the metropolitan museum of art - fidelity investments · pdf fileof this booklet, please...

TRANSCRIPT

2097/51959-001 current/40368379v4

The Metropolitan Museum of Art

Summary Plan Description

403(b) Retirement Plan

for Non-Union Employees

The information contained herein has been provided by The Metropolitan Museum of Art and is solely the responsibility of The Metropolitan Museum of Art.

2097/51959-001 current/40368379v4

Table of Contents

INTRODUCTION TO THE BASIC PLAN ............................................................................................... 1

Our Commitment to Helping You Save for Retirement ...................................................................... 1

About This Booklet: It’s Your Summary Plan Description (SPD)........................................................ 2

Basic Plan Overview ........................................................................................................................... 3

ELIGIBILITY, PARTICIPATION AND VESTING .................................................................................... 4

Eligibility and Participation .................................................................................................................. 4

Vesting ................................................................................................................................................ 4

Breaks in Service ............................................................................................................................ 5

Designating a Beneficiary ................................................................................................................... 6

HOW THE BASIC PLAN WORKS ......................................................................................................... 7

You Contribute .................................................................................................................................... 7

The Museum Contributes ................................................................................................................... 7

Benefits of Pre-Tax Contributions ....................................................................................................... 7

Important Information about IRS Contribution Limits ......................................................................... 7

Excess Contributions ...................................................................................................................... 8

Loans .................................................................................................................................................. 8

Repaying Your Loan ....................................................................................................................... 9

What Happens If … You Default on Your Loan? ............................................................................ 9

Withdrawals ........................................................................................................................................ 9

HOW YOUR CONTRIBUTIONS ARE INVESTED ............................................................................... 10

Your Investment Options .................................................................................................................. 10

Obtaining Information about the Investment Funds ......................................................................... 10

Changing Your Investment Elections ............................................................................................... 11

Your Account Balance .................................................................................................................. 12

A Note About Administration Fees .................................................................................................... 12

PAYMENT OF BENEFITS.................................................................................................................... 13

When Your Account Is Paid to You .................................................................................................. 13

iii

2097/51959-001 current/40368379v4

Required Distributions .................................................................................................................. 13

How Your Account Is Paid to You .................................................................................................... 13

Tax Consequences of Distributions .................................................................................................. 15

Rollovers at the Time of Distribution ............................................................................................ 15

WHAT HAPPENS IF: UNDERSTANDING SOME SPECIAL RULES .................................................. 16

What Happens If …You are Terminated .......................................................................................... 16

What Happens If …You Are Re-Hired .............................................................................................. 16

What Happens If …You Go On Leave ............................................................................................. 17

What Happens If …You Become Disabled....................................................................................... 17

What Happens If …You Die.............................................................................................................. 18

IMPORTANT TERMS ........................................................................................................................... 19

ADMINISTRATION INFORMATION .................................................................................................... 20

Plan Name and Number ................................................................................................................... 20

Employer ........................................................................................................................................... 20

Employer Identification Number ....................................................................................................... 20

Type of Plan ...................................................................................................................................... 20

Plan Administrator ............................................................................................................................ 20

How Benefits are Funded ................................................................................................................. 20

Plan Year .......................................................................................................................................... 21

Legal Process ................................................................................................................................... 21

Plan Interpretation ............................................................................................................................ 21

Benefit Insurance .............................................................................................................................. 22

Non-Assignment of Benefits ............................................................................................................. 22

Qualified Domestic Relations Order (QDRO) ............................................................................... 22

Future of the Plan ............................................................................................................................. 23

Continuation of Participation for Employees in the Uniformed Services (USERRA) ....................... 23

Military Leave and Plan Loans ..................................................................................................... 23

When You Return from Military Leave ......................................................................................... 23

Heroes Earnings Assistance and Relief Tax Act of 2008 (HEART ACT) ..................................... 24

iii

2097/51959-001 current/40368379v4

PROCESS FOR SUBMITTING A CLAIM ............................................................................................. 25

Claims Procedure ............................................................................................................................. 25

Initial Claim ................................................................................................................................... 25

If a Claim Is Wholly or Partially Denied ........................................................................................ 26

Claim Denial Review .................................................................................................................... 26

HOW YOU MAY LOSE BENEFITS ..................................................................................................... 29

YOUR RIGHTS UNDER ERISA ........................................................................................................... 30

Receive Information About Your Plan and Benefits ......................................................................... 30

Prudent Actions by Plan Fiduciaries ................................................................................................. 30

Enforce Your Rights .......................................................................................................................... 31

Assistance with Your Questions ....................................................................................................... 31

APPENDIX A – INVESTMENT OPTIONS ........................................................................................... 32

Tier 1 – Target Date Retirement Funds ........................................................................................ 32

Tier 2 – Index Funds ..................................................................................................................... 32

Tier 3 – Actively Managed Funds ................................................................................................. 33

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 1

Updated for January 1, 2014 2097/51959-001 current/40368379v4

INTRODUCTION TO THE BASIC PLAN

Our Commitment to Helping You Save for Retirement

The Metropolitan Museum of Art (the “Museum”) is committed to providing all of its

employees with a “best-in-class” retirement program built on a philosophy of shared

responsibility. This means that the Museum will provide benefits to help you build a

foundation for retirement savings, and provide supporting communications, tools and

resources to help you reach your personal financial goals.

The Retirement Program’s primary purpose is to help you save for the future. Its components

are designed to work together to help build your retirement savings. This document outlines

the provisions of one of the Retirement Program’s components: The Metropolitan Museum of

Art 403(b) Retirement Plan for Non-Union Employees (otherwise referred to in this document

as the “Basic Plan” or the “Plan”). The Basic Plan, a mandatory condition of your

employment with the Museum, helps build your retirement savings in addition to the

Matching Plan (a voluntary component of the Museum’s Retirement Program) and any other

savings you may have, using contributions from you and the Museum. For more information

about the Matching Plan, please see the Summary Plan Description or Plan document for the

Matching Plan, available from the Benefits Office in the Human Resources Department.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 2

Updated for January 1, 2014 2097/51959-001 current/40368379v4

About This Booklet: It’s Your Summary Plan Description (SPD)

This booklet serves as the Summary Plan Description (SPD) for the Basic Plan. It describes

the benefits as they apply to eligible employees effective January 1, 2014.

We encourage you to read this booklet carefully and share it with your family members.

While it is not intended to provide all of the details of the Plan, this booklet is intended to help

you understand how the Plan works and answer the questions most frequently asked about

benefits under the Plan. You can find complete details about the Plan in the official Plan

document. If there is any difference between the information in this booklet and in the official

Plan document, the Plan document will govern.

In this booklet, we have tried to describe the Plan in everyday language, but some terms

have specific meanings. For your convenience, we have summarized some of these special

terms in the section of this booklet titled “Important Terms”. These terms are capitalized

throughout the booklet.

If you have any questions about your benefits or if you have difficulty understanding any part

of this booklet, please contact The Metropolitan Museum of Art Benefits Office in the Human

Resources Department.

