operational performance of credit …shodhganga.inflibnet.ac.in/bitstream/10603/4466/14/14_chapter...

TRANSCRIPT

96

CHAPTER - 5

OPERATIONAL PERFORMANCE OF CREDIT RATING

AGENCIES

A comparative analysis of the operations carried out by the

various credit rating agencies under study, viz. CRISIL, ICRA, CARE

and FITCH has been presented in this chapter. The chapter is divided

into two sections. Section-I provides the general information about

these rating agencies and Section-II describes the operational

performance of all these agencies.

SECTION-I

5.1 CREDIT RATING INFORMATION SERVICES OF INDIA LTD.

(CRISIL)

CRISIL is India‟s leading rating, research, risk and policy advisory

company, and is the fourth largest in the world. It was incorporated in

1987 and was promoted by Industrial Credit and Investment

Corporation of India Ltd. (ICICI) and Unit Trust of India (UTI). It

commenced its operations of rating in 1987-88. CRISIL has its

association with internationally recognized rating agency Standard

and Poor‟s (S&P) since 1996. CRISIL‟s majority shareholder is

Standard and Poor‟s which is a subsidiary of The McGraw-Hill

Companies. The latter is the world‟s foremost provider of independent

credit ratings, indices, risk evaluation, investment research and data.

CRISIL has been recognized by SEBI under the Securities & Exchange

Board of India (Credit Rating Agencies) Regulations, 1999. CRISIL is a

group of businesses which offers the following diversified services:

Rating and Risk Assessment,

Infrastructure Advisory, and

Business Research.

CRISIL‟s services include credit ratings and risk assessment;

research on India‟s economy, industries and companies; financial

research and analytics outsourcing; fund services; risk management

and infrastructure advisory services. Through its IPO Grading

97

initiative, CRISIL has also established a presence in the equity

research domain. It provides all these services through its different

subsidiaries.

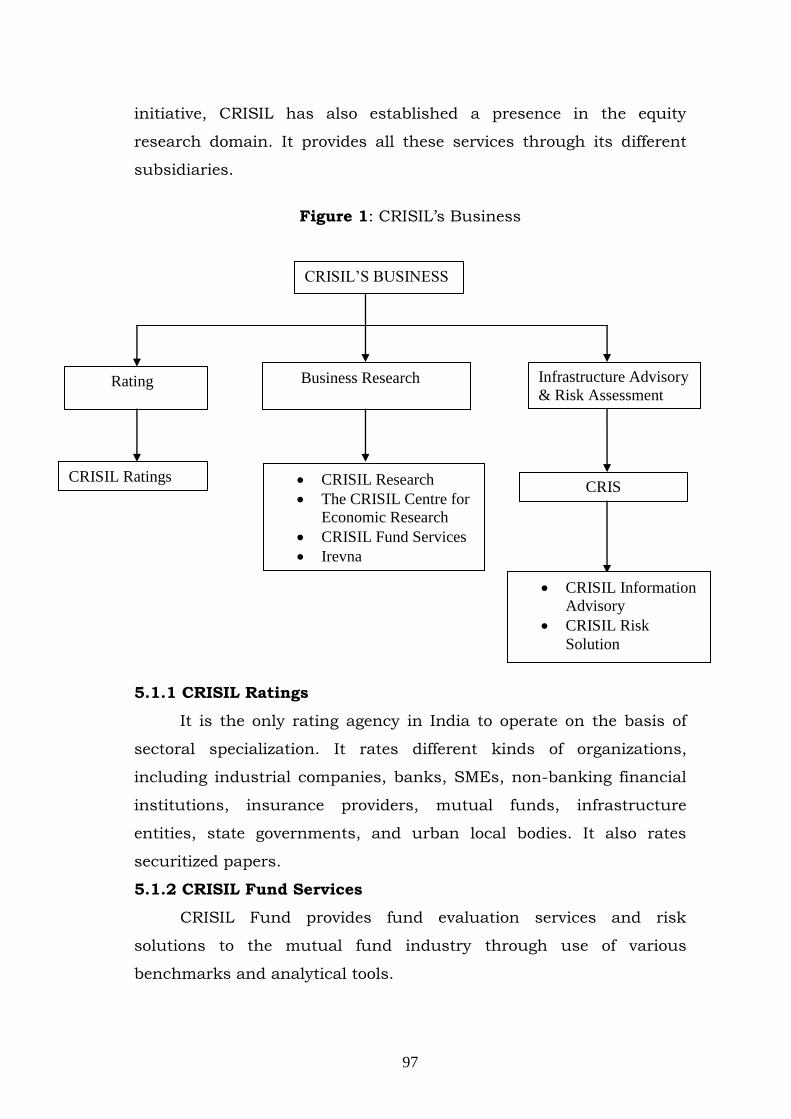

Figure 1: CRISIL‟s Business

5.1.1 CRISIL Ratings

It is the only rating agency in India to operate on the basis of

sectoral specialization. It rates different kinds of organizations,

including industrial companies, banks, SMEs, non-banking financial

institutions, insurance providers, mutual funds, infrastructure

entities, state governments, and urban local bodies. It also rates

securitized papers.

5.1.2 CRISIL Fund Services

CRISIL Fund provides fund evaluation services and risk

solutions to the mutual fund industry through use of various

benchmarks and analytical tools.

CRISIL’S BUSINESS

Rating Infrastructure Advisory

& Risk Assessment Business Research

CRISIL Ratings CRIS

CRISIL Research

The CRISIL Centre for

Economic Research

CRISIL Fund Services

Irevna

CRISIL Information

Advisory

CRISIL Risk

Solution

98

5.1.3 CRISIL Research

CRISIL Research is India's largest independent integrated

research house which provides research, analysis and forecasts on the

Indian economy, industries and companies across financial,

corporate, consulting and public sectors.

5.1.4 The CRISIL Centre for Economic Research

The CRISIL Centre for Economic Research was set up in April

2002. It provides research offerings to different financial players,

corporates and policy-makers. It offers products and services based on

economic analysis to external clients, both independently and in

collaboration with other group businesses.

5.1.5 Irevna

CRISIL entered in equity research business by acquiring Irevna.

Irevna is a division of CRISIL which provides customised equity

research and analytics, and knowledge process outsourcing, to the

world's leading financial institutions, investment banks, private equity

firms and consulting companies.

CRISIL transferred its advisory and risk consulting business

into a 100 per cent subsidiary CRISIL Risk and Infrastructure

Solutions Limited (CRIS) with effect from April 01, 2007. CRIS is

engaged in the areas of infrastructure policy and transaction advisory

services; integrated risk management services and consulting to

banks and corporates, through its divisions CRISIL Infrastructure

Advisory and CRISIL Risk Solutions.

5.1.6 CRISIL Risk and Infrastructure Solutions Limited (CRIS)

CRISIL Infrastructure Advisory works extensively in the areas

of policy-making and economic development. Its range of activities

include undertaking complex feasibility studies, creation of

appropriate policy frameworks, sector reforms, regulatory support and

project structuring for various large and complex projects.

99

CRISIL Risk Solutions business provides risk management

solutions and advice to banks and corporates in the areas of credit

and market risk.

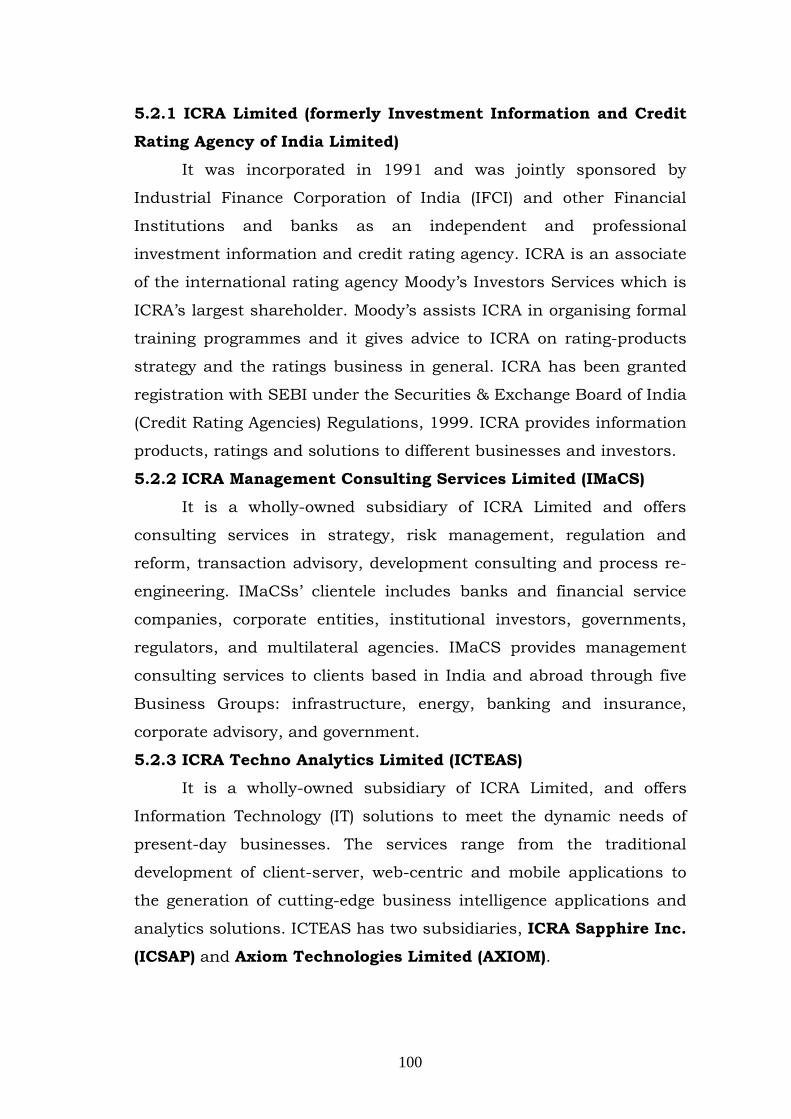

5.2 INVESTMENT INFORMATION AND CREDIT RATING AGENCY

OF INDIA LTD. (ICRA)

ICRA is a full-service credit rating agency but besides Ratings,

Group ICRA offers Consulting services, IT-based services, Information

services, and Outsourcing services. Thus, along with the ICRA

Limited, Group ICRA has three wholly-owned subsidiaries which

together form the ICRA Group of Companies (Group ICRA). These are:

ICRA Management Consulting Services Limited (IMaCS);

ICRA Techno Analytics Limited (ICTEAS); and

ICRA Online Limited (ICRON).

