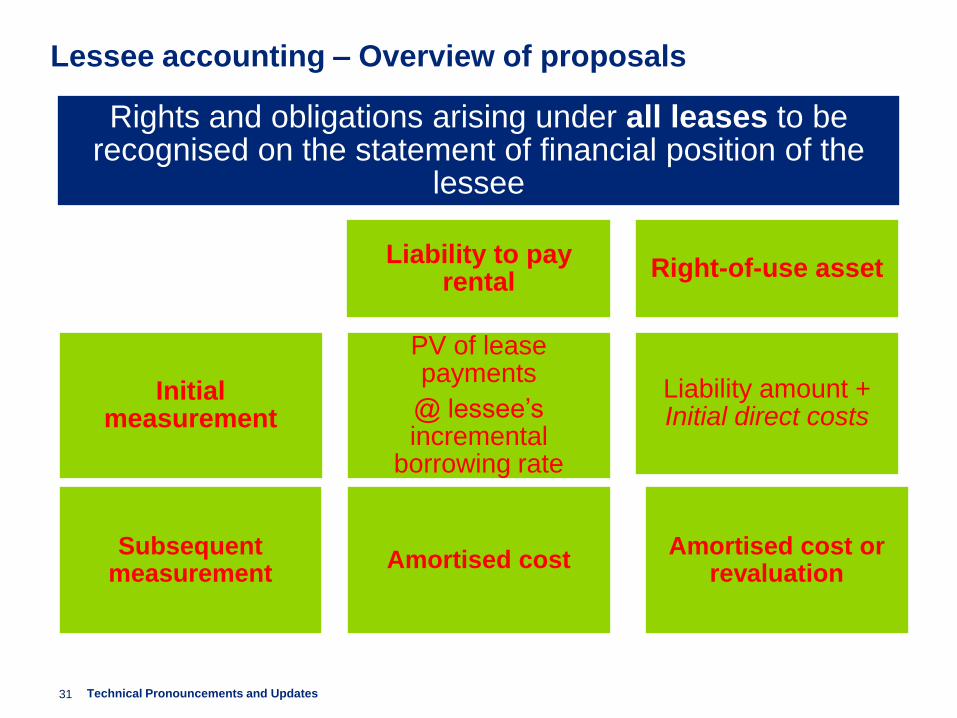

Rights and obligations arising under all leases to be recognised on the statement of financial position of the

lessee

Initial measurement

Liability to pay rental

PV of lease payments

@ lessee‟s incremental

borrowing rate

Right-of-use asset

Liability amount + Initial direct costs

31

Lessee accounting – Overview of proposals

Subsequent measurement

Amortised costAmortised cost or

revaluation

Technical Pronouncements and Updates

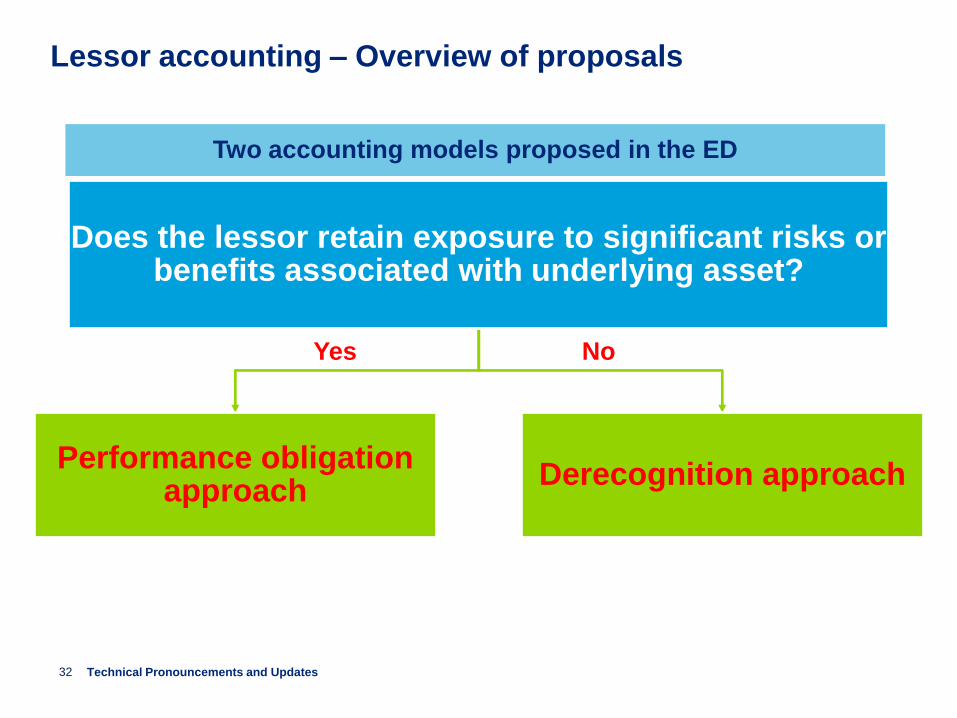

Does the lessor retain exposure to significant risks or benefits associated with underlying asset?

