pension fund perspective: the 1929 cloud

TRANSCRIPT

CFA Institute

Pension Fund Perspective: The 1929 CloudAuthor(s): Patrick J. ReganSource: Financial Analysts Journal, Vol. 43, No. 4 (Jul. - Aug., 1987), pp. 6+8+10Published by: CFA InstituteStable URL: http://www.jstor.org/stable/4479042 .

Accessed: 12/06/2014 14:34

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

CFA Institute is collaborating with JSTOR to digitize, preserve and extend access to Financial AnalystsJournal.

http://www.jstor.org

This content downloaded from 185.44.78.31 on Thu, 12 Jun 2014 14:34:34 PMAll use subject to JSTOR Terms and Conditions

by Patrick J. Regan Pension Fund Perspective vPBEAsoitsIc V. P., BEA Associates, Inc.

The 1929 Cloud "Stocks Climb Again in Late Buying Rush-Traders Regain Confidence As Reserve Bank Fails to Act on Redis- count Rate" (February 12th)

"Debt Experts Agree to Young Pro- posal-They Will Seek Plan to Set Up New International Body to Replace Reparation Board" (March 5th)

"Predicts Senate Will Bow to Flood of Tariff Protests-Many of the Higher Rates to Be Scaled Down By Republi- cans" (July 18th)

"Deadlock Halts Anglo-Soviet Talks" (August 2nd)

"Palestine Death Toll Mounts Hourly, With Fifteen Americans Among Slain; New Outbreaks Indicate Arab Revolt" (August 27th)

These front page headlines from The New York Times have a familiar ring.' They could be news events of 1987, but they actually appeared in 1929.

With the stock markets of the world surging to record levels this year, in spite of sluggish economic growth and a heavy debt burden, most valuation measures are at or approaching the upper limits of their historical ranges. Combined with a possible trade war, default on international loans and higher interest rates, the situation has prompted market historians such as John Kenneth Galbraith to note the dangerous similarities between the current period and the late 1920s. Which of these are significant and which are merely coincidental? And what do they suggest for the remain- der of the decade?

The Cast of Characters The spirit of the 1980s was best ex- pressed by Ronald Reagan's idol, Cal- vin Coolidge, in 1925: "The business of America is business."2 The Coo- lidge prosperity was enhanced by the tax cuts initiated by his Secretary of the Treasury, Andrew Mellon. Reagan

relied on the advice of "supply side" economists and Wall Streeters like Donald Regan, but the effect was the same.

Business executives and entrepre- neurs were the heroes of the day as people like RCA founder David Sar- noff became celebrities. Walter Chrys- ler, the automobile tycoon, was named "Man of the Year" by Time in January 1929, a year after the honor had been bestowed on Charles Lind- bergh. It took nearly six decades for the American public (although not Time) again to place a businessman on such a pedestal, and the successor is ironically Lee lacocca, current chair- man of the Chrysler Corporation.

The rogues of the two eras are no less colorful than the business execu- tives. Arbitrage is the elixir of the 1980s, but the biggest and most suc- cessful of the "arbs," Ivan Boesky, was toppled when it was revealed that several of his investment coups were the results of inside information. He had bribed some of the leading archi- tects of the megamerger boom, includ- ing the dynamic head of Kidder Pea- body's investment banking group, Martin Siegel. Also nabbed in the scandal were Boyd Jeffries, a leading broker who was instrumental in as- sembling blocks of stock for corporate "raiders," and several lesser known lawyers, traders and investment bank- ers. In short, several of the luminaries of the recent bull market have suffered an ignominious downfall.

In his book The Great Crash, and in his recent article "The 1929 Parallel," John Kenneth Galbraith recounted the rise and fall of the 1929 counterparts to Ivan Boesky et al.3 In 1929, Time did back-to-back cover stories on two of the men who were helping to shape the great bull market, Ivar Kreuger and Samuel Insull. Kreuger was known as the Swedish Match King because he had made so many acquisi- tions that he controlled two-thirds of all the matches made in the world. The

financing came from numerous stock offerings; he then lent the money to poor countries in exchange for nation- al monopolies on matches. The empire ultimately collapsed, and Kreuger shot himself in 1932.4 Samuel Insull built a mountain of leverage known as the utility holding company pyramid. By 1929, he controlled nearly all the elec- tric utilities in the mid-West. The In- sull empire collapsed in 1929. He was indicted for fraud and embezzlement but escaped to Istanbul.s

But no one fell farther than Richard Whitney. From an old Boston family, educated at Groton and Harvard, he was the principal broker for J.P. Mor- gan & Company and president of the New York Stock Exchange. Unfortu- nately, he had expensive tastes and cmbezzled money from clients and from the New York Yacht Club, where he served as treasurer. In 1938 he was sentenced to five to 10 years in Sing Sing.6

