outlook to action: ubs cio strategy updatevttaxseminar.org/documents/2015/morningkeynote.pdf ·...

TRANSCRIPT

0

Outlook to Action: UBS CIO Strategy Update

December 2015

UBS WMA Chief Investment Office

ab 1

Our outlook for the balance of 2015 into 2016

• Will happen

o Global growth continues apace, led mainly by developed economies

o The Fed tightens gradually while other central banks stay easy

o US earnings growth improves as headwinds dissipate

• Won't happen

o Inflation becomes a global problem

o The Federal Reserve tightens monetary policy too soon, too much, too fast

o US economy enters recession & US equities enter a bear market

• Might happen

o Gold and FX markets make one final lurch when the Fed finally hikes

o Longer-term interest rates don't move much from current levels

o Diversified portfolios deliver frustratingly low returns

ab 2

2015 has been a "flattish" year on average

Source: UBS CIO WMR, Bloomberg, 5 November 2015.

-20% -10% 0% 10%

Commodit ies

EM local bonds

EM equity

Int ' l dev FI

US IG credit

US small-cap

Cash

US high yield

US government

US mid-cap

Int ' l developed equity

US municipals

EM USD bonds

US large-cap

Total returns YTD

ab 3

At long last, global monetary policy is diverging

Source: UBS CIO WMR, UBS Investment Research, as of 5 November 2015.

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

US UK Switzerland Euro area Japan

Policy rate (%) with UBS forecasts

ab 4

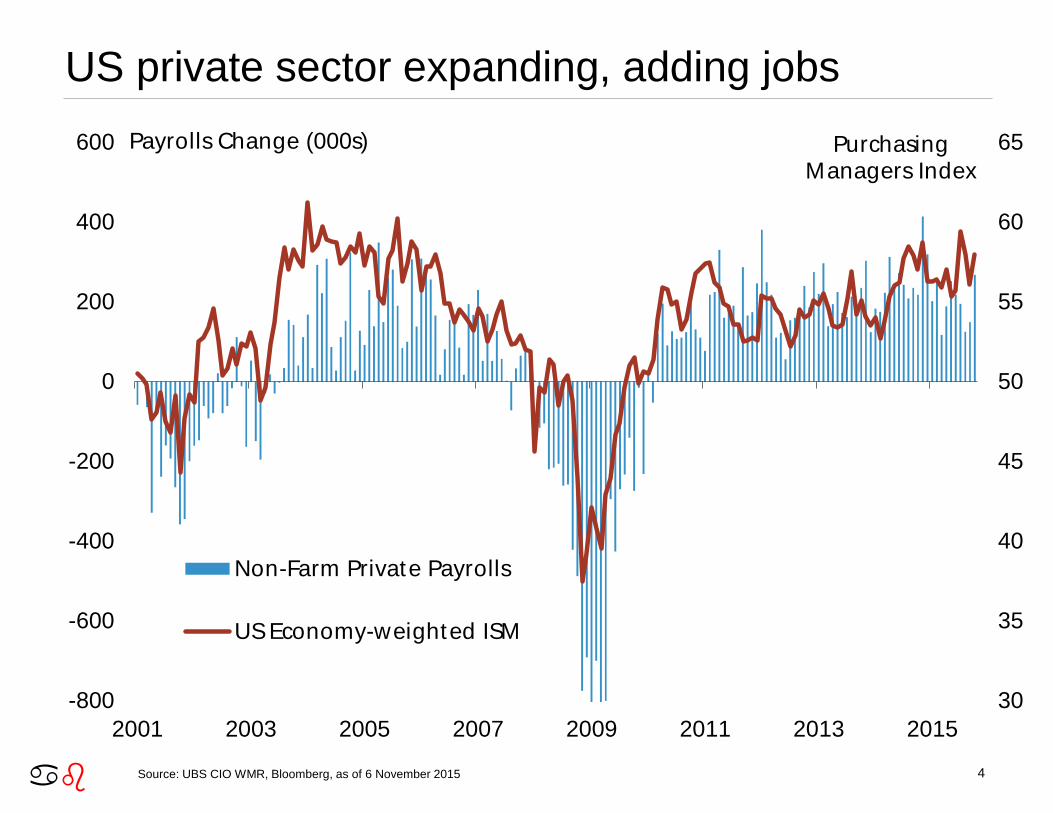

US private sector expanding, adding jobs

Source: UBS CIO WMR, Bloomberg, as of 6 November 2015

30

35

40

45

50

55

60

65

-800

-600

-400

-200

0

200

400

600

2001 2003 2005 2007 2009 2011 2013 2015

Purchasing Managers Index

Non-Farm Private Payrolls

US Economy-weighted ISM

Payrolls Change (000s)

ab 5

US consumers back in the driver's seat

Source: UBS CIO WMR, Bloomberg, as of 30 September 2015.

-6

-4

-2

0

2

4

6

1990 1993 1996 1999 2002 2005 2008 2011 2014

US GDP Growth (YoY %) US Consumpt ion Growth (YoY %)

