prabhatdairy: the bread and butter of the dairy industryprabhatdairy: the bread and butter of the...

TRANSCRIPT

Prabhat Dairy:The Bread and Butter of the Dairy IndustryHEC CONSULTANTS:

MARJOLAINE BERGERON, FELICIA PARR, RYAN WILSON, REBECA YANG

Introduction

Founded in 1998 to capitalize on market opportunities

Largely B2C business, with gradual shift. Revenues:B2B: 89% (2012) vs. 70% (2016)B2C: 11% (2012) vs. 30% (2016)

IPO in 2015 raises 3 billion rupees

Largely operate out of Maharashtra, with limited presence in north and east of Mumbai

Competitive advantage: End to end involvement in the dairy industry (sourcing and selling)

Large market with substantial growth opportunities

Introduction Analysis Alternatives Recommendation Implementation Conclusion

HOW CAN PRABHAT DAIRY BEST GROW IN THE INDIAN DAIRY INDUSTRY?

RecommendationIntroduction Analysis Alternatives Recommendation Implementation Conclusion

• Increase cash flow• Consumer trends

Increase focus on B2C in order to achieve a 50/50 split

• Gujarat• Rajastan

1. Regional development in Maharashtra with geographic expansion to Tier 2 and Tier 3 cities in:

2. Product development in order to meet Tier 1 (Mumbai) needs in Maharastra

India’s Social LandscapeIntroduction Analysis Alternatives Recommendation Implementation Conclusion

Economy• Wealth disparity• Rural vs urban distribution• Growing economy• Growing middle class

Political• High government power• Governmental help to

Indian companies

Geographic• Difficult infrastructure• Tier 1-2-3 cities• Large country

Cultural• Multiple languages• Difference in preferences

(milk products)

Prabhat has been very successful in is own country. The company has an advantage

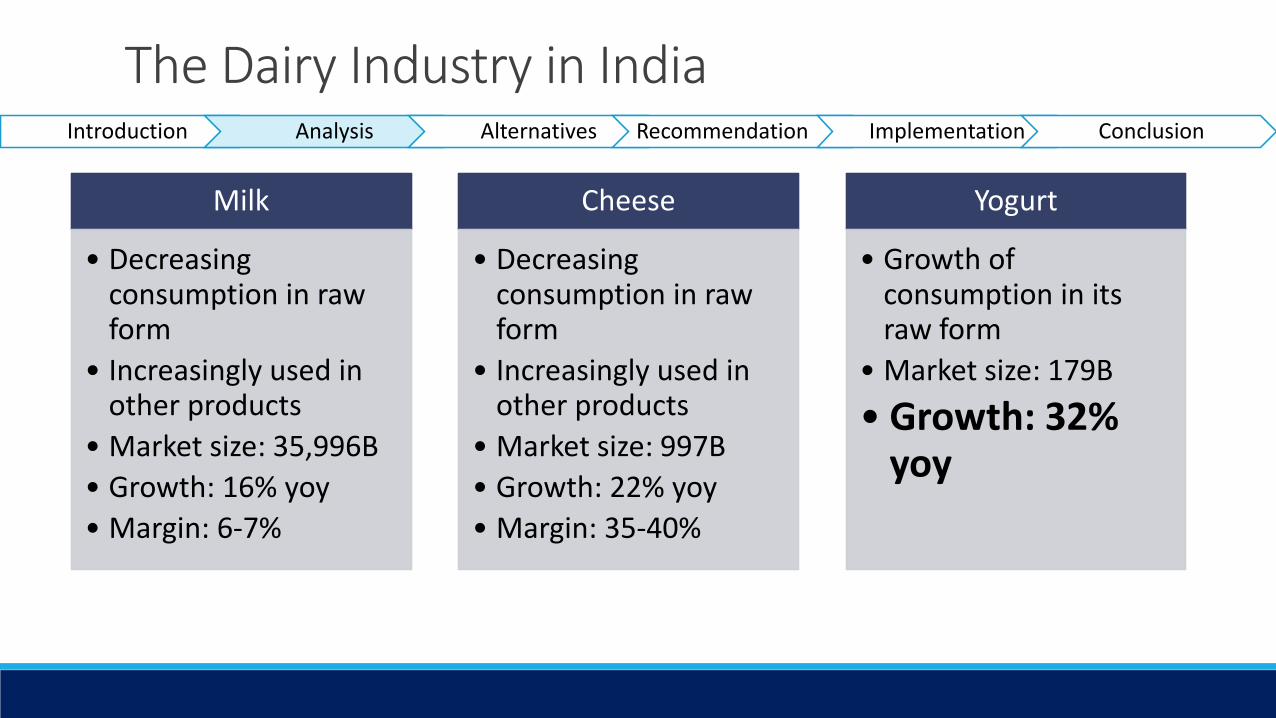

The Dairy Industry in IndiaIntroduction Analysis Alternatives Recommendation Implementation Conclusion