The commercial bankers of the late 1920s were no less swashbuckling than the financiers. The two bankers who typified the era and ended up in the history books were Charles Mitch- ell and Albert Wiggin. Mitchell was president of the National City Bank, and its profits grew rapidly as he pur- sued two areas of questionable activi- ty-Latin American loans and the fi- nancing of stock market speculation. The investment banking operation, af- ter paying a six-figure "consulting fee" to the son of the president of Peru, underwrote over $75 million of Peruvi- an bonds, which they sold to custom- ers and on which they made an excep- tional profit margin. Mitchell defied the Federal Reserve Board and contin- ued to lend the bank's funds at 15 per cent call money (while borrowing from the Fed at 5 per cent) to finance stock market speculation, including the bank's own underwritings. Mitchell was awarded a bonus of over $1 mil- lion for the first half of 1929. By 1933, however, the president of Peru had

FINANCIAL ANALYSTS JOURNAL / JULY-AUGUST 1987 O 6

This content downloaded from 185.44.78.31 on Thu, 12 Jun 2014 14:34:34 PMAll use subject to JSTOR Terms and Conditions

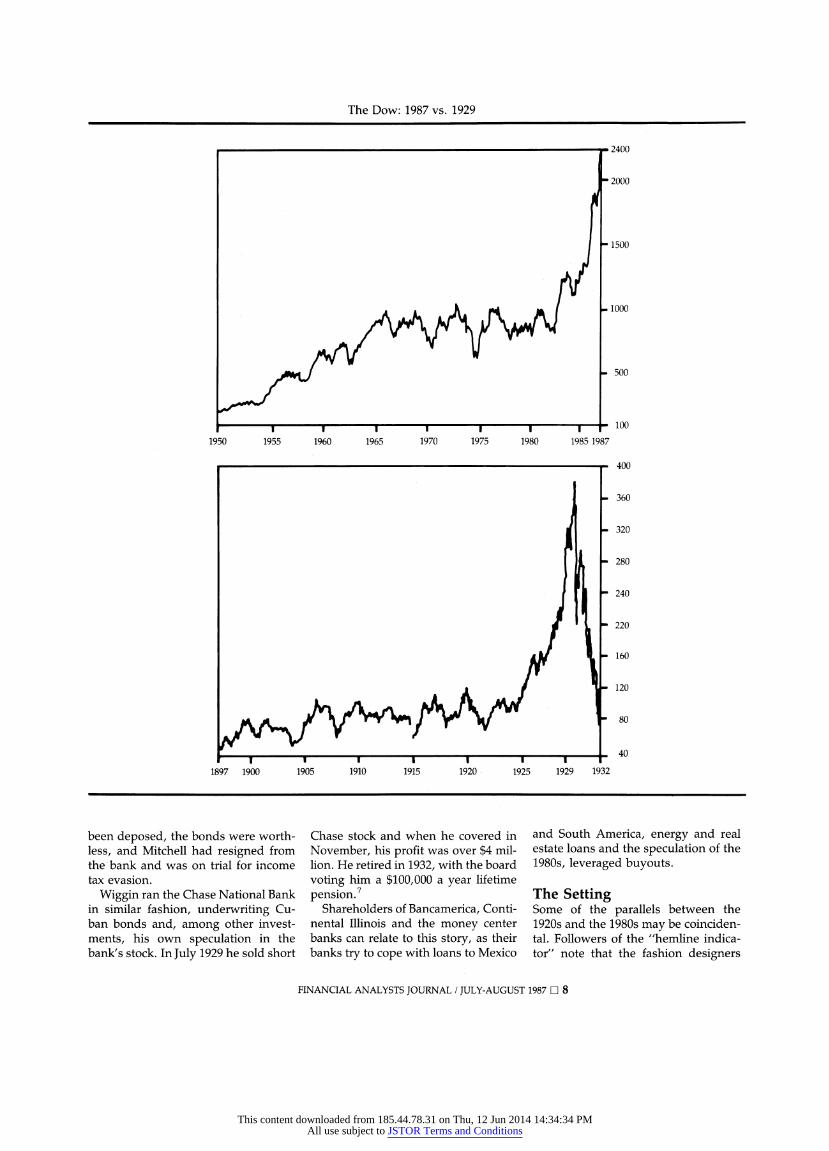

The Dow: 1987 vs. 1929

2400

2000

- 1500

1000

- 500

P | ? | I I I - ~~~~~~~~~~~~~~~~100 1950 1955 1960 1965 1970 1975 1980 1985 1987

* 400

360

- 320

280

240

220

-160

120

80

40

1897 1900 1905 1910 1915 1920 1925 1929 1932

been deposed, the bonds were worth- less, and Mitchell had resigned from the bank and was on trial for income tax evasion.

Wiggin ran the Chase National Bank in similar fashion, underwriting Cu- ban bonds and, among other invest- ments, his own speculation in the bank's stock. In July 1929 he sold short

Chase stock and when he covered in November, his profit was over $4 mil- lion. He retired in 1932, with the board voting him a $100,000 a year lifetime pension.7

Shareholders of Bancamerica, Conti- nental Illinois and the money center banks can relate to this story, as their banks try to cope with loans to Mexico

and South America, energy and real estate loans and the speculation of the 1980s, leveraged buyouts.

