preprocessing techniques - mcmaster universitycs777/presentations/preprocessing.pdfxin huang ,...

TRANSCRIPT

Preprocessing Techniques

Nael El ShawwaOlesya PeshkoAlberto Olvera

Jonathan Li

Mathematical Programming System (MPS)

Named after an early IBM LP productEmerged as the defacto standard file formatVery old, based on a punch card systemColumn orientedFields start in columns 1, 5, 15, 25, 40 and 50Sections are marked by “header cards” which start in column 1

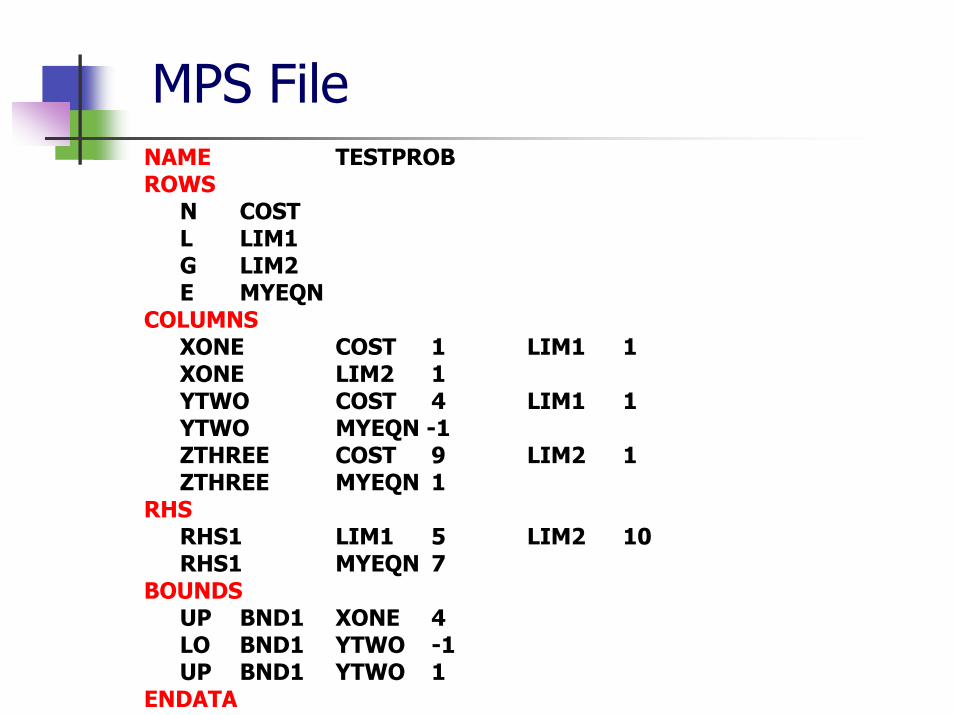

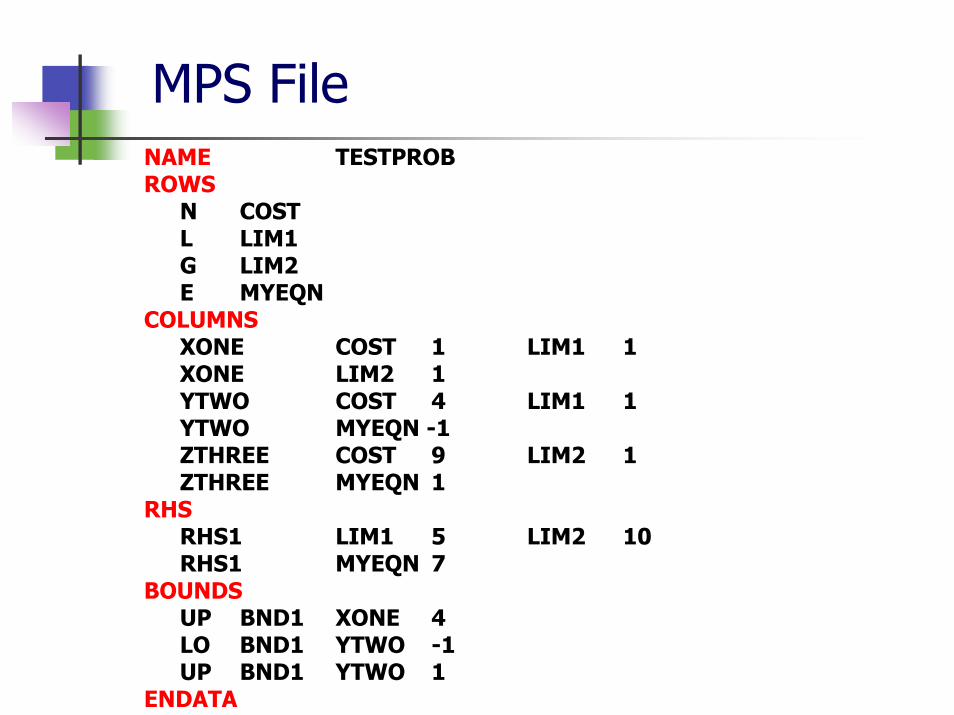

MPS FileNAME TESTPROB ROWS

N COST L LIM1 G LIM2 E MYEQN

COLUMNS XONE COST 1 LIM1 1 XONE LIM2 1 YTWO COST 4 LIM1 1 YTWO MYEQN -1 ZTHREE COST 9 LIM2 1 ZTHREE MYEQN 1

RHSRHS1 LIM1 5 LIM2 10 RHS1 MYEQN 7

BOUNDSUP BND1 XONE 4 LO BND1 YTWO -1 UP BND1 YTWO 1

ENDATA

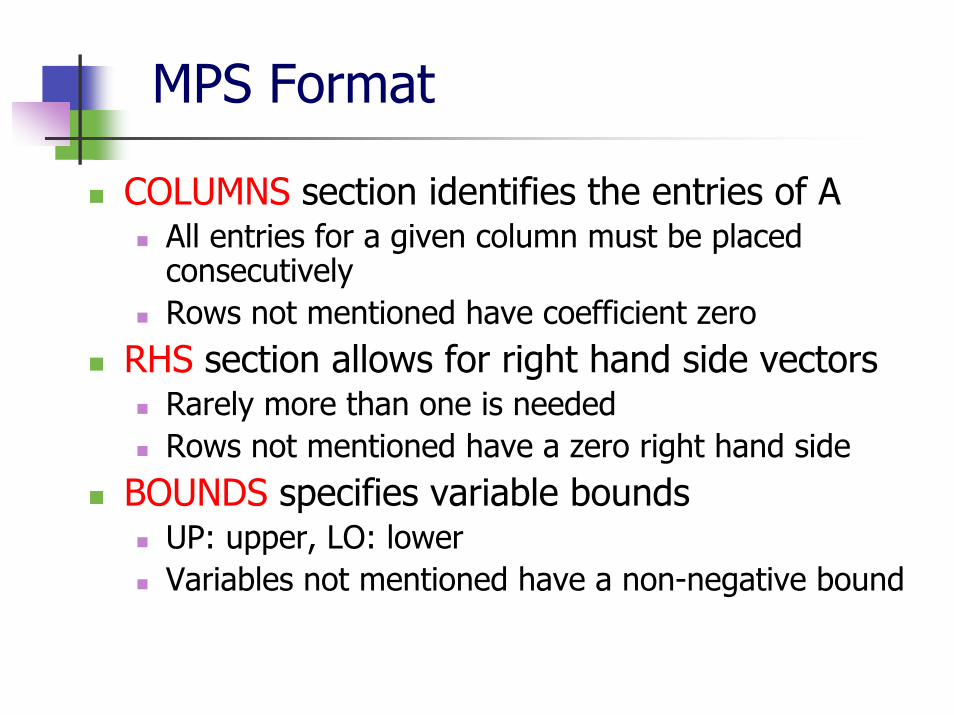

MPS Format

NAME record can have any value in column 15ROWS section identifies the names of constraints

E for equality rowsL for ≤ rowsG for ≥ rowsN for non-constraining rowsThe order is irrelevant

MPS Format

COLUMNS section identifies the entries of AAll entries for a given column must be placed consecutivelyRows not mentioned have coefficient zero

RHS section allows for right hand side vectorsRarely more than one is neededRows not mentioned have a zero right hand side

BOUNDS specifies variable boundsUP: upper, LO: lowerVariables not mentioned have a non-negative bound

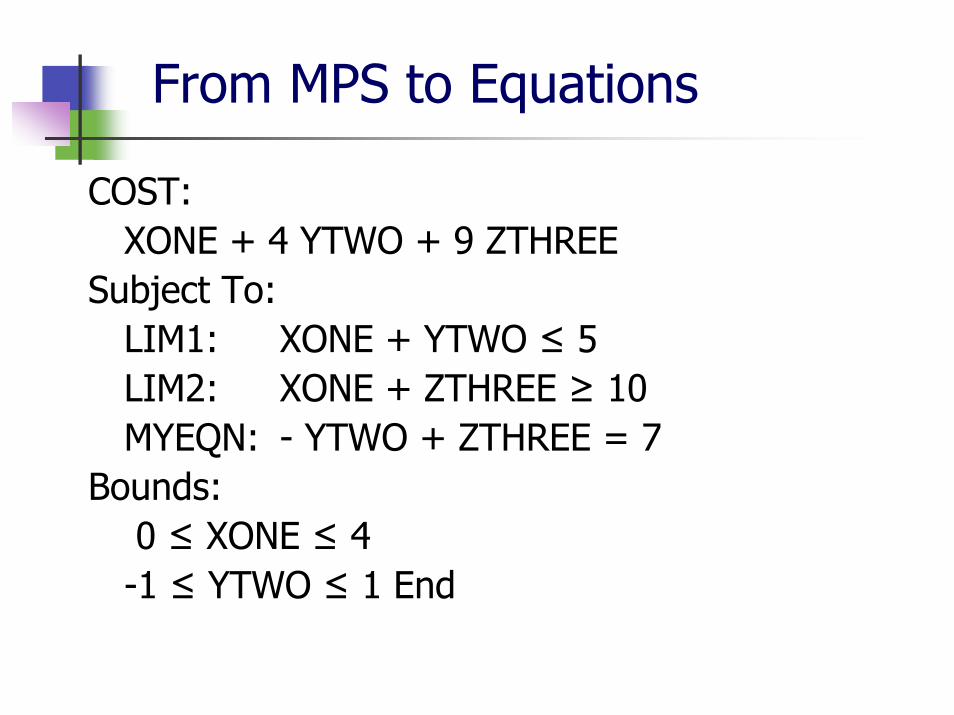

From MPS to Equations

COST: XONE + 4 YTWO + 9 ZTHREE

Subject To: LIM1: XONE + YTWO ≤ 5 LIM2: XONE + ZTHREE ≥ 10 MYEQN: - YTWO + ZTHREE = 7

Bounds: 0 ≤ XONE ≤ 4 -1 ≤ YTWO ≤ 1 End

MPS FileNAME TESTPROB ROWS

N COST L LIM1 G LIM2 E MYEQN

COLUMNS XONE COST 1 LIM1 1 XONE LIM2 1 YTWO COST 4 LIM1 1 YTWO MYEQN -1 ZTHREE COST 9 LIM2 1 ZTHREE MYEQN 1

RHSRHS1 LIM1 5 LIM2 10 RHS1 MYEQN 7

BOUNDSUP BND1 XONE 4 LO BND1 YTWO -1 UP BND1 YTWO 1

ENDATA

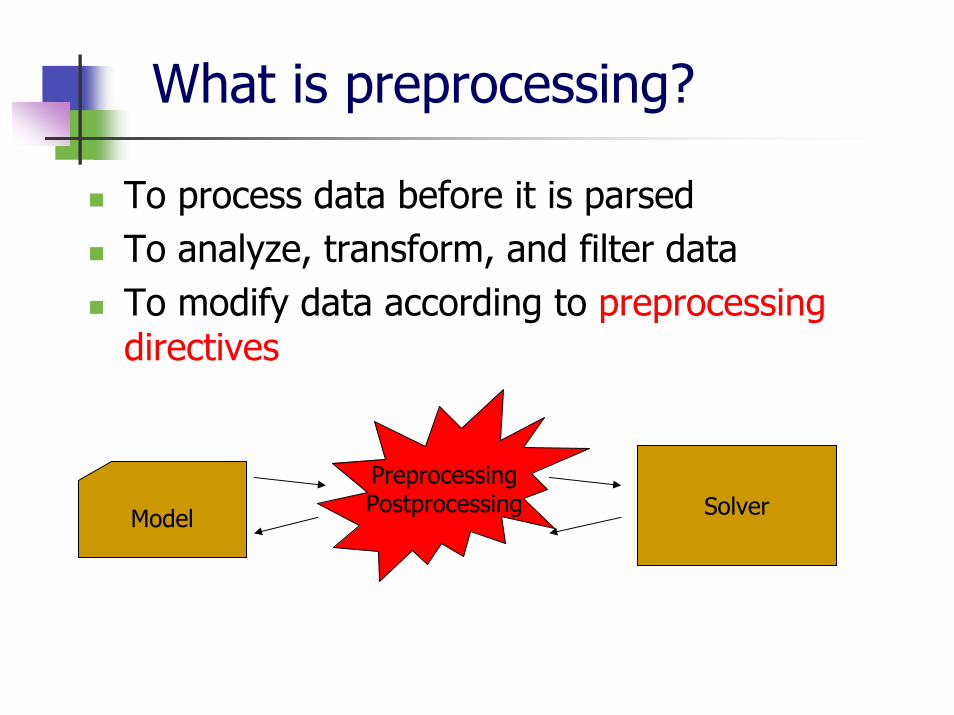

What is preprocessing?

To process data before it is parsedTo analyze, transform, and filter dataTo modify data according to preprocessing directives

Model

PreprocessingPostprocessing Solver

Why should it be done?

To simplify the problem, reduce sizeEliminate redundancy in variables/constraintsSatisfy solver limitations To avoid possible numerical pitfalls and improve numerical characteristicsAims to speed up solution and efficiency

Optimization in Preprocessing

“More extensive preprocessing does not necessarily imply faster overall solution

time. Since some preprocessing techniques are quite time consuming, we have to

balance the effect of the removed redundancies with the time spent in preprocessing”

Xin Huang , Preprocessing and Post-processing in Linear Optimization, M.Sc. Thesis McMaster University, June 2004

Optimization in Preprocessing

Hard to find the best balance between effects of preprocessing and time spent preprocessing

In practice only fast techniques are chosenExpensive techniques are frequently used as tools in very large scale problems

Who does it?

The solver?Hidden heuristics the modeling system is unaware of - possible pitfalls?Solver can take advantage of certain information

The modeling system?It is the modeling systems job to filter model data for the solver, the solver just solves it

My opinion…

Not everyone uses a modeling systemSome just pass data files to solvers

Everybody uses a solverThrough a modeling system or the solver interface

The solver developers know more about their own heuristics than the modeling system developers…

How can it be justified that preprocessing is the modeling system’s job?

Preprocessing Techniques

Basic TechniquesInfeasible variablesEmpty rows or columnsFixed variablesSingleton rows or columnsForcing constraintsDuplicate rows or columns

Preprocessing Techniques

Advanced TechniquesDominated variablesTightening boundsMake A sparserScaling

Basic Preprocessing Techniques

Olesya Peshko

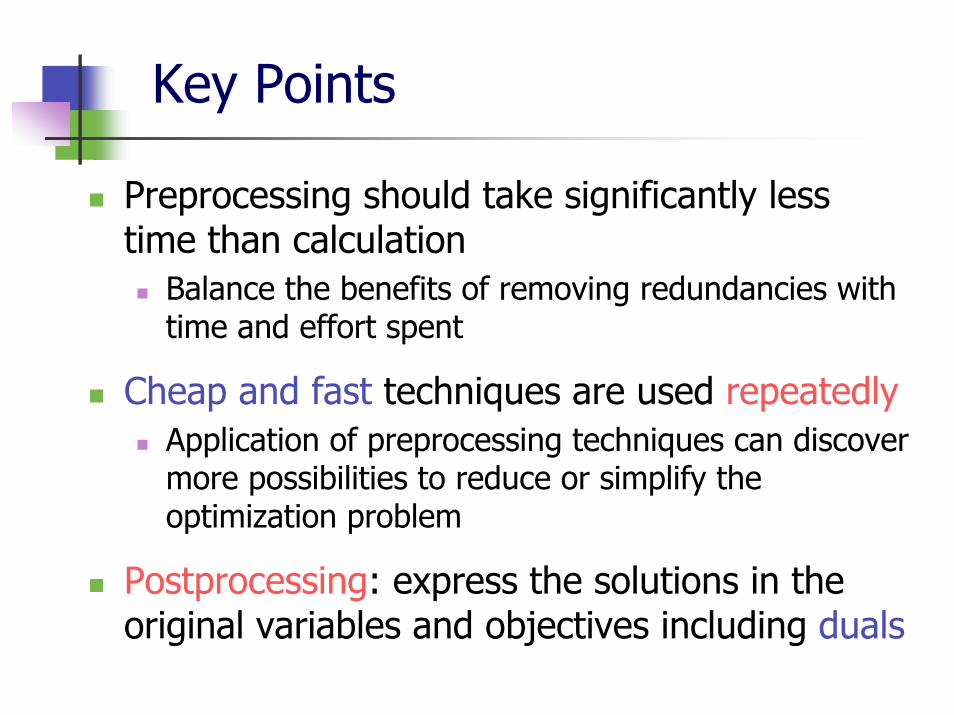

Key Points

Preprocessing should take significantly less time than calculation

Balance the benefits of removing redundancies with time and effort spent

Cheap and fast techniques are used repeatedlyApplication of preprocessing techniques can discover more possibilities to reduce or simplify the optimization problem

Postprocessing: express the solutions in the original variables and objectives including duals

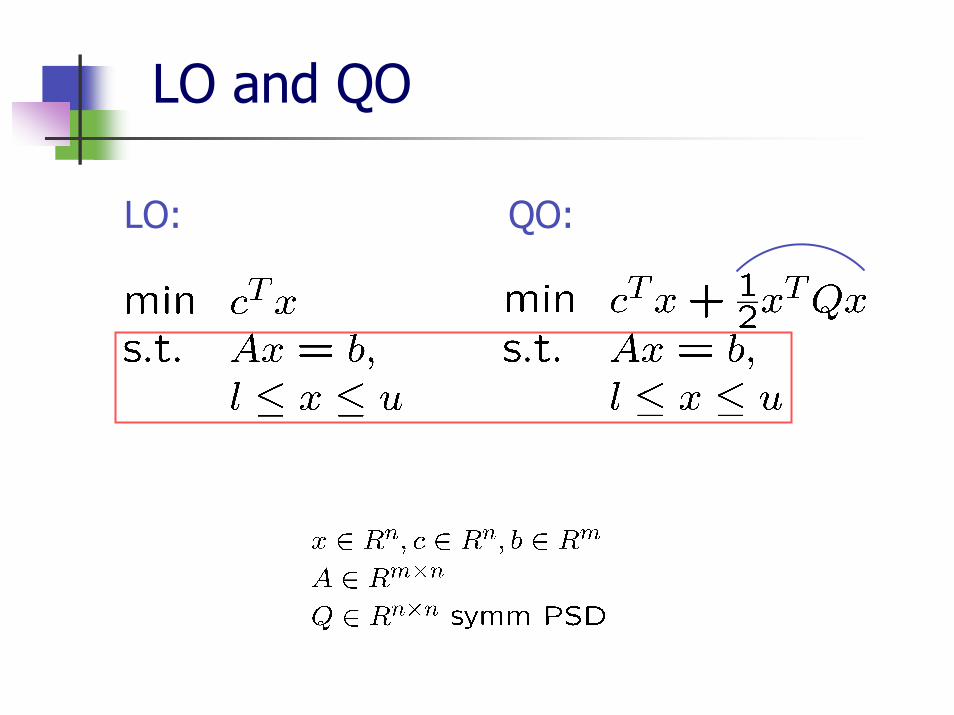

LO: QO:

LO and QO

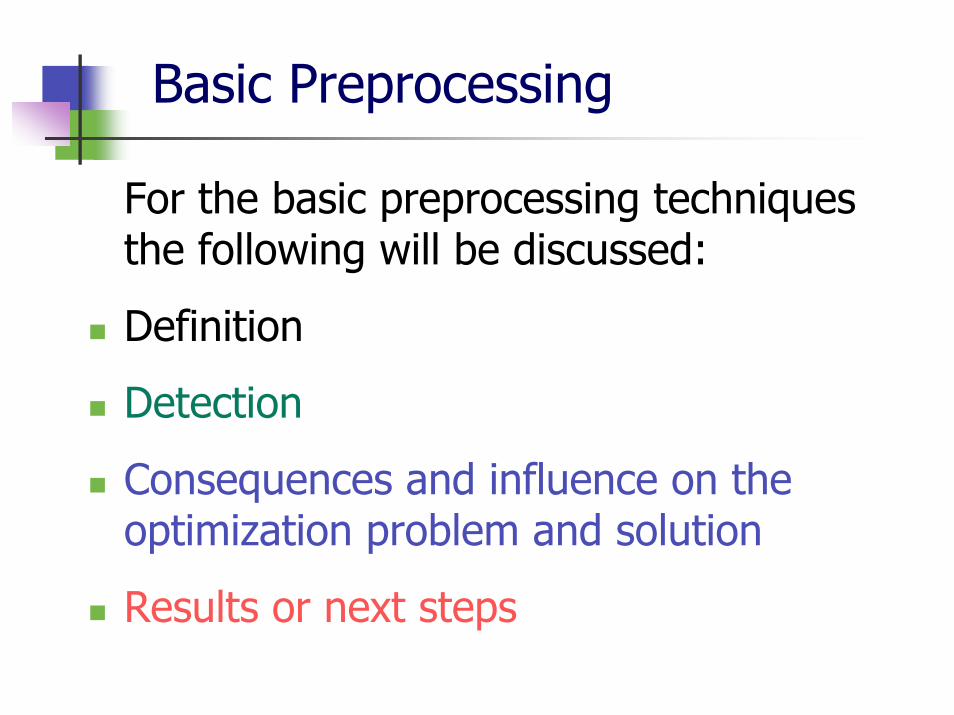

Basic Preprocessing

For the basic preprocessing techniques the following will be discussed:

Definition

Detection

Consequences and influence on the optimization problem and solution

Results or next steps

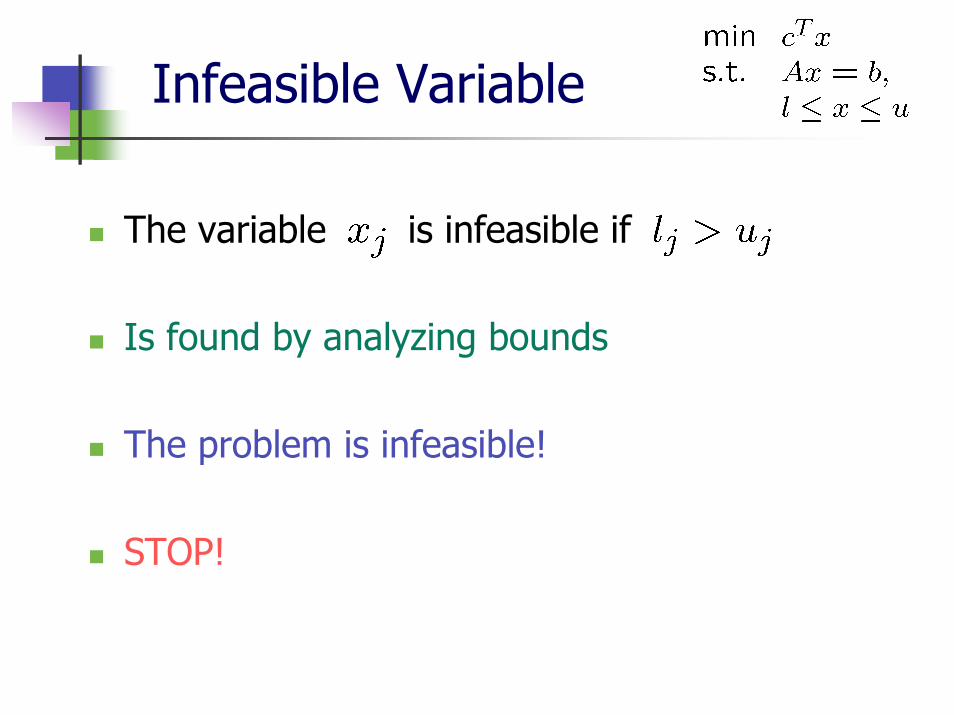

Infeasible Variable

The variable is infeasible if

Is found by analyzing bounds

The problem is infeasible!