Milk

• Decreasing consumption in raw form

• Increasingly used in other products

• Market size: 35,996B• Growth: 16% yoy• Margin: 6-7%

Cheese

• Decreasing consumption in raw form

• Increasingly used in other products

• Market size: 997B• Growth: 22% yoy• Margin: 35-40%

Yogurt

• Growth of consumption in its raw form

• Market size: 179B• Growth: 32%

yoy

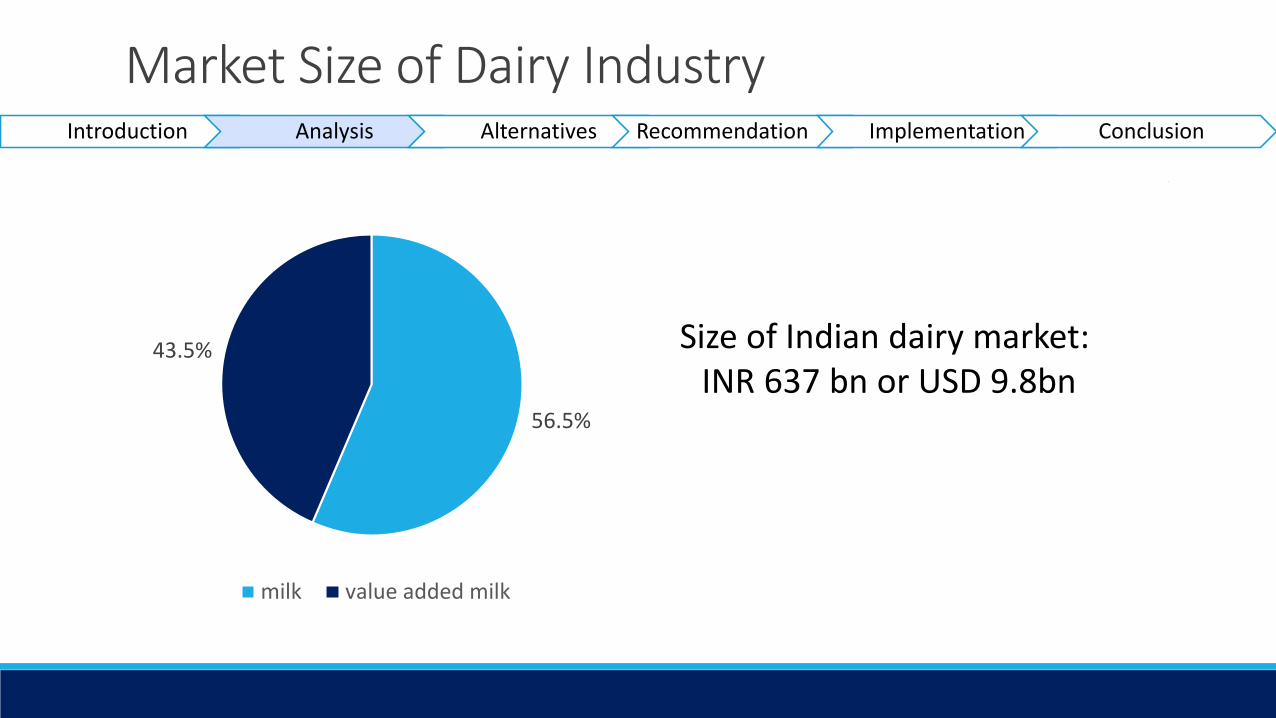

Market Size of Dairy IndustryIntroduction Analysis Alternatives Recommendation Implementation Conclusion

56.5%

43.5%

milk value added milk

Size of Indian dairy market: INR 637 bn or USD 9.8bn

Competitive LandscapeIntroduction Analysis Alternatives Recommendation Implementation Conclusion

Cooperatives• Highest market share• Highest market coverage• 10-15% milk

procurement players• Vertically integrated

Multinational companies (Danone, Nestle, Mondelez)• Value added market

mainly• Higher pricing (15%

more)

Private domestic players (pure play

dairy companies and dairy division)

CompetitionIntroduction Analysis Alternatives Recommendation Implementation Conclusion

Kwality Hatsun AgroPrabhat Parag

22.4% 23.6% 10.6% 25.5%Gross Margins

Competitors have different profiles and margins

The Dairy Industry : Supply ChainIntroduction Analysis Alternatives Recommendation Implementation Conclusion