ab 6

Chinese growth is not slowing rapidly

Source: UBS CIO WMR, Bloomberg, as of 30 October 2015

ab 7

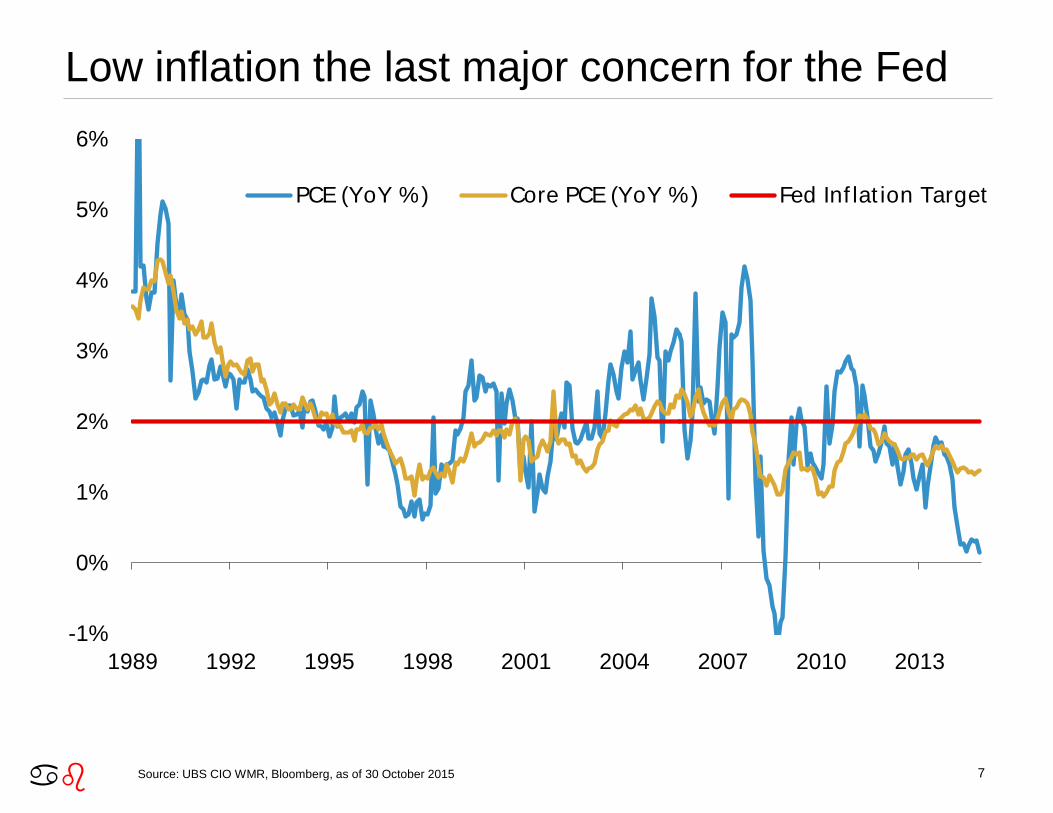

Low inflation the last major concern for the Fed

Source: UBS CIO WMR, Bloomberg, as of 30 October 2015

-1%

0%

1%

2%

3%

4%

5%

6%

1989 1992 1995 1998 2001 2004 2007 2010 2013

PCE (YoY %) Core PCE (YoY %) Fed Inf lat ion Target

ab 8

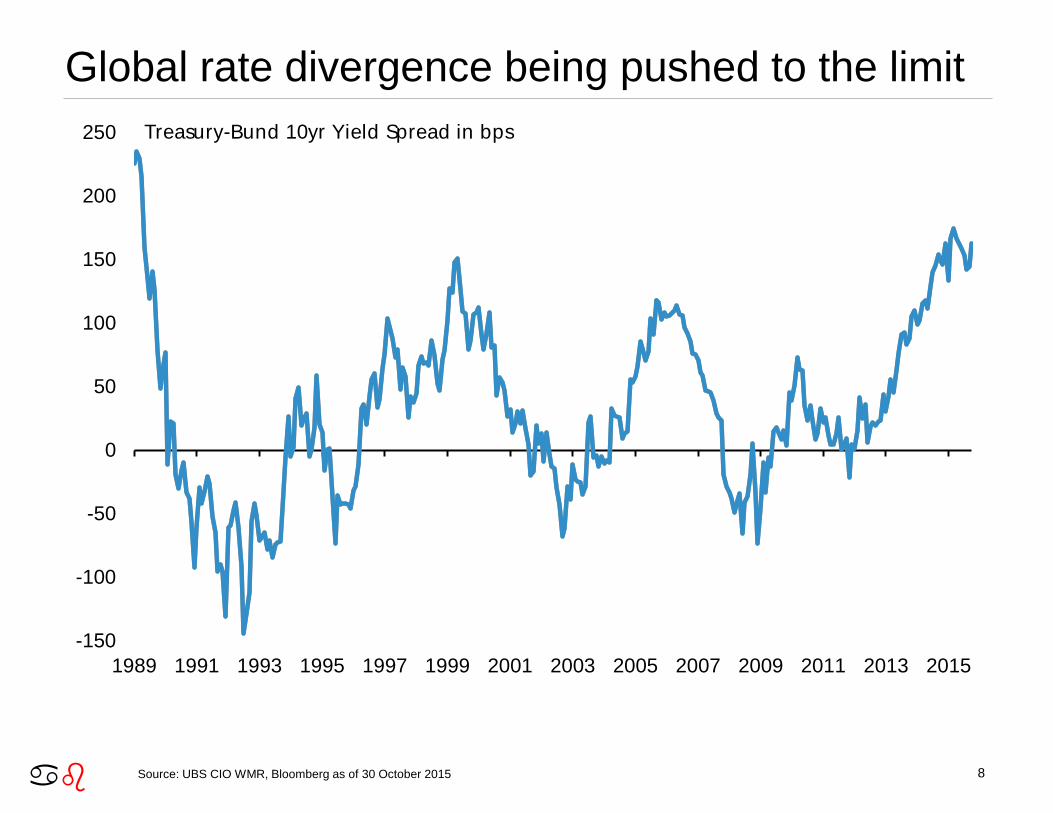

Global rate divergence being pushed to the limit

Source: UBS CIO WMR, Bloomberg as of 30 October 2015

-150

-100

-50

0

50

100

150

200

250

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Treasury-Bund 10yr Yield Spread in bps

