organic foods in spain 2003 - martin joensen · organic foods in spain 2003 martin joensen 2 ......

TRANSCRIPT

Organic foods in Spain 2003

Author: Martin Joensen

Faroe Islands, August 2003

Organic foods in Spain 2003 Martin Joensen

2

Table of contents

1 EXECUTIVE SUMMARY ................................................................4

2 INTRODUCTION ..............................................................................5

2.1 BACKGROUND FOR THE REPORT ..............................................................................5

2.2 SOURCES OF INFORMATION......................................................................................6

2.3 DEFINITION OF ORGANIC FOODS ..............................................................................7

3 THE ORGANIC SECTOR ................................................................8

3.1 SPANISH ORGANIC HISTORY.....................................................................................8

3.2 PRESENT MARKET STAGE .........................................................................................8

3.3 POLITICAL ENVIRONMENT .....................................................................................10

3.4 LOCAL CONSUMPTION............................................................................................11

3.5 PRICE PREMIUM......................................................................................................12

3.6 ORGANIC LABELING...............................................................................................14

3.7 SECTOR ORGANIZATIONS .......................................................................................16

4 DISTRIBUTION...............................................................................17

4.1 RETAILER TYPES ....................................................................................................19

4.1.1 The conventional super-/hypermarkets .............................................................19

4.1.2 The organic supermarket chains .......................................................................23

4.1.3 The organic food shops .....................................................................................25

4.1.4 The health food shops........................................................................................27

4.1.5 Organic consumer cooperatives........................................................................28

4.1.6 Pharmacies ........................................................................................................29

4.1.7 Direct sales ........................................................................................................30

4.2 FUTURE RETAILING STRUCTURE ............................................................................31

4.3 ORGANIC WHOLESALERS .......................................................................................32

Organic foods in Spain 2003 Martin Joensen

3

5 END-CUSTOMERS .........................................................................34

5.1 DEMOGRAPHIC INFORMATION ...............................................................................35

5.2 BUYING MOTIVES...................................................................................................36

5.3 USAGE RATE AND PURCHASING LOCATION............................................................39

5.4 PRICE PREMIUM ACCEPTANCE................................................................................40

5.5 PRODUCT ORIGIN AND BRANDS..............................................................................41

5.6 CUSTOMER SEGMENTATION...................................................................................41

5.6.1 The light users ...................................................................................................42

5.6.2 The medium users ..............................................................................................42

5.6.3 The heavy users .................................................................................................42

6 LOCAL PRODUCTION..................................................................43

6.1 ORGANIC LAND ......................................................................................................43

6.2 ORGANIC OPERATORS ............................................................................................44

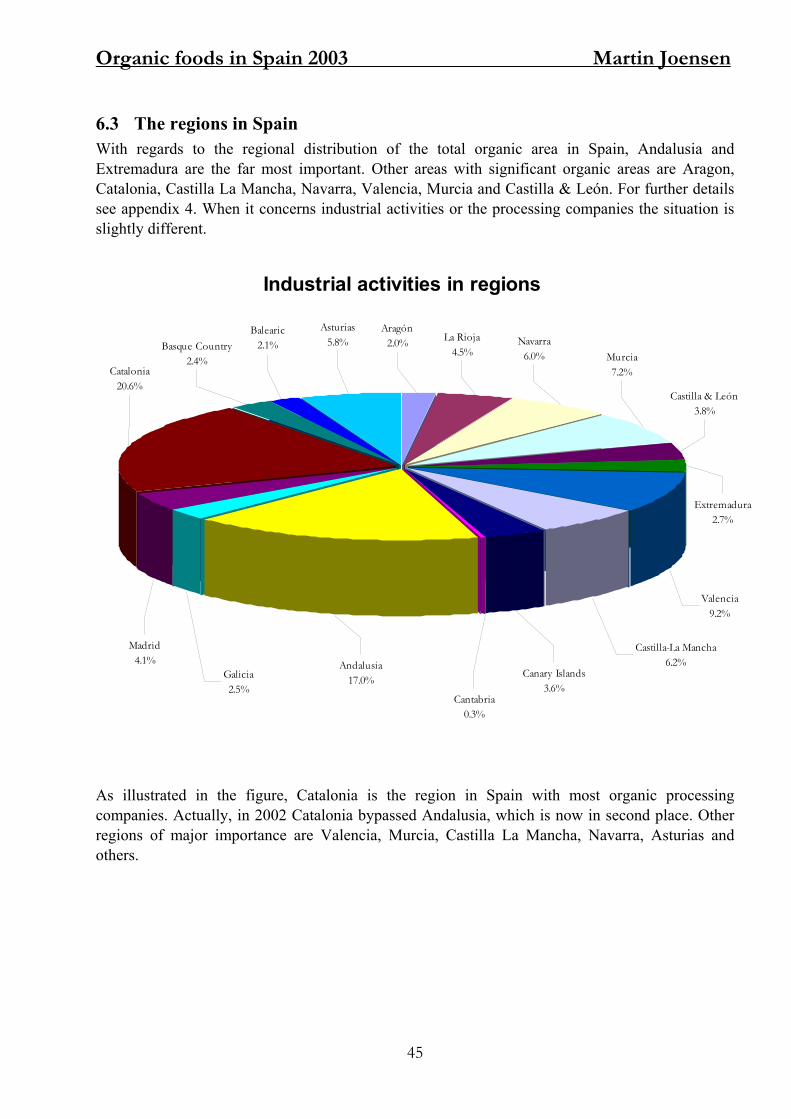

6.3 THE REGIONS IN SPAIN...........................................................................................45

6.4 LOCAL QUALITY.....................................................................................................46

7 REFERENCES .................................................................................47

7.1 PRIMARY SOURCES.................................................................................................47

7.2 SECONDARY SOURCES............................................................................................48

8 APPENDIXES...................................................................................51

8.1 APPENDIX 1 – SPANISH ORGANIC MARKET SIZE.....................................................51

8.2 APPENDIX 2 - ORGANIC RETAILING TRENDS 1997/98 – 2000 (%)..........................53

8.3 APPENDIX 3 - ORGANIC PROCESSORS’ ACTIVITIES 2002........................................54

8.4 APPENDIX 4 – ORGANIC AREA IN REGIONS ............................................................55

Organic foods in Spain 2003 Martin Joensen

4

1 Executive summary Profound changes are taking place in the sector for organic foods in Spain. From being an emergent market with low sales and few competitors, the sector is now entering the growth phase. The new market stage implies a change in market objectives and business strategies. The lack of political support is a major reason for the little developed domestic market. However, the Ministry of Agriculture, Fisheries and Food has presented an ambitious strategic plan for the whole sector. A further explanation for the relatively small consumption of organic foods (0,2 % of the total food market) is the relatively high price premium averaging around 100 %. Also, improved coordination and cooperation with regards to labeling and sector organizations would be beneficial for the sector. With regards to distribution, practically all consumption takes place in the households, who buy it from organic retailers. The retailers are supplied either directly by producers or via organic wholesalers. Unlike other European markets the specialized shops in Spain dominate organic retailing with a market share of 85 %. The lack of selling points is a central barrier for the development of local consumption. However, very recently the situation has improved considerably with the entry of 3 new organic supermarket chains. The conventional super-/hypermarkets are expected to gain importance in the upcoming years. However, until they have reached an organic product range of several hundred products, they are expected to have more positive than negative effects on the other organic retailers. Concerning the end-customers, there is little awareness about organic foods due to a lack of knowledge on this topic. The lack of knowledge among the Spanish end-customers is probably the most important barrier to the development of the domestic organic market. With regards to the present organic end-customers, the primary buying motive is health & food safety followed by taste and environmental consciousness. Most present end-customers accept a price premium for organic foods, whereas less than 50 % of the non-users are ready to pay a higher price. The brand preference among the present end-customers is not strong, but they have preferences towards local products. Concerning end-customer segmentation, the demographic information has not been found useful. Instead, a behavioral segmentation has been made based on usage rate, resulting in three segments: ‘light users’, ‘medium users’ and ‘heavy users’. Spain is a large-scale producer of a large variety of organic products. However, the products are predominantly unprocessed or semi-processed, directed for foreign markets. The total economic value of the Spanish production was 172,9 million Euros in year 2002. With regards to area under organic management, Spain ranks number 8 worldwide and the number of organic operators reached 17.725 in 2002. The most important regions in Spain are Andalusia and Extremadura in terms of organic area, but when it concerns industrial activities, Catalonia is the leading region followed by Andalusia. Both in terms of economic value, area under organic management and number of operators, Spain experienced a 30 % growth in year 2002. On the downside, there is a lack of further processed local products in Spain. Also, the further processed local organic products have still not reached the same standard as the foreign products.

Organic foods in Spain 2003 Martin Joensen

5

2 Introduction In this section the background for the report will be presented. Thereafter, the sources of information are examined followed by a definition of organic foods.

2.1 Background for the report This report is written both voluntary and as part of my Master’s Degrees in International Marketing and Management from Copenhagen Business School and ESADE in Barcelona. One of the degrees called CEMS (Community of European Management Schools)1 required an internship abroad, which in my case was at the Danish Trade Commission in Barcelona, managed by Jacob Duus Hansen. At that time, in spring 2002, no complete report on organic foods in Spain existed. With the Danish Trade Commission having expressed an interest

in investigating the area, along with my personal interest, we then set the task to write a report. Between autumn 2002 and spring 2003 I wrote a Master’s thesis with a fellow student Bertel Dahlmand Hansen. The thesis was written for the organic wholesaler Natureco S.L. that is situated in Catalonia. We had a very positive and fruitful collaboration with Dionís Guiteras Rubio and Karen Hoberg. We also enjoyed a very good cooperation with various other active players in the sector (see references). Finally, in summer 2003, I collected all the information that was obtained in the other projects in order to make this updated report on organic foods in Spain 2003. This report is my contribution to the development of the sector for organic foods in Spain. The report is originally written in English, but thanks to ‘The Friends of the Agricultural School of Manresa (AEAM), it is also available in Spanish and Catalan.

