cognitive services in community pharmacy · cognitive pharmaceutical services in community pharmacy...

TRANSCRIPT

Cognitive Pharmaceutical Services in Community

Pharmacy

Prof Charlie BenrimojProfessor of Pharmacy Practice &Head of Graduate School of Health

CHERE October 2013

Overview

• National and International Context• Australian Environment & Research

– Pharmacy Barometer– Implementation and Sustainability Model– Piloting of Model

• International Impact Study (ECHO) in Spain• Conclusion

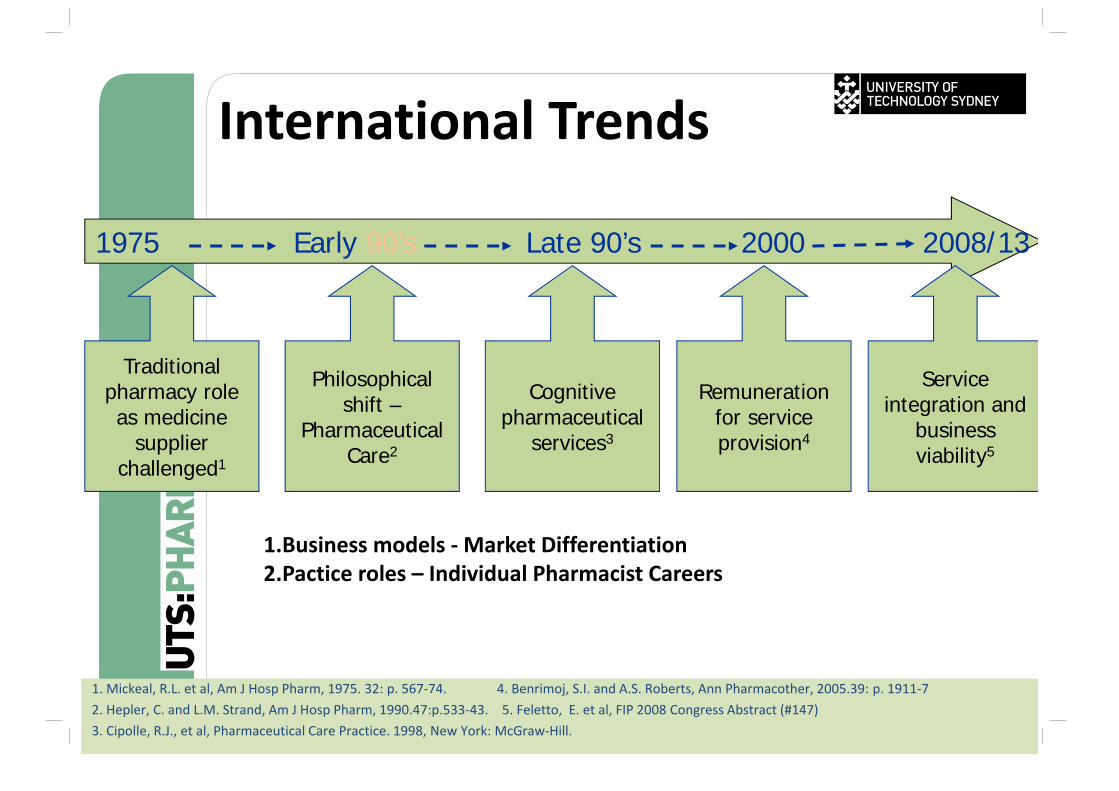

International Trends

Traditional pharmacy role as medicine

supplier challenged1

1975 Early 90’s Late 90’s 2000 2008/13

Philosophical shift –

Pharmaceutical Care2

Cognitive pharmaceutical

services3

Remuneration for service provision4

Service integration and

business viability5

1. Mickeal, R.L. et al, Am J Hosp Pharm, 1975. 32: p. 567‐74. 4. Benrimoj, S.I. and A.S. Roberts, Ann Pharmacother, 2005.39: p. 1911‐72. Hepler, C. and L.M. Strand, Am J Hosp Pharm, 1990.47:p.533‐43. 5. Feletto, E. et al, FIP 2008 Congress Abstract (#147)3. Cipolle, R.J., et al, Pharmaceutical Care Practice. 1998, New York: McGraw‐Hill.

1.Business models ‐Market Differentiation2.Pactice roles – Individual Pharmacist Careers

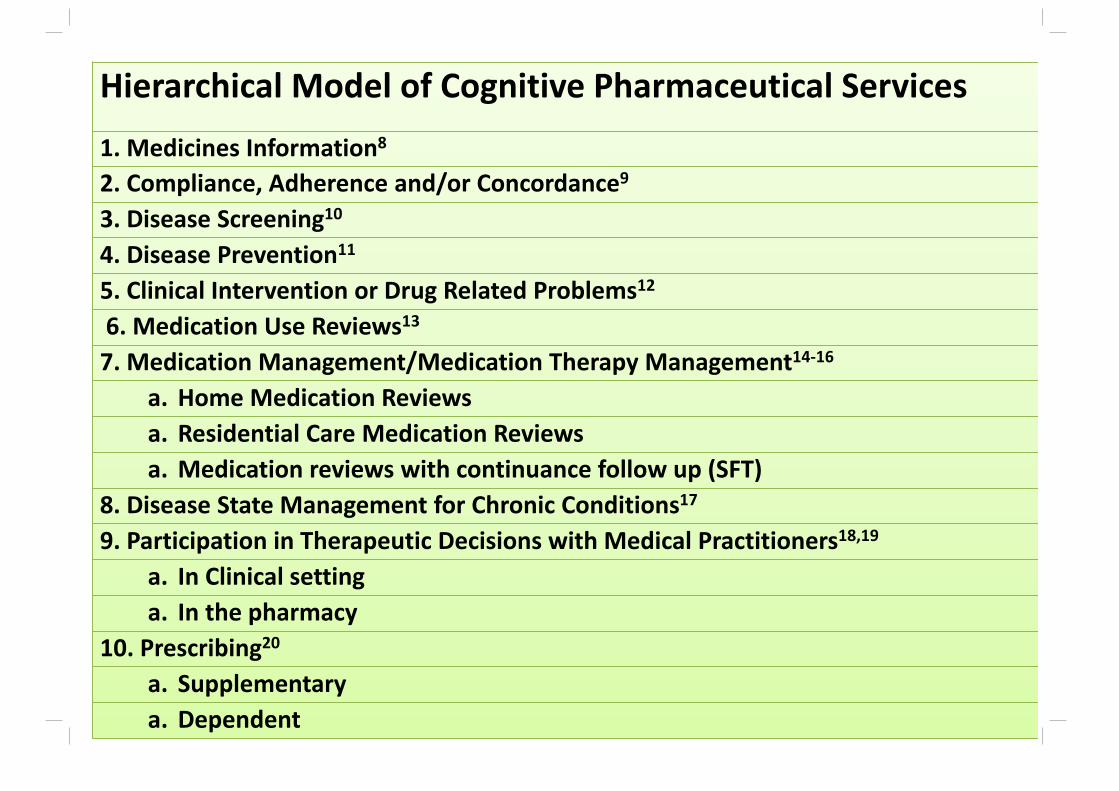

Hierarchical Model of Cognitive Pharmaceutical Services

1. Medicines Information8

2. Compliance, Adherence and/or Concordance9

3. Disease Screening10

4. Disease Prevention11

5. Clinical Intervention or Drug Related Problems12

6. Medication Use Reviews13

7. Medication Management/Medication Therapy Management14‐16

a. Home Medication Reviewsa. Residential Care Medication Reviewsa. Medication reviews with continuance follow up (SFT)

8. Disease State Management for Chronic Conditions17

9. Participation in Therapeutic Decisions with Medical Practitioners18,19

a. In Clinical settinga. In the pharmacy

10. Prescribing20

a. Supplementary a. Dependent

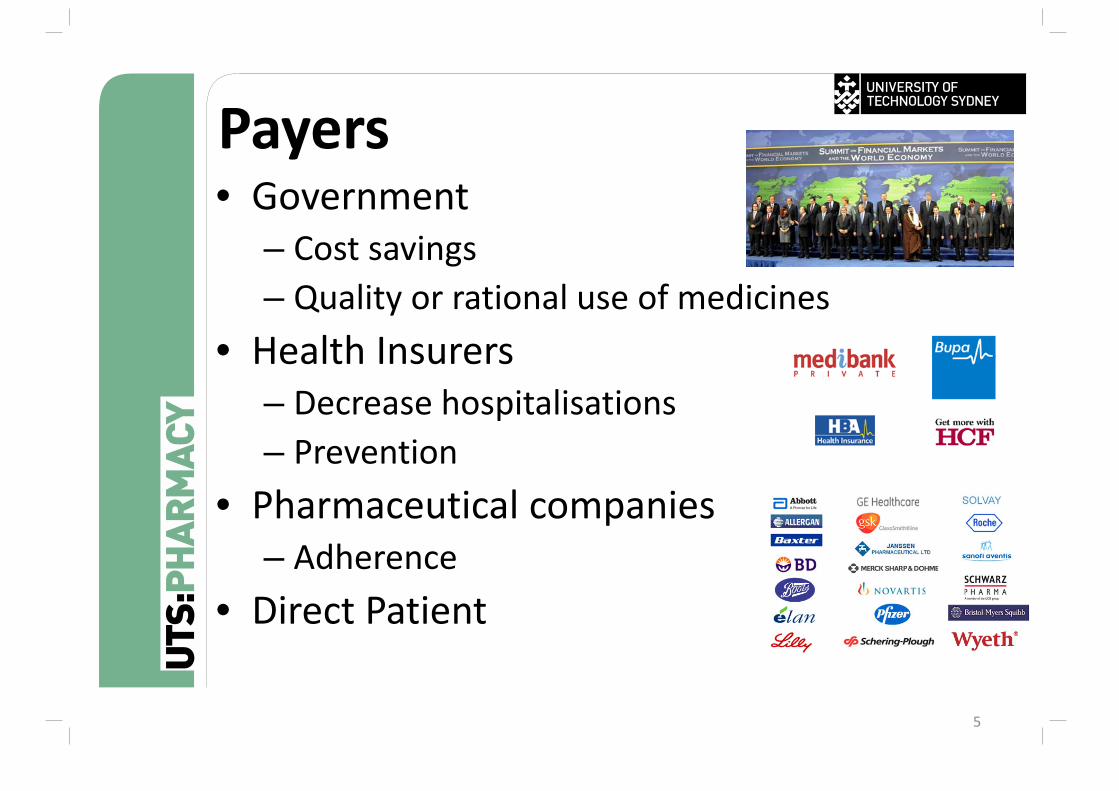

Payers• Government

– Cost savings– Quality or rational use of medicines

• Health Insurers– Decrease hospitalisations– Prevention

• Pharmaceutical companies– Adherence

• Direct Patient

5

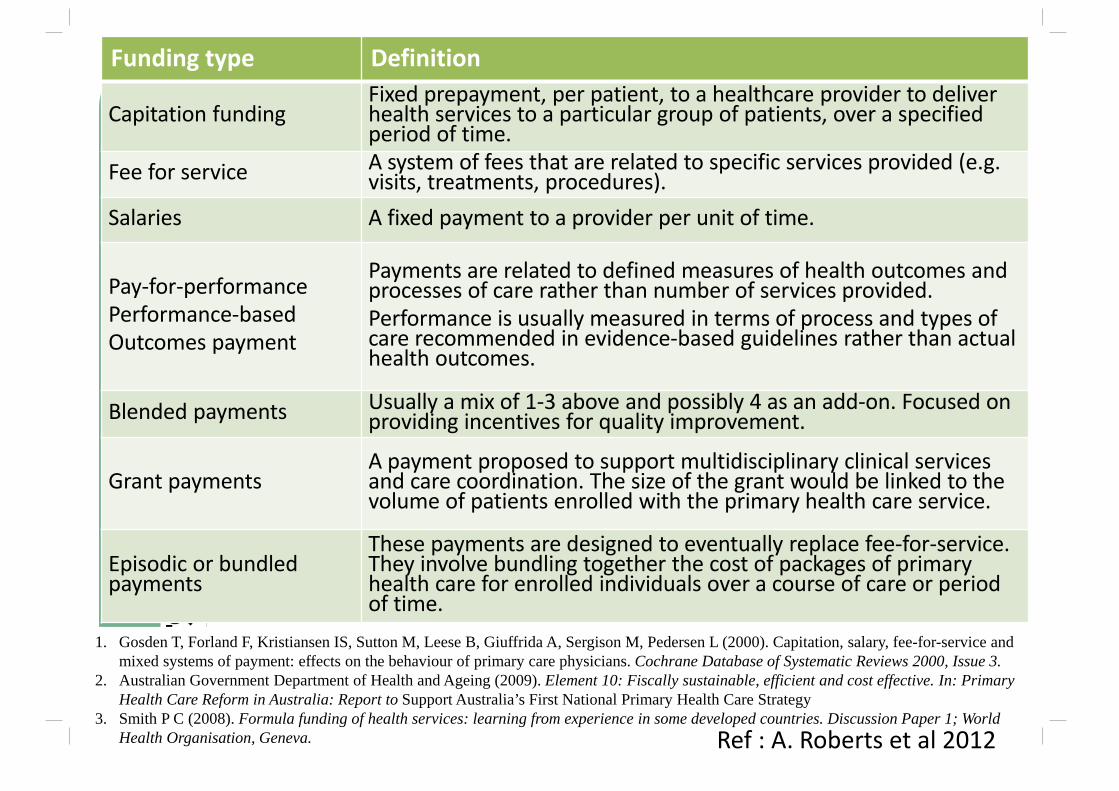

Funding type Definition

Capitation fundingFixed prepayment, per patient, to a healthcare provider to deliver health services to a particular group of patients, over a specified period of time.

Fee for service A system of fees that are related to specific services provided (e.g. visits, treatments, procedures).

Salaries A fixed payment to a provider per unit of time.

Pay‐for‐performance Performance‐basedOutcomes payment

Payments are related to defined measures of health outcomes and processes of care rather than number of services provided. Performance is usually measured in terms of process and types of care recommended in evidence‐based guidelines rather than actual health outcomes.

Blended payments Usually a mix of 1‐3 above and possibly 4 as an add‐on. Focused on providing incentives for quality improvement.

Grant paymentsA payment proposed to support multidisciplinary clinical services and care coordination. The size of the grant would be linked to the volume of patients enrolled with the primary health care service.

Episodic or bundled payments

These payments are designed to eventually replace fee‐for‐service. They involve bundling together the cost of packages of primary health care for enrolled individuals over a course of care or period of time.

1. Gosden T, Forland F, Kristiansen IS, Sutton M, Leese B, Giuffrida A, Sergison M, Pedersen L (2000). Capitation, salary, fee-for-service and mixed systems of payment: effects on the behaviour of primary care physicians. Cochrane Database of Systematic Reviews 2000, Issue 3.

2. Australian Government Department of Health and Ageing (2009). Element 10: Fiscally sustainable, efficient and cost effective. In: Primary Health Care Reform in Australia: Report to Support Australia’s First National Primary Health Care Strategy

3. Smith P C (2008). Formula funding of health services: learning from experience in some developed countries. Discussion Paper 1; World Health Organisation, Geneva. Ref : A. Roberts et al 2012

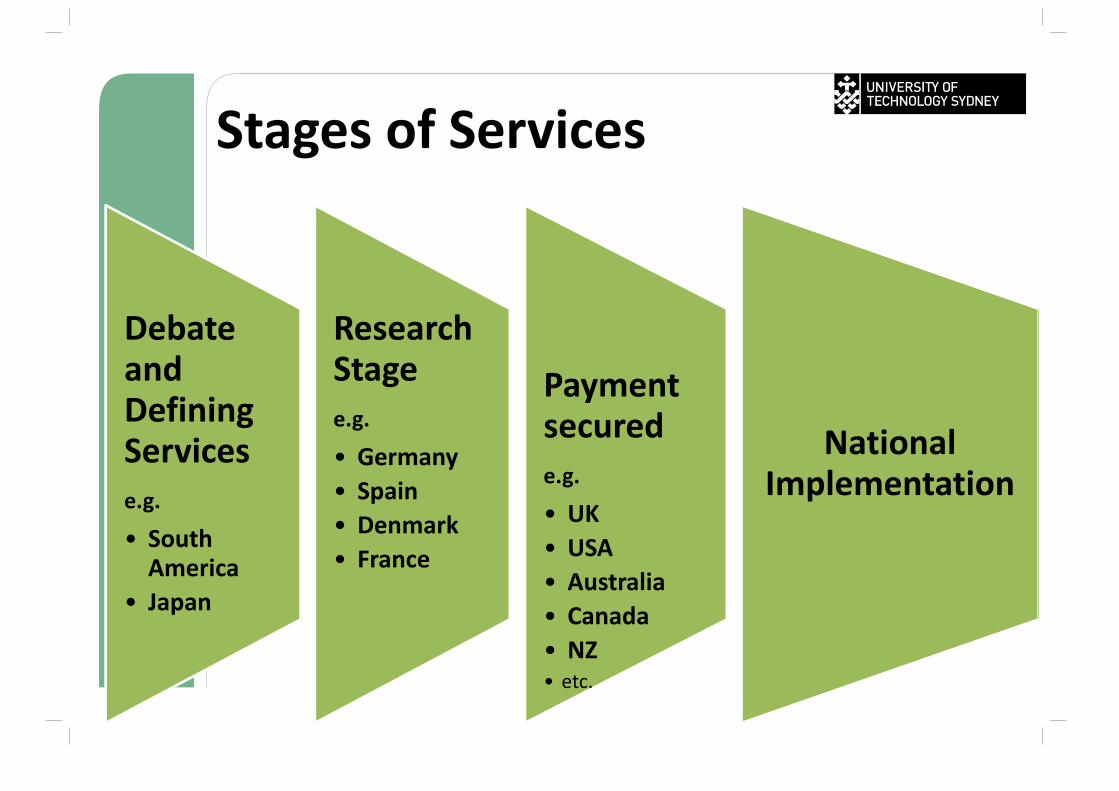

Stages of Services

Debate and Defining Servicese.g.

