performance management program measure and improve organizational performance 1 ahmad saleem, fca...

TRANSCRIPT

Performance Management Program

Measure and Improve Organizational Performance

1

Ahmad Saleem, FCA0300 [email protected]

What is Performance Measurement?

2

Performance Measurement is the comparison of actual

measurement with the expected, specified or desired

measurement

Measurement Slide 1 of 2

• What is Measurement?• Measurement is recording the quantitative attributes of any activity, event, output,

equipment, person, organization or anything – which has any quantitative recordable attributes

• Measurement is a process of obtaining the magnitude of quantity in any unit.• Measurements can be accurate or may be judgmental• Accurate

– Length, distance, time, weight, money, profit earned, patient treated, units manufactured, houses constructed etc.

• Judgmental– Comfort, Feeling, Satisfaction, Taste, Smell – He is not very happy even he got first

position – here we are talking about feeling of someone, the taste of the food is not good of any particular restaurant – may be someone likes that taste – Chocolate and Cheese many persons like the taste many dislike – however we can scale these 0 - 10

• We do lot of measurement in all our life almost on daily basis – watching our weights, time taken for some process, efforts required to perform any job, etc.

3

Measurement Slide 2 of 2

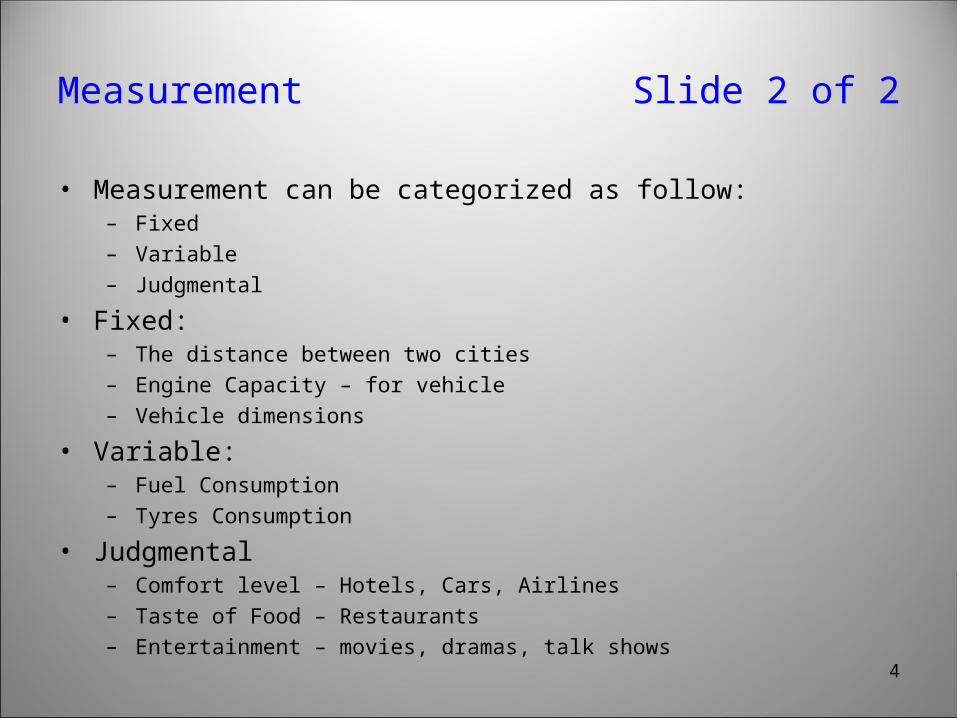

• Measurement can be categorized as follow:– Fixed– Variable– Judgmental

• Fixed:– The distance between two cities– Engine Capacity – for vehicle– Vehicle dimensions

• Variable:– Fuel Consumption– Tyres Consumption

• Judgmental– Comfort level – Hotels, Cars, Airlines– Taste of Food – Restaurants – Entertainment – movies, dramas, talk shows

4

Performance

• We can determine performance of any activity, which is measureable

• If anything is not measurable, we cannot judge its performance and that's cannot be improved – for a student if the examination result is only pass and fail – we cannot force student to improve more than passing the exams

• We can improve only those activities, which are measureable

• Performance is comparison of measurement of actual facts with some pre-determined or desired results or facts

– The performance of my car is not good – expected more mileage, more comfort– He is not performing well in his monthly exams – expecting A+ grades but he is getting

lower grades– The performance of ABC Textile Mills is not good – mainly measurement in Profits or

quality of products– The performance of XYZ Textile Mills is excellent – very high profits

5

Performance Management

• Once we have determined the Performance of any activity then it is decided that whether there is need for improvement or its present performance is satisfactory

• When we take steps for the improvement of Performance, that series of actions and steps is called “Performance Management”.