My sincere thanks to all the above-mentioned! All readers are invited to comment on this report, provide missing information and suggest improvements. Please contact [email protected] Sincerely, Martin Joensen

1 More information: www.cems.org

Organic foods in Spain 2003 Martin Joensen

6

2.2 Sources of information Both secondary and primary information has been used. The availability of secondary information concerning organic foods in Spain is limited. Therefore gathering of primary information has been a necessity. Secondary information, however, has been very useful for making international comparisons. The primary information consists of a series of interviews with various players in the sector such as organic end-customers, organic retailers, organic wholesalers, organic producers and organic associations. Among others, 22 in-depth expert interviews have been made in Spain, the Netherlands, Denmark and Belgium. In addition, short interviews have been made at five trade fairs on the topic:

• BioCultura in Barcelona • BioCultura in Madrid • Ecoviure in Manresa • BioFach in Nürnberg • Alimentaria in Barcelona

With regards to the organic end-customers a small survey has been made because no reliable end-customer information was available in Spain. The objective of the survey was to gain knowledge about end-customer profiles, behavior and preferences in order to assist management decisions in the sector. A large proportion of the Spanish population does not know that organic products exist and even fewer actually buy organic foods. Therefore, in order to ensure the validity of the survey it was limited to existing organic customers. This was obtained by conducting customer interviews in shops specializing in organic foods. With regards to the conventional supermarkets, permission was obtained to intercept customers inside the store where the organic products were situated. Other measures to secure the validity of the survey were to interview customers in different neighborhoods and to conduct interviews both in the morning and afternoon. With regards to the reliability of the information that was gained in the end-customer survey, it should be seen as a good indicator and not as completely reliable because the size of the survey was limited to 85 respondents. In order to secure a diverse sample of respondents, interviews were made with customers in all the main organic retail channels in Spain being:

• Organic foods shops • Organic supermarket chains • Health food shops • Conventional super-/hypermarkets • Organic consumer cooperatives

Organic foods in Spain 2003 Martin Joensen

7

2.3 Definition of organic foods Organic production is based on four principles.

I. Consumers are entitled to know what they are eating, i.e. what the products contain and how they are produced.

II. The food must not contain chemical compounds that are potentially harmful to human beings or to the environment.

III. The production must be sustainable, i.e. there should be efficient use of resources and minimum pollution.

IV. The welfare of animals should be taken into consideration in such a way that their natural needs are attended to.

In accordance with EU-legislation an organic product needs to fulfill the requirements in Council Regulation 2092/91, article 10. The main requirements are the following:

• At least 95% of the ingredients of agricultural origin are organic. Food products may thus contain up to 5% of ingredients produced by conventional methods as long as those ingredients are not available or in very short supply.

• The product has been subject to the inspection arrangements laid down in

the regulation throughout the production and preparation process. This means that the operators involved in the agricultural production, processing, packaging and labeling of the product must all be subject to the inspection scheme. For example, the product may only contain a very limited use of additives and antibiotics and GMO’s are prohibited. Also, other criteria such as animal welfare need to be fulfilled.

• The products need to be sold directly by the producer or processor in sealed

packaging, or placed on the market as pre-packaged food.

• The product labeling must contain the name and/or business name of the producer, processor or vendor, together with the name or code number of the inspection authority or body.

The above-mentioned definition of organic products in Spain is the same as in other EU-countries, as there is a common legislation on this area. The definition of organic foods is changing over time and generally it can be said that it is becoming wider and stricter.

Organic foods in Spain 2003 Martin Joensen

8

3 The organic sector In this section, the reader will be introduced to the Spanish organic history, the present market stage and the political environment. Also, the local consumption and the price premium for organic foods are analyzed. Finally, organic labeling and associations in the sector will be examined.

3.1 Spanish organic history2 Organic farming in Spain began in the late 1970’s with small farms and was basically promoted by young people coming from the cities. Another important factor was the fact that the first ‘pioneer’ organic farmers had guaranteed sales to foreign markets. Furthermore, the natural conditions in Spain with numerous ecosystems, a favorable climate for early cultivation and more frequent harvesting together with a relatively moderate use of agro-chemicals has been of importance. Since the 1970’s, the sector has experienced a slow but steady growth. Today, almost three decades later, the organic foods sector in Spain is still not clearly defined.

3.2 Present market stage Markets normally go through four stages: the emergent stage, the growth stage, the mature stage, and the declining stage. Five indicators, exhibited in the table below, determine which market stage a sector is in.3

Market stage characteristics

Characteristics Emergent Growth Organic foods in Spain Customers Innovators Early adapters Emergent Growth Sales Low sales Rapidly rising sales Emergent Growth Competitors Few Growing number Growth Costs High cost per customer Average cost per customer Emergent Profits Negative profits Rising profits Growth

As it occurs, all indicators place the market for organic foods in Spain in either the emergent or the growth stage. Two of the characteristics (competitors and profits) have already reached the growth phase. However, costs are still high due to low sales and inefficient production and are therefore an emergent market characteristic. The characteristics ‘customers’ and ‘sales’ are presently changing from emergent to growth. Concerning the customers, only 0,2 %4 are buying organic foods. These customers can be looked upon as innovators. According to the customer survey 18 % of the organic customers are new customers with less than one year of shopping experience and can be characterized as early adapters. With regards to sales, the Spanish market for organic foods represents less than 0,2 % of

2 Mostly taken from Gonzálvez Pérez. 3 Kotler. 4 Own Calculations, see appendix 1.

Organic foods in Spain 2003 Martin Joensen

9

the total food consumption5, which indicates that the sector is still in the emergent stage. However, the market is very dynamic and is expected to expand approximately 15 – 20 % per year in the period 2003 – 2005, indicating that the market is in the growth stage. Having these arguments in mind it is concluded that the sector for organic foods in Spain is currently in the transition phase from the emergent stage to the growth stage, as illustrated below.

Market stage cycle

The market stages have a significant impact on companies’ market objectives and strategies. In the table below the fundamental differences in the emergent market stage and growth market stages are illustrated.

Strategic importance of market stages

Emergent stage Growth stage Market objectives: Strategies (4 P’s) - Product - Price - Place (distribution) - Promotion

Create product awareness and trial Offer a basic product Charge cost-plus Build selective distribution Build product awareness among early- adopters and dealers

Maximize market share Offer product extensions and service Price to penetrate market Build intensive distribution Build awareness and interest in the mass market

5 For further details see appendix 1.

Time

Emergent DeclineMatureGrowthSales

Organic foods in Spain

Organic foods in Spain 2003 Martin Joensen

10

3.3 Political environment The lack of political support is a major reason for the little developed domestic market. With regards to legislation, the environmental policy in Spain is primarily based on EU legislation. The overall responsibility for any subject related to organic food products and food production, is held by CRAE (Comision Reguladora de Agricultura Ecológica), a commission regulating organic agriculture. This Commission is an entity managed by the Spanish Ministry of Agriculture, Fisheries and Food. However, the 17 autonomous regions in Spain are in charge of implementing the decree.6 Although Spain has implemented most of EU’s environmental directives, the Spanish policy is generally fragmented and inconsistent.7 As Theo de Bruijn states: “The policy style of Spain is described as closed, non-cooperative, bureaucratic and intangible”.8 This can be illustrated by an ongoing case where the Spanish government has implemented a law that erases the protection of the terms: ‘biológico’, ‘bio’ and ‘orgánico’. According to CRAE, this action taken by the government is illegal, contradicting the EU decree and the corresponding Spanish law. Consequently, this matter is now in the Spanish Supreme Court where CRAE on behalf of the organic sector has sued the government. Up to now, the Spanish government has not given much support to research in organic farming or to organic marketing campaigns. There is no special centre for research on organic farming and the only related activities are those of the advisory working groups of the CRAE.9 However, a few regional privately organized research programs have been carried out. On the positive side, the Ministry of Agriculture, Fisheries and Food has presented an ambitious strategic plan for the whole sector. The purpose of the plan is to define the frame of reference for a general debate about the objectives and necessary actions in the sector that need public support.10 Therefore, the Ministry has posted an online questionnaire on their homepage and is encouraging all interested players in the sector to provide feedback on the plan. The feedback period is until October 30th 2003 and the final plan is supposed to be presented in December 2003. The plan contains objectives within the 8 areas: production, processing, distribution, end-customers, education & training, control authorities, coordination in the sector, and research & development. The implementation period for this strategic plan is intended to be 2004 to 2006. Indeed, it will be very interesting to see the outcome of this plan in terms of real actions.

6 Escudero: ”Spain’s Organic Product Market”. 7 Trade partners UK 2002. 8 Bruijn, Page 292. 9 Gonzálvez Pérez. 10 Ministry of Agriculture, Fisheries and Food, (MAPYA): “Plan Estratégico de Agricultura Ecológica”.

