pceia english version

TRANSCRIPT

OVERVIEW

This chapter provides an introduction to the wide range of topics which the book covers. Emphasis is placed on the following areas:

• Importance of Insurance

• How Insurance Works

• What Insurance Is

• Functions of Insurance

• Classes of Insurance

• Historical Aspects of Insurance

• The Role of an Insurance Agent

1.1. INTRODUCTION

Human beings are exposed to various kinds of risks in their daily lives and activities and have to endure the consequences of such misfortune. Misfortune can arise in many forms which, inevitably, lead to different types and nature of losses.

Some examples are:

• A sole breadwinner of a family is involved in an accident and dies prematurely. Undoubtedly, the dependents will face two immediate obvious forms of losses – emotional andfinancial.

• The premises of a factory may be destroyed by fire. The owners of the factory will face, besides other losses, the loss of income which the factory

Overview

1.1. Introduction 1.2. Importance of Insurance 1.3. How Insurance Works 1.4. What is Insurance?

1.5. Functions of Insurance

1.6. Classes of Insurance 1.7. Historical Aspects of Insurance

1.8. The Role of an Insurance Agent

1

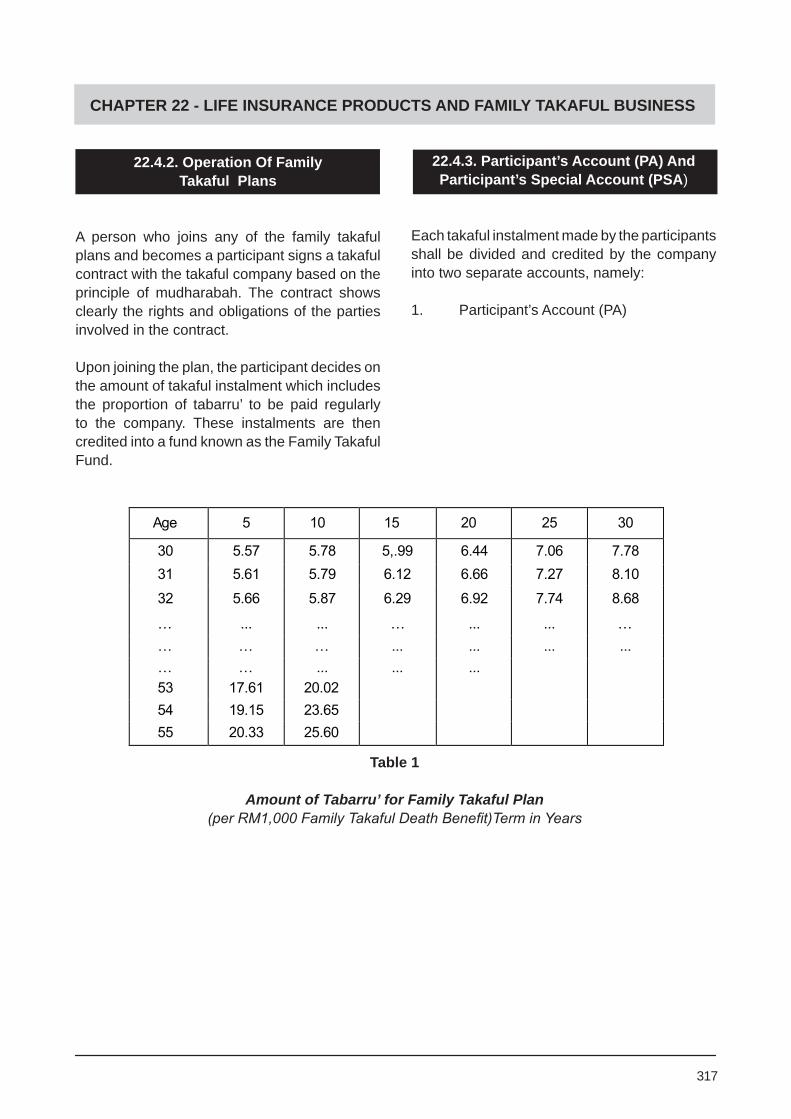

CHAPTER 1 - INTRODUCTION TO INSURANCE

would have been able to generate if the fire had not occurred. On the other hand, those employed by the factory may face the prospect of redundancy and unemployment.

We can give countless examples of events which lead tohumangrievancesandfinanciallosses.

The natural question to ask then is

“What arrangement(s) can be made to overcome or at least reduce the consequences of misfortune that may befall any one person?”

In answering the above question, we have to admit that not all forms of loss can be made good or be expressed in pecuniary terms. For instance, the emotional trauma arising from the death of loved one cannot be made good by any conceivable compensatory system.

Perhaps, what can be done is to devise a compensatory system which will at least seek

- to reduce the impact of financial loss consequent to an unfortunate event; and

- to prepare or free oneself for the forthcoming and unexpected financial burden or losses.

Onesuchpossiblearrangement,whereby thefinanciallossisinconsequenceofanunfortunateincidentsuchasdeathorafire,canbethroughthe purchase of insurance.

1.2. IMPORTANCE OF INSURANCE

The Need for Income

Every moment, individuals, families and business units are exposed to losses arising from their property, occupations, activities and

responsibilities. Who will bear these financiallosses and where will the funds be obtained from to offset such losses? Usually, in the absence of legal remedies, contract arrangements or cooperative efforts, losses will fall on the individual or business unit concerned. To solve this problem, an arrangement is introduced for coping with some of the risks and possible losses faced by individuals and business enterprises. This arrangement works on the law of large numbers, i.e. by spreading the risk of loss faced byaspecificpersonorenterprisetoallpartieswho pool their resources to pay for individual losses. This loss sharing arrangement is called insurance.

The insurer is the intermediary who manages this risk pool. The insurer holds and invests the premiums in trust for policyowners, and pays them in the event that these losses for which insurance protection is taken, occur.

Let us consider for a moment as to what would happen in modern society without insurance organization.

Living costs money. Money is required to buy essential needs like food, clothing and accommodation, as well as to acquire other comforts of life. If one wants to have a decent life,oneshouldhaveacontinuousflowofincomeaslongasoneisalive.Thiscontinuousflowofincome can be ensured only in two ways.

Sources of Income

A person may create his source of income by either setting up his own business or working for other people where, upon completion for the jobs done, he will receive payment in the form of a salary, wages, allowances or commissions.

The other means is through investment income by way of dividends, bonuses or interest on the capital invested.

2

CHAPTER 1 - INTRODUCTION TO INSURANCE

However, both sources are always at the risk of being affected by circumstances over which the individual has no control.

Unfortunate Events or Risks

Earning capacity may be ended abruptly due to death, old age, sickness or accident that may result in disability (permanent or temporary).

Likewise, the investments may suddenly depreciate in value or the goods in which capital isinvestedmaybedestroyedbyfire.

In any of these contingencies, the individual or the dependents have to bear the consequences of the financial or emotional losses. Thoseaffected have no other sources to which they can look for relief for sharing part or all of the loss.

The painful experience as a consequence of losses is obvious to anyone.

1.3 HOW INSURANCE WORKS

Let us next understand how insurance works to compensateforthefinanciallossesconsequentto the occurrence of a risk or perils.

Rather thanprovidingamoreformaldefinitionof the terms “risk” and “peril” now (see Chapter 2), we shall look at some instances where we can say that a risk or peril has occurred.

Some Forms of Risk

• Shipwreck at sea;

• Anoutbreakoffireresultingin material damage;

• Loss of income due to disability or premature death.

Pooling of Risks

It is not possible for an individual to predict or prevent such occurrences but through insurance, arrangements can be made to provide against theirfinancialeffects,i.e.lossofpropertyand/or earning.

Insurance in its various forms aims at safeguarding the interest of the individuals who are insured. This is achieved by having losses experienced by the unfortunate few compensated by the contributions, i.e. the premium, of the many that are exposed to the same risk.