ab 9

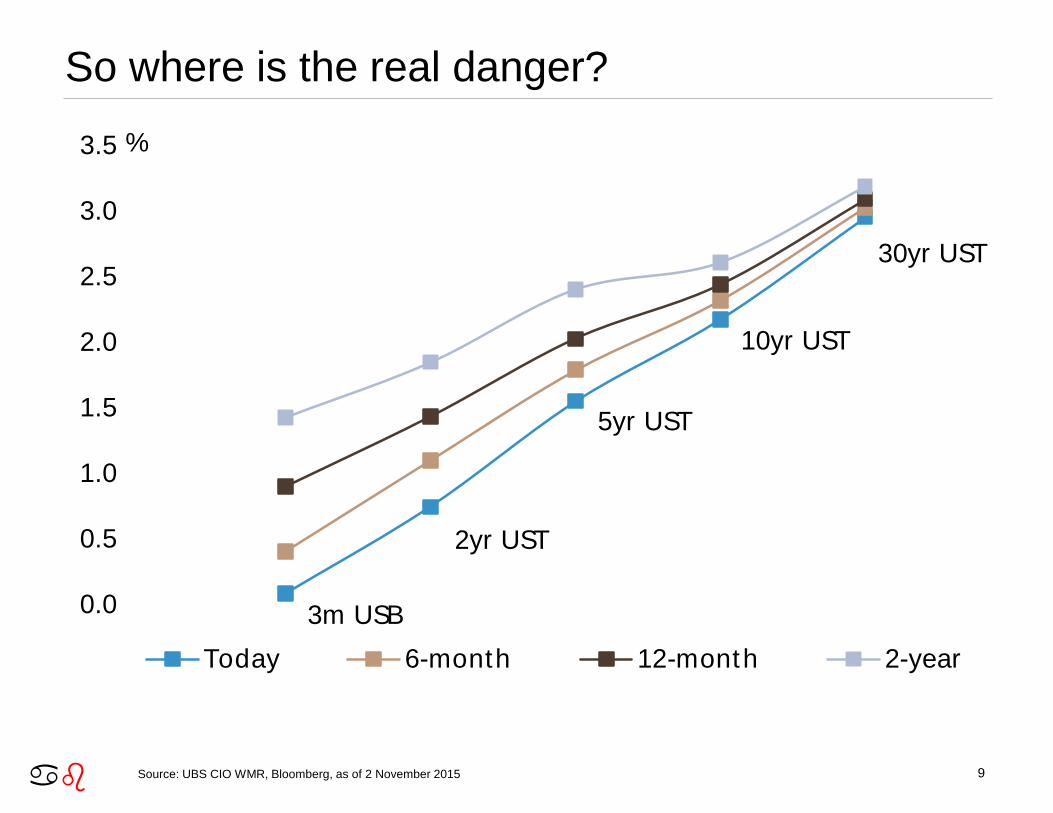

So where is the real danger?

Source: UBS CIO WMR, Bloomberg, as of 2 November 2015

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Today 6-month 12-month 2-year

3m USB

2yr UST

5yr UST

10yr UST

30yr UST

%

ab 10

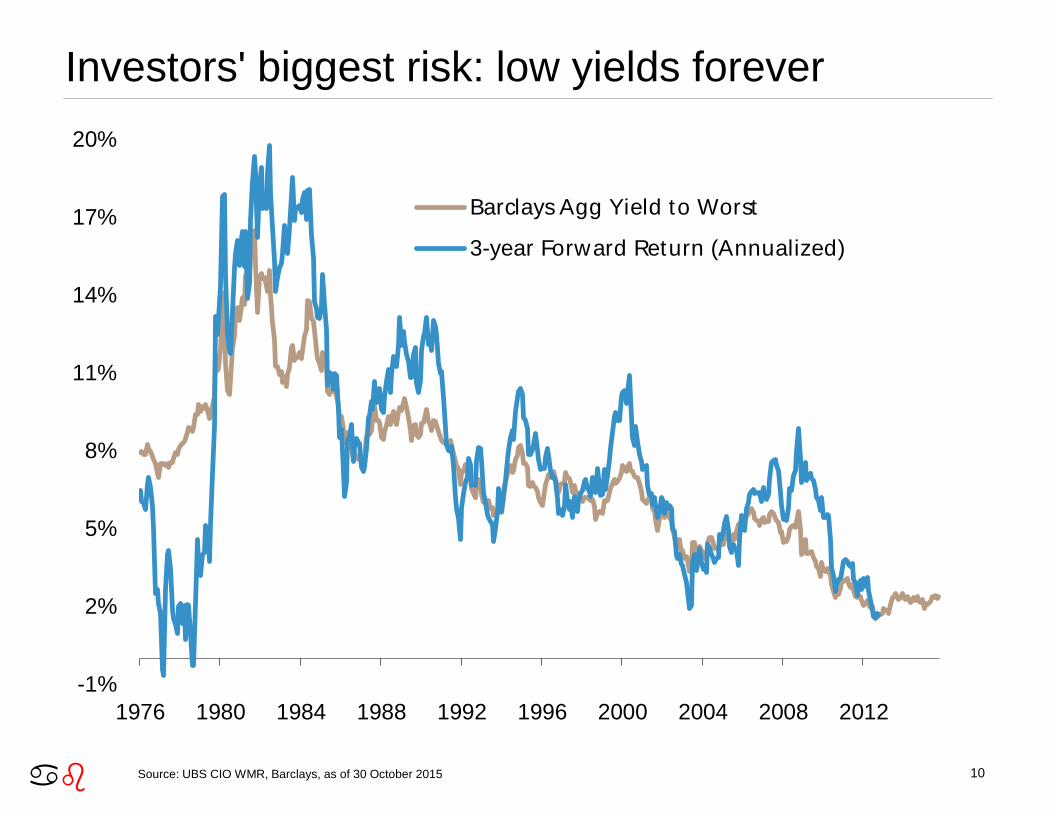

Investors' biggest risk: low yields forever

Source: UBS CIO WMR, Barclays, as of 30 October 2015

-1%

2%

5%

8%

11%

14%

17%

20%

1976 1980 1984 1988 1992 1996 2000 2004 2008 2012

Barclays Agg Yield to Worst

3-year Forward Return (Annualized)