Figure 2: ICRA’s Business

Group ICRA

Credit Rating /

Grading

Management

Consulting IT Software ICRA Online

Limited

( ICRON )

M. Serve Business

Solutions Pvt. Ltd.

( M. Serve )

ICRA Techno

Analysis Limited

( ICTEAS )

ICRA Management

Consulting Services

Ltd. ( IMACS )

ICRA Limited

( ICRA )

Axiom Technologies

Ltd. ( AXIOM )

ICRA Sapphire Inc.

( ICSAP )

100

5.2.1 ICRA Limited (formerly Investment Information and Credit

Rating Agency of India Limited)

It was incorporated in 1991 and was jointly sponsored by

Industrial Finance Corporation of India (IFCI) and other Financial

Institutions and banks as an independent and professional

investment information and credit rating agency. ICRA is an associate

of the international rating agency Moody‟s Investors Services which is

ICRA‟s largest shareholder. Moody‟s assists ICRA in organising formal

training programmes and it gives advice to ICRA on rating-products

strategy and the ratings business in general. ICRA has been granted

registration with SEBI under the Securities & Exchange Board of India

(Credit Rating Agencies) Regulations, 1999. ICRA provides information

products, ratings and solutions to different businesses and investors.

5.2.2 ICRA Management Consulting Services Limited (IMaCS)

It is a wholly-owned subsidiary of ICRA Limited and offers

consulting services in strategy, risk management, regulation and

reform, transaction advisory, development consulting and process re-

engineering. IMaCSs‟ clientele includes banks and financial service

companies, corporate entities, institutional investors, governments,

regulators, and multilateral agencies. IMaCS provides management

consulting services to clients based in India and abroad through five

Business Groups: infrastructure, energy, banking and insurance,

corporate advisory, and government.

5.2.3 ICRA Techno Analytics Limited (ICTEAS)

It is a wholly-owned subsidiary of ICRA Limited, and offers

Information Technology (IT) solutions to meet the dynamic needs of

present-day businesses. The services range from the traditional

development of client-server, web-centric and mobile applications to

the generation of cutting-edge business intelligence applications and

analytics solutions. ICTEAS has two subsidiaries, ICRA Sapphire Inc.

(ICSAP) and Axiom Technologies Limited (AXIOM).

101

ICSAP is a wholly-owned subsidiary of ICTEAS and is based in

Connecticut, USA. It provides business analytics and software

development services backed by offshore teams.

AXIOM is also a wholly-owned subsidiary of ICTEAS and it

operates in Kolkata, India. AXIOM provides various customization and

implementation services on the Oracle E-Business Suite.

5.2.4 ICRA Online Limited (ICRON)

It is a wholly-owned subsidiary of ICRA Limited. ICRON was

incorporated in January 1999 and is providing software and

outsourcing solutions since then. ICRON has a wholly-owned

subsidiary M-Serve Business Solutions Private Limited, a KPO

services company which is headquartered in Kolkata, India. ICRON

has two Strategic Business Units.

The Knowledge Process Outsourcing Division (KPO Division)

ICRON diversified into the Knowledge Process Outsourcing

(KPO) business in April 2004, with focus on the banking, financial

services and insurance as well as on retail, healthcare and

pharmaceuticals sectors. The KPO Division of ICRON offers Knowledge

Process Outsourcing services by translating data and information into

structured business inputs.

The Information Services and Technology Solutions Division (MFI

Division)

The MFI Division serves the Mutual Fund Industry through

Research, Analytics and Mutual Fund Ranking. Besides, the company

provides several innovative products to meet the varied needs of its

clients.

5.3 CREDIT ANALYSIS & RESEARCH LTD. (CARE)

Credit Analysis & Research Ltd. was incorporated in 1993 by

consortium of Banks/financial institutions in India. The three largest

shareholders of CARE are IDBI Bank, Canara Bank and State Bank of

India. CARE‟s Ratings are recognized by Govt. of India and all

regulatory authorities like RBI and SEBI. CARE has been granted

102

registration with SEBI under the Securities & Exchange Board of India

(Credit Rating Agencies) Regulations, 1999. CARE is a founder

member of Association of Credit Rating Agencies in Asia (ACRAA).

CARE is set up with two divisions:

5.3.1 CARE Ratings

CARE Ratings offers a wide range of rating and grading services

across sectors. Types of debt instruments rated by CARE Ratings

include commercial paper, fixed deposit, bonds, debentures, hybrid

instruments, structured obligations, preference shares, loans, etc.

CARE Ratings provide investors and risk managers with credit

opinions based on detailed in-depth research, which encompasses

detailed analysis of risks that affect credit quality of an issuer.

5.3.2 CARE Research and Information Services

CARE Research & Information Services is an independent

division of CARE. The research division undertakes two activities, i.e.,

providing an in-house support to the ratings division and providing

sectoral research to financial intermediaries, corporates, analysts,

policy-makers, etc. as an aid to their decision-making process. CARE

Research & Information Services offers both subscription based

reports and also customised reports on request.

Sector Research

Sector Research includes an in-depth analysis of business

environment of industry, trends, future direction, coverage on sectors

in India, including updates at regular intervals for a year forward.

Customised Research

Customised Research involves business analysis and position in

the market, financial analysis, future outlook, etc. which helps the

clients to make better credit/investment decisions.

5.4 FITCH RATINGS INDIA PRIVATE LTD. (FITCH)

Fitch Ratings India Private Ltd., formerly Duff and Phelps Credit

Rating (India) Private Ltd. (DCR), was established in 1996. Duff &

Phelps India became wholly-owned subsidiary of FITCH in November

103

2001. Fitch Ratings‟ credit ratings provide the agency's views

regarding the future performance and the relative ability of an entity

to meet financial commitments, such as interest, preferred dividends,

repayment of principal, insurance claims or counterparty obligations.

FITCH rates sovereigns, financial institutions, insurance companies,

corporates, municipalities, structured finance obligations, etc. FITCH

has been recognized by SEBI under the Securities & Exchange Board

of India (Credit Rating Agencies) Regulations, 1999.

SECTION-II

In this section, an attempt has been made to study the various

operations conducted by the rating agencies covering the following

dimensions:

1) Activities Undertaken

2) Instruments and Products Rated

3) Methodology Adopted

4) Rating Symbols Used

5) Rating Process Adopted.

5.5 ACTIVITIES UNDERTAKEN BY THE CREDIT RATING

AGENCIES

Credit rating agencies (subsequently denoted as CRAs)