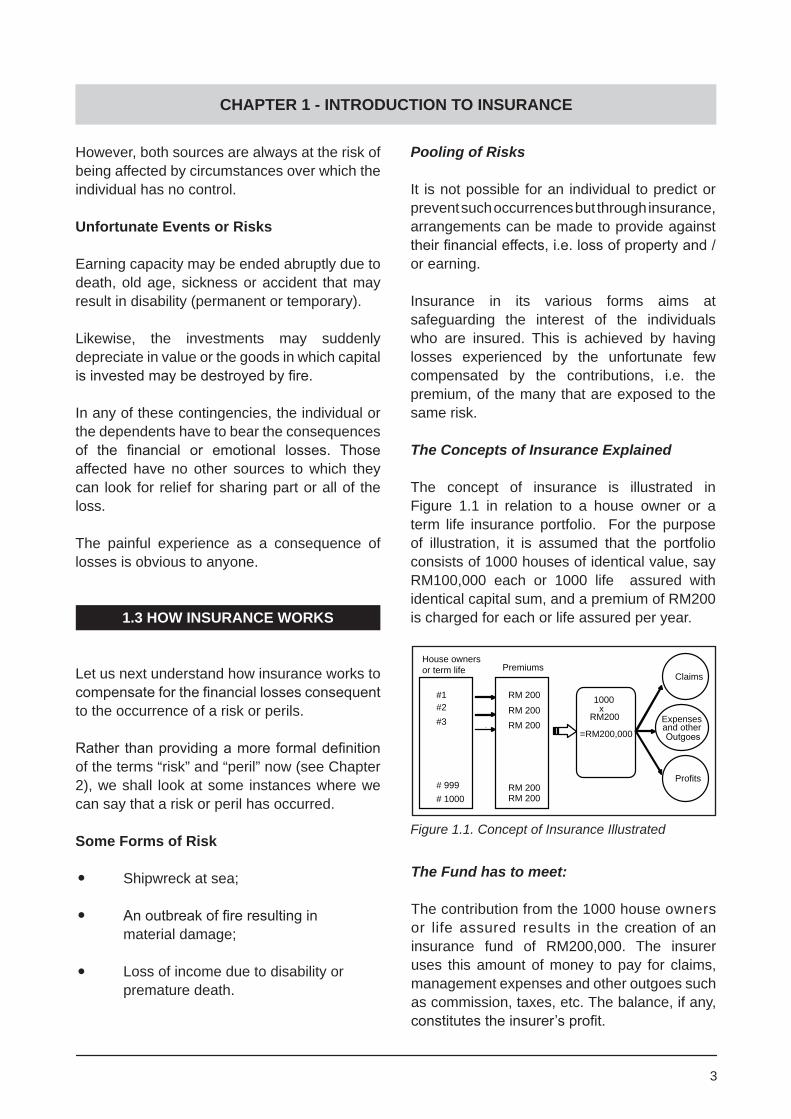

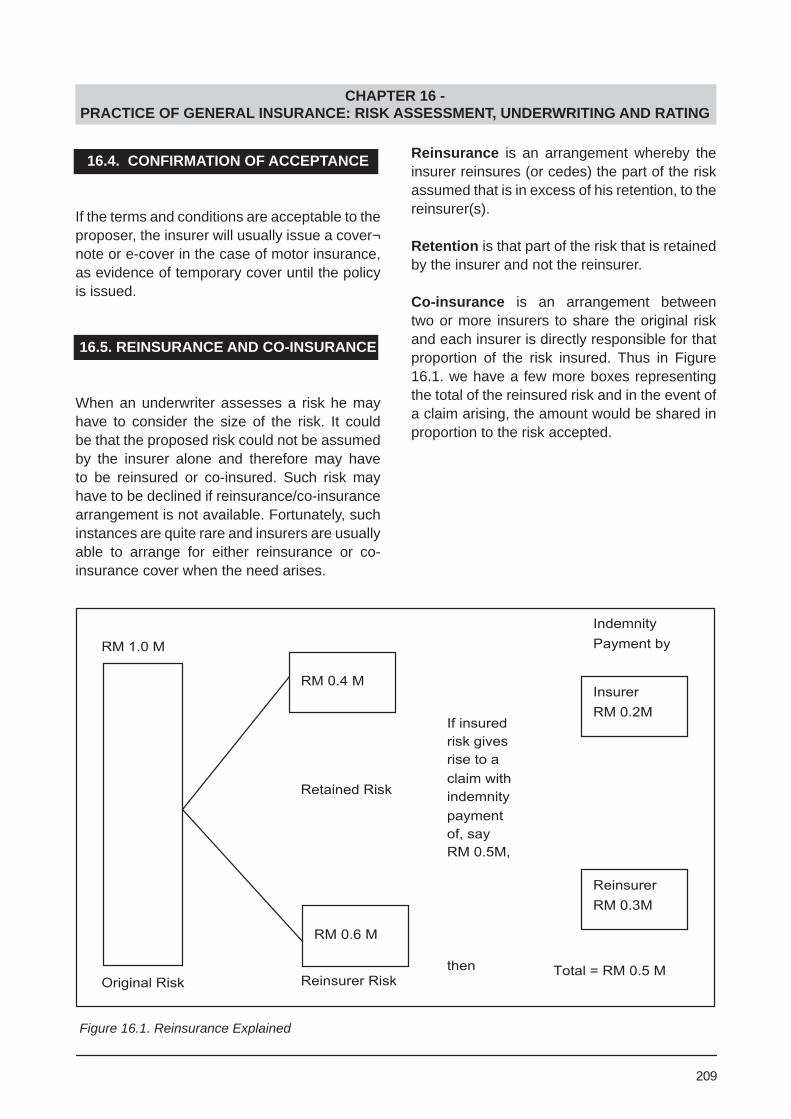

The Concepts of Insurance Explained

The concept of insurance is illustrated in Figure 1.1 in relation to a house owner or a term life insurance portfolio. For the purpose of illustration, it is assumed that the portfolio consists of 1000 houses of identical value, say RM100,000 each or 1000 life assured with identical capital sum, and a premium of RM200 is charged for each or life assured per year.

3

Figure 1.1. Concept of Insurance Illustrated

The Fund has to meet:

The contribution from the 1000 house owners or life assured results in the creation of an insurance fund of RM200,000. The insurer uses this amount of money to pay for claims, management expenses and other outgoes such as commission, taxes, etc. The balance, if any, constitutestheinsurer’sprofit.

#1 RM 200

RM 200RM 200

RM 200RM 200

House ownersor term life Premiums

1000x

RM200

=RM200,000

Claims

Expenses and other Outgoes

Profits

#3#2

# 999# 1000

CHAPTER 1 - INTRODUCTION TO INSURANCE

4

The Fund Can Become Deficit

Thus, in the situation illustrated earlier, the fund createdisjustsufficienttopayforamaximumof two claims and this leaves the expenses and other outgoes of the insurer uncovered. If more than two claims were to arise, the insurance fundwouldbeindeficitandclearly,theinsurerwould experience a loss on this portfolio.

Premiums have to be Adequate in a Competitive Business Environment

It becomes clear from the above that for the insurer to operate profitably in a competitiveenvironment, premiums have to be fixed at adequate levels, and management and other expenses controlled. It is beyond the scope of this book to explore the question of what could constitute an adequate premium for a given risk; however, we will look at the basics of the techniques and the terminology involved in subsequent chapters. For now, let us acquaint ourselves with the law of large numbers.

The Law of Large Numbers

Insurance as a device for spreading the loss of a few among many can only work when insurers are able to underwrite a large number of similar risks. When insurers are able to write a large number of similar risks, the law of large numbers operates.

The law of large numbers states that as the number of loss exposures increases, the predicted loss tends to approach the actual loss. Although the law of large numbers is a simple concept, it can only operate efficiently ifthefollowingrequirementsarefulfilled:

• There are a large number of similar loss exposures.

• The loss exposures must be independent.

• There is a random or chance occurrence of loss.

The operation of the law of large numbers will ensure better prediction of future losses. This is important to insurers because they must charge a premium (based on predicted future losses) that will be adequate for paying losses for the period of insurance.

1.4. WHAT IS INSURANCE?

Having seen the role of insurance and how it works in very general terms, it is now appropriate to put down in precise terms what insurance is all about.

Insurance, as an organization, seeks to provide protection against financial loss caused byfortuitous events.

Insurance Defined

Insurancecanthereforebedefinedas:

An economic institution based on the principal of mutuality, formed for the purpose of establishing a common fund, the need for which arises from chance occurrences of nature, whose probability can be fairly estimated.

The insurance service, therefore, involves payment of contracted benefits or compensation to the insured or a third party against unforeseen losses.

Essential Features of Insurance

The essential features of insurance, therefore, are:

i. It is an economic institution.

ii. It is based on the principle of mutuality or cooperation.

CHAPTER 1 - INTRODUCTION TO INSURANCE

5

iii. Its objective is to accumulate funds to pay for claims that arise as a result of theoperationofspecificrisks.

iv. Only certain risks can be insured against, namely those whose occurrence can be confidently estimated with a certain degree of accuracy.

1.5. FUNCTIONS OF INSURANCE

In this section we will look at the various functions of insurance.

1.5.1. Primary Function

The primary function of insurance is the equitable distribution of the financial lossesof the few who are insured among the many insured. This immediately leads to the secondary functions stated below.

1.5.2. Secondary Functions

• Stabilization of Costs

Through the purchase of insurance, business enterprises avoid the necessity of having to freeze capital to provide for financialprotectionagainstlosses.Thisprovides a means of stabilizing the costs involved in managing risks.

• Stimulation of Business Enterprise

The risk transfer mechanism provided by insurance has made possible the present-day large-scale commercial and industrial enterprises. These large-scale enterprises would not have started

if the owners were not able to transfer their risks through insurance.

• Provision of Security for Expansion of Business

Insurance helps to remove the fears and worries of losses of individuals and business executives. This removal of fears and worries helps to establish confidence and enables the forward-planning of economic activities.

• Reduction of Losses

Insurers help to reduce losses (both in frequency and security) through their actions and recommendations in rating, survey, inspection services and salvage.

• Provision of a Means of Saving

Insurance functions as a means of saving, primarily through the use of endowment insurance.

An endowment insurance is a combination of protection plus savings. The investment part of the contract is a savings accumulation. By combining the two features in a single plan, endowment assurance provides both protection and savings to the insured.

• Provision of Sources of Capital for Investment

Insurers accumulate large funds which they hold as custodians and out of which claims and losses are met. These funds are usually invested (to earn interest) in the public and private sectors. Such investments help considerably in the overall development of the economy.

CHAPTER 1 - INTRODUCTION TO INSURANCE

6

• Provision of Employment for Many

The insurance industry in Malaysia has created various categories of employment opportunities. Following are the statistics for 2007:

No. of PersonnelEmployed

20,6001,1621,84478,58739,165

Market Structure

1.Insurers2.Insurance Brokers 3.Adjusters4.Registered Life Agents5.Registered General Agents

While the nature of jobs for brokers and adjusters are independent and more of specialized roles, the various job functions in an insurance company such as underwriting, claims handling, accounts, audit/compliance, human resource/administration, electronic data processing, marketing and servicing, investment and other support functions are inter-dependent.

1.6. CLASSES OF INSURANCE

The pooling of risk is the fundamental principle underlying the insurance business and it is useful to classify insurance business broadly into Life Insurance and General Insurance.

What is Life Insurance?

Life insurance can be defined as a contractwhich pays an agreed sum of money on the happening of a contingency (event), or of a variety of contingencies, dependent on a human life.

As we progress through the book, you may note thattheabovedefinitionisnotpreciseinrelationtowithprofitpolicies,forthereisnoagreedsumof money at the outset.

Life insurance contracts can be arranged to provide cover against the following forms of risks:

• Premature death

• Loss of a continuous stream of income during retirement (i.e. during old age)

• Sickness or disability

What is General Insurance?

General insurance business can be taken to be all other forms of insurance business (including the reinsurance of liabilities under a policy in respect thereof) which is not life insurance business as definedintheInsuranceAct1996.

Risks Covered by General Insurance

General insurance contracts, to mention a few, can be arranged to provide cover against the followingformsofrisktotheinsuredand/orthirdparties in respect of

• loss or damage to property, e.g. to motor vehicles, ships, buildings, stocks-in-trade;

• legal liability caused by products or goods sold, or the process carried out;

• death or injury to a person by an accident.

More about the basis underlying the conduct of the Life Insurance and the General Insurance classes of business is provided in Part B and Part C of this book.

CHAPTER 1 - INTRODUCTION TO INSURANCE

7

1.7. HISTORICAL ASPECTSOF INSURANCE

This section will provide a brief introduction to the historical aspects of insurance.

The earliest beginnings of insurance were in the field of marine insurance. Men engagedin trade by sea attempted to minimize their losses which resulted from the perils of the sea, by spreading the losses amongst all who were similarly engaged. In the normal course of events, many ships arrived safely in port and only a few suffered losses. The many who were successful thus contributed to overcome the suffering of those who were unsuccessful. In other words, the misfortune of the unfortunate few was borne by the many.

This was achieved by the payment of a premium intoacommonfund.Somuchbenefitfollowedthis action that traders adopted the idea in many countries and gradually there came into existence groups of men who specialized in managing the fund and who studied the rates of loss which occurred in different types of maritime adventure. This was the beginning of marine insurance.

At a much later date came life insurance and other modern forms of insurance, all of which worked on the principle of spreading the losses of the few over the fund created by the contribution of the many.

Initially life insurance policies were sold as short-term policies, cover being renewed at the option of the insurer at the end of the period. Such an approach had disadvantages and perhaps, was the only possible one that could be adopted when there were no mortality tables.

The year 1706marked the emergence of theAmicable Society for a Perpetual Assurance, which adopted a scheme under which each member was required to contribute a fixedsum annually. The accumulated contributions were divided at the end of the year among

the dependents of the members who had died during the year.

Membership was open to persons between the ages of 12 and 45 and members’ contributions were uniformly fixed at £5 perannum(whichwasincreasedto£6.20lateron).In the early years of its operation the company did not guarantee a definite sumassured butafter 1757 a minimum sum assured at death was laid down. A variable premium based on agewasfixedonlyin1807.

An important landmark in the development of life insurance related to the use of the Mortality Table in conjunction with compound interest rates,when in1762TheEquitableAssurancefor the first time fixed premium rates basedon modern lines, adopting the level premium system.

1.7.1. Insurance in Malaysia

The beginning of insurance in Malaysia can be tracedtothecolonialperiodbetweenthe18thand19thcenturieswhenBritishtradingfirmsoragencyhouses established in this country acted as agencies for the UK-based insurance companies, among whichwereHarrison&Crossfield,Boustead,andSime Darby.

The insurance industry in Malaysia had been largely patterned on the British system whose influencestillcontinuestobefelt.Evenaslateas 1955, it was reported that foreign insurance domination of the local insurance market was as much as 95% of the total business transacted.

After independence in 1957, however, concerted efforts were made to introduce domestic insurance companies. The early 1960switnessed the growth of a few life insurance companies which wound up soon after because of their unsound operations and inadequate technical background.