ab 11

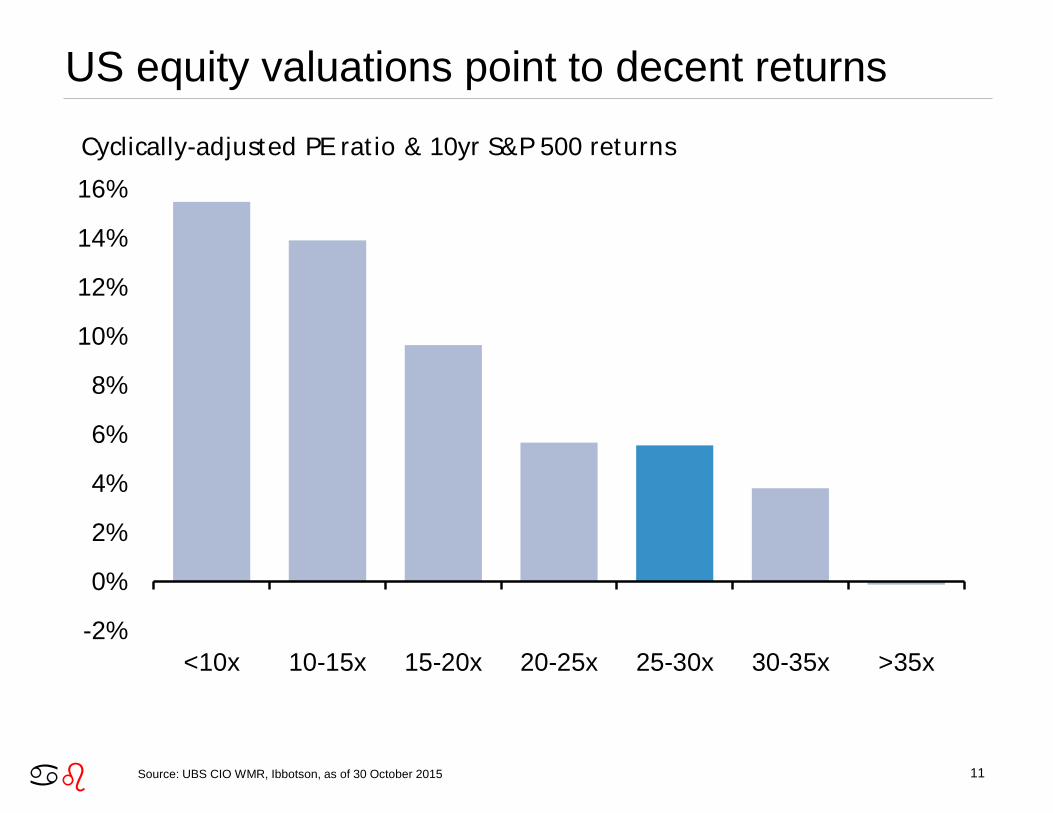

US equity valuations point to decent returns

Source: UBS CIO WMR, Ibbotson, as of 30 October 2015

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

<10x 10-15x 15-20x 20-25x 25-30x 30-35x >35x

Cyclically-adjusted PE rat io & 10yr S&P 500 returns

ab 12

Valuation much more attractive outside the US

Source: UBS CIO WMR, Research Affiliates, as of 30 September 2015; * Data for EM starts in 1994

0

5

10

15

20

25

30

US France Germany Italy Spain EM

Current Shiller PE Median Shiller PE

25th Percent ile Shiller PE 75th Percent ile Shiller PE

" Shiller" P/E rat ios for major country equity markets, 1969 - 2015*

ab 13

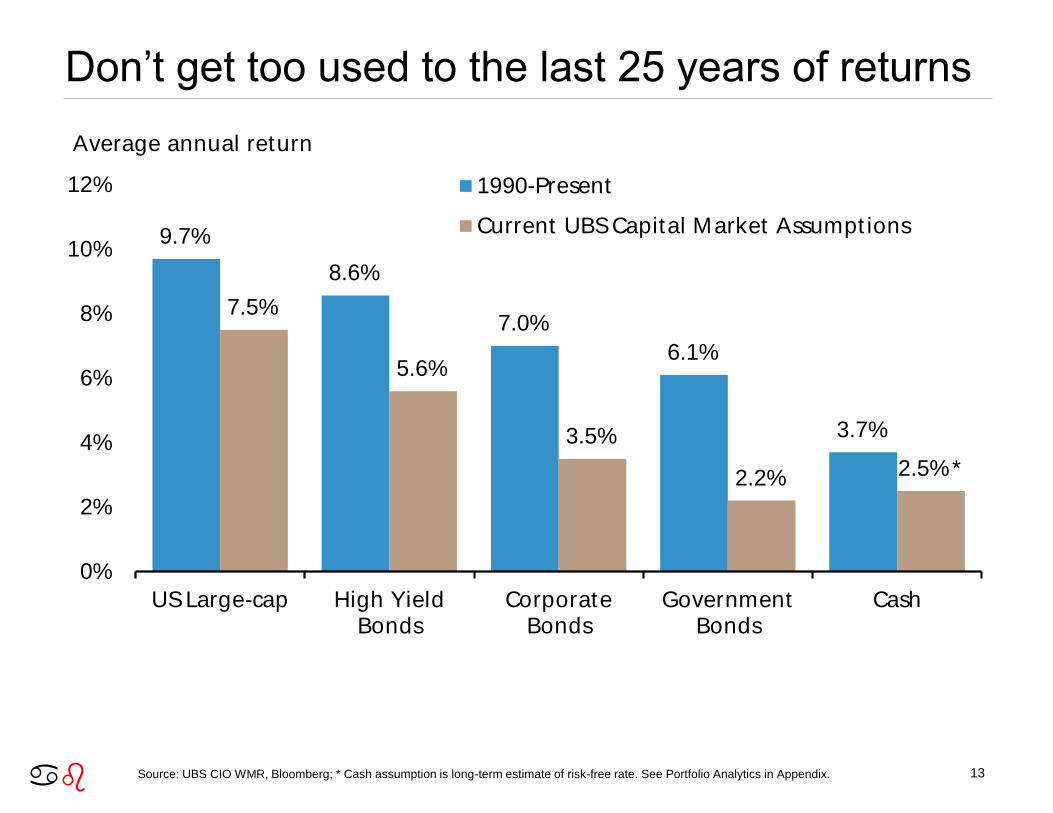

Don’t get too used to the last 25 years of returns

Source: UBS CIO WMR, Bloomberg; * Cash assumption is long-term estimate of risk-free rate. See Portfolio Analytics in Appendix.