specialize in analysing and evaluating the creditworthiness of

corporate and sovereign issuers of debt securities. Credit rating

agencies are expected to become more important in the wake of

various services/activities being undertaken by various credit rating

agencies, along with the rating services that provide information and

guidance to institutional and individual investors/creditors. These

agencies enhance the ability of borrowers/issuers to access the money

market and the capital market for lapping a large volume of resources

from a wider range of the investing public. These services provided by

the credit rating agencies also assist the regulators in promoting

transparency in the financial markets. A comparative view of the

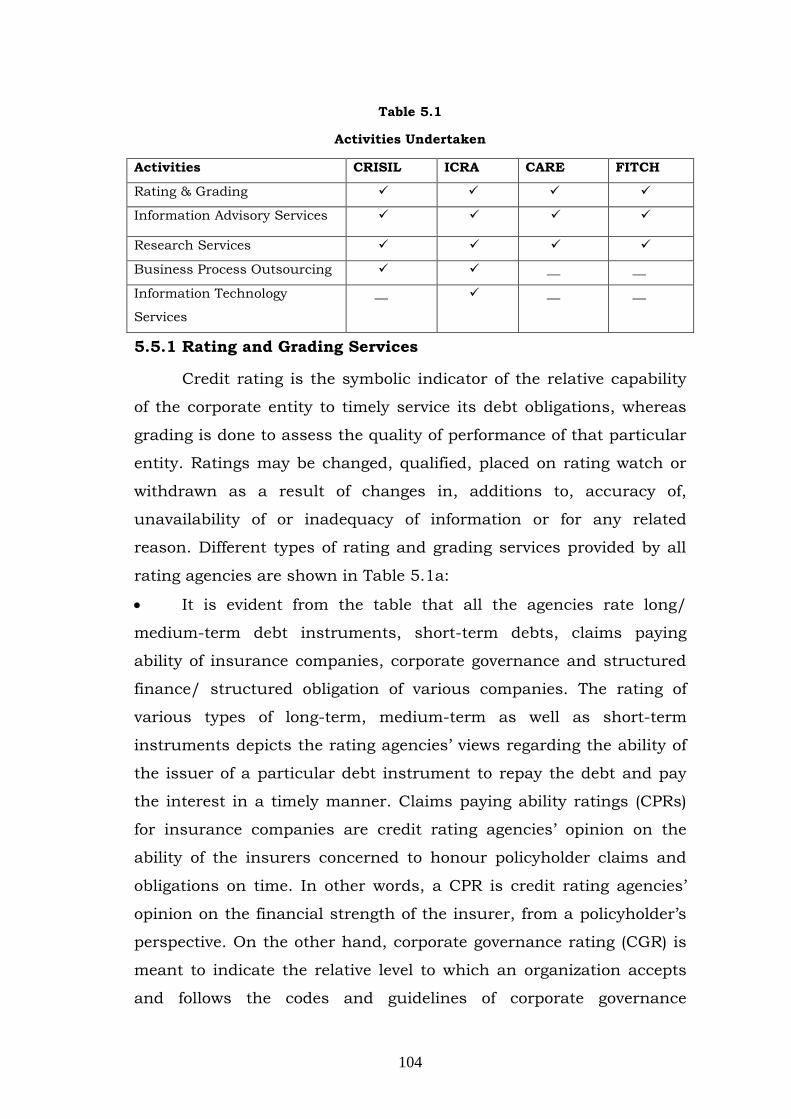

activities undertaken by all these agencies is presented in Table 5.1

104

Table 5.1

Activities Undertaken

Activities CRISIL ICRA CARE FITCH

Rating & Grading

Information Advisory Services

Research Services

Business Process Outsourcing __ __

Information Technology

Services

__ __ __

5.5.1 Rating and Grading Services

Credit rating is the symbolic indicator of the relative capability

of the corporate entity to timely service its debt obligations, whereas

grading is done to assess the quality of performance of that particular

entity. Ratings may be changed, qualified, placed on rating watch or

withdrawn as a result of changes in, additions to, accuracy of,

unavailability of or inadequacy of information or for any related

reason. Different types of rating and grading services provided by all

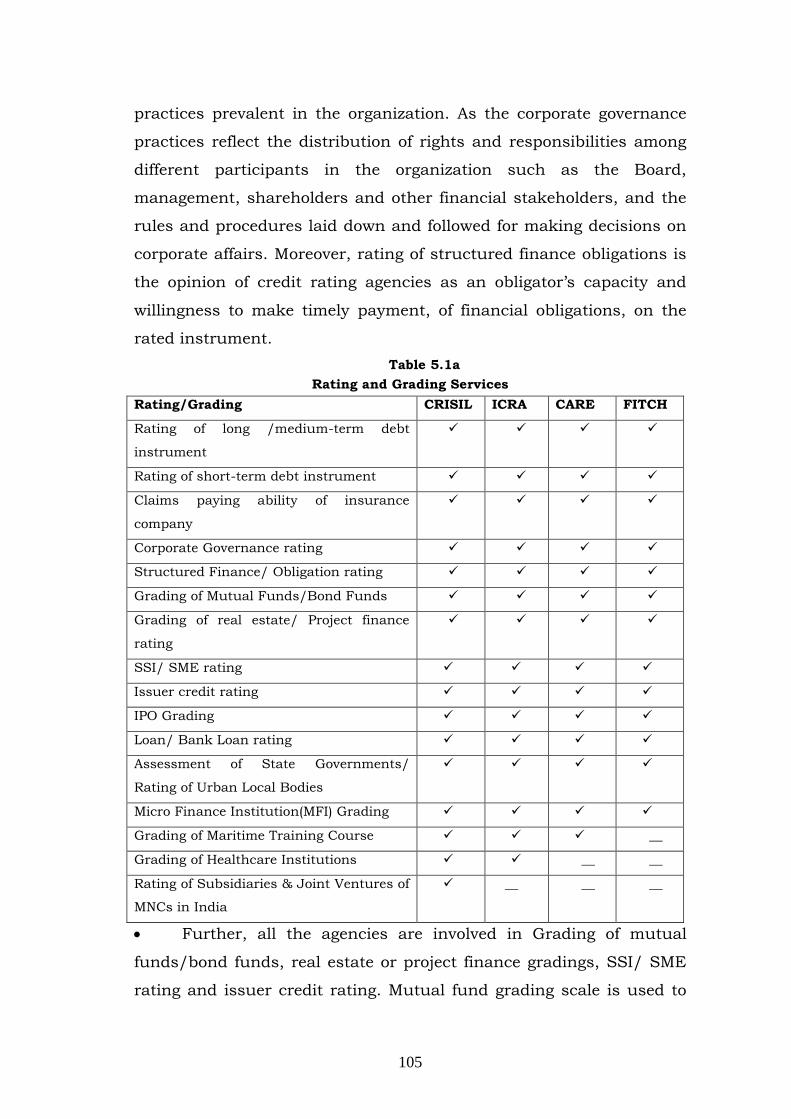

rating agencies are shown in Table 5.1a:

It is evident from the table that all the agencies rate long/

medium-term debt instruments, short-term debts, claims paying

ability of insurance companies, corporate governance and structured

finance/ structured obligation of various companies. The rating of

various types of long-term, medium-term as well as short-term

instruments depicts the rating agencies‟ views regarding the ability of

the issuer of a particular debt instrument to repay the debt and pay

the interest in a timely manner. Claims paying ability ratings (CPRs)

for insurance companies are credit rating agencies‟ opinion on the

ability of the insurers concerned to honour policyholder claims and

obligations on time. In other words, a CPR is credit rating agencies‟

opinion on the financial strength of the insurer, from a policyholder‟s

perspective. On the other hand, corporate governance rating (CGR) is

meant to indicate the relative level to which an organization accepts

and follows the codes and guidelines of corporate governance

105

practices prevalent in the organization. As the corporate governance

practices reflect the distribution of rights and responsibilities among

different participants in the organization such as the Board,

management, shareholders and other financial stakeholders, and the

rules and procedures laid down and followed for making decisions on

corporate affairs. Moreover, rating of structured finance obligations is

the opinion of credit rating agencies as an obligator‟s capacity and

willingness to make timely payment, of financial obligations, on the

rated instrument.

Table 5.1a

Rating and Grading Services

Rating/Grading CRISIL ICRA CARE FITCH

Rating of long /medium-term debt

instrument

Rating of short-term debt instrument

Claims paying ability of insurance

company

Corporate Governance rating

Structured Finance/ Obligation rating

Grading of Mutual Funds/Bond Funds

Grading of real estate/ Project finance

rating

SSI/ SME rating

Issuer credit rating

IPO Grading

Loan/ Bank Loan rating

Assessment of State Governments/

Rating of Urban Local Bodies

Micro Finance Institution(MFI) Grading

Grading of Maritime Training Course __

Grading of Healthcare Institutions __ __

Rating of Subsidiaries & Joint Ventures of

MNCs in India

__ __ __

Further, all the agencies are involved in Grading of mutual

funds/bond funds, real estate or project finance gradings, SSI/ SME

rating and issuer credit rating. Mutual fund grading scale is used to

106

rate the underlying credit risk of debt funds portfolio or risk

associated with investing in individual mutual fund schemes. The

Mutual fund/ Debt Fund rating signifies the likelihood of schemes to

achieve the objectives and meet the obligations to investors. Grading

of real estate developers and projects provides an independent opinion

on the relative performance capability of real estate development

entities. For the investor (buyer of property), the gradings

communicate the risks associated with the developer‟s ability to

deliver in accordance with the terms, quality parameters, and time

stipulated. For developers, the gradings provide a scientific

assessment of their abilities and risk profiles, serve to assist them in

presenting their case to lenders. SSI/ SME rating signifies the

prospect of SSI/ SME of timely servicing of interest and principle as

per terms. Issuer Ratings, on the other hand, provide an opinion on

the general creditworthiness of the rated entities and not specific to a

particular debt instrument.

All agencies are also involved in IPO Grading and Bank loan

rating. IPO Grade represents a relative assessment of the

“fundamentals” of the issue graded in relation to the universe of other

listed equity securities in India. The bank loan ratings provide a

uniform benchmark for credit and pricing decisions in the bank loan

market, offering comments on the likelihood of repayment of loans to

banks. The rating agencies focus both on the risk of default, and the

likelihood of ultimate recovery in the event of default.

The grading of microfinance institutions as well as the

assessment of State Governments and rating of Urban Local Bodies is

being done by all the agencies. MFI Grading is a symbolic indicator of

credit rating agency‟s current opinion on the relative capability of the

Microfinance Institution (MFI) concerned to manage its microfinance

activities in a sustainable manner. The rating of State Governments

and Urban Local Bodies include the ratings of those borrowings which

107

are guaranteed by such bodies including those of State Electricity

Boards, Irrigation Corporations, Road Development Corporation, etc.

With the passage of time CRISIL, ICRA and CARE have started

grading of maritime training institutions/courses. Grading of maritime

training institutions/courses depicts the level of consistency of

institution‟s resources and processes with those required for

delivering the best quality of maritime education and training. The

grading of healthcare institutions is done by CRISIL and ICRA only.

Healthcare Grading presents an independent opinion on the quality of

care provided by healthcare entities to their patients.

CRISIL has also pioneered the rating of subsidiaries and joint

ventures of multinationals in India and has rated several

multinational entities.

5.5.2 Information and Advisory Services

The information and advisory services are the next very

important activity being undertaken by rating agencies, which include

information services, advisory services, project and infrastructure

advisory services, investment and risk management advisory,

Financial Restructuring advisory, etc. as highlighted in Table 5.1b. A

glance at the table provides that all the agencies provide advisory

services and such services are usually undertaken by the agencies

through their advisory arms. Further, all the agencies are engaged in

the information services which primarily focus on addressing the

unique information needs of investors and the capital market

community. Information services promote the efficiency in business

and financial markets by providing proper information to the users as

and when required. The Project/ Infrastructure advisory services are

undertaken by three agencies except FITCH. These agencies evaluate

the credit risks of the projects in areas such as roads, ports, power

and telecom to advise investors and banks about the regulatory

framework, the specific project risks and the ways of risk mitigation.

Investment and risk management advisory services are undertaken by

108

CRISIL and ICRA in which risk management advice is offered on the

efficient management of risk to banks and other lenders. Services

relating to financial restructuring advice are provided by ICRA and

CARE under which these agencies give advice to various companies

about the optimal capital structure and the financial restructuring

options. CARE is the only agency to perform credit appraisal services

which help banks and other non-banking finance companies to set up

or modify their credit appraisal systems.

