p op q uiz 1. what schools are you considering? list your top three options. 2. what majors are you...

TRANSCRIPT

POP QUIZ

1. What schools are you considering? List your top three options.

2. What majors are you considering? (top 3)3. What careers are you considering? (top 3)4. How are you planning on paying for your

education?

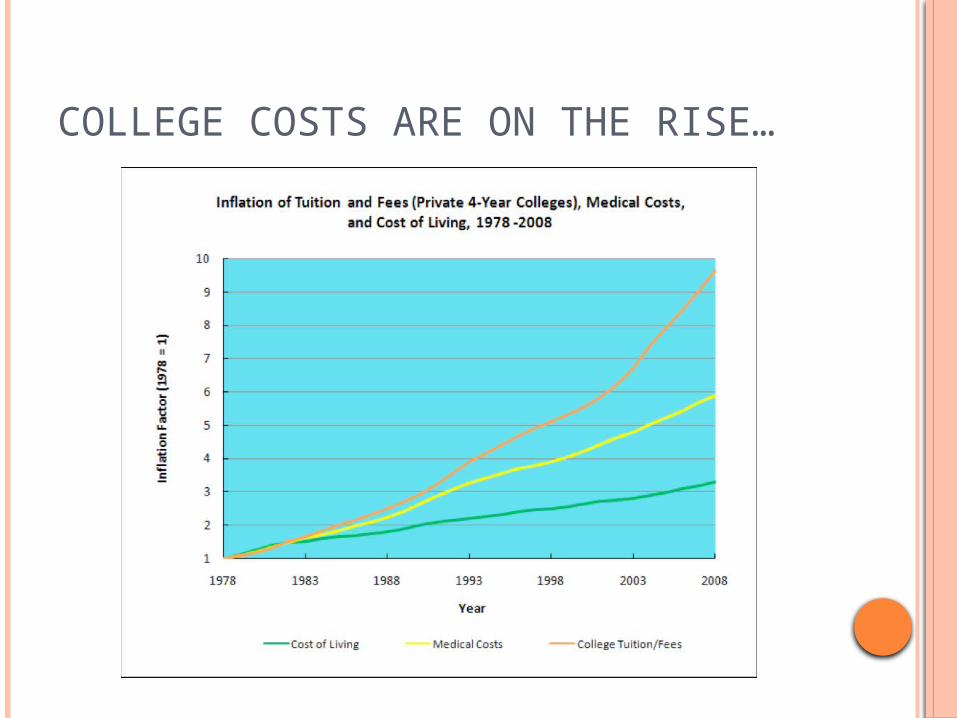

COLLEGE COSTS ARE ON THE RISE…

FINANCIAL AIDThe Economics of College…

WHAT IS FEDERAL FINANCIAL AID?

The government offers NEEDS based assistance for college

You must demonstrate documented financial need.

There are private loans and aid available, this only deals with what’s available FEDERALLY

DIFFERENT TYPES

Grants Do NOT need paid back Needs based Federal Pell Grant Maximum $5,550

Federal Work Study Part time work program to earn money while in

school Loans

They DO need paid back, with INTEREST Different types

DIRECT STAFFORD LOANS

The main loan from the government Advantages

Lower interest Flexible repayment options For four year school, community college, trade,

career, or technical school Borrow from the US Department of Education

Two types…Subsidized and Unsubsidized

DIRECT SUBSIDIZED STAFFORD LOANS

Based on need…school decides how much you get

Not charged interest while in school at least half time

6 month grace period after you leave school 3.4% interest rate

DIRECT UNSUBSIDIZED STAFFORD LOANS

Do NOT need to demonstrate financial need School decides how much you get Start collecting interest as soon as you get

them Pay the interest while in school, its cheaper If you don’t pay the interest, the interest accrued

is added to your principal, increasing the amount that you pay

6.8%

PARENT PLUS

Parents have different types of loans. Often, people under a certain age cannot get

loans unless parents sign on as guarantors or take out a parent PLUS loan themselves.

MAX STAFFORD LOAN AMOUNTS…Year Dependent

Undergraduate Student (except students whose parents are unable to obtain PLUS Loans)

Independent Undergraduate Student (and dependent students whose parents are unable to obtain PLUS Loans)

Graduate and Professional Degree Student

First Year $5,500—No more than $3,500 of this amount may be in subsidized loans.

$9,500—No more than $3,500 of this amount may be in subsidized loans.