Farmers

Milk Cooperatives

Own outlets, retail stores

Private Dairies

Own outlets, retail stores

Private Traders

Restaurants, private shops

Private milk vendors

Customers

• 7% supply growth vs. 10% demand

• Access to suppliers: 65 million farmers are outside of the cooperative system

Shift towards B2CIntroduction Analysis Alternatives Recommendation Implementation Conclusion

0 200 400 600 800 1000 1200 1400

2015

2016

Revenues in INR 10M

B2B B2C

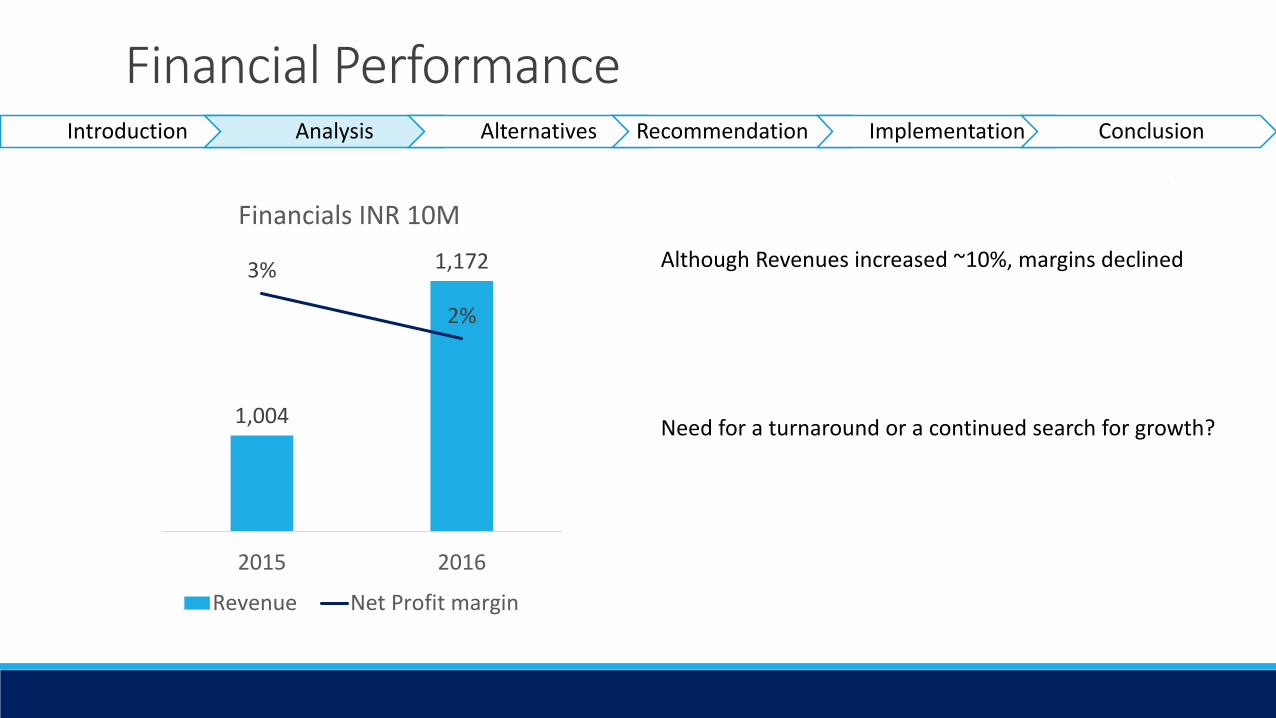

Financial PerformanceIntroduction Analysis Alternatives Recommendation Implementation Conclusion

1,004

1,1723%

2%

0%

1%

1%

2%

2%

3%

3%

900

950

1,000

1,050

1,100

1,150

1,200

2015 2016

Financials INR 10M

Revenue Net Profit margin

Although Revenues increased ~10%, margins declined

Need for a turnaround or a continued search for growth?

Prabhat Analysis

Present in both B2B and B2C marketsManufacturing plants (2016)

Product innovationDistribution network (milk collection

points + chilling center)Competitive pricing (15% lower)

Liquidity + cash flow difficultiesB2C branding (non-uniformity)

Only present in one state

Growing GDP per capita in IndiaGrowing demand for dairy products (10%

in India)Many Indian farmers are not part of

cooperativesProfitability in B2C market

Politically sensitive industryCompetitions (coop. And MNC’s)

