opportunities and obstacles for digitalisation in …...opportunities and obstacles for...

TRANSCRIPT

Opportunities and obstacles for digitalisation in European regulation

Dieter Pscheidl

Head of European Affairs

Vienna Insurance Group AG

International Insurance Forum 2017

Insurance in the DIGITAL World

Vienna, 14 November 2017

2

VIG = market experience from 14 EU Member States

Different levels of customer demand for digitalisation

Opportunities

Obstacles

Agenda

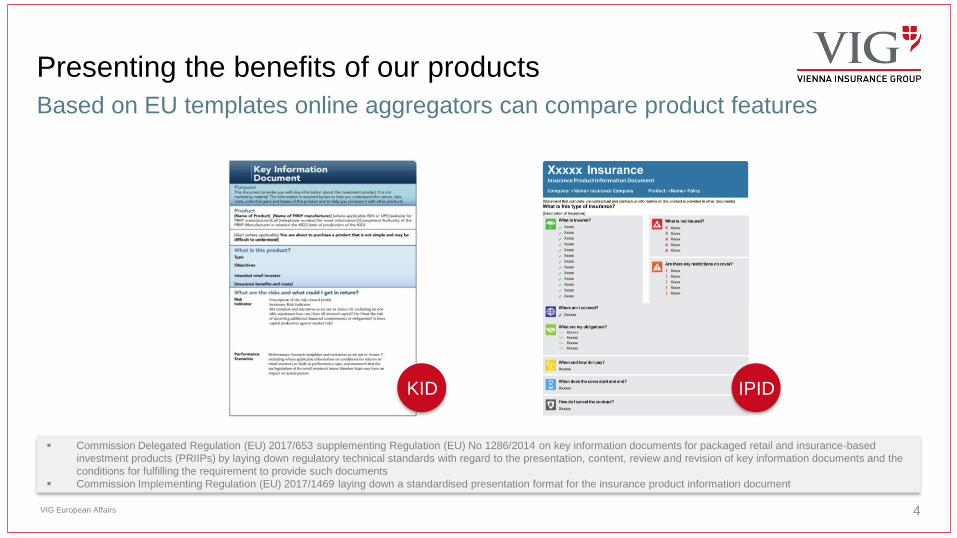

Presenting the benefits of our products

Based on EU templates online aggregators can compare product features

4VIG European Affairs

KID IPID

Commission Delegated Regulation (EU) 2017/653 supplementing Regulation (EU) No 1286/2014 on key information documents for packaged retail and insurance-based

investment products (PRIIPs) by laying down regulatory technical standards with regard to the presentation, content, review and revision of key information documents and the

conditions for fulfilling the requirement to provide such documents

Commission Implementing Regulation (EU) 2017/1469 laying down a standardised presentation format for the insurance product information document

