res - status quo, potential and prospects · res - status quo, potential and prospects ......

TRANSCRIPT

RES - Status Quo, Potential and Prospects

Vasileios Tsolakidis, CRES

20 June 2017, Thessaloniki

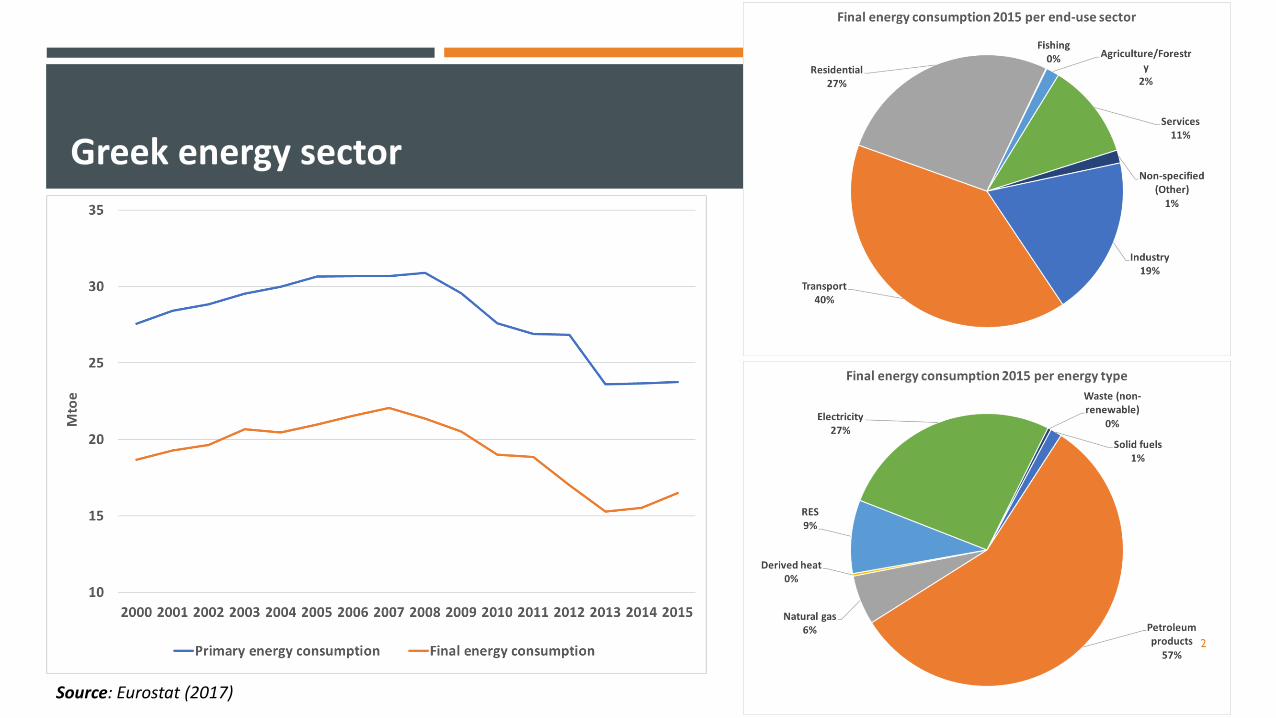

Greek energy sector

2

Source: Eurostat (2017)

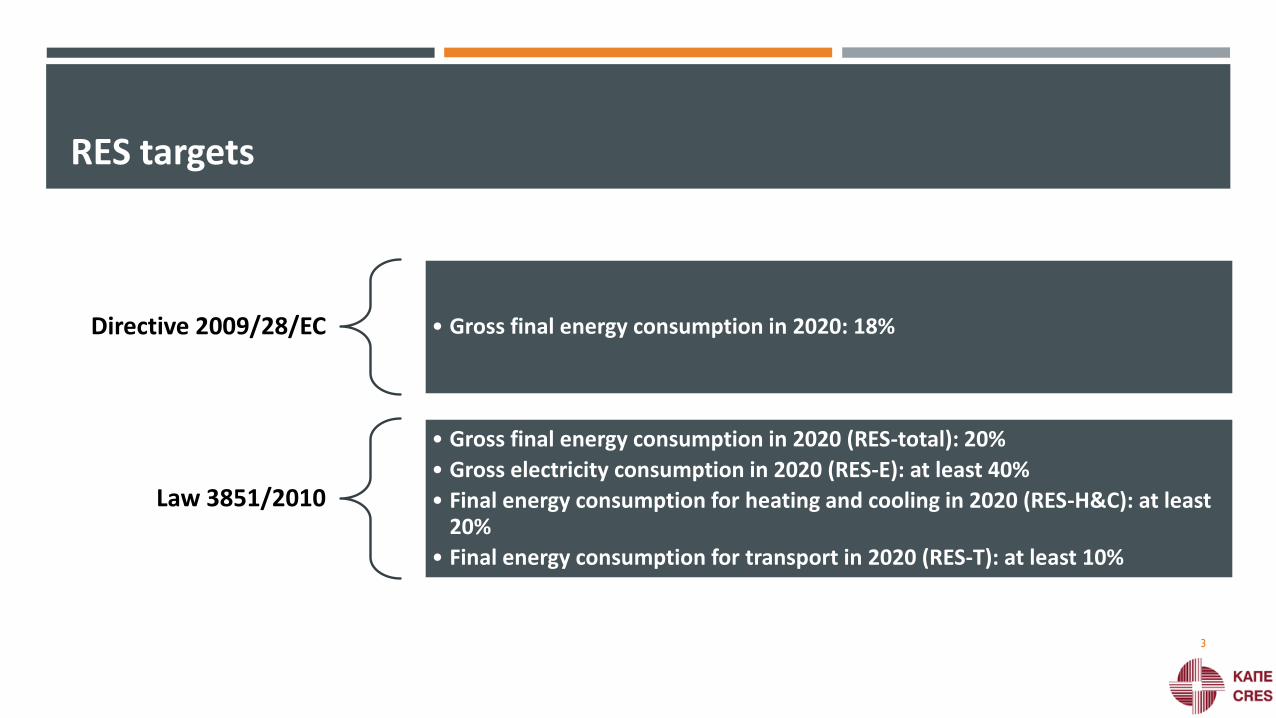

RES targets

Directive 2009/28/EC • Gross final energy consumption in 2020: 18%

Law 3851/2010

• Gross final energy consumption in 2020 (RES-total): 20%

• Gross electricity consumption in 2020 (RES-E): at least 40%

• Final energy consumption for heating and cooling in 2020 (RES-H&C): at least 20%

• Final energy consumption for transport in 2020 (RES-T): at least 10%

3

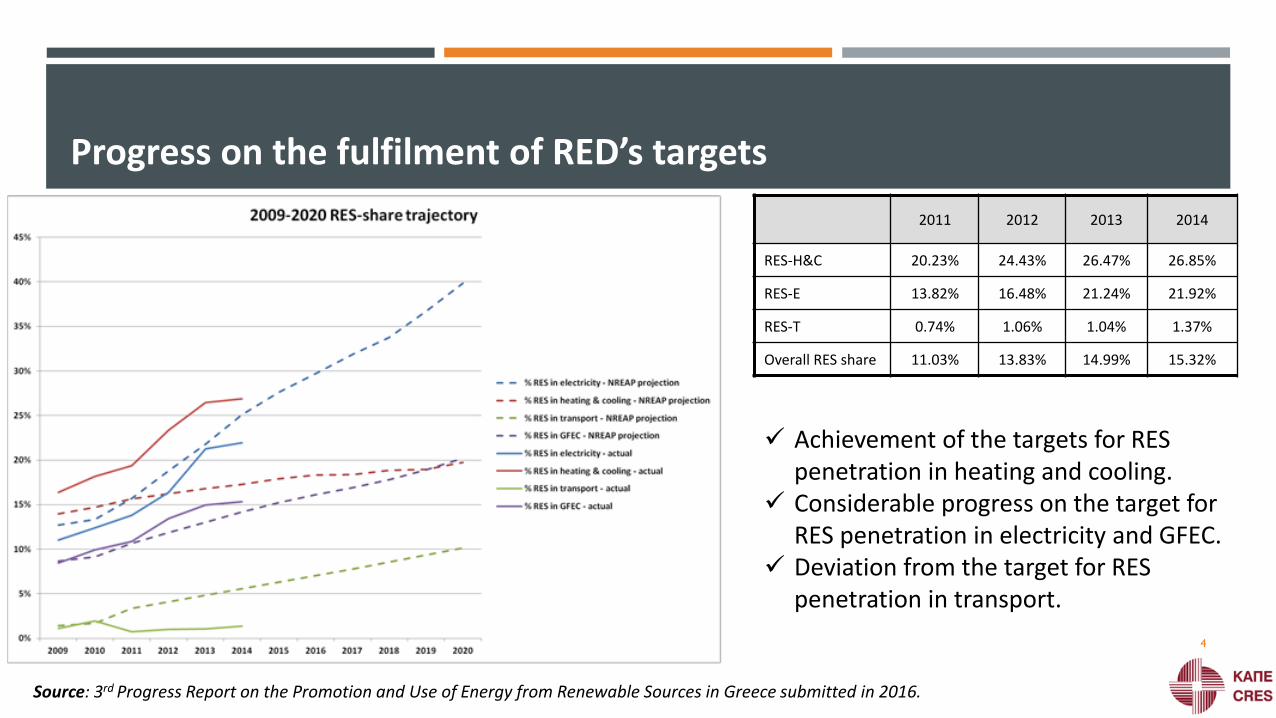

Progress on the fulfilment of RED’s targets

2011 2012 2013 2014

RES-H&C 20.23% 24.43% 26.47% 26.85%

RES-E 13.82% 16.48% 21.24% 21.92%

RES-T 0.74% 1.06% 1.04% 1.37%

Overall RES share 11.03% 13.83% 14.99% 15.32%

✓ Achievement of the targets for RES penetration in heating and cooling.

