real estate

DESCRIPTION

Real Estate. Creating wealth with real estate. Homeownership has grown. Rent versus Buy. If you’re planning to move within five years, renting gives you more flexibility. - PowerPoint PPT PresentationTRANSCRIPT

1

Real Estate

Creating wealth with real estate

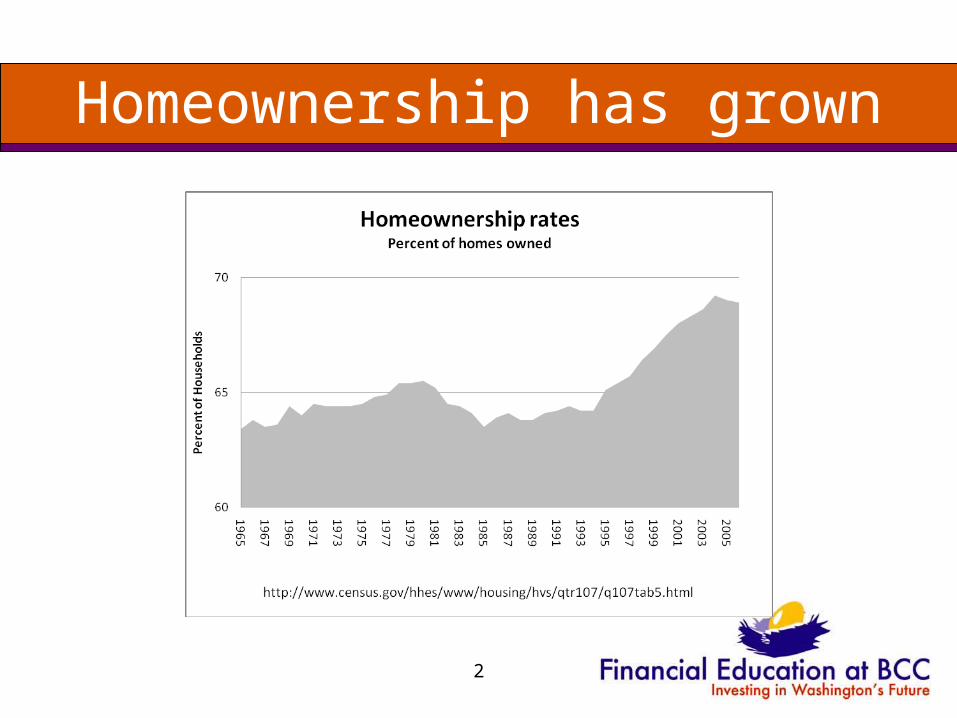

Homeownership has grown

2

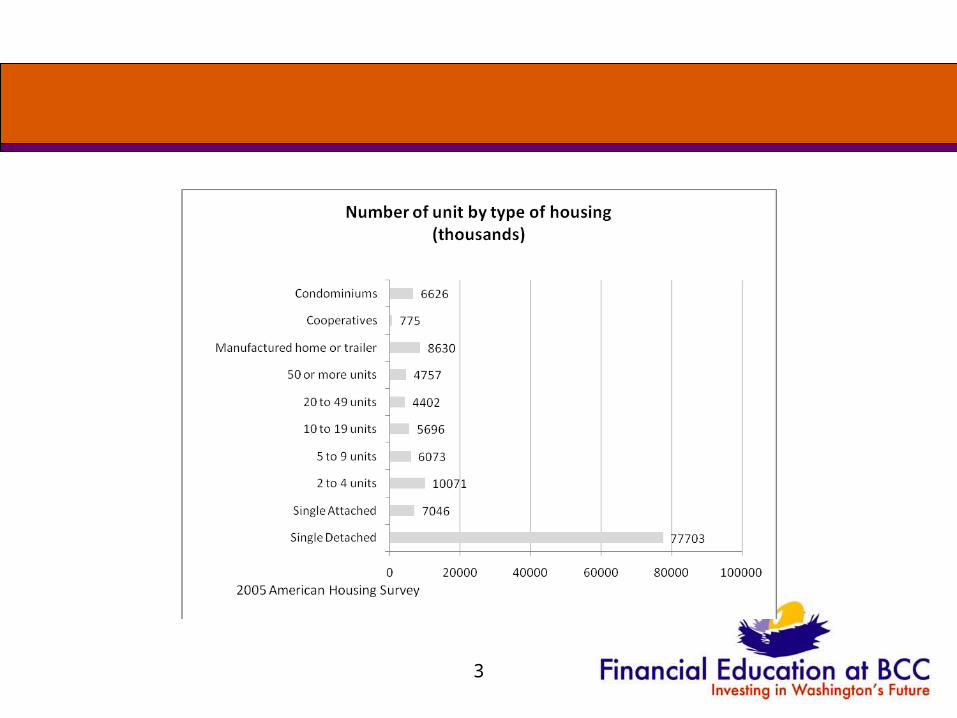

3

Rent versus Buy1. If you’re planning to move within five years, renting

gives you more flexibility.

2. If you’re uncertain about your present or near future financial circumstances, renting requires less financial commitment and risk.

3. If time does not permit you to look for the area you would be making such an investment into. You should research very carefully before you buy a house.

4. Renting often offers fewer responsibilities such as repairs, yard maintenance or needing to buy appliances, which could be expensive and take time.

4

Activity – Rent versus Buy

• Do a rent versus buy analysis using this calculator

• http://www.ginniemae.gov/rent_vs_buy/rent_vs_buy_calc.asp?Section=YPTH

•

5

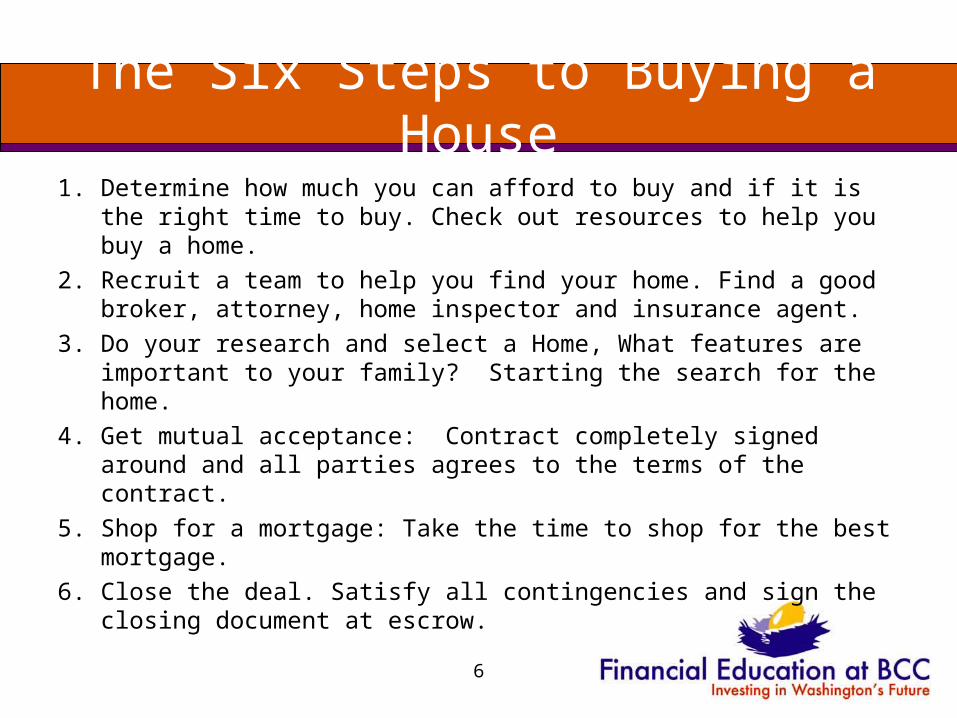

The Six Steps to Buying a House

1. Determine how much you can afford to buy and if it is the right time to buy. Check out resources to help you buy a home.

2. Recruit a team to help you find your home. Find a good broker, attorney, home inspector and insurance agent.

3. Do your research and select a Home, What features are important to your family? Starting the search for the home.

4. Get mutual acceptance: Contract completely signed around and all parties agrees to the terms of the contract.

5. Shop for a mortgage: Take the time to shop for the best mortgage.

6. Close the deal. Satisfy all contingencies and sign the closing document at escrow.

6

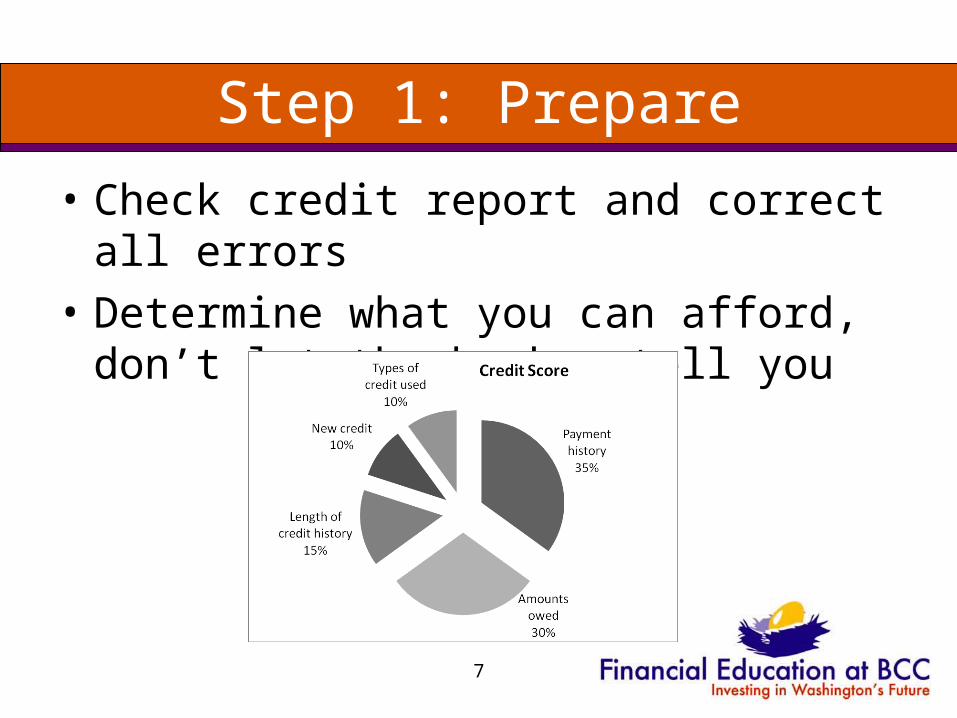

Step 1: Prepare

• Check credit report and correct all errors

• Determine what you can afford, don’t let the broker tell you

7

What can you afford?