$20,500—No more than $8,500 of this amount may be in subsidized loans.

Second Year $6,500—No more than $4,500 of this amount may be in subsidized loans.

$10,500—No more than $4,500 of this amount may be in subsidized loans.

Third and Beyond (each year)

$7,500—No more than $5,500 of this amount may be in subsidized loans.

$12,500—No more than $5,500 of this amount may be in subsidized loans.

Maximum Total Debt from Stafford Loans When You Graduate (aggregate loan limits)

$31,000—No more than $23,000 of this amount may be in subsidized loans.

$57,500—No more than $23,000 of this amount may be in subsidized loans.

$138,500—No more than $65,500 of this amount may be in subsidized loans. The graduate debt limit includes Stafford Loans received for undergraduate study.

REPAYING YOUR LOANS!

6 months before you begin repayment Where do I access my loan information?

www.nslds.ed.gov There are many different repayment plans

and options

REPAYMENT PLANS

Standard repayment Fixed amount each month Done in ten years Higher monthly payments

Extended repayment Fixed annual repayment over up to 25 years.

More than $30,000 in Direct loans to be eligible Lower monthly payment, higher overall payment

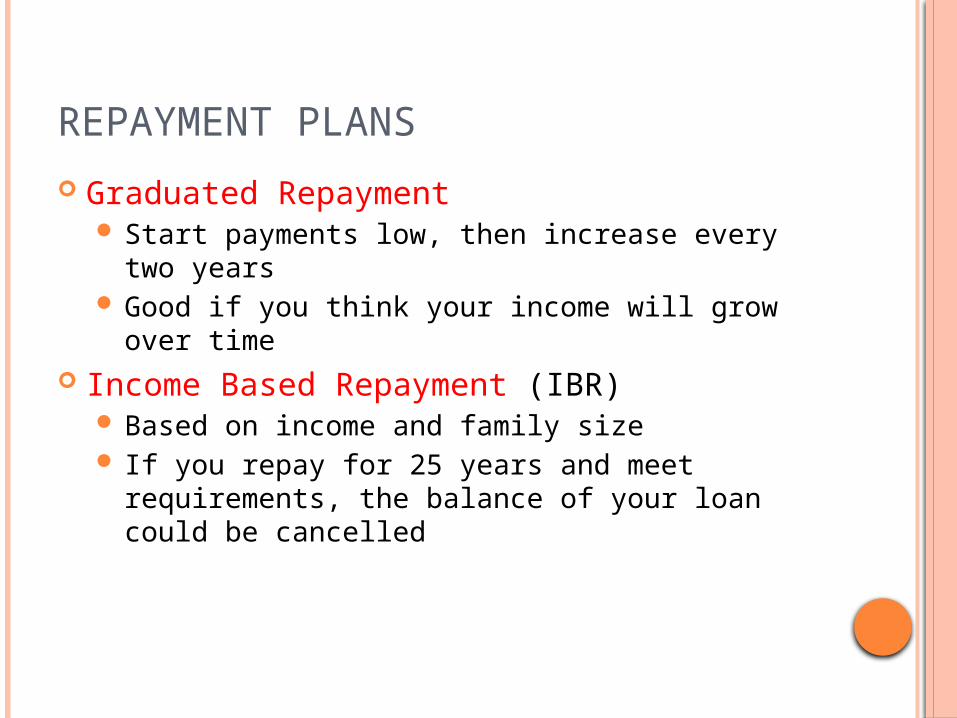

REPAYMENT PLANS

Graduated Repayment Start payments low, then increase every two

years Good if you think your income will grow over

time Income Based Repayment (IBR)