Performance obligation approach

Derecognition approach

Yes No

32

Lessor accounting – Overview of proposals

Two accounting models proposed in the ED

Yes No

Technical Pronouncements and Updates

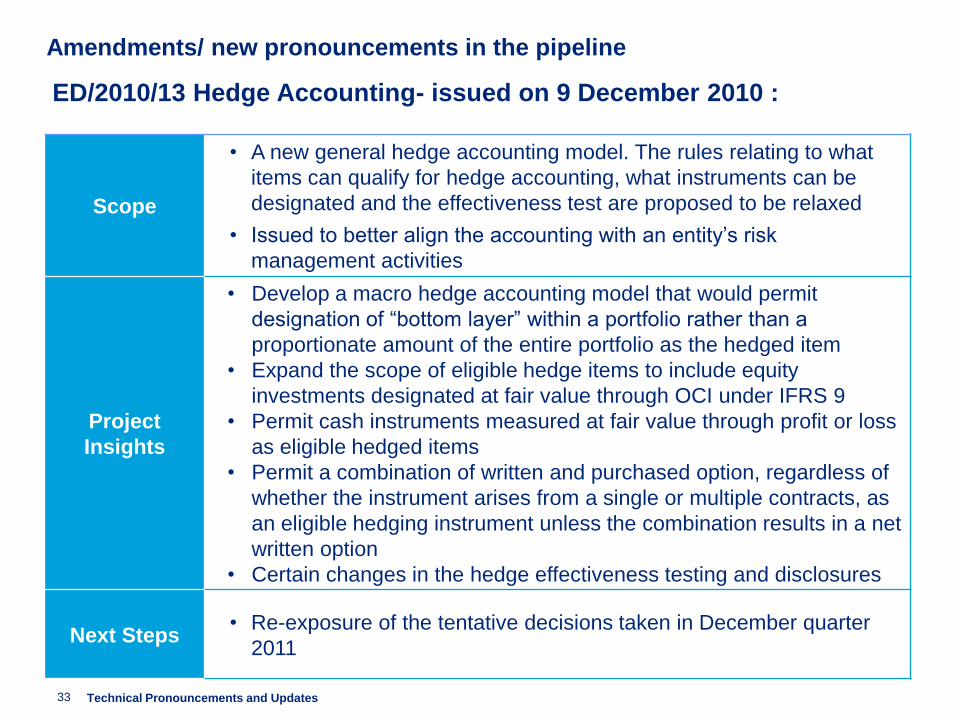

Amendments/ new pronouncements in the pipeline

Scope

• A new general hedge accounting model. The rules relating to what

items can qualify for hedge accounting, what instruments can be

designated and the effectiveness test are proposed to be relaxed

• Issued to better align the accounting with an entity‟s risk

management activities

Project

Insights

• Develop a macro hedge accounting model that would permit

designation of “bottom layer” within a portfolio rather than a

proportionate amount of the entire portfolio as the hedged item

• Expand the scope of eligible hedge items to include equity

investments designated at fair value through OCI under IFRS 9

• Permit cash instruments measured at fair value through profit or loss

as eligible hedged items

• Permit a combination of written and purchased option, regardless of

whether the instrument arises from a single or multiple contracts, as

an eligible hedging instrument unless the combination results in a net

written option

• Certain changes in the hedge effectiveness testing and disclosures

Next Steps• Re-exposure of the tentative decisions taken in December quarter

2011

33

ED/2010/13 Hedge Accounting- issued on 9 December 2010 :

Technical Pronouncements and Updates

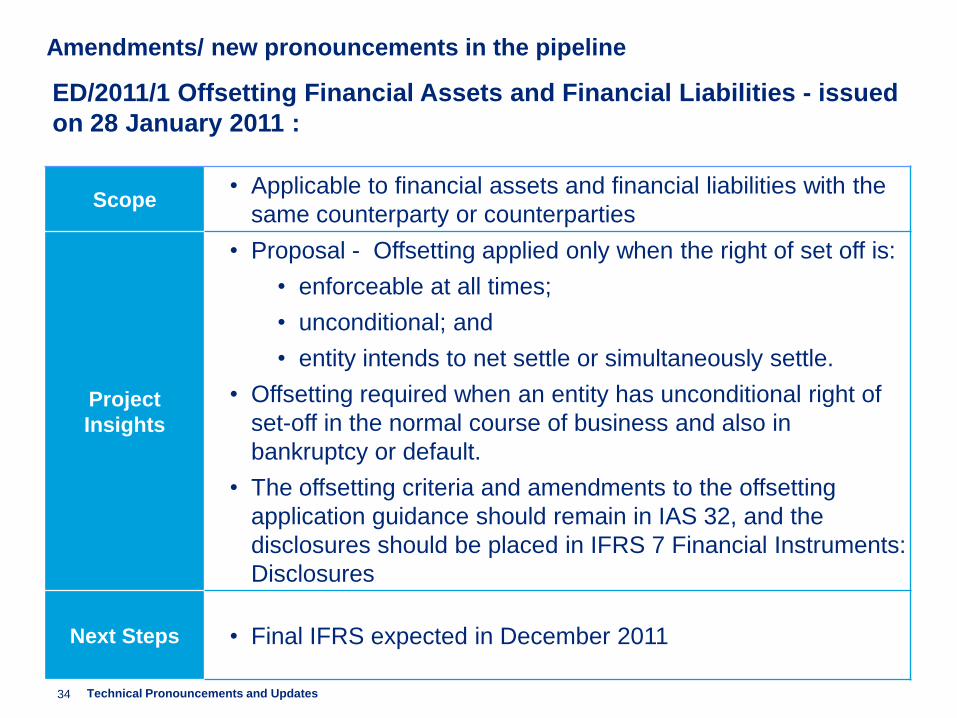

Amendments/ new pronouncements in the pipeline

Scope• Applicable to financial assets and financial liabilities with the

same counterparty or counterparties

Project

Insights

• Proposal - Offsetting applied only when the right of set off is:

• enforceable at all times;

• unconditional; and

• entity intends to net settle or simultaneously settle.

• Offsetting required when an entity has unconditional right of

set-off in the normal course of business and also in

bankruptcy or default.