CHAPTER 1 - INTRODUCTION TO INSURANCE

8

Control of Insurance Business

These unhealthy features culminated in the Government’s intervention through the enactmentoftheInsuranceAct1963toregulatetheinsuranceindustry.This1963ActhassincebeenreplacedbytheInsuranceAct1996.

Since January 1997, the InsuranceAct 1996has become the principal legislation governing the conduct of insurance business in Malaysia

1.8. THE ROLE OF AN INSURANCE AGENT

The roles of an insurance agent are:

• to bring financial relief to aggrieved dependents of insured people who may meet with untimely death;

• tobringfinancialreliefintheevent of property loss;

• to inculcate the discipline of saving amongst the working population;

• to provide other forms of insurance-related services to the public.

To be an effective agent, one should be able to recognize the insuring needs of one’s clients. Clients should be advised of the right type of products so that they meet their insuring needs and the policies do not lapse. Insurance agents are expected to provide, in a sense, the best possible advice to their clients.

It is greatly hoped that the reader will persevere through the rest of this book and acquire the technical and sales-related knowledge to achieve success in his or her career.

CHAPTER 1 - INTRODUCTION TO INSURANCE

9

SELF - ASSESSMENT QUESTIONS

CHAPTER 1

1. WhichofthefollowingstatementsisNOTtrueaboutthelawoflargenumbers?

a. The loss exposures must be independent. b. There must be a large number of similar loss exposures. c. There must be a random or chance occurrence of losses. d. There must be a large number of insureds experiencing the same loss at the same time out of the same event.

2. WhichofthefollowingisNOTanessentialfeatureofinsurance?

a. All risks can be insured. b. It is an economic institution. c. It is based on the principle of mutuality. d. Itisanaccumulationoffundstopayforclaimsresultingfromaspecific risk.

3. WhichofthefollowingisNOTariskcoveredbyinsurance?

a. loss of life due to a motor accident. b. loss or damage arising from a motor vehicle accident. c. liability to third parties arising from the sale of products. d. financiallossduetoadropinthemarketpriceofacompany’sshares.

4. The secondary functions of insurance will include all of the following, EXCEPT

a. risk transfer mechanism. b. means of savings. c. cost stabilization. d. reducing losses.

CHAPTER 1 - INTRODUCTION TO INSURANCE

10

CHAPTER 1 - INTRODUCTION TO INSURANCE

5. Life insurance contracts can be arranged to provide cover against the following forms of risk:

I. bank loans. II. premature death. III. sickness or disability. IV. continuous stream of income during retirement (i.e. old age).

a. I and II. b. I, II and IV. c. III and IV. d. All of the above.

6. Amongstmanyotherrisks,generalinsurancecontractswillcoverthefollowing, EXCEPT:

a. property. b. accident. c. natural death. d. legal liability.

7. Insurance, as an organization, seeks to provide protection against ___________ caused by fortuitous events.

a. emotional losses. b. sentimental losses. c. financiallosses. d. non-financiallosses.

8. WhichONEofthefollowingfactsisNOTtrueaboutbothlifeandgeneral insurance?

a. Life insurance policies are subject to the principle indemnity whereas general insurance policies are not. b. General insurance policies are subject to the principle of indemnity whereas life insurance policies are not. c. Life insurance policies and general insurance policies will both pay when a person suffers permanent disablement due to an accident. d. Life assurance is a long-term contract whereas general insurance is a yearly renewable contract.

CHAPTER 1 - INTRODUCTION TO INSURANCE

11

9. The operation of the principle of the law of large numbers will ensure

a. better prediction of future losses. b. better understanding of the market. c. better understanding of the customers. d. bettercashflowfortheinsurer.

10. The essential features of insurance are:

I. It is economic institution. II. It is based on the principle of mutuality or co-operation. III. Its objective is to accumulate funds to pay for claims that arise as a result of the operationofspecificrisks. IV. Onlycertainriskscanbeinsuredagainst,namelythose,whoseoccurrencecanbe confidentlyestimatedwithacertaindegreeofaccuracy.

a. I and II. b. II and IV. c. II, III and IV. d. All of the above.

YOU WILL FIND THE ANSWERS AT THE BACK OF THE BOOK.

CHAPTER 2 - NATURE OF RISK AND RISK MANAGEMENT

12

Overview 2.1. Concepts of Risk 2.2. Related Concepts 2.3. Basic Categories of Risk

2.4. Methods of Handling Risks 2.5. Risk Management

2.6. Characteristics of Insurable Risk

OVERVIEW

This chapter focuses on risk and a detailed discussion of the following is provided:

• Characteristics of Risk

• Concepts Related to Risk

• The Measurement of Risk

• The Management of Risk

• The Characteristics of Insurable Risks

2.1. CONCEPTS OF RISK

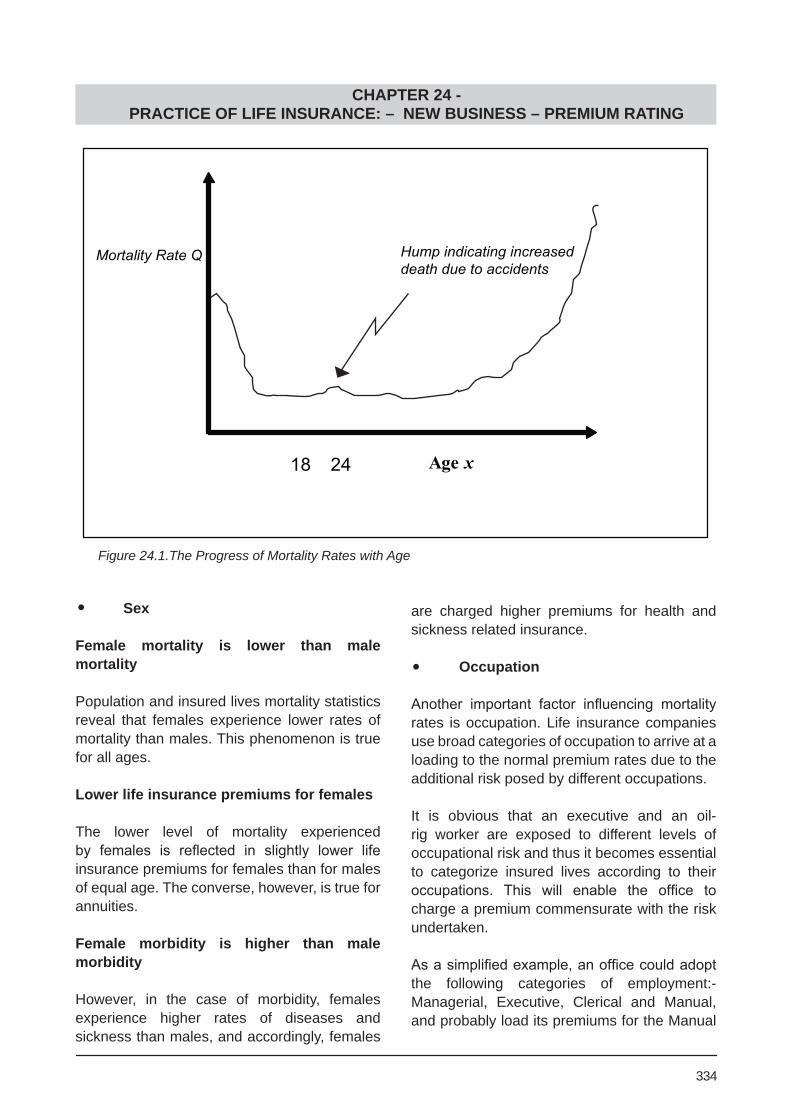

We live in a world in which we are continually exposed to perils. A peril is usually a cause of loss.Typicalperils includefire,collision,flood,sickness and premature death. When perils occur, propertymay be destroyed or lost andpeople injured or killed. Any loss of property or liveswillinvariablyleadtofinanciallosses.

Figure 2.1. Examples of Perils and their Consequent Losses

CHAPTER 2 - NATURE OF RISK AND RISK MANAGEMENT

Although we are continually exposed to perils,weareuncertainastowhensuchloss-producingeventswilloccur.Inotherwords,weare uncertain about the losses we may suffer in the future. An uncertainty regarding loss is often termed as “risk”. Since risk exists whenever the futureisunknown,itcanbesaidtobepresenteverywhere and in all circumstances. It is present in human lives and in industry.

Measurement of Risk

Even though we are uncertain about a future loss, it ispossible todetermine thechanceofloss using a branch of mathematics known as the probability theory. The term “probability” refers to an area of study which measures the chance of occurrence of particular events. The study of chance, events or probability can beapproachedalongthreepossiblelines:Apriori,empirical and judgmental.

Application of A Priori Probability

A priori probability is determined when the total numbers of possible events are known. For example, theprobabilityofgettingafiveonaroll of dice is 1/6 or 0.1666. The priori concept has limited practical application in the study of risk and insurance because situations where the possible outcomes have an equal chance of occurrence are very rare.

Application of Empirical Probability

Empirical probability is determined on the basis of historical data. For example, a transportcompany which operates a fleet of 1000vehicles and experiences an average of 50 accidents over the previous year has a 50/1000 or 0.05 probability of an accident occurring the next year. The underlying concept that makes it possible for empirical probability to be measured accurately is the law of large numbers. (See 1.3.)

Application of Judgmental Probability

Judgmental probability is determined based on the judgment of the person predicting the outcomes. Judgmental probability is used when there is a lack of historical data or credible statistics. For example, judgmental probabilityis used in insurance of nuclear plants because of a lack credible statistics. In practice, actual outcomes differ from expected outcomes

Inpractice,an insurancecompany,dependingontheavailabilityandcredibilityofdata,usestheempirical or judgmental probability techniques to predict future losses. In any events, eithertechnique provides an estimation of the future loss. This implies that actual outcomes may not be the same as the expected outcomes. Forexample,aninsurancecompanywhichhaspredicted that 30 of its insured cars may be destroyed next year faces the possibility that the numberofcarsactuallydestroyedmaybe20,40 and 50 or even 100. Such random variations from predicted outcomes arise because the requirements of the law of large numbers are seldom met in practice.

Other Possible Definitions of Risk

Even though an insurance company has a large number of similar loss exposures and thereforeisabletopredictanexpectedloss,itis nevertheless subject to uncertainly because the actual loss may not be the same as the predictedloss.Andwhenuncertainlyexists,riskremains. In this respect,we can takeanotherstepfurtherbydefiningriskasthevariation inoutcomes in a given situation. In addition to the two definitions given, the term “risk” has alsobeen loosely referred to as

• the possibility of loss;

• the exposure to danger;

• the subject matter of insurance.

13

CHAPTER 2 - NATURE OF RISK AND RISK MANAGEMENT

In conclusion, it can be said that risk hasseveral meanings and the meaning of risk will therefore depend on the context in which it is being used.

2.2. RELATED CONCEPTS

Beforeweconsidertheotheraspectsofrisk,itis important to distinguish risk from the following concepts:

• Loss : a reduction or disappearance of economic value.

• Peril : a cause of loss.

• Hazard: a condition that increases the chance of loss.

There are two major types of hazards.

Physical Hazard Defined

Physical hazard is a physical characteristic that increases the outcome of a loss. Examples of physical hazards include the wooden construction of building and the poor mechanical condition of a motor car.

Moral Hazard Defined

Moral hazard is a character defect in an individual that increase the outcome of a loss. Examplesofmoralhazardsincludedishonesty,carelessness and unreasonableness.