• How affordable is the real estate in your area?

• National Association of Home Builders Housing Affordability Index measures the percentage of homes sold that a median income family could afford http://www.demographia.com/db-nahb0001.htm

8

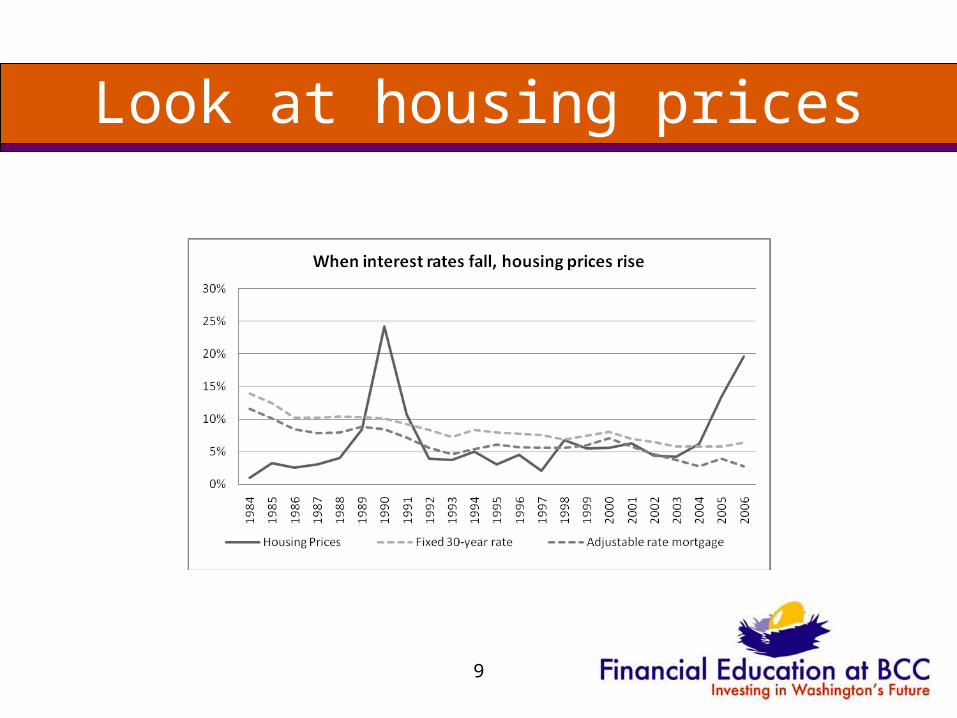

Look at housing prices

9

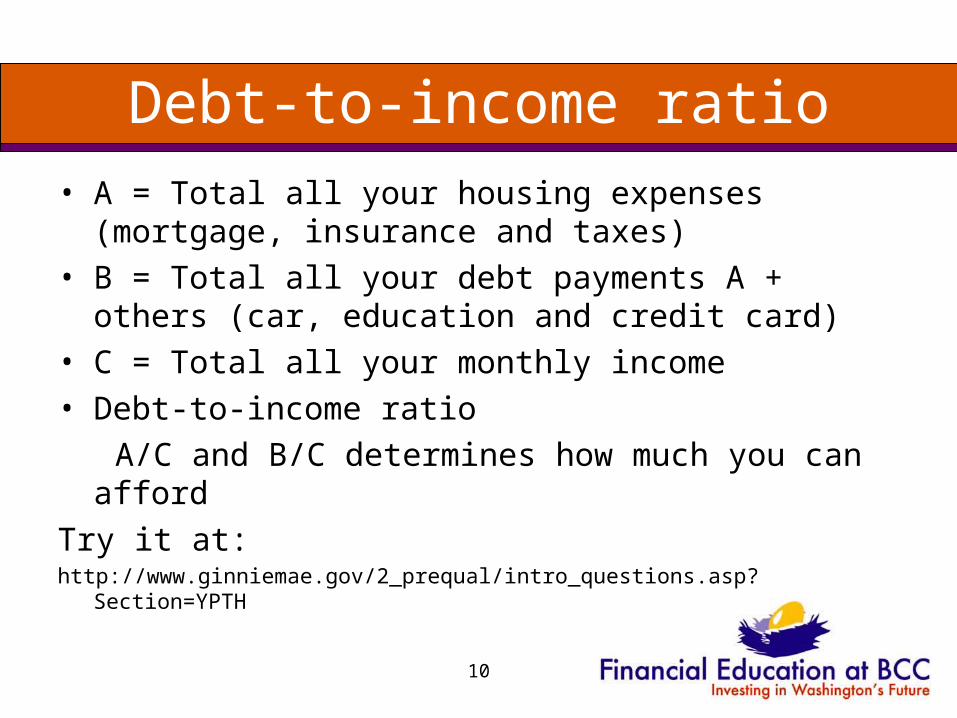

10

Debt-to-income ratio• A = Total all your housing expenses (mortgage,

insurance and taxes)• B = Total all your debt payments A + others (car,

education and credit card)• C = Total all your monthly income• Debt-to-income ratio

A/C and B/C determines how much you can afford

Try it at:http://www.ginniemae.gov/2_prequal/intro_questions.asp?Section=YPTH

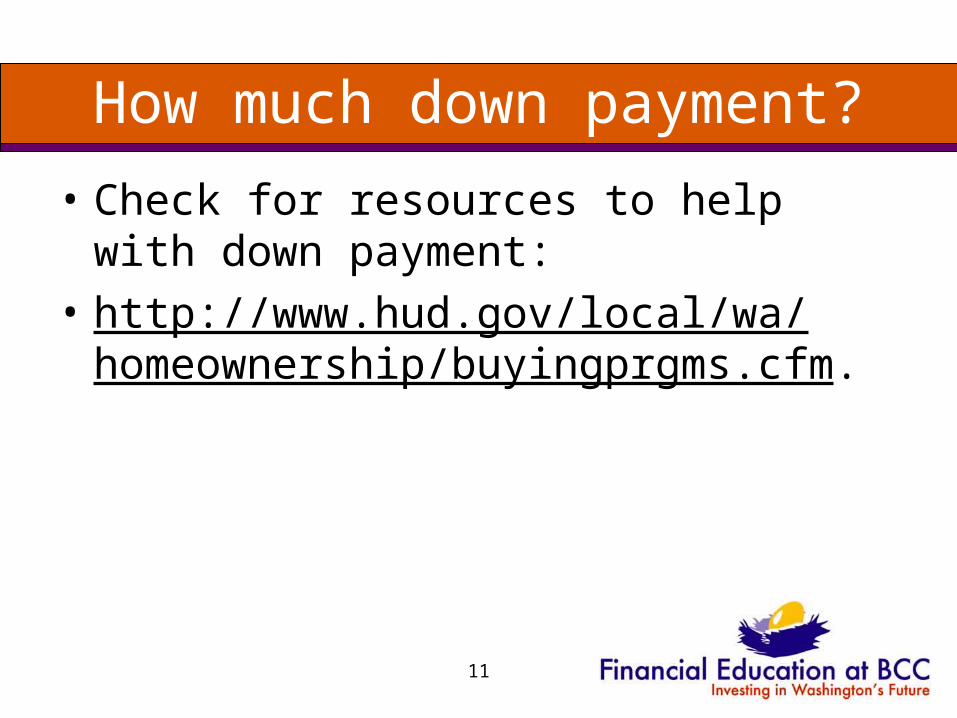

How much down payment?

• Check for resources to help with down payment:

• http://www.hud.gov/local/wa/homeownership/buyingprgms.cfm.