• Through Performance Management Program we can establish the procedure through which measurements can be improved.

• For this, we need to identify the areas where improvement can be made – set the standards for each area for the improvement, note down the present measurement and periodically measure readings to observe the improvement

6

For this presentation purpose, we will discuss the Performance Management of Organizations, where achievement of their Objectives is the main measurement.

7

Organization’s Objectives

• Commercial Organizations– Profitability– Expansion

• Social Organizations– Providing social services– Collecting Donations– Helping others

• Commercial + Social – Hospitals – Providing health services– Earning to sustain

8

Strategy towards Performance Management

• Establish the Potential Performance Level

• Measure the Present Performance level

• Establish areas where performance can be improved

• Gaps – how much and reasoning

• Establish how much improvement can be made

• Set Goals and Targets for improvement

• Measure improvement periodically

9

Why Performance Management

• We do need High Performance Management Program for the following main reasons:

– Long term Survival and higher return on investments

– Achievement of the Objectives in efficient and effective manners

– Less waste and lower operational cost

– A competitive advantage and higher sales

– Better financial results, high profits, income and wages

– Reducing Top Management pressure and tension

– Better motivation and teamwork among employees

10

Critical Factors for High Performance

1. Strategic Direction 2. Business Plan3. Core Activities for Business Plan – Departmental Profile4. Organizational Culture – Attitude, Values and Discipline5. Setting Targets and Key Performance Indicators – For Departments, Employees and Machinery6. Resource Management – Commonly 4Ms

1. Man Power (Human Resource)2. Material (Stocks)3. Machinery (Fixed Assets)4. Money (Funds)5. Energy6. Knowledge7. Time

7. Costing, Contribution Margin and Breakeven Analysis8. Budgeting9. Systems, SOPs, Controls and Policies10. Knowledge Management11. Role of IT12. Role of Accounts Department13. Risk Management14. Performance Measurement 11

Strategic Directions & Management

• Strategic Management is defined as the set of decisions and actions that result in formation and implementation of plans to achieve a Company’s objectives. It comprises nine critical tasks.

1. Formulate the company’s mission, purpose, philosophy and goals2. Conduct an analysis that reflects the Company’s internal conditions and capabilities.3. Assess the Company’s external environment.4. Analyze the Company’s options by matching its resources with the external

environment5. Identify the most desirable option by evaluating the each option in the light of

Company’s mission6. Select a set of long-term objectives and grand strategies that will achieve the most

desirable options7. Develop annual objectives and short-term strategies that are compatible with the long

term objectives and grand strategies8. Implement the strategies choices by means of budgeted resources allocations in which

the matching the tasks, people, structures, technologies and reward system9. Evaluate the success of the strategic process as a input for future decision making

12

Strategic Directions

• Strategic planning is for long-term – ranging from 3 – 5 years

• It establishes the major scope of working for the Organization

• Any mid term and short terms planning are based on the Strategic Directions

• What normally includes in Strategic Directions:– Size of the setup, products types, target market, potential buyers, marketing strategies, logistics

strategies, expansion plan, human resource, financing etc.• Examples:

– Credit Cards – Alfalah Credit Cards, Citi etc.– Telecommunication – Telenor , Mobilink– Food - Domino Pizza, Pizza Hut– Airlines – Aero Asia, Air Blue, Western– Textile Unit - Spinning Unit – Special Counts– Weaving Units – Special Fabrics

13

Business Plan

• Business Plan is the overall plan for the Organization, which ties all the Organizational functions together

• Assessing the potential of the Organization• Assessment of the present position• Set overall Goals for the Organization• Setting Departmental Goals• Identify the Capability Gaps• Prepare complete Business Plan – taking into consideration all above-mentioned

factors• Creating overall plans for all departments• Monitoring the plan on regular intervals• Making necessary adjustments – when required

