pakistan microfinance review...

TRANSCRIPT

PAKISTANMICROFINANCE REVIEW 2014

ANNUAL ASSESSMENT OF THE MICROFINANCE INDUSTRY

F I N A N C I A L S E R V I C E S F O R A L L

Produced by Pakistan Microfinance NetworkDesign and Layout by O3 Interfaceswww.o3interfaces.com

Pakistan Microfinance Review 2014Annual Assessmentof the Microfinance Industry

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

i

Editorial Board

Mr. Ghalib NishtarChairperson Editorial BoardPresident, Khushhali Bank Limited (KBL)

Dr. Saeed AhmedDirector, Agriculture Credit and Microfinance Department,State Bank of Pakistan (SBP)

Mr. Blain StephensCOO and Director of Analysis Microfinance Information eXchange, Inc. (MIX)

Mr. Raza KhanStatistics & Results Adviser, Results & Evaluation Team- Economic Growth Group,Department for International Development (UK)

Mr. Yasir AshfaqGroup Head, Financial Services Group, Pakistan Poverty Alleviation Fund (PPAF)

Mr. Abrar MirSEVP & Group Executive Banking Products Group,United Bank Limited (UBL)

Mr. Masood Safdar GillDirector Program, Urban Poverty Alleviation Program, National Rural Support Programme (NRSP)

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

ii

PMR Team

Mr. Ali BasharatAuthor and Managing Editor

Mr. Ammar ArshadCo–Author and Data Collection

Ms. Khadija AliCo–Author and Data Collection

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

iii

Acronyms and Abbreviations

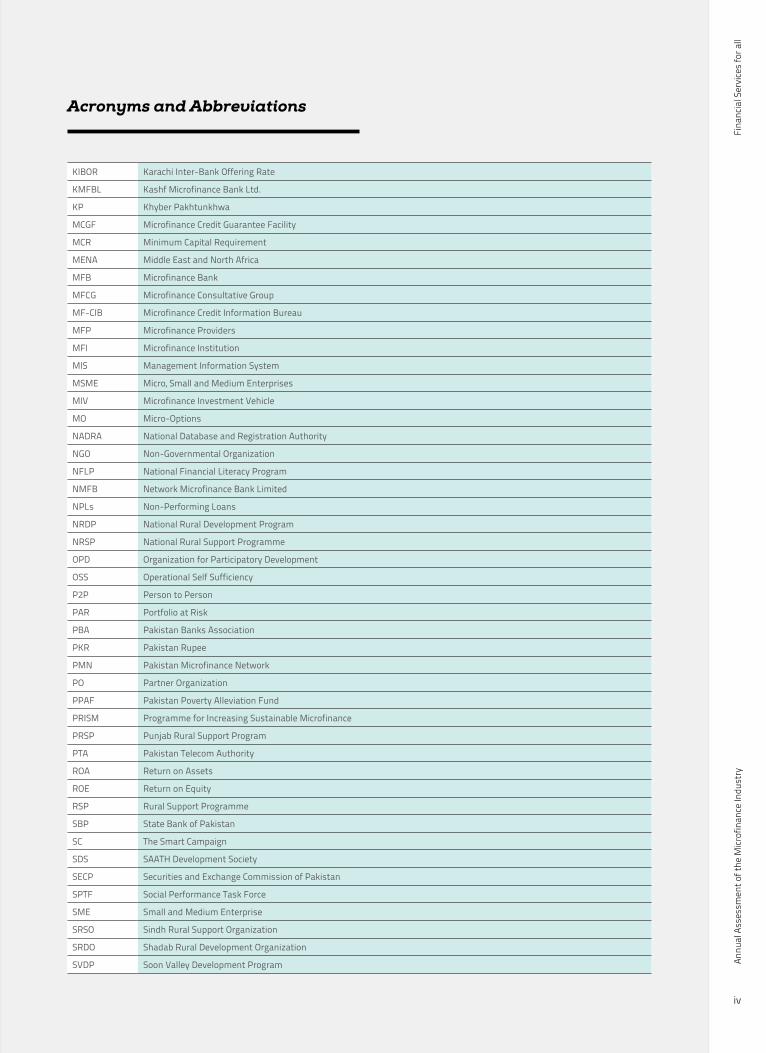

AC &MFD Agriculture and Microfinance Division

ADB Asian Development Bank

AMRDO Al-Mehran Rural Development Organization

AML Anti-Money Laundering

BPS Basis Points

CAR Capital Adequacy Ratio

CIB Credit Information Bureau

CDD Customer Due Diligence

CGAP Consultative Group to Assist the Poor

CNIC Computerized National Identity Card

CPP Client Protection Principles

CPI Consumer Price Index

CPC Consumer Protection Code

DFI Development Financial Institution

DFID Department for International Development, UK

DPF Depositor’s Protection Fund

ECA Eastern and Central Europe

ESM Environment and Social Management

EUR Euro

FATF Financial Action Task Force

FIP Financial Inclusion Program

FMFB The First Microfinance Bank Ltd.

FSS Financial Self Sufficiency

FY Financial Year

G2P Government to Person

GBP Great Britain Pound

GDP Gross Domestic Product

GLP Gross Loan Portfolio

GNI Gross National Income

GoP Government of Pakistan

IAFSF Improving Access to Financial Services Support Fund

IFAD International Fund for Agricultural Development

IFC International Finance Corporation

JIWS Jinnah Welfare Society

KBL Khushhali Bank Ltd.

KF Kashf Foundation

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

iv

Acronyms and Abbreviations

KIBOR Karachi Inter-Bank Offering Rate

KMFBL Kashf Microfinance Bank Ltd.

KP Khyber Pakhtunkhwa

MCGF Microfinance Credit Guarantee Facility

MCR Minimum Capital Requirement

MENA Middle East and North Africa

MFB Microfinance Bank

MFCG Microfinance Consultative Group

MF-CIB Microfinance Credit Information Bureau

MFP Microfinance Providers

MFI Microfinance Institution

MIS Management Information System

MSME Micro, Small and Medium Enterprises

MIV Microfinance Investment Vehicle

MO Micro-Options

NADRA National Database and Registration Authority

NGO Non-Governmental Organization

NFLP National Financial Literacy Program

NMFB Network Microfinance Bank Limited

NPLs Non-Performing Loans

NRDP National Rural Development Program

NRSP National Rural Support Programme

OPD Organization for Participatory Development

OSS Operational Self Sufficiency

P2P Person to Person

PAR Portfolio at Risk

PBA Pakistan Banks Association

PKR Pakistan Rupee

PMN Pakistan Microfinance Network

PO Partner Organization

PPAF Pakistan Poverty Alleviation Fund

PRISM Programme for Increasing Sustainable Microfinance

PRSP Punjab Rural Support Program

PTA Pakistan Telecom Authority

ROA Return on Assets

ROE Return on Equity

RSP Rural Support Programme

SBP State Bank of Pakistan

SC The Smart Campaign

SDS SAATH Development Society

SECP Securities and Exchange Commission of Pakistan

SPTF Social Performance Task Force

SME Small and Medium Enterprise

SRSO Sindh Rural Support Organization

SRDO Shadab Rural Development Organization

SVDP Soon Valley Development Program

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

v

TMFB Tameer Microfinance Bank Ltd

UBL United Bank Limited

USD United State Dollar

USSPM Universal Standards for Social Performance Management

VDO Village Development Organization

WPI Wholesale Price Index

Did you know?

Pakistan Microfinance Industry has a dedicated and robust Credit

Information Bureau (MF-CIB)

PMN VISION

Frontiers of Formal Financial Services reach out to all

MISSION

Support the financial sector, especially retail financial service providers, to

enhance their scale, quality, diversity and sustainability in order to achieve

inclusive financial services

Pakistan is ranked among the top 10 countries to have an enabling

environment for financial inclusion by the Economist Intelligence Unit’s

Global Microscope report

Did you know?

Pakistan has been called the Laboratory of Innovation in

Branchless Banking by CGAP

Pakistan Microfinance industry now has assets over PKR 100 billion

Core Values

CollaborationInnovationDiversity

EmpowermentTransparency

Did you know?

Pakistan Microfinance Industry has a dedicated and robust Credit

Information Bureau (MF-CIB)

PMN VISION

Frontiers of Formal Financial Services reach out to all

MISSION

Support the financial sector, especially retail financial service providers, to

enhance their scale, quality, diversity and sustainability in order to achieve

inclusive financial services

Pakistan is ranked among the top 10 countries to have an enabling

environment for financial inclusion by the Economist Intelligence Unit’s

Global Microscope report

Confidenceof Regulator

Availability ofFunds for

Mid-Sized MFPs

Mitigate ExternalInterference

RetailsDeposits

InvestorConfidence

TurnaroundTime

MainstreamingNon-Bank MFPs

Access toClearing House

Microfinance CreditGuarantee Facility

Draft NBMFIRegulations

2010 2011 2012 2013 2014

Numberof ActiveBorrowers

6 MonthsKIBORDiscountRateConsumerPriceInflation(Avergae)06

08

10

12

14

16

1.5

02

2.5

03

3.5

MACRO-ECONOMY

Perc

enta

ge

Activ

e bo

rrow

ers

in m

illio

ns

2.05 Yr 2010

2.07 Yr 2011

2.35 Yr 2012

2.83Yr 2013

3.14Yr 2014

4.20Yr 2015 5.04

Yr 2016

6.30 Yr 2017

7.87 Yr 2018

9.84 Yr 2019

Historical and Projected Growth of

Active BorrowersAmount in Millions

Increase inGrowth

3xprojected growth

0.6Billions of GLP

2014USD

3 MILLIONactive borrowers>

Policy & RegulatoryAchievements

Confidenceof Regulator

Availability ofFunds for

Mid-Sized MFPs

Mitigate ExternalInterference

RetailsDeposits

InvestorConfidence

TurnaroundTime

MainstreamingNon-Bank MFPs

Access toClearing House

Microfinance CreditGuarantee Facility

Draft NBMFIRegulations

2010 2011 2012 2013 2014

Numberof ActiveBorrowers

6 MonthsKIBORDiscountRateConsumerPriceInflation(Avergae)06

08

10

12

14

16

1.5

02

2.5

03

3.5

MACRO-ECONOMY

Perc

enta

ge

Activ

e bo

rrow

ers

in m

illio

ns

2.05 Yr 2010

2.07 Yr 2011

2.35 Yr 2012

2.83Yr 2013

3.14Yr 2014

4.20Yr 2015 5.04

Yr 2016

6.30 Yr 2017

7.87 Yr 2018

9.84 Yr 2019

Historical and Projected Growth of

Active BorrowersAmount in Millions

Increase inGrowth

3xprojected growth

0.6Billions of GLP

2014USD

3 MILLIONactive borrowers>

Policy & RegulatoryAchievements

20102011201220132014

0 10 20 30 40 50 60

ACTIVE BORROWERS BY URBAN/RURAL AREAS

58%female borrowers 42%

male borrowers

5.3Million Depositors

in 2014

Regulatoryframework for NBMFIs

Funding

Center ofExcellence

0%

20%

40%

60%

80%

100%

AppropriateProduct Design & Delivery

Channels

TransparencyPrivacy of Client Data

Prevention ofOver-Indebtedness

Mechanism forComplaint Resolution

Responsible PricingFair & RespectfulTreatment of Clients

% of indicators that are not met

% of indicators that are partially met

% of indicators that are fully met

DisasterRisk Management

Equity

Debt

Deposits

0

20

40

60

80

100

44%

23%

33%

CAPITALSTRUCTURE

Rural

Urban

CLIENTPROTECTION

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

xi

Highlights

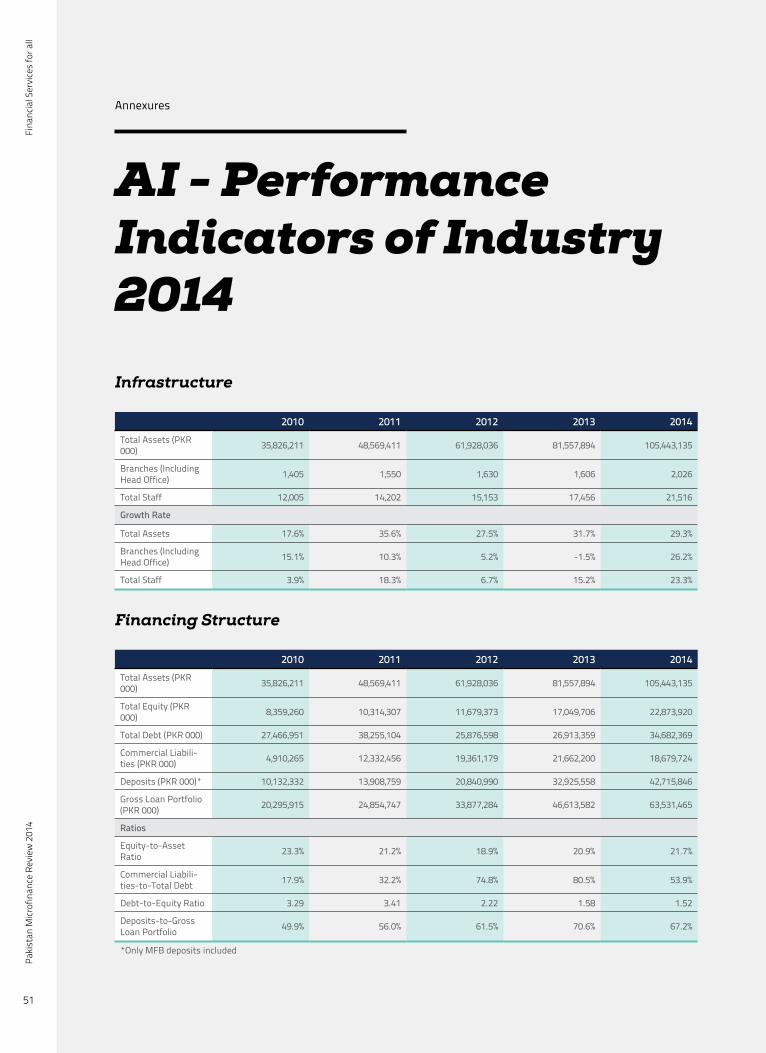

Year 2010 2011 2012 2013 2014Active Borrowers (in millions) 1.6 1.7 2. 0 2.4 2.8

Gross Loan Portfolio(PKR billions) PKR 20.2 PKR 24.8 PKR 33.1 PKR 46.6 PKR 61.072

Active Women Borrowers(in millions)

0.8 0.9 1.3 1.4 1.6

Branches1,405 1,550 1,460 1,606 1,747

Total Staff12,005 14,202 14,648 17,456 19,881

Total Assets (PKR billions) 35.8 48.6 61.9 81.5 100.7

Deposits (PKR billions) 10.1 13.9 20.8 32.9 42.72

Total Debt (PKR billions) 27.5 38.3 24.9 26.9 31.1

Total Revenue(PKR billions) 7.5 10.1 12.5 17.3 24.3

OSS (percentage)99.7 108.4 109.5 118.1 120.6

FSS (percentage)81.7 100.5 107.5 116.5 119.6

PAR > 30 (percent-age) 4.1 3.2 3.7 2.5 1.1

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

xii

Contents

THE YEAR IN REVIEW

THE WAY FORWARD

INDUSTRY PERFORMANCE

ANNEXURES

01

40

10

50Macro-economy and Microfinance Industry 01Policy and Regulatory Environment 02Microfinance Industry Initiatives 04Conclusion 07

Inclusive Finance and Microfinance Industry 41Towards Accelerated Growth 42Adapting Government Credit Schemes 42Impact Investment 43Diversifying Funding Sources 43Capacity Building Program 44Micro, Small & Medium Enterprise (MSME) Lending

45

Anti-Money Laundering (AML), Customer Due Diligence (CDD) and Terrorist Financing

46

Agriculture Value Chains 46

Section 2A: Industry Performance 11Section 2B: Social Performance 27

Performance indicators of industry 51Performance indicators of individual MFPs 59Social Performance Indicators of Individual MFPs

103

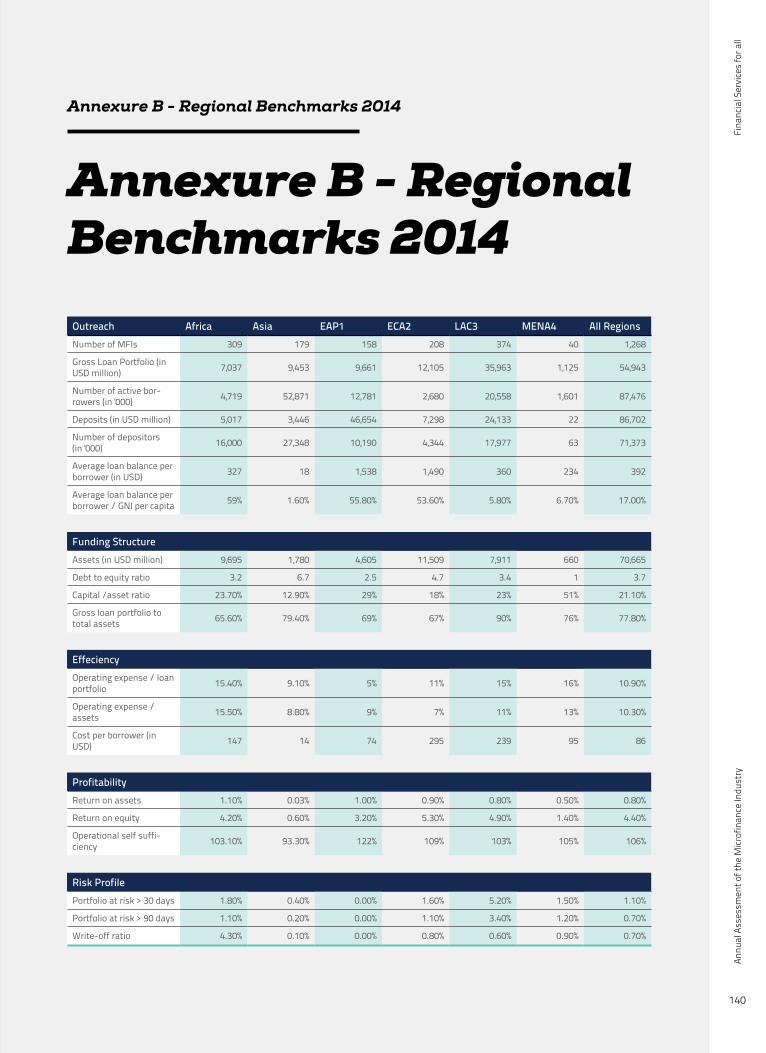

Regional Benchmarks 140Sources of Data 141Adjustment to Financial Data 152Terms and Definitions 155