2.3. BASIC CATEGORIES OF RISK

Risk can be classified into two majorcategories:

• Fundamental and particular risks;

• Pure and speculative risks.

2.3.1. Fundamental and Particular Risks

Fundamental Risks Defined

A fundamental risk affects the entire economy or large numbers of persons / groups within the economy. Examples include the risk of property damage from earthquake, flood andtyphoon(forcesofnature), theriskofdamagetoproperty,thelossoflivesarisingoutofwar,and the risk of mass unemployment.

Particular Risks Defined

A particular risk affects individuals and not the entire community or country. Examples include the risk of damage to property from fire andthe risk of death or injury resulting from road accidents

Whose Responsibility?

Becauseoftheirdifferenceineffects,particularrisks are the responsibility of individuals whereas fundamental risks are the responsibility of the government and society as a whole.

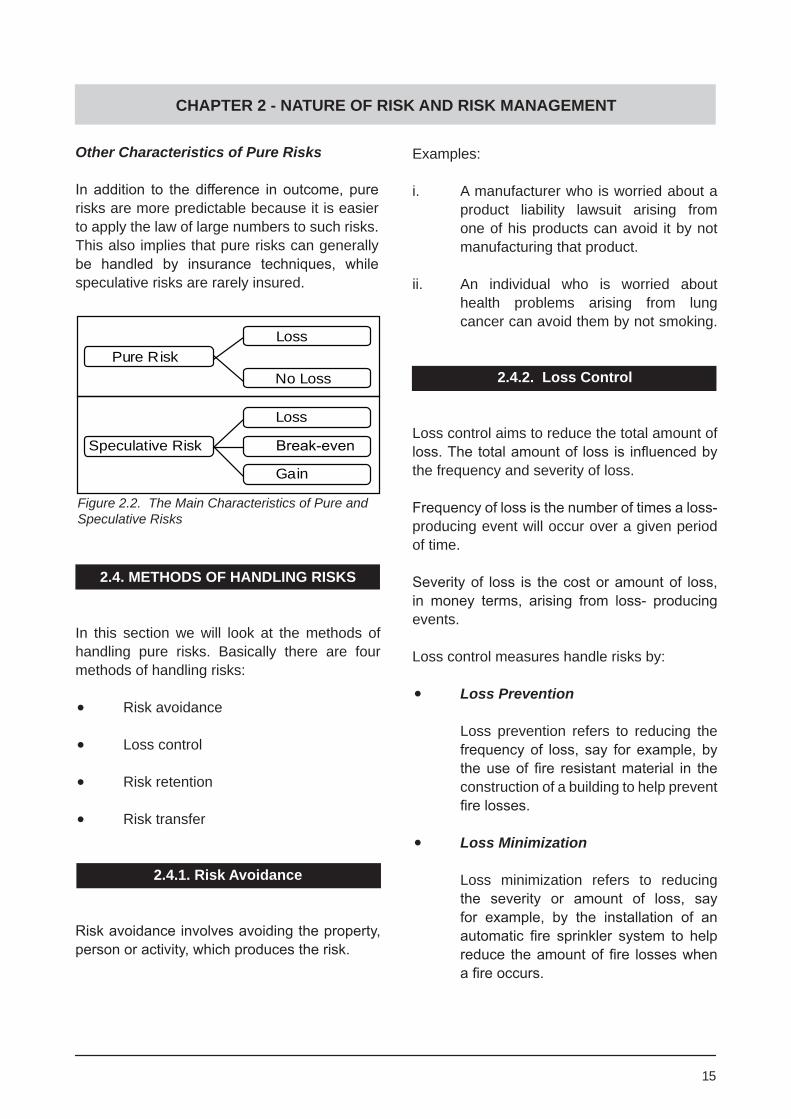

2.3.2. Pure and Speculative Risks

Pure Risks Defined

Pure risk exists when there is the possibility of either loss or no loss. Examples include the risk of damage to property resulting from fire andthe risk of premature death.

Speculative Risks Defined

Speculative risk exists when there is the possibility of profit, loss or no loss.Examplesinclude investment in the stock market or real estate, venturing intobusiness,andbetting ina horse race.

14

CHAPTER 2 - NATURE OF RISK AND RISK MANAGEMENT

Figure 2.2. The Main Characteristics of Pure and Speculative Risks

Other Characteristics of Pure Risks

In addition to thedifference in outcome,purerisks are more predictable because it is easier to apply the law of large numbers to such risks. This also implies that pure risks can generally be handled by insurance techniques, whilespeculative risks are rarely insured.

2.4. METHODS OF HANDLING RISKS

In this section we will look at the methods of handling pure risks. Basically there are four methods of handling risks:

• Risk avoidance

• Loss control

• Risk retention

• Risk transfer

2.4.1. Risk Avoidance

Riskavoidanceinvolvesavoidingtheproperty,personoractivity,whichproducestherisk.

Examples:

i. A manufacturer who is worried about a product liability lawsuit arising from one of his products can avoid it by not manufacturing that product.

ii. An individual who is worried about health problems arising from lung cancer can avoid them by not smoking.

2.4.2. Loss Control

Loss control aims to reduce the total amount of loss.Thetotalamountof lossis influencedbythe frequency and severity of loss.

Frequencyoflossisthenumberoftimesaloss-producing event will occur over a given period of time.

Severityof loss is thecostoramountof loss,in money terms, arising from loss- producingevents.

Loss control measures handle risks by:

• Loss Prevention

Loss prevention refers to reducing the frequencyof loss, say forexample, bytheuseof fire resistantmaterial in theconstruction of a building to help prevent firelosses.

• Loss Minimization

Loss minimization refers to reducing the severity or amount of loss, sayfor example, by the installation of anautomatic fire sprinkler system to helpreduce theamountoffire losseswhenafireoccurs.

15

Pure Risk

Speculative Risk

Loss

No Loss

Loss

Break-even

Gain

CHAPTER 2 - NATURE OF RISK AND RISK MANAGEMENT

2.4.3. Risk Retention

Risk retention involves the retaining of risks by an individual or organization. When risks are retained, the losses incurredareborneby theparty retaining the risks. Risk retention may be planned or unplanned. When risk retention is planned, risks are retained deliberately.Unplanned risk retention involves the retaining of risks unknowingly.

2.4.4. Risk Transfer

Risk transfer involves the transferring of risks to an organization or individual. When a risk is transferred, the losswill be paid for by theorganization or individual to whom the risk is transferred. There are two ways of transferring risks.

• Insurance Contract

Example: A house owner can transfer the loss incurred when his house is destroyedbyfirebyenteringintoafireinsurance contract.

• Non Insurance Contract

Example: A supermarket can transfer potential liability arising from the sale of a defective product by entering into an agreement whereby the manufacturer agrees to compensate the supermarket from any liability arising from the defective product.

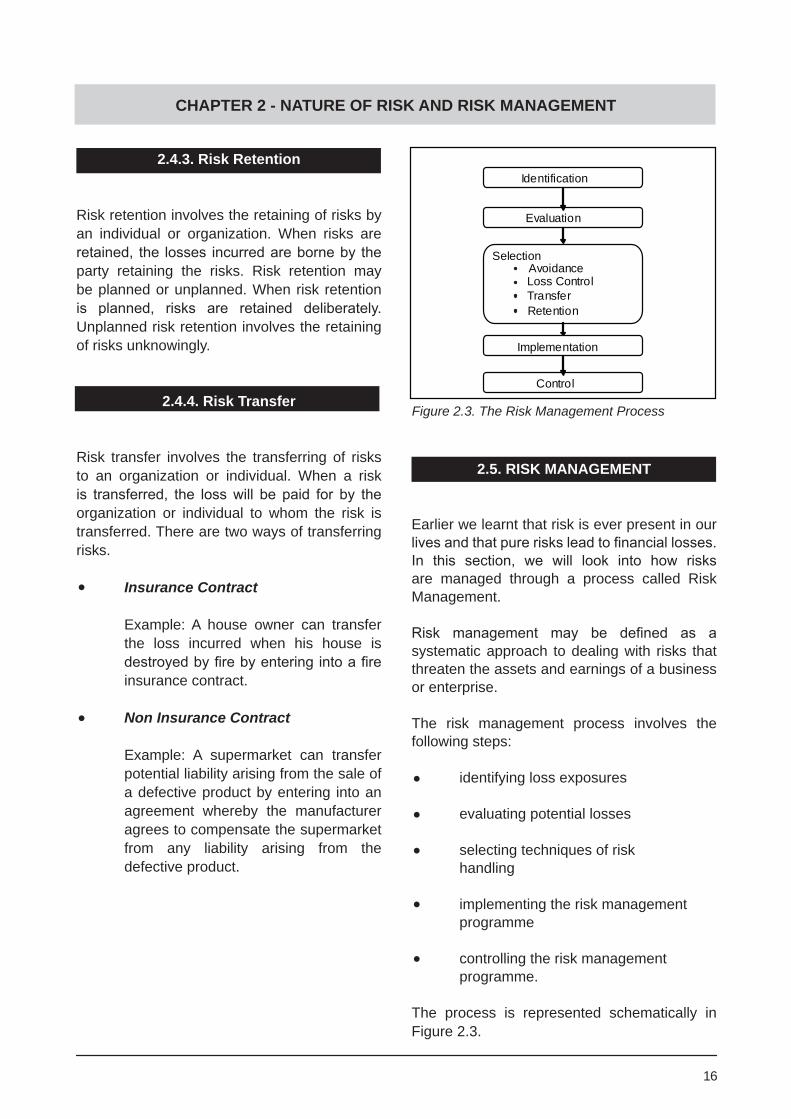

Figure 2.3. The Risk Management Process

Identification

Evaluation

SelectionAvoidanceLoss ControlTransferRetention

Implementation

Control

16

2.5. RISK MANAGEMENT

Earlier we learnt that risk is ever present in our livesandthatpurerisksleadtofinanciallosses.In this section, we will look into how risksare managed through a process called Risk Management.

Risk management may be defined as asystematic approach to dealing with risks that threaten the assets and earnings of a business or enterprise.

The risk management process involves the following steps:

• identifying loss exposures

• evaluating potential losses

• selecting techniques of risk handling

• implementing the risk management programme

• controlling the risk management programme.

The process is represented schematically in Figure 2.3.

CHAPTER 2 - NATURE OF RISK AND RISK MANAGEMENT

17

2.5.4. Implementing the Risk Management Programme

After the selection of the most appropriate technique or combination of techniques, thenext step is to implement the risk management programme.

2.5.5. Controlling the Risk Management Programme

Once implemented, a risk managementprogramme needs to be monitored to ensure that it is achieving the results expected and to makechangestotheprogramme,ifnecessary.

2.6. CHARACTERISTICS OF INSURABLE RISK

Not all risks are capable of being insured. Risks that are insurable must fulfil certaincharacteristics. The main characteristics are as follows:

2.6.1. Financial Value

Insurance is concerned with situations where monetary compensation can be given following aloss.Therefore,insurablerisksshouldinvolvelosses that are capable of being financiallymeasured. The following are some examples of such risks:

2.5.1. Identifying Loss Exposures

Thefirststepinriskmanagementistoidentifyall pure loss exposures including

• physical damage to property;

• business interruption losses;

• liability lawsuits;

• lossesarisingfromfraud,criminal acts and dishonesty of employees;

• losses arising from the death or disability of key employees.

Lossexposurescanbeidentifiedfromvarioussources including questionnaires, financialstatements,flowchartsandpersonalinspectionof facilities.