• The offsetting criteria and amendments to the offsetting

application guidance should remain in IAS 32, and the

disclosures should be placed in IFRS 7 Financial Instruments:

Disclosures

Next Steps • Final IFRS expected in December 2011

34

ED/2011/1 Offsetting Financial Assets and Financial Liabilities - issued

on 28 January 2011 :

Technical Pronouncements and Updates

Amendments/ new pronouncements in the pipeline

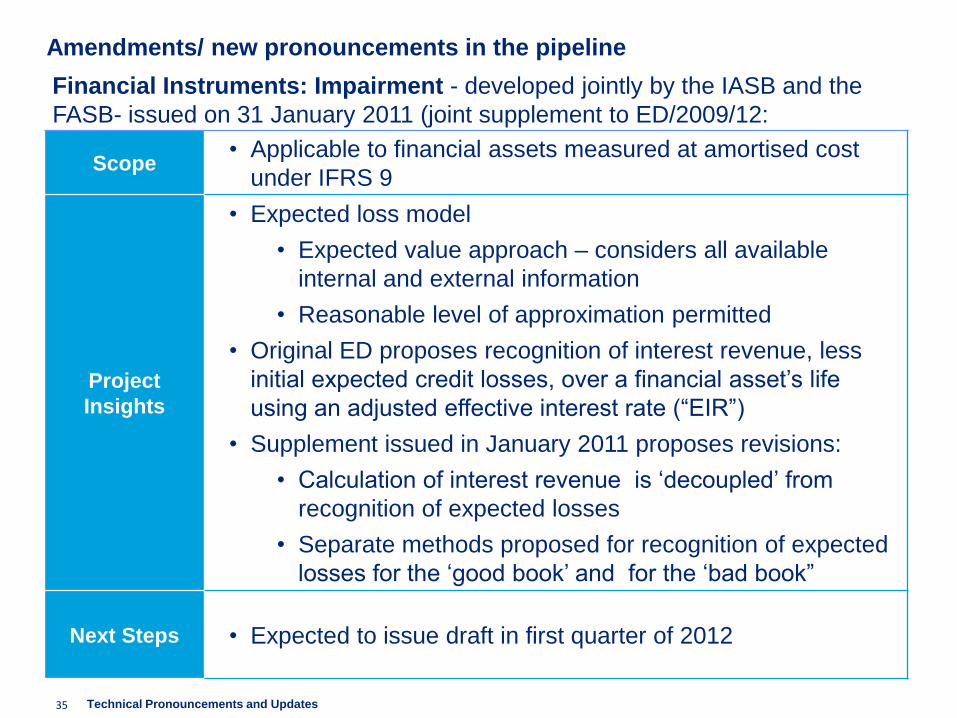

Scope• Applicable to financial assets measured at amortised cost

under IFRS 9

Project

Insights

• Expected loss model

• Expected value approach – considers all available

internal and external information

• Reasonable level of approximation permitted

• Original ED proposes recognition of interest revenue, less

initial expected credit losses, over a financial asset‟s life

using an adjusted effective interest rate (“EIR”)

• Supplement issued in January 2011 proposes revisions:

• Calculation of interest revenue is „decoupled‟ from

recognition of expected losses

• Separate methods proposed for recognition of expected

losses for the „good book‟ and for the „bad book”

Next Steps • Expected to issue draft in first quarter of 2012

35

Financial Instruments: Impairment - developed jointly by the IASB and the

FASB- issued on 31 January 2011 (joint supplement to ED/2009/12:

Technical Pronouncements and Updates

Amendments/ new pronouncements in the pipeline

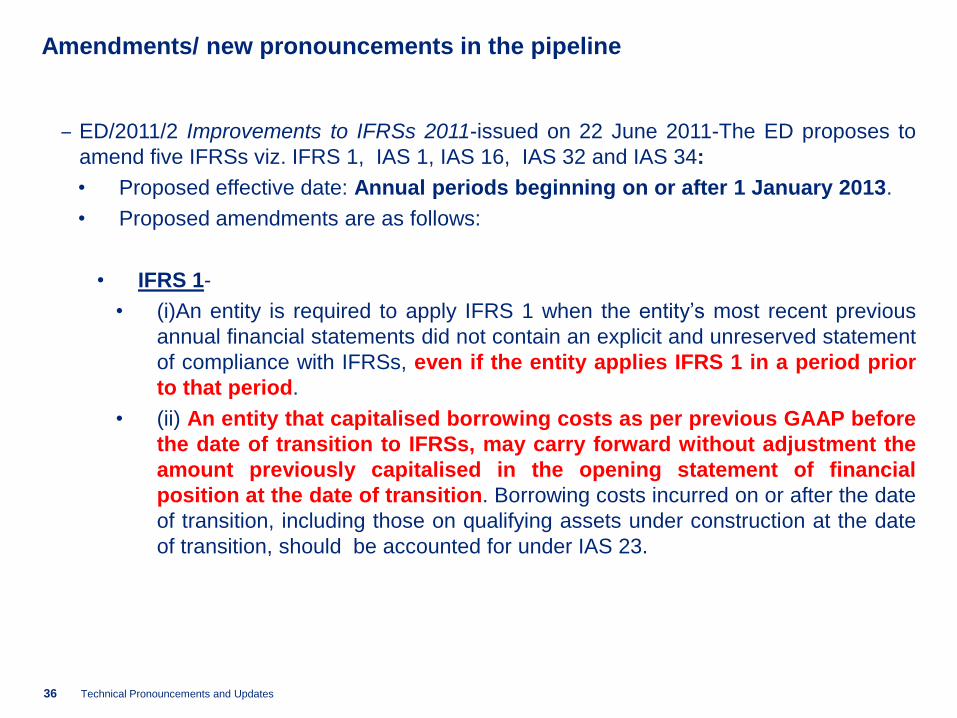

‒ ED/2011/2 Improvements to IFRSs 2011-issued on 22 June 2011-The ED proposes to

amend five IFRSs viz. IFRS 1, IAS 1, IAS 16, IAS 32 and IAS 34:

• Proposed effective date: Annual periods beginning on or after 1 January 2013.