Section 1

The Year in Review

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

1

Section 1

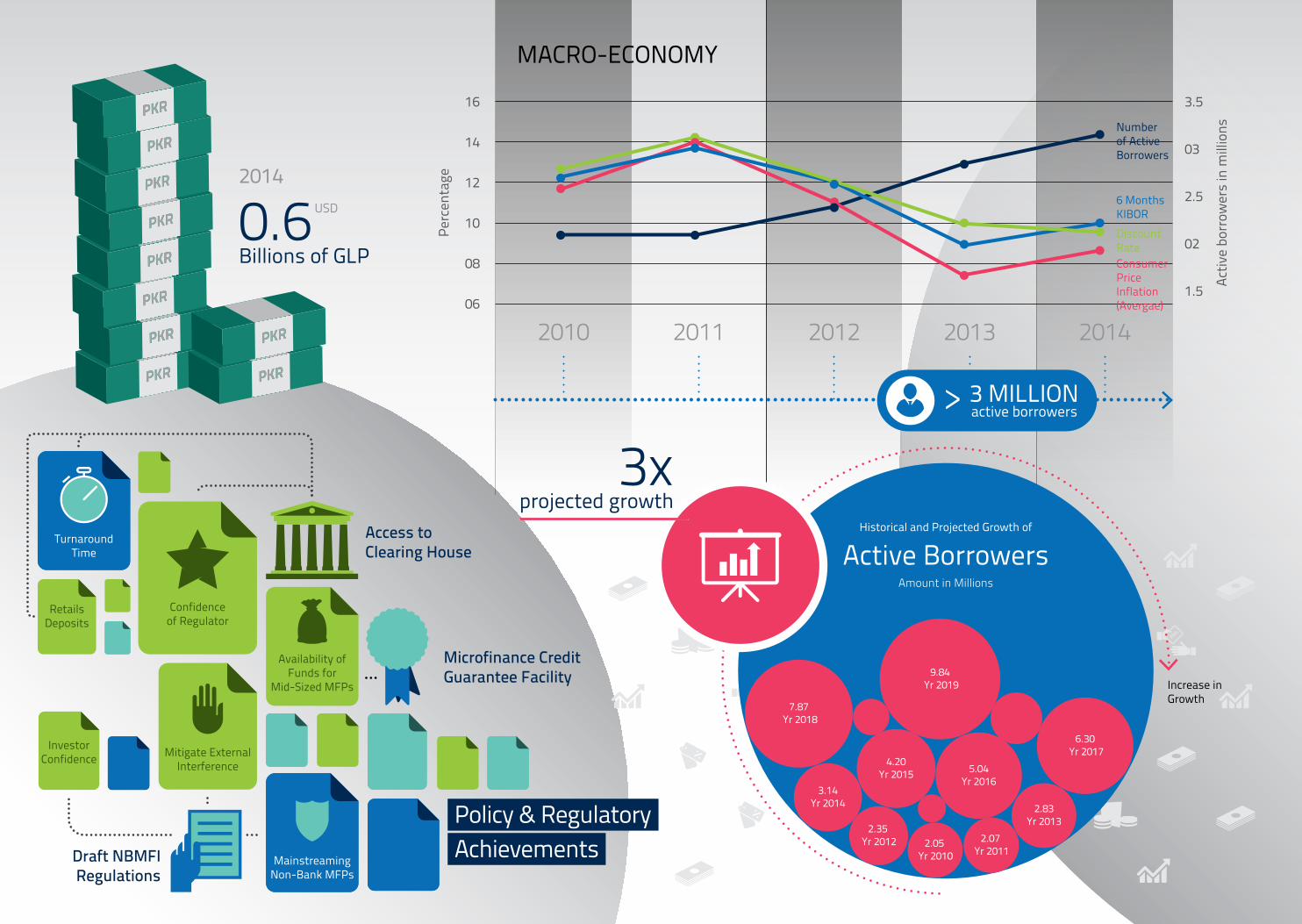

The year 2014 saw the industry achieve a major mile-stone by crossing the 3 million active borrowers mark for the first time. Overall, the industry witnessed double digit growth in not only credit but also in sav-ings and insurance.

Although the national economy grew at a modest rate, the macroeconomic stability ensured a favor-able environment for the players. Despite the per-sistent energy crisis and security challenges, posi-tive economic indicators like lower inflation, falling interest rates and uptake on private credit led to a positive impact on the sector in terms of growth and sustainability.

On the policy and regulatory side, the microfinance banks (MFBs) have been allowed to become mem-bers of the national clearing house which will greatly enhance their ability to mobilize their retail depos-its. In addition, to facilitate mid-tier players to raise funds from commercial sources, risk coverage under the Microfinance Credit Guarantee Fund (MCGF) was

enhanced to 60 percent by the State Bank of Pakistan (SBP). One of key challenge facing the industry has been the lack of a regulatory umbrella for the non-bank microfinance providers (MFPs). In this regard, the last year saw the Securities and Exchange Com-mission of Pakistan (SECP) sharing a draft of pro-posed regulations with players for comments.

Among other major developments in the sector last year an industry risk register is being developed by the Pakistan Microfinance Network (PMN). In addi-tion, branchless banking continues to witness growth and the Microfinance Credit Information Bureau (MF-CIB) is fully operational with most of the MFPs gen-erating enquiries. The PM Interest Free Loan Scheme announced in 2013 was formally launched last year through the Pakistan Poverty Alleviation Fund (PPAF), with an aim of reaching out to 1 million clients in the next three years. As part of the responsible fi-nance initiative, client protection assessments were carried out under the SMART campaign.

The year 2014 was a better year for Pakistan’s econ-omy as it witnessed lower than expected inflation, reduction in fiscal deficit and improvement in private sector credit. In addition, the overall economy grew by 4.1 percent compared to the 3.7 percent in 2013. However, this was less than the target of 4.4 percent for the year 2014.

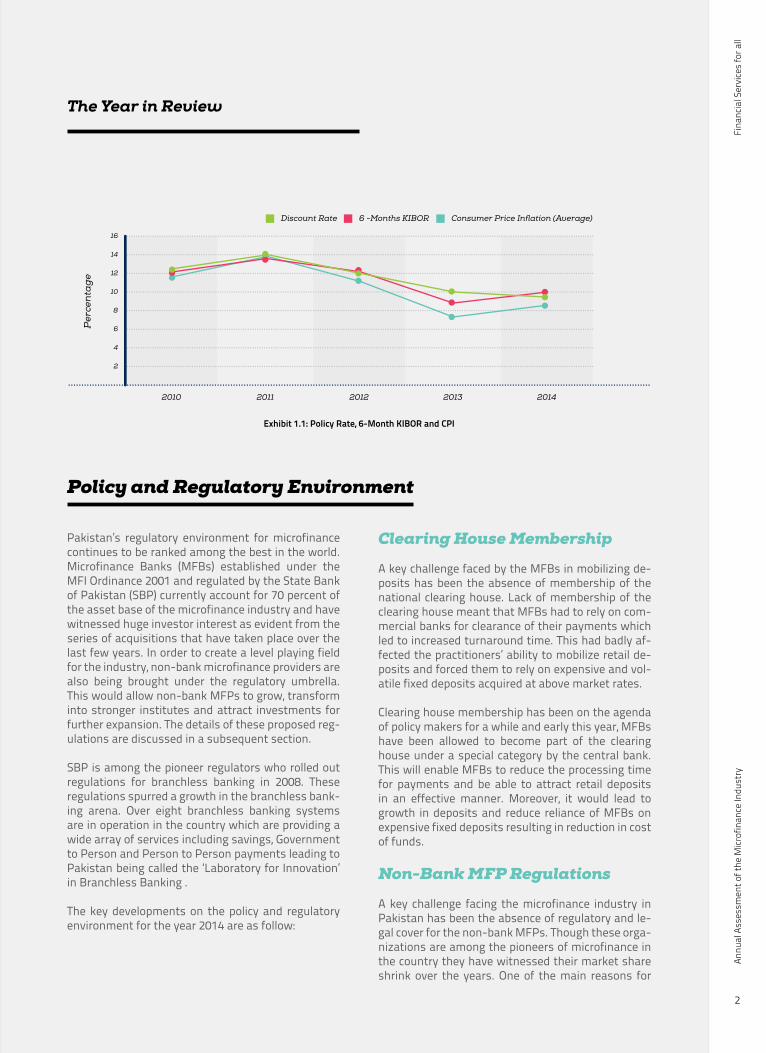

Inflation for the year clocked at 8.6 percent - high-er than the previous year’s 7.4%, but lower than the expected rate of 11-12 percent. However, despite the lower inflation, the central bank took a cautious approach to monetary policy with the policy rate re-maining constant for the better part of the year.

The end of the year saw the policy rate cut by 50 bps taking it from 10 percent to 9.5 percent as shown in Exhibit 1.1. This trend which continued in early 2015, would likely result in the lowering of borrowing costs of Microfinance Providers (MFPs).

Another positive for the year was the uptake in pri-vate sector credit growth which registered a double digit growth of 11.4 percent. This increase which was the highest in the last six years came on the back of an increased supply of loanable funds, improvement in business confidence and lower effective cost of borrowing. This augurs well for MFPs which are wit-nessing increased dependence upon commercial bor-rowing to meet their funding needs.

Macro-economy and the Microfinance Industry

The Year in Review

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

2

The Year in Review

Pakistan’s regulatory environment for microfinance continues to be ranked among the best in the world. Microfinance Banks (MFBs) established under the MFI Ordinance 2001 and regulated by the State Bank of Pakistan (SBP) currently account for 70 percent of the asset base of the microfinance industry and have witnessed huge investor interest as evident from the series of acquisitions that have taken place over the last few years. In order to create a level playing field for the industry, non-bank microfinance providers are also being brought under the regulatory umbrella. This would allow non-bank MFPs to grow, transform into stronger institutes and attract investments for further expansion. The details of these proposed reg-ulations are discussed in a subsequent section.

SBP is among the pioneer regulators who rolled out regulations for branchless banking in 2008. These regulations spurred a growth in the branchless bank-ing arena. Over eight branchless banking systems are in operation in the country which are providing a wide array of services including savings, Government to Person and Person to Person payments leading to Pakistan being called the ‘Laboratory for Innovation’ in Branchless Banking .

The key developments on the policy and regulatory environment for the year 2014 are as follow:

Clearing House Membership

A key challenge faced by the MFBs in mobilizing de-posits has been the absence of membership of the national clearing house. Lack of membership of the clearing house meant that MFBs had to rely on com-mercial banks for clearance of their payments which led to increased turnaround time. This had badly af-fected the practitioners’ ability to mobilize retail de-posits and forced them to rely on expensive and vol-atile fixed deposits acquired at above market rates.

Clearing house membership has been on the agenda of policy makers for a while and early this year, MFBs have been allowed to become part of the clearing house under a special category by the central bank. This will enable MFBs to reduce the processing time for payments and be able to attract retail deposits in an effective manner. Moreover, it would lead to growth in deposits and reduce reliance of MFBs on expensive fixed deposits resulting in reduction in cost of funds.

Non-Bank MFP Regulations

A key challenge facing the microfinance industry in Pakistan has been the absence of regulatory and le-gal cover for the non-bank MFPs. Though these orga-nizations are among the pioneers of microfinance in the country they have witnessed their market share shrink over the years. One of the main reasons for

Policy and Regulatory Environment

2

4

6

8

10

12

14

16

2010 2011 2012 2013 2014

Consumer Price Inflation (Average)6 -Months KIBORDiscount Rate

Per

cen

tag

e

Exhibit 1.1: Policy Rate, 6-Month KIBOR and CPI

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

3

Section 1

this has been lack of regulatory umbrella. Due to this non-bank MFPs have found it difficult to attract commercial financing. Moreover, this has resulted in a lack of recourse mechanism for clients and practi-tioners and the non-bank MFPs have remained vul-nerable to the risk of external interference.

Keeping in view the above, a steering committee was formed in 2012 chaired by Chairman Securities and Exchange Commission of Pakistan (SECP) that in-cluded all key stakeholders of the industry like SBP, Pakistan Poverty Alleviation Fund (PPAF), PMN and key MFPs to extend legal and regulatory cover for the non-bank MFPs. Last year a draft of proposed regu-lations were shared with the players for their feed-back. A summary of the main points raised by the players and PMN is as follows:

• It is hoped that SECP shall play a stewardship role post-regulations similar to that of SBP in case of MFBs.

• A liberal interest rate regime for non-bank MFPs should be followed that focuses on market in-struments of competition and full disclosures as followed by SBP.

• The current and proposed Non-Bank Financial Companies (NBFC) laws do not adequately ca-ter to the microfinance sector as they do not provide for micro-financing as a distinct form of business carried out by NBFCs. Certain con-ditions and requirements of the NBFC Laws are not realistic when taken in the context of the working microfinance industry in Pakistan; thus, there is a need for microfinance to be treated as a distinct class of NBFCs and specific regulations applicable upon them are required.

• With the exception of one non-bank MFP, all others are not for profit entities and many of them would like to continue as non-profit under the proposed regulatory framework. Therefore the proposed regulatory framework, in addition to designating NBMFIs as a specific class of NBFCs, should allow for the creation of a further distinction in the NBFC Laws between “for prof-it” non-bank MFP and “not for profit” non-bank MFPs.

• Since the proposed regulations cater for the es-tablishment of a consultative group with repre-sentatives of the sector to review the regulations and restrictions, limits, requirements, criterion, etc. it has been proposed that the consultative group meet with SECP every six months to bring the regulator and the industry on the same page

and to revise the regulations as the industry evolves.

It is hoped that regulations will come into effect by the end of 2015 with adequate time being provided for non-bank MFPs to conform to their requirements. These regulations will play a role of catalyst for this segment of the microfinance industry to attract both debt and equity capital from the private sector and be recognized as a mainstream part of the financial landscape in Pakistan.

Amendments in Microfinance Credit Guarantee Facility (MCGF)

MCGF was launched in 2009 under the auspices of the Financial Inclusion Program (FIP) with the aim of boosting commercial funding to the industry by of-fering partial risk coverage to lenders. In order for the sector to become sustainable and grow into a viable part of the financial industry, commercial funding is undeniably important. Initially MFBs and later, MFIs and RSPs were allowed to utilize the facility to ob-tain loans from commercial banks and also issue re-deemable capital. However, the uptake of the facility among small and mid-sized MFBs was low as many had riskier profiles compared to their larger, more es-tablished peers.

SBP recently revised guidelines regarding the MCGF in order to facilitate and promote lending from com-mercial financial institutions for small to mid-sized MFPs. In this regard, a tiering criterion has been de-veloped and the risk coverage for the lender has been enhanced.

Initially under the MCGF, 25 percent first loss guar-antee or 40 percent partial guarantee was provided in case of bilateral loans or redeemable capital to the lenders. However, now in the case of bilateral loans to Tier 2 MFPs, 60 percent partial guarantee is now being provided. Tier 2 MFPs are defined as those en-tities that have been in business for 3 years instead of 5 years which is a criterion for Tier 1 MFPs and have a GLP above PKR 500 million as compared to PKR 3 billion for Tier 1. Among other conditions, the Tier 2 MFP needs to have an improving trend in its return on assets (ROA) for the past three years and for last year the ROA needs to be greater than -10 percent. In addition, the Portfolio at Risk (PAR) > 30 days also needs to below 10 percent.

These amendments will likely lead to enhancement in lending to small and mid-sized MFPs which are largely reliant on funding from the national apex and

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

4

The Year in Review

have yet to initiate commercial borrowing relation-ships. This would allow them to not only enhance but also diversify their funding sources leading to in-

crease in outreach and upscaling of loan sizes.

Risk Register

Risk taking is an inherent element of financial ser-vices, and like all financial institutions, microfinance providers (MFPs) face risks that they must manage effectively to achieve their financial and social objec-tives. Poorly managed risks can lead to losses en-dangering the safety and soundness of microfinance institutions. Hence, it is imperative for microfinance providers to have a formal risk management struc-ture in place to counter potential threats.

As part of PMN’s long term strategy to achieve sus-tainable growth in the Pakistan microfinance sector, the Network is taking constructive steps to promote sound risk management practices among microfi-nance practitioners. One initiative PMN has under-way is the development of a comprehensive risk reg-ister for the microfinance sector in Pakistan.

A risk register is a tool widely used by organizations for the identification and assessment of risks. The tool is considered a vital component of the risk man-agement process which serves as a central source for the organization’s risk information and acts as a risk directory. The tool is used by organizations to list var-ious risks, highlighting their probability and severity of impact, along with possible risk mitigation steps and strategies.

PMN is of the opinion that such a tool will enable MFPs (especially those with no existing risk manage-ment structures in place) to understand the nature of risks faced by the institutes at the departmen-tal and strategic level. The risk register will provide management and key stakeholders with significant information on various threats, which can be utilized to design risk management strategies to mitigate potential threats.

Prime Minister Interest Free Loan Scheme

The Government of Pakistan (GoP) launched an inter-est-free microloan scheme last year to address the issues of poverty and rising unemployment in the

country. Under the scheme, PKR 3.5 billion were ear-marked for the poor and destitute segments of the population. Initially, the industry stakeholders were apprehensive about the scheme as it could have distorted the market for conventional microfinance. However, in order to safeguard the interest of the MFPs it was decided that the funds for the scheme would be routed through the national apex, PPAF and loans will be extended to those individual who fall be-low 40 on the poverty scorecard. In order to mitigate the overlap between interest free loans and conven-tional microloans, the loans under this scheme would only be extended in Union Councils that have low or no penetration of conventional microfinance.

Currently, 24 MFPs have partnered with PPAF in ex-tending interest free loans under this scheme. It is hoped that the scheme would lead to over 1 million additional active borrowers over the next three years. Since this scheme is targeted toward those areas where conventional microfinance has little or no pen-etration, it provides MFPs an opportunity to expand outreach in newer geographic markets. Moreover, it has the potential to allow for borrowers of interest free loans to graduate to conventional microfinance. This is ensured as the interest free loan would be provided only once to an individual and after the completion of the first cycle he/she would be eligible only for a conventional microfinance loan. Lastly in an industry that views funding as one of the key con-straints to growth, it is felt that despite the skepti-cism, this scheme can be useful for the industry with change in design and understanding that the interest free loan program can help in graduation of clients to the next level and mainstreaming them into the microfinance segment.