11

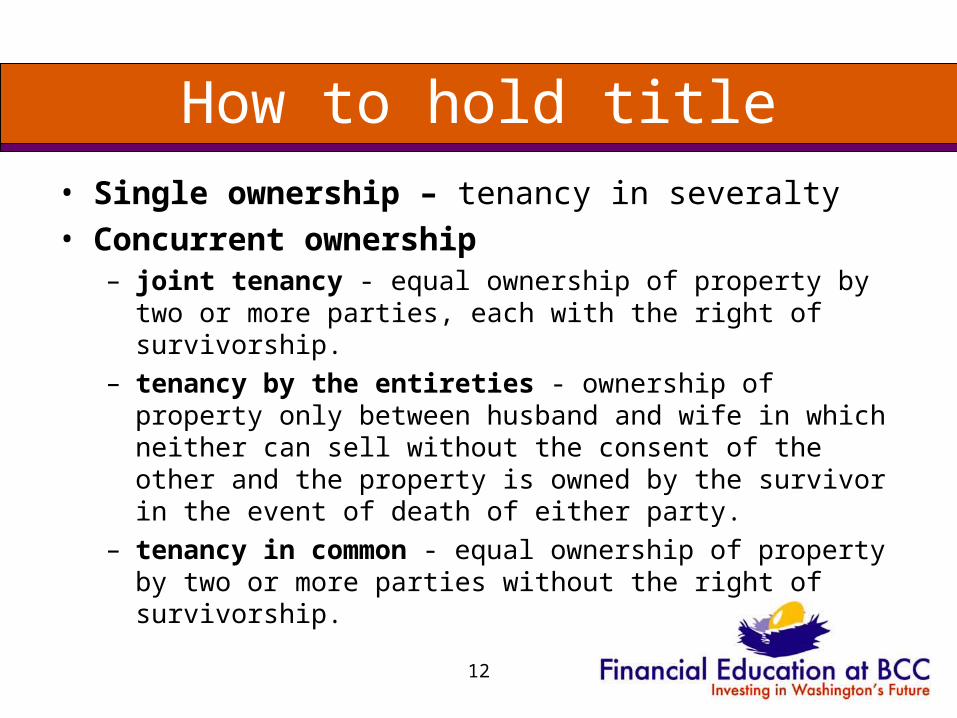

How to hold title• Single ownership – tenancy in severalty• Concurrent ownership

– joint tenancy - equal ownership of property by two or more parties, each with the right of survivorship.

– tenancy by the entireties - ownership of property only between husband and wife in which neither can sell without the consent of the other and the property is owned by the survivor in the event of death of either party.

– tenancy in common - equal ownership of property by two or more parties without the right of survivorship.

12

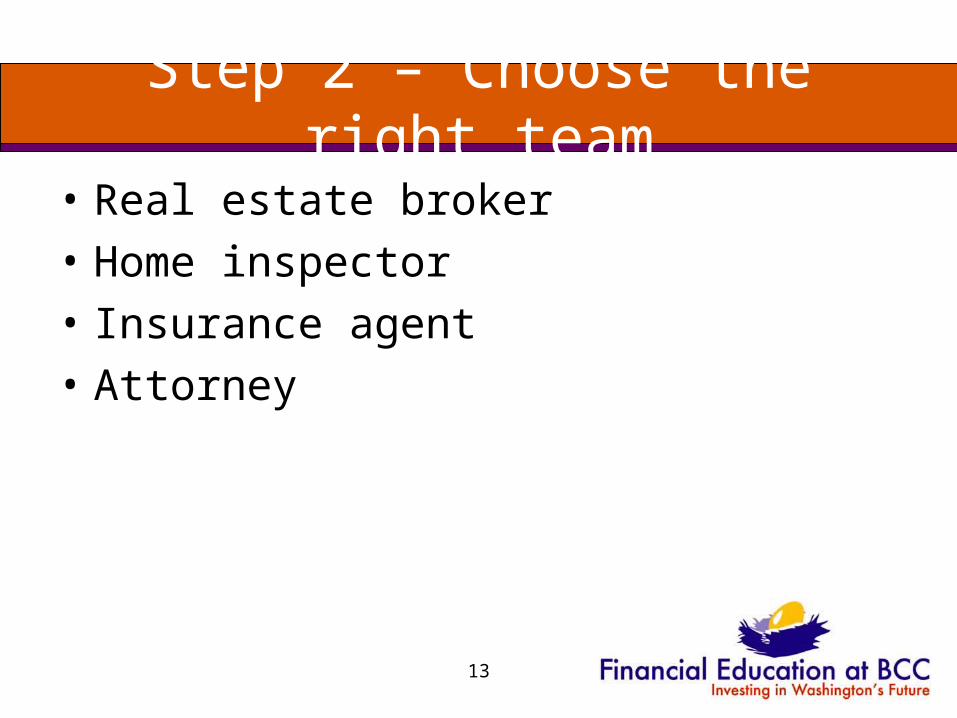

Step 2 – Choose the right team

• Real estate broker

• Home inspector

• Insurance agent

• Attorney

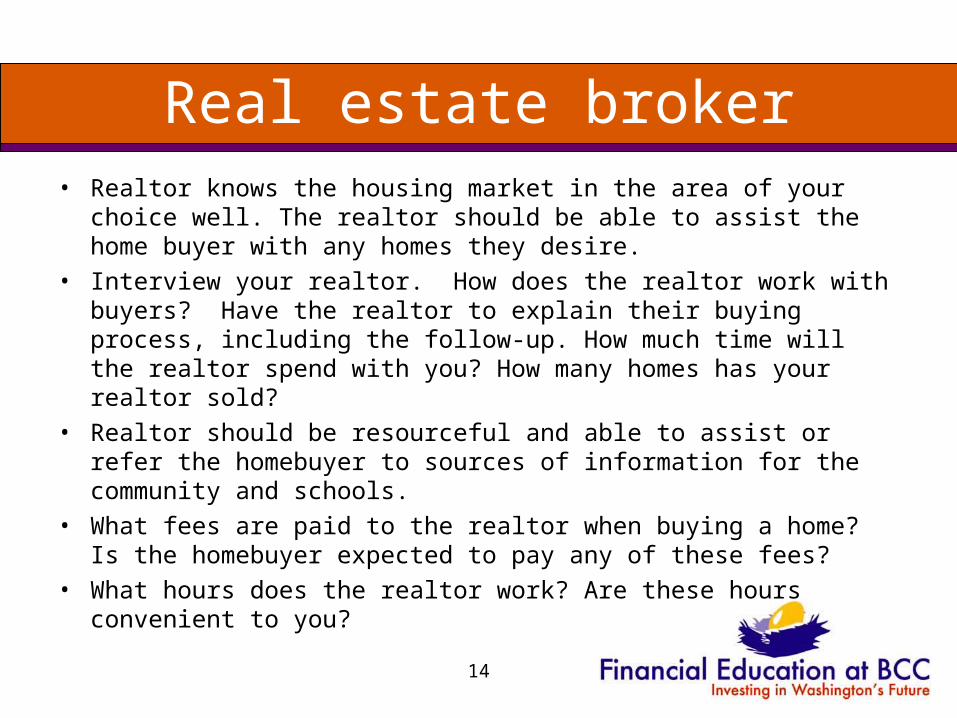

13

Real estate broker• Realtor knows the housing market in the area of your choice well.

The realtor should be able to assist the home buyer with any homes they desire.

• Interview your realtor. How does the realtor work with buyers? Have the realtor to explain their buying process, including the follow-up. How much time will the realtor spend with you? How many homes has your realtor sold?

• Realtor should be resourceful and able to assist or refer the homebuyer to sources of information for the community and schools.

• What fees are paid to the realtor when buying a home? Is the homebuyer expected to pay any of these fees?

• What hours does the realtor work? Are these hours convenient to you?

14

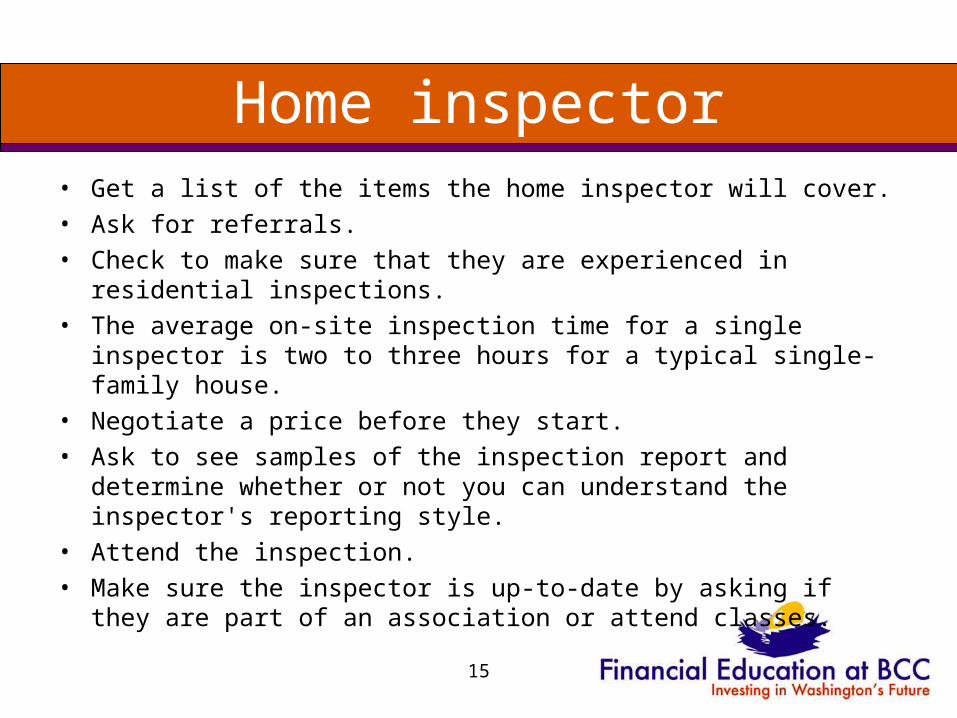

Home inspector• Get a list of the items the home inspector will cover.• Ask for referrals. • Check to make sure that they are experienced in residential

inspections. • The average on-site inspection time for a single inspector is two to

three hours for a typical single-family house. • Negotiate a price before they start. • Ask to see samples of the inspection report and determine whether

or not you can understand the inspector's reporting style. • Attend the inspection. • Make sure the inspector is up-to-date by asking if they are part of an

association or attend classes.