• Proposed amendments are as follows:

• IFRS 1-

• (i)An entity is required to apply IFRS 1 when the entity‟s most recent previous

annual financial statements did not contain an explicit and unreserved statement

of compliance with IFRSs, even if the entity applies IFRS 1 in a period prior

to that period.

• (ii) An entity that capitalised borrowing costs as per previous GAAP before

the date of transition to IFRSs, may carry forward without adjustment the

amount previously capitalised in the opening statement of financial

position at the date of transition. Borrowing costs incurred on or after the date

of transition, including those on qualifying assets under construction at the date

of transition, should be accounted for under IAS 23.

36 Technical Pronouncements and Updates

Amendments/ new pronouncements in the pipeline

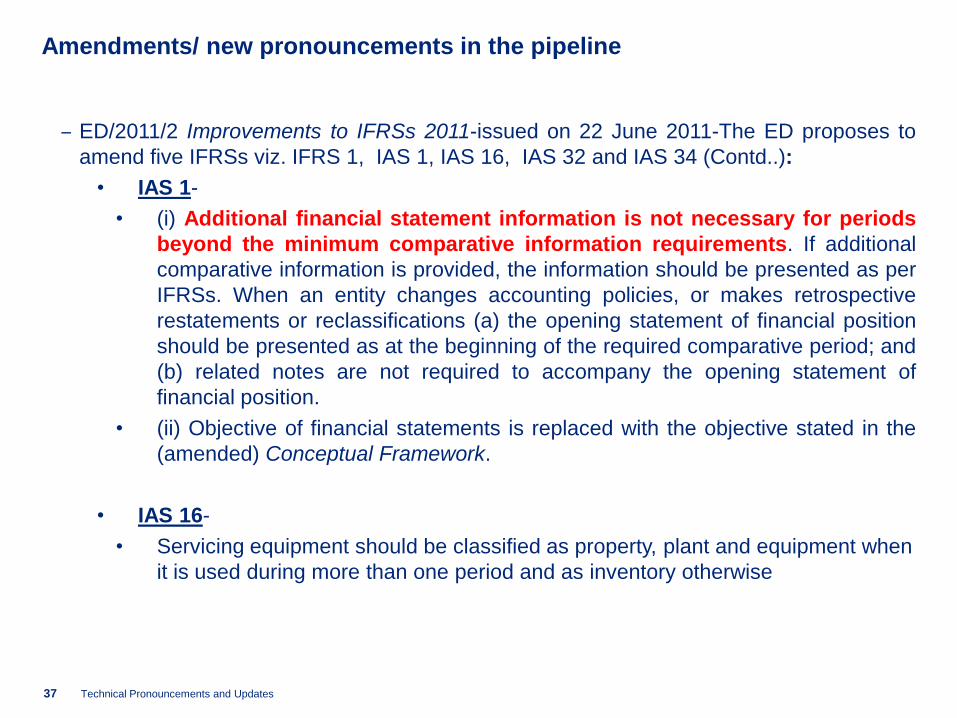

‒ ED/2011/2 Improvements to IFRSs 2011-issued on 22 June 2011-The ED proposes to

amend five IFRSs viz. IFRS 1, IAS 1, IAS 16, IAS 32 and IAS 34 (Contd..):

• IAS 1-

• (i) Additional financial statement information is not necessary for periods

beyond the minimum comparative information requirements. If additional

comparative information is provided, the information should be presented as per

IFRSs. When an entity changes accounting policies, or makes retrospective

restatements or reclassifications (a) the opening statement of financial position

should be presented as at the beginning of the required comparative period; and

(b) related notes are not required to accompany the opening statement of

financial position.

• (ii) Objective of financial statements is replaced with the objective stated in the

(amended) Conceptual Framework.

• IAS 16-

• Servicing equipment should be classified as property, plant and equipment when

it is used during more than one period and as inventory otherwise

37 Technical Pronouncements and Updates

Amendments/ new pronouncements in the pipeline

‒ ED/2011/2 Improvements to IFRSs 2011-issued on 22 June 2011-The ED proposes to

amend five IFRSs viz. IFRS 1, IAS 1, IAS 16, IAS 32 and IAS 34 (Contd..):

• IAS 32-

• Income-tax relating to distributions to holders of an equity instrument and

Income-tax relating to transaction costs of an equity transaction should be

accounted for as per IAS 12.