Increasing price of cattle fodder + milk)Infrastructure in India not fully

developped

S W

O T

Introduction Analysis Alternatives Recommendation Implementation Conclusion

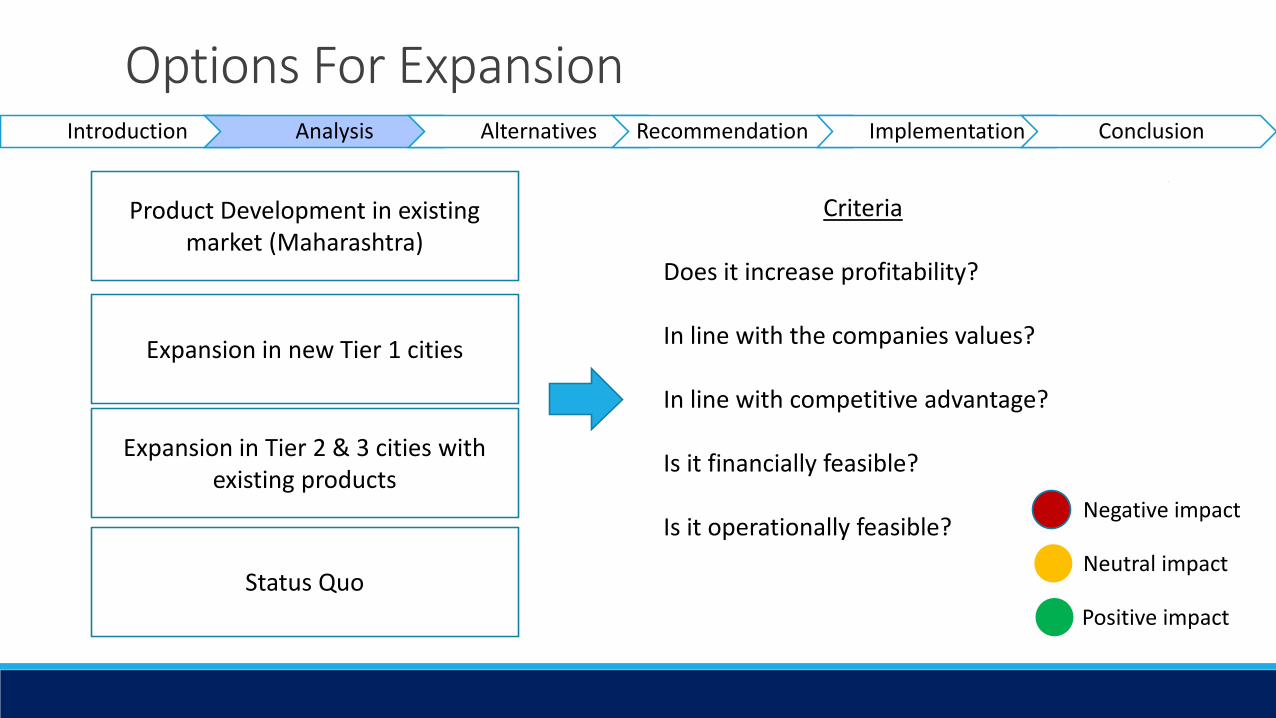

Options For Expansion

Product Development in existing market (Maharashtra)

Expansion in new Tier 1 cities

Expansion in Tier 2 & 3 cities with existing products

Status Quo

Criteria

Does it increase profitability?

In line with the companies values?

In line with competitive advantage?

Is it financially feasible?

Is it operationally feasible?Negative impact

Neutral impact

Positive impact

Introduction Analysis Alternatives Recommendation Implementation Conclusion

Alternative Evaluation

Alternatives Does it increaseprofitability?

Is it in line withcompanyvalues?

Is it in line withthe competitive

advantage?

Is it financiallyfeasible?

Is itoperationally

feasible?

ProductDevelopmentExpand to NEWTier 1 cities

Tier 2 & 3 citieswith existingproductsStatus Quo

Introduction Analysis Alternatives Recommendation Implementation Conclusion

RecommendationIntroduction Analysis Alternatives Recommendation Implementation Conclusion

• Increase cash flow• Consumer trends

Increase focus on B2C in order to achieve a 50/50 split

• Gujarat• Rajastan

1. Regional development in Maharashtra with geographic expansion to Tier 2 and Tier 3 cities in:

2. Product development in order to meet Tier 1 (Mumbai) needs in Maharastra

1 – Expand using existing productsIntroduction Analysis Alternatives Recommendation Implementation Conclusion

