outlook for the european monetary union: the message from eastern europe

TRANSCRIPT

OUTLOOK FOR THE EUROPEAN MONETARY UNION: THE MESSAGE FROM EASTERN EUROPE

RICHARD J. SWEENEY*

The European Community (EC) seems headed toward moneta y union, either with “permanent1y”jixed exchange rates or with a common currency. Ceteris paribus, the breakup of the Soviet empire in Eastern Europe makes moneta y union less desirable. One can expect further shocks fiom the East. Analyzing stock markets’ reactions to events in the East fiom late 1988 to early 1990 shows that these shocks typically diferentially afect EC members, particularly Germany. These differential shocks often call for adjustments in relative national price levels, which can be accomplished most easily with exchange-rate adjustments. The likelihood of such pressures reduces the credibility of a system of pegged rates and makes the system more vulnerable to spec- ulative runs. A common currency is more credible by its nature but may give an inflationa y bias to the European Monetary Union.

I. INTRODUCTION

Members of the European Community (EC) are committed to move toward mon- etary union within the next few years, though some EC leaders reportedly have doubts. The European Monetary System (EMS) already is in place: Some members of the EC-including Germany, France, and Italy-are committed to holding their rates within pre-specified limits relative to the other currencies in the EMS. (The United Kingdom joined in October 1990.) The success of the EMS over the 1980s sur- prised many observers. Many now view a successful move toward monetary union as a real possibility. At one point, the stated goal was either permanently fixed exchange rates or a single currency within the EC. In mid-June 1991, the goal appar- ently was fixed rates within relatively nar-

*Sullivan/Dean Professor of International Business and Finance, School of Business Administration, Georgetown University. This is a revised version of a paper presented at the Western Economic Association International 65th Annual Conference, San Diego, July 2,1990, in a session organized by Axel Leijonhufvud, University of California, Los Angeles. The author is grateful for helpful comments from Thomas D. Willett, from four referees, and from participants in the con- ference session.

Contemporary Policy Issues Vol. IX. October 1991

row bands in 1994 and a common currency to be introduced later.

The EMS and any successor European Monetary Union (EMU) face potentially greater stresses from Eastern Europe dur- ing the 1990s than they did during most of the 1980s. The breakup of the Soviet empire in Eastern Europe has resulted, on net, in pleasant political change for devel- oped countries, including EC members. The economic outlook for Eastern Europe is daunting, however, and EC members clearly will be deeply involved there through aid, trade, investment, popula- tion movements, and other ways. Disloca- tions in the Soviet Union threaten similar disturbances. During the coming decade, a varied series of positive and negative economic surprises will come from the East. One should remember that the dem- onstrations leading to the overthrow of the regimes in Eastern Europe often were accompanied by financial market anxiety. The disturbances from other sources may show less variance than they did during the past two decades. But ceteris paribus, the increased likelihood of shocks from the East compounds the problems that the EC will face.

20

OWestern Economic Association International

SWEENEY: OUTLOOK FOR EUROPEAN MONETARY UNION 21

The major issue for any EMU may be its credibility. The EMS has been surpris- ingly successful, but credible pre-commit- ment to fixed rates seems intrinsically hard to achieve. The post-World War I1 record of parity changes discourages confidence in the possibility of long-term fixity of rates, and theoretical discussions of cred- ible pegging reveal that success depends quite sensitively on the assumptions made. The credibility problem is greater given the possibility of greater shocks from the East. In this case, the EMU will likely be more credible with a single com- mon currency since this would allow changes in parities only at a higher price than would altering pegged rates.

Any future shocks from the East will likely fall differentially on members of the EC. In many cases, Germany will be more exposed than will other members due to cultural and economic ties as well as to simple geography. These differential shocks often will imply adjustments in intra-EC real exchange rates. In the ab- sence of a single currency, the necessity for adjusting real exchange rates will place pressure on individual EC members to ad- just nominal exchange rates rather than face inflation or deflation. If they give in and adjust rates, then their actions will re- duce the credibility of a pegged-rate EMU to resist future parity changes. Further, one may begin to view the EMU less as a currency union than as simply a system of temporarily pegged rates. The EMU members' adjusting their rates substan- tially weakens the credibility of long-term fixity of the EMU'S rates. If the EMU loses long-term credibility of rate fixity, then this will seriously reduce the likelihood of any single European currency or basket of currencies rivaling the dollar's interna- tional reserve currency role.

Section I1 discusses the role that eastern shocks will likely play on the desirability of a strong EMU. That section argues that eastern shocks will likely make parity changes desirable since the shocks typi-

cally will fall differentially on the EC members. A review of differential stock market reactions to disturbances from late 1988 to early 1990 provides some support for this view. This review is an "event study" much like the type used in finance since the late 1960s. (see Fama et al., 1969, for an early finance application. Also, see Chalk, 1986.) The present study may be the first to apply the approach to interna- tional political economy questions. (In a study complementing the present work, Eichengreen, 1990, examines European stock markets but does not use an event study framework.') In terms of standard optimum currency area theory, the differ- ential impact of eastern disturbances makes the EC less attractive than other- wise for monetary union. This, in turn, makes any system of fixed parities less credible and thus more vulnerable to spec- ulative runs-the classic problem of pegged-rate regimes.

Section I11 discusses the choice between permanently pegged exchange rates or a common currency. A system of pegged rates is inherently less credible than is a common currency. The probability is high that, sometime in the future, members will face the choice of either adjusting parities or enduring painful deflation for some and unwanted inflation for others. Adjust- ing parities is intrinsically harder and more costly under a common currency since this involves reintroducing a na- tional currency, redeveloping a national payments system, and reintegrating this system with other systems. On the other hand, a major cost of a common currency

1. Eichengreen (1990) calculates coefficients of vari- ation in differences in the closing index values for the Paris and Frankfurt stock exchanges on the last Friday of each quarter. (The indices are adjusted for consumer price levels and, in one version, for exchange rates.) He compares these with similar calculations for the To- ronto and Montreal exchanges. Using calculations for levels, which likely will be non-stationary and thus have distribution parameters not corresponding to those calculated, may not be prudent. This paper com- pares rates of return where non-stationarity problems are much less likely.

22 CONTEMPORARY POLICY ISSUES

is precisely that it raises the difficulties of adjusting parities rather than national price levels in extreme circumstances. A further problem with a common currency is that Germany probably would have to play a lesser role in governing monetary expansion by a European central bank than it does under a system of pegged rates. Under pegged rates, reserve losses can force other EMS members to fall in line with conservative German inflation pol- icy.

Section IV offers some conclusions. The EC may not be a good candidate for form- ing a currency area. In particular, the pos- sibility of great, differential shocks from the East-both Eastern Europe and the So- viet Union-weakens the case. If members of the EC decide to form a currency area, then they will likely have much greater long-run success by adopting a single cur- rency than they would by trying to main- tain fixed rates. Similarly, a long transition period of pegged rates before adopting a common currency would likely leave the EMU vulnerable to parity changes that re- duce credibility and perhaps shake politi- cal agreement on the desirability of a cur- rency union. However, a common cur- rency might give the German central bank a weaker voice in overall EC monetary policy than would a system of fixed rates. Therefore, one cost of a common cur- rency-as compared with fixed rates- might be an inflationary bias.

11. THE EC AND THE SHOCKS DURING THE 1990s

One has little reason to believe that the types of disturbances that have character- ized the managed floating experience since March 1973 will be greatly different during the next decade. To be sure, OPEC shocks as great as those of 1973-1974 and 1979 may not recur. The disruption to t‘he world economy from the Iraq-Kuwait cri- sis has been much less than it was from earlier oil crises. Further, one cannot be certain that the commodity, agricultural,

and other particular disturbances of the 1970s and 1980s will surface again. Never- theless, the decade ahead appears to be subject to the same types and magnitudes of disturbances as have the past two de- cades. The new and different feature-par- ticularly for the EC2-is the greater chance of shocks from Eastern Europe and the So- viet Union. The end of Soviet hegemony in other Eastern European countries has increased the likelihood of political distur- bances there. The Soviet Union itself also faces the possibility of major political dis- ruptions. Further, both Eastern Europe and the Soviet Union face economic prob- lems that few analysts were predicting as few as five-or even three-years ago. The Soviet Union always has been a possible- and sometimes an actual-source of dis- turbances, but one never had to worry about a separate Czechoslovakian shock. The actual international disturbances re- sulting from conflict in Poland during the 1980s were smaller than those that may occur in the future due to problems in that country. Soviet political and military moves toward Poland sometimes put downward pressure on the deutschemark (DM) during the 1980s, but no open con- flict or social chaos actually occurred. This may change during the 1990s.