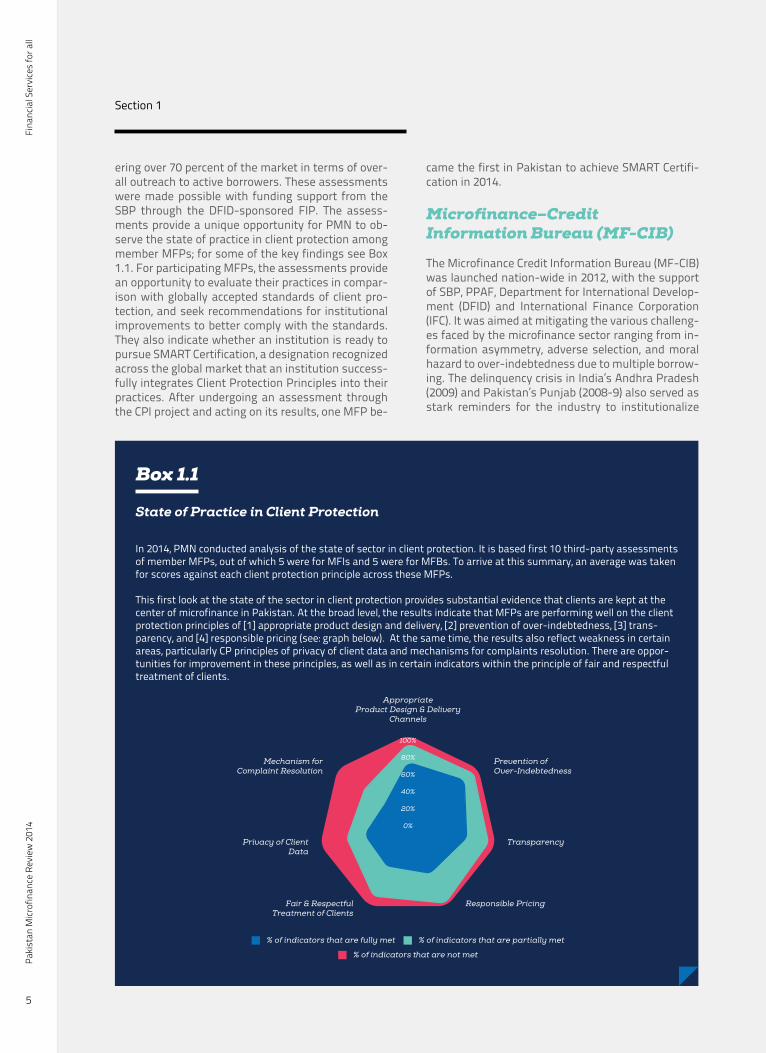

Client Protection Assessments in collaboration with the SMART Campaign

Third-party client protection assessments using the SMART Campaign’s Smart Assessment Tool were conducted for six MFPs during the year in review. In total, 18 assessments have been conducted since the inception of the Client Protection Initiative (CPI), cov-

Microfinance Industry Initiatives

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

5

Section 1

ering over 70 percent of the market in terms of over-all outreach to active borrowers. These assessments were made possible with funding support from the SBP through the DFID-sponsored FIP. The assess-ments provide a unique opportunity for PMN to ob-serve the state of practice in client protection among member MFPs; for some of the key findings see Box 1.1. For participating MFPs, the assessments provide an opportunity to evaluate their practices in compar-ison with globally accepted standards of client pro-tection, and seek recommendations for institutional improvements to better comply with the standards. They also indicate whether an institution is ready to pursue SMART Certification, a designation recognized across the global market that an institution success-fully integrates Client Protection Principles into their practices. After undergoing an assessment through the CPI project and acting on its results, one MFP be-

came the first in Pakistan to achieve SMART Certifi-cation in 2014.

Microfinance–Credit Information Bureau (MF-CIB)

The Microfinance Credit Information Bureau (MF-CIB) was launched nation-wide in 2012, with the support of SBP, PPAF, Department for International Develop-ment (DFID) and International Finance Corporation (IFC). It was aimed at mitigating the various challeng-es faced by the microfinance sector ranging from in-formation asymmetry, adverse selection, and moral hazard to over-indebtedness due to multiple borrow-ing. The delinquency crisis in India’s Andhra Pradesh (2009) and Pakistan’s Punjab (2008-9) also served as stark reminders for the industry to institutionalize

Box 1.1

State of Practice in Client Protection

In 2014, PMN conducted analysis of the state of sector in client protection. It is based first 10 third-party assessments of member MFPs, out of which 5 were for MFIs and 5 were for MFBs. To arrive at this summary, an average was taken for scores against each client protection principle across these MFPs.

This first look at the state of the sector in client protection provides substantial evidence that clients are kept at the center of microfinance in Pakistan. At the broad level, the results indicate that MFPs are performing well on the client protection principles of [1] appropriate product design and delivery, [2] prevention of over-indebtedness, [3] trans-parency, and [4] responsible pricing (see: graph below). At the same time, the results also reflect weakness in certain areas, particularly CP principles of privacy of client data and mechanisms for complaints resolution. There are oppor-tunities for improvement in these principles, as well as in certain indicators within the principle of fair and respectful treatment of clients.

0%

20%

40%

60%

80%

100%

AppropriateProduct Design & Delivery

Channels

Prevention ofOver-Indebtedness

Mechanism forComplaint Resolution

TransparencyPrivacy of ClientData

Responsible PricingFair & RespectfulTreatment of Clients

% of indicators that are not met

% of indicators that are partially met% of indicators that are fully met

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

6

The Year in Review

the use of the Bureau as an integral part of the loan approval process in order to manage credit risk and assess credit worthiness.

Over the past three years, the MF-CIB has gradually matured into a reliable risk mitigation tool and has been gradually integrated into the ecosystem of the sector. The enquiry numbers in the year 2014, bar-ring a seasonal decline, showed an upward trend as shown in Exhibit 1.2.

Currently, 70% of the organizations are actively gen-erating enquiries (35 out of 50 members) and it is ex-pected that enquiry numbers would grow even more after the complete rollout as some MFPs are current-ly in a partial rollout state.

Attention is also being paid to improve the gover-nance structure of the Bureau and make it more inclusive and representative. The Credit Bureau Act, which is expected to be ratified by the Parliament this year, will also result in increased transparency from the service provider’s perspective. The pricing mech-anism is being scrutinized and PMN is working with the Bureau and MFPs to create a framework for de-termining prices in future.

PMN is also conducting a financial literacy program aimed at raising awareness amongst the clients vis-à-vis the Bureau’s importance and utilization. More-over, a grievance addressing mechanism delineating the rights and obligations of MFPs, Bureau and Cli-ents is also being worked out.

Branchless Banking

Branchless banking is an important tool available to the microfinance industry to expand outreach by le-veraging cellular technology infrastructure. Moreover,

it allows for provision of financial services at lower costs than the traditional banking structures making it an ideal channel for reaching out to the unbanked.

Branchless banking in Pakistan continued to expand in the year 2014 with over 60% increase in the value of transactions which reached PKR 375.9 billion as compared to PKR 234.6 billion in December, 2013. The number of transactions exhibited over 23% increase reaching to 66.8 million from 54.1 million in at the end of 2013. A 35.6% increase was also observed in

the number of m-wallet accounts which reached 4.7 million from 3.4 million in the same time period.

Pakistan’s branchless banking market is still in an evolutionary phase with eight players competing for market share of agents, number and value of transactions, etc. With the agent network currently standing at 186,000 agents exhibiting a 49% increase from 125,000 in the year, there are concerns about the quality of agents due to a widespread sharing phenomenon. At present, the market is focused on Over the Counter (OTC) transactions. This fuels a commission war to lure agents hence dictating the process of agent acquisition and a nominal addition of new access points which would be, in real terms, expansion of the agent network. A few players are, however, bringing innovation to build business cases around mobile wallets.

The SBP has continued to facilitate efforts for a broader vision financial inclusion through strength-ening the ecosystem for digital transaction accounts. The SBP signed an MOU with NADRA in November 2014 according to which, biometric verification cost has been brought down to PKR 10 for each m-wallet account opening at the industry level. The placement of biometric verification apparatus across all telecom operators’ offices enables account opening within a

Exhibit 1.2: Yearly trend in MF-CIB enquiries

20

40

60

80

110

120

140

160

Jan 14 Feb 14 Mar 14 Apr 14 May 14 Jun 14 Jul 14 Aug 14 Sep 14 Oct 14 Nov 14 Dec 14

En

qu

ries

in T

hou

san

ds

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

7

Section 1

few seconds via fingerprint verification, and coupled with PTA’s directive of mandatory biometric mobile SIM verification, this will result in the country’s mo-bile clientele ready to be inducted in the branchless banking arena. This has also proven to be a catalyst for the explosive growth of m-wallets since the be-ginning of 2015.

Branchless banking can serve as a growth driver ow-ing to its capacity to increase outreach by lowering delivery cost and aiding profitability of institutions.

Over 12 microfinance institutions are currently pro-viding disbursement and recovery services to their clients through digital channels. Some players have also started extending insurance services to their clients through branchless banking channels. The industry is poised to witness accelerated growth in future in volume and variety of financial services.

The microfinance industry in Pakistan having wit-nessed continuous growth over the last few years in not only credit but also savings, insurance and remit-tances, is ideally positioned to play an important role in the inclusive finance sphere. It can offer a wide va-riety of financial services to the unbanked particularly at the base of the pyramid.

The current macroeconomic stability in the coun-try provides an ideal environment for the sector to grow and expand. Falling interest rates on the back of lower inflation and uptake on private credit provides an opportunity for the microfinance sector to reduce costs and fund their expansion by borrowing from commercial sources.

With major policy and regulatory initiatives like clear-ing house membership for MFBs and enhanced risk coverage for lenders to mid-tier MFPs being taken,

players are better poised to address funding chal-lenges. Also, the launch of non-bank MFPs regula-tory framework will lead to strengthening of these institutes and provide them with an opportunity to expand.

Branchless banking continues to gain popularity and provides opportunities to not only expand outreach and reduce costs but also expand the variety of fi-nancial services on offer. MF-CIB is fully operation with enquiries being generated by MFPs and remains a key catalyst for future growth of the industry. In addition, significant steps towards ensuring respon-sible inclusive finance, by working towards global best practices in client protection have been taken. Establishment of an industry risk register will allow members to identify risks and take steps to mitigate their impact.

Conclusion

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

8

The Year in Review

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

9

Section 1

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

10

Industry Performance

Section 2

Industry Performance

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

11

Section 2

The section is divided into two parts. Section 2A covers the financial performance of the microfinance industry whereas Section 2B deals with the social performance of the industry.

