public version contains request for confidential treatment · pdf filepublic version contains...

TRANSCRIPT

PUBLIC VERSION

CONTAINS REQUEST FOR CONFIDENTIAL TREATMENT

February 16, 2016

The Honorable Kimberly D. Bose Secretary Federal Energy Regulatory Commission 888 First Street, N.E. Washington, D.C. 20426 Re: ISO New England Inc., Eversource Energy Service Company Docket No. ER16-116 Dear Secretary Bose:

On October 19, 2015, Eversource Energy Service Company (“Eversource”) submitted, on behalf of its transmission-owning affiliate, The Connecticut Light and Power Company (“CL&P”), a cost treatment proposal and related tariff revisions to Attachment F of Section II of ISO New England Transmission, Markets and Rates Tariff to recover approximately $15.7 million incurred by CL&P in planning and developing the Central Connecticut Reliability Project (“CCRP”), a component of the New England East West Solution (“NEEWS”) transmission project.

On December 16, 2015, the Commission Staff issued a Deficiency Letter asking

Eversource to provide additional information on certain categories of costs relating to CCRP, including system planning studies, Allowance for Funds Used During Construction (“AFUDC”), and siting and permitting work. On December 31, 2015, the Commission granted Eversource Energy’s motion for an extension of time to submit the requested information by February 15, 2016.

David B. Raskin 202 429 6254 [email protected]

1330 Connecticut Avenue, NW Washington, DC 20036-1795 202 429 3000 main www.steptoe.com

Kimberly D. Bose, Secretary February 16, 2016 Page 2 of 3

Eversource hereby submits this filing in response to Commission Staff’s December 16, 2016 Deficiency Letter.1 In response to Commission Staff’s request, Eversource is submitting in this filing a number of documents, including copies of invoices, work orders, and other documents relating to third-party consultants who provided assistance to Eversource in connection with the NEEWS Project, including CCRP. As explained further below, Eversource respectfully requests confidential treatment for those materials.

Request for Confidential Treatment Eversource requests confidential treatment for materials and information related to its

vendors and the vendors’ employees. Vendor-specific information, including pricing and employee related information, is competitively sensitive, and disclosure of this information could cause business injury both to Eversource and its vendors. Vendor-specific negotiations/pricing and employee information ordinarily are not made public, and public disclosure of such information could expose Eversource’s and/or its vendors’ pricing positions to competitors. To prevent disclosure of amounts that specific vendors charged, Eversource is retaining in the public version of this filing the amounts that such vendors charged but redacting vendor names and other identifying information associated with such amounts. In addition, certain attachments to this filing contain confidential vendor-specific information and/or information relating to the vendor’s employees throughout the document. As to these documents, Eversource requests confidential treatment for the entire documents.

Pursuant to Order No. 769 and the Commission’s regulations regarding privileged

materials thereunder,2 Eversource provides a public version and a privileged/confidential version of its filing. In the public version, Eversource has redacted certain portions of the Responses and Attachments 3 to 13, 15, 20, and 22 relating to vendor names, as well as removing the vendors’ invoices in Attachments 16, 17, 18, and 21. In the non-public version, Eversource has identified and highlighted the portions of the Responses and attachments that are confidential. In addition, pursuant to the Commission’s regulations, Eversource has marked the confidential version with the designation “CONTAINS PRIVILEGED/CONFIDENTIAL INFORMATION – DO NOT RELEASE.” Eversource also includes with this filing a proposed protective agreement (Appendix A), which individuals may sign to gain access to the confidential materials.3 In addition, in compliance with Commission Staff’s directive in Question No. 5, Eversource is providing proposed tariff revisions to Attachment F of the ISO New England Inc. (“ISO-NE”) Transmission, Markets and Services Tariff (“Tariff”) based upon the currently effective version of Attachment F, as approved by the Commission in Docket No. ER15-1629.

1 Because February 15, 2016 was a federal holiday (President’s Day) and the Commission was

not open for business, Eversource Energy is submitting its Response to the Deficiency Letter today. 2 Filing of Privileged Materials and Answers to Motions, Order No. 769, 141 FERC ¶ 61,049

(2012); see also 18 C.F.R. § 388.112 (2015). 3 Eversource’s October 19, 2015 filing included a proposed form of protective agreement under

Section 388.112 of the Commission’s regulations in connection with its request that certain documents related to Mr. Boguslawski’s testimony be treated as Critical Energy Infrastructure Information (“CEII”).

Kimberly D. Bose, Secretary February 16, 2016 Page 3 of 3

If you have any questions concerning this Response, please do not hesitate to contact the undersigned.

Respectfully submitted, /s/

Phyllis E. Lemell Assistant General Counsel Rosemary K. Leitz Senior Counsel Eversource Energy Service Company P.O. Box 270 Hartford, CT 06141-0270

David B. Raskin Viet H. Ngo Steptoe & Johnson LLP 1330 Connecticut Avenue, NW Washington, DC 20036

Counsel for Eversource Energy Service Company

cc: Jonathan Fernandez Service List (w/attachment)

Eversource Energy Service Company Docket No. ER16-116

Response to Commission Staff Request for Information February 16, 2016

Page 1 of 20

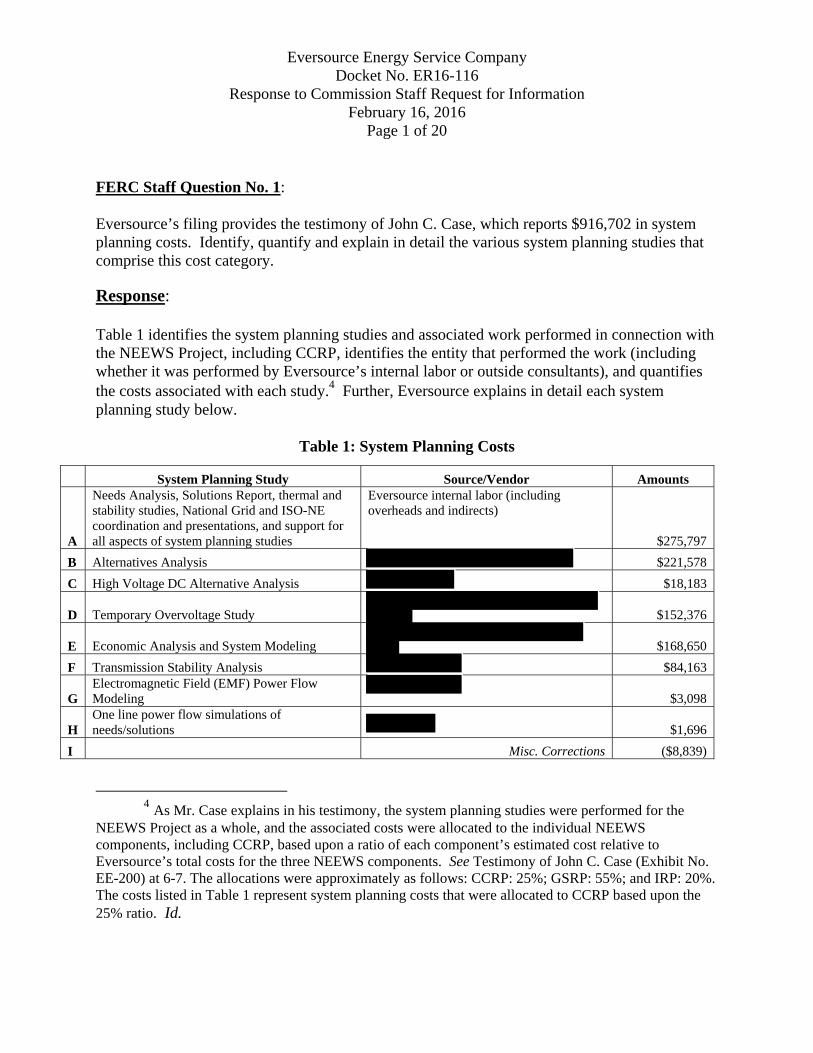

FERC Staff Question No. 1: Eversource’s filing provides the testimony of John C. Case, which reports $916,702 in system planning costs. Identify, quantify and explain in detail the various system planning studies that comprise this cost category.

Response:

Table 1 identifies the system planning studies and associated work performed in connection with the NEEWS Project, including CCRP, identifies the entity that performed the work (including whether it was performed by Eversource’s internal labor or outside consultants), and quantifies the costs associated with each study.4 Further, Eversource explains in detail each system planning study below.

Table 1: System Planning Costs

4 As Mr. Case explains in his testimony, the system planning studies were performed for the

NEEWS Project as a whole, and the associated costs were allocated to the individual NEEWS components, including CCRP, based upon a ratio of each component’s estimated cost relative to Eversource’s total costs for the three NEEWS components. See Testimony of John C. Case (Exhibit No. EE-200) at 6-7. The allocations were approximately as follows: CCRP: 25%; GSRP: 55%; and IRP: 20%. The costs listed in Table 1 represent system planning costs that were allocated to CCRP based upon the 25% ratio. Id.

System Planning Study Source/Vendor Amounts

A

Needs Analysis, Solutions Report, thermal and stability studies, National Grid and ISO-NE coordination and presentations, and support for all aspects of system planning studies

Eversource internal labor (including overheads and indirects)

$275,797

B Alternatives Analysis $221,578

C High Voltage DC Alternative Analysis $18,183

D Temporary Overvoltage Study

$152,376

E Economic Analysis and System Modeling

$168,650

F Transmission Stability Analysis $84,163

G Electromagnetic Field (EMF) Power Flow Modeling $3,098

H One line power flow simulations of needs/solutions $1,696

I Misc. Corrections ($8,839)

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 2 of 20

The $916,702 of system planning costs attributable to CCRP are identified by Eversource’s internal labor (discussed further in subsection A) and contract work/outside services (discussed further in subsections B to H). A. System Planning Study Support - Eversource Internal Labor - $275,797 Eversource’s internal planners and engineers were responsible for the overall planning process and system planning studies related to the NEEWS Project, including CCRP, as well as interactions with regulators, ISO-NE and New England stakeholders. As Mr. David Boguslawski explained in his testimony, there were numerous studies and efforts related to the planning and development of the NEEWS Project, including CCRP.5 These studies were often broad in scope, long in duration, and iterative. There were overlapping issues among the studies, and an Eversource employee was often involved in several system planning studies related to NEEWS throughout the day. Eversource’s planners and engineers were involved in all aspects of the NEEWS/CCRP system planning studies identified in Table 1 above, including the Needs Analysis and Option Analysis/Solutions Report.6 In addition, Eversource’s personnel worked on two additional studies that ISO-NE required in order to reassess the reliability needs of the NEEWS Project, including CCRP: (1) needs re-assessment and confirmation of need in 2010; and (2) verification of solutions and NEPOOL Task Force presentations. As Mr. Boguslawski explains in his testimony, the NEEWS Project was a major, complex addition to the New England 345-kV transmission system.7 Where there were limitations on internal resources due to workload issues, or if the expertise for highly specialized studies was not available internally, Eversource retained outside consultants and engineering firms to assist with the system planning studies. The costs for the outside consultants associated with a specific NEEWS/CCRP planning study are provided below, as well as a detailed explanation of the study:

5 See Direct Testimony of David H. Boguslawski (Exhibit No. EE-100) at 7-9, 13-14 (describing

how the system planners from Eversource and National Grid worked with ISO-NE with respect to the Southern New England Electric Transmission Reinforcement (“SNETR”) Study/Needs Analysis and the Options Analysis and Solution Report. See also Prepared Joint Testimony of David B. Boguslawski of Northeast Utilities Service Company and Paul Renaud of National Grid USA (filed on September 18, 2008 in Docket No. ER08-1548) at 11-12.

6 The ISO-NE planning process includes a Needs Assessment that examines the adequacy of the regional transmission system to maintain reliability while promoting the operation of efficient wholesale electric markets in New England.