14

Core Activities - Departments

• For the execution of Business Plan, the Organization is required to do certain activities – the grouping of same type of activities will form the Departments

• In general departments:– Sales & Marketing– Production & Production Planning– Purchases– Stores– Accounts & Finance– Costing & Budgeting– Administration and HR

• Establish the core activities and objectives of the Departments:– For example, by establishing IT department, we expect that the emails should be

running smoothly, no viruses, web site should be functional, networking among all computers should be operational, server should not be down

15

Departmental Profile

• Departmental Job Description• Tasks • Key Result Areas, Key Performance Areas and Key Performance Indicators• Human Resource required – budget in numbers and value• Head of Department• Processes involved in the department• Activities and monetary budget• Documents and Reports• Information and Knowledge• Software related requirement• MIS & EIS (Management Information System and Executive Information System)

16

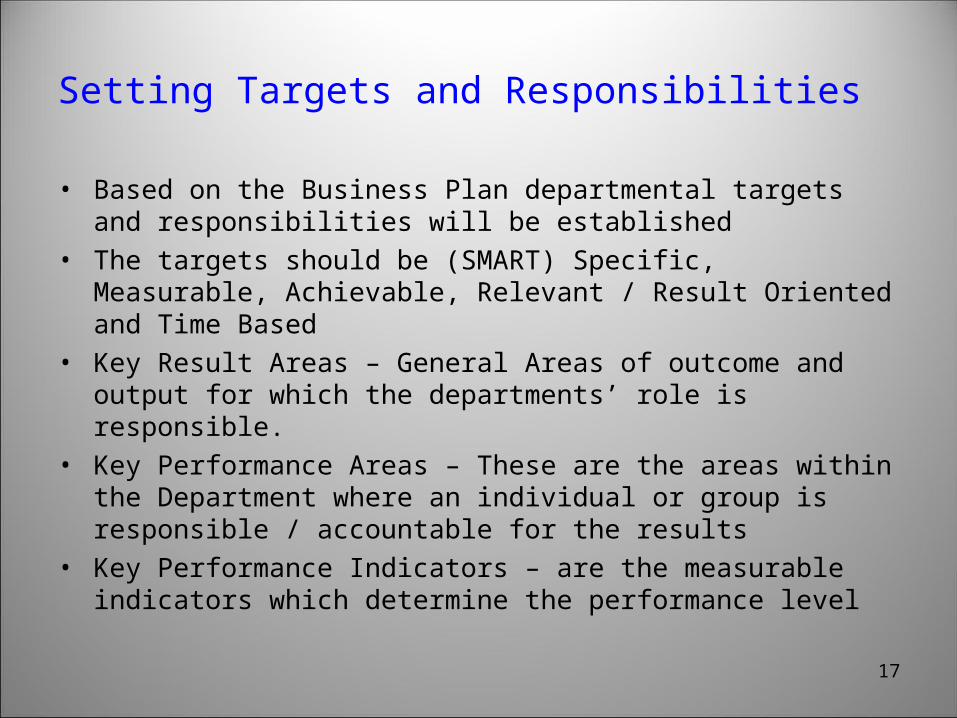

Setting Targets and Responsibilities

• Based on the Business Plan departmental targets and responsibilities will be established

• The targets should be (SMART) Specific, Measurable, Achievable, Relevant / Result Oriented and Time Based

• Key Result Areas – General Areas of outcome and output for which the departments’ role is responsible.

• Key Performance Areas – These are the areas within the Department where an individual or group is responsible / accountable for the results

• Key Performance Indicators – are the measurable indicators which determine the performance level