Industry Performance

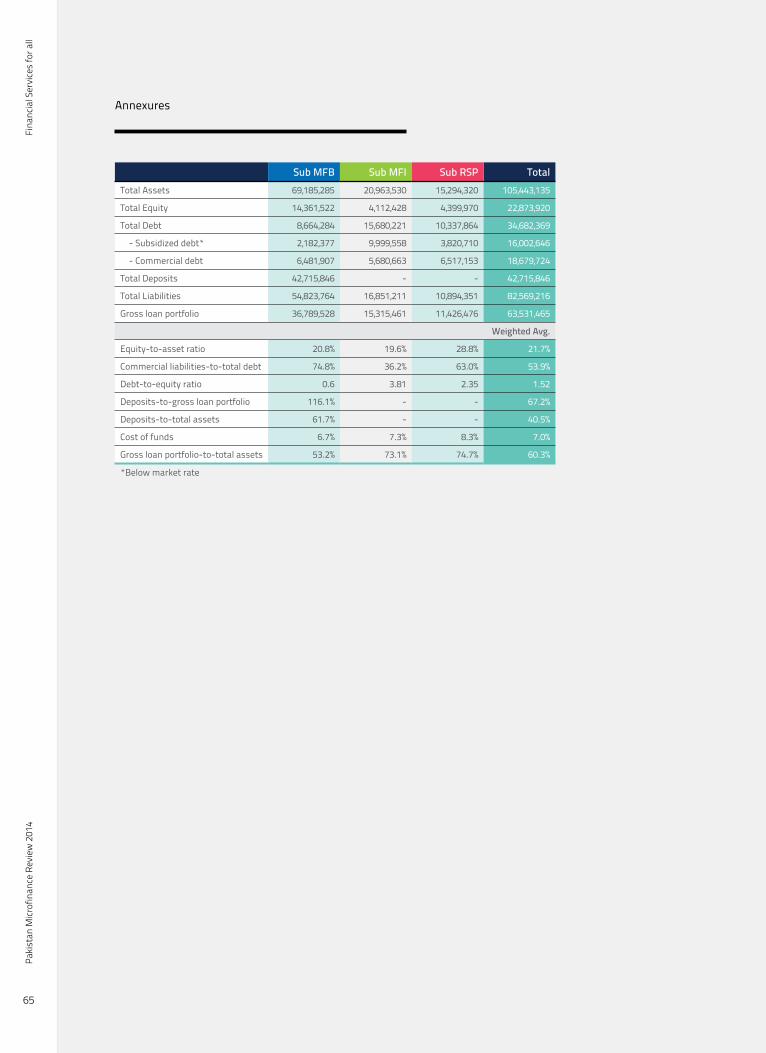

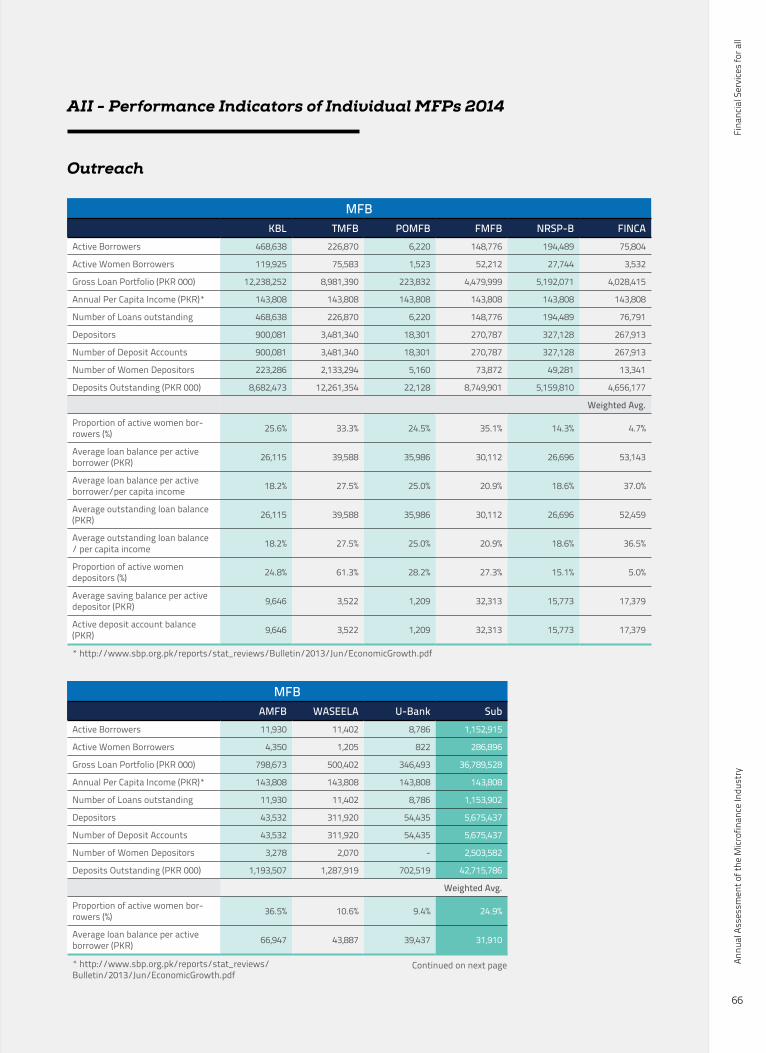

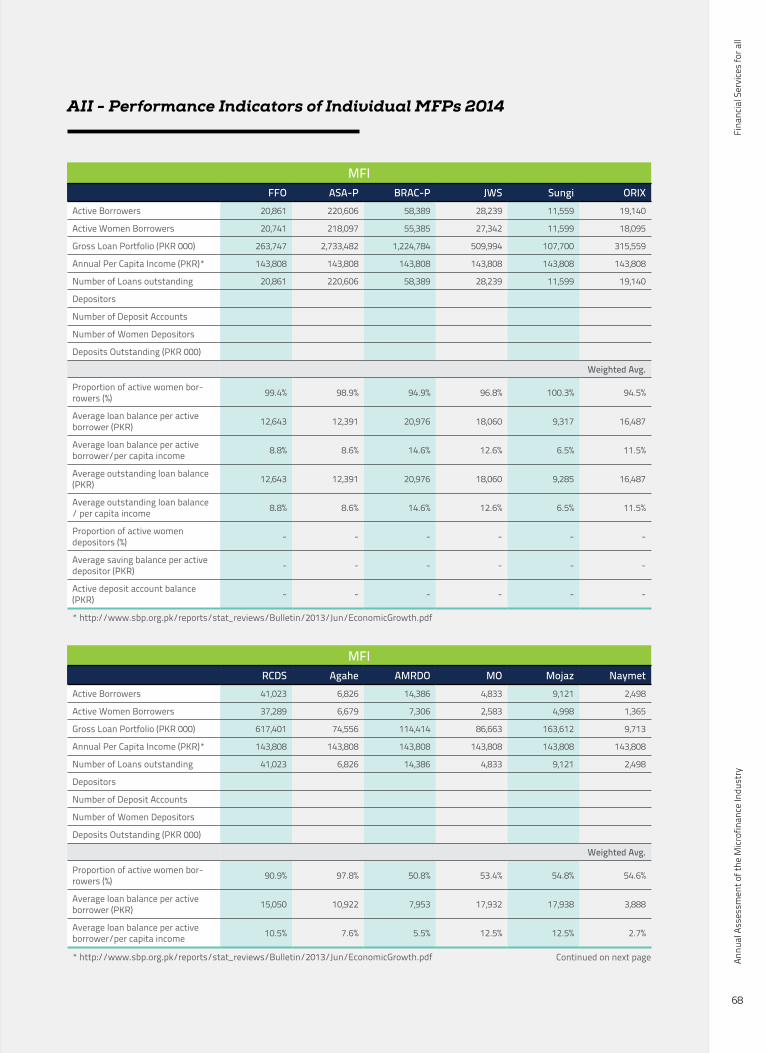

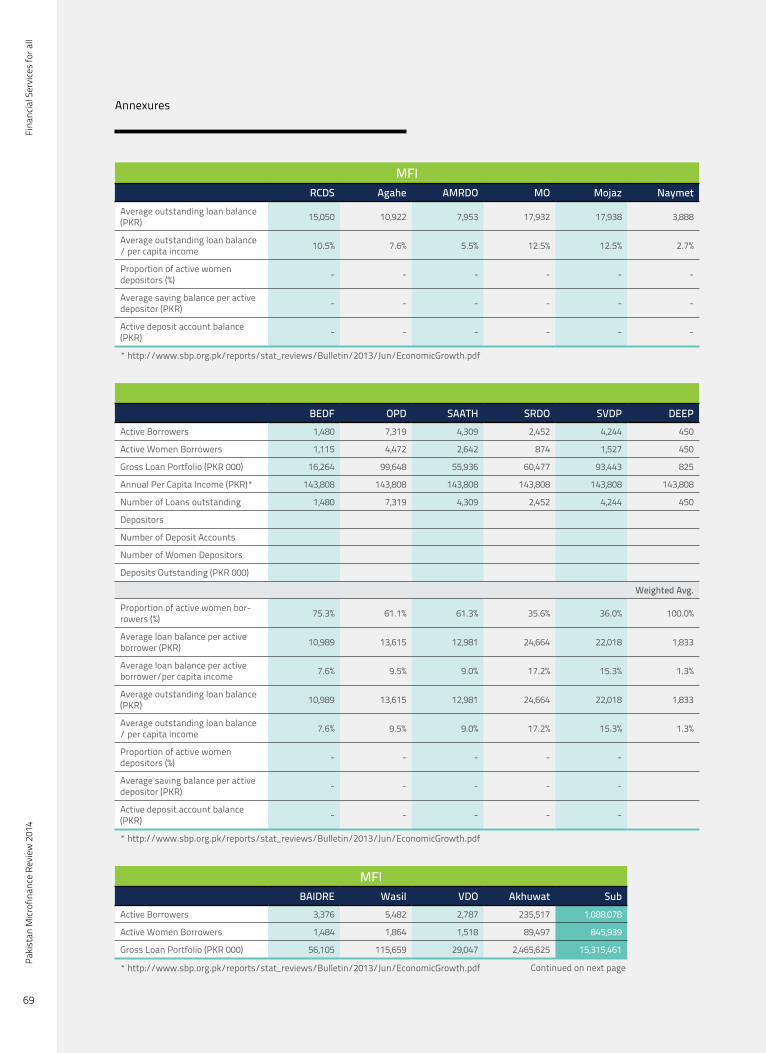

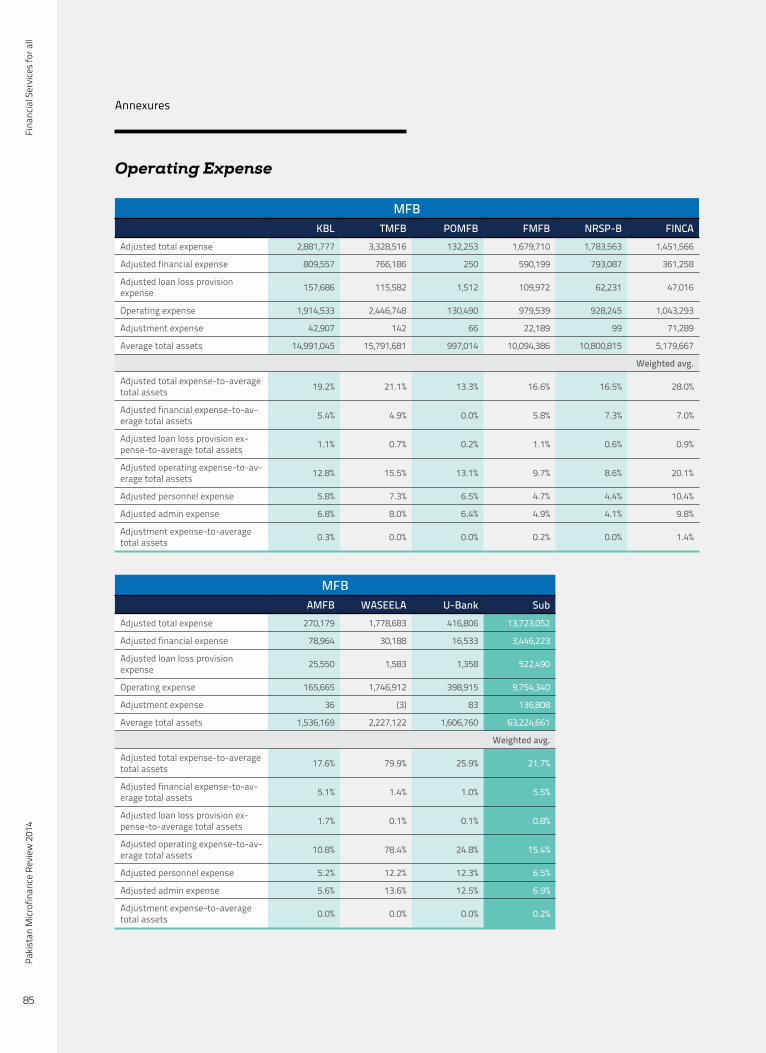

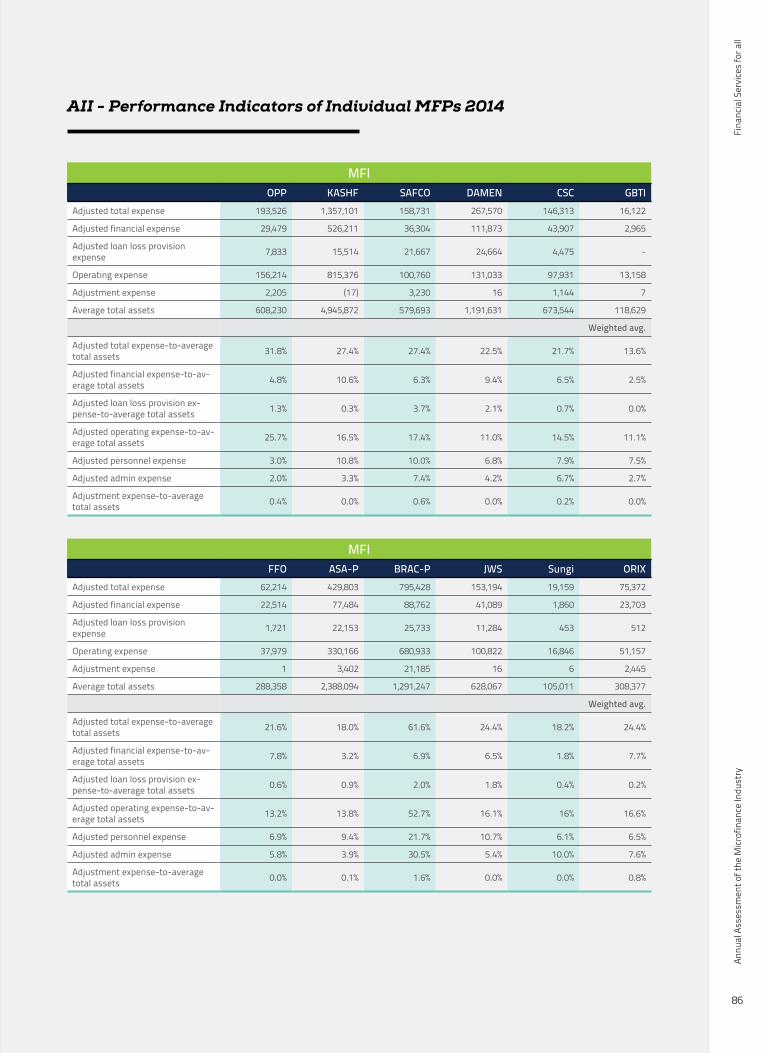

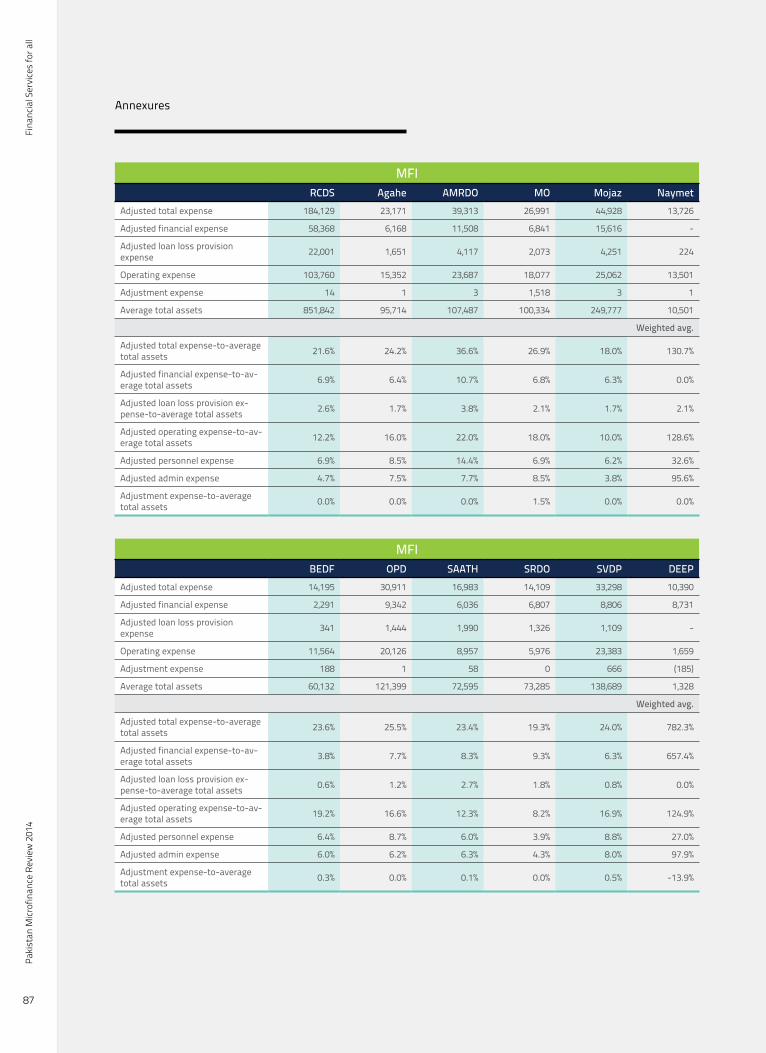

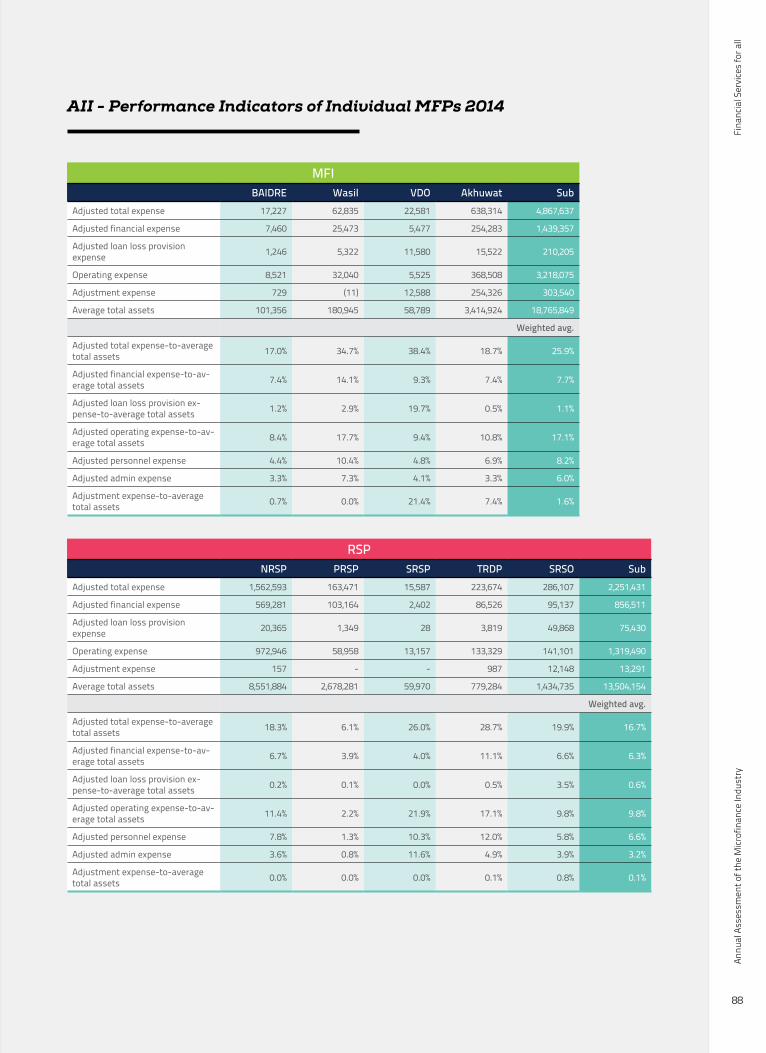

This section provides a detailed analysis of the fi-nancial performance of Pakistan’s microfinance in-dustry in 2014. Performance has been assessed on three levels: industry wise, across peer groups and institution wise. The analysis is backed by 88 finan-cial indicators, calculated from the audited financial statements of the reporting organizations. These indicators have been compared across time and re-gions to develop a reliable and fair assessment of sector.