15

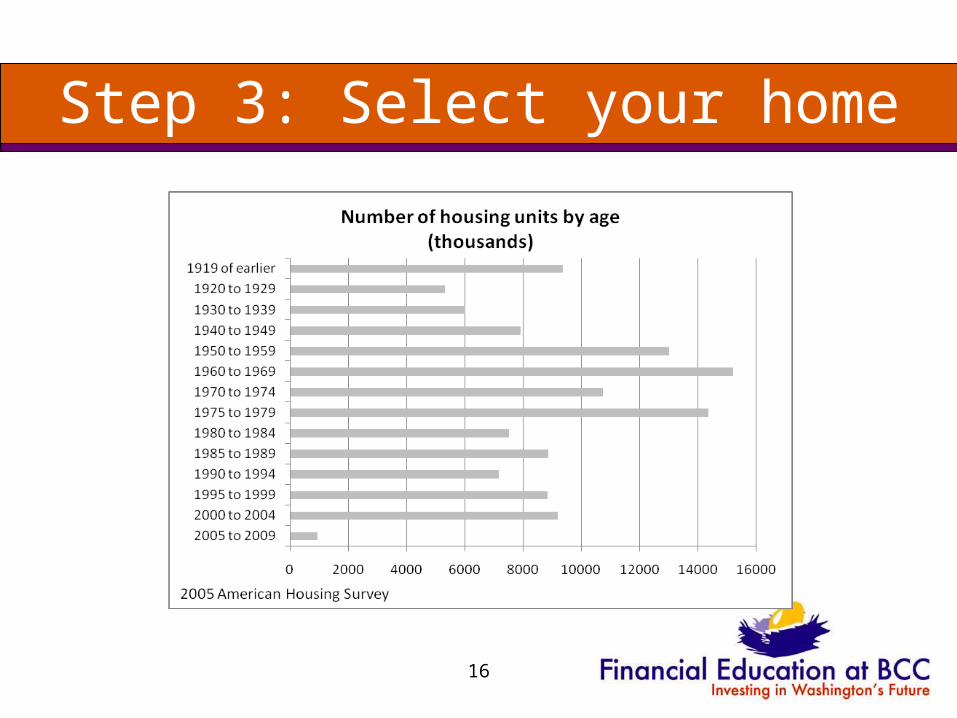

Step 3: Select your home

16

Factors

• Neighborhood – transportation, school, shopping, hospital, traffic, security, parking, etc.

• Price range• Type of home – style, age, condition, yard, etc.• Interior – bedrooms, bathrooms, flooring,

kitchen, living room, dining room, fireplace, workshop, in-law, etc.

17

Activity – Your dream home

• Using The Basics and Wishlist from the handouts, determine what kind of home you want to buy

18

Step 4: Making an offer and getting mutual acceptance

• Sales Price. For most home purchasers, the sales price is the most important term.

• Title. The seller should provide title, free and clear of all claims by others against your new home.

• Mortgage Clause. The agreement of sale should provide that your earnest money or “deposit” will be refunded if the sale has to be canceled because you are unable to get a mortgage loan.

• Pests. Your lender will require a certificate from a qualified inspector stating that the home is free from termites and other pests and pest damage.

• Home Inspection. An inspection will determine the condition of the plumbing, heating, cooling and electrical systems.

• Lead-Based Paint Hazards in Housing Built Before 1978. If you buy a home built before 1978, you have certain rights concerning lead-based paint and lead poisoning hazards.

• Other Environmental Concerns. Your city or state may have laws requiring buyers or sellers to test for environmental hazards such as leaking underground oil tanks, the presence of radon or asbestos, lead water pipes, and other such hazards, and to take the steps to clean-up any such hazards.

• Sharing of Expenses. You need to agree with the seller about how expenses related to the property such as taxes, water and sewer charges, condominium fees, and utility bills, are to be divided on the date of settlement.

19

Activity – Purchase Agreement

• Look at the purchase agreement and give factors that you should consider.

20

21

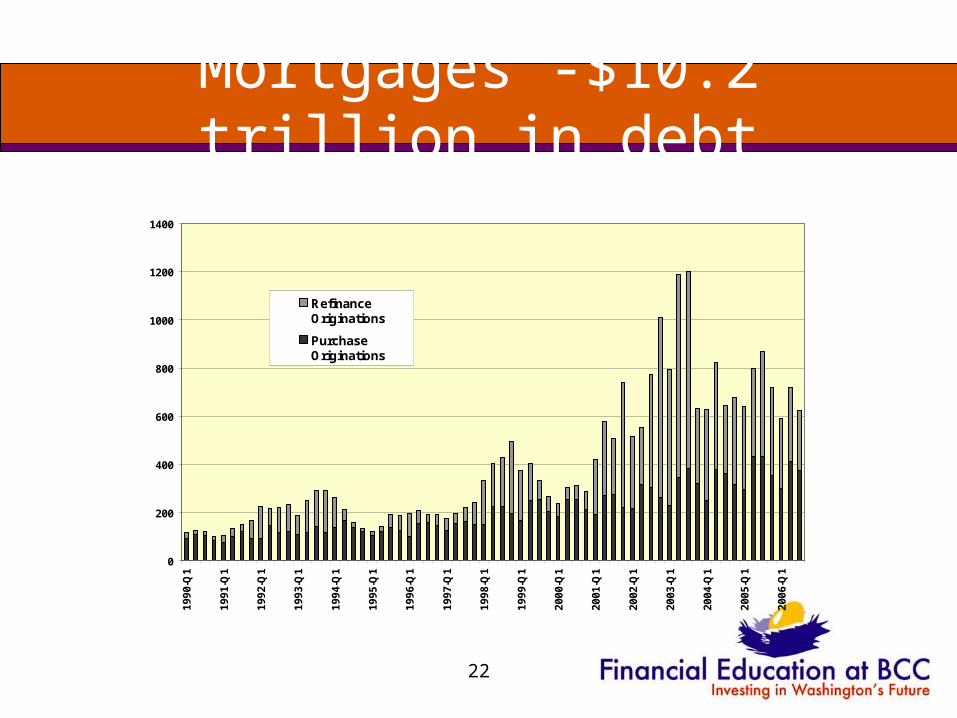

Step 5: Obtain a loan

The home is part of the American dream, but you can’t get one without a mortgage.

22

Mortgages -$10.2 trillion in debt

0

200

400

600

800

1000

1200

1400

19

90

-Q1

19

91

-Q1

19

92

-Q1

19

93

-Q1

19

94

-Q1

19

95

-Q1

19

96

-Q1

19

97

-Q1

19

98

-Q1

19

99

-Q1

20

00

-Q1

20

01

-Q1

20

02

-Q1

20

03

-Q1

20

04

-Q1

20

05

-Q1

20

06

-Q1

RefinanceOriginations

PurchaseOriginations

Source: Mortgage Bankers Association

Mortgages and Refinances($ billions)

23

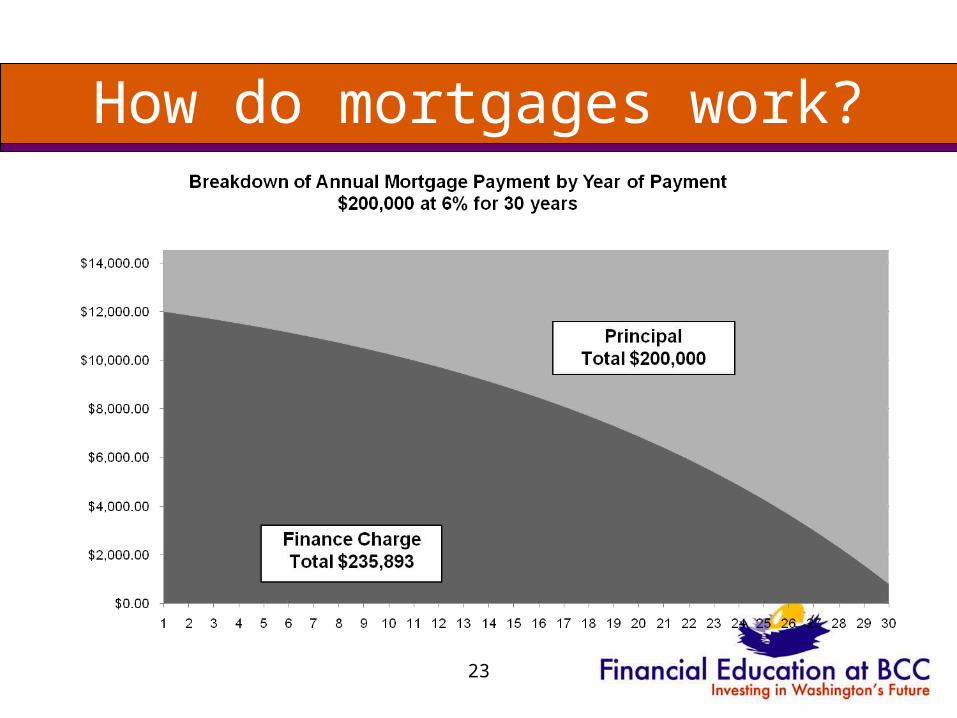

How do mortgages work?