9.7%

8.6%

7.0%

6.1%

3.7%

7.5%

5.6%

3.5%

2.2% 2.5%*

0%

2%

4%

6%

8%

10%

12%

US Large-cap High YieldBonds

CorporateBonds

GovernmentBonds

Cash

1990-Present

Current UBS Capital Market Assumpt ions

Average annual return

ab 14

A modest outlook with moderate risks

• US economy is growing at or above its potential and absorbing remaining labor

slack

o Eurozone growth set to accelerate further in 2016

o China & EM slowing but stable

• Muted asset returns given rich starting points

o Bonds are expensive, stocks aren't cheap, the US dollar is still strong

o International investments offer better long-term value

o US credit now cheaper but the cycle is well past the mid-point

• Risks to our Outlook

o US growth turns over for lack of investment and foreign demand

o Oil prices remain low as supply remains high, demand weak

o The "random" stories all break negative, especially in EM

ab 15

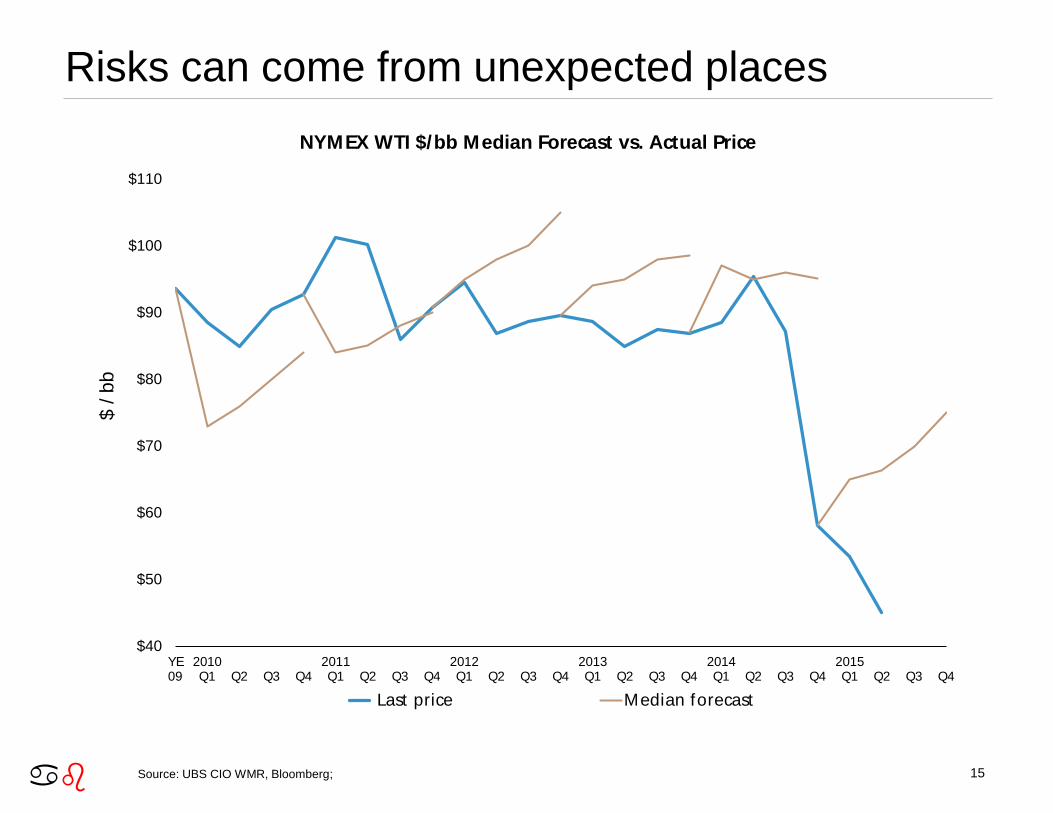

Risks can come from unexpected places

Source: UBS CIO WMR, Bloomberg;

$40

$50

$60

$70

$80

$90

$100

$110

Q4Q3Q22015Q1Q4Q3Q2

2014Q1Q4Q3Q2

2013Q1Q4Q3Q2

2012Q1Q4Q3Q2

2011Q1Q4Q3Q2

2010Q1

YE09

$ / b

b

NYMEX WTI $/bb Median Forecast vs. Actual Price

Last price Median forecast

ab 16

Some are clear ahead of time

Source: UBS CIO WMR, Barclays, as of 31 August 2015

-1%

2%

5%

8%

11%

14%

17%

20%

1976 1980 1984 1988 1992 1996 2000 2004 2008 2012

Barclays Agg Yield to Worst

3-year Forward Return (Annualized)