• IAS 34-

• In interim financial reports, total assets for a particular reportable segment

would be disclosed only when the amounts are regularly provided to the chief

operating decision maker and there has been a material change in the total

assets for that segment from the amount disclosed in the last annual financial

statements

38 Technical Pronouncements and Updates

Amendments/ new pronouncements in the pipeline

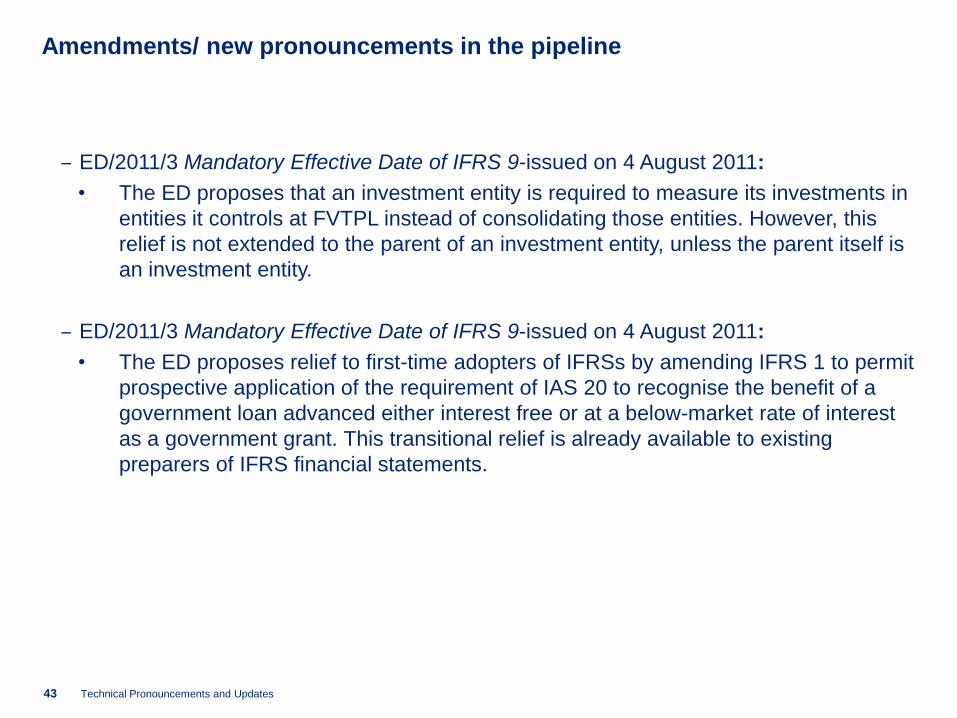

‒ ED/2011/3 Mandatory Effective Date of IFRS 9-issued on 4 August 2011:

• The ED proposes to defer the mandatory effective date of both the 2009 and 2010

versions of IFRS 9 to annual periods beginning on or after 1 January 2015 (from the

existing date of 1 January 2013) with early application permitted.

‒ ED/2011/3 Mandatory Effective Date of IFRS 9-issued on 4 August 2011:

• The ED proposes that an investment entity is required to measure its investments in

entities it controls at FVTPL instead of consolidating those entities. However, this

relief is not extended to the parent of an investment entity, unless the parent itself is

an investment entity.

‒ ED/2011/3 Mandatory Effective Date of IFRS 9-issued on 4 August 2011:

• The ED proposes relief to first-time adopters of IFRSs by amending IFRS 1 to permit

prospective application of the requirement of IAS 20 to recognise the benefit of a

government loan advanced either interest free or at a below-market rate of interest

as a government grant. This transitional relief is already available to existing

preparers of IFRS financial statements.

39 Technical Pronouncements and Updates

Amendments/ new pronouncements in the pipeline

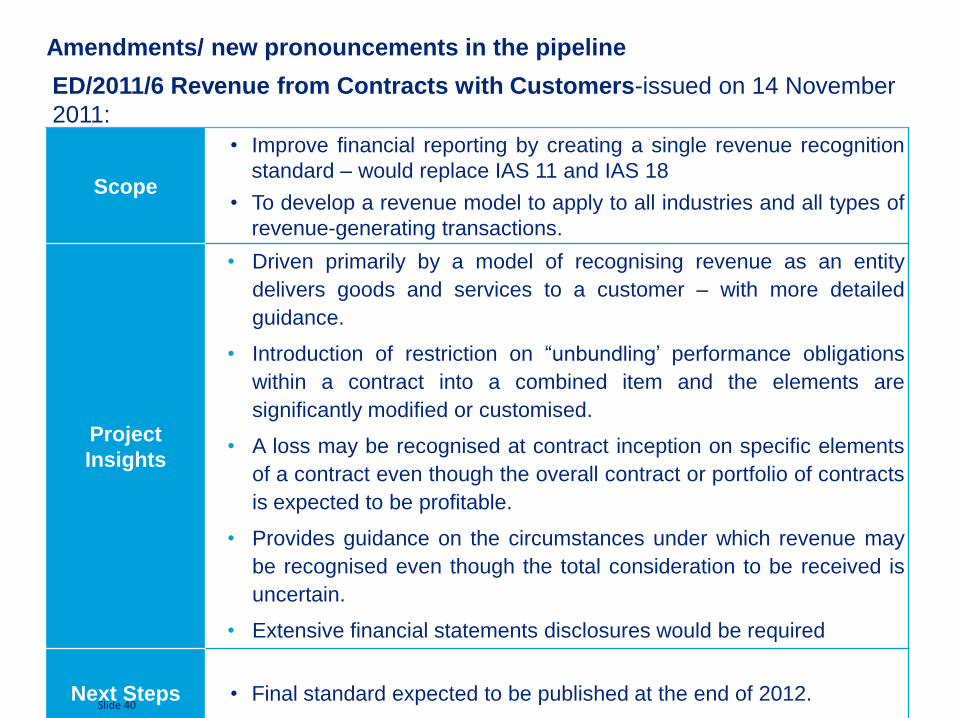

Scope

• Improve financial reporting by creating a single revenue recognition

standard – would replace IAS 11 and IAS 18

• To develop a revenue model to apply to all industries and all types of

revenue-generating transactions.

Project

Insights

• Driven primarily by a model of recognising revenue as an entity

delivers goods and services to a customer – with more detailed

guidance.

• Introduction of restriction on “unbundling‟ performance obligations

within a contract into a combined item and the elements are

significantly modified or customised.

• A loss may be recognised at contract inception on specific elements

of a contract even though the overall contract or portfolio of contracts

is expected to be profitable.

• Provides guidance on the circumstances under which revenue may

be recognised even though the total consideration to be received is

uncertain.