Organic foods in Spain 2003 Martin Joensen

11

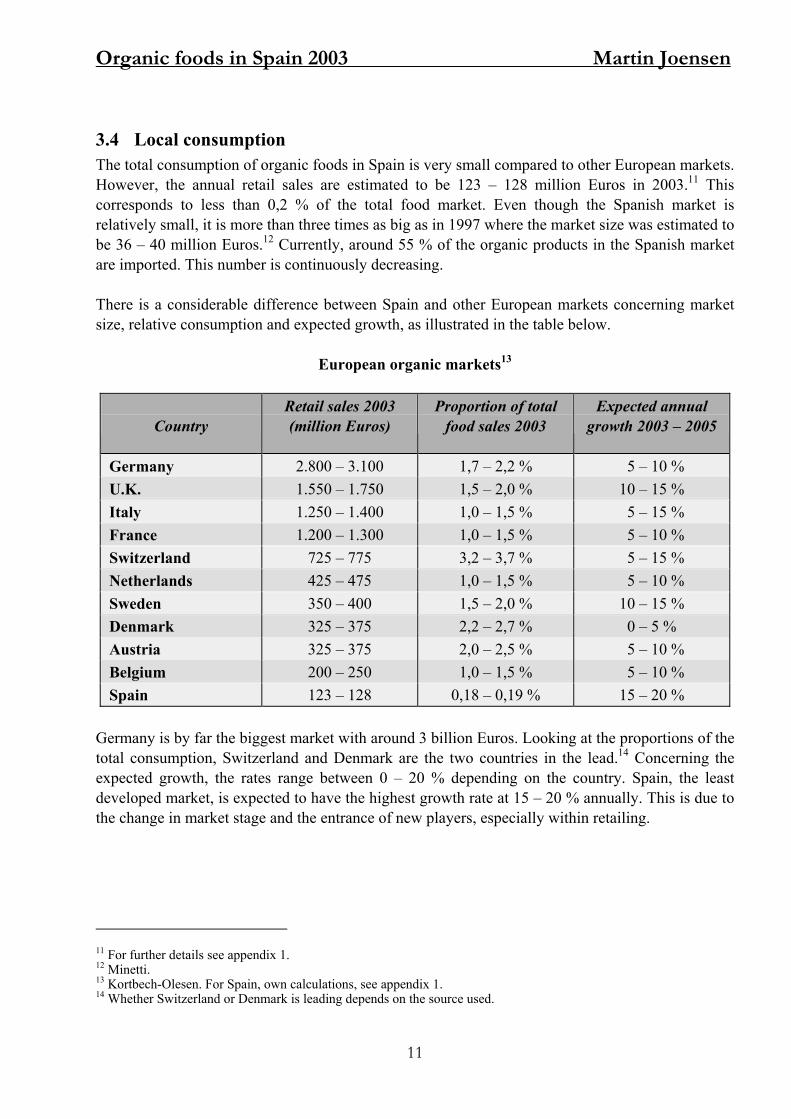

3.4 Local consumption The total consumption of organic foods in Spain is very small compared to other European markets. However, the annual retail sales are estimated to be 123 – 128 million Euros in 2003.11 This corresponds to less than 0,2 % of the total food market. Even though the Spanish market is relatively small, it is more than three times as big as in 1997 where the market size was estimated to be 36 – 40 million Euros.12 Currently, around 55 % of the organic products in the Spanish market are imported. This number is continuously decreasing. There is a considerable difference between Spain and other European markets concerning market size, relative consumption and expected growth, as illustrated in the table below.

European organic markets13

Country

Retail sales 2003 (million Euros)

Proportion of total food sales 2003

Expected annual growth 2003 – 2005

Germany 2.800 – 3.100 1,7 – 2,2 % 5 – 10 % U.K. 1.550 – 1.750 1,5 – 2,0 % 10 – 15 % Italy 1.250 – 1.400 1,0 – 1,5 % 5 – 15 % France 1.200 – 1.300 1,0 – 1,5 % 5 – 10 % Switzerland 725 – 775 3,2 – 3,7 % 5 – 15 % Netherlands 425 – 475 1,0 – 1,5 % 5 – 10 % Sweden 350 – 400 1,5 – 2,0 % 10 – 15 % Denmark 325 – 375 2,2 – 2,7 % 0 – 5 % Austria 325 – 375 2,0 – 2,5 % 5 – 10 % Belgium 200 – 250 1,0 – 1,5 % 5 – 10 % Spain 123 – 128 0,18 – 0,19 % 15 – 20 %

Germany is by far the biggest market with around 3 billion Euros. Looking at the proportions of the total consumption, Switzerland and Denmark are the two countries in the lead.14 Concerning the expected growth, the rates range between 0 – 20 % depending on the country. Spain, the least developed market, is expected to have the highest growth rate at 15 – 20 % annually. This is due to the change in market stage and the entrance of new players, especially within retailing.

11 For further details see appendix 1. 12 Minetti. 13 Kortbech-Olesen. For Spain, own calculations, see appendix 1. 14 Whether Switzerland or Denmark is leading depends on the source used.

Organic foods in Spain 2003 Martin Joensen

12

3.5 Price premium When asking the players in the sector about the price difference between organic food products and conventional food products the answers were very diverse. Therefore, it was necessary to make a proper comparison. The price difference between products depends very much on the type of retailers that are being compared and the products that are selected for the comparison. Therefore, the methodology for the comparison needs to be correct. For this comparison all the important organic retailers in Spain have been examined as listed below.

• Organic foods shops • Organic supermarket chains • Health food shops • Conventional super-/hypermarkets • Organic consumer cooperatives

Within each retailer type, 1-3 shops have been examined. Concerning the conventional super-/hypermarkets, the hypermarket ‘Alcampo’ was chosen as a representative because generally, the smaller supermarkets do still not carry organic products. The prices for organic foods are compared to the prices for conventional foods in both super-/hypermarkets and traditional food shops. For the supermarkets a comparison was made with ‘Caprabo’ and with regards to the hypermarkets ‘Alcampo’ was selected. Concerning the products that were compared a mixed basket was made containing different food products that are consumed by an average person. In this basket, there were both fresh and durable foods; little-processed and much-processed products as well as low-price and high-price products. In cases where there were many similar products, an average priced product was put into the basket. One could argue that organic food products are of higher quality than conventional food products and therefore, an organic egg or organic cereals cannot be compared with conventional food products. This is a valid argument. However, the great majority of the Spanish consumers do not know what it means when a product is organic.15 In their mind, an egg is an egg and cereals are cereals. Consequently, from most end-consumers’ point of view the comparison of organic and conventional food products in Spain is fully valid. Concerning the results of the comparison it can be concluded that on average the price premium for organic foods in Spain is around 100 %. However, as mentioned before, there are variations depending on products and retailer types. As illustrated in the table below the price premium varies between 10 – 200 %.

15 Fundación Entorno.

Organic foods in Spain 2003 Martin Joensen

13

Basket of products

Product Price premium Tomatoes 400 kg. 87 % Integral toast bread 400 g. 36 % Cheese 45 % - 125 g. 72 % Eggs 6 (53 – 63 g.) 144 % Chicken breast 500 g. 132 % Apple juice 1 liter 84 % Strawberry marmalade 300 g. 115 % Peas (frozen) 500 g. 140 % Baby food 220 g. 112 % Long-life milk 3,5 % 1 liter 88 % Mixed pasta 500 g. 92 % Choco flakes 375 g. 81 % Rice biscuits 100 g. 46 % Sponge cakes 150 g. 106 % Chocolate spread 350 g. 206 % Sweets 50 g. 138 % Canned tuna 100 g. 111 % Boiled ham 100 g. 113 % Smoked salmon 100 g. 105 % Fresh beef (leg) 500 g. 10 % Yoghurt 200 g. 89 %

Average 100 %

When comparing the organic retailers: organic foods shops, organic supermarket chains and health food shops to each other, no notable price difference was found. These three retailer types have a 121 % price premium over conventional foods in the super-/hypermarkets and a 77 % price premium over conventional foods in the traditional shops, averaging at around 100 %. Furthermore, it has been found that organic foods in these three retailer types is 37 % more expensive than organic foods in the conventional super-/hypermarkets and 18 % more expensive than in the organic consumer cooperatives. When comparing organic foods in the super-/hypermarkets to conventional foods that are sold in the same super-/hypermarkets the price difference is only 32 %. This is mainly because the supermarkets only carry those organic products that have a high rate of turnover. For this reason, the super-/hypermarkets carry few organic products and tend to look for cheap products.16

16 Hansen.

Organic foods in Spain 2003 Martin Joensen

14

3.6 Organic labeling In Spain there are several different organic labels. The locally produced products typically carry the Spanish common label, which is used by all autonomous regions with the exception of Andalusia. Andalusia was the first region to introduce an organic label that has been kept ever since.17 Common label Label of Andalusia Each region writes its own name on the label. In the example above (to the right) the label for the region of Galicia is illustrated. In addition to the public labels there is an increasing number of private labels. The most recognized and trusted private label is the Vida Sana trademark (below to the left), which has been in existence for many years. Vida Sana trademark EU label

Apart from the Spanish labels, the official organic EU label (above to the right), as well as labels from other EU-countries are in use. Obviously, such a high number of organic labels is confusing for the consumer who has a hard time to decide which labels to trust.

17 González Ruiz et al.

Organic foods in Spain 2003 Martin Joensen

15

In general, the Spanish population’s ability to recognize labels and to know the correct meaning is very limited. As it can be seen in the figure below this is also valid for organic labels. In 2001 only 8 % of the general adult Spaniards were able to identify the common label. Furthermore, only half of these (4 %) knew the correct meaning of it.18 In Denmark and Sweden the level of knowledge is close to 100 %.19 With respect to trust in organic labeling (European or the local) only 22 % of the Spaniards thought that the label is a guarantee for more control compared to non-organic products.20

With regards to existing organic customers in Spain the situation is very different. According to the end-customer survey 79 % of the respondents state that they know the organic labels and 85 % of these say that they trust them. Obviously, the number of organic labels needs to decrease drastically in order to remove the confusion and distrust among consumers. This opinion is shared by 73,6 % of the distributors and retailers in Spain.21 Moreover, with only one or very few labels it would be much easier to promote the sector as a whole.

