quadrant real estate advisors llc u.s. economic &...

TRANSCRIPT

Quadrant Real Estate Advisors LLC

U.S. Economic & Market

Commentary2nd Quarter 2017

www.quadrantrea.com

Atlanta, Georgia London, England

Kurt Wright, CFA Chief Executive Officer

(770) 752‐6713 [email protected]

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 1 www.quadrantrea.com

Table of Contents

Executive Summary…………………………………………………………………………………………………………………… ....2

State of the U.S. Economy………………………………………………………………………………………………………….….3

Commercial Real Estate Market Relative Value….………………………………………………………………………….6

Commercial Real Estate Market Quadrants………….…………………………………………………………………….….7

Public Debt Market Review…………………………………………………………………………………………………………...8

Public Equity Market Review……………………………………………………………………………………………………….10

Private Debt Market Review……………………………………………………………………….………………………………..12

Private Equity Market Review……………………………………….……………………………………………………………..15

Property Sector Updates & Outlooks……..……………………………………………………………………………………..18

Contacts & Important Disclosures.………………………………………………………………………………………………..28

About Quadrant Real Estate Advisors

Quadrant Real Estate Advisors LLC (“Quadrant”) is a United States SEC registered investment adviser

and Australian Securities and Investments Commission (ASIC) Foreign Registered Corporation (ABN

39 123 863 963). QREA Europe LLP ("QREA") is a subsidiary of Quadrant. QREA Europe LLP

(registration number 610613) is authorized and regulated by the Financial Conduct Authority.

Quadrant has approximately $9.0 billion of commercial and multifamily real estate investments

under management on behalf of institutional investors. Clients include insurance companies,

pension funds, sovereign wealth management funds, and high net worth investors.

Since 1993 Quadrant’s senior management has worked together as a team providing the firm’s

clients with access to both privately placed and publicly traded U.S. commercial real estate debt and

equity investments through commingled funds and single client accounts. In addition to experience,

senior management controls 100% of the firm, thereby providing true alignment of interests and

accountability.

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 2 www.quadrantrea.com

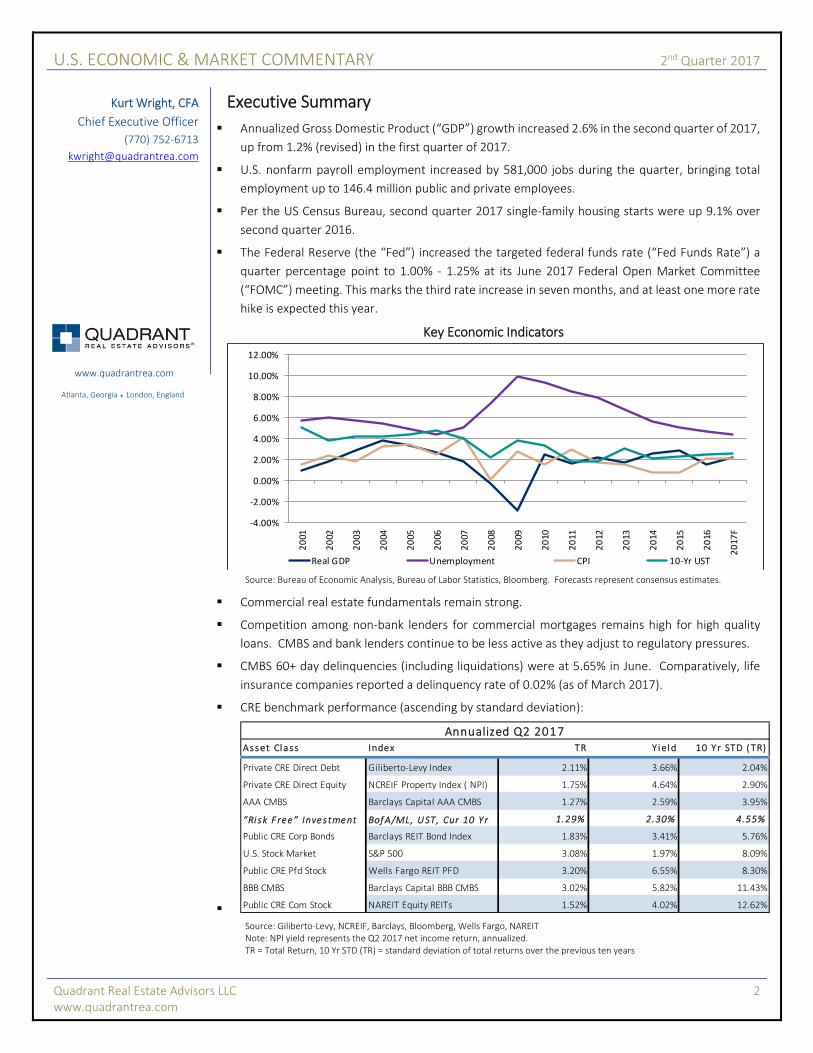

Executive Summary

Annualized Gross Domestic Product (“GDP”) growth increased 2.6% in the second quarter of 2017,

up from 1.2% (revised) in the first quarter of 2017.

U.S. nonfarm payroll employment increased by 581,000 jobs during the quarter, bringing total

employment up to 146.4 million public and private employees.

Per the US Census Bureau, second quarter 2017 single‐family housing starts were up 9.1% over

second quarter 2016.

The Federal Reserve (the “Fed”) increased the targeted federal funds rate (“Fed Funds Rate”) a

quarter percentage point to 1.00% ‐ 1.25% at its June 2017 Federal Open Market Committee

(“FOMC”) meeting. This marks the third rate increase in seven months, and at least one more rate

hike is expected this year.

Key Economic Indicators

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Bloomberg. Forecasts represent consensus estimates.

Commercial real estate fundamentals remain strong.

Competition among non‐bank lenders for commercial mortgages remains high for high quality

loans. CMBS and bank lenders continue to be less active as they adjust to regulatory pressures.

CMBS 60+ day delinquencies (including liquidations) were at 5.65% in June. Comparatively, life

insurance companies reported a delinquency rate of 0.02% (as of March 2017).

CRE benchmark performance (ascending by standard deviation):

Source: Giliberto‐Levy, NCREIF, Barclays, Bloomberg, Wells Fargo, NAREIT Note: NPI yield represents the Q2 2017 net income return, annualized. TR = Total Return, 10 Yr STD (TR) = standard deviation of total returns over the previous ten years

‐4.00%

‐2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

F

Real GDP Unemployment CPI 10‐Yr UST

Asset Class Index TR Y ield 10 Yr STD (TR)

Private CRE Direct Debt Giliberto‐Levy Index 2.11% 3.66% 2.04%

Private CRE Direct Equity NCREIF Property Index ( NPI) 1.75% 4.64% 2.90%

AAA CMBS Barclays Capital AAA CMBS 1.27% 2.59% 3.95%

“Ri sk F ree” Investment BofA/ML, UST, Cur 10 Yr 1.29% 2.30% 4.55%

Public CRE Corp Bonds Barclays REIT Bond Index 1.83% 3.41% 5.76%

U.S. Stock Market S&P 500 3.08% 1.97% 8.09%

Public CRE Pfd Stock Wells Fargo REIT PFD 3.20% 6.55% 8.30%

BBB CMBS Barclays Capital BBB CMBS 3.02% 5.82% 11.43%

Public CRE Com Stock NAREIT Equity REITs 1.52% 4.02% 12.62%

Annualized Q2 2017

Kurt Wright, CFA

Chief Executive Officer

(770) 752‐6713

www.quadrantrea.com

Atlanta, Georgia London, England

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 3 www.quadrantrea.com

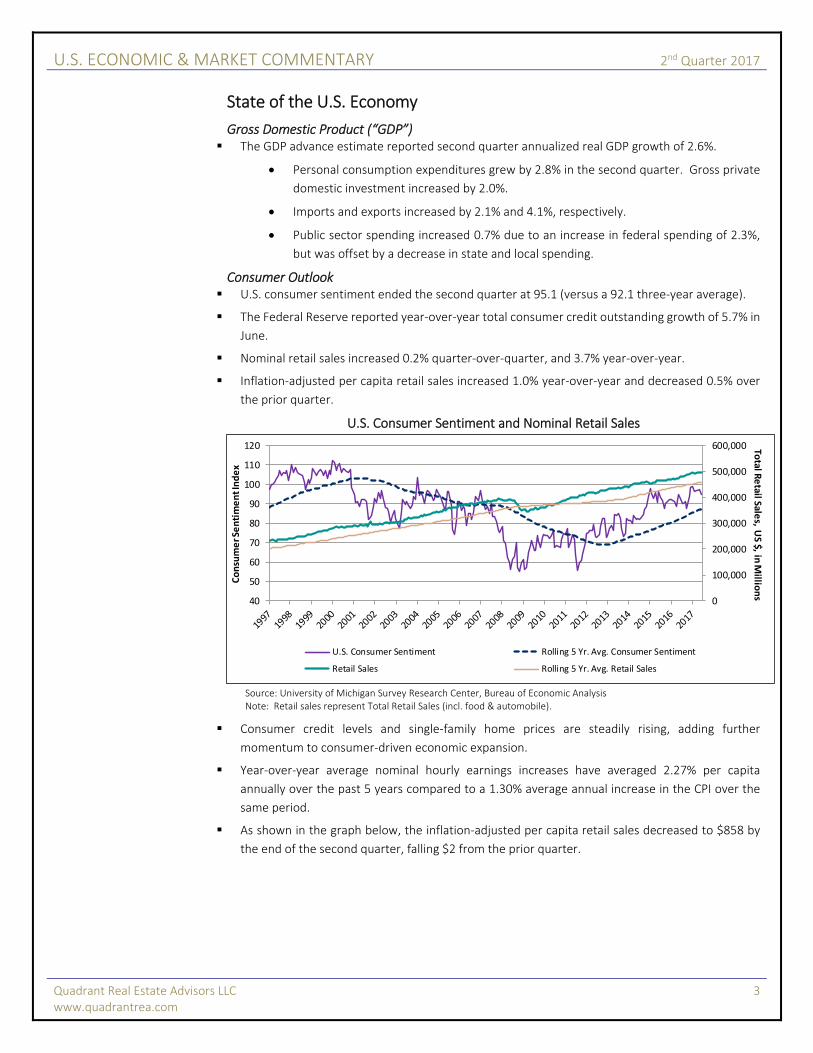

State of the U.S. Economy

Gross Domestic Product (“GDP”) The GDP advance estimate reported second quarter annualized real GDP growth of 2.6%.

Personal consumption expenditures grew by 2.8% in the second quarter. Gross private

domestic investment increased by 2.0%.

Imports and exports increased by 2.1% and 4.1%, respectively.

Public sector spending increased 0.7% due to an increase in federal spending of 2.3%,

but was offset by a decrease in state and local spending.

Consumer Outlook U.S. consumer sentiment ended the second quarter at 95.1 (versus a 92.1 three‐year average).

The Federal Reserve reported year‐over‐year total consumer credit outstanding growth of 5.7% in

June.

Nominal retail sales increased 0.2% quarter‐over‐quarter, and 3.7% year‐over‐year.

Inflation‐adjusted per capita retail sales increased 1.0% year‐over‐year and decreased 0.5% over

the prior quarter.

U.S. Consumer Sentiment and Nominal Retail Sales

Source: University of Michigan Survey Research Center, Bureau of Economic Analysis Note: Retail sales represent Total Retail Sales (incl. food & automobile).

Consumer credit levels and single‐family home prices are steadily rising, adding further

momentum to consumer‐driven economic expansion.

Year‐over‐year average nominal hourly earnings increases have averaged 2.27% per capita

annually over the past 5 years compared to a 1.30% average annual increase in the CPI over the

same period.

As shown in the graph below, the inflation‐adjusted per capita retail sales decreased to $858 by

the end of the second quarter, falling $2 from the prior quarter.