• Extensive financial statements disclosures would be required

Next Steps • Final standard expected to be published at the end of 2012.Slide 40

ED/2011/6 Revenue from Contracts with Customers-issued on 14 November

2011:

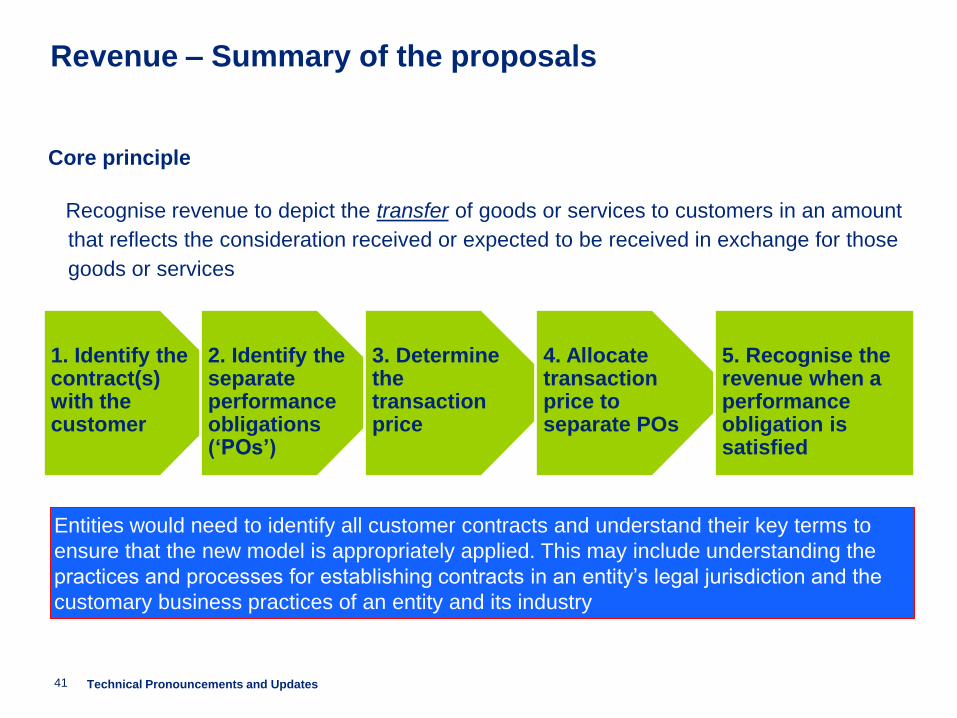

Core principle

Recognise revenue to depict the transfer of goods or services to customers in an amount

that reflects the consideration received or expected to be received in exchange for those

goods or services

41

Revenue – Summary of the proposals

1. Identify the contract(s) with the customer

2. Identify the separate performance obligations („POs‟)

3. Determine the transaction price

4. Allocate transaction price to separate POs

5. Recognise the revenue when a performance obligation is satisfied

Entities would need to identify all customer contracts and understand their key terms to

ensure that the new model is appropriately applied. This may include understanding the

practices and processes for establishing contracts in an entity‟s legal jurisdiction and the

customary business practices of an entity and its industry

Technical Pronouncements and Updates

Amendments/ new pronouncements in the pipeline

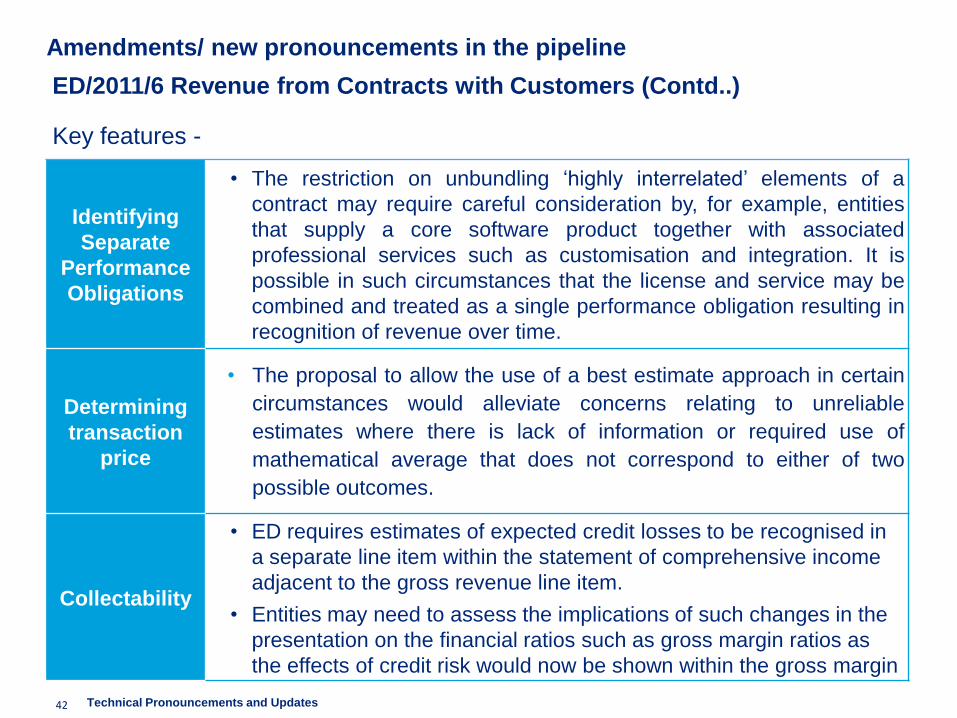

Identifying

Separate

Performance

Obligations

• The restriction on unbundling „highly interrelated‟ elements of a

contract may require careful consideration by, for example, entities

that supply a core software product together with associated

professional services such as customisation and integration. It is

possible in such circumstances that the license and service may be

combined and treated as a single performance obligation resulting in

recognition of revenue over time.

Determining

transaction

price

• The proposal to allow the use of a best estimate approach in certain

circumstances would alleviate concerns relating to unreliable

estimates where there is lack of information or required use of

mathematical average that does not correspond to either of two

possible outcomes.

Collectability

• ED requires estimates of expected credit losses to be recognised in

a separate line item within the statement of comprehensive income

adjacent to the gross revenue line item.