The Metropolitan Museum of Art

Human Resources Department

1000 Fifth Avenue

New York, New York 10028-0198

212-650-2285

This document is intended to help you understand the main features of the Basic Plan. It should not be

considered as a substitute for the Plan document, which governs the operation of the Basic Plan. The Plan

document sets forth all of the details and provisions concerning the Basic Plan and is subject to amendment. If

any questions arise that are not covered in this document or if this document appears to conflict with the legal

Plan document, the text of the legal Plan document will determine how questions will be resolved. To request a

copy of the Plan document, please contact the Benefits Office in the Human Resources Department.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 3

Updated for January 1, 2014 2097/51959-001 current/40368379v4

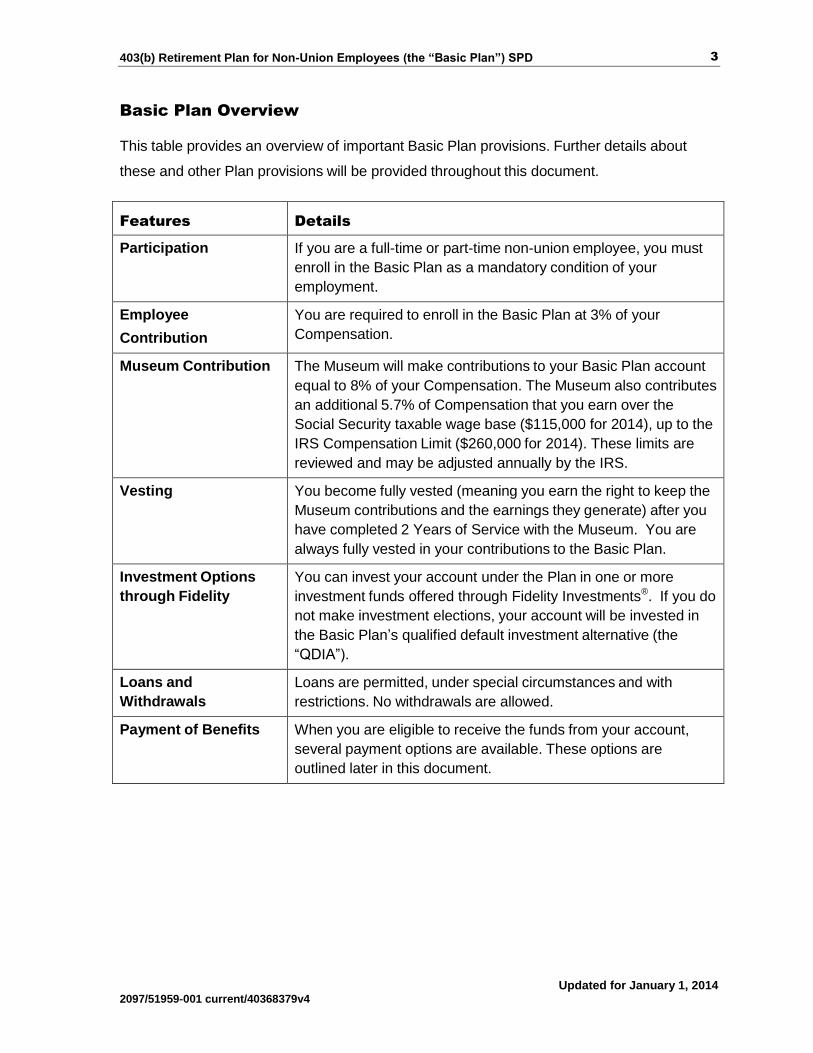

Basic Plan Overview

This table provides an overview of important Basic Plan provisions. Further details about

these and other Plan provisions will be provided throughout this document.

Features Details

Participation If you are a full-time or part-time non-union employee, you must

enroll in the Basic Plan as a mandatory condition of your

employment.

Employee

Contribution

You are required to enroll in the Basic Plan at 3% of your

Compensation.

Museum Contribution The Museum will make contributions to your Basic Plan account

equal to 8% of your Compensation. The Museum also contributes

an additional 5.7% of Compensation that you earn over the

Social Security taxable wage base ($115,000 for 2014), up to the

IRS Compensation Limit ($260,000 for 2014). These limits are

reviewed and may be adjusted annually by the IRS.

Vesting You become fully vested (meaning you earn the right to keep the

Museum contributions and the earnings they generate) after you

have completed 2 Years of Service with the Museum. You are

always fully vested in your contributions to the Basic Plan.

Investment Options

through Fidelity

You can invest your account under the Plan in one or more

investment funds offered through Fidelity Investments®. If you do

not make investment elections, your account will be invested in

the Basic Plan’s qualified default investment alternative (the

“QDIA”).

Loans and

Withdrawals

Loans are permitted, under special circumstances and with

restrictions. No withdrawals are allowed.

Payment of Benefits When you are eligible to receive the funds from your account,

several payment options are available. These options are

outlined later in this document.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 4

Updated for January 1, 2014 2097/51959-001 current/40368379v4

ELIGIBILITY, PARTICIPATION AND VESTING

Eligibility and Participation

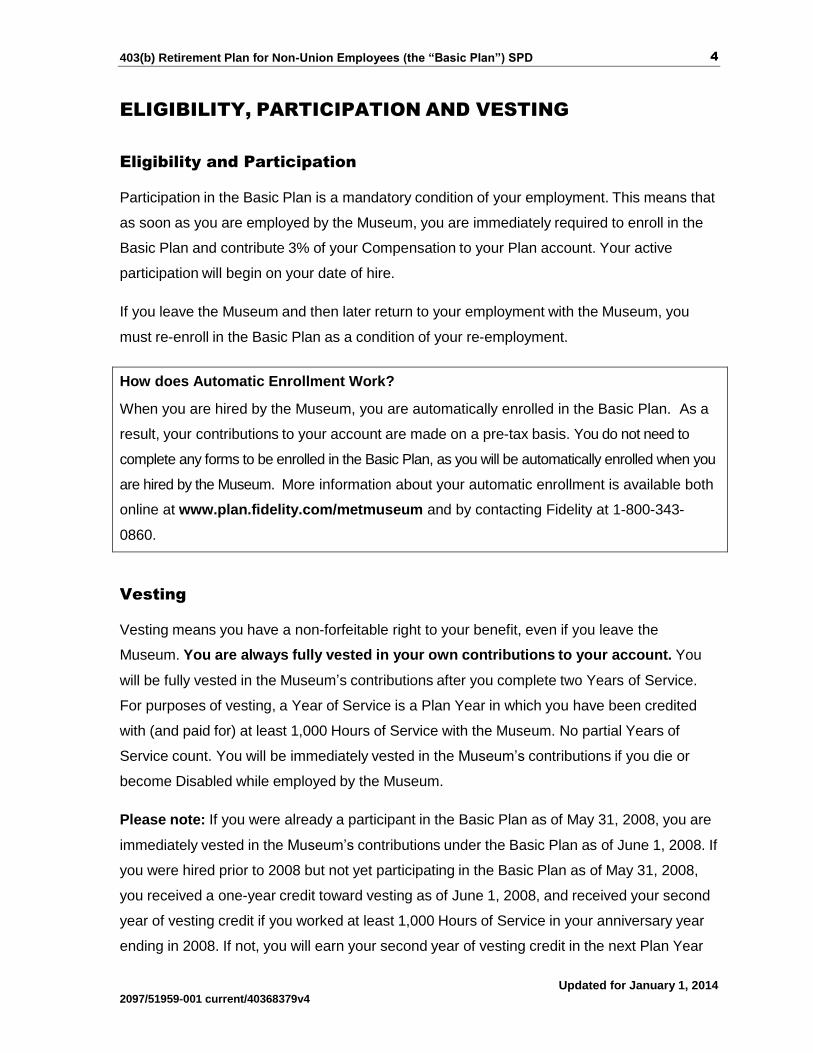

Participation in the Basic Plan is a mandatory condition of your employment. This means that

as soon as you are employed by the Museum, you are immediately required to enroll in the

Basic Plan and contribute 3% of your Compensation to your Plan account. Your active

participation will begin on your date of hire.

If you leave the Museum and then later return to your employment with the Museum, you

must re-enroll in the Basic Plan as a condition of your re-employment.

How does Automatic Enrollment Work?

When you are hired by the Museum, you are automatically enrolled in the Basic Plan. As a

result, your contributions to your account are made on a pre-tax basis. You do not need to

complete any forms to be enrolled in the Basic Plan, as you will be automatically enrolled when you

are hired by the Museum. More information about your automatic enrollment is available both

online at www.plan.fidelity.com/metmuseum and by contacting Fidelity at 1-800-343-

0860.