2.5.2. Evaluating Potential Losses

After identifying potential losses, the nextstep is to evaluate the potential losses of the firm. Evaluation involves the estimation ofthe frequency and severity of loss exposures and ranking them according to their relative importance. Loss exposures with high loss potential will be given priority in the risk management programme.

2.5.3. Selecting Risk Handling Techniques

Riskhandlingtechniquesincluderiskavoidance,loss control, risk retention and risk transfer.The selection of a risk handling technique may bebasedonfinancialornon-financial criteria.Selectionbasedonfinancialcriteriawillconsiderhow the choice will affect the organization’s profitability or rate of return. Non-financialconsiderations will include humanitarian aspects and legal requirements.

Risks Financial Measurementi. Damage to Property Cost of Repairs

ii. Injury to Others Court Awards

iii. Death of a Life Assured The ability to pay the premium in relation to the sum assured and his

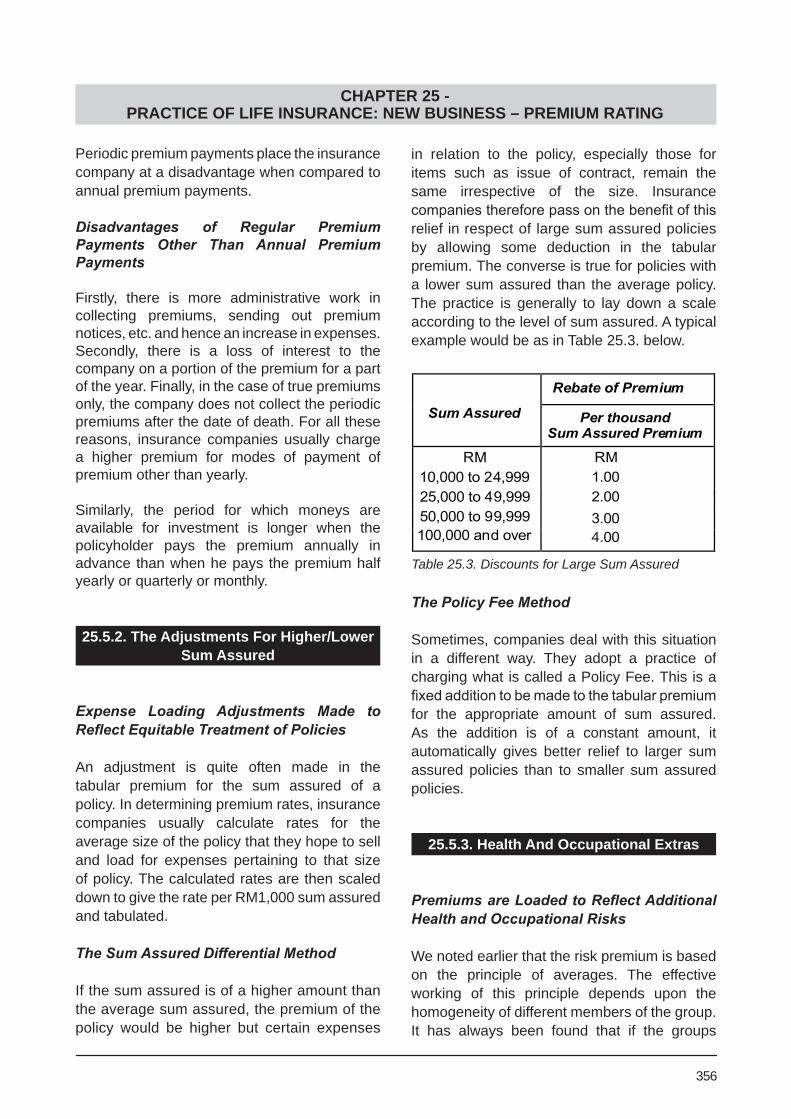

financial standing

CHAPTER 2 - NATURE OF RISK AND RISK MANAGEMENT

18

2.6.2. Large Number of Similar Risks

There must be a large number of similar risks before any one of the risks is capable of being insured. There are two reasons for this:

• To enable the insurer to predict losses more accurately.

• Ifthereareonlyfewrisks,the principle of losses of a few to be borne by many cannot be applied.

2.6.3. Pure Risks Only

Insurance is concerned only with pure risks becauseinapurerisksituation,onewillsufferalossorincurnoloss,thusthereisnopossibilityofprofiting fromapure risk.Speculative riskshold out the prospect of loss, break-even orprofit,andthusarerarelyinsured.Aninsuredinsuch a situation would be less inclined to put in efforts to bring about a gain because the insurer will indemnify any loss.

2.6.4. No Catastrophic Losses

Fora risk tobe insurable, the lossshouldnotbe so catastrophic in nature as to render it too heavy to be borne by an insurer. A catastrophic loss arises when a very large number of risks incur losses at the same time or when one risk results in a huge loss. Examples of catastrophic losses include losses arising from wars and earthquakes.

2.6.5. Fortuitous Losses

Another characteristic of insurable risk is that the loss must be fortuitous. A fortuitous loss is one that is accidental and unintentional. Insurance

cannotfunctionproperlyandefficientlyiflossesare intentionally or fraudulently brought about by the insured.

2.6.6. Insurable Interest

Generally, a person who wishes to effectinsurance must have insurable interest in the property, rights, interest, life, limb or potentialliability to be insured. The existence of insurable interest in contracts of insurance is one of the main factors that differentiate insurance from gambling. (Insurable interest will be dealt with further in Chapter 3.)

2.6.7. Legal and Not Against Public Policy

The object of insurance must be legal and not against public policy. A ship engaged in smuggling or a wager on a life is not an insurable risk because such a risk is of an illegal nature. Fines and penalties imposed by law are not insurable because it is against public policy to provide insurance for such events.

2.6.8. Reasonable Premium

The final characteristic of an insurable risk isthat the premium must be reasonable in relation to the potential loss. A risk that has a very high probability of loss or near certainty would involve a premium that may be unreasonable from the prospective insured’s point of view. On the other hand,theinsurancepremiumrequiredtocoverthe riskof fireonaballpointpenwortha fewcents may be quite unreasonable in relation to the potential loss in view of the insurer’s claim handling expenses.

CHAPTER 2 - NATURE OF RISK AND RISK MANAGEMENT

SELF - ASSESSMENT QUESTIONS

CHAPTER 2

1. Which of the following is NOT a characteristic of an insurable risk?

a. It should not be against public policy. b. It must be accidental in nature. c. It must be a speculative risk. d. It must be a pure risk.

2. Which of the following is the least effective approach to risk management?

a. avoiding the risk. b. transferring the risk. c. retaining the risk. d. ignoring the risk.

3. WhichofthefollowingisNOTalosspreventionandlossreductiontechniqueinfire insurance?

a. trainingemployeesinfireprevention. b. disposal of waste material in a proper manner and good housekeeping. c. useofnon-combustiblematerialinbuildingconstruction. d. installation of a burglar alarm system.

4. Which of the following is NOT a loss prevention and loss reduction technique in life and health insurance?

a. trainingemployeesinfirstaid. b. avoiding cigarette smoking. c. insuringalifeforanamountinlinewithhisfinancialstandinginlife. d. installing grills in windows of the house in which the life assured is living.

5. Which of the following is NOT a pure risk?

a. Fire. b. Flood. c. Theft. d. Operating a supermarket.

19

CHAPTER 2 - NATURE OF RISK AND RISK MANAGEMENT

6. Which of the following descriptions is incorrect?

a. Peril is the prime cause of a loss. b. Hazardswillinfluencetheoutcomeoflosses. c. An uncertainly regarding loss is often termed as risk. d. Moral hazard can be determined by the physical characteristics of a risk.

7. Whenapersonstopsplayingfootballbecausehedoesnotwantgethurt,therisk control method used is known as

a. loss prevention. b. risk avoidance. c. risk transfer. d. risk retention.

8. The best description of a pure risk would be

a. breakeven,gainorloss. b. break even or loss. c. gain or loss. d. loss.

9. Which of the following determines the total amount of loss under the loss control method of handling pure risk?

I. frequency. II. severity of loss. III. physical hazard. IV. moral hazard.

a. I and II. b. II and III. c. III and IV. d. All of the above.

20

CHAPTER 2 - NATURE OF RISK AND RISK MANAGEMENT

10. Thebestdefinitionofinsurableinterestwouldbe

a. any form of relationship a proposer has with the subject matter of insurance. b. any future relationship that can come about between the proposer and subject matter of insurance. c. an interest that is created by having the prospect of inheriting the subject matter of insurance. d. thelegalrighttoinsurearisingfromthelegitimatefinancialinterest,which an insured has in a subject matter of insurance.

YOU WILL FIND THE ANSWERS AT THE BACK OF THE BOOK.

21

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

22

Overview 3.1. Principles of Insurance 3.2. Takaful 3.3. Shariah Supervisory Council

3.4. Takaful and Insurance

3.5. Principles of Takaful Operation

3.6. Aspects of Takaful Operation 3.7. Types of Takaful Business

OVERVIEW

The following basic principles of insurance are covered in this chapter:-

• Insurable Interest

• Utmost Good Faith

• Indemnity

• Subrogation

• Contribution

• Proximate Cause

This chapter also provides an introduction to takaful:

• An Introduction to Takaful

• The Shariah Supervisory Council

• Takaful and Insurance

• Principles of Takaful Operation

• Aspects of Takaful Operation

• Types of Takaful Business

3.1. PRINCIPLES OF INSURANCE

Insurance contracts are not only subject to the general principles of the law of contract but also certain special legal principles that are embodied in insurance contracts.

Special Legal Principles Embodied in Insurance Contracts

• Insurable Interest,

• Utmost Good Faith,

• Indemnity,

• Subrogation,

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

Table 3.1. Subject Matter of Insurance

• Contribution, and

• Proximate Cause

3.1.1. Insurable Interest

Insurance must be supported by insurable interest

Insurance is quite different from gambling. One of the major differences between insurance and gambling is that unlike the latter, insurance must be supported by insurable interest.

Before looking at the concept of insurable interest, it is important for readers to be familiar with two related concepts, namely:

• Subject matter of insurance, and

• Subject matter of the insurance contract.

3.1.1.1. Subject Matter of Insurance

In the insurance business, the subject matter of insurance may be any property, potential legal liability, rights, life or limbs insured under a policy. The types of subject matter of insurance are as varied as the types of insurance available. Some examples of the subject matter of insurance under the various types of insurance can be found in Table 3.1 below.

3.1.1.2. Subject Matter of the Insurance Contract

The subject matter of insurance should not be confused with the subject matter of the insurance contract, which is the financialinterest of an insured in the subject matter of insurance. To distinguish between the two, consider a person who has insured his house valuedatRM100,000againstfireorhisownlifefor RM100,000 against death. In this case, the house or life is the subject matter of insurance andtheinsured’sfinancialinterestinthehousevalued at RM 100,000 or his life is the subject matter of the insurance contract.

3.1.1.3. What is Insurable Interest?

Insurable Interest Explained

Insurable interest is the legal right to insure arisingfromthelegitimatefinancialinterestwhichan insured has in a subject matter of insurance. Thephrase “legitimatefinancial interest” refersto a financial interest which is recognized atlaw. Thus, when a person’s financial interestin a subject matter of insurance is not legally recognized, he lacks the necessary insurableinterest to effect a valid insurance. It is for this reason that a thief cannot effect a valid insurance on the goods stolen by him nor can a person effect a valid insurance on the life of another if he hasnofinancialrelationshiprecognizedbylawtothat life as this would be considered wagering.