Not only will the EC likely face larger shocks from the East than it has in the past, these shocks may well have differen- tial impacts on the EC members. By exam- ining the effects on asset markets of the recent disturbances in the East, one can see some evidence for the possibility that fu-

2. As one referee observed, because the EC mem- bers now may have better fiscal and monetary control as well as less divergent policies, this source of pres- sures for intra-EMS currency realignments may be smaller than it has been in the past. Further, EC members’ “peace dividend” from relaxing tensions with the Soviet Union may enable them to finance their reactions to the problems of Eastern Europe with no increased pain overall, though Germany’s costs from reunification make this view less plausible. Future ceteris paribus disturbances from the East will create greater problems.

SWEENEY: OUTLOOK FOR EUROPEAN MONETARY UNION 23

ture disturbances will have differential im- pacts. One might find evidence on the dif- ferential impacts of eastern shocks in both stock markets and foreign exchange mar- kets. (The discussion below covers both markets.) Note that for one to draw clear- cut conclusions from foreign exchange markets with intervention, as is the case with the EC, one needs data on both ex- change rate movements and official inter- vention. Data on official intervention are difficult to obtain? For this reason, the analysis relies mainly on stock market re- actions.

A. Diferential Stock Market Reactions The reactions of European stock mar-

kets to some eastern disturbances since 1988 indicate the degree to which one might expect differential effects in the fu- ture.

From the perspective of mid-1991,1989 seems like a wonderful year politically for Eastern Europe. This is because the ending of the story in 1989 was clear. During the course of the year, however, some events often were unclear: One did not know whether demonstrations in a particular country would lead to democracy and freer markets or to bloody repression and regional instability-or potentially even to NATO and Warsaw bloc conflict. Demon- strations often can lead to stock market declines, not because market participants disagree with the demonstrators’ goals but because the situation could spin into social, political, and military chaos that would harm cash flows to firms listed on the exchanges. One can view this relation-

3. A substantial body of literature presents theo- retical arguments and empirical results suggesting that sterilized intervention is ineffective for more than a few days. However, the market reactions examined below focus on windows of one or two days in gen- eral. Further, in the absence of daily data on interven- tion and movements in the monetary base, the degree of short-run sterilization is unknown. In addition, whether sterilized intervention has the same limited effect for EMS members as it does for those outside pegging systems is unknown.

ship in terms of a simple finance model in which the value of a stock market equals the value of the expected cash flows to stock owners discounted by a risk-ad- justed rate, where the risk adjustment de- pends on the market’s beta on the world market (Brealey and Myers, 1988). There- fore, if the stock market falls in reaction to an unanticipated event, one interprets that as arising from a combination of falls in the expected cash flows or a rise in the risk-adjusted discount rate.

Whether the demonstrations were per se bad is unclear, but they suggested the pos- sibility of disruptions in cash flows. Vari- ous factors can harm cash flows-e.g., dis- ruption of production in the foreign coun- try experiencing the demonstrations and hence trade with that country and repatri- ation of profits from investments there, as well as military and political spillovers into neighboring countries. Further, com- panies in neighboring countries may ex- pect lower cash flows either due to in- creased taxes to finance aid, population flows, etc., or due to a lower-quality and more heterogeneous workforce expected in the f ~ t u r e . ~ Falls in expected cash flows do not imply that actual cash flows will necessarily fall in the future but that the probability they will fall has increased. In- dividual markets’ betas on the world mar- ket might be unaffected-West Germany’s beta, for example-but the risk premium on the world market still might rise. This will raise the discount rate used to value the expected cash flows. For both reasons, the individual markets will likely decline. The decline will be greater, however, the larger the impact of the disturbance on the individual market’s expected cash flows. On the other hand, one can expect that favorably resolving the danger will raise

4. German firms could well have expected to face a larger tax burden, lowerquality workers both from the DDR and from other Eastern European nations, and problems of combining workers having FDR work habits with workers having work habits developed under communist regimes.

24 CONTEMPORARY POLICY ISSUES

the value of the stock markets, particularly those most threatened by instability.

Clarifying the method used here is im- portant. The maintained hypothesis is that events in the East have effects on EC mem- bers that one can detect in financial data. An auxiliary hypothesis is that events cho- sen for the study were both significant and surprises and, hence, one can detect them in the data. Anticipated events’ effects are likely already incorporated in stock prices in forward-looking markets and, hence, the events have no apparent effect. The null hypothesis is that events in Eastern Europe had no differential effect on differ- ent countries’ markets. The alternative is that they had-and likely will continue to have-larger effects on Germany (on aver- age) than on EC members farther from Central Europe, such as Portugal, Spain, or even the United Kingdom. Similarly, one can expect the United States and the world as a whole to show smaller effect^.^ If events have little apparent influence, then one views them as violating the aux- iliary hypothesis rather than as throwing any light on the null of no differential ef- fects.6

5. On several occasions during the 1980s, actual and rumored Soviet political military moves regarding Poland led to falls in the DM as people switched to both U.S. dollars and gold. One could expect the United States to be involved in major problems in Cen- tral Europe. But evidently, the market reasonably viewed the United States as being less threatened than Germany.

6. Surely, few would argue against the maintained hypothesis that events in the East affect EC financial markets. One might view events having seemingly lit- tle reaction as supporting arguments for the null on the grounds that little reaction in all markets is con- sistent with the view of no differential reaction. One also might conclude that these events were important but not surprises and, hence, that their effects already were incorporated in the financial markets. Or the re- searcher might have picked events that were not im- portant. Note that the more incompetent the re- searcher, the larger the number of such events and the more one will likely fail to reject a false null if one counts events with little reaction as favoring the null. (This is similar to the problem in event studies whereby choosing the wrong window or too long or too short a window biases the test against rejecting a false null of no effect.) Instead, one might argue that events having major reactions are the discriminating tests and that one should ignore the others.