Easy access to 65M non-cooperative suppliers

Competitive pricing

Distribution channel success

Successful brand

Lower income consumers

Into Tier 2 and Tier 3 cities

3 states:- Maharashtra- Rajastan- Gujarat

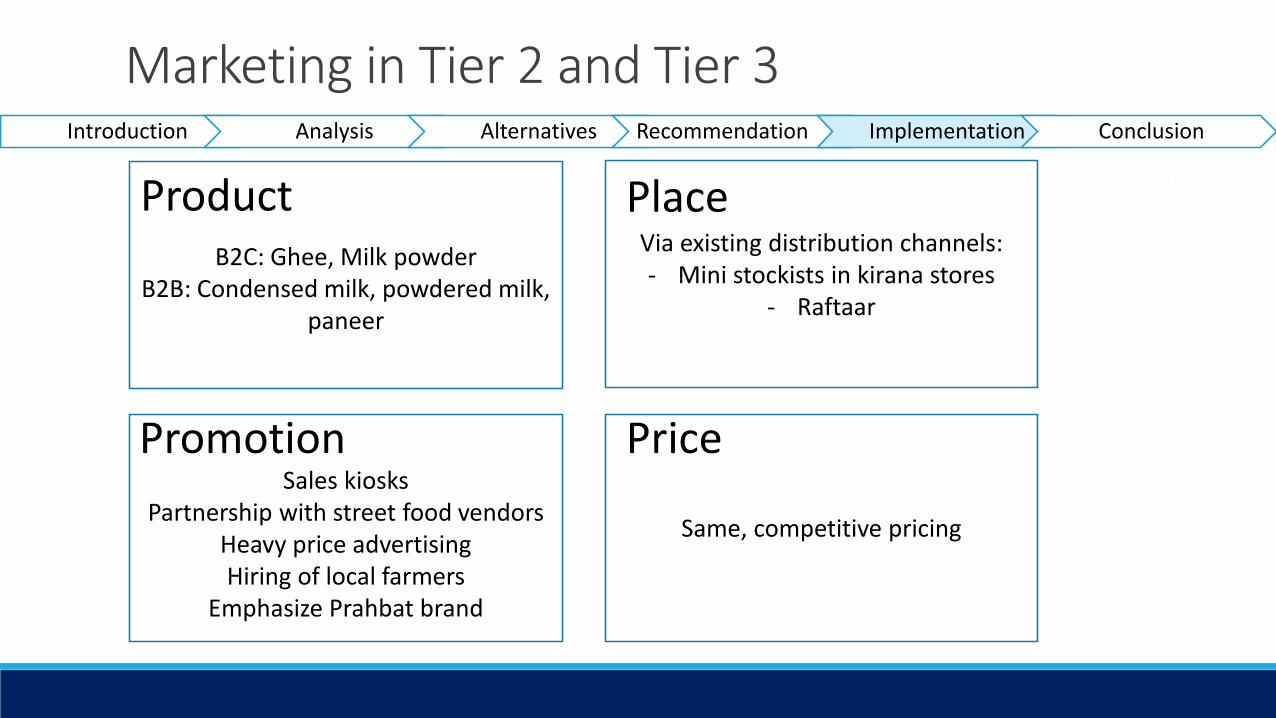

Marketing in Tier 2 and Tier 3 Introduction Analysis Alternatives Recommendation Implementation Conclusion

B2C: Ghee, Milk powderB2B: Condensed milk, powdered milk,

paneer

Via existing distribution channels:- Mini stockists in kirana stores

- Raftaar

Sales kiosksPartnership with street food vendors

Heavy price advertisingHiring of local farmers

Emphasize Prahbat brand

Same, competitive pricing

Product Place

Promotion Price

Implementation Timeline: Existing productsIntroduction Analysis Alternatives Recommendation Implementation Conclusion

2017H1

2017H2

2018H1

2018H2

2019H1

2019H2

2020H1

2020H2

2021H1

2021H2

Expansion into Tier 2 and Tier 3 in Maharastra

Implement existing distribution strategies

Develop marketing plan

Product launch

Product and marketing assessement

Expansion into Tier 2 and Tier 3 in Rajastan and Gujarat

Market research

Increase processing capacities

Develop distribution network

Launch in state 1 & 2

2 – Develop new product in MumbaiIntroduction Analysis Alternatives Recommendation Implementation Conclusion

Higher price sensitivity

Competitive pricing

Rapid growth in yogurt consumption projected

Successful brand

Higher end tastes

New, higher-end greek“Flava”yogurt product inMumbai as a pilot project

Marketing for “Flava” YogurtIntroduction Analysis Alternatives Recommendation Implementation Conclusion

Greek yogurt under “Flava” namePartnership with local grocery store

chain

Emphasize competitive pricingAdvertise health aspects

Under successful Flava nameHigh quality goods

Social media campaign – Make your own

340 Rupees

Product Place

Promotion Price

Implementation Timeline: New ProductIntroduction Analysis Alternatives Recommendation Implementation Conclusion

2017H1

2017H2

2018H1

2018H2

2019H1

2019H2

2020H1

2020H2

2021H1

2021H2

Market & operationsresearch

Research & development

Develop marketing plan

Product launch

Product and marketing assessement

What this recommendation means

Problem Our SolutionDevelop product offering for brand competencies?

Pilot Project: Develop new, higher end greekyogurt brand “Flava” to be in line with consumer trends

Where should you distribute in order to expand B2C presence?