STOP!

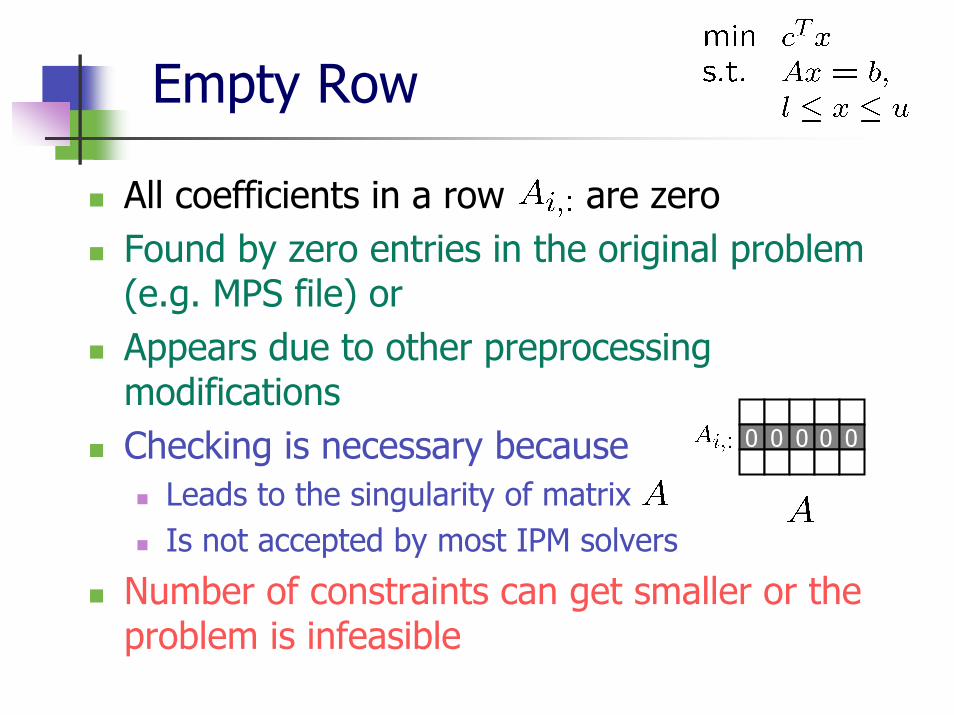

Empty Row

All coefficients in a row are zeroFound by zero entries in the original problem (e.g. MPS file) orAppears due to other preprocessing modificationsChecking is necessary because

Leads to the singularity of matrix Is not accepted by most IPM solvers

Number of constraints can get smaller or the problem is infeasible

0 0 0 0 0

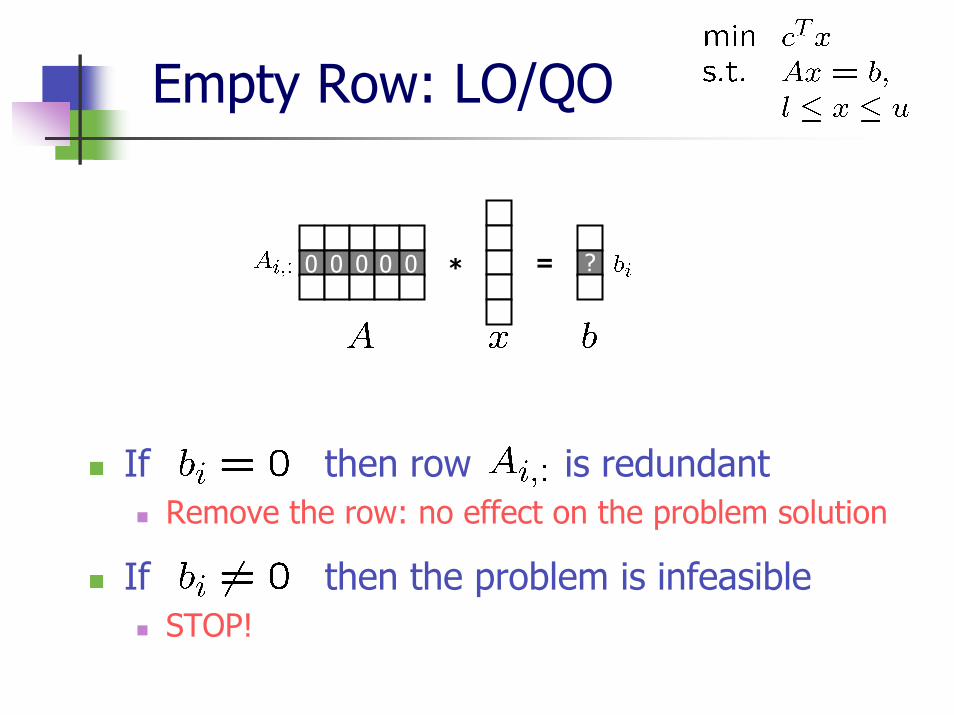

Empty Row: LO/QO

If then row is redundantRemove the row: no effect on the problem solution

If then the problem is infeasibleSTOP!

* =0 0 0 0 0 ?

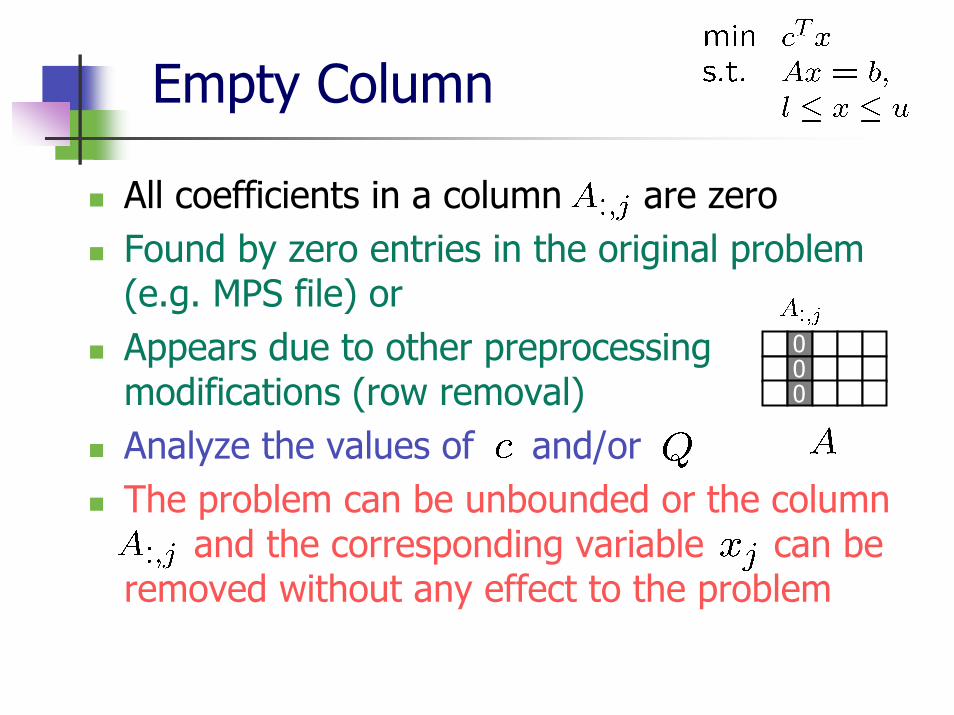

Empty Column

All coefficients in a column are zeroFound by zero entries in the original problem (e.g. MPS file) orAppears due to other preprocessing modifications (row removal)Analyze the values of and/orThe problem can be unbounded or the column

and the corresponding variable can be removed without any effect to the problem

000

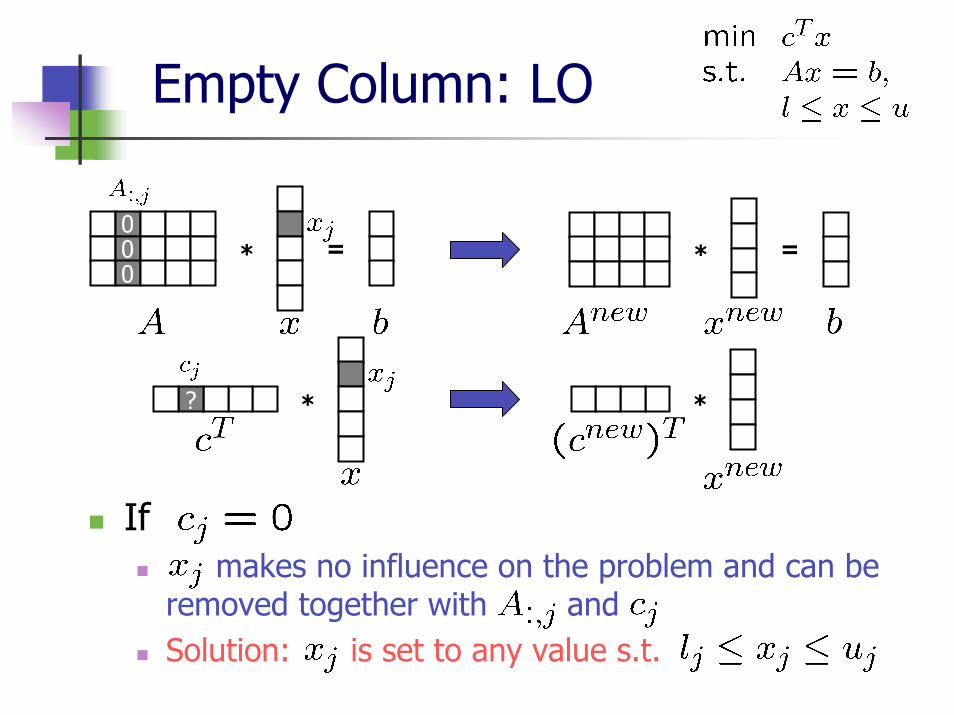

Empty Column: LO

If makes no influence on the problem and can be

removed together with and Solution: is set to any value s.t.

* =* =000

?

* *?

Empty Column: LO

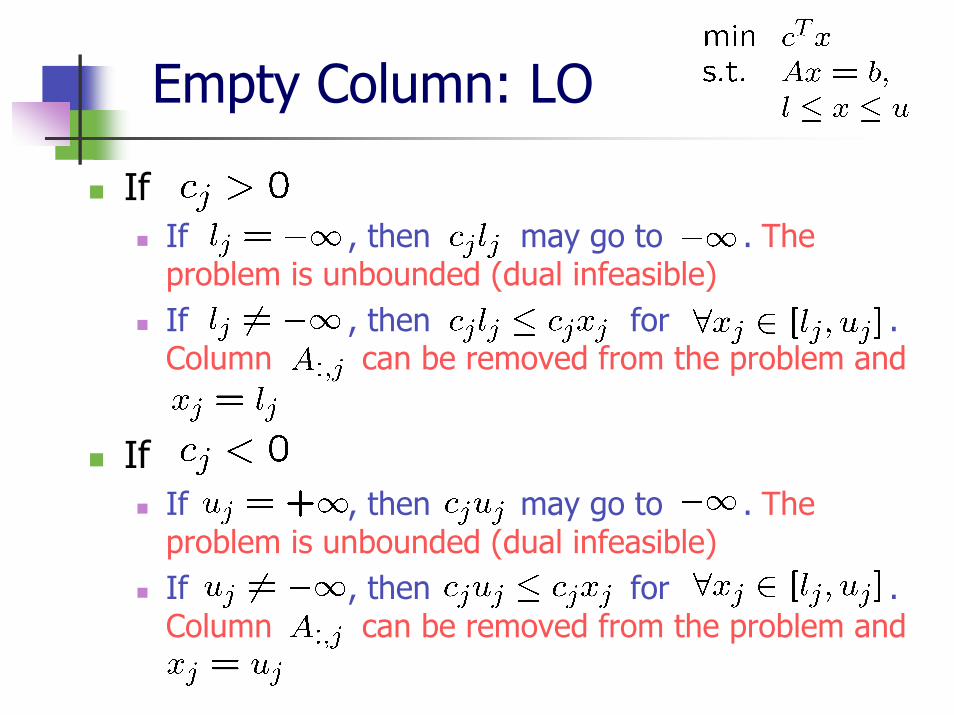

If If , then may go to . The problem is unbounded (dual infeasible)If , then for .Column can be removed from the problem and

If If , then may go to . The problem is unbounded (dual infeasible)If , then for .Column can be removed from the problem and

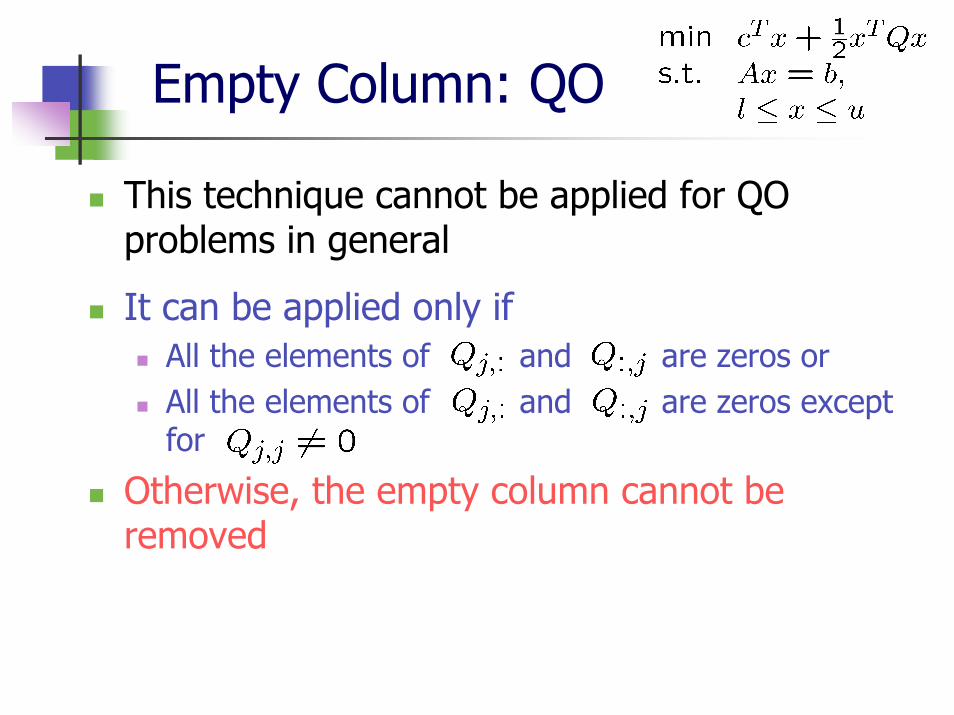

Empty Column: QO

This technique cannot be applied for QO problems in general

It can be applied only if All the elements of and are zeros orAll the elements of and are zeros except for

Otherwise, the empty column cannot be removed

Empty Column: QO

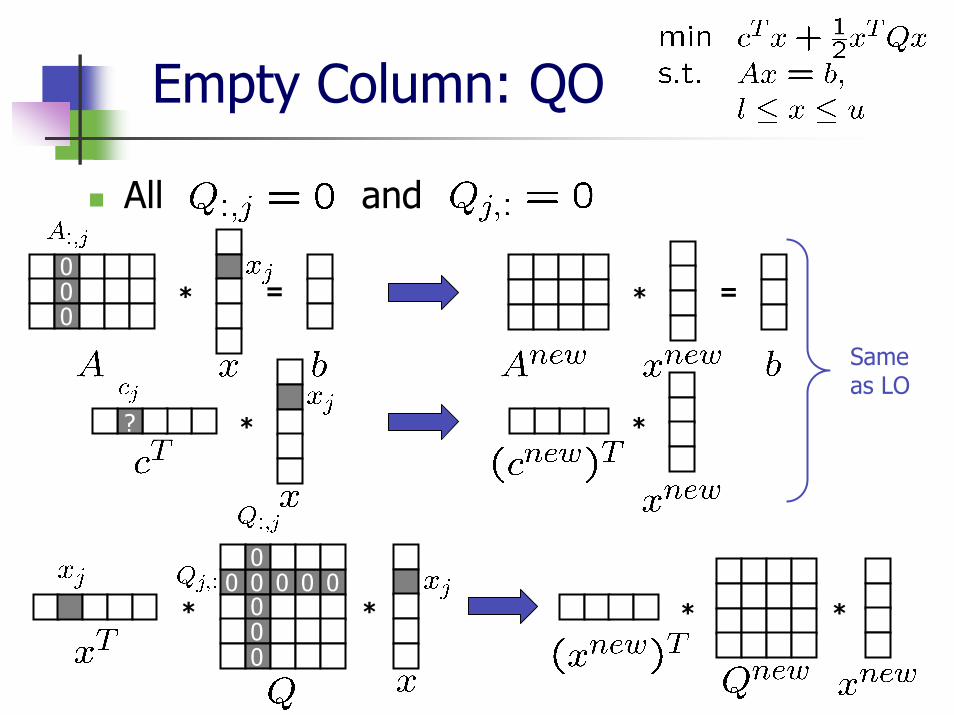

All and

* =* =000

****

00000

0 0 0 0

Same as LO

* *?