• South America

• Japan

Research Stagee.g.

• Germany• Spain• Denmark• France

Payment securede.g.

• UK• USA• Australia• Canada• NZ• etc.

National Implementation

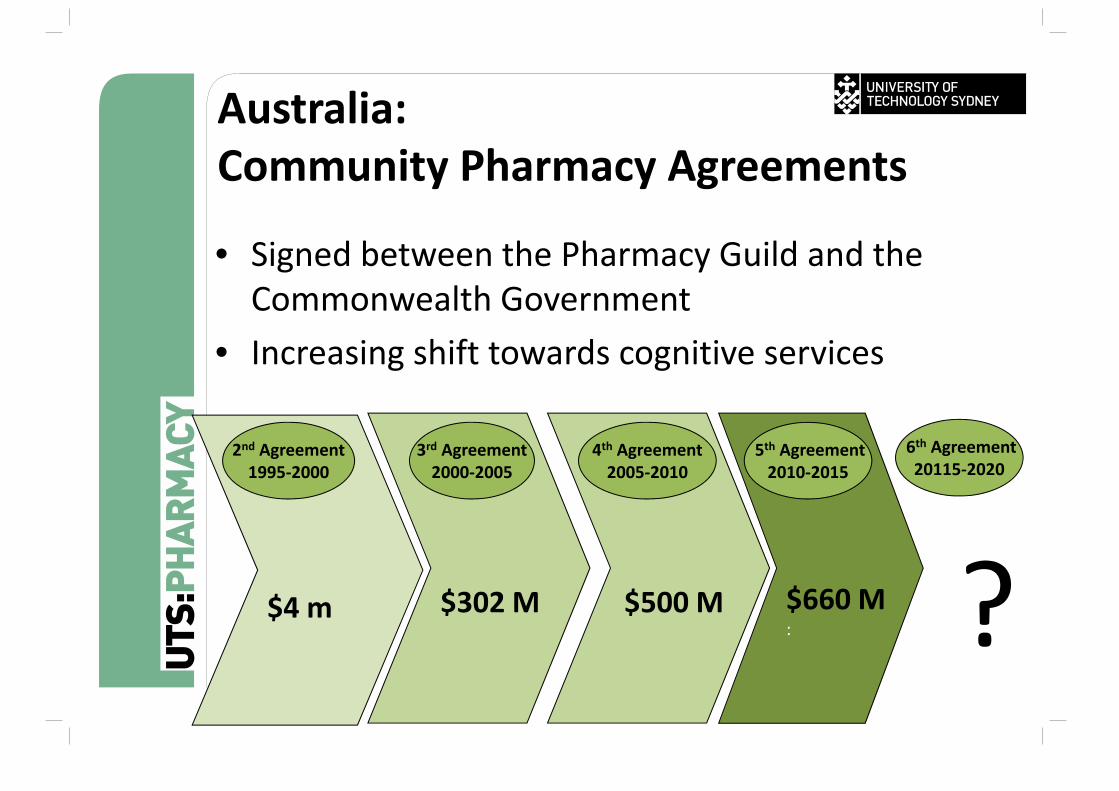

Australia:Community Pharmacy Agreements

• Signed between the Pharmacy Guild and the Commonwealth Government

• Increasing shift towards cognitive services

$4 m

2nd Agreement1995‐2000

$302 M

3rd Agreement2000‐2005

$500 M

4th Agreement2005‐2010

$660 M:

6th Agreement20115‐2020

5th Agreement2010‐2015

?

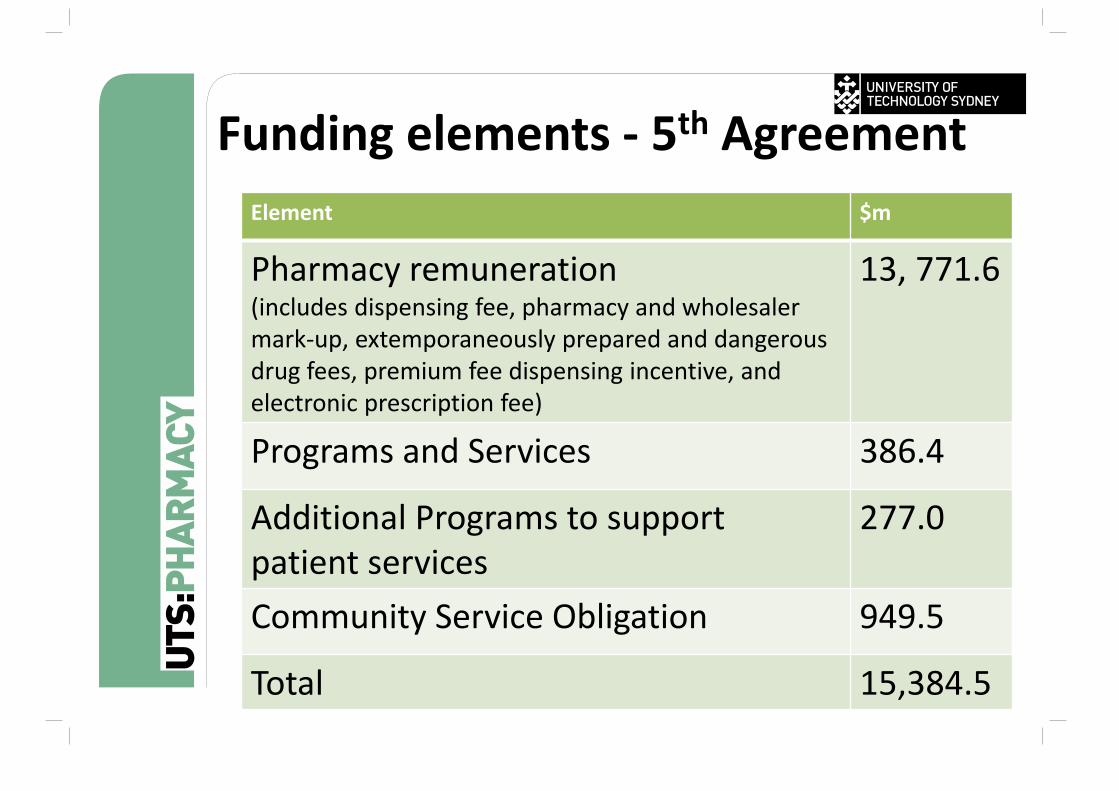

Funding elements ‐ 5th AgreementElement $m

Pharmacy remuneration(includes dispensing fee, pharmacy and wholesaler mark‐up, extemporaneously prepared and dangerous drug fees, premium fee dispensing incentive, and electronic prescription fee)

13, 771.6

Programs and Services 386.4

Additional Programs to support patient services

277.0

Community Service Obligation 949.5

Total 15,384.5

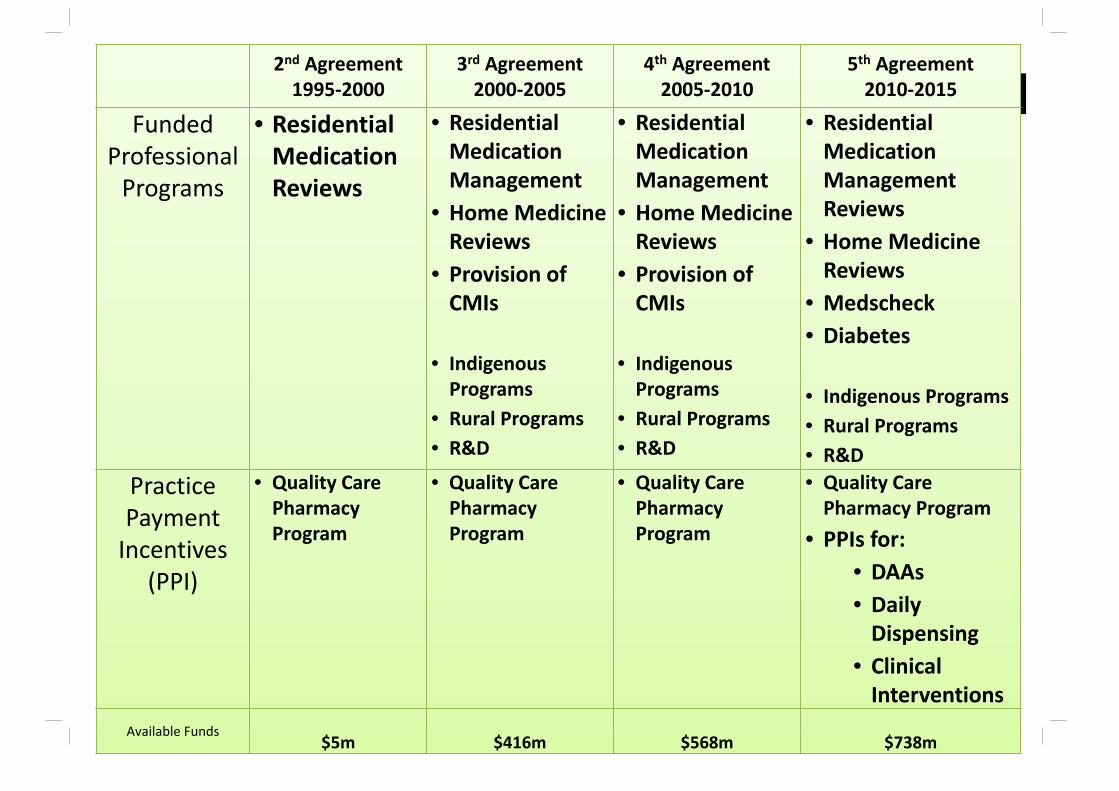

2nd Agreement1995‐2000

3rd Agreement2000‐2005

4th Agreement2005‐2010

5th Agreement2010‐2015

Funded Professional Programs

• Residential Medication Reviews

• Residential Medication Management

• Home Medicine Reviews

• Provision of CMIs

• Indigenous Programs

• Rural Programs• R&D

• Residential Medication Management

• Home MedicineReviews

• Provision of CMIs

• Indigenous Programs

• Rural Programs• R&D

• Residential Medication Management Reviews

• Home Medicine Reviews

• Medscheck• Diabetes

• Indigenous Programs• Rural Programs• R&D

Practice Payment Incentives

(PPI)

• Quality Care Pharmacy Program

• Quality Care Pharmacy Program

• Quality Care Pharmacy Program

• Quality Care Pharmacy Program

• PPIs for:• DAAs• Daily Dispensing

• Clinical Interventions

Available Funds$5m $416m $568m $738m

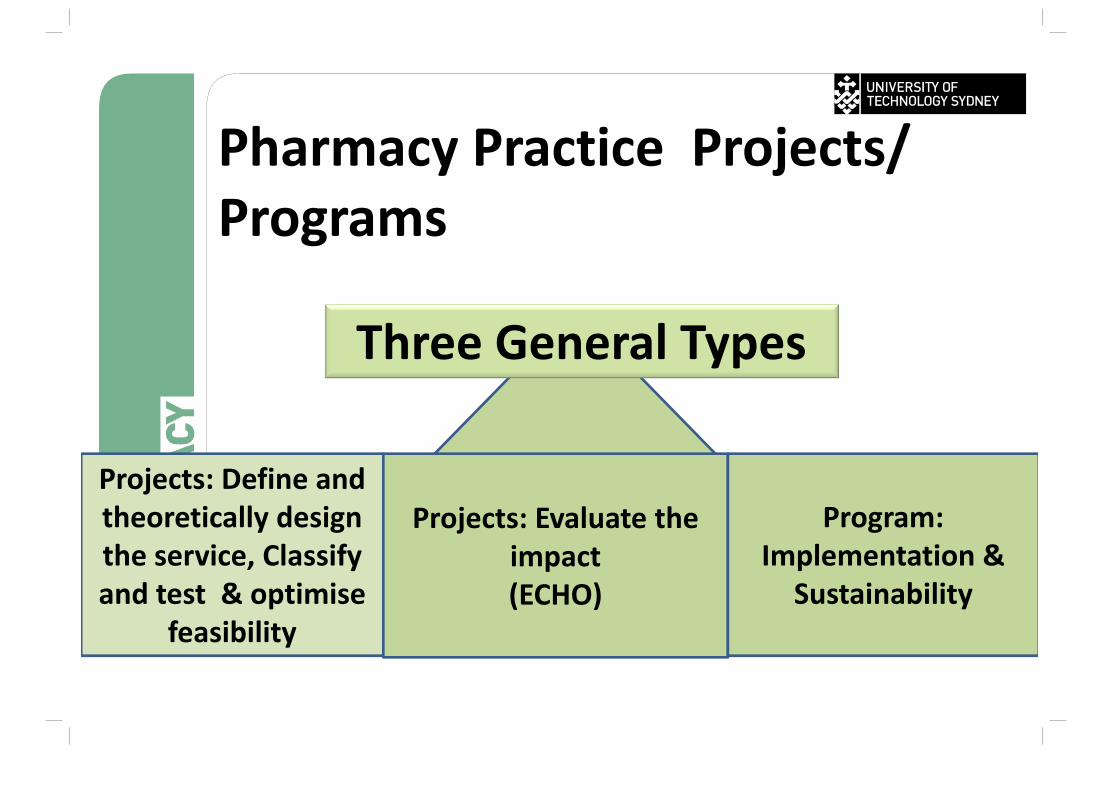

Pharmacy Practice Projects/ Programs

Three General Types

Projects: Define and theoretically design the service, Classify and test & optimise

feasibility

Projects: Evaluate the impact(ECHO)

Program: Implementation &

Sustainability

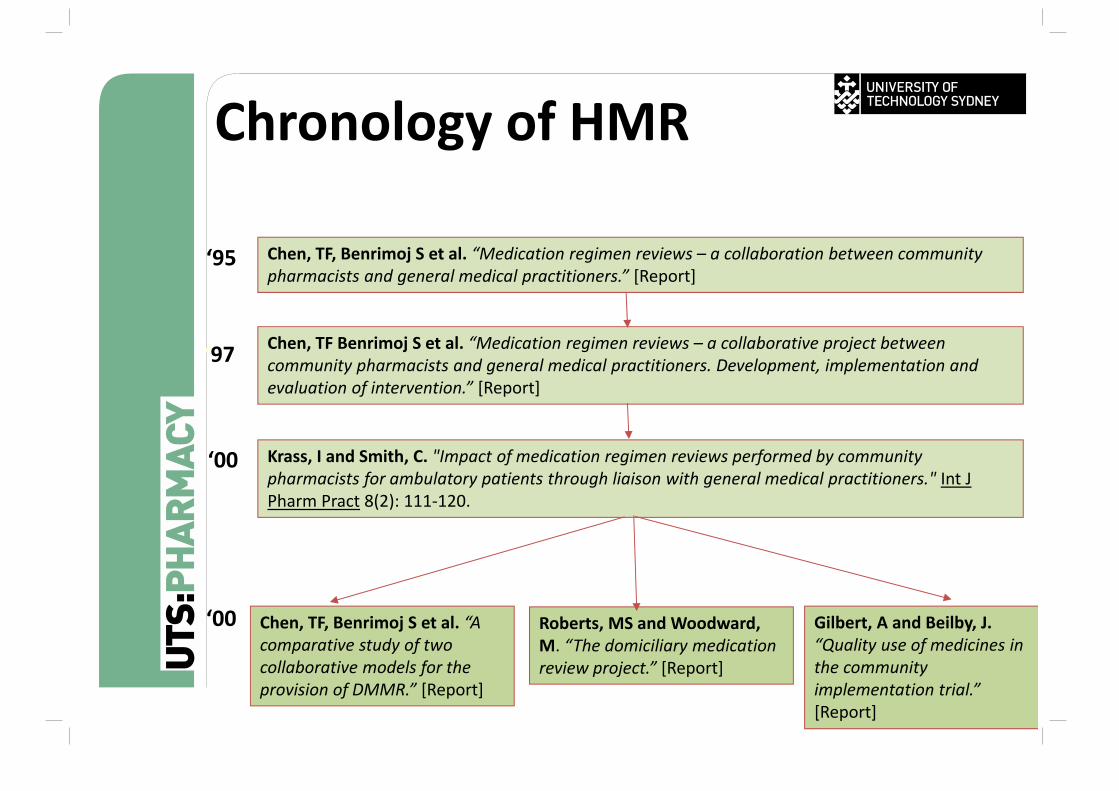

Chronology of HMR

Chen, TF, Benrimoj S et al. “Medication regimen reviews – a collaboration between community pharmacists and general medical practitioners.” [Report]

‘95

Chen, TF Benrimoj S et al. “Medication regimen reviews – a collaborative project between community pharmacists and general medical practitioners. Development, implementation and evaluation of intervention.” [Report]

‘97

Krass, I and Smith, C. "Impact of medication regimen reviews performed by community pharmacists for ambulatory patients through liaison with general medical practitioners." Int J Pharm Pract 8(2): 111‐120.

