q1 financial presentation 2018 dof asa asa/ir/2018/dof_q1_2018.pdf · plsv. 8 years petrobras ;...

TRANSCRIPT

Q1 Financial Presentation 2018

DOF ASA

2DOF ASA – Q1 presentation 2018

Highlights Group

DOF ASA – Q1 presentation 2018 3

Average utilisation Group fleet 72% in Q1 Improved markets and signs of higher activity in certain regions Several contract awards during March and April Repair issue of NOK 202 million completed in February

All numbers based on management reporting

EBITDA Q1 MNOK 520 (excl hedge accounting)

Highlights

DOF ASA – Q1 presentation 2018

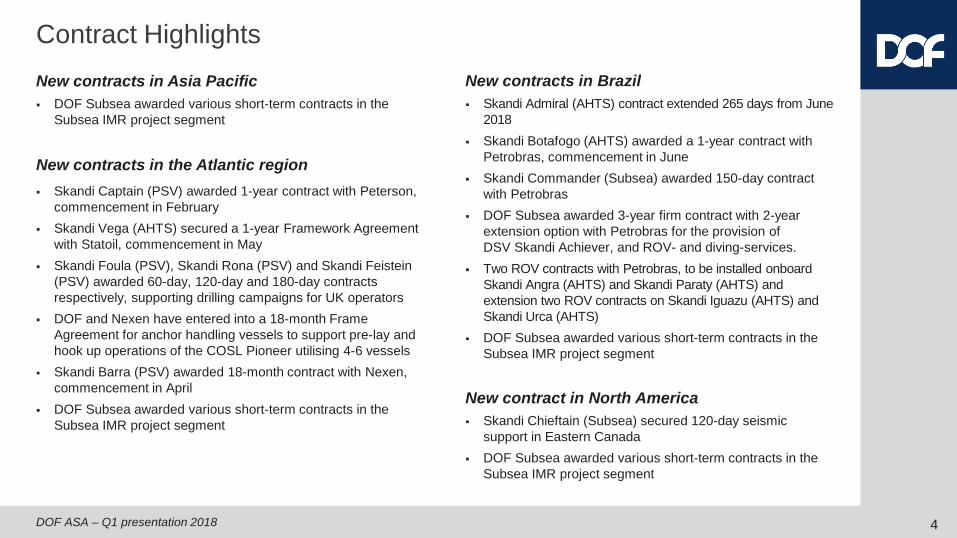

Contract Highlights

4

New contracts in Asia Pacific DOF Subsea awarded various short-term contracts in the

Subsea IMR project segment

New contracts in the Atlantic region Skandi Captain (PSV) awarded 1-year contract with Peterson,

commencement in February Skandi Vega (AHTS) secured a 1-year Framework Agreement

with Statoil, commencement in May Skandi Foula (PSV), Skandi Rona (PSV) and Skandi Feistein

(PSV) awarded 60-day, 120-day and 180-day contracts respectively, supporting drilling campaigns for UK operators

DOF and Nexen have entered into a 18-month Frame Agreement for anchor handling vessels to support pre-lay and hook up operations of the COSL Pioneer utilising 4-6 vessels

Skandi Barra (PSV) awarded 18-month contract with Nexen, commencement in April

DOF Subsea awarded various short-term contracts in the Subsea IMR project segment

New contracts in Brazil Skandi Admiral (AHTS) contract extended 265 days from June

2018 Skandi Botafogo (AHTS) awarded a 1-year contract with

Petrobras, commencement in June Skandi Commander (Subsea) awarded 150-day contract

with Petrobras DOF Subsea awarded 3-year firm contract with 2-year

extension option with Petrobras for the provision of DSV Skandi Achiever, and ROV- and diving-services.