Empty Column: QO

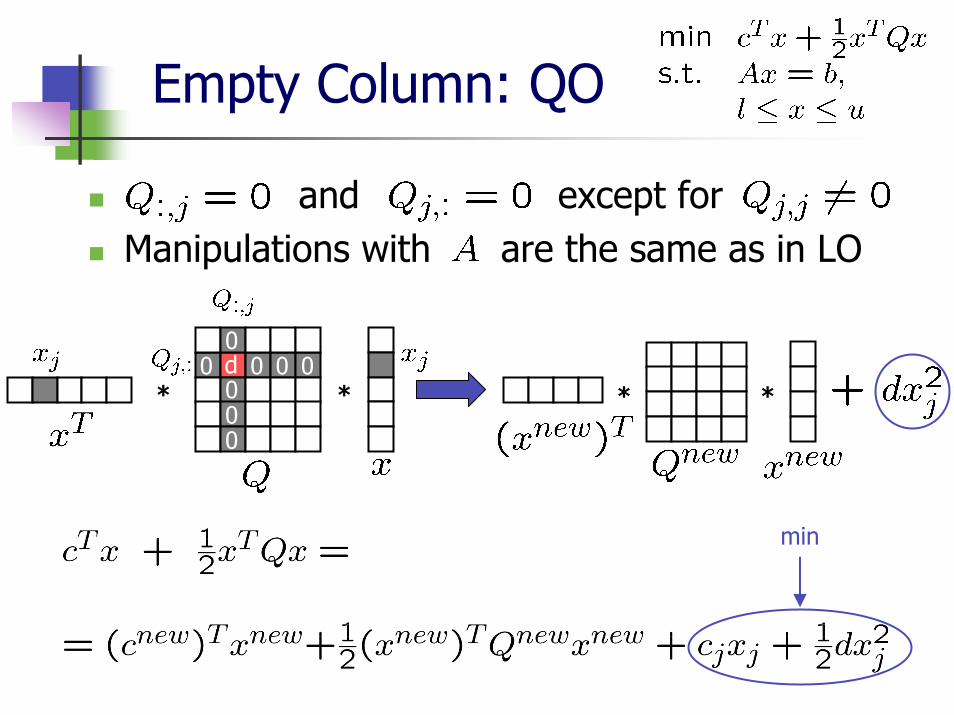

and except for Manipulations with are the same as in LO

****

0d000

0 0 0 0

min

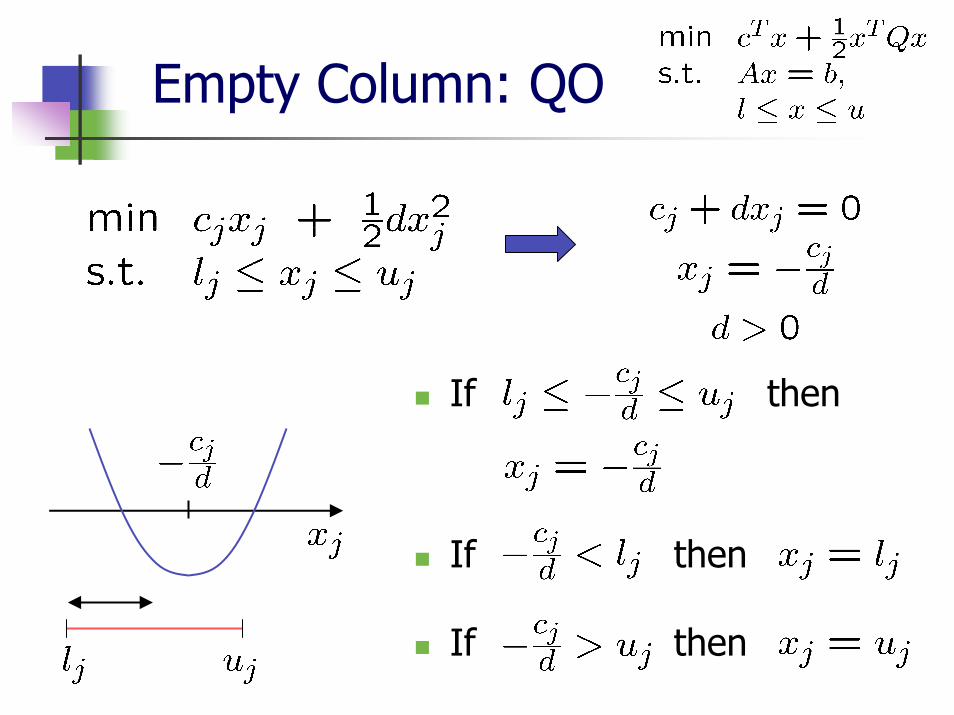

Empty Column: QO

If then

If then

If then

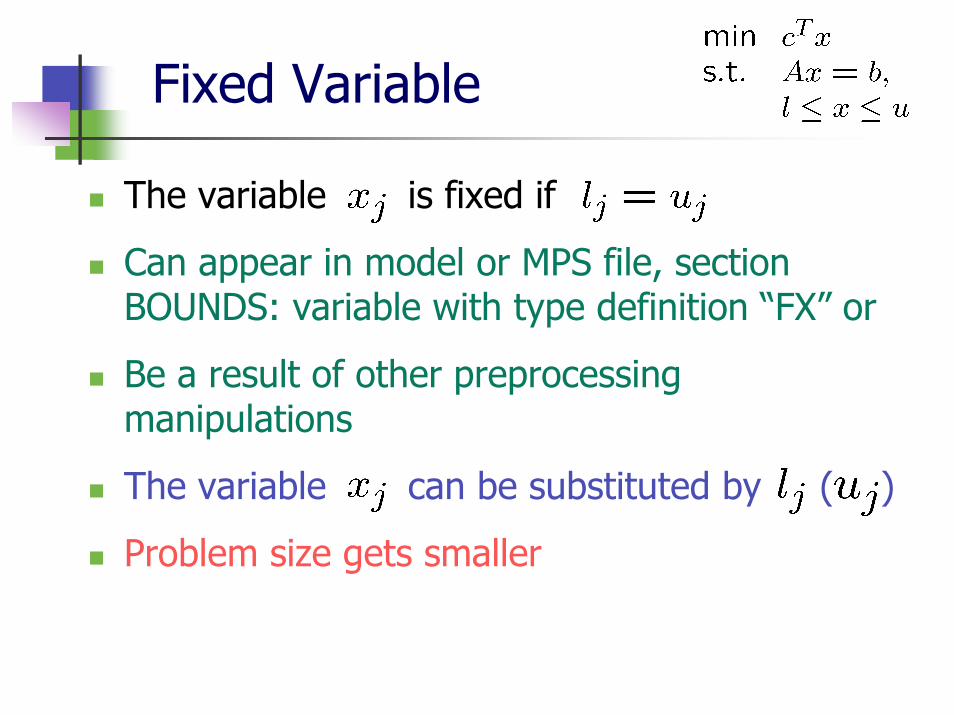

The variable is fixed if

Can appear in model or MPS file, section BOUNDS: variable with type definition “FX” or

Be a result of other preprocessing manipulations

The variable can be substituted by ( )

Problem size gets smaller

Fixed Variable

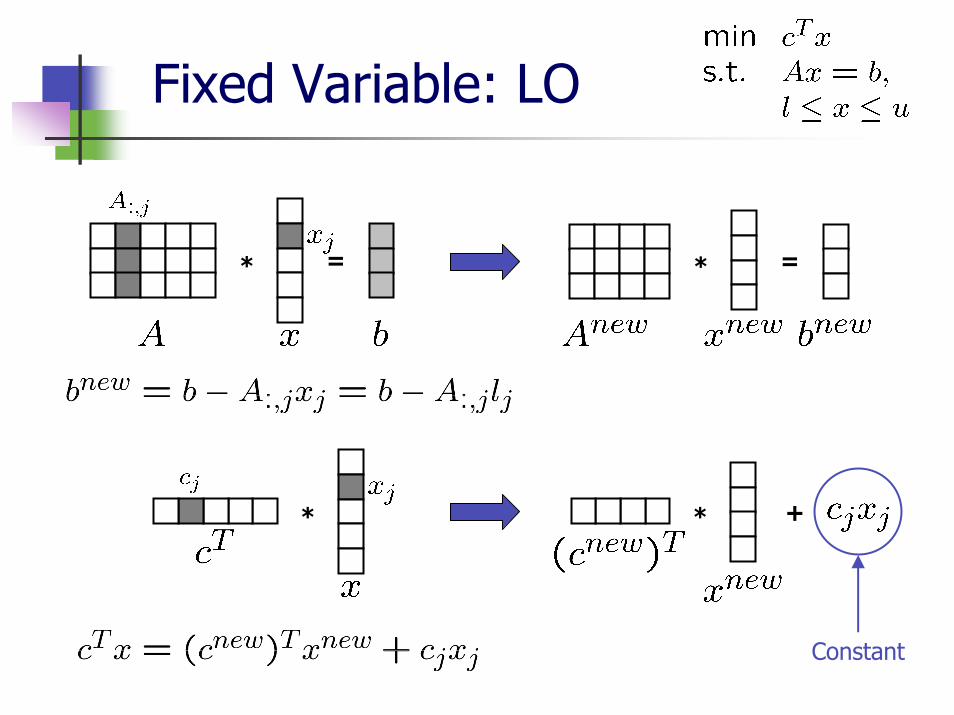

Fixed Variable: LO

* = * =

* * +

Constant

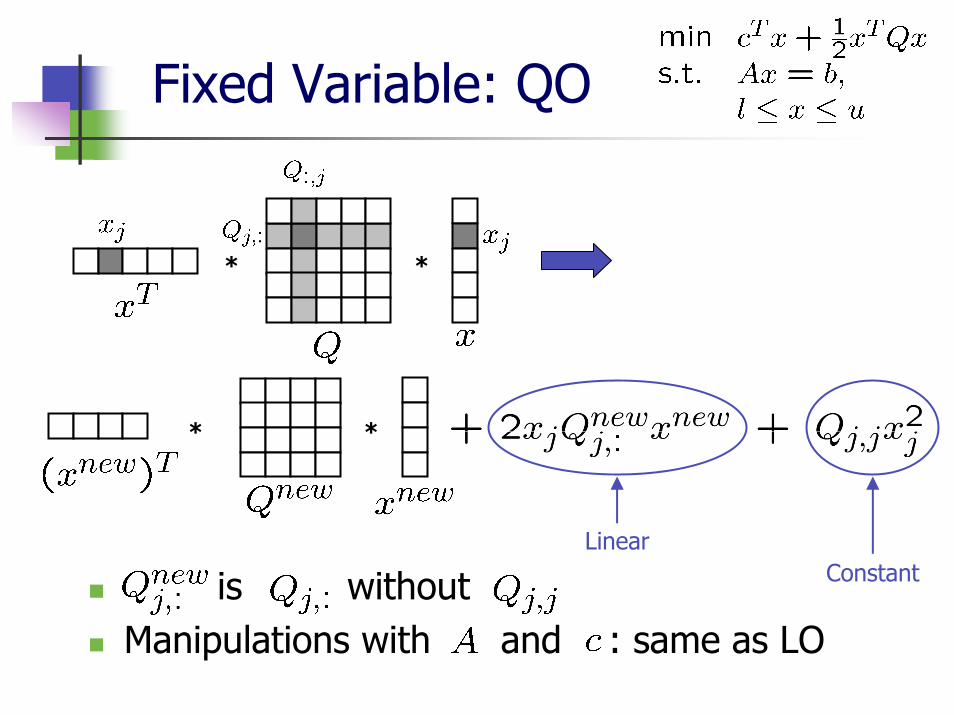

Fixed Variable: QO

is withoutManipulations with and : same as LO

**

**

ConstantLinear

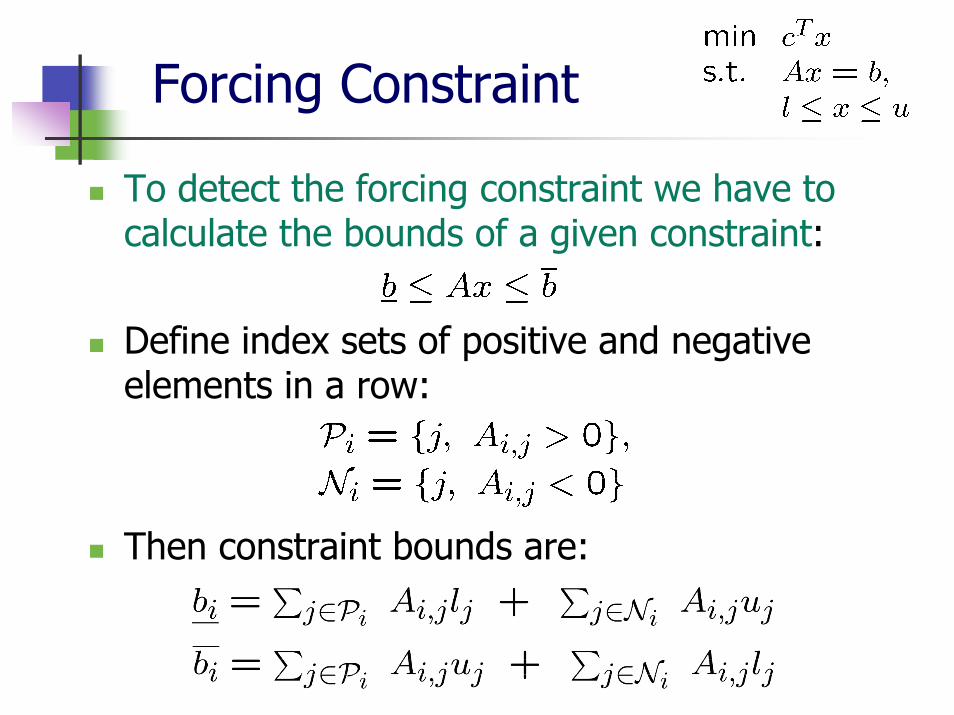

Forcing Constraint

To detect the forcing constraint we have to calculate the bounds of a given constraint:

Define index sets of positive and negative elements in a row:

Then constraint bounds are:

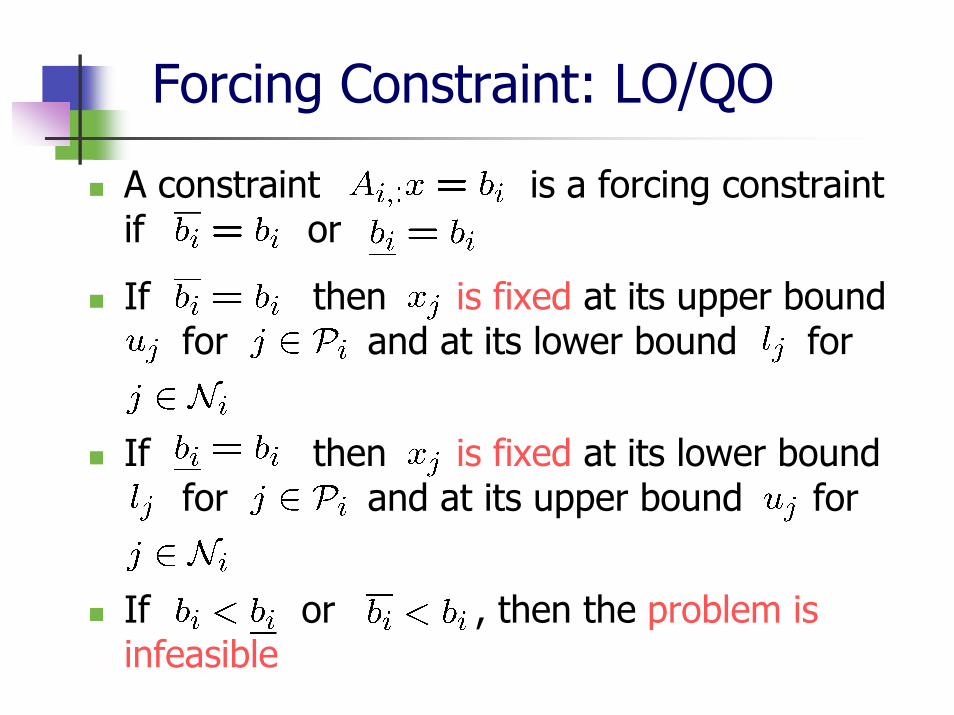

Forcing Constraint: LO/QO

A constraint is a forcing constraint if or

If then is fixed at its upper boundfor and at its lower bound for

If then is fixed at its lower boundfor and at its upper bound for

If or , then the problem is infeasible

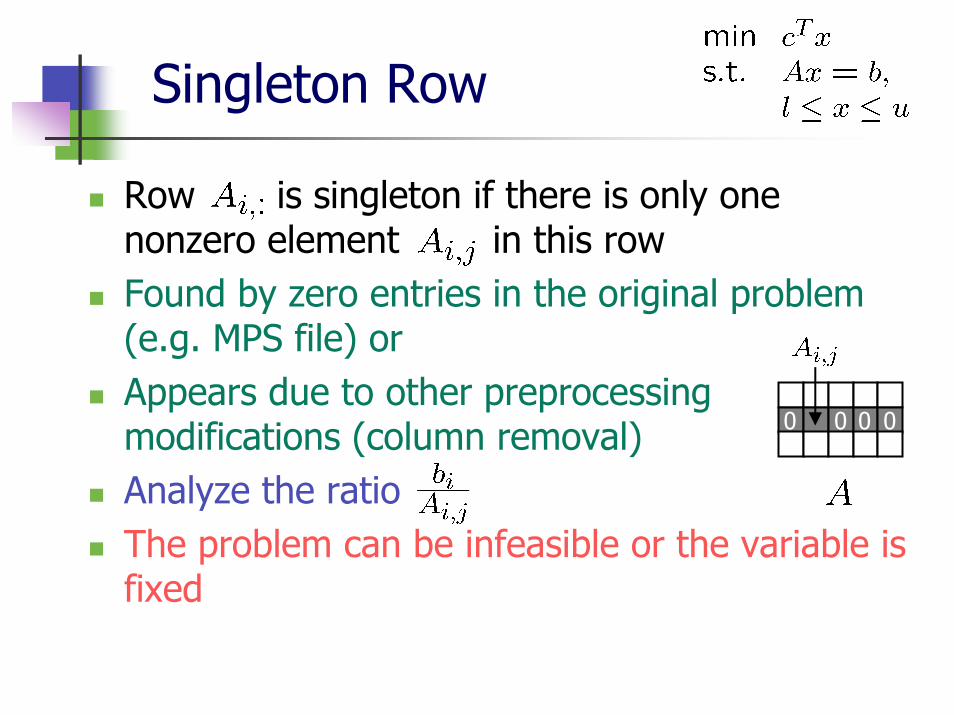

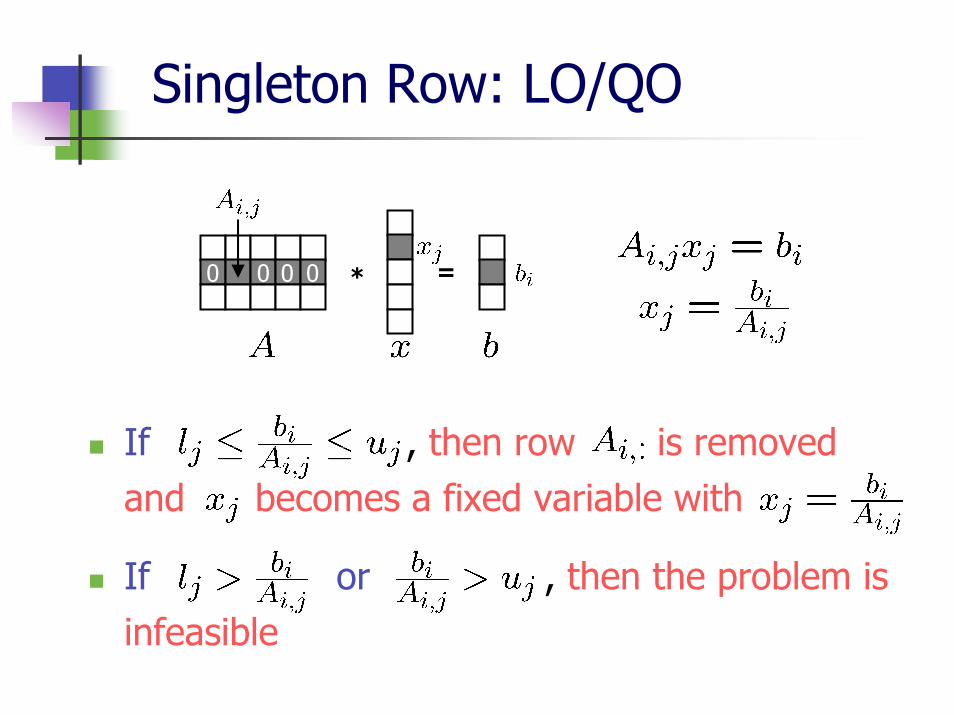

Singleton Row

Row is singleton if there is only one nonzero element in this rowFound by zero entries in the original problem (e.g. MPS file) orAppears due to other preprocessing modifications (column removal)Analyze the ratio The problem can be infeasible or the variable is fixed

0 0 0 0

If , then row is removed and becomes a fixed variable with

If or , then the problem is infeasible

Singleton Row: LO/QO

* =0 0 0 0

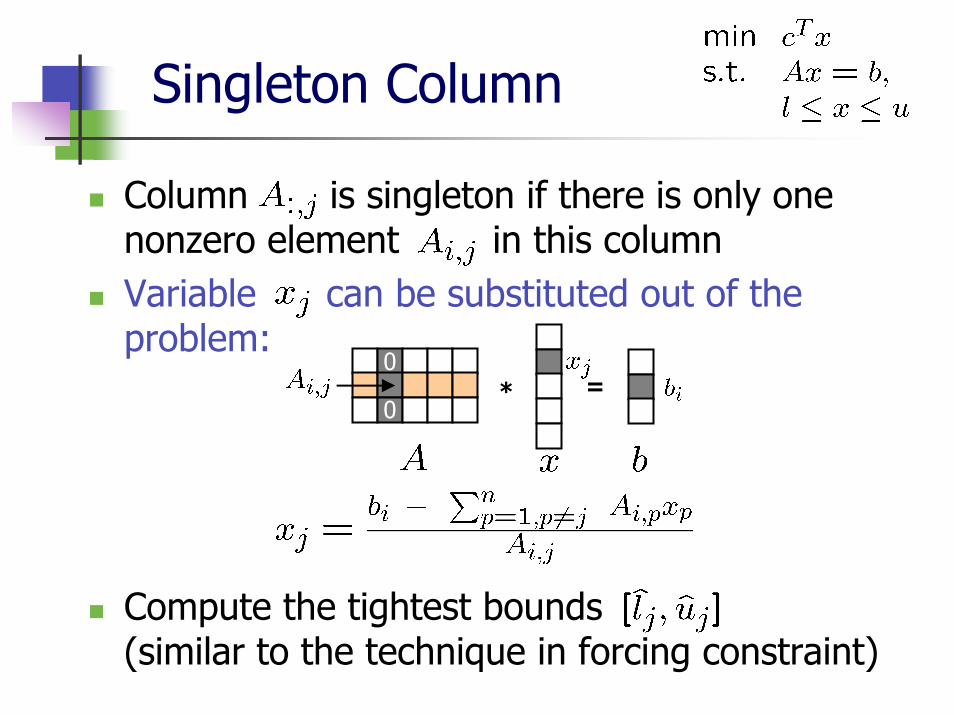

Singleton Column

Column is singleton if there is only one nonzero element in this columnVariable can be substituted out of the problem:

Compute the tightest bounds (similar to the technique in forcing constraint)

* =0

0

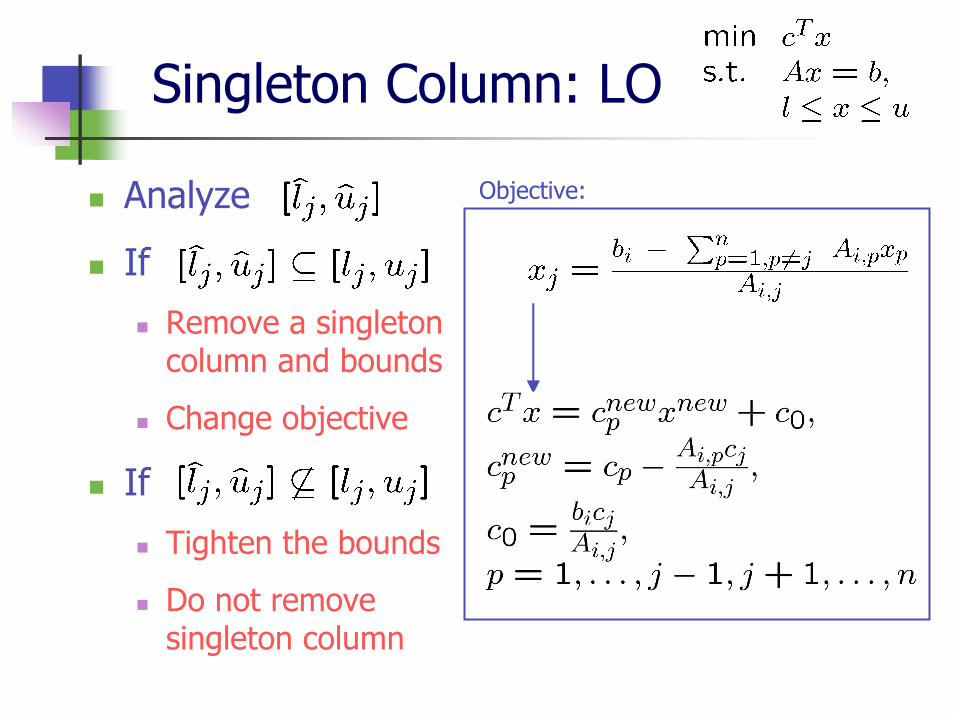

Singleton Column: LO

Analyze

If

Remove a singleton column and bounds

Change objective

If

Tighten the bounds

Do not remove singleton column

Objective:

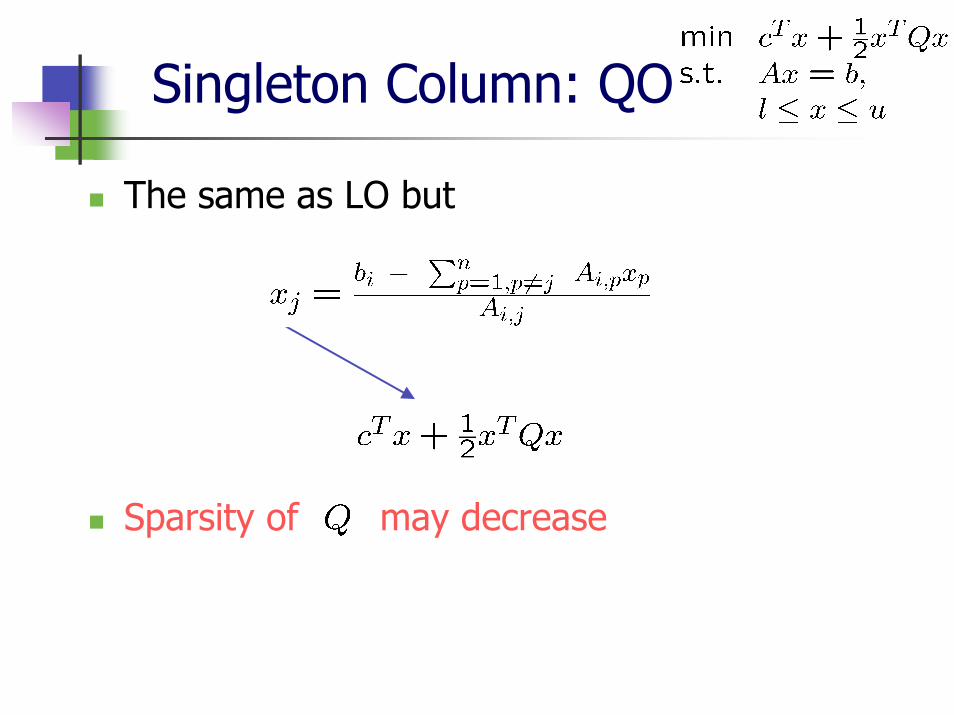

Singleton Column: QO

The same as LO but

Sparsity of may decrease

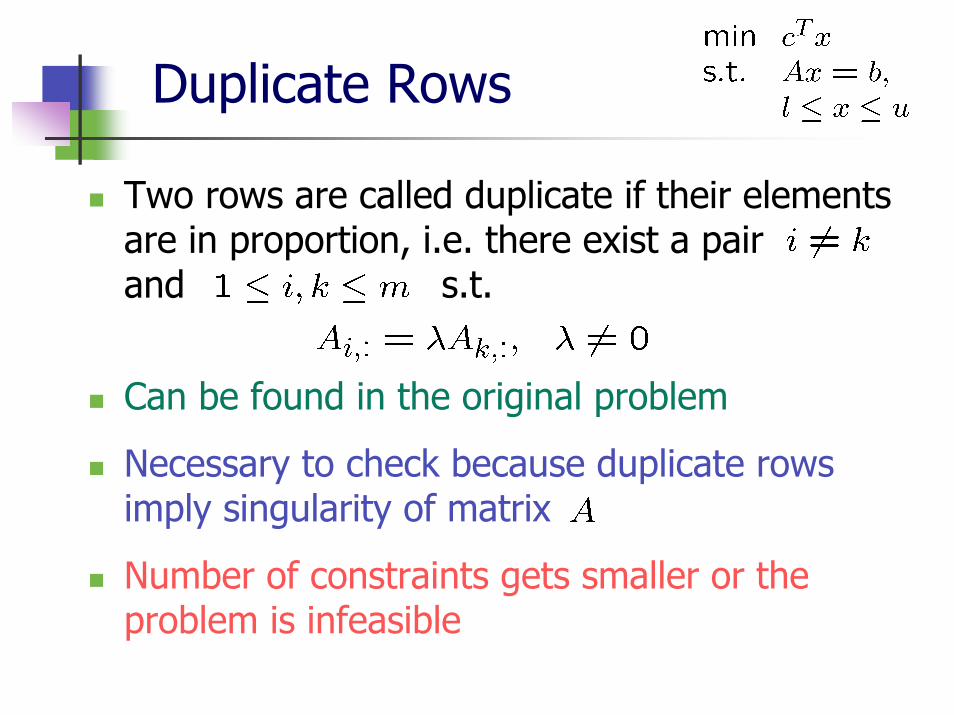

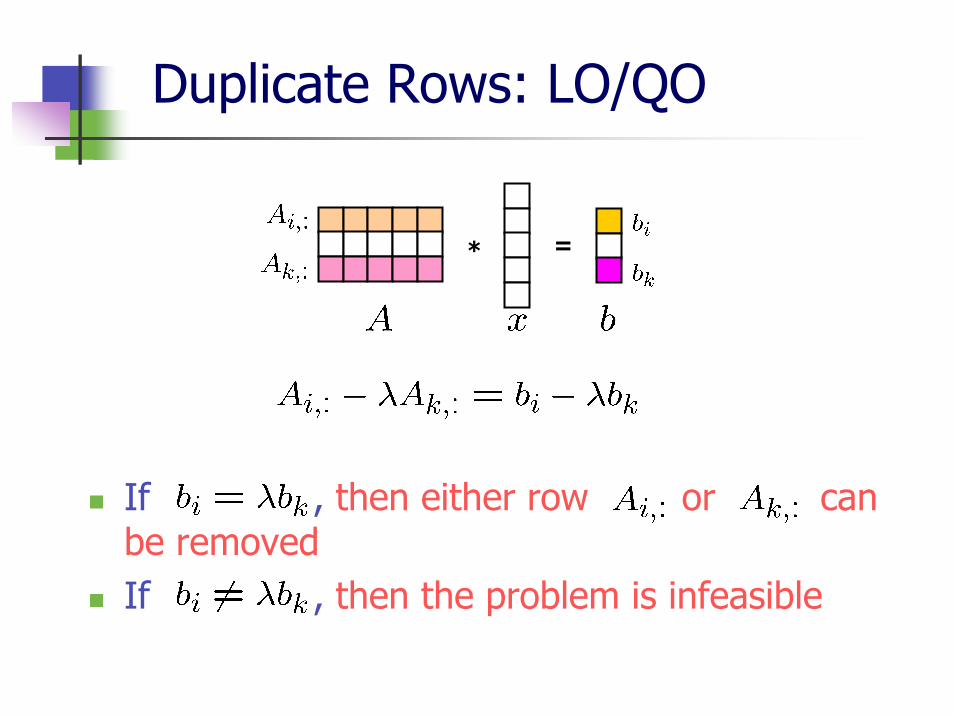

Duplicate Rows

Two rows are called duplicate if their elements are in proportion, i.e. there exist a pair and s.t.

Can be found in the original problem

Necessary to check because duplicate rows imply singularity of matrix

Number of constraints gets smaller or the problem is infeasible

Duplicate Rows: LO/QO

If , then either row or can be removedIf , then the problem is infeasible

* =

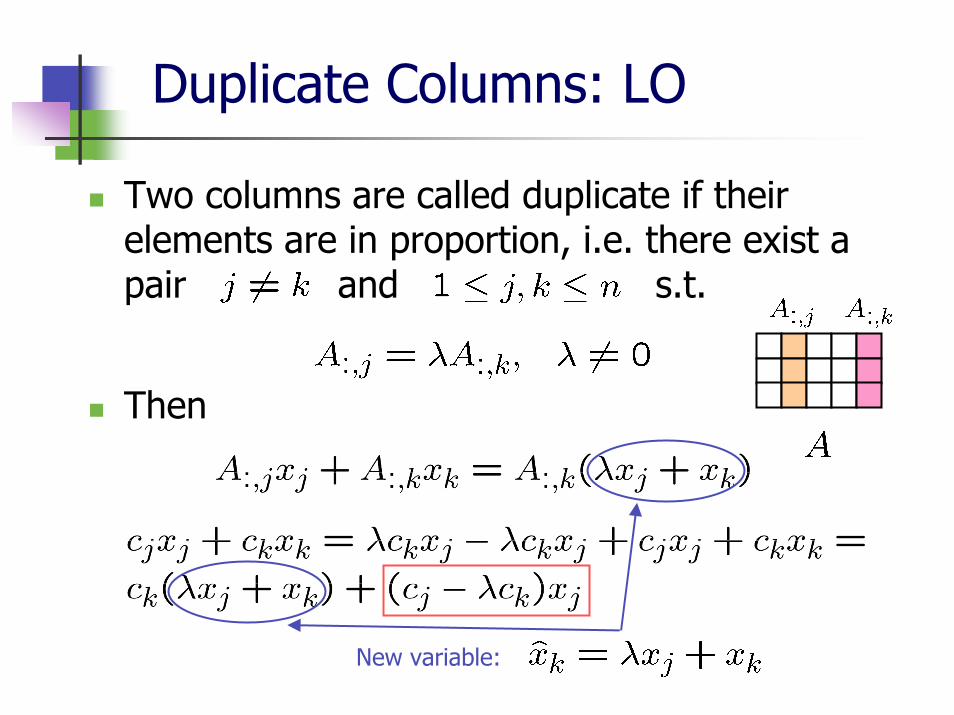

Duplicate Columns: LO

Two columns are called duplicate if their elements are in proportion, i.e. there exist a pair and s.t.

Then

New variable:

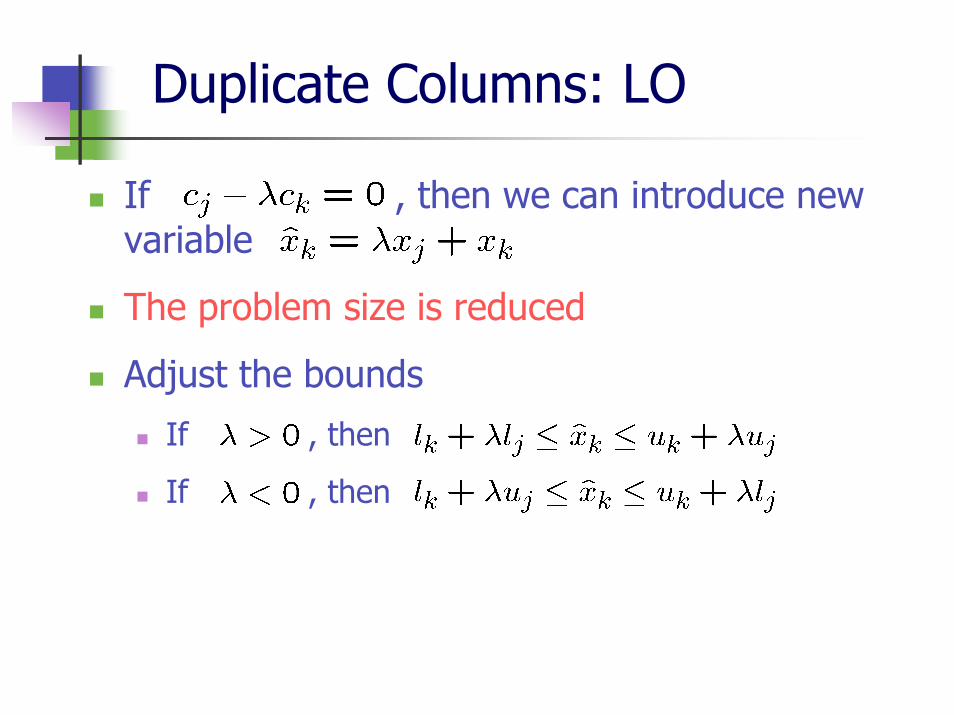

Duplicate Columns: LO

If , then we can introduce new variable

The problem size is reduced

Adjust the bounds

If , then

If , then

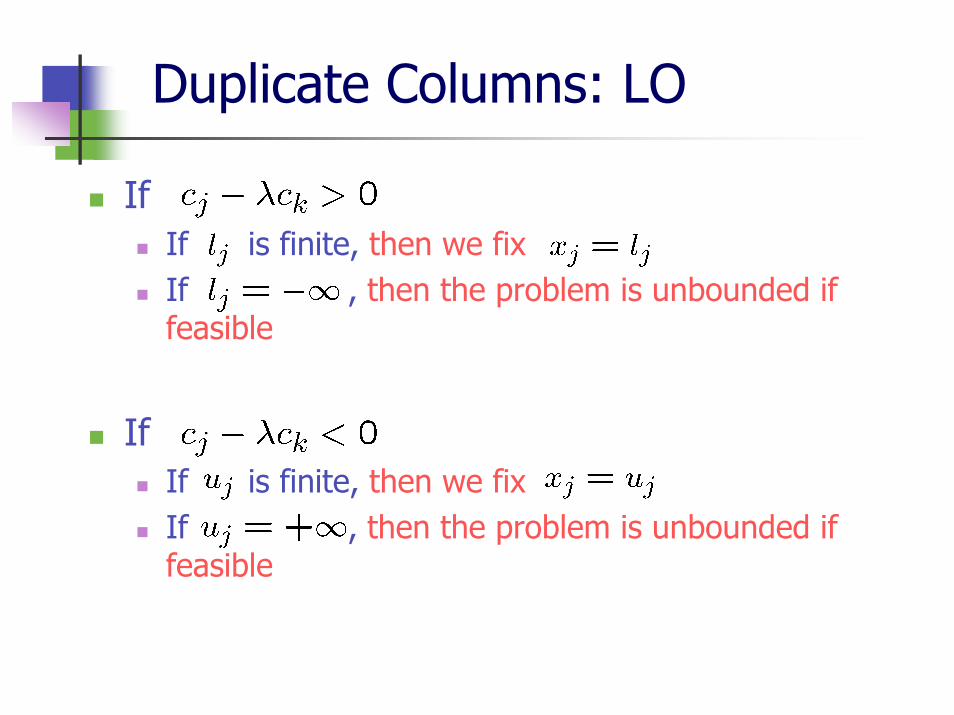

Duplicate Columns: LO

IfIf is finite, then we fix If , then the problem is unbounded if feasible

IfIf is finite, then we fix If , then the problem is unbounded if feasible

Advanced Preprocessing Techniques

Nael El Shawwa

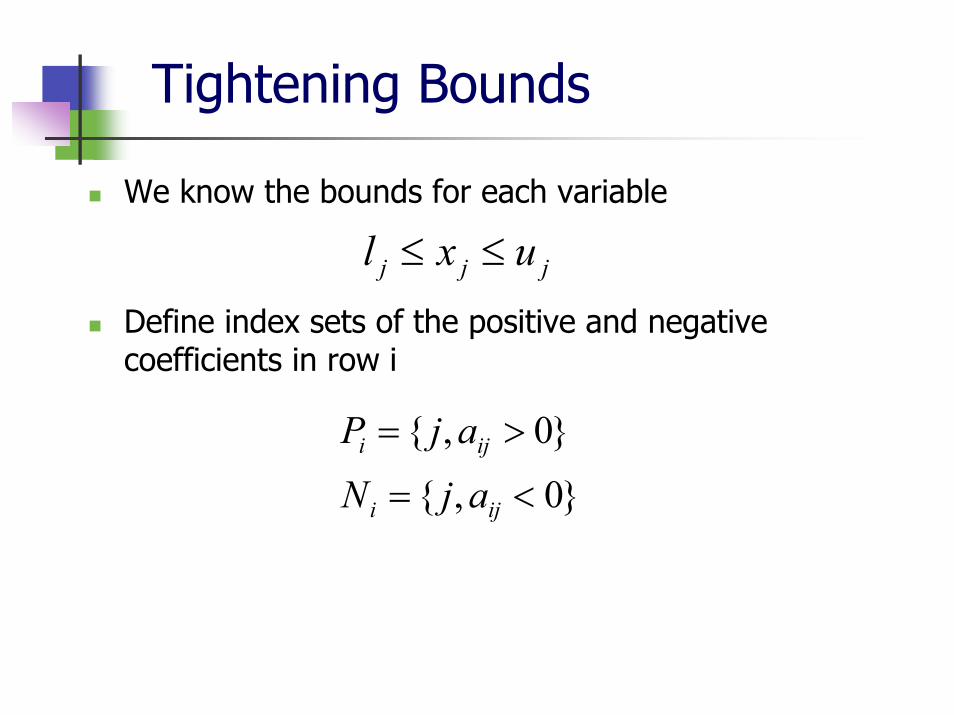

Tightening Bounds

We know the bounds for each variable

Define index sets of the positive and negative coefficients in row i

jjj uxl ≤≤

}0,{

}0,{

<=

>=

iji

iji

ajN

ajP

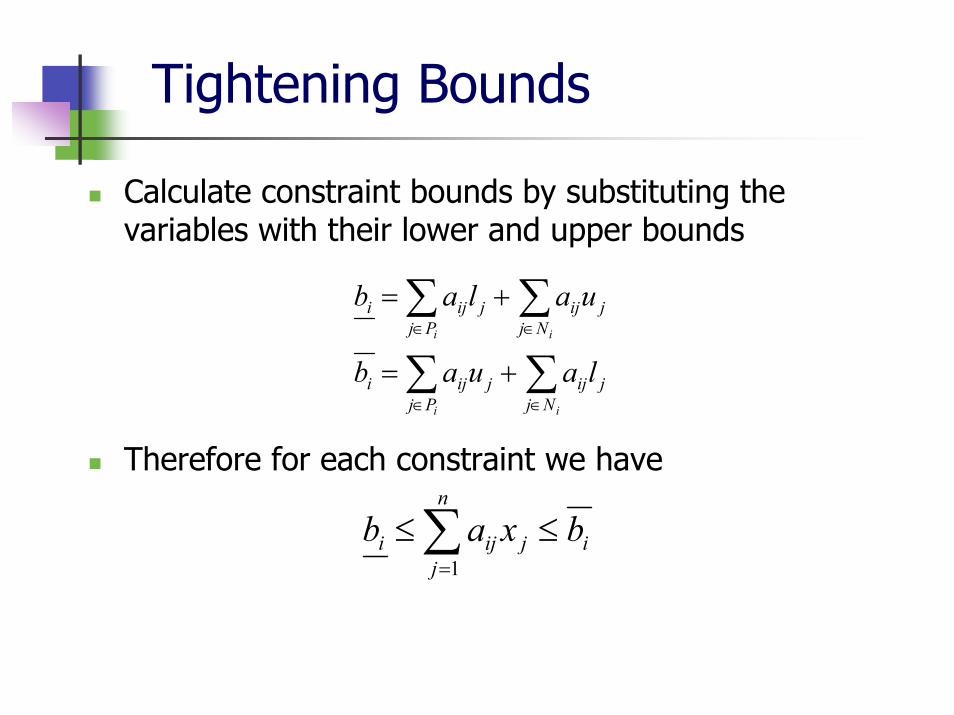

Tightening Bounds

Calculate constraint bounds by substituting the variables with their lower and upper bounds

Therefore for each constraint we have

∑ ∑

∑ ∑

∈ ∈

∈ ∈

+=

+=

i i

i i

Pj Njjijjiji

Pj Njjijjiji

lauab

ualab

∑=

≤≤n

jijiji bxab

1

Tightening Bounds

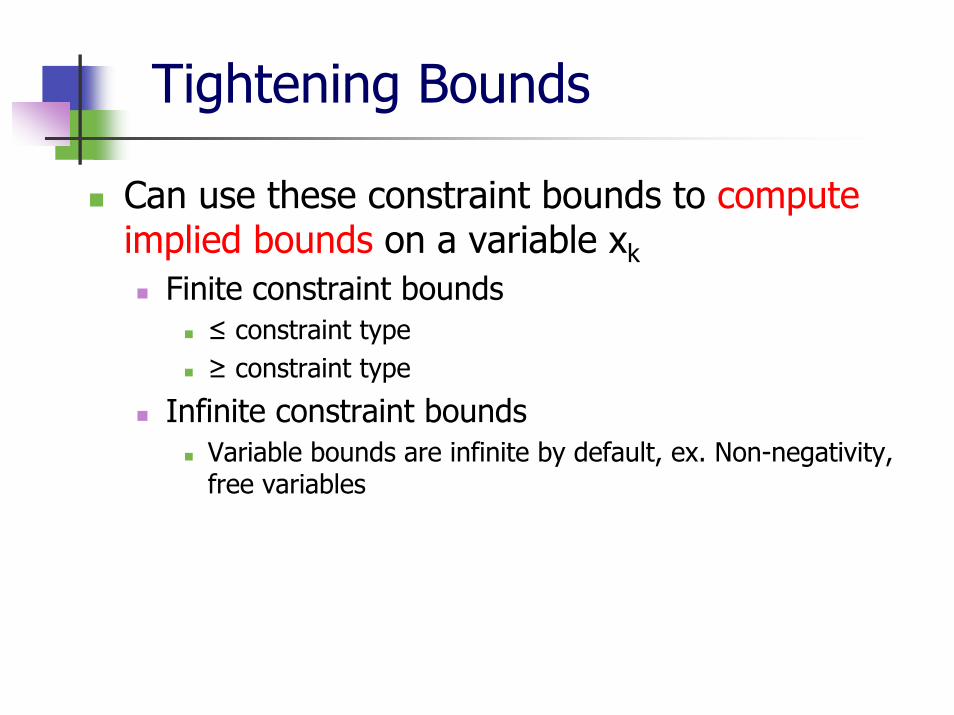

Can use these constraint bounds to compute implied bounds on a variable xk

Finite constraint bounds≤ constraint type≥ constraint type

Infinite constraint boundsVariable bounds are infinite by default, ex. Non-negativity, free variables