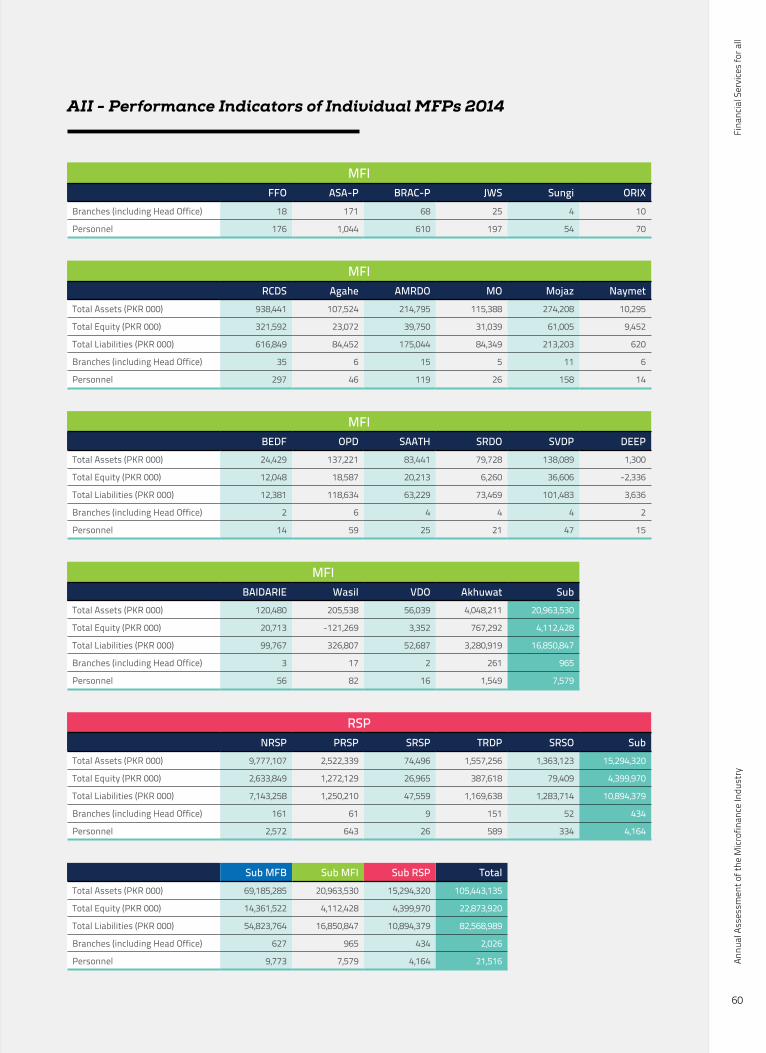

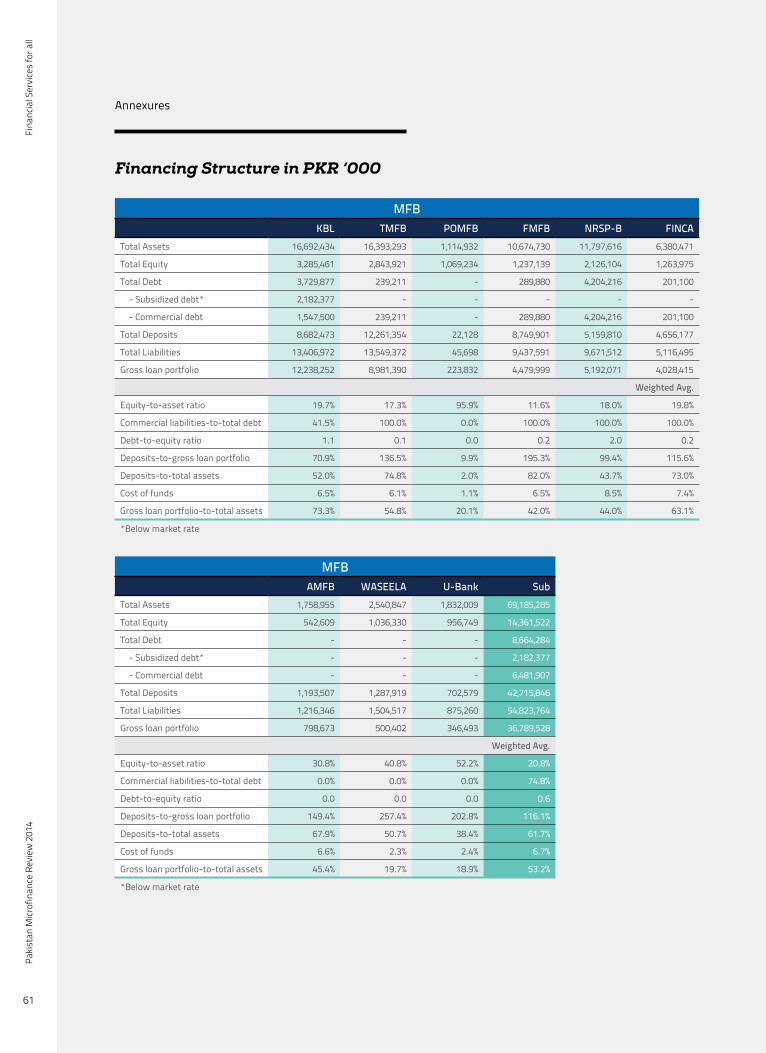

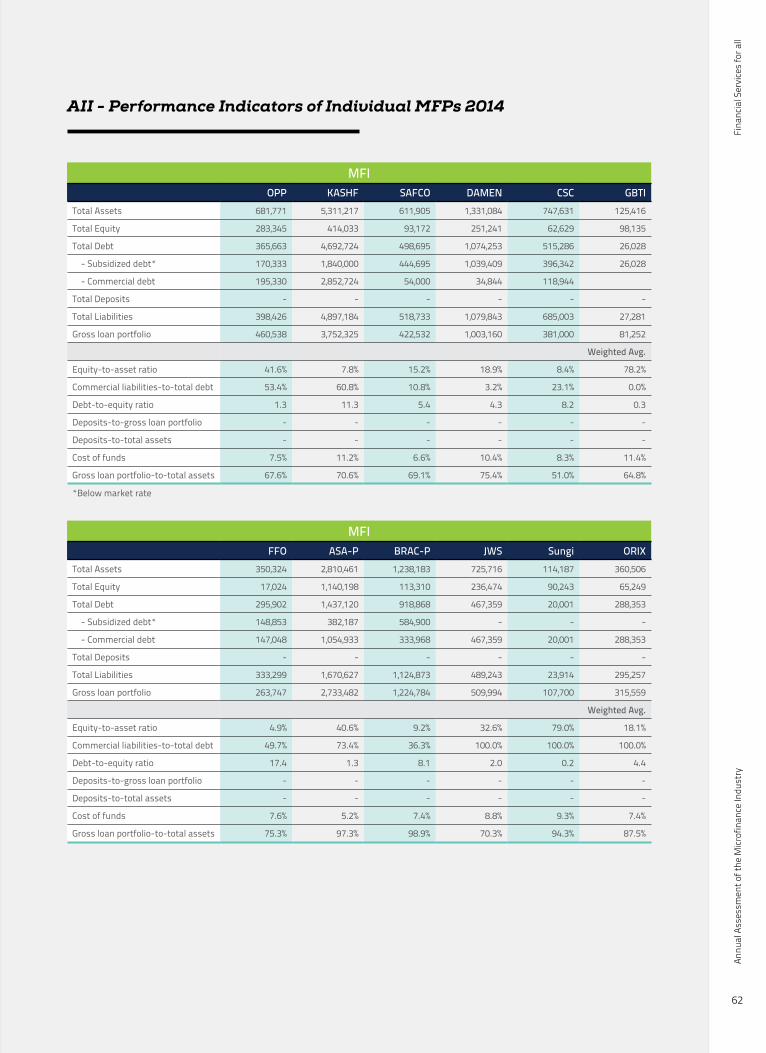

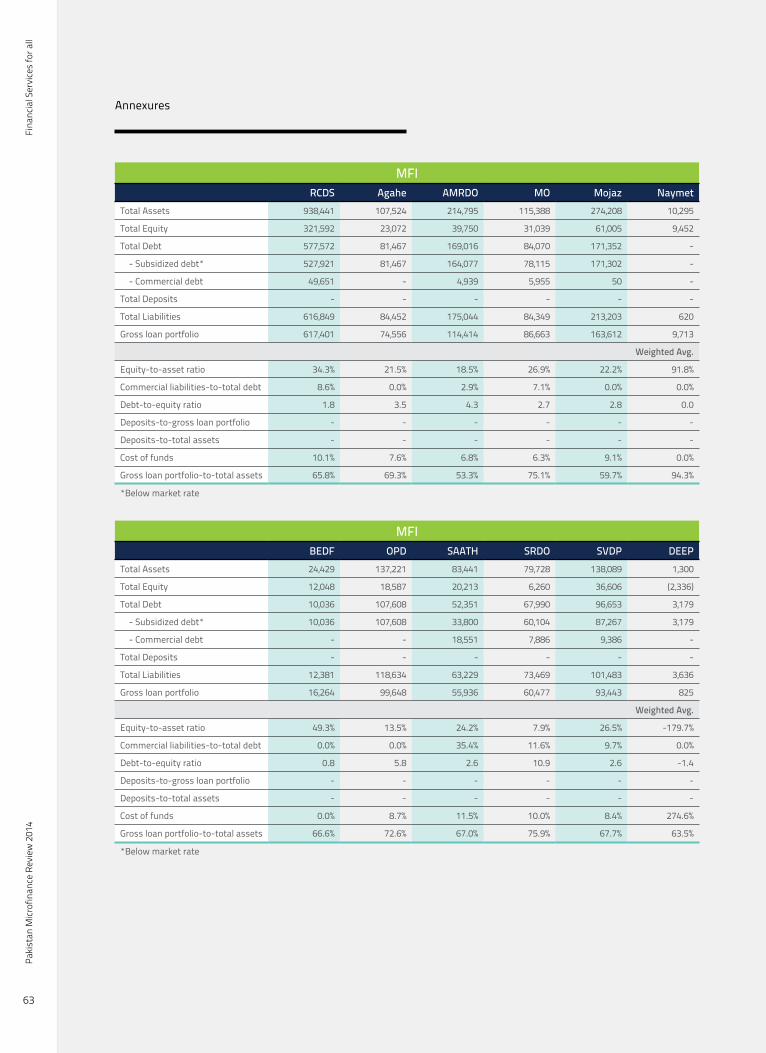

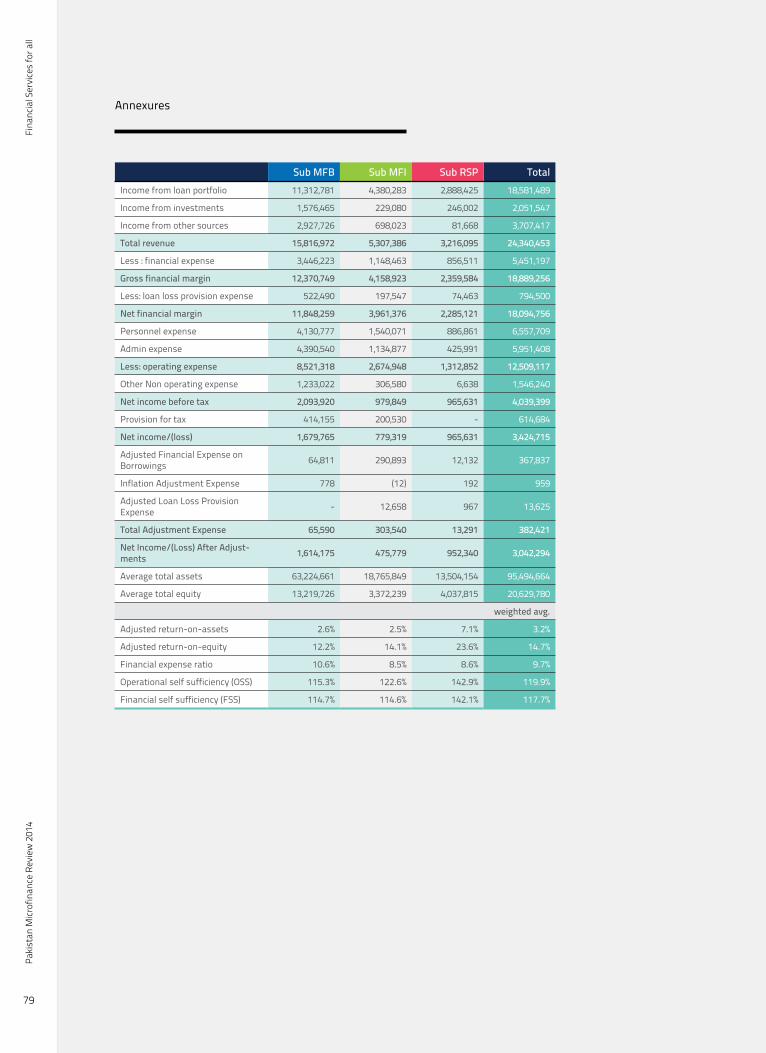

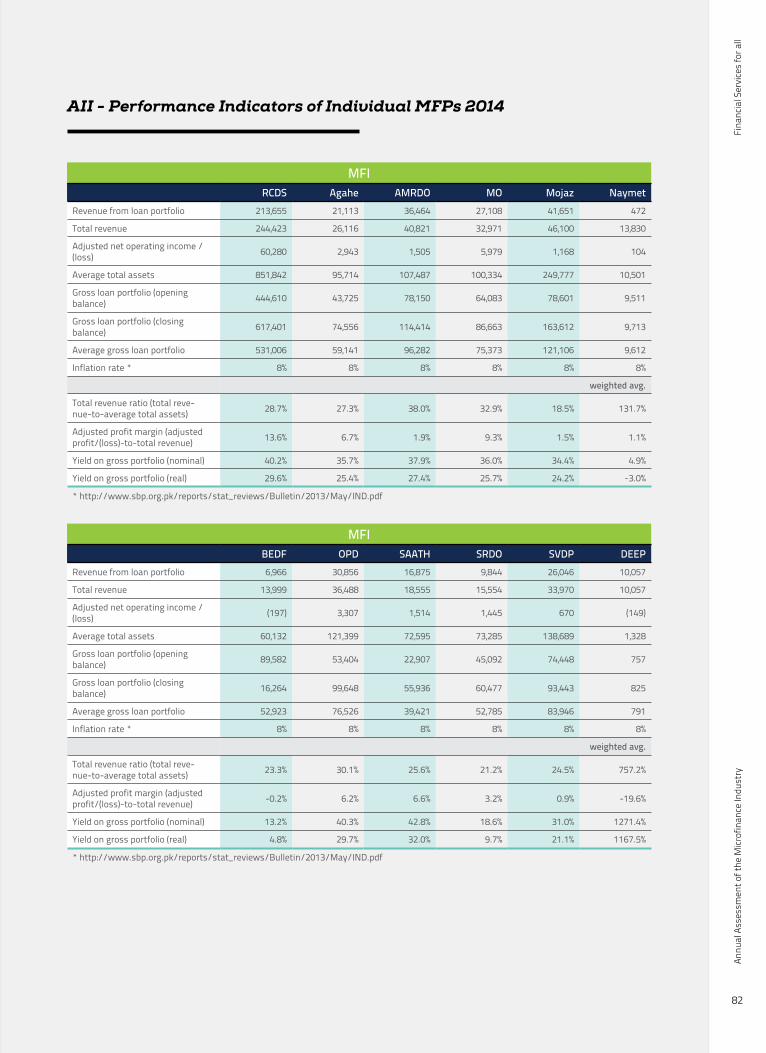

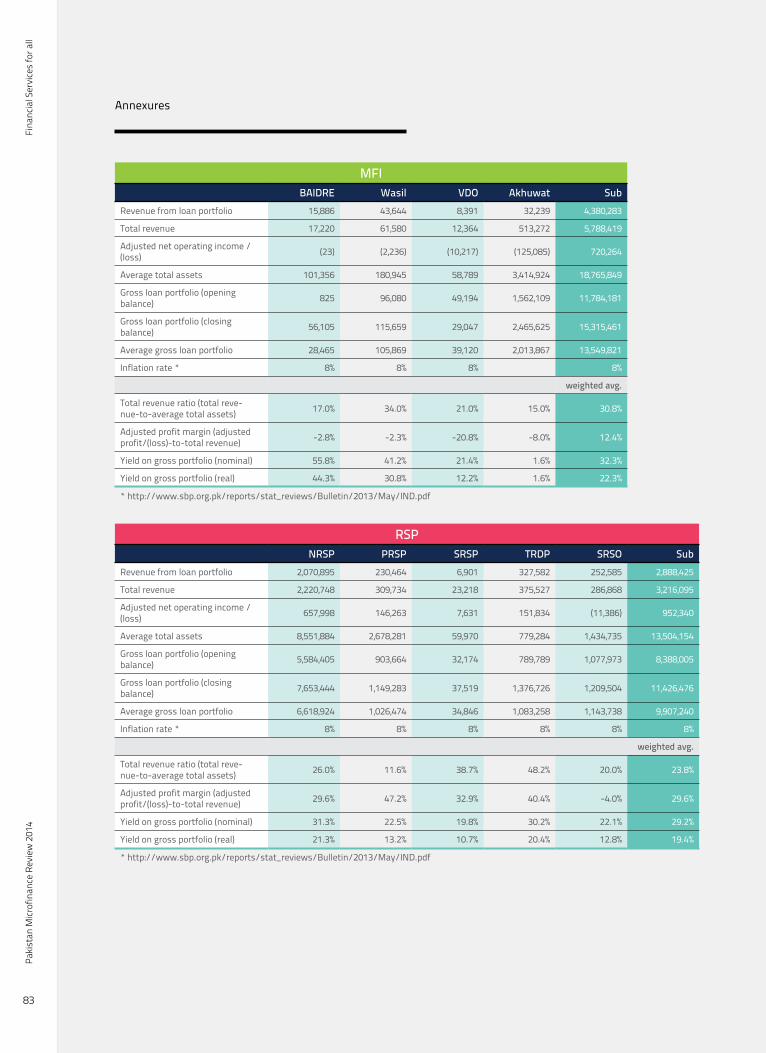

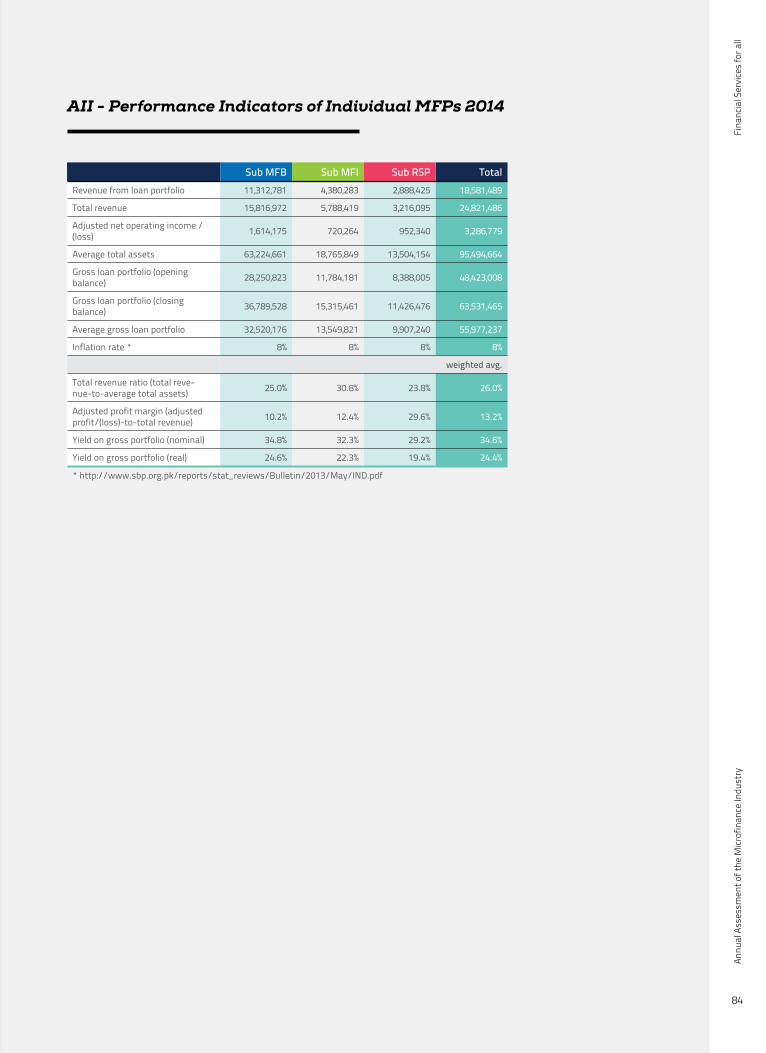

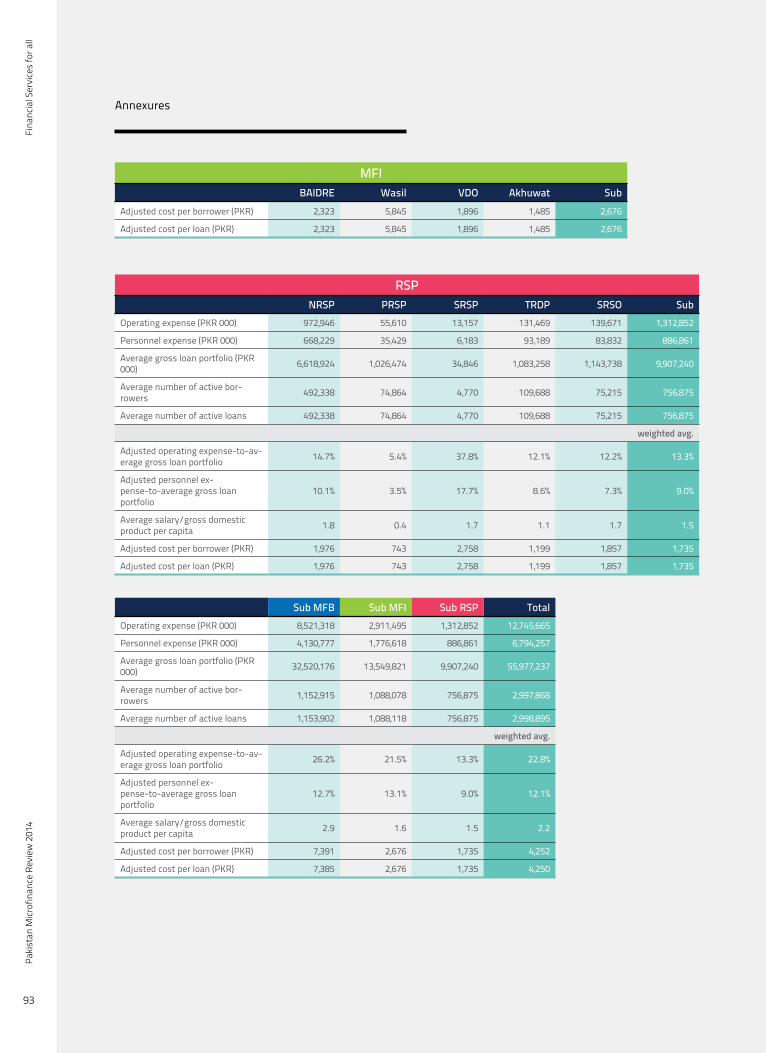

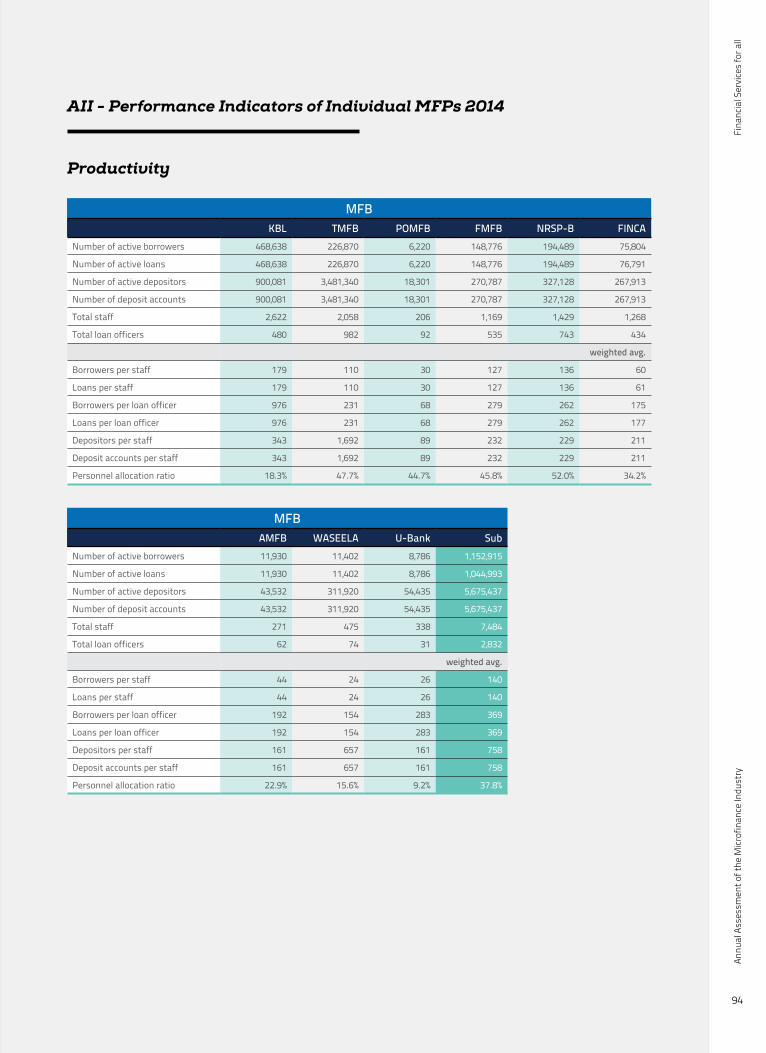

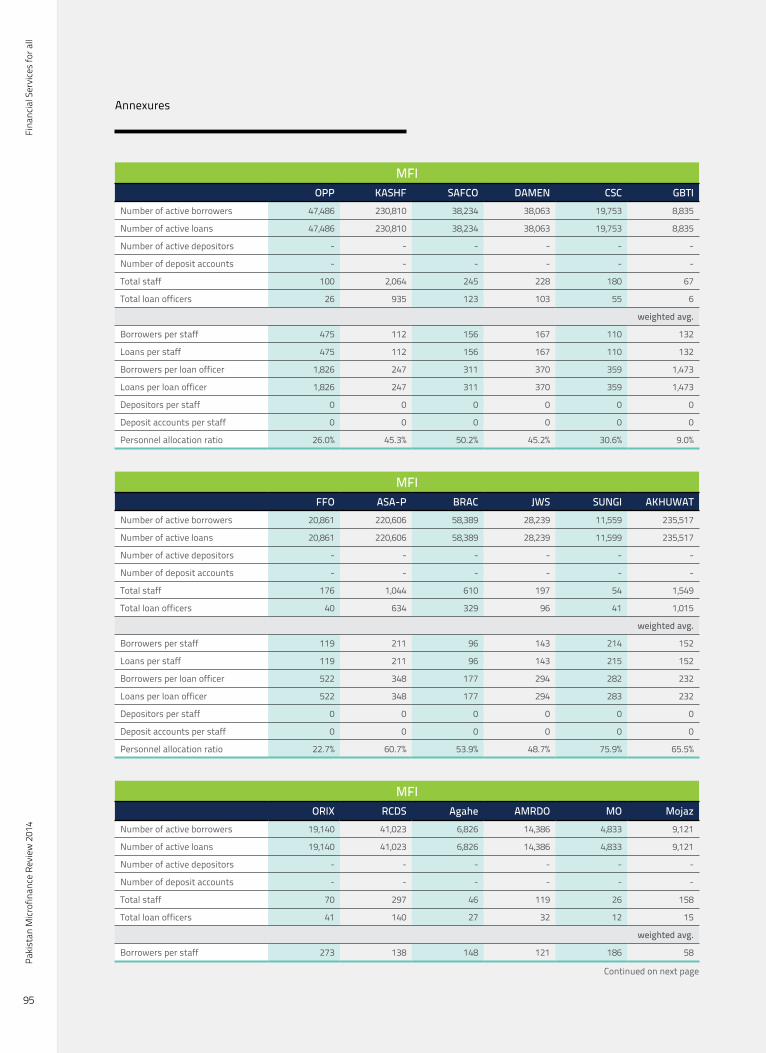

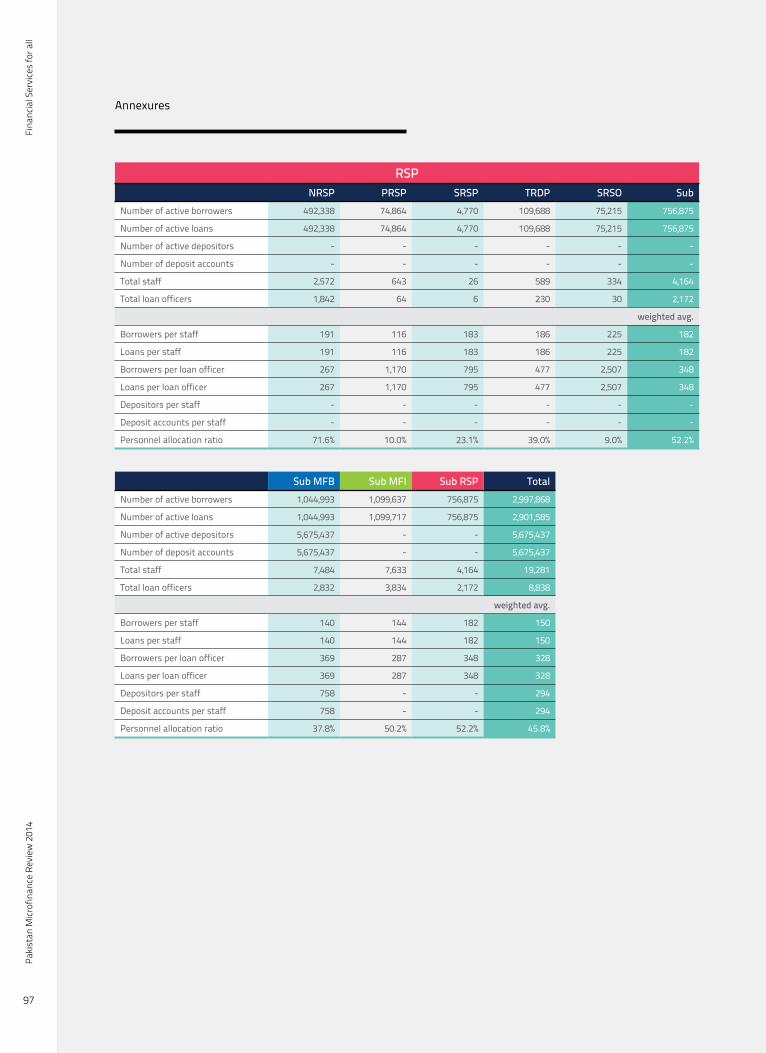

Detailed financial information is provided in Annex A-I and A-II of the PMR. Aggregate data has been re-produced for five years, whereas, the peer group and

institution specific data has been made available only for the year 2014.

A total of 42 MFPs submitted their audited financial statements for PMR 2014. During the period, five new respondents provided their dataset for the first time. For a complete list of reporting organizations refer to Annex B.

Industry players are categorized into three groups for benchmarking and comparison purposes: Microfi-nance Banks (MFBs), Microfinance Institutions (MFIs) and Rural Support Programmes (RSPs). See Box 2A.1 for detailed definitions.

Section 2A: Industry Performance

Box 2A.1

Peer Groups

Microfinance Institution: A non-bank non-government organization (NGO) providing microfinance services. Orga-nizations in this group are registered under a variety of regulations, including the Societies Act, Trust Act, and the Companies Ordinance. The MFI peer group includes local as well as multinational NGOs such as BRAC-Pakistan and ASA-Pakistan.

Microfinance Bank: A commercial bank licensed and prudentially regulated by the SBP to exclusively service the microfinance market. The first MFB was established in 2000 under a presidential decree. Since then, ten MFBs have been licensed under the Microfinance Institutions Ordinance, 2001. Eight of them are operating at national level, while two at the provincial level. MFBs are legally empowered to accept and intermediate deposits from the public.

Rural Support Programme: An NGO registered as a non-profit company under the Companies Ordinance. An RSP is differentiated from the MFI peer group based on the purely rural focus of its credit operations. As a group, the RSPs are registered with and supervised by the Securities and Exchange Commission of Pakistan (SECP).

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

12

Industry Performance

The distribution of respondents (number of reporting organizations) by peer group is given in Exhibit 2A.1. The MFI peer group comprises of the largest number of respondents followed by MFBs and then RSPs.

Scale and outreach

This section focuses on outreach indicators to pro-vide performance analysis of the industry in terms ofcredit growth and composition, deposit mobilization, depth of outreach and gender.

Scale and Outreach: Breadth

Outreach witnessed growth in all key indicators in

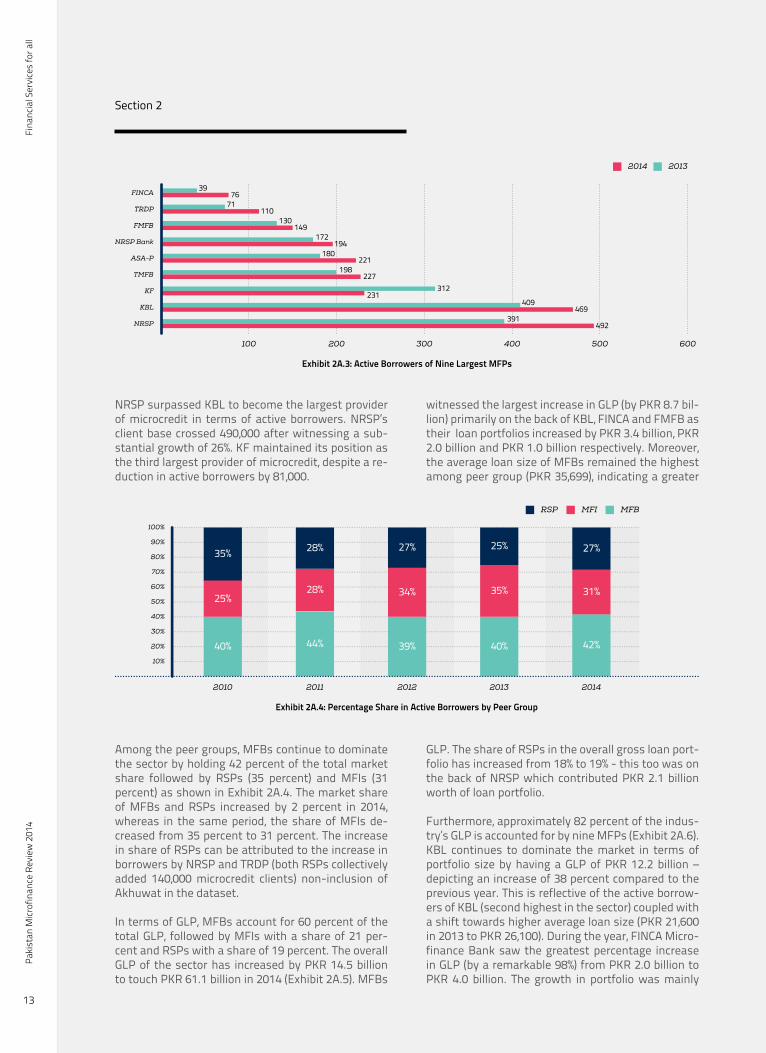

2014 – active borrowers grew by 15 percent from 2.4 million to touch 2.8 million, whereas, the gross loan

portfolio increased significantly by 31 percent from PKR 46.6 billion to PKR 61.1 billion (Exhibit 2A.2). Among the MFPs, growth in active borrowers was led by National Rural Support Program (NRSP) which

added 101,000 borrowers to its portfolio in 2014 – depicting an increase of 26 percent year-over-year. Khushhali Bank (KBL) and ASA Pakistan (ASA-P) also witnessed significant growth, with borrowers increasing from 409,000 to 469,000 and 180,000 to 221,000 respectively. In the current year, Kashf Foun-dation (KF) saw a significant reduction in borrowers (by 26 percent) from 312,000 in 2013 to 230,000 in 2014. This reduction was primarily due to write-offs of non-performing loans.

The industry in terms of outreach was dominated

by nine MFPs that accounted for 79 percent of the outreach as shown in Exhibit 2A.3. During the period,

MFI, 27%

RSP, 5%

MFB, 9%

Exhibit 2A.1 Distribution of Respondents by Peer Groups

Act

ive

bor

row

ers

in m

illio

ns

GL

P in

PK

R B

illio

ns

0.50

1.00

1.50

2.00

2.50

3.00

10

20

30

40

50

60

70

2009 2010 2011 2012 2013 2014

Active borrowersGLP

Exhibit 2A.2: Growth in Number of Active Borrowers and GLP

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

13

Section 2

NRSP surpassed KBL to become the largest provider of microcredit in terms of active borrowers. NRSP’s client base crossed 490,000 after witnessing a sub-stantial growth of 26%. KF maintained its position as the third largest provider of microcredit, despite a re-duction in active borrowers by 81,000.

Among the peer groups, MFBs continue to dominate the sector by holding 42 percent of the total market share followed by RSPs (35 percent) and MFIs (31 percent) as shown in Exhibit 2A.4. The market share of MFBs and RSPs increased by 2 percent in 2014, whereas in the same period, the share of MFIs de-creased from 35 percent to 31 percent. The increase in share of RSPs can be attributed to the increase in borrowers by NRSP and TRDP (both RSPs collectively added 140,000 microcredit clients) non-inclusion of Akhuwat in the dataset.