18 Fundación Entorno. 19 Hamm et al. 20 Fundación Entorno. 21 DHVMC.

Organic foods in Spain 2003 Martin Joensen

16

3.7 Sector organizations In Spain, there are a number of organic organizations and associations but they are generally lacking support and resources. Also, improved coordination and cooperation between the different organizations is needed in order to be more beneficial for the sector. Historically, the most important association for the sector for organic foods in Spain has been ‘Asociación Vida Sana’. Vida Sana has a broad range of activities all related to environment and health. Today, the majority of players in the sector do not perceive Vida Sana as a neutral organization, but as an organization with commercial interest. This is especially due to Vida Sana’s relations with the BioCop Group, which operates within both wholesaling and retailing of organic products in Spain. Other associations of importance are The Friends of the Agricultural School of Manresa (AEAM), Biolur, Ekonekazaritza, Aula de Agricultura Ecologica of Sevilla, Asociación de Agroecoloxia and FANEGA.22 Presently, only 10 Spanish organizations and companies are members of IFOAM. Concerning organic producers and processors, there is an association called FA-BIO, but according to a market study only 54 % of the producers and processors state that they belong to some organization.23 This number includes those who consider the local control authorities as an association. However, according to the same market study 73,7 % of the producers and processors still find it necessary to create an organization for the sector as such. The major motive behind this is the need to organize and structure the sector, exchange of information and achieve government support.

With regards to the organic consumers, they are in the process of being represented through the local control authorities. This initiative is based on EU-requirements and the implementation in Spain has recently begun. In Catalonia for instance, the board of the control authorities CCPAE consists of 12 members. Out of these 12 members, 6 are representing commercial interests including producers, processors, and distributors. The other 6 representatives are required to be non-commercial. In Catalonia it has been decided that 3 of the non-commercial members shall come from the administration and the other 3 represent the consumers. Presently, only 1 out of the 3 consumer representatives has an ‘organic background’, the other 2 members come from general consumer organizations in Catalonia. Consequently, only 1 out of the 12 board members is representing the organic consumer, which means that the organic consumer’s influence on the decision-making is very limited.

22 Gonzálvez Pérez. 23 DHVMC.

Organic foods in Spain 2003 Martin Joensen

17

4 Distribution Distribution of organic foods is very different from distribution of conventional food in Spain. Concerning conventional food, households consume around ¾ of the total consumption whereas the remaining ¼ is consumed in restaurants, hotels and institutions.24

Conventional food consumption (Value)

73 73 72 72 72 73

24 25 26 26 26 25

2 2 2 2 2 2

0

10

20

30

40

50

60

70

80%

Households Restaurants and hotels Institutions

1996 1997 1998 1999 2000 2001

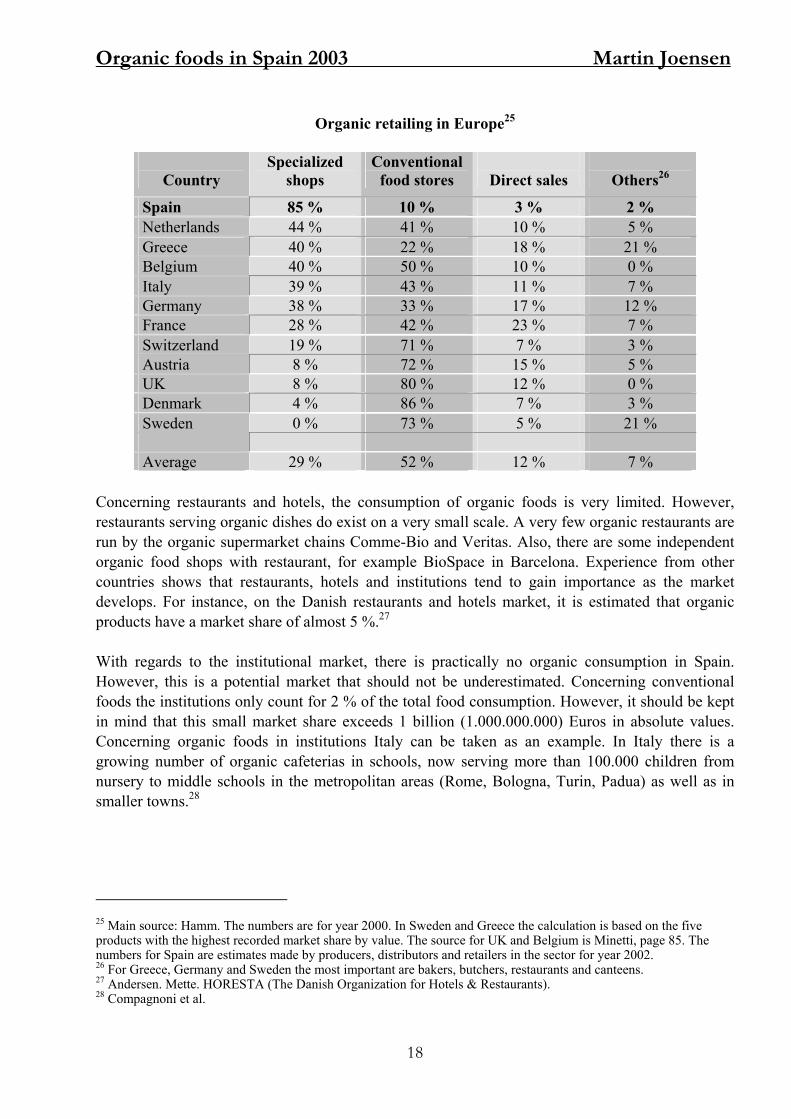

With regards to organic foods practically all consumption takes place in households. The households buy the food in different retailer types, which differ considerably from each other. In this relation it must be mentioned that lack of selling points is a very central barrier for the development of local consumption. However, very recently, the situation has improved considerably. Concerning retailer types, the specialized shops dominate the Spanish organic market with a 85 % market share. The specialized shops consist of organic food shops, health food shops and the recently established organic supermarket chains, This organic retailing structure differs considerably from other European markets because is no other market the specialized shops have such a high market share. The conventional food stores, super- and hypermarkets in the case of Spain, only have a 10 % market share and the remaining 5 % are direct sales and other smaller retailers, namely organic consumer cooperatives and pharmacies. Further elaboration can be seen in the table on next page.

24 The total consumption of conventional food corresponded to 61,44 billion (61.440.000.000) Euros in 2001.

Organic foods in Spain 2003 Martin Joensen

18

Organic retailing in Europe25

Country

Specialized shops

Conventional food stores

Direct sales

Others26

Spain 85 % 10 % 3 % 2 % Netherlands 44 % 41 % 10 % 5 % Greece 40 % 22 % 18 % 21 % Belgium 40 % 50 % 10 % 0 % Italy 39 % 43 % 11 % 7 % Germany 38 % 33 % 17 % 12 % France 28 % 42 % 23 % 7 % Switzerland 19 % 71 % 7 % 3 % Austria 8 % 72 % 15 % 5 % UK 8 % 80 % 12 % 0 % Denmark 4 % 86 % 7 % 3 % Sweden 0 % 73 % 5 % 21 % Average 29 % 52 % 12 % 7 %

Concerning restaurants and hotels, the consumption of organic foods is very limited. However, restaurants serving organic dishes do exist on a very small scale. A very few organic restaurants are run by the organic supermarket chains Comme-Bio and Veritas. Also, there are some independent organic food shops with restaurant, for example BioSpace in Barcelona. Experience from other countries shows that restaurants, hotels and institutions tend to gain importance as the market develops. For instance, on the Danish restaurants and hotels market, it is estimated that organic products have a market share of almost 5 %.27 With regards to the institutional market, there is practically no organic consumption in Spain. However, this is a potential market that should not be underestimated. Concerning conventional foods the institutions only count for 2 % of the total food consumption. However, it should be kept in mind that this small market share exceeds 1 billion (1.000.000.000) Euros in absolute values. Concerning organic foods in institutions Italy can be taken as an example. In Italy there is a growing number of organic cafeterias in schools, now serving more than 100.000 children from nursery to middle schools in the metropolitan areas (Rome, Bologna, Turin, Padua) as well as in smaller towns.28

25 Main source: Hamm. The numbers are for year 2000. In Sweden and Greece the calculation is based on the five products with the highest recorded market share by value. The source for UK and Belgium is Minetti, page 85. The numbers for Spain are estimates made by producers, distributors and retailers in the sector for year 2002. 26 For Greece, Germany and Sweden the most important are bakers, butchers, restaurants and canteens. 27 Andersen. Mette. HORESTA (The Danish Organization for Hotels & Restaurants). 28 Compagnoni et al.

Organic foods in Spain 2003 Martin Joensen

19

4.1 Retailer types The following sections will provide a more detailed description and analysis of the different types of organic retailers in Spain. The characteristics of each retailer type will be presented, including how they prioritize business opportunities versus ideology. Also, the future expectations for each of them will be analyzed.

4.1.1 The conventional super-/hypermarkets Today, the conventional super-/hypermarkets in Spain are estimated to have a 10 % retailing market share of organic foods. According to a market study made by DHVMC in 2002, 30 % of the supermarkets and 22 % of the hypermarkets carry some organic products.31 However, it must be stressed that the number of organic products in the super-/hypermarkets is limited to 30-100 organic products compared to 1.191, which is the case for the conventional supermarket chain Coop Norden (FDB) in Denmark.32 The most important conventional super-/hypermarkets in Spain that have introduced organic foods are Alcampo, Carrefour, Eroski, El Corte Inglés and Mercadona. The conventional super-/hypermarkets’ motives for having organic foods in the product range are primarily of commercial nature.

