optimal test for markov switching parametersecon.ucsb.edu/~doug/245b/papers/optimal test for... ·...

TRANSCRIPT

Optimal Test for Markov Switching Parameters�

Marine Carrascoy Liang Huz Werner Plobergerx

May 2009

Abstract

This paper proposes a class of optimal tests for the constancy of parameters inrandom coe¢ cients models. Our testing procedure covers the class of Hamilton�smodels, where the parameters vary according to an unobservable Markov chain,but also applies to nonlinear models where the random coe¢ cients need not beMarkov. Standard approaches do not apply. We use Bartlett-type identities for theconstruction of the test statistics. It has several desirable properties. First, it onlyrequires estimating the model under the null hypothesis where the parameters areconstant. Second, we show that the tests of this class are asymptotically optimal inthe sense that they maximize a weighted power function. Moreover, we show thatthe contiguous alternatives converge to the null with a nonstandard rate of decay.

�An earlier version of this paper has circulated under the title "Optimal Test for Markov Switching."Carrasco gratefully acknowledges partial �nancial support from the National Science Foundation undergrant SES-0211418.

yUniversity of Montreal, email: [email protected] of Leeds, email: [email protected] University in St Louis, email: [email protected]

1. Introduction

In this paper, we focus on testing the constancy of parameters in dynamic models. Theparameters are constant under the null hypothesis, whereas they are random and weaklydependent under the alternative. The model of interest is very general and includes asspecial case the Markov switching model of Hamilton (1989) where the regime changesin the parameters are driven by an unobservable two-state Markov chain and the statespace models. The random coe¢ cients need not be Markov and the model under the nullneed not be linear and could be a GARCH model for instance.Two distinct features make testing the stability of coe¢ cients particularly challenging.

The �rst is that the hyperparameters that enter in the dynamics of the random coe¢ cientsare not identi�ed under the null hypothesis. As a result, the usual tests, like the likelihoodratio test, do not have a chi-square distribution. The second feature is that the informationmatrix is singular under the null hypothesis. This is due to the fact the underlying regimesare not observable. The �rst feature known as the problem of nuisance parameters thatare not identi�ed under the null hypothesis also arise when testing for structural change orthreshold e¤ects. It has been investigated in many papers: Davies (1977, 1987), Andrews(1993), Andrews and Ploberger (1994), Hansen (1996) among others. However, the secondfeature of our testing problem implies that the �right�(i.e. contiguous) local alternativesare of order T�1=4, while they are of the order T�1=2 in the case of structural change andthreshold models. The optimality discussed below shows that there do not exist tests withnontrivial power against local alternatives that converge faster than T�1=4: Therefore, itis necessary to consider this rate of convergence when discussing power. Consequently,the results of Andrews and Ploberger (1994) do not apply here and we need to expandthe likelihood to the fourth order to derive the properties of our test.Our contribution is twofold. First, we propose a new test for parameter stability. This

test is based on functionals of the �rst two derivatives of the likelihood evaluated underthe null and the autocorrelations of the process describing the random parameters. It hasa �avour of White�s (1982) information matrix test and shares some of its advantages.In particular, it requires the estimation of the model under the null hypothesis only.This feature is particularly desirable when testing the stability of the coe¢ cients in acomplex model such as the GARCH model which is typically very di¢ cult to estimateunder the alternative. Another advantage of our test is that it does not require a fullspeci�cation of the dynamics of the random coe¢ cients. We only need to know theircovariance structure. It means that our test will have power against a wide variety ofalternatives. The second contribution of our paper is to show that the proposed testis optimal in the sense that there exists no test that is more powerful for a speci�calternative that we are going to characterize. The proof consists in showing that for �xedvalues of the nuisance parameters, our test is equivalent to the likelihood ratio test. Then,the nuisance parameters are integrated out with respect to some prior distribution. Weappeal to Neyman-Pearson theorem to prove optimality.There are few papers proposing tests for Markov-switching. Garcia (1998) studies

the asymptotic distribution of a sup-type Likelihood ratio test. Hansen (1992) treats

2

the likelihood as a empirical process indexed by all the parameters (those identi�ed andthose unidenti�ed under the null). His test relies on taking the supremum of LR over thenuisance parameters. Both papers require estimating the model under the alternatives,which may be cumbersome. None investigates local powers. Gong and Mariano (1997)reparametrize their linear model in the frequency domain and construct a test basedon the di¤erences in the spectrum between null and alternative. Although they do notdiscuss the asymptotic power of their tests, a closer reading of their paper shows thattheir test shares certain features with our test. A Bayesian model selection procedure forMarkov switching is proposed by Kim and Nelson (2001). Some work has been done ontesting for independent mixtures, Chesher (1984), Lee and Chesher (1986), Davidson andMacKinnon (1991), among others. Recently, Cho and White (2007) propose a likelihoodratio test for iid mixture in dynamic models and show that this test has power againstMarkov-switching alternatives even though it ignores the temporal dependence of theMarkov chain. Finally, Rotnizky et al. (2000) investigate the properties of the maximumlikelihood estimators (MLE) in models where the information matrix is singular. Althoughthe parameters are identi�ed, the MLE have a slower rate of convergence than usual. Oursetting is quite di¤erent because (i) some of our parameters are not identi�ed under thenull hypothesis and (ii) we are interested in testing, not estimating the model.To illustrate our method, we apply our test to the US stock prices and �nd that

the residual of the regression of the log stock price index on the log dividend exhibits anasymmetric behavior over the phases of the business cycle with slow increases and fast de-creases. It is worth mentioning other applications of our test. In a recent paper, Hamilton(2005) argues that a linear statistical model cannot capture the recurring cyclical patternobserved in economic aggregates. He applies our test to show that there are nonlinearitiesin the unemployment rate over the business cycle and that a Markov switching model isparticularly well designed to capture these nonlinearities. Other published applicationsof our test include Warne and Vredin (2006), Kahn and Rich (2007), and Hu and Shin(2008).The outline of the paper is as follows. Section 2 describes the test statistic. Section 3

establishes the optimality. Section 4 investigates the power of the test. In Section 5, wedescribe simulation results. In Section 6, we apply our test to investigate the asymmetryin stock price dynamics. Finally, Section 7 concludes. In Appendix A, we de�ne the tensornotations used to derive the fourth order expansion of the likelihood. These notations areinteresting in their own as they could be used in other econometric problems involvinghigher-order expansions. The proofs are collected in Appendix B.

2. Assumptions and test statistic

Let us assume that we observe a sample of data y1; y2; :::; yT (they could be multivari-ate, univariate, of whatever nature). We are interested in models for the conditionaldistributions of the yt. Let us denote by ft (:) the conditional density (with respect tosome dominating measure) of yt given yt�1; :::; y1: We assume that we know ft (:) up toa p-dimensional vector of parameters, say �t. We are interested in testing whether these

3

parameters are constant over time. Namely, we test

H0 : �t = �0, for some unspeci�ed �0 (2.1)

againstH1 : �t = �0 + �t; (2.2)

where the switching variable �t is not observable. We will construct asymptotically optimaltests for this testing problem under some assumptions on the structure of the �t. So ourbasic probability spaces are the sets of all (y1; y2; ::; yT ; �1; �2; :::; �T ) :Assumption 1. The latent variable �t is stationary and its distribution may depend onsome unknown parameters �. They are nuisance parameters that are not identi�ed underH0. We assume that � belongs to a compact set B. Moreover, �t is strongly exogenous inthe sense that the joint likelihood of (y1; y2; ::; yT ; �1; �2; :::; �T ) factorizes in the followingway

TYt=1

f (ytj�t; yt�1; yt�2; :::; y1) q��tj�t�1; �t�2; :::; �1; �

�(2.3)

and the values of �t belongs to some compact subset of Rp; �; containing �0.So we assume that even under the null there exists a distribution of the �t. Neverthe-

less, it can be easily seen that under the null (2.1) this distribution does not play any rolewith regard to the distribution of the data (yT ; yT�1; yT�2; :::; y1). Hence we can - whenwe �x �0 - consider our null to be simple. The distribution of �t does not in�uence thedensity of the data. It will, however, show its usefulness in the calculations later on.

Remark 1. Under the null (when the parameter is constant), the density (2.3) can befactorized into

TYt=1

f (ytj�0; yt�1; yt�2; :::; y1)TYt=1

q��tj�t�1; �t�2; :::; �1; �

�;

which shows that in this case the yt and the �t are mutually independent.

Assumption 2. yt is stationary under H0 and the following conditions on the conditionallog-density of yt given yt�1; :::; y1 (under H0); lt; are satis�ed. lt = lt (�), as a function ofthe parameter �, is at least 5 times di¤erentiable and for k = 1; :::; 5;

sup�2N

E�0

� l(k)t (�) 20� <1;

where l(k)t denote the k-th derivative of the likelihood with respect to the parameter � andN is a neighborhood around �0. E�0 is the expectation with respect to the probabilitymeasure corresponding to the parameter �0:

4

For the �norm�of the derivatives we can e.g. take the usual L2 norm

l(k)t (�) =

vuuut X0�i1;i2;::�k;

Ppj=1 ij=k

@klt

@�i11 @�i22 ::@�

ipp

!2:

Usually the �rst derivatives of the likelihood is associated with the vector of scores andthe second one with the Hessian. This interpretation is su¢ cient for a statement of theresults. For the proofs of our theorems, however, we need derivatives of higher orders.Their precise nature will be discussed in Appendix A.We do not impose restrictions on the moments of yt. For instance yt could be a

stationary IGARCH process. However, we rule out the case where yt is a random walk.To deal with unit root, we would have to alter the test statistic by proper rescaling and itsasymptotic distribution would be di¤erent, see Hu (2008). As in Andrews and Ploberger(1994, Section 4.1.), the vector of observable variables yt may include exogenous variables.

For technical reasons, we need to maintain some restrictions on the process �t.Assumption 3. �t is a function � of a latent Markov process #t de�ned on an arbitrarystate space. We assume that #t is stationary and �-mixing with geometric decay. Itimplies in particular that there exist 0 < � < 1 and a measurable non-negative functiong such that

supjhj�1

jE [h (#t+m) j#t]� E [h (#t)]j � �mg (#t) : (2.4)

andEg (#t) <1: (2.5)

Furthermore we assume that

E�t = 0; (2.6)

maxtk�tk � M <1: (2.7)

Moreover, the constant � and the bound M are independent of � de�ned in Assumption1 and E kgk can be bounded by a constant independent of �.