Use existing distribution competencies for Tier 2 and Tier 3 cities and form partnership in grocery stores in Mumbai for new product

How can you increase profitability and enhance working capital?

Growth will increase working capitalPenetration of B2C markets with existing and new products will increase profitability

Introduction Analysis Alternatives Recommendation Implementation Conclusion

These solutions will help you be successful in meeting your goal of achieving 50-50 B2B: B2C

Financial AssumptionsIntroduction Analysis Alternatives Recommendation Implementation Conclusion

050

100150200250300350400450

2017 2018 2019 2020 2021

New product investments & expenses INR M

DistributionPersonnelMarketingMarket ResearchProduct Development

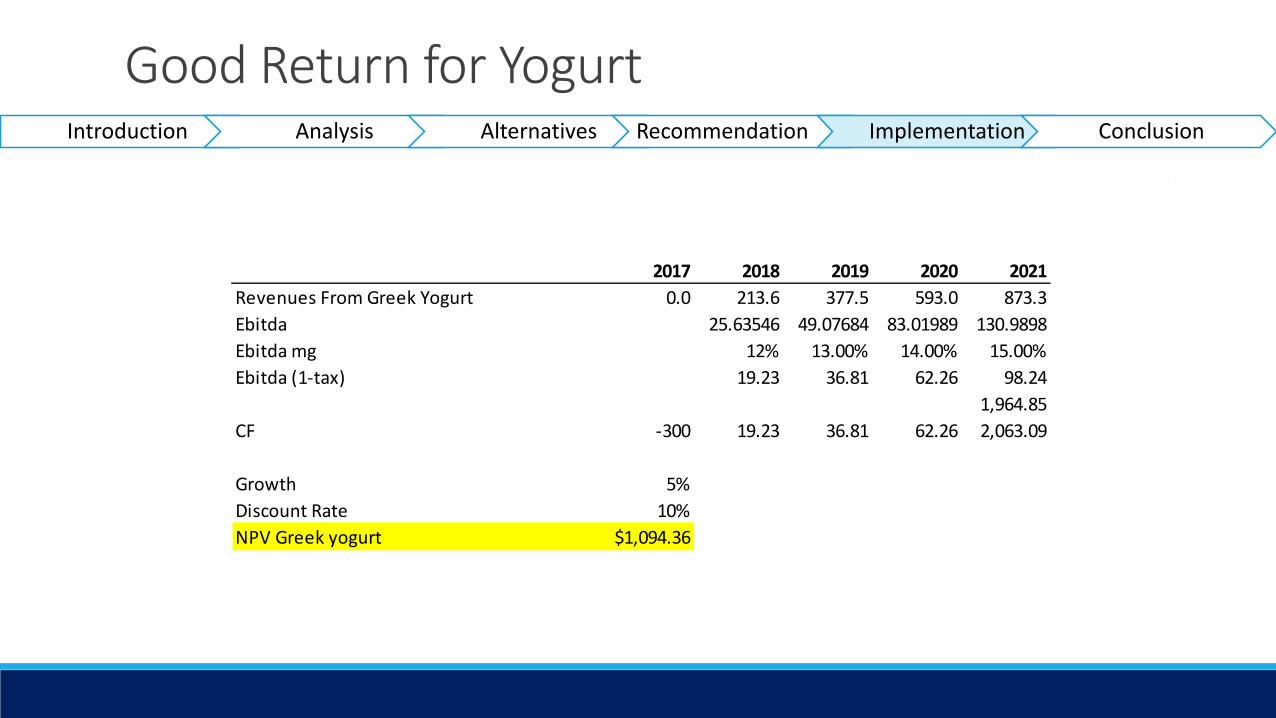

Good Return for YogurtIntroduction Analysis Alternatives Recommendation Implementation Conclusion

2017 2018 2019 2020 2021Revenues From Greek Yogurt 0.0 213.6 377.5 593.0 873.3Ebitda 25.63546 49.07684 83.01989 130.9898Ebitda mg 12% 13.00% 14.00% 15.00%Ebitda (1-tax) 19.23 36.81 62.26 98.24

1,964.85CF -300 19.23 36.81 62.26 2,063.09

Growth 5%Discount Rate 10%NPV Greek yogurt $1,094.36

Financial AssumptionsIntroduction Analysis Alternatives Recommendation Implementation Conclusion

020406080

100120140160

2017 2018 2019 2020 2021

Expansion T2&T3 investments & expenses INR M

LaunchesDistributionHigher Production CapabilitiesMarket Research

Good Return for ExpansionIntroduction Analysis Alternatives Recommendation Implementation Conclusion