0

100,000

200,000

300,000

400,000

500,000

600,000

40

50

60

70

80

90

100

110

120 Total R

etail Sale

s, US $, in

Millio

ns

Consumer Sentiment Index

U.S. Consumer Sentiment Rolling 5 Yr. Avg. Consumer Sentiment

Retail Sales Rolling 5 Yr. Avg. Retail Sales

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 4 www.quadrantrea.com

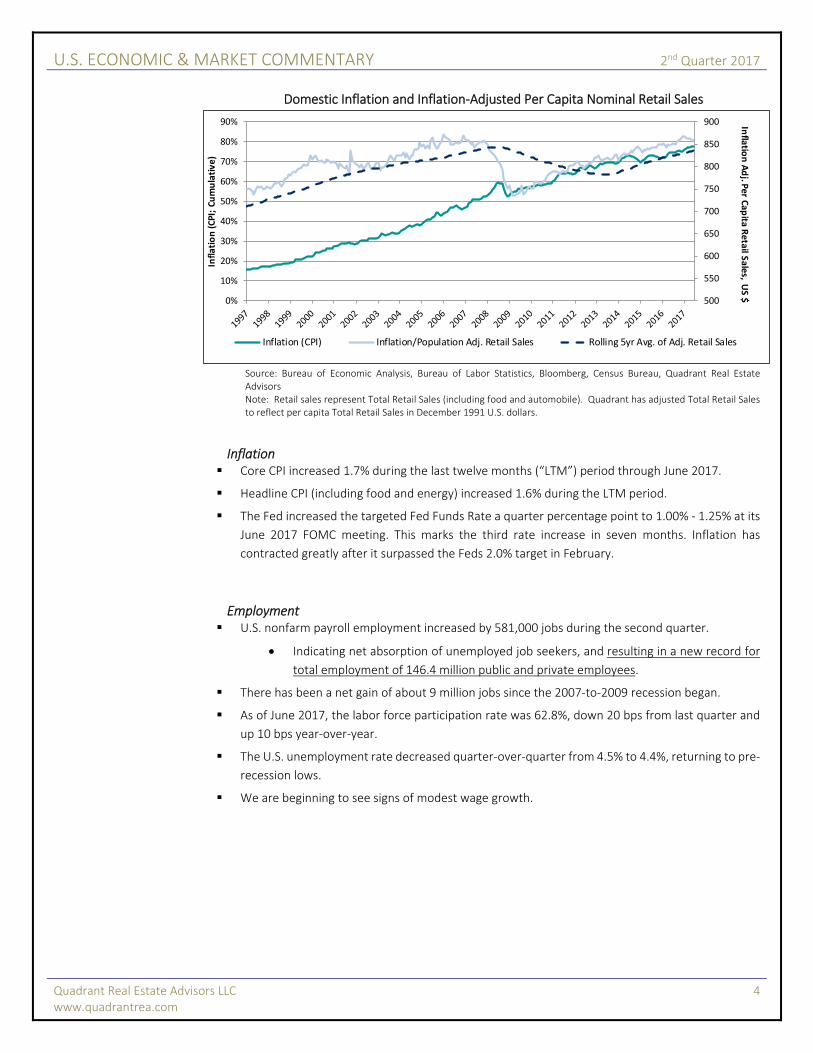

Domestic Inflation and Inflation‐Adjusted Per Capita Nominal Retail Sales

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Bloomberg, Census Bureau, Quadrant Real Estate Advisors Note: Retail sales represent Total Retail Sales (including food and automobile). Quadrant has adjusted Total Retail Sales to reflect per capita Total Retail Sales in December 1991 U.S. dollars.

Inflation Core CPI increased 1.7% during the last twelve months (“LTM”) period through June 2017.

Headline CPI (including food and energy) increased 1.6% during the LTM period.

The Fed increased the targeted Fed Funds Rate a quarter percentage point to 1.00% ‐ 1.25% at its

June 2017 FOMC meeting. This marks the third rate increase in seven months. Inflation has

contracted greatly after it surpassed the Feds 2.0% target in February.

Employment U.S. nonfarm payroll employment increased by 581,000 jobs during the second quarter.

Indicating net absorption of unemployed job seekers, and resulting in a new record for

total employment of 146.4 million public and private employees.

There has been a net gain of about 9 million jobs since the 2007‐to‐2009 recession began.

As of June 2017, the labor force participation rate was 62.8%, down 20 bps from last quarter and

up 10 bps year‐over‐year.

The U.S. unemployment rate decreased quarter‐over‐quarter from 4.5% to 4.4%, returning to pre‐

recession lows.

We are beginning to see signs of modest wage growth.

500

550

600

650

700

750

800

850

900

0%

10%

20%

30%

40%

50%

60%

70%

80%

90% Infla

tion Adj. P

er Cap

ita Retail S

ales, U

S $

Infla

tion (C

PI; Cu

mulative)

Inflation (CPI) Inflation/Population Adj. Retail Sales Rolling 5yr Avg. of Adj. Retail Sales

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 5 www.quadrantrea.com

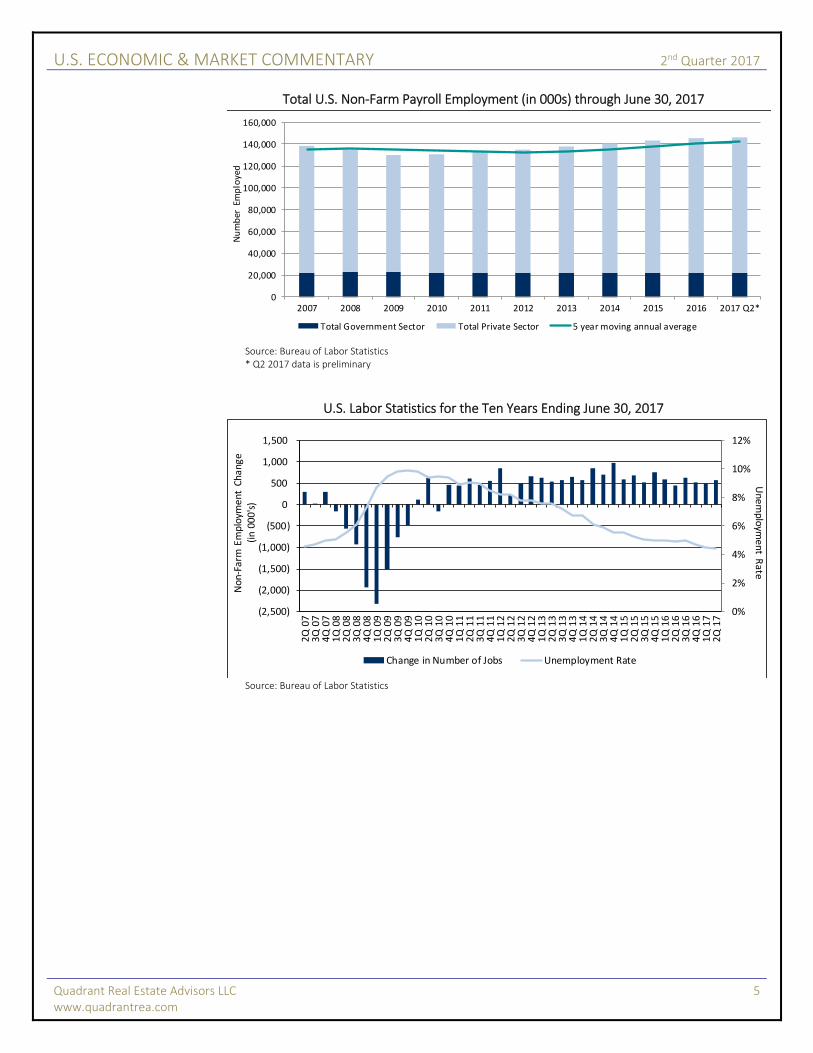

Total U.S. Non‐Farm Payroll Employment (in 000s) through June 30, 2017

Source: Bureau of Labor Statistics * Q2 2017 data is preliminary

U.S. Labor Statistics for the Ten Years Ending June 30, 2017

Source: Bureau of Labor Statistics

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Q2*

Number Employed

Total Government Sector Total Private Sector 5 year moving annual average

0%

2%

4%

6%

8%

10%

12%

(2,500)

(2,000)

(1,500)

(1,000)

(500)

0

500

1,000

1,500

2Q 07

3Q 07

4Q 07

1Q 08

2Q 08

3Q 08

4Q 08

1Q 09

2Q 09

3Q 09

4Q 09

1Q 10

2Q 10

3Q 10

4Q 10

1Q 11

2Q 11

3Q 11

4Q 11

1Q 12

2Q 12

3Q 12

4Q 12

1Q 13

2Q 13

3Q 13

4Q 13

1Q 14

2Q 14

3Q 14

4Q 14

1Q 15

2Q 15

3Q 15

4Q 15

1Q 16

2Q 16

3Q 16

4Q 16

1Q 17

2Q 17

Unemplo

yment R

ate

Non‐Farm

Employm

ent Chang

e

(in 00

0's)

Change in Number of Jobs Unemployment Rate

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 6 www.quadrantrea.com

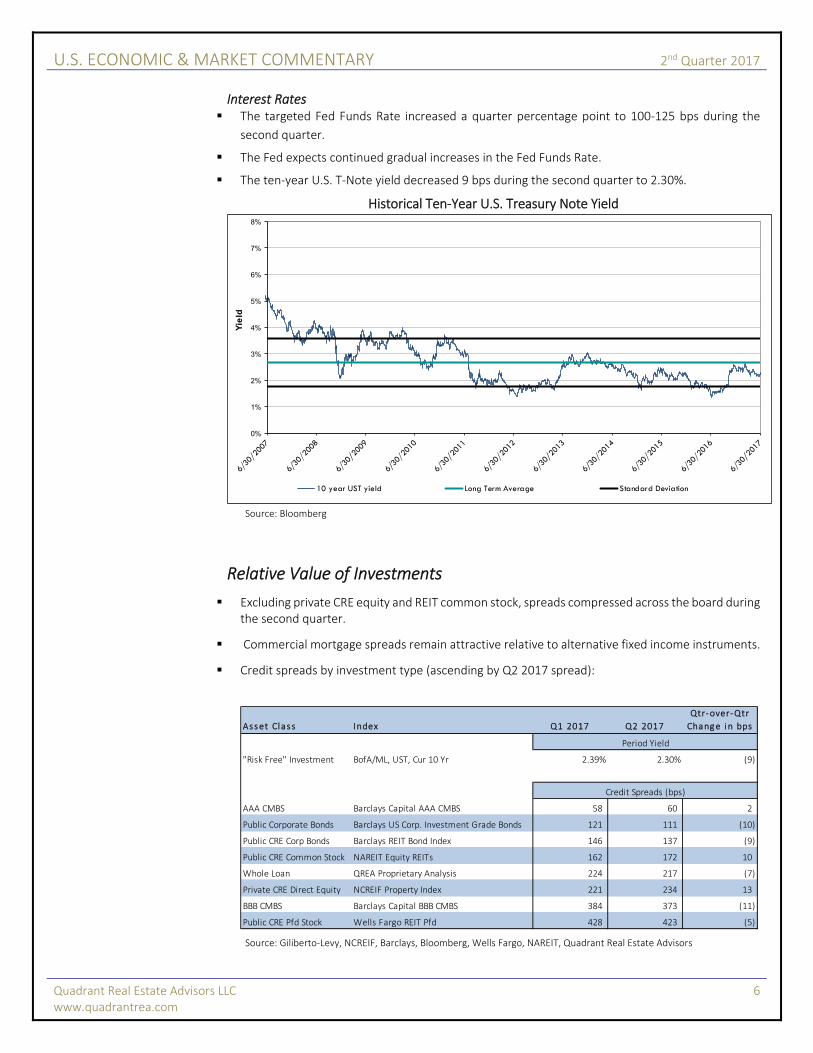

Interest Rates The targeted Fed Funds Rate increased a quarter percentage point to 100‐125 bps during the

second quarter.

The Fed expects continued gradual increases in the Fed Funds Rate.

The ten‐year U.S. T‐Note yield decreased 9 bps during the second quarter to 2.30%.

Historical Ten‐Year U.S. Treasury Note Yield

Source: Bloomberg

Relative Value of Investments

Excluding private CRE equity and REIT common stock, spreads compressed across the board during the second quarter.

Commercial mortgage spreads remain attractive relative to alternative fixed income instruments.