The assumption E�t = 0 is not restrictive as the model can always be reparametrizedto ensure this condition. #t �-mixing is satis�ed by e.g. irreducible and aperiodic Markovchain with �nite state space. The property that #t is �-mixing with geometric decay willimply that �t is geometric ergodic. max

tk�tk � M < 1 will also be satis�ed by any

�nite state space Markov chain, however it will not be satis�ed by an AR(1) process withnormal error. This condition could be relaxed to allow for distributions of �t with thintails but this extension is beyond the scope of the present paper. Although some form ofmixing is necessary for the �t, one should be able to relax condition (2.4).In our proofs we need some form of "near epoch dependence"-i.e. the conditional ex-

pectations of functions of the random variables involved must converge to the expectationquickly. However, we do not require �t itself to be Markov. This would be too restrictive

5

as the autocorrelation of a stationary Markov process is necessarily of the form (2.9). Ourassumption, however, allows e.g. �t to be a MA-process of the form

�t = et + a1et�1 + :::+ apet�p;

where the et are i.i.d.. In this case, #t = (�t; et; :::; et�p)0 is Markov. This example illus-

trates the potential autocorrelation functions of �t - in fact, one can easily see that the setof autocorrelations satisfying our assumption approximates an arbitrary autocorrelationin any of the usual topologies.

The test statistic TST , for a given �; is of the form.

TST (�) = TST

��; ��= �T �

1

2Tb" (�)0b" (�)

where

�T =1

2

1pT

Xt

tr��l(2)t + l

(1)t l

(1)0t

�E� (�t�

0t)�+

2pT

Xt>s

tr(l(1)t l(1)0s E� (�t�

0s))

!(2.8)

� 1

2pT

Xt

�2;t

��; ��;

and b" (�) is the residual from the OLS regression of 12�2;t

��; ��on l(1)t

���; and � is the

constrained maximum likelihood estimator of � under H0 (i.e. the ML estimator underthe assumption of constant parameters).As � is unknown and can not be estimated consistently under H0, we use sup-type

tests like in Davies (1987)

supTS = sup�2 �B

TST (�)

or exponential-type tests as in Andrews and Ploberger (1994)

expTS =Z�B

exp (TST (�)) dJ (�)

where J is some prior distribution for � with support on �B; a compact subset of B. Wewill establish admissibility for a class of expTS statistics.

Remarks.1. In some applications, it may be of interest to test for the variability of one subset of

parameters. To accommodate this case, it su¢ ces to set the elements of �t correspondingto the constant coe¢ cients equal to zero. Then, �T involves only the elements of the scoreand Hessian corresponding to the varying coe¢ cients. However, in the computation ofb" (�), one needs to project 1

2�2;t

��; ��on the whole vector l(1)t

���(including the score

with respect to the constant coe¢ cients).

6

2. The asymptotic distribution of the tests will not be nuisance parameter free ingeneral. Therefore we have to rely on bootstrap to compute the critical values.3. The test statistic TS depends only on the score and derivative of the score under

the null and on the estimator of � under H0. Therefore it does not require estimatingthe model under the alternative. This is a great advantage over competing tests likethose of Garcia (1998) and Hansen (1992) because estimating a Markov switching modelis particularly burdensome (Hamilton, 1989) or even intractable if the model is highlynonlinear as in the GARCH model.4. The test relies on the second Bartlett identity (Bartlett, 1953a,b). It is related

to the Information Matrix test introduced by White (1982). Chesher (1984) shows theInformation Matrix test has power against models with random coe¢ cients. He showsthat a score test of the hypothesis that parameters have zero variance is close to theInformation Matrix test. Davidson and McKinnon (1991) derive information-matrix-typetests for testing random parameters. The main di¤erence with our setting is that theyassume that the parameters are independent, whereas we assume that the parametersare serially correlated and we fully exploit this correlation. Recently, Cho and White(2007) show that a test based on independent mixture has power against Markov-switchingalternatives.5. The form of our test is largely insensitive to the dynamics of the latent process �t.

It depends only on the form of the autocorrelation of �t.6. We assume throughout the paper that the model under the null is correctly speci�ed.

The issue of misspeci�cation is not addressed here.7. The main di¤erence with structural change and threshold testing is that here the

local alternatives are of order T�1=4: This is due to the fact that the regimes �t areunknown and one needs to estimate them at each period. So in some sense, there is acurse of dimensionality where the number of parameters (including the probabilities tobe in each regime) increases with the number of observations. It is also linked to thesingularity of the information matrix under the null hypothesis.

Although the optimality results are proved under the general Assumptions 1 to 3, theexpression of the test statistic can be simpli�ed under the following special case.

Example 2.1. Assume that �t can be written as chSt where St is a scalar Markov chainwith V (St) = 1, h is a vector specifying the direction of the alternative (for identi�cationh is normalized so that khk = 1); and c is a scalar specifying the amplitude of the change.Moreover,

corr (St; Ss) = �jt�sj (2.9)

for some �1 < � < 1: In such case, � = (c2; h0; �)0 :

Example 2.1 implies that all the random coe¢ cients jump at the same time. However,it does not impose that all coe¢ cients should be random under the alternative. To dealwith the case where a subset of coe¢ cients remain constant under the alternative, itsu¢ ces to set the corresponding elements of h equal to zero. Assumption 3 imposes somerestrictions on the Markov chain St. If St has a �nite state space, then it will be geometric

7

ergodic provided its transition probability matrix satis�es some restrictions described e.g.in Cox and Miller (1965, page 124). More precisely, if St is a two-state Markov chain,which takes the values a and b, and has transition probabilities p = P (St = ajSt�1 = a)and q = P (St = bjSt�1 = b), St is geometric ergodic if 0 < p < 1 and 0 < q < 1: Underthis condition, St satis�es (2.9) with � = p+ q � 1:

St can also have a continuous state space as long as it is bounded. Consider anautoregressive model

St = �St�1 + "t

where "t is iid U [�1; 1] and�1 < � < 1: Then St has bounded support (�1=(1�j�j); 1=(1�j�j)) and has mean zero. Moreover, it is easy to check that St is geometric ergodic usingTheorem 3 page 93 of Doukhan (1994), hence (2.9) is satis�ed. For this choice of St, ytfollows a random coe¢ cient model under the alternative.

In example 2.1, �2;t (�; �) can be rewritten as

�2;t (�; �) = c2h0

"�@2lt@�@�0

+

�@lt@�

��@lt@�

�0�+ 2

Xs<t

�(t�s)�@lt@�

��@ls@�

�0#h; (2.10)

and �B =�c2; h; � : c2 > 0; khk = 1; � < � < ��

and �1 < � < �� < 1:

The maximum of TST (�) with respect to c2 can be computed analytically. As a result,we get

supTS = supfh;�:khk=1;�<�<��g

1

2

�max

�0;

��Tpb"�0b"���2

(2.11)

where ��T is �T (�) =c2 and b"� = b" (�) =(pTc2) so that ��T and b"� do not depend on c2:

Note that becausePT

t=1 l(1)t

���= 0; the term ��T is equal to 1

0b"� where 1 is a n � 1vector of 1. Interestingly, the ratio ��T=

pb"�0b"� corresponds to the t� statistic for testingH0 : � = 0 in the arti�cial regression

1 = ��2;t

��; ��=(2c2) + �l

(1)t

���+ residual.

For an account on the role of arti�cial regressions in speci�cation tests, see Davidson andMacKinnon (2004, Chapter 15).Below, we give three classes of models to which our estimation procedure applies.

Example 2.2. (Markov-switching model). Hamilton (1989) proposed to model the changein the log of the real gross national product as a Markov-switching model of the form8<:

yt = �0 + �1St + zt;zt = �1zt�1 + :::+ �rzt�r + "t

"t � iidN (0; �2)

where St is a two-state Markov chain that takes the values 0 and 1 with transition prob-abilities p and q. This model has been used extensively to model the business cycle, seee.g. Clements and Krolzig (2003) and Morley and Piger (2006).

8

Various extensions of this model have been applied in macroeconomics and �nance.Markov-switching GARCH models is increasingly used in �nance, see Hamilton and Sus-mel (1994), Dueker (1997), Gray (1997), Haas, Mittnik and Paolella (2004) among others.Consider the model 8<:

"t = �t�t;�2t = �0 (St) + �2 (St) "

2t�1 + �1 (St)�

2t�1

�t � iidN (0; 1)

where St is a homogenous Markov chain with k dimensional state space. Then, #t = Stis bounded, Markov of order 1 and geometric ergodic provided its transition probabilitiesbelong to (0; 1). The estimation of this model is particularly tedious. This model hasbeen successfully tested in Hu and Shin (2008) using our test procedure.

Example 2.3. (State space model). Assume that the dynamic of an observable vectoryt can be described as

yt = A0xt +H 0�t + wt

�t+1 = F�t + vt+1

where vt and wt are uncorrelated white noises and xt is a vector of exogenous or prede-termined variables.The state vector �t is not observable. The state space models are very popular because

they can be easily estimated by Kalman �lter. To simplify our discussion, assume that �tis scalar. A way to test the null hypothesis that �t is constant H0 : �t = �0 is to test thatthe variance of vt (�2 say) is equal to zero. Various di¢ culties arise. First, the parameterof interest (�2) is on the boundary of the parameter space under the null. Second, thecoe¢ cient F is not identi�ed under H0. Hence, testing H0 : �

2 = 0 is non standard.These issues are addressed in Andrews (1999, 2001).

Example 2.4. (Non Markov random coe¢ cient model). Consider a stochastic volatilitymodel 8>><>>:

yt = �+ �yt�1 + ut�t;�t = exp(vt);

vt = �+ �vt�1 + et + �et�1;ut � iidN (0; 1)

where ut and et are independent and et is iid(0; � 2). #t = (vt; et)0 is Markov, geometric

ergodic provided j�j < 1 and et has positive density around 0 although �t itself is notMarkov. This model is easy to estimate under the null hypothesis where �t is constant.