As organic foods are one of the fastest growing sectors in the food market, it is seen as an attractive future market by super-/hypermarkets. As Pedro López, Controlled Production Manager at Alcampo says: “…we believe that organic products will be successful in the supermarkets…”33

29 Super-/hypermarkets larger than 400 m2. Source: Escudero,” Spain Retail Food Sector Report 2001”. 30 When the stores were visited, most employees did not know what it meant that a product was organic. 31 DHVMC. 32 Milman. 33 López Salcedo.

Core business Conventional products Organic sales arguments Health and food safety THE BUSINESS FACTS Shops per capita Many (1 per 8.000 inhabitants)29 Size of store 400-20.000 m2 Shop design Professional. Lacking organic sign-posting Organic price premium 32 % Durable organic products Very limited Fresh organic products Very limited Variety within product groups None THE RESOURCES Management Skilled managers and top-management Strategic planning Professional Personnel Very little knowledge of organic products30 Capital to invest Much

Ideology Business opportunity

Conventional Supermarkets

Organic foods in Spain 2003 Martin Joensen

20

Future market potential

Customer demand

Improve company image

Attract new customers to

the stores

Reasons for carrying

organic foods

People’s health and

environment

Differentiate from

competitors

Primary reasons

Secondary reasons

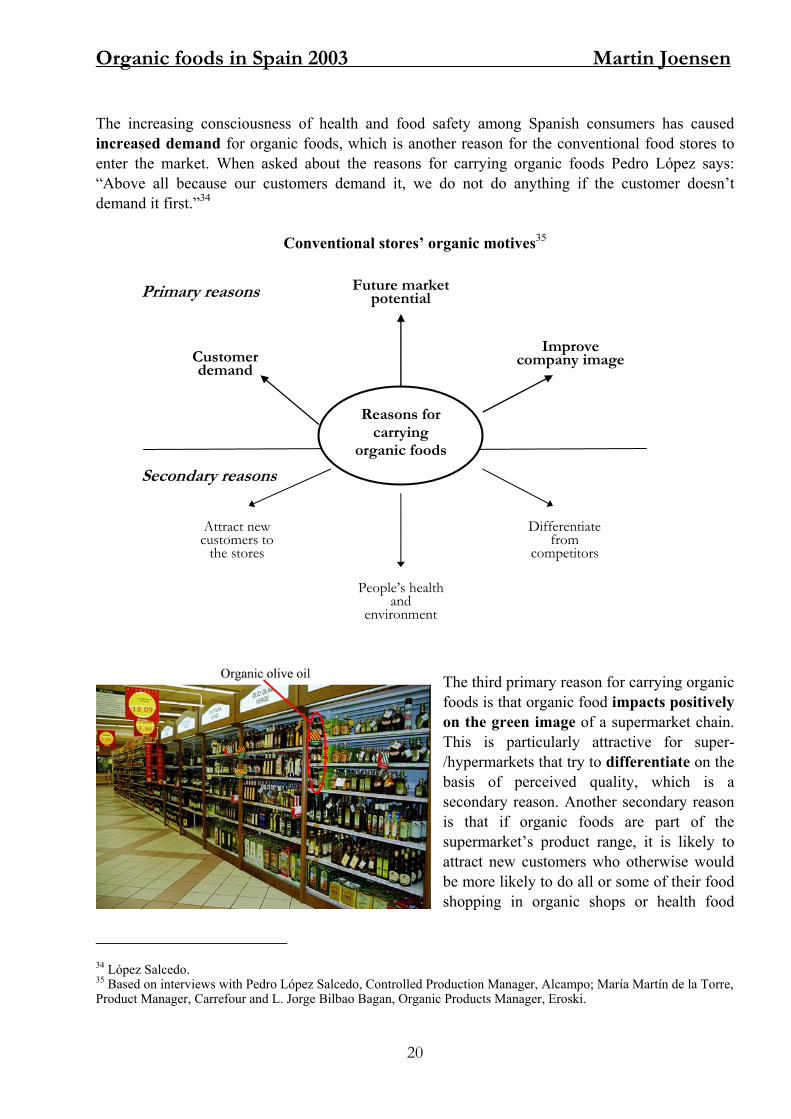

The increasing consciousness of health and food safety among Spanish consumers has caused increased demand for organic foods, which is another reason for the conventional food stores to enter the market. When asked about the reasons for carrying organic foods Pedro López says: “Above all because our customers demand it, we do not do anything if the customer doesn’t demand it first.”34

Conventional stores’ organic motives35

The third primary reason for carrying organic foods is that organic food impacts positively on the green image of a supermarket chain. This is particularly attractive for super-/hypermarkets that try to differentiate on the basis of perceived quality, which is a secondary reason. Another secondary reason is that if organic foods are part of the supermarket’s product range, it is likely to attract new customers who otherwise would be more likely to do all or some of their food shopping in organic shops or health food

34 López Salcedo. 35 Based on interviews with Pedro López Salcedo, Controlled Production Manager, Alcampo; María Martín de la Torre, Product Manager, Carrefour and L. Jorge Bilbao Bagan, Organic Products Manager, Eroski.

Organic foods in Spain 2003 Martin Joensen

21

shops. Finally, people’s health and environmental consciousness is mentioned by one of the hypermarkets as a motive for carrying organic foods. When asking María Martin, Product Manager at Carrefour about the criteria used when selecting new organic products she gives the short and precise answer: “That they have a rate of turnover.”36 Pedro López, Controlled Production Manager at Alcampo agrees and elaborates: “What we are looking for? Products that sell, rate of turnover of products, and then we look for people who can supply these products. We have a problem, which is that we can think of organic products that sell well, but today we cannot find producers…”37 This is confirmed by examining the current product range in the shops, which is limited to beef, milk, olive oil, yogurt, cereals, rice cakes and a few others. With regards to future expectations there are several reasons to expect that conventional super-/hypermarkets will gain increasing importance in the upcoming years. First, there is a clear tendency in other European markets that conventional super-/hypermarkets are continuously increasing their organic market shares. This is generally at the cost of specialized shops. The only exceptions are Denmark and Sweden, where the conventional supermarkets were the first movers, having already entered the market in the early 1980’s and gained a market share close to 100%. Further details about retailing trends in other European markets can be seen in appendix 2.

Super-/hypermarkets’ organic market share38

0

10

20

30

40

50

60

70

80

90

100

Spain

Greec

e

Germ

any

Net

herlan

ds

France

Italy

Belgiu

m

Switz

erlan

d

Austria UK

Den

mar

k

Swed

en

%

1997/98 2000

Secondly, an increase of the organic product range is expected to become an important conventional retailer strategy. Clear signs of this can already be seen amongst leading conventional retailers such as Albert Heijn in the Netherlands, Grona Konsum in Sweden and Sainsbury’s in the 36 Martín. 37 López Salcedo. 38 Main sources used are: Yussefi and Willer for 1997/98 and Hamm for year 2000.

Organic foods in Spain 2003 Martin Joensen

22

UK.39 In Spain, some of the major super-/hypermarket chains have also made a strategic decision to focus more on organic foods and introduce more organic products in the future. Carrefour, for instance, has already released plans to carry 120 organic products by the end of 2005 compared to 40 products in 2003.40 Although this is a significant increase, it is still not much compared to the 2.000 – 4.000 organic products that some of the specialized shops carry. A step already taken by Carrefour and Alcampo is the launching of private labels, which are generally cheaper than branded goods.41 Carrefour has its own organic label, while Al Campo has so far only a label for controlled production, a less strict production form than organic production.

Carrefour organics Alcampo controlled products42

A final reason to expect the conventional super-/hypermarkets in Spain to gain importance is that they are generally gaining market shares. This is especially the case concerning durable food products where the super-/hypermarkets hold 77,8% of the total market. Supermarkets that are close to people’s homes are expected to increase their market share of dry products even further.43 With regards to fresh products, the super-/hypermarkets have experienced an increase of 5,8 % in five years and now hold 41,7 % of the total market. Other factors being equal, this should cause a similar increase in organic retailing.

39 Reuters. 40 Martín. 41 Reuters; Hansen. 42 Auchan is the name of the chain in France. It is unclear why this name is used in their Spanish logo. 43 Ministry of Agriculture, Fisheries and Food, (MAPYA): “La Alimentación en España 2000”, Madrid 2001.

Organic foods in Spain 2003 Martin Joensen

23

4.1.2 The organic supermarket chains The phenomenon “organic supermarket chain” is very new in Spain since the first organic supermarkets were established in year 2002. The strategy of the organic supermarket chains is to offer healthy quality products for customers with a medium to high income. The chains have an organic product range that lies between 2500 and 4000 products and thereby the independent organic food shops are bypassed in the number of products. The chain’s shops also carry books and magazines, cosmetics, natural medicine, herbs and dietetic products. Compared to the organic food shops, the chains seek to widen the range of fresh products as well as the selection within each product group. This is done in order to provide a better basis for one-point shopping. In the table below, the basic information on the three organic supermarket chains in Spain is shown.