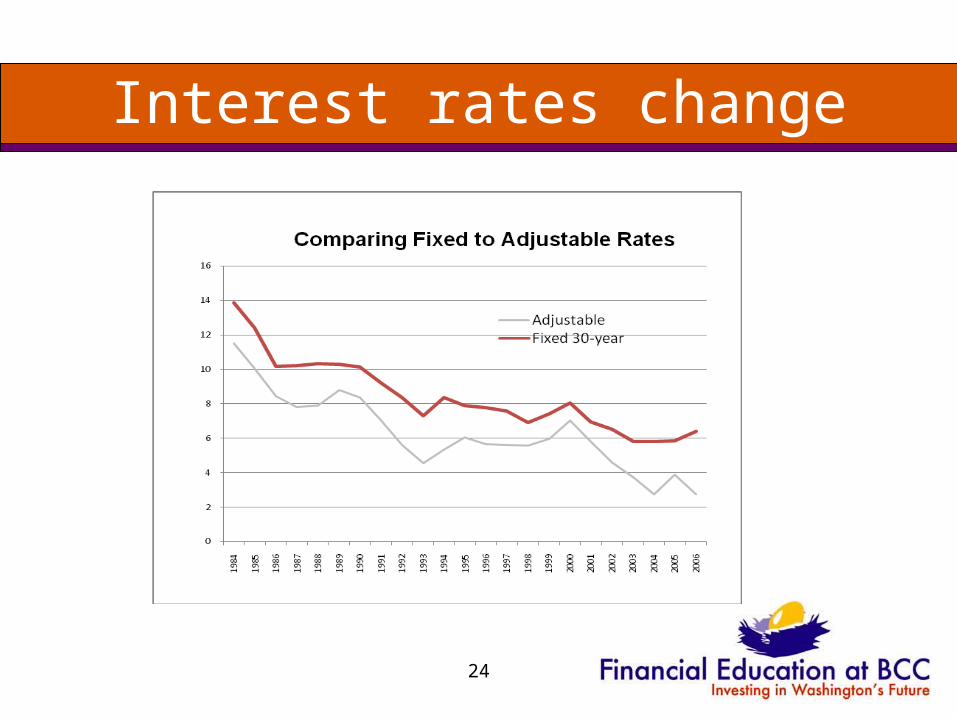

Interest rates change

24

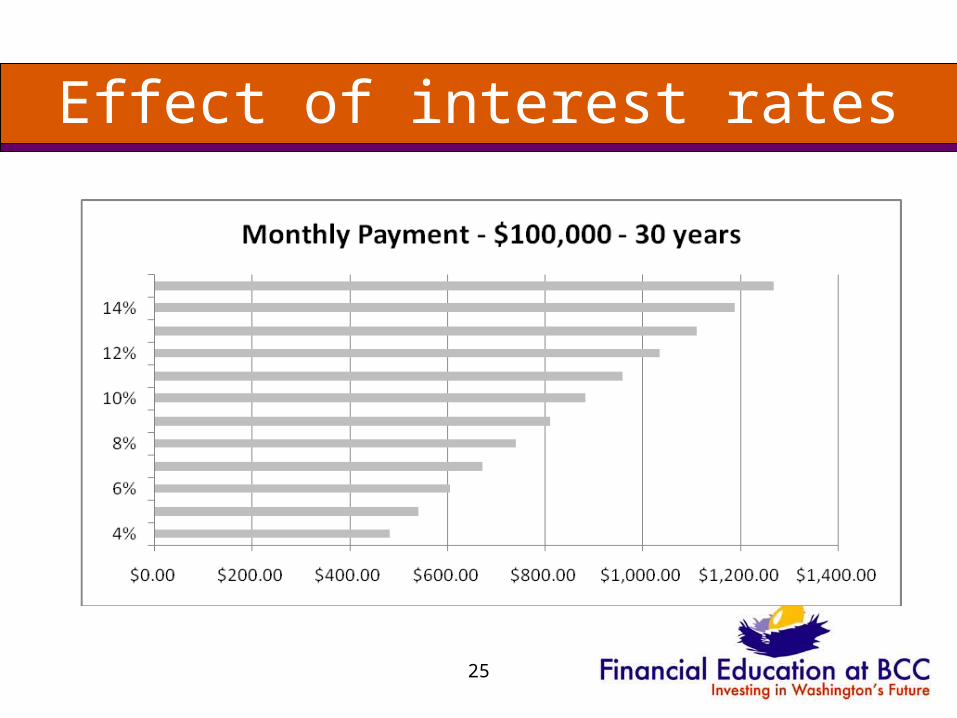

Effect of interest rates

25

26

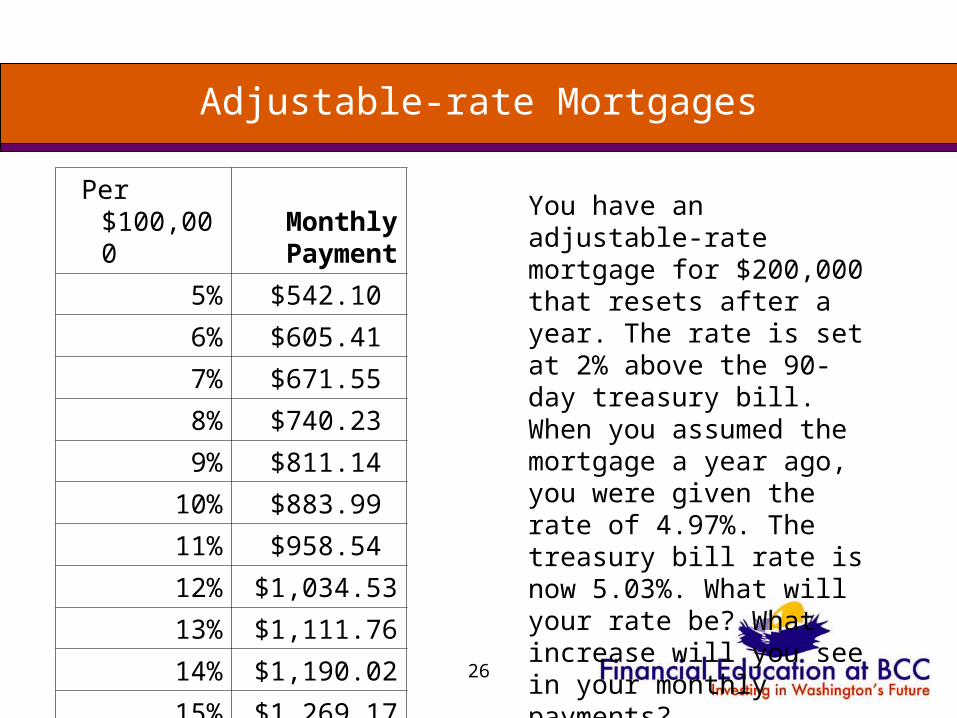

Adjustable-rate Mortgages

Per $100,000

Monthly Payment

5% $542.10

6% $605.41

7% $671.55

8% $740.23

9% $811.14

10% $883.99

11% $958.54

12% $1,034.53

13% $1,111.76

14% $1,190.02

15% $1,269.17

You have an adjustable-rate mortgage for $200,000 that resets after a year. The rate is set at 2% above the 90-day treasury bill. When you assumed the mortgage a year ago, you were given the rate of 4.97%. The treasury bill rate is now 5.03%. What will your rate be? What increase will you see in your monthly payments?