7 See Boguslawski Testimony (Exhibit No. EE-100) at 2.

Total System Planning Costs $916,702

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 3 of 20

B. Alternatives Analysis - $221,578

The firms of were retained to assist in developing the alternatives analysis for NEEWS, including CCRP. After determining the electrical need for the NEEWS Project, it was necessary for Eversource planners (working in conjunction with ISO-NE) to establish preferred solutions that would address the needs, and that are feasible, constructible and economical. This effort involved an analysis of numerous electrical scenarios and contingencies, with a large volume of iterations to support the complex NEEWS project. C. High Voltage DC Alternative Analysis - $18,183

Eversource retained to assist with the study of a high voltage direct current (HVDC) solution design option. As an alternative to the standard overhead three phase alternating current design, an HVDC option was studied to test its reliability and other system modifications that such a design would entail. An HVDC alternative would eliminate the high temporary overvoltages and could be more visually appealing since it would require only two conductors rather than three. D. Temporary Overvoltage Study - $152,376

provided support for the Temporary

Overvoltage Study. In the planning process, there was a possibility that a significant portion of CCRP would have to be undergrounded.8 Capacitance of large scale cables that are utilized in underground transmission is much larger than that of an overhead line. This capacitance can lead to high sustained voltages that could cause damage to utility or customer equipment and could result in extended outages. The impact of this capacitance on the transmission network and how to mitigate the impact is analyzed in a Temporary Overvoltage study. E. Economic Analysis and System Modeling - $168,650

Eversource hired to perform economic analysis and system modeling studies to demonstrate the impact that system congestion and the proposed

8 Under Connecticut laws, there is a rebuttable presumption that transmission facilities 345-kV and above should be undergrounded where adjacent to certain land uses. See Testimony of Prepared Joint Direct Testimony of David B. Boguslawski of Northeast Utilities Service Company and Paul Renaud of National Grid USA at 49 (filed on September 17, 2008 in Docket No. ER08-1548) (citing Conn. Gen. Stats. § 16-50p(i), as amended by Public Act 07-04). In addition, Connecticut siting legislation (the Public Utilities Environmental Standards Act) expresses a preference for underground transmission solutions, which the Connecticut Siting Council considers in balancing considerations of need, cost, and environmental impact (See CGS Sec. 16-50l(vi), 16-50p(a)(3)(D), and 16-50r(b)). Accordingly, to secure approval, a proposed overhead transmission line must be compared to a thoroughly investigated, feasible underground alternative and shown to be decisively superior with respect to cost and/or environmental impact.

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 4 of 20

NEEWS Project, including CCRP, would have on electricity prices. This economic modeling was heavily dependent on power flows and congestion analysis across various electrical interfaces. Additional economic studies were performed to identify other benefits that a project may provide, such as the impact of the project on tax revenues and jobs. F. Transmission System Stability Analysis - $84,163

was hired to assist Eversource’s planning staff with performing the stability

analysis. Stability analysis is a required study to connect a new transmission project to the existing electrical system, and to demonstrate that the project will not have an adverse system impact. Stability analysis analyzes the dynamics of a power system to determine system performance following a disturbance, to ensure that the disturbance does not result in potential cascading issues. G. Electromagnetic Field power flow modeling - $3,098

assisted Eversource’s planning staff in an analysis of load flow data for

purposes of optimizing the line phasing to minimize Electromagnetic Fields (EMF) of the NEEWS Project. EMF for various project configurations must be studied in connection with the regulatory approval process. The NEEWS Project affected EMF levels along the proposed and alternative routes, and as a result EMF was required to be studied as part of the siting filings. H. One line power flow simulations of needs/solutions - $1,696

Eversource employed s proprietary software simulation models as a resource tool to communicate the complex nature of the power system needs and solutions for the NEEWS Project to stakeholders. These models demonstrated system performance, showed the system deficiencies (needs) and how to address those needs (solutions) with one –line diagrams simulating the power flows on the system, before and after the project was completed. I. Miscellaneous corrections - ($8,839) In 2008 and 2009, charges totaling $8,839 were removed from system planning as part of normal cost review procedures. Corrections for these charges to system planning are reflected as credits to the CCRP work order.

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 5 of 20

FERC Staff Question No. 2:

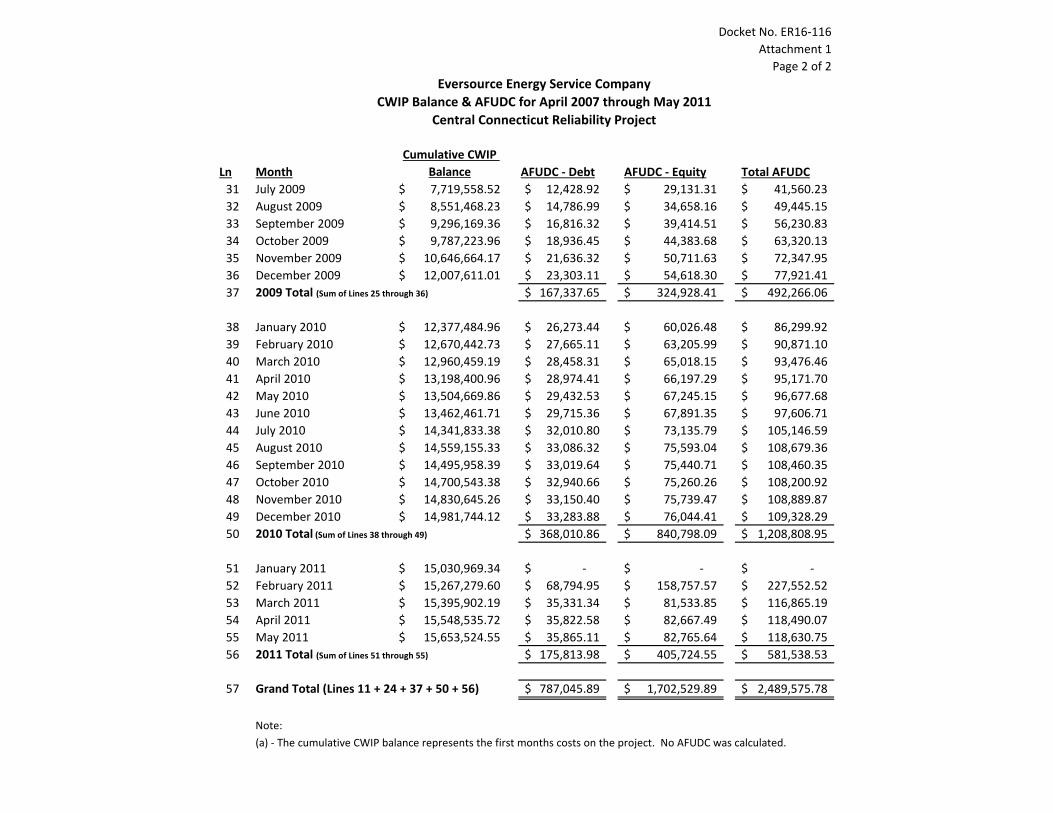

The testimony of John C. Case reports an Allowance for Funds Used During Construction (AFUDC) of $2,489,576. Eversource explains that CL&P accrued AFUDC for the period prior to the Commission granting authorization for CL&P to include CWIP in Local Network Service rates under the ISO New England Tariff in Docket No. ER08-1548. For the AFUDC that Eversource accrued on the CCRP prior to June 1, 2011, provide an excel spreadsheet table showing the CWIP balance that the AFUDC rate was applied to, the AFUDC accrued by year, and the total amount of AFUDC accrued for all of those years combined. Show the amounts accrued for both borrowed funds and other funds.

Response:

See Attachment 1, which is an excel spreadsheet table that shows the CWIP balances for the period March 2007 through May 2011, the AFUDC accrued on a per month basis, and the total amount of AFUDC accrued for the relevant period.

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 6 of 20

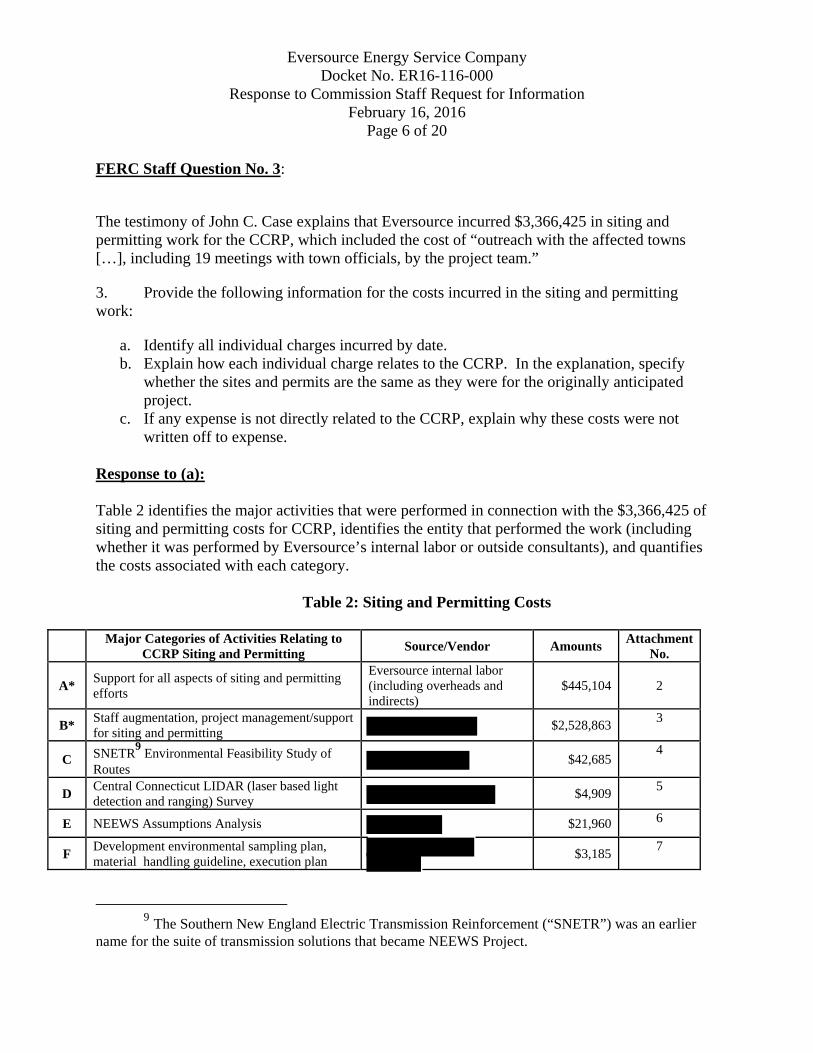

FERC Staff Question No. 3:

The testimony of John C. Case explains that Eversource incurred $3,366,425 in siting and permitting work for the CCRP, which included the cost of “outreach with the affected towns […], including 19 meetings with town officials, by the project team.”

3. Provide the following information for the costs incurred in the siting and permitting work:

a. Identify all individual charges incurred by date. b. Explain how each individual charge relates to the CCRP. In the explanation, specify

whether the sites and permits are the same as they were for the originally anticipated project.

c. If any expense is not directly related to the CCRP, explain why these costs were not written off to expense.

Response to (a):

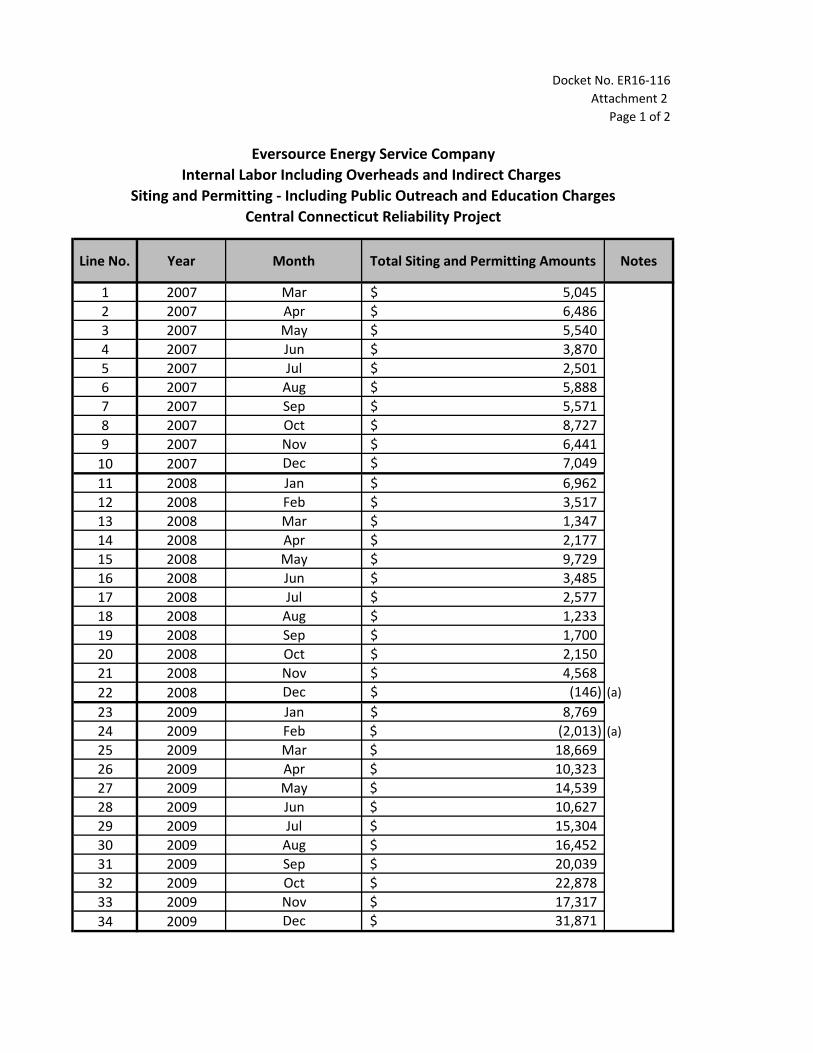

Table 2 identifies the major activities that were performed in connection with the $3,366,425 of siting and permitting costs for CCRP, identifies the entity that performed the work (including whether it was performed by Eversource’s internal labor or outside consultants), and quantifies the costs associated with each category.