Organic supermarket chains in Spain

Logo of organic

supermarket chain

Holding company NaturaSí Ecovéritas BioCop Group Foreign interests Yes N.a. Yes Number of shops 31 3 544 Superm. in Spain 1 2 2 Future ambition Expansion 30 shops by 2006 18 shops by 2005 First opening Apr 2002 Sep 2002 Oct 2002 Location Madrid Barcelona Barcelona

NaturaSí is an Italian group and so far the only concrete official plan is to open another shop in Madrid in 2003. Ecovéritas is founded by six businessmen, among others Carles Gumbau Torresilla, Marketing Professor at the recognized Spanish business university, ESADE; Silvio Elías, Vice President and partner of the conventional supermarket chain Caprabo and Josep Pont Amenós, co-owner of the Spanish olive oil producer Borges. Comme-Bio is owned by Alter Vida, which is owned by the BioCop Group and the main shareholder (75 %) in BioCop is the Pan European Food Fund in Luxemburg.

44 All the shops are in Spain, but 3 of them are independent shops and do not form part of the concept ‘organic supermarket chains’. The future shops will be both own shops and franchises.

Core business Organic foods Organic sales arguments Health, food safety, taste & lifestyle THE BUSINESS FACTS Shops per capita Very few (1 per 1.000.000 inhabit.) Size of store 200-600 m2 Shop design Professional Organic price premium 77 – 121 % Durable organic products Complete Fresh organic products Many Variety within product groups Some THE RESOURCES Management Shop managers & top management Strategic planning Professional Personnel Semi skilled Capital to invest Much (backed up by strong groups)

Organic foods in Spain 2003 Martin Joensen

24

Ideology Business opportunity

Organic S.

chains

The new supermarket chains are commercially oriented and have managed to gain much attention due to professional marketing and good commercial contacts.

With regards to future development, the organic supermarkets have high ambitions and are investing aggressively with clear economic motives. On average, one new shop is expected to open every month for the next 3-4 years. The organic supermarket chains have not entered the market with the strategy of solely focusing on the existing organic customers. They want to win over customers from the conventional food retailers as well as gaining market share from the other organic retailers.

Hence, the organic supermarkets will position themselves between the conventional supermarkets and the independent organic food shops. Concerning the expansion by capturing customers from the conventional food retailers Carles Torrecilla, co-founder of Veritas explains: “People care about going to school, care about the girlfriend, everything except food!! The share of the personal budget dedicated to food decreases continuously, it can’t be right that people do not spend money on food! People should enjoy food and not only buy cheap food in Caprabo (conventional supermarket chain in Spain).”45 This market expansion by changing peoples’ mentality requires a considerable marketing effort as there is no public funding for promoting the organic sector in Spain. Although the organic supermarket chains want to capture customers from the conventional supermarkets, they are not perceived as competitors by the conventional super-/hypermarkets because the conventional super-/hypermarkets’ core business will continue to be conventional products.46 However, as it was revealed in the previous section, many supermarkets have a strategy

45 Torrecilla Gumbau. 46 López Salcedo.

Organic foods in Spain 2003 Martin Joensen

25

regarding organic products and the organic supermarket chains must therefore expect a somewhat increased competition from that side. In comparison to the existing organic retailers, the organic supermarkets’ strategy is to slightly tone down the ideological aspects of organic foods. They will stress such criteria as trust, accountability, product range, packaging formats, closeness (local products) and shop design. Another question is if there is space for severeal organic supermarket chains in Spain. Experience from Holland shows that there were organic supermarket 3 chains in the beginning, but now they have merged and have become one chain.

4.1.3 The organic food shops The core business of these shops is to sell organic products, but some of them also carry non-organic products. Typically, more than 2/3 of the product range is organic. Often these shops sell books and magazines related to health issues as well as natural medicine, herbs and dietetic products. As illustrated below, the organic food shops are not solely business oriented as it is important for them that there are sustainable values behind the actions.

Concerning the future outlook for the organic food shops, they are expected to benefit from the organic advertising campaigns made by the conventional super-/hypermarkets. On the other hand, the independent organic food shops will face a continuously increasing competition, especially from the newly established organic supermarkets chains.

47 The shop owner typically works in the shop together with a few other employees.

Core business Organic foods Organic sales arguments Health and food safety, taste and ideology THE BUSINESS FACTS Shops per capita Very few (Less than 1 per 100.000 inhabit.) Size of store 50-400 m2 Shop design Unprofessional (often lack of organization) Organic price premium 77 – 121 % Durable organic products Complete Fresh organic products Variable Variety within product groups Limited THE RESOURCES Management Individual managers47 (no top management) Strategic planning Very limited Personnel Skilled, possess expertise Capital to invest None

“I think that in the beginning more chains will open, but later, in a future with conventional distribution, they will merge and there will be 2 or 3 remaining.” Ana Arruti, Purchasing Manager. Comme-Bio, Spain.

Ideology Business opportunity

Organic food shops Tradition.al - Visionary

Organic foods in Spain 2003 Martin Joensen

26

It is important to be aware that the independent organic food shops can be divided into two categories: ‘the visionary organic shops’ and ‘the traditional organic shops’. The visionary shop owners recognize the importance of the commercial aspect of the business and are willing to adapt to the ongoing market changes. This is for example reflected in shop design and utilization of space in the shops. The visionary shops are expected to have better prospects for success in the future market for organic foods in Spain. The owners of the traditional shops are generally reluctant to change and believe that marketing efforts and other business actions compromise the organic idea. Another obstacle for the future development of organic food shops is that many shop owners have reached an age where a

generation shift is soon needed. One shop owner explains: “I don’t know what I will do when I am leaving. This [the shop] will go, I will close it. I don’t know, it is not clear to me, because I wouldn’t like just to leave it to anybody, you know? After so many years of work and then leave it to people with whom you don’t have a relation is simply not my idea. I wouldn’t like that!” The same tendency has already been detected in Holland. Allard ten Dam, General Manager of one of the Dutch wholesaler ‘De Nieuwe

Band’ explains: “…the traditional customers are declining because one after another organic food shop is closing. Mostly, the owners started 20-25 years ago and now they are tired and don’t have any energy more to change their shop, to change their mentality. They don’t want to get involved with more commercial material and they stop.”48

48 Dam.

Organic foods in Spain 2003 Martin Joensen

27

Ideology Business opportunity

Health Food Shops

4.1.4 The health food shops In Spain, there are approximately 2500 health food shops.49 These shops are very small but due to the high number they presently hold a considerable market share of the organic retailing. As the word indicates, the health food shops mainly carry health products such as natural medicine, herbs and food products that are perceived to be healthy. In these shops organic foods play a minor role. However, as the organic products are gaining the image of being healthy, the health food shops are increasingly including these in their product range. The organic products in the health food shops are mixed with conventional health food products. This makes it difficult for the end-customers to make a distinction. As illustrated below, they are more business oriented than idealistic.

In the medium term, there is a certain potential for increasing the organic turnover in the health food shops as these shops have various conventional food products that could easily be replaced by substituting organic products.50 In the picture to the right, a few organic products are mixed with other conventional

products. However, as the health food shops are more business driven than ideologically driven, it demands a considerable proportion of customers who are willing to pay the price premium, because the organic products are approximately 100 % more

49 Gonzálvez Pérez. 50 Other products that can be considered as substitutes to organic foods in Spain are functional food and Delicatessen.

Core business Natural medicine, dietetic and health food Organic sales arguments Health and cure THE BUSINESS FACTSS Shops per capita Moderate (1 per 16.000 inhabitants) Size of store 20-40 m2 Shop design Poor Organic price premium 77 – 121 % Durable organic products Very limited Fresh organic products Poor Variety within product groups Poor THE RESOURCES Management Individual managers (no top management) Strategic planning Very limited Personnel Skilled, (but lack organic knowledge) Capital to invest None

Organic foods in Spain 2003 Martin Joensen

28

expensive than the conventional products they would replace. Furthermore, the growth potential is limited due to the small shelf place available in the shops. It is not unusual that a shop of less than 30 m2 has more than 40 suppliers of which 5 are supplying organic foods. On a long-term basis, the health food shops are likely to develop into a niche retailer with regards to organic foods. This is due to lack of focus on organic products and increased competition from the other organic retailers. In France, for instance, the sales via small health food shops were important up until the 1990’s. Today, however, supermarkets and organic supermarket chains are gaining more and more importance.51

4.1.5 Organic consumer cooperatives Organic cooperatives arose as consumers began to organize shared purchasing. Presently there are approximately 25 in Spain, especially in Andalusia, Catalonia and in the Basque Country. They typically have 100 – 300 members and some have a shop as well.52 As illustrated below, they are very ideologically oriented. Besides the retailing function, the consumer cooperatives also serve as a meeting point for people with a high interest in the ideology behind organic production. The consumer cooperatives are the most ideological organic retailer type.

They do not place much effort in increasing their market share. Therefore, it is likely that they will lose relative importance as the market grows. However, in absolute values they are expected to maintain the current status of a nice retailer.

51 Reynaud and Schmidt. 52 Valls.

Core business Organic foods Organic sales arguments Ideology, environment, health & food safety THE BUSINESS FACTS Shops per capita Very few (Less than 1 per 1.000.000 inhabit.) Size of store Around 50 - 150 m2 Shop design Little importance Organic price premium 65 – 103 % Durable organic products Many Fresh organic products Moderate Variety within product groups Some THE RESOURCES Management Working groups Strategic planning Very limited Personnel Voluntaries, well informed. Capital to invest None

Ideology Business opportunity

Organic consumer

cooperatives

Organic foods in Spain 2003 Martin Joensen

29

4.1.6 Pharmacies In the last few years, the competition on the pharmaceutical market has been intensified as the total number of pharmacies in Spain has risen from 16.700 in 1983 to 19.300 in 1999. In addition, new competition has risen from the so-called ‘para-pharmacias’, selling everything the pharmacies do not have monopoly on. They have developed from 0 in 1992 to a total of 213 in 2001. Generally, pharmacies in Spain do not carry organic foods. However, some pharmacies have recently introduced organic food products. These products generally replace other non-organic health food products, which the pharmacy carried before. A weakness of the pharmacies is that they are used to delivering products to customers according to prescriptions, which means that they do not have much sales experience. The motives for carrying organic foods are similar to the health shops’ motives, which are customer demand and the fact that organic products are perceived to be healthier.