In terms of GLP, MFBs account for 60 percent of the total GLP, followed by MFIs with a share of 21 per-cent and RSPs with a share of 19 percent. The overall GLP of the sector has increased by PKR 14.5 billion to touch PKR 61.1 billion in 2014 (Exhibit 2A.5). MFBs

witnessed the largest increase in GLP (by PKR 8.7 bil-lion) primarily on the back of KBL, FINCA and FMFB as their loan portfolios increased by PKR 3.4 billion, PKR 2.0 billion and PKR 1.0 billion respectively. Moreover, the average loan size of MFBs remained the highest among peer group (PKR 35,699), indicating a greater

GLP. The share of RSPs in the overall gross loan port-folio has increased from 18% to 19% - this too was on the back of NRSP which contributed PKR 2.1 billion worth of loan portfolio.

Furthermore, approximately 82 percent of the indus-try’s GLP is accounted for by nine MFPs (Exhibit 2A.6). KBL continues to dominate the market in terms of portfolio size by having a GLP of PKR 12.2 billion – depicting an increase of 38 percent compared to the previous year. This is reflective of the active borrow-ers of KBL (second highest in the sector) coupled with a shift towards higher average loan size (PKR 21,600 in 2013 to PKR 26,100). During the year, FINCA Micro-finance Bank saw the greatest percentage increase in GLP (by a remarkable 98%) from PKR 2.0 billion to PKR 4.0 billion. The growth in portfolio was mainly

NRSP

KBL

KF

TMFB

ASA-P

NRSP Bank

FMFB

TRDP

FINCA

100 200 300 400 500 600

20132014

39

71

130149

172194

180221

198227

312

409

391492

469

231

110

76

Exhibit 2A.3: Active Borrowers of Nine Largest MFPs

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014

MFBMFIRSP

35%

25%

40% 44% 39% 40% 42%

28% 34% 35% 31%

28% 27% 25% 27%

Exhibit 2A.4: Percentage Share in Active Borrowers by Peer Group

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

14

Industry Performance

supported by a large deposit base of the bank. TMFB, backed by its above average loans sizes, remained the second largest player in terms of portfolio size with a GLP of PKR 9.0 billion.

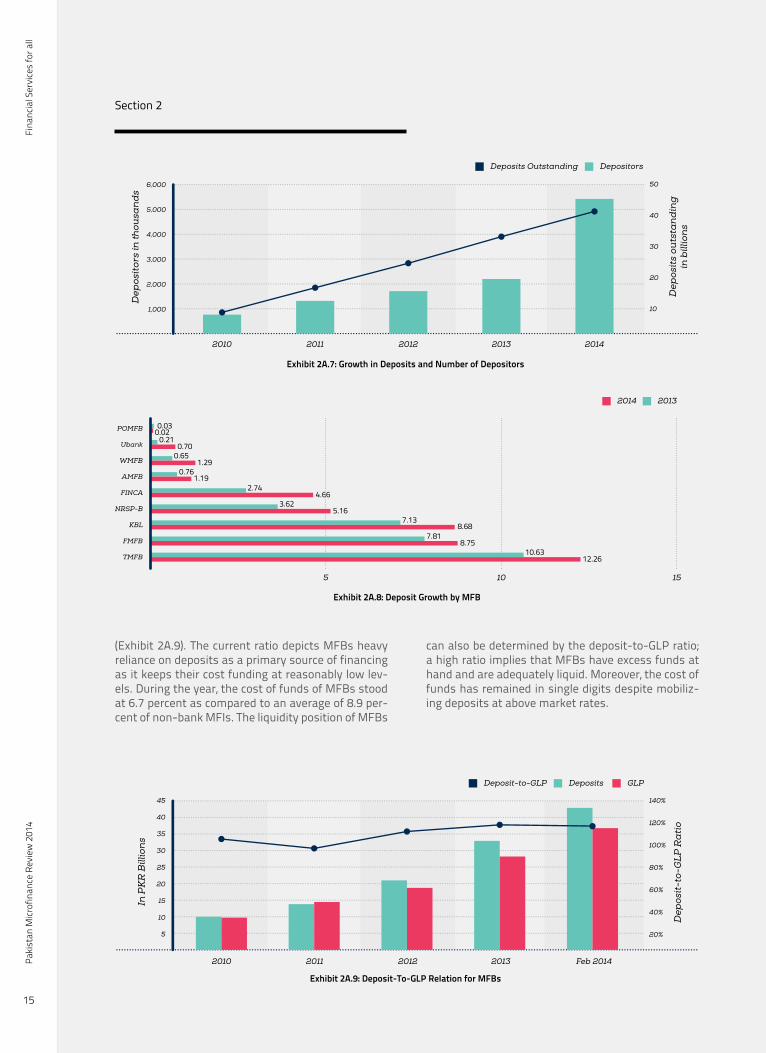

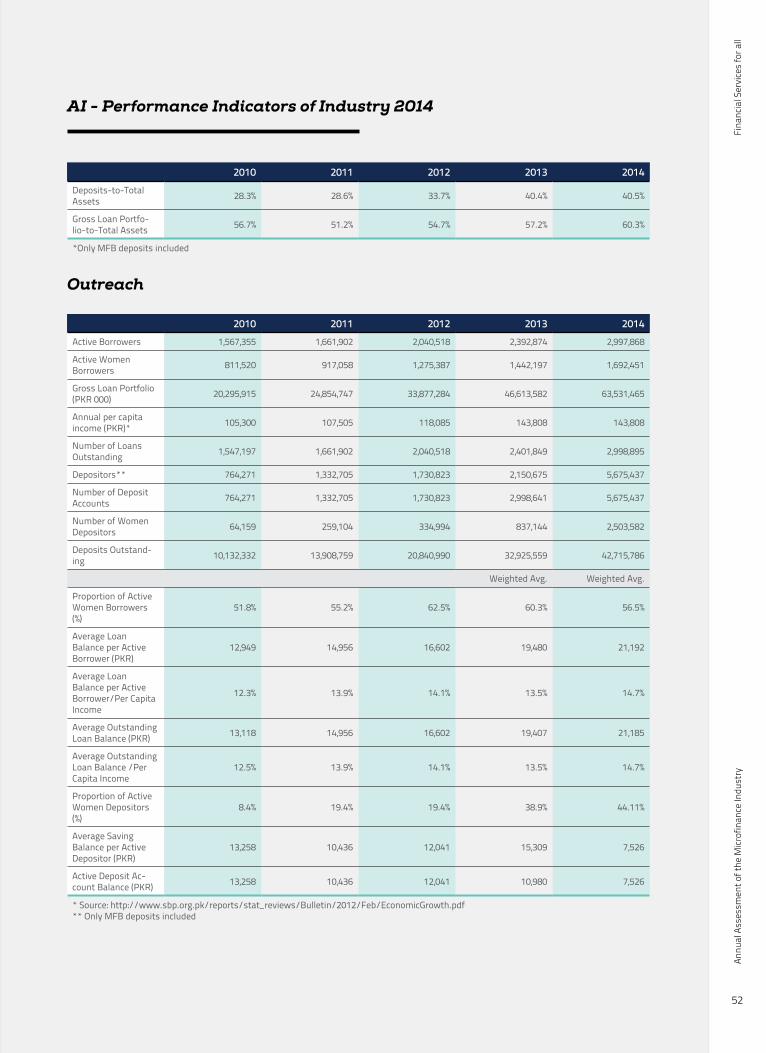

In the year under review, the sector witnessed a stag-gering rise in the number of depositors (by 150 per-cent) from 2.2 million in 2013 to 5.7 million in 2014. Similarly, the value of deposits grew by 30 percent in the same year, from PKR 32.9 billion to PKR 42.7 billion (Exhibit 2A.7). Resultantly, deposits now rep-

resent 78 percent of the total liabilities of the MFB peer group – an increase from 72 percent in the pre-vious year. Moreover, deposits continue to outgrow the loan portfolio of MFBs, as is evident from the de-posits-to-gross loan portfolio ratio which currently stands at 116.1%.The largest increase in the number of depositors came from TMFB which added 2.65 million new de-positors (an increase of over 300 percent). The hefty

growth in depositors can be attributed to the surge in branchless banking activities, especially the opening of m-wallet accounts, along with increasing govern-ment disbursements for safety net programs such as the Benazir Income Support Program (BISP). TMFB was followed by KBL and NRSP Bank which contrib-uted 226,000 and 219,000 depositors respectively in the reporting year. In terms of growth in value of deposits, FINCA was the largest contributor to the value of deposits; by adding PKR 1.9 billion worth of deposits to increase

its deposit base from PKR from PKR 2.7 billion in 2013 to PKR 4.7 billion in 2014 (Exhibit 2A.8). FINCA was followed by TMFB whose deposits grew by PKR 1.6 billion to close its balance sheet at PKR 12.3 bil-lion deposits.

The Deposit-to-GLP ratio for MFBs remained stag-nant in the current year; the ratio decreased by 1 per-cent from 117 percent in 2013 to 116 percent in 2014

10

20

30

40

50

60

70

2010 2011 2012 2013 2014

MFBMFIRSP

9.83.96.6

14.6

5.05.3

18.7

7.66.7

28.1

10.2

8.4

36.8

12.9

11.4

PK

R in

Bill

ion

s

Exhibit 2A.5: GLP (PKR billions) by Peer Group 2013-14

Exhibit 2A.6: GLP of Nine Largest MFPs

KBL

TMFB

NRSP

NRSP Bank

FMFB

FINCA

KF

ASA-P

SRSO

20132014

1.1

1.9

3.5

2.04.0

3.54.5

2.7

3.8

1.2

5 10 15

4.85.2

5.67.7

8.39.0

8.912.2

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

15

Section 2

(Exhibit 2A.9). The current ratio depicts MFBs heavy reliance on deposits as a primary source of financing as it keeps their cost funding at reasonably low lev-els. During the year, the cost of funds of MFBs stood at 6.7 percent as compared to an average of 8.9 per-cent of non-bank MFIs. The liquidity position of MFBs

can also be determined by the deposit-to-GLP ratio; a high ratio implies that MFBs have excess funds at hand and are adequately liquid. Moreover, the cost of funds has remained in single digits despite mobiliz-ing deposits at above market rates.

