published by the magazine driven by & for … · the magazine driven by & for the...

TRANSCRIPT

PULSE FAST COMPANY

HOT SPOTS

FRESH FACES

A political debate: Outsourcing professionals weigh in p14-15

Discover why Mother Africa is one Hot Mama p26-27

Real Time with CBRE’s Bill Concannon p42-47

ISSUE 02 | NovEmbEr / dEcEmbEr 2012 ThE MagazinE DrivEn by & for ThE oUTSoUrcing ProfESSionaLpUblIShEd by www.IAop.orG

forEcaSTS& TrEnDS What new directions are we heading in? Pulse delivers the wake up call.

PLUS Practical Advice: Three Knowledge Center stories to learn from p30-37

© Ca

n Stoc

k Pho

to Inc

.

2 PULSE November/December 2012

PULSE ISSUE 02 | NovEmbEr/dEcEmbEr 2012

f o r e ca s t s & t r e n d s e d i t i o n

FAST COMPANYPulse is taking it to the polls:

Who really wins?p14-15

A wake up call: winds of change are coming!

p16-25

FORECASTCorporate Real Estate CEO

Bill Concannon Keeps it Real p42-47

FRESH FACES

f u rt h e r r e a d i n g

Latin America Summit Wrap-Up .............................................................. p10-11

Outsourcing in its New Avatar .................................................................. p12-13

Hot Spot: Africa .......................................................................................... p26-27

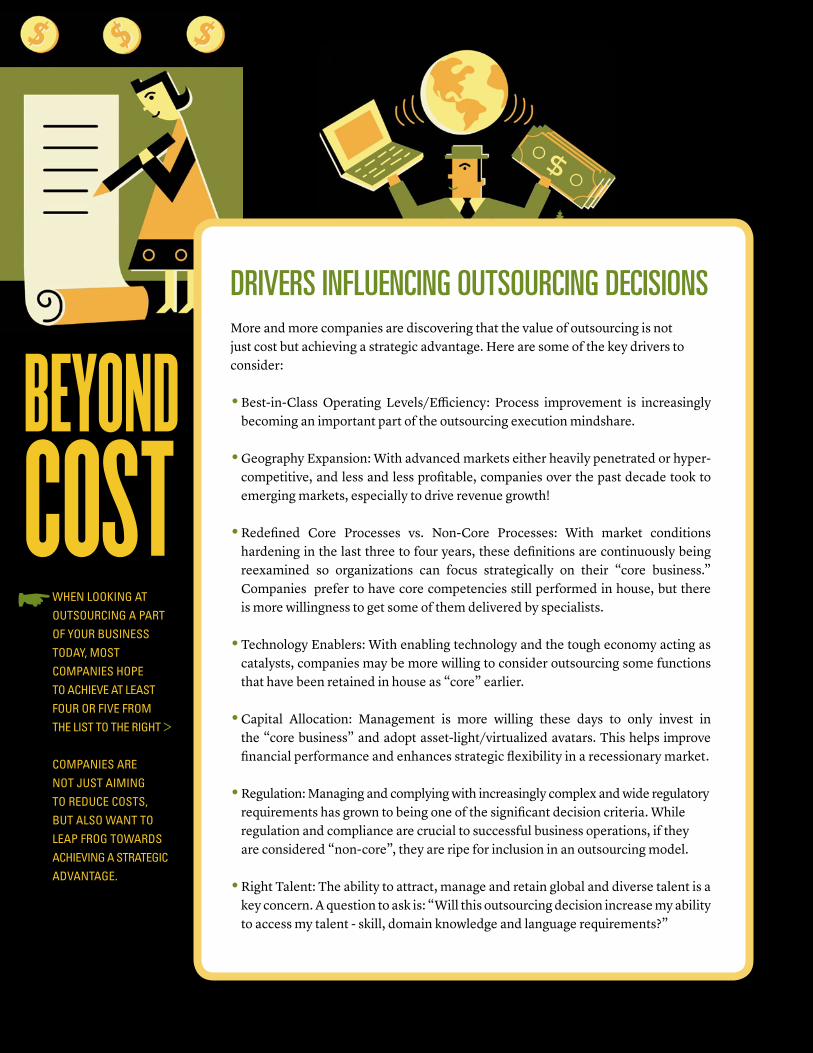

Beyond Cost ............................................................................................... p38-41

ThE MagazinE DrivEn by & for ThE oUTSoUrcing ProfESSionaL

PULSE POLL

t r e n d s & f o r e ca s t e d i t i o n

r e g u l a r f e at u r e s

Letter from the CEO ................................................ p5

Pulse Contributors ................................................... p6

Taking the Pulse ....................................................... p7

The Beat: News & Commentary .............................. p8

The Sandbox ........................................................... p28

Joining IAOP: New Members & Benefits ......... p48-49

Pulse Roundup ................................................. p50-51

Pulse Professional ............................................. p52-55

Pulse Flash .............................................................. p61

For The 2013 Outsourcing World SummitPhoenix, Arizona Feb. 18-20, 2013

p50

WARMING UP

KNOWLEdGE CENTER TRIFECTAAvoiding IT Service Contract Pitfalls ...... p30-31

Proactive Remedies ................................. p32-35

Human Side to Outsourcing ....................... p36-37

© Can Stock Photo Inc. / dndavis

PULSE November/December 2012 5

WELCOME TO THE FORECASTS& TRENdS ISSUE OF PULSE! As I write this message, the seasons are changing in my part of the world. With the U.S. presidential election ahead and ongoing global economic woes, we’re seeing varying opinions here at IAOP about what the winds of change will bring in the coming year. While we don’t yet know who will be elected and exactly what that will mean to the industry, I can say with certainty that outsourcing is here to stay and that’s a good thing - for jobs, taxes, the global economy and society at large. We’ll be joining with the National Outsourcing Association (NOA) in spreading the word on a global basis that “Outsourcing Works” and collaborate to change our profession’s sometimes negative image. You’ll see a focus on this at The 2013 Outsourcing World Summit. More information will be coming about this and I encourage you all to get involved as it will make a difference. As CEO of this association, I see examples every day of the good that outsourcing brings. In our “View from the C-Suite” story, you’ll hear more about the CSR practices of CB Richard Ellis (CBRE) from CEO of Global Corporate Services William

Concannon. Bill has been recognized for his contributions to outsourcing and society at large as a member of our Outsourcing Hall of Fame, and CBRE is the winner of the inaugural Global Outsourcing Social Responsibility Impact Award (GOSRIA). There’s plenty that can be learned from these positive examples. I witnessed the good works of outsourcing being spread in Latin America at our recent Latin America Outsourcing Summit in Brazil with professionals from many different countries coming together to see how they can collaborate across borders. If you missed it, you can check out some of the photos in our Pulse Flash. Outsourcing also is positive for emerg-ing destinations. In our Hot Spot on Africa, you’ll read about how many countries are poised for future growth from outsourcing. There’s no doubt outsourcing is good for professionals and their careers. We see the value IAOP’s corporate and profes-sional development programs bring every day. Companies are spending wisely and want to invest in the best individuals. The credentials that come with being a Certified Outsourcing Professional (COP) enable professionals and their

organizations to show their worth, especially when economies are tight. Outsourcing flourishes by sharing best practices and thinking. In our Best of Knowledge Center, you’ll find stories based on presentations from some of our global chapters. Our chapter network continues to grow and we’ll soon by launching a new Guidance Counsel of chapter chairs to help set standards and serve as a resource for new and existing chapters to continue to raise the bar on our collective thought leadership. Our forecast and trends story is always one to follow, and we’re proud of our track record of predicting what will be important. Thanks to our many members and thought leaders for gazing into the crystal ball for us and sharing their outlooks for 2013, views on politics and more. My prediction is that 2013 will be another good one for outsourcing, IAOP and PULSE because of you!

DEBI HAMILLCeo IAoP

will political elections take outsourcing in a new direction?

if so, where are we heading?

CEO’S DESK

we are delighted that cops will be facilitating our new Advanced Track at The 2013 outsourcing world Summit in phoenix, Arizona, Feb. 18-20. read our pulse professional section for the latest on the cop program and see pulse round-up for new additions at the Summit.

PULSE CONT

RIBUT

ORSn ov e m b e r / d e c e m b e r 2 0 1 2 i s s u e : 0 2

PUBLISHER

IAopdebi hamill, CEO EDITOR-IN-CHIEF

Sandy [email protected]

MANAGING EDITORJag dalal, [email protected]

PULSE BLOG EDITORKate [email protected]

MANAGING DIRECTORKim [email protected]

CREATIVE DIRECTORpamela Zarrella

EDITORIAL BOARDmichael F. corbett, Chairman, IAOPmatthew p. Shocklee, COP, Managing Director & Global Ambassador, IAOP John hindle, Outsourcing Marketing, AccentureNeil hirshman, COP, Partner, Kirkland & EllisEugene Kublanov, COP, Managing Director, KPMGpradip Khemani, Director, Blue Shield of Californiacara Koppenhoefer, Manager, Humana

ADVERTISING renee [email protected]+1.845.452.0600 ext.109

CONTRIBUTIONSPULSE welcomes contributors! Please email: [email protected]

IAop2600 South Rd. Suite 44-240Poughkeepsie, NY 12601+1.845.452.0600

This publication (and any part thereof) may not be reproduced, transmitted or stored in any print or electronic format (including but not limited to any online service, any database or any part of the internet) or in any other format in any media whatsoever, without the prior written per-mission of the publisher. IAOP accepts no liability for the accuracy of the contents or any opinions expressed herein.

lUcy hErlAAr Trainer of people and pets. A consultant, trainer and coach

on the human side of outsourcing, she lives in belgium where she

also trains dogs.

TUE GoldSchmIEdING An attorney at Gorrissen Federspiel law firm in denmark

specializing in Ip and technology. As a new father, he can be found up late at night reading contracts or changing diapers.

olE horSFEldT A partner and vice president of Ip & technology at Gorrissen Federspiel, who participates in triathlons,

and marathons when he isn’t working on complex IT contracts in outsourcing.