Two ROV contracts with Petrobras, to be installed onboard Skandi Angra (AHTS) and Skandi Paraty (AHTS) and extension two ROV contracts on Skandi Iguazu (AHTS) and Skandi Urca (AHTS)

DOF Subsea awarded various short-term contracts in the Subsea IMR project segment

New contract in North America Skandi Chieftain (Subsea) secured 120-day seismic

support in Eastern Canada DOF Subsea awarded various short-term contracts in the

Subsea IMR project segment

DOF ASA – Q1 presentation 2018 5

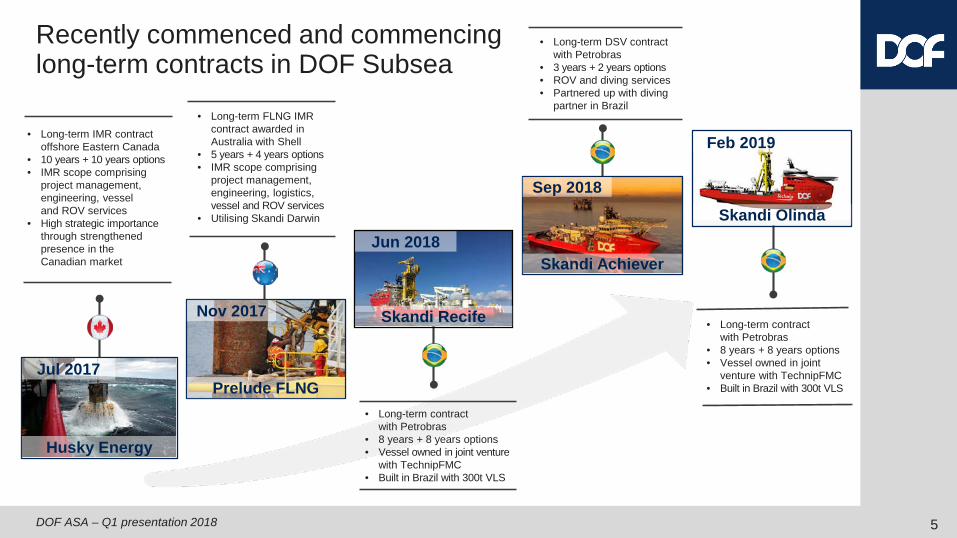

• Long-term FLNG IMR contract awarded in Australia with Shell

• 5 years + 4 years options• IMR scope comprising

project management, engineering, logistics, vessel and ROV services

• Utilising Skandi Darwin

Prelude FLNG

Nov 2017

• Long-term contract with Petrobras

• 8 years + 8 years options• Vessel owned in joint venture

with TechnipFMC• Built in Brazil with 300t VLS

• Long-term DSV contract with Petrobras

• 3 years + 2 years options• ROV and diving services• Partnered up with diving

partner in Brazil

Skandi Recife

Jun 2018Skandi Achiever

Sep 2018

• Long-term contract with Petrobras

• 8 years + 8 years options• Vessel owned in joint

venture with TechnipFMC• Built in Brazil with 300t VLS

Skandi Olinda

Feb 2019• Long-term IMR contract offshore Eastern Canada

• 10 years + 10 years options• IMR scope comprising

project management, engineering, vessel and ROV services