✓ Considerable progress on the target for RES penetration in electricity and GFEC.

✓ Deviation from the target for RES penetration in transport.

Source: 3rd Progress Report on the Promotion and Use of Energy from Renewable Sources in Greece submitted in 2016.

4

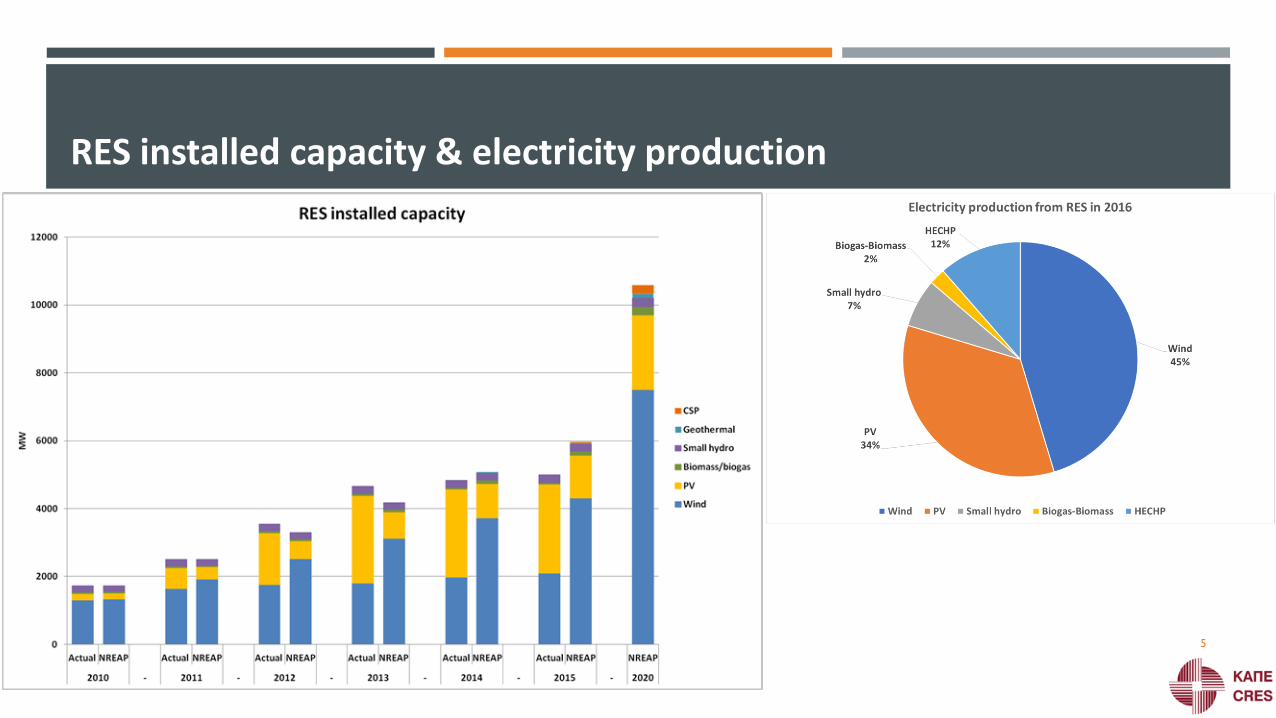

RES installed capacity & electricity production

5

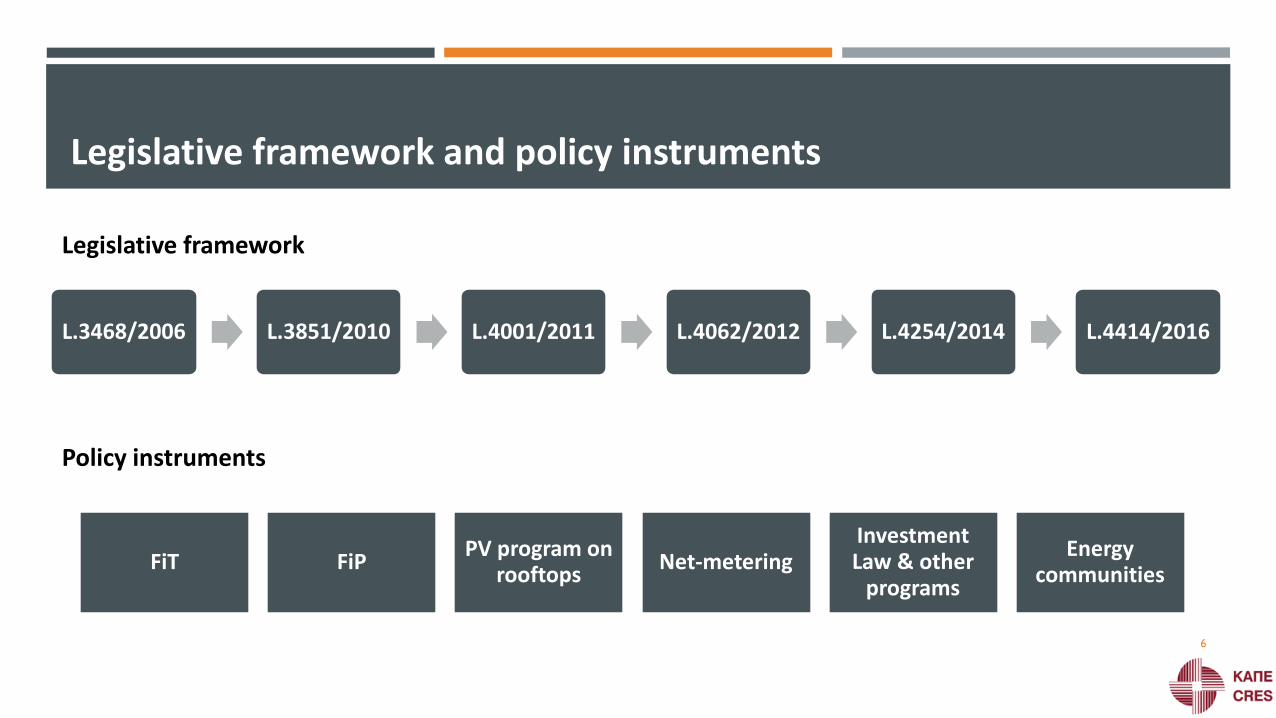

Legislative framework and policy instruments

L.3468/2006 L.3851/2010 L.4001/2011 L.4062/2012 L.4254/2014 L.4414/2016

FiT FiPPV program on

rooftopsNet-metering

Investment Law & other

programs

Energy communities

Legislative framework

Policy instruments

6

FiP

The Feed-in-Premium scheme was introduced from 01.01.2016 according to the foreseen requirements and provisions of the EC State Aid Guidelines for Environmental Protection and Energy 2014-2020.

Exemptions to specific categories giving the opportunity to receive the granted aid in the form of FiT.

RES plants should be subjected to specific obligations based on their direct participation in the electricity market providing incentives in order to optimize their hourly generation forecasts during the transitory period.

Adoption of competitive bidding processes for granting the relevant RES operating aid from 01.01.2017.

The first round of a competitive bidding process equal to at minimum 5% of the new installed RES capacity in the period 2015-2016 was conducted within 2016.