27

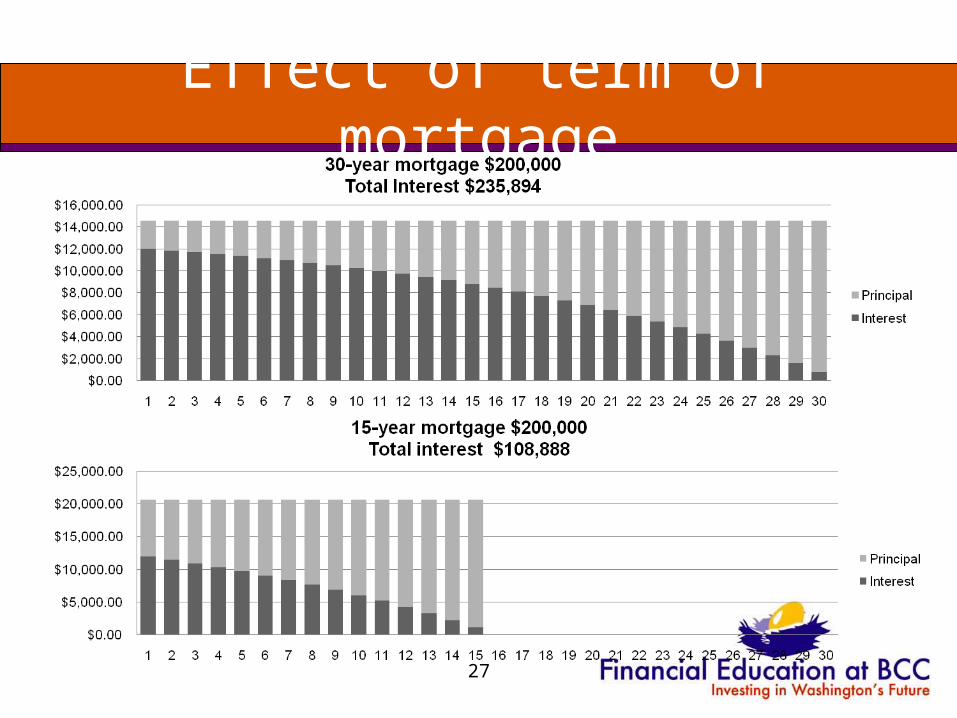

Effect of term of mortgage

28

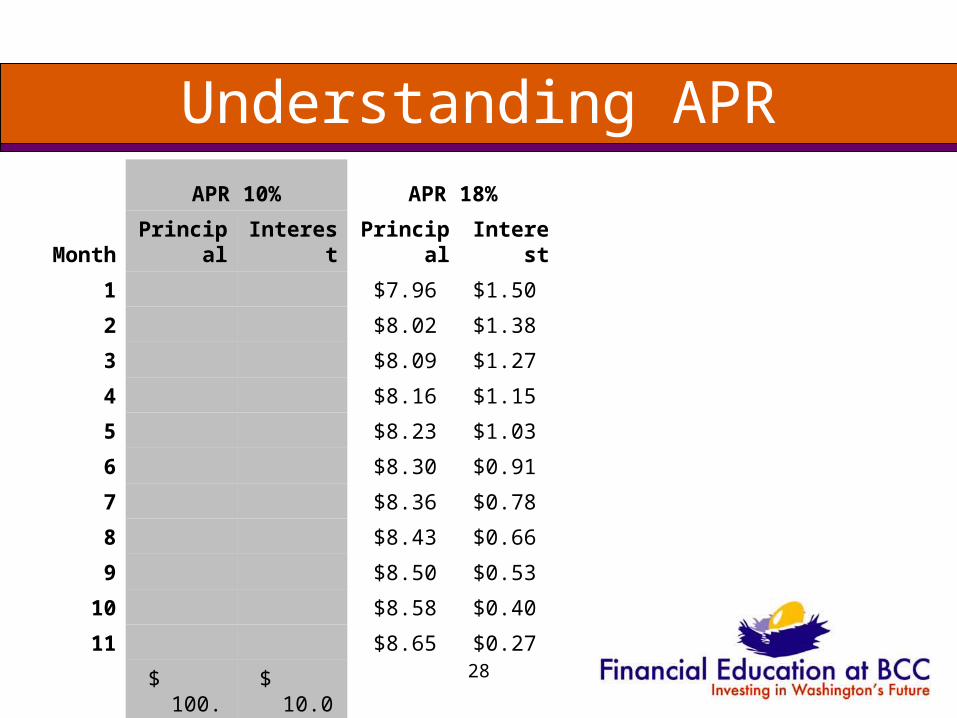

Understanding APRAPR 10% APR 18%

Month Principal Interest Principal Interest

1 $7.96 $1.50

2 $8.02 $1.38

3 $8.09 $1.27

4 $8.16 $1.15

5 $8.23 $1.03

6 $8.30 $0.91

7 $8.36 $0.78

8 $8.43 $0.66

9 $8.50 $0.53

10 $8.58 $0.40

11 $8.65 $0.27

12 $ 100.00 $ 10.00 $8.72 $0.14

$ 100.00 $ 10.00 $100.00 $10.02

29

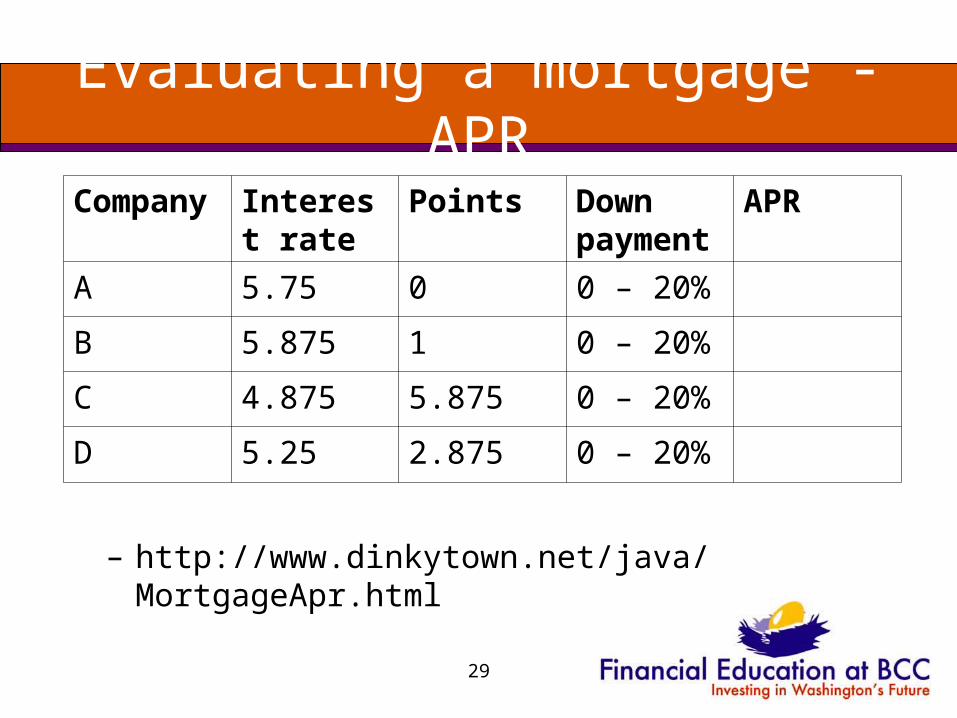

Evaluating a mortgage - APR

– http://www.dinkytown.net/java/MortgageApr.html

Company Interest rate

Points Down payment

APR

A 5.75 0 0 – 20%

B 5.875 1 0 – 20%

C 4.875 5.875 0 – 20%

D 5.25 2.875 0 – 20%

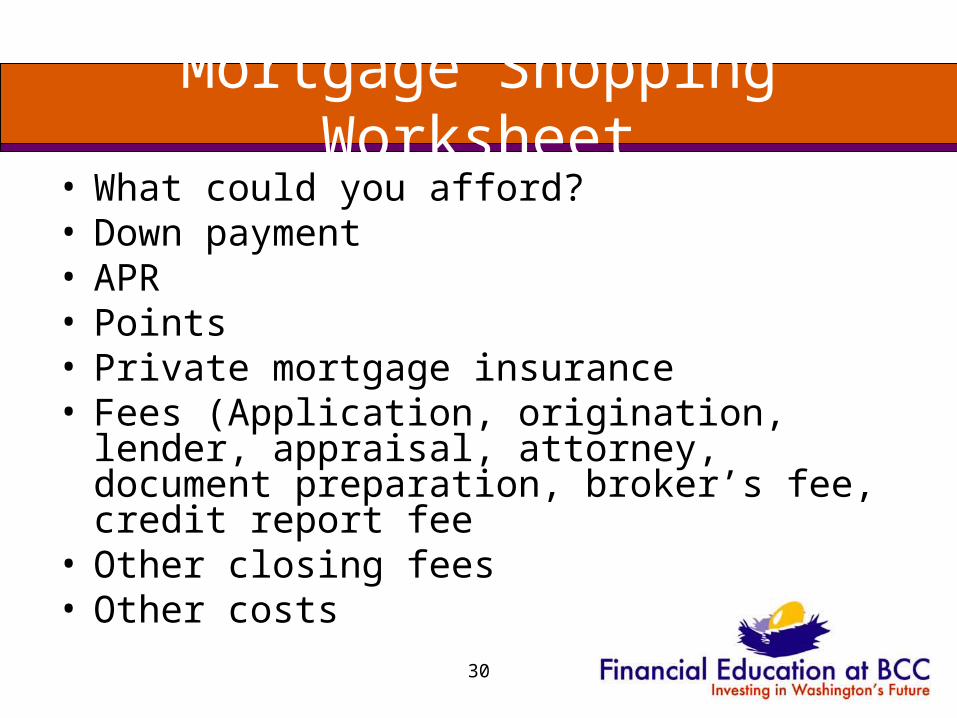

30

Mortgage Shopping Worksheet• What could you afford?• Down payment• APR• Points• Private mortgage insurance• Fees (Application, origination, lender, appraisal,