• High strategic importance through strengthened presence in the Canadian market

Husky Energy

Jul 2017

Recently commenced and commencing long-term contracts in DOF Subsea

DOF ASA – Q1 presentation 2018 6

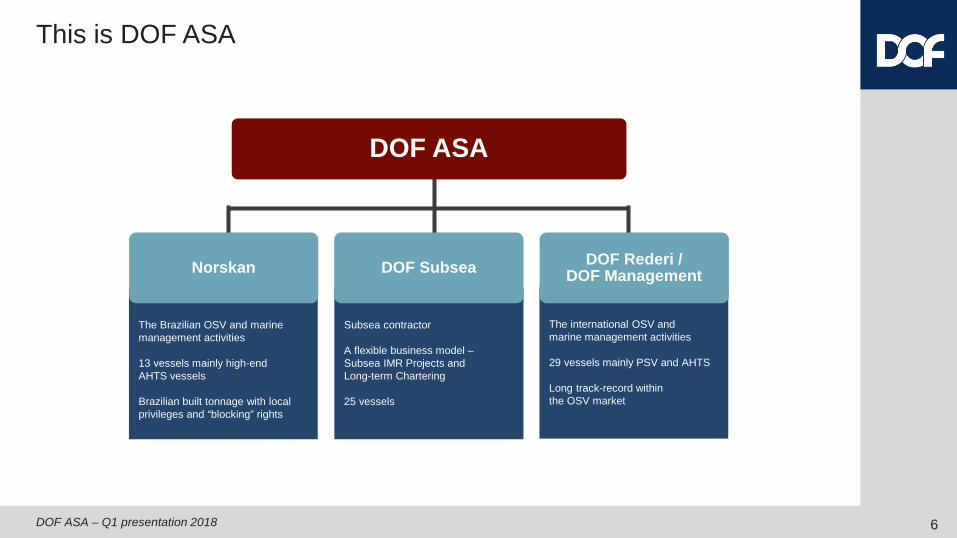

The international OSV and marine management activities

29 vessels mainly PSV and AHTS

Long track-record within the OSV market

Subsea contractor

A flexible business model –Subsea IMR Projects and Long-term Chartering

25 vessels

The Brazilian OSV and marine management activities

13 vessels mainly high-end AHTS vessels

Brazilian built tonnage with local privileges and “blocking” rights

DOF ASA

DOF SubseaNorskan DOF Rederi / DOF Management

This is DOF ASA

DOF ASA – Q1 presentation 2018

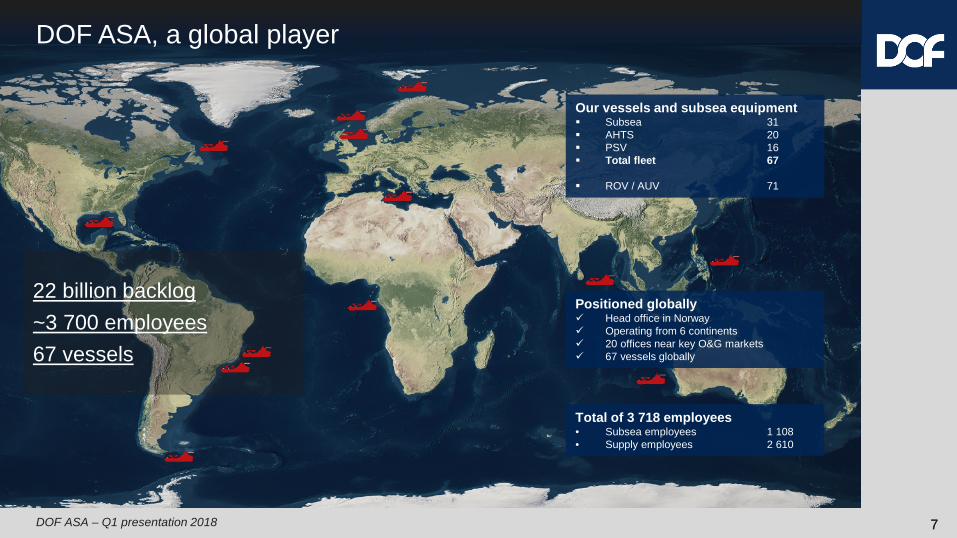

Total of 3 718 employees• Subsea employees 1 108• Supply employees 2 610

Positioned globally Head office in Norway Operating from 6 continents 20 offices near key O&G markets 67 vessels globally

Our vessels and subsea equipment Subsea 31 AHTS 20 PSV 16 Total fleet 67

ROV / AUV 71

DOF ASA, a global player

22 billion backlog~3 700 employees67 vessels

77

DOF ASA – Q1 presentation 2018

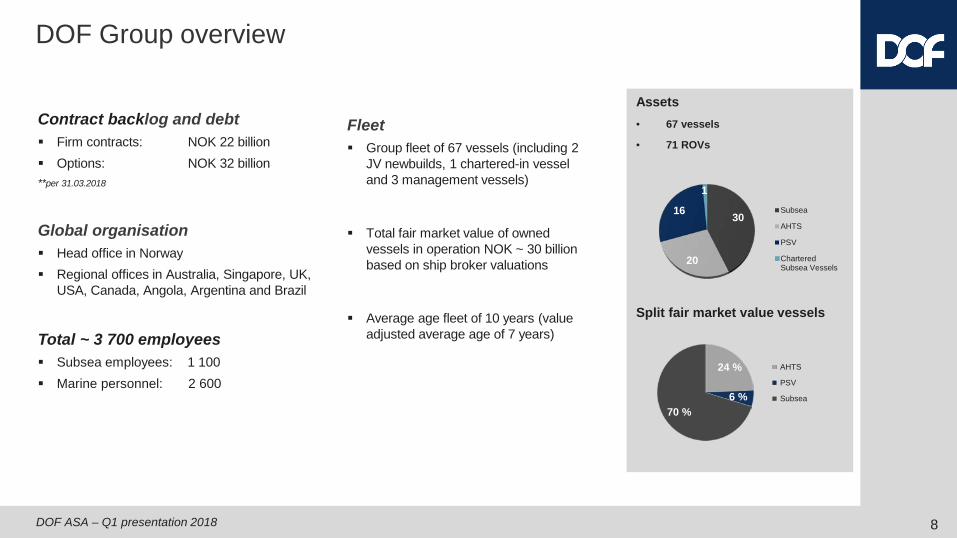

Assets• 67 vessels

• 71 ROVs

Split fair market value vessels

DOF Group overview

Fleet Group fleet of 67 vessels (including 2

JV newbuilds, 1 chartered-in vessel and 3 management vessels)