Table 2: Siting and Permitting Costs

Major Categories of Activities Relating to

CCRP Siting and Permitting Source/Vendor Amounts

Attachment No.

A* Support for all aspects of siting and permitting efforts

Eversource internal labor (including overheads and indirects)

$445,104

2

B* Staff augmentation, project management/support for siting and permitting

$2,528,863 3

C SNETR9 Environmental Feasibility Study of

Routes $42,685

4

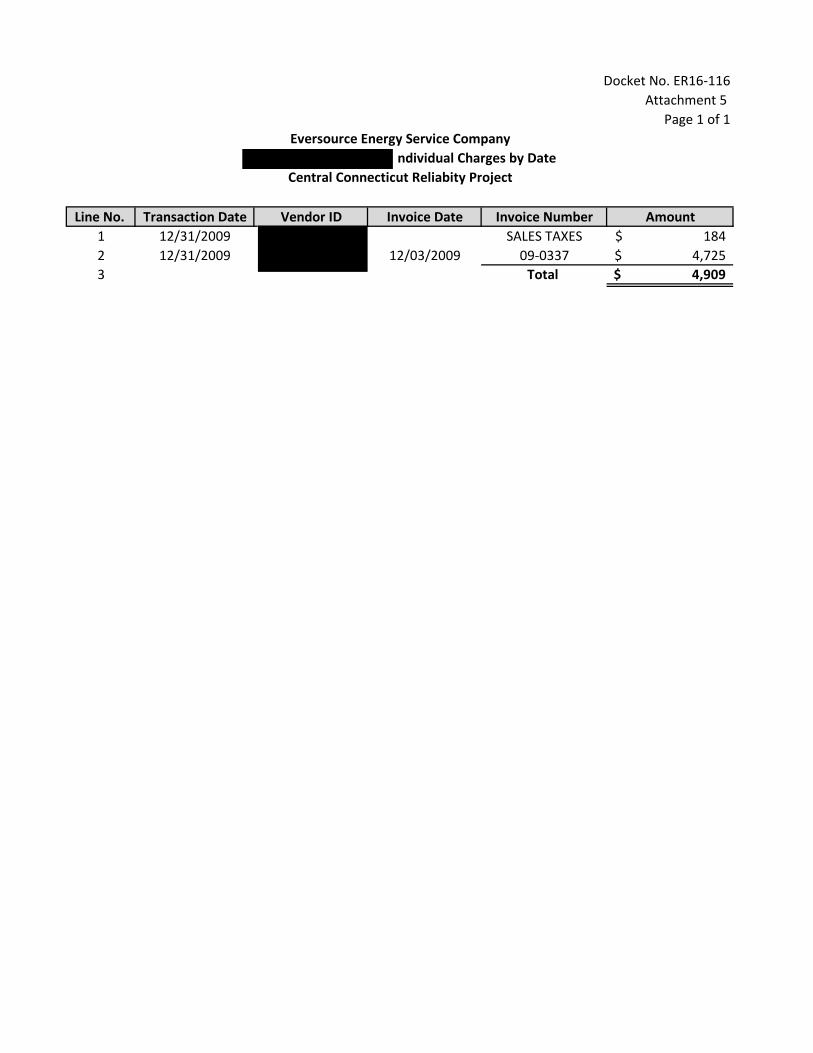

D Central Connecticut LIDAR (laser based light detection and ranging) Survey

$4,909 5

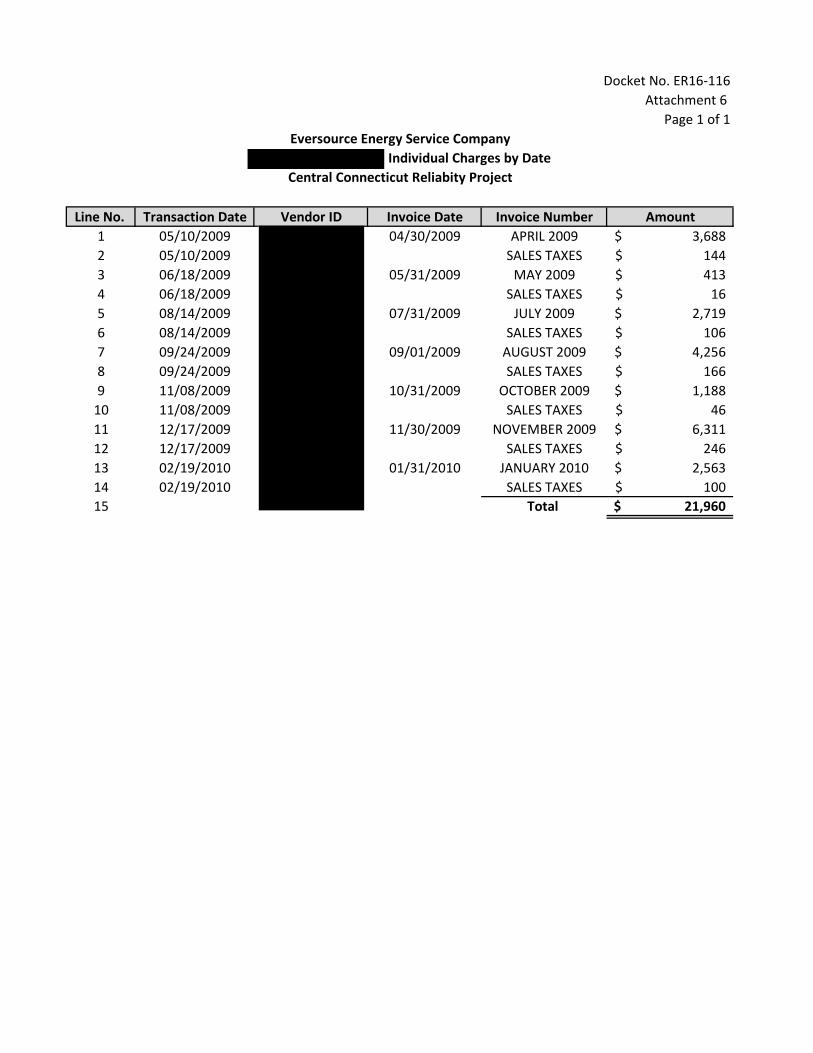

E NEEWS Assumptions Analysis $21,960 6

F Development environmental sampling plan, material handling guideline, execution plan

$3,185

7

9 The Southern New England Electric Transmission Reinforcement (“SNETR”) was an earlier

name for the suite of transmission solutions that became NEEWS Project.

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 7 of 20

G Consultant for Video Broadcasting Service - expertise in photo, lighting, camera