ab 17

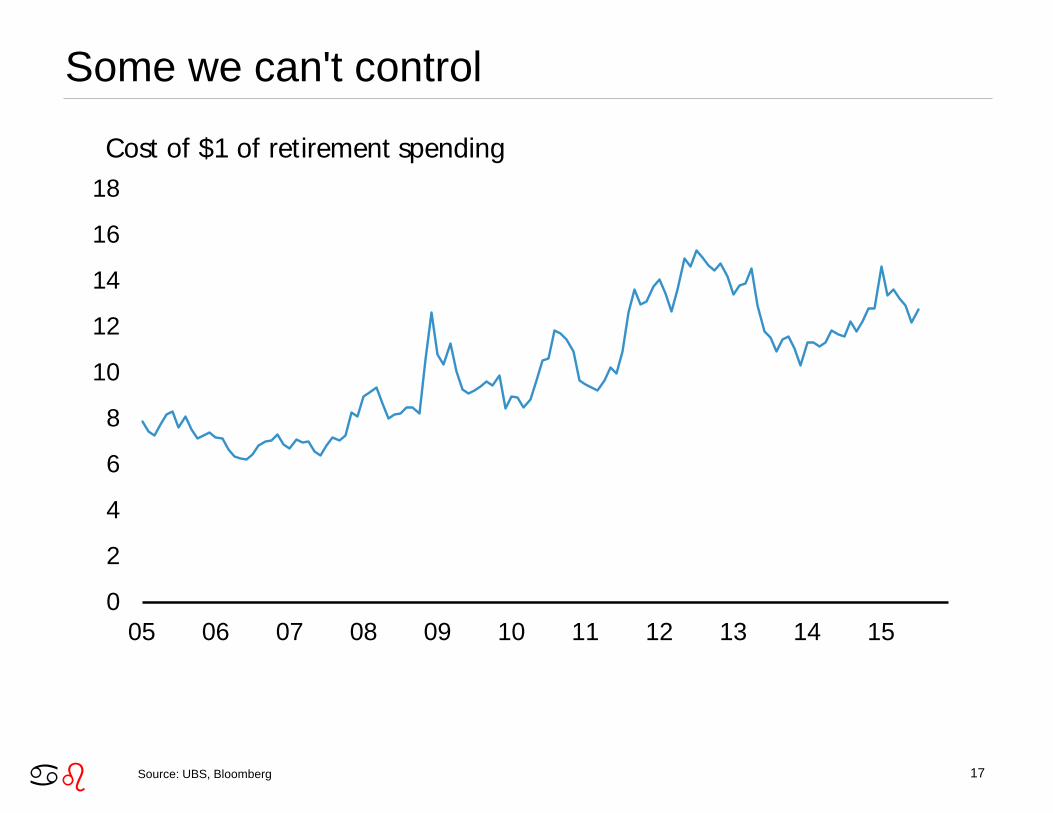

Some we can't control

Source: UBS, Bloomberg

0

2

4

6

8

10

12

14

16

18

05 06 07 08 09 10 11 12 13 14 15

Cost of $1 of retirement spending

ab 18

Others are self-created

ab 19

How did you feel on Friday, August 28th?

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

Monday Tuesday Wednesday Thursday Friday Full Week

Da

ily

Re

turn

Source: Bloomberg, UBS. Data covers 8/24/2015 – 8/28/2015.

ab 20

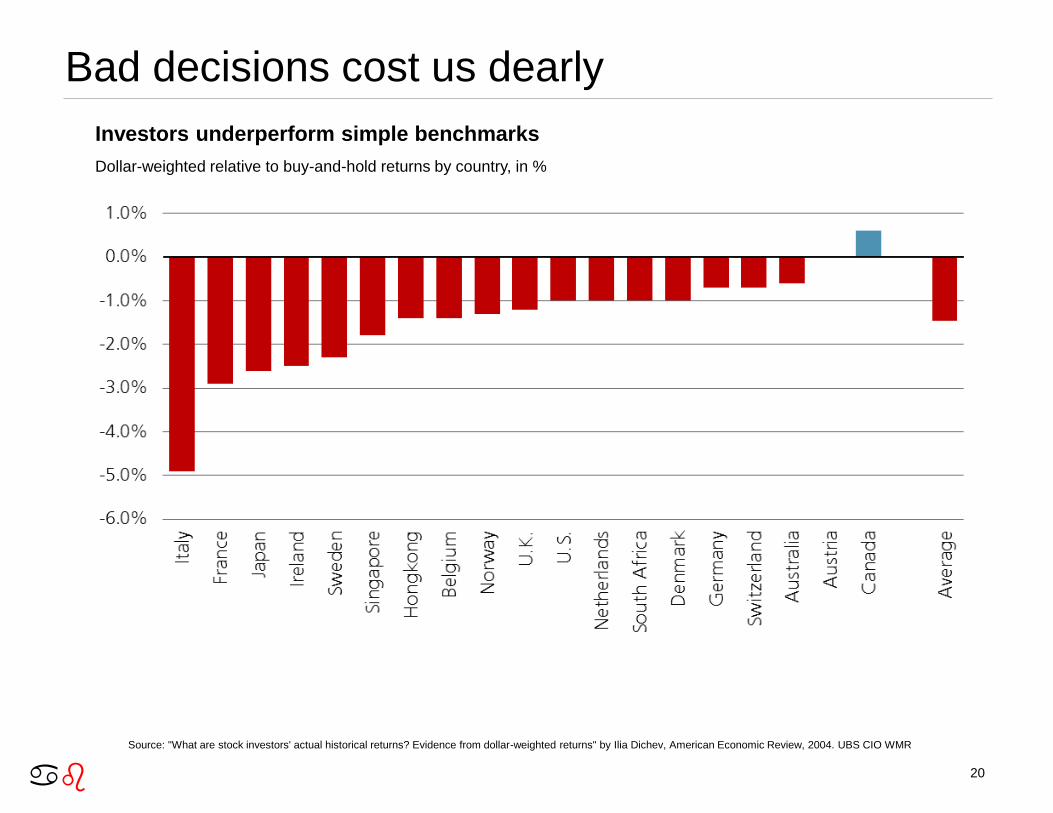

Bad decisions cost us dearly

Investors underperform simple benchmarks

Dollar-weighted relative to buy-and-hold returns by country, in %

Source: "What are stock investors' actual historical returns? Evidence from dollar-weighted returns" by Ilia Dichev, American Economic Review, 2004. UBS CIO WMR