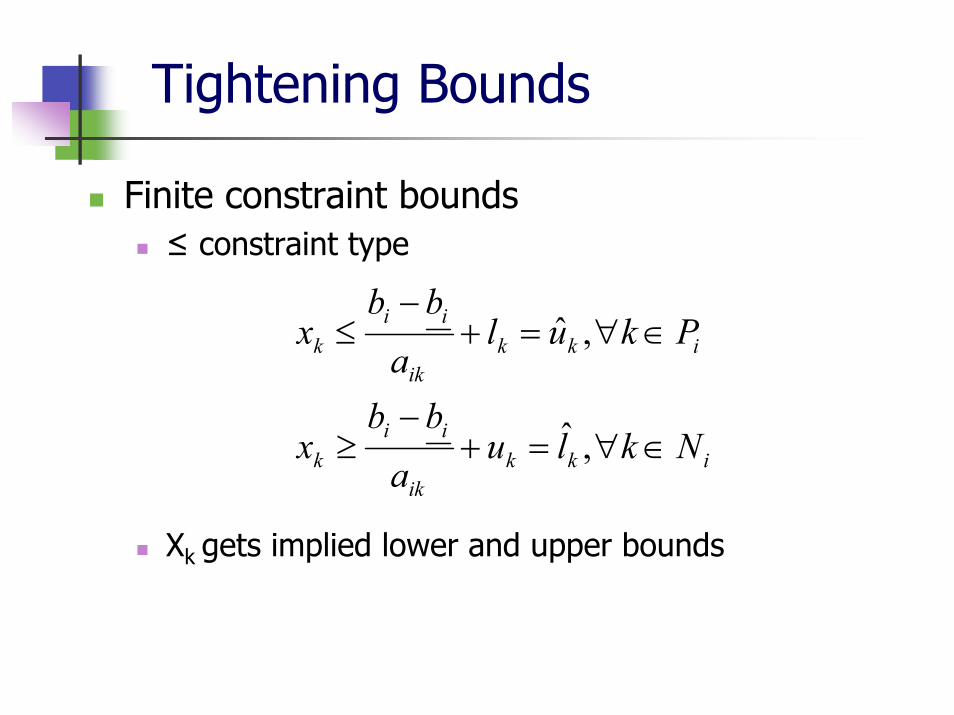

Tightening Bounds

Finite constraint bounds≤ constraint type

Xk gets implied lower and upper bounds

ikkik

iik

ikkik

iik

Nklua

bbx

Pkula

bbx

∈∀=+−

≥

∈∀=+−

≤

,ˆ

,ˆ

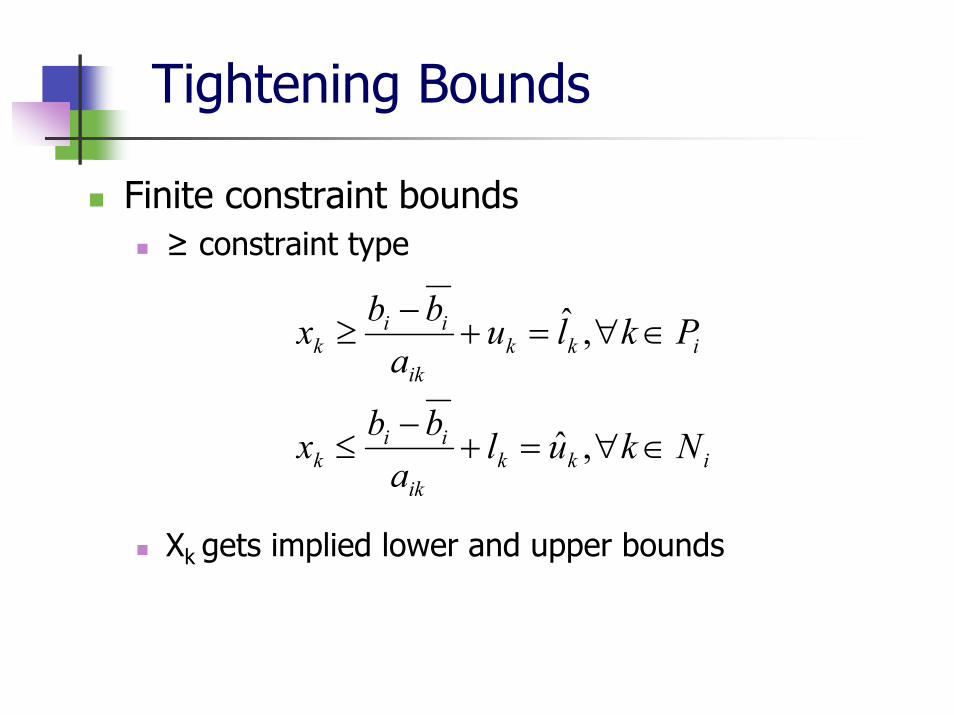

Tightening Bounds

Finite constraint bounds≥ constraint type

Xk gets implied lower and upper bounds

ikkik

iik

ikkik

iik

Nkula

bbx

Pklua

bbx

∈∀=+−

≤

∈∀=+−

≥

,ˆ

,ˆ

Tightening Bounds

Compare the new implied bounds with the original bounds

If they conflict then the problem is infeasibleIf they are tighter, then update the boundsIf they are looser, then maintain the bounds

What about infinite bounds?J. Gondzio, Presolve analysis of linear programs prior to applying the interior point method, INFORMS Journal on Computing 9, No. 1 (1997) pp. 73-91.Xin Huang , Preprocessing and Post-processing in Linear Optimization, M.Sc. Thesis McMaster University, June 2004

Tightening Bounds

Dual variablesA similar approach to the one presented for primal variables can be applied. [See Xin Huang’s Thesis]

Note: dual variable yi is free, so the variable bounds are infinite

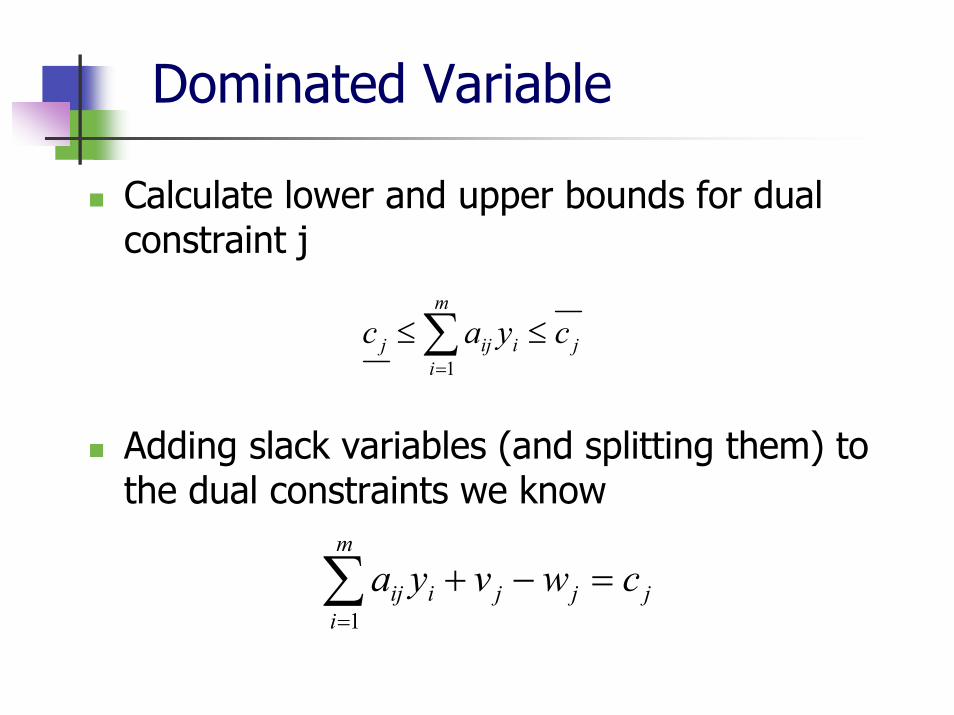

Dominated Variable

Calculate lower and upper bounds for dual constraint j

Adding slack variables (and splitting them) to the dual constraints we know

∑=

≤≤m

ijiijj cyac

1

∑=

=−+m

ijjjiij cwvya

1

Dominated Variable

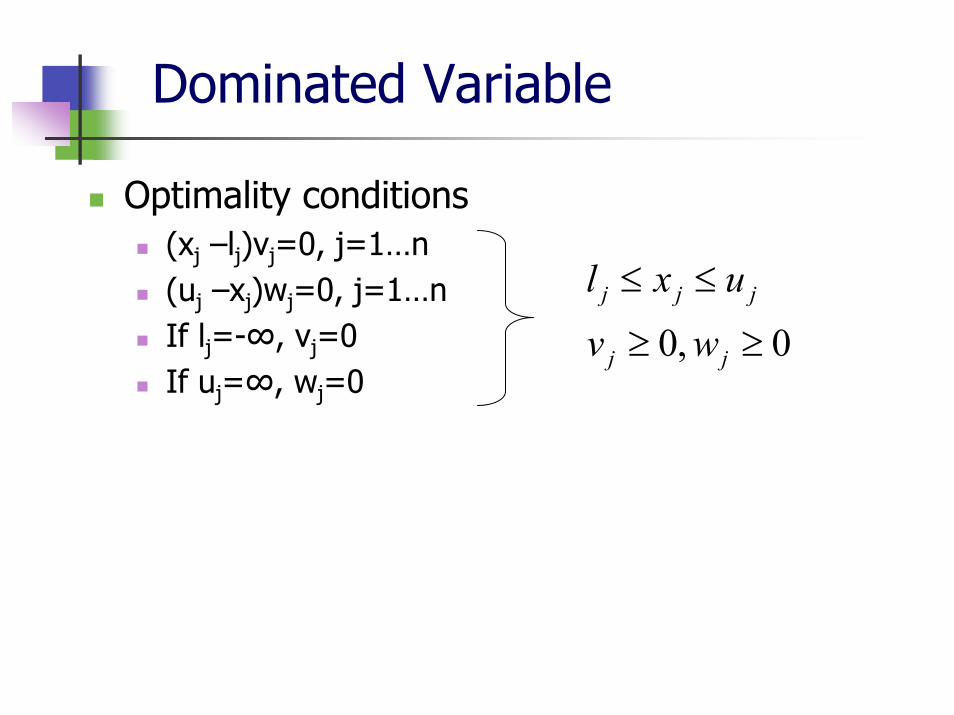

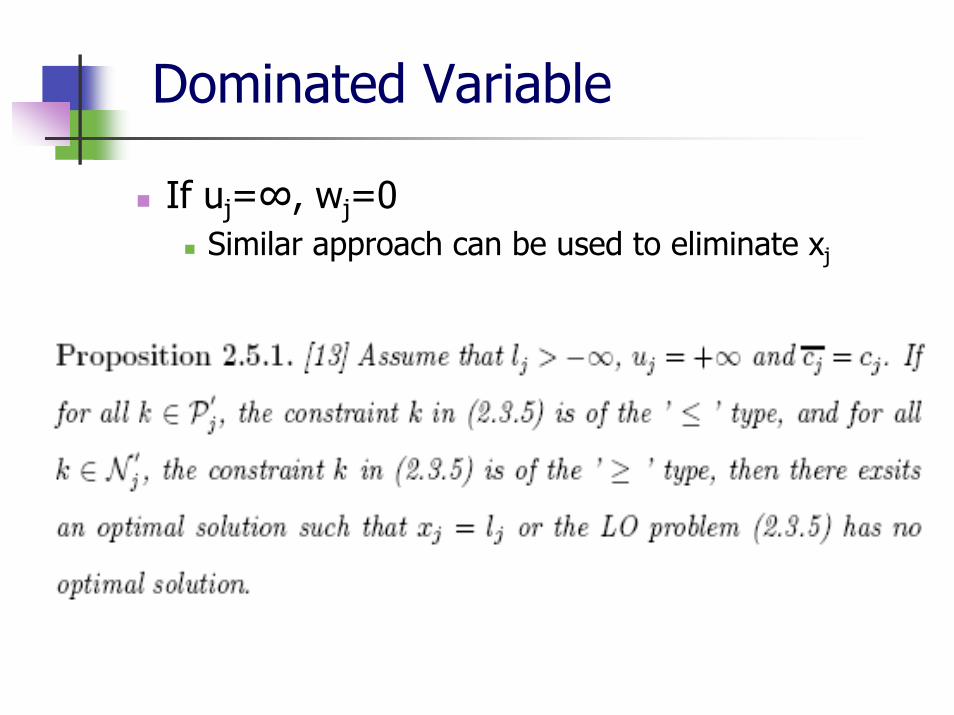

Optimality conditions(xj –lj)vj=0, j=1…n(uj –xj)wj=0, j=1…nIf lj=-∞, vj=0If uj=∞, wj=0

0,0 ≥≥

≤≤

jj

jjj

wv

uxl

Dominated Variable

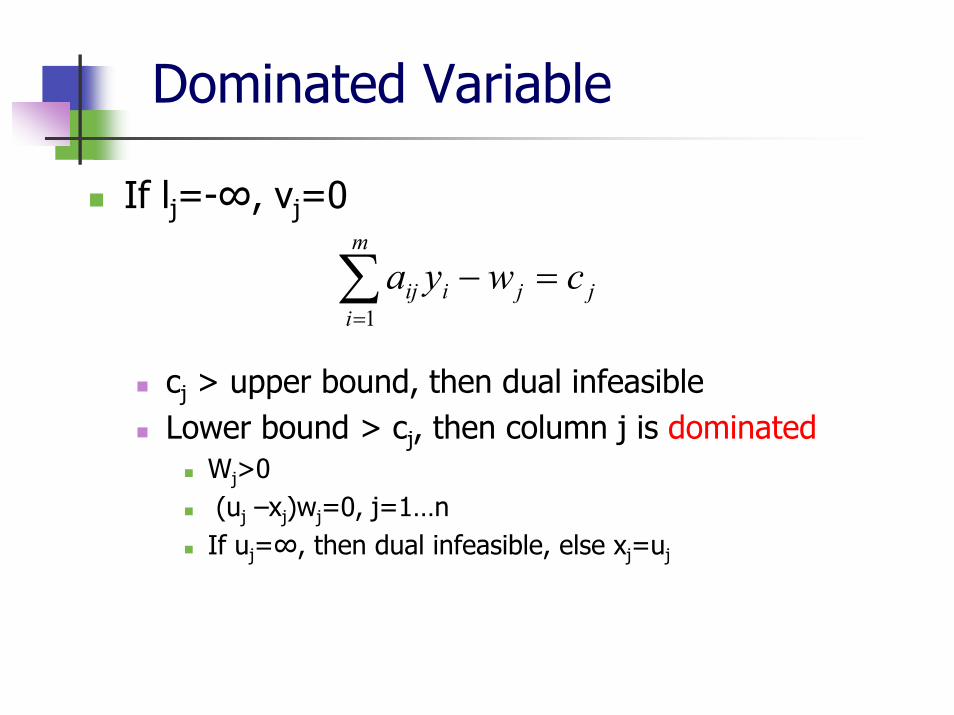

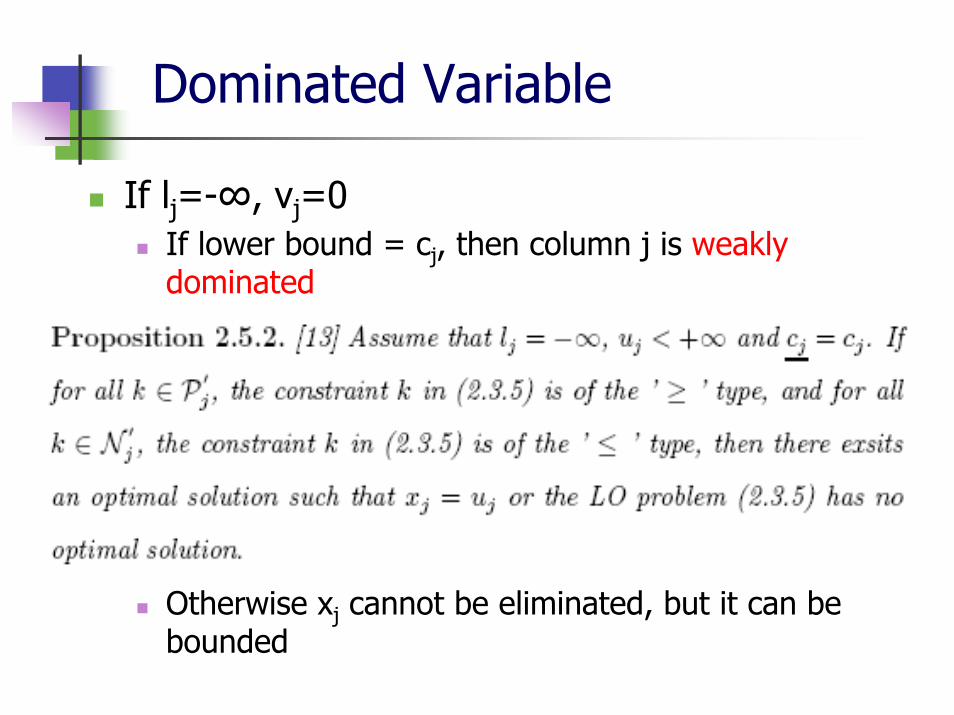

If lj=-∞, vj=0

cj > upper bound, then dual infeasible Lower bound > cj, then column j is dominated

Wj>0(uj –xj)wj=0, j=1…nIf uj=∞, then dual infeasible, else xj=uj

∑=

=−m

ijjiij cwya

1

Dominated Variable

If lj=-∞, vj=0If lower bound = cj, then column j is weakly dominated

Otherwise xj cannot be eliminated, but it can be bounded

Dominated Variable

If uj=∞, wj=0Similar approach can be used to eliminate xj

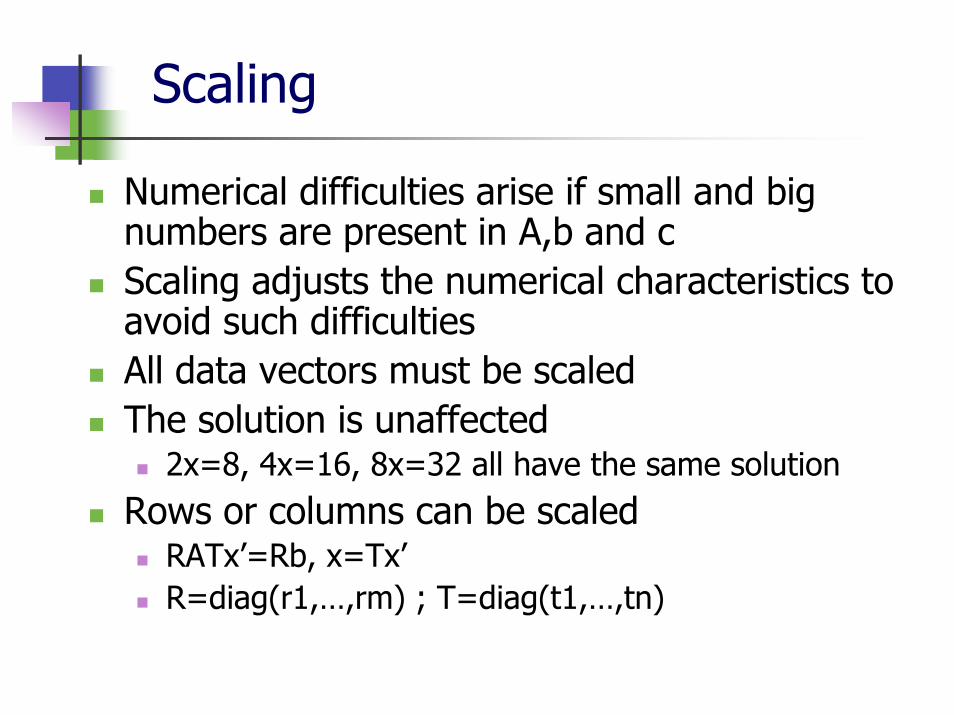

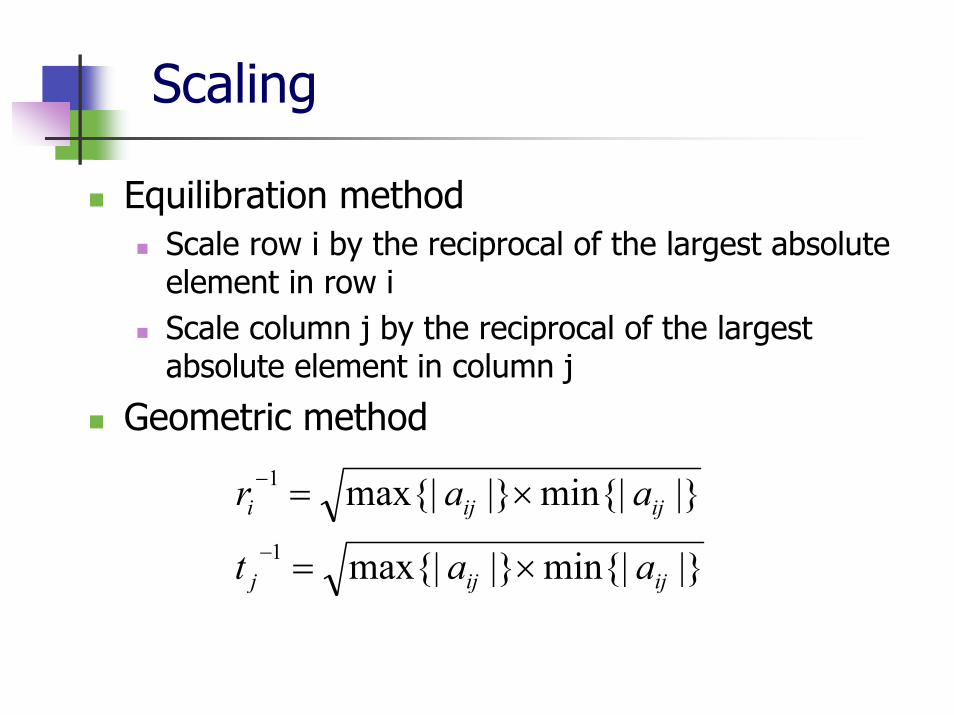

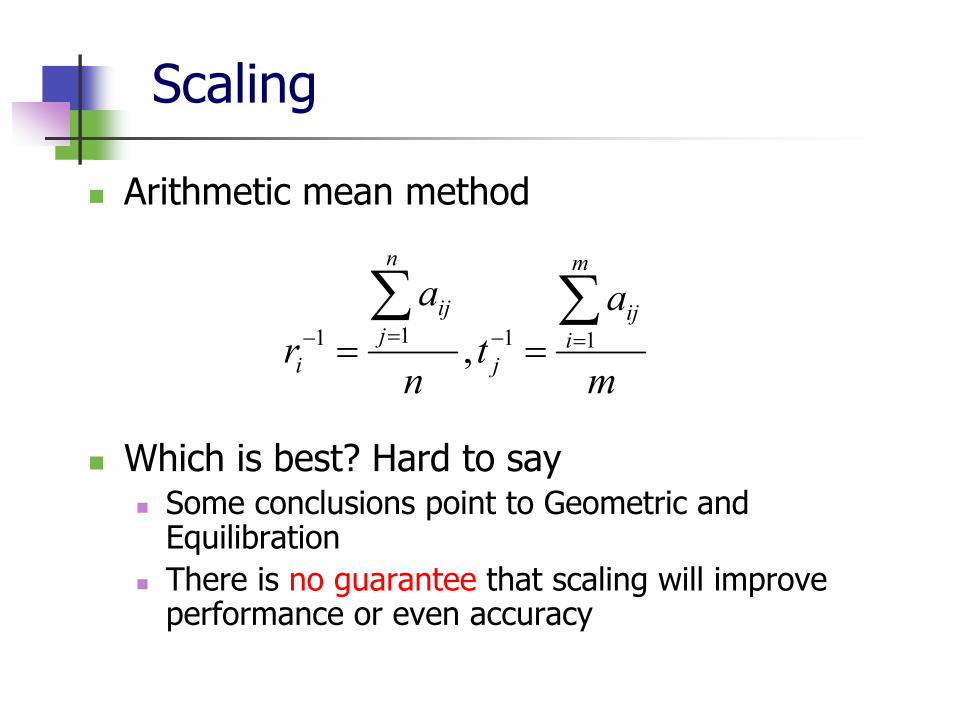

Scaling

Numerical difficulties arise if small and big numbers are present in A,b and cScaling adjusts the numerical characteristics to avoid such difficultiesAll data vectors must be scaledThe solution is unaffected