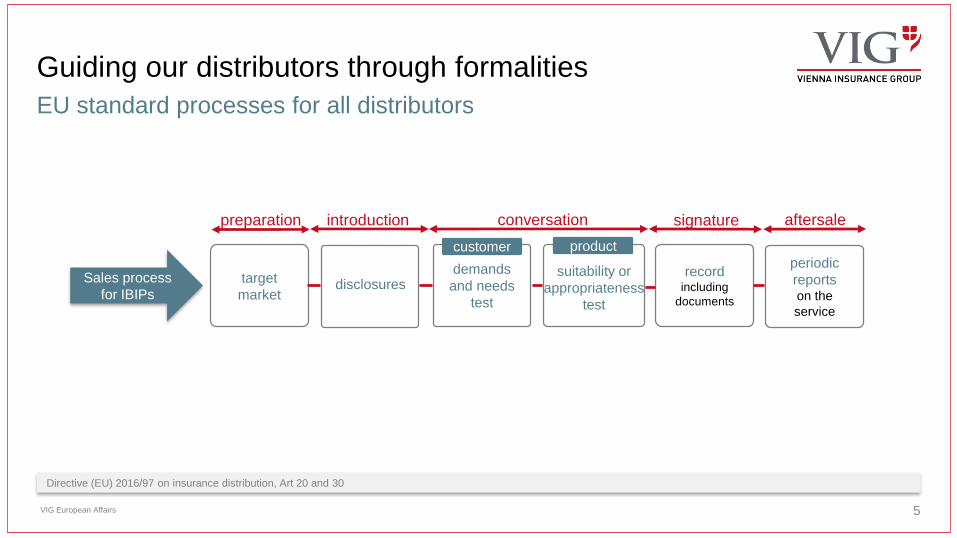

EU standard processes for all distributors

5

Guiding our distributors through formalities

VIG European Affairs

Directive (EU) 2016/97 on insurance distribution, Art 20 and 30

introduction conversation signature aftersalepreparation

suitability or

appropriateness

test

periodic

reportson the

service

demands

and needs

test

recordincluding

documents

disclosurestarget

market

customer product

Sales process

for IBIPs

Legally non-formalised conversation with the customer

may be supported by digital tools

6

Assessing the demands and needs of our customers

pension

housing

travel

mobility

work

sports

Directive (EU) 2016/97 on insurance distribution, Art 20

VIG European Affairs

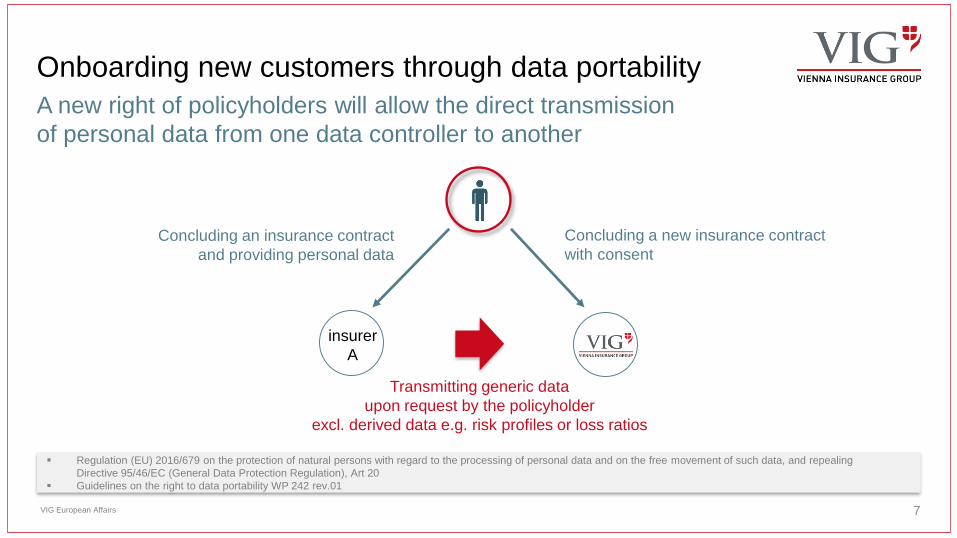

Onboarding new customers through data portability

A new right of policyholders will allow the direct transmission

of personal data from one data controller to another

7

Regulation (EU) 2016/679 on the protection of natural persons with regard to the processing of personal data and on the free movement of such data, and repealing

Directive 95/46/EC (General Data Protection Regulation), Art 20

Guidelines on the right to data portability WP 242 rev.01

VIG European Affairs

insurer

A

Transmitting generic data

upon request by the policyholder

excl. derived data e.g. risk profiles or loss ratios

Concluding an insurance contract

and providing personal data

Concluding a new insurance contract

with consent

8

Regulation (EU) 2016/679 on the protection of natural persons with regard to the processing of personal data and on the free movement of such data, and repealing

Directive 95/46/EC (General Data Protection Regulation), Art 22

Guidelines on profiling by Art 29 WP (tbd)