NIlANJAN chAUdhUrI An engineer who heads global marketing for Aditya birla Group, he appreciates the role his

generation plays in creating today’s tech-nology and enjoys reading and writing.

KUlwINdEr SINGh Speaker and writer on market messaging and

branding. A member of the advisory board of cmo council India,

he enjoys football and badminton.

JørN w. rASmUSSEN brings real-life experience to writing outsourcing

contracts. when he’s not busy influencing the danish outsourcing industry,

he enjoys collecting different artifacts.

PULSE November/December 2012 7

“Today’s shared services skill sets are becoming more about the future of management and a career path that is about being able to create and sustain organizations and third parties in a cohesive manner ... This leadership isn’t just in accounting or paperwork, for example, but for leaders in a new management category that some have termed the Chief Integration Office.” – guest bloggers on “Buddy Can You Spare some Talent” Rick Bertheaud and Bryan Furlong of KPMG

f e e d bac k a n d c o m m e n ta ry f ro m t h e p u l s e c o m m u n i t y

taKing thE

pulSE

We welcome guest bloggers. Join the dialogue at iaoppulseblog.blogspot.com[

pUTTING INTEGrATIoN INTo ThE c-SUITE

In their blog, “Buddy Can You Spare some Talent”, on Sept. 13, guest bloggers Rick Bertheaud and Bryan Furlong of KPMG, coin CIO as “Chief Integration Office.” They write: “Today’s shared services skill sets are becoming more about the future of management and a career path that is about being able to create and sustain organizations and third parties in a cohesive manner. It’s about building a global brand with extended global business services. What you learn managing all the pieces and parts of a shared service center for accounting, is readily applicable to managing a service center for pharmacovigilance or R & D. This leadership isn’t just in accounting or paperwork, for example, but for leaders in a new management category that some have termed the Chief Integration Office.”

KEEp ThE NAmE

Responding to a blog “Change the Rhetoric or Change Our Name,” our readers say educating the public on “outsourcing” versus “offshoring” is needed – but some things don’t change easily. “I’ve seen many debates lately about dropping the term “outsourcing.” While the word still has a negative connotation, I don’t necessarily agree with dropping it

and replacing it with words like ‘sourcing,’ ‘managed services,’ and ‘right sourcing.’ You’ve made an excellent point that outsourcing isn’t always offshoring. But to those not in the business I feel they will never understand or agree. I’ve been doing this for close to 20 years and it hasn’t changed,” writes James Westwood.

Thanks readers!Thanks to denis perron of montreal, canada and all the others on the positive feedback to our launch issue. we love hearing from you and getting your inputs on pUlSE magazine and blog.

please keep the comments coming.

LETTERS TO THE EDITOR

Send Pulse letters to [email protected].

comING NExT ISSUE IN pUlSE: Preview to The 2013 Outsourcing World Summit with a special print edition distributed at the Phoenix, Arizona Show. Plus, a look at highlights of the Certified Outsourcing Professional (COP) program, Europe as our Hot Spot and ITO is featured in the Verticals section. Don’t miss it! To contribute to these stories, contact: [email protected]

Denis writes:

dEAr pUlSE TEAm,

What a professional magazine! It gives us a quick review of what is going on in outsourcing. It assembles multitude of emails and info. This is an excellent initiative. I will make sure to read this magazine when published.

SNEAK prEvIEw

The Pulse blog offered an inside look at “The Moral Case on Outsourcing: How Good, Bad, or Ugly is it for America and the World?” by Scott Phillips. “Outsourcing is widely reviled as a cause of job loss. But by allowing companies to preserve businesses that would otherwise fail—to reduce costs and remain viable in the face of competitive threats—it also results in companies surviving and, therefore, jobs being saved,” he writes.

Be a guest blogger. Shout it out at: http://iaoppulseblog.blogspot.com/

8 PULSE November/December 2012

IAOP’s Director of Thought Leadership Jagdish Dalal closely followed the headlines relating to outsourcing and the U.S. elections. During the campaign, some positions and opinions expressed by candidates were based on few facts and realities, he says, examining two stories on different sides of the issues.

© Ca

n Stoc

k Pho

to Inc

. / na

sir11

64©

Can S

tock P

hoto

Inc. /

wac

ker

ThE NEwS hEAdlINES ThE IAop dISh

or lIFTING US Up?

A careful reading of the article points out that globalization and capital maximization are directly related. According to the author, shipping jobs overseas promotes globalization and acts to lift the economics of “third world” countries and at the same time, free up human capital in advanced countries for other work. The article also challenges the thinking that the local economy suffers as a result of such offshoring action and, therefore, is not a solid platform to criticize Mitt Romney and Bain Capital for shipping jobs overseas.

IS GlobAlIZATIoN brINGING US dowN?

JULY 10, 2012 THE ECONOMIST: TAKE THIS JOB AND SHIP IT

This story deals with the topic of outsourcing and its impact on “globalization,” examining quotes from Nobel Prize winning economist

Paul Krugman. “First, I think the process of globalization, which has moved billions of people out of dire poverty, is worth defending loudly and proudly,” the author writes.

loNGEr TErm vISIoN NEEdEd

The story correctly points out that the globalization is not necessarily a primary cause for unemployment and that the impact on workers from the inevitable globalization must be dealt with as a separate issue rather than attacking globaliza-tion. It points out that the impact of globalization is felt less in some of the European countries because of their national human protection net of health care and welfare support. A higher level of support in educating displaced workers in competing globally is another way to benefit from globalization. The steel industry is a good example of how U.S. companies have battled and come back from the dead by leveraging and learning from globalization, Dalal says.

ShorT SIGhTEd polITIcAl plAy

JULY 10, 2012 NEW YORK TIMES: THE FOLLY OF ATTACKING OUTSOURCING

The story looks at the net impact of globalization – more convenience, cheaper goods and greater efficiency - and tackles the issue of the impact on

workers – especially in the U.S. “Hewing to the standard anti-outsourcing playbook may gain a few votes in November. But American workers need more. They need a set of policies that gives them a stake in the fruits of the more prosperous global economy that globalization can bring,” the author says.

The Beat / NEWS & COMMENTARY AS COvERED BY JAg DALAL

THE 2013 OUTSOURCING WORLD SUMMIT

JW Marriott Phoenix Desert Ridge | Phoenix, ArizonaFebruary 18-20, 2013

Produced in association with FORTUNE® Custom Content

Build on the Past. Manage the Present. Step into the Future.Gain insights from more than 100 inspiring speakers and network with over 800 industry professionals at IAOP’s annual event, The 2013 Outsourcing World Summit and take your outsourcing relationships from good to great.

Register now at www.IAOP.org/OWS2013 for EARLY BIRD SAVINGS!

C

M

Y

CM

MY

CY

CMY

K

OWS13 Ad_PULSE.pdf 10/17/2012 9:22:52 AM

© Can Stock Photo Inc. / dndavis

10 PULSE November/December 2012

they came from peru, chile, argentina, costa rica, colombia, guatemala, mexico, france, nicaragua and the u.s. to learn and network with industry leaders and fellow outsourcing professionals, and went away with new know-how, connections, ideas and inspiration.

brazil hosted the hottest ticket in town: the 2012 latin america outsourcing summit

© Ca

n Stoc

k Pho

to Inc

. / sp

arkstu

dio

PULSE November/December 2012 11

The 2nd Annual Latin America Outsourcing Summit did not disappoint with top-notch speakers, educational breakout sessions, thought-provoking panel discussions, award recognitions and networking (see our Pulse Flash for some of the social side).

The two-day info-packed conference covered innovation outsourcing in Latin America, reducing the impact of manpower shortage in IT, outsourcing best practices by MultiLatinas at mitigating risk, maximizing sourcing value through supply intelligence and outsourcing trends in Latin America.

IAOP thanks the speakers; partners Brasscom and Fortune; as well as sponsors Accenture, ANDI, Baker & McKenzie, BRQ, Grupo Assa, Infosys, KellyOCG, Softtek, Toutatis and Wipro.

plANNING AlrEAdy IS UNdErwAy For ThE NExT

lATAm SUmmIT. wANT To hoST IT IN yoUr coUNTry?

drop US A NoTE ANd lET US KNow!

“I encourage you to see outsourcing not only from an export standpoint from Brazil but also as a domestic market opportunity. Just as outsourcing improves the operations of businesses globally, it can improve the operations of business domestically. Building the domestic base will help service providers in Brazil be more competitive.”

– Michael Corbett, Chairman of IAOP

razil hosted the hottest ticket in town: the 2012 latin america outsourcing summit

Marco Stefanini, COP, CEO and President of Stefanini, was honored with the Hall of Fame award at a delicioso luncheon attended by over 100 people.

© Ca

n Stoc

k Pho

to Inc

. / sp

arkstu

dio

b y: k u lw i n d e r s i n g h

Political Turns & New Challenges are Coming With the outsourcing industry registering robust performance year after year, will it continue to flourish in view of the profound changes in the business & political ecosystem it operates in?

12 PULSE November/December 2012

© Ca

n Stoc

k Pho

to Inc

. / pa

trimo

nio

outsourcing in its new avatarThe outsourcing industry will likely emerge as a force to reckon with since all state-level political decisions in their true sense are based on their financial viability and it is unlikely that any government will establish an agenda that jeopardizes economic interests.

Global businesses view outsourcing as part of their overall business strategy and measures to curb this trend can drasti-cally affect bottom lines. For global businesses, the need to achieve core competencies, reduce and eliminate costs and achieve economies of scale will continue to drive the growth of the outsourcing industry.

Certainly, there will be new challenges. For example, the recent trend of near-shoring will put pressure on Asian leaders to develop new business/engagement models. Several global businesses in the U.S. have already started allocating work to nearshore locations such as Mexico and Guatemala and others may follow suit.

To overcome this challenge, global IT and ITeS (Information Technology Enabled Services) firms can set up their branches in these locations and utilize their experience and expertise to deliver better results than local operators.

Another option is to move up the value-chain by supporting and enabling business transactions and specializing in other areas of non-core business operations. Providers can focus on knowledge intense work of large banks, pharmaceutical companies and consultancies, since some irreplaceable advantages exist in this context, such as ready availability of doctors, lawyers, chartered accountants, designers, etc. For IT firms, the shift to a product-based business model will enable improved outcomes.