7

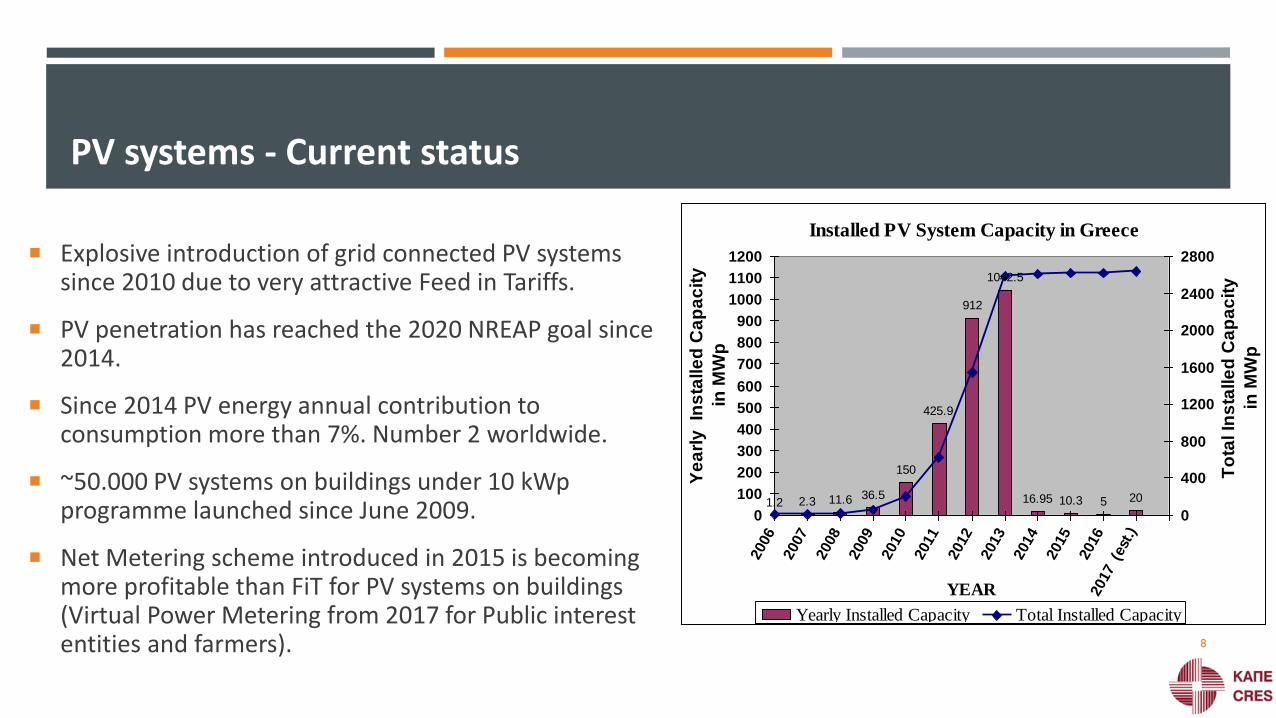

Installed PV System Capacity in Greece

1.2 2.3 11.6 36.5

150

425.9

912

1042.5

16.95 10.3 5 20

0

100

200

300

400

500

600

700

800

900

1000

1100

1200

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017 (

est

.)

YEAR

Ye

arl

y In

sta

lle

d C

ap

ac

ity

in M

Wp

0

400

800

1200

1600

2000

2400

2800

To

tal In

sta

lle

d C

ap

ac

ity

in M

Wp

Yearly Installed Capacity Total Installed Capacity

PV systems - Current status

Explosive introduction of grid connected PV systems since 2010 due to very attractive Feed in Tariffs.

PV penetration has reached the 2020 NREAP goal since 2014.

Since 2014 PV energy annual contribution to consumption more than 7%. Number 2 worldwide.

~50.000 PV systems on buildings under 10 kWpprogramme launched since June 2009.

Net Metering scheme introduced in 2015 is becoming more profitable than FiT for PV systems on buildings (Virtual Power Metering from 2017 for Public interest entities and farmers). 8

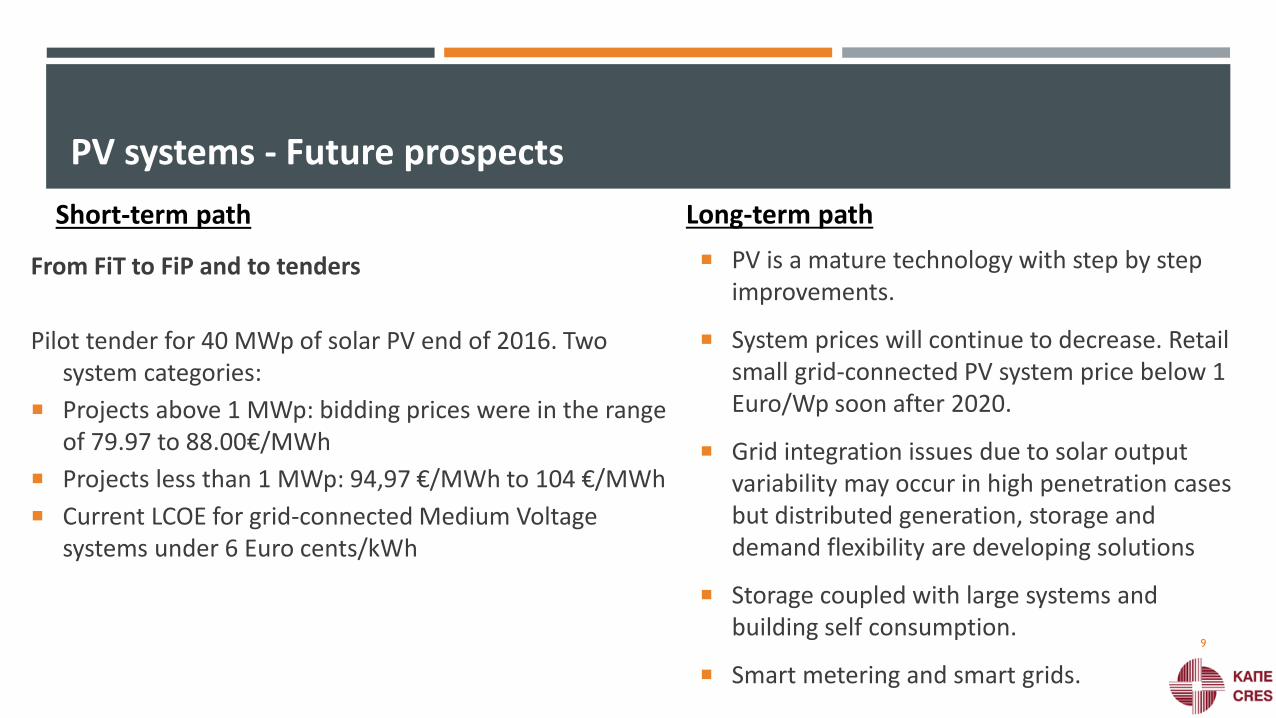

From FiT to FiP and to tenders

Pilot tender for 40 MWp of solar PV end of 2016. Two system categories:

Projects above 1 MWp: bidding prices were in the range of 79.97 to 88.00€/MWh

Projects less than 1 MWp: 94,97 €/MWh to 104 €/MWh

Current LCOE for grid-connected Medium Voltage systems under 6 Euro cents/kWh

PV systems - Future prospects

PV is a mature technology with step by step improvements.

System prices will continue to decrease. Retail small grid-connected PV system price below 1 Euro/Wp soon after 2020.

Grid integration issues due to solar output variability may occur in high penetration cases but distributed generation, storage and demand flexibility are developing solutions

Storage coupled with large systems and building self consumption.

Smart metering and smart grids.

Short-term path Long-term path

9

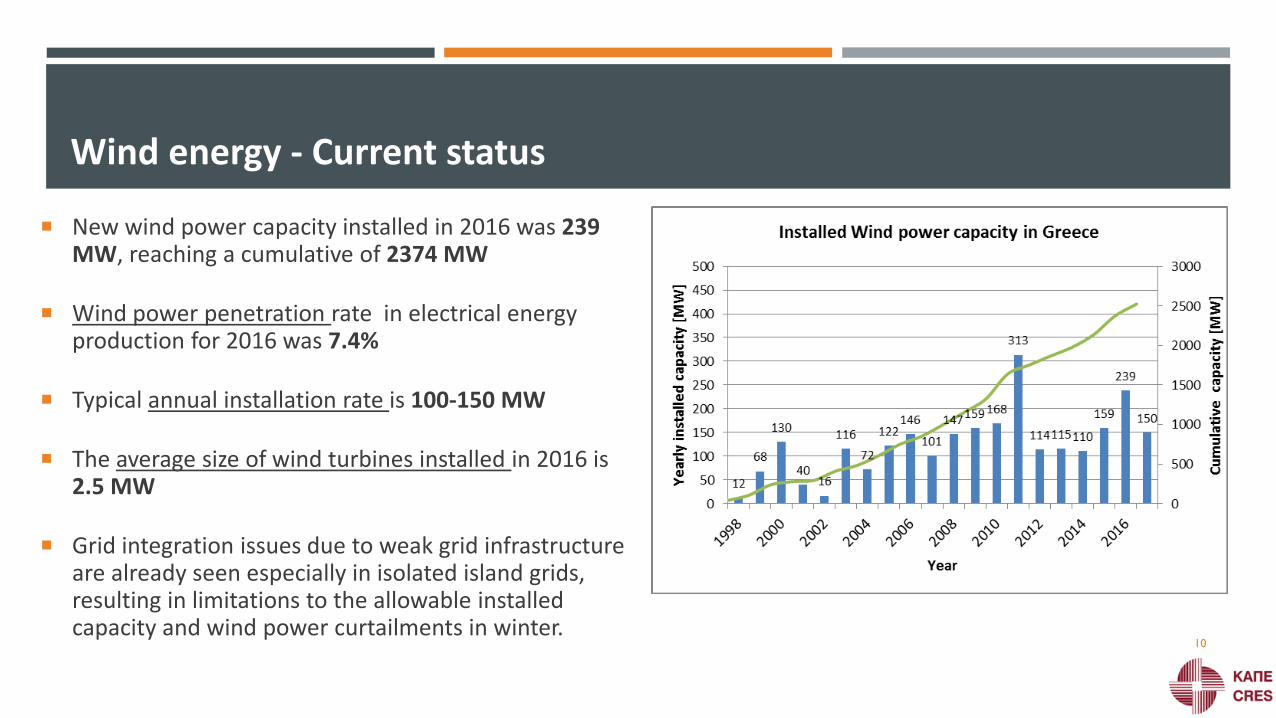

Wind energy - Current status

New wind power capacity installed in 2016 was 239 MW, reaching a cumulative of 2374 MW

Wind power penetration rate in electrical energy production for 2016 was 7.4%

Typical annual installation rate is 100-150 MW

The average size of wind turbines installed in 2016 is 2.5 MW

Grid integration issues due to weak grid infrastructure are already seen especially in isolated island grids, resulting in limitations to the allowable installed capacity and wind power curtailments in winter.