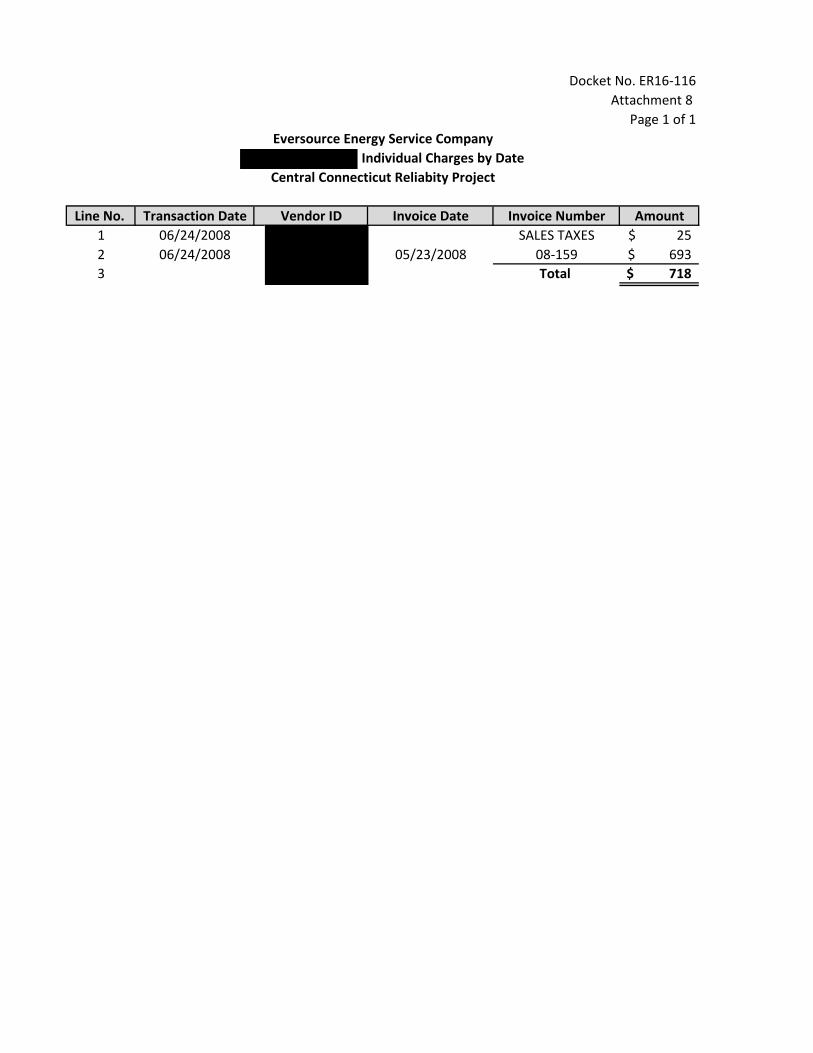

$718 8

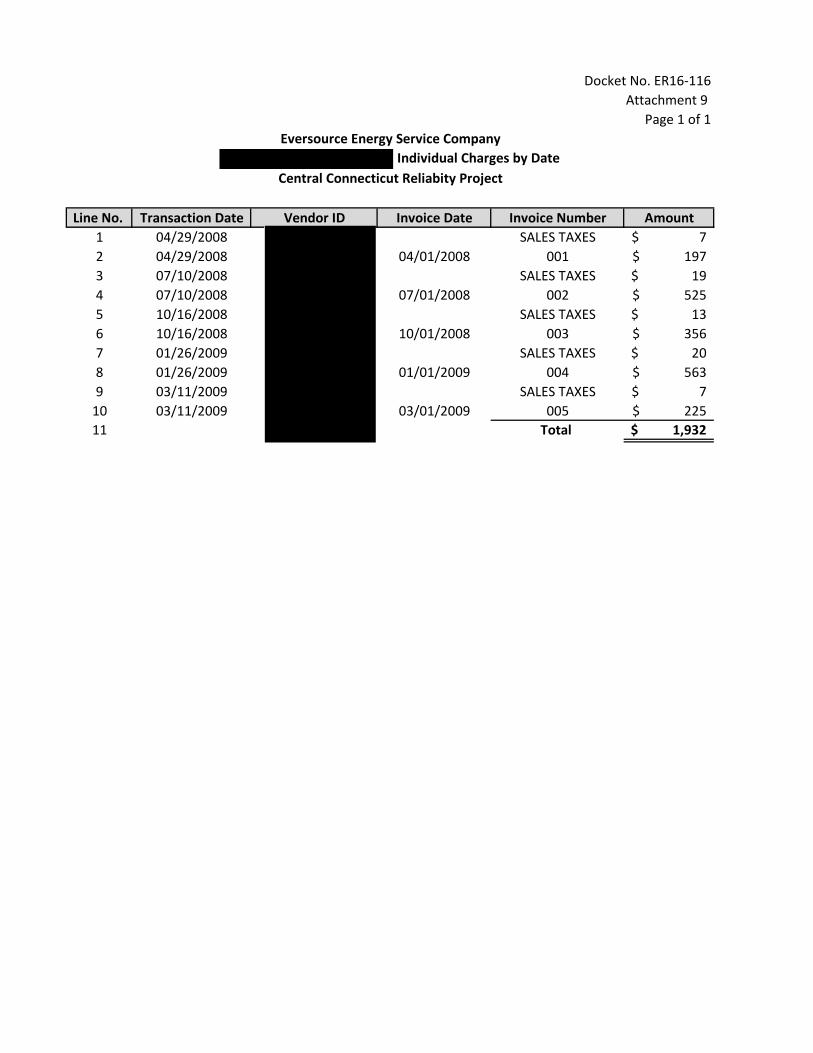

H NEEWS Economic Assessment $1,932 9

I** NEEWS Brochure Design $1,771 10

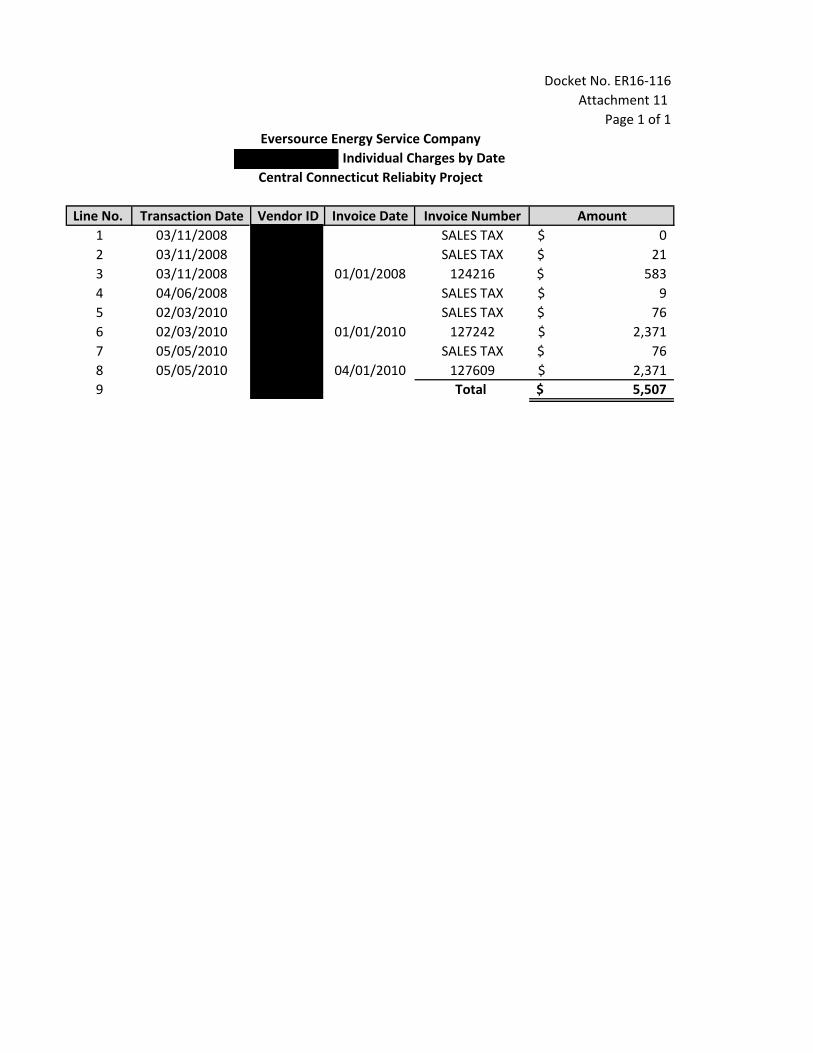

J** NEEWS Information kiosks for permitting & outreach

$5,507 11

K** Public Relations - Assistance in communications plan and strategy

$318,729 12

L Meals $24 13

M Work Order Adjustments ($8,962)

Total Siting and Permitting $3,366,425

* Portions of the costs in Categories A and B are associated with public outreach and education activities, as explained further in the Response to Question 4. ** The entirety of the costs in Categories I, J, and K relate to services associated with CCRP public outreach and education activities (as discussed in the Response to Question 4). In addition to Table 2 above, the corresponding attachment labeled in the last column identify all individual charges by date:10

• Attachment 2 provides charge information by month for Eversource’s internal labor (Item A in the table);

• Attachment 3 provides charge information by month for (Item B); and • Attachments 4-13 provides charge information by month for Items C through L

Response to (b): All of the charges/activities identified in Table 2 and the supporting attachments (Attachments 2 to 13) are attributable to the siting and permitting of CCRP. The preferred “site” for CCRP and the permits expected to be required for it never changed from the project’s inception until it was subsumed into the Greater Hartford Central Connecticut Reliability Project (“GHCC”) 115-kV projects. However, various alternative routes and variations, including an all underground route, were necessarily investigated. The preferred site for the 345-kV CCRP transmission line was an approximately 37 mile long right-of-way between CL&P’s Frost Bridge Substation in Watertown, CT and its North Bloomfield Substation in Bloomfield, CT. The principal permits expected to be required were a certificate of environmental compatibility and public need from the Connecticut Siting Council and a Section 404 permit from the United States Army Corps of

10 In Attachment 2, Eversource is providing charge information for the CCRP-related siting and

permitting work for its internal employees on monthly basis for comparability with other data. Eversource notes that its employees are paid on a bi-weekly basis.

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 8 of 20

Engineers. The need for which CCRP was originally designed (increasing transfer capacity from east to west across the Western Connecticut Import Interface) will be addressed by a proposed underground line between two different substations (Newington and Southwest Hartford). This is the GHCC 115-kV project, which is still in development. However, another 115-kV overhead transmission line project in the Greater Hartford suite of 115-kV projects is proposed to be constructed on a 10.4 mile segment of the right-of-way previously designated for CCRP. This is the Frost Bridge to Campville project, for which a Siting Council application was filed in December 2015. The same major permits will be required for this project as would have been required for CCRP.11 Some of the environmental analyses of the preferred route, as well as many of the outreach efforts undertaken for CCRP have been useful in composing and prosecuting the Frost Bridge to Campville siting and permitting applications. The segment of right-of-way on which the Frost Bridge to Campville line is proposed to be built traverses four of the eight towns that would have been hosts to the CCRP line (Watertown, Thomaston, Harwinton, and Litchfield). Below Eversource provides a more detailed discussion of each category of activities/charges incurred in connection with the siting and permitting of CCRP.12 A. Siting and Permitting Support - Eversource Internal Labor $445,104

Eversource employees and personnel worked on a number of activities relating to the siting/permitting of CCRP, including the following activities, which were required as part of the state and local regulatory proceedings and permitting processes for CCRP:

1. Alternatives route analysis a. Environmental feasibility and characterization for comparison of all potential

alternatives was performed. In the evaluation of project alternatives, it was necessary to evaluate each alternative based upon its environmental impacts in order to provide insight into the feasibility, potential siting and permitting risks, and benefits of the project in relation to other alternatives.

2. Development of Municipal Consultation Filing (“MCF”)

11 As explained further in the Mr. Boguslawski’s testimony, ISO-NE approved the NEEWS

Project under Section I.3.9 of the ISO-NE Tariff in September 2008; subsequent to this approval, ISO-NE re-evaluated the reliability needs for the NEEWS components to reflect changes in system conditions. See Boguslawski (Exhibit No. EE-100) at 3-4;15-20.

12 In his testimony, Mr. Boguslawski describes the circumstances surrounding the development and evolution of CCRP as one originally designed component of an overall integrated transmission project that was redesigned and subsumed into a successor transmission project. See Exhibit No. EE-100 at 2-5. Mr. Boguslawski also explains that based upon the circumstances surrounding CCRP, it would be reasonable and appropriate to recover the CCRP costs as part of the NEEWS Project, rather than part of the new GHCC project. As Mr. Boguslawski explains, the new GHCC project was not proposed as a transmission project until July 2014 and did not receive Section I.3.9 approval from ISO-NE until April 16, 2015. Id. 33-34.

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 9 of 20

a. Once Eversource selected the preferred alternative routes for the project, Eversource developed the MCF, which was required as part of the state siting process for CCRP. The MCF content and volume is very similar to the actual siting filing and is used to help explain the project to the affected municipalities. The development of the MCF included environmental field work, such as wetlands flagging and characterization, and quantifying and minimizing impacts to resource areas. This also included the drafting and review of the MCF documents. After completing the filing, public outreach is conducted (see item 5, below), in the form of delivering and explaining the MCF to the affected municipalities and later receiving informed comments and input from the affected municipalities. This input is then considered in the finalization of the siting filing.

3. Work Activities related to the pre-filing of the siting application and preparation of the application included:

i. Preparation for and presentation to the Local Inland Wetland Commission for Locational Review.

ii. Connecticut Department of Environmental Protection Natural Diversity Database (Threatened and Endangered species) consultation and review

iii. Development of the Connecticut Siting Council application, including the solutions report.

4. Army Corps of Engineers Permit application a. An Army Corps of Engineers (“ACOE”) permit is a lengthy, involved process

(typically 12-18 months) and requires an intensive amount of investigation and documentation to be prepared in advance of a filing. Work began on this regulatory filing immediately after Eversource identified a preferred solution for CCRP, and the CCRP team advanced several of the efforts required to support an ACOE permit application, including but not limited to:

i. Phase 1 Environmental Assessment (Hazardous material investigation); ii. Phase 1 cultural resource review; and

iii. U.S. Fish and Wildlife preparation and consultation

5. Public outreach and education efforts relating to CCRP a. As a state regulated utility, Eversource engages in public outreach and education

activities at the outset of every major utility project, including transmission projects. Such public outreach and education, including the municipal consultation process, is not only required under Connecticut laws as part of the siting process, but is also important to maintain Eversource’s standing in the communities we serve, and is good corporate stewardship. Public outreach and education includes the pre-siting efforts that inform and educate landowners and homeowners who may be impacted by the project, as well as the various stakeholders (municipalities, communities, businesses, local organizations, and environmental groups). This public outreach and education process is essential to

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 10 of 20

alleviate concerns, answer questions, and address solutions that are related to transmission siting. The specific public outreach and education activities, including the municipal consultation process, that were performed in connection with CCRP are discussed further in the response to Question No. 4. As explained in the Response to Question No. 4, none of the costs that are included as part of the CCRP public outreach and education efforts are costs that related to lobbying activities or to influence public officials with respect to the siting/permitting of CCRP.

B. Siting and Permitting Support - $2,528,863

Due to the large size and scope of the NEEWS Project, including CCRP, it was necessary for Eversource to retain outside support to augment its internal staff to ensure compliance with regulatory filings in accordance with the required project schedule. Eversource retained

, a well-recognized fully integrated engineering, architecture, construction, environmental, and consulting firm that provides consulting services relating to, among other things, transmission construction. was engaged to provide expertise and resources in several project areas, including the siting and permitting of the NEEWS Project, including CCRP. personnel provided support and assistance with respect to the siting/permitting work activities performed by Eversource’ employees, as discussed above. Individuals at involved in the siting and permitting activities had their time and charges allocated to the appropriate category of costs, but not to specific tasks or activities within those categories. C. Environmental Feasibility Study of Routes - $42,685

performed a high-level analysis and comparison of the environmental aspects of the various NEEWS Project routes, and associated mapping of the routes. This work provided the basis for performing a quantitative and qualitative comparison of the possible routes to facilitate the selection of feasible and preferred routes. D. LIDAR Survey - $4,909

performed a laser based light detection and ranging (“LIDAR”) survey

of the proposed CCRP route, providing a topographical survey with input on terrain and vegetation along the project corridor, which assisted Eversource’s efforts in designing the transmission line. E. NEEWS Assumptions Analysis - $21,960 Eversource retained an internationally recognized expert in bulk power reliability, to review the assumptions that were used in the planning and development of NEEWS, including CCRP. Mr. Loehr also advised Eversource as to the reliability standards and

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 11 of 20

criteria of North American Electric Reliability, Northeast Power Coordinating Council, and ISO-NE. F. Project Environmental Plans Development - $3,185 Eversource retained an environmental and infrastructure consulting, to develop several plans for the NEEWS Project, including an environmental sampling plan, material (contaminated soil and water) handling guideline, and an execution plan. G. Video Broadcast Services - $718 The NEEWS Project siting work required the assistance of various video services, including recording project information videos for the open houses, which were conducted as part of Eversource’s public outreach and education efforts. H. NEEWS Economic Assessment - $1,932

worked with the NEEWS Project team as an independent economist responsible for reviewing the economic models and job analysis projections for the NEEWS Project. I. NEEWS Brochure - $1,771 The was hired to assist in developing all NEEWS information brochures, mapping, and handouts as part of Eversource’s public outreach and education efforts.

J. NEEWS Information Kiosks for Permitting and Outreach - $5,507

The NEEWS Project team developed kiosks for the open houses related to the NEEWS Project, including CCRP, that were subject specific (i.e., EMF, engineering, vegetation management).

, an exhibit company, designed and constructed the kiosks that were used during the NEEWS open house events. The charges for this vendor and allocated to CCRP were primarily associated with the storage fees and that were incurred for the time between open house events.