Another important aspect that needs to be considered in the near term is to distribute revenue sources geographically to counter the possibility of economic downturn in a specific area. The old adage of “not placing all your eggs in the same basket” will become increasingly relevant in the next decade.

Currently, a major percentage of IT/ITeS firms depend on U.S. based firms for contracts, something that needs to be changed by increasing focus on other geographies such as European countries and Asian economic powerhouses like Japan and China. Already, some firms have started using China as a resource base and a delivery location to service their clients in U.S. and Europe, and some others have formed joint ventures.

On a broader scale, the concept of preferred outsourc-ing destination will cease to exist with use of automated

systems and technology advancements. New entrants and established players will have to strive just as hard to get new contracts. Also, soft skills will become just as important as technical skills, as global businesses start to allocate more of their mission-critical businesses and processes to offshore destinations.

More research and development projects will be given out, something that will begin replacing the conventional “work-as-

per-instructions” model. Corrections in pay-packages are also imminent; executives in the new ecosystem will have more or less the same salaries, irrespective of their geographical location.

For outsourcing firms, the message is clearly to adapt to evolving market conditions. As Charles Darwin rightly said, “It is not the strongest of the species that survives, nor the most intelligent that survives. It is the one that is the most adaptable to change.”

It simply means that to move to the next level, outsourcing firms will have to be smart and agile, and read the market right, as the global outsourcing industry transitions to the next era.

Kulwinder Singh As Director of Global Marketing and Communication, Kulwinder is responsible for Synechron’s corporate brand and integrated marketing efforts worldwide. Prior to joining Synechron in June 2012, he served as Business Head at Scribble Media and Entertainment Pvt Limited.b y: k u lw i n d e r s i n g h

FAST COMPANY

As Charles Darwin rightly said,“It is not the strongest of the species that survives, nor the most intelligent that survives. It is the one that is the most adaptable to change.”

PULSE November/December 2012 13

Here is a sampling of the many responses, with mixed opinions, from outsourcing professionals around the world:

Before the U.S. Presidential election results were known, PULSE asked: How will political changes affect the global outsourcing industry in 2013?

“Political uncertainty will have little impact on outsourcing activities. This is regardless of who wins the U.S. presidential race as well as other congressional seats. Continuing economic challenges in the U.S. will be more of a guiding factor than changes in laws and regulations.”

Jag Dalal CoP, IAoP Managing Director Thought Leadership

“Given the anticipated slowdown in the global economy, due to the Euro crisis, and the much debated outcome of the next presidential election in the United States, outsourcing will gain strength as a business model, since scrutiny on operational costs will be paramount. Some locations like India or China could be disadvantaged, based on the policy decisions of the next U.S. President towards outsourcing. In general, the outsourcing industry is only looking to gain more attention in 2013.”

Kumanan Murughan, CoP, HP

“I do not believe the election will have an impact. The global economy has become its own engine, feeding the movement of goods and services and delivery of those across borders without much regard for the political elections. Barring significant security, tax or protectionist regulatory changes, companies will make these decisions independent of politicians. Instead, they will make them based on the needs of their customers, the ability to deliver profitability and the best interest of their shareholders.”

Marilyn Jentzen Vice President, Operations Center Strategy, Global Growth & Operations, Thomson ReutersGrowth & Operations, Growth & Operations,

14 PULSE November/December 2012

Before the U.S. Presidential election results were known, PULSE asked: How will political changes affect the global outsourcing industry in 2013?

“politics is such a mess,

it’s anyone guess on the

impact.” - Tom Sultenfuss

President, ContactWorks, Texas

“Since there is still the cause - the fall of aggregate effective consumer demand - the global economic crisis in the near future will continue. We can make wild guesses as to why and when its next aggravation might happen, be it in spring or fall. The election of the President of the United States, for instance, is a huge supplement to this issue, as well as other variables that affect the course of crisis development.”

Alexey Perekatov Vice-President, Corporate Marketing, Miratech, Ukraine

“Politics will certainly play an impor-tant role with regards to government to citizen contracts both in the realm of outsourcing and offshoring. As far as the non-government contracts are concerned - until and unless there are punitive sanctions in terms of tax benefits and grants not being available to the companies offshoring their work - it will not impact the spirit and magnitude of offshoring.”

Rajesh Dhuddu CoP, Vice President, Market Development, Quatrro Global Services Private Limited

“The political debate and economic situation has put the outsourcing industry in the spotlight. In 2013 we have to better explain the role of the economics of the outsourcing industry, its role in creating jobs and global business opportunities for companies. At the same time, new technologies like cloud computing and mobile technology will change the nature of outsourcing engage-ments. Outsourcing will happen at new, sometimes unexpected places.”

Cheri MangumHead of Marketing, Freeborders, Inc.

Cheri MangumHead of Marketing, Freeborders, Inc.

FAST COMPANY???

PULSE November/December 2012 15

© Ca

n Stoc

k Pho

to Inc

. / m

ichak

lootw

ijk

16 PULSE November/December 2012

© Ca

n Stoc

k Pho

to Inc

. / se

razetd

inov

PULSE November/December 2012 17

TrEnDS &forEcaSTSmadame frinton tells all

2013: A World of Change for Outsourcing

As the world turns, global economic, political and social forces will impact outsourcing in the coming year. Our annual trends report – publishedbefore the results of the U.S. presidential election were known – show the uncertain climate will lead to more caution but also potentially closer and more creative relationships and opportunities. The clouds will lift in some areas

our future gazers predict ...

b y: s a n dy f r i n to n

18 PULSE November/December 2012

GlObAl ClImATe “The long-drawn out industry woes thanks to belt-tightening in Europe, elections in the U.S., and a general lackluster growth in developing nations (India and China in particu-lar), supported by downgrading of sovereign debt ratings by S&P, Moody’s and Fitch has put a dampener on aggressive pursuits relating to global sourcing,” says Bobby Varanasi, COP, COP-GOV, COOPM, who is chairman and CEO of Matryzel Consulting, Inc.

With the current economic situation, Roy Wang, hiSoft, U.S. RDS-PDS Senior Project Manager, says he doesn’t see the global outsourcing market improving until about the second half of 2013.

Reflecting on 2012, Alexey Perekatov, Vice-President, Corporate Marketing, Miratech, Ukraine, notes that very weak economies in Europe combined with slow growth in the U.S. and in such emerging nations as China, India and Brazil dampened the prospects of outsourcing industry growth for the near term.

“The biggest advances in developing nations are yet to come,” he says. “One outsourcing trend that has continued to be strong is to foster outsourcing to bring the economy into a healthy state.”

“Fully developed nations have been shifting to knowledge-based economies for decades,” he notes. “The challenge for developed nations such as the U.S. and Japan is to maintain their leads in such areas as intellectual property, investment in R&D and higher education, while displacing factory workers and shifting (outsourcing) much of manufacturing overseas. This means that mature economies will see more advanced and optimized outsourcing services, whereas emerging ones will deploy outsourcing more broadly as a tactic to reduce operating costs and streamline business workflows.”

Overall, Matthew P. Shocklee, COP, Managing Director & Global Ambassador, IAOP, sees continued growth ahead in the industry with increased focus on global positioning of work and related services with a focus on the total value of the service with increasing emphasis on risk, compliance and security.

NeArShOre ForEcAST: poISEd For ExploSIoN Near shore destinations for the U.S. (such as Costa Rica, Panama, Honduras) will play a bigger role in offshoring decision-making, predicts IAOP’s Director of Thought Leadership, Jag Dalal.

Nearshore countries continue to offer strong prospects by providing the benefits of less travel time and expense, greater efficiencies due to time zone compatibility and the ability to harness closer cultural affinity, according to Julia Santos, Markets Executive Advisor, Ernst & Young.

Atul Vashistha, COP, Chairman & CEO of Neo Group, is calling that 2013 will be a “breakout year” for the Latin America domestic market trend, seeing this not just as a nearshore trend but the rise of regional demand.

Advisor Anupam Govil, Partner, Avasant and President, Avasense, says a “perfect convergence” of factors have come together to set the stage for the accelerated growth of outsourcing in the region, including continued above average GPD growth, rise of MultiLatinas, maturity of service providers, increased interest by U.S. buyers in nearshoring and the region being well suited to handle

hErE’S how oUTSoUrcING IS ExpEcTEd To plAy oUT For dIFFErENT pArTS oF ThE world, AccordING To prEdIcTIoNS GAThErEd by pUlSE From INdUSTry ThoUGhT lEAdErS:

“If (CSr) is not at the forefront of every out-sourced engagement, the company has failed the consumer.” – Julia Santos COP, Markets Executive Advisor, Ernst & Young

t r e n d s & f o r e ca s t s

PULSE November/December 2012 19

growing technology trends of cloud computing, mobility, social, big data and security.

Colombia-based Carvajal IT & Services expects a good year in 2013 with a strong brand in the region, government support for outsourcing and an ample talented labor pool, says Director Diego Ossa.

“In LATAM we are expecting a maintained slope towards higher incomes,” he says. “As service providers, innovating and improving our portfolios, any challenge in Europe or United States, even within LATAM, means opportunities we’re willing to catch.”

Camilo Pena Ramirez, CEO & Founder of Knowledge Process & Professionals in Chile expects Colombia, Chile and Brazil to be the growth areas, noting that government support is helping smaller, highly specialized companies enter the global service industry.

But our trend watchers also see some potential challenges ahead with availability of labor and tax barriers.

“Latin America will need to address its tax barriers to offshoring in order to leverage the outsourcing model to its full advantage,” Santos says. “Countries, like Brazil, will need to make their tax structure simple and beneficial to the investor. The red tape involved in offshoring to a particular country will discourage investment. As the Latin American region continues to grow, the income per person will grow and the purchasing power will be stronger than most emerging or under developed regions.”

OffShOreForEcAST: wEAKEr oUTlooKSlower revenue growth in India and China is predicted. Economic and political challenges in India will challenge Indian service providers and will continue to add margin pressures for their existing and new outsourcing activities, Dalal says.