2x=8, 4x=16, 8x=32 all have the same solutionRows or columns can be scaled

RATx’=Rb, x=Tx’R=diag(r1,…,rm) ; T=diag(t1,…,tn)

Scaling

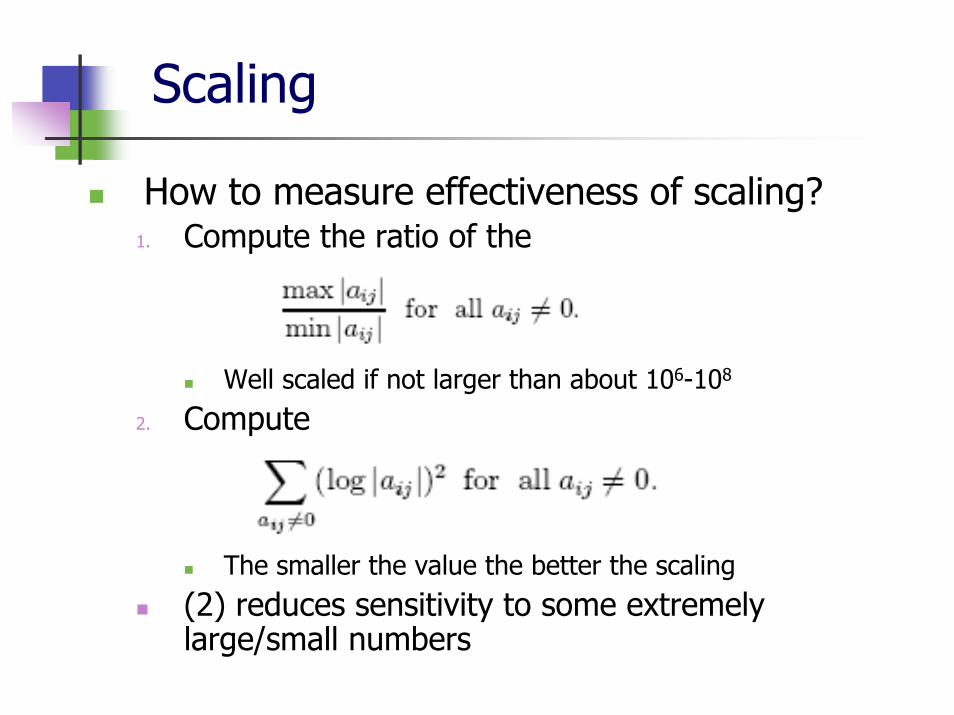

How to measure effectiveness of scaling?1. Compute the ratio of the

Well scaled if not larger than about 106-108

2. Compute

The smaller the value the better the scaling(2) reduces sensitivity to some extremely large/small numbers

Scaling

Scaling

Equilibration methodScale row i by the reciprocal of the largest absolute element in row iScale column j by the reciprocal of the largest absolute element in column j

Geometric method

|}min{||}max{|

|}min{||}max{|1

1

ijijj

ijiji

aat

aar

×=

×=−

−

Scaling

Arithmetic mean method

Which is best? Hard to saySome conclusions point to Geometric and EquilibrationThere is no guarantee that scaling will improve performance or even accuracy

m

at

n

ar

m

iij

j

n

jij

i

∑∑=−=− == 1111 ,

Advanced Preprocessing Techniques (Cont’d)

Alberto Olvera

Preprocessing Techniques

Advanced TechniquesDominated variablesTightening boundsScalingMake A Sparser (Reducing Sparsity)Finding Linear dependency (Full Rank)

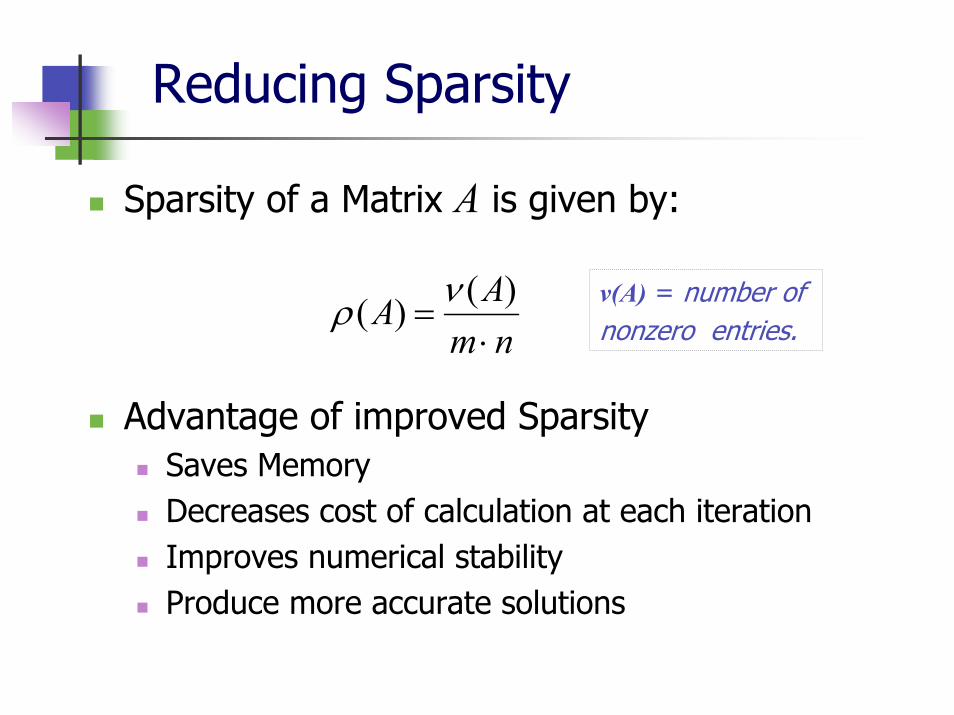

Reducing Sparsity

Sparsity of a Matrix A is given by:

Advantage of improved SparsitySaves MemoryDecreases cost of calculation at each iterationImproves numerical stabilityProduce more accurate solutions

nmAA⋅

=)()( νρ v(A) = number of

nonzero entries.

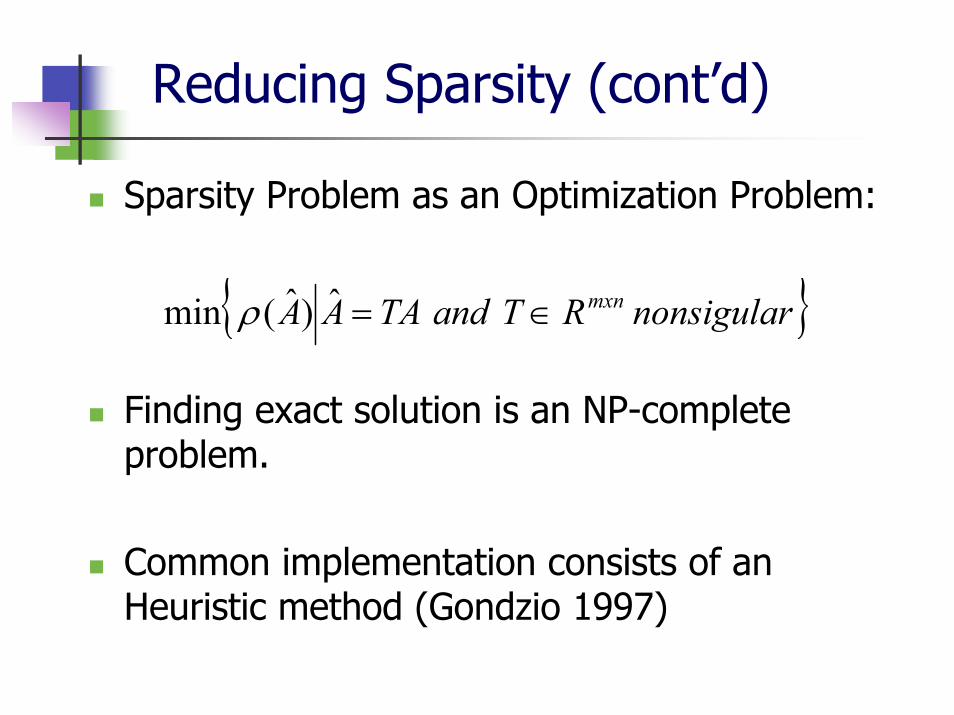

Reducing Sparsity (cont’d)

Sparsity Problem as an Optimization Problem:

Finding exact solution is an NP-complete problem.

Common implementation consists of an Heuristic method (Gondzio 1997)

{ }nonsigularRTandTAAA mxn∈=ˆ)ˆ(min ρ

Reducing Sparsity (cont’d)

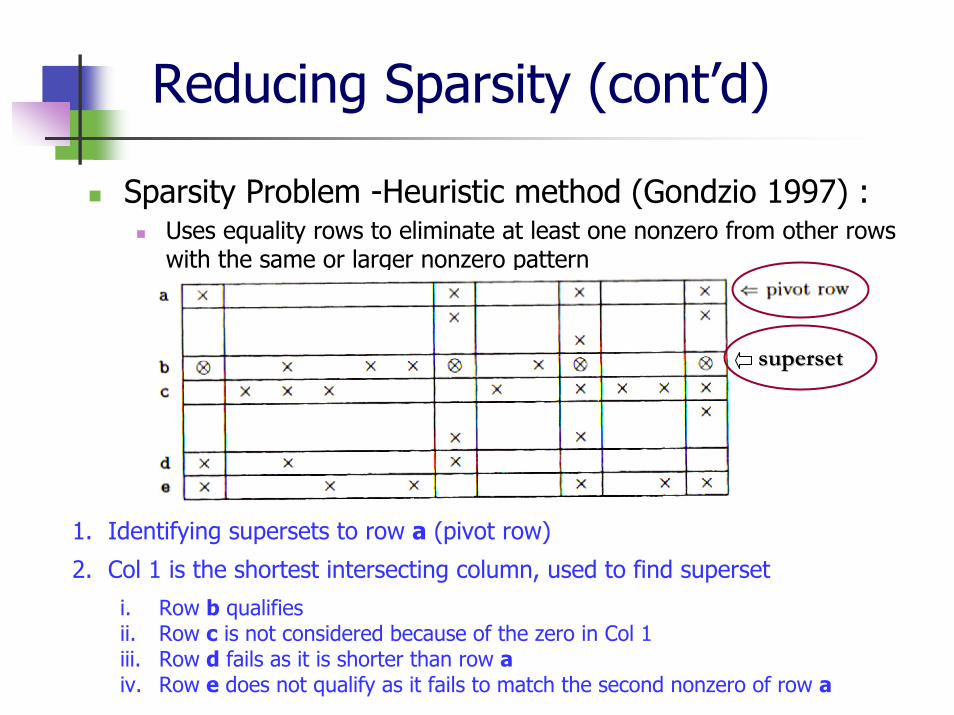

Sparsity Problem -Heuristic method (Gondzio 1997) :Uses equality rows to eliminate at least one nonzero from other rows with the same or larger nonzero pattern

1. Identifying supersets to row a (pivot row)

i. Row b qualifiesii. Row c is not considered because of the zero in Col 1iii. Row d fails as it is shorter than row aiv. Row e does not qualify as it fails to match the second nonzero of row a

2. Col 1 is the shortest intersecting column, used to find superset

supersetsuperset

Reducing Sparsity (cont’d)

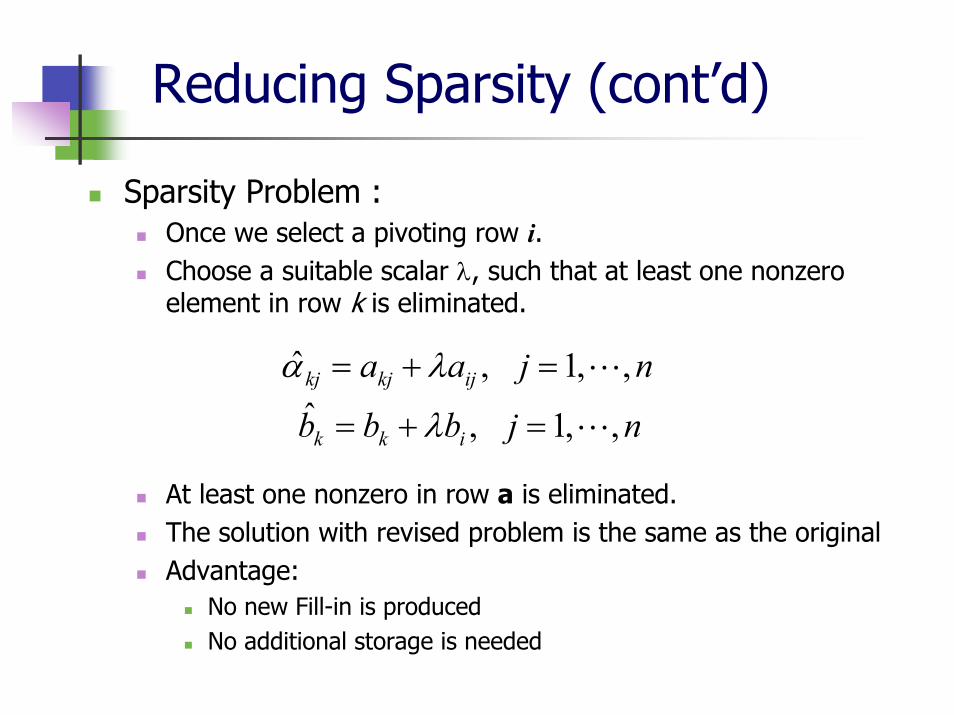

Sparsity Problem :Once we select a pivoting row i.Choose a suitable scalar λ, such that at least one nonzero element in row k is eliminated.

At least one nonzero in row a is eliminated.The solution with revised problem is the same as the originalAdvantage:

No new Fill-in is producedNo additional storage is needed

njaa ijkjkj ,,1,ˆ =+= λα

njbbb ikk ,,1,ˆ =+= λ

Making A Full Rank

Finding Linear dependency

Trivial reduction by identifying linearly dependent equalities.

Implemented efficiently based on Gaussian elimination

Advanced Techniques

Theoretically, Gaussian Elimination can be used to check the dependency of the rows.

For system A x = b, we combine matrix A(mxn) with vector b to get the matrix A = [A | b ] with the size of m(n+1).

A sequence of elementary row operations can be applied to the rows in matrix A to identify its rank.

Implementation goal:Avoid creating much fill-inKeep numerical stabilityObjective: just find linearly dependent rows

Preprocessing Scheme

The usual order of actions during preprocessing is:i. Problem Reformulationii. Presolveiii. Scaling

PresolveIt is not necessary to include all discussed techniquesSome more test from other references can be added.

Preprocessing Scheme

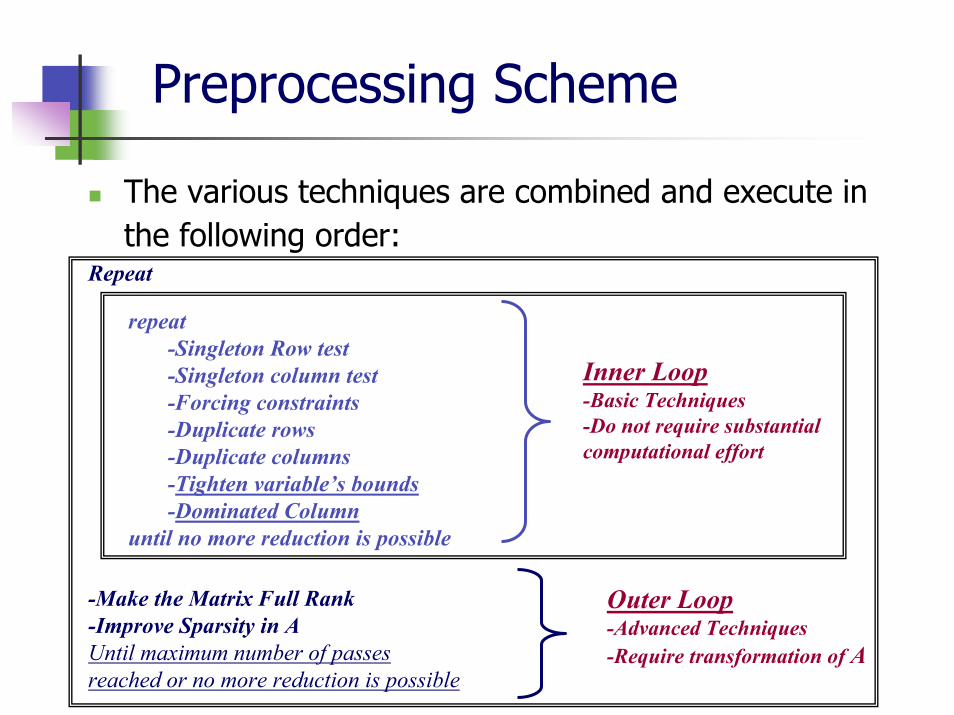

The various techniques are combined and execute in the following order:

Repeat

-Make the Matrix Full Rank-Improve Sparsity in AUntil maximum number of passes reached or no more reduction is possible

Outer Loop-Advanced Techniques-Require transformation of A

Inner Loop-Basic Techniques-Do not require substantial computational effort

repeat-Singleton Row test -Singleton column test-Forcing constraints-Duplicate rows-Duplicate columns-Tighten variable’s bounds-Dominated Column

until no more reduction is possible

Preprocessing Scheme

Preprocessing Scheme

Significant part of the total reduction is done in the inner loop

In the outer loop the techniques require algebraic transformation of matrix A, therefore this are the most costly operations.

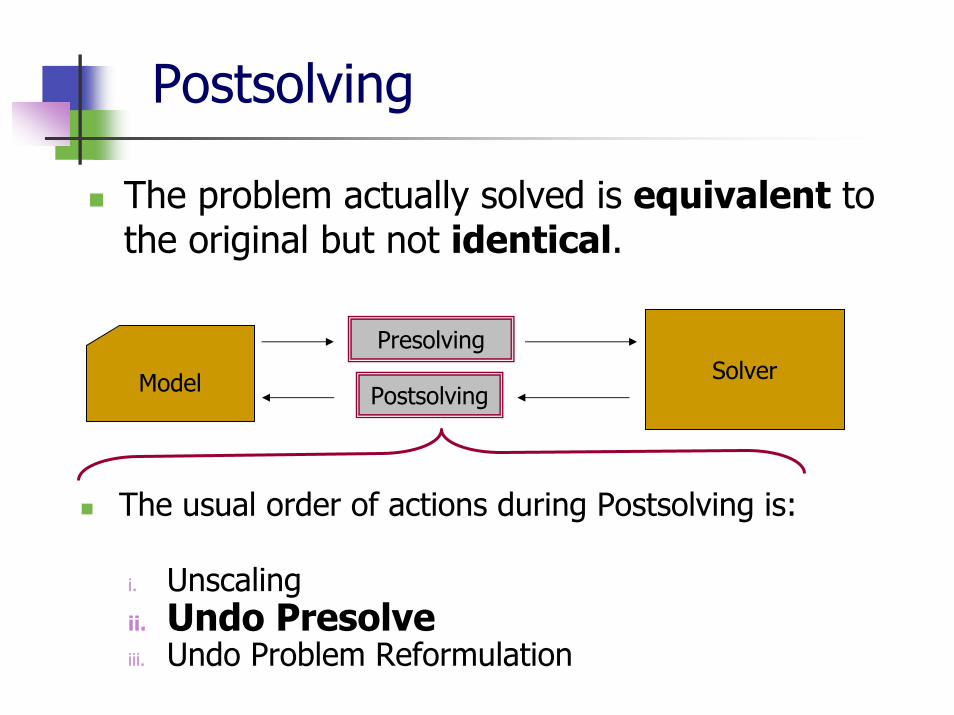

Postsolving

The problem actually solved is equivalent to the original but not identical.