Total fair market value of owned vessels in operation NOK ~ 30 billion based on ship broker valuations

Average age fleet of 10 years (value adjusted average age of 7 years)

Contract backlog and debt Firm contracts: NOK 22 billion Options: NOK 32 billion**per 31.03.2018

Global organisation Head office in Norway Regional offices in Australia, Singapore, UK,

USA, Canada, Angola, Argentina and Brazil

Total ~ 3 700 employees Subsea employees: 1 100 Marine personnel: 2 600

30

20

16

1

Subsea

AHTS

PSV

CharteredSubsea Vessels

8

24 %

6 %70 %

AHTS

PSV

Subsea

DOF ASA – Q1 presentation 2018 9

A value-driven organisation

Safe the RITE way enhances our behaviour-based programme, integrating three main elements: “Values”, “Safe Behaviours” and “Rules, processes and procedures”.

A code to work by, globally

DOF has in 2017 released a refreshed Code of Business conduct. Everywhere the DOF Group does business we act responsibly and ethically. See our new Code of business conduct on our website: www.dof.com/TheCode

Sustainable operations

DOF released its annual stand-alone Sustainability report according to the GRI guideline. The DOF Sustainability Report for 2017 is available at: www.dof.com/Sustainability

DOF ASA – Q1 presentation 2018

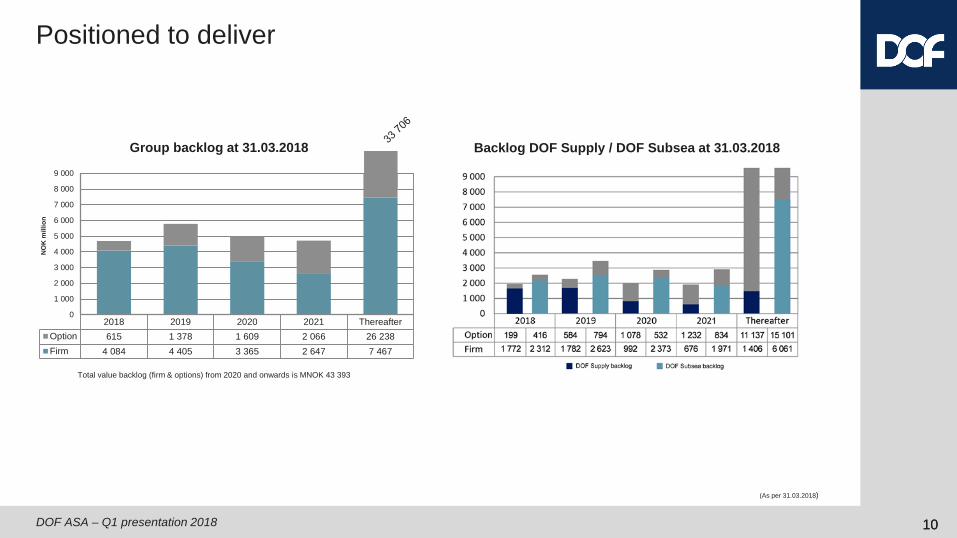

Positioned to deliver

Total value backlog (firm & options) from 2020 and onwards is MNOK 43 393

1010

(As per 31.03.2018)

Group backlog at 31.03.2018 Backlog DOF Supply / DOF Subsea at 31.03.2018

2018 2019 2020 2021 ThereafterOption 615 1 378 1 609 2 066 26 238Firm 4 084 4 405 3 365 2 647 7 467

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

NO

K m

illio

n

DOF ASA – Q1 presentation 2018

Vessel Yard Delivery Type Contract Financing

Skandi Recife Vard Brazil Q2 2018 PLSV 8 years Petrobras Loan agreement signed with BNDES