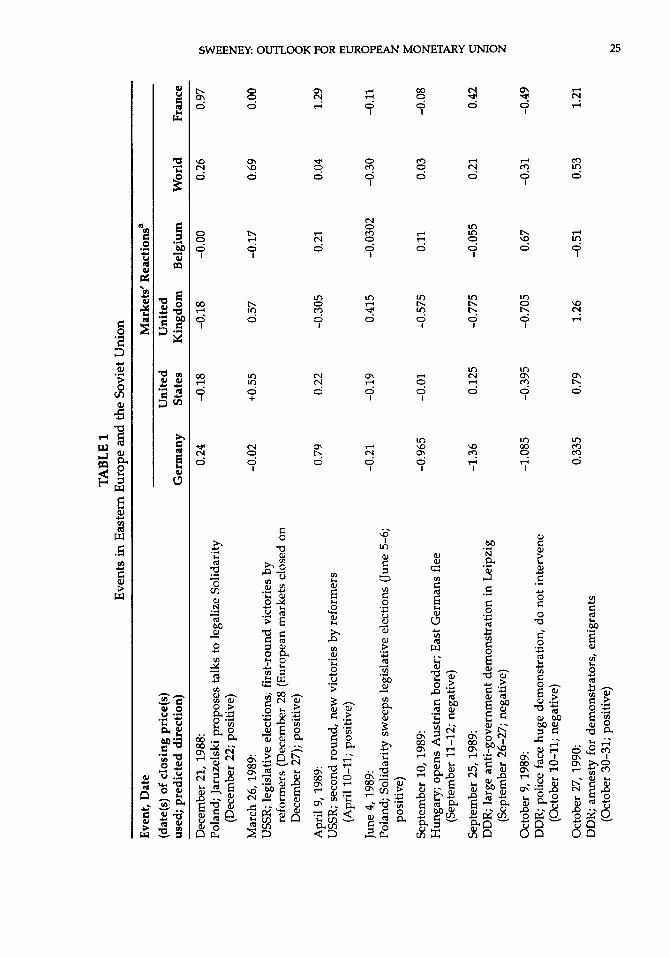

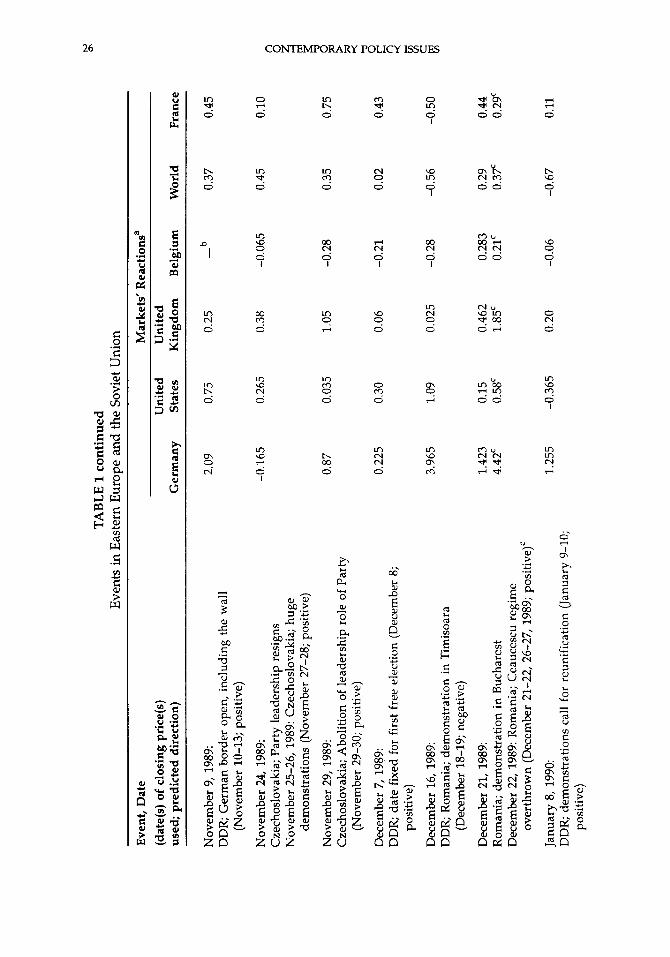

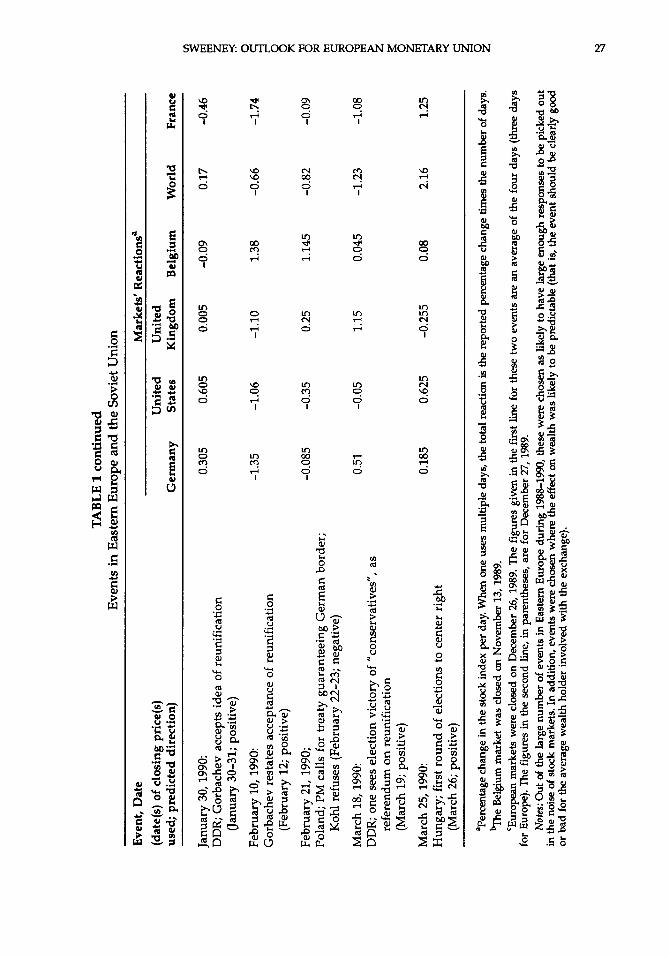

Table 1 lists some eastern disturbances along with their expected effects and the actual stock market returns (in domestic currencies) around the events.’ The author chose the events before examining the data. The events selected, which came from a much more extensive list, were those having economic implications that might show up in the data-implications that might be signed u priori. (The author made predictions before examining the data*.) Researchers sometimes adjust raw returns, such as those in table 1, so as to account for overall market moves on the days in question. A common adjustment is to subtract some broader index. As an ap- proximate adjustment for the European in- dexes, one can subtract either the Stan- dard & Poor’s return or the world return.

One cannot expect an entirely clear message from an indicator having as much noise as do stock markets. Never- theless, some patterns seemingly exist. These disturbances mostly affected Euro- pean markets, and one can see that the effects of some events were larger for Ger- many than they were for other western countries.

7. The study used data from the Wall Street Iournal for four stock market indexes (chosen before examin- ing the data): the Frankfurt DAX, the Standard & Poor’s 500, the London €T-30 Share, and the Brussels Stock Index. The study used Goldman-Sachs data for France’s stock market and the world stock market. The two data sources gave virtually identical numerical re- sults.

Table 1 shows the dates of the prices used to cal- culate the markets’ reactions. The study often used two days so as to allow the market a chance to adjust fully to information that might not have immediately clear implications. Reactions are reported as an average per day. The study took further account of the fact that many events occurred during the evening or during weekends or holidays when the markets were closed. Generally, the author decided on the dates to use be- fore examining the data.

8. Predictions such as these always must be some- what tentative. One reason is that the reaction to, say, an election should depend on the surprise content of the election. The issue is not whether the results were ”good in the market’s view but whether they were better or worse than expected. One might argue, then, that wrong signs are due to the researcher’s incompe- tence in signing effects rather than evidence against the null of differential effects.

TABLE 1

Eve

nts

in E

aste

rn E

urop

e and

the

Sovi

et U

nion

Eve

nt, D

ate

Mar

kets

' Rea

ctio

nsa

(dat

e(s)

of c

losi

ng p

rice

@)

Uni

ted

Uni

ted

used

; pre

dict

ed d

irec

tion

) G

erm

any

Stat

es

Kin

gdom

B

elgi

um

Wor

ld

Fran

ce

Dec

embe

r 21,

1988

: Po

land

; Jar

uzel

ski p

ropo

ses

talk

s to

lega

lize

Solid

arity

Mar

ch 2

6, 19

89:

USS

R; le

gisl

ativ

e el

ectio

ns, f

irst-r

ound

vic

torie

s by

(Dec

embe

r 22;

posi

tive)

refo

rmer

s (D

ecem

ber 2

8 (E

urop

ean

mar

kets

clo

sed

on

Dec

embe

r 27)

; po

sitiv

e)

Apr

il 9,

1989

: U

SSR;

sec

ond

roun

d, n

ew v

icto

ries

by r

efor

mer

s

June

4,1

989:

Po

land

; Sol

idar

ity s

wee

ps le

gisl

ativ

e el

ectio

ns (

June

5-6

;

Sept

embe

r 10,

198

9:

Hun

gary

; op

ens

Aus

tria

n bo

rder

; Ea

st G

erm

ans

flee

Sept

embe

r 25,

1989

: D

DR;

lar

ge a

nti-

gove

rnm

ent

dem

onst

ratio

n in

Lei

pzig

Oct

ober

9, 1

989:

D

DR;

pol

ice

face

hug

e de

mon

stra

tion,

do

not

inte

rven

e

Oct

ober

27,

1990

: D

DR;

am

nest

y fo

r de

mon

stra

tors

, em

igra

nts

(Apr

il 10-11; p

ositi

ve)

posi

tive)

(Sep

tem

ber

11-1

2;

nega

tive)

(Sep

tem

ber 2

6-27

; ne

gativ

e)

(Oct

ober

10-

11;

nega

tive)

(Oct

ober

30-

31;

posi

tive)

0.24

-0

.18

-0.1

8 -0

.00

0.26

0.

97

-0.0

2 +0

.55

0.57

-0

.17

0.69

0.

00

0.79

0.

22

-0.3

05

0.21

0.

04

1.29

-0.2

1 -0

.19

0.41

5 -0

.030

2 -0

.30

-0.1

1

-0.9

65

-0.0

1 -0

.575

0.

11

0.03

-0

.08

-1.3

6 0.

125

-0.7

75

-0.0

55

0.21

0.

42

-1.0

85

-0.3

95

-0.7

05

0.67

-0

.31

-0.4

9

0.33

5 0.

79

1.26

-0

.51

0.53

1.

21

t;:

TABL

E 1

cont

inue

d E

vent

s in

Eas

tern

Eur

ope and

the

Sovi

et U

nion

Even

t, D

ate

Mar

kets

' Rea

ctio

nsa

(dat

e(s)

of c

losi

ng p

rice

(s)

Uni

ted

Uni

ted

used

; pr

edic

ted

dire

ctio

n)

Ger

man

y St

ates

K

ingd

om

Bel

gium

W

orld

Fr

ance

Nov

embe

r 9,1

989:

2.