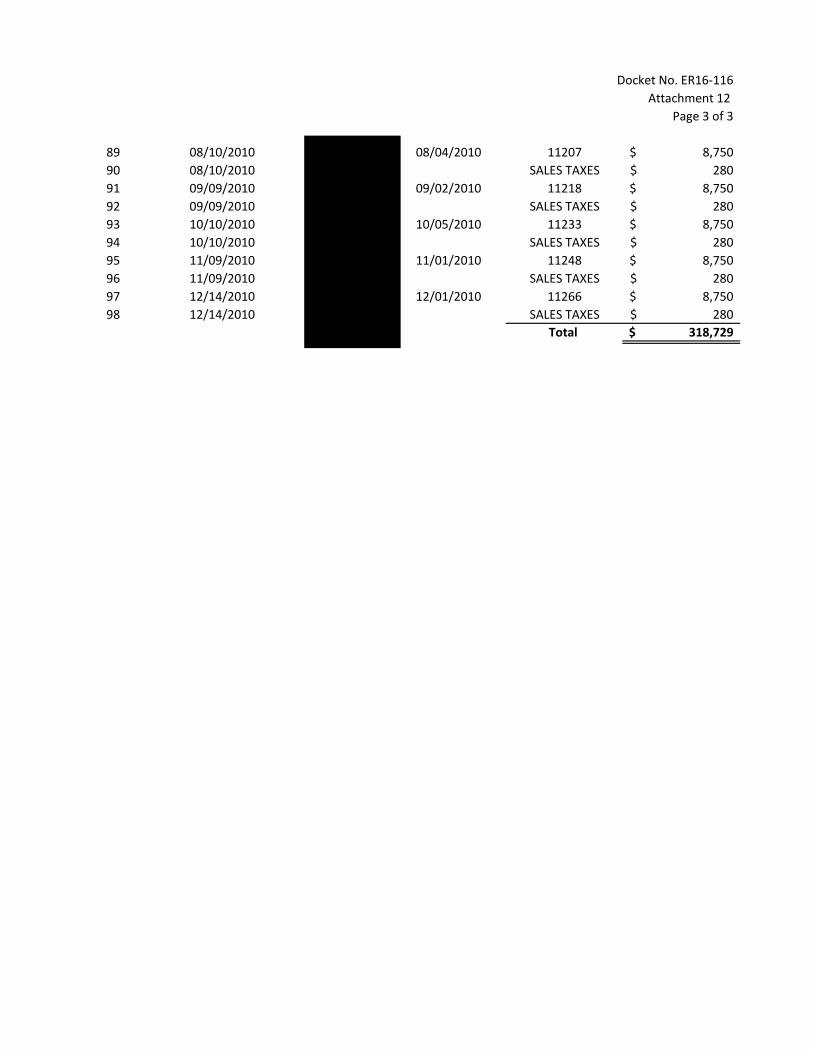

K. Communication Plans and Public Outreach Strategy – $318,729

Eversource retained , a public relations and strategic communications firm, to assist in the development of NEEWS communications plans, stakeholder identification, and public outreach and education. Specifically, this firm was retained to assist in organizing, managing, supporting and executing communications with key

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 12 of 20

stakeholders in support of the overall NEEWS Project, including CCRP. The services that this firm provided to CCRP are discussed further in the Response to subpart (d) to Question 4.

L. Meals - $24 Eversource’s records show that in November 2010, there was a charge of $24 for food service from the on-site cafeteria at Eversource’s Berlin, CT facility.

M. Work order adjustments In 2008, there was a net credit in the amount of $7,435 in the CCRP work order, and in 2009, a credit in the amount of $1,527 was recorded to the CCRP work order. It appears that both credits belong to Eversource’s three NEEWS components, not just CCRP. Eversource is researching both issues and will adjust the CCRP work order, as appropriate. Response to (c): All of the charges included in Table 2 were directly related to CCRP – i.e., they were charges incurred by CL&P to plan and develop the original design of CCRP as part of the costs of the overall NEEWS Project. Even those charges that were common to the NEEWS components (i.e., referred to as “NEEWS Programmatic Costs” in the filing and explained further in Mr. Case’s testimony), and allocated to CCRP, were directly related to CCRP because those common efforts/activities allowed CCRP (and the other NEEWS components) to benefit from the prior and shared experience, lessons learned and work efforts. This resulted in more efficient and streamlined process and quicker resolution of issues related to the NEEWS Project, including CCRP. These are appropriate capital costs for CCRP and were not written off to expense. In addition, to ensure costs are tracked and recorded accurately, Eversource project managers, cost analysts and contract administrators reviewed timesheets, invoices and schedules and budgets regularly to ensure proper charging as part of Eversource’s accounting process.

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 13 of 20

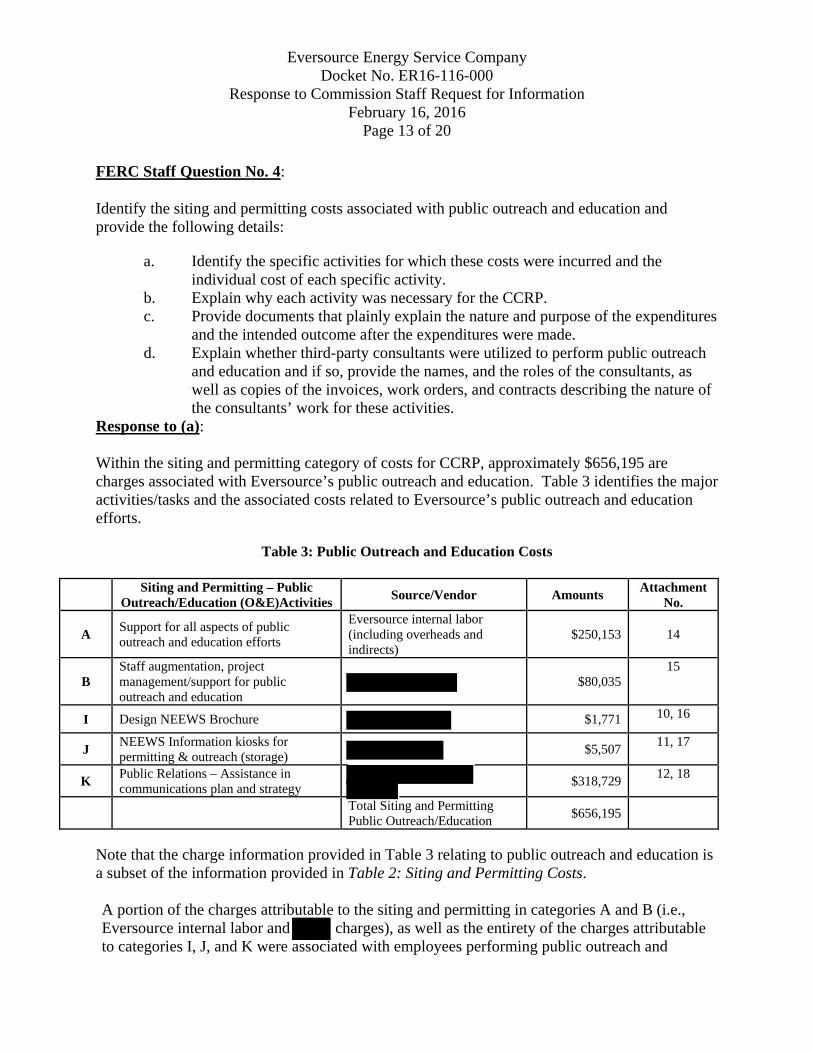

FERC Staff Question No. 4:

Identify the siting and permitting costs associated with public outreach and education and provide the following details:

a. Identify the specific activities for which these costs were incurred and the individual cost of each specific activity.

b. Explain why each activity was necessary for the CCRP. c. Provide documents that plainly explain the nature and purpose of the expenditures

and the intended outcome after the expenditures were made. d. Explain whether third-party consultants were utilized to perform public outreach

and education and if so, provide the names, and the roles of the consultants, as well as copies of the invoices, work orders, and contracts describing the nature of the consultants’ work for these activities.

Response to (a): Within the siting and permitting category of costs for CCRP, approximately $656,195 are charges associated with Eversource’s public outreach and education. Table 3 identifies the major activities/tasks and the associated costs related to Eversource’s public outreach and education efforts.

Table 3: Public Outreach and Education Costs

Siting and Permitting – Public

Outreach/Education (O&E)Activities Source/Vendor Amounts

Attachment No.

A Support for all aspects of public outreach and education efforts

Eversource internal labor (including overheads and indirects)

$250,153

14

B Staff augmentation, project management/support for public outreach and education

$80,035 15

I Design NEEWS Brochure $1,771 10, 16

J NEEWS Information kiosks for permitting & outreach (storage)

$5,507 11, 17

K Public Relations – Assistance in communications plan and strategy

$318,729 12, 18

Total Siting and Permitting Public Outreach/Education

$656,195

Note that the charge information provided in Table 3 relating to public outreach and education is a subset of the information provided in Table 2: Siting and Permitting Costs.

A portion of the charges attributable to the siting and permitting in categories A and B (i.e., Eversource internal labor and charges), as well as the entirety of the charges attributable to categories I, J, and K were associated with employees performing public outreach and

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 14 of 20

education functions. The major public outreach and education activities related to NEEWS, including CCRP, are set forth below:

• Developed proactive public outreach and education plans for various issues pertaining to the following:

• Stakeholder identification • Business interruption/coordination, including farmland and

crop loss • Landowner Issues, such as easement acquisition, right of way

encroachment reviews and removals, planning for landowner wood retention from clearing activities, and access roads.

• Construction protocols, such as vegetation and clearing activities.

• Parks and trails and public recreation areas

• Established and monitored the NEEWS Project communication tools, such as:

• A dedicated Project Hotline and email link from the website to facilitate inquiries from stakeholders, with a targeted response time of 24 hours or the next business day

• A comprehensive project website (www.NEEWSprojects.com)

• NEEWS informational brochures

• Consultation meetings with municipal officials

• As discussed further below, Eversource was required under Connecticut law (Conn. Gen. Stat. § 16-50l (e)) to consult with the municipality in which the transmission project is proposed to be located and with others affected at least sixty days prior to the filing of a siting application with the Connecticut Siting Council.

• Develop and staff public open houses

• NEEWS information kiosks

In connection with Commission Staff’s question for the costs of individual activities, Eversource’s employees who worked on public outreach and education activities relating to the

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 15 of 20

NEEWS Project, including CCRP, did not keep track of their time based upon specific work activities, but charged their time to a CCRP work order.13

In addition to Eversource’s internal labor, Eversource also retained third party consultants, as identified in Table 3, and the public outreach and education related services that they provided are discussed further below and in the Response to Question No. 3.

Response to (b): The major activities identified in Table 3 above are related to Eversource’s public outreach and education activities as part of Eversource’s effort to site and permit the NEEWS Project, including CCRP. In the 2008 order granting NEEWS transmission incentives under Order No. 679, the Commission recognized the significant risks that the NEEWS Project faced, including “multiple regulatory risks associated with siting and permitting authorization, as well as public opposition to the routing of the Project components.”14 To mitigate these risks, it was necessary for Eversource to have an effective public outreach and education program in place for the suite NEEWS Projects, including CCRP, to communicate and provide relevant information related to the NEEWS Project to the public and affected stakeholders in New England, including Eversource’s customers, affected towns and municipalities, homeowners and residents, neighboring utilities, businesses, organizations, community groups and federal and state regulators.

Unlike a newly-created, stand-alone entity that seeks to develop a proposed transmission project (such as a Transco), CL&P is a state regulated utility, and along with its other operating company affiliates, has been providing electric distribution and transmission service to customers in New England for many decades. As existing regulated utilities providing reliable electric services to the public, regulatory obligations and good corporate stewardship requires frequent and comprehensive education and dialogue with customers, regulators and other interested entities. As the Commission recognizes, building new transmission facilities faces a host of complex challenges, and siting of transmission cannot be conducted efficiently or timely without such extensive outreach and communication. Eversource has successfully used this outreach process to build some of the most challenging regionally-needed transmission reliability projects in New England.

13 See Case Testimony (Exhibit No. EE-200) at 17-18 (describing that Eversource tracks and

record NEEWS costs on a component-by-component basis and that CCRP, like other project components, was assigned a specific project number that served as the “parent” work order number and there were several other sub work orders that rolled up to the CCRP parent project number).

14 See Northeast Utilities Service Co., 125 FERC ¶ 61,183 P 31 (2008) (“2008 NEEWS Incentive Order”), rehearing denied, 135 FERC ¶ 61,270 (2011).