Skandi Olinda Vard Brazil Q1 2019 PLSV 8 years Petrobras Loan agreement signed with BNDES

Two newbuildings remaining with 8-year contracts

Co-owned 50/50 with TechnipFMC

11

12DOF ASA – Q1 presentation 2018

FinancialsManagement Reporting

DOF ASA – Q1 presentation 2018 13

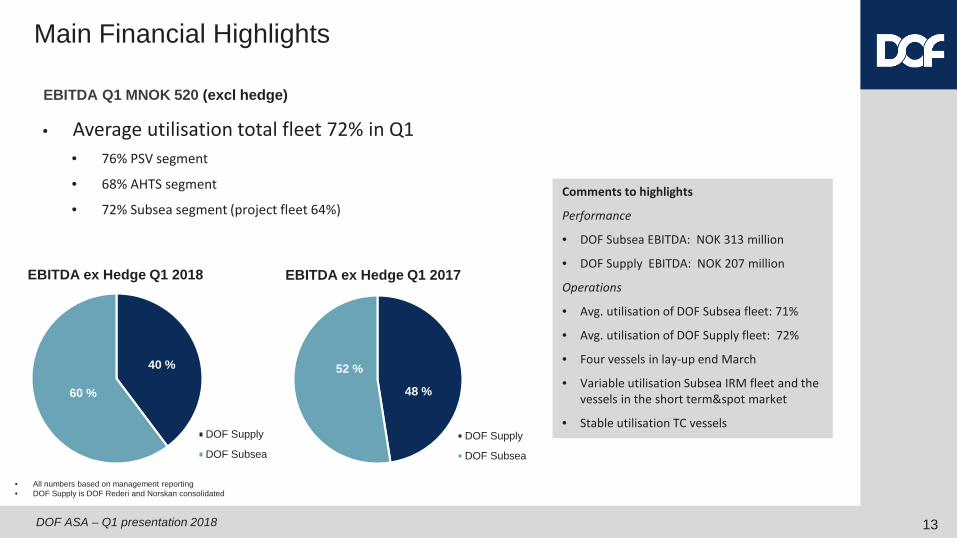

• Average utilisation total fleet 72% in Q1• 76% PSV segment

• 68% AHTS segment

• 72% Subsea segment (project fleet 64%)

• All numbers based on management reporting• DOF Supply is DOF Rederi and Norskan consolidated

EBITDA Q1 MNOK 520 (excl hedge)

Main Financial Highlights

Comments to highlights

Performance

• DOF Subsea EBITDA: NOK 313 million

• DOF Supply EBITDA: NOK 207 million

Operations

• Avg. utilisation of DOF Subsea fleet: 71%

• Avg. utilisation of DOF Supply fleet: 72%

• Four vessels in lay-up end March

• Variable utilisation Subsea IRM fleet and thevessels in the short term&spot market

• Stable utilisation TC vessels

40 %

60 %

EBITDA ex Hedge Q1 2018

DOF Supply

DOF Subsea

48 %

52 %

EBITDA ex Hedge Q1 2017

DOF Supply

DOF Subsea

DOF ASA – Q1 presentation 2018

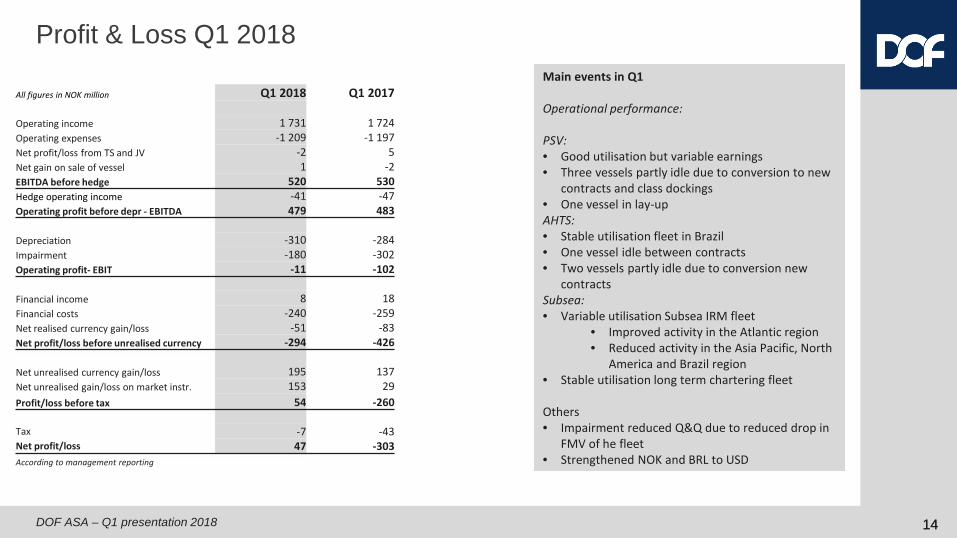

Profit & Loss Q1 2018Main events in Q1

Operational performance:

PSV:• Good utilisation but variable earnings• Three vessels partly idle due to conversion to new

contracts and class dockings• One vessel in lay-upAHTS:• Stable utilisation fleet in Brazil • One vessel idle between contracts• Two vessels partly idle due to conversion new

contractsSubsea:• Variable utilisation Subsea IRM fleet

• Improved activity in the Atlantic region• Reduced activity in the Asia Pacific, North

America and Brazil region• Stable utilisation long term chartering fleet

Others• Impairment reduced Q&Q due to reduced drop in

FMV of he fleet• Strengthened NOK and BRL to USD

1414

All figures in NOK million Q1 2018 Q1 2017

Operating income 1 731 1 724 Operating expenses -1 209 -1 197 Net profit/loss from TS and JV -2 5 Net gain on sale of vessel 1 -2 EBITDA before hedge 520 530 Hedge operating income -41 -47 Operating profit before depr - EBITDA 479 483

Depreciation -310 -284 Impairment -180 -302 Operating profit- EBIT -11 -102

Financial income 8 18 Financial costs -240 -259 Net realised currency gain/loss -51 -83 Net profit/loss before unrealised currency -294 -426

Net unrealised currency gain/loss 195 137 Net unrealised gain/loss on market instr. 153 29 Profit/loss before tax 54 -260

Tax -7 -43 Net profit/loss 47 -303 According to management reporting

DOF ASA – Q1 presentation 2018

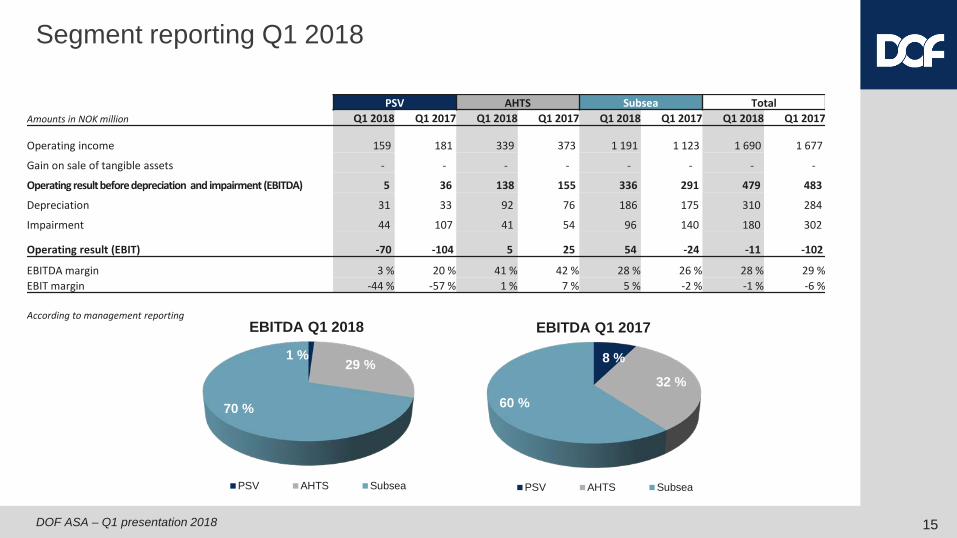

Segment reporting Q1 2018

PSV AHTS Subsea TotalAmounts in NOK million Q1 2018 Q1 2017 Q1 2018 Q1 2017 Q1 2018 Q1 2017 Q1 2018 Q1 2017

Operating income 159 181 339 373 1 191 1 123 1 690 1 677

Gain on sale of tangible assets - - - - - - - -

Operating result before depreciation and impairment (EBITDA) 5 36 138 155 336 291 479 483

