pakistan microfinance review...

TRANSCRIPT

Pakistan MicrofinanceReview 2015

A n A n n u a l A s s e s s m e n t o f

t h e M i c r o f i n a n c e I n d u s t r y

A n A n n u a l A s s e s s m e n t o f

t h e M i c r o f i n a n c e I n d u s t r y

Launch Ed it ion

F i n a n c i a l s e r v i c e s f o r a l l

2

Editorial Board Mr. Ghalib Nishtar Chairperson Editorial Board President, Khushhali Bank Limited (KBL) Syed Samar Husnain Executive Director, Development Finance Group State Bank of Pakistan (SBP) Mr. Blain Stephens COO and Director of Analysis Microfinance Information eXchange, Inc. (MIX) Ms. Gemma Stevenson Private Sector Development Advisor Finance, Markets and Jobs Team, Economic Growth Group Department for International Development (UK) Mr. Yasir Ashfaq Group Head, Financial Services Group, Pakistan Poverty Alleviation Fund (PPAF) Mr. Azfar Jamal Executive Vice President, Head Payment Services & E-Banking National Bank of Pakistan (NBP) Mr. Masood Safdar Gill Director Program, Urban Poverty Alleviation Program, National Rural Support Programme (NRSP)

PMN Team Mr. Ali Basharat Author and Managing Editor Mr. Ammar Arshad Co- Author and Data Collection Ms. Saba Abbas Co –Author and Data Collection Ms. Saquiba Aziz Data Collection

Highlights

Year 2011 2012 2013 2014 2015 Active Borrowers (in millions)

1.7 2. 0 2.4 2.8 3.6

Gross Loan Portfolio (PKR billions)

24.8 33.1 46.6 61.1 90.2

Active Women Borrowers (in millions)

0.9 1.3 1.4 1.6 2.0

Branches 1,550 1,460 1,606 1,747 2,754 Total Staff 14,202 14,648 17,456 19,881 25,560 Total Assets (PKR billions)

48.6 61.9 81.5 100.7 145.1

Deposits (PKR billions)

13.9 20.8 32.9 42.7 60.0

Total Debt (PKR billions)

38.3 24.9 26.9 31.1

44.5

Total Revenue (PKR billions)

10.1 12.5 17.3 24.3 32.8

OSS (percentage) 108.4 109.5 118.1 120.6 124.1 FSS (percentage) 100.5 107.5 116.5 119.6 121.0 PAR > 30 (percentage) 3.2 3.7 2.5 1.1 1.5 Year 2011 2012 2013 2014 2015

Acronyms and Abbreviations

AC &MFD Agriculture and Microfinance Division ADB Asian Development Bank AMRDO Al-Mehran Rural Development Organization AML Anti-Money Laundering BPS Basis Points CAR Capital Adequacy Ratio CIB Credit Information Bureau CDD Customer Due Diligence CGAP Consultative Group to Assist the Poor CGL Credit Guarantee Limits CNIC Computerized National Identity Card CPP Client Protection Principles CPI Consumer Price Index CPI Client Protection Initiative CPC Consumer Protection Code DFI Development Financial institute DFID Department for International Development, UK DPC Deposit Protection Corporation DPF Depositor’s Protection Fund ECA Eastern and Central Europe ESM Environment and Social Management EUR Euro FATF Financial Action Task Force FIP Financial Inclusion Program FINCA FINCA Microfinance Bank Ltd. FMFB The First Microfinance Bank Ltd. FSS Financial Self Sufficiency FY Financial Year G2P Government to Person GBP Great Britain Pound GDP Gross Domestic Product GLP Gross Loan Portfolio GNI Gross National Income GoP Government of Pakistan IAFSF Improving Access to Financial Services Support Fund IFAD International Fund for Agricultural Development IFC International Finance Corporation JWS Jinnah Welfare Society KBL Khushhali Bank Ltd. KF Kashf Foundation KIBOR Karachi Inter-Bank Offering Rate KP Khyber Pakhtunkhwa KYC Know Your Customer LCPS Low Cost Private Schools MIV Microfinance Investment Vehicle MIX Microfinance Information Exchange MCGF Microfinance Credit Guarantee Facility MCR Minimum Capital Requirement MENA Middle East and North Africa MFB Microfinance Bank MFCG Microfinance Consultative Group MF-CIB Microfinance Credit Information Bureau MFP Microfinance Providers

MFI Microfinance Institution MFT Microfinance Transparency MIS Management Information System MSME Micro, Small and Medium Enterprises MIV Microfinance Investment Vehicle MO Micro-Options NADRA National Database and Registration Authority NBMFI Non-Bank Microfinance Institutes NGO Non-Governmental Organization NFLP National Financial Literacy Program NFIS National Financial Inclusion Strategy NMFB Network Microfinance Bank Limited NPLs Non-Performing Loans NRDP National Rural Development Program NRSP National Rural Support Programme OPD Organization for Participatory Development OSS Operational Self Sufficiency P2P Person to Person P2G Person to government PAR Portfolio at Risk PBA Pakistan Banks Association PBS Pakistan Bureau of Statistics PKR Pakistan Rupee PMN Pakistan Microfinance Network PO Partner Organization PPAF Pakistan Poverty Alleviation Fund PPI Grameen Progress out of Poverty Index PRISM Program for Increasing Sustainable Microfinance PRSP Punjab Rural Support Program PTA Pakistan Telecom Authority ROA Return on Assets ROE Return on Equity RSP Rural Support Programme SBP State Bank of Pakistan SC The Smart Campaign SDS SAATH Development Society SECP Securities and Exchange Commission of Pakistan SPTF Social Performance Task Force SME Small and Medium Enterprise SRSO Sindh Rural Support Organization SRDO Shadab Rural Development Organization SVDP Soon Valley Development Program TMFB Tameer Microfinance Bank Ltd UBL United Bank Limited USD United State Dollar USSPM Universal Standards for Social Performance Management VDO Village Development Organization WPI Wholesale Price Index

Table of Contents

EditorialBoard 2

PMNTeam 3

Highlights 4

AcronymsandAbbreviations 5

TheYearinReview 9Macro-economyandMicrofinanceIndustry 9PolicyandRegulatoryEnvironment 10NationalFinancialInclusionStrategy(NFIS) 10Non-BankMicrofinanceCompanies(NBMFC)Regulations 11LimittoFinancingagainstGoldBackedLoans 12

MicrofinanceIndustryInitiatives 12BranchlessBanking 12MicrofinanceCreditInformationBureau(MF-CIB) 13EstimatingMicrofinanceMarketPotential 14Micro-EnterpriseLending 15PrimeMinisterInterestFreeLoanScheme 16CreditGuaranteeSchemeforSmall&MarginalizedFarmers 16ClientProtectionInitiative(CPI) 17

Conclusion 19

FinancialPerformanceReview 20SCALEANDOUTREACH 21ScaleandOutreach:Breadth 21ScaleandOutreach:Depth 26

FinancialStructure 29AssetBase 29AssetComposition 31FundingProfile 32

ProfitabilityandSustainability 33Productivity 36Risk 38CreditRisk 38

Conclusion 38

SocialPerformance 39Introduction 39

AnalysisoftheSector’sSPIndicators 39TargetMarket 40DevelopmentGoals 40PovertyTargeting 41PovertyMeasurementTools 42Governance&HR 43ProductsandServices:Financial 45

Credit 45Deposits 47Insurance 47OtherFinancialServices 49

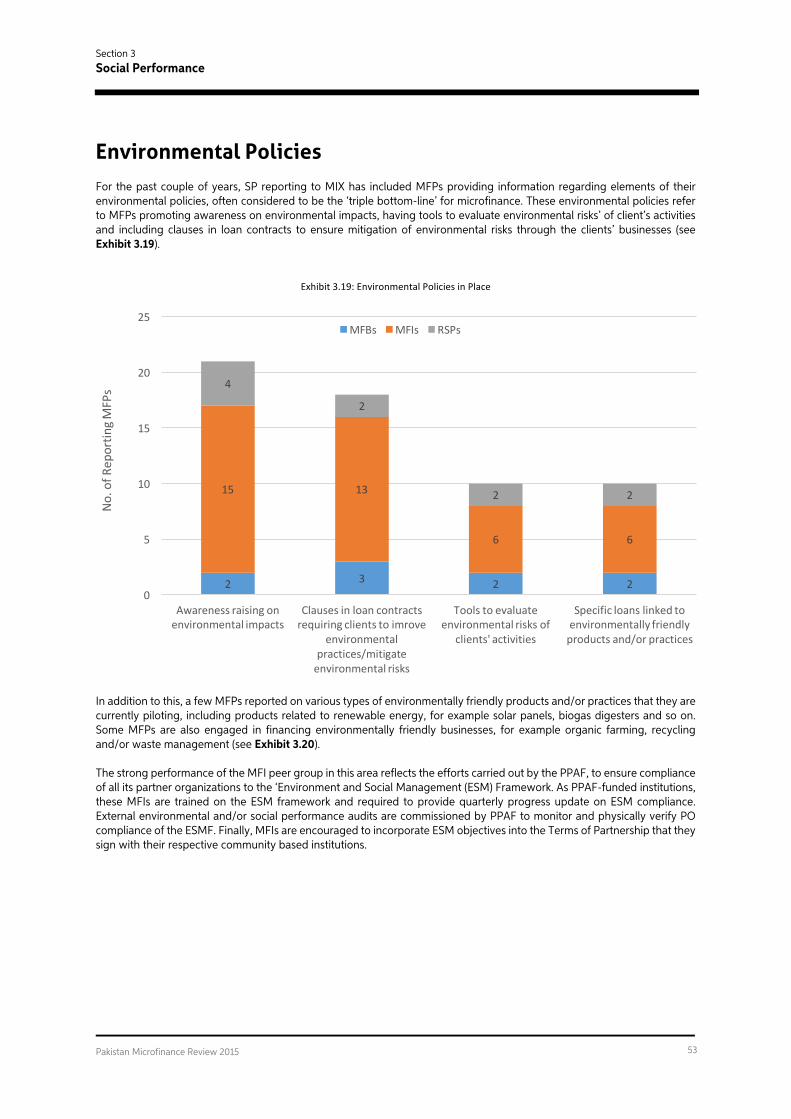

ProductsandServices:Non-Financial 49TransparencyofCost 50ClientProtection 52EnvironmentalPolicies 53