The Setting Some of the parallels between the 1920s and the 1980s may be coinciden- tal. Followers of the "hemline indica- tor" note that the fashion designers

FINANCIAL ANALYSTS JOURNAL / JULY-AUGUST 1987 O 8

This content downloaded from 185.44.78.31 on Thu, 12 Jun 2014 14:34:34 PMAll use subject to JSTOR Terms and Conditions

have re-introduced the thigh-high miniskirt-the shortest hemlines since 1968 and 1929, both significant stock market peaks. The price of farmland peaked in 1925 and the Florida real estate boom in 1926, whereas the present-day equivalents were 1981 and 1983.

Other similarities are more disturb- ing. In 1925, Britain's Chancellor of the Exchequer, Winston Churchill, placed the country on a pre-World War I gold standard, with the pound at $4.86. With the pound so overvalued, Britain lost exports and jobs and suffered a general strike in 1926. The U.S. en- joyed a favorable balance of trade, and gold moved from Britain. In 1927, the central bankers of England, France and Germany came to the U. S. to resolve the international monetary cri- sis. As a result, the Federal Reserve cut the discount rate from 4 to 3.5 per cent. The "excess liquidity" simply fed the stock market boom, but the easy credit pleased our European neigh- bors.8

Japan is in a similar situation now. The dollar has been overvalued, the Japanese have registered huge trade surpluses and they have been urged by central bankers to reduce interest rates in order to stabilize the yen. Not surprisingly, the strong yen has stalled Japanese exports and the coun- try finds itself on the verge of a reces- sion. The excess liquidity has gone into financial assets and driven Japa- nese stock prices to the equivalent of our 1929 levels.

In April, the Japanese market sur- passed the U.S. as the largest capital- ization in the world, at $2.7 trillion. But the Japanese market is equal to 129 per cent of gross national product (vs. 63 per cent in the U.S.), with the

average stock at 56 times earnings (vs. 18 in the U.S.) and four times book value (vs. 2.4 in the U.S.).9 It has all the marks of a speculative bubble. In February, the government sold 1,650,000 shares of Nippon Telegraph and Telephone to individuals, one share to a person, at $8,322 each. The stock soon tripled, giving it a price- earnings ratio of 350 and a market capitalization greater than the entire German stock market.

In sum, there are numerous paral- lels between 1929 and 1987. As the accompanying charts of the Dow Jones industrials indicate, the Dow was in a trading range of 60 to 100 for two decades before it exploded in the late 1920s to hit 380. Similarly, the Dow was in a 600-1000 trading range for two decades before the recent move to 2400.

One of the most successful forecast- ers in this market has been Robert Prechter, the leading interpreter of the Elliott Wave Theory. Ralph Nelson El- liott developed a cycle theory in the 1930s, and Prechter claims that we are in a super cycle similar to the 1920s, with an expected high of 3600 on the Dow by 1988. Unfortunately, the the- ory then calls for a decline of greater than 90 per cent, as in the 1929-32 period.

Denouement Are such events preordained? Perhaps with so many commentators and his- torians pointing out the road signs, we can avoid the boom/bust cycle. Of course, some politicians seem intent on pushing us over the brink. Con- gressman Richard Gephardt, in his quest for the presidency, has intro- duced trade legislation that is nearly as protectionist as the Smoot-Hawley tar-

iff of 1930, which many blame for turning a recession into a depression. If a trade war does break out, the Japanese market will be vulnerable to a collapse, and our market will proba- bly retreat to at least the middle range of its historical valuation.

Footnotes

1. Copies of the leading news stories in their front page format appear in The Times In Review.. 1920-29 (New York: Arno Press, 1973).

2. From a speech to the Society of American Newspaper Editors on January 17, 1925. As mentioned in Bartlett's Familiar Quotations, Four- teenth Edition (Boston: Little, Brown & Co., 1968).

3. John Kenneth Galbraith, The Great Crash (Boston: Houghton Miffin, 1961) and Galbraith, "The 1929 Par- allel," The Atlantic Monthly, January 1987, pp. 62-66.

4. For data on the post-1929 affairs of the key financiers of the era, see John Brooks, Once in Goldconda. A True Drama of Wall Street 1920-38 (New York: Harper & Row, 1970).

5. For information on the key events and characters that led to regula- tion of the industry, see Matthew Josephson, The Money Lords.. The Great Finance Capitalists 1925-1950 (New York: Weybright & Talley, 1972).

6. John Train, Famous Financial Fiascos (New York: Clarkson N. Potter, 1985).

7. Brooks, Once in Goldconda, op. cit. 8. Galbraith, The Great Crash, op. cit,

pp. 14-15. 9. "Japan Stock Market Overtakes the

U. S. As The Worlds' Largest," Wall Street Journal, April 13, 1987, pg. 12.

FINANCIAL ANALYSTS JOURNAL / JULY-AUGUST 1987 E 10

This content downloaded from 185.44.78.31 on Thu, 12 Jun 2014 14:34:34 PMAll use subject to JSTOR Terms and Conditions