3. Local alternatives and asymptotic optimality

In this section, we establish the admissibility of expTS test. First of all let us discuss somegeneral principles for the construction of admissible tests. A test is admissible if there is no

9

other test that is uniformly more powerful. Consider a general testing problem of testinga null H0 against an alternative H1 and let �0 and �1 be two measures concentrated on H0

and H1; respectively. Furthermore assume that the probability measures for our modelsare given by densities f (�) (with respect to a common dominating measure), where thevariable � 2 H0 [H1. Then a test rejecting whenR

f (�) d�1Rf (�) d�0

> K

is admissible (this is an easy generalization of the Neyman-Pearson lemma. For an exactproof, see Strasser (1995)).We therefore have a wide latitude in the construction of admissible tests. We will

use our freedom of choice to construct tests which have additional nice properties, likethe ease of implementation. To establish admissibility, it is enough to �nd a sequenceof alternatives for which our test is equivalent to the Likelihood Ratio test. For thesealternatives, our test will be optimal.The null hypothesis for a given � is denoted as

H0 (�) : �t = �

and the sequence of local alternatives is given by

H1T (�) : �t = � + �(T )t : (3.1)

where�(T )t =

�t4pT:

The local alternative is of order T�1=4 as in Gong and Mariano (1997) and Cho andWhite (2007). Although Gong and Mariano (1997) never evaluate the asymptotic powerof their test, a closer look at their results shows that it is compatible with our theory. Intheir paper, the process representing �our��t is of the form �1St, where St is a processtaking only values 0 and 1. They test for �1 = 0 by constructing an LM-test for an-other parameter (in their notation) � = �21: Hence their test should have power againstalternatives for which � = O(1=

pT ), which implies that �1 = O(1= 4

pT ):

We start by giving a summary of our results and the intuition. Theorem 3.1 belowshows that for �0 known, a test based on

exp

1

2pT

TXt=1

�2;t (�; �0)�1

8E�0

��2;t (�; �0)

2�! (3.2)

is equivalent to the likelihood ratio test for testing H0 (�0) versus H1T (�0) and thereforeis admissible for these hypotheses. In practice, �0 is unknown and is therefore replacedby the MLE �. The problem is that the test based on (3.2) is not robust to parameteruncertainty, indeed the distribution of (3.2) with �0 replaced by � di¤ers from the dis-tribution of (3.2) with �0. As a consequence, we modify our test statistic by replacing

10

�2;t

��; ��by "t

��; ��, its projection on the space orthogonal to l(1)t

���: The resulting

test statistic is robust to parameter uncertainty. To see this, we apply the mean valuetheorem (� is omitted for convenience):

1pT

TXt=1

"t

���=

1pT

TXt=1

"t (�0) +1

T

TXt=1

@"t���

@�

�� � �0

�where � is an intermediate value. Hence under standard conditions, we have

1

T

TXt=1

@"t���

@�! E�0

�@"t (�0)

@�

�= �cov�0

�"t (�0) ; l

(1)t (�0)

�= 0:

The new test statistic is robust to parameter uncertainty but is no longer equivalent to thelikelihood ratio of H0 (�0) against H1T (�0). We show that it is equivalent to the likelihoodratio of H0 (�0) against

H1T (�T ) : �t = � +�t4pT� dp

T

where d is de�ned in (3.13). Hence, it is optimal for this alternative.Let Q�T denote the joint distribution of (�1; :::; �T ), indexed by the unknown parameter

�. Let P�;� be the probability measure on y1; y2; :::; yT corresponding toH1T (�), and P� bethe probability measure on y1; y2; :::; yT corresponding to H0 (�) : The ratio of the densitiesunder H0 (�) and H1T (�) is given by

`�T (�) �dP�;�dP�

=

Z TYt=1

ft�� + �t=T

1=4�dQ�T=

TYt=1

ft (�) :

Theorem 3.1. Under Assumptions 1-3, we have under H0 (�)

`�T (�) = exp

1

2pT

TXt=1

�2;t (�; �)�1

8E���2;t (�; �)

2�! P! 1: (3.3)

where the convergence in probability is uniform over � and � 2 N .

The proof of Theorem 3.1 is the main contribution of the paper and is given in Ap-pendix B.We can easily see from (2.8) that �2;t (�; �0) is a stationary and ergodic martingale

di¤erence sequence, hence the central limit theorem applies. Moreover, for each sequence

N 3 �T ! �0 2 N ; (3.4)

the distribution of 12pT

PTt=1 �2;t (�; �T ) will converge in distribution, under P�T , to a

Gaussian random variable with expectation 0 and variance 14E��2;t (�; �0)

2� :11

Corollary 3.2. For every sequence �T satisfying (3.4) and any �, the P�T ;� are contiguouswith respect to P�T :

This result follows immediately from the CLT mentioned above and Strasser (1995).Denote

`T

��0 �

dpT

��dP�0� dp

T

dP�0=

QTt=1 ft

��0 � d=

pT�

QTt=1 ft (�0)

= exp

(TXt=1

�lt

��0 � d=

pT�� lt (�0)

�):

Using a second order Taylor expansion around �0 � dpT, we obtain the following lemma.

Lemma 3.3. For all �0 2 N , and for all vectors d

`T

��0 �

dpT

�= exp

� 1p

T

TXt=1

d0l(1)t

��0 �

dpT

�+1

2E�0

�d0l

(1)t

��0 �

dpT

��2!! 1

uniformly (in d on all compacts) in probability.

Again, our regularity conditions guarantee the convergence of 1pT

PTt=1 d

0l(1)t (�0) to a

normal distribution with mean zero and variance E��d0l

(1)t (�0)

�2�, hence we can con-

clude that P�0� dpT

are contiguous with respect to P�0 : Since contiguity is a transitive

relationship, we may conclude that for all vectors d; P�0� dpT;� is contiguous with respect

to P�0 : FromdP�T ;�dP�0

=dP�T ;�dP�T

dP�TdP�0

we can conclude that with

�T = �0 �dpT; (3.5)

dP�T ;�dP�0

=

exp

1

2pT

TXt=1

�2;t (�; �T )�1

8E�0

��2;t (�; �T )

2�� 1pT

TXt=1

d0l(1)t (�T ) +

1

2E�0

��d0l

(1)t (�T )

�2�!! 1

where the convergence is - again - uniform in probability with respect to P�0.Now, we can proceed to construct optimal tests of H0 (�0) against the alternatives

H1T (�T ). First assume that we know �0 2 �. Then contiguous alternatives to H0 (�0) aredescribed by the probability measures

P�T ;�;

12

where �T is given by (3.5). We now want to compare tests with respect to their powersagainst these alternatives. In particular, we want to characterize tests by optimalityproperties. We start with a sequence of tests T and then show that there does not existanother sequence of tests 'T which is asymptotically �better� for the null and all thecontiguous alternatives. So let us formally de�ne �better�tests.

De�nition 3.4. A sequence 'T of tests is asymptotically better than T at �0 if it is�better�under the null

lim sup

Z'TdP�0 � lim inf

Z TdP�0

and �better�under the alternatives, that is, for all �T and �

lim inf

Z'TdP�T ;� � lim sup

Z TdP�T ;�:

This de�nition is essentially the same as that used by Andrews and Ploberger (1994)and a bit di¤erent from the one in Strasser (1995). Although the latter can be very usefulwhen analyzing the asymptotic behavior of possible power functions for testing problems,our de�nition turns out to be more practical in econometric analysis because it directlydeals with the asymptotic behavior of tests. Our de�nition here is, however, close enoughto the one in Strasser (1995) so that we can use the standard proofs of optimality.

De�nition 3.5. A test T is said to be admissible if there exists no asymptotically bettertest.

Let 'T be some test statistic that has asymptotic level � (i.e. limR'TdP�0 = �)

and asymptotic power function (i.e. limR'TdP�T ;� exists). Let K � 0 be an arbitrary

constant, and � be an arbitrary, but �nite measure concentrated on a compact subset ofB �Rp. Without limitation of generality we can assume that � (B �Rp) = 1. Then letus de�ne the loss function as

L ('T ) = K

Z'TdP�0 �

Z �Z'TdP�0�d=

pT ;�

�d�(�; d): (3.6)

By Fubini�s theorem, we have

L ('T ) =

Z(K �

dP�0�d=pT ;�

dP�0)'TdP�0d�(�; d) (3.7)

=

Z �K �

�ZdP�0�d=

pT ;�

dP�0d�(�; d)

��'TdP�0

From (3.7) we can easily see that, for �xed K; L('T ) is minimized by the tests T ; whichsatisfy

T =

8<: 1 ifnR dP�0�d=

pT;�

dP�0d�(�; d)

o> K

0 ifnR dP�0�d=

pT;�

dP�0d�(�; d)

o< K

9=; : (3.8)

13

So the minimal loss only depends on the distributions of thenR dP�0�d=

pT;�

dP�0d�(�; d)

o.

We can easily see that the measuresRP�0�d=

pT ;�d�(�; d) are contiguous with respect to

P�0, too. Hence the minimal loss equals

�Z ��Z

dP�0�d=pT ;�

dP�0d�(�; d)

��K

�(+)dP�0;

where, for an arbitrary real number x, x (+) denotes the positive part of x.Let us now assume that we have a competing sequence of tests 'T . Note that

(3.8) does not uniquely determine a test. Indeed, the behavior of the test on the eventhnR dP�0�d=pT;�

dP�0d�(�; d)

o= K

idoes not matter. Hence the following de�nition will be

useful.

De�nition 3.6. The tests 'T and '0T are asymptotically equivalent (with respect to ourloss function L) if and only if for all " > 0

limE�0 j'T � '0T j I������Z dP�0�d=

pT ;�

dP�0d�(�; d)

��K

���� > "

�= 0:

So, heuristically speaking, 'T and '0T give us the same decision provided the test

statisticR dP�0�d=

pT;�

dP�0d�(�; d) is di¤erent from the critical value K. Moreover, we have the

following result.

Theorem 3.7. Let T be de�ned by (3.8) and 'T be an arbitrary test.(i) If 'T and T are asymptotically equivalent in the sense of De�nition 3.6. Then

lim (L( T )� L ('T )) = 0: (3.9)

(ii) If 'T and T are not asymptotically equivalent, then

lim inf (L( T )� L ('T )) < 0: (3.10)

Hence (3.9) implies that T and 'T are asymptotically equivalent.

We conclude from Theorem 3.7 that the tests T and all asymptotically equivalentsequences of tests are admissible. Any tests with genuinely better power functions wouldhave smaller loss, which is impossible. Hence, we have to show that our test is asymptot-ically equivalent to tests T .For this purpose, let us �rst observe that the processes

ZT (�; �) =1

2pT

TXt=1

�2;t (�; �)�1

8E�0

��2;t (�; �)

2�� 1pT

TXt=1

d0l(1)t (�)+

1

2E�0

��d0l

(1)t (�)

�2�;

are, for all � so that k� � �0k = O(1)=pT (and hence in particular the �T de�ned by

(3.5)), uniformly tight in the space C (B), the space of continuous functions on B. Indeed,

14

since the �2;t (�; �T ) are stationary martingale di¤erences, we can apply a central limittheorem and conclude that the ZT (�) converges in distribution (with respect to P�T ) toa Gaussian process with a.s. continuous trajectories. Since the P�T are contiguous to P�0 ;the limiting process(es) under P�0 must have continuous trajectories too, and we haveuniform tightness of the distributions with respect to P�0.

De�nition 3.8. De�ne �T as the tests that reject whenRexp(ZT (�; �T ))d�(�; d) > K

and accept whenRexp(ZT (�; �T ))d�(�; d) < K.