ChallengesandOpportunities 55RoleofMicrofinanceinFinancialInclusioninPakistan 55MainstreamingNon-BankMicrofinancePlayers 55CreditScoring 56MobileWallets 57Exploringnewhorizons:Servingnewmarkets 57HealthandMicrofinance 58FinanceforLowCostPrivateSchools(LCPS) 59

DepositProtectionFund;movingtowardsasecurefinanciallandscape 60DepositsMobilization:UntyingGordian’sKnot 60Funding 61SettingupofPakistanMicrofinanceInvestmentCompanyLimited(PMICL) 62

Section 1 The Year in Review

Pakistan Microfinance Review 2015

9

The Year in Review Microfinance industry witnessed continued growth and expansion in outreach in the year 2015. There were notable developments in the policy environment which can lead to stronger players and the sector can play a crucial role in furthering financial inclusion in the country. Major developments were witnessed on the policy and regulatory side like the launch of National Financial Inclusion Strategy (NFIS) and introduction of regulatory framework for Non-Bank Microfinance Institutes (NBMFI) by Securities & Exchange Commission of Pakistan (SECP). In addition, results of second Access to Finance Survey Results were shared. With the launch of NFIS, a roadmap for achievement of financial inclusion in the country has been laid out. A key challenge facing the microfinance industry has been the absence of regulatory framework for non-bank microfinance players. Now with the introduction of the rules and regulations for NBMFI a level playing field has been created in the industry and provides an opportunity for non-bank players to scale up their businesses. Improving security situation, low inflation and subsequent reduction in the policy rate by the central bank bode well for the industry. However, falling agriculture commodity prices can adversely affect the industry particularly those operating predominantly in the rural areas. A number of new initiatives were launched while existing ones were improved upon. One of the main initiatives last year was the re-estimation of microfinance market in the country. In addition, 2015 saw the completion of three years Client Protection Initiative (CPI), funded by State Bank of Pakistan (SBP) under the auspices of Financial Inclusion Program (FIP). Moreover, Microfinance Credit Information Bureau (MF-CIB) has become an essential component of credit approval process by practitioners and credit scoring models are being developed based on its data. Branchless banking continues to witness huge excel at all fronts simulated by an enabling environment. A number of microfinance banks (MFBs) have initiated lending to micro-enterprises. The Microfinance Growth Strategy 2020 launched by PMN during the year forecasts that the sector would require additional debt for on-lending of up to PKR 300 billion to reach up to 10 million borrowers. In order to meet the funding demands of the sector, PPAF, Department for International Development (DFID) through Karandaaz Pakistan and the German Development Bank KfW have joined hands to establish Pakistan Microfinance Investment Company Limited (PMICL), private-sector investment finance company. The major objective of the new entity is to attract commercial funding to serve increasing demand of those who are financially excluded and further improve the capability and capacity of the sector to absorb these funds. The NFIS also recognizes microfinance as an important instrument for increasing financial inclusion in the country and an important milestone of the strategy includes enhancing commercial funding for the microfinance sector through creation PMICL.

Macro-economy and Microfinance Industry Pakistan’s economy grew by 4.2 percent in the financial year 2015 which is the highest growth rate witnessed in the last seven years1. Despite improvement in the all the main macro-economic indicators like inflation, fiscal balance and current account balance and improvement in security situation persistent energy shortages and low investment rates remained a challenge for the economy and it could not meet the target of 5.1 percent growth for the year2. Despite the challenging external environment, the microfinance industry grew by nearly 20 percent in terms of outreach for the year 20153. Inflation measured by CPI continued to witness a downward trend in the year. The average inflation for the year stood at 4.5 percent as compared to 8.6 in the financial year 2014 at the back of falling oil and commodity prices. This created room for the central bank to cut the policy rate considerably4. Policy rate witness a decrease of 350 basis points in the year as

1 Annual Report 2014-15 (State of the Economy), SBP 2 Ibid 3 MicroWATCH, A quarterly outreach publication, PMN, Multiple Issues 4 Annual Report 2014-15 (State of the Economy), SBP

Section 1 The Year in Review

Pakistan Microfinance Review 2015

10

shown in the Exhibit 1.1 below to a 42 year low5. This will lower financing cost of retail players resulting in higher profitability. This low rate environment can be a good opportunity for players to tap debt capital markets for raising funds.

Exhibit 1.1: Discount rate, KIBOR and CPI Trend

While falling commodity prices have resulted in lower inflation and reduction in policy rate, it can have adverse implication for the growers. In many cases farmers have not been able to recover the cost of production reducing their ability to invest further in upcoming crops. This situation can have serious implications for the microfinance sector as more than 55 percent of its borrowers belong to rural areas6. Implications can be in form of diversion of loan towards consumption purposes or in extreme cases lead to delinquencies for the practitioners. Despite the policy rate touching a historical low, expansion in the private sector credit remained low as compared to the previous year7. Commercial banks continued to invest in the government securities in order to generate riskless returns. With most of the existing private sector concentrated towards manufacturing sector areas like SMEs and agriculture continue to remain unserved. In this situation, MFPs will continue find it challenging to raise funds from the commercial banks.

Policy and Regulatory Environment Pakistan’s overall regulatory environment continues to be ranked among the best globally8. Key developments were witnessed in the industry on the policy and regulatory domain in 2015. Last year saw the launch of National Financial Inclusion Strategy (NFIS) and roll-out of regulations for non-bank MFPs which was among the key challenges being faced by the sector.

National Financial Inclusion Strategy (NFIS) The year 2015 saw to the launch of National Financial Inclusion Strategy (NFIS) which has outlined a roadmap for financial inclusion in the country. Developed by the State Bank of Pakistan with active assistance The World Bank the strategy aims to “build a dynamic and inclusive financial sector to support Pakistan’s growth in 21 century”. The strategy will direct efforts and initiatives to expand and deepen financial inclusion during the course of five years (2015-2020) and has set objectives to be achieved through a comprehensive and well-thought action plan. 5 Ibid 6 MicorWATCH, A quarterly outreach publication, PMN, Issue 38, 2016 7 Annual Report 2014-15 (State of the Economy), SBP 8TheGlobalMicroscope2015:Theenablingenvironmentforfinancialinclusion,EIU,2015

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

FY11 FY12 FY13 FY14 FY15

Percen

tage

DiscountRate ConsumerPriceInflation(Average) 6-MonthsKIBOR

Section 1 The Year in Review

Pakistan Microfinance Review 2015

11

The state of financial inclusion in Pakistan depicts a dismal picture. Only 16 percent of the adult population can be categorized as banked and 23 percent of the population use formal financial services9. The situation worsens in rural areas where only 14 percent of the adult population is banked. In case of women only 11 percent are banked. The state of financial inclusion is no more evident when compared regionally as shown in the Table 1.1 below where Pakistan’s continues to lag behind. Despite sustained efforts by the policy makers, regulators and donors and enjoying an enviable enabling environment a lot more need to be done. In this regard, NFIS will play a crucial role in furthering financial inclusion in the country by coordinating the efforts of all the stakeholders by defining responsibilities among them and developing a comprehensive approach to promoting access and usage of formal financial services.

Table 1.1: Regional comparison of financial inclusion10 Countries Account Formalsavings FormalborrowingPakistan 13% 3% 2%India 53% 14% 6%Bangladesh 31% 7% 10%SriLanka 83% 31% 18%

The framework for action for the strategy identifies four targeted action or key drivers to achieve financial inclusion in the country. These four drivers are 1) promoting digital transactions and reaching scale through bulk payments; 2) expanding and diversifying access points; 3) improving capacity of financial services providers; and 4) increasing levels of financial capability. The success of these drivers is dependent upon the meeting four preconditions or key enablers which are

1. Public and private sector commitment to the NFIS 2. Enabling Legal and Regulatory Requirements 3. Adequate supervisory and judicial capacity 4. Financial payments, information and communication technology

Achievement of financial inclusion in the country requires efforts from a wide range of stakeholders and in order to direct their efforts a coordination mechanism has been developed which includes a NFIS Council to be chaired by the Finance Minister, a steering committee headed by Governor SBP and establishment of NFIS Secretariat.