Higher salaries and shorter work hours will reduce their advantage over other outsourcing destinations, including onshore activities.

Greater consolidation of China and India-based service providers and advisors also is predicted in the coming year by IAOP’s Shocklee.

The bright spots include: impact sourcing and CSr,

professional certifications, nearshore and onshore

destinations, technology solutions, and services that

control risk and protect data.

The bright spots include: impact sourcing and CSr,

professional certifications, nearshore and onshore

destinations, technology solutions, and services that

control risk and protect data.

t r e n d s & f o r e ca s t s

© Ca

n Stoc

k Pho

to Inc

. / se

razetd

inov

“businesses will consider outsourcing “locally” or even bringing some of the offshored work back on shore.”

- Jag Dalal, IAOP

onShorE: a PoSiTivE viSiont r e n d s & f o r e ca s t s

© Ca

n Stoc

k Pho

to Inc

. / se

razetd

inov

20 PULSE November/December 2012

PULSE November/December 2012 21

ONShOreForEcAST: poSITIvE vISIoN Economists are predicting continuing high unemploy-ment in the U.S. and some of the other leading industrial nations in Europe. This will lower wages for certain skills and will encourage more businesses to consider outsourcing “locally” or even bringing some of the offshored work back on shore, Dalal says.

Says Varanasi: “From a U.S. standpoint, jobs (and the threat of taxes) shall continue to demand cautious initiatives from companies, while domestic delivery will become more of a mainstream conversation going forward.”

Cliff Justice, principal and U.S. leader, KPMG Shared Services and Outsourcing Advisory, also sees growth ahead in onshore delivery models.

“Many of the global service providers are assessing opportunities to add capacity in the U.S. and Europe to address components of the services value chain that are unable to be delivered effectively offshore,” says Justice. “We expect to see more asset acquisitions of Western-based capacity that provides a platform for industry- specific or technology-specific capabilities in the domestic markets.”

Accenture’s Managing Director, Business Process Out-sourcing Sam Ciruolo also sees the current global crisis driving significant demand for outsourcing services in Europe and the Americas.

Outsourcing in U.S. state and local government will continue to accelerate given the continued sluggish economy and dwindling tax base, increasing demand for rural sourcing.

“Rural sourcing will benefit from this as states begin to focus on creating outsourcing ecosystems to more affordably support state infrastructures,” Shocklee says.

emerGING NATIONSForEcAST: locAl mArKET GrowTh “The benefits of outsourcing and the need for fueling domestic economies through instituting efficiencies and productivity goals into national agendas will further drive a more widespread adoption of outsourcing in local markets,” Varanasi says. “The tryst here would be the value articulation, which will not be around cost savings, but value arbitrage. Nations on a fast-track development model will be hard-pressed to adopt sourcing strategies to retain market competitiveness and economic resilience.”

“Nations on a fast-track development model will be hard-pressed to adopt sourcing strategies to retain market competitiveness and economic resilience.” – bobby varanasi COP, COP-GOV, COOPM, Chairman and CEO of Matryzel Consulting, Inc.

“rural sourcing will benefit as states begin to focus on creating outsourcing ecosystems to more affordably support state infrastructures.” – matthew p. Shocklee COP, Managing Director & Global Ambassador, IAOP

t r e n d s & f o r e ca s t s

22 PULSE November/December 2012

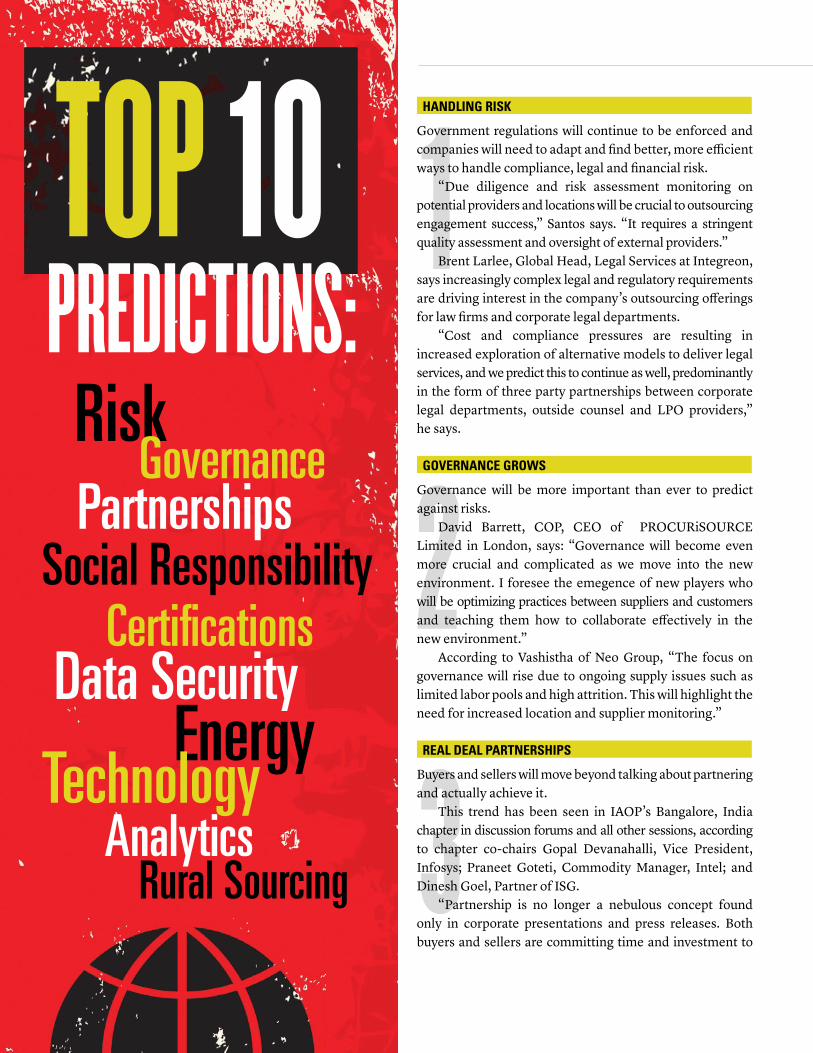

ToP 10PrEDicTionS: Risk governance Partnerships Social Responsibility Certifications Data Security EnergyTechnology Analytics Rural Sourcing

1

23

hANdlING rISK

Government regulations will continue to be enforced and companies will need to adapt and find better, more efficient ways to handle compliance, legal and financial risk. “Due diligence and risk assessment monitoring on potential providers and locations will be crucial to outsourcing engagement success,” Santos says. “It requires a stringent quality assessment and oversight of external providers.” Brent Larlee, Global Head, Legal Services at Integreon, says increasingly complex legal and regulatory requirements are driving interest in the company’s outsourcing offerings for law firms and corporate legal departments. “Cost and compliance pressures are resulting in increased exploration of alternative models to deliver legal services, and we predict this to continue as well, predominantly in the form of three party partnerships between corporate legal departments, outside counsel and LPO providers,” he says.

GovErNANcE GrowS

Governance will be more important than ever to predict against risks. David Barrett, COP, CEO of PROCURiSOURCE Limited in London, says: “Governance will become even more crucial and complicated as we move into the new environment. I foresee the emegence of new players who will be optimizing practices between suppliers and customers and teaching them how to collaborate effectively in the new environment.” According to Vashistha of Neo Group, “The focus on governance will rise due to ongoing supply issues such as limited labor pools and high attrition. This will highlight the need for increased location and supplier monitoring.”

rEAl dEAl pArTNErShIpS

Buyers and sellers will move beyond talking about partnering and actually achieve it. This trend has been seen in IAOP’s Bangalore, India chapter in discussion forums and all other sessions, according to chapter co-chairs Gopal Devanahalli, Vice President, Infosys; Praneet Goteti, Commodity Manager, Intel; and Dinesh Goel, Partner of ISG. “Partnership is no longer a nebulous concept found only in corporate presentations and press releases. Both buyers and sellers are committing time and investment to

t r e n d s & f o r e ca s t s

PULSE November/December 2012 23

456

78910

developing a mutually beneficial partnership with concrete outcomes, be it co-creation of value, transformation or innovation,” the chapter co-chairs said. Given the uncertain financial landscape, companies will seek creative ways to work with their providers, says Santos. “We will see more dramatic rationalization of preferred suppliers where companies send work to a few strategic providers and have more collaborative long-term relation-ships,” she says.

SocIAl rESpoNSIbIlITy & ImpAcTS

Corporate social responsibility – including fair wages and labor practices, environmental impact, local community support and sustainability - will move to the forefront of engagements between providers and customers. “Companies will be seeking to implement the same standards with external partners that they have with their employees and their home environments,” predicts Santos. “If this (CSR) is not at the forefront of every outsourced engagement, the company has failed the consumer.” Large and mid-sized companies will put a renewed emphasis on the social impacts of sourcing to spread their cost bases and also drive their economic agendas, says Varanasi.

proFESSIoNAl cErTIFIcATIoN ANd TAlENT

Having employees with the right credentials, expertise and talents will continue to be important in the coming year. Despite the economy, IAOP’s CEO Debi Hamill says the association has seen strong interest in its training and professional development programs and the number of Certified Outsourcing Professionals®(COPs) is only expected to continue to rise in the coming year. D. Zachary Misko, Vice President of Workforce Strategy, KellyOCG, says the new talent supply chain will require greater partnerships between recruitment process outsourcing (RPO) providers and their clients, predicting “one big pot of global hiring solutions” will emerge.

dATA SEcUrITy

Security of data as well as availability of systems and net-works will remain a major issue for customers and providers. “Cyber-attack threats, as predicted by the U.S. government agencies will become an issue for businesses to tackle - whether outsourced or not,” says Dalal, noting the serious “denial of service” attack on financial and energy ompanies globally in September and early October 2012.

TEchNoloGy

Trends in technology will drive outsourcing growth in vari-ous segments. IAOP’s Shocklee predicts IT Infrastructure outsourcing will see growth with the focus on Big Data and associated cost of storage management and associated escalating costs. He also expects the continued explosion of data driven devices and impact of social media on business will cause increased focus in outsourcing. Dalal sees cloud computing options continuing to play a bigger role in IT outsourcing decisions for smaller and mid-size companies. However, larger businesses will still be concerned with capacity and security issues and will consider cloud sourcing as a lower alternative to outsourcing, he says.