09

DD

R; G

erm

an b

orde

r op

en, i

nclu

ding

the

wal

l (N

ovem

ber

10-1

3; p

ositi

ve)

Nov

embe

r 24,

1989

: -0

.165

C

zech

oslo

vaki

a; P

arty

lead

ersh

ip re

sign

s N

ovem

ber 2

5-26

,198

9: C

zech

oslo

vaki

a; h

uge

Nov

embe

r 29,

198

9:

0.87

C

zech

oslo

vaki

a; A

bolit

ion

of l

eade

rshi

p ro

le o

f Pa

rty

Dec

embe

r 7,

198

9:

0.22

5 D

DR

; dat

e fix

ed f

or f

irst

fre

e el

ectio

n (D

ecem

ber

8;

Dec

embe

r 16

, 198

9:

3.96

5 D

DR

; R

oman

ia; d

emon

stra

tion

in T

imis

oara

dem

onst

rati

ons

(Nov

embe

r 27

-28;

pos

itive

)

(Nov

embe

r 29

-30;

pos

itive

)

posi

tive)

(Dec

embe

r 18

-19;

neg

ativ

e)

Dec

embe

r 21

,198

9:

1.42

3 R

oman

ia; d

emon

stra

tion

in B

ucha

rest

4.

42'

Dec

embe

r 22

, 198

9: R

oman

ia; C

eauc

escu

reg

ime

Janu

ary

8, 1

990:

1.

255

DD

R;

dem

onst

rati

ons c

all

for

reun

ific

atio

n (J

anua

ry 9-

10;

over

thro

wn

(Dec

embe

r 21

-22,

26-

27,

1989

; pos

itive

)'

posi

tive)

0.75

0.26

5

0.03

5

0.30

1.09

0.15

0.

58'

-0.3

65

0.25

0.38

1.05

0.06

0.02

5

0.46

2 1.

85'

0.20

b -

-0.0

65

-0.2

8

-0.2

1

-0.2

8

0.28

3 0.

21'

-0.0

6

0.37

0.45

0.35

0.02

-0.5

6

0.29

0.

3F

-0.6

7

0.45

8 0.

43

E z E

-0.5

0

0.44

0.

29'

0.11

TABL

E 1

cont

inue

d E

vent

s in

Eas

tern

Eur

ope and

the

Sovi

et U

nion

Even

t, D

ate

(dat

e(s)

of c

losi

ng p

rice

@)

used

; pr

edic

ted

dire

ctio

n)

Mar

kets

' R

eact

ions

a U

nite

d U

nite

d G

erm

any

Stat

es

Kin

gdom

B

elgi

um

Wor

ld

Fran

ce

Janu

ary

30,1

990:

D

DR

; Gor

bach

ev a

ccep

ts id

ea o

f re

unif

icat

ion

Febr

uary

10,

1990

: G

orba

chev

rest

ates

acc

epta

nce

of r

euni

fica

tion

(Jan

uary

30-

31;

posi

tive)

(Feb

ruar

y 12

; po

sitiv

e)

v)

0 2

-1.3

5 -1

.06

-1.1

0 1.

38

-0.6

6 -1

.74

8 71:

Febr

uary

21,

1990

; -0

.085

-0

.35

0.25

1.

145

-0.8

2 -0

.09

Pola

nd; P

M c

alls

for

trea

ty g

uara

ntee

ing

Ger

man

bor

der;

2

(Mar

ch 19

; po

sitiv

e)

8

Koh

l ref

uses

(Fe

brua

ry 2

2-23

; ne

gativ

e)

0 k!

Mar

ch 1

8,19

90:

0.51

-0

.05

1.15

0.

045

-1.2

3 -1

.08

DD

R; o

ne s

ees

elec

tion

vict

ory

of "c

onse

rvat

ives

", a

s re

fere

ndum

on

reun

ific

atio

n

5 j;r 8

Mar

ch 2

5, 19

90:

0.18

5 0.

625

-0.2

55

0.08

2.

16

1.25

H

unga

ry;

firs

t rou

nd o

f el

ectio

ns to

cen

ter

righ

t

i (M

arch

26;

posi

tive)

aPer

cent

age c

hang

e in

the

stoc

k in

dex

per

day.

Whe

n on

e us

es m

ultip

le d

ays,

the

tota

l rea

ctio

n is

the

repo

rted

per

cent

age

chan

ge ti

mes

the

num

ber

of da

ys.

%e

Bel

gium

mar

ket

was

clo

sed

on N

ovem

ber 13,1989.

'Eur

opea

n m

arke

ts w

ere

clos

ed o

n D

ecem

ber 26, 1989. T

he f

igur

es g

iven

in t

he f

irst

line

for

thes

e tw

o ev

ents

are

an

aver

age

of t

he f

our

days

(thr

ee d

ays

for

Euro

pe).

The

figu

res

in th

e se

cond

line

, in

pare

nthe

ses,

are

for

Dec

embe

r 27,1989.

Note

s: O

ut o

f th

e la

rge

num

ber

of ev

ents

in E

aste

rn Europe

duri

ng 1988-1990,

thes

e w

ere

chos

en a

s lik

ely

to h

ave

larg

e en

ough

resp

onse

s to

be

pick

ed o

ut

in th

e no

ise

of st

ock

mar

kets

. In

addi

tion,

eve

nts

wer

e ch

osen

whe

re th

e ef

fect

on

wea

lth w

as li

kely

to b

e pr

edic

tabl

e (t

hat i

s, th

e ev

ent

shou

ld b

e cl

earl

y go

od

or b

ad f

or th

e av

erag

e w

ealth

hol

der

invo

lved

with

the

exch

ange

).

28 CONTEMPORARY POLICY ISSUES

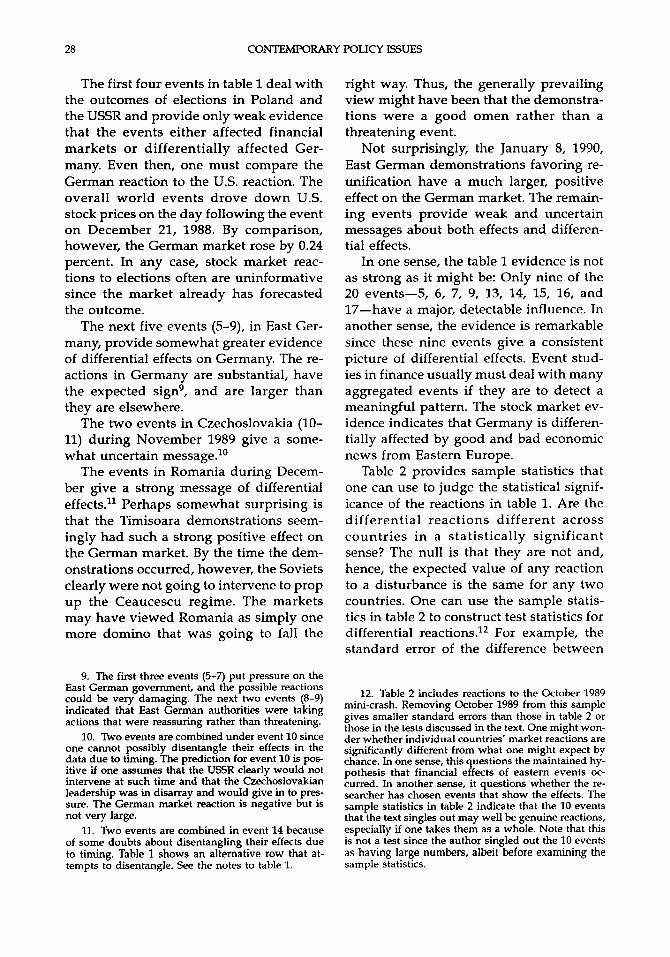

The first four events in table 1 deal with the outcomes of elections in Poland and the USSR and provide only weak evidence that the events either affected financial markets or differentially affected Ger- many. Even then, one must compare the German reaction to the U.S. reaction. The overall world events drove down U.S. stock prices on the day following the event on December 21, 1988. By comparison, however, the German market rose by 0.24 percent. In any case, stock market reac- tions to elections often are uninformative since the market already has forecasted the outcome.

The next five events (5-9), in East Ger- many, provide somewhat greater evidence of differential effects on Germany. The re- actions in Germany are substantial, have the expected sign9, and are larger than they are elsewhere.