‘00

Chen, TF, Benrimoj S et al. “A comparative study of two collaborative models for the provision of DMMR.” [Report]

Roberts, MS and Woodward, M. “The domiciliary medication review project.” [Report]

Gilbert, A and Beilby, J.“Quality use of medicines in the community implementation trial.” [Report]

‘00

See also: http://beta.guild.org.au/research/

Barriers and Facilitators

• Barriers– Pharmacist‐related

• Attitude e.g. fear of change, lack of self‐confidence

• Practice skills e.g. limited communication skills

– Resource‐related• E.g. lack of management and

incentives, lack of protocols and guidelines

– System‐related• E.g. limited acceptance by other

health professionals– Academic and education

related• Knowledge and training

– Other • Lack of mentors and models, lack

of vision

• Facilitators– Experiential

• Remuneration• Pharmacist competence• Use of protocols• Interaction with patient groups• Profile within local community• Atmosphere of pharmacy• Motivation

– Potential• Advertising• Proven benefits of service• Working as a team• Documentation system• Communication skills• Professional reward• Autonomy

Roberts A.S., Benrimoj S.I., Chen T.F., Williams K.A., Aslani P. Implementing cognitive services in community pharmacy: a review of facilitators of practice change. I J P P (2006) 14: 163-170.

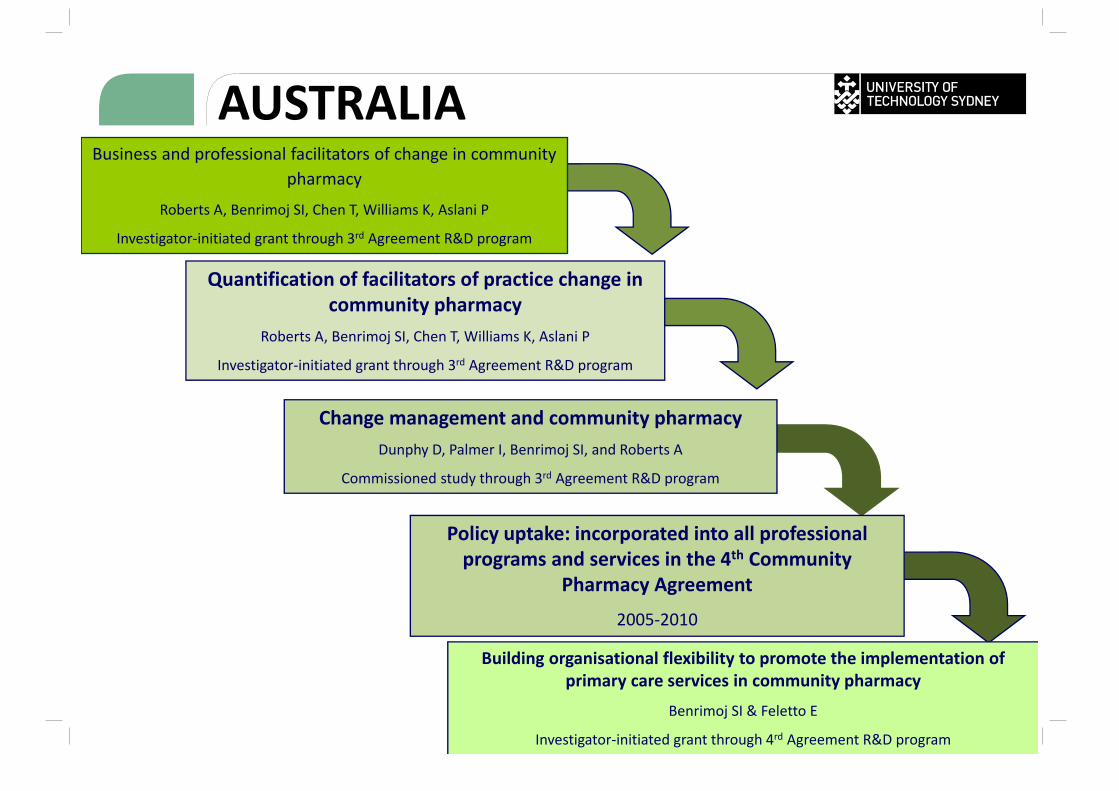

Quantification of facilitators of practice change in community pharmacy

Roberts A, Benrimoj SI, Chen T, Williams K, Aslani P

Investigator‐initiated grant through 3rd Agreement R&D program

Policy uptake: incorporated into all professional programs and services in the 4th Community

Pharmacy Agreement

2005‐2010

SOURCE17. http://beta.guild.org.au/research/funded_projects.asp

Building organisational flexibility to promote the implementation of primary care services in community pharmacy

Benrimoj SI & Feletto E

Investigator‐initiated grant through 4rd Agreement R&D program

Business and professional facilitators of change in community pharmacy

Roberts A, Benrimoj SI, Chen T, Williams K, Aslani P

Investigator‐initiated grant through 3rd Agreement R&D program

Change management and community pharmacyDunphy D, Palmer I, Benrimoj SI, and Roberts A

Commissioned study through 3rd Agreement R&D program

AUSTRALIA

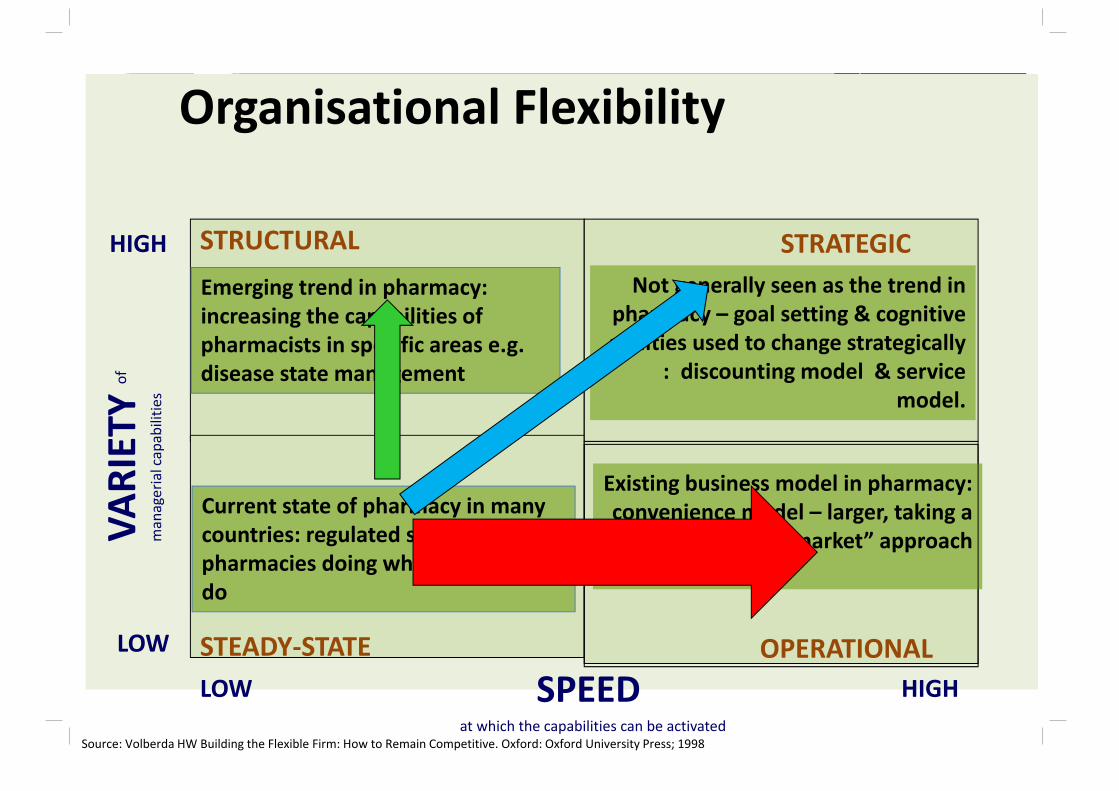

Organisational Flexibility

LOW HIGH

LOW

HIGH

SPEED at which the capabilities can be activated

VARIETY

of

managerial capabilitie

s

STRUCTURAL

STEADY‐STATE

STRATEGIC

OPERATIONAL

Source: Volberda HW Building the Flexible Firm: How to Remain Competitive. Oxford: Oxford University Press; 1998

Current state of pharmacy in many countries: regulated system, pharmacies doing what they always do

Emerging trend in pharmacy: increasing the capabilities of pharmacists in specific areas e.g. disease state management

Not generally seen as the trend in pharmacy – goal setting & cognitive abilities used to change strategically

: discounting model & service model.

Existing business model in pharmacy: convenience model – larger, taking a

“supermarket” approach

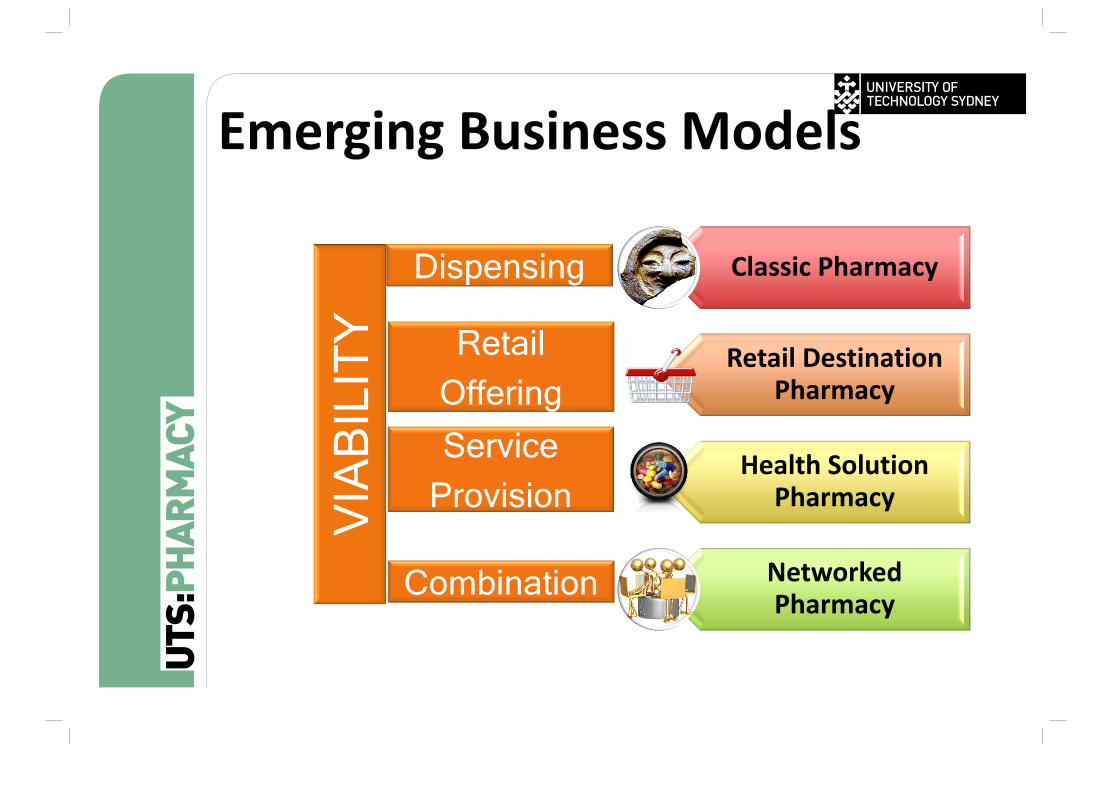

Classic Pharmacy

Retail Destination Pharmacy

Health Solution Pharmacy

NetworkedPharmacy

Dispensing

Retail Offering

Service Provision

Combination

VIA

BIL

ITY

Emerging Business Models

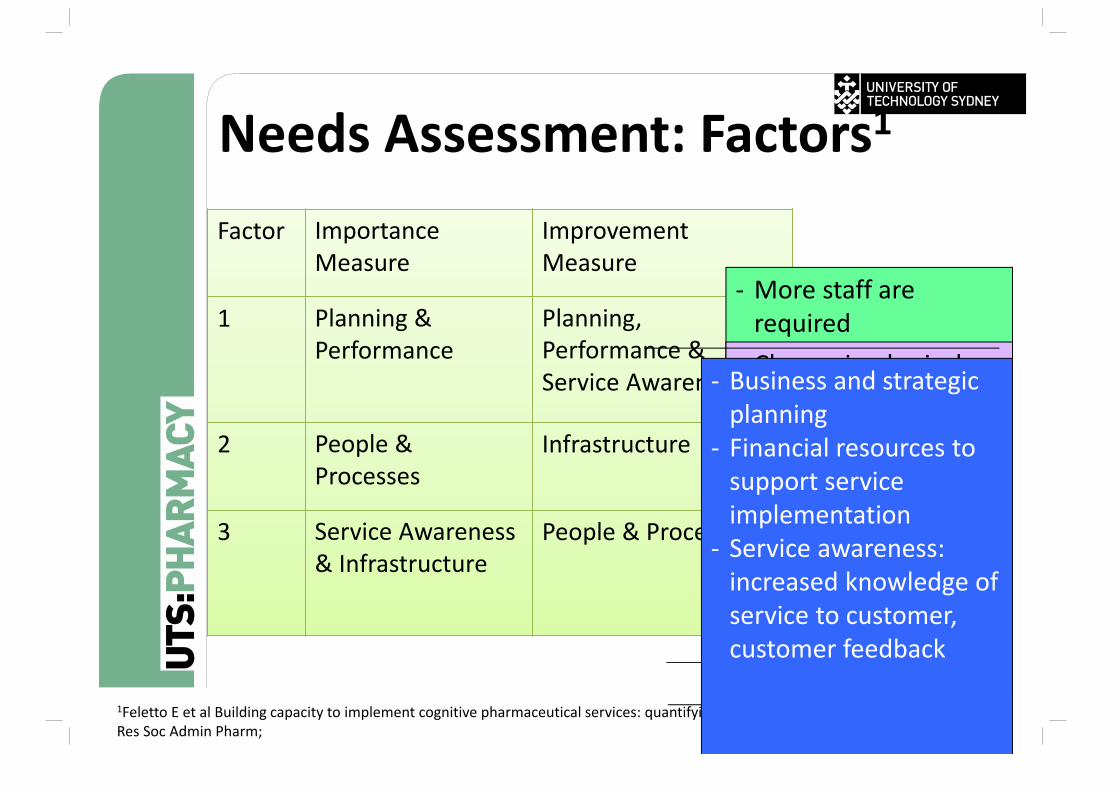

Needs Assessment: Factors1

Factor Importance Measure

Improvement Measure

1 Planning & Performance

Planning, Performance & Service Awareness

2 People & Processes

Infrastructure

3 Service Awareness & Infrastructure

People & Processes

‐ More staff are required

‐ Staff with specialized knowledge

‐ Define operational process to guide the provision of services

‐ Change in physical layout for service provision

‐ Aid in increasing the customer awareness of services available

1Feletto E et al Building capacity to implement cognitive pharmaceutical services: quantifying the needs of community pharmacies Res Soc Admin Pharm;

‐ Business and strategic planning

‐ Financial resources to support service implementation

‐ Service awareness: increased knowledge of service to customer, customer feedback

Remuneration to individuals

• Direct employee providing services• Professional Service Managers (industry, pharmacy groups and individual pharmacies)

• Consultant pharmacist• Specialisations based on Setting ( e.g. nursing homes, hospital, community)

Community Pharmacy EconomicDrivers

• PBS Reform • Accelerated Price Reductions and Disclosure• Generic substitution• Changing remuneration systems• Discount models• Medicare local reform (local purchasing)

• Wholesaler• Direct Distribution• Reduction on wholesalers trading terms

• Community Pharmacy Agreements• Shift from product based to service based

• Retail Trade trends

UTS Pharmacy BarometerSponsored by Bankwest Objective : Impact on community pharmacy

business and professional practice, and on individual community pharmacists.