Depreciation 31 33 92 76 186 175 310 284

Impairment 44 107 41 54 96 140 180 302

Operating result (EBIT) -70 -104 5 25 54 -24 -11 -102

EBITDA margin 3 % 20 % 41 % 42 % 28 % 26 % 28 % 29 %EBIT margin -44 % -57 % 1 % 7 % 5 % -2 % -1 % -6 %

According to management reporting

15

1 %29 %

70 %

EBITDA Q1 2018

PSV AHTS Subsea

8 %

32 %60 %

EBITDA Q1 2017

PSV AHTS Subsea

DOF ASA – Q1 presentation 2018

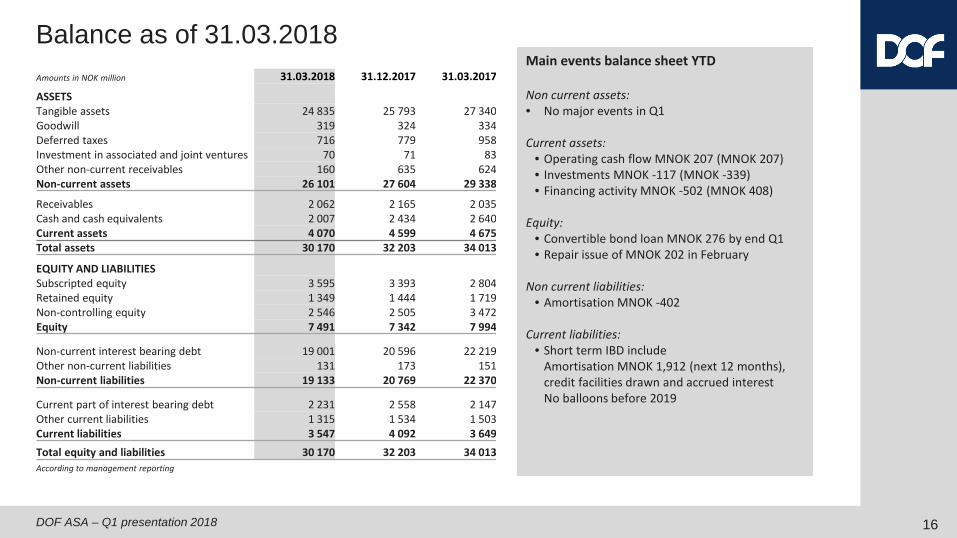

Balance as of 31.03.2018Main events balance sheet YTD

Non current assets:• No major events in Q1

Current assets:• Operating cash flow MNOK 207 (MNOK 207)• Investments MNOK -117 (MNOK -339)• Financing activity MNOK -502 (MNOK 408)

Equity:• Convertible bond loan MNOK 276 by end Q1• Repair issue of MNOK 202 in February

Non current liabilities:• Amortisation MNOK -402

Current liabilities:• Short term IBD include

Amortisation MNOK 1,912 (next 12 months), credit facilities drawn and accrued interestNo balloons before 2019

16

Amounts in NOK million 31.03.2018 31.12.2017 31.03.2017

ASSETSTangible assets 24 835 25 793 27 340Goodwill 319 324 334Deferred taxes 716 779 958Investment in associated and joint ventures 70 71 83Other non-current receivables 160 635 624Non-current assets 26 101 27 604 29 338

Receivables 2 062 2 165 2 035Cash and cash equivalents 2 007 2 434 2 640Current assets 4 070 4 599 4 675Total assets 30 170 32 203 34 013

EQUITY AND LIABILITIESSubscripted equity 3 595 3 393 2 804Retained equity 1 349 1 444 1 719Non-controlling equity 2 546 2 505 3 472Equity 7 491 7 342 7 994

Non-current interest bearing debt 19 001 20 596 22 219Other non-current liabilities 131 173 151Non-current liabilities 19 133 20 769 22 370

Current part of interest bearing debt 2 231 2 558 2 147Other current liabilities 1 315 1 534 1 503Current liabilities 3 547 4 092 3 649Total equity and liabilities 30 170 32 203 34 013According to management reporting

DOF ASA – Q1 presentation 2018 17

• All numbers based on management reporting• DOF Supply is DOF Rederi and Norskan consolidated

