putting the new standard in accounting for advertising costs into context

TRANSCRIPT

Putting the New Standard in Accounting for Advertising Costs into Context

Paul Munter

Paul Muntet, Ph.D., CPA, is the KPMG Peat Marwick Professor of Accounting and chairman of the Depcutment of Accounting at the University of Miami in Coral Cables, Florida. He is editor-in-chiefof The Journal of Corporate Accounting and Finance.

n Statement on Auditing Standards (SAS) No. 69, ‘The Meaning of ‘Present Fairly in Conformity with Generally Accepted I Accounting Principles’ in the Independent Auditor’s Report,” the

Auditing Standards Board established a clear hierarchy as to the applicability of accounting standards. In the GAA hierarchy established by SAS No. 69, statements of position (SOPS) and guides issued by the American Institute of CPAs (AICPA) were designated as authoritative standards if cleared by the Financial Accounting Standards Board (FASB)-as Level 2 documen*and should be considered to be GAA to the extent that these documents address transactions that would materially affect an entity’s financial statements. [For a thorough discussion of the implications of SAS No. 69, see Munter and Ratcliffe, Applying GAAP and GAAS (Mathew Bender, Inc.), Chapter 30.1 As such, it is vitally important that practitioners keep abreast ofAcSEC‘s activities.

ANEW STANDARD Accounting for advertising costs has long been a topic ignored by

the accounting standards setters. That has changed as AcSEC has moved to establish standards for companies who incur advertising costs. The conclusions of AcSEC were distributed for public comment in a proposed SOP entit1ed“Reportingon AdvertisingCosts.”Recently, the FASB voted to clear the SOP for final issuance. As such, it will become the authoritative standard for accounting for advertising costs for periods beginning after June 15, 1994.

While the standards of this SOP are, of themselves, important additions to the financial reporting literature, perhaps just as important is the plan by AcSEC to use this SOP as a model for other projects. Indeed, AcSEC has indicated that this SOP is just the first step in a multistep project by AcSEC to examine the accounting and reporting of other costs for which little definitive guidance exists- such as internally developed intangible assets like preopening and

Journal of Corporate Accounting and FinanceBpring 1994 353

Paul Munter

startup costs. The fundamental question addressed in this project is whether future economic benefits that meet the definition of an asset arise from such costs.

DEFINITION OF AN ASSET: FASB’S CONCEPTUAL FRAMEWORI(

In addressing the fhdamental issue associated with the accounting for advertising costs, AcSEC examined the FASB’s definition of an asset found in Statement of Financial Accounting Concepts (SFAC) No. 6, “Elements of Financial Statements.” In SFAC No. 6, the FASB defines an asset as

probable future economic benefits obtained or controlled by a particular entity as a result of past transactions or events. .. .AcSEC’s

consideration of whether advertising

capitalized and amortized can be compared to the FASB’s own deliberations. ..

COStS S h o u l d be In many ways, AcSEC’s consideration of whether advertising

costs should be capitalized and amortized can be compared to the FASB’s own deliberations on the accounting for research and development (R&D) costs. In FAS No. 2, “Accounting for Research and Development Costs,” the FASB concluded that all R&D costs should be charged to expense as incurred. The FASB based its conclusions on the following factors:

1. Uncertainty ofFuture Benefits. With R&D costs there is a high degree of uncertainty as to whether future benefits will be derived from individual R&D projects.

2. Lack of Causal Relationship between Expenditures and Benefits. A direct relationship between R&D costs and specific future revenue generally cannot be demonstrated. Thus, even if there were not uncertainties about the future benefits, it would be difficult to establish a defensible amortization approach.

3. Accounting Recognition of Economic Resources. Accounting Principles Board (APB) Statement No. 4, “Basic Concepts and Accounting Principles Underlying Financial Statements of Business Enterprises,” defines economic resources as the scarce means for carrying on economic activities. Based on this, the FASB argued that the economic resources of a particular enterprise are generally regarded as those scarce resources for which there is an expectation of future benefits to the enterprise either through use or sale. However, the criterion of measurability would require thet a resource not be recognized as an asset unless, at the time it is acquired or developed, its future economic benefits can be identified and objectively measured.

4. Expense Recognition and Matching. Therecognition ofexpenses is categorized in APB Statement No. 4 as being based on one of the following three principles: (a) associating cause and effect, (b) systematic and rational allocation, or (c) immediate recognition. As is noted in point 2 above, the FASB concluded that neither cause and effect nor a systematic and rational allocation basis could be

354 Journal of Corporate Accounting and FinanceBpring 1994

f i t t ing the New Sta&rd in Accounting for Advertising Costs into Context

established. Thus, the remaining choice for expense recognition would be to immediately expense the costs as incurred.