attorney, document preparation, broker’s fee, credit report fee

• Other closing fees• Other costs

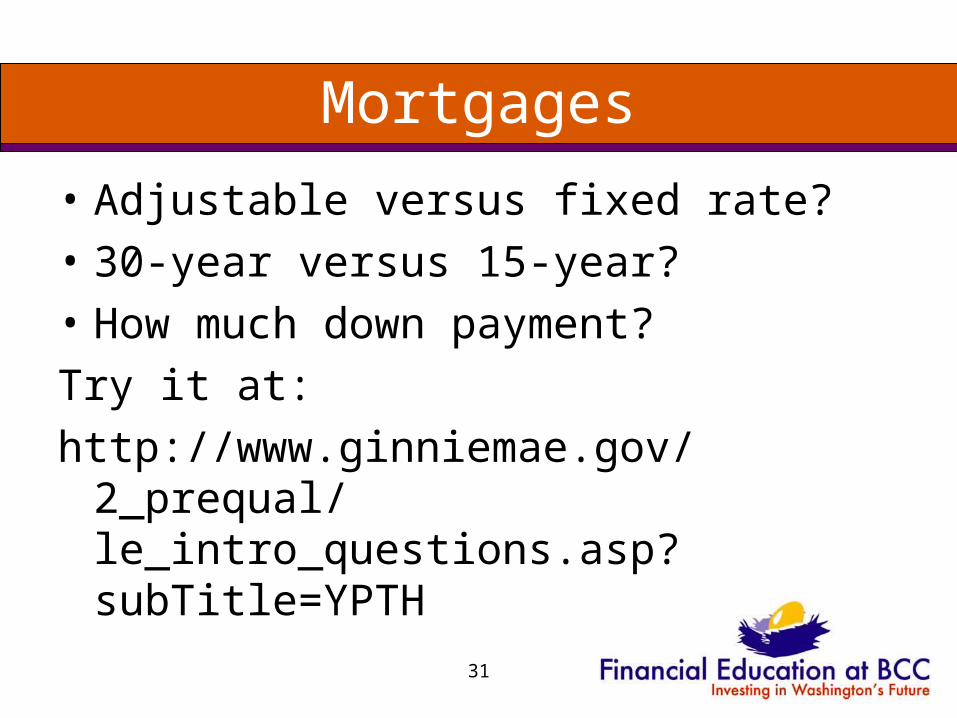

Mortgages

• Adjustable versus fixed rate?

• 30-year versus 15-year?

• How much down payment?

Try it at:

http://www.ginniemae.gov/2_prequal/le_intro_questions.asp?subTitle=YPTH

31

Activity – Shop for a mortgage

• Break into groups.

• Using the mortgage evaluation form, evaluate 3 mortgages

32

Step 6: Close the deal

• Satisfy all contingencies and then close the deal

33

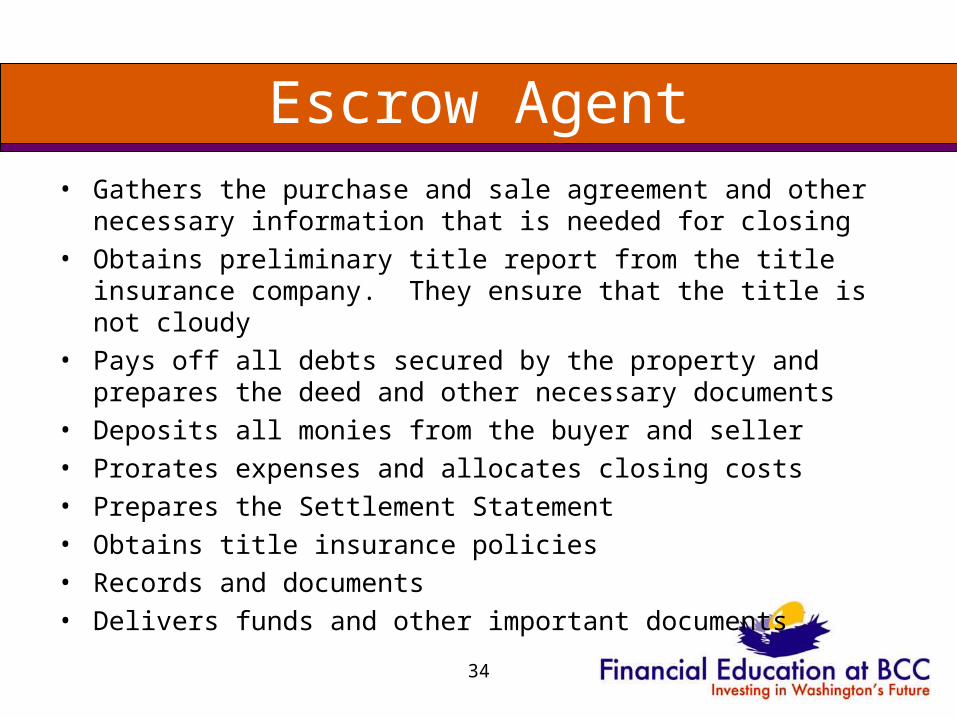

Escrow Agent• Gathers the purchase and sale agreement and other necessary

information that is needed for closing• Obtains preliminary title report from the title insurance company.

They ensure that the title is not cloudy • Pays off all debts secured by the property and prepares the deed

and other necessary documents• Deposits all monies from the buyer and seller• Prorates expenses and allocates closing costs• Prepares the Settlement Statement• Obtains title insurance policies• Records and documents• Delivers funds and other important documents

34

Activity – Settlement Statement

• In the forms packet, look at the DFI explanation of the Settlement Statement

35

Mr. and Mrs. Lee Buys A Home

• Follow the six step buying process to prepare you for buying your next home. All analysis, decision making and follow up must be included in your written presentation.

• Mr. and Mrs. Lee are relocating to Seattle Washington from Houston Texas. They have three children: ages 13, 5, and 15. They want a 4 bedroom homes with a minimum of 3 baths.

• Mrs. Lee’s concerns are schools, shopping, and community activity for the children to participate in. She wants to live in suburban area. They are moving from a 3200 sq feet home on 1.5 acres; which just sold for $250,000 (seller’s net of $198,000)

• Mr. Lee concern is the distance from his job site to his home. He also likes to work on small projects in the garage. A shop will be ideal.

• Their joint income is $150,000 per year. Ms Lee is a stay-home mom.• Debts: 30,000 on two cars, 15,000 in credit card; rental home with outstanding

mortgage of $35,000; stocks and bonds=Market value of $45,000;

36

Your rightsAccording to the Real Estate Settlement Procedures Act, you have the following rights.• To shop for the best loan for you and compare the charges of different mortgage

brokers and lenders.• To be informed about the total cost of your loan including the interest rate, points and

other fees. • To ask for a Good Faith Estimate of all loan and settlement charges before you agree

to the loan and pay any fees. • To know what fees are not refundable if you decide to cancel the loan agreement. • To ask your mortgage broker to explain exactly what the mortgage broker will do for

you. • To know how much the mortgage broker is getting paid by you and the lender for your

loan. • To ask questions about charges and loan terms that you do not understand.• To a credit decision that is not based on your race, color, religion, national origin, sex,

marital status, age, or whether any income is from public assistance. • To know the reason if your loan was turned down.

37

Your rights

• The Fair Housing Act prohibits discrimination by direct providers of housing, such as landlords and real estate companies as well as other entities, such as municipalities, banks or other lending institutions and homeowners insurance companies whose discriminatory practices make housing unavailable to persons because of race, religion, sex, national origin, family status, or disability.