We now want to show that the tests T and �T are asymptotically equivalent. Wecan easily see that a su¢ cient condition for asymptotic equivalence isZ

exp(ZT (�; �T ))d�(�; d)=

ZdP�0�d=

pT ;�

dP�0d�(�; d)! 1: (3.11)

We know that for all �nite sets �i; di;

exp(ZT (�i; �0 � di=pT ))=

dP�0�di=pT ;�i

dP�0! 1: (3.12)

So suppose that for all " > 0 and � > 0; we could �nd a partition S1; :::; SK so that withprobability greater than 1� " for all i, (�; d) ; ( ; e) 2 Si, jZT (�; �0� d=

pT )�ZT ( ; �0�

e=pT )j < �; jdP�0�d=

pT;�

dP�0� dP�0�e=

pT;

dP�0j < �: Then, (3.11) will be an easy consequence of

(3.12).The existence of such a partition for the ZT is an immediate consequence of the

uniform tightness of the distribution of ZT : According to our assumptions, the di¤erence

between the ZT and the log of the densitiesdP�0�di=

pT;�i

dP�0converges to zero uniformly

in probability. Hence the density process is uniformly tight, too, which immediatelyguarantees the existence of the partition.Then, the tests �T are asymptotically equivalent to the tests T . Consequently, we

have the following result.

Theorem 3.9. Let 'T be a sequence of tests that is asymptotically better (in the senseof De�nition 3.4) than �T . Then 'T is asymptotically equivalent to �T .

We now are able to construct asymptotically optimal tests for each parameter �0. Theproblem, however, is that we do not know �0: Hence we will try to �nd for each �0 ameasure ��0 so that the corresponding test statisticZ

exp(ZT (�; �0 � d=pT ))d��0(�; d)

does not depend on �0. For this purpose, de�ne

d (�) = d(�; �0) = (I (�0))�1 cov

�1

2�2;t (�; �0) ; l

(1)t (�0)

�(3.13)

where I (�0) denote the information matrix. Then, we have the following result.

15

Theorem 3.10. Assume that J is a measure with mass 1 concentrated on a compactsubset of B. Let d be as in (3:13) ; then de�ne

ST (�) =

Z �exp(ZT (�; � � d(�; �)=

pT ))�dJ (�) :

Let b� be the maximum likelihood estimator for � under H0; i.e.b� = argmaxX lt(�):

ThenexpTS� ST (�0)! 0 (3.14)

in probability under P�0 ;where

expTS =Z �

exp(TST (�;b�))� dJ (�) ; (3.15)

andTST (�;b�) = 1

2pT

X�2;t

��;b��� 1

2Tb" (�)0b" (�) ; (3.16)

where b" (�) is the residual from the OLS regression of 12�2;t

��; ��on l(1)t

���:

Let Pb� be the probability measure corresponding to the value of the maximum likeli-hood estimator. (We can understand our parametric family as a mapping, which attachesto every � a measure P�: Then the measure Pb� results from an evaluation of this mappingat b�: It is a random measure). Let K(b�) be real numbers so that

Pb��hexpTS < K(b�)i� � 1� �

Pb��hexpTS > K(b�)i� � �

and assume K(b�) ! K. Then the tests 'T , which reject if expTS > K(b�), and acceptif expTS < K(b�); are for all �0 asymptotically equivalent under P�0 to tests rejecting ifST (�0) > K, and accepting if ST (�0) < K. Moreover, we have

P�0 ([ST (�0 ) < K]) � 1� �

andP�0 ([ST (�0 ) > K]) � �

Hence, any sequence of tests better than 'T is asymptotically equivalent to 'T withrespect to the probability measures P�0 for all �0 2 �.

The restriction to prior measures with compact support might be a bit restrictive. Inmost cases, we should be able to approximate prior measures with noncompact supportby ones with compact support.The admissibility of the sup test could be proved using a similar approach to Andrews

and Ploberger (1995).

16

4. Power of the test

The distribution of the TST (�;b�) itself is of considerable interest, too. We are interestedin functionals of TST (�;b�); so we have to consider the limiting behavior of TST (�;b�) asa process indexed by the parameter �. Again, we restrict ourselves to compact subsets ofB. Hence the appropriate limiting theory to consider is the convergence of distribution ofrandom elements with values in the space of continuous functions de�ned on a compactsubset of B.

Lemma 4.1. Assume Assumptions 1 to 3 hold. Consider Example 2.1. Under H0 andH1T (�T ), we have

TST (�;b�)� 1pT

TXt=1

��2;t (�; �0)

2� d (�)0 l

(1)t (�0)

�� 12E�0

��2;t (�; �0)

2� d (�)0 l

(1)t (�0)

�2!!

converges to zero uniformly on all compact sets. Moreover under H0, we have

TST (�;b�) D) G(�);

where D) denotes the convergence in distribution of a sequence of stochastic processes

and G(�) is a Gaussian process with mean -12E�0

���2;t(�;�0)

2� d (�)0 l

(1)t (�0)

�2�and co-

variance

Cov(G(�1); G(�2)) = E�0

���2;t (�1; �0)

2� d (�1)

0 l(1)t (�0)

���2;t (�2; �0)

2� d (�2)

0 l(1)t (�0)

��� k (�1; �2) :

UnderH1T (�T ) ; TST (�;b�) converges to a Gaussian process with mean k (�; �0)� 12k (�; �)

and variance k (�1; �2), where �0 is the true value of the parameter � under the alternative.

The last statement follows from Le Cam�s third lemma (see van der Vaart, 1998) andfrom the fact that the joint distribution of the TST (�;b�) and the logarithms of the densitiesof the local alternatives converges to a joint normal, and these two Gaussian randomvariables are correlated. With the help of this lemma, we can conclude that our test has

nontrivial power against local alternatives if E�0

���2;t(�;�0)

2� d (�)0 l

(1)t (�0)

�2�> 0.

It is, however, also possible that

E�0

��2;t (�; �0)

2� d (�)0 l

(1)t (�0)

�2!= 0; (4.1)

17

in which case TST (�;b�) will converge to zero and the test expTS will have no power.Some insight about this phenomenon can be gained by examining:

E�0

���2;t2� d0l

(1)t

�2�= E�0

���2;t2

�2�� 2d0E�0

�l(1)t

�2;t2

�+ d0 (I (�0))

�1 d

= E�0

���2;t2

�2�� E�0

�l(1)t

�2;t2

�0 �E�0

�l(1)t l

(1)0t

���1E�0

�l(1)t

�2;t2

�using (3.13). Hence (4.1) is satis�ed if and only if �2;t belongs to the linear span of

the components of l(1)t . Another way to see this is the following. Notice that becausePl(1)t

�b�� = 0; P �2;t(�;�)2

=P"t (�) where "t (�) is the projection

�2;t(�;�)2

on the space

orthogonal to l(1)t . Hence, TST (�;b�) can be rewritten asTST (�;b�) = 1p

T

X"t (�)�

1

2T

X"2t (�) :

If �2;t��; ��belongs to the space spanned by l(1)t ; then "t (�) = 0 and TST (�;b�) = 0.

Hence, if �2;t��; ��belongs to the space spanned by l(1)t for all �, the test expTS will have

no power. However, this is unlikely to happen except in very special cases. Let us constructsuch an example. Assume for a moment that � = 0 and all the other prerequisites ofAssumptions 1-3 and Example 2.1 are ful�lled. Then �2;t is a linear functional of the

second-order derivatives of the log-likelihood, namely h0�@2lt@�@�0 +

�@lt@�

� �@lt@�

�0�h. Then

(4.1) means that the second order derivatives can be written as a linear combination ofthe scores. This is a geometric condition, which has profound statistical implications. E.g.in Murray and Rice (1993, p. 16), it is used to characterize linear exponential families. Atypical example would be the normal distribution. We have two parameters, mean andvariance, and we can easily see that if we take h = (1; 0)0 (we allow the mean to switchbut not the variance), then (4.1) is ful�lled (for all � because here � is simply c2). Thiscorresponds to testing for independent mixture of two normals with di¤erent unknownmeans and same unknown variance. This same e¤ect was noticed in Gong and Mariano(1997) who remark that their test does not work in this situation. Note that on theother hand, our test has power against a Markov-switching model (� 6= 0) with unknownswitching mean and unknown constant variance. This case will be examined in details inSection 5.If (4.1) is ful�lled for all �, then it is impossible to construct a test with nontrivial power

against these speci�c local alternatives. The TST (�;b�) are consistent approximations ofthe log-density of one measure under the null (corresponding to �0 and to �0 � d=

pT ,

�, respectively). If the density between these two measures converges to 1, then anyreasonable distance like e.g. total variation converges to zero. So in this kind of situation

18

null and alternative are not distinct probability measures, which makes it impossible toconstruct consistent tests. Any test will have trivial local power for an alternative of orderT�1=4.Moreover, under our assumptions, this phenomenon is the exception rather than the

rule. The following proposition characterizes the set of alternatives against which our testdoes not have local power.

Proposition 4.2. Suppose Assumptions 1 to 3 hold. Consider Example 2.1. Assumefurthermore that for all t; s; h0

�@lt@�

� �@ls@�

�0h can not be represented as a linear combination

of components of�@lt@�

�: Then for each h, there exist at most �nitely many � so that (4.1)

is ful�lled.

Since in expTS, we integrate over a range of values for h and �; expTS will have localpower under the assumptions of Proposition 4.2.

5. Monte Carlo study

In this section, we investigate the power of supTS and expTS in four di¤erent models.