17

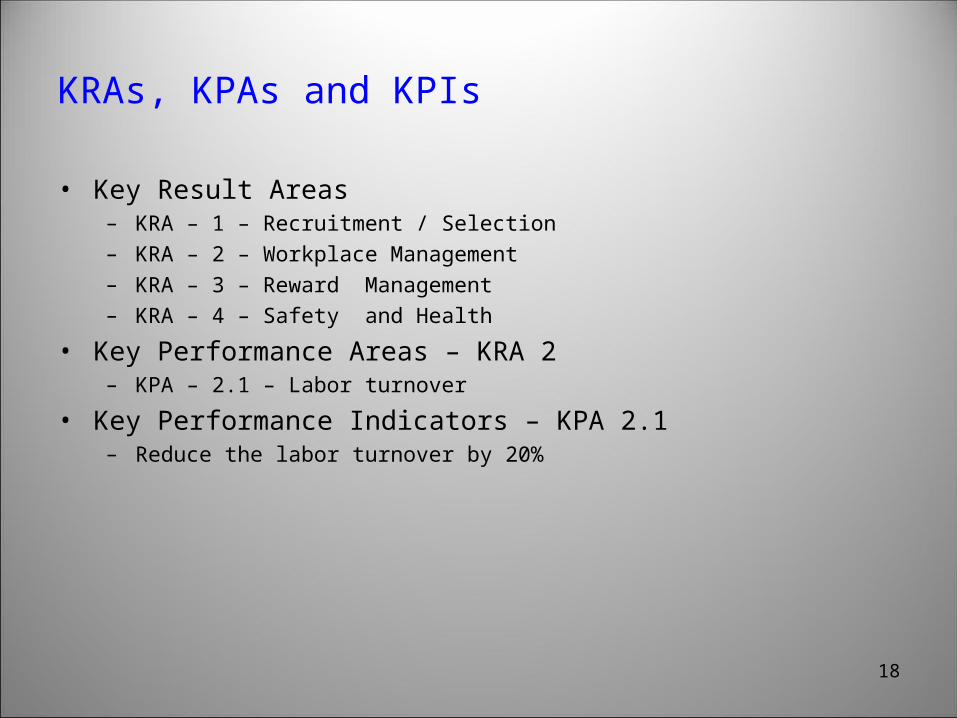

KRAs, KPAs and KPIs

• Key Result Areas– KRA – 1 – Recruitment / Selection– KRA – 2 – Workplace Management– KRA – 3 – Reward Management– KRA – 4 – Safety and Health

• Key Performance Areas – KRA 2– KPA – 2.1 – Labor turnover

• Key Performance Indicators – KPA 2.1– Reduce the labor turnover by 20%

18

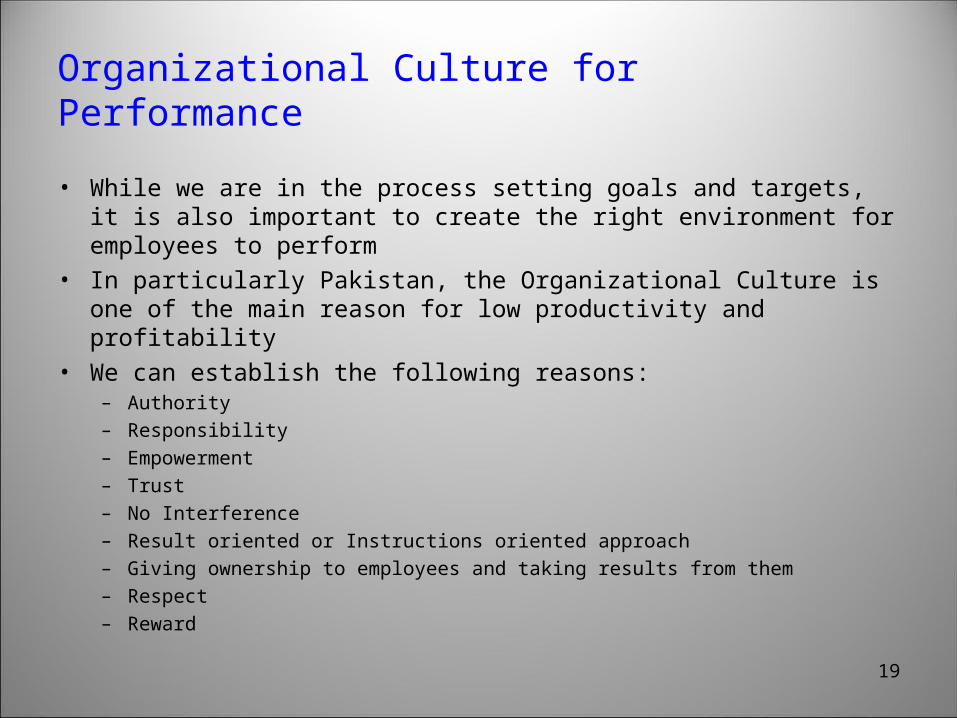

Organizational Culture for Performance

• While we are in the process setting goals and targets, it is also important to create the right environment for employees to perform