Credit spreads by investment type (ascending by Q2 2017 spread):

Source: Giliberto‐Levy, NCREIF, Barclays, Bloomberg, Wells Fargo, NAREIT, Quadrant Real Estate Advisors

0%

1%

2%

3%

4%

5%

6%

7%

8%

Yield

10 year UST yield Long Term Average Standard Deviation

Asset Class Index Q1 2017 Q2 2017

Qtr‐over‐Qtr

Change in bps

Period Yield

"Risk Free" Investment BofA/ML, UST, Cur 10 Yr 2.39% 2.30% (9)

Credit Spreads (bps)

AAA CMBS Barclays Capital AAA CMBS 58 60 2

Public Corporate Bonds Barclays US Corp. Investment Grade Bonds 121 111 (10)

Public CRE Corp Bonds Barclays REIT Bond Index 146 137 (9)

Public CRE Common Stock NAREIT Equity REITs 162 172 10

Whole Loan QREA Proprietary Analysis 224 217 (7)

Private CRE Direct Equity NCREIF Property Index 221 234 13

BBB CMBS Barclays Capital BBB CMBS 384 373 (11)

Public CRE Pfd Stock Wells Fargo REIT Pfd 428 423 (5)

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 7 www.quadrantrea.com

Commercial Real Estate Market Quadrants

2nd Quarter 2017 Total Returns

Source: Barclays Investment Grade vintage CMBS (Public Debt), NAREIT and Wells Fargo Hybrid & Preferred Securities Equity REIT Index (Public Equity), Giliberto‐Levy Commercial Mortgage Performance Index (Private Debt), NCREIF (Private Equity) LTM – Last Twelve Months

Public Debt:

Delinquencies (60 day +) rose to 5.65% in June and are forecasted to keep rising.

CMBS lenders have been less active in the last few quarters as they have been adjusting to new

regulations; however, second quarter market share is up from 6% to 11%.

Per Morgan Stanley, private label CMBS originations ended 2016 at $66 billion, approximately 31%

lower than 2015’s $95.8 billion. Expectations for 2017 originations range from $55‐$65 billion.

Demand for high grade CMBS will remain strong.

Public Equity

REIT performance has shown a continued recovery after a poor second half 2016.

Private Debt

Portfolio lenders continue to have strong demand for high quality loans.

Delinquency rates remain near 0%.

Credit spreads for transitional loans range from approximately 250 to 450 basis points over libor.

Loan coupons for ten year fixed rate first mortgages are in the 4% range.

Private Equity:

Performance continues to reflect strong CRE fundamentals, vacancy rates are stable, rents are

rising and construction remains reasonable.

Cap rates are near or at their lows; however, financing remains inexpensive for high quality

properties, which should allow for cap rates to remain low.

1.27%1.77%

2.11%1.75%

‐0.50% ‐0.63%

2.08%

7.05%

‐2.00%

‐1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

Public Debt Public Equity Private Debt Private Equity

Total Return ‐ Q2 2017 Total Return ‐ LTM

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 8 www.quadrantrea.com

Public Debt Market Review

Demand Demand for high grade CMBS bonds continues to be strong.

Per the Securities Industry and Financial Markets Association, second quarter average daily non‐

agency CMBS trading volume was approximately $1.7 billion, down approximately 1% year‐over‐

year.

The median of primary dealers’ positions in non‐agency CMBS was $5.8 billion during the second

quarter of 2017, compared to a median of $6.3 billion in the second quarter of 2016.

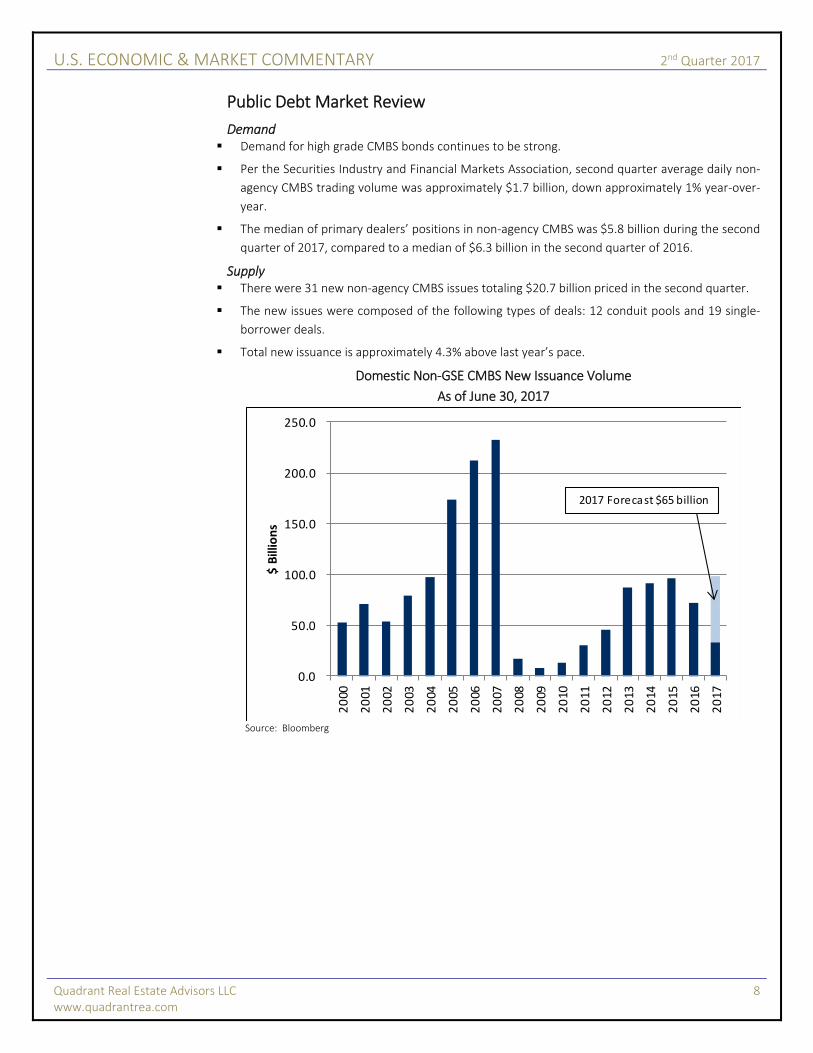

Supply There were 31 new non‐agency CMBS issues totaling $20.7 billion priced in the second quarter.

The new issues were composed of the following types of deals: 12 conduit pools and 19 single‐

borrower deals.

Total new issuance is approximately 4.3% above last year’s pace.

Domestic Non‐GSE CMBS New Issuance Volume

As of June 30, 2017

Source: Bloomberg

0.0

50.0

100.0

150.0

200.0

250.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

$ Billions

2017 Forecast $65 billion

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 9 www.quadrantrea.com

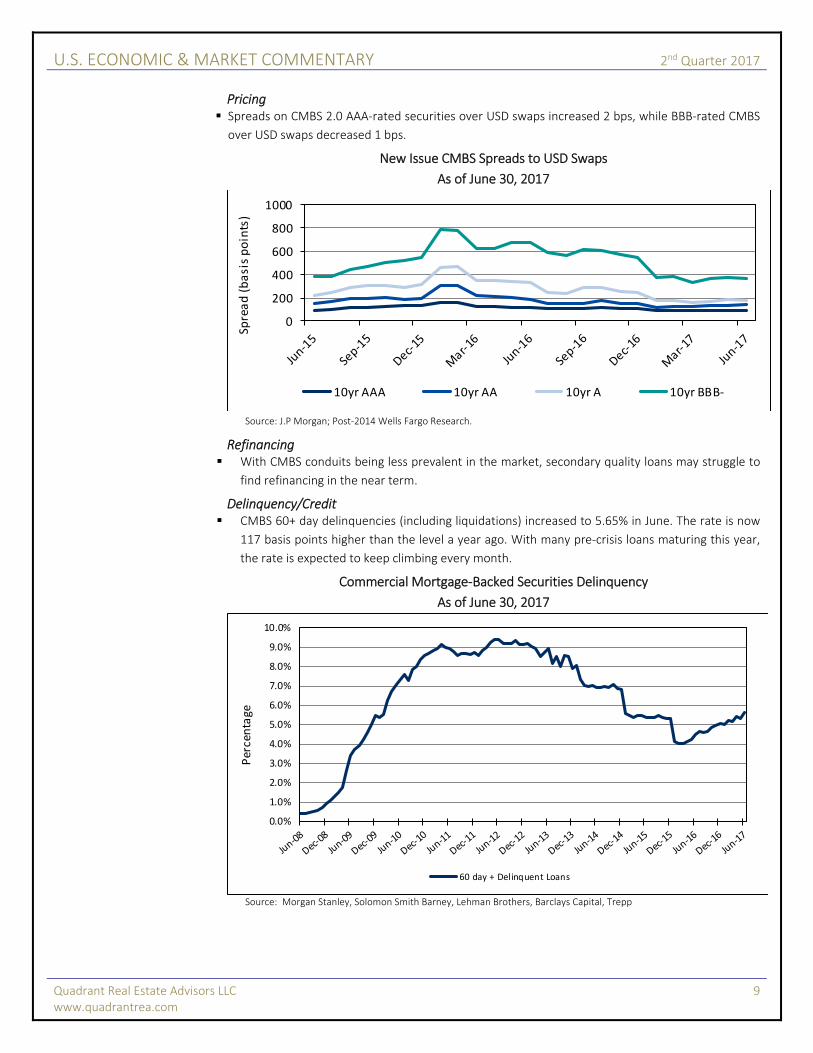

Pricing Spreads on CMBS 2.0 AAA‐rated securities over USD swaps increased 2 bps, while BBB‐rated CMBS

over USD swaps decreased 1 bps.

New Issue CMBS Spreads to USD Swaps

As of June 30, 2017

Source: J.P Morgan; Post‐2014 Wells Fargo Research.

Refinancing With CMBS conduits being less prevalent in the market, secondary quality loans may struggle to

find refinancing in the near term.

Delinquency/Credit CMBS 60+ day delinquencies (including liquidations) increased to 5.65% in June. The rate is now

117 basis points higher than the level a year ago. With many pre‐crisis loans maturing this year,

the rate is expected to keep climbing every month.

Commercial Mortgage‐Backed Securities Delinquency

As of June 30, 2017

Source: Morgan Stanley, Solomon Smith Barney, Lehman Brothers, Barclays Capital, Trepp

0

200

400

600

800

1000

Spread (basis points)

10yr AAA 10yr AA 10yr A 10yr BBB‐

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Percentage

60 day + Delinquent Loans

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 10 www.quadrantrea.com

Problem Loan Liquidation and Modification In May, 48 loans with an original balance of $1.9 billion reported losses totaling $439.0 million. In

June, 23 loans reported losses totaling $150.0 million, bringing the total losses year‐to‐date to $2.4

billion, in line with 2016.

The average loss severity decreased from 2016 levels, with the year‐to‐date average reported at

24.2% compared with an average rate of 35.5% in 2016.

OUTLOOK:

Demand from fixed income investors for high grade CMBS is expected to remain strong. Supply,

however is expected to be limited given that CMBS issuers must consider compliance with the newly

enacted risk retention rules.

Public Equity Market Review

Pricing The NAREIT Equity REITs Index increased 1.52% during the second quarter of 2017.

Sector Activity REITs raised $10.2 billion of senior unsecured debt (29 transactions). Secondary offerings of

common equity totaled $8.8 billion, and secondary offerings of preferred equity totaled $1.2

billion. There were four IPO’s in the second quarter, raising $765.0 million.