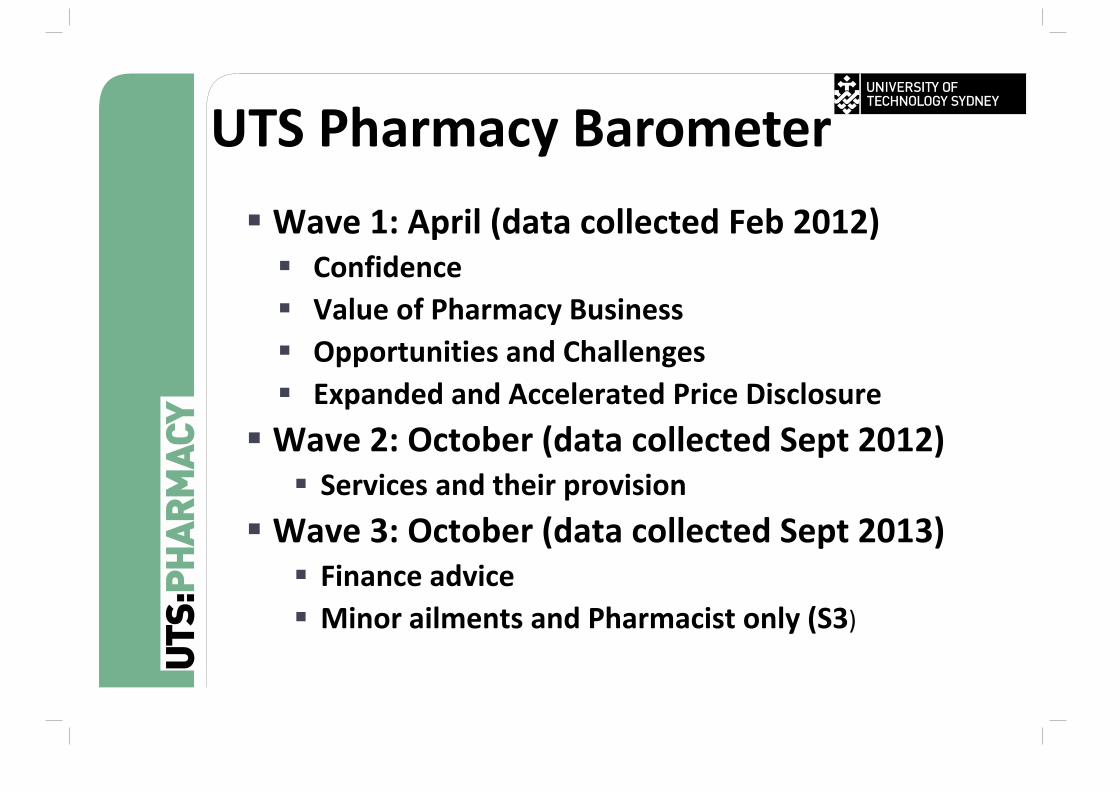

Wave 1: April (data collected Feb 2012) Confidence Value of Pharmacy Business Opportunities and Challenges Expanded and Accelerated Price Disclosure Wave 2: October (data collected Sept 2012) Services and their provision

Wave 3: October (data collected Sept 2013) Finance advice Minor ailments and Pharmacist only (S3)

UTS Pharmacy Barometer

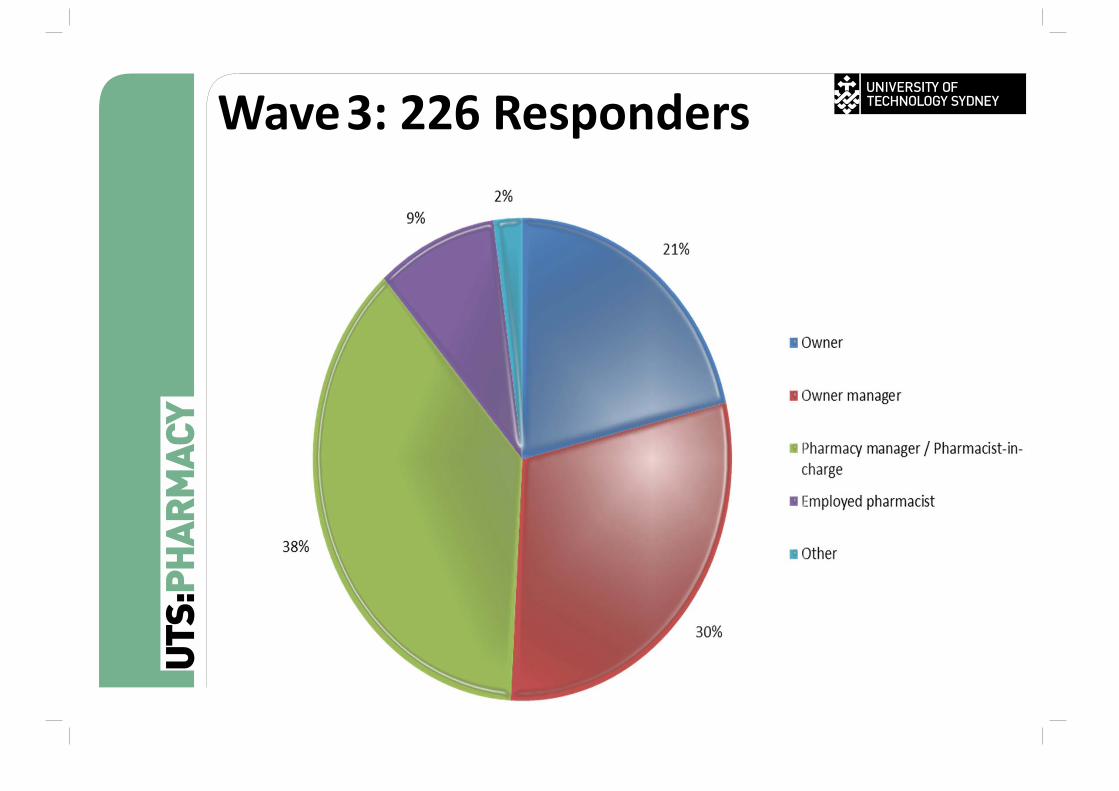

Wave3: 226 Responders

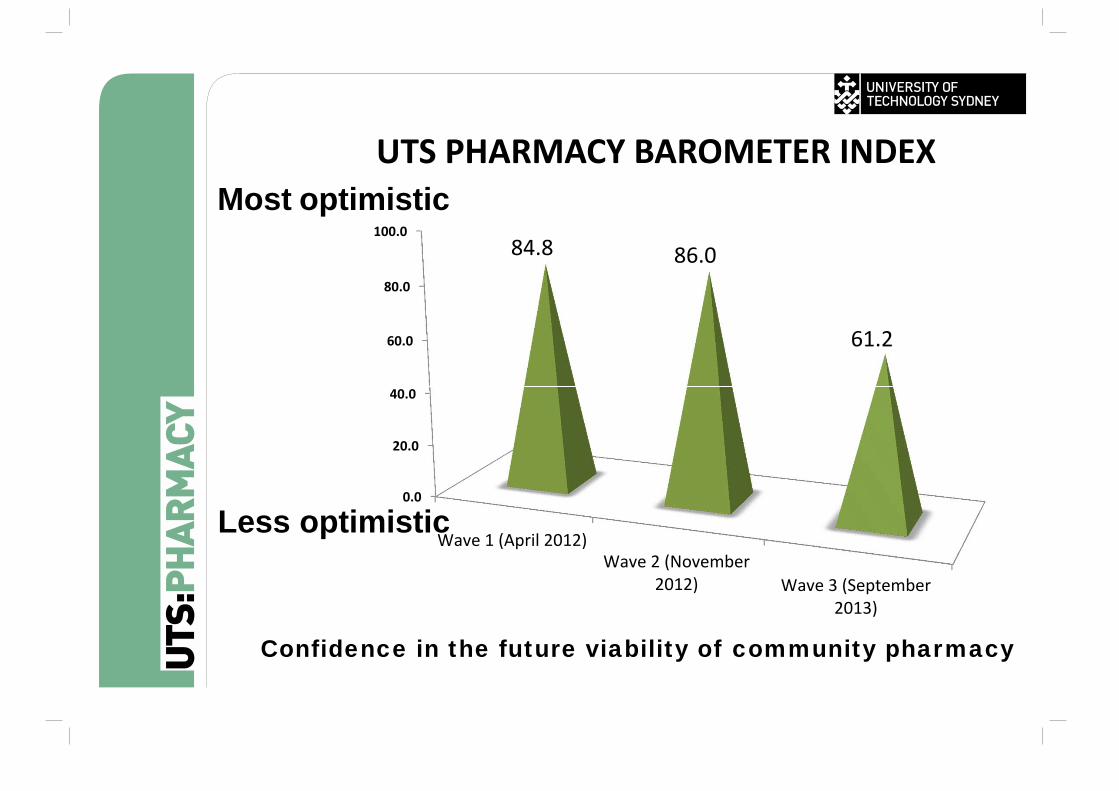

Confidence in the future viability of community pharmacy

0.0

20.0

40.0

60.0

80.0

100.0

Wave 1 (April 2012)Wave 2 (November

2012) Wave 3 (September2013)

84.8 86.0

61.2

UTS PHARMACY BAROMETER INDEXMost optimistic

Less optimistic

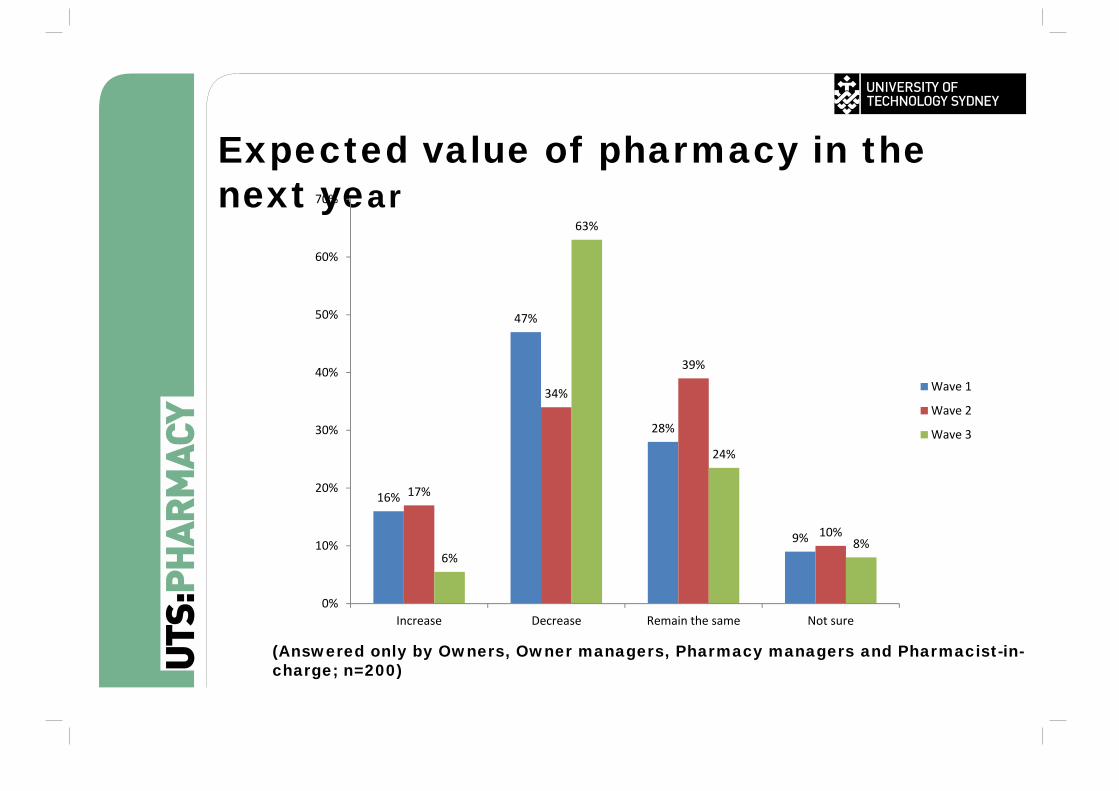

Expected value of pharmacy in the next year

16%

47%

28%

9%

17%

34%

39%

10%

6%

63%

24%

8%

0%

10%

20%

30%

40%

50%

60%

70%

Increase Decrease Remain the same Not sure

Wave 1

Wave 2

Wave 3

(Answered only by Owners, Owner managers, Pharmacy managers and Pharmacist-in-charge; n=200)

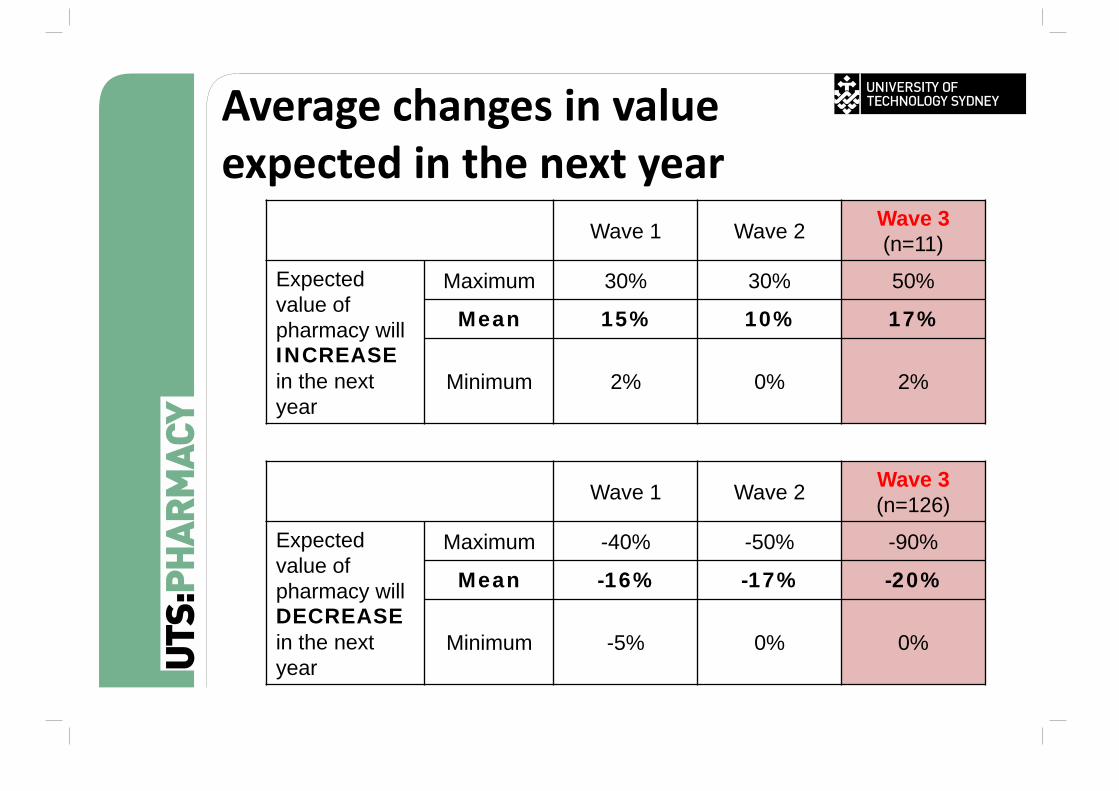

Average changes in valueexpected in the next year

Wave 1 Wave 2 Wave 3 (n=11)

Expected value of pharmacy will INCREASEin the next year

Maximum 30% 30% 50%

Mean 15% 10% 17%

Minimum 2% 0% 2%

Wave 1 Wave 2 Wave 3 (n=126)