Dep

osit

ors

in th

ousa

nd

s

1,000

2,000

3,000

4,000

5,000

6,000

Dep

osit

s ou

tsta

nd

ing

in b

illio

ns

10

20

30

40

50

2010 2011 2012 2013 2014

DepositorsDeposits Outstanding

Exhibit 2A.7: Growth in Deposits and Number of Depositors

Exhibit 2A.8: Deposit Growth by MFB

POMFB

Ubank

WMFB

AMFB

FINCA

NRSP-B

KBL

FMFB

TMFB

20132014

0.030.02

0.210.70

0.651.29

0.761.19

2.744.66

3.625.16

7.138.68

7.818.75

10.6312.26

5 10 15

Exhibit 2A.9: Deposit-To-GLP Relation for MFBs

In P

KR

Bill

ion

s

5

10

15

20

25

30

35

40

45

Dep

osit

-to-

GL

P R

ati

o

20%

40%

60%

80%

100%

120%

140%

Deposits GLPDeposit-to-GLP

2010 2011 2012 2013 Feb 2014

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

16

Industry Performance

Micro-insurance indicators – number of policy hold-ers and sum insured – both showed a significant improvement in the year 2014. The number of poli-cy holders grew by 23.8 percent over the year, rising from 3.0 million to 3.8 million, while the sum insured increased by 50.0 percent from PKR 40.3 billion to PKR 60.4 billion (see Exhibit 2A.10).

The greatest increase in micro-insurance came from the MFB peer group whose policy holders and sum insured increased by 46 percent and 80 percent re-

spectively. During the year, MFBs enhanced the cov-erage of their insurance products by securing more credit clients, along with their spouses. However, among individual institutes, NRSP remained the larg-est providers of micro-insurance; holding a market share of 22 percent and 24 percent in terms of policy holders and total sum insured, respectively. Among the types of insurance policies, health insurance con-stituted almost 51 percent of total insurance policies followed by credit life at 49 percent.

Scale and Outreach: Depth

The depth of outreach in microcredit operations is measured by a proxy indicator: average loan balance per borrower in proportion to per capita Gross Nation-al Income (GNI). A value below 20 percent is assumed to mean that the MFP is poverty focused. Except for KBL and NRSP Bank, all of the other MFBs fall above this benchmark (Exhibit 2A.11). Comparison across peer groups shows that the ratio of average loan bal-ance to per capita GNI for MFBs has been on the rise

for the past four years. MFBs tend to target the upper end of the market through relatively larger loan siz-es, and hence have a ratio of 20 percent compared to MFIs and RSPs which have a ratio of 10 percent each.

The ratio of average loan balance to per capita GNI witnessed a modest increase for MFBs (by 2 percent) and MFIs (by 1 percent), while the ratio for RSPs re-mained stagnant at 10.0 percent. This could be inter-preted as the sector continuing to target the poor but also has implications for appropriate loan sizes in the

Pol

icy

Hol

der

s in

mill

ion

s

1.70

2.20

2.70

3.20

3.70

4.20

Su

m In

sure

d in

PK

R B

illio

ns

10

20

30

40

50

60

70

2010 2011 2012 2013 2014

Policy HoldersSum Insured

Exhibit 2A.10: Growth in Number of Policy Holders and Sum Insured

5%

10%

15%

20%

25%

2009 2010 2011 2012 2013 2014

MFBMFIRSPIndustryCut-off

Ave

rag

e L

oan

Ba

lan

ceP

er G

DP

Exhibit 2A.11: Depth of Outreach by Peer Groups

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

17

Section 2

context of Pakistan’s inflationary environment. Ero-sion in the value of money means that a loan worth PKR 30,000 in one year would be considerably lower in value in the following year.

Lending Methodology

In the Pakistan microfinance sector, majority of MFPs follow the group lending methodology – in 2014, 68 percent of the active borrowers represented group

lending (see Exhibit 2A.12). However, over the past four years, the share of individual lending has been increasing gradually, as many MFPs which were fol-lowing the group lending methodology, also started focusing on Individual lending methodology. In the

period under review, individual lending showed an increse of 8 percent, whereas, group lending has de-creased from 76 percent to 68 percent. During the reporting year, FINCA, Kashf Foundation and TMFB

were the main drivers for the increase in the share of individual borrowing from 24 percent in 2013 to 27 percent in 2014.

Gender Distribution

The proportion of women borrowers depicted a downward movement in the current year, decreas-ing from 60.3 percent in 2013 to 58.0 percent in 2014 (Exhibit 2A.13). The proportion of women borrowers

for MFBs and MFIs increased slightly by 1 percent, whereas, the proportion of women borrowers for RSPs remained unchanged. Out of the three peer groups, the client base of MFBs is mostly composed of male borrowers, while MFIs and RSPs are more

oriented towards women borrowers.

Women borrowers remain an integral part of the Pakistan microfinance sector and lending to women

500

1,000

1,500

2,000

2,500

3,000

3,500

2010 2011 2012 2013 2014

Individual BorrowingGroup Borrowing

90%

10% 12% 22% 24% 27%

88%78%

76%73%

Act

ive

Bor

row

ers

in T

hou

san

ds

Exhibit 2A.12: Lending Methodology

Exhibit 2A.13: Gender Distribution of Credit Outreach by Peer Groups

20%

10%

30%

40%

50%

60%

70%

80%

90%

100%

Male BorrowersFemale Borrowers

MFB MFI RSP Total

25%

75%

89%

11%

74%

26%

58%

42%

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

18

Industry Performance

has been encouraged by various donor and regulato-ry bodies. The national apex – PPAF – provides fund-ing to MFPs based on a commitment that at least 40 percent of the borrowers will be women. Large players such as NRSP, ASA Pakistan, and SRSO have portfolios that mostly constitute of women borrow-ers, whereas, Kashf Foundation only lends to women borrowers.

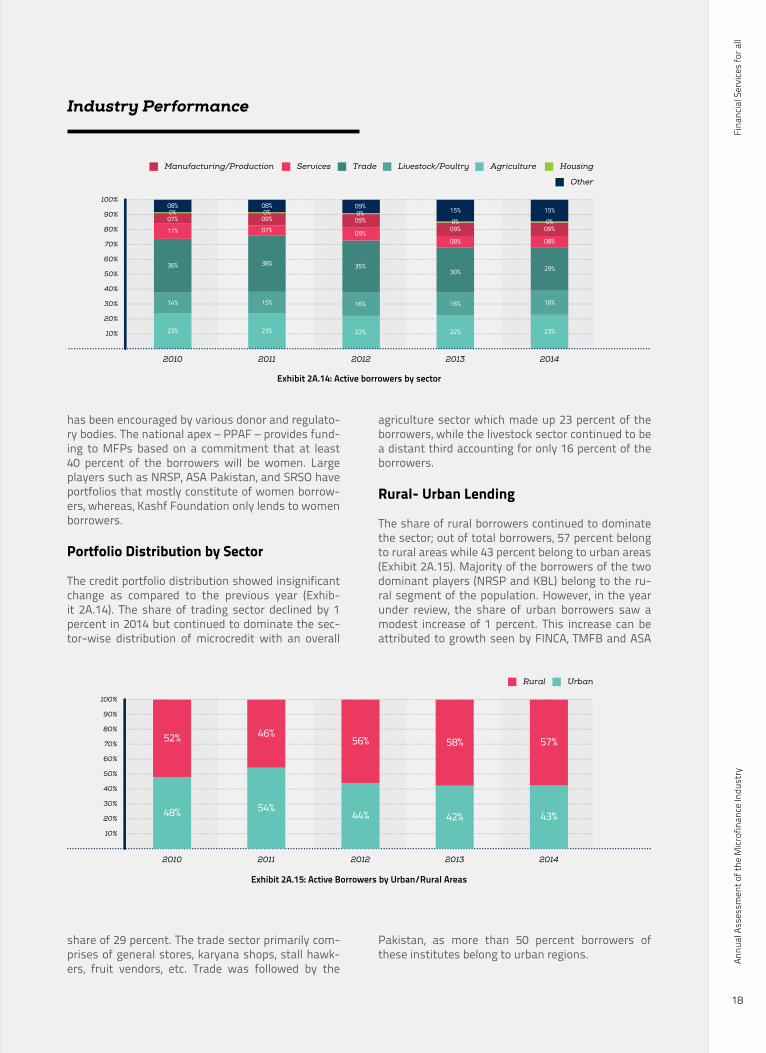

Portfolio Distribution by Sector

The credit portfolio distribution showed insignificant change as compared to the previous year (Exhib-it 2A.14). The share of trading sector declined by 1 percent in 2014 but continued to dominate the sec-tor-wise distribution of microcredit with an overall

share of 29 percent. The trade sector primarily com-prises of general stores, karyana shops, stall hawk-ers, fruit vendors, etc. Trade was followed by the

agriculture sector which made up 23 percent of the borrowers, while the livestock sector continued to be a distant third accounting for only 16 percent of the borrowers.

Rural- Urban Lending

The share of rural borrowers continued to dominate the sector; out of total borrowers, 57 percent belong to rural areas while 43 percent belong to urban areas (Exhibit 2A.15). Majority of the borrowers of the two dominant players (NRSP and KBL) belong to the ru-ral segment of the population. However, in the year under review, the share of urban borrowers saw a modest increase of 1 percent. This increase can be attributed to growth seen by FINCA, TMFB and ASA

Pakistan, as more than 50 percent borrowers of these institutes belong to urban regions.

2010 2011 2012 2013 2014

UrbanRural

20%

10%

30%

40%

50%

60%

70%

80%

90%

100%

48%

52%

54%

46%

44%

56%

42%

58%

43%

57%

Exhibit 2A.15: Active Borrowers by Urban/Rural Areas

Exhibit 2A.14: Active borrowers by sector

20%

10%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014

Other

Agriculture HousingLivestock/PoultryTradeServicesManufacturing/Production

23% 23% 22% 22% 23%

16%

29%

08%

09%0%

15%

16%

30%

08%

09%0%

15%

16%

35%

09%

09%0%

09%

15%

38%

07%09%0%

08%

14%

36%

11%

07%0%

08%

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

19

Section 2

Financial Structure

Asset Base

The asset base for the industry stood at over PKR 100.71 billion in the year 2014, an increase from PKR 81.55 billion in the previous year showing a year on year increase of 23 percent.

MFBs accounted for 69 percent of the asset base of the industry followed by MFIs at 16 percent and RSPs by 15 percent. The asset size of MFB peer group stood at PKR 69.2 billion compared to PKR 55.4 bil-lion in the last year (see Exhibit 2A.16) showing an

increase of more than 24 percent. The MFI and RSP peer groups witnessed an increase of 20 percent in their asset size as compared to the previous year. As-set base for MFIs and RSPs stood at PKR 16.2 billion and PKR 15.3 billion in 2014, respectively.

Among the players, KBL is the largest MFP by asset size with PKR 16.7 billion of assets closely followed by TMFB with assets over PKR 16.4 billion as shown in Exhibit 2A.17. At third place is NRSP Bank with an asset base of PKR 11.8 billion. Among the MFIs, KF is the largest player by asset size with assets of PKR 5.3 billion followed by ASA-P with assets of PKR 2.8 billion. In the RSP peer group, NRSP is the largest player with an asset base of PKR 9.8 billion followed

by PRSP with assets of PKR 2.5 billion. Overall the industry continued to remain concentrated with nine large MFPs, which include five MFBs, making up 83 percent of the industry.

Asset Composition

The asset utilization ratio which had remained range bound over the last few years showed notable im-provement rising to 60.6 percent in 2014 as com-pared to 54.5 percent in 2013 as shown in Exhibit

2010 2011 2012 2013 2014

MFBMFIRSP

20

10

30

40

50

60

70

80

PK

R in

bill

ion

s

Exhibit 2A.16: Total Asset Base by Peer Group

Exhibit 2A.17: Asset Base of Larger MFPs

KBL

TMFB

NRSP Bank

FMFB

NRSP

FINCA

Kashf

ASA-P

PRSP

20132014

2.82.5

2.02.8

5.34.0

6.47.3

5 10 15 20

9.89.5

10.79.8

11.815.2

16.413.3

16.7

4.6

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

20

Industry Performance

2A.18. Improvements were witnessed in the asset utilization ratio of the MFI and RSP peer group which stood at 79.2 percent and 74.7 percent respectively whereas the MFBs experienced an increase from 50.7 percent in 2013 to 53.2 percent in 2014.

Despite the improvement in the asset utilization ratio in the year 2014, it was below its regional peers as shown in the Exhibit 2A.19. For the industry to im-prove its bottom line there is a need to improve their utilization ratio through better liquidity management.

Asset composition remained varied across the in-dustry. MFIs accounted for the highest advances to total assets ratio closely followed by RSPs as shown in Exhibit 2A.20. Improvement in the ratio for MFIs and RSPs is largely due to increase in grace period being offered by the national apex. MFB peer group has lower advances to total assets as a number of players have recently been acquired and their credit business is in formative stages. In addition, one of the larger players, FMFB, has only been able to deploy half of its deposit base leading to lower value for the

entire peer group. Over time, as these re-established players grow and achieve scale, there will be further increase in the ratio for MFBs.

Funding Profile

The capital structure of the industry continued to wit-ness the trend of increasing deposits and decrease in debt in 2014 as shown in Exhibit 2A.21. Deposits now make up 44 percent of the total funding of the sector as compared to 39 percent in 2013. Debt has fallen to 33 percent of the funding from 39 percent in the same time period. Equity witnessed a slight increase to account for 23 percent of the total fund-ing on the back of increasing profitability among the practitioners.

The capital structure continues to be differ among the peer groups with non-bank MFPs relying on debt and equity for funding as they are prohibited to mobi-

2010 2011 2012 2013 2014

Asset Utilization Ratio

20%

10%

30%

40%

50%

60%

70%

Exhibit 2A.18: Asset Utilization Trend 2010-14

Africa East Asiaand thePacific

Eastern Europeand

Central Asia

Latin Americaand The

Caribbean

Middle Eastand

North Africa

South Asia Pakistan

20%

40%

60%

80%

100%

Exhibit 2A.19: Regional Comparison of Asset Utilization Ratio

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

21

Section 2

lize deposits. Meanwhile, MFBs continue to witness notable success in deposit mobilization which is re-flected in their increasing reliance on deposits as a

source of funds.

64 percent of the MFBs funding is made up of depos-its up from 62 percent in the previous year as shown in Exhibit 2A.22. In case of MFI peer group, debt con-tinues to make up 80 percent of the funding whereas in the case of RSPs debt accounts for 70 percent of the capital, slightly up from 69 percent in the preced-ing year.

While MFBs are relying on deposits to meet the bulk of their funding needs, it is pertinent to note that out of nine MFBs reporting for PMR only six have a

deposit base larger than their GLP. In addition, two thirds of the deposits are accounted for by three MFBs namely, TMFB, KBL and FMFB.

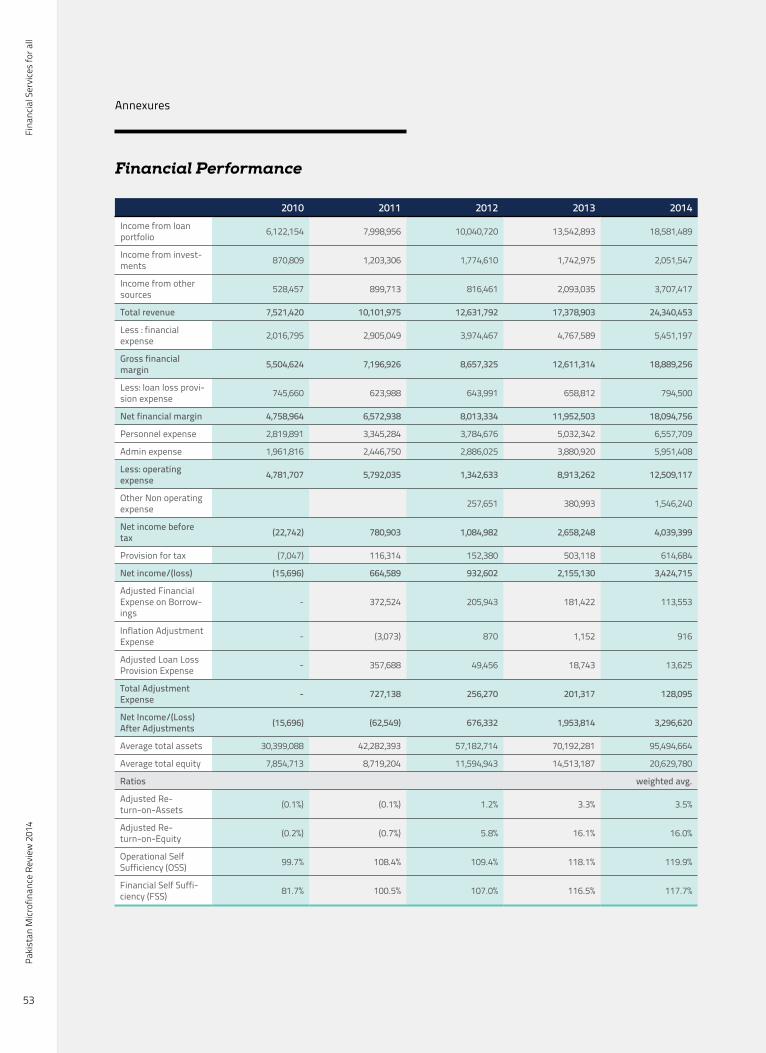

Profitability and Sustainability

The total net income and total revenues for the in-dustry stood at PKR 3.5 billion and PKR 24.3 billion in the year 2014 respectively. The unadjusted ROA and ROE for the industry stood at 4.2 percent and 20.7 percent for the year. Out of the total profit for the in-dustry the MFB peer group accounted for 47 percent of the profit whereas the MFI and RSP peer groups made up 25 percent and 28 percent.

The industry continues to be sustainable with Oper-ational Self Sufficiency (OSS) and Financial Self Suffi-

Equity, 23%

Debt, 33%

Deposits, 44%

Exhibit 2A.21: Capital Structure of Microfinance Industry

Exhibit 2A.20: Asset Composition among Peer Groups

2013 2014 2013 2014 2013 2014

20%

40%

60%

80%

100%

MFIMFB RSP

55%

22%

4%

19%

53%

24%

3%

20%

76%

0%4%

20%

79%

0%3%

18%

70%

9%5%

16%

75%

7%4%

14%

AdvancesInvestmentsFixed AssetsCash and Bank Balance

Pro

por

tion

of

Tot

al A

sset

s

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

22

Industry Performance

ciency (FSS) not only above 100 percent but also show an improving trend as seen in Exhibit 2A.23. Out of the 41 reporting organizations 35 have an OSS above 100 percent. Improvement in OSS and FSS is fuelled primarily by increasing GLP and growth in outreach. This points towards the increasing maturity of the practitioners business models. In addition, MFPs are

now ideally geared towards accelerated growth and innovation.