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 16 of 20

Not only were Eversource’s public outreach and education efforts important for good corporate stewardship purposes, they were also required under Connecticut laws. Specifically, related to its siting application process, under a Connecticut siting laws, Eversource was required to engage in a municipal consultation process prior to submitting its siting application with the Connecticut Siting Council and other state and local agencies.15 Specifically, Connecticut General Statutes § 16-50l (e) provides as follows:

… at least sixty days prior to the filing of an application with the council, the applicant shall consult with the municipality in which the facility may be located and with any other municipality required to be served with a copy of the application under subdivision (1) of subsection (b) of this section [any adjoining municipality having a boundary not more than 2500 feet from such facility] concerning the proposed and alternative sites of the facility… Such consultation with the municipality shall include, but not be limited to good faith efforts to meet with the chief elected official of the municipality. At the time of the consultation, the applicant shall provide the chief elected official with any technical reports concerning the public need, the site selection process and the environmental effects of the proposed facility.

Once the required initial contact with the municipal chief elected official is made, the town typically requests broader official consultations and presentations to the public. Thus, in connection with the municipal consultation requirement discussed above, Eversource held informational and briefing meetings with municipal officials in the affected municipalities and towns in Connecticut. Several of these meetings were public Board of Selectmen meetings. Eversource’s records indicate that the NEEWS Project team had the following meetings with Connecticut municipalities and towns specific to CCRP:

• Watertown on January 29, 2009 and October 8, 2009;

• Thomaston on April 1, 2009 and September 1, 2009;

• Simsbury on April 2, 2009 and September 14, 2009;

• New Hartford on March 20, 2009;

• Litchfield on March 10, 2009 and August 18, 2009;

15 In the 2008 NEEWS Incentive Order, the Commission noted that this municipal consultation

process is designed to obtain input and comments from the public and government representatives in each of the Connecticut municipalities in which the preferred or alternative routes of the proposed project is located. See NEEWS 2008 Order at P 32.

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 17 of 20

• Harwinton on March 19, 2009 and August 19, 2009;

• Canton on January 29, 2009 and October 7, 2009; and

• Bloomfield on March 23, 2009.16

In these meetings, the NEEWS Project team typically provided an overview of the NEEWS Project, including CCRP, and the reliability need on the transmission system that the NEEWS Project and its components were designed to address, the proposed project scope, project benefits, and expected timeline. To provide Commission Staff information as to the purpose of these meetings, Attachment 19 contains a PowerPoint presentation dated October 8, 2009 that was used to provide a briefing to the Town Manager of the Town of Watertown. This presentation is consistent with the public outreach conducted in similar meetings with public and municipal officials. Eversource believes that its public outreach and education efforts were effective in informing and educating the public and stakeholders of the NEEWS Project, including CCRP, and was an important factor in the timely and cost-effective construction of a major transmission project that provides benefits to customers in New England. In particular, Eversource’s component projects of NEEWS that have been completed (the Greater Springfield Reliability Project (“GSRP”) and Interstate Reliability Project (“IRP”)) were completed and placed in service on or ahead of schedule, and on or under budget. Eversource believes that this was directly attributable to the effective public outreach and education efforts that Eversource undertook.

Response to (c) and (d): Table 3 identifies the third-party consultants who assisted Eversource with its public outreach and education efforts. A description of the services that these third-party consultants provided to Eversource is discussed below. In addition, Eversource is providing documents that further describe the scope of the consultants’ work, as well as related invoices with respect to the public outreach and education assistance provided to Eversource. Of the five third-party consultants identified in Table 3, the two principal firms that provided public outreach and education assistance to Eversource were: (1) ; and (2)

16 Citing to page 10 of John Case’s testimony (Exhibit No. EE-200), Commission Staff stated

Eversource had “19 meetings with town officials, by the project team.” At the referenced page, Mr. Case did not specify the number of meetings that Eversource had with town officials.

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 18 of 20

The public outreach and education services that agreed to provide to Eversource is set forth in the 2009 New England East-West Solution Project Execution Plan. This document sets forth all the various services that agreed to provide to Eversource, including public outreach and education services. The executive summary and relevant excerpts from the Project Execution Plan pertaining to public outreach and education services are attached in Attachment 20. In particular, the document noted the significant public opposition risks to a major transmission project such as the NEEWS Project and its components, and sets forth a comprehensive strategy to mitigate these risks through effective communications with stakeholders, including municipalities, residents, businesses, community-based organizations, through the various phases of siting and construction of the transmission project. The staff member who assisted Eversource’s public outreach and education efforts consisted of one person ( Public Relations Manager). provided input into Eversource’s public outreach and education plans and strategies that would eventually be responsible for executing during the project. provided public outreach and education related services between January 2009 and April 2011. Invoices associated with time for each of those months are identified and included in Attachment 21. The total costs allocated to the public outreach category reflect a combination of time/billable hours plus an allocated amount for overhead costs, such as general office charges.17

is a public relations firm with capabilities in brand management, media, public, municipal, government and investor relations. was hired to assist in the development of public outreach and education strategies and plans to communicate information on the NEEWS Project to potential project stakeholders. Specifically, helped to plan, organize, manage and support outreach activities with a particular focus on preparing for and successfully executing outreach associated with Connecticut’s mandatory MCF process. also provided support and assistance to the public outreach and education activities performed by Eversource’s employees, as discussed in the response to Question No. 4(a) above. did not engage in lobbying activities for the NEEWS Project or CCRP.18 The scope of public outreach and

17 See also note c of Attachment 3 (describing how the allocated portion was determined). 18 Consistent with the Commission’s Uniform System of Accounts, Eversource records lobbying

activities to FERC Account No. 426.4, which provides that lobbying activities consist of “expenditures for the purpose of influencing public opinion with respect to the election or appointment of public officials, referenda, legislation, or ordinances…or approval, modification, or revocation of franchisees; or for the purpose of influencing the decisions of public officials.” Eversource’s activities that fall into the scope of Account 426.4 were not charged to the NEEWS Project, including CCRP, but recorded to FERC Account 426.4 in accordance with the Commission’s rules, and not recovered in transmission rates.

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 19 of 20

education services provided by is set forth in Attachment 22.19

Two employees supported Eversource’s public outreach and education efforts: (1) ; and (2) were hired on a fixed-

price monthly amount, and all associated monthly invoices for their services charged to CCRP are provided in Attachment 18.

Other Vendors Who Provided Services Related to Public Outreach and Education The two other outside consultants provided assistance related to Eversource’s public outreach and education efforts: The activities/services provided by these vendors are described in the Response to Question No. 3. As explained, the services provided by these consultants were relatively limited in scope, such as the design of the NEEWS information brochures and NEEWS kiosks for open house events to inform and educate the public of the NEEWS Project, including CCRP. Copies of the invoices of these consultants are provided in Attachments 16-17.

19 The individuals at who were engaged by Eversource for the public outreach/education

efforts associated with the NEEWS Project are not the same individuals who work for the separately-incorporated lobbying branch of . While Eversource has engaged the lobbying branch of for lobbying support at the corporate level, the charges associated with those efforts are charged to separate purchase orders that are specifically excluded from any project costs.

Eversource Energy Service Company Docket No. ER16-116-000

Response to Commission Staff Request for Information February 16, 2016

Page 20 of 20

FERC Staff Question No. 5:

Eversource’s proposed revisions to Attachment F of the ISO New England Tariff do not reflect tariff revisions included in the currently effective version of Attachment F, which were accepted by the Commission in Docket No. ER15-1629-000, effective June 1, 2015. Eversource is directed to have ISO New England re-submit the proposed revisions to Attachment F of the ISO New England Tariff to recover the approximately $15.7 million in costs for the CCRP based on the current effective version of the ISO New England Tariff.

Response: As directed by Commission Staff, Eversource is re-submitting its proposed tariff revisions to Attachment F of the ISO New England Tariff (clean and redlined) using the currently effective version of Attachment F, which was accepted by the Commission in Docket No. ER15-1629, effective June 1, 2015.

ATTACHMENT F

ANNUAL TRANSMISSION REVENUE REQUIREMENTS

The Transmission Revenue Requirements for each PTO will reflect the PTO’s costs with respect to Pool

Supported PTF and the HTF, including costs attributable to those PTOs deemed to own or support PTF

pursuant to Section II.49 of the Tariff. The Transmission Revenue Requirements will be an annual

calculation based on the previous year’s calendar data as shown, in the case of PTOs that are subject to

the Commission’s jurisdiction, in the PTO’s FERC Form 1 report for that year; provided, however, that if

a PTO is deemed to own or support PTF pursuant to Section II.49 of the Tariff, such PTO may include

the costs as incurred by its Related Person for PTF facilities and Transmission Support Expenses as the

basis for establishing its initial and subsequent Annual Transmission Revenue Requirements, only until

such PTO has a full calendar year of cost data under its ownership. Such PTO’s costs will be determined

from FERC Form 1 data if available, or if not available, from other supporting data certified by an auditor

of the PTO or Related Person, and in a format comparable to that used to report such costs in FERC Form

1. Such costs shall be based on actual data in lieu of allocated data if specifically identified in the Form 1

report in accordance with the following formula and Schedule 12:

I. The Transmission Revenue Requirement shall equal the sum of the PTO’s (A) Return and

Associated Income Taxes, (B) Transmission Depreciation and Amortization Expense, (C)

Transmission Related Amortization of Loss on Reacquired Debt, (D) Transmission Related

Amortization of Investment Tax Credits, (E) Transmission Related Municipal Tax Expense, (F)

Transmission Related Payroll Tax Expense, (G) Transmission Operation and Maintenance

Expense, (H) Transmission Related Administrative and General Expense, (I) Transmission

Related Integrated Facilities Charges, minus (J) Transmission Support Revenue, plus (K)

Transmission Support Expense, plus (L) Transmission Related Expense from Generators, plus

(M) Transmission Related Taxes and Fees Charge, minus (N) Revenue for Short-Term service

under the OATT and (O) Transmission Rents Received from Electric Property.

The details for implementation of Attachment F, as well as the definitions of the terms used in the

Attachment F formula, shall be established in accordance with the Attachment F Implementation Rule

contained in this OATT.

ATTACHMENT F

IMPLEMENTATION RULE

This rule sets forth details with respect to the determination each year of the Transmission Revenue

Requirements for each PTO. Such Transmission Revenue Requirements shall reflect the PTO’s costs for

Pool Transmission Facilities (“PTF”) and the Highgate Transmission Facilities (“HTF”), including costs

attributable to those PTOs deemed to own or support PTF pursuant to Section II.49 of the Tariff. The

Transmission Revenue Requirements for each PTO will reflect the PTO’s costs with respect to Pool

Supported PTF and the HTF. The Transmission Revenue Requirements will be an annual calculation

based on the previous year’s calendar data as shown, in the case of PTOs which are subject to the

Commission’s jurisdiction, in the PTO’s FERC Form 1 report for that year; provided, however, that if a

PTO is deemed to own or support PTF, such PTO may include the costs as incurred by its Related Person

for PTF facilities and Transmission Support Expenses as the basis for establishing its initial and

subsequent Annual Transmission Revenue Requirements, only until such PTO has a full calendar year of

cost data under its ownership. Such PTO’s costs will be determined from FERC Form 1 data if available,

or if not available, from other supporting data certified by an auditor of the PTO or Related Person, and in

a format comparable to that used to report such costs in FERC Form 1. Such costs shall be based on

actual data in lieu of allocated data if specifically identified in the Form 1 report in accordance with the

following formula and Schedule 12. The HTF Transmission Revenue Requirements shall be subject to the

limitations of inclusion of such costs as set forth in Appendix B to this Attachment. The owners of the

HTF, or their designated agent, will submit the annual HTF Transmission Revenue Requirements

calculation based on the previous calendar year's cost data from their FERC Form 1 or equivalent

information from their official books and records, as appropriate.

The Post-96 Transmission Revenue Requirement for each PTO that is based on data for calendar year

2004 or later shall include an Incremental Return and Associated Income Taxes on the PTO's PTF

transmission plant investments included in the Regional System Plan and placed in-service on or after

January 1,2004 (such investments referred to herein as "Post-2003 PTF Investment"). The Incremental

Return and Associated Income Taxes for Post-2003 PTF Investment shall incorporate an incentive ROE

adder of 100 basis points for plant investment placed in service by December 31, 2008 or as otherwise

permitted in Docket Nos. ER04-157, et al. for any projects included in the RSP, and shall incorporate any

incentive ROE adder approved by the FERC under Order No. 679 for other plant investments (however;

the 125 basis point ROE incentive adder granted to NEEWS under Order No. 679 in Docket No. ER08-

1548 and the 50 basis point ROE incentive adder for RTO participation shall not apply to the costs related

to the Central Connecticut Reliability Project, consistent with FERC’s order) and for MPRP CWIP and

NEEWS CWIP. The total ROE for any project, including any authorized ROE incentives for Post-2003

PTF Investment and any other incentive ROE approved by FERC under Order No. 679 shall be capped by

the top of the applicable zone of reasonableness determined by FERC for the relevant period. The data

used in determining each PTO's Incremental Return and Associated Taxes for Post-2003 Investment shall

be based on actual data in lieu of allocated data if specifically identified in the PTO's accounting records.