Non-Bank Microfinance Companies (NBMFC) Regulations Over the last few years it has been felt the industry has reached a stage where regulatory cover needed to be extended to non-bank microfinance players. Based on lessons from regional countries particularly Post Andhra Pradesh Crisis in India, regulatory umbrella among other things protects the industry from external influences. In addition, the growth and increasing market share of microfinance banks (MFBs) had made evident the benefits of working as a regulated institute. Keeping this in view, PMN along with PPAF and other stakeholders had approached Securities & Exchange Commission of Pakistan (SECP) with aim of regulating the non-bank MFPs. Subsequently, a working group was formed which included representatives from PPAF, PMN, SBP and leading industry players with aim of developing rules and regulations. In the last quarter of 2015, Securities & Exchange Commission of Pakistan (SECP) issued regulations for non-bank microfinance companies by virtue of which non-bank microfinance players can now become regulated financial institutions. Necessary amendments were made in the Non-Bank Finance Company’s framework to allow for the establishment of Non-Bank Microfinance Institutes (NBMFIs). NBMFIs are recognized as a separate class in the NBMFC Rules 2003 as Investment Finance Services License for Microfinancing. In addition, comprehensive framework was issued by amending NBFC Regulations 2008. After this issuance of regulations only those entities that are licensed by SBP or SECP can conduct microfinance business. The regulations require all existing and new entities to become a company under the Companies Ordinance, 1984 and obtain a license for conducting microfinance business. Companies that are already registered as a company only need to obtain the license. In addition, the law requires non-bank MFPs to follow adhere to fit and proper criteria for top leadership and management, meet the minimum equity requirement of PKR 50 million and 70 percent of assets of the entity to be utilized for microfinance activities. Other salient features of the regulations are as follow:

9 www.a2f2015.com 10 The Global Findex Database 2014, The World Bank

Section 1 The Year in Review

Pakistan Microfinance Review 2015

12

1. General provision of 0.5 percent of the net outstanding microfinance portfolio 2. Maximum loan size for individuals is PKR 200,000 for a general loan and PKR 500,000. For microenterprises the

loan limit has been set at PKR 500,000 while overall exposure cannot exceed PKR 700,000. 3. Uniform provisioning requirement from 30 days to 180 days. 4. For loans above PKR 5,000 CIB inquiry is required.

These regulations allow for setting up both non-profit entities and for-profit entities. Giving MFIs an option to convert to for-profit entity which was previously enables them to attract equity investors and scale up their business substantially. Furthermore, the exposure limits for borrowers are the same as set by SBP for MFBs. The same goes for provisioning requirement as well. Also, now with this framework in place MFIs with a capital of above PKR 1 billion can also issue Certificate of Deposits (CODs) to raise funds. This is a watershed moment for the microfinance industry as it would mainstream non-microfinance institutes. Earlier microfinance institutes had been registered in multiple legal jurisdictions and working under a legal framework that can be categorized as ambiguous at best. Lastly, it is hoped that SECP will play a similar role as played by SBP in nurturing MFBs and interact frequently with the players for the mutual benefit of the industry.

Limit to Financing against Gold Backed Loans Financing against gold backed loans by Microfinance Banks (MFBs) had gained widespread popularity in the last few years. It had allowed MFBs to move from traditional group lending to individual lending and also, increase their loan sizes. This mode of financing drew its strength from the fact that gold and gold ornaments has been a traditional mode of savings among the masses and in times of emergency has been liquidated often at a deep discount. Obtaining a loan against this gold without having to liquidate provided a better alternative to potential borrowers and saw to its massive popularity. This product effectively transformed gold from a non-liquid asset into a liquid and earning asset. Pioneered by Tameer Microfinance Bank (TMFB), it was soon adopted by other MFBs. At this time up to 5 MFBs are dealing in this product. Percentage of gross loan portfolio (GLP) financed against gold by MFBs ranges from 20 percent to 55 percent. However, concerns were raised about the practices especially whether the loan were being utilized for consumption purpose rather than productive. Also, were the loan amounts being determined based on the value of the gold or based on the repayment capacity of the client? These concerns led to strengthening of the belief that gold backed loans were against the spirit of microfinance which promotes lending without physical collateral. This coupled by falling gold prices leading reduced value of collateral available with MFBs led the central bank to place a limit on financing against gold. SBP by virtue of amendment in the prudential regulation R-5 dealing with maximum loan size and eligibility of borrowers for MFBs placed a limit that aggregate loan exposure of a MFB cannot exceed 35 percent of its GLP11. Existing MFBs having an exposure of more than 35 percent were given two years to bring their portfolios in compliance with the above regulation. In addition, SBP also stressed that MFB’s to develop a collateral handling policy duly approved by their Board for managing the security, procedures and contingency planning for the gold collateral.

Microfinance Industry Initiatives The year saw a number of new initiatives being undertaken. Importantly, the year saw the re-estimation of microfinance market potential and successful completion of Client Protection Initiative (CPI).

Branchless Banking With a firmly established regulatory environment and a supporting institutional framework, the branchless banking sector of Pakistan continued to excel on all fronts in the calendar year 2015. The mandatory biometric SIM verification for all new and existing mobile phone customers in the same year, as instructed by Pakistan Telecommunication Authority (PTA), also played a crucial role in stimulating branchless banking activity.

11 AC & MFD Circular 02 of 2015, June 18, 2015, SBP

Section 1 The Year in Review

Pakistan Microfinance Review 2015

13

As of 30th September 2015, the value of branchless banking transactions stood at PKR 526 billion as compared to PKR 376 billion in the same period previous year12 – depicting an increase of 40 percent. Moreover, the number of branchless banking transactions, for the first time, crossed the 100 million mark resting at 101 million as of 30th September, 2015. It is important to note that approximately 5 percent of the 101 million transactions were carried out by agents for liquidity management, whereas, the remaining 95 percent were customer oriented transactions (which include transactions through over-the-counter and m-wallets). However, branchless banking agents had a significant share (of 40 percent) in the value of transactions – PKR 208 billion worth of transactions were conducted for liquidity management. In terms of customer oriented transactions, over-the-counter transactions amounted to 69 percent of the total number of transactions and 71 percent of the total value of transactions. Fund transfers through CNIC (sending and receiving) remained the top contributor in terms of volume and value of transactions with a share of 33 percent and 44 percent respectively. Bill payments (utility and internet) had the second largest share in terms of both, volume (29 percent) and value (18 percent) within customer oriented transactions12. The branchless banking platform is also proving to be an effective instrument in channelizing the government-to-person payments in salary disbursements, pension, and tax collection services. An amount of PKR 22 billion was disbursed to 4.5 million beneficiaries during the third quarter of 2015 as compared to PKR 16 billion disbursed to 5.5 million beneficiaries during the same quarter previous year. Majority of the G2P payment beneficiaries are associated with the Benazir Income Support Program (BISP), followed by internally displaced people. Lately, branchless banking operators have also introduced innovative Person-to-Government (P2G) payment products for collection of taxes, traffic penalties and other payments to government agencies. Mobile network operators are partnering with public entities to enhance the scope of digital financial services that can be accessed quickly and at the convenience of the users, thus facilitating both government and the individuals. Telenor’s EasyPaisa was the first service provider to set foot in this domain by offering the option to pay for traffic penalties through the branchless banking platform – including mobile wallets. Mobilink’s Mobicash has recently introduced a product where consumers can pay for their passport fees through any Mobicash agent or via their m-wallet account.

Microfinance Credit Information Bureau (MF-CIB) MF-CIB is a key part of the microfinance industry infrastructure in Pakistan. Established with the assistance of International Finance Corporation (IFC), Department for International Development (DFID) and Pakistan Poverty Alleviation Fund (PPAF), the credit registry is being increasingly used as an important tool of risk mitigation tool by the players. The bureau aims to curtail the practice of multiple borrowing leading to over-indebtedness, moral hazard and adverse selection in the sector. In addition, the bureaus ability to generate both positive and negative reports allows for utilizing credit histories Since its nationwide roll-out in 2012, the bureau is now an inseparable part of the ecosystem with eighty percent of the players making inquiries from the bureau. As seen in the Exhibit 1.2 below, there has been an obvious increase in inquiries being generated as compared to previous year with maximum number of inquiries being generated per month reaching 198 thousand in December 2015.

12 Branchless Banking Newsletter, Issue 17, 2015, State Bank of Pakistan (SBP)

Section 1 The Year in Review

Pakistan Microfinance Review 2015

14

Exhibit 1.2: Month on Month Comparison of MF-CIB Inquiries13

With the advent of the regulations for non-bank microfinance players requiring an inquiry to be generated for loans over PKR 5000 and continued increase in outreach we are likely to see increase in the inquires being generated. The bureau has currently holds over 9.5 million records and efforts are afoot to develop a credit scoring model based on the data sourced from it. Credit scoring will assist lenders in determining who will get loan, how much loan amount they should get and also help in determining the risk in lending. Since the score is based on actual data its remains a reliable assessment of a client. Moreover, it will assist members in customer acquisition and retaining good client. In addition, bad debtors can be isolated and monitored closely. Lastly, credit scoring can also lead players to apply risk based pricing mechanism by rewarding good client by charging them less and charging a higher rate to risky borrowers. With MF-CIB taking an increasingly important role in the context of microfinance industry it is natural that the microfinance client’s need to be educated about the role and importance of bureau in the lending process. How will good credit history be rewarded? What will be the effect of taking loans from multiple lenders? How badly will be the impact of default or delayed payments on the credit worthiness of a client? In order to address issues like these a literacy program has been launched for the microfinance borrowers by PMN in collaboration with IFC. The program aims to develop know how of the borrowers about credit reports being generated by the MFPs and how they should manage their credit histories.