Table 5.1b

Information and Advisory Services

Services CRISIL ICRA CARE FITCH

Information Services

Advisory Services

Project/ Infrastructure Advisory __

Investment & Risk Management Advisory __ __

Financial Restructuring Advice __ __

Credit Appraisal System __ __ __

5.5.3 Research Activities

Some Indian credit rating agencies have set up research arms to

complement their rating activities. These arms carry out research on

the economy, industries and specific companies, and make the same

available to external subscribers for a fee. Research being done by

various agencies present an in-depth analysis into the matter being

researched and helps various users to properly make use of that

information in future planning or some policy formulation. In

addition, they disseminate opinions on the performance of the

economy or specific industries. The research is also used internally by

the rating agencies for arriving at their rating opinions.

The research related activities done by various agencies are

highlighted in Table 5.1c. All the agencies are engaged in

industry/sector and corporate analysis. Under industry/sector

analysis an in-depth study of the competitive scenario, the

109

imperatives of succeeding in a global market and the relative position

of industry participants is undertaken. Under the corporate analysis

various reports about Indian corporates are provided, by the rating

agencies, with regular updates to cover the implications of changes in

business and economic conditions on corporate. Thus, this corporate

analysis facilitates investment decisions of large investors and meets

the informational requirements of others. Customised research is

done by CRISIL, ICRA and CARE. These customised research

solutions are meant to meet the specific requirements of particular

companies and provide information advantageous to them. Equity

research is done by CRISIL and CARE only. Equity research involves

assessment of the fundamental quality of the company and the

valuation of equity shares.

Table 5.1c

Research Services

Services CRISIL ICRA CARE FITCH

Industry/ Sector Analysis

Corporate Analysis

Customised Research __

Equity Research __ __

5.5.4 Business Process Outsourcing

Business process outsourcing services are being provided by

CRISIL as well as ICRA. These agencies provide knowledge process

outsourcing to various financial institutions, investment banks,

private equity firms and consulting companies at the global level, and

help them to achieve sustainable competitive advantage. The

outsourcing services being provided include financial modelling, data

analysis valuation, outsourced research, financial assets pricing, etc.

CRISIL provides knowledge process outsourcing through one of its

divisions called „Irevna‟, whereas ICRA is involved in this service

through its subsidiary ICRA Online Limited.

110

5.5.5 Information Technology Services

Information and Technology services are provided by ICRA only

through its subsidiary ICRA Techno Analytics Limited (ICTEAS).

ICTEAS provides IT products and solutions along with engineering

services. It provides onsite and offshore design expertise in the areas

like automotive, plant design, construction and instrumentation

space.

5.6 INSTRUMENTS AND PRODUCTS RATED BY RATING

AGENCIES

The primary focus of the rating exercise is to assess the

adequacy to meet debt obligations of a particular instrument in

adverse conditions. Different types of products and instruments are

being rated by all the rating agencies as shown in Table 5.2.

The table reflects that almost similar types of instruments and

products are being rated by all the agencies, but

with a distinct classification of the products or instruments. The table

depicts that various types of long-term instruments rated by credit

rating agencies include bonds, non-convertible debentures, preference

shares, loans/bank loan ratings (BLR), etc.; and medium-term

instruments include fixed deposits of companies (FD) and certificates

of deposit (CD), whereas short-term instruments being rated by the

agencies include commercial papers (CP), short-term loans (STL), etc.

The grading of other instruments including IPOs and mutual funds is

also done by all these agencies.

111

Table 5.2

Instruments & Products Rated

CRISIL ICRA CARE FITCH

Long &

Medium-Term

Instruments

Debentures

Bonds Preference

shares

Structured

Obligations

Fixed deposits Certificates of

Deposit

Loans/Bank

Loans

Short-Term Instruments

Commercial

Papers

Short-term

deposits

Loans

Others

IPOs

Mutual funds

Long-Term

Instruments

Debentures

Bonds

Preference shares

Loans/Bank

Loans

Medium-Term Instruments

Fixed

deposits

Certificates of

Deposit

Short-Term

Instruments

Commercial

Papers

Loans

Others

IPOs

Mutual funds

Long & Medium-

Term

Instruments

Non-convertible

Debentures Bonds

Fixed deposits

Certificates of

Deposit

Structured Obligations

Convertible

Preference Shares

Redeemable

Preference

Shares Loans/Bank

Loans

Short-Term

Instruments

Commercial Papers

Loans

Others

IPOs Mutual funds

Long-Term

Instruments

Debentures

Bonds

Loans/Bank Loans

Medium-Term

Notes

Fixed deposits Certificates of

Deposit

Commercial

Papers

Preferred Stock

Loans

IPOs

Mutual

Funds

5.6.1 Number of Instruments and Products Rated

Instruments and products of various issuers including

corporate sector (manufacturing and trading companies), financial

institutions and banks, finance companies, Nigams, corporations, etc.

are rated by all the credit rating agencies. Further, other institutions

being rated by the agencies include micro finance institutions,

maritime training institutions, healthcare institutions, etc. So, the

details regarding the number of issuers as well as the instruments

rated by all the four rating agencies during the time period 2001-09

have been shown in Tables 5.2a to 5.2h.

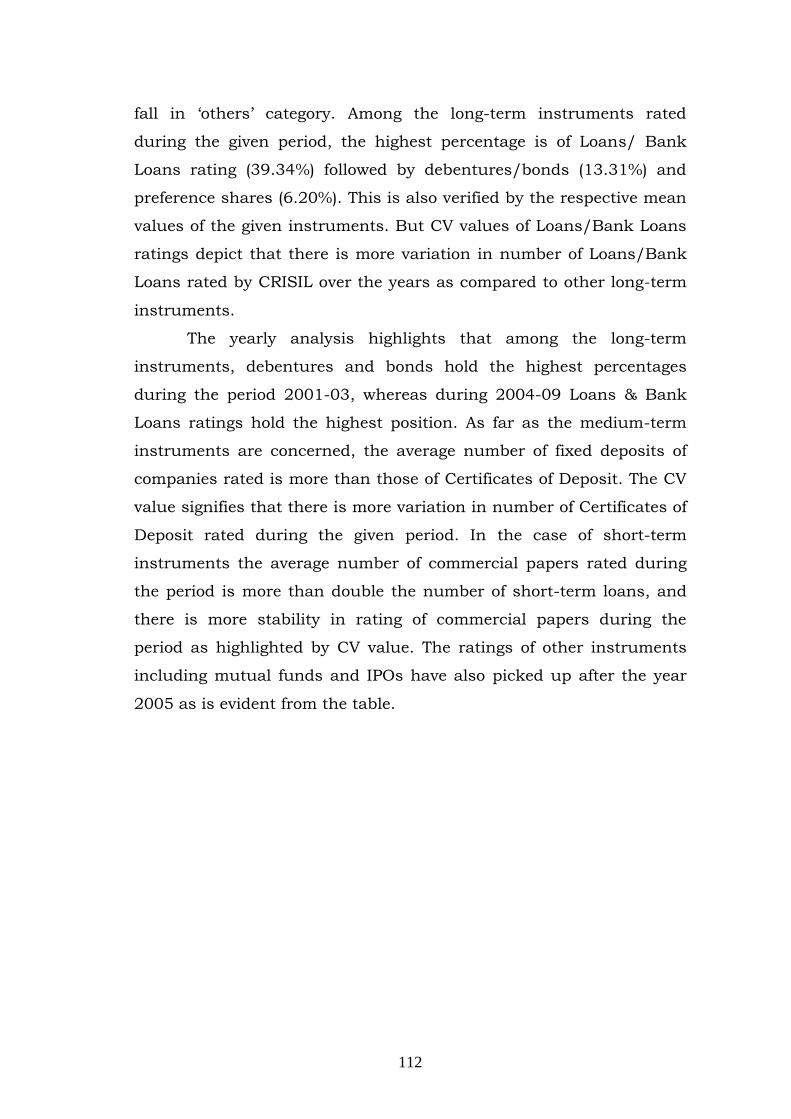

It is clear from Table 5.2a that in the case of CRISIL, 58.85 per

cent of the total rated instruments are of long-term duration, 12.97

per cent of them are of short-term duration, 6.80 per cent instruments

are of medium-term duration and 21.38 per cent of rated instruments

112

fall in „others‟ category. Among the long-term instruments rated

during the given period, the highest percentage is of Loans/ Bank

Loans rating (39.34%) followed by debentures/bonds (13.31%) and

preference shares (6.20%). This is also verified by the respective mean

values of the given instruments. But CV values of Loans/Bank Loans

ratings depict that there is more variation in number of Loans/Bank

Loans rated by CRISIL over the years as compared to other long-term

instruments.

The yearly analysis highlights that among the long-term

instruments, debentures and bonds hold the highest percentages

during the period 2001-03, whereas during 2004-09 Loans & Bank

Loans ratings hold the highest position. As far as the medium-term

instruments are concerned, the average number of fixed deposits of

companies rated is more than those of Certificates of Deposit. The CV

value signifies that there is more variation in number of Certificates of

Deposit rated during the given period. In the case of short-term

instruments the average number of commercial papers rated during

the period is more than double the number of short-term loans, and

there is more stability in rating of commercial papers during the

period as highlighted by CV value. The ratings of other instruments

including mutual funds and IPOs have also picked up after the year

2005 as is evident from the table.