ab 21

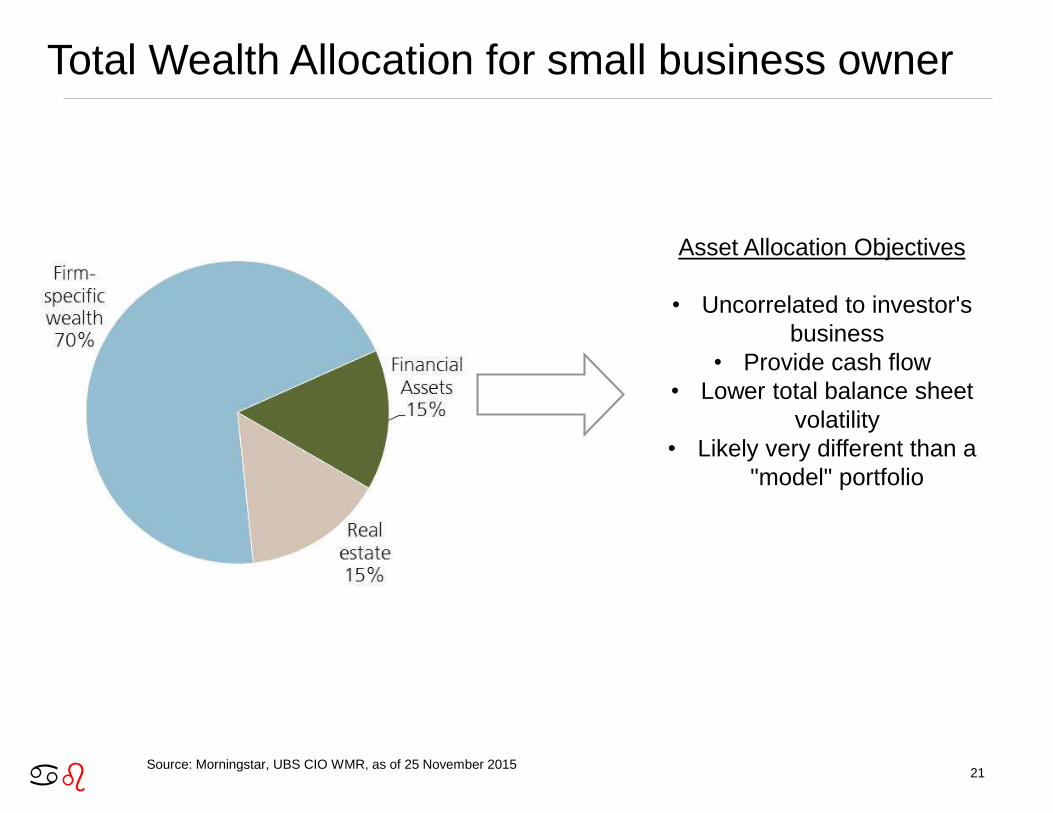

Total Wealth Allocation for small business owner

Source: Morningstar, UBS CIO WMR, as of 25 November 2015

Asset Allocation Objectives

• Uncorrelated to investor's

business

• Provide cash flow

• Lower total balance sheet

volatility

• Likely very different than a

"model" portfolio

ab 22

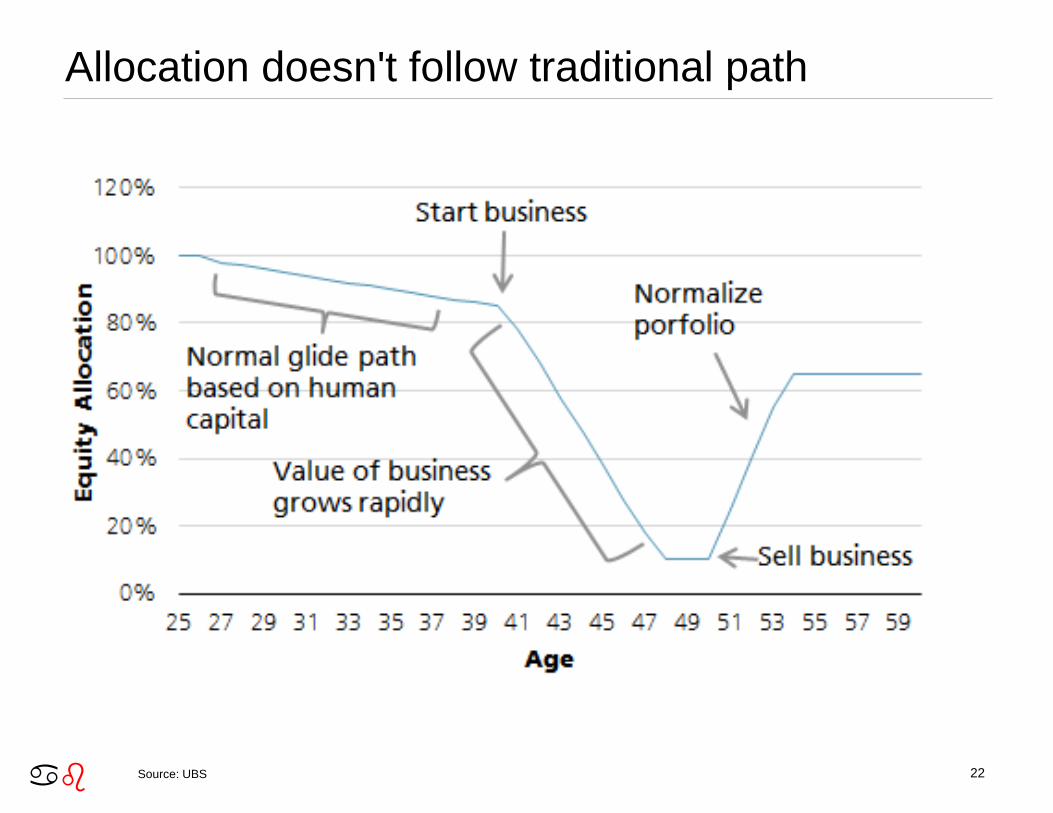

Allocation doesn't follow traditional path

Source: UBS

ab 23

Building a Goals-Based Allocation

Source: UBS

Risk/Return SpectrumLow er Risk

Shorter Term Time Frame

Higher Risk

Longer Term

Liquidity

Time Horizon: 0 – 4 years

Longevity

Time Horizon: 5 years – life

Legacy

Time Horizon: Life expectancy +

1

10

100

1,000

10,000

100,000

ab 24

AppendixSources of strategic asset allocations and investor risk profiles

Strategic asset allocations represent the longer-term allocation of assets that is deemed suitable for a particular investor. The strategic asset allocation models

discussed in this publication, and the capital market assumptions used for the strategic asset allocations, were developed and approved by the WMA AAC.

The strategic asset allocations are provided for illustrative purposes only and were designed by the WMA AAC for hypothetical US investors with a total return

objective under five different Investor Risk Profiles ranging from conservative to aggressive. In general, strategic asset allocations will differ among investors

according to their individual circumstances, risk tolerance, return objectives and time horizon. Therefore, the strategic asset allocations in this publication may not

be suitable for all investors or investment goals and should not be used as the sole basis of any investment decision. Minimum net worth requirements may apply

to allocations to non-traditional assets. As always, please consult your UBS Financial Advisor to see how these weightings should be applied or modified

according to your individual profile and investment goals.