10

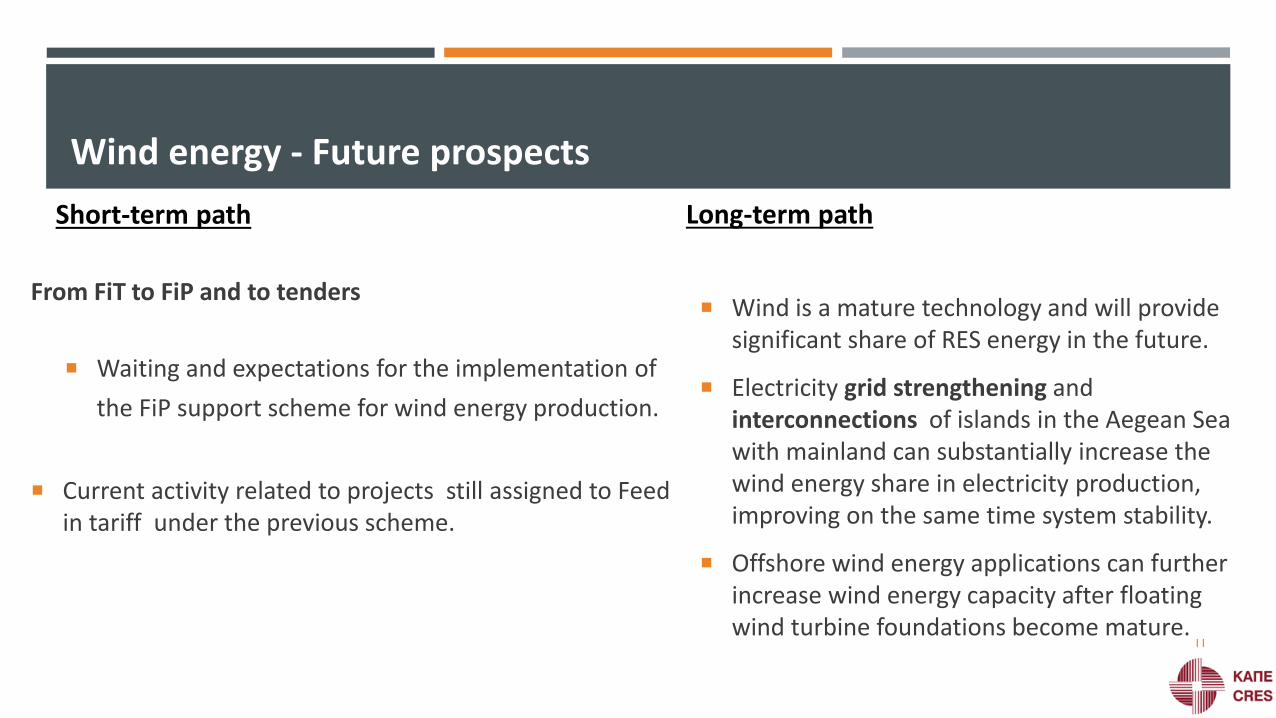

From FiT to FiP and to tenders

Waiting and expectations for the implementation of

the FiP support scheme for wind energy production.

Current activity related to projects still assigned to Feed in tariff under the previous scheme.

Wind energy - Future prospects

Wind is a mature technology and will provide significant share of RES energy in the future.

Electricity grid strengthening and interconnections of islands in the Aegean Sea with mainland can substantially increase the wind energy share in electricity production, improving on the same time system stability.

Offshore wind energy applications can further increase wind energy capacity after floating wind turbine foundations become mature.

Short-term path Long-term path

11

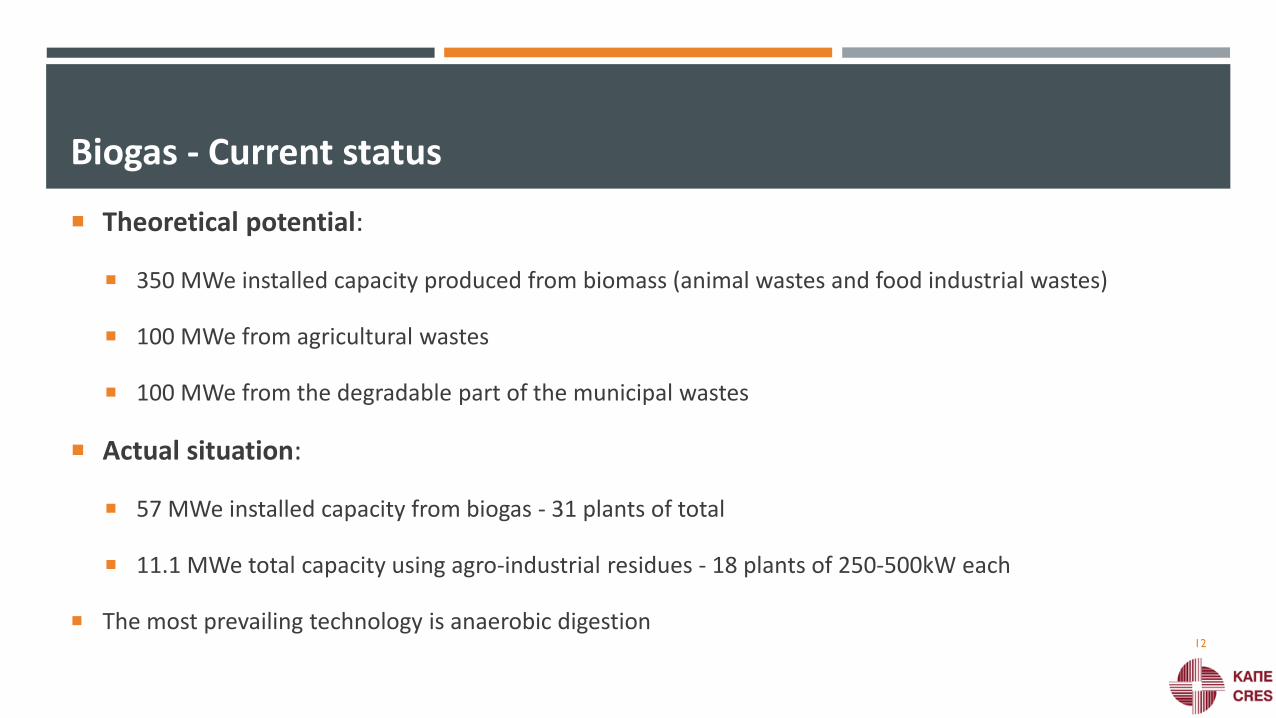

Biogas - Current status

Theoretical potential:

350 MWe installed capacity produced from biomass (animal wastes and food industrial wastes)

100 MWe from agricultural wastes

100 MWe from the degradable part of the municipal wastes

Actual situation:

57 MWe installed capacity from biogas - 31 plants of total

11.1 MWe total capacity using agro-industrial residues - 18 plants of 250-500kW each

The most prevailing technology is anaerobic digestion12

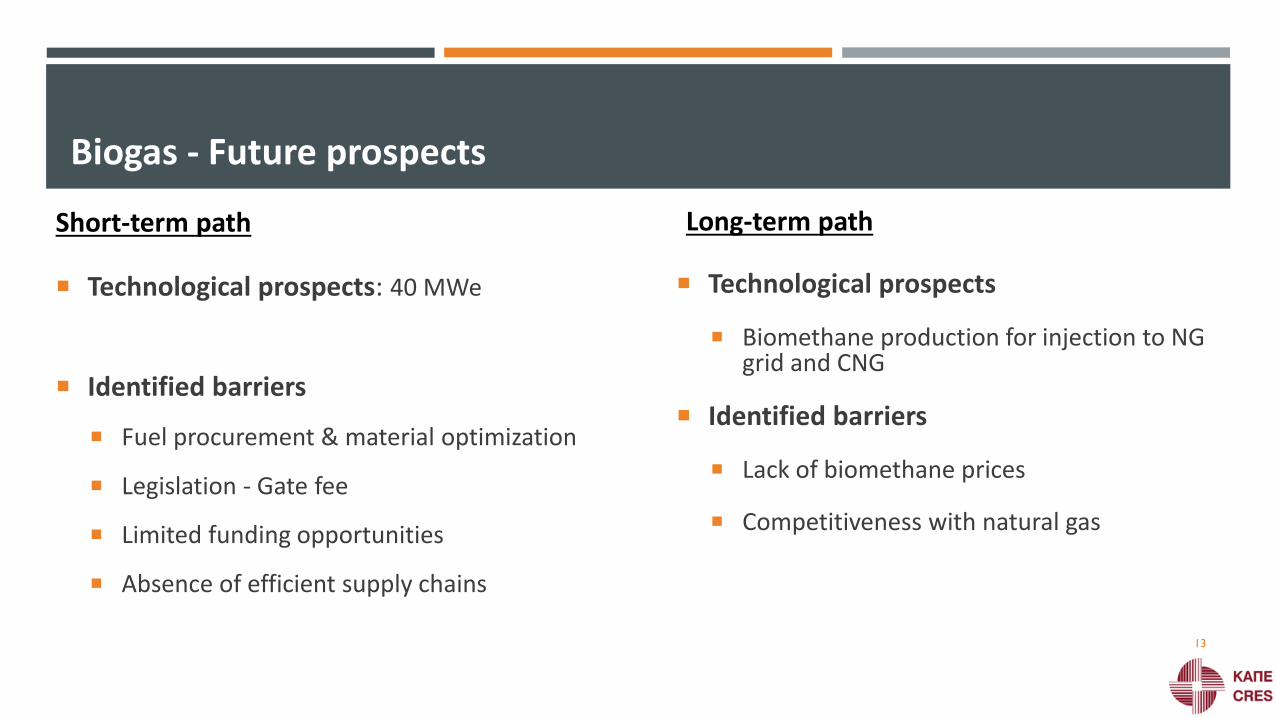

Biogas - Future prospects

Technological prospects: 40 MWe

Identified barriers

Fuel procurement & material optimization

Legislation - Gate fee

Limited funding opportunities

Absence of efficient supply chains

Technological prospects

Biomethane production for injection to NG grid and CNG

Identified barriers

Lack of biomethane prices

Competitiveness with natural gas

Short-term path Long-term path

13

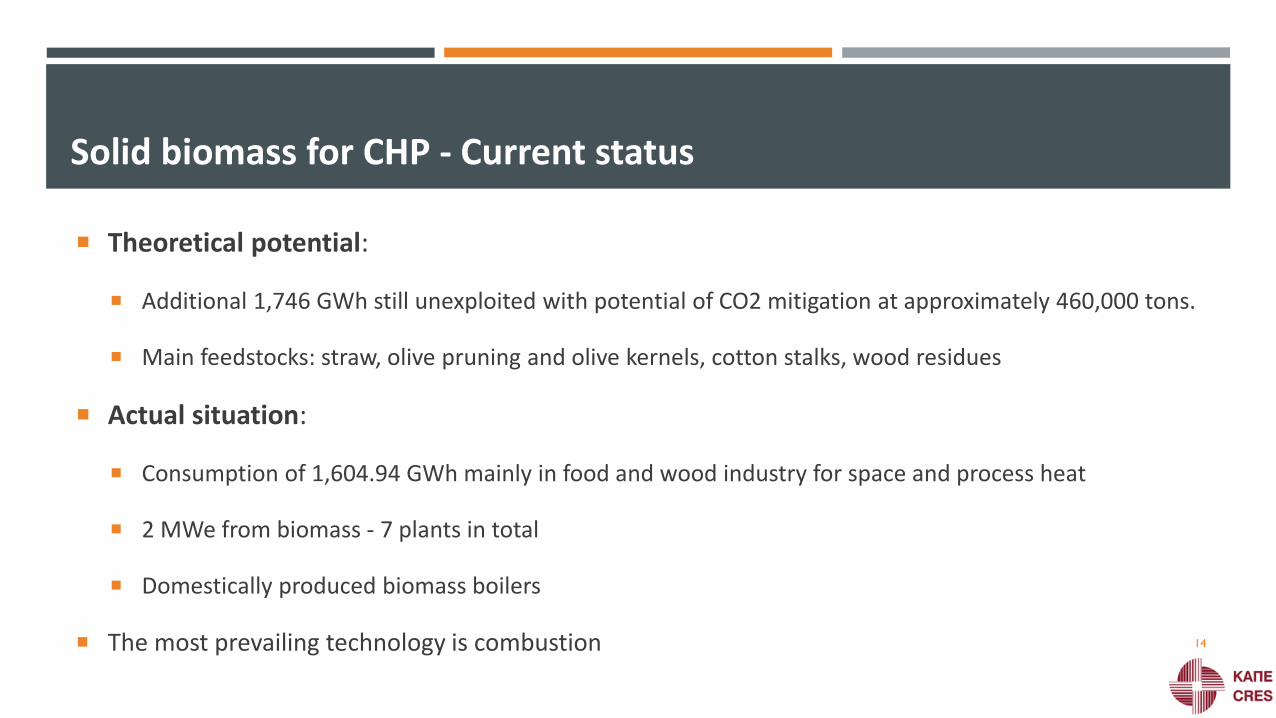

Solid biomass for CHP - Current status

Theoretical potential:

Additional 1,746 GWh still unexploited with potential of CO2 mitigation at approximately 460,000 tons.

Main feedstocks: straw, olive pruning and olive kernels, cotton stalks, wood residues

Actual situation:

Consumption of 1,604.94 GWh mainly in food and wood industry for space and process heat

2 MWe from biomass - 7 plants in total

Domestically produced biomass boilers

The most prevailing technology is combustion 14

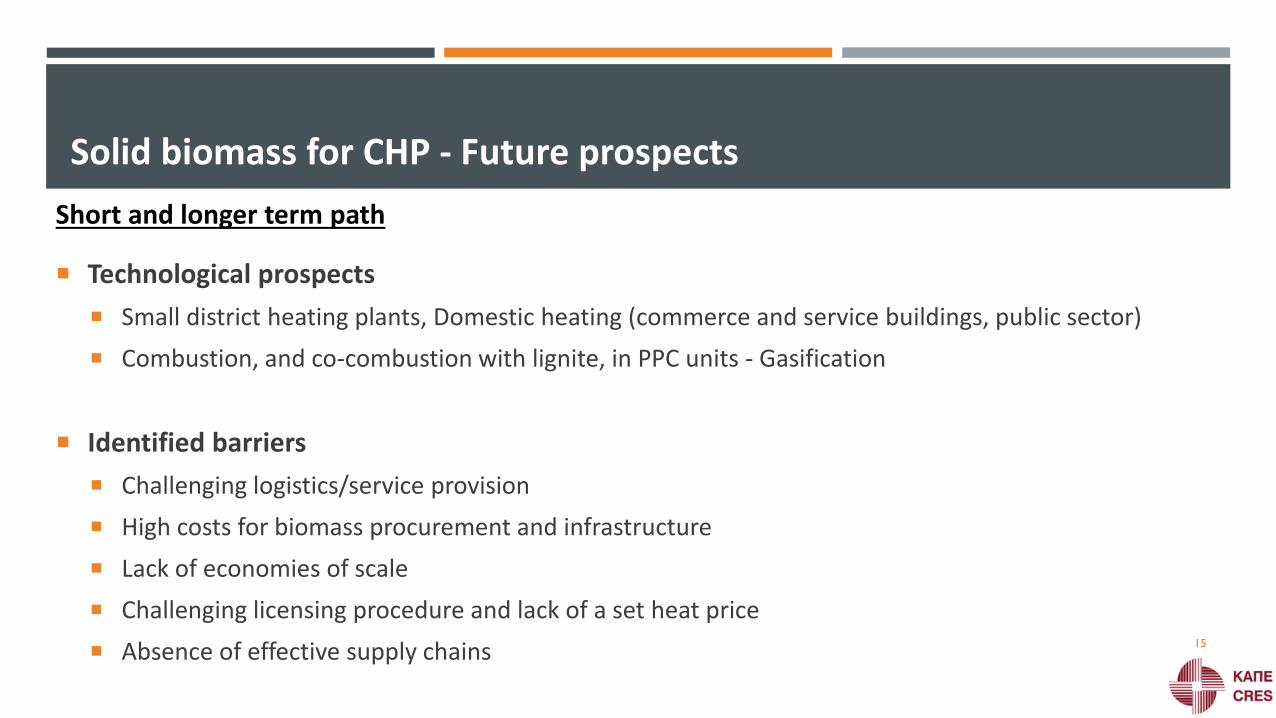

Solid biomass for CHP - Future prospects

Technological prospects

Small district heating plants, Domestic heating (commerce and service buildings, public sector)