113

Table 5.2a

Instruments Rated by CRISIL

Long-term Instruments

Medium-term

Instruments

Short-term

Instruments

Year Debentures/Bonds

Preference

shares Loan/BLR FD CD CP STL Others Total

2001 197(24.72) 89(11.17) 153(19.20) 42(5.27) 22(2.76) 131(16.44) 60(7.53) 103(12.92) 797(100)

2002 205(24.79) 79(9.55) 169(20.44) 47(5.68) 22(2.66) 145(17.53) 53(6.41) 107(12.94) 827(100)

2003 213(24.51) 92(10.59) 161(18.53) 55(6.33) 35(4.03) 137(15.77) 66(7.59) 110(12.66) 869(100)

2004 420(28.26) 107(7.20) 496(33.38) 63(4.24) 48(3.23) 149(10.03) 79(5.32) 124(8.34) 1486(100)

2005 429(22.63) 123(6.49) 705(37.18) 69(3.64) 50(2.64) 175(9.23) 67(3.53) 278(14.66) 1896(100)

2006 436(21.06) 117(5.65) 728(35.17) 88(4.25) 59(2.85) 192(9.28) 80(3.86) 370(17.87) 2070(100)

2007 487(20.66) 138(5.85) 855(36.27) 97(4.12) 69(2.93) 177(7.51) 89(3.78) 445(18.88) 2357(100)

2008 505(16.80) 145(4.82) 940(31.27) 103(3.43) 74(2.46) 190(6.32) 93(3.09) 956(31.80) 3006(100)

2009 539(15.61) 149(4.31) 1188(34.39) 111(3.21) 86(2.49) 196(5.67) 95(2.75) 109(031.56) 3454(100)

TOTAL 2231(13.31) 1039(6.20) 6595(39.34) 675(4.03) 465(2.77) 1492(8.90) 682(4.07) 3583(21.38) 16762(100)

Overall

Percentage 58.85 6.80 12.97 21.38

Mean 381.22 115.44 599.44 75.00 51.67 165.78 75.78 398.11

SD 137.61 25.53 377.97 25.46 22.60 25.37 15.04 377.05

CV 36.10 22.12 63.05 33.95 43.74 15.30 19.85 94.71

Source: Compiled from various publications and website of the agency.

Note: Figures in parentheses denote percentages.

114

Table 5.2b

Issuers Rated by CRISIL

Year

Corporate

Sector

Financial Institutions

and Banks

Finance

Companies

Nigams/

Corporations Others Total

2001 86(46.99) 28(15.30) 21(11.48) 25(13.66) 23(12.57) 183(100.00)

2002 95(43.58) 32(14.68) 26(11.93) 31(14.22) 34(15.60) 218(100.00)

2003 103(42.92) 34(14.17) 27(11.25) 27(11.25) 49(20.42) 240(100.00)

2004 110(39.71) 46(16.61) 29(10.47) 37(13.36) 55(19.86) 277(100.00)

2005 116(33.33) 54(15.52) 35(10.06) 48(13.79) 95(27.30) 348(100.00)

2006 134(31.38) 69(16.16) 57(13.35) 59(13.82) 108(25.29) 427(100.00)

2007 153(31.74) 77(15.98) 70(14.52) 65(13.49) 117(24.27) 482(100.00)

2008 138(26.49) 90(17.27) 78(14.97) 80(15.36) 135(25.91) 521(100.00)

2009 140(24.14) 109(18.79) 88(15.17) 85(14.66) 158(27.24) 580(100.00)

TOTAL 1075(32.81) 539(16.45) 431(13.16) 457(13.95) 774(23.63) 3276(100.00)

Mean 119.44 59.89 47.89 50.78 86.00

SD 22.89 28.26 25.61 22.68 47.58

CV 19.17 47.18 53.49 44.66 55.33

Source: Compiled from various publications and website of the agency.

Note: Figures in parentheses denote percentages.

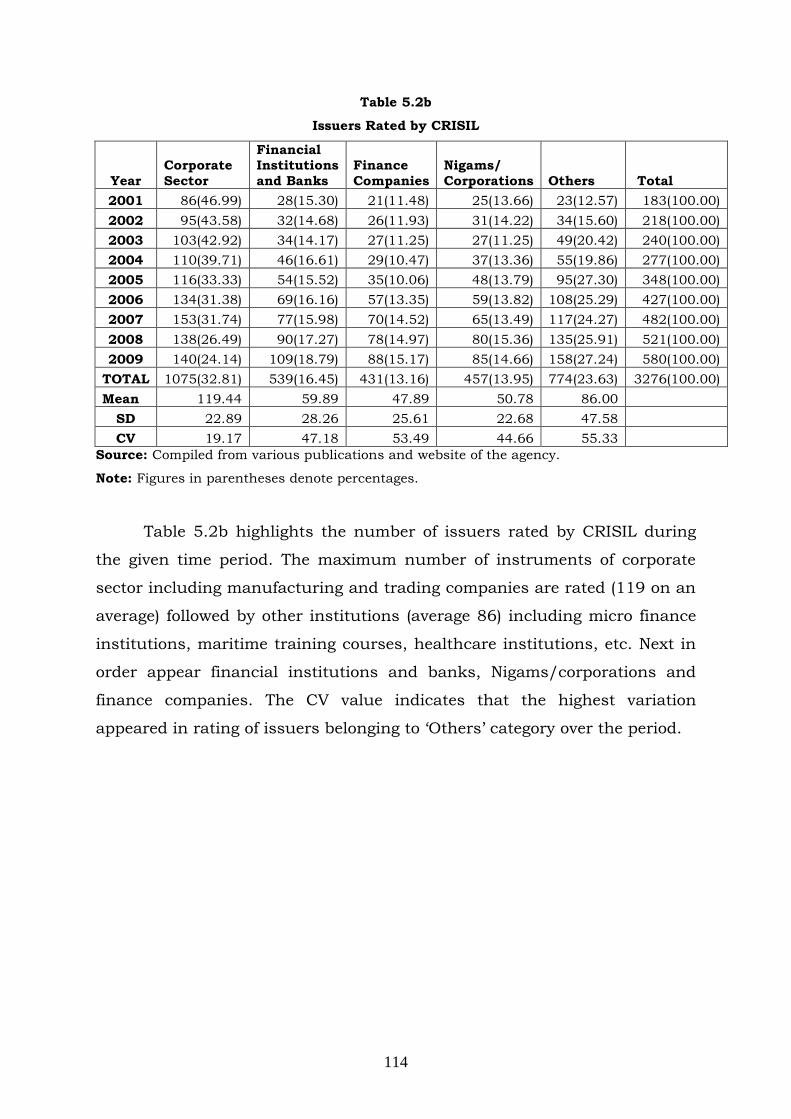

Table 5.2b highlights the number of issuers rated by CRISIL during

the given time period. The maximum number of instruments of corporate

sector including manufacturing and trading companies are rated (119 on an

average) followed by other institutions (average 86) including micro finance

institutions, maritime training courses, healthcare institutions, etc. Next in

order appear financial institutions and banks, Nigams/corporations and

finance companies. The CV value indicates that the highest variation

appeared in rating of issuers belonging to „Others‟ category over the period.

115

Table 5.2c

Instruments Rated by ICRA

Long-term Instruments Medium-term Instruments

Short-term Instruments

Year Debentures/Bonds

Preference

Shares Loan/BLR FD CD CP STL Others Total

2001 42(22.22) 24(12.70) 33(17.46) 14(7.41) 4(2.12) 27(14.29) 13(6.88) 32(16.93) 189(100.00)

2002 38(19.59) 26(13.40) 35(18.04) 15(7.73) 5(2.58) 29(14.95) 14(7.22) 32(16.49) 194(100.00)

2003 53(22.75) 28(12.02) 38(16.31) 17(7.30) 8(3.43) 35(15.02) 15(6.44) 39(16.74) 233(100.00)

2004 59(24.69) 28(11.72) 38(15.90) 17(7.11) 8(3.35) 35(14.64) 15(6.28) 39(16.32) 239(100.00)

2005 67(23.67) 34(12.01) 45(15.90) 22(7.77) 10(3.53) 42(14.84) 19(6.71) 44(15.55) 283(100.00)

2006 68(21.79) 41(13.14) 50(16.03) 23(7.37) 12(3.85) 47(15.06) 21(6.73) 50(16.03) 312(100.00)

2007 98(21.12) 58(12.50) 78(16.81) 35(7.54) 19(4.09) 74(15.95) 33(7.11) 69(14.87) 464(100.00)

2008 119(20.24) 82(13.95) 95(16.16) 57(9.69) 27(4.59) 85(14.46) 40(6.80) 83(14.12) 588(100.00)

2009 86(20.14) 58(13.58) 68(15.93) 29(6.79) 23(5.39) 59(13.82) 28(6.56) 76(17.80) 427(100.00)

TOTAL 630(21.51) 379(12.94) 480(16.39) 229(7.82) 116(3.96) 433(14.78) 198(6.76) 464(15.84) 2929(100.00)

Overall

Percentage 50.84 11.78 21.54 15.84

Mean 70.00 42.11 53.33 25.44 12.89 48.11 22.00 51.56

SD 26.63 19.84 21.97 13.69 8.19 20.44 9.58 19.46

CV 38.04 47.11 41.19 53.82 63.56 42.49 43.54 37.75

Source: Compiled from various publications and website of the agency.

Note: Figures in parentheses denote percentages.