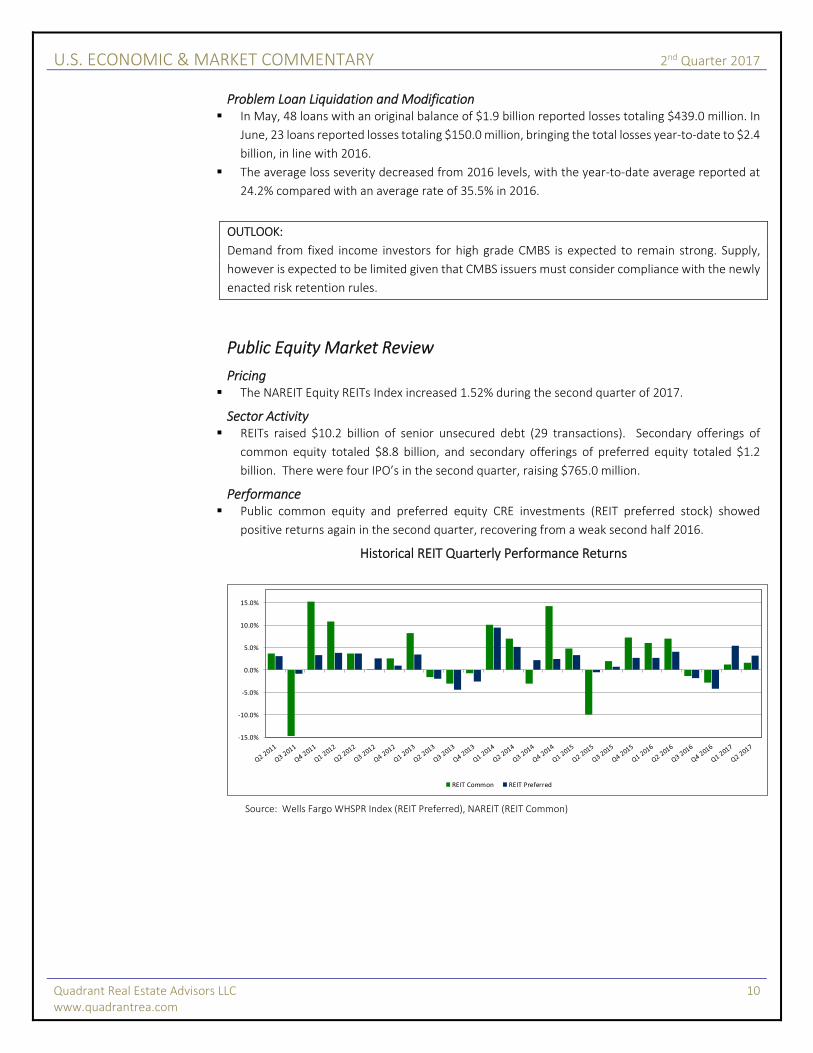

Performance Public common equity and preferred equity CRE investments (REIT preferred stock) showed

positive returns again in the second quarter, recovering from a weak second half 2016.

Historical REIT Quarterly Performance Returns

Source: Wells Fargo WHSPR Index (REIT Preferred), NAREIT (REIT Common)

‐15.0%

‐10.0%

‐5.0%

0.0%

5.0%

10.0%

15.0%

REIT Common REIT Preferred

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 11 www.quadrantrea.com

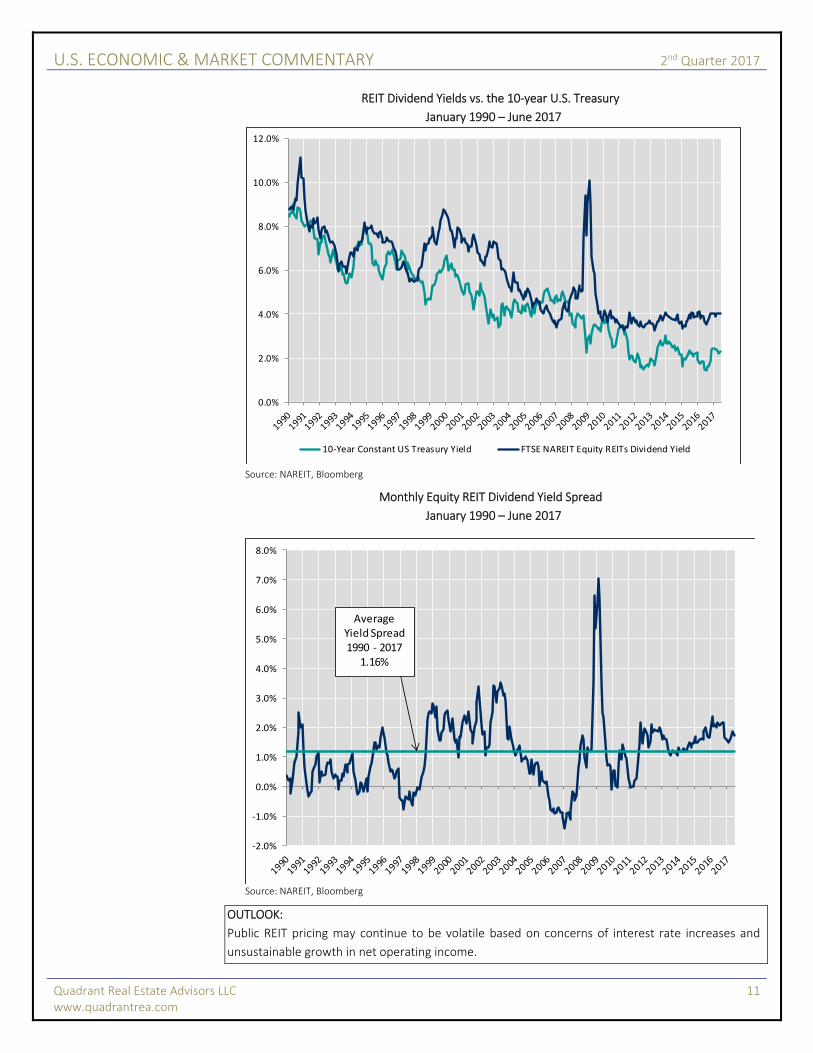

REIT Dividend Yields vs. the 10‐year U.S. Treasury

January 1990 – June 2017

Source: NAREIT, Bloomberg

Monthly Equity REIT Dividend Yield Spread

January 1990 – June 2017

Source: NAREIT, Bloomberg

OUTLOOK:

Public REIT pricing may continue to be volatile based on concerns of interest rate increases and

unsustainable growth in net operating income.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

10‐Year Constant US Treasury Yield FTSE NAREIT Equity REITs Dividend Yield

‐2.0%

‐1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Average Yield Spread 1990 ‐ 2017

1.16%

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 12 www.quadrantrea.com

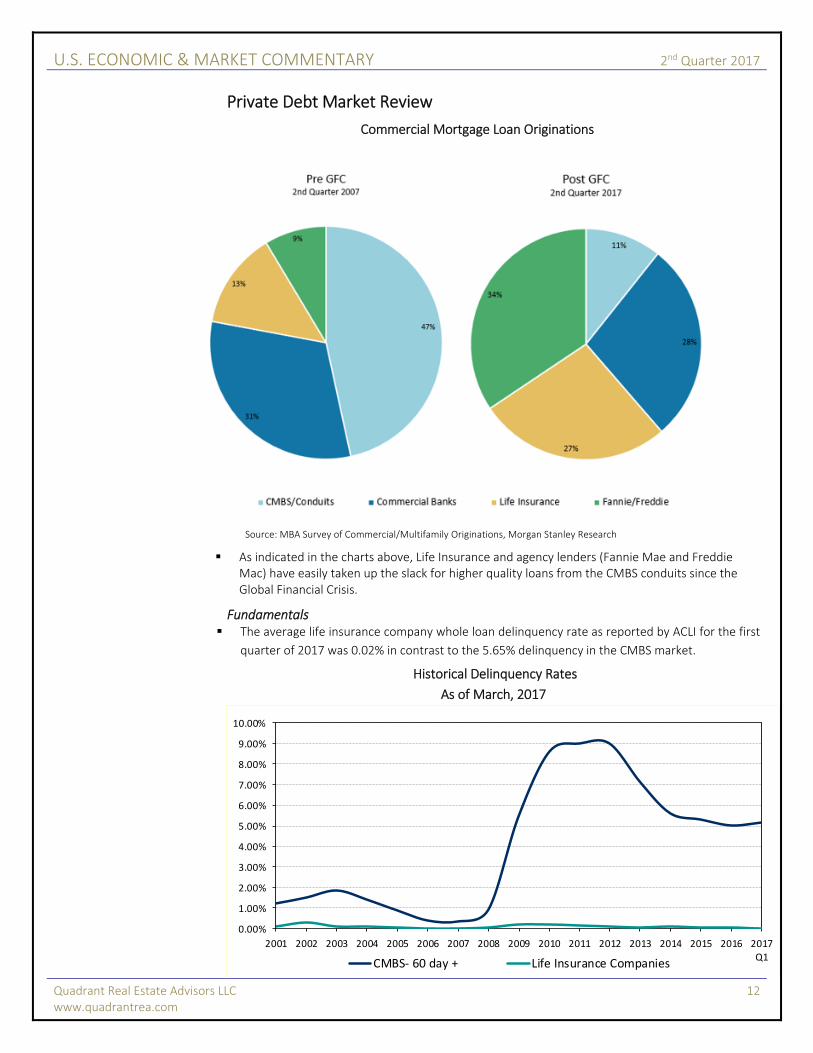

Private Debt Market Review

Commercial Mortgage Loan Originations

Source: MBA Survey of Commercial/Multifamily Originations, Morgan Stanley Research

As indicated in the charts above, Life Insurance and agency lenders (Fannie Mae and Freddie Mac) have easily taken up the slack for higher quality loans from the CMBS conduits since the Global Financial Crisis.

Fundamentals The average life insurance company whole loan delinquency rate as reported by ACLI for the first

quarter of 2017 was 0.02% in contrast to the 5.65% delinquency in the CMBS market.

Historical Delinquency Rates

As of March, 2017

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017Q1

CMBS‐ 60 day + Life Insurance Companies

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 13 www.quadrantrea.com

Source: ACLI, Barclays Capital

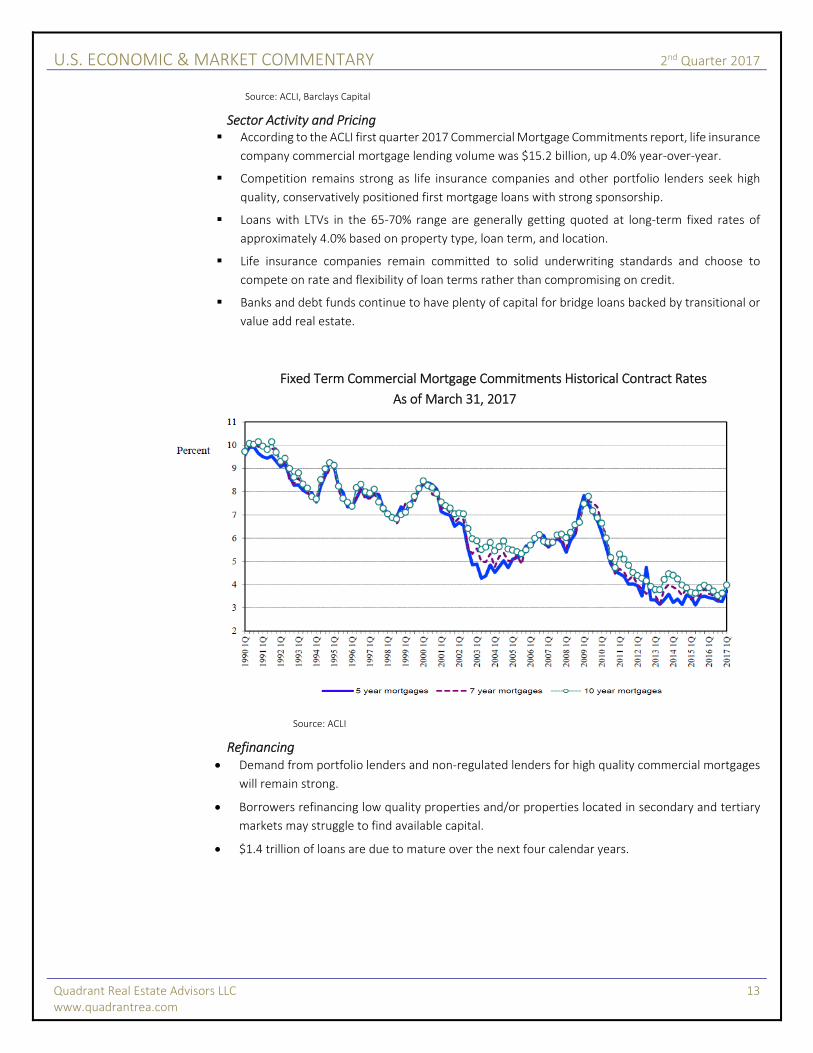

Sector Activity and Pricing According to the ACLI first quarter 2017 Commercial Mortgage Commitments report, life insurance

company commercial mortgage lending volume was $15.2 billion, up 4.0% year‐over‐year.