Estimating Microfinance Market Potential14 While there is reliable, up-to-date and periodic information available on industry benchmarks and indicators, there is an information gap related to the potential size of the market. The current figure of 27 million individual borrowers based on PMN’s old methodology was dated and hasn’t been revised since 2007. A revised and up-to-date estimation will provide invaluable information for the donors, policy makers and most importantly, practitioners. This old methodology lacked the relevance of the parameters and dataset to the present day outlook of the industry. PMN’s proposed/ current methodology uses a much robust and up-to-date framework to calculate the market potential for microcredit. A nationally representative dataset is used with supporting parameters or filters that are supported by rationale or underlying assumptions. This potential is further sliced into different segments such as occupation, labor market status and gender. Using an up-to-date nationally representative survey data (HIES-PSLM 11-12),PMN has built a pyramid model whose main parameters include willingness to demand a loan in the past or propensity to borrow in the future, income ranges and credit worthiness. There is anecdotal evidence which shows that willingness or propensity to take a loan could be a good starting point whilst calculating a market potential. The dataset contains information on socio-economic indicators that are periodically available, credible, and easily accessible and has the level of detail that would allow segmentation. The survey

13 Datacheck 14 Estimating Potential Market Size for Microcredit in Pakistan, MicroNOTE No. 27, Dec 2015

0

50,000

100,000

150,000

200,000

250,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MF-CIBInqu

iries

2014 2015

Section 1 The Year in Review

Pakistan Microfinance Review 2015

15

is carried out by the Pakistan Bureau of Statistics (PBS) every alternative year and contains information on socio-economic factors such as income, expenditure and employment status. The framework encompasses the following steps: Those individuals who have an outstanding loan from any source at the time of the survey or have borrowed in the year immediately before are selected, individuals in the age bracket of 18-65, an average loan range of PKR 20, 00 – 150,000 is selected (along with another loan range for a sensitivity analysis) and finally the total potential is divided into different segmentation. PMN has used statistical software using all these parameters and filters to calculate the total potential. The total potential market for microcredit has been calculated to be at 17 million individual borrowers. Furthermore, the old methodology did not have an estimate for ‘Micro-enterprises’. Using the same dataset(HIES 2011-12), our proposed framework for estimating microenterprises is built around a section of the survey that contains data on household heads who are either a proprietor or partner in a non-agricultural, non-financial establishment, business or shop(mobile or fixed) that employed less than 10 persons any given time during the year. The information in HIES is limited to certain enterprises that are related to manufacturing, mining, quarrying, transportation, wholesale/retail trade, hospitality, construction and other service related businesses. However, there are some enterprises that are not captured in HIES which includes agricultural, livestock and fisheries. The total market potential estimated for microenterprises has been estimated to be 6.5 million enterprises. Agriculture activities in Pakistan take mostly in the form of farming and livestock rearing. PMN uses a framework whereby it used land sizes defined by the Federal Land Commission throughout Pakistan. Since the activities carried out on the farm by household are indivisible and Pakistan hasn’t reached a level of mechanization that would enable specialization to take place at a scale, we proposed that the unit of measurement to be the farm size under any of three predominantly prevalent land tenure arrangements in Pakistan namely owner cultivated, share cropped and tenant farming types. As such, we use subsistence and economic land holdings across all provinces to be used as cut-off for small and micro agricultural farms. The total potential for farm microenterprises comes out to be 1 million enterprises.

Micro-Enterprise Lending Enterprise lending has been in vogue ever since State Bank of Pakistan (SBP) allowed MFBs to upscale their loan sizes from PKR 150 thousand to PKR 500 thousand through amendments in Prudential Regulations in 2012. Inability of commercial banks to scale down to serve the lower end of SME or very Small Enterprises (VSE) and similarity of dynamics with microfinance led to policy makers to rely on the microfinance industry to serve these markets. At present MFBs can lend up to 40 percent of the GLP in microenterprises. VSE or microenterprises make up nearly 99 percent of the SMEs in the country and play a crucial role in income and employment generation15. The segment is viewed as more stable as compared microfinance income having a higher degree of formalization, a designated business premises and possess some fixed assets. Lending to this particular segment allows, MFPs to retain graduating clients who have grown to size where micro-loans cannot meet their funding needs and diversify into a newer market segment. In addition, it provides an opportunity to increase profitability as enterprise loans have lower operational costs as compared to microloans and allows for risk based pricing of loans. Currently, eight out of ten MFBs have started lending into this segment. Out of these eight six are at pilot stage. Consolidated figures for the seven MFBs lending to this particular segment are shown in the Table 1.2.

Table 1.2: Trend of Micro-Enterprise Lending by MFBs16 Year 2013 2014 2015NumberofLoans 136 2,185 12,612GLP 33,902,858 530,587,461 3,061,824,879AverageLoanSize 249,286 242,832 242,771PAR>30Days 0% 1.0% 1.3%

According to a survey conducted by IFC regarding lending to microenterprises by MFBs, most players have built the capacity of their staff to serve this particular segment. In addition, separate risk assessment methodologies and IT system has been developed. Moreover, specialized staff has been dedicated for enterprise lending grouped in a separated division. Generally, 15 Federal Bureau of Statistics, Government of Pakistan, 2005 16 Figures obtained from 7 MFBs

Section 1 The Year in Review

Pakistan Microfinance Review 2015

16

MFBs are not extending loans to microenterprises through all of their branches and tend to serve same sectors as microfinance clients. Most of the client belong to the transport sector and followed by services and retail. Potential clients are acquired in the same manner as microfinance client and traditional delivery channels are commonly used. However, there is a growing awareness among the players to utilize branchless banking channels for distribution. Key challenges include perceptions about ability of loan officers and concern over lack of capacity to analyze micro-enterprises.

Prime Minister Interest Free Loan Scheme The Government of Pakistan (GoP) launched an interest-free microloan scheme in 2014 to address the issues of poverty and rising unemployment in the country. Under the scheme, PKR 3.5 billion were allotted from the federal budget to facilitate the poor and destitute segments of the population in generating livelihood. However, in order to safeguard the interest of the MFPs it was decided that the funds under this scheme would be routed through the national apex, PPAF and would only be extended in Union Councils that have low or no penetration of conventional microfinance. As of December, 2015, PKR 2.25 billion have been disbursed under the scheme to approximately 110,000 beneficiaries – out of which 66,000 were female and 44,000 were male applicants17. These interest free loans are being made available to men and women from households with a score of up to 40 on the Poverty Score Card (PSC) and with little or no access to banks or microcredit institutions. Most of the loans have been utilized in the livestock sector, followed by business and trading, services and agriculture. Twenty-four MFPs have partnered with PPAF in extending interest free loans under the PM interest free loan scheme. It is hoped that the scheme would lead to over 1 million additional active borrowers over the next three years. Since this scheme is targeted toward those areas where conventional microfinance has little or no penetration, it provides MFPs an opportunity to expand outreach in newer geographic markets. Moreover, it has the potential to allow for borrowers of interest free loans to graduate to conventional microfinance. This is ensured as the interest free loan would be provided only once to an individual and after the completion of the first cycle he/she would be eligible only for a conventional microfinance loan.

Credit Guarantee Scheme for Small & Marginalized Farmers In 2015, the government of Pakistan launched a credit guarantee scheme for small and marginalized farmers to ensure greater access to bank loans for production purposes. The scheme will provide 50 percent risk coverage against the principal outstanding on loans to small and marginalized farmers by commercial, specialized and microfinance banks. The federal government has made an initial allocation of PKR 1 billion in the federal budget FY 2015-16, for the scheme which may be topped up annually. The allocated funds will be used to create a guarantee fund for farmers having up to 5 acres irrigated and 10 acres non-irrigated land holdings. The objective of the scheme is to encourage participating commercial, specialized and microfinance banks to lend collateral-free to small and marginalized farmers to meet their working capital requirements. Credit Guarantee Limits (CGLs) will be assigned to all financial institutions involved in agriculture financing based on their exposure and potential in agricultural credit disbursements. The scheme is also open to all those banks which are not currently involved in agriculture financing by expressing their willingness to participate in the said scheme. The scheme aims to benefit 300,000 farmer households with production loans up to PKR 100,000 and the loan tenor will be based on cropping cycle up to a maximum period of one year18. The scheme will exclusively apply to small and marginalized farmers across the country owning/cultivating irrespective of land ownership. According to SBP, as per Agriculture Census 2010, 5.35 million farm households (out of total 8.3 million) have land-holding up to five acres in Pakistan. These small farmers have a significant share in the national agricultural output. Despite their significance, the small and marginalized farmers face difficulties in accessing formal credit due to small landholding and lack of collateral. As a result, they are forced to borrow from informal sources on unfair terms. Therefore, the scheme has been designed to enhance access of small and marginalized farmers to formal credit.