116

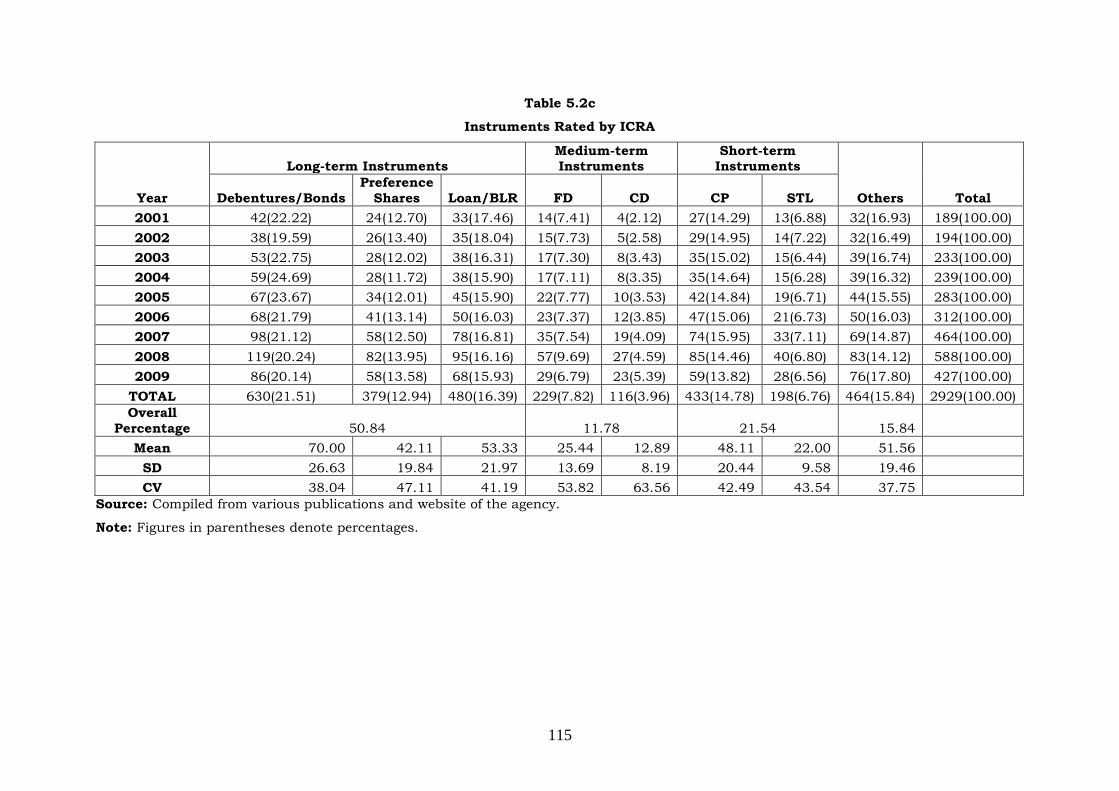

Table 5.2c highlights that during the time period 2001-09 among all

the instruments rated by ICRA, 50.84 per cent were of long-term duration;

21.54 per cent of them were of short-term duration; 11.78 per cent

instruments were of medium-term duration; and 15.84 per cent of rated

instruments fall in „others‟ category. Moreover, in the case of long-term

instruments rated by ICRA, the average number of debentures and bonds

(70) is the highest followed by loan as well as Bank loan ratings (53) and

preference shares (42). This trend has been observed during the whole

period of study. CV value further clarifies that there is more variation in the

rating of preference shares during the given period. In the case of medium-

term instruments rated by ICRA the average number of fixed deposits being

rated, i.e., 25 is almost double the number of certificates of deposit, i.e., 12.

However, in the case of short-term instruments also the average number of

commercial papers rated is more than double the number of short-term

loans rated. Among all the instruments being rated over the period, the

highest variation has been found in the rating of certificates of deposit as

depicted by their CV value.

Table 5.2d

Issuers Rated by ICRA

Year

Corporate

Sector

Financial Institutions

and Banks

Finance

Companies

Nigams/

Corporations Others Total

2001 20(30.77) 14(21.54) 12(18.46) 10(15.38) 9(13.85) 65(100.00)

2002 25(31.25) 17(21.25) 15(18.75) 10(12.50) 13(16.25) 80(100.00)

2003 32(30.77) 20(19.23) 18(17.31) 18(17.31) 16(15.38) 104(100.00)

2004 37(30.33) 21(17.21) 18(14.75) 22(18.03) 24(19.67) 122(100.00)

2005 39(29.10) 24(17.91) 24(17.91) 21(15.67) 26(19.40) 134(100.00)

2006 42(28.19) 30(20.13) 22(14.77) 26(17.45) 29(19.46) 149(100.00)

2007 45(27.11) 33(19.88) 26(15.66) 28(16.87) 34(20.48) 166(100.00)

2008 49(26.49) 36(19.46) 29(15.68) 33(17.84) 38(20.54) 185(100.00)

2009 68(30.49) 40(17.94) 36(16.14) 38(17.04) 41(18.39) 223(100.00)

TOTAL 357(29.07) 242(19.71) 230(18.73) 209(17.02) 190(15.47) 1228(100.00)

Mean 39.67 26.11 22.22 22.89 25.56

SD 14.11 9.02 7.46 9.53 11.19

CV 35.56 34.54 33.58 41.65 43.80

Source: Compiled from various publications and website of the agency.

Note: Figures in parentheses denote percentages.

117

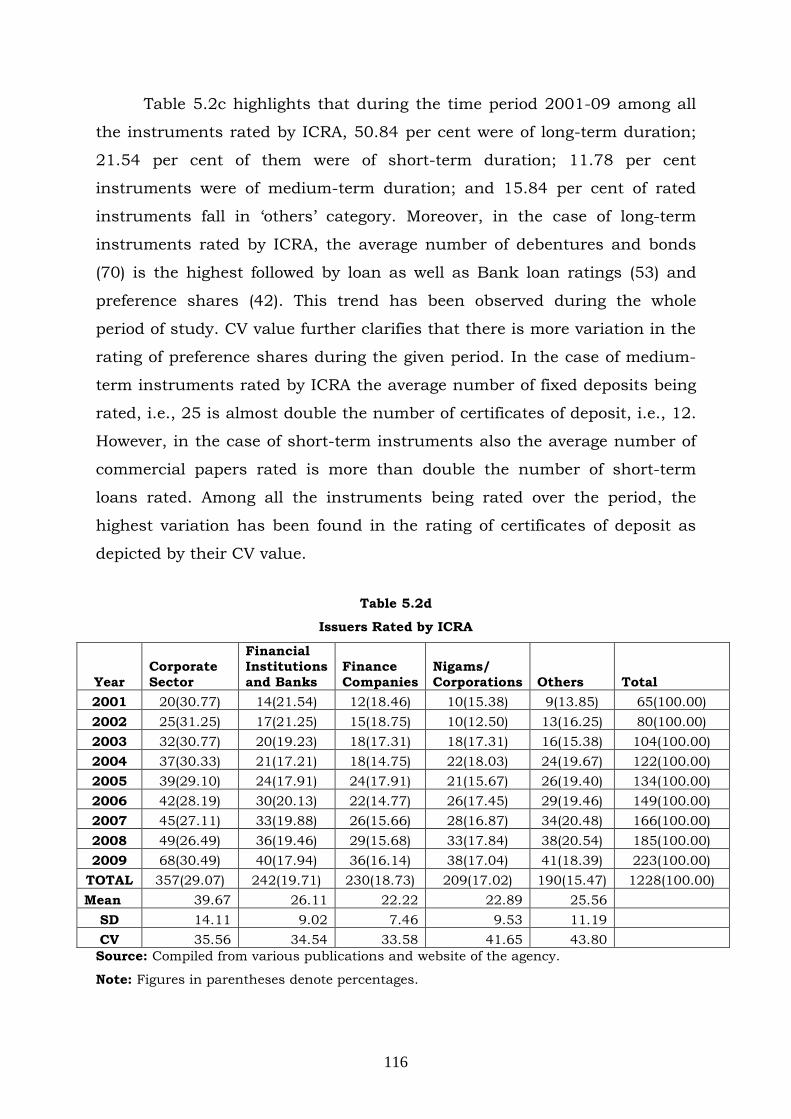

Table 5.2d carries the data showing the number of issuers rated by

ICRA during the period 2001-09. On an average 39 issuers falling in

corporate sector have been rated by ICRA during the given period, followed

by 26 financial institutions and banks, 25 issuers falling in „others‟ category,

whereas the average number of finance companies and nigams/corporations

rated by ICRA during the period are 22 each. The CV value being the highest

for issuers falling in „others‟ category clarifies that there is more variability

in rating of these types of issuers during the study period.

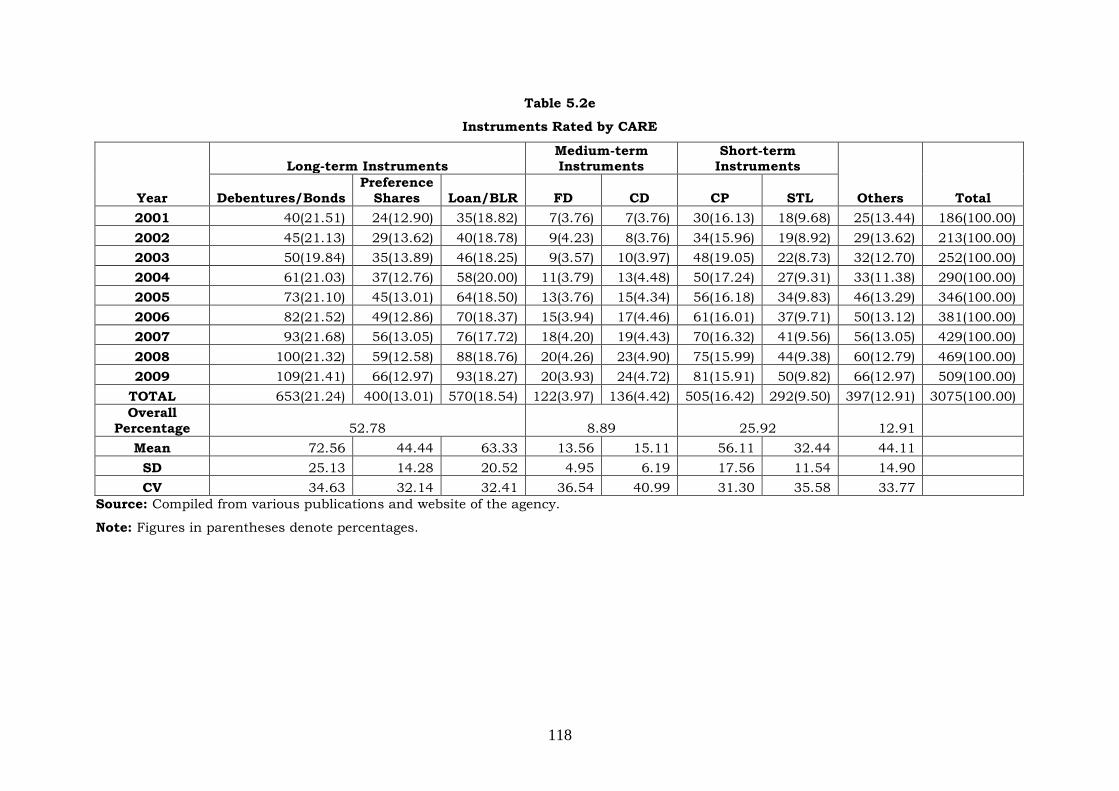

Table 5.2e exhibits the number of instruments rated by CARE. The

table explains that in the case of CARE, 52.78 per cent of the total rated

instruments were of long-term duration, 25.92 per cent of them were of

short-term duration, 8.89 per cent instruments were of medium-term

duration and 12.91 per cent of them fall in „others' category. Further, among

the long-term instruments the average number of debentures and bonds is

higher, followed by loan & bank loan rating and preference shares. Whereas

among the medium-term instruments rated almost equal number of Fixed

Deposits and Certificates of Deposit were rated during the period but year-

wise variation in rating of Certificates of Deposit is more as is clear from

their CV value. As far as short-term instruments are concerned, the average

number of commercial papers rated (56) during the given period are more

than the short-term loans (32). A good number of other instruments

including mutual funds and IPOs are also rated by CARE during the given

period.