The Post-1996 Pool PTF Rate, as calculated pursuant to Schedule 9, shall include for each PTO a

Forecasted Transmission Revenue Requirement calculated in accordance with Appendix C to this

Attachment F Implementation Rule. Additionally, the Pre-1997 and Post-1996 Pool PTF Rates shall

include an Annual True-up calculated in accordance with Appendix C to this Attachment F

Implementation Rule.

The PTOs shall make an annual informational filing on or before July 31 of each year showing the Pool

PTF Rate in effect for the period beginning June 1 of that year through May 31 of the subsequent

year.Further, the informational filing with respect to the determination of the Pool PTF Rate will include a

breakdown by PTO of the amount of the change in PTF and HTF investment during the prior year and the

PTF and HTF retirements or additions causing such change to beginning and end-of-year PTF balances

and HTF balances (although beginning-of-year PTF balances and HTF balances are not used in the

formula itself), and any additions to PTF and HTF, retirements of PTF and HTF, and reclassifications of

PTF and HTF during the year for each PTO. If there are any corrections made to the information reflected

in the informational filing after it has been submitted, the PTOs will file corrections to the informational

filing. At least forty-five days before the informational filing is made with the Commission, the PTOs

shall make available to Transmission Customers and any other interested parties a draft of the proposed

filing for review and comment prior to the filing by posting such draft on the ISO website. The filing of

the information filing does not re-open the formula rate set forth below for review, but rather is

contestable only with respect to the accuracy of the information contained in the informational filing.

The ISO shall have the discretion to conduct audits of such charges, with advisory Stakeholder input on

the scope of audit, including on any agreed-upon procedures to be used by the auditor. In this provision,

the term “agreed-upon procedures” shall have the meaning afforded to it by the American Institute of

Certified Public Accountants.

I. DEFINITIONS

Capitalized terms not otherwise defined in the Tariff and as used in this rule have the following

definitions:

A. ALLOCATION FACTORS

1. Transmission Wages and Salaries Allocation Factor shall equal the ratio of Transmission-

related direct wages and salaries including those of affiliated Companies to the PTO’s

total direct wages and salaries including those of the Affiliates’ Companies and excluding

administrative and general wages and salaries.

2. PTF/HTF Transmission Plant Allocation Factor shall equal the ratio of PTF/HTF

Transmission Plant to Total Investment in Transmission Plant, excluding capital leases in

the Phase I/II HVDC-TF (Phase I/II HVDC-TF Leases).

3. Plant Allocation Factor shall equal the ratio of the sum of Total Investment in

Transmission Plant, excluding Phase I/II HVDC-TF Leases, and Transmission Related

Intangible and General Plant to Total Plant in service excluding Phase I/II HVDC-TF

Leases.

B. TERMS

Administrative and General Expense shall equal the PTO’s expenses as recorded in FERC

Account Nos. 920-935, excluding FERC Account Nos. 924, 928 and 930.1.

Amortization of Loss on Reacquired Debt shall equal the PTO’s expenses as recorded in FERC

Account No. 428.1.

Amortization of Investment Tax Credits shall equal the PTO’s credits as recorded in FERC

Account No. 411.4.

Depreciation Expense for Transmission Plant shall equal the PTO’s transmission expenses as

recorded in FERC Account No. 403.

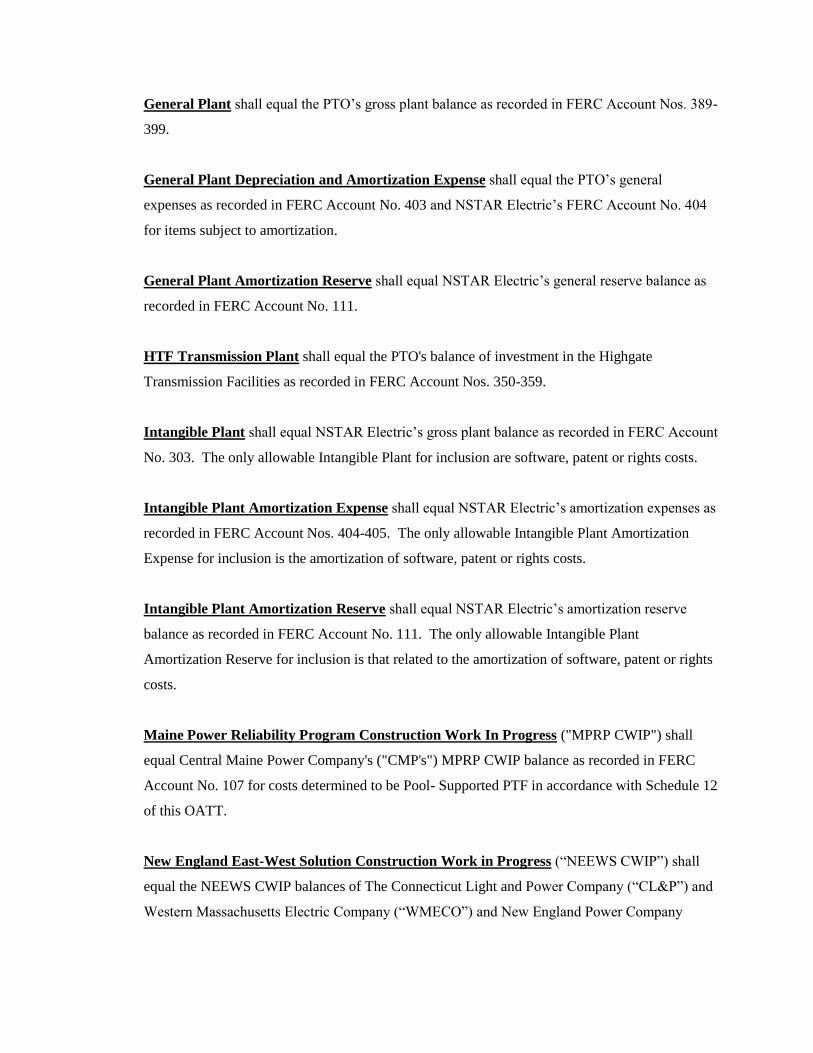

General Plant shall equal the PTO’s gross plant balance as recorded in FERC Account Nos. 389-

399.

General Plant Depreciation and Amortization Expense shall equal the PTO’s general

expenses as recorded in FERC Account No. 403 and NSTAR Electric’s FERC Account No. 404

for items subject to amortization.

General Plant Amortization Reserve shall equal NSTAR Electric’s general reserve balance as

recorded in FERC Account No. 111.

HTF Transmission Plant shall equal the PTO's balance of investment in the Highgate

Transmission Facilities as recorded in FERC Account Nos. 350-359.

Intangible Plant shall equal NSTAR Electric’s gross plant balance as recorded in FERC Account

No. 303. The only allowable Intangible Plant for inclusion are software, patent or rights costs.

Intangible Plant Amortization Expense shall equal NSTAR Electric’s amortization expenses as

recorded in FERC Account Nos. 404-405. The only allowable Intangible Plant Amortization

Expense for inclusion is the amortization of software, patent or rights costs.

Intangible Plant Amortization Reserve shall equal NSTAR Electric’s amortization reserve

balance as recorded in FERC Account No. 111. The only allowable Intangible Plant

Amortization Reserve for inclusion is that related to the amortization of software, patent or rights

costs.

Maine Power Reliability Program Construction Work In Progress ("MPRP CWIP") shall

equal Central Maine Power Company's ("CMP's") MPRP CWIP balance as recorded in FERC

Account No. 107 for costs determined to be Pool- Supported PTF in accordance with Schedule 12

of this OATT.

New England East-West Solution Construction Work in Progress (“NEEWS CWIP”) shall

equal the NEEWS CWIP balances of The Connecticut Light and Power Company (“CL&P”) and

Western Massachusetts Electric Company (“WMECO”) and New England Power Company

(“NEP”) as recorded in FERC Account No. 107 for costs determined to be Pool-Supported PTF

in accordance with Schedule 12 of this OATT.

Other Regulatory Assets/Liabilities - FAS 106 shall equal the net of the PTO's FAS 106

balance as recorded in FERC Account 182.3 and any FAS 106 balance as recorded in the PTO's

FERC Account No. 254.

Other Regulatory Assets/Liabilities - FAS 109 shall equal the net of the PTO's FAS 109

balance in FERC Account No. 182.3 and any FAS 109 balance as recorded in the PTO's FERC

Account No. 254.

Payroll Taxes shall equal those payroll expenses as recorded in the PTO's FERC Account Nos.

408.1.

Phase I/II HVDC-TF Leases shall equal the PTO's balance in capital leases as recorded in

FERC Account Nos. 350-359 and FERC Account Nos. 389-399.

Plant Held for Future Use shall equal the PTO's balance in FERC Account No.105.

Prepayments shall equal the PTO’s prepayment balance as recorded in FERC Account No. 165.

Property Insurance shall equal the PTO’s expenses as recorded in FERC Account No. 924.

PTF Transmission Plant shall equal the PTO’s transmission plant as defined in the Section II.49

of the OATT and determined in accordance with Appendix A of this Rule, which is entitled

“Rules for Determining Investment To be Included in PTF.”

PTF/HTF Transmission Plant Investment shall equal the PTO’s (a) PTF Transmission Plant

plus (b) HTF Transmission Plant.

Total Accumulated Deferred Income Taxes shall equal the net of the PTO’s deferred tax

balance as recorded in FERC Account Nos. 281-283 and the PTO’s deferred tax balance as

recorded in FERC Account No. 190.

Total Loss on Reacquired Debt shall equal the PTO’s expenses as recorded in FERC Account

189.

Total Municipal Tax Expense shall equal the PTO’s municipal tax expenses as recorded in

FERC Account Nos. 408.1.

Total Plant in Service shall equal the PTO’s total gross plant balance as recorded in FERC

Account Nos. 301-399.

Total Transmission Depreciation Reserve shall equal the PTO’s transmission reserve balance

as recorded in FERC Account 108.

Transmission Operation and Maintenance Expense shall equal the PTO’s expenses as

recorded in FERC Account Nos. 560, 561.5-561.8, 562-564 and 566-573, and shall exclude all

Phase I/II HVDC-TF expenses booked to accounts 560 through 573 and expenses already

included in Transmission Support Expense, as described in Section K which are included in

FERC Account Nos. 560-573.

Transmission Plant shall equal the PTO’s Gross Plant balance as recorded in FERC Account

Nos. 350-359.

Transmission Plant Materials and Supplies shall equal the PTO’s balance as assigned to

transmission, as recorded in FERC Account No. 154.

II. CALCULATION OF TRANSMISSION REVENUE REQUIREMENTS

The Transmission Revenue Requirement shall equal the sum of the PTO's (A) Return and Associated

Income Taxes (including the Incremental Return and Associated Income Taxes for Post-2003 PTF

Investment and for MPRP CWIP and NEEWS CWIP), (B) Transmission Depreciation and Amortization

Expense, (C) Transmission Related Amortization of Loss on Reacquired Debt, (D) Transmission Related

Amortization of Investment Tax Credits, (E) Transmission Related Municipal Tax Expense, (F)

Transmission Related Payroll Tax Expense, (G) Transmission Operation and Maintenance Expense, (H)

Transmission Related Administrative and General Expenses, (I) Transmission Related Integrated

Facilities Charges, minus (J) Transmission Support Revenue, plus (K) Transmission Support Expense,