17 http://www.pmifl.com.pk/ 18 Credit Guarantee for Small & Marginalized Farmers (CGSMF) Circular No.1, State Bank of Pakistan

Section 1 The Year in Review

Pakistan Microfinance Review 2015

17

Client Protection Initiative (CPI)

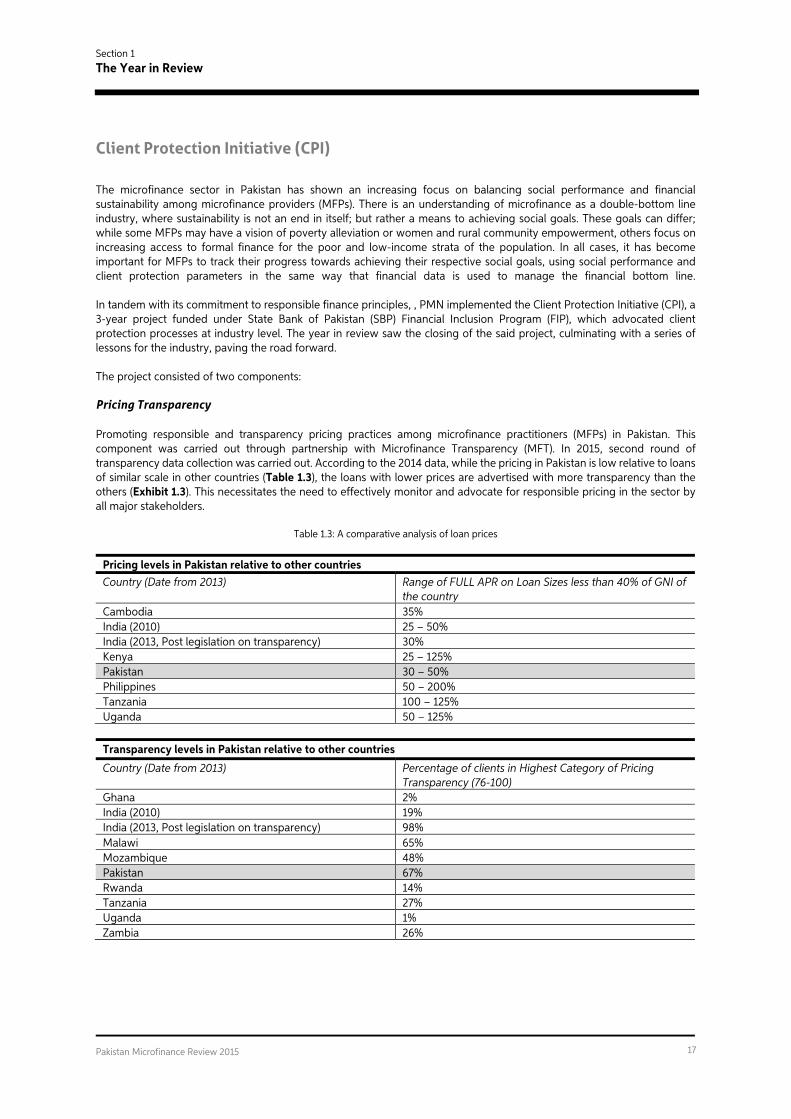

The microfinance sector in Pakistan has shown an increasing focus on balancing social performance and financial sustainability among microfinance providers (MFPs). There is an understanding of microfinance as a double-bottom line industry, where sustainability is not an end in itself; but rather a means to achieving social goals. These goals can differ; while some MFPs may have a vision of poverty alleviation or women and rural community empowerment, others focus on increasing access to formal finance for the poor and low-income strata of the population. In all cases, it has become important for MFPs to track their progress towards achieving their respective social goals, using social performance and client protection parameters in the same way that financial data is used to manage the financial bottom line. In tandem with its commitment to responsible finance principles, , PMN implemented the Client Protection Initiative (CPI), a 3-year project funded under State Bank of Pakistan (SBP) Financial Inclusion Program (FIP), which advocated client protection processes at industry level. The year in review saw the closing of the said project, culminating with a series of lessons for the industry, paving the road forward. The project consisted of two components: Pricing Transparency Promoting responsible and transparency pricing practices among microfinance practitioners (MFPs) in Pakistan. This component was carried out through partnership with Microfinance Transparency (MFT). In 2015, second round of transparency data collection was carried out. According to the 2014 data, while the pricing in Pakistan is low relative to loans of similar scale in other countries (Table 1.3), the loans with lower prices are advertised with more transparency than the others (Exhibit 1.3). This necessitates the need to effectively monitor and advocate for responsible pricing in the sector by all major stakeholders.

Table 1.3: A comparative analysis of loan prices

Pricing levels in Pakistan relative to other countries Country (Date from 2013) Range of FULL APR on Loan Sizes less than 40% of GNI of

the country Cambodia 35% India (2010) 25 – 50% India (2013, Post legislation on transparency) 30% Kenya 25 – 125% Pakistan 30 – 50% Philippines 50 – 200% Tanzania 100 – 125% Uganda 50 – 125%

Transparency levels in Pakistan relative to other countries

Country (Date from 2013) Percentage of clients in Highest Category of Pricing Transparency (76-100)

Ghana 2% India (2010) 19% India (2013, Post legislation on transparency) 98% Malawi 65% Mozambique 48% Pakistan 67% Rwanda 14% Tanzania 27% Uganda 1% Zambia 26%

Section 1 The Year in Review

Pakistan Microfinance Review 2015

18

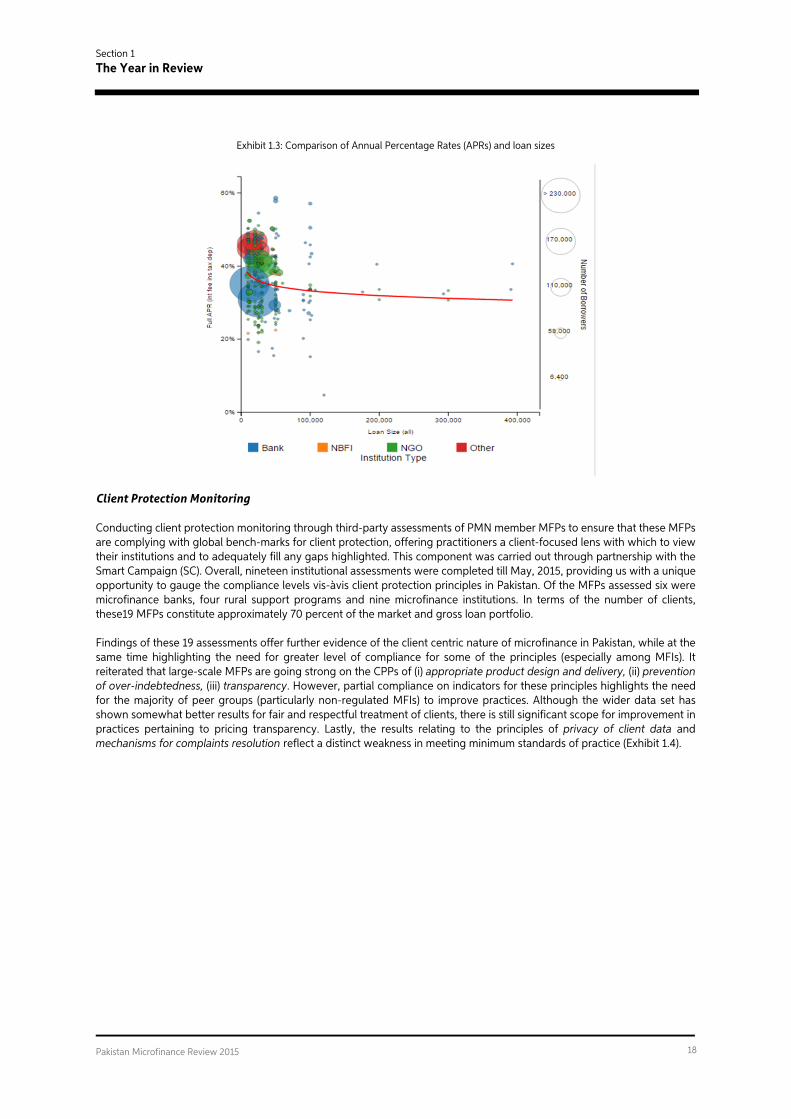

Exhibit 1.3: Comparison of Annual Percentage Rates (APRs) and loan sizes

Client Protection Monitoring Conducting client protection monitoring through third-party assessments of PMN member MFPs to ensure that these MFPs are complying with global bench-marks for client protection, offering practitioners a client-focused lens with which to view their institutions and to adequately fill any gaps highlighted. This component was carried out through partnership with the Smart Campaign (SC). Overall, nineteen institutional assessments were completed till May, 2015, providing us with a unique opportunity to gauge the compliance levels vis-àvis client protection principles in Pakistan. Of the MFPs assessed six were microfinance banks, four rural support programs and nine microfinance institutions. In terms of the number of clients, these19 MFPs constitute approximately 70 percent of the market and gross loan portfolio. Findings of these 19 assessments offer further evidence of the client centric nature of microfinance in Pakistan, while at the same time highlighting the need for greater level of compliance for some of the principles (especially among MFIs). It reiterated that large-scale MFPs are going strong on the CPPs of (i) appropriate product design and delivery, (ii) prevention of over-indebtedness, (iii) transparency. However, partial compliance on indicators for these principles highlights the need for the majority of peer groups (particularly non-regulated MFIs) to improve practices. Although the wider data set has shown somewhat better results for fair and respectful treatment of clients, there is still significant scope for improvement in practices pertaining to pricing transparency. Lastly, the results relating to the principles of privacy of client data and mechanisms for complaints resolution reflect a distinct weakness in meeting minimum standards of practice (Exhibit 1.4).