The two events in Czechoslovakia (10- 11) during November 1989 give a some- what uncertain message.'O

The events in Romania during Decem- ber give a strong message of differential effects." Perhaps somewhat surprising is that the Timisoara demonstrations seem- ingly had such a strong positive effect on the German market. By the time the dem- onstrations occurred, however, the Soviets clearly were not going to intervene to prop up the Ceaucescu regime. The markets may have viewed Romania as simply one more domino that was going to fall the

9. The first three events (5-7) put pressure on the East German government, and the possible reactions could be very damaging. The next two events (8-9) indicated that East German authorities were taking actions that were reassuring rather than threatening.

10. Two events are combined under event 10 since one cannot possibly disentangle their effects in the data due to timing. The prediction for event 10 is pos- itive if one assumes that the USSR clearly would not intervene at such time and that the Czechoslovakian leadership was in disarray and would give in to pres- sure. The German market reaction is negative but is not very large.

11. Two events are combined in event 14 because of some doubts about disentangling their effects due to timing. Table 1 shows an alternative row that at- tempts to disentangle. See the notes to table 1.

right way. Thus, the generally prevailing view might have been that the demonstra- tions were a good omen rather than a threatening event.

Not surprisingly, the January 8, 1990, East German demonstrations favoring re- unification have a much larger, positive effect on the German market. The remain- ing events provide weak and uncertain messages about both effects and differen- tial effects.

In one sense, the table 1 evidence is not as strong as it might be: Only nine of the 20 events-5, 6, 7, 9, 13, 14, 15, 16, and 17-have a major, detectable influence. In another sense, the evidence is remarkable since these nine events give a consistent picture of differential effects. Event stud- ies in finance usually must deal with many aggregated events if they are to detect a meaningful pattern. The stock market ev- idence indicates that Germany is differen- tially affected by good and bad economic news from Eastern Europe.

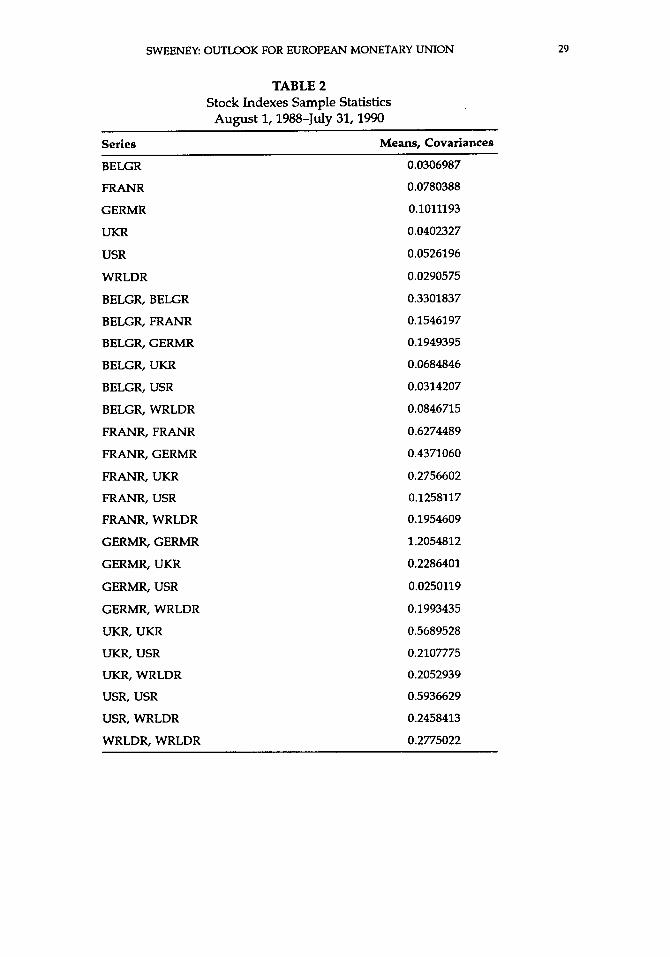

Table 2 provides sample statistics that one can use to judge the statistical signif- icance of the reactions in table 1. Are the differential reactions different across countries in a statistically significant sense? The null is that they are not and, hence, the expected value of any reaction to a disturbance is the same for any two countries. One can use the sample statis- tics in table 2 to construct test statistics for differential reactions.'* For example, the standard error of the difference between

12. Table 2 includes reactions to the October 1989 minicrash. Removing October 1989 from this sample gives smaller standard errors than those in table 2 or those in the tests discussed in the text. One might won- der whether individual countries' market reactions are significantly different from what one might expect by chance. In one sense, this questions the maintained hy- pothesis that financial effects of eastern events oc- curred. In another sense, it questions whether the re- searcher has chosen events that show the effects. The sample statistics in table 2 indicate that the 10 events that the text singles out may well be genuine reactions, especially if one takes them as a whole. Note that this is not a test since the author singled out the 10 events as having large numbers, albeit before examining the sample statistics.

SWEENEY OUTLOOK FOR EUROPEAN MONETARY UNION 29

TABLE 2 Stock Indexes Sample Statistics

Series Means, Covariance8

August 1,1988-July 31,1990

BELGR

FRANR

GERMR

UKR

USR

WRLDR

BELGR, BELGR

BELGR, FRANR

BELGR, GERMR

BELGR, UKR

BELGR, USR

BELGR, WRLDR

FRANR, FRANR

FRANR, GERMR

FRANR, UKR

FRANR, USR

FRANR, WRLDR

GERMR, GERMR

GERMR, UKR

GERMR, USR

GERMR, WRLDR

UKR, UKR

UKR, USR

UKR, WRLDR

USR, USR

USR, WRLDR

WRLDR, WRLDR

0.0306987

0.0780388

0.1011193

0.0402327

0.0526196

0.0290575

0.3301837

0.1546197

0.1949395

0.0684846

0.0314207

0.0846715

0.6274489

0.4371060

0.2756602

0.1258117

0.1954609

1.2054812

0.2286401

0.0250119

0.1 993435

0.5689528

0.2107775

0.2052939

0.5936629

0.2458413

0.2775022

30 CONTEMPORARY POLICY ISSUES

German and French market returns for the sample data from August 1, 1988, to July 31, 1990, is 0.979 percent. Events 6, 9, 13, and 14 (both versions) have differences of more than twice this value. Examining av- erage differential reactions makes more sense than examining individual events. The average of the absolute differences for the nine events singled out above13 is 1.4067 percent and the standard error for the sum is 0.325 percent. Therefore, the sum is 4.31 standard errors from The choice here for comparison was France since it had the largest non-Ger- man variance, which increases the stan- dard error and, hence, favors the null of no difference. (A referee also suggested ex- amining France.) One can easily make any other statistical comparisons.

Note that the differential stock market reactions suggest that exchange rate pres- sures exist but do not necessarily indicate the direction of the pressures. One would be hard pressed to imagine a series of shocks that affect German but not other EC stock markets and, at the same time, put no pressure on the German exchange rate. But one need not think that a one-to- one relationship exists between stock mar- ket and exchange rate movements. One can easily construct examples where a rise in the stock market might be due to shocks that require exchange rate appreciation in some cases and require depreciation in others.15

13. In one sense, this is not a clean test since the author singled out these events as having large Ger- man market reactions. On the other hand, including events having small German reactions risks biasing the test in favor of a false null, as discussed above.

14. This calculation uses the smaller of the two values for event 14. Using the larger value leads to an average absolute value of differential reactions of 1.7397, which is 5.353 standard errors from zero.

15. Sweeney (1990a) presents evidence for the Group of Ten plus Switzerland that, on average, move- ments in the U.S. real exchange rate are uncorrelated with real domestic currency changes in these countries’ stock markets. Sweeney (199Ob) interprets this as showing that sometimes the relationship is pos- itive and sometimes it is negative, rather than that no relationship exists.