Vesting

Vesting means you have a non-forfeitable right to your benefit, even if you leave the

Museum. You are always fully vested in your own contributions to your account. You

will be fully vested in the Museum’s contributions after you complete two Years of Service.

For purposes of vesting, a Year of Service is a Plan Year in which you have been credited

with (and paid for) at least 1,000 Hours of Service with the Museum. No partial Years of

Service count. You will be immediately vested in the Museum’s contributions if you die or

become Disabled while employed by the Museum.

Please note: If you were already a participant in the Basic Plan as of May 31, 2008, you are

immediately vested in the Museum’s contributions under the Basic Plan as of June 1, 2008. If

you were hired prior to 2008 but not yet participating in the Basic Plan as of May 31, 2008,

you received a one-year credit toward vesting as of June 1, 2008, and received your second

year of vesting credit if you worked at least 1,000 Hours of Service in your anniversary year

ending in 2008. If not, you will earn your second year of vesting credit in the next Plan Year

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 5

Updated for January 1, 2014 2097/51959-001 current/40368379v4

in which you work at least 1,000 Hours of Service.

Breaks in Service

If you stop working for the Museum, or do not work for the Museum for at least 500

Hours of Service in a Plan Year, you will incur a break in service. If you are later re-

hired by the Museum, or resume working at least 500 Hours of Service in a Plan Year,

this break in service may or may not affect your vesting service depending on the length

of your prior service and the length of your break in service.

- If you leave the Museum and are later re-hired within 12 consecutive months,

your vesting service will be determined as though you did not have a break in

service.

- If you leave the Museum and are later re-hired after 12 consecutive months and

experience a break in service, your prior Years of Service will be reinstated for

vesting purposes if

- You were a participant when you incurred the break in service, or

- The number of consecutive one-year breaks in service you incur is not more

than the greater of:

Five, or

The number of Years of Service credited to you before you

stopped working for the Museum.

If you are absent from work due to pregnancy, birth of your child, placement of a child

with you for adoption, or caring for your child following birth or placement for adoption,

and later return to work at the Museum, you will be credited with the Hours of Service

you would have worked (or, if such hours cannot be determined, eight hours per day

that you would have worked), up to 501 Hours of Service, generally to the extent such

crediting will prevent your incurring a break in service.

If you are absent from work due to an authorized leave of absence, the Hours of

Service you are absent will be counted as Hours of Service for the purpose of

preventing your incurring a break in service.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 6

Updated for January 1, 2014 2097/51959-001 current/40368379v4

Designating a Beneficiary

When you enroll in the Basic Plan, you should designate a Beneficiary. Your Beneficiary is

the person who will receive your benefit if you die before receiving benefits from the Plan.

Although it is not mandatory to elect a Beneficiary, we encourage you to name one using the

Fidelity online beneficiary designation tool at the Fidelity website at

www.plan.fidelity.com/metmuseum, or by calling Fidelity at 1-800-343-0860. If you die

and there is no valid Beneficiary designation on file with Fidelity, your spouse (if you are

married) or your estate (if you are not married) will automatically become your Beneficiary.

Note that if you are married and want to name someone other than your spouse as your

Beneficiary, you must obtain written consent from your spouse to do so.

It is also important to understand that if you are unmarried, name a Beneficiary and

subsequently marry, your prior designation is invalid and your spouse will be your

Beneficiary, unless you obtain proper spousal consent to designate a different Beneficiary.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 7

Updated for January 1, 2014 2097/51959-001 current/40368379v4

HOW THE BASIC PLAN WORKS

You Contribute

As a condition of your employment with the Museum, you must contribute 3% of your

Compensation to your account under the Basic Plan each payroll period on a pre-tax basis.

You may not change your contribution level at any time, and outside contributions or

rollovers to the Basic Plan are not permitted.

The Museum Contributes

The Museum will make contributions to the Basic Plan on your behalf equal to 8% of your

annual Compensation each payroll period on a pre-tax basis. The Museum’s contribution is

provided at no cost to you, and ultimately represents a significant portion of your retirement

savings.

Please note: If you earn more than the Social Security taxable wage base ($115,000 for

2014), the Museum will contribute an additional 5.7% of the Compensation that you earn

over the wage base, up to IRS compensation limit ($260,000 for 2014). These limits are

reviewed and may be adjusted annually by the IRS.

Benefits of Pre-Tax Contributions

When you participate in the Basic Plan, you are contributing to your account on a pre-tax

basis. This means that you are reducing your current taxable income because you do not pay

federal and most state and local taxes on these contributions while they are in your account.

However, pre-tax contributions are subject to Social Security and Medicare taxes paid by you

and the Museum, and must not exceed the maximum deferral limits established by the

federal government (see below).

Important Information about IRS Contribution Limits

The Basic Plan is subject to certain rules and benefit limits set forth by the Internal Revenue

Service (IRS). The following limits apply to the combined contribution amount you and the

Museum make toward both the Museum’s Basic and Matching Plans in the same calendar

year. According to IRS regulations, the combined contribution amount in any given Plan Year

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 8

Updated for January 1, 2014 2097/51959-001 current/40368379v4

to the Museum’s Retirement Program cannot exceed the lesser of:

100 percent (100%) of your Compensation*, or

$52,000 for 2014 (may be adjusted annually by the IRS).

If you are age 50 or older, you can make a catch-up contribution ($5,500 for 2014) to

increase your pre-tax savings. Catch-up contributions do not count toward the $52,000

IRS limit noted above.

*For 2014 the maximum amount of total Compensation recognized for contributions is $260,000.

Excess Contributions

The contribution limits apply to the combined contribution amount you make toward both the

Museum’s Basic and Matching Plans in the same calendar year. The Museum will monitor

your contributions to both plans so you do not exceed the limit. However, if you contribute to

the plan of any other employer, it is your responsibility to monitor compliance with this

limitation.

Loans

If you are a participant in the Basic Plan and an active employee of the Museum, you may

borrow money from your vested Basic Plan account (certain limitations apply). If you are

married, you will need spousal consent before taking a loan from your account. Additionally,

no more than one outstanding loan is permitted under the Basic Plan at any time.

The minimum amount you may take as a loan is $1,000. The maximum allowable loan

amount is $50,000 (and may be lower in some circumstances).

If your account is invested in more than one fund, the loan will be taken out proportionately

from among each of the funds in which you are invested. If you repay the outstanding

balance on your existing loan, you may be eligible to take another loan no earlier than one

year after the date the original loan was granted. A loan-processing fee is charged for every

loan requested – loan-processing fees are described in the Fee Disclosure Chart discussed

in the section of this booklet titled “A Note About Administration Fees.” You will be required

to repay your loan, with interest, according to relevant Basic Plan provisions, as summarized

below.

If you want to apply for a loan, contact Fidelity at www.plan.fidelity.com/metmuseum, or

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 9

Updated for January 1, 2014 2097/51959-001 current/40368379v4

1-800-343-0860.

Repaying Your Loan

You repay your loan according to a repayment schedule. In general:

The repayment period is up to five years (up to 20 years if you are using the loan to

purchase your principal residence).

— You repay your loan in equal installments (not less frequently than quarterly)

through mandatory payroll deductions within the repayment period, beginning

with the first payroll period after the loan is disbursed. When you repay your

loan by payroll deduction, the repayments will be invested according to your

most current investment elections you have on record.

You can also prepay your entire loan balance in one lump sum at any time during

the repayment period, without penalty. Partial prepayments are not permitted.

Loan payments generally are not tax deductible.