3.1.1.4. When Must Insurable Interest Exist?

For general insurance contracts, insurable interest must exist at the beginning and at the time of loss. Marine insurance is an exception.

As a general rule, a person who effects a general insurance contract must have insurable interest at the time he enters into it and at the time of

23

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

loss. Otherwise, the insurance effected is void. However, this general rule does not apply to marine insurance. In this class of insurance, the insured needs only to have insurable interest at the time a loss occurs to be able to enter into a valid contract. For example, an importer of goods will be able to validly arrange for insurance on the goods he expects to import so long as he later acquires insurable interest, that is by becoming the owner before an insured peril happens. On the other hand, a person cannot validly arrange for motor insurance on a car which he anticipates to own in the future.

For life insurance contracts, insurable interest must exist at the beginning only.

In contrast, the application of insurable interest to life insurance is quite straightforward. The insured needs only to have insurable interest at the time of effecting the life insurance contract. Subsection 152(1) of the Insurance Act 1996 also makes provision for this.

Who Has Insurable Interest?

In property insurance, an owner, trustee, agent, mortgagee or hirer has insurable interest in the property owned, held in trust, held in commission, mortgaged and hired respectively. On the other hand, liability insurance can be effected by anyone who has potential legal liability and legal costs and expenses associated with it. With respect to life and personal accident insurance, a person has unlimited insurable interest in his own life and limbs. Subsection 152(2) of the Insurance Act 1996 provides that a person shall be deemed to have insurable interest in relation to another person who is

a. his spouse, child or ward being under the age of majority at the time the insurance is effected;

b. his employee; or

c. a person on whom he is at the time the insurance is effected, wholly or partly, dependent.

3.1.2. Assignment

Generally speaking, an assignment is the transfer of rights and liabilities by one person to another. In insurance, the transfer of all rights and liabilities of the insured to a new insured is referred to as an assignment of policy. An assignee, the person who takes over the assigned rights, will have no better rights than those enjoyed by the assignor. Thus, if the insurer is able to repudiate liability on any grounds against the assignor, the same grounds may be used against the assignee.

3.1.2.1. Prior Consent

Prior consent of the insurer is needed for an assignment to be valid.

Insurance contracts are generally referred to as personal contracts because the insurer’s decision to enter the contract depends very much on the qualities of the insured. Thus, when an insurer enters into a contract with a particular insured that insured cannot assign his right in the policy to another less prior consent of the insurer has been obtained. For example, the vendor of a house cannot assignhisfirepolicytothepurchaserunlesstheinsurer concerned agrees to the substitution of the vendor to the purchaser as the new insured. Legally, when an insurer gives consent to the substitution of the insured by a new insured, a new contract is created between the insurer and the assignee of the original policy. This alteration istermed“novation”.

3.1.2.2. Exception to the Rule

Although prior written consent of the insurer is generally required before the assignment of policies can be effected, there are three exceptions to this rule.

24

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

25

• Marine policies

They are freely assignable by statutory provision in the Marine Insurance Act 1906. In practice, only cargo policies are freely assignable while hull policies usually contain a clause which prohibits the assignment of policies without the insurer’s consent.

Cargo policies are freely assignable because they are important documents of overseas trade and provide collateral securitytothebankswhichfinancetheoverseas trade.

• Life policies

Life policies are assignable by statutory provision under the Policies of Assurance Act 1867, subject to the conditions outlined in section 23.3. of Chapter 23.

• Transfer by will or operation of law

Certainpolicies,forexamplefirepoliciesprovide for the automatic assignment of a policy if the transfer of interest in the subject matter of insurance is made by a will or operation of law.

Assignment of Claim Amount.

In insurance, the term “assignment” is alsoused in the context of the assignment of policy proceeds. An assignment of policy proceeds arises when the insured instructs his insurer to pay the policy proceeds to a third party. For example, there is an assignment of policy proceeds when an insured instructs his fireinsurer to pay the amount of indemnity (for the damage of his house) to which he is entitled to the repairer. In life insurance, assignment of the policy proceeds occurs when the policyowner namesabeneficiarytoreceivethedeathbenefitunder his policy. In such an assignment, the insured remains a party to the insurance contract and continues to assume liabilities under it even after the assignment of policy proceeds. All

policy proceeds are freely assignable unless the contract provides otherwise.

Part XIII of the Insurance Act 1996 deals with the payment of policy monies under a life policy, including a life policy under section 23 of the Civil Law Act 1956, and a personal accident policy, effected by the policyowner upon his own life providing for payment of policy monies on his death. Section 163 of Part XIII provides that a policyowner who has attained the age of eighteen (18) years may nominate a person to receive the policy monies upon his death under the policy by notifying the insurer in writing the following details of the nominee:

a. Name,

b. Date of birth,

c. Identity card number or birth certificatenumber,and

d. Address.

Such nomination shall be witnessed by a person of sound mind who has attained the age of 18 years and who is not a nominee named under the policy.

3.1.3. The Principle Of Utmost Good Faith

3.1.3.1. Ordinary Commercial Contracts

In most commercial contracts, there is no need for the parties to disclose information not requested. Each party is expected to make the best bargain for himself so long as he does not mislead the others. The legal principle governing such contracts is caveat emptor (let the buyer beware).

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

26

Subsection 150(2) continues that the duty of disclosure does not require the disclosure of a matter that

a. diminishes the risk to the insurer;

b. is of common knowledge;

c. the insurer knows or in the ordinary course of his business ought to know; or

d. in respect of which the insurer has waived any requirement for disclosure.

Subsection 150(3) further states that “Where a proposer fails to answer or gives an incomplete or irrelevant answer to a question contained in the proposal form or asked by the insurer and the matter was not pursued further by the insurer, compliance with the duty of disclosure in respect of the matter shall be deemed to have beenwaivedbytheinsurer”.

(Read also Chapter 7 Section 7.6.2. concerning knowledge of, and statement, by an insurance agent.)

3.1.3.4. Material Fact

Material facts are to be disclosed by the insured.

Amaterial fact is a fact which will influence aprudent underwriter in deciding the acceptance of the risk or the premium to be charged. The materiality of a fact depends on the nature of the proposed insurance. For example, the alcohol consumption of a proposer may be a material fact to either a motor or a personal accident insurer but the same fact is not material to a marine cargo insurer. The materiality of a fact also depends on the circumstances surrounding a proposed risk. Thus, a fact relating to alcoholism may not be material in a motor insurance proposal if the proposer is always chauffeured.

3.1.3.2. Insurance Contracts

The insured has to disclose all important facts regarding the risk to be insured.

Different considerations apply to a contract of insurance. When an insurer is assessing a proposal he cannot examine all the material aspects of the proposed insurance. On the other hand, the proposer knows or should know everything about the risk proposed. This situation places the insurer at a disadvantage. He is not able to make a complete assessment of the risk unless the proposer is willing to disclose information material to the risk proposed. To remedy this inequitable situation, the law imposes the duty of utmost good faith on the parties to an insurance contract. Since the insured knows more about the risk, the duty of disclosure tends to be more onerous on the insured than on the insurer.

Thisdutycanbedefinedasthepositivedutytodisclose fully and accurately all material facts relating to the proposed risk that a proposer knows or is reasonably expected to know, whether asked or not.

3.1.3.3. Duty of Utmost Good Faith

Section 150 of the Insurance Act 1996 makes emphasis on the duty of Utmost Good Faith, i.e. the duty of disclosure, particularly on the part of the proposer.

Subsection 150(1) states that “Before a contract of insurance is entered into, a proposer shall disclose to the insurer a matter that

a. he knows to be relevant to the decision of the insurer on whether to accept the risk or not and the rates and terms to be applied; or

b. a reasonable person in the circumstances could be expected to knowtoberelevant.”

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

Figure 3.1. Breaches of Utmost Good Faith

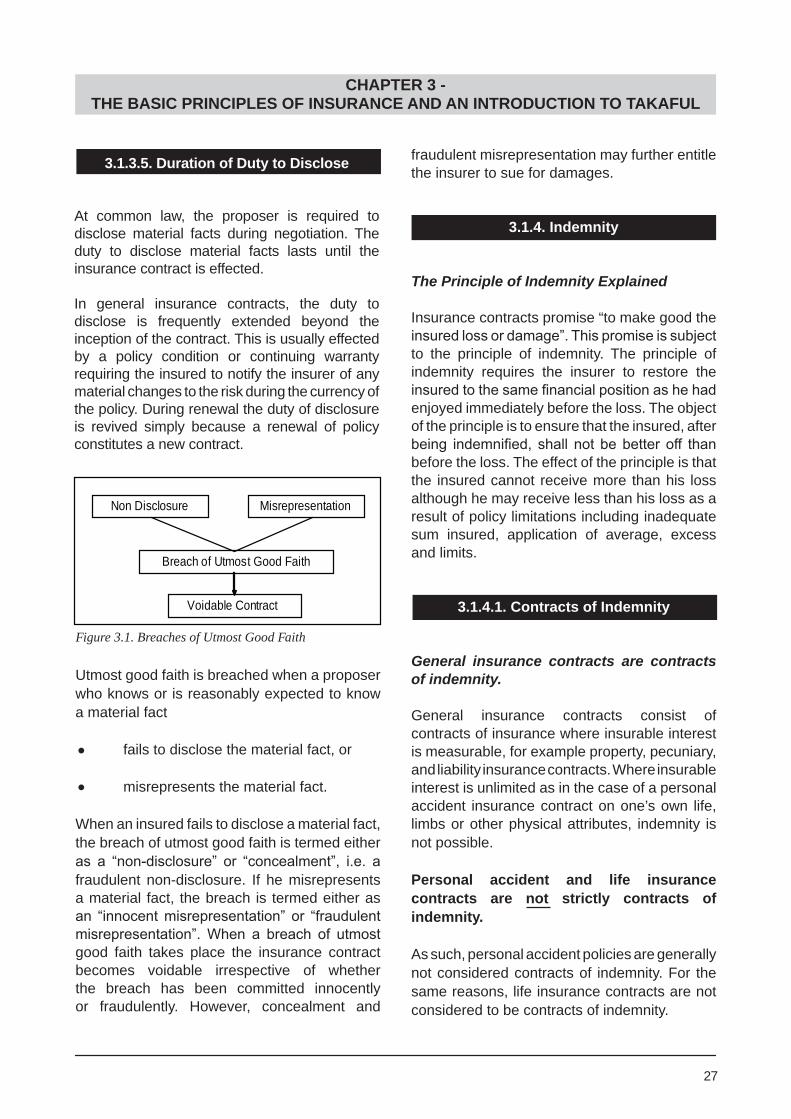

Non Disclosure Misrepresentation

Breach of Utmost Good Faith

Voidable Contract

27

3.1.3.5. Duration of Duty to Disclose

At common law, the proposer is required to disclose material facts during negotiation. The duty to disclose material facts lasts until the insurance contract is effected.

In general insurance contracts, the duty to disclose is frequently extended beyond the inception of the contract. This is usually effected by a policy condition or continuing warranty requiring the insured to notify the insurer of any material changes to the risk during the currency of the policy. During renewal the duty of disclosure is revived simply because a renewal of policy constitutes a new contract.

Utmost good faith is breached when a proposer who knows or is reasonably expected to know a material fact

• fails to disclose the material fact, or

• misrepresents the material fact.