Model SolverPostsolving

Presolving

The usual order of actions during Postsolving is:

i. Unscalingii. Undo Presolveiii. Undo Problem Reformulation

Postsolving

Postsolving operations are necessary after solving the preprocess problem.

Present a full primal-dual optimal solutions of the original solution.

from the optimal basis solution of the preprocessed problem.

Create an optimal basis solution of the original problem.

from the optimal basis solution of the preprocessed problem.

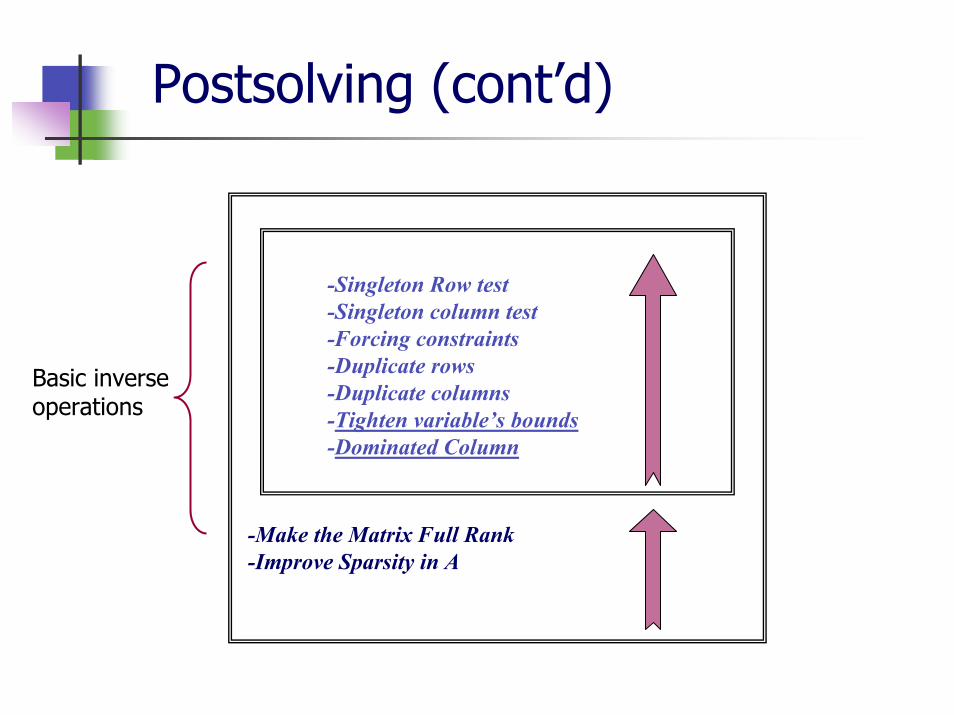

Postsolving (cont’d)

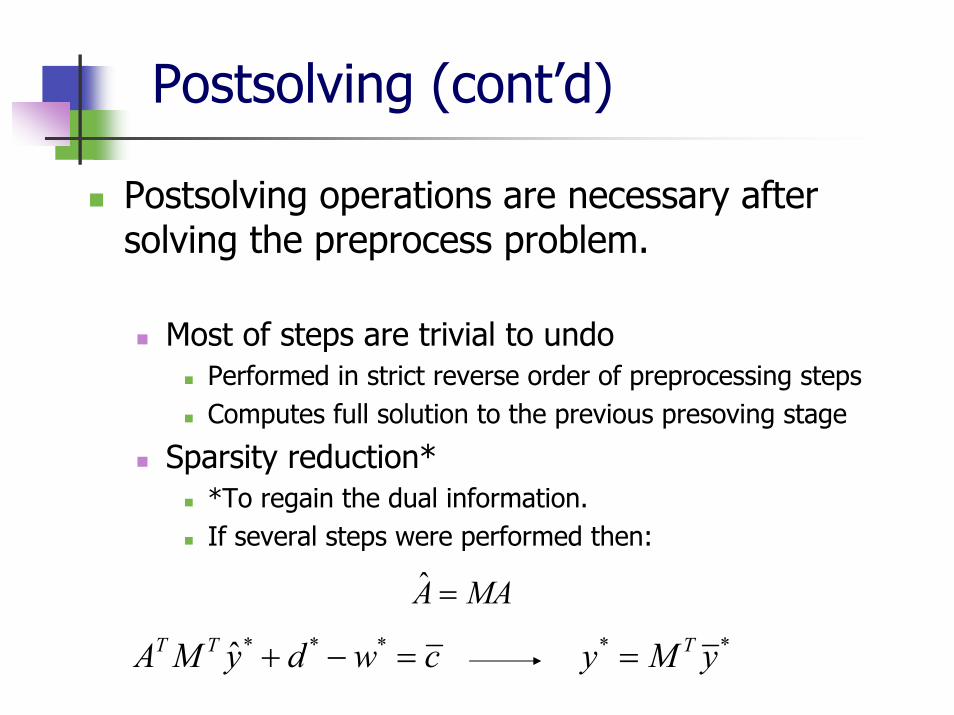

Postsolving operations are necessary after solving the preprocess problem.

Most of steps are trivial to undoPerformed in strict reverse order of preprocessing stepsComputes full solution to the previous presoving stage

Sparsity reduction**To regain the dual information.If several steps were performed then:

MAA =ˆ

cwdyMA TT =−+ ***ˆ ** yMy T=

Postsolving (cont’d)

-Make the Matrix Full Rank-Improve Sparsity in A

-Singleton Row test -Singleton column test-Forcing constraints-Duplicate rows-Duplicate columns-Tighten variable’s bounds-Dominated Column

Basic inverseoperations

Preprocessing in SDP

Jonathan Li

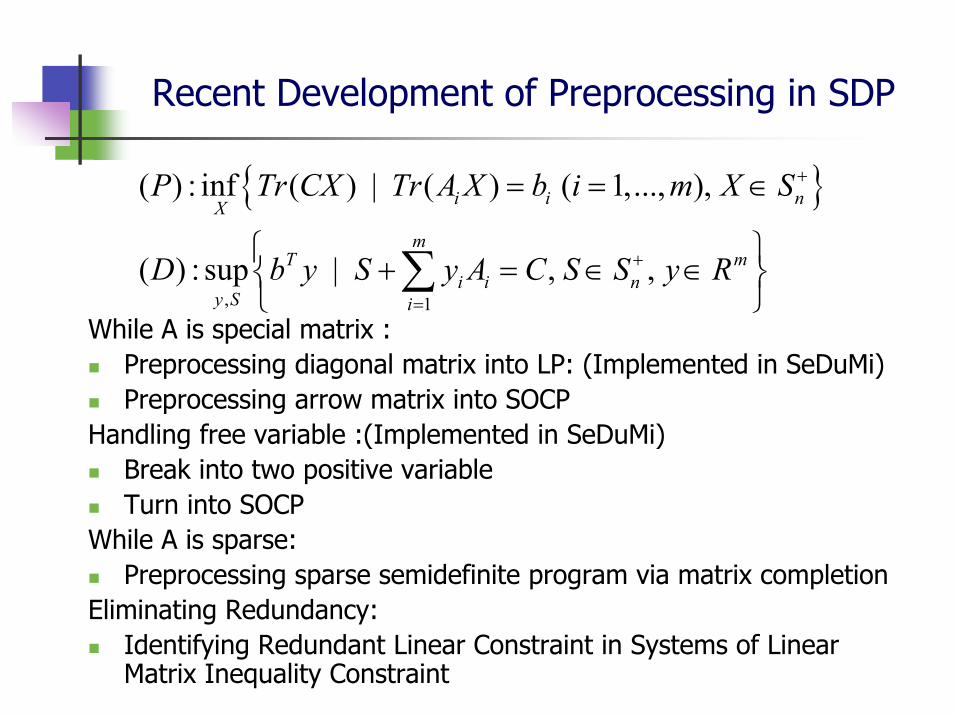

Recent Development of Preprocessing in SDP

While A is special matrix : Preprocessing diagonal matrix into LP: (Implemented in SeDuMi)Preprocessing arrow matrix into SOCP

Handling free variable :(Implemented in SeDuMi)Break into two positive variableTurn into SOCP

While A is sparse:Preprocessing sparse semidefinite program via matrix completion

Eliminating Redundancy:Identifying Redundant Linear Constraint in Systems of Linear Matrix Inequality Constraint

{ }

, 1

( ) : inf ( ) | ( ) ( 1,..., ),

( ) : sup | , ,

i i nX

mT m

i i ny S i

P Tr CX Tr A X b i m X S

D b y S y A C S S y R

+

+

=

= = ∈

⎧ ⎫+ = ∈ ∈⎨ ⎬

⎩ ⎭∑

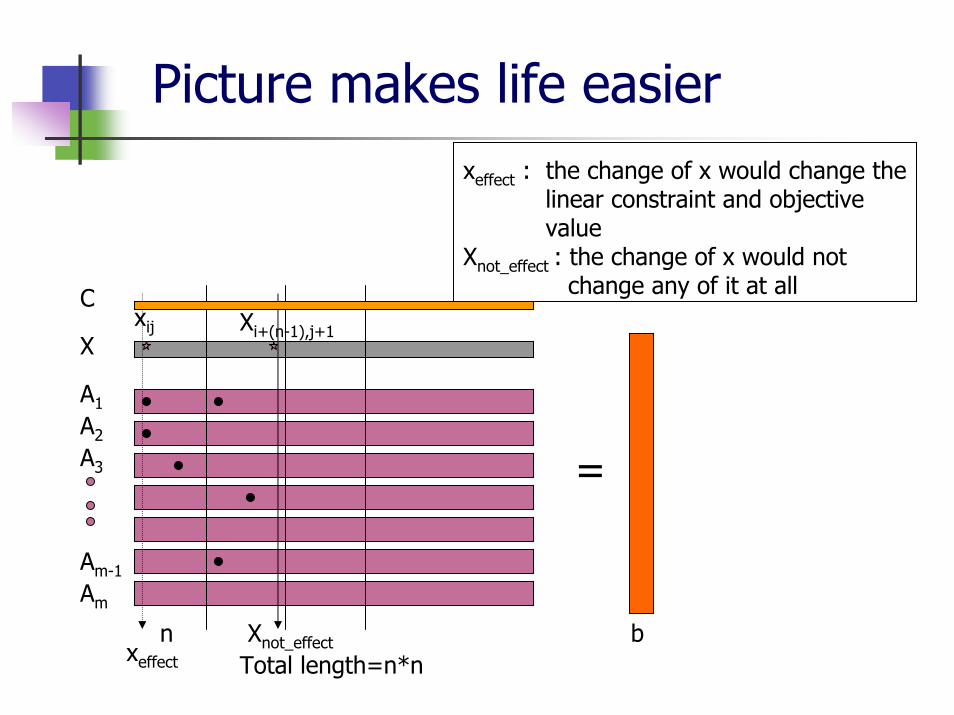

Picture makes life easier

A1

A2

A3

xeffect : the change of x would change the linear constraint and objective value

Xnot_effect : the change of x would not change any of it at all

Am-1

Am

X

Total length=n*nn

=

b

xij Xi+(n-1),j+1

xeffect

Xnot_effect

C

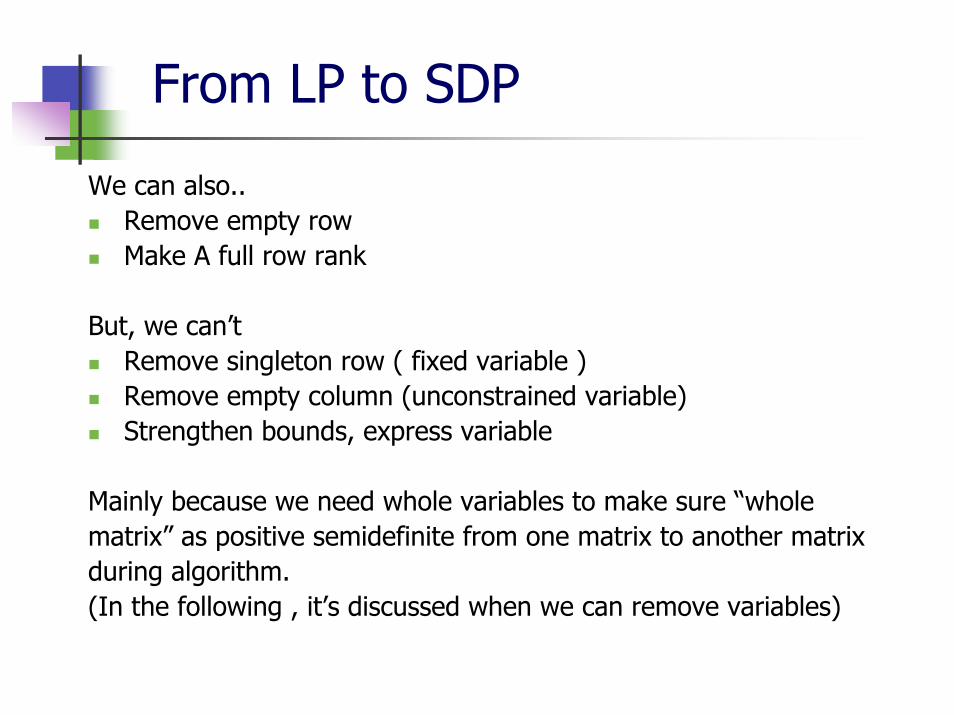

From LP to SDP

We can also..Remove empty row Make A full row rank

But, we can’t Remove singleton row ( fixed variable )Remove empty column (unconstrained variable)Strengthen bounds, express variable

Mainly because we need whole variables to make sure “whole matrix” as positive semidefinite from one matrix to another matrix during algorithm. (In the following , it’s discussed when we can remove variables)

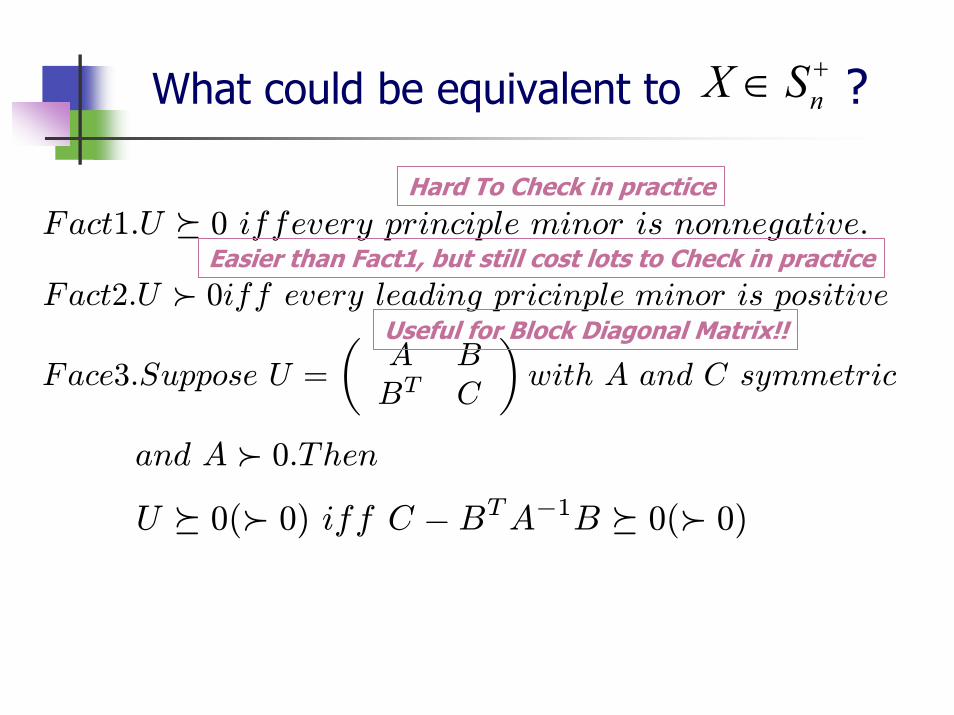

What could be equivalent to ?nX S +∈

Fact1.U º 0 iffevery principle minor is nonnegative.

Fact2.U Â 0iff every leading pricinple minor is positive

Face3.Suppose U =

µA BBT C

¶with A and C symmetric

and A Â 0.Then

U º 0(Â 0) iff C − BTA−1B º 0(Â 0)

Hard To Check in practice

Easier than Fact1, but still cost lots to Check in practice

Useful for Block Diagonal Matrix!!

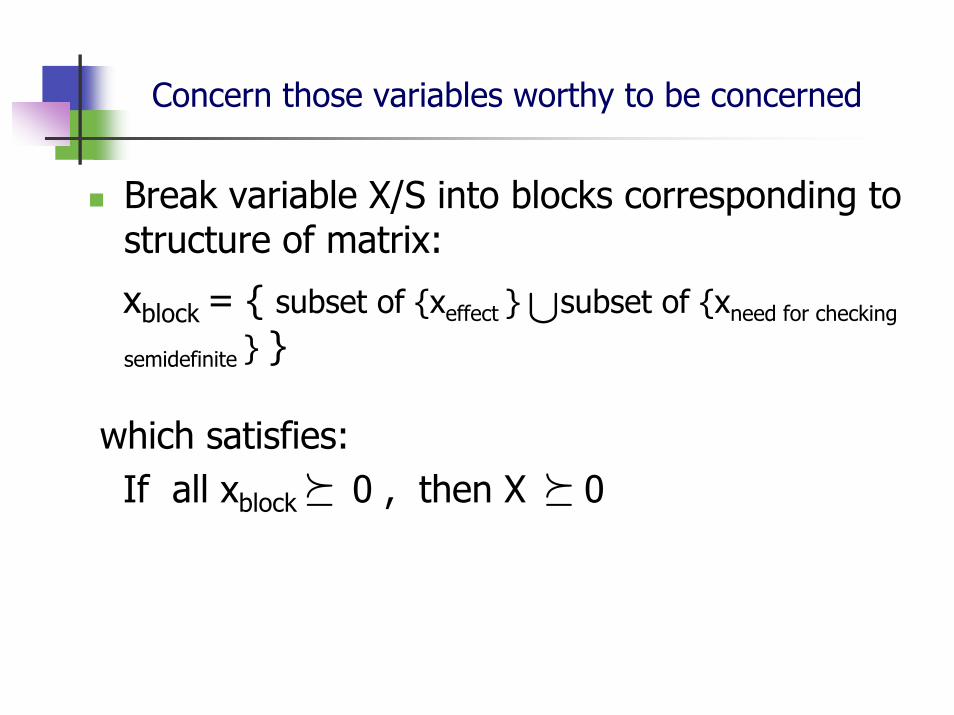

Concern those variables worthy to be concerned

Break variable X/S into blocks corresponding to structure of matrix:

xblock = { subset of {xeffect } subset of {xneed for checking

semidefinite } }

which satisfies:If all xblock 0 , then X 0

∪

º º

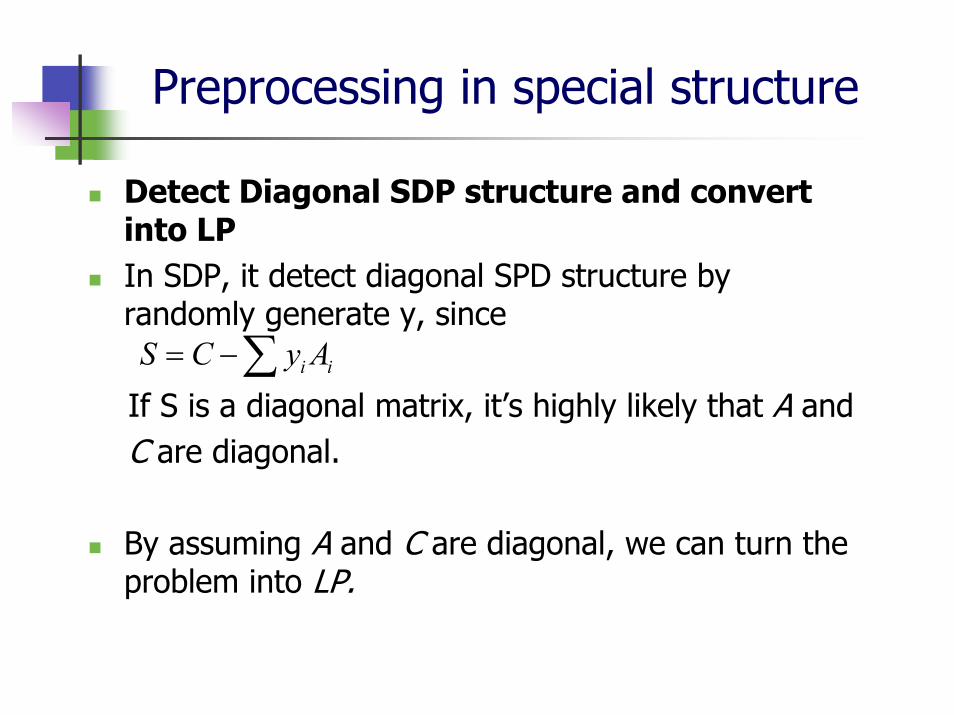

Preprocessing in special structure

Detect Diagonal SDP structure and convert into LP In SDP, it detect diagonal SPD structure by randomly generate y, since

If S is a diagonal matrix, it’s highly likely that A and C are diagonal.

By assuming A and C are diagonal, we can turn the problem into LP.

i iS C y A= −∑

Preprocessing in SeDuMi

Detect two same coefficient column in LPIn LP, if we have free variable, it’s usually handled by splitting it into two positive variables so as to fit LP standard form.Ex.xfree = xa – xb , where xa ,xb ≥ 0

However, in contrast to above technique, which wastes lots of memory and computation time, SeDuMi put free variable in a quadratic cone instead of splitting, which save memory and perform well.