VIG European Affairs

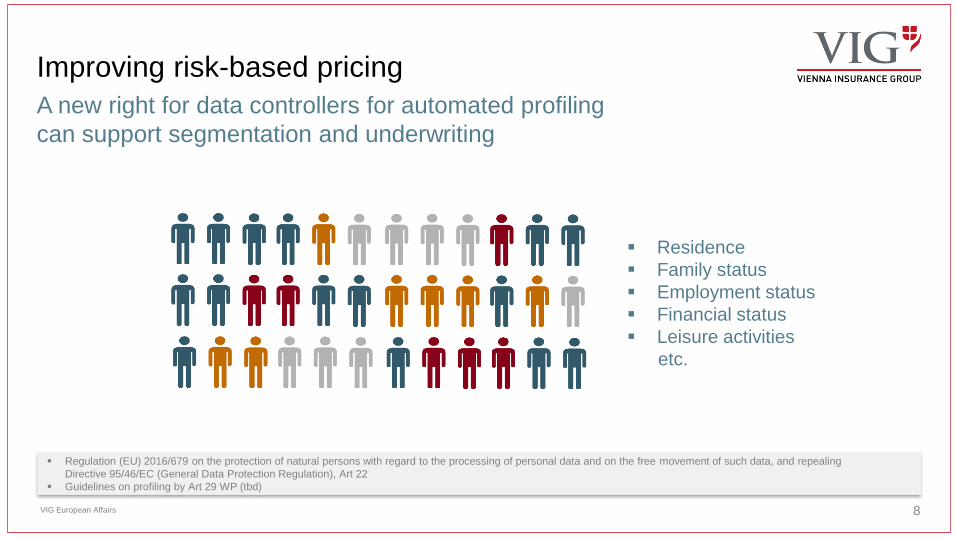

Improving risk-based pricing

A new right for data controllers for automated profiling

can support segmentation and underwriting

Residence

Family status

Employment status

Financial status

Leisure activities

etc.

Opportunities

Obstacles

Agenda

10

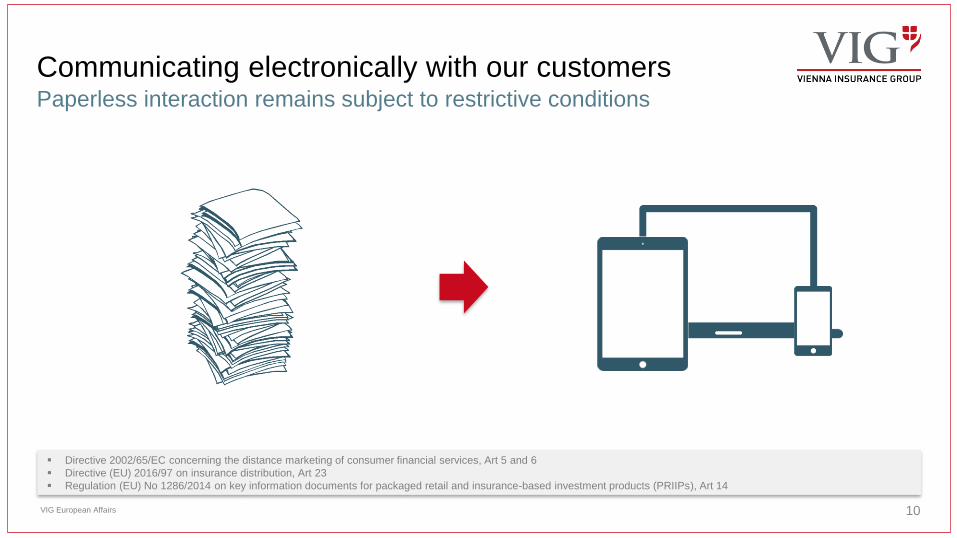

Directive 2002/65/EC concerning the distance marketing of consumer financial services, Art 5 and 6