• Entities may need to assess the implications of such changes in the

presentation on the financial ratios such as gross margin ratios as

the effects of credit risk would now be shown within the gross margin

42

ED/2011/6 Revenue from Contracts with Customers (Contd..)

Key features -

Technical Pronouncements and Updates

Amendments/ new pronouncements in the pipeline

‒ ED/2011/3 Mandatory Effective Date of IFRS 9-issued on 4 August 2011:

• The ED proposes that an investment entity is required to measure its investments in

entities it controls at FVTPL instead of consolidating those entities. However, this

relief is not extended to the parent of an investment entity, unless the parent itself is

an investment entity.

‒ ED/2011/3 Mandatory Effective Date of IFRS 9-issued on 4 August 2011:

• The ED proposes relief to first-time adopters of IFRSs by amending IFRS 1 to permit

prospective application of the requirement of IAS 20 to recognise the benefit of a

government loan advanced either interest free or at a below-market rate of interest

as a government grant. This transitional relief is already available to existing

preparers of IFRS financial statements.

43 Technical Pronouncements and Updates

44 Deloitte PowerPoint timesaver – August 2011

Changes to the Framework

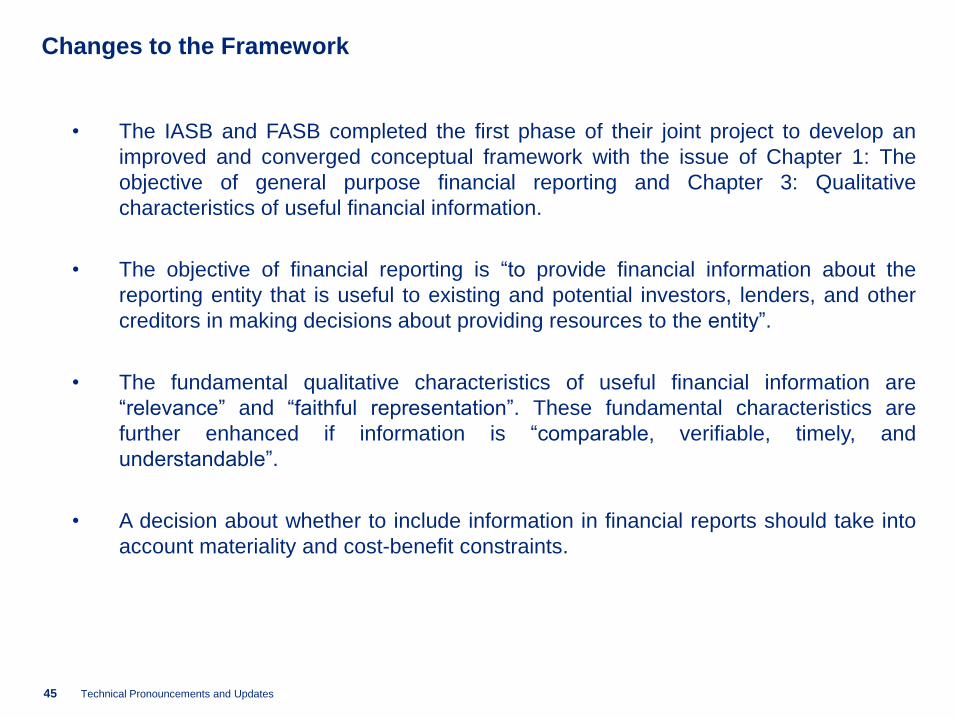

Changes to the Framework

• The IASB and FASB completed the first phase of their joint project to develop an

improved and converged conceptual framework with the issue of Chapter 1: The

objective of general purpose financial reporting and Chapter 3: Qualitative

characteristics of useful financial information.

• The objective of financial reporting is “to provide financial information about the

reporting entity that is useful to existing and potential investors, lenders, and other

creditors in making decisions about providing resources to the entity”.

• The fundamental qualitative characteristics of useful financial information are

“relevance” and “faithful representation”. These fundamental characteristics are

further enhanced if information is “comparable, verifiable, timely, and

understandable”.

• A decision about whether to include information in financial reports should take into

account materiality and cost-benefit constraints.

45 Technical Pronouncements and Updates

46 Deloitte PowerPoint timesaver – August 2011

Research and Other Projects

Research and Other Projects

‒ Conceptual Framework: The Board completed Phase A by publishing in September

2010 the Objectives and Qualitative characteristics chapters of the new Conceptual

Framework. The IASB and the FASB will amend sections of their conceptual frameworks

as they complete individual phases of the project. The boards have considered the

comments they received on the exposure draft for Phase D Reporting Entity. In the light

of those comments the boards have decided that they will need more time to finalise this

chapter than they initially anticipated. The boards have not yet published discussion

papers for Phase B Elements or Phase C Measurement. The IASB expects to

recommence development of the Conceptual Framework at the beginning of 2012.

‒ Agriculture, particularly bearer biological assets: a future project could be a limited-

scope improvement to IAS 41.

‒ Country-by-country reporting - In October 2010, the European Commission published

a questionnaire to gather views on reporting on a country-by-country basis by multi-

national entities. A future project could consider whether a similar requirement should

also be included in IFRSs, including consideration of whether such a requirement should

apply to entities in all industries or only to selected industries

‒ Discount rate - Various accounting measurements involve estimates of discounted cash

flows. IFRSs use a variety of discount rates. That variation arises because different

standards have different measurement objectives and were developed at different times.

A future project could aim to provide more consistent guidance on how to determine

discount rates.