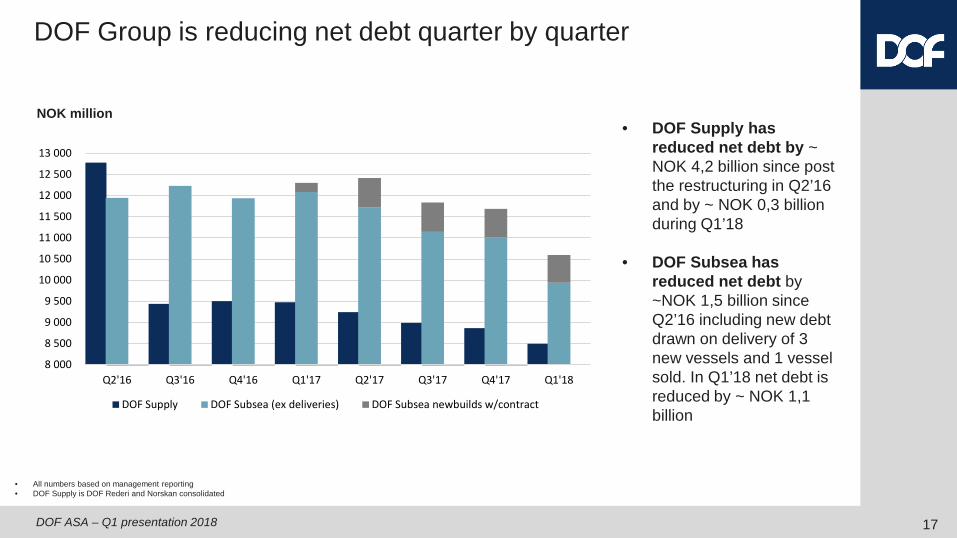

DOF Group is reducing net debt quarter by quarter

NOK million• DOF Supply has

reduced net debt by ~ NOK 4,2 billion since post the restructuring in Q2’16 and by ~ NOK 0,3 billion during Q1’18

• DOF Subsea has reduced net debt by ~NOK 1,5 billion sinceQ2’16 including new debtdrawn on delivery of 3 new vessels and 1 vesselsold. In Q1’18 net debt is reduced by ~ NOK 1,1 billion

8 000

8 500

9 000

9 500

10 000

10 500

11 000

11 500

12 000

12 500

13 000

Q2'16 Q3'16 Q4'16 Q1'17 Q2'17 Q3'17 Q4'17 Q1'18

DOF Supply DOF Subsea (ex deliveries) DOF Subsea newbuilds w/contract

DOF ASA – Q1 presentation 2018

No change in guidance for 2018 (MNOK 2 400 – MNOK 2 800)

Ebitda Q2 expected to be slightly better than Q1

Skandi Recife expected to be on-hire in June

Increased tendering activity

Mixed activity in the regions

Outlook

18

Thank youPresented by Mons Aase - CEOHilde Drønen - CFO

DOF ASA – Q1 presentation 2018

DISCLAIMER

This presentation by DOF ASA designed to provide a high level overview of aspects of the operations of the DOF ASA Group.The material set out in the presentation is current as at 9 May 2018.This presentation contains forward-looking statements relating to operations of the DOF ASA Group that are based on management’s owncurrent expectations, estimates and projections about matters relevant to DOF ASA‘s future financial performance. Words such as “likely”,“aims”, “looking forward”, “potential”, “anticipates”, “expects”, “predicts”, “plans”, “targets”, “believes” and “estimates” and similarexpressions are intended to identify forward-looking statements.References in the presentation to assumptions, estimates and outcomes and forward-looking statements about assumptions, estimatesand outcomes, which are based on internal business data and external sources, are uncertain given the nature of the industry, businessrisks, and other factors. Also, they may be affected by internal and external factors that may have a material effect on future businessperformance and results.No assurance or guarantee is, or should be taken to be, given in relation to the future business performance or results of the DOF ASAGroup or the likelihood that the assumptions, estimates or outcomes will be achieved.While management has taken every effort to ensure the accuracy of the material in the presentation, the presentation is provided forinformation only. DOF ASA , its officers and management exclude and disclaim any liability in respect of anything done in reliance on thepresentation.All forward-looking statements made in this presentation are based on information presently available to management and DOF ASAassumes no obligation to update any forward looking- statements. Nothing in this presentation constitutes investment advice and thispresentation shall not constitute an offer to sell or the solicitation of any offer to buy any securities or otherwise engage in any investmentactivity.You should make your own enquiries and take your own advice (including financial and legal advice) before making an investment in thecompany's shares or in making a decision to hold or sell your shares.

20