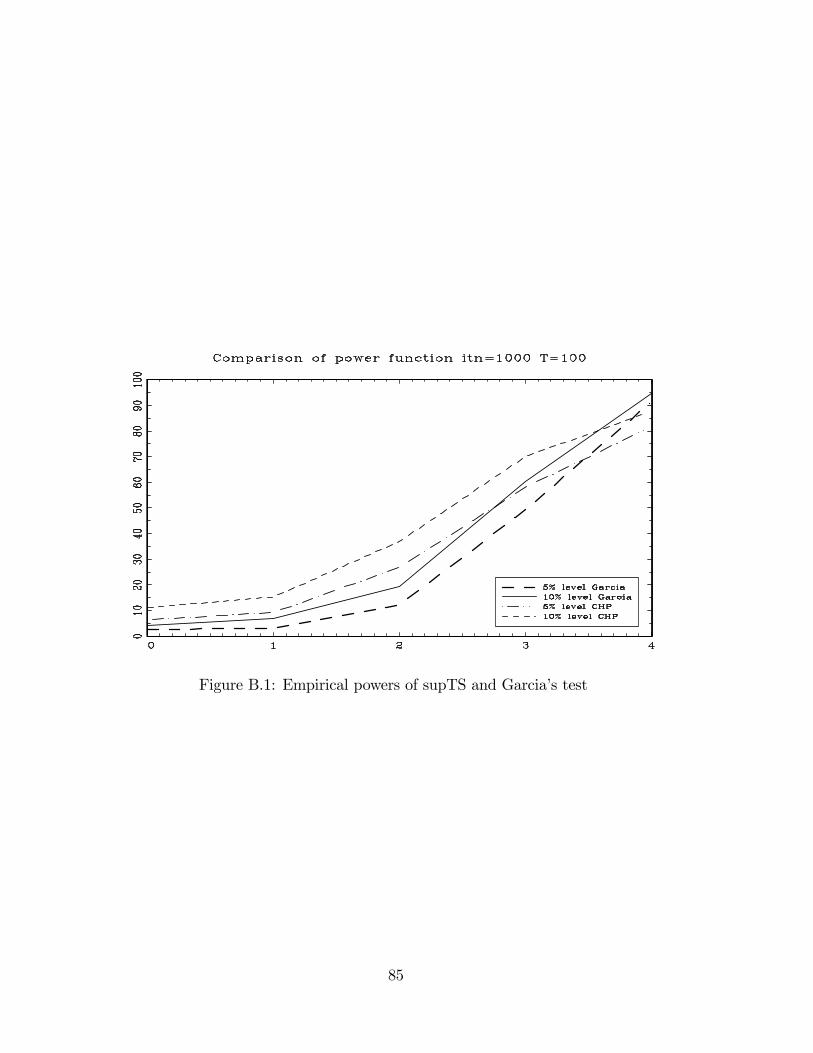

5.1. Comparison between supTS and Garcia�s test

In some simple cases where the asymptotic distribution of the test statistics is nuisanceparameter free, it is possible to tabulate the critical values of the test. Such an exampleis given by the simple model considered in Garcia (1998) with switching intercept and anuncorrelated and homoscedastic noise component,

yt = �0 + �1St + "t

where P (St = 1jSt�1 = 1) = p and P (St = �1jSt�1 = �1) = q, and "t � iidN (0; �2):Garcia�s (1998) test consists in calculating likelihood ratio test statistics (LR) for given

values of the nuisance parameters p and q and then maximizing LR with respect to p andq over an interval excluding the values close to 0 and 1.We want to compare the performance of supTS test with Garcia�s test. Since both tests

take the form of the supremum of LR, we expect them to be asymptotically equivalent.We compare the �nite sample power of the two tests.To look at the null asymptotic distribution of our test, we investigate the log likelihood

function as follows:

lt = � ln�p2��� ln (�

2)

2� (yt � �0)

2

2�2:

The �rst and second derivatives are as follows:

@lt@�0

=(yt � �0)

�2;

@lt@�2

= � 1

2�2+(yt � �0)

2

2�4;

19

@2lt@�20

= � 1

�2;

@2lt

@ (�2)2=

1

2�4� (yt � �0)

2

�6;

@2lt@�0@�2

= �(yt � �0)

�4:

So we have

l(1)t

���=

ut�2

u2t��22�4

!where ut = yt � �0 = yt � �Y .Notice that the variance �2 is unknown yet �xed, which implies that �t =

��1St 0

�0following our notation. Then we have E(�t�

0s) = c2

��t�s 00 0

�: As a consequence,

trace��l(2)t + l

(1)t l

(1)0t

�E (�t�

0t)�is equal to the (1; 1) element of

�l(2)t + l

(1)t l

(1)0t

�times c2,

namely,

trace��l(2)t + l

(1)t l

(1)0t

�E (�t�

0t)�= c2

�u2t � �2

��4

:

Similarly, we have

trace��l(1)t l(1)0s

�E (�t�

0s)�= c2�t�s

utus

�4:

Hence,1

2c2�2;t(�) =

1

2�4

"�u2t � �2

�+ 2

Xs<t

�(t�s)utus

#and

��T (�) =1

2pT �4

X"�u2t � �2

�+ 2

Xs<t

�(t�s)utus

#(5.1)

Moreover, recall that the MLE of �2 is simply

�2 =

P�yt � �Y

�2T

=

Pu2tT

:

It follows that

1pT

Xt

�u2t � �2

�=pT1

T

Xt

�u2t � �2

�=pT��2 � �2

�= 0:

Hence, ��T (�) simpli�es:

��T (�) =1pT �4

Xt

Xs<t

�(t�s)utus: (5.2)

20

The computation of ", the projection of 12��2;t(�) on l

(1)t

���consists of regressing 1

2��2;t(�)

on ut�2and u2t��2

2�4. The coe¢ cient of ut

�2goes to zero, and the coe¢ cient of u

2t��22�4

goes to 1.So asymptotically we have

"t '1

�4

Xs<t

�(t�s)utus:

It follows from Andrews and Ploberger (1996) that, under H0; ��T (�) de�ned in (5.2)

converges weakly to a linear combination of Gaussian processes

��T (�) =1pT �4

Xt

Xs<t

�(t�s)utus =)1Xi=0

�iZi

where Zi are iid standard Gaussian variables. Moreover, 1TP"2t converges to var

� 1Pi=0

�iZi

�=

11��2 :From the Continuous Mapping theorem, we obtain the asymptotic distribution of

supTS under H0 as follows:

supTS) supf�:�<�<��g

1

2

max

0;p1� �2

1Xi=0

�iZi

!!2: (5.3)

We simulate the asymptotic critical values based on (5.3) by truncating the series1Pi=0

�iZi at a large value TR. We pick TR = 50 as in Andrews and Ploberger (1996).

Asymptotic critical values are tabulated with 10; 000 replications and � selected over(�0:98; 0:98) and (�0:7; 0:7) respectively with increment 0:001. The accompanying em-pirical critical values are calculated for T = 100, with 1000 iterations and � drawn 100times from an equispaced grid on (�0:98; 0:98) and (�0:7; 0:7) respectively.

% of Dist. Emp c.v. Asym. c.v. Emp. c.v. Asym. c.v.interval [�0:98; 0:98] [�0:98; 0:98] [�0:7; 0:7] [�0:7; 0:7]99% 4:29 4:13 4:05 3:5795% 2:66 2:63 2:51 2:0790% 1:93 1:98 1:81 1:4480% 1:33 1:33 1:18 0:8770% 0:95 0:96 0:83 0:5350% 0:51 0:47 0:38 0:1610% 0:04 0 0:02 05% 0:01 0 0:01 01% 0 0 0 0Table 1: Empirical and asymptotic critical values of supTS

We can use Table 1 to assess which trimming produces a better approximation to thetheoretical distribution. It appears that empirical and asymptotic distributions are quite

21

close in the case of [�0:98; 0:98] interval. Note that the asymptotic critical values aremuch lower than those provided by Garcia and are also smaller than the cut-o¤ pointsgiven by a �2(1), the distribution obtained in the standard case.Now we can compare the power performance of supTS with Garcia�s test. The power

of our test is based on the asymptotic critical values tabulated in Table 1 with interval[�0:98; 0:98]. We draw � 100 times from an equispaced grid. Asymptotic critical valuesfor the interval [0:01; 0:99] from Table 1A in Garcia (1998) are used for his test. This isa fair comparison since � 2 [0:01; 0:99] corresponds to � 2 [�0:98; 0:98] in our case1. Wegenerate the data with p = q = 0:75, �0 = 0 and �1 = c= 4

pT : The sample size is 100 and

the number of iterations is 1000.The problem of local maxima may arise in Garcia�s test (see Hamilton (1989) and Gar-

cia (1998)). We follow the standard method and estimate the model using EM algorithmwith 12 sets of starting values and take the maximum over the values so obtained.We plot the power as a function of c in Figure B.1. The case c = 0 corresponds to the

size of the tests. Garcia�s test seems to su¤er from bigger size distortions than ours. Bothtests perform quite well, yet supTS is more powerful than Garcia�s in general. Only whenthe alternative is far away from the null (c = 4 here), his test performs slightly better.

5.2. Power of supTS and expTS in three di¤erent models

We now investigate the power of supTS and expTS in three di¤erent models. In general,the asymptotic distribution of our tests will not be nuisance parameter free. We rely onparametric bootstrap to compute the critical values.For supTS, we search the maximum over h and � in (2.11) by generating h uniformly

over the unit sphere and selecting � from an equispaced grid over (�0:7; 0:7) 2: The numberof values for h is 30 and for � is 403. We obtain the empirical critical values with 1000iterations and sample size equal to 200. Then, we compute the size-corrected power withthe same number of iterations and same sample sizes.The evaluation of the expTS statistic is more involved since we need to pick some

prior distributions for all nuisance parameters in � = (c2; h0; �)0. The most commonly usedpriors are uniform distributions. However since c2 is not bounded from above, a uniformprior is not appropriate. We de�ne G = c2 and take an exponential prior for G, which hasthe pdf of �e��G. The reason for picking an exponential distribution is that we obtain ananalytic form when taking the integral of TST (�) with respect to the distribution of G asfollows:Z 1

0

exp (TST (�)) �e��GdG =

p2�

�p"�0"�

exp

"(��T � �)2

2"�0"�

#�

���T � �p"�0"�

�� G (h; �)

1We pick this interval since in both papers it is found that it produces asymptotic critical values closerto empirical critical values.

2Since � = p+ q � 1; p; q 2 (0:15; 0:85) correspond to the bound of (�0:7; 0:7) for �:3We �nd these numbers are satisfactory for the cases considered here. An increase in the number of

draws does not have a signi�cant impact on the outcome.

22

where � (�) is the standard normal cdf. In practice, the choice of � could be very �exiblethough we must use the same value when generating the critical values and calculatingthe actual test statistic. We pick � = 1 both under the null and the alternative in thesimulations that follow. The other two nuisance parameters (h0; �)0 are selected the sameway as in supTS. Then, expTS is obtained as the average of G over the grid sets of hand �.Linear model with switching intercept, regressor coe¢ cient, and variance:

yt = x0t

�� +

C�t4pT

�+ (!0 + !1�t) "t

"t � iidN (0; 1)

C = (c1; c2)0 : xt = (1; x1t)

0 with x1t �iidN (3; 400): �t is a two-State Markov chain thattakes the values 1 and �1 with unknown transition probabilities P

��t = 1j�t�1 = 1

�= p

and P��t = �1j�t�1 = �1

�= q: In the data generating process (DGP), p = q = 0:75;

� = (1; 1)0, !0 = 1; and !1 = 0:In the simulations, we set c1 = c2 = c and investigate the size-corrected power as a

function of c.

c supTS expTS5% 10% 5% 10%

0 4:5 9:1 3:7 8:40:03 6 12:6 7:3 13:10:06 16:8 27:6 23:8 34:60:09 47:8 62:1 62:6 74:20:12 85:1 91:5 93:3 96:20:15 97:8 99:3 99:3 99:9

Table 2: Size-corrected power of supTS and expTS for a linear model

ARCH(1) model:

yt = �t"t

�2t = (! +c1�t4pT) + (a+

c2�t4pT)y2t�1

"t � iidN (0; 1)

�t is a two-State Markov chain that takes the values 1 and �1 with unknown transitionprobabilities P

��t = 1j�t�1 = 1

�= p and P

��t = �1j�t�1 = �1

�= q: In the DGP, p =

q = 0:75 and ! = a = 1=4. We set c1 = c2 = c and get the size-corrected power forvarious values of c.