5. Usefulness of Resulting Information. Since no demonstrable pattern of investment recovery has been demonstrated, the FASB concluded that it is unlikely that the ability of financial statement readers to predict the return on an investment and the variability of that return would be aided by capitalizing and amortizingR8zD costs.

AcSEC'S CONCLUSIONS ON ACCOUNTING FOR ADVERTISING COSTS

Because AcSEC adopted what amounts to an R&D model in deliberating the issue of accounting for advertising cost, it is not surprising that it concluded that advertising costs, except for those resulting from certain direct-response advertising, do not meet the recognition and measurement criteria specified by the FASB in SFAC No. 5, "Recognition and Measurement in Financial Statements of Business Enterprises," and, thus, advertising costs should be expensed as incurred. In essence, AcSEC concluded the future economic benefits of most advertising costs cannot be measured with the degree of certainty required to reflect an asset in the financial statements.

As a practical illustration that remarkably parallels the FASBs investigation of R&D costs, the Wall Street Journal has noted that sales gains reported by Super Bowl advertisers during the six-week period following the January 1991 and 1992 games varied widely. Furthermore, the advertisers admitted the difficulty of attributing sales gains directly to these advertising efforts.

Thus, the SOP would require that all advertisingcosts be expensed in the period incurred or the first time that the advertising takes place (that is, the cost of purchasing advertising space in either the print, radio, or television media would be deferred until the advertisement first appears), unless it is direct-response advertising that results in measurable probable future economic benefits. Future benefits are deemed probable if future revenues in excess of the costs incurred to generate those revenues can be clearly identified and anticipated.

Examples of costs that might qualify for capitalization are direct- response advertising such as catalogs and brochures which will be distributed in the future. To demonstrate that direct-response advertising will generate future benefits, the entity must have "persuasive" evidence that this direct-response advertisement will match the performance of similar past direct-response advertising which did, indeed, result in future benefits. Importantly, the SOP indicates that industry statistics used in lieu of the entity's own historical evidence are not considered objective evidence in support of the contention that direct-response advertising will result in future benefits.

In making a determination that the revenues will exceed the costs for direct-response advertising, the entity must consider the costs associated with all prospective customers, not just the costs associated with the customers that are expected to respond to the advertising.

*'.AcSEc concLwled the fiturn economic benefits of most advertising costs cannot be measured with the degree of certainty requi red...

Journal of Corporate Accounting and Finance/Spring 1994 355

Paul Munter

Thus, when determining that the costs of printinga catalog should be capitalized because of probable future benefits, the entity should consider the costs of printing all the catalogs compared to anticipated future catalog sales revenue, not just the costs of printing the catalogs for those expected to respond. This is an important distinction since, in general, the expected response rate for direct-mail advertising is quite low.

Finally, even if it is appropriate to capitalize certain costs associated with direct-response advertising, the SOP specifies that only incremental direct costs of the direct-response advertising are to be capitalized. Thus, the entity may not allocate indirect costs to the direct-mail advertising capitalization amount.