Expected value of pharmacy will DECREASEin the next year

Maximum -40% -50% -90%

Mean -16% -17% -20%

Minimum -5% 0% 0%

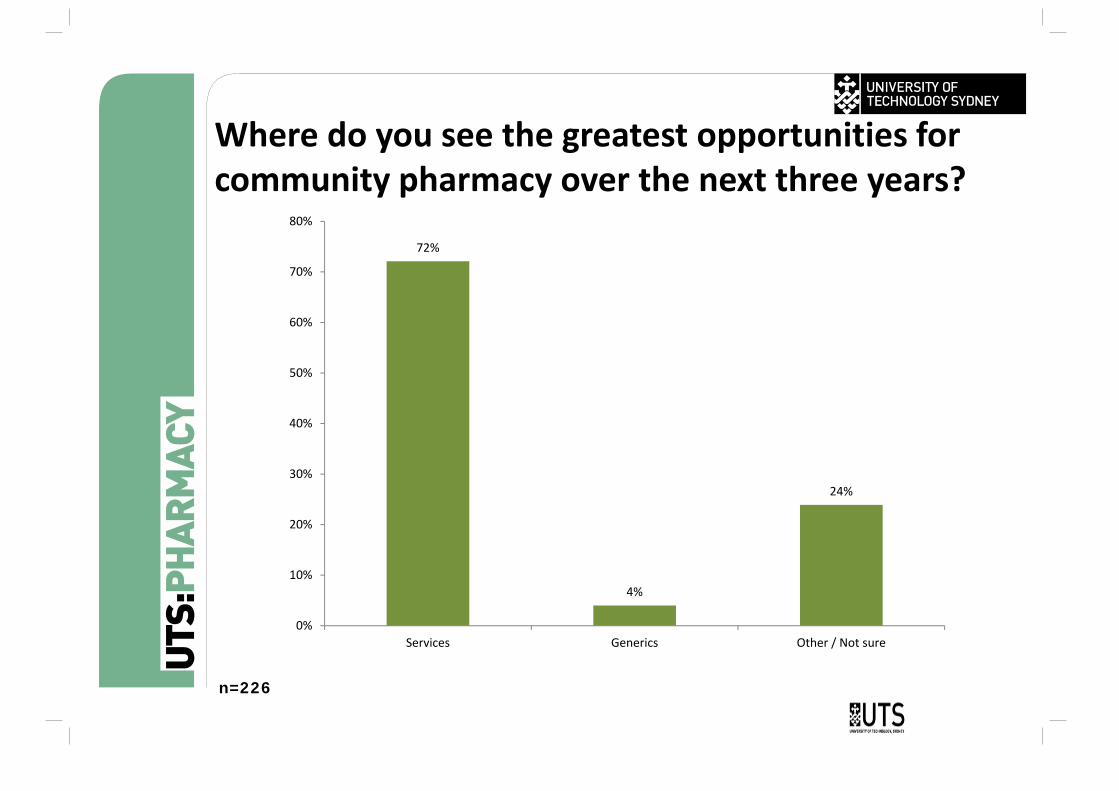

Where do you see the greatest opportunities for community pharmacy over the next three years?

n=226

72%

4%

24%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Services Generics Other / Not sure

27

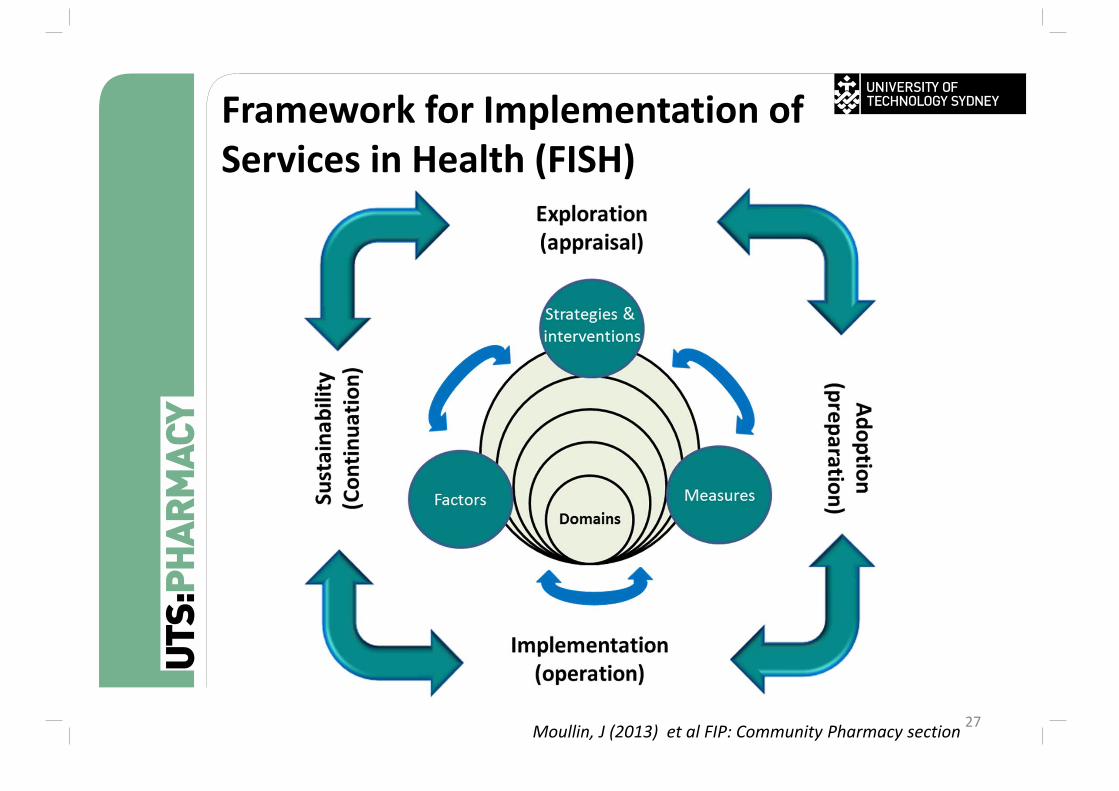

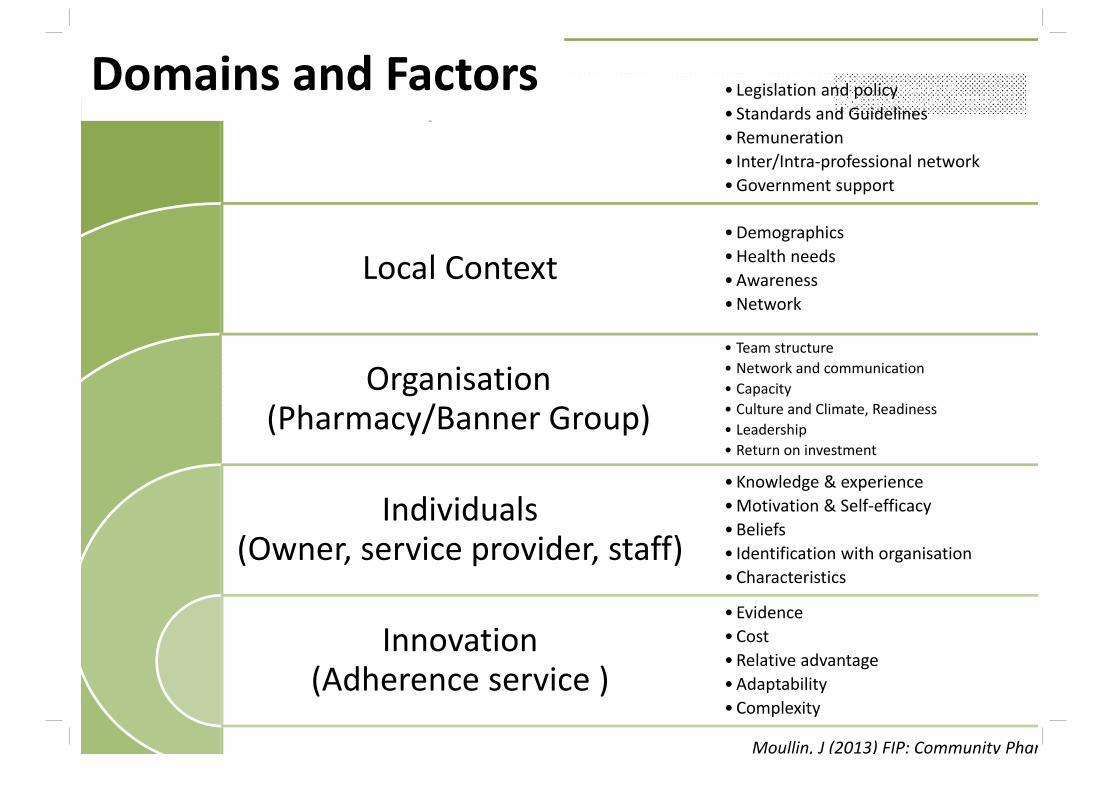

Framework for Implementation of Services in Health (FISH)

Moullin, J (2013) et al FIP: Community Pharmacy section

System

Local Context

Organisation (Pharmacy/Banner Group)

Individuals (Owner, service provider, staff)

Innovation (Adherence service )

• Legislation and policy• Standards and Guidelines•Remuneration• Inter/Intra‐professional network•Government support

•Demographics•Health needs•Awareness•Network

• Team structure• Network and communication• Capacity• Culture and Climate, Readiness• Leadership• Return on investment

• Knowledge & experience•Motivation & Self‐efficacy•Beliefs• Identification with organisation•Characteristics

• Evidence•Cost•Relative advantage•Adaptability• Complexity

Domains and Factors

Moullin, J (2013) FIP: Community Phar

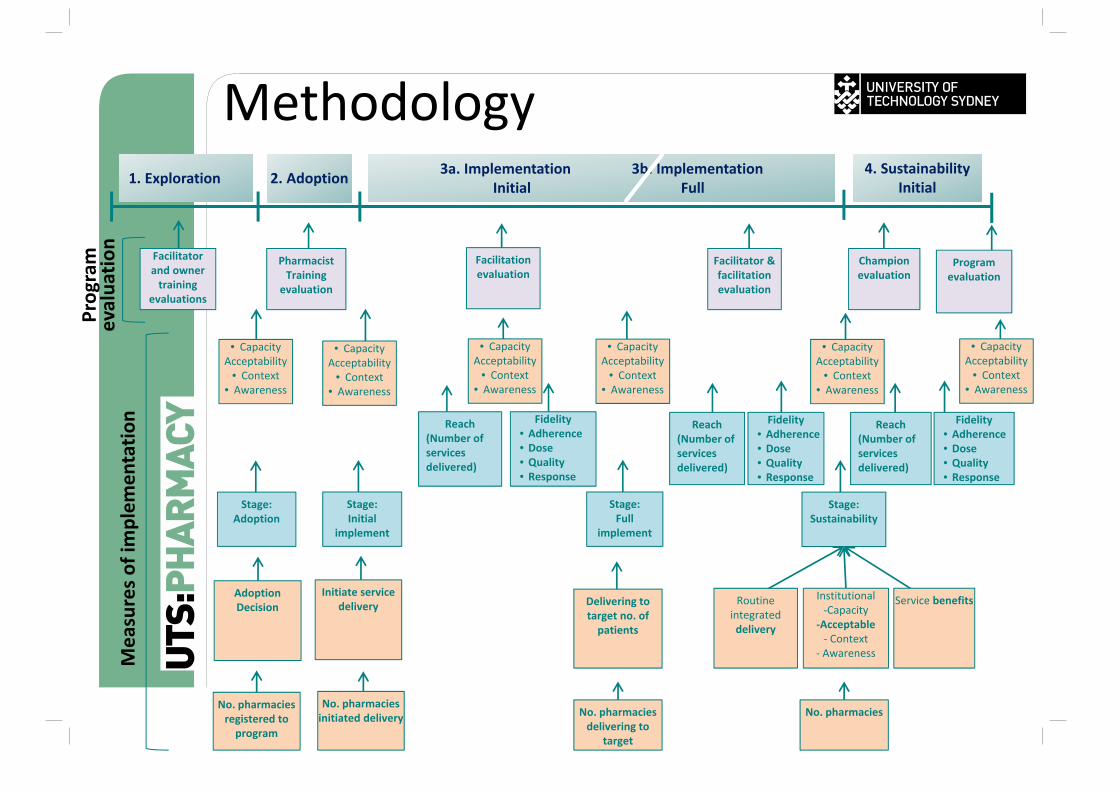

Methodology

Stage: Adoption

Stage: Initial

implement

Stage:Sustainability

Stage:Full

implement

Delivering to target no. of patients

Routine integrated delivery

Institutional‐Capacity

‐Acceptable‐ Context

‐ Awareness

Service benefitsInitiate service

deliveryAdoption Decision

No. pharmacies registered to program

No. pharmacies initiated delivery No. pharmacies

delivering to target

No. pharmacies

1. Exploration 2. Adoption 3a. Implementation 3b. ImplementationInitial Full

4. SustainabilityInitial

Reach(Number of services delivered)

Fidelity• Adherence• Dose• Quality• Response

Reach(Number of services delivered)

Fidelity• Adherence• Dose• Quality• Response

Reach(Number of services delivered)

Fidelity• Adherence• Dose• Quality• Response

Facilitator and owner training

evaluations

Pharmacist Training

evaluation

Facilitation evaluation

Champion evaluation

Program evaluation

Program

evalua

tion

Measures o

f implem

entatio

n

Facilitator & facilitation evaluation

• CapacityAcceptability

• Context• Awareness

• CapacityAcceptability

• Context• Awareness

• CapacityAcceptability

• Context• Awareness

• CapacityAcceptability

• Context• Awareness

• CapacityAcceptability

• Context• Awareness

• CapacityAcceptability

• Context• Awareness

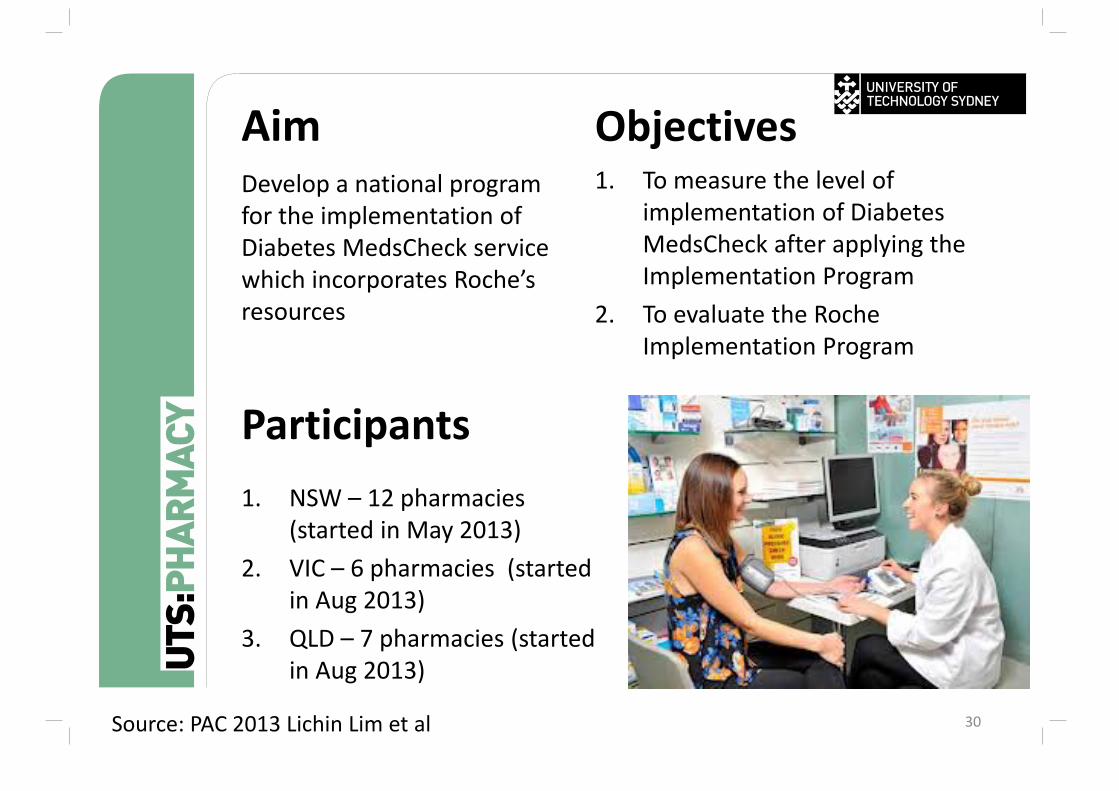

AimDevelop a national program for the implementation of Diabetes MedsCheck service which incorporates Roche’s resources

30

Objectives1. To measure the level of

implementation of Diabetes MedsCheck after applying the Implementation Program

2. To evaluate the Roche Implementation Program

Participants1. NSW – 12 pharmacies

(started in May 2013)2. VIC – 6 pharmacies (started

in Aug 2013)3. QLD – 7 pharmacies (started

in Aug 2013)