• In particularly Pakistan, the Organizational Culture is one of the main reason for low productivity and profitability

• We can establish the following reasons:– Authority– Responsibility– Empowerment– Trust– No Interference– Result oriented or Instructions oriented approach– Giving ownership to employees and taking results from them– Respect– Reward

19

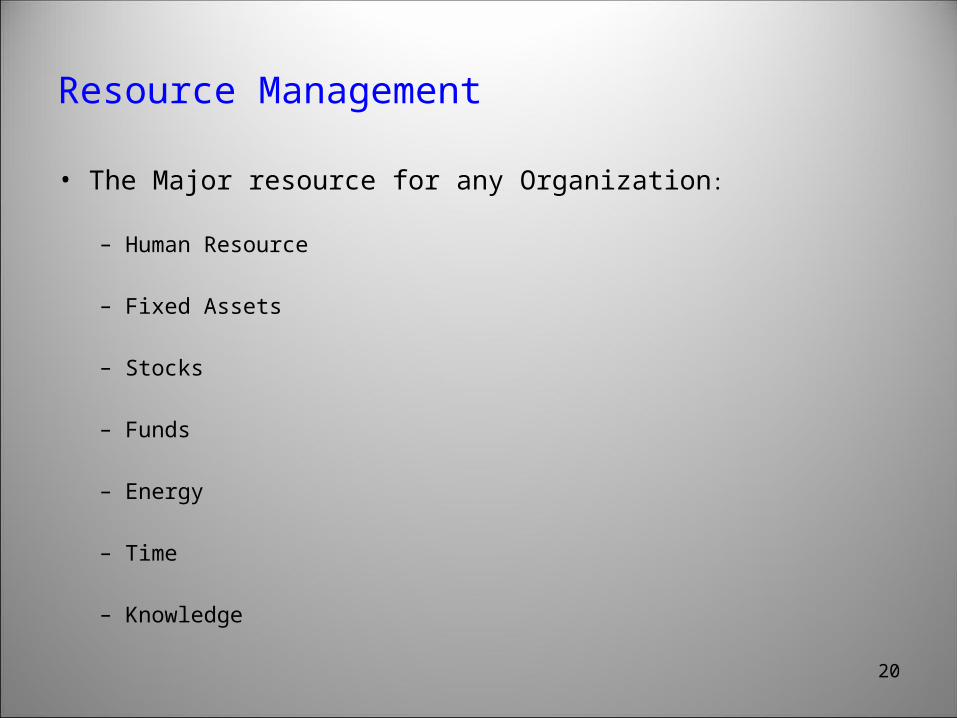

Resource Management

• The Major resource for any Organization:

– Human Resource

– Fixed Assets

– Stocks

– Funds

– Energy

– Time

– Knowledge

20

Fixed Assets

• Fixed Assets consumes major part of capital:– Necessary to establish

• Productive Assets• Non – Productive Assets

• Ratio between these two categories (Productive and non-productive assets)

• Between Productive Assets– Main Productive Assets– Production Support Assets

• Return on Assets should be calculated on all types of Assets to get more meaningful results

21

Stocks

• Stocks and materials are the critical requirement of almost all industrial based units and take major part of current assets

• The value of stocks have direct impact on the working capital

• The excessive stocks lead to:– Higher wastage due to obsolete and old items– Higher blockage of finances– Excessive carrying cost– Lower usability of old items

• Should be rightly stocked and physically controlled

22

Funds

• Funds are always considered as blood of the Organization

• Mostly organizations unable to perform due to excessive bleeding

• Owners try to save organizations through injecting additional funds but mostly no efforts are made to stop excessive spending and controlling activities

• Additional funding is arranged through expensive arrangements putting additional burden on already low performing organization

• From the beginning, strict considerations on the fund management

• Prepare Periodic Fund Statements observing the actual and projected

• Monthly and Annually prepare Projected Fund Positions

23

Energy

• With reference to present scenario of energy cost world wide, it is very important that the energy cost should be controlled and monitored.