In regards to future expectations of sales of organic foods in pharmacies, it is positive that some

pharmacies have already introduced organic products based on customer demand.53 This implies that there might be further opportunities, especially if suppliers or wholesalers take a more active approach. This especially concerns replacement of non-organic food products. Also, the “para-pharmacias” seem to be an interesting segment for organic products, because they need to replace the products on which the pharmacies have a monopoly. On the down side, the

organic products will never be the core business of the pharmacies, and with the limited space in most pharmacies, the potential is limited.

53 Collado.

Core business Medicine Organic sales arguments Health THE BUSINESS FACTSS Shops per capita Many (1 per 2.000 inhabitants) Size of store 20-100 m2 Shop design Semi professional Organic price premium Not calculated. Similar to specialized shops. Durable organic products Very limited Fresh organic products Very limited or none Variety within product groups Very limited THE RESOURCES Management Independent Managers (chains are illegal) Strategic planning Limited Personnel Skilled, but lack organic sales experience Capital to invest Very limited

Ideology Business opportunity

Pharmacies

Organic foods in Spain 2003 Martin Joensen

30

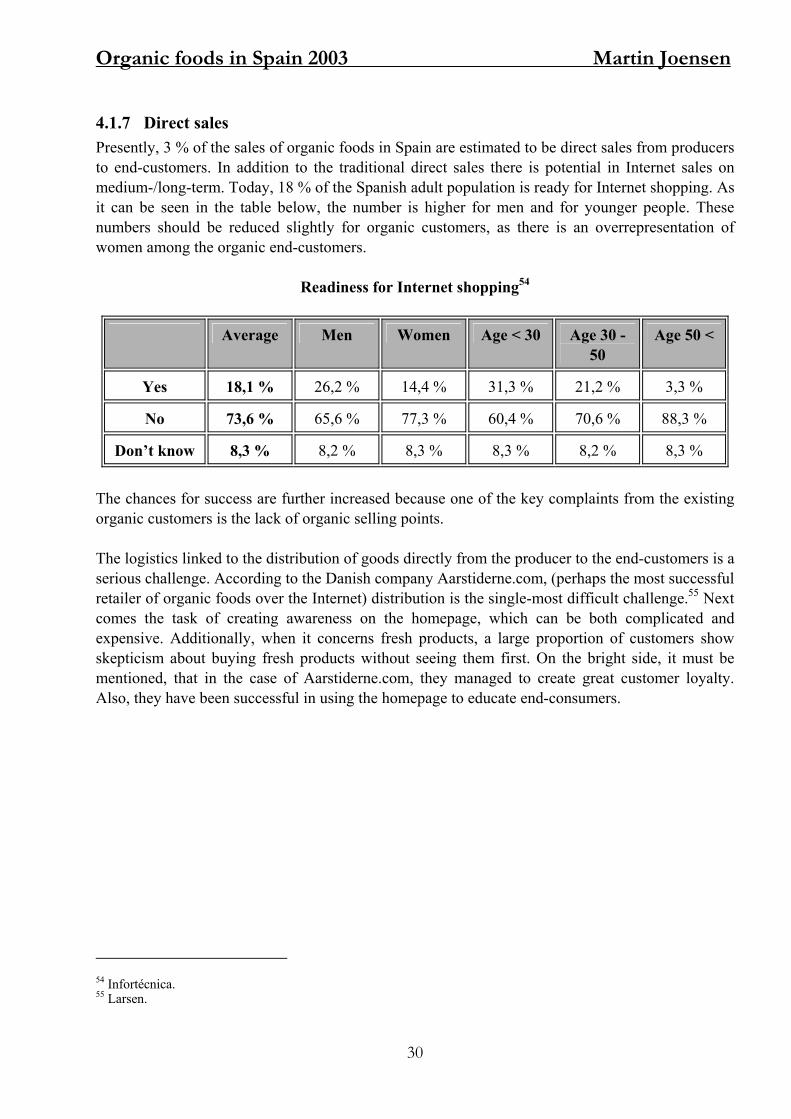

4.1.7 Direct sales Presently, 3 % of the sales of organic foods in Spain are estimated to be direct sales from producers to end-customers. In addition to the traditional direct sales there is potential in Internet sales on medium-/long-term. Today, 18 % of the Spanish adult population is ready for Internet shopping. As it can be seen in the table below, the number is higher for men and for younger people. These numbers should be reduced slightly for organic customers, as there is an overrepresentation of women among the organic end-customers.

Readiness for Internet shopping54

Average Men Women Age < 30 Age 30 - 50

Age 50 <

Yes 18,1 % 26,2 % 14,4 % 31,3 % 21,2 % 3,3 %

No 73,6 % 65,6 % 77,3 % 60,4 % 70,6 % 88,3 %

Don’t know 8,3 % 8,2 % 8,3 % 8,3 % 8,2 % 8,3 %

The chances for success are further increased because one of the key complaints from the existing organic customers is the lack of organic selling points. The logistics linked to the distribution of goods directly from the producer to the end-customers is a serious challenge. According to the Danish company Aarstiderne.com, (perhaps the most successful retailer of organic foods over the Internet) distribution is the single-most difficult challenge.55 Next comes the task of creating awareness on the homepage, which can be both complicated and expensive. Additionally, when it concerns fresh products, a large proportion of customers show skepticism about buying fresh products without seeing them first. On the bright side, it must be mentioned, that in the case of Aarstiderne.com, they managed to create great customer loyalty. Also, they have been successful in using the homepage to educate end-consumers.

54 Infortécnica. 55 Larsen.

Organic foods in Spain 2003 Martin Joensen

31

4.2 Future retailing structure To summarize the expectations of the different organic retailer types a growth/share matrix has been made. The placement of the circles in the figure indicates the position in the medium term, not the present situation. The arrows indicate in which direction the different retailers are expected to move in a long-term perspective. As it can be seen, the conventional super-/hypermarkets are expected to gain much importance. However, it is evident that the super-/hypermarkets can only be considered as competition to the other retailers with regards to those few organic products which they carry. Therefore, the serious competition from the super-/hypermarkets will not be faced until the their product range is increased to several hundred products. Until then, the conventional super-/hypermarkets are expected to have more positive than negative effects on other retailers. The fact that the competition between conventional super-/hypermarkets and the other organic retailers is not that intense is confirmed by the customer survey which reveals, for example, that only 20 % of customers in the specialized shops have bought an organic product in a conventional super-/hypermarket. The conventional super-/hypermarkets’ expected increase in the organic market share is likely to result in a reduction in the relative importance of the other retailers. This is in line with the development in most other European markets. However, it does not necessarily imply that the other retailers, especially the specialized shops will experience a decrease in sales. On the contrary, in the medium term, the other organic retailers are more likely to increase their sales as the organic market share of the super-/hypermarkets grows. Examples of this have already been seen in Spain. For example when the conventional supermarket chain ‘El Corte Inglés’, in Barcelona, introduced organic foods, the organic foods shops and the health food shops around El Corte Inglés experienced a boost in sales.56

56 Roger.

Organic foods in Spain 2003 Martin Joensen

32

In other markets similar experience has been made. The most extreme case is the Netherlands, where the super-/hypermarkets increased their organic market share from 2 % to 41 % in the period 1997/98 to 2000. At the same time the specialized organic food stores managed to increase their sales continuously. According to the statistics available, the organic food stores in the Netherlands increased their sales from 240 million Euros in 1999 to 335 million Euros in 2002, equivalent to a 10-15 % annual increase.57 One of the main reasons for the expected positive effect caused by the conventional super-/hypermarkets is that the different conventional super-/hypermarkets have concrete plans about making organic promotion campaigns. Jorge Bilbao, Organic Products Manager at the Eroski Group explains: “…recently, in the beginning of November (2002) we made a campaign to create awareness about organic products among the consumers in the Eroski Group. We had stands at the selling points where qualified personnel informed the consumers about the organic products and let the consumers taste the products…the purpose of these campaigns is more to inform and create awareness rather than sell.“58 Pedro López, from Alcampo says: “…for the upcoming year (2003) we have specific plans about development of organic products, I will not tell you what they are, but we do have a medium- and long-term strategy.”59 These campaigns are expected to expand of the organic market. Furthermore, a likely effect of this is that a certain proportion of the new organic customers will search for shops with a wider organic product range, namely the specialized shops.

4.3 Organic wholesalers In Spain there are a number of organic wholesalers who play a central role in the distribution of organic foods. These wholesalers carry up to 3.000 organic food products, both local and foreign. Several also carry a considerable number of non-organic products, whereas others specialize in organic foods. None of the wholesalers are truly nationwide, but several cover many regions by cooperating with other wholesalers or distributors. Some of the wholesalers have own distribution whereas others rely on external distribution companies. Many also carry private labels and it is not unusual for a wholesaler to manufacture organic food products as well. Very few wholesalers supply to the conventional super-/hypermarkets as these retailers normally purchase large quantities directly from the producer. Also, several organic wholesalers are not interested in supplying to the conventional super-/hypermarkets. This is due to ideological reasons or because of concern over the reaction from specialized retailers who are the wholesalers’ most important present customers. On next page some of the major organic wholesalers are listed.