AlTErNATIvE ENErGy

Driven by rising costs and service interruptions, providers with large data and telecommunications centers may look to other energy sources, such as solar or wind. “Rising utility costs, interruption of service due to natural or man-made events as well as environmental impact of accessing natural resources will drive outsourcing providers to consider alternate sources for their energy consumption,” Dalal predicts. Service providers also will have to look for architecture that utilizes consolidation of services and virtualization in order to reduce requirements for hardware, he says.

ANAlyTIcS

Analytics will be the key revenue driver for rapidly com-moditizing BPO businesses. Arijit Sengupta, CEO of BeyondCore, predicts that BPOs processing invoices, for example, will treat that business as a loss leader while charging clients for a percentage of business benefits such as Cash Conversion Cycle optimizations delivered by analyzing the invoice data.

rUrAl SoUrcING

Outsourcing in U.S. state and local government will continue to accelerate given the continued sluggish economy and dwindling tax base, increasing demand for rural sourcing. “Rural sourcing will benefit from this as states begin to focus on creating outsourcing ecosystems to more affordably support state infrastructures,” Shocklee says.

t r e n d s & f o r e ca s t s

TrEnDS & forEcaSTSgLobaLrEgion

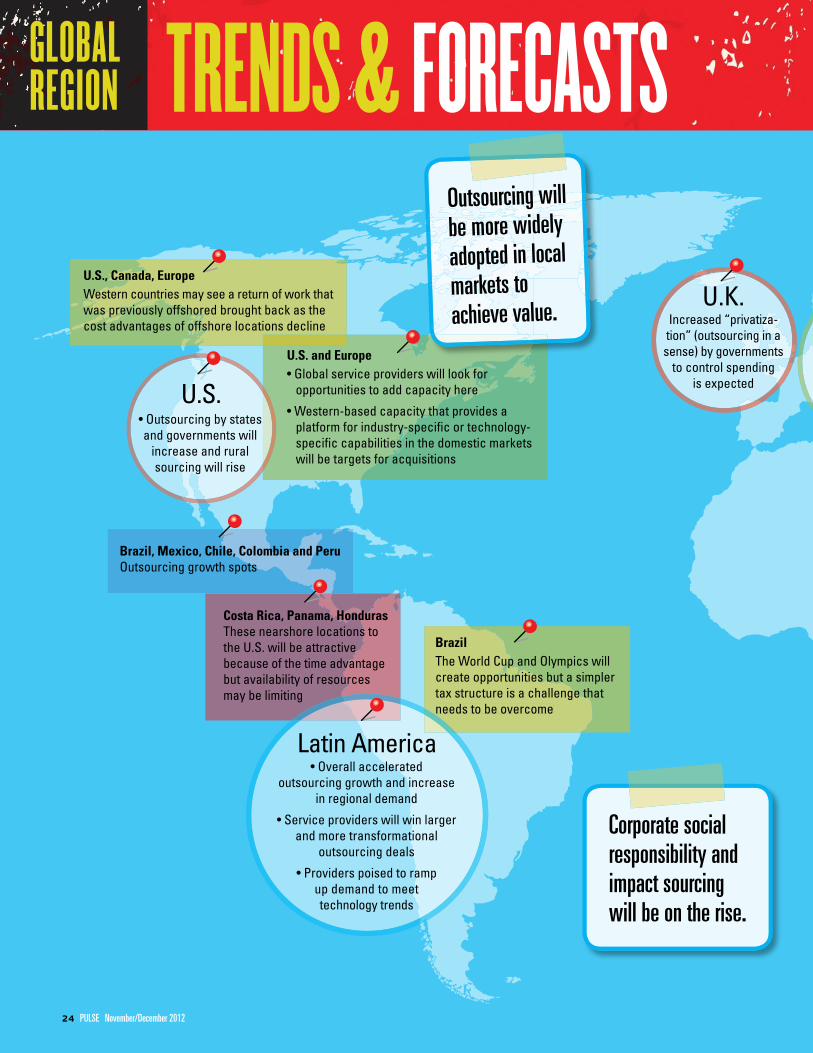

U.S., canada, EuropeWestern countries may see a return of work that was previously offshored brought back as the cost advantages of offshore locations decline

U.S. and Europe• Global service providers will look for opportunities to add capacity here

• Western-based capacity that provides a platform for industry-specific or technology- specific capabilities in the domestic markets will be targets for acquisitions

• Outsourcing by states and governments will

increase and rural sourcing will rise

U.S.

brazil, mexico, chile, colombia and peruOutsourcing growth spots

costa rica, panama, honduras These nearshore locations to the U.S. will be attractive because of the time advantage but availability of resources may be limiting

Eastern Europe

Rapid outsourcing growth predicted due to developing markets

and a wealth of talent

U.K. Increased “privatiza-tion” (outsourcing in a sense) by governments

to control spending is expected

Corporate social responsibility and impact sourcing will be on the rise.

brazil The World Cup and Olympics will create opportunities but a simpler tax structure is a challenge that needs to be overcome

• Overall accelerated outsourcing growth and increase

in regional demand

• Service providers will win larger and more transformational

outsourcing deals

• Providers poised to ramp up demand to meet technology trends

Latin America

Outsourcing will be more widely adopted in local markets to achieve value.

t r e n d s & f o r e ca s t s

24 PULSE November/December 2012

Eastern Europe

Rapid outsourcing growth predicted due to developing markets

and a wealth of talent

India

• Margins will continue to be under pressure for service providers

• Cost advantages over onshore locations will decline as salaries rise and work hours lessen rise and work hours lessen locations will decline as salaries rise and work hours lessenMiddle East

Social and political instability will make some locations less desirable

as outsourcing destinations

JapanOutsourcing market expected

to be impacted by conflict with China over Diaoyu islands

As a mature nation, maintaining leads in intellectual property, investment in R&D and higher

education will be the challenge

Africa• Growth in individual

companies will depend on political and social stability

• New high-speed telecommunication will

aid growth

Emerging destinations to watch in Africa:

TunisiaGhanaSenegal

MauritiusMoroccoSouth Africa

AsiaRevenue growth

slows with a tighten-ing of margins

India and china

• Slower revenue growth predicted

• Continued mergers and acquisitions by providers

global competition for talent will intensify and lead to new blended approaches to hiring.

Buyers and providers will partner more closely to co-create value, transformation and innovation.

t r e n d s & f o r e ca s t s

Australia • Government desire to

control spending will continue to increase privatization

• Legal process outsourcing is growing as an enabler of innovative and integrated

services

PULSE November/December 2012 25

hOtSpOt

africa – is it the “lost” continent or the “last” continent as far as outsourcing is concerned? truth is, it is both.

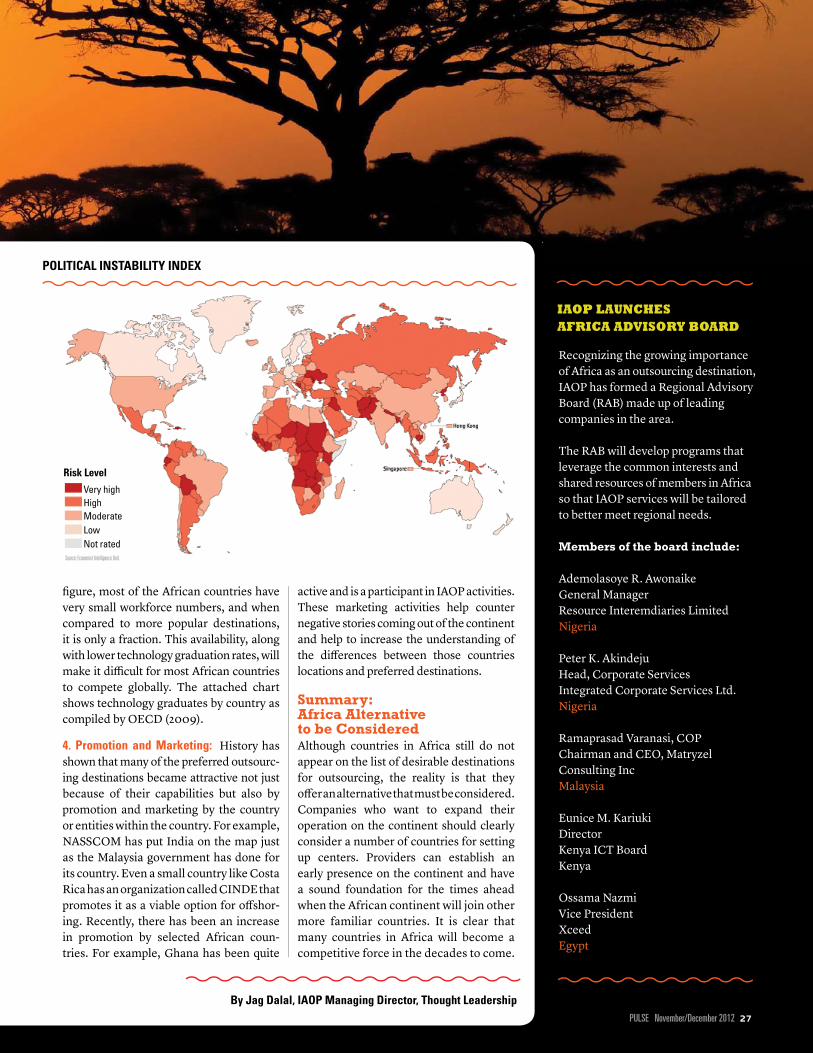

Many believe that this large destination is slowly reaching a stage where businesses will have to seriously consider it in their evaluation for sourcing. However, unlike larger populous countries such as India, China, Brazil or in North America, Africa is a continent with 47 different countries. If you include islands near Africa there are 53 countries. These islands are considered African and can be destinations. For example, the Mauritius Island is to India, what Bermuda is to the U.S. – a safe haven for companies. In a recently published Global Indexing Report (2011) by A.T. Kearney, several of the African nations were listed in the top 50 destinations. It listed Egypt as #4 (However, the ranking was made prior to recent political unrest there and A.T. Kearney indicated that regional instability will lower their ranking), Tunisia (#23), Ghana (#27), Senegal (#29), Mauritius (#36), Morocco (#37) and South Africa (#45). For this article, I will focus mostly on these countries. As the environ-ment changes in other countries, others may become attractive destinations in the future. But by most count, this is not expected in a near future.