If you are eligible to receive distributions from the Plan and you still have an outstanding loan,

the value of your distribution will be reduced by the amount of the loan that is still unpaid.

What Happens If … You Default on Your Loan?

Your loan goes into default (becomes immediately due and payable) if:

You fail to make a loan repayment before the end of the grace period,

You file for bankruptcy, or are judged to be insolvent or bankrupt, or

You leave the Museum for any reason before the loan is fully repaid.

If you default on your loan, you are required to pay the full balance within 30 days after

receiving notice of the default. Otherwise, the amount you owe (including accrued interest)

will be treated as a deemed distribution subject to taxes at the time of your default, and will be

deducted from your account when it is distributed.

Withdrawals

No withdrawals are permitted under the Basic Plan at any time, under any circumstance.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 10

Updated for January 1, 2014 2097/51959-001 current/40368379v4

HOW YOUR CONTRIBUTIONS ARE INVESTED

Your Investment Options

When you participate in the Basic Plan, you may choose to allocate your account under the

Plan into the investment funds made available to you by the Museum through Fidelity

Investments®. The Museum provides a three-tier investment structure that provides you with

the opportunity to mix your allocations among various options to best meet your individual

goals. You may also designate a certain percentage of your account to be invested in

different options. Please note that if you do not actively choose an investment option, your

contributions will be automatically invested in the Vanguard Target Date Retirement Fund

that corresponds closest to the year in which you turn age 65.1

For a complete list of the investment options under the Plan, please refer to Appendix A of

this booklet.

Obtaining Information about the Investment Funds

You will receive information on each of the investment funds directly from Fidelity at the

time of your enrollment. This information will include:

A general description of each of the investment funds,

The investment objectives of each investment fund,

The risk and return characteristics of each investment fund,

The type and level of diversification of assets of each investment fund,

A copy of the prospectus if you are a first time investor to the fund,

The identity of any ERISA investment managers, and

A description of any transaction fees or expenses charge for investment purchases

or sales.

You can also request the following information from Fidelity:

1 This is the Qualified Default Investment Alternative (QDIA) selected by the Museum.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 11

Updated for January 1, 2014 2097/51959-001 current/40368379v4

A description of the annual operating expenses of each investment fund (including

management, administrative and transaction costs that reduce the value of the

investment fund) and the aggregate amount of these expenses (expressed as a

percentage of average net assets),

Copies of any prospectuses, financial statements and reports and any other

materials relating to each investment fund (to the extent such information is

provided to the Plan),

A report of each investment fund’s latest available values of the shares or units

(and past and current investment performance), and

The value of the shares or units of each investment in which you or your

Beneficiary is invested.

We encourage you to carefully read the investment fund descriptions and the fund’s

prospectus before investing. You should evaluate the investment options available under

the Plan in the same way you would evaluate any investment to determine whether you are

comfortable with the investment risk and expected rate of return. The Plan is intended to

constitute a plan under the Employee Retirement Income Security Act of 1974, as amended

(“ERISA”) Section 404(c) and Title 29 of the Code of Federal Regulations Section

2550.404c-1. Consequently, the fiduciaries of the Plan may be relieved of liability for any

losses which are the direct and necessary result of investment instructions given by you or

your Beneficiaries. You are urged to read the literature describing each investment fund

prior to making any investment decision. Remember, you will share in any losses as well as

any gains of the funds you choose.

For specific information about the Fidelity investment fund options, contact a Fidelity

customer service representative toll-free at 1-800-343-0860, Monday through Friday

(excluding New York Stock Exchange holidays) between 8 a.m. and midnight, Eastern

Time. Or, you can visit Fidelity’s website at www.plan.fidelity.com/metmuseum.

Changing Your Investment Elections

You may change the investment of your existing account balance at any time either online at

www.plan.fidelity.com/metmuseum or by contacting Fidelity at 1-800-343-0860. Changes

will become effective as soon as administratively possible. You may also change the manner

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 12

Updated for January 1, 2014 2097/51959-001 current/40368379v4

in which your future contributions are allocated among your different investment options.

If there is a change in any of the investment funds available to you, the Museum has the right

to direct the transfer of your contributions to a fund that is most similar to the one you

previously elected.

Your Account Balance

Your account balance is updated daily and can be accessed by contacting Fidelity at 1-800-

343-0860. Representatives are available Monday through Friday (excluding New York Stock

Exchange holidays) between 8a.m. and midnight, Eastern Time. Or, you can visit Fidelity’s

website at www.plan.fidelity.com/metmuseum.

A Note About Administration Fees

All administrative expenses of the Plan shall be paid by the Museum, except that any loan,

withdrawal, contribution, benefit, taxes applicable to a contribution or other charges by

Fidelity under the Plan’s contract with Fidelity shall be paid out of the assets held by Fidelity

under the Plan’s contract with Fidelity and charged to the applicable accounts, unless the

Museum otherwise elects to pay such amounts.

Some fees and expenses attributable to the management and investment of the Plan’s

investment funds are charged (pro rata) against each of the respective investment funds.

However, certain expenses are charged directly to your account, for example, those associated

with a loan, early redemption fees, etc. For a description of these fees, refer to the “Fee

Disclosure Chart” that was provided to you when you enrolled, and which is available at

www.plan.fidelity.com/metmuseum.

Complete information about fees and expenses is available from Fidelity. In addition, information

about investment management fees is included in the prospectus describing each investment

fund, which is available online at www.plan.fidelity.com/metmuseum or by calling Fidelity at

1-800-343-0860.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 13

Updated for January 1, 2014 2097/51959-001 current/40368379v4

PAYMENT OF BENEFITS

When Your Account Is Paid to You

You are eligible to receive your benefit under the Basic Plan when you stop working at the

Museum, become Disabled or die.

You may begin to collect your benefit under the Basic Plan (unless you elect otherwise) not

later than the 60th day after the end of the Plan Year in which the latest of the following

events occurs:

You reach age 62

The 10th anniversary of your participation in the Basic Plan

You stop working at the Museum

Required Distributions

The law requires that payment of your Basic Plan account begins by the later of:

April 1 of the calendar year after the calendar year in which you reach 70½, or

Your retirement from the Museum.

If you are actively at work when you reach age 70 ½, you are not required to take this

mandatory distribution; but, you may elect to do so. However, under current laws, if you are no

longer actively at work, you must begin to receive payment of your benefit no later than April

1 following the year in which you reach age 70½. You cannot roll over a minimum distribution

to any other account. See the section of this booklet titled “What Happens If: Understanding

Some Special Rules” for information about receiving your payments if you are terminated, die

or become Disabled.

How Your Account Is Paid to You

When you are eligible to receive benefits under your Basic Plan account, you can elect to:

Roll over your benefit into an eligible retirement plan (such as an IRA, a Roth IRA

or a qualified plan),

Receive a lump sum payment (meaning all at one time) payable to you in the

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 14

Updated for January 1, 2014 2097/51959-001 current/40368379v4

amount equal to the total value of your account,

Receive an annuity payment (see below), or

Defer receiving your benefit until a later date.

When you contact Fidelity to begin receiving your benefit, you will have a range of options

regarding the form in which you may receive your benefit. If you are married, and elect to receive

your benefit in a form other than the joint and survivor annuity benefit as described below,

spousal consent is required. You will receive your payout as soon as administratively feasible

based on the payment date you elect (certain timing requirements apply). Once you are

eligible to receive distributions, you choose a benefit commencement date (with the consent

of your spouse, if applicable). You will start receiving benefits on the first day of the month

following your chosen payment date. If you do not elect to receive your benefit in an alternative

form (as described above), it will be paid as follows:

If you are not married: You will receive a single life annuity (i.e., monthly benefits

paid to you for life) that will end at the time of your death.