•

38

Investing in Real Estate

39

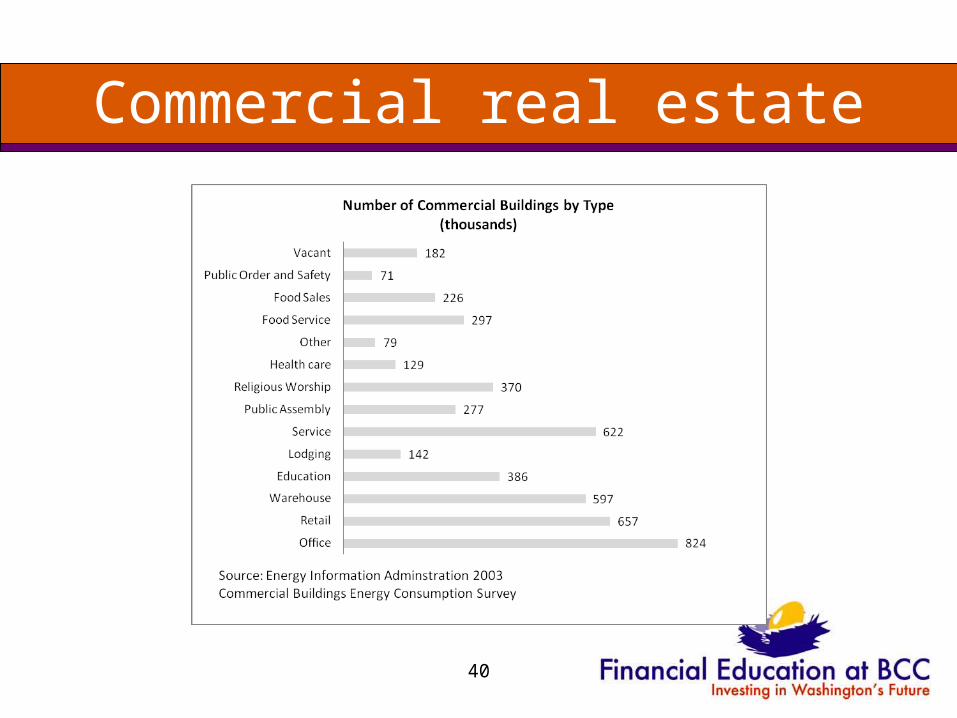

Commercial real estate

40

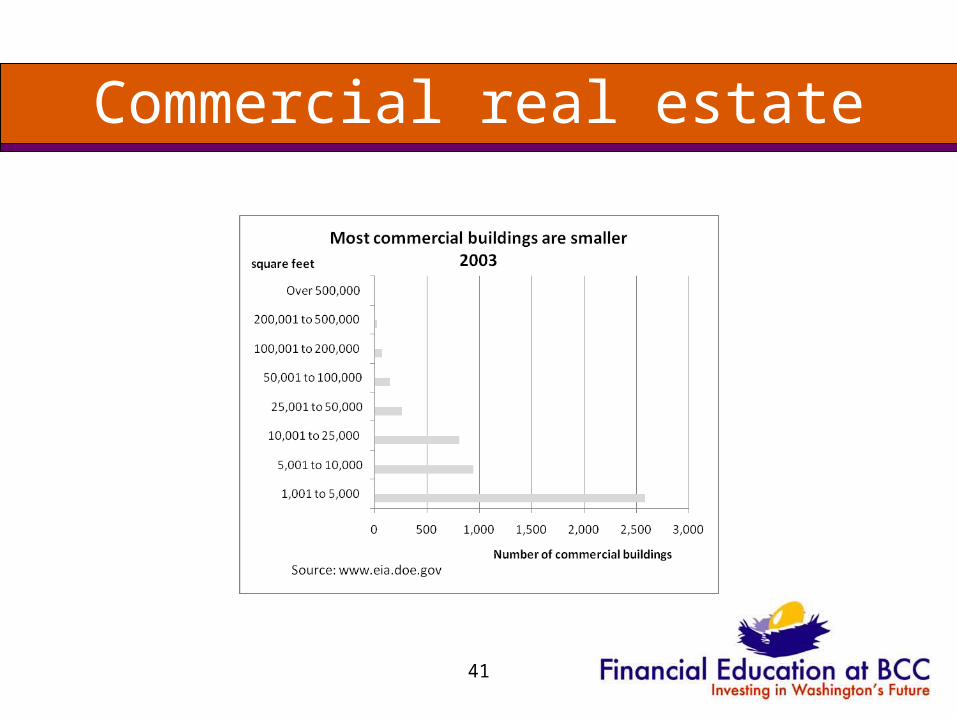

Commercial real estate

41

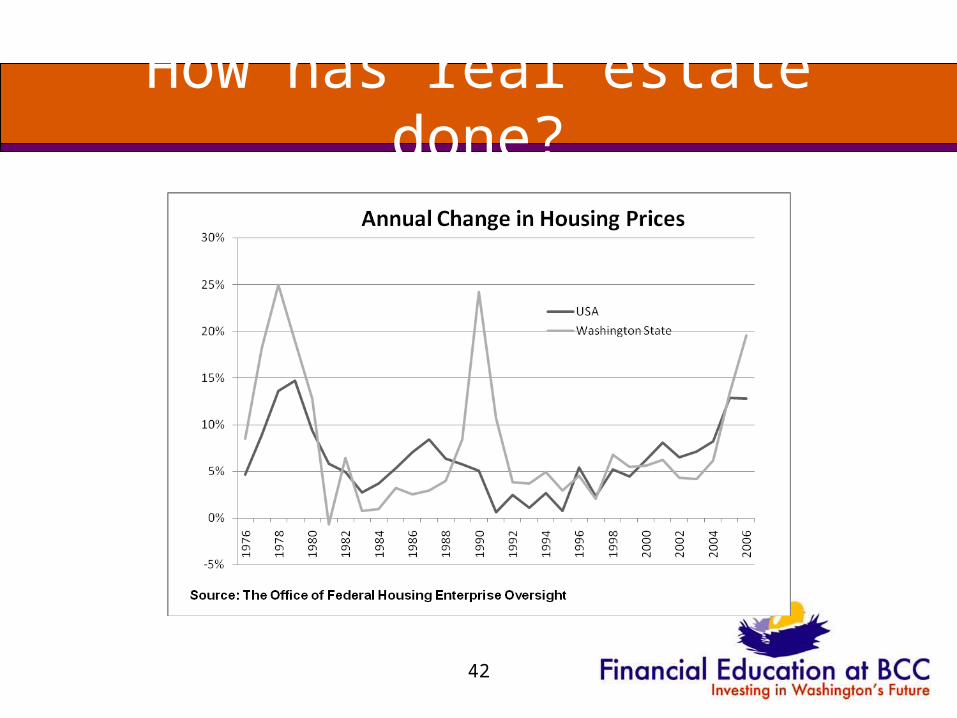

How has real estate done?

42

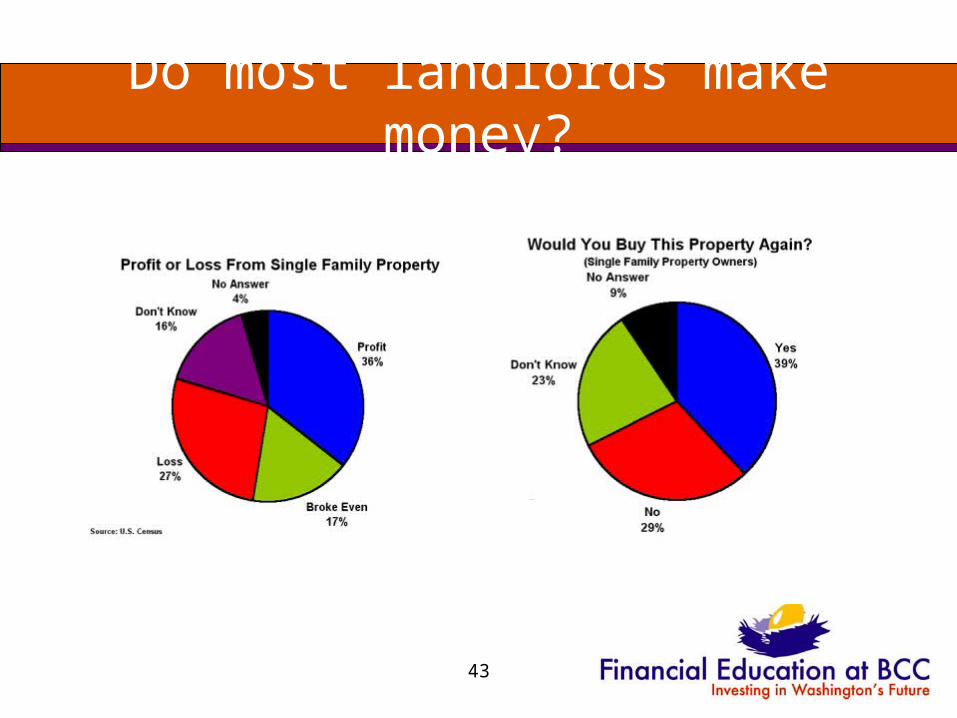

Do most landlords make money?

43

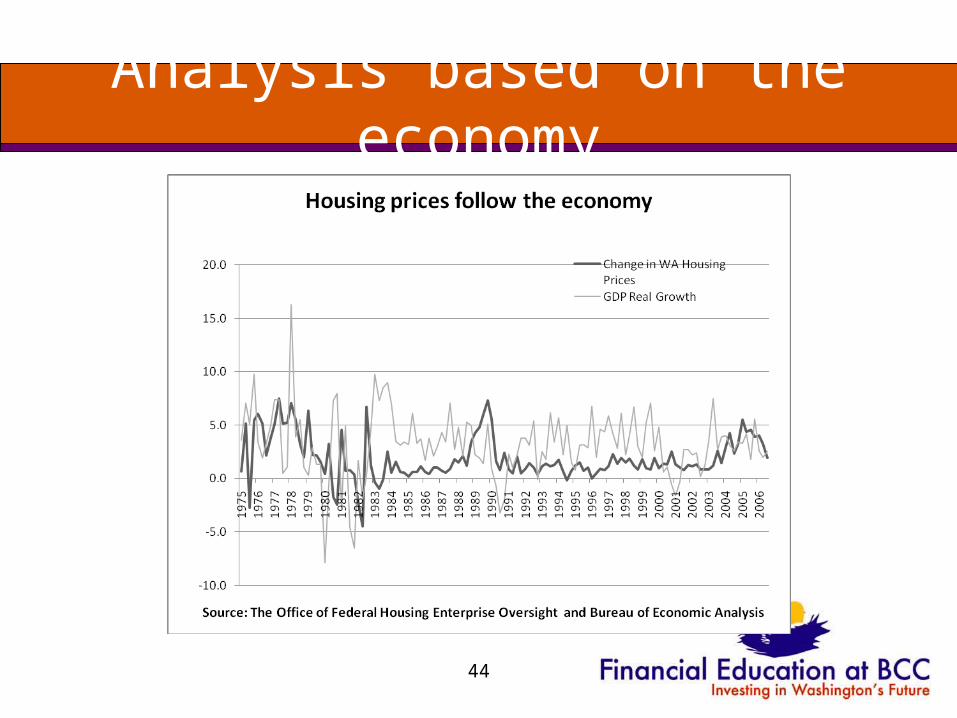

Analysis based on the economy

44