The process by which the strategic asset allocations were derived is described in detail in the publication entitled “UBS WMA’s Capital Markets Model: Explained,

Part II: Methodology,” published on 22 January 2013. Your Financial Advisor can provide you with a copy.

Deviations from strategic allocation

The recommended tactical deviations from the strategic asset allocation or benchmark allocation are provided by the Global Investment Committee and the

Investment Strategy Group within Wealth Management Research Americas. They reflect the short- to medium- term assessment of market opportunities and

risks in the respective asset classes and market segments. Positive / zero / negative tactical deviations correspond to an overweight / neutral / underweight

stance for each respective asset class and market segment relative to their strategic allocation. The current allocation is the sum of the strategic asset allocation

and the tactical deviation. Overweight: Tactical recommendation to hold more of the asset class than specified in the strategic asset allocation on pages 24-27 of

the flagship publication UBS House View: Investment Strategy Guide. Underweight: Tactical recommendation to hold less of the asset class than specified in the

strategic asset allocation on pages 24-27 of the flagship publication UBS House View: Investment Strategy Guide. Neutral: Tactical recommendation to hold the

asset class in line with its weight in the strategic asset allocation on pages 24-27 of the flagship publication UBS House View: Investment Strategy Guide.

Portfolio analytics

The portfolio analytics for each risk profile’s benchmark allocations are based on estimated forward-looking return and standard deviation assumptions (capital

market assumptions), which are based on UBS proprietary research. The development process includes a review of a variety of factors, including the return, risk,

correlations and historical performance of various asset classes, inflation and risk premium. These capital market assumptions do not assume any particular

investment time horizon. The process assumes a situation where the supply and demand for investments is in balance, and in which expected returns of all asset

classes are a reflection of their expected risk and correlations regardless of time frame. Please note that these assumptions are not guarantees and are subject to

change. UBS has changed its risk and return assumptions in the past and may do so in the future. Neither UBS nor your Financial Advisor is required to provide

you with an updated analysis based upon changes to these or other underlying assumptions.

In order to create the analysis, the rates of return for each asset class are combined in the same proportion as the asset allocations illustrated (e.g., if the asset

allocation indicates 40% equities, then 40% of the results for the allocation will be based upon the estimated hypothetical return and standard deviation

assumptions).

You should understand that the analysis shown and assumptions used are hypothetical estimates provided for your general information. The results are not

guarantees and pertain to the asset allocation and/or asset class in general, not the performance of specific securities or investments. Your actual results may

vary significantly from the results shown in this report, as can the performance of any individual security or investment.

ab25

Disclaimer Chief Investment Office (CIO) Wealth Management (WM) Research is published by UBS Wealth Management and UBS Wealth Management Americas, Business

Divisions of UBS AG (UBS) or an affiliate thereof. CIO WM Research reports published outside the US are branded as Chief Investment Office WM. In certain

countries UBS AG is referred to as UBS SA. This publication is for your information only and is not intended as an offer, or a solicitation of an offer, to buy or sell any

investment or other specific product. The analysis contained herein does not constitute a personal recommendation or take into account the particular investment

objectives, investment strategies, financial situation and needs of any specific recipient. It is based on numerous assumptions. Different assumptions could result in

materially different results. We recommend that you obtain financial and/or tax advice as to the implications (including tax) of investing in the manner described or in

any of the products mentioned herein. Certain services and products are subject to legal restrictions and cannot be offered worldwide on an unrestricted basis

and/or may not be eligible for sale to all investors. All information and opinions expressed in this document were obtained from sources believed to be reliable and in

good faith, but no representation or warranty, express or implied, is made as to its accuracy or completeness (other than disclosures relating to UBS and its

affiliates). All information and opinions as well as any prices indicated are current only as of the date of this report, and are subject to change without notice.

Opinions expressed herein may differ or be contrary to those expressed by other business areas or divisions of UBS as a result of using different assumptions

and/or criteria. At any time, investment decisions (including whether to buy, sell or hold securities) made by UBS AG, its affiliates, subsidiaries and employees may

differ from or be contrary to the opinions expressed in UBS research publications. Some investments may not be readily realizable since the market in the securities

is illiquid and therefore valuing the investment and identifying the risk to which you are exposed may be difficult to quantify. UBS relies on information barriers to

control the flow of information contained in one or more areas within UBS, into other areas, units, divisions or affiliates of UBS. Futures and options trading is

considered risky. Past performance of an investment is no guarantee for its future performance. Some investments may be subject to sudden and large falls in value

and on realization you may receive back less than you invested or may be required to pay more. Changes in FX rates may have an adverse effect on the price,

value or income of an investment. This report is for distribution only under such circumstances as may be permitted by applicable law.

Distributed to US persons by UBS Financial Services Inc. or UBS Securities LLC, subsidiaries of UBS AG. UBS Switzerland AG, UBS Deutschland AG, UBS Bank,

S.A., UBS Brasil Administradora de Valores Mobiliarios Ltda, UBS Asesores Mexico, S.A. de C.V., UBS Securities Japan Co., Ltd, UBS Wealth Management Israel

Ltd and UBS Menkul Degerler AS are affiliates of UBS AG. UBS Financial Services Incorporated of PuertoRico is a subsidiary of UBS Financial Services Inc. UBS

Financial Services Inc. accepts responsibility for the content of a report prepared by a non-US affiliate when it distributes reports to US persons. All transactions by a

US person in the securities mentioned in this report should be effected through a US-registered broker dealer affiliated with UBS, and not through a non-US affiliate.

The contents of this report have not been and will not be approved by any securities or investment authority in the United States or elsewhere. UBS Financial

Services Inc. is not acting as a municipal advisor to any municipal entity or obligated person within the meaning of Section 15B of the Securities Exchange Act (the

"Municipal Advisor Rule") and the opinions or views contained herein are not intended to be, and do not constitute, advice within the meaning of the Municipal

Advisor Rule.

UBS specifically prohibits the redistribution or reproduction of this material in whole or in part without the prior written permission of UBS and UBS accepts no liability

whatsoever for the actions of third parties in this respect.

Version as per September 2015.

© UBS 2015. The key symbol and UBS are among the registered and unregistered trademarks of UBS. All rights reserved.