Competition remains strong as life insurance companies and other portfolio lenders seek high

quality, conservatively positioned first mortgage loans with strong sponsorship.

Loans with LTVs in the 65‐70% range are generally getting quoted at long‐term fixed rates of

approximately 4.0% based on property type, loan term, and location.

Life insurance companies remain committed to solid underwriting standards and choose to

compete on rate and flexibility of loan terms rather than compromising on credit.

Banks and debt funds continue to have plenty of capital for bridge loans backed by transitional or

value add real estate.

Fixed Term Commercial Mortgage Commitments Historical Contract Rates

As of March 31, 2017

Source: ACLI

Refinancing Demand from portfolio lenders and non‐regulated lenders for high quality commercial mortgages

will remain strong.

Borrowers refinancing low quality properties and/or properties located in secondary and tertiary

markets may struggle to find available capital.

$1.4 trillion of loans are due to mature over the next four calendar years.

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 14 www.quadrantrea.com

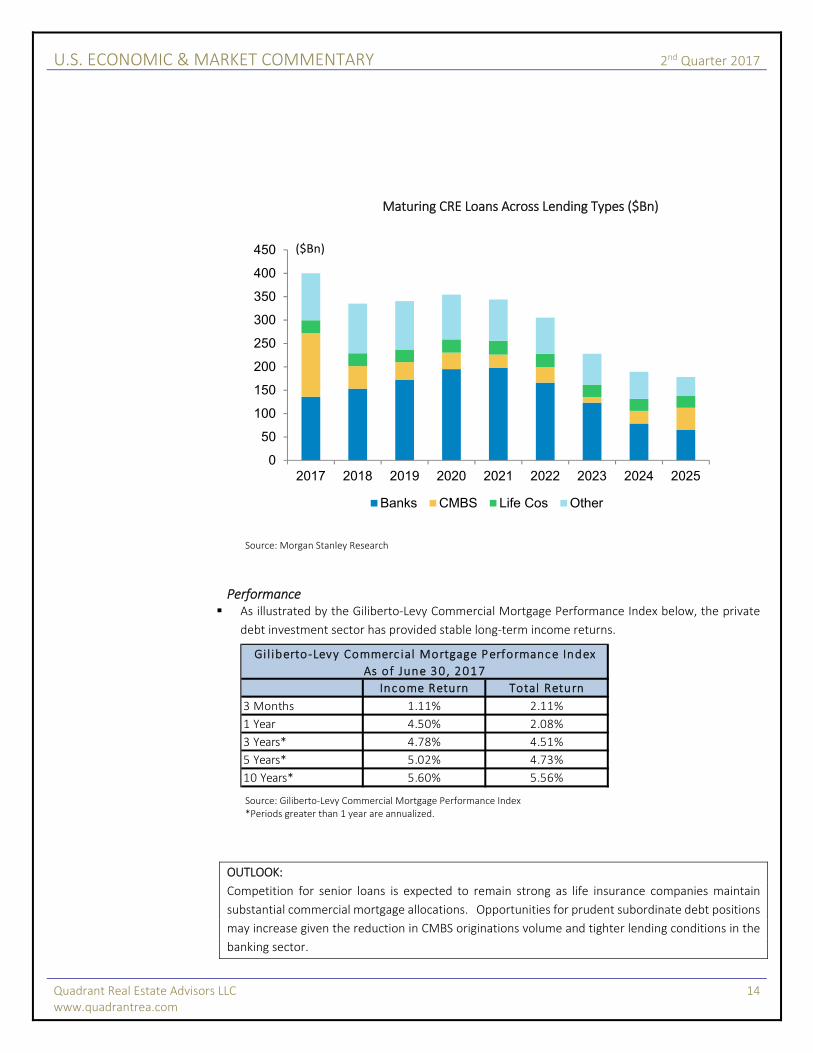

Maturing CRE Loans Across Lending Types ($Bn)

Source: Morgan Stanley Research

Performance As illustrated by the Giliberto‐Levy Commercial Mortgage Performance Index below, the private

debt investment sector has provided stable long‐term income returns.

Source: Giliberto‐Levy Commercial Mortgage Performance Index *Periods greater than 1 year are annualized.

OUTLOOK:

Competition for senior loans is expected to remain strong as life insurance companies maintain

substantial commercial mortgage allocations. Opportunities for prudent subordinate debt positions

may increase given the reduction in CMBS originations volume and tighter lending conditions in the

banking sector.

0

50

100

150

200

250

300

350

400

450

2017 2018 2019 2020 2021 2022 2023 2024 2025

Banks CMBS Life Cos Other

($Bn)

Gil iberto‐Levy Commerc ial Mortgage Performance Index

As of June 30 , 2017

Income Return Total Return

3 Months 1.11% 2.11%

1 Year 4.50% 2.08%

3 Years* 4.78% 4.51%

5 Years* 5.02% 4.73%

10 Years* 5.60% 5.56%

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 15 www.quadrantrea.com

Private Equity Market Review

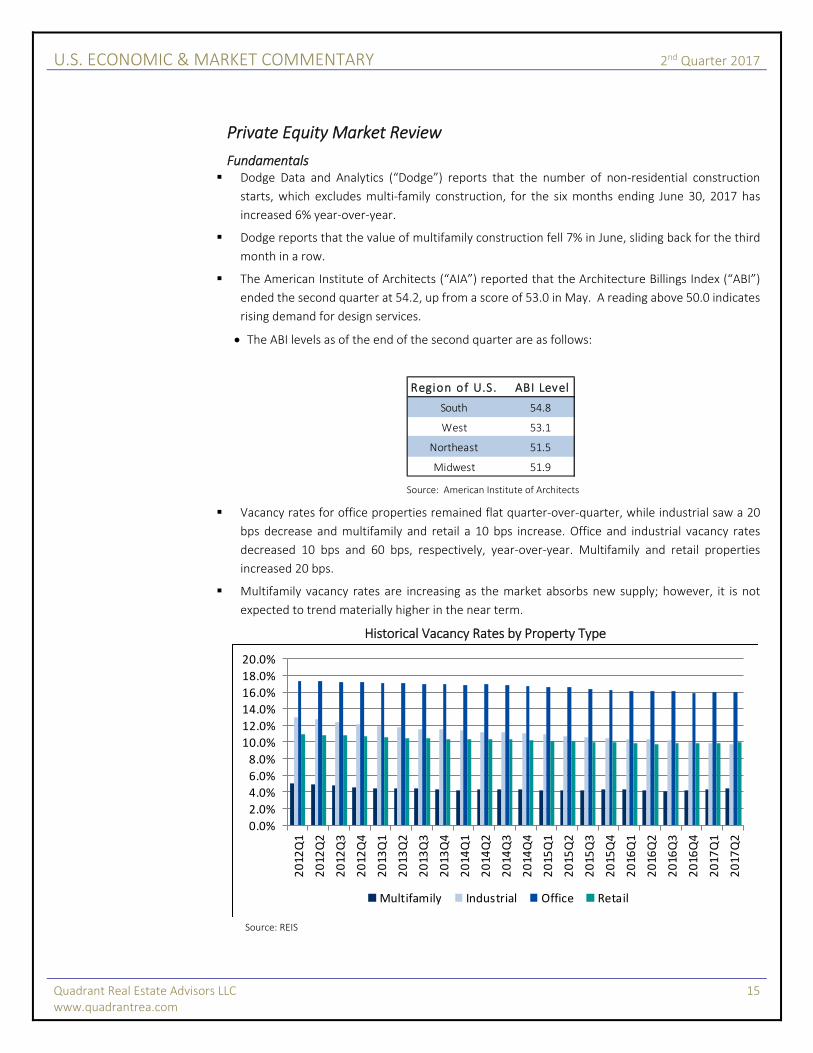

Fundamentals Dodge Data and Analytics (“Dodge”) reports that the number of non‐residential construction

starts, which excludes multi‐family construction, for the six months ending June 30, 2017 has

increased 6% year‐over‐year.

Dodge reports that the value of multifamily construction fell 7% in June, sliding back for the third

month in a row.

The American Institute of Architects (“AIA”) reported that the Architecture Billings Index (“ABI”)

ended the second quarter at 54.2, up from a score of 53.0 in May. A reading above 50.0 indicates

rising demand for design services.

The ABI levels as of the end of the second quarter are as follows:

Source: American Institute of Architects

Vacancy rates for office properties remained flat quarter‐over‐quarter, while industrial saw a 20

bps decrease and multifamily and retail a 10 bps increase. Office and industrial vacancy rates

decreased 10 bps and 60 bps, respectively, year‐over‐year. Multifamily and retail properties

increased 20 bps.

Multifamily vacancy rates are increasing as the market absorbs new supply; however, it is not

expected to trend materially higher in the near term.

Historical Vacancy Rates by Property Type

Source: REIS

Region of U.S. ABI Level

South 54.8

West 53.1

Northeast 51.5

Midwest 51.9

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

Multifamily Industrial Office Retail

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 16 www.quadrantrea.com

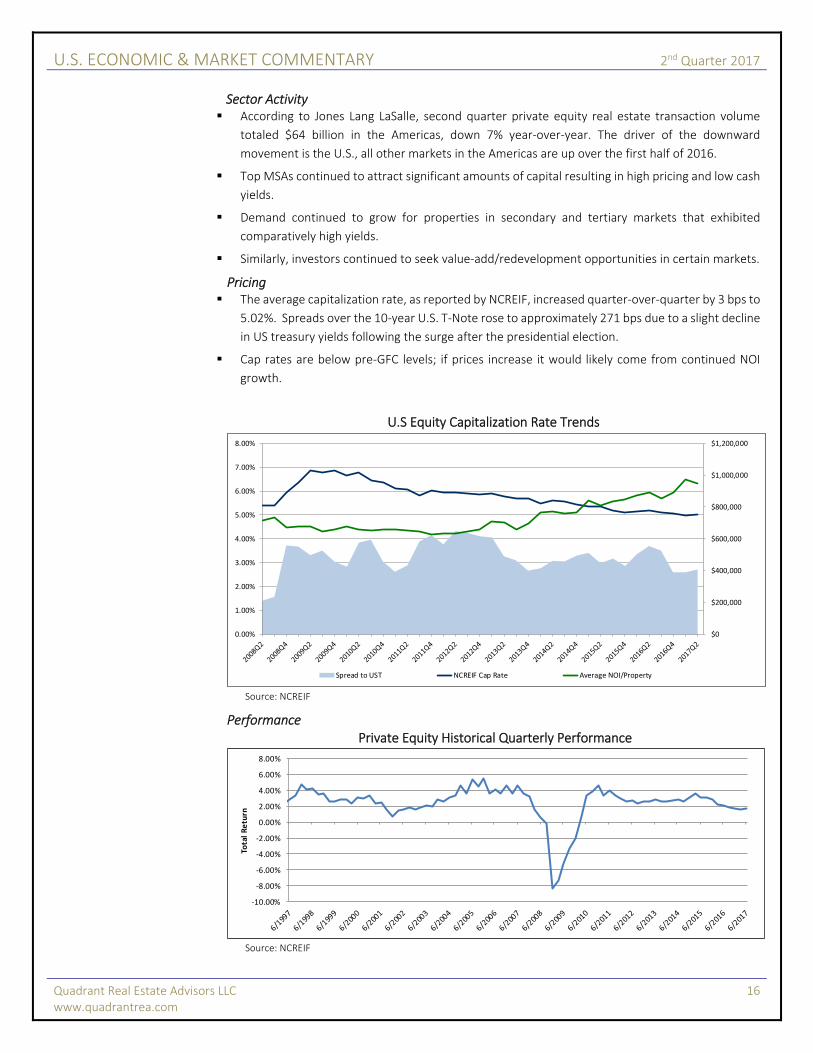

Sector Activity According to Jones Lang LaSalle, second quarter private equity real estate transaction volume

totaled $64 billion in the Americas, down 7% year‐over‐year. The driver of the downward

movement is the U.S., all other markets in the Americas are up over the first half of 2016.

Top MSAs continued to attract significant amounts of capital resulting in high pricing and low cash

yields.