118

Table 5.2e

Instruments Rated by CARE

Long-term Instruments Medium-term Instruments

Short-term Instruments

Year Debentures/Bonds

Preference

Shares Loan/BLR FD CD CP STL Others Total

2001 40(21.51) 24(12.90) 35(18.82) 7(3.76) 7(3.76) 30(16.13) 18(9.68) 25(13.44) 186(100.00)

2002 45(21.13) 29(13.62) 40(18.78) 9(4.23) 8(3.76) 34(15.96) 19(8.92) 29(13.62) 213(100.00)

2003 50(19.84) 35(13.89) 46(18.25) 9(3.57) 10(3.97) 48(19.05) 22(8.73) 32(12.70) 252(100.00)

2004 61(21.03) 37(12.76) 58(20.00) 11(3.79) 13(4.48) 50(17.24) 27(9.31) 33(11.38) 290(100.00)

2005 73(21.10) 45(13.01) 64(18.50) 13(3.76) 15(4.34) 56(16.18) 34(9.83) 46(13.29) 346(100.00)

2006 82(21.52) 49(12.86) 70(18.37) 15(3.94) 17(4.46) 61(16.01) 37(9.71) 50(13.12) 381(100.00)

2007 93(21.68) 56(13.05) 76(17.72) 18(4.20) 19(4.43) 70(16.32) 41(9.56) 56(13.05) 429(100.00)

2008 100(21.32) 59(12.58) 88(18.76) 20(4.26) 23(4.90) 75(15.99) 44(9.38) 60(12.79) 469(100.00)

2009 109(21.41) 66(12.97) 93(18.27) 20(3.93) 24(4.72) 81(15.91) 50(9.82) 66(12.97) 509(100.00)

TOTAL 653(21.24) 400(13.01) 570(18.54) 122(3.97) 136(4.42) 505(16.42) 292(9.50) 397(12.91) 3075(100.00)

Overall

Percentage 52.78 8.89 25.92 12.91

Mean 72.56 44.44 63.33 13.56 15.11 56.11 32.44 44.11

SD 25.13 14.28 20.52 4.95 6.19 17.56 11.54 14.90

CV 34.63 32.14 32.41 36.54 40.99 31.30 35.58 33.77

Source: Compiled from various publications and website of the agency.

Note: Figures in parentheses denote percentages.

119

Table 5.2f

Issuers Rated by CARE

Year

Corporate

Sector

Financial Institutions

and Banks

Finance

Companies

Nigams/

Corporations Others Total

2001 19(28.79) 14(21.21) 14(21.21) 10(15.15) 9(13.64) 66(100.00)

2002 22(26.19) 17(20.24) 18(21.43) 14(16.67) 13(15.48) 84(100.00)

2003 26(25.74) 20(19.80) 20(19.80) 17(16.83) 18(17.82) 101(100.00)

2004 27(23.68) 28(24.56) 25(21.93) 19(16.67) 15(13.16) 114(100.00)

2005 34(25.95) 26(19.85) 28(21.37) 23(17.56) 20(15.27) 131(100.00)

2006 40(27.97) 28(19.58) 29(20.28) 25(17.48) 21(14.69) 143(100.00)

2007 45(27.44) 33(20.12) 31(18.90) 28(17.07) 27(16.46) 164(100.00)

2008 47(25.82) 36(19.78) 38(20.88) 33(18.13) 28(15.38) 182(100.00)

2009 51(25.12) 38(18.72) 40(19.70) 39(19.21) 35(17.24) 203(100.00)

TOTAL 311(26.18) 240(20.20) 243(20.45) 208(17.51) 186(15.66) 1188(100.00)

Mean 34.56 26.67 27.00 23.11 20.67

SD 11.70 8.35 8.76 9.27 8.17

CV 33.84 31.32 32.45 40.09 39.53

Source: Compiled from various publications and website of the agency.

Note: Figures in parentheses denote percentages.

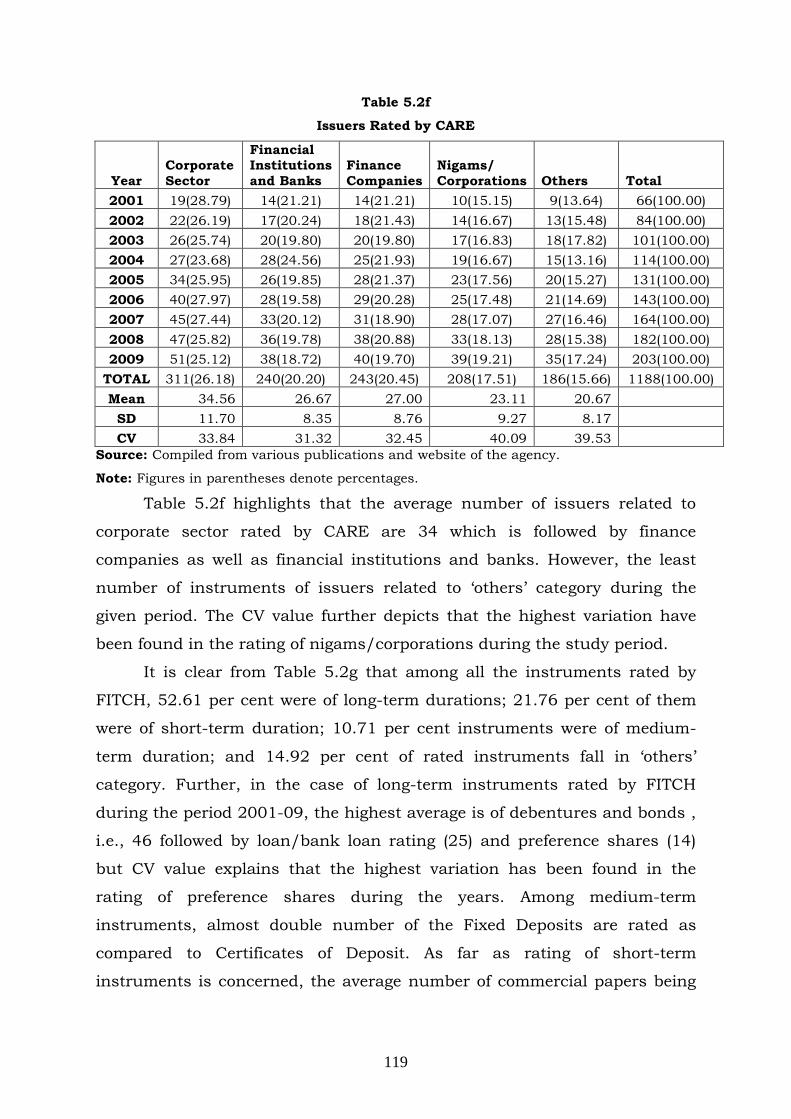

Table 5.2f highlights that the average number of issuers related to

corporate sector rated by CARE are 34 which is followed by finance

companies as well as financial institutions and banks. However, the least

number of instruments of issuers related to „others‟ category during the

given period. The CV value further depicts that the highest variation have

been found in the rating of nigams/corporations during the study period.

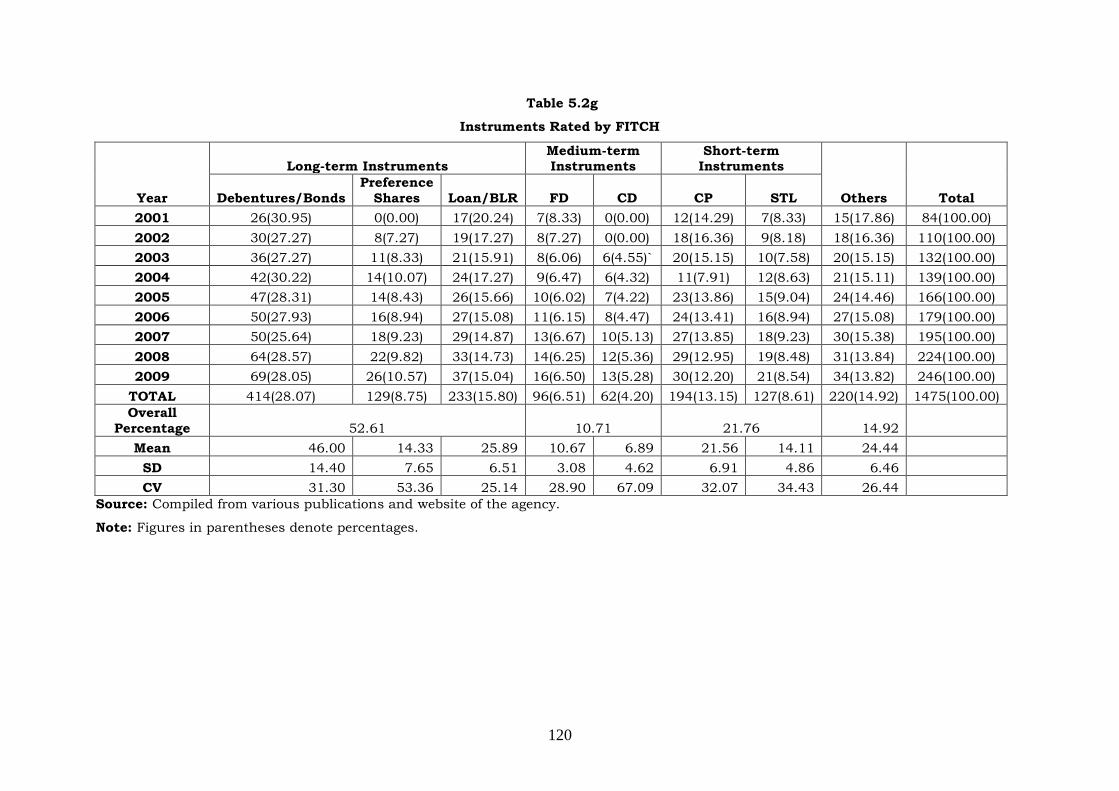

It is clear from Table 5.2g that among all the instruments rated by

FITCH, 52.61 per cent were of long-term durations; 21.76 per cent of them

were of short-term duration; 10.71 per cent instruments were of medium-

term duration; and 14.92 per cent of rated instruments fall in „others‟

category. Further, in the case of long-term instruments rated by FITCH

during the period 2001-09, the highest average is of debentures and bonds ,

i.e., 46 followed by loan/bank loan rating (25) and preference shares (14)