47 Technical Pronouncements and Updates

Research and Other Projects

‒ Equity method of accounting-The application of the equity method of accounting can

be complex in some circumstances. Complexities include the calculation of goodwill, the

partial elimination of profits on upstream and downstream transactions, and the

measurement of impairment. Some have questioned the appropriateness of the use of

the equity method and challenged whether it should be permitted, whereas others have

argued for the extension of the use of equity accounting to separate financial

statements.

A future project could reconsider when the equity method of accounting is appropriate

and, if so, whether it could be simplified. Alternatively a future project could be of more

limited scope focusing only on clarifying and/or simplifying the application of the equity

method of accounting

‒ Foreign currency translation-The existing IFRS on foreign exchange (IAS 21 The

Effects of Changes in Foreign Exchange Rates) is based on the US standard. Some

have criticised IAS 21 as designed for companies that operate in a reserve currency.

Recent volatility in exchange rates, especially in emerging economies, has led some to

ask that this standard be reconsidered. At the Board‟s request, a group of national

standard-setters led by the Korea Accounting Standards Board has been exploring this

issue. In particular, they are considering whether the project should be limited to narrow

implementation issues or should address questions of currency accounting more

generally. They are also considering whether a project should be limited to the scope of

IAS 21, or should address other situations in which exchange rates interact with other

IFRSs.48 Technical Pronouncements and Updates

Research and Other Projects

‒ Inflation accounting (revisions to IAS 29 Financial Reporting in Hyperinflationary

Economies)-IAS 29 provides guidance on the preparation of financial statements in a

functional currency that is suffering from hyperinflation. Concerns have been raised from

some countries whose economies suffer from high inflation, but which are not

hyperinflationary. Those concerns are that the effects of high inflation on an entity‟s

financial results are not adequately reflected in IFRS financial statements. A research

paper was prepared on this issue and submitted to the IASB by the Federación

Argentina de Consejos Profesionales de Ciencias Económicas. A future project could

use this research paper to consider revisions to IAS 29 to include guidance for entities

whose functional currency is that of an economy subject to high inflation, but not to

hyperinflation

‒ Interim reporting-IFRSs do not require entities to prepare interim financial reports, but

guidance is provided in IAS 34 Interim Financial Reporting on how an entity should

prepare such a report. The objective of the current standard is that the frequency of

reporting should not affect the measurement of the annual financial statements.

However, there can be tensions between this objective and the requirement to apply a

discrete accounting period approach in the preparation of interim financial reports.

Associated with this is the question of whether full remeasurement of assets and

liabilities is required at each interim reporting date. For example, should the defined

benefit obligation of a defined benefit pension plan be remeasured at each interim date

in the same level of detail as at the end of the financial year? A future project could

consider what improvements should be made to overcome these issues.49 Technical Pronouncements and Updates

Research and Other Projects

‒ Islamic (Shariah-compliant) transactions and instruments-Modern Islamic finance

emerged from a belief that conventional forms of financing may contain elements

prohibited by Shariah. As an alternative, a myriad of Islamic financial transactions have

been developed on the basis of a combination of classical trade-based contracts and

other accompanying arrangements. These products are considered to be in compliance

with Shariah precepts, yet provide some level of economic parity with comparable forms

of conventional financing. Some stakeholders have asked the IASB to investigate

whether, and if so how, financial reporting guidance for these transactions and

instruments can be incorporated into IFRSs. The IASB staff are currently researching

both the issues involved and possible approaches that the IASB might take. The

Malaysian Accounting Standards Board and others have been especially helpful in this

effort. The IASB would need to enlist the help of those knowledgeable in both Shariah

precepts and the structure of these transactions to a much greater degree than for other

IASB projects

‒ Other comprehensive income-An important issue raised by many respondents to

various IASB proposals in various projects is how to determine which items of income

and expense and gains and losses should be included in profit or loss or in other

comprehensive income, and whether items included in other comprehensive income

should subsequently be recycled to profit or loss and, if so, on what basis. A future

project could consider the conceptual and the practical issues associated with other

comprehensive income including how the issue cuts across existing IFRSs.

50 Technical Pronouncements and Updates

51 Deloitte PowerPoint timesaver – August 2011

Indian GAAP

Changes under Indian GAAP - Amendments

‒ IND AS converged with IFRSs were released by MCA. Effective dates yet to be notified.

‒ MCA has issued Companies (Accounting Standards) Amendment Rules, 2011 extending

the date up to which exchange differences on long-term monetary items can be deferred

(optional treatment permitted under para 46 of AS 11) as 31 March 2012 from the

existing date of 31 March 2011.

52 Technical Pronouncements and Updates

Changes under Indian GAAP – Amendments in Pipeline

‒ The following exposure drafts are current:

ED of Taxonomy for Non-Banking Financial Companies (NBFCs) has been hosted in ICAI‟s

website on 27-07-2011

ED of Ind AS 111 Joint Arrangements - no

ED of Ind AS 27 (as amended) Separate Financial Statements

ED of Ind AS 28 (as amended) Investments in Associates and Joint Ventures

ED of Ind AS 110 Consolidated Financial Statements - no

ED of Ind AS 112 Disclosure of Interests in Other Entities - no

ED of Ind AS 41 Agriculture

ED of Ind AS 19 (as amended) Employee Benefits – difference only in rate to be used to discount

post-employment benefit

ED of amendments to Ind AS 12 Income Taxes

ED of amendments to Ind AS 107 Financial Instruments: Disclosures

ED of amendments to Ind AS 1 The Presentation of Financial Statements

ED of amendments to Ind AS 101 First-time Adoption of Indian Accounting Standards

ED of Ind AS 113 Fair Value Measurement

ED of Guidance Note on Recognition of Revenue by Real Estate Developers (by ASB of ICAI)

ED of Guidance Note to Revised Schedule VI (by Corporate Laws and Corporate Governance

Committee of ICAI)

53 Technical Pronouncements and Updates

Thank You