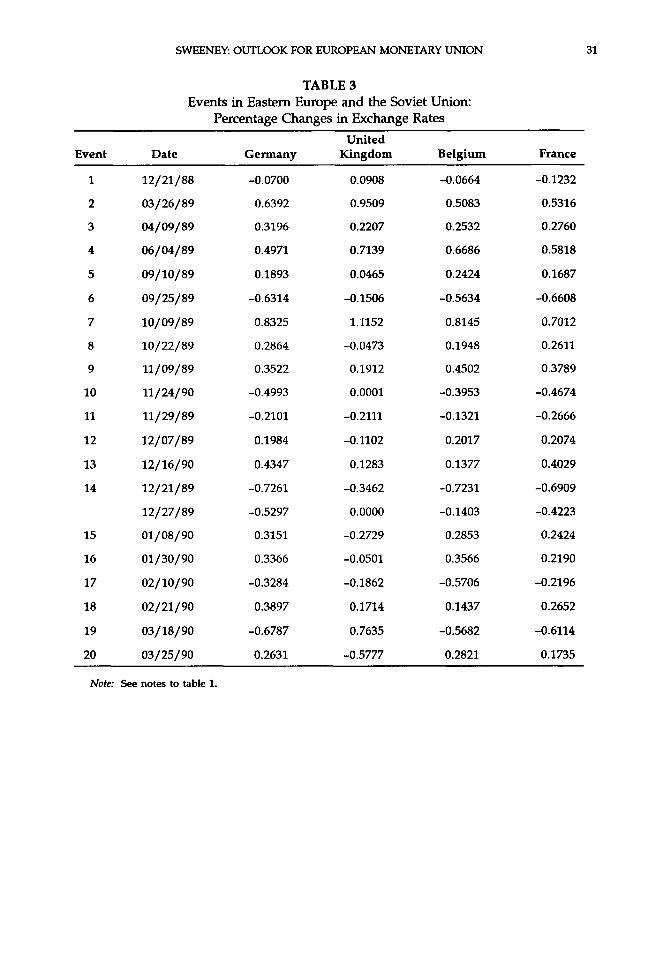

8. Differential Effects in Exchange Marked6 Table 3 shows the exchange rate

changes for the four EC currencies relative to the U.S. dollar for the same events as in table 1. One can see that detecting system- atic differential effects is quite difficult. Examining the nine events in which no- ticeable stock market reactions occurred shows French and German exchange rates moving in much the same way. As noted above, this is not unexpected in a system of pegged rates such as the EMS since de- tecting pressures would require data on intervention, and such data are not avail- able. Interestingly, the differential effects between the rate for the United King- dom-which was not in the EMS-and the rate for either France or Germany were larger than the differential effects between these latter two rates.

C. Optimum Currency Area Theory Conventional optimum currency area

theory suggests that the possibility of east- ern shocks with differential effects on EC members reduces the benefits of monetary union to the EC.I7 The optimum currency area literature views countries as subject to disturbances requiring changes in rela- tive national income and price levels or in

16. A referee suggested adding this subsection. Earlier drafts had not considered exchange rates due to difficulties of interpreting their movements when intervention occurred and data on intervention are un- available. The author made this earlier decision with- out examining any exchange rate data.

17. See Tower and Willett (1976) for an excellent survey of the older literature on optimum currency areas. See Wihlborg and Willett (1990) for an update. A referee pointed out that one cannot be certain the differential shocks would have the same effects on out- put and labor under a regime of permanently pegged rates or a common currency as it would under a man- aged float regime. Given either type of currency area, behavior in output and labor markets might show more flexibility when one clearly cannot expect ex- change rates to substitute for flexibility. This applies the Lucas critique and certainly is possible. The diffi- culties that the increase in differential shocks cause due to changes in the East still remain.

SWEENEY: OUTLOOK FOR EUROPEAN MONETARY UNION 31

TABLE 3 Events in Eastern Europe and the Soviet Union:

Percentage Changes in Exchange Rates

Event Date Germany Kingdom Belgium France United

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

12/21/88

03/26/89

04/09/89

06/04/89

09/10/89

09/25/89

10/09/89

10/22/89

11 / 09/ 89 11/ 24/90

11/ 29/ 89

12/ 07/ 89

12/16/90

12/21/89

12/ 27/ 89

01/08/90

01/30/90

02/ 10/90

02/21/90

03/18/90

03/25/90

-0.0700

0.6392

0.3196

0.4971

0.1893

-0.631 4

0.8325

0.2864

0.3522

-0.4993

-0.2101

0.1984

0.4347

-0.7261

-0.5297

0.3151

0.3366

-0.3284

0.3897

-0.6787

0.2631

0.0908

0.9509

0.2207

0.7139

0.0465

-0.1506

1.1152

-0.0473

0.1912

0.0001

-0.2111

-0.1102

0.1283

-0.3462

0.0000

-0.2729

-0.0501

-0.1862

0.1714

0.7635

-0.5777

-0.0664

0.5083

0.2532

0.6686

0.2424

-0.5634

0.8145

0.1948

0.4502

-0.3953

-0.1321

0.2017

0.1377

-0.7231

-0.1403

0.2853

0.3566

-0.5706

0.1437

-0.5682

0.2821

-0.1232

0.5316

0.2760

0.5818

0.1687

-0.6608

0.7012

0.2611

0.3789

-0.4674

-0.2666

0.2074

0.4029

-0.6909

-0.4223

0.2424

0.2190

-0.2196

0.2652

-0.6114

0.1735

Note: See notes to table 1.

32 CONTEMPORARY POLICY ISSUES

the real exchange rate.18 Changing ex- change rates is a cheaper and quicker way to change relative national price levels than is relying on changes in output prices with given exchange rates.Ig (This view of the world enjoys much empirical support but clearly is out of sync with models of rational expectations, perfect price flexi- bility, and continuous market clearing.)

Because some countries view as low the costs of forming a currency area, they may give up the flexibility of adjusting rates and incur the prospective costs of adjust- ing prices.20 The EC members may believe that if they are joined together, then they face mostly disturbances from the outside and relatively few disturbances among members. They also may believe that the outside disturbances will fall relatively evenly on members and will not require relative national price-level adjustments among members. Changing the exchange rate of the community as a whole relative to that of the rest of the world can handle the outside disturbances. Disturbances among members will require painful price adjustment. But the disturbances that hit,

18. The price levels considered here are broad in- dexes such as CPIs, PPIs, or GNP deflators rather than simply goods in current international trade. Shafer (1990) cites several important sources of pressure- though not disturbances from Eastern Europe-in dis- cussing the need for real exchange rate adjustments within the EC.

19. Note that this line of argument favors managed flexibility-rather than free-floating or permanently fixed rates-as optimal in the absence of any other costs or benefits. If exchange rates are subject to band- wagons or other types of destabilizing speculation, or if the extent of stabilizing speculation is inadequate, then optimal government intervention may be sub- stantial. If exchange markets are functioning well, then little need for intervention may exist. Sweeney (1991) examines the implications of the speed of adjustment of European real exchange rates for the desirability of an EMU.

20. Factor mobility can substitute-albeit only im- perfectly-for exchange rate flexibility. If equilibrium with given resource allocations across regions requires a change in the real exchange rate and the nominal rate is pegged with price adjustment sluggish, then capital or labor might relocate so as to reduce or elim- inate the need for real rate changes. These factor move- ments are not free. Many observers would argue that real rate adjustment is cheaper.

say, France from Italy and Germany may tend to cancel in the aggregate and thus leave no need for adjusting the French price level. According to this argument, each EC country on average may find that its net exchange rate pressure from distur- bances in EC members is near zero.’l

The possible benefits of a currency union include the discipline argument. If high and possibly erratic inflation imposes costs (Logue and Willett, 1975; Logue and Sweeney, 1981)) then a country prone to this type of price behavior due to mone- tary and fiscal policy may want to tie its policymakers’ hands through the disci- pline of maintaining fixed rates. This is the case even if other conditions favoring union are only weak or are, to some extent, negative. Some observers also focus on micro benefits-for example, the saving on exchange rate transaction costs if a group of countries adopts a common cur- rency (Gros and Thygeson, 1990).

The point one can draw from stock markets’ reactions to Eastern European developments since 1988 is that the ob- served pattern of shocks, along with what one can guess about future disturbances, weakens the argument for fixed rates. Ger- many has had, on average, the largest ab- solute reaction to eastern developments. Given the shocks, one should have ex- pected this differential reaction based on simple geography as well as on economic, historical, and cultural ties. Because of these same reasons, one should expect dif- ferential impacts of disturbances in the fu- ture.

The nature of shocks is that one cannot forecast them. Nevertheless, one can easily illustrate what might happen. Germany has an extensive border with Poland and

21. Therefore, a member of an optimum currency area faces many shocks from within the area that tend, on average, to cancel. In finance terms, the risk from other currency area members is diversifiable. The stock market results above suggest that a major fraction of disturbances from Eastern Europe are non-diversifiable for Germany.

SWEENEY OUTLOOK FOR EUROPEAN MONETARY UNION 33

is the only EC member with a Polish bor- der. Poland is embarked on an economy- wide attempt to pull back from economic decline and, indeed, the threat of eco- nomic chaos. What economic mistakes Po- land may make in this attempt is unclear. Some observers believe that if things go well, the Polish standard of living may be back to the level of early 1988-not a very exalted one at that-in five years. In these circumstances, whether democracy will prevail in Poland is not at all clear. One possibility is vast social unrest leading to a government willing to confront Ger- many on several issues, including the Ger- man minority in Poland. (Apparently, the German government now accepts the cur- rent border with Poland, and so this pos- sible dispute is out of the way.) Another possibility is civil war, though that pros- pect is quite grim and perhaps unlikely. These possibilities seemingly put more pressure on Germany than on other EC members. Why problems on Germany’s borders should have the same effect on Ireland or Portugal-or even the United Kingdom-as they do on Germany is un- clear.