Analyzing Attractiveness for Outsourcing:There are several factors that have made these and some of the other nations (such as Nigeria, Algeria and Ethiopia) slowly make their mark on the global outsourcing map. At the same time, some troubling areas still need to be addressed before companies will seriously consider African countries as a destination of choice. These include:

1. Socio-poli-Economic Environment: A tremendous amount of diversity exists among countries in Africa when considering their social, political and economic environment. One of the reasons these countries have been listed in the A.T. Kearney report is their relative political and economic stability. The accompanying graphic from The Economist (2010) clearly shows that the African continent, as a whole, is fairly unstable. Political instability creates an environment where investment capital is restricted, especially

foreign investment, making it difficult to establish or expand services business, which is capital intensive. The Heritage Foundation and Wall Street Journal 2012 analysis also showed that political stability was at best “moderate.” This is further borne out by the assessment by the Fitch Credit Rating services. Their analysis published in July 2012 showed that all of the African countries were rated as “Low Medium Grade” or lower and some of the countries could not even provide necessary information to be rated by Fitch Credit Rating. Despite these challenges, selected countries have taken steps to encourage investment and political umbrella to encourage foreign investment,

and lured established service providers to the continent. Genpact, CSC, Accenture, HP, IBM, Xerox (ACS), Xceed and TCS are among providers that have established their presence in these countries and are offering choices to their customers and prospects.

2. Infrastructure: Although infrastructure in most of the regions and countries in Africa remains a challenge, recent deployment of high-speed telecommunication “inter-continental” cables have opened up many

locations with necessary telecom capabilities. Large investments have been made by countries and private companies to create business zones where infrastructure is on par with advanced nations. Building office parks and facilities for housing processing centers is increasing. A good amount of travel infrastructure is available that connects these nations and cities with rest of the world.

3. workforce availability and qualification: Since many of the countries on the continent were previously occupied by other nations, such as England, France, Netherlands and Portugal, there is a high level of English and other European language comprehen-sion among the population. This adds to the attractiveness for the workforce when they can be proficiently multi-lingual. A high level of investment also is being made in the education sector. However, the workforce preparedness in these countries seriously lags behind other non-African destination; even with smaller populations. According to the CIA World Report, shown in the accompanying

Infrastructure is available to connect nations & cities with the rest of the world.

© Ca

n Stoc

k Pho

to Inc

. / ja

varm

an

AFRICA An Emerging Alternative

by the Numbers: Africa is a continent with 47 different countries, plus six nearby islands.

Status: A tremendous amount of social, political and economic diversity exists among the countries.

countries to watch: Egypt, Tunisia, Ghana, Senegal, Mauritius, Morocco and South Africa.

© Can Stock Photo Inc. / michaeljung

iaop launches africa advisory board

Recognizing the growing importance of Africa as an outsourcing destination, IAOP has formed a Regional Advisory Board (RAB) made up of leading companies in the area.

The RAB will develop programs that leverage the common interests and shared resources of members in Africa so that IAOP services will be tailored to better meet regional needs.

Members of the board include:

Ademolasoye R. AwonaikeGeneral ManagerResource Interemdiaries LimitedNigeria

Peter K. AkindejuHead, Corporate ServicesIntegrated Corporate Services Ltd.Nigeria

Ramaprasad Varanasi, COPChairman and CEO, Matryzel Consulting IncMalaysia

Eunice M. KariukiDirectorKenya ICT BoardKenya

Ossama NazmiVice PresidentXceedEgypt

by Jag dalal, IAop managing director, Thought leadership

figure, most of the African countries have very small workforce numbers, and when compared to more popular destinations, it is only a fraction. This availability, along with lower technology graduation rates, will make it difficult for most African countries to compete globally. The attached chart shows technology graduates by country as compiled by OECD (2009).

4. promotion and marketing: History has shown that many of the preferred outsourc-ing destinations became attractive not just because of their capabilities but also by promotion and marketing by the country or entities within the country. For example, NASSCOM has put India on the map just as the Malaysia government has done for its country. Even a small country like Costa Rica has an organization called CINDE that promotes it as a viable option for offshor-ing. Recently, there has been an increase in promotion by selected African coun-tries. For example, Ghana has been quite

active and is a participant in IAOP activities. These marketing activities help counter negative stories coming out of the continent and help to increase the understanding of the differences between those countries locations and preferred destinations.

Summary: Africa Alternative to be ConsideredAlthough countries in Africa still do not appear on the list of desirable destinations for outsourcing, the reality is that they offer an alternative that must be considered. Companies who want to expand their operation on the continent should clearly consider a number of countries for setting up centers. Providers can establish an early presence on the continent and have a sound foundation for the times ahead when the African continent will join other more familiar countries. It is clear that many countries in Africa will become a competitive force in the decades to come.

polITIcAl INSTAbIlITy INdEx

Very highHighModerateLowNot rated

risk level

Source: Economist Intelligence Unit.

PULSE November/December 2012 27

28 PULSE November/December 2012

Imag

e: ca

nstoc

kpho

to.co

m

Principal and U.S. leader, KPMG Shared Services and Outsourcing Advisory

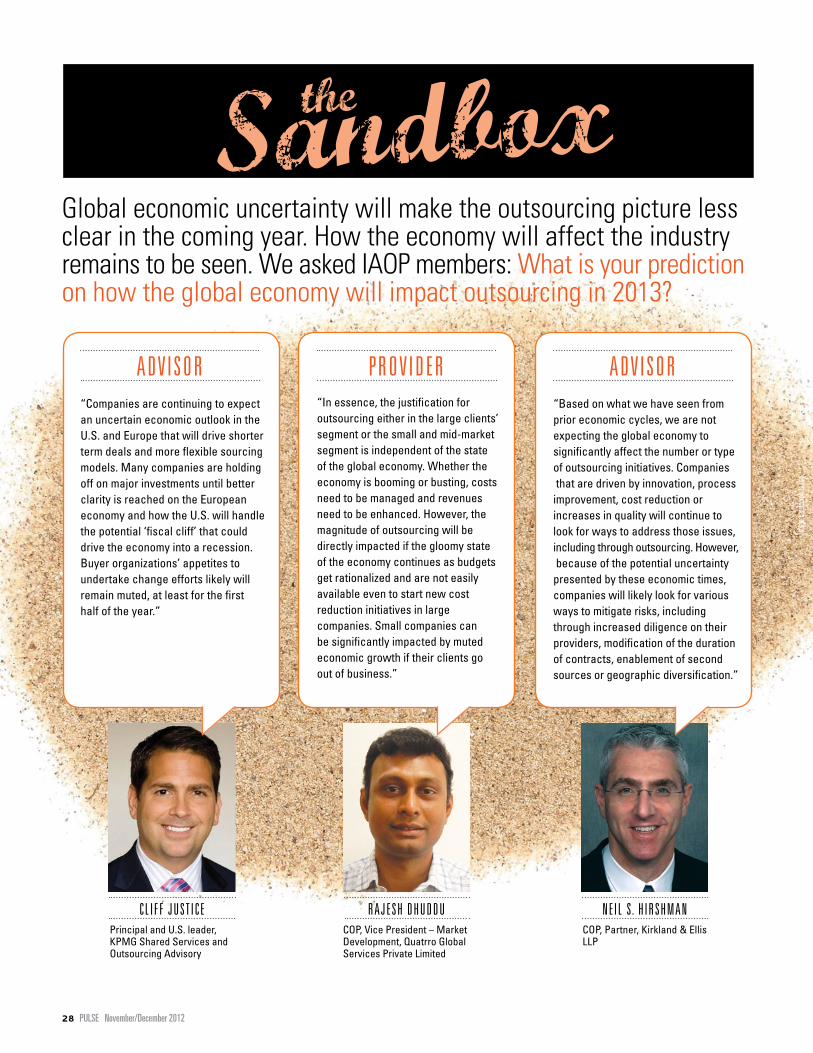

C L I F F J U S T I C E

Global economic uncertainty will make the outsourcing picture less clear in the coming year. How the economy will affect the industry remains to be seen. We asked IAOP members: What is your prediction on how the global economy will impact outsourcing in 2013?

Sandboxthe

COP, Partner, Kirkland & Ellis LLP

N E I L S. H I R S H M A N

“Based on what we have seen from prior economic cycles, we are not expecting the global economy to significantly affect the number or type of outsourcing initiatives. Companies that are driven by innovation, process improvement, cost reduction or increases in quality will continue to look for ways to address those issues, including through outsourcing. However, because of the potential uncertainty presented by these economic times, companies will likely look for various ways to mitigate risks, including through increased diligence on their providers, modification of the duration of contracts, enablement of second sources or geographic diversification.”

A dV I S O R“Companies are continuing to expect an uncertain economic outlook in the U.S. and Europe that will drive shorter term deals and more flexible sourcing models. Many companies are holding off on major investments until better clarity is reached on the European economy and how the U.S. will handle the potential ‘fiscal cliff’ that could drive the economy into a recession. Buyer organizations’ appetites to undertake change efforts likely will remain muted, at least for the first half of the year.”

A dV I S O R

COP, Vice President – Market Development, Quatrro Global Services Private Limited

R A J E S H d H U d d U

“In essence, the justification for outsourcing either in the large clients’ segment or the small and mid-market segment is independent of the state of the global economy. Whether the economy is booming or busting, costs need to be managed and revenues need to be enhanced. However, the magnitude of outsourcing will be directly impacted if the gloomy state of the economy continues as budgets get rationalized and are not easily available even to start new cost reduction initiatives in large companies. Small companies can be significantly impacted by muted economic growth if their clients go out of business.”