Directive (EU) 2016/97 on insurance distribution, Art 23

Regulation (EU) No 1286/2014 on key information documents for packaged retail and insurance-based investment products (PRIIPs), Art 14

VIG European Affairs

Communicating electronically with our customersPaperless interaction remains subject to restrictive conditions

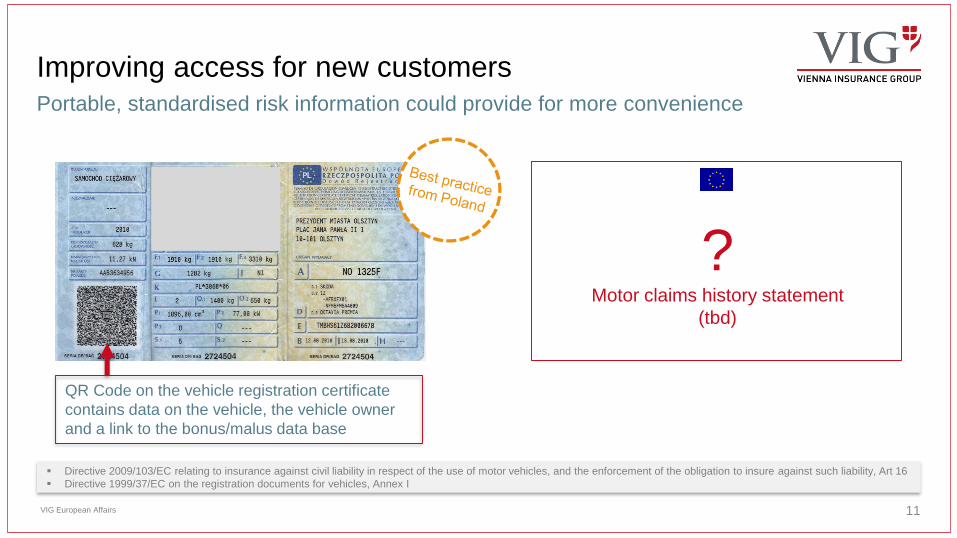

Improving access for new customersPortable, standardised risk information could provide for more convenience

11VIG European Affairs

Directive 2009/103/EC relating to insurance against civil liability in respect of the use of motor vehicles, and the enforcement of the obligation to insure against such liability, Art 16

Directive 1999/37/EC on the registration documents for vehicles, Annex I

QR Code on the vehicle registration certificate

contains data on the vehicle, the vehicle owner

and a link to the bonus/malus data base

?Motor claims history statement

(tbd)

12

Improving the underwriting of cyber risksEU template for personal data breach notifications could structure the authorities’

data base, making it a valuable source for underwriting

VIG European Affairs

Regulation (EU) 2016/679 on the protection of natural persons with regard to the processing of personal data and on the free movement of such data, and repealing

Directive 95/46/EC (General Data Protection Regulation), Art 33

Guidelines on personal data breach notifications by Art 29 WP (tbd)