• Energy cost can be reduced by creating an attitude towards saving the energy + installing right equipment

• Strict monitoring of energy consumption

24

Time

• Organizations have resources and every resource is available for certain time period

• It is important that time limits should be set for the performance of all the resources

• In the manufacturing process the performance time is very important as that will increase efficiency and reduce production cost

25

Knowledge

• For the performance of particular activities of any organization a certain amount of knowledge is always required – Textile, Cement, Banking, Hospitals, Lawyers, Chartered Accountant – every industrial sector needs knowledge to perform

• Establish what type of knowledge is required and who will be responsible

• How knowledge will be up dated?

• With the better knowledge the performance will be better

• Application of the knowledge is important – whether a person is capable to apply his/her knowledge when required

26

Human Resource

• Most Important Resource – The employees should be capable to perform, having required capabilities and willingness to take responsibility.

• Human Resource is the most important Resource for any Organization as this is the resource, which controls and utilize all other resources of the Organization.

• Hire persons with right capabilities required to perform particular job

• Provide right resources

• Provide right environment

• Provide education and training

• Have Job Analysis and Job Descriptions in writing and accepted by the Employees

• This will change the mindset and attitude of the employees towards his/her responsibilities

• Regular follow up of the Performance – non-performances should be handled immediately

• Always discuss events – not personalities

• Reward properly 27

Costing, Contribution Margin and Breakeven

• Costing– The process of identifying and evaluating the Production Cost. Costing is accumulation

of total expenditure for producing a product

• Contribution Margin– Contribution is the difference between Sales Price and its direct variable cost of the unit

– the Contribution Margin helps in determining the minimum sales targets and guidance as how profits can be increased

• Breakeven Analysis– Based on the working of Contribution Margin, we can compute breakeven analysis.

Breakeven is the stage of the Business – where organization is in balanced state – not earning any profit neither having any loss

– Breakeven Analysis can be prepared of multiple types – Cash Breakeven – whether any particular equipment or product is generating enough cash, which is required to pay liabilities relating to that equipment or product

– Simple Breakeven – simple calculation of operational profit

28

Budgeting Slide 1 of 2

• Why we need Budgeting?

– Planning – a good planning tool – for systematic and logical planning– Co-ordination – helps coordinating the activities of the Organization– Communication – better communication among different teams and departments– Motivation – Motivation for Managers to try and achieve Organizational goals– Control – controlling activities by measuring progress against the original plan– Evaluation – the evaluation of the persons and departments can be made more easily

• What type of Budgets?

– Production Budgets– Expense Budgets– Marketing Budgets– Sales Budgets– Purchase Budgets– CAPEX – Capital Expenditure Budgets– Human Resource Budget

29

Budgeting Slide 2 of 2

• Budget should be strongly integrated – independents budgets cannot be successful

• In budget preparations – involve all the persons relating to those activities – their input will be very valuable and if they are part of preparation they will take the ownership

• The budgets purely based on any past period results may lead to lower performance

• Keep budgets flexible for changes – however make changes only when justified

• Learn from the past budgets – if any past budget was a failure or a success story – try to learn its reasons

30

Process

• A “Process” is a combination of multiple activities. Activities are trigger by some event. A process has a starting point and an ending point – normally ending point of one process is the starting point of another “Process”. A Process also has some input and a complete output, which is the input of next process.

• An Organization needs multiple processes to complete its operational activities

• For example: For Inventory Department, following will be the processes:– Receipt of Material – Inspection – Receipt by Stores – Stacking – Issuance – Recording –

Returns – Re-ordering

• Parts of Processes – Activities, Systems, SOPs, Controls and Policies• Controlling the processing is important – number of activities, cost etc.

31

Systems, SOPs, Controls and Policies

• Systems– A pre-defined way of doing some activity is called system. In system, all possible

activities are worked and a procedure is prepared as how the activities will be performed by anyone in event of happening of any transaction.

– Step wise explanation as how activities will be performed

– We also mention certain documents, forms and register or record keeping tools to maintain the data processed in that particular transaction or activity.