23

c supTS expTS5% 10% 5% 10%

0 3:9 9:9 5:7 11:30:15 5:9 12:6 5:9 11:40:30 13:5 27:8 18:9 29:10:45 31:7 50 42 54:70:60 68:8 83:1 80 87:40:75 96:8 99:2 98:6 99:1

Table 3: Size-corrected power of supTS and expTS for an ARCH model

IGARCH(1,1):The model is as follows:

yt = �t"t

�2t = (! +c1�t4pT) + (a+

c2�t4pT)�2t�1 + (b+

c3�t4pT)y2t�1

"t � iidN (0; 1)

Here, we let �t take the values 0 and �1 with unknown transition probabilities P (�t =0j�t�1 = 0) = p and P (�t = �1j�t�1 = �1) = q: In the DGP p = q = 0:75 and! = a = b = 1=2: Note that under H0; the model is a IGARCH. c1; c2; and c3 are takento be equal to c. The size-corrected power is given below.

c supTS expTS5% 10% 5% 10%

0 4:9 10:3 4:2 11:10:3 7 14:8 6:6 12:30:6 11:8 20:7 11:4 21:70:9 29:5 42:3 27:4 381:2 49:6 64:6 51:1 61:81:5 87:4 93:9 86:5 90:3

Table 4: Size-corrected power of supTS and expTS for a GARCH model

Remarks.1. Our tests perform very satisfactorily in all cases. As the alternative is more distant

from the null, the power increases monotonically and goes very fast to 100.2. In linear and ARCH cases, expTS performs slightly better than supTS: The pattern

is less clear in IGARCH case.3. Since both supTS and expTS perform very well, we use supTS in the empirical

application because selecting the prior distribution is somewhat arbitrary.

6. Asymmetry in stock price dynamics

As noted by Neftçi (1984) and Hamilton (2004), the major macroeconomic variablesdisplay an asymmetric behavior over various phases of the business cycle. In this section,

24

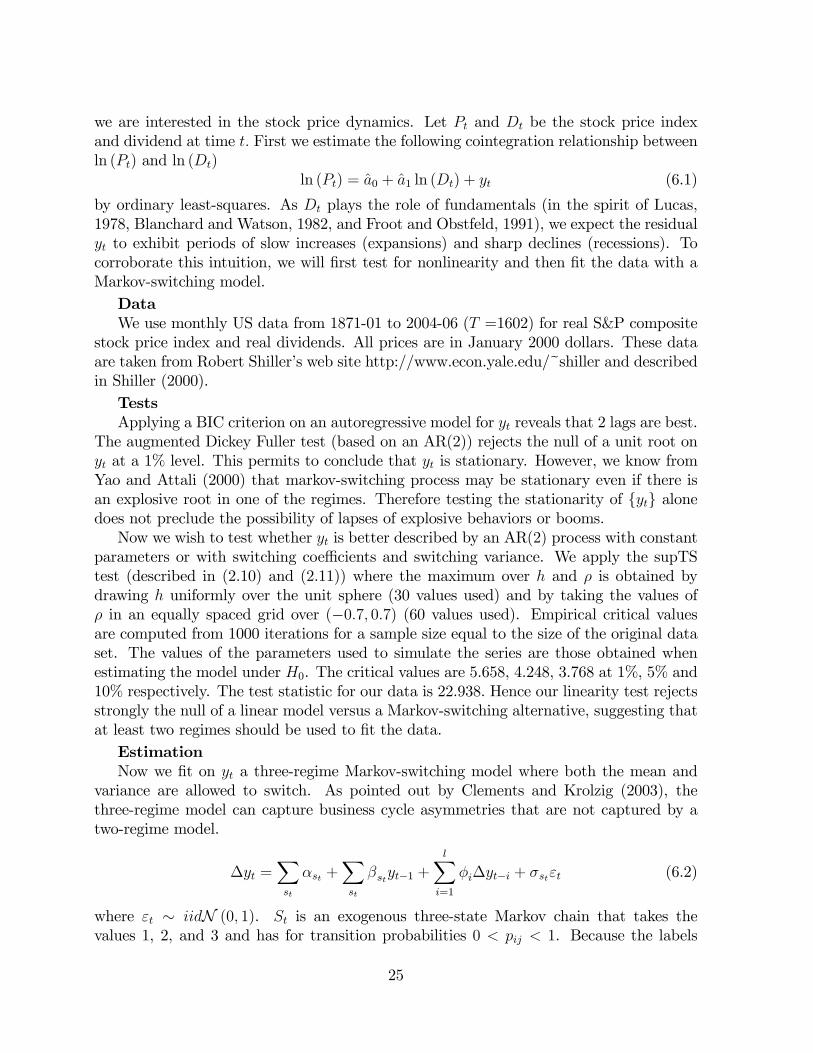

we are interested in the stock price dynamics. Let Pt and Dt be the stock price indexand dividend at time t: First we estimate the following cointegration relationship betweenln (Pt) and ln (Dt)

ln (Pt) = a0 + a1 ln (Dt) + yt (6.1)

by ordinary least-squares. As Dt plays the role of fundamentals (in the spirit of Lucas,1978, Blanchard and Watson, 1982, and Froot and Obstfeld, 1991), we expect the residualyt to exhibit periods of slow increases (expansions) and sharp declines (recessions). Tocorroborate this intuition, we will �rst test for nonlinearity and then �t the data with aMarkov-switching model.DataWe use monthly US data from 1871-01 to 2004-06 (T =1602) for real S&P composite

stock price index and real dividends. All prices are in January 2000 dollars. These dataare taken from Robert Shiller�s web site http://www.econ.yale.edu/~shiller and describedin Shiller (2000).TestsApplying a BIC criterion on an autoregressive model for yt reveals that 2 lags are best.

The augmented Dickey Fuller test (based on an AR(2)) rejects the null of a unit root onyt at a 1% level. This permits to conclude that yt is stationary. However, we know fromYao and Attali (2000) that markov-switching process may be stationary even if there isan explosive root in one of the regimes. Therefore testing the stationarity of fytg alonedoes not preclude the possibility of lapses of explosive behaviors or booms.Now we wish to test whether yt is better described by an AR(2) process with constant

parameters or with switching coe¢ cients and switching variance. We apply the supTStest (described in (2.10) and (2.11)) where the maximum over h and � is obtained bydrawing h uniformly over the unit sphere (30 values used) and by taking the values of� in an equally spaced grid over (�0:7; 0:7) (60 values used). Empirical critical valuesare computed from 1000 iterations for a sample size equal to the size of the original dataset. The values of the parameters used to simulate the series are those obtained whenestimating the model under H0. The critical values are 5.658, 4.248, 3.768 at 1%, 5% and10% respectively. The test statistic for our data is 22.938. Hence our linearity test rejectsstrongly the null of a linear model versus a Markov-switching alternative, suggesting thatat least two regimes should be used to �t the data.EstimationNow we �t on yt a three-regime Markov-switching model where both the mean and

variance are allowed to switch. As pointed out by Clements and Krolzig (2003), thethree-regime model can capture business cycle asymmetries that are not captured by atwo-regime model.

�yt =Xst

�st +Xst

�styt�1 +lXi=1

�i�yt�i + �st"t (6.2)

where "t � iidN (0; 1). St is an exogenous three-state Markov chain that takes thevalues 1, 2, and 3 and has for transition probabilities 0 < pij < 1. Because the labels

25

of the regimes are interchangeable, we set �1 � �2 � �3: The parameter of interest is� = (�1; �2; �3; �1; �2; �3; �i : i = 1; ::; l; �

21; �

22; �

23; pij : i; j = 1; 2; 3)

0: The coe¢ cients �i

are set constant across regimes because preliminary estimations showed that they did notchange values. The following proposition justi�es our two-step approach.

Proposition 6.1. Assume ln (Dt) is strictly exogenous for "t, in the sense that "t isuncorrelated with ln (D1) ; ln (D2) ; ::; ln (DT ). The MLE estimates of (a0; a1; �) coincidewith the estimators obtained from a two-step procedure consisting in estimating (a0; a1)

0

by OLS in (6.1) �rst and then applying MLE on (6.2). Moreover the resulting � areindependent of (a0; a1) implying that the �rst step does not a¤ect the second step.

We estimate model (6.2) by maximum likelihood using the EM algorithm described inHamilton (1989) and BFGS for optimization. We use 9 sets of starting values and selectthe one corresponding to the largest value of the likelihood. The results are given below.

estimate standard error�1 0:00241 0:00137�2 �0:00283 0:00321�3 �0:0247 0:0156�1 �0:00842 0:00635�2 �0:0120 0:00814�3 �0:0767 0:0450� 0:345 0:0253�21 6:51e� 4 2:54e� 5�22 0:00223 2:68e� 4�23 0:010 0:00299P11 0:940 0:0210P12 0:0598 0:0210P21 0:0969 0:0406P22 0:899 0:0409P31 2:68e� 13 1:69e� 11P32 0:0281 0:0330

The standard errors are heteroskedasticity-robust standard errors. The associated sta-tionary distribution is Pr(St = 1) = 0:586, Pr(St = 2) = 0:361, and Pr(St = 3) = 0:0531:Regime 1 (St = 1) corresponds to a unit root process with low volatility and a positive

drift. 58.6% of the data lies in this regime. Regime 2 (St = 2) corresponds to a unitroot too, but with higher volatility and negative drift. 36.1% of the data lies in regime2. Regime 3 (St = 3) corresponds to a strong mean reverting process with even largervolatility. One possible interpretation is the following. Regime 1 corresponds to thenormal periods with slow increases. And in the normal periods, the investors have moreor less homogeneous beliefs so the volatility is very low. Regime 2 captures periods ofmoderate decreases. In these periods, investors have more heterogeneous beliefs about

26

the market behavior, which leads to a larger volatility compared to Regime 1. Regime3 represents the crisis regime. It corresponds to sharp declines accompanied by a largevolatility.Through �ltering, we compute the probabilities to be in regime i conditional on the