Combustion, and co-combustion with lignite, in PPC units - Gasification

Identified barriers

Challenging logistics/service provision

High costs for biomass procurement and infrastructure

Lack of economies of scale

Challenging licensing procedure and lack of a set heat price

Absence of effective supply chains

Short and longer term path

15

Biofuels - Current status

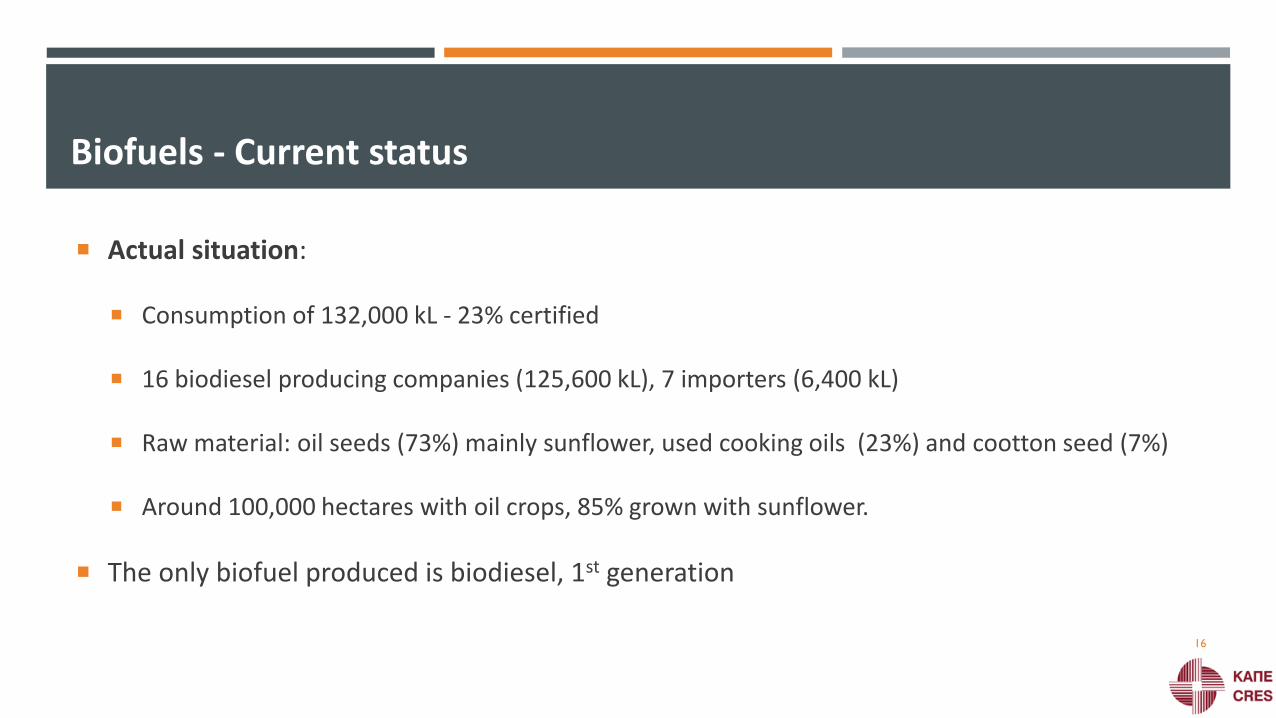

Actual situation:

Consumption of 132,000 kL - 23% certified

16 biodiesel producing companies (125,600 kL), 7 importers (6,400 kL)

Raw material: oil seeds (73%) mainly sunflower, used cooking oils (23%) and cootton seed (7%)

Around 100,000 hectares with oil crops, 85% grown with sunflower.

The only biofuel produced is biodiesel, 1st generation

16

Biofuels - Future prospects

Technological prospects

Advanced biofuels

Identified barriers

Technologies still not mature

High investment costs

Limited funding opportunities

Recommendations

R&D efforts towards more efficient technologies

Short and longer term path

17

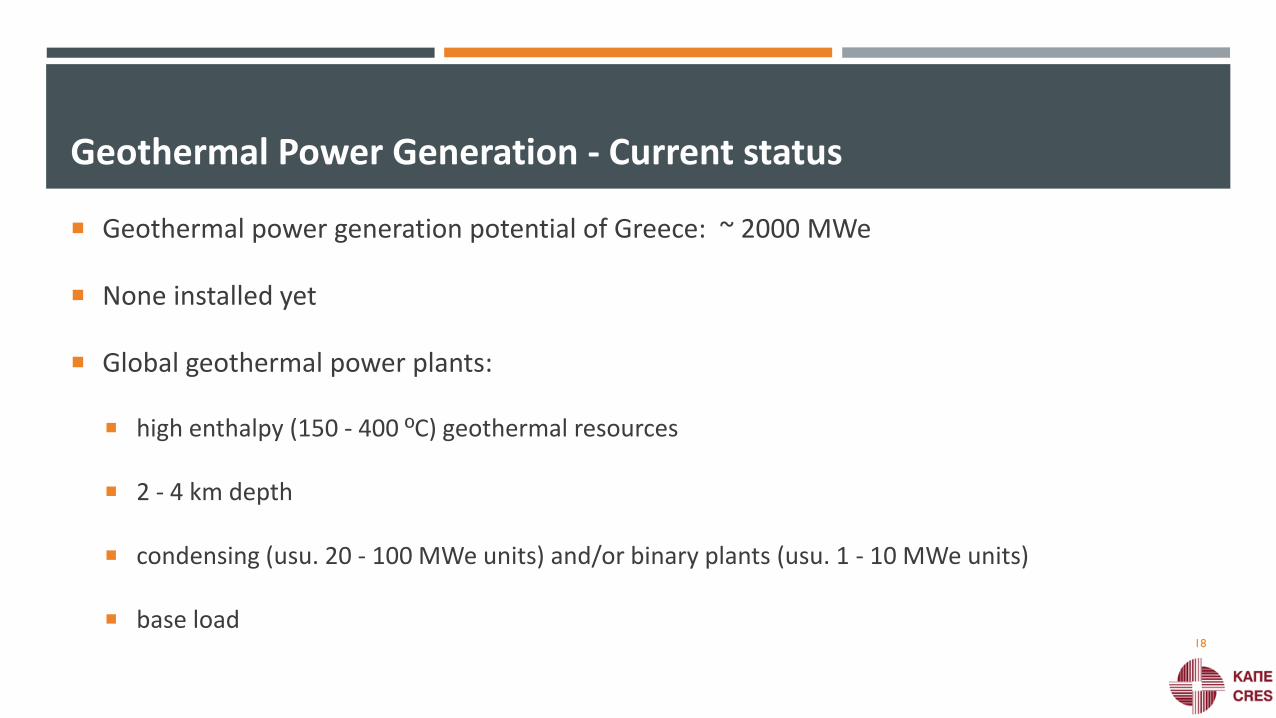

Geothermal Power Generation - Current status

Geothermal power generation potential of Greece: ~ 2000 MWe

None installed yet

Global geothermal power plants:

high enthalpy (150 - 400 ºC) geothermal resources

2 - 4 km depth

condensing (usu. 20 - 100 MWe units) and/or binary plants (usu. 1 - 10 MWe units)

base load18

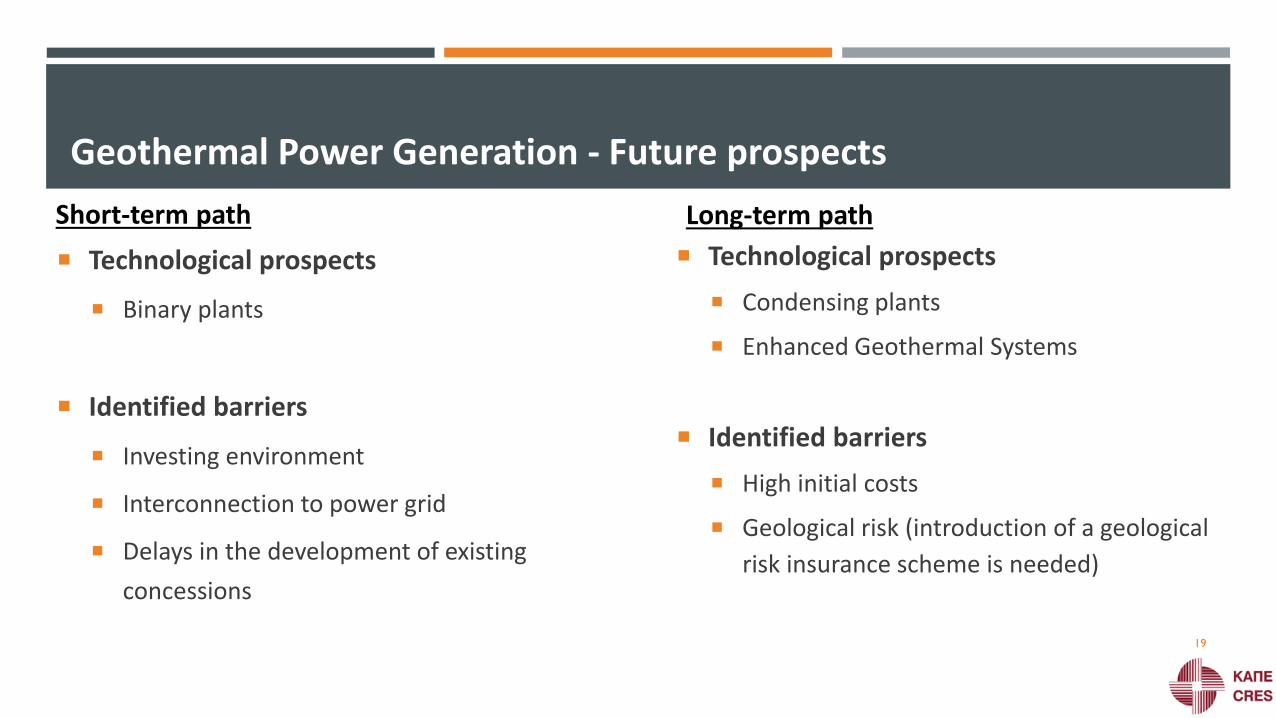

Geothermal Power Generation - Future prospects

Technological prospects

Binary plants

Identified barriers

Investing environment

Interconnection to power grid

Delays in the development of existing

concessions

Technological prospects

Condensing plants

Enhanced Geothermal Systems

Identified barriers

High initial costs

Geological risk (introduction of a geological

risk insurance scheme is needed)