Based on income and family size If you repay for 25 years and meet requirements,

the balance of your loan could be cancelled

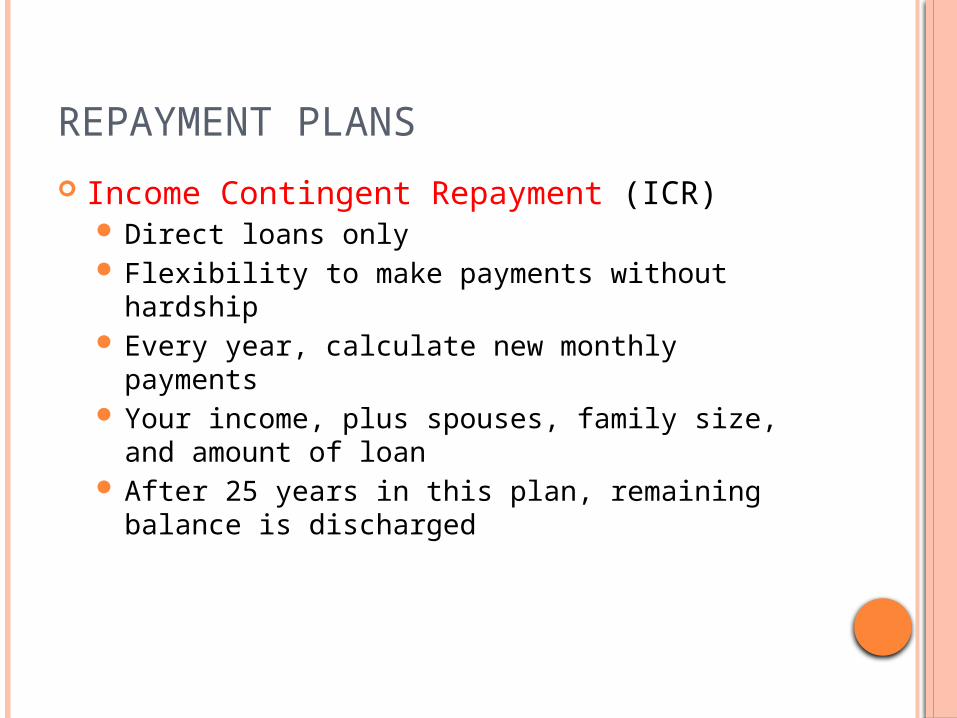

REPAYMENT PLANS

Income Contingent Repayment (ICR) Direct loans only Flexibility to make payments without hardship Every year, calculate new monthly payments Your income, plus spouses, family size, and

amount of loan After 25 years in this plan, remaining balance is

discharged

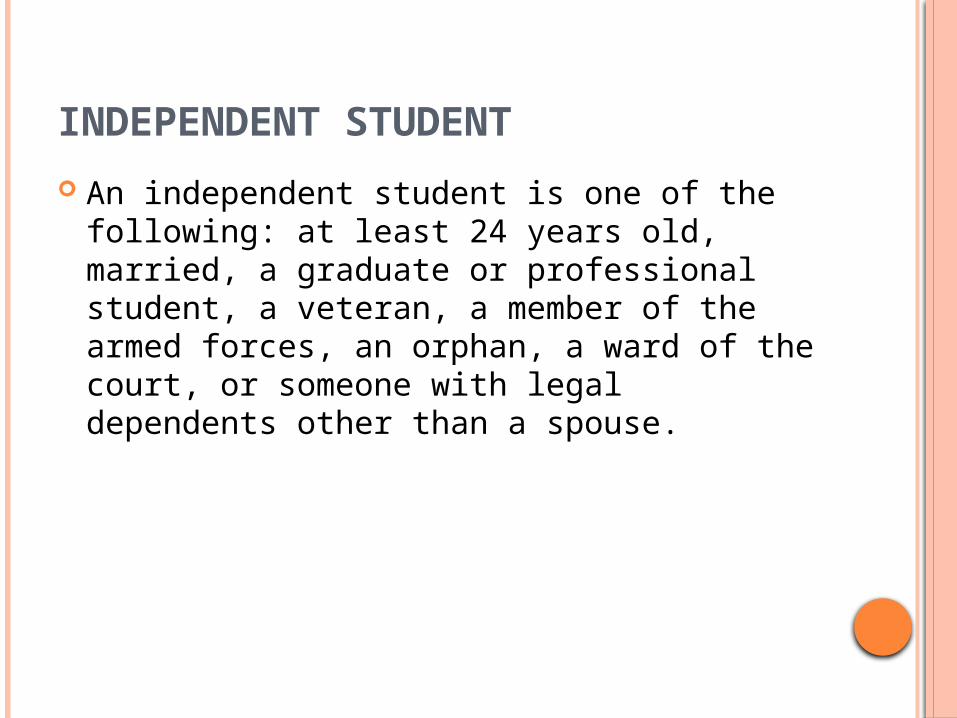

INDEPENDENT STUDENT

An independent student is one of the following: at least 24 years old, married, a graduate or professional student, a veteran, a member of the armed forces, an orphan, a ward of the court, or someone with legal dependents other than a spouse.