2017 2018 2019 2020 2021Revenues From Expansion 358.9 768.1 986.2Ebitda 0 46.66069 107.535 147.9374Ebitda mg 12% 13.00% 14.00% 15.00%Ebitda (1-tax) 0.00 35.00 80.65 110.95

2,219.06CF -300 0.00 35.00 80.65 2,330.01

Growth 5%Discount Rate 10%NPV Expansion $1,255.41

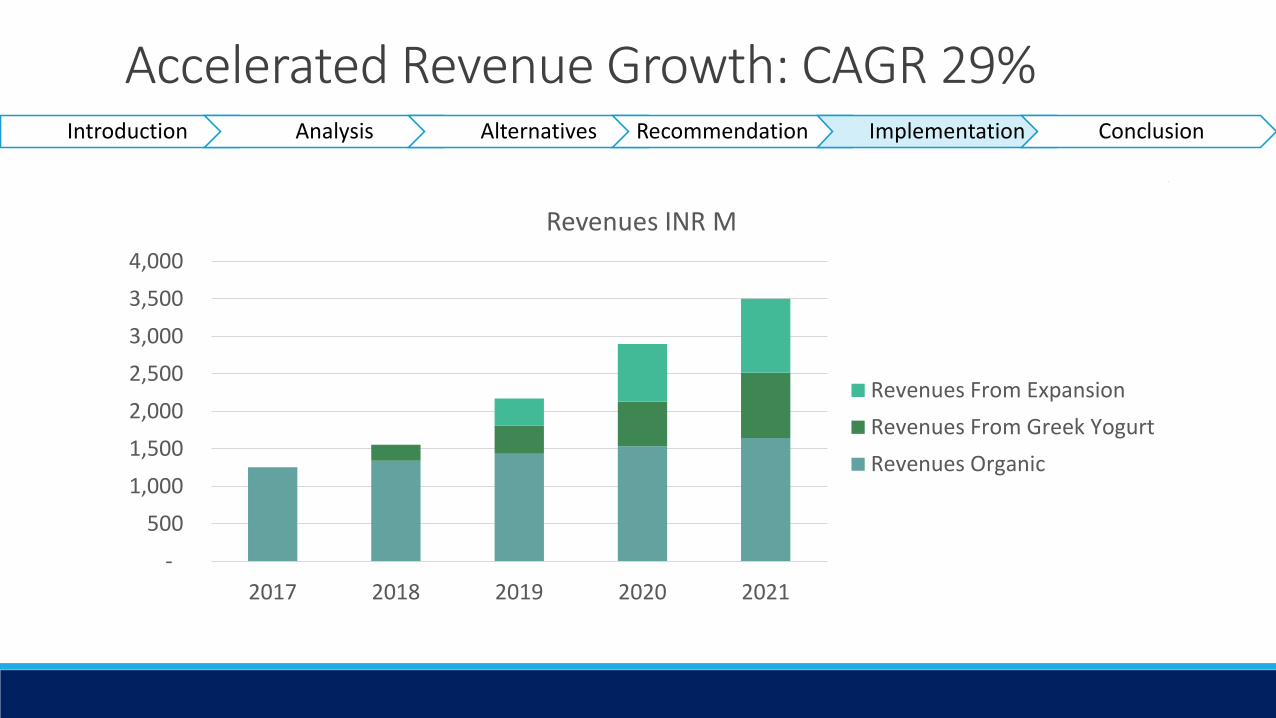

Accelerated Revenue Growth: CAGR 29%Introduction Analysis Alternatives Recommendation Implementation Conclusion

- 500

1,000 1,500 2,000 2,500 3,000 3,500 4,000

2017 2018 2019 2020 2021

Revenues INR M

Revenues From ExpansionRevenues From Greek YogurtRevenues Organic

Other Financial ConsiderationsIntroduction Analysis Alternatives Recommendation Implementation Conclusion

Working Capital: Natural increase due to investment and expansion phase◦ Will be addressed with negotiation with Business clients and higher revenues from B2C

Positioning with the Shareholders: Growth Company

Risk Analysis

Risk Prevention Mitigation Impact LikelihoodLow success with high end brand in Tier 1 cities

Test market (Mumbai) and marketing

Production withdrawalor focus marketing on lower priced items

Medium Medium

Production capacity does not meet demand

Market researchand testing

Follow-on issue for extra funding

Medium Low

Incumbents fight back and take market share

Competitive pricing Revisiting marketing mix

Medium High

New expansion negatively affects cash flow

Conservativecosting and budgeting

Percentage reduction in receivables to encourage payment

Medium Low

Introduction Analysis Alternatives Recommendation Implementation Conclusion

HOW CAN PRABHAT DAIRY BEST GROW IN THE INDIAN DAIRY INDUSTRY?