Section 1 The Year in Review

Pakistan Microfinance Review 2015

19

Exhibit 1.4: Overall compliance to the CPPs by the Pakistan microfinance sector

Despite an overall positive trend of client-centric processes, further work needs to be done in each CPP, and in some more than others, to bring the compliance levels at par with the global standards of client protection.

Conclusion Microfinance industry in Pakistan has grown at a double digit rate over the last few years. We anticipate that trend will likely continue in the coming years. With NFIS in place, industry is geared up to play an important role in furthering the financial inclusion agenda in the country. In addition, with regulations in place for non-bank microfinance players a key impediment in the growth and development has been addressed. Current macroeconomic stability and positive indictors provide a supportive environment for the practitioners. While easing of the monetary policy will likely result in bringing down the borrowing costs and increase profitability. However, low uptake in private sector credit and continued interest of commercial bank in investing in government papers despite diminishing yields, will likely make it difficult to borrow for players to borrow from commercial banks. However, the prevailing low interest environment provides players a perfect opportunity to explore capital markets for both debt and equity. Overall, the sector is poised for growth backed by an enabling environment and strong industry infrastructure that includes MF-CIB and branchless banking operations. Government backed credit schemes like the PM Interest Free Loan Scheme and Credit Guarantee Scheme for Small and Marginalized farmers allow for expanding outreach in newer areas and segments while mitigating risks. Responsible finance initiatives ensure client protection continues to remain a priority for the sector. In addition, microfinance players are positioning themselves to tap the lower end of the SME segment. Moreover, the creation of PMICL is a key development in line with the Microfinance Growth Strategy 2020 and the NFIS. PMICL will provide the much-needed liquidity to the microfinance sector to reach out to 10 million clients by 2020, contributing towards the overall objective to increase financial inclusion in the country.

0%

20%

40%

60%

80%

100%

AppropriateProductDesign&DeliveryChannels

PreventionofOver-Indebtedness

Transparency

ResponsiblePricingFair&RespectfulTreatmentofclients

PrivacyofClientData

MechanismsforComplaintsResolution

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

20

Financial Performance Review This section provides a detailed analysis of the financial performance of Pakistan's microfinance industry in 2015. Performance has been assessed on three levels: industry wise, across peer groups and institution wise. The analysis is backed by 88 financial indicators, calculated from the audited financial statements of the reporting organizations. These indicators have been compared across time and regions to develop a reliable and fair assessment of sector. Detailed financial information is provided in the Annex A-I and A-II of the PMR. Aggregate data has been reproduced for five years, whereas, the peer group and institution specific data has been made available only for the year 2015. A total of 44 MFPs submitted their audited financial statements for PMR 2015. During the period, three new respondents provided their dataset for the first time. For a complete list of reporting organizations refer to Annex B. Industry players are categorized into three groups for benchmarking and comparison purposes: Microfinance Banks (MFBs), Microfinance Institutions (MFIs) and Rural Support Programmes (RSPs). See Box 2.1 for detailed definitions.

Box 2.1: Peer Groups

Microfinance Institution: A non-bank non-government organization (NGO) providing microfinance services. Organizations in this group are registered under a variety of regulations, including the Societies Act, Trust Act, and the Companies Ordinance. The MFI peer group includes local as well as multinational NGOs such as BRAC-Pakistan and ASA-Pakistan. As of now these organizations are in process of transformation into Non-Bank MFI under the new regulatory framework laid out for non-bank players by SECP.

Microfinance Bank: A commercial bank licensed and prudentially regulated by the SBP to exclusively service the microfinance market. The first MFB was established in 2000 under a presidential decree. Since then, seven MFBs have been licensed under the Microfinance Institutions Ordinance, 2001. MFBs are legally empowered to accept and intermediate deposits from the public. Currently there are 11 MFBs operating in the country.

Rural Support Programme: An NGO registered as a non-profit company under the Companies Ordinance. An RSP is differentiated from the MFI peer group based on the purely rural focus of its credit operations. As of now these organizations are in process of transformation into Non-Bank MFI under the new regulatory framework laid out for non-bank players by SECP.

The distribution of respondents (number of reporting organizations) by peer group is given in Exhibit 2.1. The MFI peer group is comprised of the largest number of respondents followed by MFBs and then RSPs.

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

21

Exhibit 2.1: Distribution of respondents by peer groups

SCALE AND OUTREACH This section focuses on outreach indicators to provide performance analysis of the industry in terms of credit growth and composition, deposit mobilization, depth of outreach and gender.

Scale and Outreach: Breadth Microfinance borrowers increased by 21 percent from 2.99 million in 2014 to 3.63 million by 2015 as shown by the Exhibit 2.2. The GLP increased by 43 percent from PKR 63.53 billion to PKR 90.10 billion in the same time period. Among the players, Akhuwat added 170 thousand new borrowers; NRSP added 97 thousand to its tally while NRSP Bank added another 63 thousand over last one year.

Exhibit 2.2: Growth in Number of Active Borrowers and GLP

The market continues to be dominated by 9 MFPs in term of outreach and account for 80 percent of the active borrowers. The largest provider of micro-credit is NRSP with 589 thousand active borrowers followed by KBL with 520 thousand borrowers while at third place is Akhuwat with 405 thousand as shown in the Exhibit 2.3.

29

10

5

MFI MFB RSP

0

20

40

60

80

100

0.000.501.001.502.002.503.003.504.00

2011 2012 2013 2014 2015

GLPinPKR

Billions

Activ

ebo

rrow

ersinmillions

Activeborrowers GLP

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

22

Exhibit 2.3: Active Borrowers of Largest MFPs

Among the peer groups MFBs continues to lead but their overall share declined from 42 percent in 2014 to 39 percent in 2015 as shown in Exhibit 2.4. In the same time period, the share of MFIs increased from 31 percent to 38 percent. This increase is mostly at the back of the growth in outreach witnessed by Akhuwat in the last one year. Despite strong performance the RSPs, there share also declined from 27 percent to 23 percent in the last one year.

Exhibit 2.4: Share in Active Borrowers by Peer Group

In terms of Gross Loan Portfolio (GLP), MFBs accounted for 61 percent of the share followed by MFIs with a 23 percent share and RSPs with a 16 percent as shown in Exhibit 2.5. Despite accounting for 39 percent of the outreach, MFBs account for 61 percent of the industry’s GLP because of larger loan size relative to other peer groups.

590

521

406

247

287

263

258

177

106

492

469

236

231

227

221

194

149

110

0 100 200 300 400 500 600 700

NRSP

KBL

Akhuwat

KF

TMFB

ASA-P

NRSPBank

FMFB

TRDP

ActiveBorrowersinThousands

2014 2015

44% 39% 40% 42% 39%

28% 34% 35% 31% 38%

28% 27% 25% 27% 23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015

MFB MFI RSP

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

23

Exhibit 2.5: Share of GLP by Peer Group

The total GLP for the industry stood at PKR 90.1 billion up from PKR 63 billion in the previous year. Out of the total GLP, MFBs share stood at PKR 55.4 billion whereas MFIs and RSPs accounted for PKR 21.0 billion and 13.7 billion, respectively (see Exhibit 2.6).

Exhibit 2.6: GLP by Peer Groups

In terms of GLP, KBL continues to remain the largest provider of credit with a GLP of 17.5 billion. It is followed by TMFB with a GLP of 12.2 billion as shown in the Exhibit 2.7. At third place is NRSP with a GLP of PKR 10.1 billion. The top ten MFPs combine to make up 82 percent of the industry’s GLP.

59% 57% 60% 58% 61%

20% 23% 22% 24% 23%

21% 20% 18% 18% 16%

0%10%20%30%40%50%60%70%80%90%100%

2011 2012 2013 2014 2015

MFB MFI RSP

14.6 18.728.1

36.855.4

5.07.6

10.2

15.3

21.0

5.36.7

8.4

11.4

13.7

-

10

20

30

40

50

60

70

80

90

100

2011 2012 2013 2014 2015

PKRinBillions

MFB MFI RSP

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

24

Exhibit 2.7: GLP by 10 Largest MFPs

Total deposits for the industry segment stood at PKR 60 billion in 2015 as compared to PKR 42.7 billion in 2014 showing an increase of 42 percent over the year as shown in the Exhibit 2.8. In the same time period the number of depositors increased to 10.6 million from 5.7 million witnessing a phenomenal growth of 88 percent. This increase can have attributed to growth in the number of m-wallet accounts. As a result of Government of Pakistan’s policy of biometric verification of all mobile sim card holders, now m-wallet accounts can now be opened by simple text message. This window has enabled branchless banking operators to open m-wallet accounts in convenient manner and the subsequent growth witnessed is a proof of this fact. TMFB has the largest number of deposit accounts with 4.95 million depositors. It is followed by WMFB with 3.1 million accounts and KBL at third with 1.1 million accounts. Both TMFB and WMFB have been allowed to open m-wallet accounts using USSD string and bulk of the deposit accounts are m-wallet accounts.

Exhibit 2.8: Growth in deposits and number of depositors

Overall, TMFB has the largest deposit base with PKR 15.6 billion among the MFBs up from 12.3 billion in the previous year; followed by KBL with PKR 12.2 billion and FMFB at third place with PKR 9.96 billion as shown in the Exhibit 2.9.