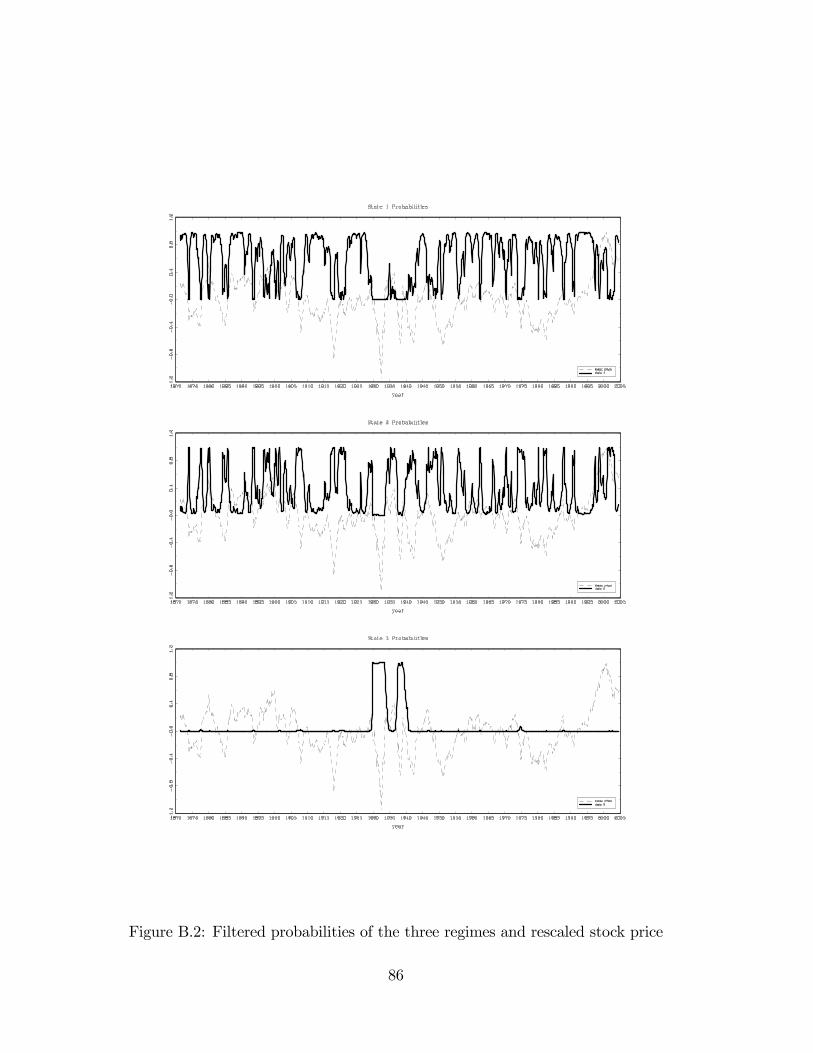

data: Pr(St = ijy1; :::; yT ): When the probability is greater than 0.5, it is considered thatthe process at time t is in regime i. Regime 3 corresponds to the following two periods:October 1929 to November 1933 and April 1937 to November 1939. Regime 3 identi�es thebig crash in October 1929 and another sharp decline in the stock market price experiencedin 1937. Similarly we isolate the dates where Regime 2 dominates. Starting in 1950, thesedates are 1950 (6-12), 1951 (1-3), 1955 (6-12), 1956 (1-9), 1957 (8-10), 1962 (3-11), 1966(3-9), 1969 (12), 1970 (1-8), 1971 (11-12), October 1973 to January 1976, 1980 (1-5),1981 (7-12), 1982 (1-10), 1984 (8), 1987 (7-12), 1988 (1,2), 1990 (7-12), 1991 (1-3), 1997(4-6), 1998 (6-12), 1999 (1-11), and January 2001 to May 2003. Regime 2 correspondsroughly to the bear market and captures most of the droughts in the US stock marketcycles reported by Pagan and Sossounov (2003) including the crash of October 1987 andthe information technology crisis of 2001-2002.In Figure B.2, we plot the graphs of the probabilities of the three regimes. In the

background of each plot, there is the graph of the log stock price centered by its mean overthe full data set and rescaled so that the maximum value equals 1. The process yt spendsmost of the time in the unit-root regime 1. It follows an asymmetric pattern exhibitingslow increases and fast decreases that are well captured by the Markov-switching model.

7. Conclusion

This paper presents the �rst optimal test against Markov switching alternatives. Ourtest applies to a wide range of models that are popular in macroeconomics and �nance.It is simple to implement as it requires only the estimation of the parameters under thenull hypothesis of constant parameters. Hence, it should be used as a �rst step beforeestimating a complicated nonlinear model.Our test relies on a prior distribution for the switching coe¢ cients �t and, in this

sense, has a Bayesian interpretation. Bayesian inference for Markov-switching models isan active research area, see e.g. Chib (1996), Kim and Nelson (1999), Frühwirth-Schnatter(2001).

27

References

[1] Andrews, D.W.K, (1993). �Tests for Parameter Instability and Structural ChangePoint�, Econometrica, 61, 821-856.

[2] Andrews, D. (1994) �Empirical process methods in econometrics�, in Handbook ofEconometrics, Vol. IV, ed. by R.F. Engle and D.L. McFadden.

[3] Andrews, D. (1999) �Estimation When a Parameter Is on the Boundary�, Econo-metrica, 67, 1341-1383.

[4] Andrews, D. (2001) �Testing When a Parameter Is on the Boundary of the Main-tained Hypothesis�, Econometrica, 69, 683-734.

[5] Andrews, D.W.K., Ploberger, W., (1994). �Optimal Tests When a Nuisance Para-meter Is Present Only under the Alternative�, Econometrica, 62, 1383-1414.

[6] Andrews, D.W.K., Ploberger, W. (1995). �Admissibility of the likelihood ratio testwhen a nuisance parameter is present only under the alternative�, The Annals ofStatistics 23, 1609-1629.

[7] Andrews, D. and W. Ploberger (1996) �Testing for Serial Correlation Against anARMA(1,1) Process�, Journal of the American Statistical Association, Vol. 91, 1331-1342.

[8] Bartle, R. G. (1966) The elements of integration, Wiley and Sons, NY.

[9] Bartlett, M. S. (1953a) �Approximate con�dence intervals�, Biometrika, 40, 12-19.

[10] Bartlett, M. S. (1953b) �Approximate con�dence intervals, II. More than one para-meter�, Biometrika, 40, 306-317.

[11] Blanchard, O. and M.Watson (1982) �Bubbles, Rational Expectations, and FinancialMarkets�, in Crises in the Economic and Financial Structure, ed. by P. Wachtel,LexingtonBooks, Lexington, MA.

[12] Chesher, A. (1984) �Testing for Neglected Heterogeneity�, Econometrica, 52, 865-872.

[13] Chib, S. (1996) �Calculating posterior distributions and modal estimates in Markovmixture models�, Journal of Econometrics, 75, 79-97.

[14] Chirinko, R. and H. Schaller (2001) �Business Fixed Investment and �Bubbles�: TheJapanese Case�, American Economic Review, 91, 663-680.

[15] Cho, J.S. and H. White (2007) �Testing for Regime Switching�, Econometrica, 75,1671-1720.

28

[16] Clements, M. and H.-M. Krolzig (2003) �Business Cycle Asymmetries: Characteriza-tion and Testing Based on Markov-Switching Autoregressions�, Journal of Businessand Economic Statistics, 21, 196-211.

[17] Cox D.R. and H. D. Miller (1965) The Theory of Stochastic Processes, Methuen &Co. Ltd, London, UK.

[18] Davidson, R. and J. MacKinnon (1991) �Une nouvelle forme du test de la matriced�information�, Annales d�Economie et de Statistique, N. 20/21, 171-192.

[19] Davidson, R. and J. MacKinnon (2004) Econometric Theory and Methods, OxfordUniversity Press, New York.

[20] Davies, R.B. (1977) �Hypothesis testing when a nuisance parameter is present onlyunder the alternative�Biometrika, 64, 247-254.

[21] Davies, R.B. (1987) �Hypothesis testing when a nuisance parameter is present onlyunder the alternative�Biometrika, 74, 1, 33-43.

[22] Doukhan, P. (1994) Mixing: Properties and Example, Springer-Verlag, New York.

[23] Dueker, M.J. (1997) �Markov Switching in GARCH Processes and Mean-RevertingStock Market Volatility�, Journal of Business & Economic Statistics, 15/1, 26-34.

[24] Froot, K. and M. Obstfeld (1991) �Intrinsic Bubbles: The Case of Stock Prices�,American Economic Review, 81, 1189-1213.

[25] Frühwirth-Schnatter, S. (2001) �Markov Chain Monte Carlo Estimation of Classicaland Dynamic Switching and Mixture Models�, Journal of the American StatisticalAssociation, 96, 194-209.

[26] Garcia, R.(1998). �Asymptotic Null Distribution of the Likelihood Ratio Test inMarkov Switching Models�, International Economic Review, 39, 763-788.

[27] Gong, F. and Mariano, R.S. (1997). �Testing Under Non-Standard Conditions inFrequency Domain: With Applications to Markov Regime Switching Models of Ex-change Rates and the Federal Funds Rate�, Federal Reserve Bank of New York Sta¤Reports, No. 23.

[28] Gray, S. (1996), �Modeling the Conditional Distribution of Interest Rates as aRegime-Switching Process,�Journal of Financial Economics, 42, 27-62.

[29] Haas, M., S. Mittnik, and M. Paolella (2004), �A New Approach to Markov-SwitchingGARCH Models,�Journal of Financial Econometrics, 2, 493-530.

[30] Hamilton, J.D. 1989. �A new Approach to the Economic Analysis of NonstationaryTime Series and the Business Cycle�, Econometrica 57, 357-384.

29

[31] Hamilton, J. D., and R. Susmel (1994), �Autoregressive Conditional Heteroskedas-ticity and Changes in Regime�, Journal of Econometrics 64, 307-333.

[32] Hamilton, J.D. (2005) �What�s Real About the Business Cycle?�, Federal ReserveBank of St Louis Review, 87, 435-452.

[33] Hansen, B. (1992) �The Likelihood Ratio Test Under Non-Standard Conditions:Testing the Markov Switching Model of GNP�, Journal of Applied Econometrics,7, S61-S82.

[34] Hu, L. (2008) �Optimal Test for Stochastic Unit Root with Markov Switching�,mimeo, Leeds University.

[35] Hu, L. and Y. Shin (2008) �Optimal Testing for Markov Switching GARCHModels�,Studies in Nonlinear Dynamics and Econometrics, 12, Issue 3.

[36] Kahn, J. and R. Rich (2007) �Tracking the New Economy: Using Growth Theory toDetect Changes in Trend Productivity�, forthcoming in Journal of Monetary Eco-nomics.

[37] Kim, C.-J. and C. Nelson (1999) State-Space Models with Regime Switching, MITPress.

[38] Kim, C.-J. and C. Nelson (2001) �A Bayesian Approach to Testing for Markov Switch-ing in Univariate and Dynamic Factor Models�, International Economic Review, 42,989-1013.