As we know, SeDuMi has SOCP solver, we can transform the problem into it.

Preprocessing sparse semidefinite program via matrix completion

In the paper : Preprocessing sparse semidefinite program via matrix completion, a heuristic is proposed to handle SDP problem while data matrix A is sparse.

Basic idea : Reduce the overload from computing and storing those “0” in sparse matrix.

Matrix completion : During computing, it tries to concern only those variablesaffecting linear part, in the mean time, it guarantees the feasibility of those variables being left out to eventually satisfy whole matrix as positive semidefinite.

Preprocessing sparse semidefinite program via matrix completion

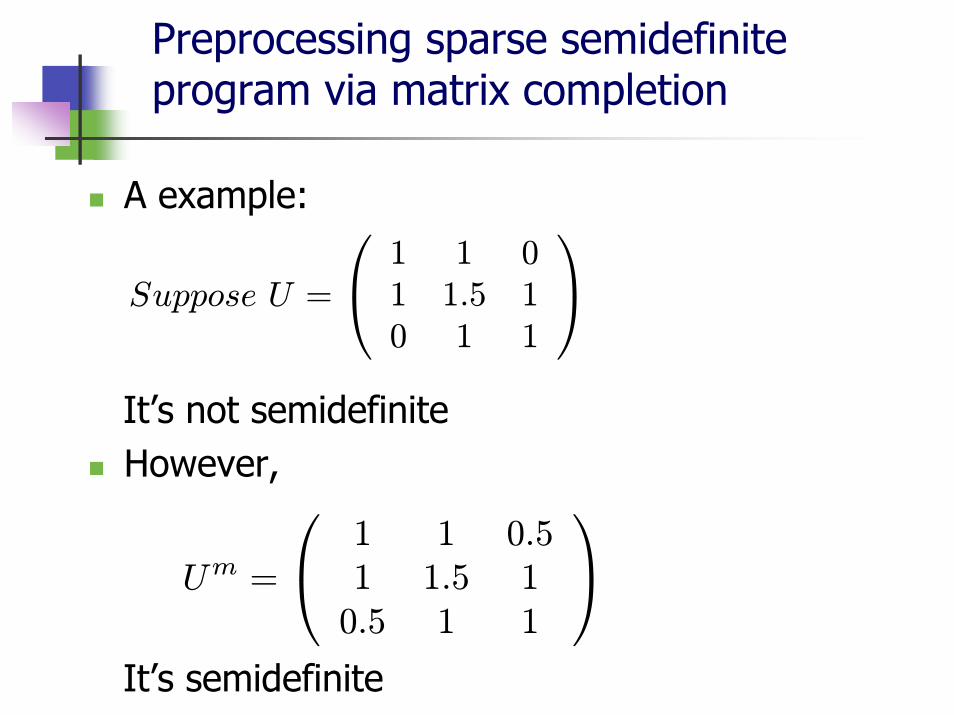

A example:

It’s not semidefiniteHowever,

It’s semidefinite

Suppose U =

⎛⎝ 1 1 01 1.5 10 1 1

⎞⎠

Um =

⎛⎝ 1 1 0.51 1.5 10.5 1 1

⎞⎠

Preprocessing sparse semidefinite program via matrix completion

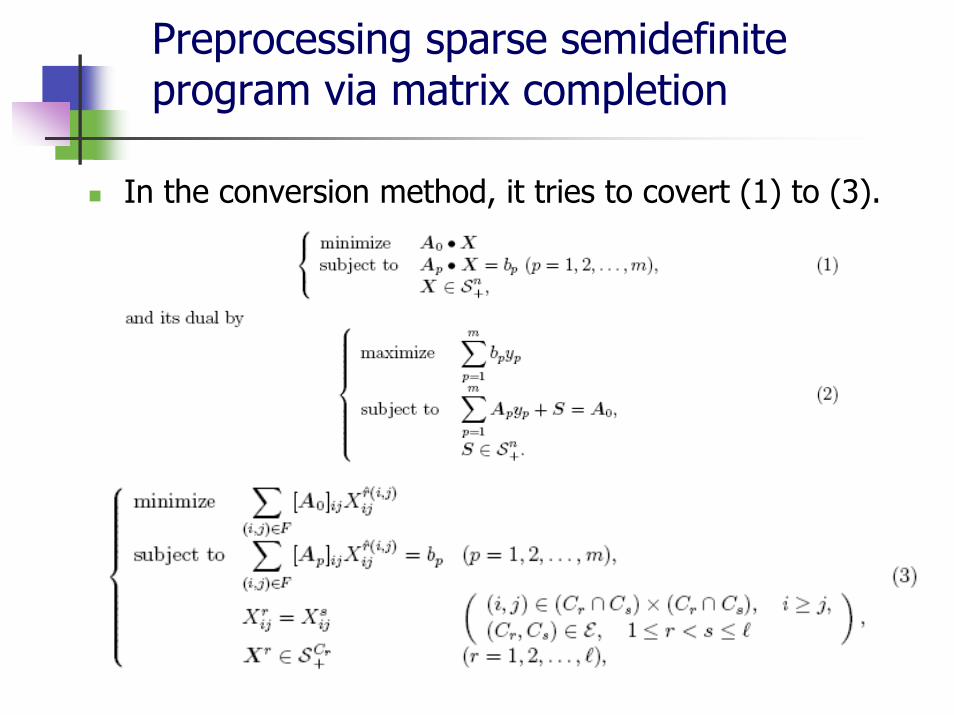

In the conversion method, it tries to covert (1) to (3).

Preprocessing sparse semidefinite program via matrix completion

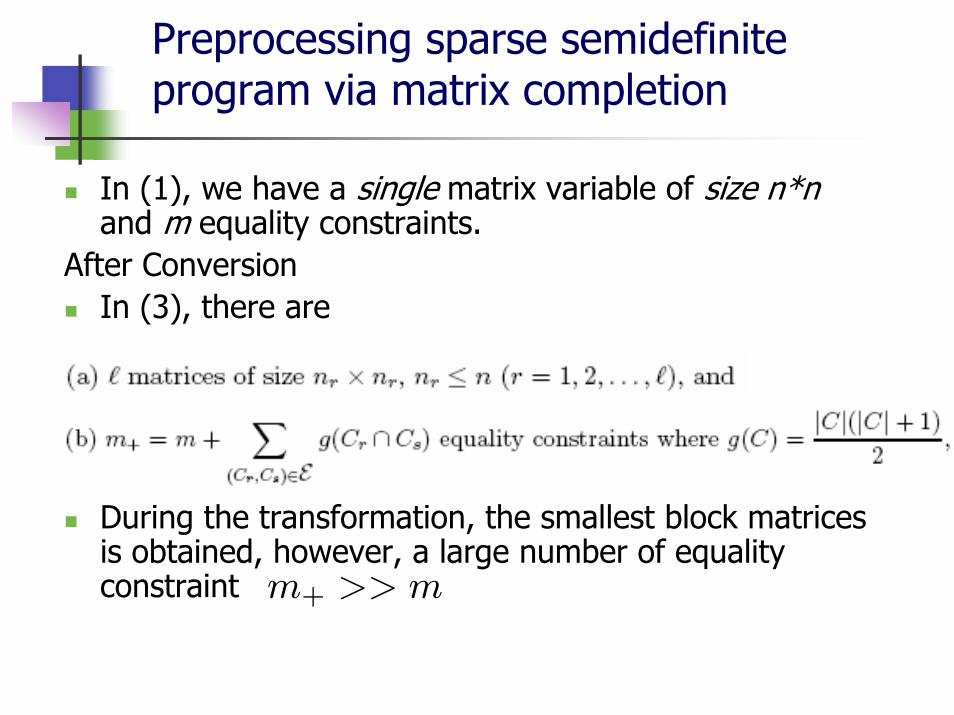

In (1), we have a single matrix variable of size n*nand m equality constraints.

After ConversionIn (3), there are

During the transformation, the smallest block matrices is obtained, however, a large number of equality constraint m+ >> m

Preprocessing sparse semidefinite program via matrix completion

One of the keys to obtaining a good conversion is to balance the factors (a) and (b) above to minimize the number of flops required by an SDP solver.

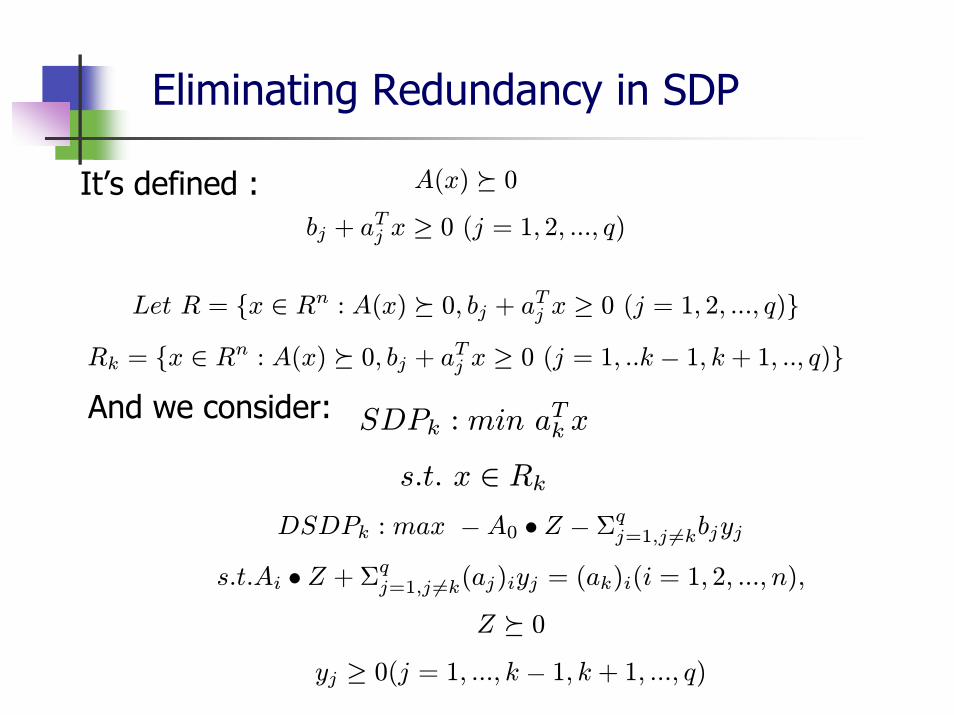

Eliminating Redundancy in SDP

Identifying Redundant Linear Constraint in Systems of Linear Matrix Inequality Constraint

In LP, eliminating redundant constraint is a basic technique, in SDP, it’s more difficult to eliminate Linear constraint when we take the cone into consideration also.

Eliminating Redundancy in SDP

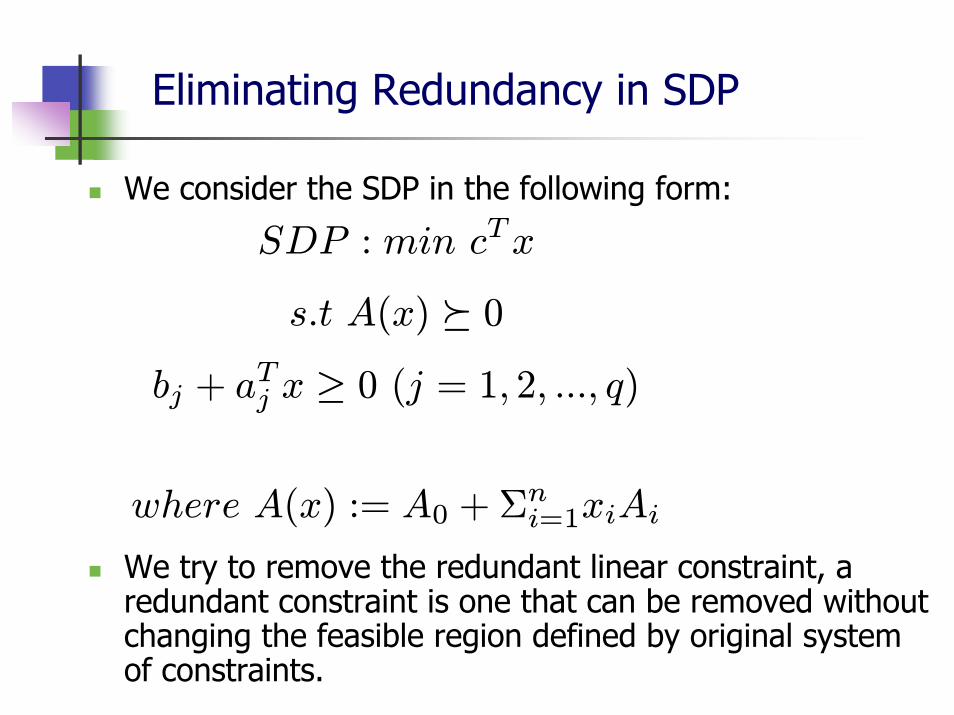

We consider the SDP in the following form:

We try to remove the redundant linear constraint, a redundant constraint is one that can be removed without changing the feasible region defined by original system of constraints.

SDP : min cTx

s.t A(x) º 0

bj + aTj x ≥ 0 (j = 1, 2, ..., q)

where A(x) := A0 + Σni=1xiAi

Eliminating Redundancy in SDP

A(x) º 0

bj + aTj x ≥ 0 (j = 1, 2, ..., q)

Let R = {x ∈ Rn : A(x) º 0, bj + aTj x ≥ 0 (j = 1, 2, ..., q)}

Rk = {x ∈ Rn : A(x) º 0, bj + a

Tj x ≥ 0 (j = 1, ..k − 1, k + 1, .., q)}

It’s defined :

And we consider: SDPk : min aTk x

s.t. x ∈ Rk

DSDPk : max − A0 • Z − Σqj=1,j 6=kbjyj

s.t.Ai • Z + Σqj=1,j 6=k(aj)iyj = (ak)i(i = 1, 2, ..., n),

Z º 0

yj ≥ 0(j = 1, ..., k − 1, k + 1, ..., q)

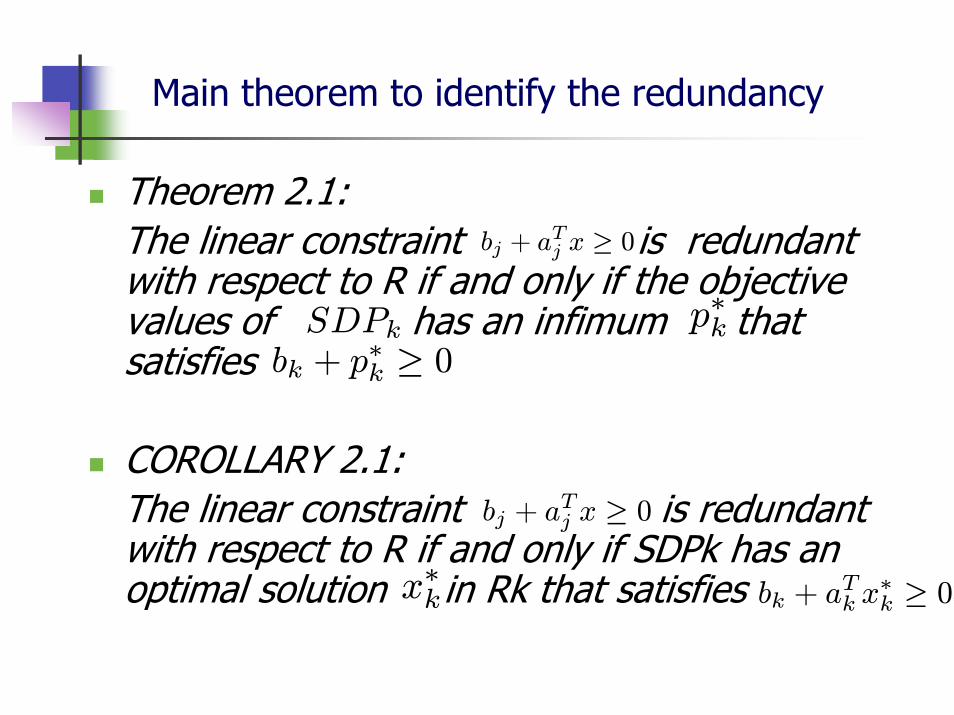

Main theorem to identify the redundancy

Theorem 2.1:The linear constraint is redundant with respect to R if and only if the objective values of has an infimum that satisfies

COROLLARY 2.1:The linear constraint is redundant with respect to R if and only if SDPk has an optimal solution in Rk that satisfies

bj + aTj x ≥ 0

SDPk p∗kbk + p

∗k ≥ 0

bj + aTj x ≥ 0

x∗k bk + aTk x∗k ≥ 0

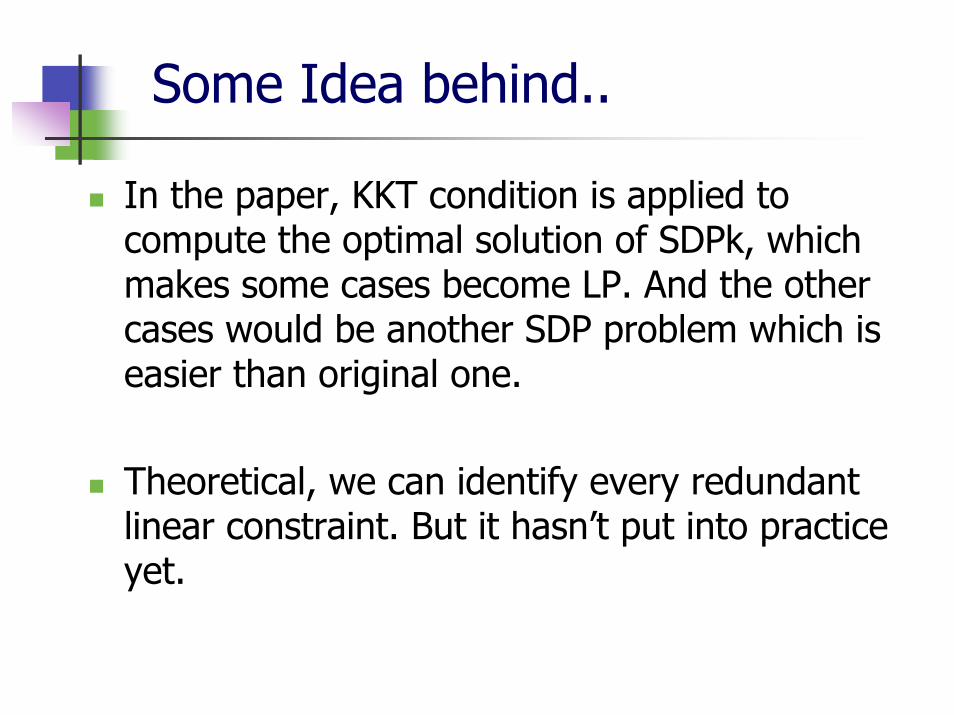

Some Idea behind..

In the paper, KKT condition is applied to compute the optimal solution of SDPk, which makes some cases become LP. And the other cases would be another SDP problem which is easier than original one.

Theoretical, we can identify every redundant linear constraint. But it hasn’t put into practice yet.

References

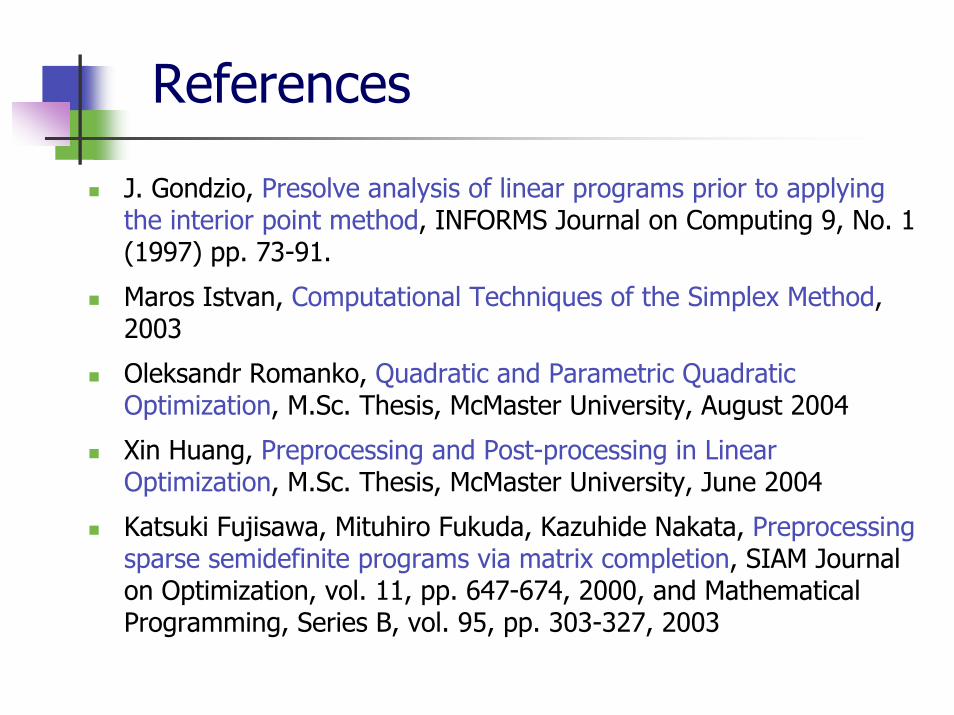

J. Gondzio, Presolve analysis of linear programs prior to applying the interior point method, INFORMS Journal on Computing 9, No. 1 (1997) pp. 73-91.

Maros Istvan, Computational Techniques of the Simplex Method, 2003

Oleksandr Romanko, Quadratic and Parametric Quadratic Optimization, M.Sc. Thesis, McMaster University, August 2004

Xin Huang, Preprocessing and Post-processing in Linear Optimization, M.Sc. Thesis, McMaster University, June 2004

Katsuki Fujisawa, Mituhiro Fukuda, Kazuhide Nakata, Preprocessing sparse semidefinite programs via matrix completion, SIAM Journal on Optimization, vol. 11, pp. 647-674, 2000, and Mathematical Programming, Series B, vol. 95, pp. 303-327, 2003