57 Melita. 58 Bilbao Bagan. 59 López Salcedo.

Organic foods in Spain 2003 Martin Joensen

33

Natureco, SL Avda. del Prat, No. 20-22 08180 Moià (Barcelona) Spain Tel: +34 938 300 166 Fax: +34 938 208 404 E-mail: [email protected]

Aikider, SL Ciudad del Transporte c/Tudela, s/n 31119 – Imarcoain – Navarra Spain Tel: +34 948 314 136 Fax: +34 948 314 120 E-mail: [email protected]

Biomundo, SL C/ Carretilla 26 Rivas Vaciamadrid - Madrid 28529 Spain Tel: +34 916 665 992 Fax: +34 916 665 652 E-mail: [email protected]

Natursoy, SL Josep Gallés,36-52 08183 Castelltercol (Barcelona) Spain Tel: +34 938 666 042 Fax: +34 938 666 250 E-mail: [email protected]

BIOCOP, SA Ctra. C-155 km 12, 7 nr 3 08185 Lliça de Vall (Barcelona) Spain Tel: +34 938 436 517 Fax: +34 938 439 600 E-mail: [email protected]

Món Verd, SCCL C/ Àvila, 71-75 Àtic 08005 Barcelona Spain Tel: +34 934 855 596 Fax: +34 934 855 609 E-mail: [email protected]

Hortec, SCCL Nau j-5 Mercabarna 08040 Barcelona Spain Tel: +34 932 634 304 Fax: +34 932 630 797 E-mail: [email protected]

Élafos, SL Industria 22 50793 Fabara Spain Tel: +34 976 635 381 Fax: +34 976 635 409 E-mail: [email protected]

Organic foods in Spain 2003 Martin Joensen

34

5 End-customers Since the market for organic foods in Spain represents around 0,2 % of the total food market it is roughly estimated that only 0,2 % of the end-customers in Spain can be characterized as organic end-customers.60 The main reason for this is that in Spain there is little awareness about organic foods due to lack of knowledge among end-customers. This is probably the most important barrier to the development of the domestic market. When the Spanish customers are asked whether organic products exist, only 43 % of them give an affirmative answer with regards to food.61 Furthermore, those consumers who possess knowledge about the existence of organic products have unclear or incorrect knowledge about what it means when a product is organic.

Consumer definitions of organic foods62

Products are considered organic because they: According to definition • Are recycled No • Are recyclable No • Do not contain pesticides or chemical fertilizers Yes • Save water No • Are biodegradable No • Do not damage the ozone layer No • Save energy No • Are natural (Yes)

As indicated, the majority of the reasons mentioned by the Spanish consumer have limited or no relation with the definition of organic products. This means that there is great confusion among Spanish consumers about organic foods, although all the reasons given are very positively loaded. Furthermore, it is positive that those Spanish consumers who are aware of the existence of organic foods have a very positive impression. Furthermore, the consumers are increasingly conscious about what they eat. Also, a survey suggests that the Spaniards increasingly care about the environment.63

60 Two modifications have been made in this calculation. On the one hand, the organic customers on average use around half of their food budget on organic foods. On the other hand, organic products are approximately twice as expensive as conventional products. Thus, 0,2 % of the market is approximately equal to 0,2 % of the customers. 61 Fundación Entorno. 62 Fundación Entorno. 63 Fundación Entorno.

Organic foods in Spain 2003 Martin Joensen

35

5.1 Demographic information When questioning organic retailers in Spain about the typical demographics of their customers, they state that: “They are very varied”64 or “It is very difficult to generalize.”65 The customer survey did not provide any clear demographic segments either. With regards to age, all age groups

are represented. However, compared to the general age distribution of the Spanish population, the end-customers in the age 31 – 49 are more frequently represented as organic customers. Rather than indicating that they shop organically more frequently than other groups, the most likely explanation is that this group generally shops more frequently than average. According to our survey, females do 63,5 % of the shopping for organic foods, leaving only 36,5 % to the males. However, this is similar to general shopping habits for other products in Spain.66 With regards to children, the survey revealed that 38 % of

the respondents in age group 18 – 49 years have children. According to the research made by Wier et al,67 households with children younger than 7 years buy more organic foods than households without children. Looking at the educational background it is concluded that people from all educational levels buy organic foods.

Organic customers’ educational level

Housewives18 %

Retired8 %

Students9 %

No/lower21 %

Medium26 %

Higher18 %

As it can be seen, 26 % of the respondents had a medium education and 18 % an higher education, which is not considerably different from the Spanish population as a whole.68 In regards to the income level of the present organic customers in Spain, the retailers interviewed share very similar

64 This shop owner requested to be anonymous. 65 Santiago. 66 ACNielsen España 67 Wier and Smed. 68 The Economist Intelligence Unit

Organic foods in Spain 2003 Martin Joensen

36

opinions. One organic food shop owner says: “They are average people, who maybe do not belong to the lowest social class, the very poor ones; but there are workers, there are many doctors, many nurses, teachers, many people like that…”69 This statement makes logical sense since organic foods in Spain on average cost 100 % more than conventional food products.

5.2 Buying motives In Spain many consumers have ‘egoistic’ motives for buying organic foods, such as health and food safety for themselves or their family. Others have more idealistic reasons such as environment and animal protection. Most customers however, buy organic foods for more than one reason. The buying motives are often a mixture of several dimensions related to health, taste, environment, and many other factors.

83

31 30

8 7 6 5 4

0

10

20

30

40

50

60

70

80

90

100

%

Health &food safety

Taste Environ-ment

Fair trade Morenatural

Animalprotection

Localproducts

Curiosity

Organic purchasing reasons in Spain

According to the end-customer survey, the most important reason for purchasing organic products in Spain is that they are perceived to be healthier and safer than conventional foods. An eminent factor is the fear of allergies, cancer and other illnesses caused by conventional foods that contain pesticides, growth hormones, GMOs70 and additives. This fear is not scientifically documented, but out of prudence many choose to buy organic foods believing that there is a reduced health risk, documented or not. Food safety has become particularly important in the aftermath of the European Union’s problems with BSE and other animal diseases.71 It is a fact that there is a very limited use of additives and antibiotics in organic foods as well as the prohibiting of GMO. Also, organic food products have a higher nutritional value than non-organic foods. Illustrated below are some of the results from a scientific study made by researchers at Rutgers University, USA.72 69 Guevara. 70 GMOs are Genetically Modified Organisms. 71 Escudero: “Spain Food Processing Ingredients Sector Report 2001”. 72 BioCultura

Organic foods in Spain 2003 Martin Joensen

37

Nutritional value of conventional/organic vegetables73

Calcium Magnesium Potassium Sodium Manganese Iron Copper

Beans Organic 40,5 60,0 99,7 8,6 60,0 227,0 69,0 Conventional 15,5 14,8 29,1 0,0 2,0 10,0 3,0 Lettuce Organic 71,0 49,3 176,5 12,2 169,0 516,0 60,0 Conventional 16,0 13,1 53,7 0,0 1,0 9,0 3,0 Tomato Organic 23,0 59,2 148,3 6,5 68,0 1938,0 53,0 Conventional 4,5 4,5 58,6 0,0 1,0 1,0 0,0

As it can be seen, there is a drastic difference in the nutritional value. In this study it is concluded that conventional products have 87 % less nutritional value compared to organic products. This means that the consumer of conventional food only gets 13 % of minerals etc. that should be in the food. The second important motive for purchasing organic foods in Spain is that organic foods are said to taste better. Apart from the end-customer’s opinion on this, the commercial players in the sector for organic foods in Spain agree that organic foods taste better.74 In other markets, such as the Danish, taste especially was an important factor in the early market stages when craftsman companies producing high quality foods characterized the market.75 As the market develops and other producers enter, there are more divided opinions on whether or not organic foods taste better. A third important purchasing motive is environmental consciousness. In Spain, the environment has lesser influence than in most other countries.

Little personal influence on the environment76 (in %)

1999 2000 2001 Russia 87 93 91 India 80 76 85 Mexico 44 58 55 Japan 56 53 53 Spain 32 51 44 UK 45 43 44 France 80 85 43 Germany 34 33 32 USA 28 27 31

73 Milliequivalents per 100 grams 74 DHVMC. 75 Økologisk Landscenter. 76 Fundación Entorno.

Organic foods in Spain 2003 Martin Joensen

38

This is because the environment is generally not considered as a personal responsibility and many consumers in Spain think that they personally can do little about environmental protection. When asking the Spanish population in 2001 if they ‘either worried or worried a lot’ about the environment, 89 % answered ‘yes’. However, when it concerns personal responsibility for the environment, 44% of the Spaniards felt that they could do little about it. In comparison to other developed countries Spain has an intermediate ranking as the level in the most optimistic countries is around 30 %. On the other hand, compared to developing countries, where around 90 % of the inhabitants feel that they can do little about environmental problems, the Spaniards are very optimistic. Another measurement for the buying motives are the sales arguments used by retailers. However, it important to note, that the retailers’ selling arguments do not necessarily correspond to the consumers’ motivation for purchasing. The retailers may be wrong in their perception of what is important for consumers. Therefore, this information should only be seen as a supplement to the primary information from the end-customer survey and the retailer interviews.

Retailers’ sales arguments77 (1 = low importance 7 = high importance)

Country Food safety Nature conservation

Taste Animal welfare

Spain 7 1 5 2 Belgium 7 7 7 6 France 7 5 6 5 Austria 7 5 5 6 Sweden 7 6 1 2 Italy 7 6 1 1 Greece 7 2 3 1 UK 7 5 3 3 Switzerland 6 6 2 6 Germany 6 4 5 4 Netherlands 6 4 2 3 Denmark78 5 1 - 4 Average 6,6 4,3 3,6 3,6