Looking forward

Prahbat Dairy exists in a market with significant opportunities

High levels of expected growth, but significant competition:◦ Multinationals◦ Cooperatives

Strong basis in Maharashtra to leverage upon

Recommendation:

1. Expand in 2 new provinces and offer all existing products in T2 & T3 cities

2. Test new product in Mumbai market (T1) with gradual phasing into other T1 cities

3. Supported by marketing initiatives and development of distribution network

Introduction Analysis Alternatives Recommendation Implementation Conclusion

Result: Revenue growth of over 29% year over year for the next 5 years

THANK YOU

Appendix

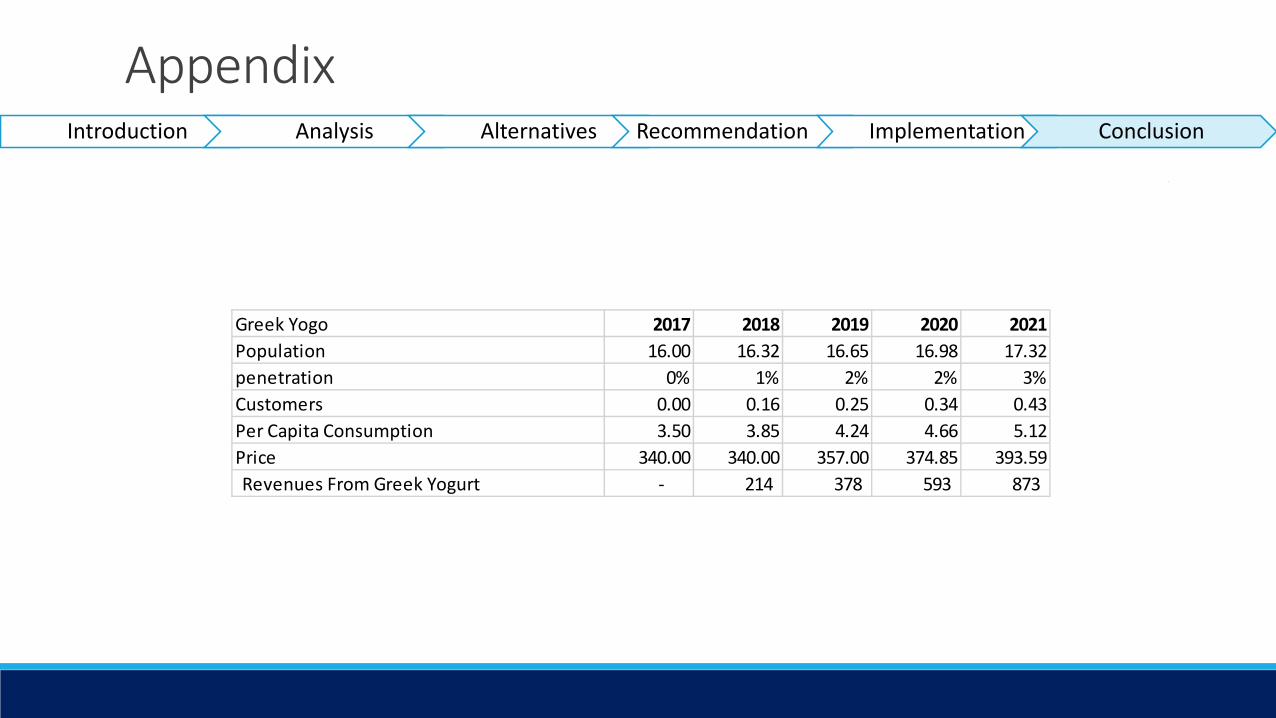

Greek Yogo 2017 2018 2019 2020 2021Population 16.00 16.32 16.65 16.98 17.32penetration 0% 1% 2% 2% 3%Customers 0.00 0.16 0.25 0.34 0.43Per Capita Consumption 3.50 3.85 4.24 4.66 5.12Price 340.00 340.00 357.00 374.85 393.59Revenues From Greek Yogurt - 214 378 593 873

Introduction Analysis Alternatives Recommendation Implementation Conclusion

AppendixIntroduction Analysis Alternatives Recommendation Implementation Conclusion

New ProductOperating Expenses 2017 2018 2019 2020 2021Product Development 130Market Research 65Marketing 149.5 149.5 149.5 149.5 149.5Personnel 45.5 45.5 45.5 45.5 45.5Distribution 13 13 13 13 13Total 403 208 208 208 208

Capital Expenditures 300

Total Opex + Capex 1,535.00

Expansion T2 and T3 2017 2018 2019 2020 2021Market Research 65Higher Production Capabilities 32.5Distribution 65 65 65 65Launches 78 78Total 65 98 65 143 143

Capital Expenditures 300

Total Opex + Capex 814