Data

protection

authority‘s

data base

Insurance

company

covering

cyber risks

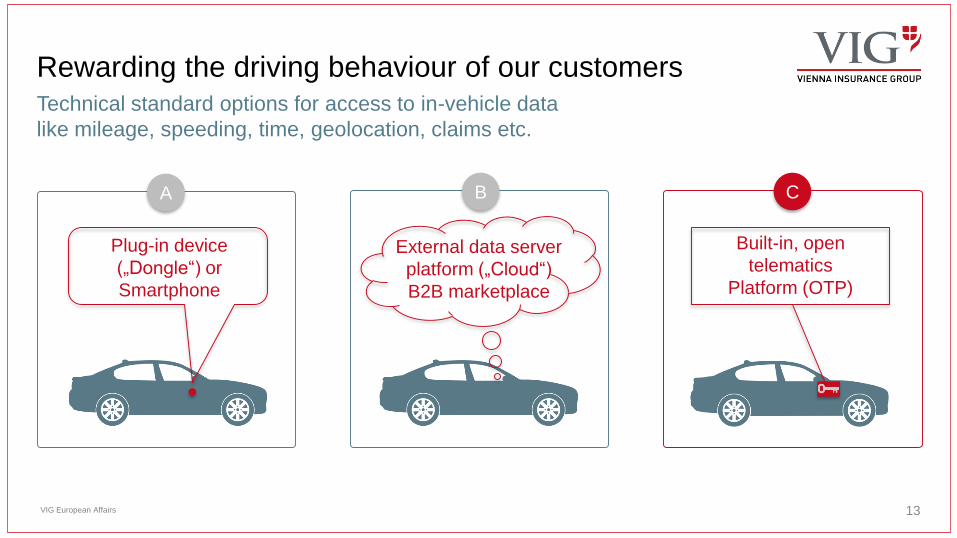

Rewarding the driving behaviour of our customers

13

Technical standard options for access to in-vehicle data

like mileage, speeding, time, geolocation, claims etc.

VIG European Affairs

Customer

External data server

platform („Cloud“)

B2B marketplace

Built-in, open

telematics

Platform (OTP)

Plug-in device

(„Dongle“) or

Smartphone

A B C

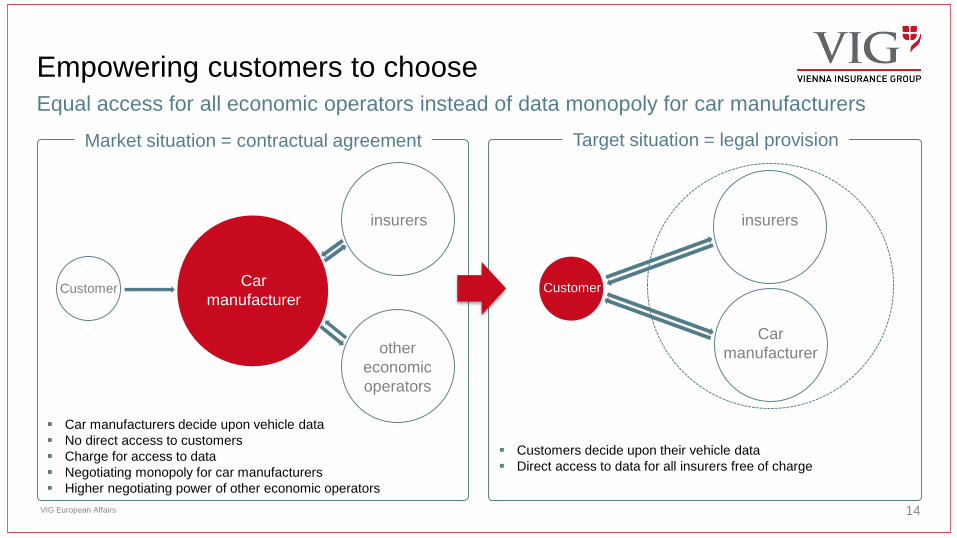

Empowering customers to choose

14

Car manufacturers decide upon vehicle data

No direct access to customers

Charge for access to data

Negotiating monopoly for car manufacturers

Higher negotiating power of other economic operators

CustomerCar

manufacturer

Target situation = legal provisionMarket situation = contractual agreement

Customers decide upon their vehicle data

Direct access to data for all insurers free of charge

Car

manufacturer

Customer

Equal access for all economic operators instead of data monopoly for car manufacturers

VIG European Affairs

insurers

other

economic

operators

insurers

Q & A

Dieter Pscheidl

Head of European Affairs

Vienna Insurance Group AG

E-Mail: [email protected]

Direct line: + 43 50 390 – 20079

www.vig.com

© VIG 2017 - Reproduction in whole or in part of the content of this presentation are made with the consent of the VIG and must be clearly attributed to the VIG.

Check against delivery.