Germany is not the only country subject to such differential shocks. Italy has a bor- der with Yugoslavia and is across the nar- row Adriatic Sea from both Yugoslavia and Albania. What will happen in Yugo- slavia is quite unclear. But one thing is clear: Many of the bad things that can hap- pen have a much larger potential for pull- ing in Italy and Greece than for pulling in the United Kingdom or even Germany.

A worthwhile exercise is to work out the exchange rate implications of some of these possible differential shocks. Suppose things go really wrong in Poland and most view this as a major threat to Germany. One can expect to see capital flee Ger- many. This capital flight would be facili- tated by removing all capital controls within the EC, a process that has occurred in most countries-Ireland and Spain have until the end of 1992-and is scheduled for

all by the end of 1995. This puts down- ward pressure on the DM, not only rela- tive to the U.S. dollar but also relative to other EC members who are less troubled by the hypothetical shock. The only solu- tion is reducing the German real exchange rate relative not only to the U.S. rate but also to other EC members’ rates. Under currency union, Germany cannot devalue the DM to reduce its real exchange rate. Instead, Germany must force down its real exchange rate by imposing a (relative) de- flation on its price level. This necessity for deflation may occur when prices are under extra upward pressure. One can imagine that German output prices might rise during troubled times due to a desire to shift from financial assets within Ger- many to real assets. For example, the prices of cars may rise. Under optimum currency area views of sluggish adjust- ment, this need for relative deflation will likely lead to a recession in Germany. In the face of the initial upward pressure on German prices, this will result in stagfla- tion. In turn, the German contraction will likely spread to the rest of the EC as a recession. The Bundesbank may well have the iron to impose all this on itself and its neighbors to maintain its fixed rates.

Change the example a bit. Suppose that the DM starts out strong in the EC-due partly to Germany’s relatively better infla- tion performance-so that downward pressure on other EC members‘ exchange rates already exists. Now things go quite well in Eastern Europe, and Germany is the main economic beneficiary. This puts upward pressure on the DM, and the real German exchange rate must appreciate. Germany, committed to fixed rates, cannot appreciate the DM. Germany could engi- neer rises in the country’s prices. Or it could, in effect, tell its EC partners that they must force (relative) disinflation on their prices. Since the partners, by as- sumption, already are feeling inflationary pressures, this is an unwelcome message.

34 CONTEMPORARY POLICY ISSUES

Will they depreciate or pay the price in a recession? The answer is unclear.

Precisely because the answer is unclear, wealth holders will judge the EC commit- ment to fixed rates as less than fully cred- ible. During times of pressure, wealth holders will pull funds out of countries judged likely to devalue. This is now a trivial matter due to removing capital con- trols. Further, strong incentives exist to take open positions against a currency whose government is committed-but not credibly-to maintaining a parity. Lack of capital controls will facilitate these open positions. This will put upward pressure on the interest rates on assets denomi- nated in the suspect currency as specula- tors try to borrow these funds so as to move into stronger currencies. To be sure, the forward rate will depreciate to main- tain covered interest rate parity on high- quality, short-term money market instru- ments. This is simply a sign of the current high degree of financial market integra- tion among developed countries with open financial markets. Speculative runs have much greater potential to force parity changes now than they have had in the past. One central banker estimates that the foreign exchange markets-spot and for- ward-routinely deal with between $750 billion and $1 trillion in transactions per day.

111. "PERMANENTLY" FIXED RATES VERSUS A COMMON CURRENCY

EMS members now are in a stage of monetary union whereby they are sup- posed to confine intra-EMS exchange rate movements to pre-specified bands. The EC members have agreed that stage two of the transition to EMU will start in Jan- uary 1994. During this stage, EC members will place progressively tighter bands on exchange rate movements. Policymakers envision a third stage of a common cur- rency. EC members have not formally agreed to move to a common currency, and the move may be postponed or even

abandoned due to events. Apparently, however, the EC now favors a common currency over a system of permanently pegged exchange rates. Plans are to create a European central bank-the Eurofed- shortly after starting stage two. As such, national central banks gradually will give up some and perhaps all control over monetary policy. In any stage three with a common currency, the national central banks will be reduced to important but mundane matters such as administering the payments system. (On a European cen- tral bank, see the papers in Canzoneri et al., 1991.) EC members met in December 1990 to discuss the EMU and to draw up a new treaty for European economic and monetary union. In April 1990, the EC heads of state agreed that the national par- liaments should ratify the treaty by the end of 1992 (Economist, July 7-13, 1990).

As section I1 discussed, the outlook for the 1990s reduces the benefits of monetary union that one could foresee when discus- sion began during the 1980s. Momentum seemingly is on the side of the EMU, how- ever. Recently, the United Kingdom has indicated it may be more willing to partic- ipate and has joined the EMS. Therefore, one should consider the design of a union in circumstances where its value is les- sened and it faces greater trials.

"Permanently" fixed exchange rates may be a contradiction in terms. By the very nature of governments' need to take positive actions so as to keep the rates fixed, the alternative of allowing the rates to change always exists. Governments change rates by altering parities, by going to free floating, or by going to a managed float. As long as independent national cen- tral banks exist, parity changes always are possible. When maintaining the peg is nei- ther difficult nor costly for governments, confidence is high that governments will maintain the peg. The crux is periods of high costs and, therefore, hard choices. An unstable mechanism may exist here. The less confidence private market partici-

SWEENEY OUTLOOK FOR EUROPEAN MONETARY UNION 35

pants have in the peg, the more they spec- ulate against it and, thus, the more diffi- cult maintaining the rate becomes. On the government side, the more difficult main- taining the rate becomes, the more likely the government will give in and change the rate. This feeds back to generate an even larger volume of speculation. In practical terms, the financial integration and capital mobility of the 1990s support arguments that the only limit on open po- sitions that speculators may be able to take is their willingness to endure exchange rate exposure and face interest rate differ- entials. Discussions of the 1950s and 1960s point out that the exchange rate risk is minimal. This is the one-way speculative option, whereby the currency may go down (giving the speculator exchange rate profits) or stay the same (costing the spec- ulator only the interest rate differential over perhaps a very short time) but surely will not go up (ensuring no possibility of exchange rate losses).

Credibility is much stronger under a common currency. To change parities, a government also must introduce a new currency and revise the payments sys- tem-perhaps extensively. The govern- ment can do both, but at great cost. Fur- ther, the transition will likely lead to dis- ruptions. For example, wealth holders may well believe that capital controls are in the offing or that new taxes or restric- tions are likely. As a result, they may be anticipating capital outflows as well as trade and production disruptions. The benefits of dropping the common cur- rency and altering the rate are the same as the benefits of altering a "permanently" fixed rate. The costs under a common cur- rency are substantially higher, however. This relatively poorer benefit-cost ratio is what gives a common currency the credi- bility advantage. The high costs of aban- doning the common currency are a way of giving credibility to precommitment.

From the viewpoint of establishing a successful monetary union, a common

currency strongly dominates fixed rates on credibility grounds. This is particularly important in a world where capital mobil- ity is very high and the EC is committed to removing all capital controls. Other benefits exist at the micro level. For exam- ple, a common currency avoids the foreign exchange transactions occurring under fixed rates, though these costs are likely substantially lower under credibly fixed rates-that is, during times of few pres- sures-than they are under floating rates.

This argument suggests that the appar- ent momentum to commit ultimately to a common currency makes sense if the alter- native is trying to maintain permanently pegged rates. By the same logic, limiting the duration of stage two-under which rates are pegged-and introducing a com- mon currency early allows less time for things to occur that might derail currency union.

The major cost of a common currency may be a loss of discipline. The Bun- desbank has the reputation as the most conservative and most anti-inflation of the EC central banks, though other EC central banks have appeared even tougher during certain periods and some non-EC central banks also have enviable records. For dis- cussion purposes, assume the Bundesbank is the most conservative EC central bank in the long run. (For evidence supporting this view, see Banaian et al., 1983, and Burdekin and Willett, 1990.) In the EMS, then, the Bundesbank can-to a fair de- gree-set the pace for monetary expansion and inflation. Other members of the EMS will lose reserves if they try to expand the money stock at a rate too far out of line with the actions of the Bundesbank. They must either fall in line or alter their parity. The latter alternative weakens the credi- bility of the EMS. In the end, countries must either go along with Bundesbank conservatism or adjust their parities. If parity adjustments are at all common, then the EMS loses credibility and will likely collapse. This is the Bundesbank's ulti-

36 CONTEMPORARY POLICY ISSUES

mate threat: Do what the Bundesbank war& in terms of conservative monetary policy or face the possibility of the EMS falling apart.