Source: PAC 2013 Lichin Lim et al

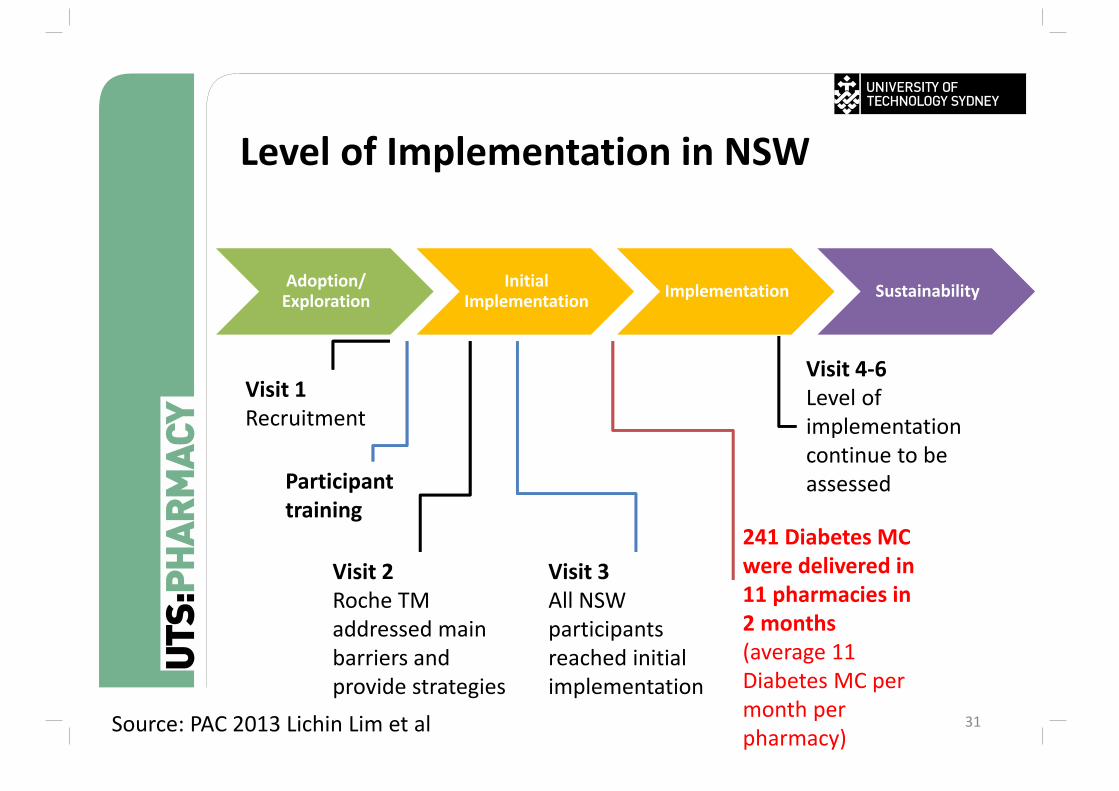

31

Adoption/ Exploration

Initial Implementation Implementation Sustainability

Level of Implementation in NSW

Visit 3All NSW participants reached initial implementation

Visit 4‐6 Level of implementation continue to be assessed

Visit 1Recruitment

Visit 2Roche TM addressed main barriers and provide strategies

Participant training

241 Diabetes MC were delivered in 11 pharmacies in 2 months (average 11 Diabetes MC per month per pharmacy)Source: PAC 2013 Lichin Lim et al

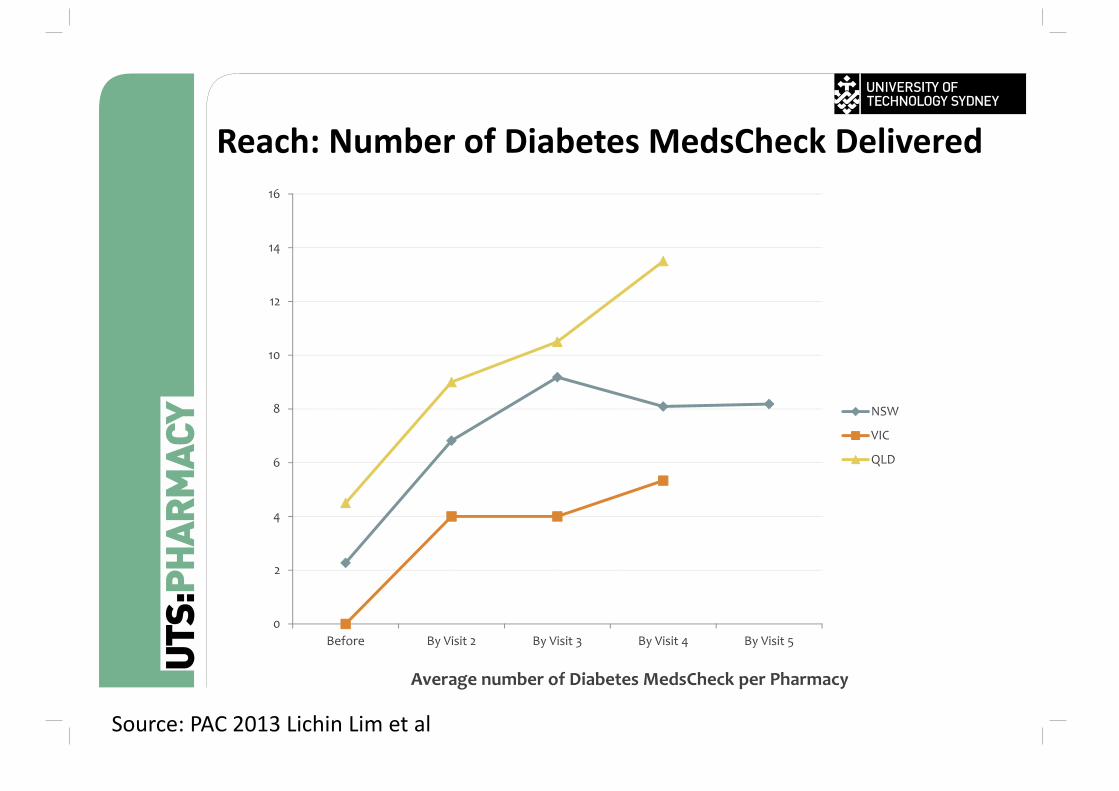

Reach: Number of Diabetes MedsCheck Delivered

0

2

4

6

8

10

12

14

16

Before By Visit 2 By Visit 3 By Visit 4 By Visit 5

Average number of Diabetes MedsCheck per Pharmacy

NSW

VIC

QLD

Source: PAC 2013 Lichin Lim et al

33

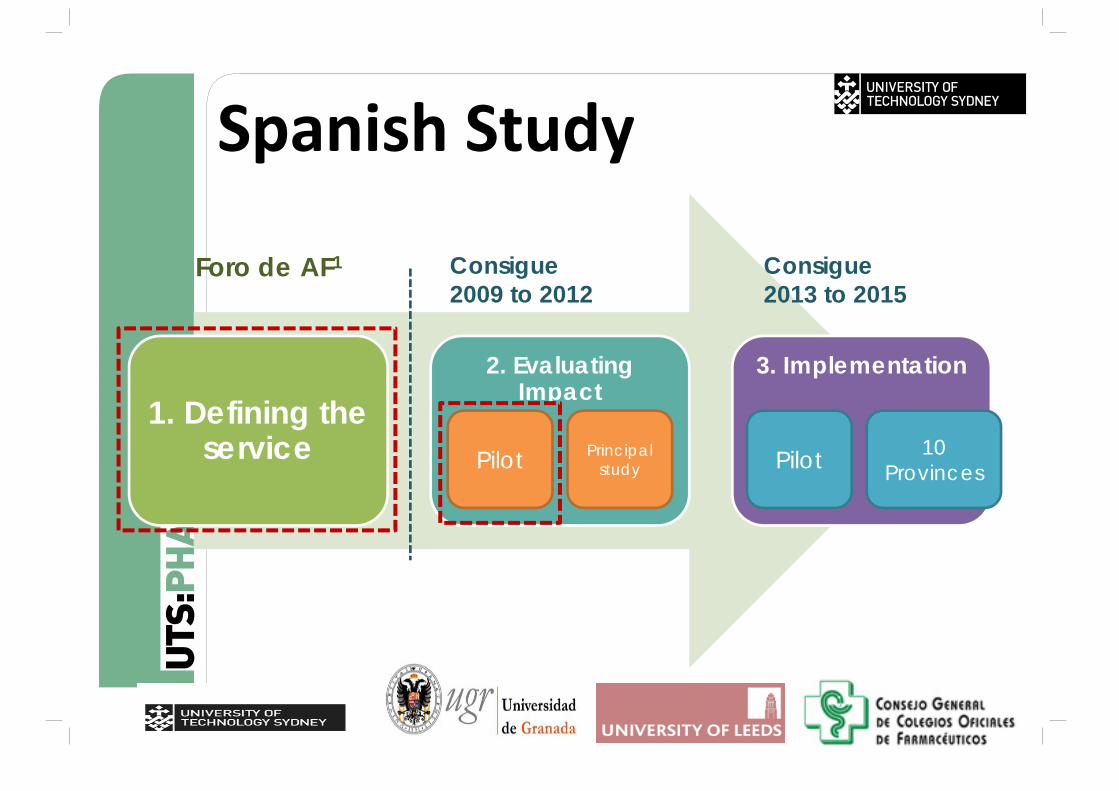

Spanish Study

1. Defining the service

2. Evaluating Impact

3. Implementation

Pilot Principal study Pilot 10

Provinces

Foro de AF1 Consigue2009 to 2012

Introducción

Consigue2013 to 2015

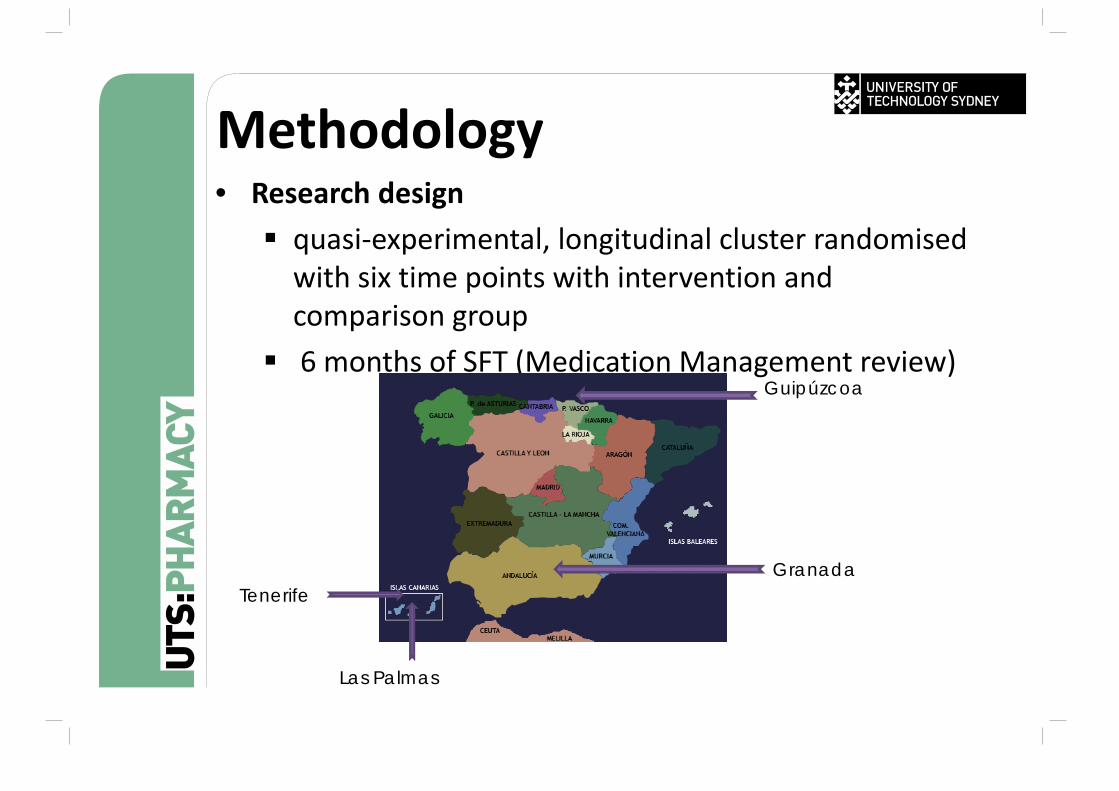

Methodology • Research design quasi‐experimental, longitudinal cluster randomised with six time points with intervention and comparison group

6 months of SFT (Medication Management review)

Granada

Las Palmas

Tenerife

Guipúzcoa

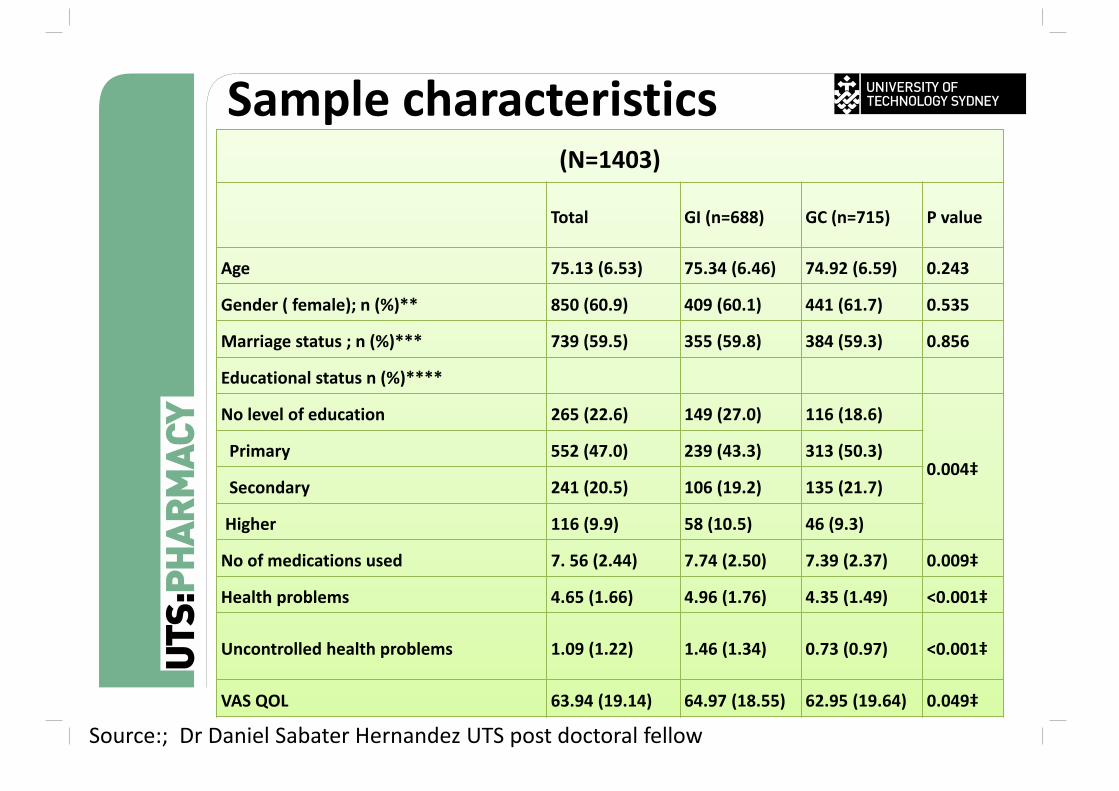

Sample characteristics(N=1403)

Total GI (n=688) GC (n=715) P value

Age 75.13 (6.53) 75.34 (6.46) 74.92 (6.59) 0.243

Gender ( female); n (%)** 850 (60.9) 409 (60.1) 441 (61.7) 0.535

Marriage status ; n (%)*** 739 (59.5) 355 (59.8) 384 (59.3) 0.856

Educational status n (%)****

No level of education 265 (22.6) 149 (27.0) 116 (18.6)

0.004‡Primary 552 (47.0) 239 (43.3) 313 (50.3)

Secondary 241 (20.5) 106 (19.2) 135 (21.7)

Higher 116 (9.9) 58 (10.5) 46 (9.3)