When an insured fails to disclose a material fact, the breach of utmost good faith is termed either as a “non-disclosure” or “concealment”, i.e. afraudulent non-disclosure. If he misrepresents a material fact, the breach is termed either as an “innocentmisrepresentation” or “fraudulentmisrepresentation”.When a breach of utmostgood faith takes place the insurance contract becomes voidable irrespective of whether the breach has been committed innocently or fraudulently. However, concealment and

fraudulent misrepresentation may further entitle the insurer to sue for damages.

3.1.4. Indemnity

The Principle of Indemnity Explained

Insurance contracts promise “to make good the insuredlossordamage”.Thispromiseissubjectto the principle of indemnity. The principle of indemnity requires the insurer to restore the insuredtothesamefinancialpositionashehadenjoyed immediately before the loss. The object of the principle is to ensure that the insured, after being indemnified, shall notbebetteroff thanbefore the loss. The effect of the principle is that the insured cannot receive more than his loss although he may receive less than his loss as a result of policy limitations including inadequate sum insured, application of average, excess and limits.

3.1.4.1. Contracts of Indemnity

General insurance contracts are contracts of indemnity. General insurance contracts consist of contracts of insurance where insurable interest is measurable, for example property, pecuniary, and liability insurance contracts. Where insurable interest is unlimited as in the case of a personal accident insurance contract on one’s own life, limbs or other physical attributes, indemnity is not possible.

Personal accident and life insurance contracts are not strictly contracts of indemnity.

As such, personal accident policies are generally not considered contracts of indemnity. For the same reasons, life insurance contracts are not considered to be contracts of indemnity.

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

28

3.1.4.2. Measure of Indemnity and Methods of Indemnity

The measure of indemnity depends on the nature of insurance. Generally, indemnity in property insurance is based on either replacement cost less depreciation, or the market value, while in liability insurance it is measured by the amount of court award or negotiated out of court settlement plus approved costs and expenses. Indemnity in pecuniary insurance is measured by the amount of financial losssufferedbytheinsured,forexampleinafidelityguarantee insurance, indemnity is measured by theamountoffinanciallosssufferedasaresultof an employee’s dishonesty.

The methods of indemnity include payment by cash, repair, replacement or reinstatement.

3.1.5. The Principle Of Subrogation

The principle of subrogation provides that an insurerwhohasindemnifiedaninsuredforalossmay exercise the insured’s rights to claim from the third party in respect of the loss. The principle of subrogation has been developed to prevent the insured from getting more indemnity when he has two or more avenues to recover his loss. For example, when an insured object valued at RMl,000 has been destroyed by a negligent third party the insured may have two parties, in the absence of subrogation, to recover his loss, that is from the insurer and the negligent third party. If the insured recovers his loss from both parties

he would be able to recover a total of RM2,000. Topreventtheinsuredfrommakingaprofitoutof his loss, the insurer who has indemnifiedthe insured would exercise the insured’s rights under the principle of subrogation and attempt to recover from the negligent third party the amount paid to the insured. Subrogation is considered as a corollary of indemnity, that is it is a natural consequence of indemnity. Since subrogation arises when indemnity arises, it is not applicable to non-indemnity contracts.

3.1.5.1. How does Subrogation Arise?

Subrogation may arise in the following ways:

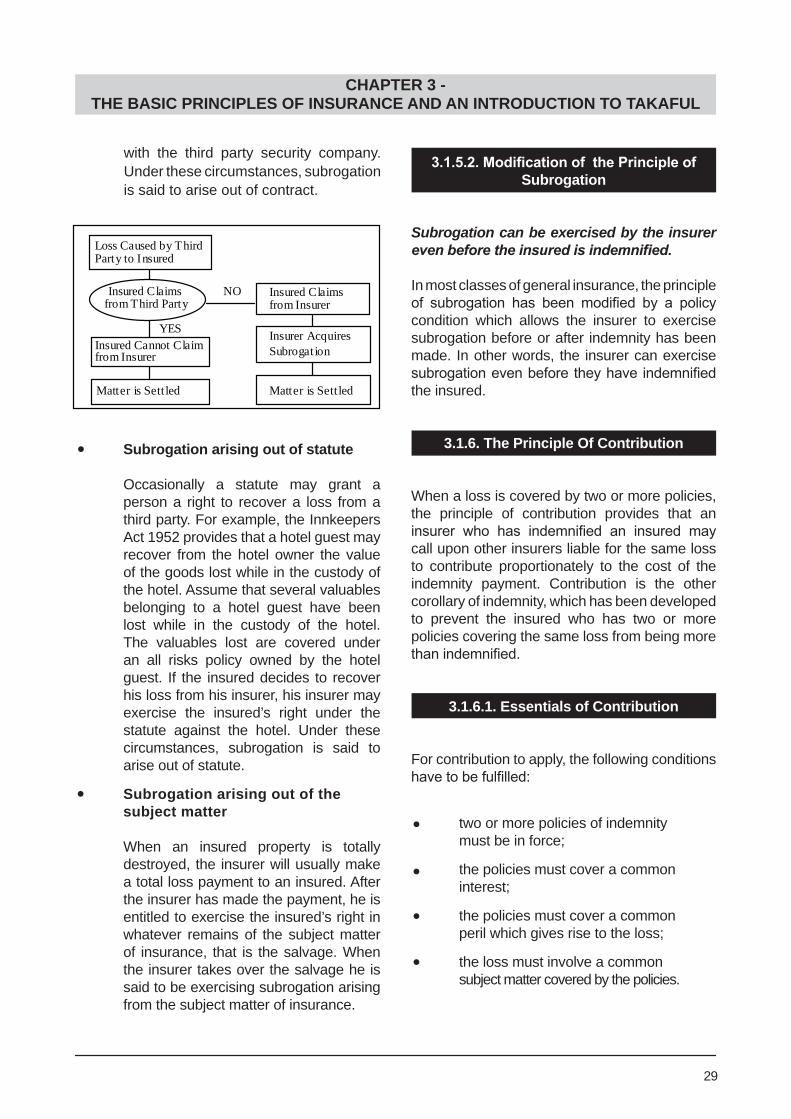

• Subrogation arising out of tort

When a tort, for example an act of negligence committed by a third party damages or destroys a property insured under a policy, the insured would have a righttobeindemnifiedunderthepolicy,as well as a right to recover the loss from the negligent third party. If the insured decides to recover his loss under his policy, the insurer will have subrogation right against the third party. Under these circumstances, subrogation is said to arise out of tort.

• Subrogation arising out of contract

Alternatively, the insured may have incurred a loss which is not only covered under a policy, for example a money policy, but is also covered under a contract entered between the insured and a third party, that is the security company carrying the money. The insured therefore may be able to recover his loss from either the insurer or the security company. If the insured decides to recover his loss from the insurer, the insurer may exercise the right of the insured to recover under the contract

Table 3.2. Classes of Insurance and Methods of Indemnity

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

with the third party security company. Under these circumstances, subrogation is said to arise out of contract.

• Subrogation arising out of statute

Occasionally a statute may grant a person a right to recover a loss from a third party. For example, the Innkeepers Act 1952 provides that a hotel guest may recover from the hotel owner the value of the goods lost while in the custody of the hotel. Assume that several valuables belonging to a hotel guest have been lost while in the custody of the hotel. The valuables lost are covered under an all risks policy owned by the hotel guest. If the insured decides to recover his loss from his insurer, his insurer may exercise the insured’s right under the statute against the hotel. Under these circumstances, subrogation is said to arise out of statute.

• Subrogation arising out of the subject matter

When an insured property is totally destroyed, the insurer will usually make a total loss payment to an insured. After the insurer has made the payment, he is entitled to exercise the insured’s right in whatever remains of the subject matter of insurance, that is the salvage. When the insurer takes over the salvage he is said to be exercising subrogation arising from the subject matter of insurance.

3.1.5.2.ModificationofthePrincipleofSubrogation

Subrogation can be exercised by the insurer even before the insured is indemnified.

In most classes of general insurance, the principle of subrogation has been modified by a policycondition which allows the insurer to exercise subrogation before or after indemnity has been made. In other words, the insurer can exercise subrogationevenbeforetheyhaveindemnifiedthe insured.

3.1.6. The Principle Of Contribution

When a loss is covered by two or more policies, the principle of contribution provides that an insurer who has indemnified an insured maycall upon other insurers liable for the same loss to contribute proportionately to the cost of the indemnity payment. Contribution is the other corollary of indemnity, which has been developed to prevent the insured who has two or more policies covering the same loss from being more thanindemnified.

3.1.6.1. Essentials of Contribution

For contribution to apply, the following conditions havetobefulfilled:

• two or more policies of indemnity must be in force;

• the policies must cover a common interest;

• the policies must cover a common peril which gives rise to the loss;

• the loss must involve a common subject matter covered by the policies.

29

Loss Caused by Third Party to Insured

YES

NO Insured Claims from Insurer

Insurer Acquires Subrogation

Matter is Sett led

Insured Cannot Claim from Insurer

Insured Claims from Third Party

Matter is Sett led

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

3.1.6.2.ModificationsofthePrincipleofContribution

The application of the principle of contribution can also bemodified by a policy condition. Inmost classes of general insurance the policy condition usually provides that when contribution exists, the insurer would pay the proportion of the loss for which he is liable.

3.1.7. The Principle Of Proximate Cause

3.1.7.1. Importance of the Principle of Proximate Cause

Onus of proof of loss rests on the insured.

Which among the many causes of losses can be taken to be the dominant cause of loss? This cause is the proximate cause.

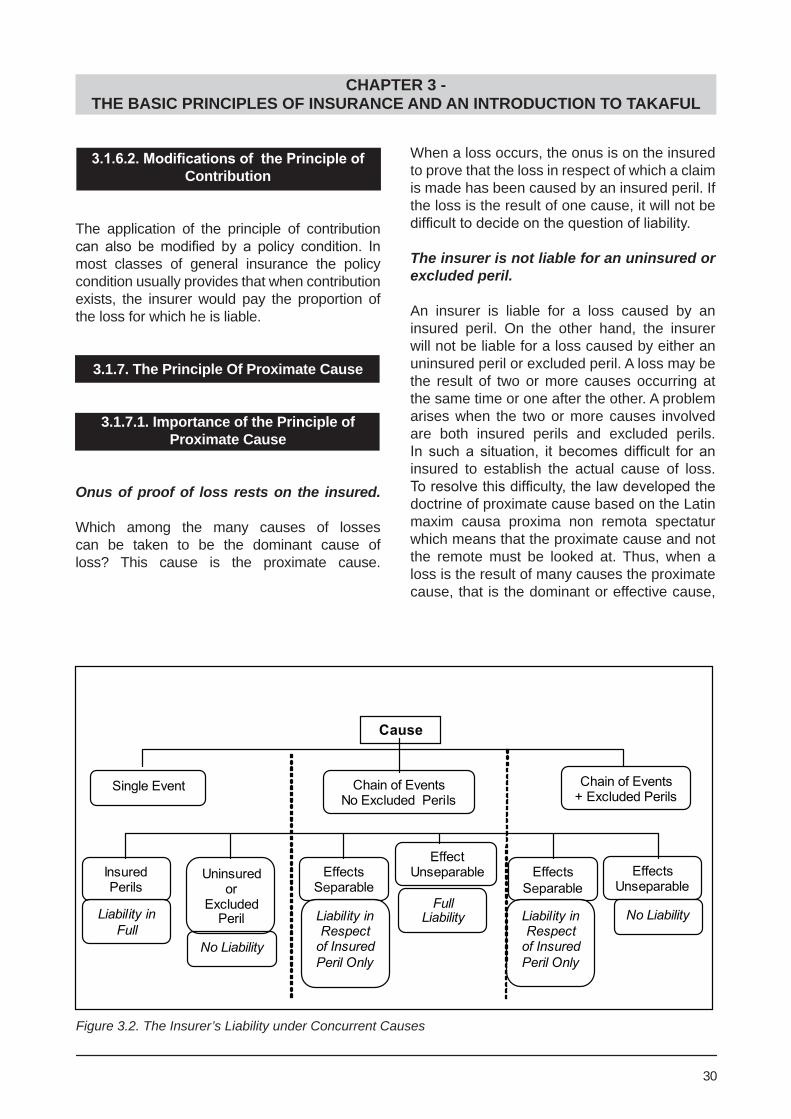

When a loss occurs, the onus is on the insured to prove that the loss in respect of which a claim is made has been caused by an insured peril. If the loss is the result of one cause, it will not be difficulttodecideonthequestionofliability.