Demand continued to grow for properties in secondary and tertiary markets that exhibited

comparatively high yields.

Similarly, investors continued to seek value‐add/redevelopment opportunities in certain markets.

Pricing The average capitalization rate, as reported by NCREIF, increased quarter‐over‐quarter by 3 bps to

5.02%. Spreads over the 10‐year U.S. T‐Note rose to approximately 271 bps due to a slight decline

in US treasury yields following the surge after the presidential election.

Cap rates are below pre‐GFC levels; if prices increase it would likely come from continued NOI

growth.

U.S Equity Capitalization Rate Trends

Source: NCREIF

Performance Private Equity Historical Quarterly Performance

Source: NCREIF

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

Spread to UST NCREIF Cap Rate Average NOI/Property

‐10.00%

‐8.00%

‐6.00%

‐4.00%

‐2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

Total Return

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 17 www.quadrantrea.com

OUTLOOK: Transaction activity over the next several years for high quality properties will be supported by relatively inexpensive financing options, global capital (equity and debt) inflows, and strong commercial real estate fundamentals. Nominal cap rates are very low in certain primary markets, which limits near‐term valuation upside for stabilized assets in these markets. The spread between primary and secondary markets has begun to tighten as investors seek yield beyond the top CBD markets, although that phenomenon may be short lived if financing becomes less plentiful in those markets. The relatively high cap rate spread over U.S. T‐Notes provides a degree of buffer to rising benchmark interest rates in the near term, which helps reduce rate‐driven downside valuation risk. Furthermore, any incremental increase in inflation, which Quadrant expects to be a prerequisite for the Fed to begin material interest rate increases, should support rising long‐term CRE private equity valuations as rents and construction costs rise (i.e. increasing income and limiting new supply).

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 18 www.quadrantrea.com

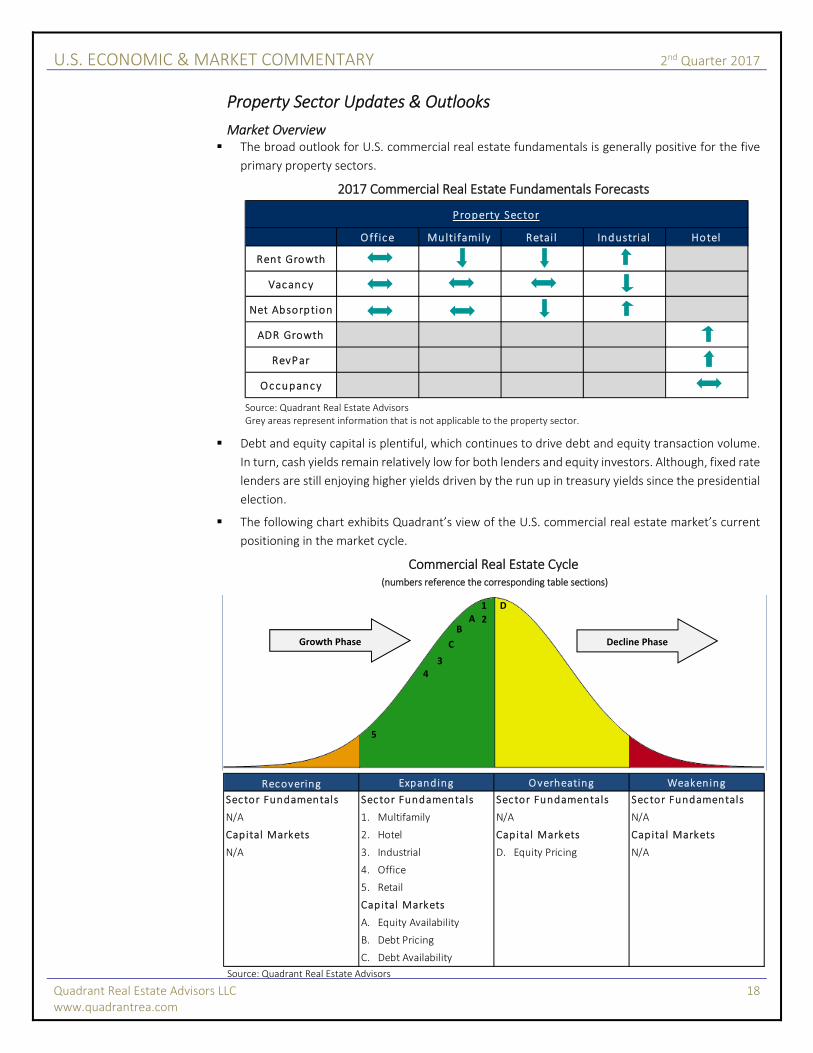

Property Sector Updates & Outlooks

Market Overview The broad outlook for U.S. commercial real estate fundamentals is generally positive for the five

primary property sectors.

2017 Commercial Real Estate Fundamentals Forecasts

Source: Quadrant Real Estate Advisors Grey areas represent information that is not applicable to the property sector.

Debt and equity capital is plentiful, which continues to drive debt and equity transaction volume.

In turn, cash yields remain relatively low for both lenders and equity investors. Although, fixed rate

lenders are still enjoying higher yields driven by the run up in treasury yields since the presidential

election.

The following chart exhibits Quadrant’s view of the U.S. commercial real estate market’s current

positioning in the market cycle.

Commercial Real Estate Cycle (numbers reference the corresponding table sections)

Source: Quadrant Real Estate Advisors

Off ice Multifamily Retai l Industrial Hotel

Rent Growth

Vacancy

Net Absorption

ADR Growth

RevPar

Occupancy

Property Sector

Recovering Expanding Overheating Weakening

Sector Fundamentals Sector Fundamentals Sector Fundamentals Sector Fundamentals

N/A 1. Multifamily N/A N/A

Capital Markets 2. Hotel Capital Markets Capital Markets

N/A 3. Industrial D. Equity Pricing N/A

4. Office

5. Retail

Capital Markets

A. Equity Availability

B. Debt Pricing

C. Debt Availability

Growth Phase Decline Phase

1

2

3 4

5

A D

B

C

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 19 www.quadrantrea.com

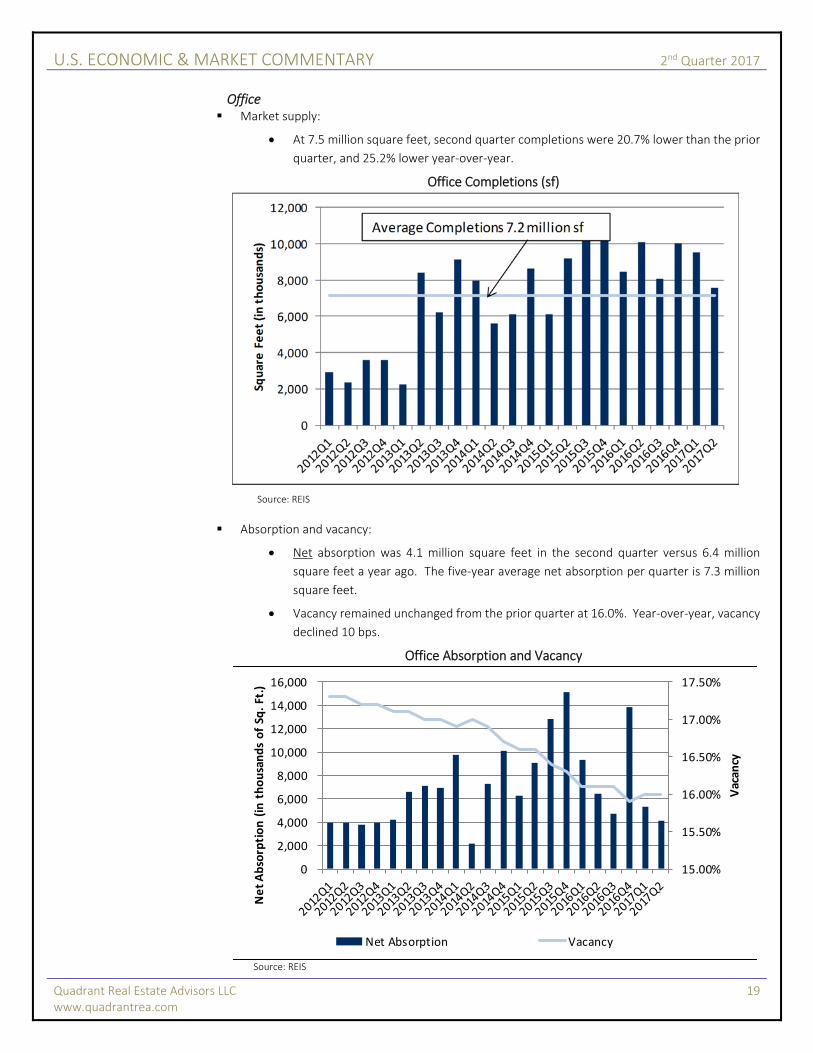

Office Market supply:

At 7.5 million square feet, second quarter completions were 20.7% lower than the prior

quarter, and 25.2% lower year‐over‐year.

Office Completions (sf)

Source: REIS

Absorption and vacancy:

Net absorption was 4.1 million square feet in the second quarter versus 6.4 million

square feet a year ago. The five‐year average net absorption per quarter is 7.3 million

square feet.

Vacancy remained unchanged from the prior quarter at 16.0%. Year‐over‐year, vacancy

declined 10 bps.

Office Absorption and Vacancy

Source: REIS

15.00%

15.50%

16.00%

16.50%

17.00%

17.50%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Vacan

cy

Net Absorption (in thousands of Sq

. Ft.)

Net Absorption Vacancy

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 20 www.quadrantrea.com

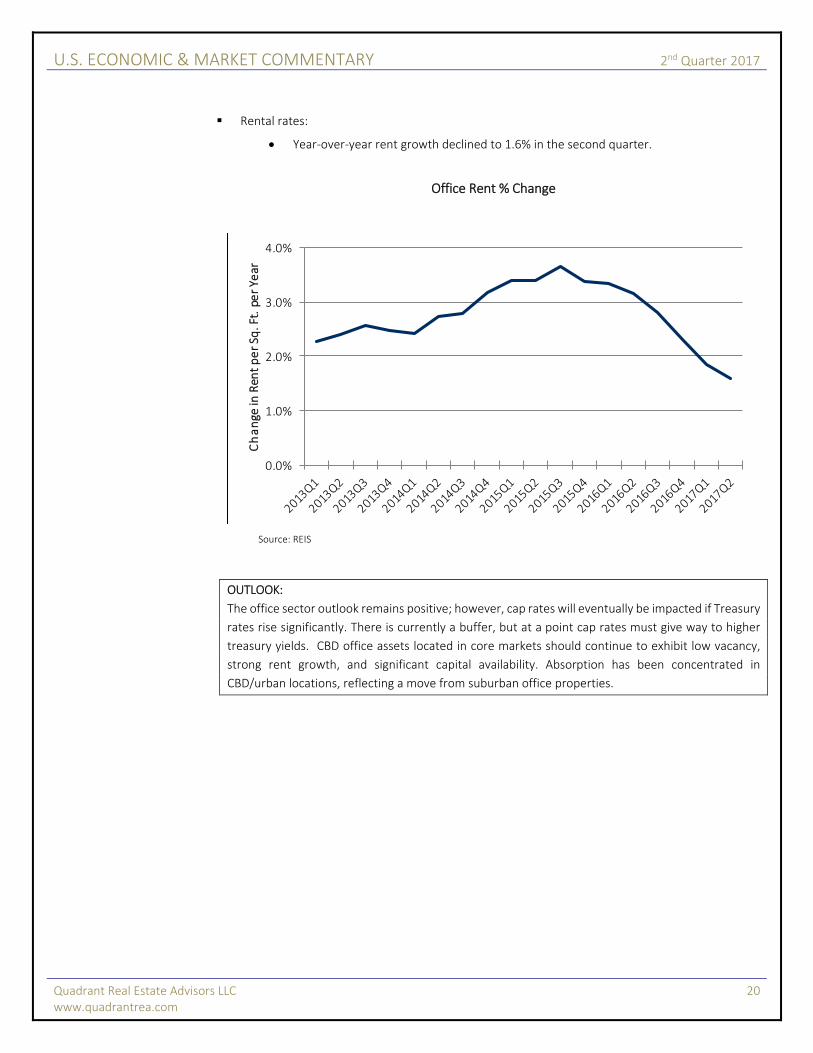

Rental rates:

Year‐over‐year rent growth declined to 1.6% in the second quarter.