P R O V I d E R

Imag

e: ca

nstoc

kpho

to.co

m

PULSE November/December 2012 29

www.kirkland.com

Chicago • Hong Kong • London • Los Angeles • MunichNew York • Palo Alto • San Francisco • Shanghai • Washington, D.C.

1,500 attorneys. 10 offices. 1 team.Kirkland & Ellis is an international law firm with 1,500 attorneysin 10 offices worldwide who form one team with a primary goal ofhelping you successfully achieve your objectives. Kirkland lawyershave long-standing experience in complex outsourcing transactions(including business process and information technology),representing both customers and providers in onshore, nearshoreand offshore outsourcing transactions.

IAOP has named Kirkland & Ellis to the World’s Best OutsourcingAdvisors list each year since the list’s inception.

2012 PULSE Magazine IAOP (8.5x11 color)_Kirkland_Kirkland 8/28/2012 12:11 PM Page 1

30 PULSE November/December 2012

PULSE k n ow l e d g e c e n t e rk n ow l e d g e c e n t e r

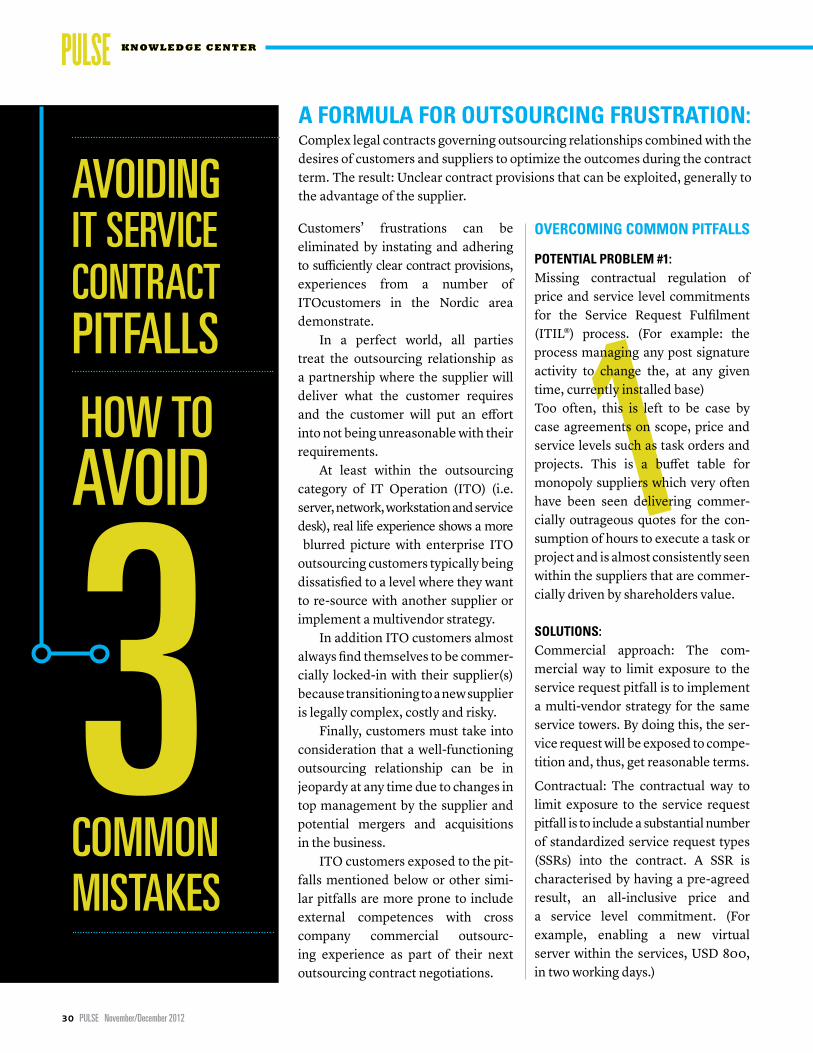

Customers’ frustrations can be eliminated by instating and adhering to sufficiently clear contract provisions, experiences from a number of ITOcustomers in the Nordic area demonstrate. In a perfect world, all parties treat the outsourcing relationship as a partnership where the supplier will deliver what the customer requires and the customer will put an effort into not being unreasonable with their requirements. At least within the outsourcing category of IT Operation (ITO) (i.e. server, network, workstation and service desk), real life experience shows a more blurred picture with enterprise ITO outsourcing customers typically being dissatisfied to a level where they want to re-source with another supplier or implement a multivendor strategy. In addition ITO customers almost always find themselves to be commer-cially locked-in with their supplier(s) because transitioning to a new supplier is legally complex, costly and risky. Finally, customers must take into consideration that a well-functioning outsourcing relationship can be in jeopardy at any time due to changes in top management by the supplier and potential mergers and acquisitions in the business. ITO customers exposed to the pit-falls mentioned below or other simi-lar pitfalls are more prone to include external competences with cross company commercial outsourc-ing experience as part of their next outsourcing contract negotiations.

A FormUlA For oUTSoUrcING FrUSTrATIoN:Complex legal contracts governing outsourcing relationships combined with the desires of customers and suppliers to optimize the outcomes during the contract term. The result: Unclear contract provisions that can be exploited, generally to the advantage of the supplier.

1AvOIDINg IT SERvICE CONTRACT PITFALLS

hOW TOAvOID

3 COMMON MISTAkES

ovErcomING commoN pITFAllS

poTENTIAl problEm #1: Missing contractual regulation of price and service level commitments for the Service Request Fulfilment (ITIL®) process. (For example: the process managing any post signature activity to change the, at any given time, currently installed base)Too often, this is left to be case by case agreements on scope, price and service levels such as task orders and projects. This is a buffet table for monopoly suppliers which very often have been seen delivering commer-cially outrageous quotes for the con-sumption of hours to execute a task or project and is almost consistently seen within the suppliers that are commer-cially driven by shareholders value.

SolUTIoNS: Commercial approach: The com-mercial way to limit exposure to the service request pitfall is to implement a multi-vendor strategy for the same service towers. By doing this, the ser-vice request will be exposed to compe-tition and, thus, get reasonable terms.

Contractual: The contractual way to limit exposure to the service request pitfall is to include a substantial number of standardized service request types (SSRs) into the contract. A SSR is characterised by having a pre-agreed result, an all-inclusive price and a service level commitment. (For example, enabling a new virtual server within the services, USD 800, in two working days.)

PULSE November/December 2012 31

An independent commercial outsourcing specialist, Jørn w. rasmussen is the owner of Pathios and previously was CTO of Maersk Line.

SolUTIoNS: Commercial approach: Decide that the hardware for (parts of ) the outsourcing scope is provisioned and provided by the customer themselves. In the ITO business area this is very often seen with workstations and physical servers but is rarer in the areas of storage, backup and network equipment.

Contractual: Ensure that all services are available as a service composed of unit prices for hardware, housing and services (effort). At the commence-ment of the outsourcing contract, the supplier is delivering the hardware as part of the services and the contract hold provisions that the hardware influenced price / performance levels are negotiated e.g. once a year. If the supplier cannot keep on providing commercially attractive prices, the customer should have the right to substitute the hardware unit with similar hardware procured by the customer themselves. This threat itself has proven to make the supplier renegotiate in good faith.2

3For ThE FUll prESENTATIoN mAdE AT IAop’S NordIc chApTEr, SEE IAop’S KNowlEdGE cENTEr, FIrmbUIldEr.com.

poTENTIAl problEm #3: Lack of a cross service key perfor-mance indicator (KPI) regime with associated penalties.In many contracts there are virtually no KPIs, apart from the traditional availability service levels, which leaves the customer blindfolded to the on-going non-visual quality of the operation and, thus, also to a rising risk for severe incidents as a conse-quence of the build-up effect of con-tinuous operational service failures. In addition it leaves the parties without measurements to base service improvements on and finally it leaves the supplier without incentives to improve the services delivered.

SolUTIoNS:

Contractual: Include a significant number of KPIs into the signed agreement, for example, between 50 and 100, which are all measured every month. A number of these (for example, 25) then are included in a KPI default level regime where each KPI is given a weight factor, consistent breach of a KPI is multiplying with an impact factor. Every month the total across the KPIs is calculated and a penalty applied matching the relative KPI performance level.

The customer should insist that as many as possible of such recurring and reasonable predictable tasks are defined and described before the con-tract is signed and a pool of several hundred can be expected. In addition, a project estimation model must be implemented where the supplier is obligated to use SSRs where possible, including the agreed price and SLA. The remaining part of the project should be broken down to logical work packages – for example, a maximum of 30 hours with a specified purpose and named resources.The supplier should have the right to add project management of a maximum of, for example 15 percent, of the work package volume. Finally, the customer should ensure that they can decide to have a third party delivering (part of ) the work packages.

poTENTIAl problEm #2: Lack of customer step-in right for hard- ware procurement, such as when procuring on-demand integrated services. Reasonably enough, it is very hard to negotiate prices at signature time that reflect long contract period when hardware prices and performance have continuously improved over the last 20 years. As a result, customers often find themselves in a situation a couple of years into the contract where it is obvious that they paid too much for new hardware. Renegotiation at this point in time is troublesome due to the operational lock-in and benchmark clauses are often costly to execute and provide only limited regulation.

ITo cUSTomErS AlmoST AlwAyS FINd ThEmSElvES To bE commErcIAlly locKEd-IN wITh ThEIr SUpplIEr(S) bEcAUSE TrANSITIoNING To A NEw SUpplIEr IS lEGAlly complEx, coSTly ANd rISKy.