No of medications used 7. 56 (2.44) 7.74 (2.50) 7.39 (2.37) 0.009‡

Health problems 4.65 (1.66) 4.96 (1.76) 4.35 (1.49) <0.001‡

Uncontrolled health problems 1.09 (1.22) 1.46 (1.34) 0.73 (0.97) <0.001‡

VAS QOL 63.94 (19.14) 64.97 (18.55) 62.95 (19.64) 0.049‡

Source:; Dr Daniel Sabater Hernandez UTS post doctoral fellow

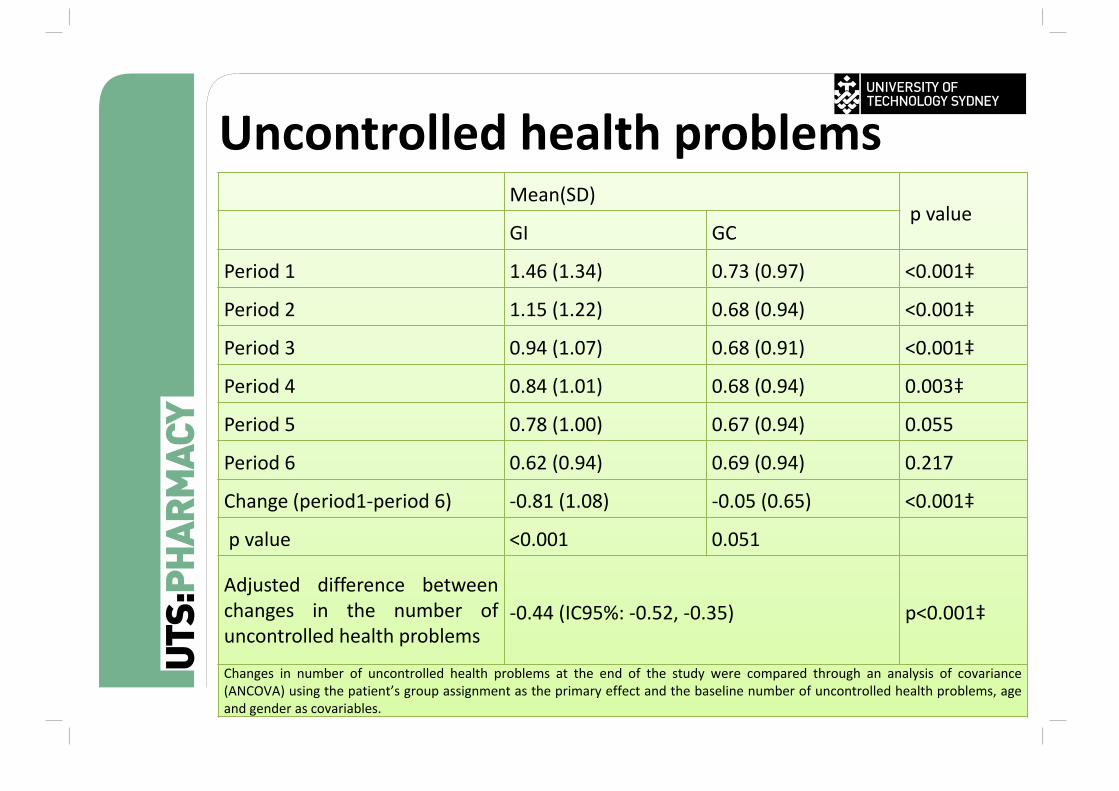

Uncontrolled health problemsMean(SD)

p valueGI GC

Period 1 1.46 (1.34) 0.73 (0.97) <0.001‡

Period 2 1.15 (1.22) 0.68 (0.94) <0.001‡

Period 3 0.94 (1.07) 0.68 (0.91) <0.001‡

Period 4 0.84 (1.01) 0.68 (0.94) 0.003‡

Period 5 0.78 (1.00) 0.67 (0.94) 0.055

Period 6 0.62 (0.94) 0.69 (0.94) 0.217

Change (period1‐period 6) ‐0.81 (1.08) ‐0.05 (0.65) <0.001‡

p value <0.001 0.051

Adjusted difference betweenchanges in the number ofuncontrolled health problems

‐0.44 (IC95%: ‐0.52, ‐0.35) p<0.001‡

Changes in number of uncontrolled health problems at the end of the study were compared through an analysis of covariance(ANCOVA) using the patient’s group assignment as the primary effect and the baseline number of uncontrolled health problems, ageand gender as covariables.

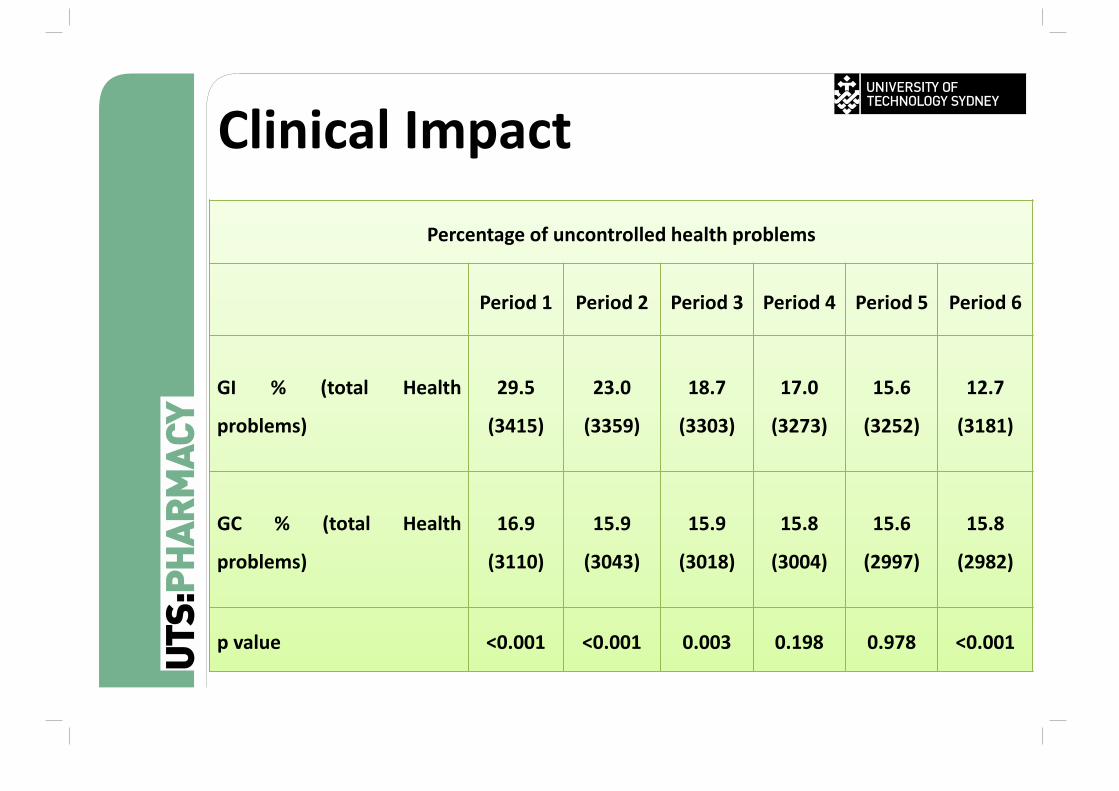

Clinical Impact

Percentage of uncontrolled health problems

Period 1 Period 2 Period 3 Period 4 Period 5 Period 6

GI % (total Health

problems)

29.5

(3415)

23.0

(3359)

18.7

(3303)

17.0

(3273)

15.6

(3252)

12.7

(3181)

GC % (total Health

problems)

16.9

(3110)

15.9

(3043)

15.9

(3018)

15.8

(3004)

15.6

(2997)

15.8

(2982)

p value <0.001 <0.001 0.003 0.198 0.978 <0.001

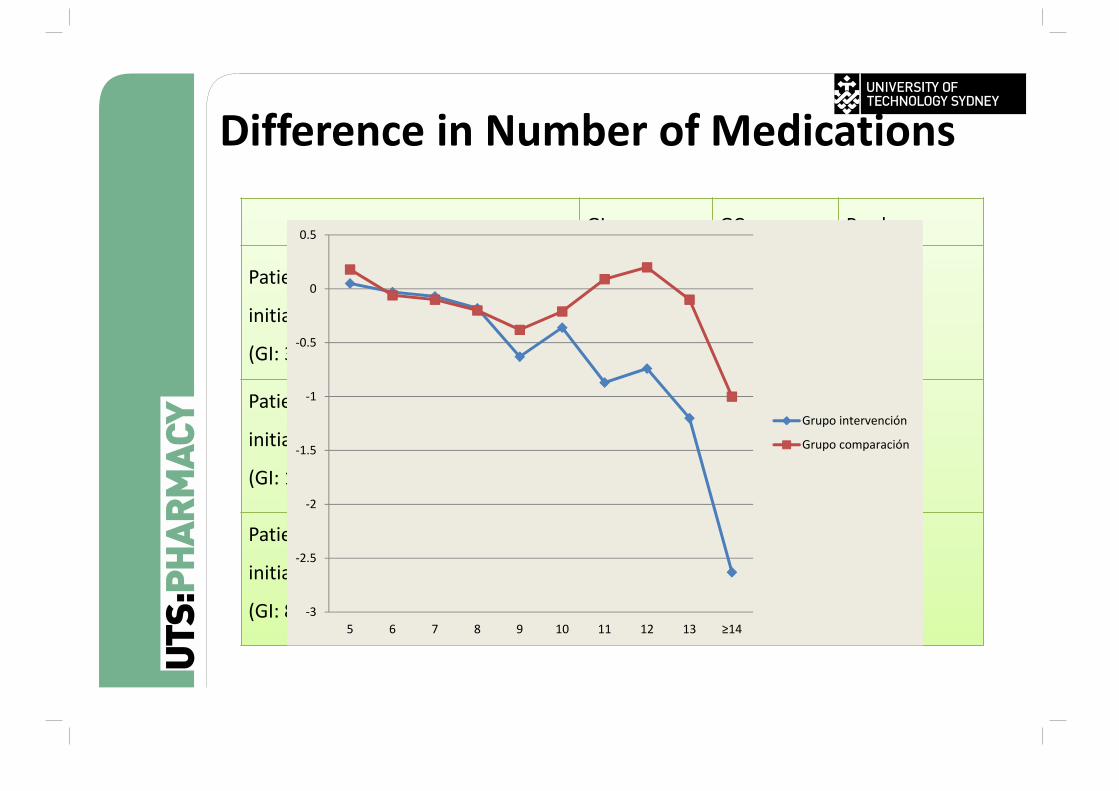

Difference in Number of Medications

GI GC P value

Patients using 5 to 7 medications

initially; mean (SD)

(GI: 369 vs. GC: 435)

‐0.02 (0.91) 0.01 (0.82) 0.649

Patients using 8 to 10 medications

initially; mean (SD)

(GI: 189 vs. GC: 189)‐0.36 (1.29) ‐0.25 (1.08) 0.378

Patients using 5 to 7 medications

initially; mean (SD)

(GI: 88 vs. GC: 63)‐1.20 (1.81) ‐0.19 (1.39) <0.001‡

‐3

‐2.5

‐2

‐1.5

‐1

‐0.5

0

0.5

5 6 7 8 9 10 11 12 13 ≥14

Grupo intervención

Grupo comparación

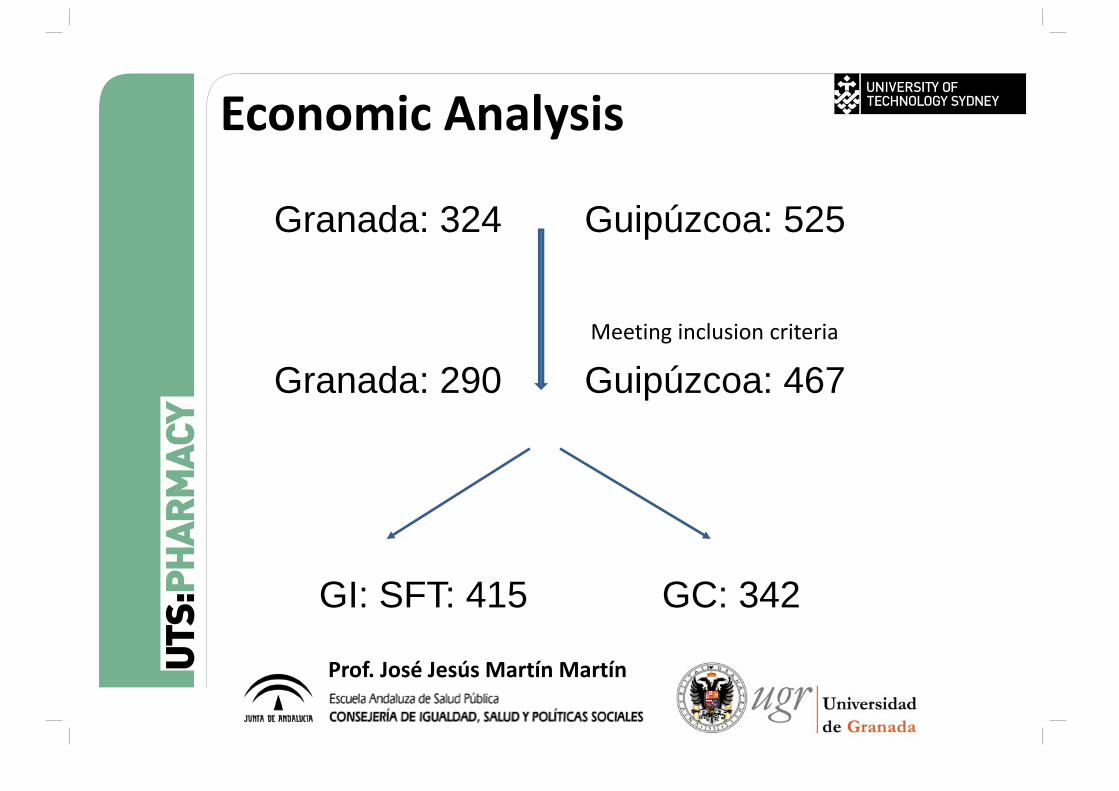

Granada: 324 Guipúzcoa: 525

Meeting inclusion criteria

Granada: 290 Guipúzcoa: 467

GI: SFT: 415 GC: 342

Economic Analysis

Prof. José Jesús Martín Martín

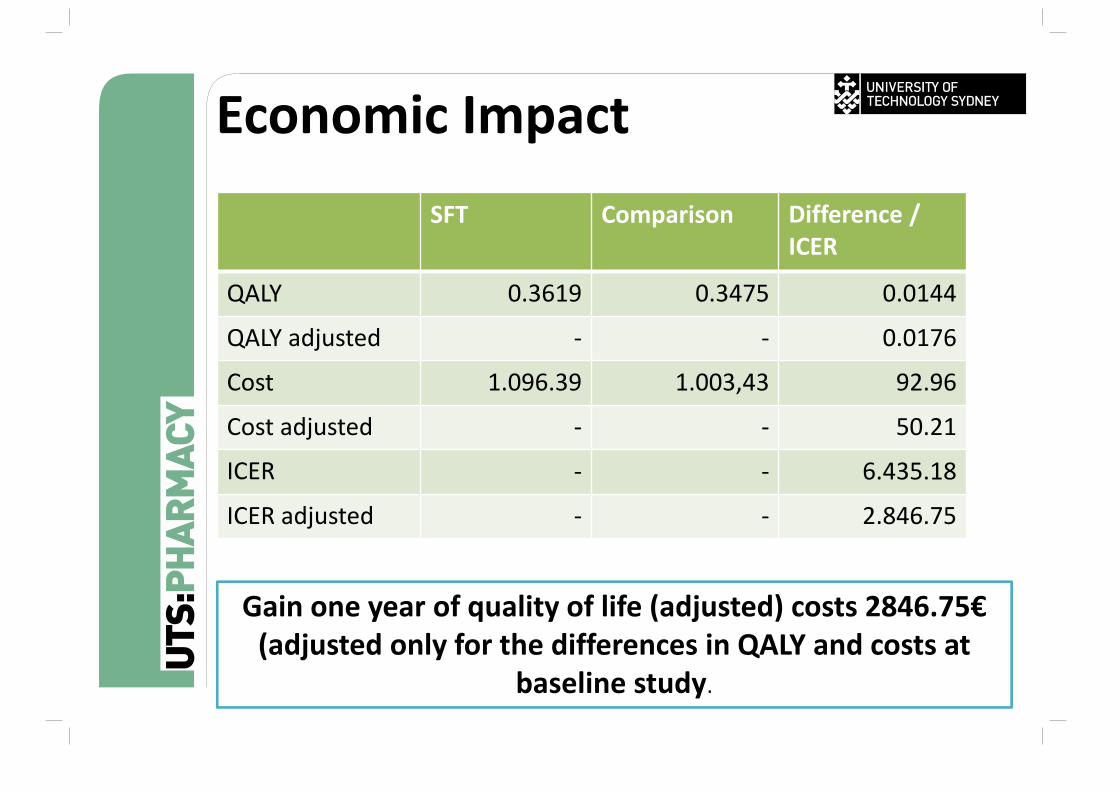

Economic Impact SFT Comparison Difference /

ICER

QALY 0.3619 0.3475 0.0144

QALY adjusted ‐ ‐ 0.0176

Cost 1.096.39 1.003,43 92.96

Cost adjusted ‐ ‐ 50.21

ICER ‐ ‐ 6.435.18

ICER adjusted ‐ ‐ 2.846.75

Gain one year of quality of life (adjusted) costs 2846.75€(adjusted only for the differences in QALY and costs at

baseline study.