[39] Lang, S. (1993) Real and Functional Analysis, Springer-Verlag, New York.

[40] Lee, L-F. and A. Chesher (1984) �Speci�cation Testing when Score Test StatisticsAre Identically Zero�, Journal of Econometrics, 31, 121-149.

[41] Lucas, R. (1978) �Asset Prices in an Exchange Economy�, Econometrica, 66, 429-445.

[42] Morley, J. and J. Piger (2006) �The importance of Nonlinearity in ReproducingBusiness Cycle Features�, in Nonlinear Time Series Analysis of Business Cycles,edited by C. Milas, P. Rothman, and D. van Dijk. Elsevier, Amsterdam.

[43] Murray, M.K and J.W. Rice (1993) Di¤erential Geometry and Statistics, Chapman-Hall, London.

[44] Neftçi, S. (1984) �Are Economic Time Series Asymmetric over the Business Cycle?�,Journal of Political Economy, 92, 307-328.

[45] Pagan, A. and K. Sossounov (2003) �A simple framework for analysing bull and bearmarkets�, Journal of Applied Econometrics, 18, 23-46.

30

[46] Rotnitzky, A., D. Cox, M. Bottai, and J. Robins (2000) �Likelihood-based inferencewith singular information matrix�, Bernoulli, 62, 243-284.

[47] Shiller, R. (2000) Irrational Exuberance, Princeton University Press, Princeton, NewJersey.

[48] Strasser, H. (1995) Mathematical Theory of Statistics. Springer Verlag, New York.

[49] van der Vaart, A.W. (1998) Asymptotic Statistics, Cambridge University Press, Cam-bridge, UK.

[50] Warne, A. and A. Vredin (2006) �Unemployment and In�ation Regimes�, Studies inNonlinear Dynamics & Econometrics, Vol. 10, Issue 2.

[51] White, H. (1982) �Maximum Likelihood Estimation of Misspeci�ed Models�, Econo-metrica, 50, 1-25.

[52] Yao, J.-F. and J.-G. Attali (2000) �On stability of nonlinear AR processes withMarkov switching�, Advances in Applied Probability, 32, 394-407.

31

APPENDIX

A. Notations

A.1. Multilinear Forms

Central to the proofs in this paper are Taylor series expansions to the fourth order. We willhave to organize and manipulate expressions involving multivariate derivatives of higherorders. We therefore will be careful with our notation. Clearly it would be possible to usepartial derivatives, but then our expressions will get really complicated. Hence we willadopt some elements from multilinear algebra, which will facilitate our computations.Key to our analysis is the concept of a multilinear form. Consider vector spaces V , F .

Then a multilinear form (or - simply - �form�) of order p from V into F is a mappingM from V � :: � V (where we take the product p times) to F which is linear in each ofthe arguments. So

�M(x(1); x(2); :::; x(i)1 ; :::; x

(p)) + �M(x(1); x(2); :::; x(i)2 ; ::::; x

(p)) (A.1)

= M(x(1); x(2); :::; �x(i)1 + �x

(i)2 ; :::; x

(p)): (A.2)

The �rst important concept we need to discuss is the de�nition of a derivative. Es-sentially, we will follow the di¤erential calculus outlined in Lang (1993), p. 331 ¤. Let fbe a function de�ned on an open set O of the �nite-dimensional vector space V into the�nite dimensional space F . Then f is said to be di¤erentiable if for all x 2 O there existsa linear mapping Df = Df(x) from V to F so that

limr!0

supkhk=r

kf(x+ h)� f(x)�Df(x)(h)k =r ! 0: (A.3)

The above expression should not be misinterpreted. Df(x) attaches to each x 2 O alinear mapping, so Df(x)(h) is for each h 2 V an element of F . Df(x) is called aFrechet-derivative. It is in a way a formalization of the well known �di¤erential� inelementary calculus. So Df(x) is a linear mapping between V and F . It is an elementarytask to show that the space of all linear mappings between V and F , denoted by L(V; F )is a �nite dimensional vector space again. Hence we can consider the mapping

x! Df(x);

which maps O into L(V; F ), so we may use the concept of Frechet-di¤erentiability againand di¤erentiate Df . We then get the second derivative D2f(x). This second derivativeat a point is a linear mapping from V to L(V; F ) (an element from L(V; L(V; F ))). Thatmeans that, for each h 2 V; D2f(x)(h) is an element of L(V; F ), so for k 2 V D2f(x)(h)(k)is an element of F . Moreover, we can easily see that - by construction - the expressionD2f(x)(h)(k) is linear in h and k. Hence D2f(x) maps each pair (h; k) into F and islinear in each of the arguments, so we can think of D2f(x) as a bilinear form from V �Vinto F .

32

It is easily seen that, in case f has enough �derivatives�, we can iterate this processand de�ne the n-th derivative Dnf as derivative of Dn�1f;

Dnf = D(Dn�1f):

Again we can interpret Dnf as an element of L(V; L(V; :::L(V; F )))) or - again - as amultilinear mapping from V �V �V �V::�V into F . This means that Dnf (x) attachesto each n-tupel (x1; ::::; xn) of elements of V an element of F , in such a way that themapping is linear in each of its arguments.Most importantly, we have again a Taylor formula

f(x+ h) = f(x) +Df(x)(h) +1

2D2f(x)(h; h) + ::::+

1

n!Dnf(x)(h; ::h) +Rn

with

Rn =1

n!

Z 1

0

(1� t)nDn+1f(x+ th)(h; :::; h)dt; (A.4)

if f is at least n+ 1 times continuously di¤erentiable.Furthermore it is relatively easy to verify that f being n times continuously di¤eren-

tiableDnf is symmetric

i.e.Dnf(x)(h1; :::; hn) = Dnf(x)(h�(1); :::; h�(n)) (A.5)

for every permutation �.Moreover, let us consider for �xed x; h the function g(t) = f(x+ ht) for t in a neigh-

borhood of 0, and let g(n) be the n-th derivative of g. Then

g(n)(0) = Dnf(x)(h; :::; h): (A.6)

It is now an elementary, but tedious, exercise to show that due to the symmetry (A.5)the multilinear form Dnf(x) is uniquely de�ned by its values Dnf(x)(h; :::; h). (As anexample, it might be instructive to consider the case of a scalar bilinear form B: We caneasily see that

B(h; k) +B(k; h) =1

4(B(h+ k; h+ k)�B((h� k; h� k)):

Symmetry implies that the left hand side of the above equation equals 2B(h; k) =2B(k; h):)This result allows us to �translate�all the well-known results from elementary calculus

to our formalism. Clearly the derivative is linear, we have a product rule - if f and g arescalar functions, then D(fg) = f �Dg + (Df) � g, and more importantly we have a chainrule. If we compose functions f; g; we have

D(f � g) = Df(Dg):

33

The algebra of multilinear forms is often treated as a special case of tensor algebra.Although this branch of mathematics is well developed, it is rarely used in econometrics.Furthermore, many of the advanced concepts are of no use to us. Hence we will stay withmultilinear forms, and only de�ne the operations and concepts we need. The experts willsee that they are special cases of tensor algebra. Our key simpli�cation will be that we�x our reference space and the coordinate system once and for all - we simply forbid theuse of other coordinate systems and spaces.We are in a rather advantageous position:

� We are mostly interested in manipulating the derivatives of a scalar function, namelythe logarithm of the likelihood function.

� Working independently of a coordinate system is not a priority for us (contrary totheoretical physics, where gauge invariance plays a major role).

� We are analyzing derivatives, so most of our multilinear forms are symmetric.

Assume that our reference, �nite dimensional vector space V is k�dimensional andthat b1; ::bk is a basis for this space. Although the basis is arbitrary, we will from nowon assume this basis to be �xed. It is essential for our approach that we �x theunderlying vector space and the basis, since all of our de�nitions relate in one wayor another to our chosen basis. It should be noted that we follow this approach not out ofnecessity - coordinate independent de�nitions of tensors are commonplace in di¤erentialgeometry and mathematical physics, but purely out of convenience. E.g. we do not needto distinguish between co- and contravariant tensors - so we do not have to distinguishbetween �upper�and �lower�indices.With the help of our basis, any vector x can uniquely be written as

x =kXi=1

xibi:

We will now mainly work with scalar multilinear forms (i.e. the values of the form arereal numbers). Hence we will assume - except when explicitly stated otherwise - that amultilinear form to be scalar. Let nowM be such a multilinear form Then, using linearity,we have

M(x(1); x(2); :::; x(p)) =X

M(bi1 ; :::; bip)x(1)i1x(2)i2::x

(p)ip; (A.7)

where the sum symbol corresponds to p sums extending over all values of i1; :::; ip between1 and k. So we can easily see that there is a one-to-one correspondence between the kp

numbers M(bi1 ; :::; bip) and the multilinear forms. For each set of numbers we de�ne auniquely determined multilinear form, and for each multilinear form we can �nd coe¢ -cients. Hence, having �xed the coordinate system, we can identify the multilinear formM with its coordinates M(bi1 ; :::; bip). Multilinear forms (with the usual operations) oforder p form a �nite dimensional vector space. The only di¤erence to a �usual�vector

34

space is the enumeration of the coordinates. We do not index them by the numbers of1; :::; K, but our index set consists of the p-tuples (1; :::; 1) ; (2; 1; :::),...(k; k; ::; k)This way we can work with multilinear forms and related mathematical objects without

having to discuss tensor algebra. We can easily see that bilinear forms (forms of ordertwo) are k � k�matrices.

1. We can easily see that multilinear forms form a vector space, and the mappingattaching each multilinear form its coordinates is an isomorphism. Hence we donot need to distinguish between multilinear forms and kp numbers indexed by amulti-index (i1; :::; ip):

2. Let us call a multilinear form C de�ned by coordinates�ci1;:::;ip

�symmetrical if

and only for all (i1; :::; ip) and all permutations � of numbers between 1 and k

ci1;:::;ip = c�(i1);:::;�(ip):

We can easily see that this property is equivalent to our de�nition above, (A.5)).For a form C de�ned by coordinates

�ci1;:::;ip

�de�ne its symmetrization C(S) by�

C(S)�i1;:::;ip

=1

k!

Xall permutation � of f1;::;kg

c�(i1);:::;�(ip):

Then C(S) is symmetrical. Moreover, for all h 2 V

C(h; :::h) = C(S)(h; :::; h); (A.8)

and, for any form C; C(S) is the only symmetrical form with the property (A.8).

3. Another special case of multilinear forms are our derivatives of scalar functionsde�ned on open subsets of our space V . We can easily see that the coordinates Dnfcan be calculated in the following way. De�ne the function g by

g((x1; :::; xp) = f(X

xibi); (A.9)