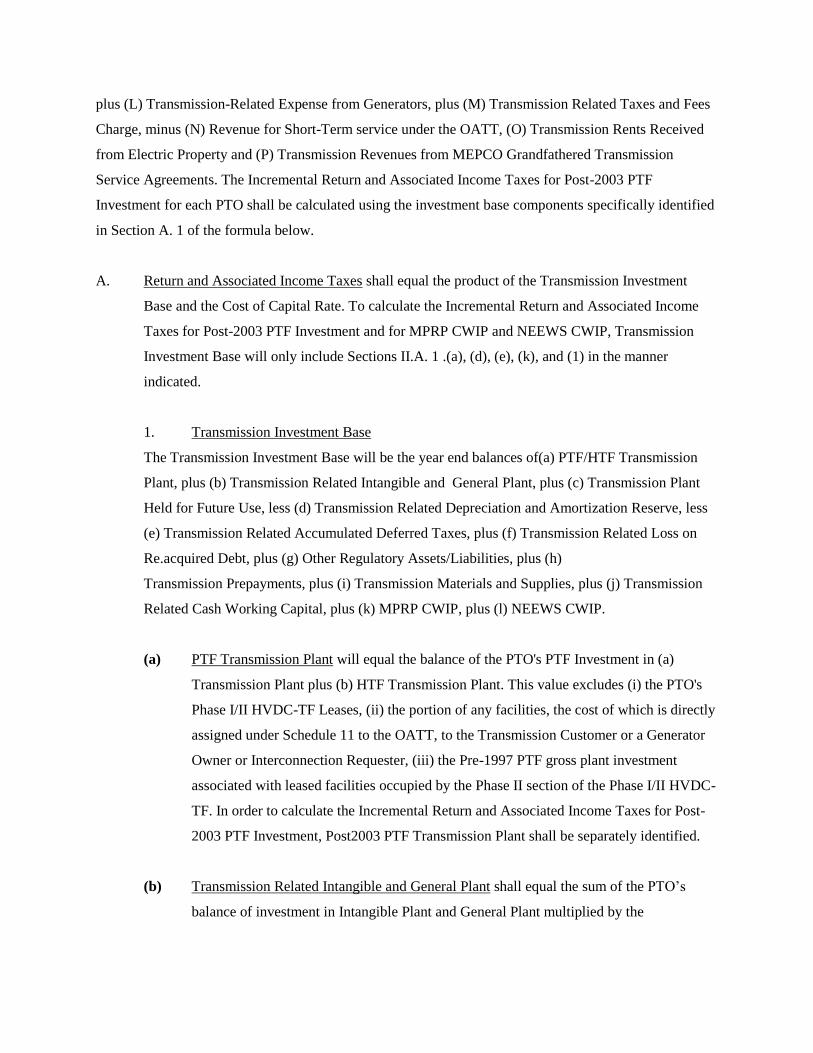

plus (L) Transmission-Related Expense from Generators, plus (M) Transmission Related Taxes and Fees

Charge, minus (N) Revenue for Short-Term service under the OATT, (O) Transmission Rents Received

from Electric Property and (P) Transmission Revenues from MEPCO Grandfathered Transmission

Service Agreements. The Incremental Return and Associated Income Taxes for Post-2003 PTF

Investment for each PTO shall be calculated using the investment base components specifically identified

in Section A. 1 of the formula below.

A. Return and Associated Income Taxes shall equal the product of the Transmission Investment

Base and the Cost of Capital Rate. To calculate the Incremental Return and Associated Income

Taxes for Post-2003 PTF Investment and for MPRP CWIP and NEEWS CWIP, Transmission

Investment Base will only include Sections II.A. 1 .(a), (d), (e), (k), and (1) in the manner

indicated.

1. Transmission Investment Base

The Transmission Investment Base will be the year end balances of(a) PTF/HTF Transmission

Plant, plus (b) Transmission Related Intangible and General Plant, plus (c) Transmission Plant

Held for Future Use, less (d) Transmission Related Depreciation and Amortization Reserve, less

(e) Transmission Related Accumulated Deferred Taxes, plus (f) Transmission Related Loss on

Re.acquired Debt, plus (g) Other Regulatory Assets/Liabilities, plus (h)

Transmission Prepayments, plus (i) Transmission Materials and Supplies, plus (j) Transmission

Related Cash Working Capital, plus (k) MPRP CWIP, plus (l) NEEWS CWIP.

(a) PTF Transmission Plant will equal the balance of the PTO's PTF Investment in (a)

Transmission Plant plus (b) HTF Transmission Plant. This value excludes (i) the PTO's

Phase I/II HVDC-TF Leases, (ii) the portion of any facilities, the cost of which is directly

assigned under Schedule 11 to the OATT, to the Transmission Customer or a Generator

Owner or Interconnection Requester, (iii) the Pre-1997 PTF gross plant investment

associated with leased facilities occupied by the Phase II section of the Phase I/II HVDC-

TF. In order to calculate the Incremental Return and Associated Income Taxes for Post-

2003 PTF Investment, Post2003 PTF Transmission Plant shall be separately identified.

(b) Transmission Related Intangible and General Plant shall equal the sum of the PTO’s

balance of investment in Intangible Plant and General Plant multiplied by the

Transmission Wages and Salaries Allocation Factor and the PTF/HTF Transmission Plant

Allocation Factor.

(c) Transmission Plant Held for Future Use shall equal the PTO’s balance of Transmission-

related Plant Held for Future Use multiplied by the PTF/HTF Transmission Plant

Allocation Factor.

(d) Transmission Related Depreciation and Amortization Reserve shall equal the PTO’s

balance of Total Transmission Depreciation Reserve, plus the balance of Transmission

Related Intangible Plant Amortization Reserve, Transmission Related General Plant

Depreciation Reserve and Transmission Related General Plant Amortization Reserve.

Transmission Related Intangible Plant Amortization Reserve, Transmission Related

General Plant Depreciation Reserve and Transmission Related General Plant

Amortization Reserve shall equal the product of the sum of Intangible Plant Amortization

Reserve, General Plant Depreciation Reserve and General Plant Amortization Reserve,

and the Transmission Wages and Salaries Allocation Factor. This sum shall be multiplied

by the PTF/HTF Transmission Plant Allocation Factor. In order to calculate the

Incremental Return and Associated Income Taxes for Post-2003 PTF Investment,

Transmission Depreciation Reserve associated with Post-2003 PTF Investment shall

equal the PTO’s balance of Total Transmission Depreciation Reserve multiplied by the

ratio of Post-2003 PTF Transmission Plant to Total Investment in Transmission Plant,

excluding capital leases in the Phase I/II HVDC-TF Leases.

(e) Transmission Related Accumulated Deferred Taxes shall equal the PTO’s electric

balance of Total Accumulated Deferred Income Taxes, multiplied by the Plant Allocation

Factor, further multiplied by the PTF/HTF Transmission Plant Allocation Factor. To

calculate the Incremental Return and Associated Income Taxes for Post-2003 PTF

Investment, Transmission Related Accumulated Deferred Income Taxes associated with

Post-2003 PTF Investment shall equal the PTO’s balance of total property-related

accumulated deferred income taxes as recorded in FERC accounts 281 and 282,

multiplied by the ratio of Total Investment in Transmission Plant, excluding Phase I/II

HVDC-TF Leases, to Total Plant in Service excluding Phase I/II HVDC-TF Leases,

further multiplied by the ratio of Post-2003 PTF Transmission Plant to Total Investment

in Transmission Plant, excluding Phase I/II HVDC-TF Leases.

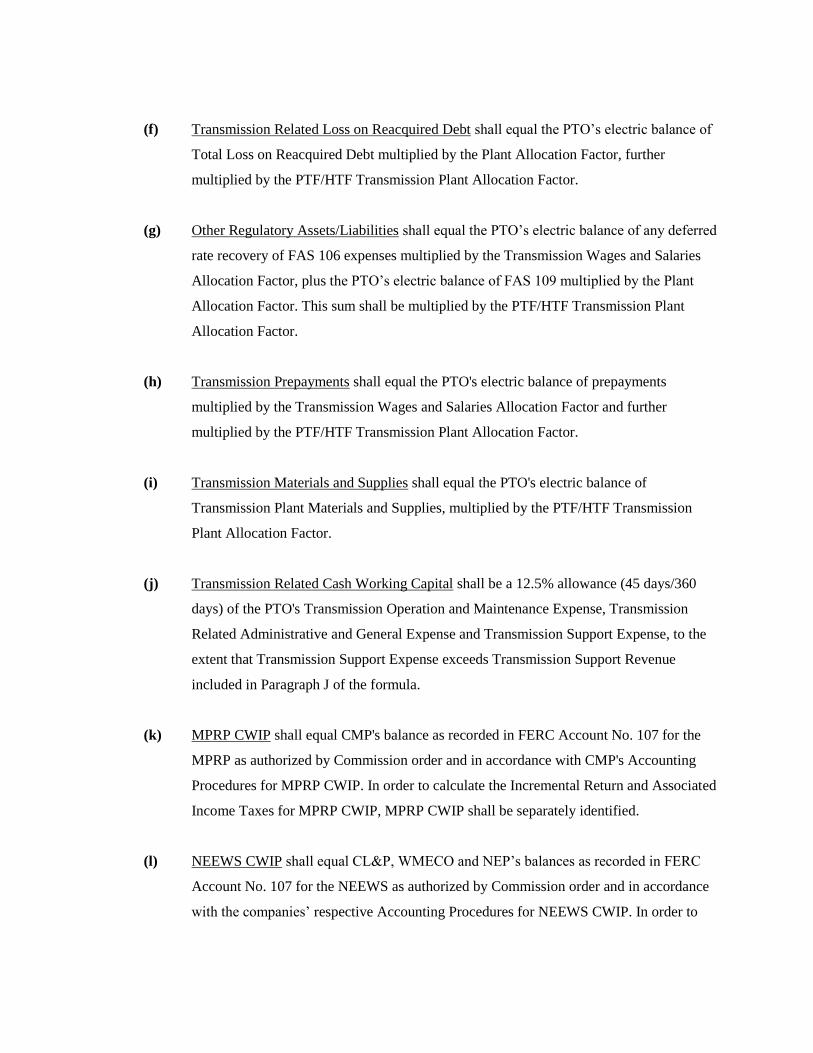

(f) Transmission Related Loss on Reacquired Debt shall equal the PTO’s electric balance of

Total Loss on Reacquired Debt multiplied by the Plant Allocation Factor, further

multiplied by the PTF/HTF Transmission Plant Allocation Factor.

(g) Other Regulatory Assets/Liabilities shall equal the PTO’s electric balance of any deferred

rate recovery of FAS 106 expenses multiplied by the Transmission Wages and Salaries

Allocation Factor, plus the PTO’s electric balance of FAS 109 multiplied by the Plant

Allocation Factor. This sum shall be multiplied by the PTF/HTF Transmission Plant

Allocation Factor.

(h) Transmission Prepayments shall equal the PTO's electric balance of prepayments

multiplied by the Transmission Wages and Salaries Allocation Factor and further

multiplied by the PTF/HTF Transmission Plant Allocation Factor.

(i) Transmission Materials and Supplies shall equal the PTO's electric balance of

Transmission Plant Materials and Supplies, multiplied by the PTF/HTF Transmission

Plant Allocation Factor.

(j) Transmission Related Cash Working Capital shall be a 12.5% allowance (45 days/360

days) of the PTO's Transmission Operation and Maintenance Expense, Transmission

Related Administrative and General Expense and Transmission Support Expense, to the

extent that Transmission Support Expense exceeds Transmission Support Revenue

included in Paragraph J of the formula.

(k) MPRP CWIP shall equal CMP's balance as recorded in FERC Account No. 107 for the

MPRP as authorized by Commission order and in accordance with CMP's Accounting

Procedures for MPRP CWIP. In order to calculate the Incremental Return and Associated

Income Taxes for MPRP CWIP, MPRP CWIP shall be separately identified.

(l) NEEWS CWIP shall equal CL&P, WMECO and NEP’s balances as recorded in FERC

Account No. 107 for the NEEWS as authorized by Commission order and in accordance

with the companies’ respective Accounting Procedures for NEEWS CWIP. In order to

calculate the Incremental Return and Associated Income Taxes for NEEWS CWIP,

NEEWS CWIP shall be separately identified.

2. Cost of Capital Rate

The Cost of Capital Rate will equal (a) the PTO's Weighted Cost of Capital, plus (b)

Federal Income Tax plus (e) State Income Tax.

(a) The Weighted Cost of Capital will be calculated based upon the capital structure at the

end of each year and will equal the sum of (i), (ii), and (iii) below. The Cost of Capital

Rate to be used in calculating the Incremental Return and Associated Income Taxes for

Post-2003 PTF Investment and for MPRP CWIP and NEEWS CWIP, shall only reflect

item (iii) below and shall apply in the manner indicated below.

(i) the long-term debt component, which equals the product of the actual weighted average

embedded cost to maturity of the PTO's long-term debt then outstanding and the ratio that

long-term debt is to the PTO's total capital.

(ii) the preferred stock component, which equals the product of the actual weighted average

embedded cost to maturity of the PTO's preferred stock then outstanding and the ratio

that preferred stock is to the PTO's total capital.

(iii) the return on equity component, shall be the product of the allowed ROE of the PTO's

common equity and the ratio that common equity is to the PTO's total capital. For pre-

1997 and post-1996 assets, the ROE is 11.07%. In order to calculate the Incremental

Return and Associated Income Taxes for Post-2003 PTF Investment and for MPRP

CWIP and NEEWS CWIP, the incremental return on equity shall be the product of: (1)

the PTO's incremental return on equity of 1.0% for plant investments associated with

projects included in the RSP and placed in service by December 31, 2008 or otherwise

permitted in Docket Nos. ER04-157, et al.; (2) any ROE incentive approved by the FERC

under Order No. 679 for other plant investments (however; the 125 basis point ROE