The insurer is not liable for an uninsured or excluded peril.

An insurer is liable for a loss caused by an insured peril. On the other hand, the insurer will not be liable for a loss caused by either an uninsured peril or excluded peril. A loss may be the result of two or more causes occurring at the same time or one after the other. A problem arises when the two or more causes involved are both insured perils and excluded perils. In such a situation, it becomes difficult for aninsured to establish the actual cause of loss. Toresolvethisdifficulty,thelawdevelopedthedoctrine of proximate cause based on the Latin maxim causa proxima non remota spectatur which means that the proximate cause and not the remote must be looked at. Thus, when a loss is the result of many causes the proximate cause, that is the dominant or effective cause,

30

Figure 3.2. The Insurer’s Liability under Concurrent Causes

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

mustbe identifiedandattributedasthecauseof the loss.

Points to remember:

Insured perils are perils which are expressly covered by a policy.

Uninsured perils are perils not mentioned in the policy and therefore not covered by the policy unless they occur as a result of an insured peril. Examplesofuninsuredperilsinafirepolicyaresmoke and water damage.

Excluded perils are perils which have been expressly excluded from the policy.

3.1.7.2. Application of the Doctrine of Proximate Cause

3.1.7.2.1. Concurrent Causes

When two or more perils including one that is insured occur concurrently and the ensuing loss can be separated according to their effects, the insurer will be liable for the loss caused by the insured peril. However, if the loss cannot be separated the insurer will be liable for the full amount provided there is no excluded peril involved.

When an excluded peril is one of the concurrent causes, the insurer is liable for the loss caused by the insured peril only if the loss can be separated. If the loss cannot be separated the insurer will not be liable for the loss.

Figure 3.3 illustrates the points covered above.

3.1.7.2.2. Chain of Events

When there is an unbroken chain of events, the insurer will be liable for the loss insured under the policy from the insured peril onwards provided no excluded peril precedes an insured peril.

Let us look at some examples which explain the principles involved.

1. Examples of cases where no excluded peril is involved:

a. A building is insured under a fire insurance policy. The building catches fire due to an electrical short circuit. The local fire brigade is called and the fire is put out within one hour but the building and contents are badly damaged by the fire and water fromthefirefighters’hoses.

While the electrical short circuit is an uninsured peril, it is the proximate cause of the loss. The insurer is liable for any loss caused directly by thefireandalsoforthelossesresulting from the water from the firefighters’ hoses because such loss is considered adirectresultofthefire.

b. While crossing a road, a life assured is knocked down by a vehicle and dies. The accidental collision resulting in the death is the proximate cause of the loss and the insurer is liable.

2. Examples of cases where an excluded peril is involved:

a. A shop and its contents are insured underafirepolicy.A tankofacetylene gas used for welding explodes and causes fire to a motor repair shop. The explosion of gas used for commercial purposes is an excluded peril. If the explosion (an excluded peril) occurs before the fire (an insured peril), the insurer will not be liable for any loss caused by the fire. However, if the explosion happens after the fire, the insurer will be liable for the fire loss before the occurrence of the explosion.

b. A life assured is greatly depressed and throws himself over the balcony of a ten-storeyed building, resulting

31

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

in his death. His death occurs within one year of taking out a whole life assurance policy. As a result of the exclusion of the suicide clause in the policy, the insurer is not liable for the death by suicide.

Broken Chain of Events

When there is a broken chain of events, the proximate cause of loss is the one immediately following the last interruption.

Example 1:

An insured has a personal accident policy. While crossing a river he accidentally falls into it. He then suffers a heart attack and subsequently drowns. In this case, the drowning and not the heart attack is the proximate cause because there is a break in the chain of events between the drowning and the heart attack. The insurer isliabletopaythebenefitsunderthepersonalaccident policy.

Example 2:

An insured is involved in an accident and hospitalizedbutsubsequentlydiesofadiseaseunrelated to the accident. In this event the insurer will only be liable to pay the weekly hospital benefits arising out of the accident.No death benefits will be payable under thepersonal accident policy because the death is caused by an excluded peril, that is a disease.

3.2. TAKAFUL

In this section we will discuss takaful, an alternative to conventional insurance. Although the objective of providing protection may be similar, the actual workings of takaful differ from conventional insurance.

3.2.1. Overview Of Takaful

All human beings are exposed to the possibility of meeting with mishaps and disasters that result in misfortune and suffering such as death, destruction of property, loss of business or wealth, etc.

Islamic teachings encourage peace, brotherhood, and economic security of humankind. Islam teaches us to help each other regardless of religion. When one is facing a misfortune others should come to help so as to minimize the financial losses or emotionaldistress.Thisalso reflects the inherentnatureof mankind to find a solution collectively.The same basis is used in insurance where contribution from many help mitigate the losses of the unfortunate few. This insurance concept is generally accepted by Muslim jurists and does not contradict with the Shariah or Islamic religious laws. In essence, insurance is synonymous to a system of mutual help.

What is Takaful?

Takaful is an alternative to the contemporary insurance contract. Takaful is a form of insurance based on the principle of mutual assistance. Takaful is a noun stemming from the Arabic verb kafala meaning to protect or to guarantee. Essentially takaful means mutual help among a group to support the needy within the group through a fund contributed by group members.

The concept of takaful already existed during the time of the Prophet when Muslims contributed to a fund under the system of aqila for the purpose of helping members of their own community who were liable to pay “blood money (diyat)” in a situation wherea personis murdered unintentionally or to pay ransom to release war prisoners.

32

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

Essential Elements in Takaful

Within Islamic beliefs, the following are the underlying concepts that drive the acceptance of the takaful system:

• Piety or individual purification: People are accountable to Allah and their success in the hereafter depends on their performance in this life on earth.

• Brotherhood via ta’awun or mutual assistance: Policyholders cooperate among themselves for their common good.

• Charity through tabarru’ or donation: Every policyholder pays his contribution to help those that need assistance.

• Mutual guarantee.

• Self-sustaining operations as opposed to profit maximization: Losses are divided and gains are spread according to an agreed takaful model.

The basis of mutual help in takaful is grounded on the Islamic values of

1. sincere intention (niat) to help and support the needy by the group members as well as the manager of the fund; and

2. compliance to Shariah principles whereby business is conducted openly in accordance with utmost good faith, honesty, full disclosure, truthfulness and fairness in all dealings as well as avoidance of unlawful elements.

3.2.2. The Formation Of Takaful Companies In Malaysia

Malaysia is a model of an Islamic country that is serious in implementing an Islamic economy parallel with the conventional economy. The

introduction of Islamic financial products inMalaysia dates back to the 1980’s with the introduction of the first Islamic bank in thecountry, Bank Islam Malaysia Berhad. The successful introduction of Islamic banking products paved the way for other Islamic products in the market. The formation of takaful companies is part of the aspiration of the Malaysian government to establish an Islamic financial system in Malaysia. Takafulcompanies play a major role in providing insurance based on a system of operation that is in accordance with Islamic law or Shariah.

The Takaful Act 1984, passed by Parliament on 15 November 1984, was enacted to regulate the operations of takaful in Malaysia incompliancewithShariahprinciples.Thefirsttakaful company in Malaysia, Syarikat Takaful Malaysia Berhad, started its operations in 1984.

Takaful operations have been regulated and supervised by Bank Negara Malaysia (BNM) since 1988 with the appointment of the BNM Governor as the Director General of Takaful.

3.2.3. Takaful Act 1984

The Takaful Act 1984 is the source of Takaful legislation in Malaysia. The Insurance Act 1963 forms the basis of the Takaful Act 1984.

The Takaful Act 1984 is divided into four parts:

Part I: This provides for the interpretation, classification and references to takafulbusiness. Takaful business is divided into two broad categories, general takaful and family takaful. Those who enter the plans are called takaful participants. Any employee retirement schemewhichpaysbenefitatretirement,deathor disability shall not be treated as takaful business.

Part II: This provides the mode and conduct of takaful business such as restriction on the usage of the word ‘takaful’, conditions of registration, restrictions on takaful operators, the

33

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL

3.4. TAKAFUL AND INSURANCE

Insurance as a concept does not contradict the practices and requirements of Shariah. However, Muslim jurists generally view that conventional insurance, which is based on exchange transaction, does not conform to the rules and requirements of Shariah because of involvement in the following elements either in its buy-and-sell agreement, operations or investments:

1. Al-Gharar – uncertainty in the contract of insurance.

2. Al-Maisir – gambling as the consequence of the presence of uncertainty.

3. Al-Riba – the existence of interest or usury in its investment activities.

The takaful system, on the other hand, is based on mutual cooperation among members, where members contribute to a certain agreed fund for the purpose of sharing responsibility, assurance, protection and assistance between group members or takaful participants. It is a pact among a group of persons who agree to jointly indemnify the loss or damage that may inflict upon any of them, out of the collectedfund.

3.5. PRINCIPLES OF TAKAFUL OPERATION

Takaful operation incorporates the concept of takaful that applies the concept of tabarru’ and the principle of mudharabah.

3.5.1. The Concept Of Takaful

Takaful is a method of joint guarantee among a group of people in a scheme to share the burden of unexpected financial losses that

establishment and maintenance of takaful funds and allocation of surplus, the establishment and maintenance of a takaful guarantee scheme fund, requirements relating to takaful, and other miscellaneous requirements on the conduct of takaful business.

Part Ill:Thispartspecifies thepowersvestedin Bank Negara and the appointment of the Governor as the Director General of Takaful in regulating takaful business, the powers of investigation of Bank Negara and provisions for the winding-up and transfer of business of a takaful operator.

Part IV: This provides for the administration and enforcement of matters such as indemnity, submission of annual reports and statistical returns, offences and prosecution of offences.

3.3. THE SHARIAH SUPERVISORY COUNCIL

One of the important features of the Takaful Act 1984 and which is not provided in conventional insurance is a provision in the Articles of Association of takaful operators for the establishment of a Shariah Supervisory Council or Shariah Supervisory Board.

The function of the Council is to advise the takaful company on its operations in order to ensure that it is not involved in any element which is not approved by Shariah. Members of the Council are Muslim jurists who are well versed in Shariah matters.

The Council is not directly involved in the management of the takaful company but only decides whether the company’s activities comply with Shariah. The auditor of the company must ensure the decisions of the Council are followed. Decisions of the Council must always be according to ruling by shura or mutual consultation and agreement, and not be based on decision by majority.

34

CHAPTER 3 - THE BASIC PRINCIPLES OF INSURANCE AND AN INTRODUCTION TO TAKAFUL