© Can Stock Photo Inc. / docent

© Ca

n Stoc

k Pho

to Inc

. / sa

ransk

32 PULSE November/December 2012

PULSE k n ow l e d g e c e n t e r

Proactive remedies are essentially an early warning system where certain events give the customer access to certain commercial and legal remedies based on the risk level of the particular trigger event. The purpose of giving the customer the right to exercise these remedies is to allow the customer to pre-empt any breaches by capturing and correcting negative

PROACTIvE REMEDIES hELP OUTSOURCINg CUSTOMERS MANAgE RISkS

trends in the delivery of the outsourced services. Optimally, proactive remedies will give the service provider an incen-tive to invest in risk management and correct negative trends before any material breaches materialize. When used as an active part of the customer’s contract management, proactive remedies serve as a strong risk management tool and give the service provider an incentive to invest in risk management and halt negative trends at an early state.

oUTSoUrcING ANd TrAdITIoNAl rEmEdIES

At least in theory, the outsourcing busi-ness model is an efficient and world-class business tool. By outsourcing, customers can access resources and competencies that would not other-wise be available and service providers can use economics of scale in order to offer reduced costs for those expenses related to hardware and software. The service provider’s perceived ability to standardize and consolidate platforms and use of technology should reduce unit costs and provide for higher tech-nology efficiency than a customer itself would be able to. Additionally, because service and technology provision is a service pro-vider’s trade, a service provider should be able to provide higher availability, better security, greater resilience and more effective processes for software development and maintenance. Despite the emergence of the out-sourcing model in IT services, business processes and many other lines of business, surveys, statistics and the everyday interaction with clients having outsourced, show that the outsourcing business model has not delivered on its promises.

A rEcENT TrENd EmErGING IN ThE pAST ThrEE To FIvE yEArS hAS bEEN To INclUdE So-cAllEd proAcTIvE rEmEdIES IN oUTSoUrcING coNTrAcTS.

© Ca

n Stoc

k Pho

to Inc

. / re

drock

erz

PULSE November/December 2012 33

pErFormANcE oF ThE SErvIcE provIdEr: These focus on negative trends in terms of performance of services by the service provider and as such offer a great scope for individualiza-tion according to each customer’s priorities and requirements.

ExAmplES: Service level drops; key performance indicators or project milestones not delivered on time or to budget; disruptions being attributable to human errors; inability of the service provider to cure a breach within agreed time limits; persistent or repeated breach, non-performance of processes such as change management (and other relevant ITIL processes); the material non-performance of the supplier’s obligations to a sub-contractor

FINANcIAl INFormATIoN or orGANIZATIoNAl dEvElopmENT: These events relate to financial information or organizational development and can also cover a wide variety of events that can potentially, and depending on the circumstances and context, have a negative effect on the performance of the outsourcing contract in the foreseeable future, even if the transaction or the effect of the infor-mation is not immediately noticeable.

ExAmplES:Acquisition, merger or divestures by the service provider; increases in the turnover rate among the service provider’s key personnel; change of the project executive; a lowering of the service provider’s credit rating; a stock exchange profit warning issued by the service provider or its parent company.

common types of trigger events

A majority of all outsourcing agreements fail in one or several aspects and nearly all outsourcing agreements are renegotiated and re-scoped due to customer pressure be-cause of performance issues or simply because prices have been undermined by market developments. The most common remedy for non-performance is service credits and remediation of services and deliverables. Service credits capture only aspects of the service delivery, namely non-performance of service levels for operational items such as availability, time to recover, failover capabilities, etc. In theory this remedy should work but customers increasingly voice that service credits are so low that they are unimportant and that service providers simply see service credits as a common day-to-day event that is likely to be fully compensated for in the service provider’s business case. In regards to remediation of services and deliverables, this will typically first be available when the deadlines for delivering the services and deliverables have passed. In most cases the damage will already have been done at this point. Further, customers will in most cases have to rely on the service provider’s ability to adequately determine and implement any remedial efforts and this process will often not be transparent to the customer. All other remedies are in practice remote in nature. Most often service credits rule out that damages can be obtained and in any case, indirect loss and loss of profits are always excluded. That leaves termination for breach as the remain-ing remedy. Considering the costs and risks associated with procuring replacement services and transitioning the existing services to a replacement service provider or insourcing the services, only the persistent and the very material breach of an outsourcing contract will be sufficient to justify termination even though a customer may be fundamentally dissatisfied with the performance of the service provider. What all of these traditional remedies have in common is that they are reactive and the consequence of the above mentioned factors is that the accountability of service providers is low. In such a contractual environment there is little incentive for the service provider to capture negative trends before these develop into actual breaches of the outsourcing contracts.

bUSINESS procESSES ANd mANy oThEr lINES oF bUSINESS, SUrvEyS, STATISTIcS ANd ThE EvErydAy INTErAcTIoN wITh clIENTS hAvING oUTSoUrcEd, Show ThAT ThE oUTSoUrcING bUSINESS modEl hAS NoT dElIvErEd oN ITS promISES.

{ } © Ca

n Stoc

k Pho

to Inc

. / sa

ransk

PULSE k n ow l e d g e c e n t e r

PROACTIvE REMEDIES hELP OUTSOURCINg CUSTOMERS MANAgE RISkS CONT.

rISK lEvElS Each trigger event will be assigned a certain number of risk levels and these risk levels will be maintained for a specified period of time, for example for six months after the trigger event occurred, or for as long as the trigger event is ongoing. Generally, there are three to five different risk levels for each trigger event. Risk levels should be designed to reflect how the customer requires the supplier to react to the occurrence of the trigger events. With each increasing risk level there is also an increase in the severity of the proactive remedies available to the customer, so that with each higher risk level the customer will have more options available to attempt to pre-empt a breach of the contract. In order to secure the applicability of the trigger events and the associated risk levels, it is important to ensure that the trigger events are worded clearly and measurable. In ensuring measurability the parties avoid any disputes as to whether or not a trigger event has occurred, which risk level is reached, and, by extension, whether or not the customer can evoke any of the proactive remedies associated with that particular trigger event and risk level.

proAcTIvE rEmEdIES Each risk level gives the customer the option to use the proactive remedies associated with that particular risk level. Generally a time period should be specified for each remedy, stating for how long the proactive remedies available under each risk level are available to the customer. Assuming that lowering of the service provider’s credit rating has been defined as a trigger event, it should be stated that for a certain period of time, for example, six months after the credit rating has been lowered, the remedy is available to the customer. Alternatively, remedies may also be available only for as long as the trigger event in question is ongoing, for example, if service levels are lower than stipulated by the contract, the cus-tomer will have access to the remedies until the service levels have been restored. Essentially, proactive remedies allow for very specific and individualized remedies to be applied for those trigger events which are particularly important to the customer and require a specific reaction. Examples of proactive remedies available under risk level one can be that the service provider must initiate specific reporting on the issues related to the trigger event in question on a regular basis, or the service provider must prepare and submit a specification of the approximate expected efforts and resources to be used to address the trigger event in question.

Essentially, proactive remedies

allow for very specific and

individualized remedies to be

applied for those trigger events

which are particularly important

to the customer and require a

specific reaction.

34 PULSE November/December 2012

Proactive remedies under risk level two and three will typically be more severe, for example the customer may require an independent third party to evaluate and provide recommendations with regard to the trigger event in question and the supplier is obliged to implement such recommendations. Typically proactive remedies available under lower risk levels will also be available under the higher levels. For example, proactive remedies under risk level one will also be available under risk level two, and proactive remedies under risk level one and two will also be available under risk level three, etc.

whEN ArE proAcTIvE rEmEdIES rElEvANT? Proactive remedies are relevant when there is a technical, practical or financial lock-in. In other words, the customer is one way or another bound to a specific service provider for a multi-year contract period. Minimum commitment, expensive termination for convenience, and/or a long transition phase are all examples of customer lock-in. Furthermore, the fact that the outsourced services rely on particular (patented) technology or know-how being utilized may also lead to a technical lock-in as there may only be one service provider with access to the technology or know-how. Under these circumstances there may not be alternative service providers. This also holds true for special competences in narrow fields of service where there are few specialized service providers. Proactive remedies are also relevant where the customer’s actual loss due to non-performance by the service provider will not be compensated under the outsourcing contract (business loss being excluded). It is therefore possible to say, that the financial incentive to include proactive remedies in an outsourcing contract is right when the likely financial loss implied by a risk actualizing is larger than the supplier’s additional fee for taking over the risks and investing in preventing the risk.

For the full presentation from the IAOP Nordic Chapter meeting, see Firmbuilder.com

Tue Goldschmieding is an attorney and ole horsfeldt is a partner at Gorrissen Federspiel. Both specialize in IP and technology. Gorrissen Federspiel has included proactive remedies in large scale and complex outsourcing contracts since 2005.

share your smarts through iaop chapters

IAop’s chapters are the brains behind many of the association’s programs and presentations, and its chapter chairs are recognized for their thought leadership.

This ever-expanding network of more than 50 geographic and topical groups within IAOP play an important role in sharing ideas, stretching profes-sionals’ thinking and contributing to the richness of IAOP’s Knowledge Center, FirmBuilder. Chapter presentations also augment many quality presenta-tions made at the annual Outsourcing World Summit. The three stories featured here in our “Best of Knowledge Center” are from presentations made at meetings of the Nordic and Brussels chapters. IAOP chapters provide a forum for members to collectively focus on professional development, networking and the advancement of outsourcing within specific areas of common interest. Each chapter is led by chairs and co-chairs with deep knowledge in the area covered. IAOP members are encouraged to participate in as many chapters and chapter meetings as they wish. Non-members are welcomed to attend any chapter meeting as IAOP’s guest.

Geographic chapters: Atlanta, Australia, Beijing,Brazil, Brussels, Canada, Chicago, Colombia, Delaware Valley, Eastern Europe, Germany, Hong Kong, India, Italy, Malaysia, Midwest, Minnesota, New England, New York, Nordic, North Africa, Ohio River Valley, Pacific Northwest, Philippines, Qingdao/Shandong, Rocky Mountain, Russia, San Francisco, Shanghai, South Africa, Southern California, Spain (Madrid), Switzerland, United Kingdom & Ireland, Texas, Washington D.C.

Topical and industry chapters: Cloud Computing, Contracting Process, Contact/Call Center, Data Security & Privacy, Engineering, Financial Services, Global Human Capital, Global Technology Industry, Governance, IT Infrastructure, Life Sciences, Legal & Compliance, Legal Process Outsourcing, Outsouring Tools & Technology Innovation, Process Excellence, Sales & Marketing, Transboundary Sourcing, Voice of the Customer

PULSE November/December 2012 35

36 PULSE November/December 2012

PULSE k n ow l e d g e c e n t e r