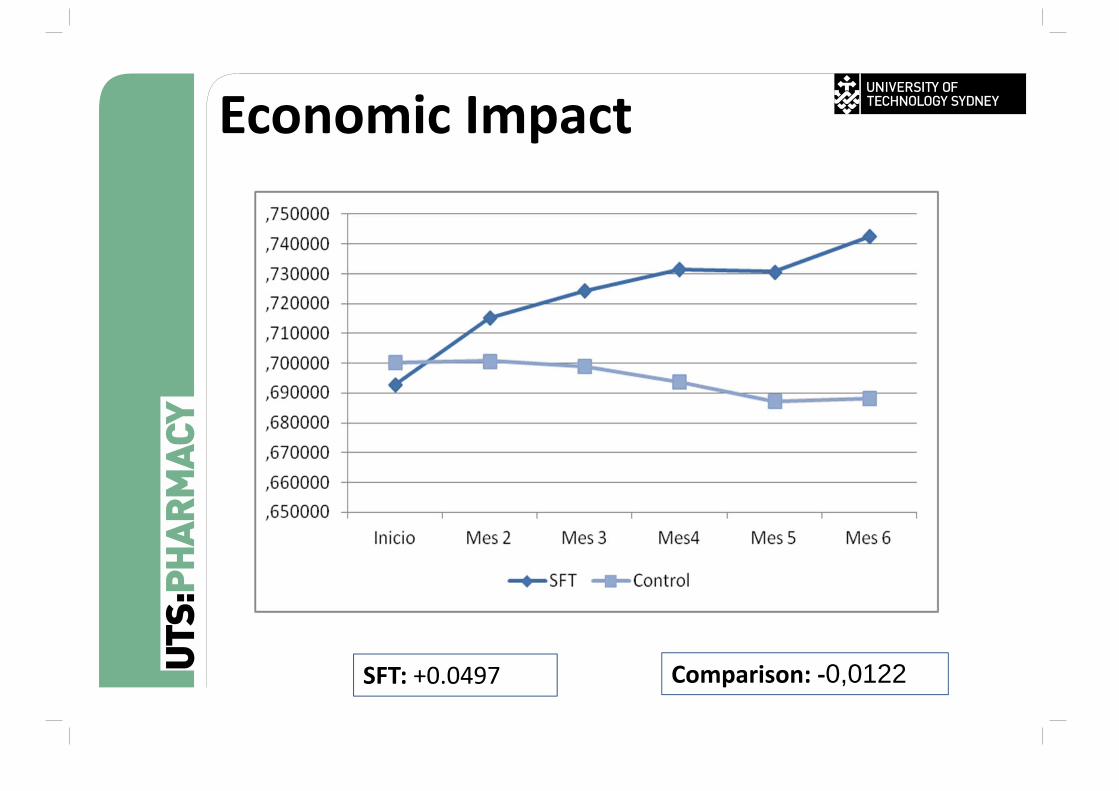

Comparison: ‐0,0122SFT: +0.0497

Economic Impact

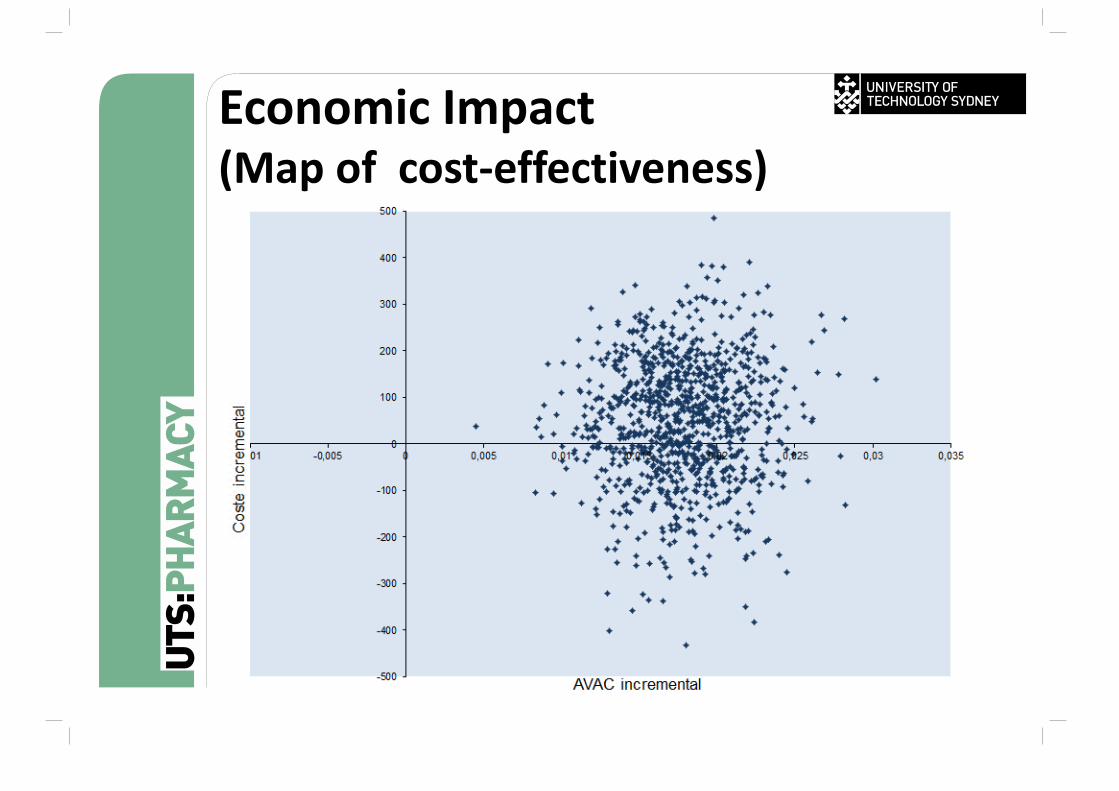

Economic Impact (Map of cost‐effectiveness)

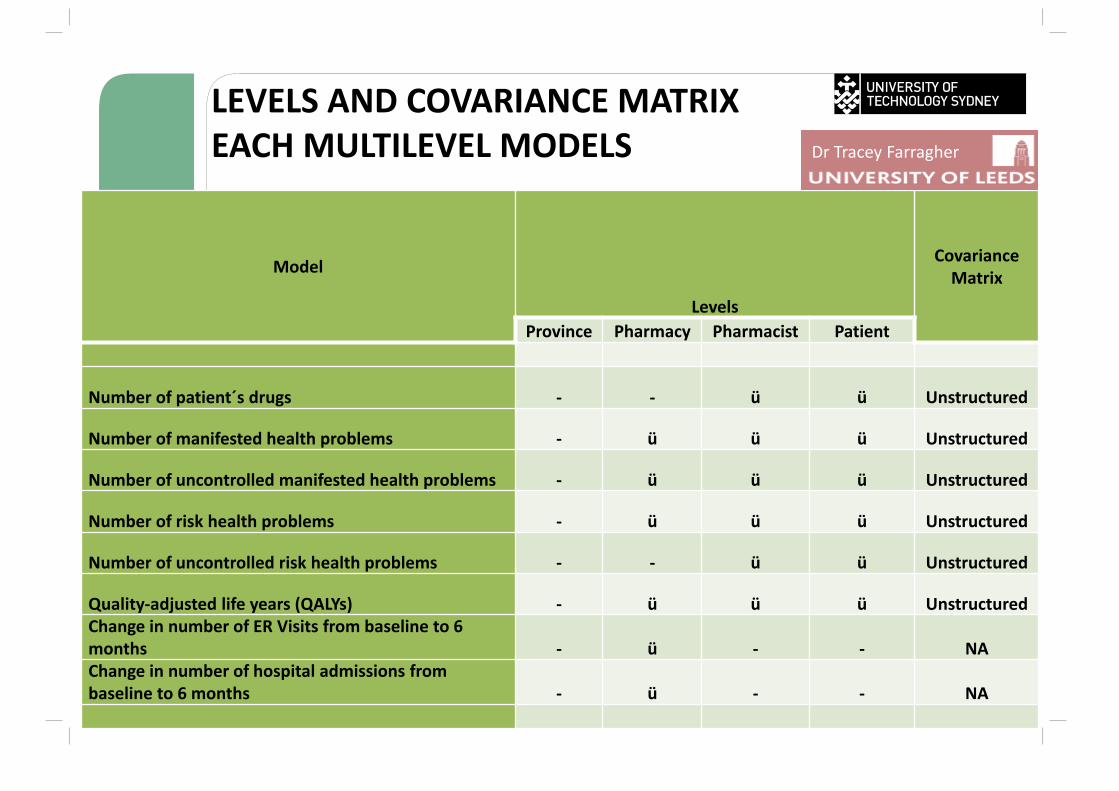

LEVELS AND COVARIANCE MATRIX EACH MULTILEVEL MODELS

Model

Levels

Covariance Matrix

Province Pharmacy Pharmacist Patient

Number of patient´s drugs ‐ ‐ ü ü Unstructured

Number of manifested health problems ‐ ü ü ü Unstructured

Number of uncontrolled manifested health problems ‐ ü ü ü Unstructured

Number of risk health problems ‐ ü ü ü Unstructured

Number of uncontrolled risk health problems ‐ ‐ ü ü Unstructured

Quality‐adjusted life years (QALYs) ‐ ü ü ü UnstructuredChange in number of ER Visits from baseline to 6 months ‐ ü ‐ ‐ NAChange in number of hospital admissions from baseline to 6 months ‐ ü ‐ ‐ NA

Dr Tracey Farragher

45

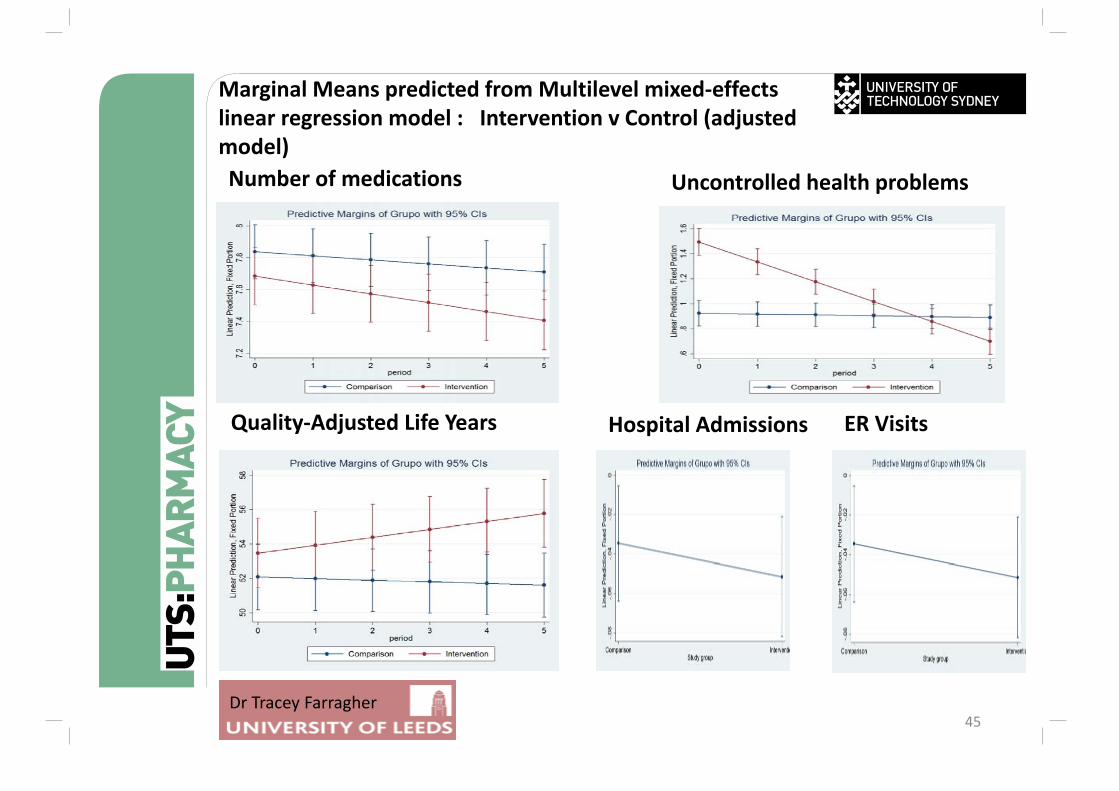

Number of medications

Marginal Means predicted from Multilevel mixed‐effects linear regression model : Intervention v Control (adjusted model)

Uncontrolled health problems

Quality‐Adjusted Life Years Hospital Admissions ER Visits

Dr Tracey Farragher

Conclusion1. Future very challenging for Community

Pharmacy2. Current business model highly questionable 3. Develop new markets in service provision4. Support for the Change ‐ Implementation

and Sustainability program

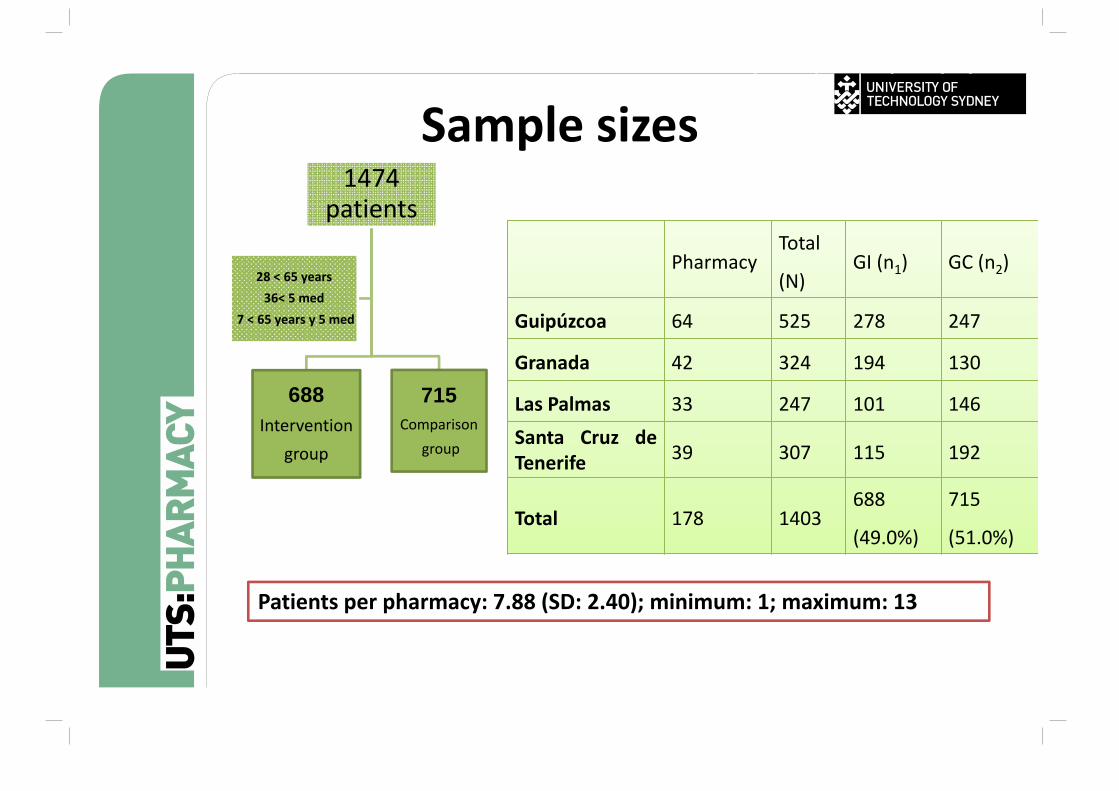

Sample sizes1474

patients

688Intervention

group

715Comparison

group

28 < 65 years36< 5 med

7 < 65 years y 5 med

PharmacyTotal

(N)GI (n1) GC (n2)

Guipúzcoa 64 525 278 247

Granada 42 324 194 130

Las Palmas 33 247 101 146Santa Cruz deTenerife 39 307 115 192

Total 178 1403688

(49.0%)

715

(51.0%)

Patients per pharmacy: 7.88 (SD: 2.40); minimum: 1; maximum: 13

conSIGUE Impacto (estudio principal)