If you are married: You will receive a joint and survivor benefit. This means that

your payments will be lower than they would be under the single life annuity form

(i.e., monthly benefits paid to you for life), but your spouse at the time benefits

commence will receive payments for the remainder of his or her life after your

death equal to 100% of the monthly benefits paid to you during your life. You may

alternatively elect to have your monthly benefits paid in the form of a qualified

optional survivor annuity which provides for a reduced monthly benefit for your life

with 50% of such monthly benefit paid during your spouse’s life.

Note: If you elect to receive payments under the joint and survivor annuity you may, with

your spouse’s consent, revoke such election at any time before receiving any benefits. In

addition, you may revoke an election not to take joint and survivor benefits at any time before

receiving benefits under the Basic Plan; provided, however, that if you elect to receive any

form of payment other than the joint and survivor annuity, you must obtain spousal consent

again.

If you choose an optional form of payment (i.e., not a single-life or joint and survivor annuity),

with the consent of your spouse, if applicable, certain distribution restrictions apply. You can

contact Fidelity online at www.plan.fidelity.com/metmuseum or at 1-800-343-0860 for more

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 15

Updated for January 1, 2014 2097/51959-001 current/40368379v4

details.

Tax Consequences of Distributions

If you receive the value of your Basic Plan benefit as a lump-sum payment, federal income

taxes are required to be withheld equal to 20% of the taxable portion of your payment,

unless you roll over your distribution directly into an IRA, an eligible employer plan or other

eligible plan. If it is not rolled over, your distribution may be subject to a 10% early payment

penalty tax in addition to regular income tax unless:

You are at least age 55 at the time you leave the Museum,

You are at least age 59½ at the time payment is made to you, or

If another exception applies.

For more information on the additional 10% tax, please see IRS Form 5329. You are

responsible for complying with applicable federal, state and local tax laws and regulations

when you receive the distribution. You will receive more information about the applicable tax

rules when you request a distribution from the Plan.

Rollovers at the Time of Distribution

You may defer federal income taxes (and the 10% penalty tax described above) on any

single sum taxable distribution to the extent that the distribution is eligible for rollover and you

do in fact roll it over into an IRA or another eligible plan. If you make a direct rollover into a

traditional IRA or other eligible plan, you will not pay federal income taxes until you withdraw

the money from the traditional IRA or other eligible plan.

The tax information contained in this SPD is intended only as a general summary of the

federal income tax consequences of participation in the Basic Plan and is not a complete

summary of such consequences. You are urged to consult with your own tax advisor with

respect to your specific tax situation.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 16

Updated for January 1, 2014 2097/51959-001 current/40368379v4

WHAT HAPPENS IF:

UNDERSTANDING SOME SPECIAL RULES

What Happens If …You are Terminated

The full vested value of your account becomes payable to you when your employment with

the Museum is terminated. You may elect an immediate payment in one of the forms

available under the Basic Plan or defer payment of your benefits if you prefer (as described

in the preceding sections).

Your employment with the Museum is considered terminated if you lose your employment

status with the Museum due to, but not limited to, retirement, death, disability, resignation or

dismissal with or without cause.

If you are terminated but not fully vested in the Museum’s contributions, you will not be

eligible to receive the non-vested contributions in your account balance. These contributions

may be restored if you are re-hired by the Museum within the allowable timeframe (see

below).

What Happens If …You Are Re-Hired

If your employment with the Museum ends and you are later re-employed by the Museum,

your prior Years of Service will count for vesting purposes if:

You participated in the Basic Plan before you left the Museum, or

If you are re-hired no later than five years after you left the Museum, or if the

number of years you were not employed by the Museum does not exceed the

number of years you were employed by the Museum before your employment

ended.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 17

Updated for January 1, 2014 2097/51959-001 current/40368379v4

What Happens If …You Go On Leave

If you go on an authorized leave of absence, you are not considered terminated unless you

fail to return to the Museum in the appropriate timeframe. See the section of this booklet

titled “Continuation of Participation for Employees in the Uniformed Services (USERRA)” for

more information about your benefits while on military leave.

If you take an approved paid leave of absence (including short-term disability

leave), you may continue to make pre-tax contributions to the Basic Plan as if you

were an active employee. You may take loans but you cannot receive a final

distribution of your Plan accounts.

If you take an approved unpaid leave of absence other than a long-term disability

leave, you will not be able to make contributions to the Basic Plan and you will not

receive any Museum contributions during that time. You may take loans but you

cannot receive a final distribution of your Plan accounts.

If you are eligible for a leave under the federal Family and Medical Leave Act

(FMLA), you are entitled to take up to 12 weeks of leave for certain family and

medical situations (or 26 weeks in a single 12-month period for military caregiver

leave). In general, your FMLA leave is treated like any other paid or unpaid leave

under the Plan, as noted above. If your FMLA leave is paid, your leave will be

treated like other paid leaves; if your FMLA leave is unpaid, it will be treated like

other unpaid leaves. Periods of FMLA absences will not be counted toward a

break in service.

What Happens If …You Become Disabled

If you become “Disabled” while you are actively employed by the Museum, you will not be

able to make contributions to the Plan and you will not receive any further Museum

contributions. “Disabled” under the Plan means that you are unable to engage in any

substantial gainful activity by reason of any medically determinable physical or mental

impairment that can be expected to result in death or to be of long-continued and indefinite

duration, as certified by a physician acceptable to the Plan Administrative Committee. If you

are Disabled, you may not take loans, but you will become 100% vested in the value of your

account balance, regardless of your actual Years of Service, and you will be eligible to

receive payment in any of the forms described in the section of this booklet titled “How Your

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 18

Updated for January 1, 2014 2097/51959-001 current/40368379v4

Account is Paid to You.”

What Happens If …You Die

If you die while actively employed with the Museum or before your benefits

commencement date:

If you are married, 100% of the value of your account will be provided in monthly

benefits for the life of your spouse, starting on the payment date your spouse

elects, provided that your spouse may elect to receive such amount in a lump sum

or any other optional form available under the Plan. If your spouse is not your

Beneficiary (which is possible only if your spouse actively forfeits his or her right to

be your Beneficiary), distribution rules will be as described in the bullet below.

If you are unmarried, the value of your account will be distributed to your

Beneficiary or Beneficiaries in the proportion you designate (i.e., divided between

Beneficiaries in a certain percentage, etc.). The distribution will be made in one of

the optional forms available under the Basic Plan as determined by the Beneficiary

receiving the payment.

If you die on or after the date your benefit payments have started: The remaining

amount of your account balance will be paid to your spouse (or Beneficiary, if not your

spouse) in the form in which you elected to receive it. Certain rules apply regarding

distribution of your benefits after your death.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 19