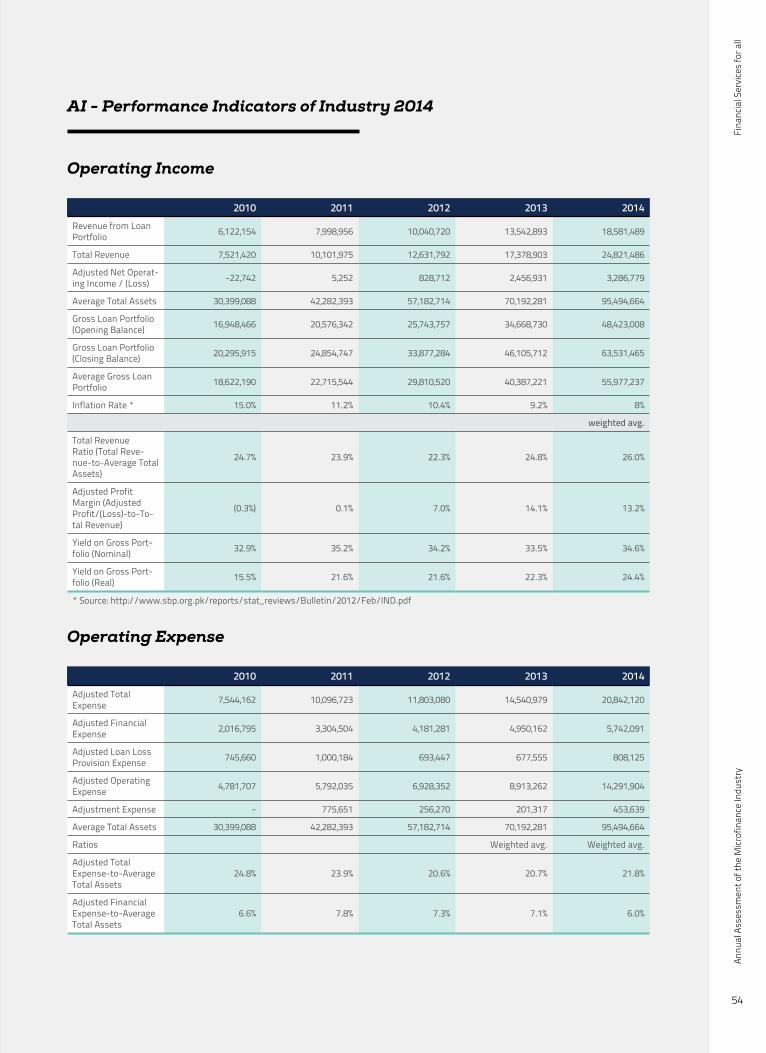

The total revenue ratio for the industry increased to 28.5 percent from 24.8 in 2013 on the back of in-creasing GLP and income generated from branchless banking operations. In addition, the yield on gross portfolio remained stable, (shown in Exhibit 2A.24) to close at 34.6 percent.

Compared globally, the yield on gross portfolio (nom-inal) continues to be on the higher side (see Exhibit 2A.25). However, the higher yield is largely as a result of high operating costs which are a function of the relatively smaller loan sizes offered by the industry. As the loan sizes increase over time especially after the start of lending to microenterprises it is antici-

pated that operating costs will decline resulting in reduction of yield on loan portfolio.

20%

40%

60%

80%

100%

120%

140%

2010 2011 2012 2013 2014

Financial self sufficiency (FSS)Operational Self Sufficiency (OSS)

Exhibit 2A.23: OSS and FSS Trend

Exhibit 2A.22: Capital Structure by Peer Group

20%

10%

30%

40%

50%

60%

70%

80%

90%

2013 2014 2013 2014 2013 2014

MFIMFB RSP

EquityDebtDeposits

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

23

Section 2

The total revenues for the sector stood at PKR 24.3 billion up from PKR 17.3 billion in the previous year. Out of the total revenue, 76.9 percent is made up from earnings from loan portfolio followed by 15.5 percent from financial services including branchless banking and 7.6 percent from earnings on the financial assets

(see Exhibit 2A.26 ). The total income from branchless banking stood at PKR 2.3 billion in 2014 as compared to PKR 2.0 billion in the previous year. The increase is partially due to the addition of Waseela MFB in the dataset for the first time.

5

10

15

20

25

30

2010 2011 2012 2013 2014

Loan PortfolioFinancial ServicesFinancial Assets

PK

R in

bill

ion

s

Exhibit 2A.26: Revenue Streams

Exhibit 2A.24: Total Revenue Ratio & Yield on Gross Portfolio Trend

5%

10%

15%

20%

25%

30%

35%

40%

2010 2011 2012 2013 2014

Yield on Gross Portfolio (Real)Yield on Gross Portfolio (Nominal)Total Revenue Ratio

Exhibit 2A.25: Regional Comparison of Yield on Gross Portfolio (Nominal)

Africa East Asiaand thePacific

Eastern Europeand

Central Asia

Latin Americaand The

Caribbean

Middle Eastand

North Africa

South Asia Pakistan

5%

10%

15%

20%

25%

30%

35%

Yield on Gross Portfolio (Nominal)

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

24

Industry Performance

Expense to asset ratio witnessed a slight increase in the 2014 as shown in Exhibit 2A.27. The total expense ratio increased to 21.9 percent as compared to 20.7 percent in the previous year. The increase was driven

by the increase in the operating expenses which was partially due to inclusion of a number of smaller and growing organizations in the dataset and partially due to increasing administrative expenses.

Africa East Asiaand thePacific

Eastern Europeand

Central Asia

Latin Americaand The

Caribbean

Middle Eastand

North Africa

South Asia Pakistan

5%

10%

15%

20%

Operating Expense / Assets

Exhibit 2A.28: Regional Comparison of Operating Expense

Exhibit 2A.27: Expenses to Asset Ratio Trend

10%

20%

30%

2010 2011 2012 2013 2014

Adjusted Loan Loss Provision Expense/ Total AssetsAdjusted Financial Expense/ Total Assets

Adjusted Operating Expense/ Total AssetsAdjusted Total Expense / Total Assets

Exhibit 2A.29: Operating Expense to GLP Trend

5%

10%

15%

20%

25%

30%

2010 2011 2012 2013 2014

Admin Expense/ Gross Loan PortfolioPersonnel Expense/ Gross Loan Portfolio

Operating Expense / Gross Loan Portfolio

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

25

Section 2

The operating expense was on the higher end as compared to other regions as seen in Exhibit 2A.28. This points towards the fact that MFPs in Pakistan have yet to achieve scale and only then costs can be reduced. Branchless banking can play a crucial role in bringing down the operating costs of the industry.

Operating expense to GLP also witnessed an increase in 2014 after exhibiting a declining trend over the last few years as shown in Exhibit 2A.29. Operating ex-pense to GLP stood at 23.0 percent as compared to 22.1 percent in the previous year. The increase in the expense was due to rise in the administrative ex-pense.

Productivity

The personnel allocation ratio for the industry saw a modest improvement in 2014. The ratio increased to 44.5 percent compared to 44.0 percent in the pre-vious year (see Exhibit 2A.30). The personnel alloca-tion ratio continued to vary among the peer groups. RSPs continued to have the highest value with 52.2 percent, followed by MFIs with 48 percent and MFBs

with the lowest value at 37.8 percent.

The productivity indicators of the industry continued to exhibit improvement in the year 2014. Loans per staff and loans per loan officers rose to 152 and 342 as compared to 144 and 327 in the previous year. De-positors per staff increased to 293 as compared to 269 in the same time period (see Exhibit 2A.31).

Loan per staff officer continued to vary among the peer groups. MFBs had the highest number of loans per staff with 369 loans followed by RSPs with 348 and MFIs with 308.

Risk

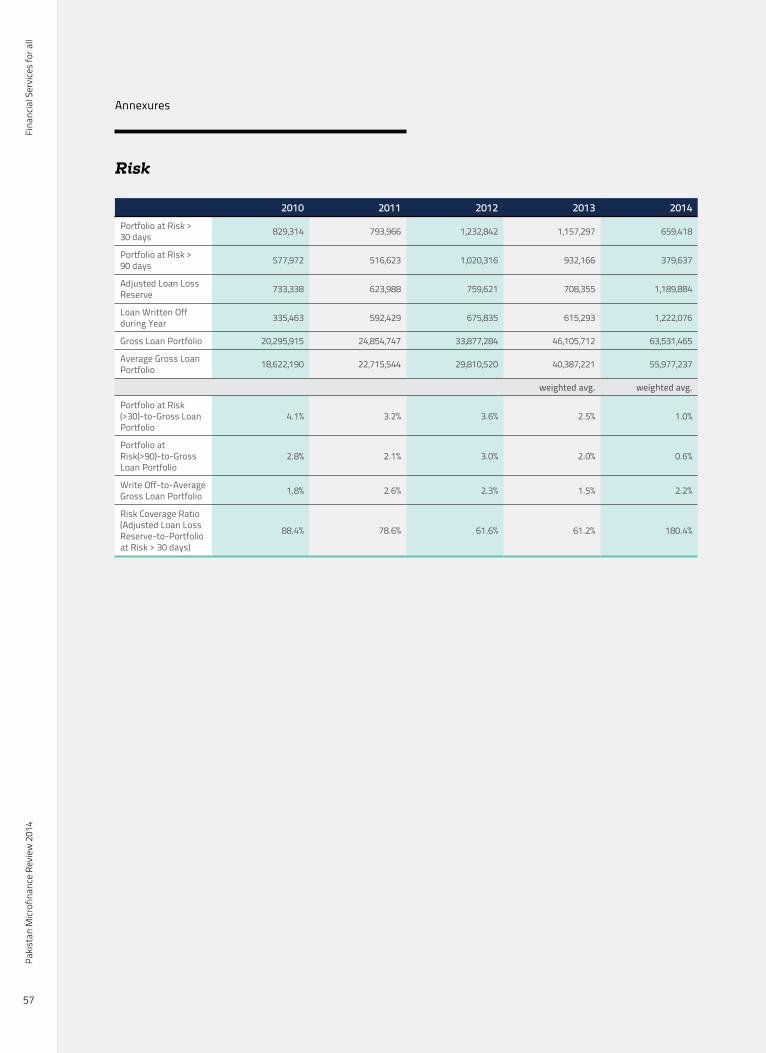

Credit Risk

Portfolio at Risk (PAR)>30 days decreased to 1.1 per-cent in 2014 as compared to 2.5 percent in 2013 (see Exhibit 2A.32). However, write-offs in the same peri-od increased to 2.3 percent from 1.1 percent. The in-crease in the write-offs was primarily due to increase

Exhibit 2A.30: Personnel Allocation Ratio Trend

2010 2011 2012 2013 2014

Personnel Allocation Ratio

40%

42%

44%

46%

48%

50%

52%

Exhibit 2A.31: Productivity of MFPs

50

100

150

200

250

300

350

400

2010 2011 2012 2013 2014

Loans per StaffDepositors per StaffLoans per Loan Officers

Fina

ncia

l Ser

vice

s fo

r all

Annu

al A

sses

smen

t of t

he M

icrof

inan

ce In

dust

ry

26

Industry Performance

in the ratio by one player, namely KF. Write off ratio stood at 16.5 percent for KF in 2014.

Overall, the PAR > 30 days continues to remain below the 5.0 percent cutoff point reflecting positive portfo-lio quality of the industry. However, it also may point towards the fact that players are risk averse and there is still plenty of opportunity in the market for growth in outreach.

Risk coverage ratio for the industry stood at 180.0 percent in 2014 up from 61.2 percent in the previous year. This high value for the risk coverage ratio was largely due to the requirement of national apex for its funded institutes to have loan loss provision equal to 5.0 percent of their total outstanding portfolio.

Conclusion

On the whole 2014 was a good year for the industry. It witnessed double digit growth in outreach in all areas including credit, deposits and insurance. The growth in the number of depositors was more pronounced due to the opening of a large number of m-wallet accounts. Female borrowers continued to constitute a majority of the borrowers and group lending re-

mained the dominant approach to lending. However, individual lending was becoming increasingly popular with practitioners. Majority of the lending activities continued to target the trade and agriculture sector. In addition, rural borrowers continued to account for the majority of the borrowers for the industry.

The total asset base of the industry stood over PKR 100 billion with MFBs making up nearly 70 percent of it. MFBs continued to rely on deposits as their main funding source whereas MFIs and RSPs are depen-dent on debt for on-lending. The industry continues to remain sustainable and out of 41 reporting orga-nizations, 35 MFPs are sustainable. Operating costs remained high for MFPs and there is room for im-provement in this area. In addition, the productivity indicators continued to exhibit an improving trend. PAR>30 days continued to remain below the 5 per-cent cut-off point reflecting positive portfolio quality. The industry continues to remain concentrated with nine MFPs dominating the market out of which five are MFBs.

On the whole the industry is poised for growth and can play a crucial role in the inclusive finance sphere.

2010 2011 2012 2013 2014

Portfolio at Risk >30 daysWrite OffCut off

1%

2%

3%

4%

5%

6%

7%

4.1%

1.8%

2.9%

2.6%

3.7%

2.3%

2.5%

1.5%

1.1%

2.3%

Exhibit 2A.32: PAR>30 Days & Write Offs Trend

Fina

ncia

l Ser

vice

s fo

r all

Paki

stan

Micr

ofin

ance

Rev

iew

201

4

27

Section 2

Introduction

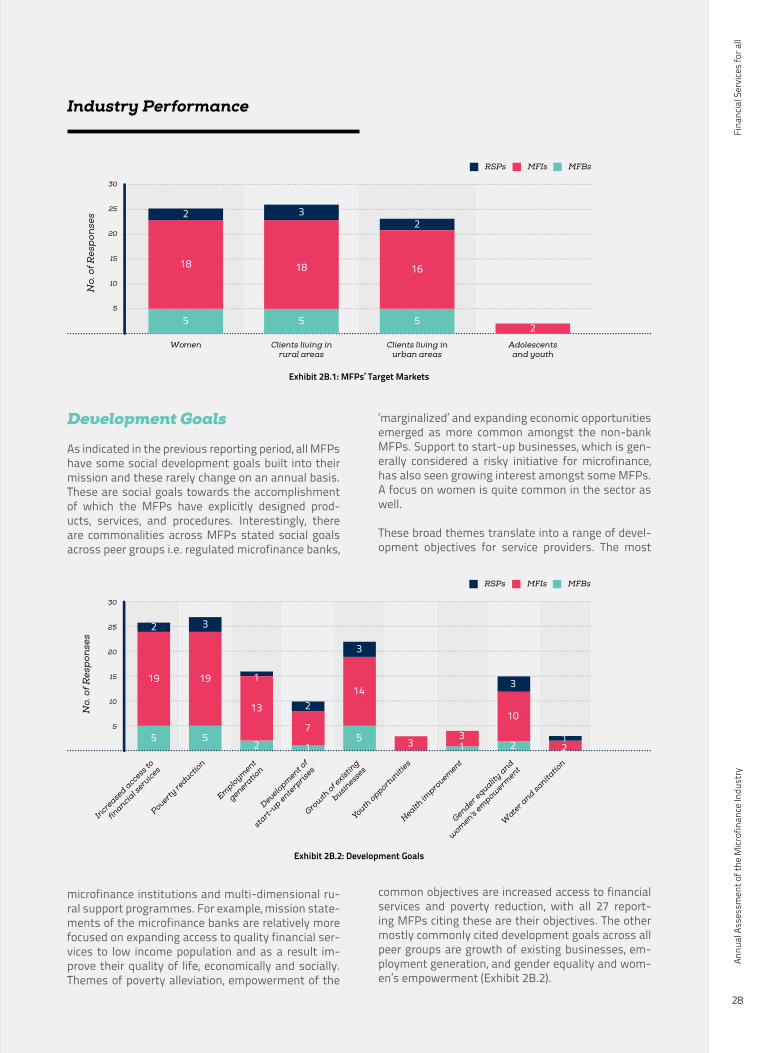

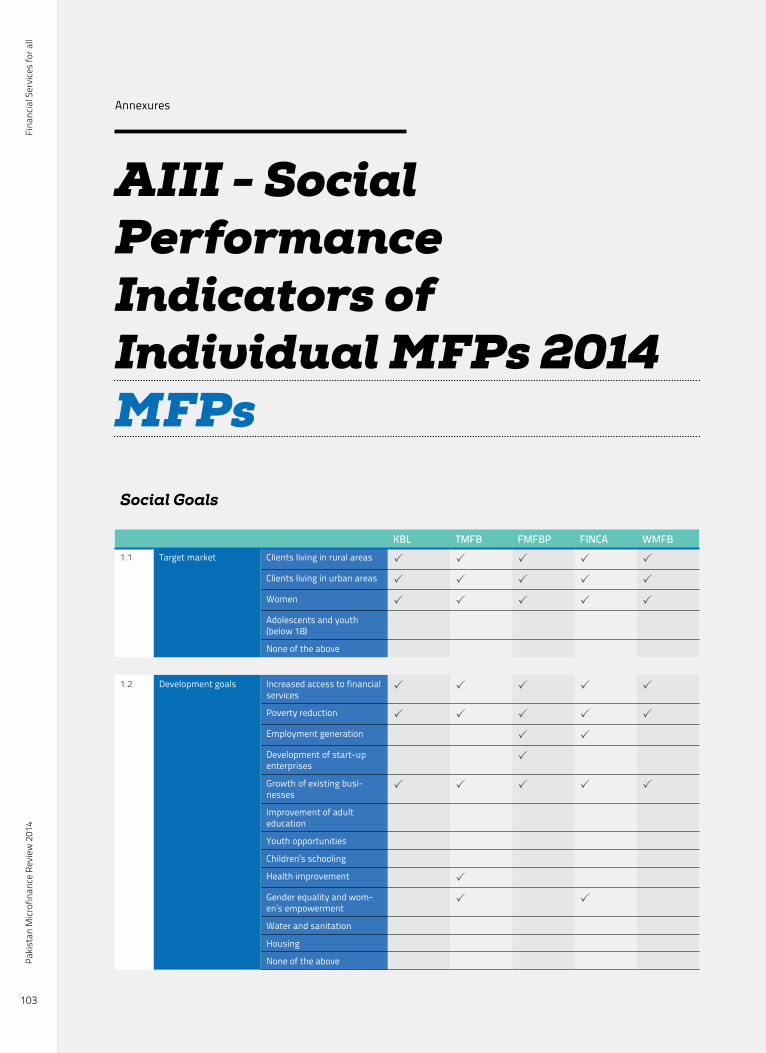

The last few years have seen a dedicated effort on behalf of the microfinance industry, both globally and in Pakistan, to focus on social performance (SP) along with financial sustainability. Microfinance is a double-bottom line industry, where sustainability is not an end in itself; but rather a means to achieving social goals. These goals can differ: some MFPs may have a vision of poverty alleviation, others of women empowerment, while yet others may be working for increasing access to formal financial services.

In order to better attain an institution’s intended goals, microfinance stakeholders around the world now believe that an MFP’s systems, activities and outputs must be deliberately geared towards its so-cial vision, to make the impact that the institution is aiming for. For an MFP, therefore, social performance management means focusing simultaneously on its financial and social bottom lines.