17.5

12.2

10.1

9.1

5.6

5.5

4.8

4.6

3.8

1.3

12.2

9.0

7.7

5.2

4.5

4.0

2.5

3.8

2.7

1.2

- 5 10 15 20

KBL

TMFB

NRSP

NRSPBank

FMFB

FINCA

Akhuwat

KF

ASA-P

BRAC-P

Billions

2014 2015

0

10

20

30

40

50

60

70

0

2,000

4,000

6,000

8,000

10,000

12,000

2011 2012 2013 2014 2015 Depo

sitso

utstandinginbillions

Depo

sitorsinthou

sand

s

Depositors DepositsOutstanding

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

25

Exhibit 2.9: Deposit Growth by MFB

Despite the impressive growth in the deposit size by MFBs the overall deposit to GLP ratio for the industry continued to exhibit a decreasing trend as show in the Exhibit 2.10. The deposit to GLP ratio for MFBs decreased to 108 percent from last year’s 116 percent. This point’s towards the fact that the credit growth has outpaced the growth in deposits and MFBs will have to rely on a combination of debt and deposits to meet their funding needs.

Exhibit 2.10: Deposit-To-GLP Relation for MFBs

Micro-insurance indicators including both the number of policy holder and sum insured continued to show an increasing trend. The number of policy holders grew to 4.5 million from 3.7 million in the previous year showing a growth of 22 percent (see Exhibit 2.11). In the same time period, the sum insured grew by 35 percent to close at PKR 81.3 billion as compared to PKR 60.4 billion in the previous year. The segment remains dominated by health insurance and credit life insurance. NRSP remains the largest provider of micro-insurance with 926 thousand policy holders; at second place is KBL with 577 thousand and is followed by KF with 498 thousand policy holders. In terms of sum insured, KBL is the largest provider of micro-insurance with PKR 19.2 billion of sum insured followed by NRSP with PKR 16.3 billion and at third place is TMFB with PKR 13.1 billion sum insured.

15.7

12.5

9.7

7.3

6.1

4.5

3.2

1.1

0.0

12.3

8.7

8.7

5.2

4.7

1.2

1.3

0.7

0.0

0 5 10 15 20

TMFB

KBL

FMFB

NRSP-B

FINCA

AMFB

WMFB

Ubank

POMFB

InPKRBillions

2014 2015

0%

20%

40%

60%

80%

100%

120%

140%

0

10

20

30

40

50

60

70

2011 2012 2013 2014 2015

Depo

sit-to

-GLPRatio

InPKR

Billions

Deposits GLP Deposit-to-GLP

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

26

Exhibit 2.11: Growth in Number of Policy Holders & Sum Insured

Scale and Outreach: Depth The depth of outreach in microcredit operations is measured by a proxy indicator: average loan balance per borrower in proportion to per capita Gross National Income (GNI). A value below 20 percent is assumed to mean that the MFP is poverty focused. Comparison across peer groups shows that the ratio of average loan balance to per capita GNI for MFBs has been on the rise since the past three years (see Exhibit 2.12). MFBs tend to target the upper end of the market through relatively larger loan sizes, and hence have a ratio of 25 percent compared to MFIs and RSPs which have a ratio of 10 percent and 11 percent, respectively.

Exhibit 2.12: Depth of Outreach by Peer Groups

Here it must be kept in mind that low account size does not guarantee a lower income clientele nor does a higher loan size means that the MFPs are moving out of their target markets. Since, many of the MFPs use a graduation model of loan sizes, overtime first time borrowers decline resulting in increasing of loan sizes19. This situation holds true for MFPs in Pakistan which have large number of returning clients among its active borrowers. This is particularly true for MFBs who are upscaling loan sizes to cater to funding needs of micro-enterprises. Another reason can be the realization among 19 Measuring Results of Microfinance Institutions, Richard Rosenberg, June 2009, CGAP

0

10

20

30

40

50

60

70

80

90

1.20

1.70

2.20

2.70

3.20

3.70

4.20

4.70

5.20

2011 2012 2013 2014 2015

SumInsuredinPKR

Billions

PolicyH

olde

rsinm

illions

PolicyHolders SumInsured

0%

5%

10%

15%

20%

25%

30%

2011 2012 2013 2014 2015

AverageLoanBalancePerGDP

MFB MFI RSP Cut- off Industry

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

27

practitioners that the loan sizes are unnecessarily conservative and increasing loan sizes is not related to catering for lower income segments20. This is also true for players in Pakistan as number of them have lately recalibrated their loan sizes to keep up with the requirements of their clients and inflation. Lending Methodology Overall, group lending methodology continues to dominate the industry; however, individual lending is gaining in popularity. This is evident from the increase in the share of individual borrowing which increased from 24 percent in 2014 to 27 percent in 2015. For higher loan sizes, players have shown a clear inclination towards individual lending. Among the peer groups, MFBs have shown a preference towards individual lending as compared to group lending. Moreover, for larger loan sizes players have shown a clear bias towards individual lending.

Exhibit 2.13: Lending Methodology Trend

Gender Distribution Women borrowers continue to account for the majority of microfinance borrowers in the country. Nearly 55 percent of the active borrowers are women as compared to 58 percent in 2014. The situation varies among the three peer groups with 75 percent of borrowers of the RSPs and MFIs are women whereas only 24 percent of borrowers of MFBs are women as shown in the Exhibit 2.14.

20 Ibid

10% 12% 22% 24%27%

90%88%

78%76%

73%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2011 2012 2013 2014 2015

Activ

eBo

rrow

ersInThou

sand

s

IndividualBorrowing GroupBorrowing

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

28

Exhibit 2.14: Gender Distribution of Credit Outreach by Peer Group

Portfolio Distribution by Sector Credit portfolio distribution by sector exhibited little change over the last one year. Agriculture and livestock continued to account for the majority of the borrowers with 39 percent share, followed by service and trade making up 35 percent of the market share and manufacturing accounting for 8 percent of the industry’s borrowers.

Exhibit 2.15: Active Borrowers by Sector

76%

25% 25%

45%

24%

75% 75%

55%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MFB MFI RSP Total

MaleBorrowers FemaleBorrowers

23% 22% 22% 23% 20%

15% 16% 16% 16% 19%

38% 35% 30% 29% 25%

7% 9%8% 8% 10%

9% 9%9% 9% 8%

0% 0%0% 0% 0%

8% 9% 15% 15% 18%

0%10%20%30%40%50%60%70%80%90%100%

2011 2012 2013 2014 2015

Agriculture Livestock/Poultry Trade Services Manufacturing/Production Housing Other

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

29

Rural Urban Lending The rural borrowers continue to dominate the sector as compared to urban borrowers despite the fact that rural borrowers witnessed a decrease from 57 percent in 2014 to 54 percent in 2015. Borrowers of two of the largest players NRSP, NRSP Bank and KBL remain predominantly focused on rural areas.

Exhibit 2.16:-Active Borrowers by Urban / Rural Areas

Financial Structure Asset Base The total asset base of the microfinance industry stood at PKR 145 billion in 2015. The asset base grew by 45 percent as compared to PKR 100 billion in 2014. MFBs accounted for 67 percent of the industry of the assets followed by MFIs and RSPs with 20 percent and 13 percent share, respectively (see Exhibit 2.17).

Exhibit 2.17: Share of Asset Base by Peer Group

54%44% 42% 43% 46%

46%56% 58% 57% 54%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015

Urban Rural

67%

20%

13%

MFB MFI RSP

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

30

The asset base of MFB’s increased by 40 percent from PKR 69 billion in 2014 to 97 billion in 2015 as shown by the Exhibit 2.18. In the same time period the asset base of MFIs witnessed an increase of 81 percent which was largely due to inclusion of Akhuwat in the dataset. In addition, RSPs saw an increase of 27 percent in their assets.

Exhibit 2.18: Total Asset Base by Peer Group

10 of the larger MFPs accounted for 80 percent of the asset base of the industry (see Exhibit 2.19). This included 5 MFBs, 3 RSPs and 2 MFIs. The top three MFPs by asset size are all MFBs. The largest MFP by asset base is KBL with an asset base of PKR 26.6 billion. It is followed by TMFB with an asset base of PKR 21.0 billion. At third place is NRSP Bank with a balance sheet size of PKR 14.3 billion. Among the non-bank players NRSP has the largest asset base with PKR 12.9 billion.

Exhibit 2.19: Asset Base of Larger MFPs

3039

5569

97

6 10 13 1629

12 11 13 15 19

0

20

40

60

80

100

120

2011 2012 2013 2014 2015

PKRinbillions

0 5 10 15 20 25 30

KBLTMFB

NRSPBankNRSPFMFBFINCAKashf

AkhuwatASA-PPRSP

Billions

AssetBaseofLargerMFPs

2014 2015

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

31

Asset Composition On the whole asset utilization ratio continued to show an improving trend as seen in the Exhibit 2.20. Reliance on deposits for funding needs and longer grace period for loans being extended to the sector have reduced the need among players for keeping large cash balances resulting in a better asset utilization ratio. Also, improving ratio can also indicate towards better treasury management.

Exhibit 2.20: Asset Utilization Ratio

The ratio varies among the peer groups with RSPs having the highest with 73.5 percent closely followed by MFIs with 72.5 percent. MFBs have a value of 56.9 percent. The figure is lower for the MFB peer group as the number of newly acquired and established entities have smaller credit portfolios. Compared to the regional peers the asset utilization ratio is on the lower end and there remain sufficient room for improvement as shown in the Exhibit 2.21. Use of extended grace period and financing instruments with bullet repayments will lead to an improvement in the ratio.