Office Rent % Change

Source: REIS

OUTLOOK:

The office sector outlook remains positive; however, cap rates will eventually be impacted if Treasury

rates rise significantly. There is currently a buffer, but at a point cap rates must give way to higher

treasury yields. CBD office assets located in core markets should continue to exhibit low vacancy,

strong rent growth, and significant capital availability. Absorption has been concentrated in

CBD/urban locations, reflecting a move from suburban office properties.

0.0%

1.0%

2.0%

3.0%

4.0%Change in

Ren

t per Sq

. Ft. per Ye

ar

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 21 www.quadrantrea.com

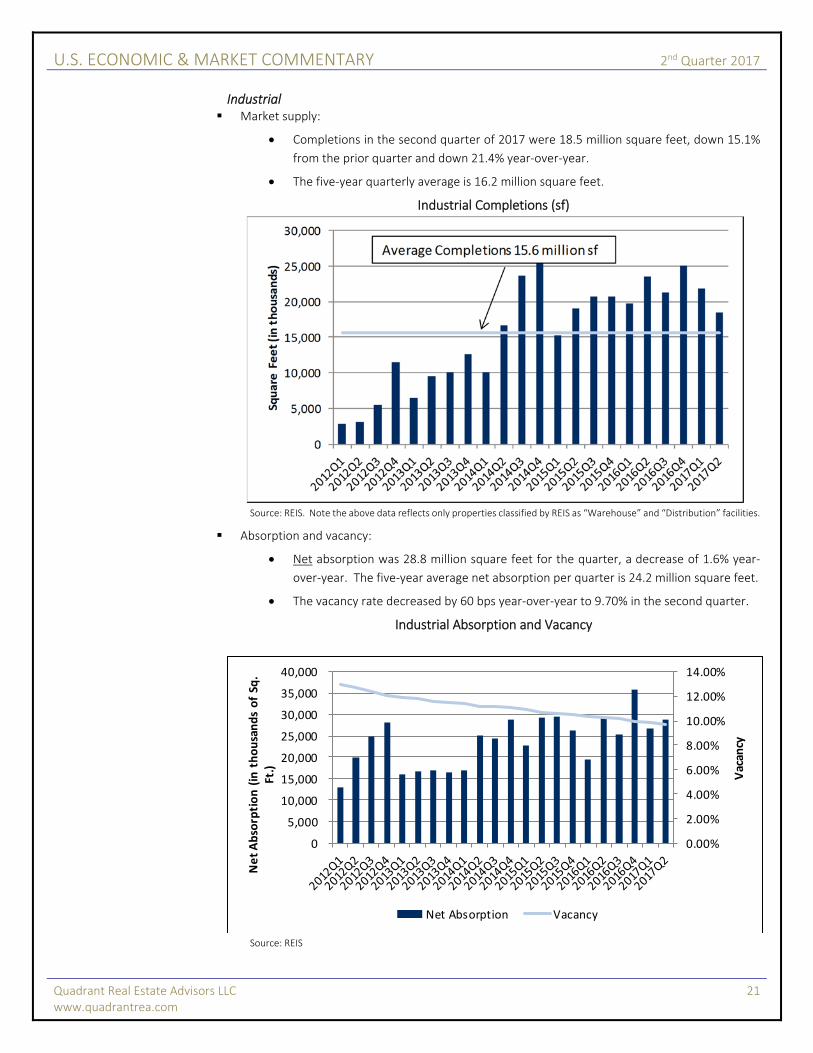

Industrial Market supply:

Completions in the second quarter of 2017 were 18.5 million square feet, down 15.1%

from the prior quarter and down 21.4% year‐over‐year.

The five‐year quarterly average is 16.2 million square feet.

Industrial Completions (sf)

Source: REIS. Note the above data reflects only properties classified by REIS as “Warehouse” and “Distribution” facilities.

Absorption and vacancy:

Net absorption was 28.8 million square feet for the quarter, a decrease of 1.6% year‐

over‐year. The five‐year average net absorption per quarter is 24.2 million square feet.

The vacancy rate decreased by 60 bps year‐over‐year to 9.70% in the second quarter.

Industrial Absorption and Vacancy

Source: REIS

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Vacan

cy

Net Absorption (in thousands of Sq

. Ft.)

Net Absorption Vacancy

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 22 www.quadrantrea.com

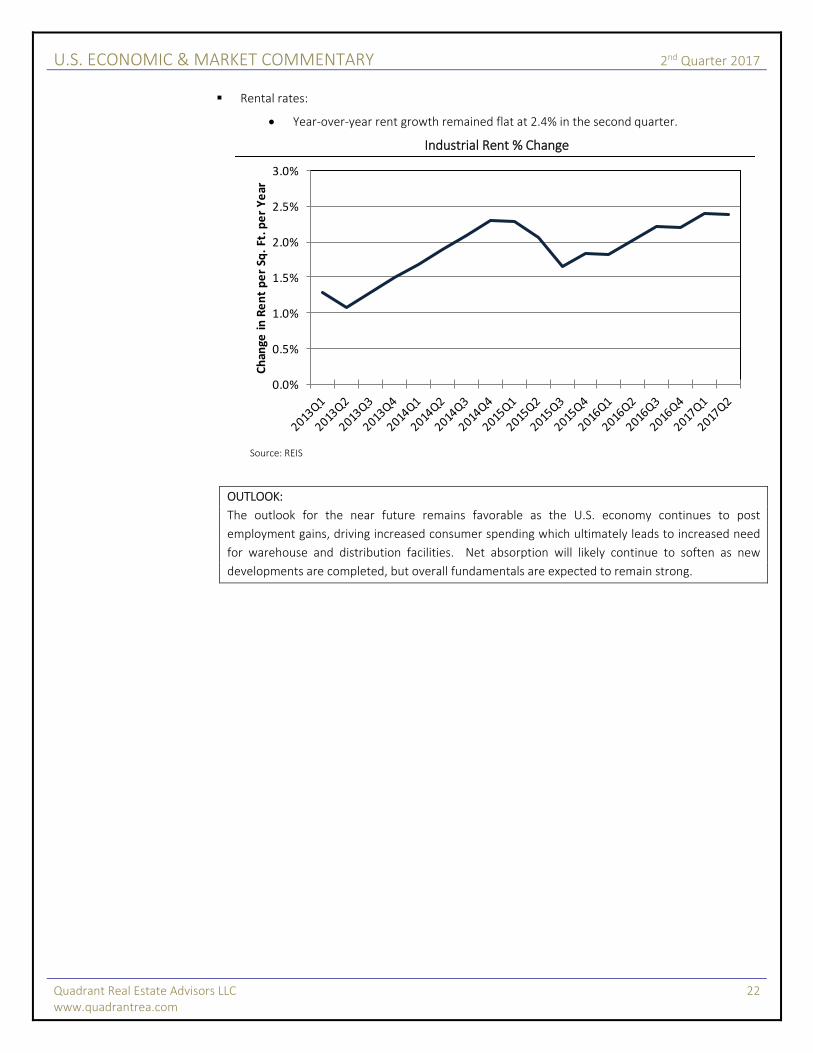

Rental rates:

Year‐over‐year rent growth remained flat at 2.4% in the second quarter.

Industrial Rent % Change

Source: REIS

OUTLOOK:

The outlook for the near future remains favorable as the U.S. economy continues to post

employment gains, driving increased consumer spending which ultimately leads to increased need

for warehouse and distribution facilities. Net absorption will likely continue to soften as new

developments are completed, but overall fundamentals are expected to remain strong.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Chan

ge in Rent per Sq

. Ft. p

er Year

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 23 www.quadrantrea.com

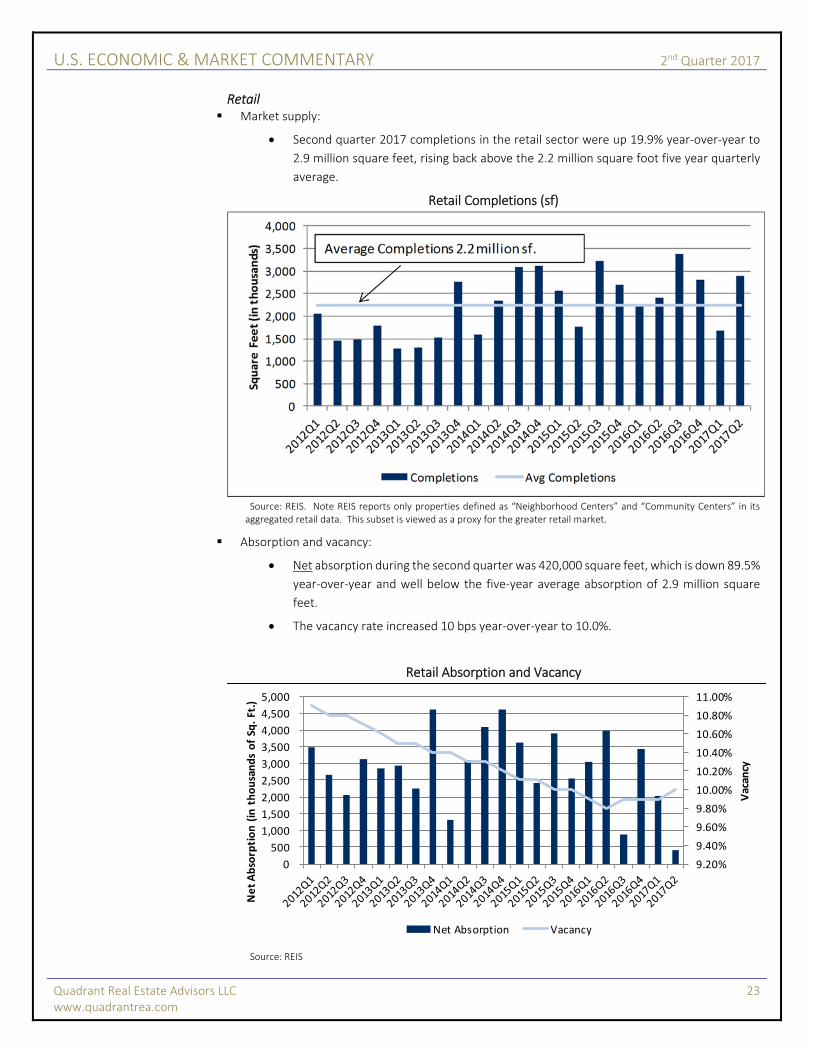

Retail Market supply:

Second quarter 2017 completions in the retail sector were up 19.9% year‐over‐year to

2.9 million square feet, rising back above the 2.2 million square foot five year quarterly

average.

Retail Completions (sf)

Source: REIS. Note REIS reports only properties defined as “Neighborhood Centers” and “Community Centers” in its aggregated retail data. This subset is viewed as a proxy for the greater retail market.

Absorption and vacancy:

Net absorption during the second quarter was 420,000 square feet, which is down 89.5%

year‐over‐year and well below the five‐year average absorption of 2.9 million square

feet.

The vacancy rate increased 10 bps year‐over‐year to 10.0%.

Retail Absorption and Vacancy

Source: REIS

9.20%

9.40%

9.60%

9.80%

10.00%

10.20%

10.40%

10.60%

10.80%

11.00%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Vacan

cy

Net Absorption (in thousands of Sq

. Ft.)