Short-term path Long-term path

19

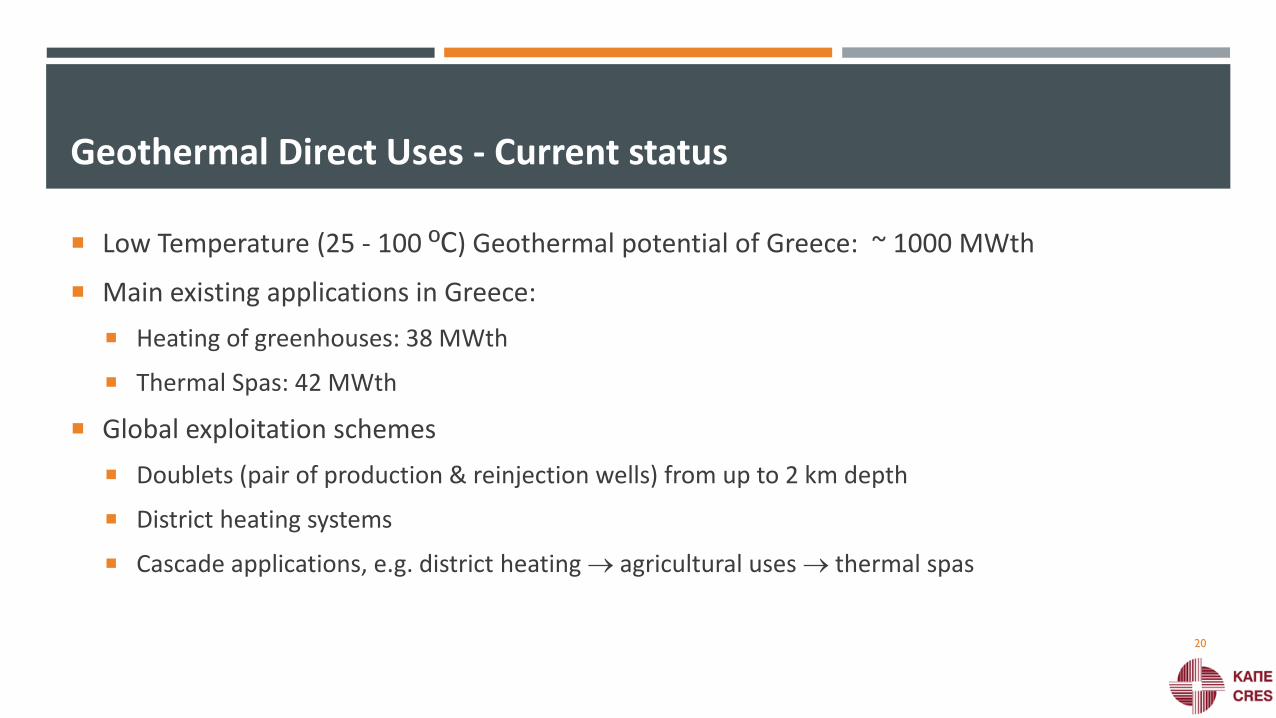

Geothermal Direct Uses - Current status

Low Temperature (25 - 100 ºC) Geothermal potential of Greece: ~ 1000 MWth

Main existing applications in Greece:

Heating of greenhouses: 38 MWth

Thermal Spas: 42 MWth

Global exploitation schemes

Doublets (pair of production & reinjection wells) from up to 2 km depth

District heating systems

Cascade applications, e.g. district heating agricultural uses thermal spas

20

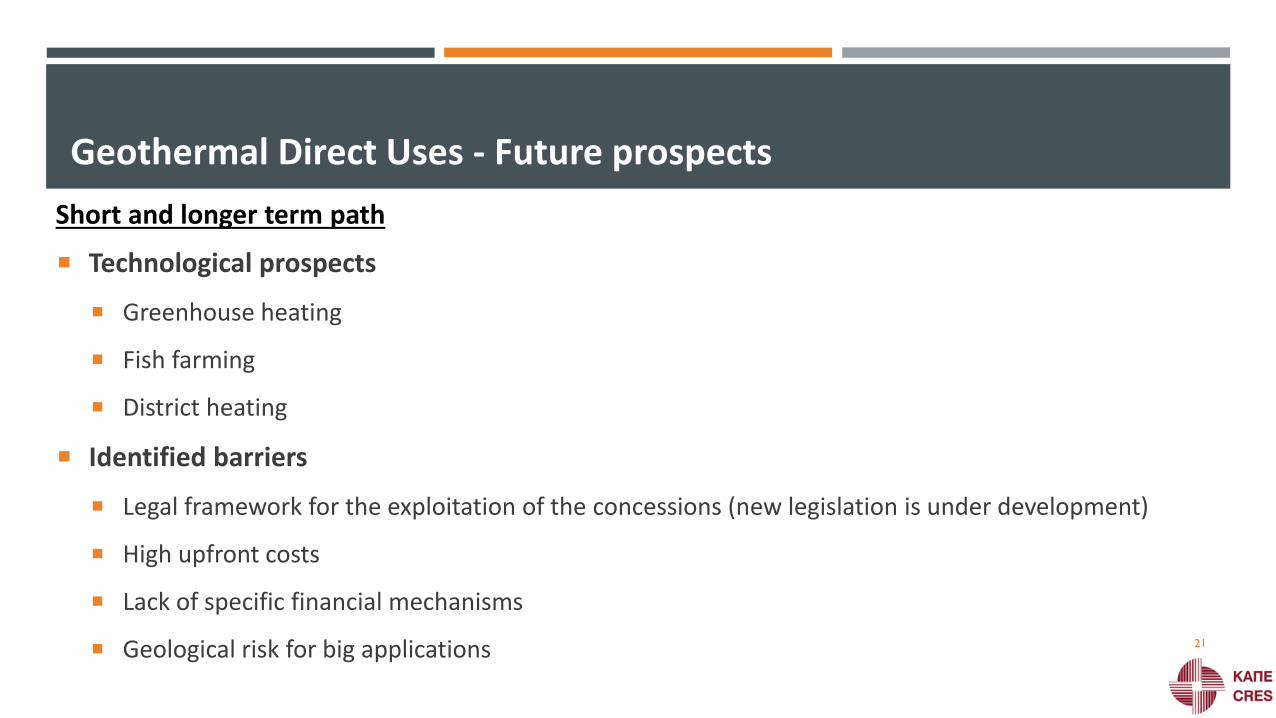

Geothermal Direct Uses - Future prospects

Technological prospects

Greenhouse heating

Fish farming

District heating

Identified barriers

Legal framework for the exploitation of the concessions (new legislation is under development)

High upfront costs

Lack of specific financial mechanisms

Geological risk for big applications

Short and longer term path

21

Ground Source Heat Pumps - Current status

Shallow Geothermal potential of Greece: can cover all heating/cooling needs of buildings

Main applications in Greece: approximately 3000 units of 150 MWth total installed capacity