Exhibit 2.21: Regional Comparison of Asset Utilization

51.2%54.7% 54.5%

61.5% 62.2%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

2011 2012 2013 2014 2015

AssetUtilizationRatio

61.36%

82.82%

72.32%78.85% 79.04%

88.43%

62.2%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

Africa EastAsiaandthePacific

EasternEuropeandCentral

Asia

LatinAmericaandTheCaribbean

MiddleEastandNorthAfrica

SouthAsia Pakistan

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

32

Funding Profile Overall, the share of deposits in the industry’s capital structure continues increase over time. Currently, 45 percent of the industry’s funding needs are met by deposits as show in the Exhibit 2.22. The share of the debt among the capital structure currently stood at 33 percent in the previous year. The percentage of equity decreased by 1 percent as compared to last year to close at 22 percent in 2015.

Exhibit 2.22: Capital Structure of the Industry

However, the capital structure varies among the peer groups. MFBs are using a combination of debt and equity to meet their funding needs. Despite impressive growth in deposits, MFBs are borrowing from diverse set of lenders to meet their funding needs. 67 percent of the funding needs of the MFB peer group is met by deposits up from 64 percent in 2014 (See Exhibit 2.23). In the same period, debt by MFBs decreased marginally by 1 percent to close at 12 percent. In case of MFIs and RSPs, they are totally dependent on debt for on lending. For MFIs the percentage of debt funding decreased from 80 percent to 77 percent in 2015. This can be attributed to inability of most of the players in this peer group to raise additional debt. RSPs also, witnessed a modest increase of 1 percent in debt in the same time period. With funding lines from national apex fully funded these MFIs are finding it hard to obtain funds from commercial lenders.

Exhibit 2.23: Capital Structure by Peer Group

21% 20% 22% 23% 22%

50%44% 35% 33% 33%

29% 37%43% 44% 45%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015

Equity Debt Deposits

22% 21% 20% 23%30% 29%

13% 12%

80% 77%70% 71%

64% 67%

0%10%20%30%40%50%60%70%80%90%

2014 2015 2014 2015 2014 2015

MFBs MFIs RSPs

Equity Debt Deposits

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

33

Profitability and Sustainability The total revenue for the industry stood at PKR 32.8 billion up from PKR 24.3 billion in 2014. The net income for the industry stood at PKR 5.1 billion up from PKR 3.5 billion in the previous year. The unadjusted ROE and ROA for the industry stood at 19.2 percent and 4.0 percent respectively in 2015. The industry continues to be sustainable with two main indicators of sustainability continue to show improving trend. The FSS for the industry stood at 121 percent in 2015 as against 120 percent in 2014 as shown in the Exhibit 24. In the same time period the OSS for the industry stood at 124 percent as against 121 percent in the previous year. Out of the 44 reporting organization, 39 have an OSS above 100 percent. The increase in revenue is due to increase in GLP which is due to a combination of rising loan sizes and increasing outreach.

Exhibit 2.24: OSS and FSS Trend

The year saw a decline in the total revenue ratio for the industry which fell from 29 percent in 2014 to 26 percent in 2015 (see Exhibit 2.25). This can be partially attributed to the decrease in the yield of gross portfolio which fell from 36 percent to 35 percent in the same time period.

Exhibit 2.25: Total Revenue Ratio & Yield on Portfolio

0%

20%

40%

60%

80%

100%

120%

140%

2011 2012 2013 2014 2015

Financialselfsufficiency(FSS) OperationalSelfSufficiency(OSS)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2011 2012 2013 2014 2015

Totalrevenueratio Yieldongrossportfolio(Nominal) Yieldongrossportfolio(Real)

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

34

Despite the decrease in the yield on loan portfolio, it remains on a higher end when compared to regional peers as shown in the Exhibit 2.26. As the industry matures and reaches scale the yield will decrease further. Moreover, rising loan sizes will also play a crucial role in decreasing operating costs leading to decrease in the yield.

Exhibit 2.26: Regional Comparison of Nominal Yield

With the total revenue for the industry standing at PKR 32.8 billion in the 2015, 79 percent of the revenue is made up by earnings from loan portfolio; revenue from investment in financial assets make up 12 percent while earnings from financial services account for remaining 9 percent as shown in the Exhibit 2.27. The total income from branchless banking stood at PKR 3.90 billion as compared to PKR 2.3 billion in 2014.

Exhibit 2.27: Revenue Streams

The expense to asset ratio witnessed a decrease as compared to last year. Total expense to assets ratio witnessed a decrease from 23.7 percent in 2014 to 21.5 percent in 2015 (see Exhibit 2.28). This decrease was largely due to decline in financial expense and operating expense ratios. The decrease in financial expense can be attributed to falling interest rates in the country. The decrease in operating expense is result of maturing of the industry and increasing loan sizes.

31.8%

21.2%19.1%

25.1%28.0%

23.2%

34.6%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Africa EastAsiaandthePacific

EasternEuropeandCentral

Asia

LatinAmericaandTheCaribbean

MiddleEastandNorthAfrica

SouthAsia Pakistan

Yieldongrossportfolio(nominal)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2011 2012 2013 2014 2015

PKRinbillions

LoanPortfolio FinancialServices FinancialAssets

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

35

Exhibit 2.28: Expense Ratios Trend

Operating expense to GLP ratio continued to exhibit a declining trend after witnessing a small increase last year. The ratio declined to 21.7 percent from 22.8 percent in 2014 (see Exhibit 2.29). The decrease was on the back of declining administrative and personnel expense. Increasing loan sizes especially with the sector expands credit operations to cover microenterprises this ratio will witness further decline in coming years.

Exhibit 2.29: Operating Expense to GLP Trend

In comparison to regional peers, the unadjusted operating expense/asset for Pakistan lies close to the average (see Exhibit 2:30). However, it is on the higher end as compared to South Asia. There is a need for players to make concentrated efforts to work on reducing costs and improving efficiency

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2008 2009 2010 2011 2012 2013 2014 2015

Adjustedtotalexpense/totalassets Adjustedfinancialexpense/totalassets

Adjustedloanlossprovisionexpense/totalassets Adjustedoperatingexpense/totalassets

0%

5%

10%

15%

20%

25%

30%

2010 2011 2012 2013 2014 2015

Operatingexpense/Grossloanportfolio Personnelexpense/Grossloanportfolio

Adminexpense/Grossloanportfolio

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

36

Exhibit 2.30: Regional Comparison of Operating Expense/Assets

Productivity The personnel allocation ratio witnessed a decline after seeing a modest improvement in the previous year. The ratio declined to 40.9 percent from 46 percent on 2014 as shown in the Exhibit 2.31. The ratio continues to vary among the peer groups with MFIs having the highest value at 46.5 percent; followed by RSPs with 44.9 percent and MFBs with 32.9 percent.

Exhibit 2.31: Personnel Allocation Ratio Trend

Compared with regional peers, the personnel allocation ratio for the microfinance industry in Pakistan remained at a lower end with the exception of Africa and East Europe as seen in the Exhibit 2:32.

11.91%

5.65%7.04%

15.40%14.25%

5.54%

10.9%

0%2%4%6%8%

10%12%14%16%18%

Africa EastAsiaandthePacific

EasternEuropeandCentral

Asia

LatinAmericaandTheCaribbean

MiddleEastandNorthAfrica

SouthAsia Pakistan

OperatingExpense/Assets

42.9%

50.5% 49.8%

44.0% 46%

30.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

2010 2011 2012 2013 2014 2015

Personnelallocationratio

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

37

Exhibit 2.32: Regional Comparison of Personnel Allocation Ratio

Productivity indicators exhibited a mixed trend in the year 2015 (see Exhibit 2.33). While loans per staff and loans per loan officer witnessed a decline the number of depositors per staff witnessed an increase. As the number of m-wallet accounts increase we are likely to see the continuation of this trend. Loans per staff and loans per loan officers may witness further dip as individual lending continues to increase. Moreover, as MFBs move into the microenterprise segment, more close scrutiny and monitoring by loan officers would mean further decrease in this ratio.

Exhibit 2.33: Productivity of MFPs

37.99%

47.43%

31.94%

44.76%

54.02%58.83%

39.2%

0%

10%

20%

30%

40%

50%

60%

70%

Africa EastAsiaandthePacific

EasternEuropeandCentral

Asia

LatinAmericaandTheCaribbean

MiddleEastandNorthAfrica

SouthAsia Pakistan

Personnelallocationratio

0

50

100

150

200

250

300

350

400

450

2011 2012 2013 2014 2015

Loansperstaff Depositorsperstaff LoansperLoanOfficers

Section 2 Financial Performance Review

Pakistan Microfinance Review 2015

38

Risk Credit Risk PAR > 30 days witnessed a slight increase from 1.1 percent in 2014 to 1.5 percent increase in 2015 as shown in the Exhibit 2.34. However, write offs declined from 2.3 percent to 1.2 percent in the same time period. Overall, the industry PAR> 30 days remained below the 5 percent benchmark reflecting positively on the portfolio quality of the industry. With MF-CIB fully operational and in the process of becoming part of the MFPs risk management process, we are likely to witness further mitigation in the credit risk.

Exhibit 2.34: PAR>30 days & Write off Trend