Updated for January 1, 2014 2097/51959-001 current/40368379v4

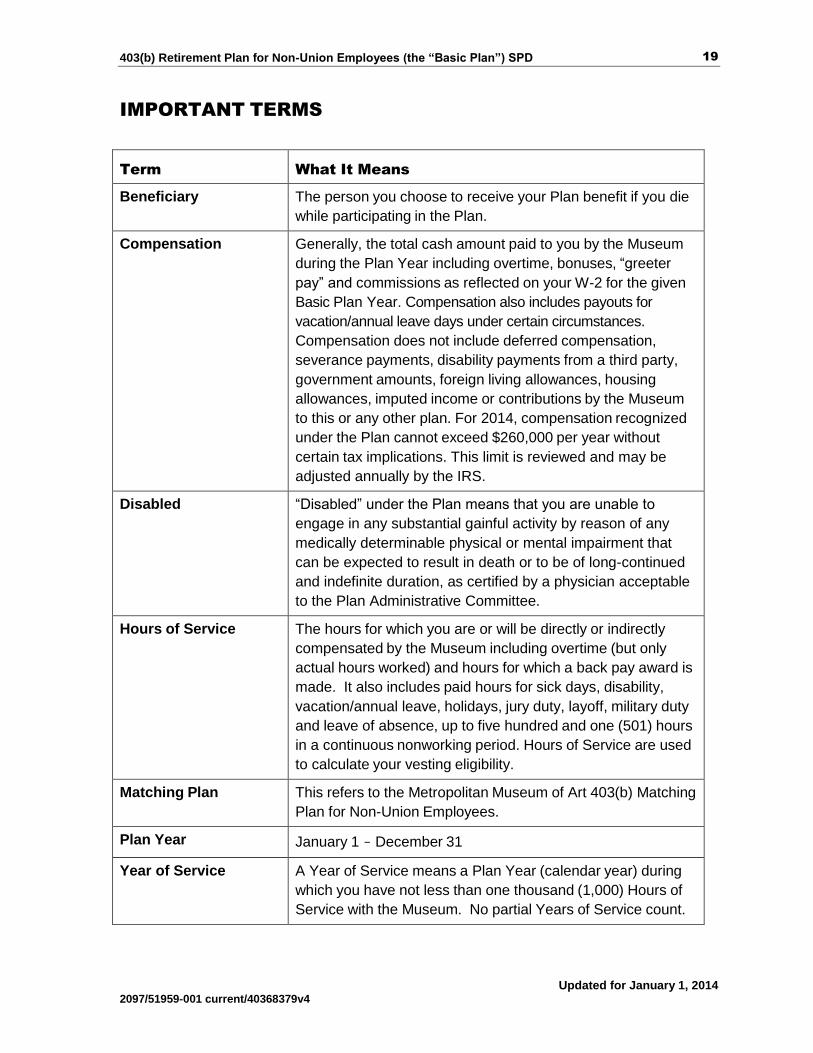

IMPORTANT TERMS

Term What It Means

Beneficiary The person you choose to receive your Plan benefit if you die

while participating in the Plan.

Compensation Generally, the total cash amount paid to you by the Museum

during the Plan Year including overtime, bonuses, “greeter

pay” and commissions as reflected on your W-2 for the given

Basic Plan Year. Compensation also includes payouts for

vacation/annual leave days under certain circumstances.

Compensation does not include deferred compensation,

severance payments, disability payments from a third party,

government amounts, foreign living allowances, housing

allowances, imputed income or contributions by the Museum

to this or any other plan. For 2014, compensation recognized

under the Plan cannot exceed $260,000 per year without

certain tax implications. This limit is reviewed and may be

adjusted annually by the IRS.

Disabled “Disabled” under the Plan means that you are unable to

engage in any substantial gainful activity by reason of any

medically determinable physical or mental impairment that

can be expected to result in death or to be of long-continued

and indefinite duration, as certified by a physician acceptable

to the Plan Administrative Committee.

Hours of Service The hours for which you are or will be directly or indirectly

compensated by the Museum including overtime (but only

actual hours worked) and hours for which a back pay award is

made. It also includes paid hours for sick days, disability,

vacation/annual leave, holidays, jury duty, layoff, military duty

and leave of absence, up to five hundred and one (501) hours

in a continuous nonworking period. Hours of Service are used

to calculate your vesting eligibility.

Matching Plan This refers to the Metropolitan Museum of Art 403(b) Matching

Plan for Non-Union Employees.

Plan Year January 1 − December 31

Year of Service A Year of Service means a Plan Year (calendar year) during

which you have not less than one thousand (1,000) Hours of

Service with the Museum. No partial Years of Service count.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 20

Updated for January 1, 2014 2097/51959-001 current/40368379v4

ADMINISTRATION INFORMATION

Plan Name and Number

This Summary Plan Description describes the provisions of the Basic Plan. The full name of

the Basic Plan is The Metropolitan Museum of Art 403(b) Retirement Plan for Non-Union

Employees. The Plan number, which distinguishes the Basic Plan from the other Museum

plans, is 002.

Employer

The Metropolitan Museum of Art

1000 Fifth Avenue

New York, NY 10028

Employer Identification Number

The employer identification number of the Museum assigned by the IRS is 13-1624086.

Type of Plan

The Plan is a Code Section 403(b) plan which provides for a mandatory employee

contribution and employer non-elective contributions.

Plan Administrator

The Metropolitan Museum of Art

1000 Fifth Avenue

New York, NY 10028

212-650-2285

Benefits under the Plan will be paid only if the Plan Administrator (or its delegate) decides in

its discretion that the applicant is entitled to benefits. The Plan Administrative Committee,

members of which are selected by the Board of Trustees, is responsible for administering

and interpreting the Plan on behalf of the Museum.

How Benefits are Funded

The Plan is funded by your contributions and contributions from the Metropolitan Museum of

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 21

Updated for January 1, 2014 2097/51959-001 current/40368379v4

Art. Contributions are held in custodial accounts maintained by Fidelity or in individual

accounts maintained by Voya (formerly ING) (for contributions through June 1, 2013), and are

separate from any Museum assets.

Plan Year

The Plan Year for the Basic Plan is January 1 through December 31.

Legal Process

The Plan will be governed and construed in accordance with the laws of the State of New

York, except as such laws may be superseded by ERISA, the Internal Revenue Code, or

other applicable federal law.

Any legal process related to the Basic Plan should be directed to:

Office of the Senior Vice President, Secretary and General Counsel

The Metropolitan Museum of Art

1000 Fifth Avenue

New York, New York 10028

You may also serve legal process upon the Plan Administrator.

Receiving Financial Advice

If you have questions about financial planning with respect to your benefits under the Basic

Plan, you should seek advice from a personal advisor. The Museum cannot advise you

regarding tax, investment or legal considerations relating to the Basic Plan.

Plan Interpretation

To the fullest extent permitted by law, the Museum will have the exclusive discretion to

determine all matters, including factual matters, relating to eligibility, coverage and benefits

under the Plan. The Museum will also have the exclusive discretion to determine all matters,

including factual matters, relating to interpretation and operation of the Plan. Decisions by the

Museum will be conclusive and binding.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 22

Updated for January 1, 2014 2097/51959-001 current/40368379v4

Benefit Insurance

Benefits under this type of Plan are not insured by the Pension Benefit Guaranty

Corporation (a federal agency that insures certain pension plan benefits upon plan

termination), because the benefits you receive under this type of plan are based upon the

vested amount in your account.

Non-Assignment of Benefits

Your rights and benefits under the Plan cannot be assigned, sold, transferred, or pledged by

you or reached by your creditors or anyone else except under limited circumstances.

However, the law does permit the assignment of all or a portion of your interest in the Plan to

your former spouse or children as part of a Qualified Domestic Relations Order.

Qualified Domestic Relations Order (QDRO)

A Qualified Domestic Relations Order (QDRO) is a legal judgment, decree or order that

recognizes the rights of an alternate payee under the Basic Plan with respect to a child’s or

other person’s support, alimony or marital property rights. The Museum is legally required to

recognize a QDRO. If you become legally separated or divorced, a portion or all of your

benefit under the Basic Plan may be assigned to someone else to satisfy a legal obligation

you may have to a spouse, former spouse, child or other person.

There are specific requirements the court order must meet in order to be recognized by the

Museum. There are also specific procedures regarding the amount and timing of payments.

Participants and Beneficiaries may obtain, without charge, a copy of the procedures

governing QDRO determinations under the Plan from the Plan Administrator by contacting

the Benefits Office in the Human Resources Department.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 23

Updated for January 1, 2014 2097/51959-001 current/40368379v4

Future of the Plan

It is the Museum’s intent that the Basic Plan will continue indefinitely. However, the Museum

reserves the right to amend, modify, suspend or terminate the Plan, in whole or in part, in

accordance with the Plan provisions. Plan amendment, modification, suspension or

termination may be made for any reason, and at any time, and may, in certain

circumstances, result in the reduction or elimination of benefits or other features of the Plan

to the extent allowed by law. In the event the Plan is terminated, your right to your account

will be fully vested.