To be sure, EMS rules do not require that the country with its currency under downward pressure be the only one to in- tervene. The Bundesbank also could pur- chase that currency. In practice, however, the Bundesbank has the option of refusing to intervene. The Bundesbank’s traditional independence from the German federal government gives both the bank and the government the ability to resist pressure to prop up other currencies if they wish to abstain. The government always can maintain that it can do very little to force the Bundesbank to intervene. Of course, many instances and many reasons exist for the Bundesbank to give in and expand more than it might wish. Clearly, though, it has substantial veto powers over exces- sive European monetary expansion.

The Bundesbank is not the only finan- cially prudent central bank. The Banque de France has performed quite well on the discipline front since the mid-1980s. Nev- ertheless, the Bundesbank has the longest and most credible record of prudence among the central banks. (Evidence exists that central banks with the greatest auton- omy tend to have the best inflation perfor- mance. See Banaian et al., 1983,1988.) The trade-offs of restrictive versus expansion- ary monetary policy suggest that one should give the most weight to the views of the Bundesbank and of those banks with similar viewpoints.

The shape of a European central bank under a common currency is unclear at this point.22 The Delors report calls for cre- ating an “independent” central bank. Draft statutes call for making the Eurofed’s directors politically indepen-

22. See H a w (1990) for an interesting discussion of how to set up institutions so as to achieve an effec- tive, low-inflation Eurofed. The Economist (July 7-13, 1990) discusses some current debates over the Eurofed.

dent and also for making price-level sta- bility the Eurofed’s single objective (Econ- omist, November 17, 1990, p. 87). How ef- fective implementing such independence would be is unclear.23 One thing seems clear, however: The Bundesbank will lose its ability to force other members to choose between doing what it wants or allowing the system to collapse. Clearly, central bank decisions would result from political discussions in which the Bundesbank’s backing from an inflation- fearing German population would carry a smaller role than it does presently. Instead, Bundesbank power would depend more on the size of Germany’s economy and the backing of the German government. Cer- tainly, the bias toward inflation of a com- mon currency would be greater than that of the DM under the EMS.24 Further, when a system of fixed rates is working, the Bundesbank may well be able to force a lower average inflation rate than it can under a common currency.

IV. CONCLUSIONS

The EMS’S success has surprised many observers. Substantial support now exists for a broader European Monetary Union with either permanently fixed exchange rates or a common currency. However, events in Eastern Europe since late 1988

23. On the dangers of an inflationary Eurofed, see Dowd (1989). For evidence on independent central banks and their inflation records, see Banaian et al. (1983) and Burdekin and Willett (1990).

24. This is not to say that long-run average inflation under the Eurofed with a common currency would be higher than long-run average inflation in the EC under separate currencies. As long as countries are not ad- justing their rates, the Bundesbank should be able to set a pace giving lower inflation than would a common currency. The problem is that in the longer run, the system of pegged rates very likely will fail and perhaps give higher average inflation than would a common currency. The long-run trade-off may involve giving up a DM with its relatively low inflation so as to secure a common currency with inflation that is higher than that which would prevail under the DM but perhaps lower than what the EC average would be with sepa- rate currencies.

SWEENEY: OUTLOOK FOR EUROPEAN MONETARY UNION 37

foreshadow more instability in that re- gion. Stock market data show that events in Eastern Europe can have major eco- nomic effects on EC countries. Differential effects occur, however. Because these dif- ferential effects suggest adjusting ex- change rates, they weaken the case for ei- ther fixed rates or a common currency.

Clearly, a common currency has a much better chance of survival, and a common currency can survive without the controls and distortions used during the 1950s and 1960s to prop up the pegged-rate Breton Woods system. If the analysis of the threat of disturbances from Eastern Europe is correct, then the EMS and any successor EMU faces the enhanced prospect of spec- ulative runs. The key variable in such runs is credibility of commitment to the an- nounced parities. The credibility of a com- mon currency is simply much greater. This is true because the benefits of changing rates are the same under both fixed rates and a common currency, but the costs of changing are much higher under a com- mon currency.

Credibility is not the only advantage a common currency has over fixed rates. One major disadvantage, however, is the likelihood that a common currency will weaken anti-inflation discipline, at least as

compared with the countries having a strong aversion to inflation. The structure of the EMS gives conservative central banks much power to set the pace of mon- etary expansion. The traditional indepen- dence of the Bundesbank, along with the support for monetary restraint of a Ger- man public scarred by memories of hyper- inflation, give the Bundesbank the power to set conservative policies and make them stick. Designing a European central bank with an inflationary bias no greater than that of the present system may well be possible-the draft statute looks favor- able to an anti-inflation view. Officials quite possibly may adopt such a plan. But even if they do, some analysts may doubt whether the bank would operate or be al- lowed to operate as designed. Some expe- rience-albeit not very informative expe- rience-will exist in the behavior of the Eurofed in the pegged-rate transition to a common currency. Thus, adopting a com- mon currency will be an act of faith in the anti-inflation commitment and abilities of a virtually untested Eurofed. A common currency may well be too big a gamble as opposed to a system of floating rates with perhaps some EMS-like arrangements during calm periods.

38 CONTEMPORARY POLICY ISSUES

REFERENCES

Banaian, K., L. Laney, J. McArthur, and T. D. Willett, "Subordinating the Fed to Political Authorities Will Not Control Inflationary Tendencies," in T. D. Wdett, ed., Political Business Cycles, Duke University Press, Durham, N.C., 1988.

Banaian, K., L. Laney, and T. D. Willett, "Central Bank Independence: An International Comparison," Federal Reserve Bank of Dallas Economic Review, March 1983,l-13.

Brealy, R. A., and S. C. Myers, Principles of Corporate Finance, McGraw-Hill Book Co., New York, 1988.

Burdekin, R., and T. D. Willett, "Central Bank Reform: The Federal Reserve in International Perspec- tive," working paper, Claremont Colleges, 1990.

Canzoneri, M., V. Grilli, and P. Masson, Designing P Central Bankfor Europe, Centre for Economic Pol- icy Research, London, 1991.

Chalk, A., "Market Forces and Aircraft Safety: The Case of the DC-10," Economic Inquiry, January 1986, 43-60.

Dowd, K., "The Case Against a European Central Bank," The World Economy, September 1989,361- 372.

Economist, "A Survey of the European Community," July 7-13, 1990(a).

, "Statutes and Kultur," November 17, 1990(b), p. 87.

Eichengreen, B., "Is Europe an Optimum Currency Area?" paper for a conference on European Eco- nomic Integration and External Relations, Basle,

Gros, D., and N. Thygeson, "The Institutional Ap- proach to Monetary Union in Europe," Economic Journal, September 1990, 925-935.

August 23-25,1990.

Hasse, R., "A European Central Bank as an Instrument of European Monetary Union," paper presented at Western Economic Association International 65th Annual Conference, San Diego, 1990.

Logue, D. E., and R. J. Sweeney, "Inflation and Real Growth: Some Empirical Results," Journal of Money, Banking and Credit, November 1981,497- 501.

Logue, D. E., and T. D. Willett, "ANote on the Relation Between the Rate and Variability of Inflation," Economica, May 1976, 151-158.

Shafer, W., "Internal Market and Exchange Rate," paper presented at Western Economic Associa- tion International 65th Annual Conference, San Diego, 1990.

Sweeney, R., "Foreign Exchange Risk in International Portfolios," in R. Aggarwal and D. Schirm, eds., Global Portfolio Diversification, North Holland Press, Amsterdam, 199O(a) forthcoming.

, "Mean Reversion in the Real Exchange Rate: The Evidence from Equities Markets," working paper, Georgetown University, School of Business Administration, Washington, D.C.,

, "European Monetary Union: The Implica- tions of the Speed of Relative National Price Level Adjustment," working paper, Georgetown Uni- versity, School of Business Administration, Wash- ington, D.C., 1991.

Tower, E., and T. D. Willett, The Theory of Optimum Currency Areus and Exchunge Rate Flexibility, Spe- cial Paper in International Economics, Depart- ment of Economics, Princeton University, Princeton, N.J., 1976.

Wihlborg, C., and T. D. Willett, "Optimum Currency Areas Revisited," paper presented at the confer- ence on Financial Regulation and Monetary Ar- rangements (available in working paper form from Gothenburg Studies in Financial Econom- ics).

mop).