Horizontal systems

Borehole heat exchangers

Open loops

Seawater source systems

22

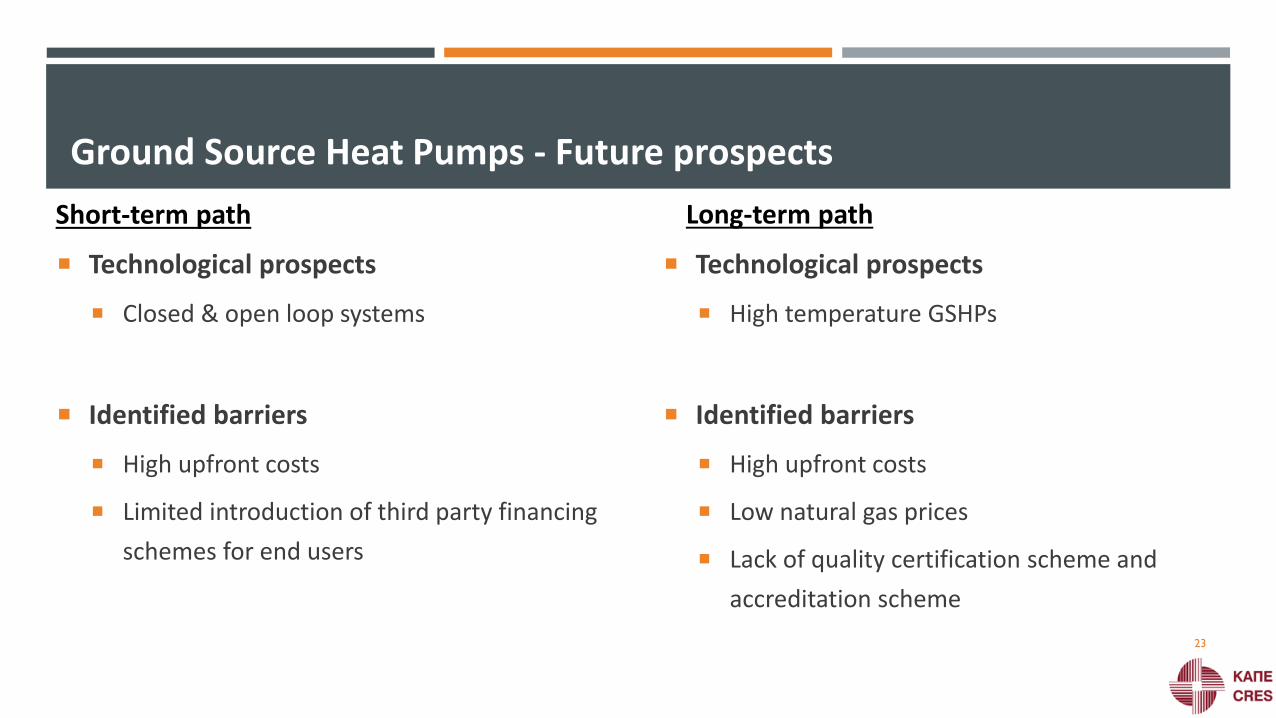

Ground Source Heat Pumps - Future prospects

Short-term path Long-term path

Technological prospects

Closed & open loop systems

Identified barriers

High upfront costs

Limited introduction of third party financing

schemes for end users

Technological prospects

High temperature GSHPs

Identified barriers

High upfront costs

Low natural gas prices

Lack of quality certification scheme and

accreditation scheme

23

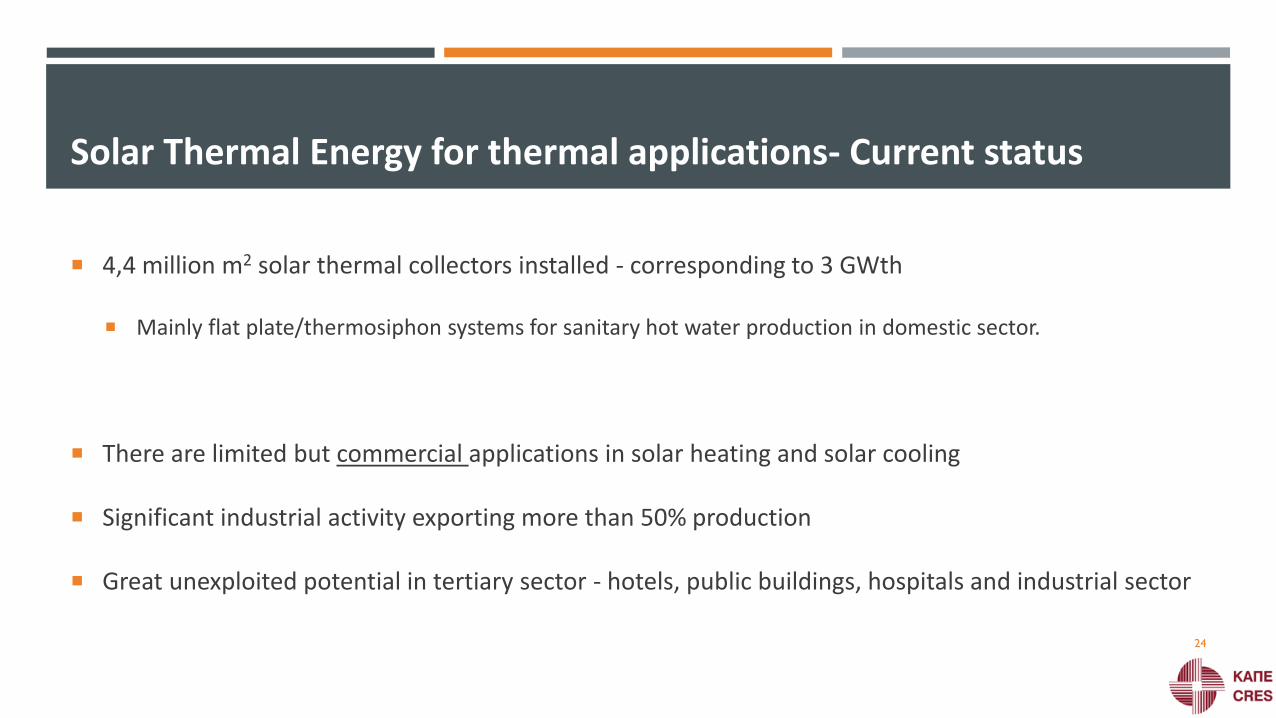

Solar Thermal Energy for thermal applications- Current status

4,4 million m2 solar thermal collectors installed - corresponding to 3 GWth

Mainly flat plate/thermosiphon systems for sanitary hot water production in domestic sector.

There are limited but commercial applications in solar heating and solar cooling

Significant industrial activity exporting more than 50% production

Great unexploited potential in tertiary sector - hotels, public buildings, hospitals and industrial sector

24

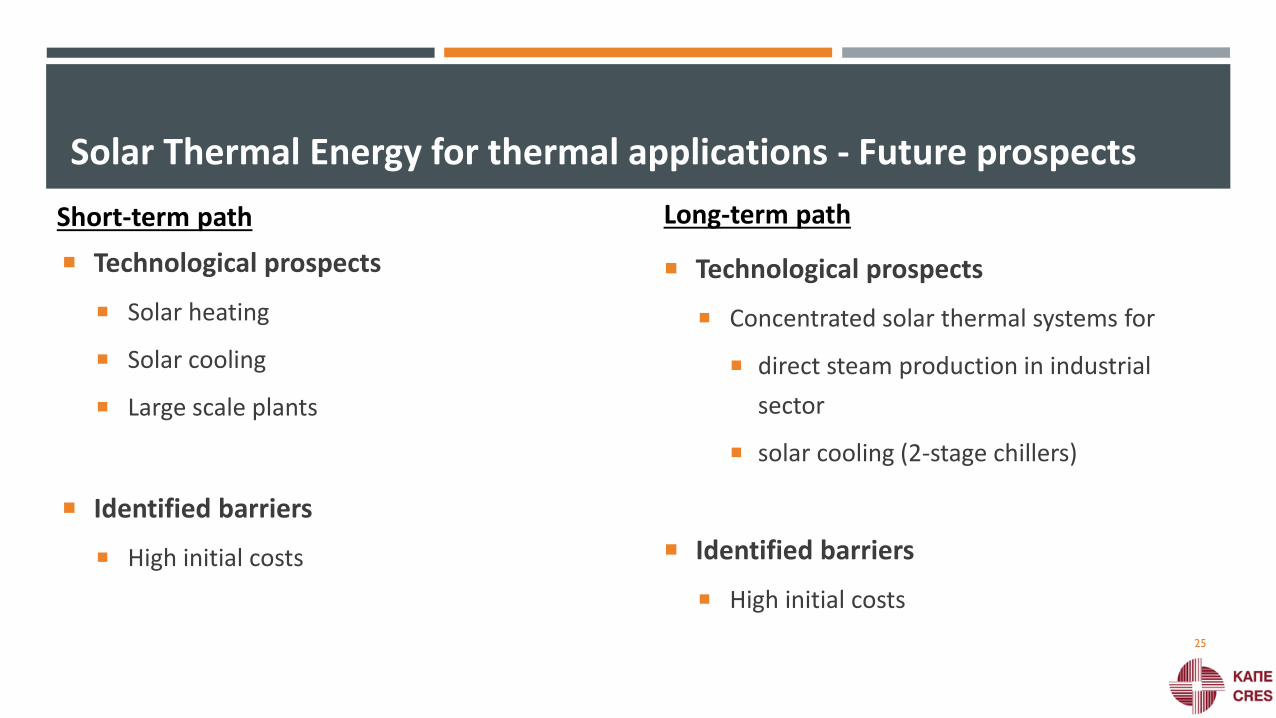

Solar Thermal Energy for thermal applications - Future prospects

Technological prospects

Solar heating

Solar cooling

Large scale plants

Identified barriers

High initial costs

Short-term path Long-term path

Technological prospects

Concentrated solar thermal systems for

direct steam production in industrial

sector

solar cooling (2-stage chillers)

Identified barriers

High initial costs

25

CSP - Solar Thermal Energy for power applications - Current status

“Minos” and “Maximus”, were selected for funding, in the first round of EU's NER300 programme

“Minos” is under development :

• 52 MW tower CSP with Molten Salt Storage, replacing > 100GWh per year of oil based generation, base load

renewable energy power without intermittency issues

• Permitted with Electricity Production Permit, Grid connection and Environmental Terms granted

• Currently working on concluding EPC and financing partners

26

CSP - Solar Thermal Energy for power applications - Future prospects

Technological prospects

Base - load CSP plants with storage (3-7 hours)

Identified barriers

Capital intensive

Levelized cost of energy produced by CSPs is quite high

27

Thank you for your attention…

28