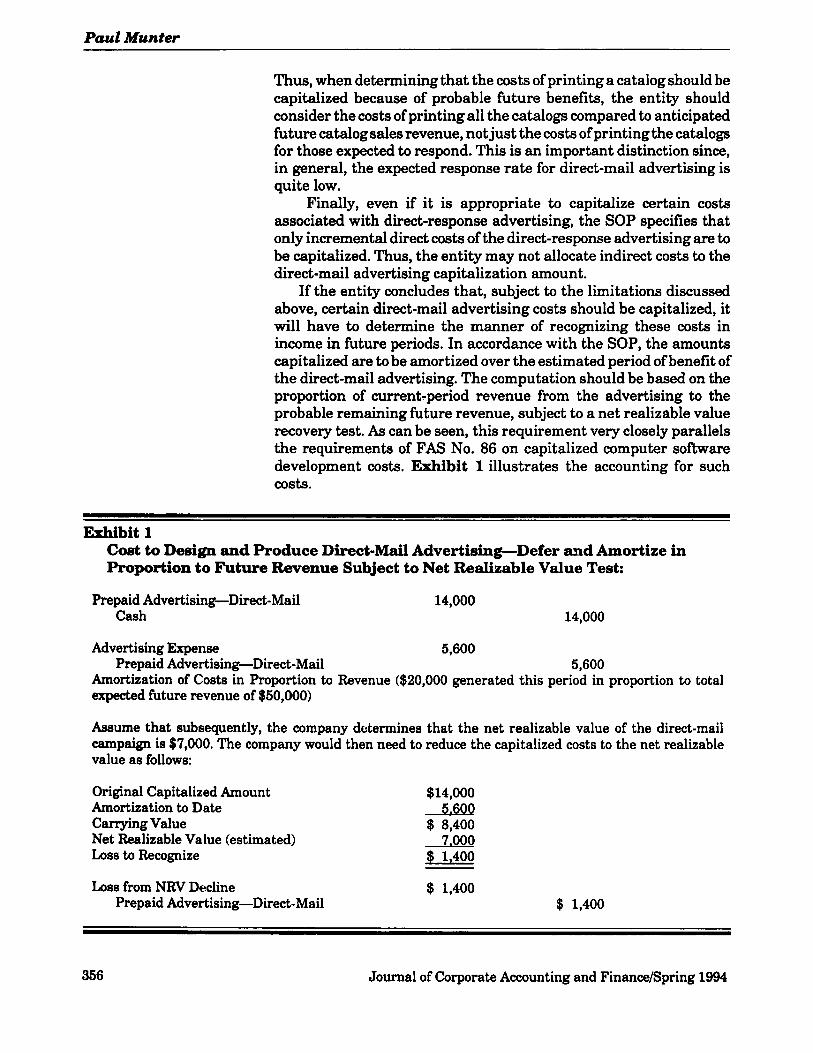

If the entity concludes that, subject to the limitations discussed above, certain direct-mail advertising costs should be capitalized, it will have to determine the manner of recognizing these costs in income in future periods. In accordance with the SOP, the amounts capitalized are to be amortized over the estimated period of benefit of the direct-mail advertising. The computation should be based on the proportion of current-period revenue from the advertising to the probable remaining future revenue, subject to a net realizable value recovery test. As can be seen, this requirement very closely parallels the requirements of FAS No. 86 on capitalized computer software development costs. Exhibit 1 illustrates the accounting for such costs.

~~ _ _ _ _ _ ~

Exhibit 1 Cost to Design and Produce Direct-Mail Advertising-Defer and Amortize in Proportion to Future Revenue Subject to Net Realizable Value Test:

Prepaid Advertising-Direct-Mail Cash

14,000 14,000

Advertising Expense 5,600

Amortization of Costs in Proportion to Revenue ($20,000 generated this period in proportion to total expected future revenue of $50,000)

Prepaid Advertising-Direct-Mail 5,600

Assume that subsequently, the company determines that the net realizable value of the direct-mail campaign is $7,000. The company would then need to reduce the capitalized costs to the net realizable value as follows:

Original Capitalized Amount Amortization to Date Carrying Value Net Realizable Value (estimated) Loss to Recognize

$14,000 5.600 $ 8,400

7.000 $ 1,400

Loss from NRV Decline $ 1,400 Prepaid Advertising-Direct-Mail $ 1,400

356 Journal of Corporate Accounting and Finance/Spring 1994

Putting the New Standard in Accounting for Advertising Costs into Contert

... it is quite common for entities to mpr t prepaid advertising costs on the balance Sheets.

CONCLUSION As was noted earlier, this SOP will become effective for fiscal

periods beginning after June 15,1994. Obviously, for many companies that currently take an aggressive posture on the capitalization of advertising costs, there will be significant adjustments needed to their accounting practices to comply with these provisions. In fact, an examination of many recent financial reports reveals that it is quite common for entities to report prepaid advertisingcosts on the balance sheets. Also, for many of these companies, the amounts represent between 3 and 8 percent of reported total assets.

Furthermore, while there was some criticism of AcSEC for these conclusions, it can be argued that these conclusions are entirely consistent with the FASBs conclusions on R&D and software development costs.

One final note also deserves mention here. AcSEC indicated a t the outset of this proposal that this was just the beginning of its efforts to examine costs which are deferred on company balance sheets such as start-up costs and the like. To the extent that AcSEC continues on its efforts to examine the accounting for such costs, it appears quite likely that it will conclude that it is appropriate to expense most of those costs as well. As such, practitioners should continue to monitor AcSEC's efforts in this area as it deliberates related matters. +

Journal of Corporate Accounting and FinanceBpring 1994 357