Continuation of Participation for Employees in the Uniformed

Services (USERRA)

The Uniformed Services Employment and Reemployment Rights Act of 1994 (USERRA)

guarantees certain rights to eligible employees who enter military service. The terms

“Uniformed Services” or “Military Service” mean the Armed Forces (i.e., Army, Navy, Air

Force, Marine Corps, Coast Guard), the reserve components of the Armed Services, the

Army National Guard and the Air National Guard when engaged in active duty for training,

inactive duty training, or full-time National Guard duty, the commissioned corps of the Public

Health Service, and any other category of persons designated by the President in time of war

or national emergency.

Upon reinstatement of employment with the Museum following military service, you are

entitled to the seniority, rights and benefits associated with the position held at the time

employment was interrupted, plus additional seniority, rights and benefits that would have

been attained if employment had not been interrupted. Such leave will not constitute a break

in service.

Military Leave and Plan Loans

If you have a loan from your Plan account, your loan repayments will be suspended while

you are on military leave. Payments will resume once you complete the leave ⎯ at the same

frequency and at least the same amount as your payments before the leave. The term of the

loan will not extend beyond the original term, plus the period of military leave.

When You Return from Military Leave

Upon your return from military leave, you can make additional pre-tax contributions up to the

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 24

Updated for January 1, 2014 2097/51959-001 current/40368379v4

amount you would have been permitted to contribute had you not taken such leave. You can

make these contributions during the period that starts on your return from leave and ends on

the earlier of:

Three times the length of your military leave, and

Five years after your return from military leave.

Heroes Earnings Assistance and Relief Tax Act of 2008 (HEART ACT)

If you are subject to USERRA and die while performing qualified military service, your

survivors are entitled to any benefits under the Plan as if you were an active employee on

the date of your death.

If you think you may be eligible for any of these special rights relating to military leave, please

contact Fidelity at www.plan.fidelity.com/metmuseum or 1-800-343-0860.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 25

Updated for January 1, 2014 2097/51959-001 current/40368379v4

PROCESS FOR SUBMITTING A CLAIM

If you have any questions about the Basic Plan or if you wish to make a claim for benefits,

you should contact the Plan Administrative Committee. If you feel you have a right to a benefit

under the Plan that you have not received, you may file an appeal of the claim for the benefit

determination with the Plan Administrative Committee as provided below.

Claims Procedure

Initial Claim

Any claim that is made with respect to eligibility, participation, contributions, benefits or other

aspects of the operation of the Plan are to be made in writing to a person designated by the

Museum for such purposes (the “Designated Person”). As of the date of this booklet, the

Designated Person is the Plan Administrative Committee. The Designated Person will

provide you with the necessary forms and make all determinations as to the right of any

person to a disputed benefit. If you are denied benefits under the Plan, you will be notified in

writing of the denial of the claim within ninety (90) days after the Designated Person receives

the claim, provided that in the event of special circumstances such period may be extended.

With respect to any claim, the ninety (90) day period may be extended for a period of up to

ninety (90) days (for a total of one hundred eighty (180) days). If the initial ninety (90) day

period is extended, the Designated Person will notify you in writing within ninety (90) days of

receipt of the claim. The written notice of extension will indicate the special circumstances

requiring the extension of time and provide the date by which the Museum expects to make a

determination with respect to the claim. If the extension is required due to your failure to

submit information necessary to decide the claim, the period for making the determination will

be tolled from the date on which the extension notice is sent to you on the earlier of the

following: the date on which you respond to the Designated Person’s request for information,

or expiration of the forty-five (45) day period commencing on the date that you are notified

that the requested additional information must be provided. If notice of the denial of a claim is

not furnished within the required time period described, the claim shall be deemed denied as

of the last day of such period.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 26

Updated for January 1, 2014 2097/51959-001 current/40368379v4

If a Claim Is Wholly or Partially Denied

If your claim is wholly or partially denied, you will be notified of the following:

The specific reason or reasons for the denial,

Specific reference to pertinent Plan provisions upon which the denial is based,

A description of any additional material or information necessary for you to

complete the claim request and an explanation of why such material or information

is necessary,

Appropriate information as to the steps to be taken and the applicable time limits if

you want to submit the adverse determination for review, and

A statement of your right to bring a civil action under Section 502(a) of ERISA

following an adverse determination on review.

Claim Denial Review

If a claim has been wholly or partially denied, you may submit the claim for review by the

Plan Administrative Committee. Any request for review of a claim must be made in writing to

the Museum no later than sixty (60) days after you receive notification of denial or, if no

notification was provided, the date the claim is deemed denied. At this point, you may:

Be provided with reasonable access to, and copies of, relevant documents,

records, and other information relevant to your claim, and

Submit written comments, documents, records, and other information relating to the

claim. The review of the claim determination shall take into account all comments,

documents, records, and other information submitted by you relating to the claim,

without regard to whether such information was submitted or considered in the

initial claim determination.

The decision of the Plan Administrative Committee upon review will be made within sixty (60)

days after receipt of your request for review, unless special circumstances (including, without

limitation, the need to hold a hearing) require an extension. If the sixty (60) day period is

extended, the Museum will, within sixty (60) days of receipt of the claim for review, notify you

in writing. The written notice of extension should indicate the special circumstances requiring

the extension of time and provide the date by which the Museum expects to make a

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 27

Updated for January 1, 2014 2097/51959-001 current/40368379v4

determination with respect to the claim upon review. If the extension is required due to your

failure to submit information necessary to decide the claim, the period for making the

determination will be tolled from the date on which the extension notice is sent to you until

the earlier of the date on which you respond to the Museum’s request for information, or

expiration of the forty-five (45) day period commencing on the date that you are notified that

the requested additional information must be provided.

If notice of the decision upon review is not furnished within the required time period

described, the claim on review shall be deemed denied as of the last day of such period. The

Plan Administrative Committee, in its sole discretion, may hold a hearing regarding the claim

and request that you attend. If a hearing is held, you will be entitled to be represented by

counsel.

The Plan Administrative Committee’s decision upon review of your claim will be

communicated to you in writing. If the claim upon review is denied, the notice to you will

provide:

The specific reason or reasons for the decision, with references to the specific Plan

provisions on which the determination is based,

A statement that you are entitled to receive, upon request and free of charge,

reasonable access to, and copies of, all documents, records and other information

relevant to the claim, and

A statement of your right to bring a civil action under Section 502(a) of ERISA.

A document, record or other information is considered “relevant” to a claim for this purpose if

it was relied upon in making the benefit determination, was submitted, considered, or

generated in the course of making the benefit determination, without regard to whether such

document, record or other information was relied upon in making the benefit determination, or

demonstrates compliance with the administrative process and safeguards required by law

when making the benefit determination.

All interpretations, determinations and decisions of the Designated Person and the Museum

with respect to any claim, including without limitation the appeal of any claim, or any matter

relating to the Plan, will be made by the Designated Person and the Museum, in their sole

discretion, based on the Plan and comments, documents, records, and other information

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 28

Updated for January 1, 2014 2097/51959-001 current/40368379v4

presented to it, and shall be final, conclusive and binding.

The claims procedures set forth in this section are intended to comply with United States

Department of Labor Regulation § 2560.503-1 and should be construed in accordance with

such regulation. In no event shall these procedures be interpreted as expanding the rights of

Claimants beyond what is required by United States Department of Labor Regulation

§ 2560.503-1.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 29

Updated for January 1, 2014 2097/51959-001 current/40368379v4

HOW YOU MAY LOSE BENEFITS

Certain circumstances may reduce or eliminate the benefits you would otherwise receive

from the Plan. For example:

If you are not fully vested when you leave the Museum, you will not be entitled to

the full value of the Museum’s matching contributions made on your behalf.