• System Example:– For Inventory Receipt:

• On receipt of materials from suppliers, the Gate keeper will check the supporting Documents

• If documents are correct, the Gate Keeper will enter the Document number in the register and also make entry in the computer system and prepares “Gate Inward Pass”

• After the making entry in the relevant record, the material will be placed for inspection

32

Systems, SOPs, Controls and Policies

• Controls– We normally place controls in order to avoid any risk being present in the transaction

/activity either by nature of the transaction or otherwise– Controls means that matters being handled according to one’s desire without his/her

presence there.– Controls can be established through:

• Authorization – Documents – Reconciliations – Physical Monitoring – Budgets – Access Control

– Example:• In case of Inventory receipt procedure, we need to have control that no un-

authorized material enter in the premises – so a control has been placed with the Gate Keeper that he will ensure that material is accompanied with the Authorized Document.

• Policies– A deliberate plan of action to guide decisions in different situations– Example:

• In case of Inventory Receipt, we need a policy statement that in the event of excess receipt of material what action gate keeper should take

33

Knowledge Management

• Knowledge Management relates to every type of information and record needs to be maintained:

• We can divide knowledge Management in the following categories:– Data– Documents and Forms– Reports– Information– Knowledge

• Data– Data is the raw facts, attributes of any transaction or activities, normally relates to one

single transaction and maintained and recorded on certain documents and forms

• Documents and Forms– Documents and different forms are used to record the data related to activities and

transactions. There can be multiple types of documents used to record the basic data

34

Knowledge Management• Reports

– A report normally represents the compiled and consolidated data taken for a particular time period. Reports are used to communicate information formed by the compilation of data

• Information – IN Formation– Information is anything that someone is capable of perceiving. This can be written

communication, spoken communication, art, music, signals – Information is not necessarily in the form of report– Reports normally source of information– Information normally relates to particular state of facts at a particular time– Minimum and Maximum stocks level of inventory is Information

• Knowledge– Conversion of information in to actionable process is called knowledge. Often

information is being carried out by different persons but different persons take different action according to their knowledge regarding that information.

– Minimum and Maximum levels may be computed by differently based on the knowledge of the person preparing the information

35

Role of IT

• Information Technology plays critical role in Performance Management, however its role is on monitoring and managing side.

• Basic factors and systems needs be established by the Management and Users and then we can use Information Technology for better monitoring and compliance of our desired systems

• Through use of IT, we can get accurate reports and information necessary to make correct, timely and relevant decisions.

• Poor design or development of IT can creates serious impact on the Organizational performance

36

Role of Accounts Department

• ONE OF MOST IMPORTANT role in Performance Management

• The role of Accounts Department is one of the most important and critical as almost every transaction has the financial impact and passed through the Accounts Department

• The Accounts Department plays the role of COCKPIT for the Business – The Cockpit provides the pilots all the control and information, similarly the Accounts Department is in position to provide all the controls and information to the Top Management.

• If Accounts Department fails to implement the desired control and in providing the required information, the Organization starts losing its track.

• The implementation of controls, deployment of checks and balances is the key responsibility of Accounts Department

37

Role of Accounts Department

• The Accounts Department should try to consider following while checking every transaction:

– Justification

– Authorization

– Relevance

– Reasonableness

– Support Record and Documents

– Physical Execution

– As per Systems, Rules, Policies

– Budgeted

– For the purpose of Organization

– Required and related Information

38

Risk Management

• There are certain risk to the Organization in relation to different activities performed, which may also have impact on the Organization’s working. These are different than the operational risks. (At Strategic level)

• The Organization should make sure that all possible risks and threats have been properly addressed and someone must be responsible to take care of these risks.

• The risks should be identified and preventive measures should be taken:

• Examples:– Risk from Competition – continuous improvement is answer – Theft of critical data and information – IT should take special care– Sudden change in foreign currency rates – limited and controlled exposure– Micro Soft – new companies, new products– Boeing – Airbus 39

Performance Measurement

• After establishing all the systems and parameters in place, now it is required that Performances should be measured and Analyzed on regular basis.

• The System should be like this, that the performance of department “A” should be checked by department “B”, and departments B’s performance will be checked by department “C” and department “C”s performance should be checked by department “A”.

• The system should be monitored on regular basis – consistency is very important

• A separate department may be helpful, who should be responsible for compliance of all activities necessary to maintain Performance of the Organization.

40

Most Important Factors

• Human Resource• Attitude, Culture and Discipline of the Organization• Accounts Department• Strategic Planning and Directions• Fund Management

• Belief – We can do that

41

42

Thank You