Net Absorption Vacancy

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 24 www.quadrantrea.com

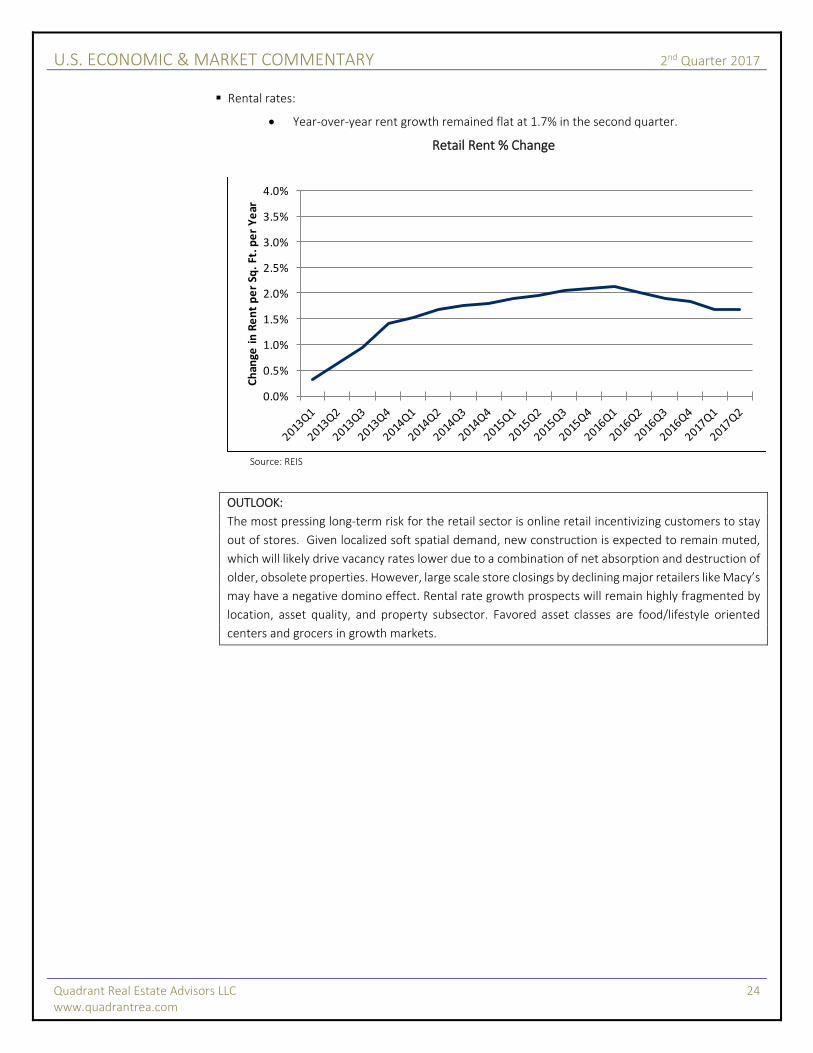

Rental rates:

Year‐over‐year rent growth remained flat at 1.7% in the second quarter.

Retail Rent % Change

Source: REIS

OUTLOOK:

The most pressing long‐term risk for the retail sector is online retail incentivizing customers to stay

out of stores. Given localized soft spatial demand, new construction is expected to remain muted,

which will likely drive vacancy rates lower due to a combination of net absorption and destruction of

older, obsolete properties. However, large scale store closings by declining major retailers like Macy’s

may have a negative domino effect. Rental rate growth prospects will remain highly fragmented by

location, asset quality, and property subsector. Favored asset classes are food/lifestyle oriented

centers and grocers in growth markets.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Chan

ge in Rent per Sq

. Ft. p

er Year

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 25 www.quadrantrea.com

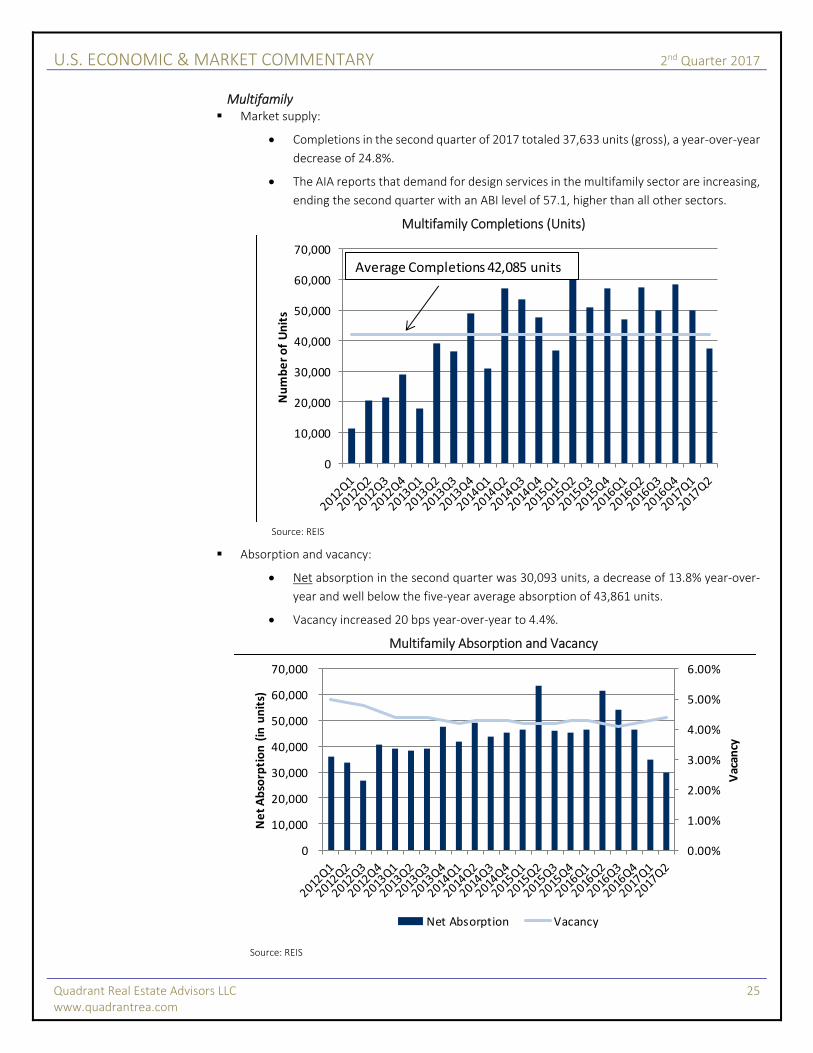

Multifamily Market supply:

Completions in the second quarter of 2017 totaled 37,633 units (gross), a year‐over‐year

decrease of 24.8%.

The AIA reports that demand for design services in the multifamily sector are increasing,

ending the second quarter with an ABI level of 57.1, higher than all other sectors.

Multifamily Completions (Units)

Source: REIS

Absorption and vacancy:

Net absorption in the second quarter was 30,093 units, a decrease of 13.8% year‐over‐

year and well below the five‐year average absorption of 43,861 units.

Vacancy increased 20 bps year‐over‐year to 4.4%.

Multifamily Absorption and Vacancy

Source: REIS

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Number of Units

Average Completions 42,085 units

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Vacan

cy

Net Absorption (in units)

Net Absorption Vacancy

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 26 www.quadrantrea.com

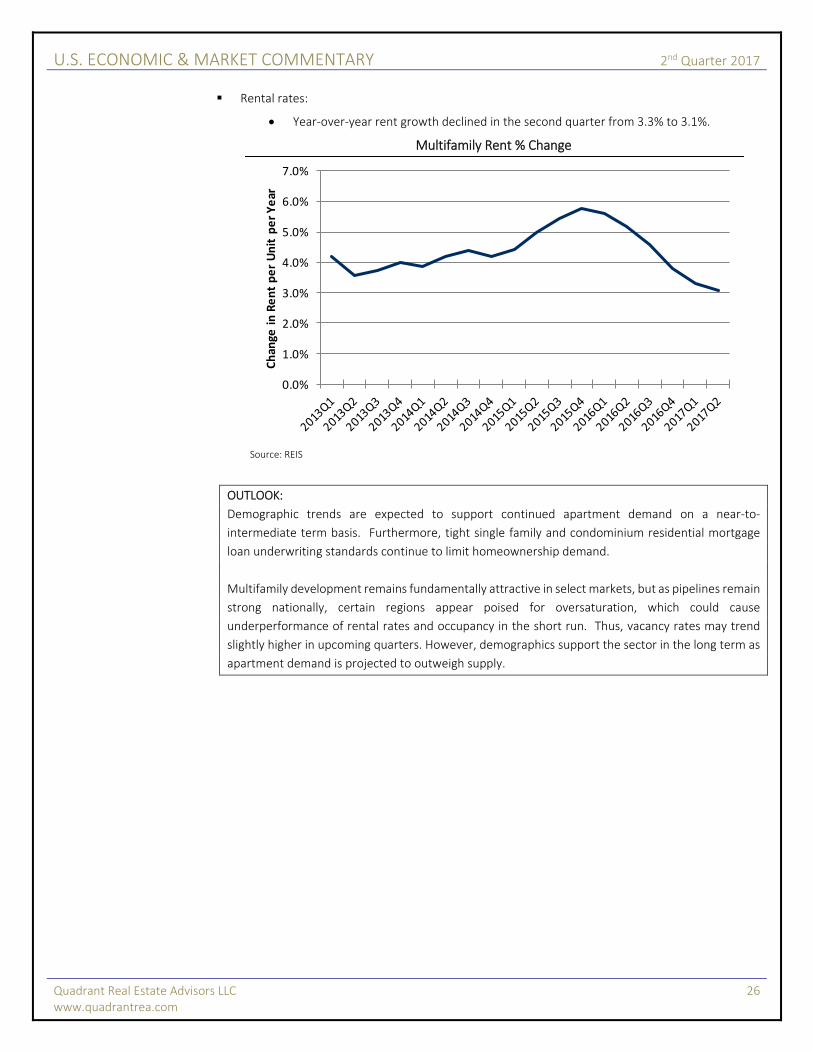

Rental rates:

Year‐over‐year rent growth declined in the second quarter from 3.3% to 3.1%.

Multifamily Rent % Change

Source: REIS

OUTLOOK:

Demographic trends are expected to support continued apartment demand on a near‐to‐

intermediate term basis. Furthermore, tight single family and condominium residential mortgage

loan underwriting standards continue to limit homeownership demand.

Multifamily development remains fundamentally attractive in select markets, but as pipelines remain

strong nationally, certain regions appear poised for oversaturation, which could cause

underperformance of rental rates and occupancy in the short run. Thus, vacancy rates may trend

slightly higher in upcoming quarters. However, demographics support the sector in the long term as

apartment demand is projected to outweigh supply.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Chan

ge in Rent per Unit per Year

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 27 www.quadrantrea.com

Hotels Market demand:

Lodging demand remains robust.

According to STR the U.S. hotel industry’s occupancy in the second quarter increased

0.7% to 73.4%.

Market supply:

According to the June 2017 STR Pipeline Report, the total active hotel development

pipeline (by number of rooms) was up 11.6% year‐over‐year.

The In‐Construction metric was up 12.4% year‐over‐year.

The total active pipeline included projects in the In‐Construction, Final Planning, and

Planning stages, but it did not include projects in the Pre‐Planning stage.

Key metrics:

According to STR, RevPAR increased 2.8% to $94.73.

Similarly, ADR increased 2.1% to $129.12.

OUTLOOK:

Economic improvement and upward trending consumer sentiment are expected to support further

RevPAR, ADR, and occupancy improvement in the near‐term. However, RevPAR and ADR growth

may slow and fall negative as new supply comes on line. Given the hotel sector’s particularly high

correlation to the broad economic environment and business/consumer sentiment, downside risk is

primarily tied to the risk of slowing GDP growth and/or geopolitical threats that could affect both

business and leisure travel.

U.S. ECONOMIC & MARKET COMMENTARY 2nd Quarter 2017

Quadrant Real Estate Advisors LLC 28 www.quadrantrea.com

Contacts

United States:

Thomas Mattinson

Executive Vice President

+1 (1) 770 752 6714

U.K. & Europe:

Linda Nel

Senior Vice President

+1 (1) 770 752 6726

Important Disclosures

This report is for informational purposes only and does not constitute, form, nor should be construed

as an offer to sell or a solicitation of an offer to buy investments or any fund and does not constitute

any commitment or recommendation on the part of Quadrant Real Estate Advisors. An investment

offering will be made only through a confidential private offering memorandum subject at all time to

revision and completion.

The information contained herein is derived from various sources which Quadrant believes but does

not guarantee to be accurate as of the date hereof. Neither Quadrant nor any of its affiliates nor any

other person makes any representation or warranty, express or implied, as to the accuracy or

completeness of the information contained in this newsletter and nothing contained herein shall be

relied upon or construed as a promise or reorientation of past or future performance.