The amount paid out from the Plan may be less than you anticipated, depending

on the market value of your account in each investment fund at the time your

account is paid out.

Your account cannot be used as collateral or to satisfy any debts or liabilities,

except if a qualified domestic relations order (“QDRO”) so decrees. Then,

money in your Plan account may be payable to someone other than you or your

designated beneficiary.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 30

Updated for January 1, 2014 2097/51959-001 current/40368379v4

YOUR RIGHTS UNDER ERISA

As a participant in the Basic Plan, you are entitled to certain rights and protections under the

Employee Retirement Income Security Act of 1974 (ERISA). ERISA provides that all Plan

participants shall be entitled to:

Receive Information About Your Plan and Benefits

Examine, without charge, at the Museum’s Human Resources Department and at

other specified locations, such as work sites, all documents governing the Plan

including a copy of the latest annual report (Form 5500 Series) filed by the Plan

with the U.S. Department of Labor and available at the Public Disclosure Room of

the Employee Benefits Security Administration.

Obtain, upon written request to the Museum, copies of documents governing the

operation of the Plan, including copies of the latest annual report (Form 5500

Series). The Museum may make a reasonable charge for the copies.

Receive a summary of the Plan’s annual financial report. The Museum is required

by law to furnish each participant with a copy of this summary annual report.

Obtain a statement telling you whether you have a right to receive a benefit at your

normal retirement age (age 62) and if so, what your benefits would be at normal

retirement age under the Plan if you stop working now. If you do not have a right to

a benefit, the statement will tell you how many more years you need to work in

order to have a right to a benefit. This statement must be requested in writing and

is not required to be given more than once every 12 months. The Plan must

provide the statement free of charge.

Prudent Actions by Plan Fiduciaries

In addition to creating rights for Plan participants, ERISA imposes duties upon the people

who are responsible for the operation of the employee benefit plan. The people who operate

your Plan, called “fiduciaries” of the Plan, have a duty to do so prudently and in the interest of

you and other Plan participants and Beneficiaries. No one, including your employer or any

other person, may fire you or otherwise discriminate against you in any way to prevent you

from obtaining a benefit or exercising your rights under ERISA.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 31

Updated for January 1, 2014 2097/51959-001 current/40368379v4

Enforce Your Rights

If your claim for a benefit is denied or ignored, in whole or in part, you have the right to know

why this was done, to obtain copies of documents relating to the decision without charge,

and to appeal any denial, all within certain time schedules. Under ERISA, there are steps you

can take to enforce the above rights. For instance, if you request a copy of the Plan

document or the latest annual report from the Plan and do not receive them within 30 days,

you may file suit in a Federal court. In such a case, the court may require the Museum to

provide the materials and pay you up to $110 a day until you receive the materials, unless

the materials were not sent because of reasons beyond the control of the administrator.

If you have a claim for benefits that is denied or ignored, in whole or in part, you may file a suit

in a state or federal court, but only after you have exhausted the Plan’s claims and appeals

procedures as described in the “Process for Submitting a Claim” section of this booklet. In

addition, if you disagree with the Plan’s decision or lack thereof concerning the qualified status

of a domestic relations order, you may file suit in a Federal court, but only after you have

exhausted the Plan’s claims and appeals procedures as applicable to such determination.

If Plan fiduciaries misuse the Plan’s money, or if you are discriminated against for asserting

your rights, you may seek assistance from the U.S. Department of Labor, or you may file suit

in a federal court. The court will decide who should pay court costs and legal fees. If you are

successful, the court may order the person you have sued to pay these costs and fees.

If you lose, the court may order you to pay these costs and fees, for example, if the court

finds your claim is frivolous.

Assistance with Your Questions

If you have any questions about the Basic Plan, you should contact the Plan Administrator. If

you have any questions about this statement or about your rights under ERISA, or if you

need assistance in obtaining documents from the Plan Administrator, you should contact the

nearest office of the Employee Benefits Security Administration, U.S. Department of Labor,

listed in your telephone directory or the Division of Technical Assistance and Inquiries,

Employee Benefits Security Administration, U.S. Department of Labor, 200 Constitution

Avenue, N.W., Washington, DC 20210. You may also obtain certain publications about your

rights and responsibilities under ERISA by calling the publications hotline of the Employee

Benefits Security Administration.

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 32

Updated for January 1, 2014 2097/51959-001 current/40368379v4

APPENDIX A – INVESTMENT OPTIONS

Tier 1 – Target Date Retirement Funds

Target Date Retirement Funds are one-decision funds designed for investors who don’t

necessarily have the time or knowledge to create and maintain a retirement portfolio, or the

interest in doing so. Each Target Date Retirement Fund invests in broadly diversified

Vanguard funds — most of which are index-based — and is a complete portfolio in itself.

When you pick a Target Date Retirement Fund, you have one less thing to worry about,

because the asset allocation in your retirement portfolio will contain the diversification and

risk mix appropriate for your age. Currently, Fidelity offers the following 12 Vanguard Target

Date Retirement Funds:

Vanguard Target Retirement Income Fund Investor Shares

Vanguard Target Retirement 2010 Fund Investor Shares

Vanguard Target Retirement 2015 Fund Investor Shares

Vanguard Target Retirement 2020 Fund Investor Shares

Vanguard Target Retirement 2025 Fund Investor Shares

Vanguard Target Retirement 2030 Fund Investor Shares

Vanguard Target Retirement 2035 Fund Investor Shares

Vanguard Target Retirement 2040 Fund Investor Shares

Vanguard Target Retirement 2045 Fund Investor Shares

Vanguard Target Retirement 2050 Fund Investor Shares

Vanguard Target Retirement 2055 Fund Investor Shares

Vanguard Target Retirement 2060 Fund Investor Shares

Tier 2 – Index Funds

Index funds are mutual funds that are intended to match the performance of a market

benchmark at a low cost. For those who want to assume a greater involvement in the

management of their own investments, these options provide the flexibility to build your own

strategy to meet your needs. Fund options include:

403(b) Retirement Plan for Non-Union Employees (the “Basic Plan”) SPD 33

Updated for January 1, 2014 2097/51959-001 current/40368379v4

Vanguard 500 Index Fund Signal Class

Vanguard Developed Markets Index Fund Admiral Shares

Vanguard Emerging Markets Stock Index Fund Signal Shares

Vanguard Extended Market Index Fund Signal Shares

Vanguard Short-Term Bond Index Fund Signal Shares

Vanguard Intermediate-Term Government Bond Index Fund Signal Shares

Vanguard Total Bond Market Index Fund Signal Shares

Tier 3 – Actively Managed Funds

Actively managed funds seek to outperform the market (although they can also

underperform the market). They typically have higher fees than index funds because they

are actively managed by a portfolio manager who is buying and selling securities to meet

the fund’s investment objectives. You may want to consider these options if you are

comfortable diversifying your investments on your own. Fund options include:

Fidelity® Strategic Real Return Fund*

GMO Benchmark-Free Allocation Series Fund Class R6

LKCM Small Capital Equity Fund Class Institutional

MFS Institutional International Equity Fund

Vanguard Prime Money Market Fund Investor Class

Vanguard Wellington Fund Admiral Shares

Vanguard Windsor II Fund Admiral Shares

*Short-term Redemption Fee of 0.75% for shares held less than 60 days

Voya (formerly ING) Fund Closed to New Contributions and Investments June 1, 2013

The Voya (formerly ING) “Fixed Account” was closed to new contributions and investments

effective June 1, 2013. Current balances may remain with Voya, but no future contributions

can move into the account.