but CV value explains that the highest variation has been found in the

rating of preference shares during the years. Among medium-term

instruments, almost double number of the Fixed Deposits are rated as

compared to Certificates of Deposit. As far as rating of short-term

instruments is concerned, the average number of commercial papers being

120

Table 5.2g

Instruments Rated by FITCH

Long-term Instruments Medium-term Instruments

Short-term Instruments

Year Debentures/Bonds

Preference

Shares Loan/BLR FD CD CP STL Others Total

2001 26(30.95) 0(0.00) 17(20.24) 7(8.33) 0(0.00) 12(14.29) 7(8.33) 15(17.86) 84(100.00)

2002 30(27.27) 8(7.27) 19(17.27) 8(7.27) 0(0.00) 18(16.36) 9(8.18) 18(16.36) 110(100.00)

2003 36(27.27) 11(8.33) 21(15.91) 8(6.06) 6(4.55)` 20(15.15) 10(7.58) 20(15.15) 132(100.00)

2004 42(30.22) 14(10.07) 24(17.27) 9(6.47) 6(4.32) 11(7.91) 12(8.63) 21(15.11) 139(100.00)

2005 47(28.31) 14(8.43) 26(15.66) 10(6.02) 7(4.22) 23(13.86) 15(9.04) 24(14.46) 166(100.00)

2006 50(27.93) 16(8.94) 27(15.08) 11(6.15) 8(4.47) 24(13.41) 16(8.94) 27(15.08) 179(100.00)

2007 50(25.64) 18(9.23) 29(14.87) 13(6.67) 10(5.13) 27(13.85) 18(9.23) 30(15.38) 195(100.00)

2008 64(28.57) 22(9.82) 33(14.73) 14(6.25) 12(5.36) 29(12.95) 19(8.48) 31(13.84) 224(100.00)

2009 69(28.05) 26(10.57) 37(15.04) 16(6.50) 13(5.28) 30(12.20) 21(8.54) 34(13.82) 246(100.00)

TOTAL 414(28.07) 129(8.75) 233(15.80) 96(6.51) 62(4.20) 194(13.15) 127(8.61) 220(14.92) 1475(100.00)

Overall

Percentage 52.61 10.71 21.76 14.92

Mean 46.00 14.33 25.89 10.67 6.89 21.56 14.11 24.44

SD 14.40 7.65 6.51 3.08 4.62 6.91 4.86 6.46

CV 31.30 53.36 25.14 28.90 67.09 32.07 34.43 26.44

Source: Compiled from various publications and website of the agency.

Note: Figures in parentheses denote percentages.

121

rated are 21 as compared to 14 in the case of short-term loans. The other

instruments including mutual funds and IPOs are also rated by FITCH

during the years of study. Among all the instruments rated the highest

variation has been found in the rating of Certificate of Deposits as signified

by its CV value.

Table 5.2h

Issuers Rated by FITCH

Year

Corporate

Sector

Financial

Institutions

and Banks

Finance

Companies

Nigams/

Corporations Others Total

2001 16(45.71) 7(20.00) 7(20.00) 5(14.29) 0(0.00) 35(100.00)

2002 19(43.18) 9(20.45) 8(18.18) 5(11.36) 3(6.82) 44(100.00)

2003 21(41.18) 9(17.65) 10(19.61) 7(13.73) 4(7.84) 51(100.00)

2004 23(37.10) 13(20.97) 12(19.35) 9(14.52) 5(8.06) 62(100.00)

2005 25(36.76) 14(20.59) 13(19.12) 10(14.71) 6(8.82) 68(100.00)

2006 28(34.15) 17(20.73) 14(17.07) 13(15.85) 10(12.20) 82(100.00)

2007 29(32.22) 19(21.11) 16(17.78) 15(16.67) 11(12.22) 90(100.00)

2008 31(32.29) 20(20.83) 17(17.71) 16(16.67) 12(12.50) 96(100.00)

2009 34(30.91) 23(20.91) 20(18.18) 19(17.27) 14(12.73) 110(100.00)

TOTAL 226(35.42) 131(20.53) 117(18.34) 99(15.52) 65(10.19) 638(100.00)

Mean 25.11 14.56 13.00 11.00 7.22

SD 5.90 5.57 4.27 5.02 4.71

CV 23.51 38.27 32.86 45.68 65.23

Source: Compiled from various publications and website of the agency.

Note: Figures in parentheses denote percentages.

Table 5.2h depicts that among the issuers whose instruments being

rated by FITCH during the period 2001-09, average number is the highest

(25) for corporate sector (manufacturing & trading companies), whereas

average number is the least (7) for institutions falling in „others‟ category

which includes micro finance institutions only. Whereas financial

institutions and banks, finance companies and nigams/ corporations hold

the second, third and fourth position respectively. CV values reveal that the

highest variations have been in rating of institutions belonging to „others‟

category during the period.

122

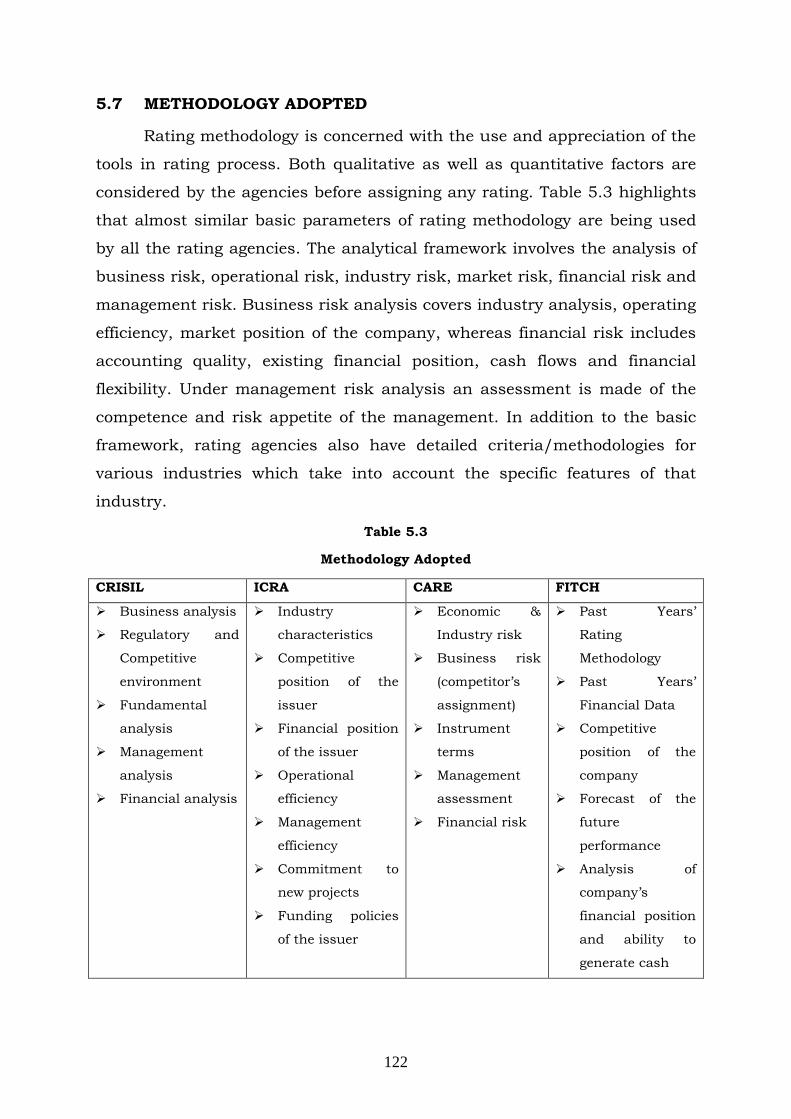

5.7 METHODOLOGY ADOPTED

Rating methodology is concerned with the use and appreciation of the

tools in rating process. Both qualitative as well as quantitative factors are

considered by the agencies before assigning any rating. Table 5.3 highlights

that almost similar basic parameters of rating methodology are being used

by all the rating agencies. The analytical framework involves the analysis of

business risk, operational risk, industry risk, market risk, financial risk and

management risk. Business risk analysis covers industry analysis, operating

efficiency, market position of the company, whereas financial risk includes

accounting quality, existing financial position, cash flows and financial

flexibility. Under management risk analysis an assessment is made of the

competence and risk appetite of the management. In addition to the basic

framework, rating agencies also have detailed criteria/methodologies for

various industries which take into account the specific features of that

industry.

Table 5.3

Methodology Adopted

CRISIL ICRA CARE FITCH

Business analysis

Regulatory and

Competitive

environment

Fundamental

analysis

Management

analysis

Financial analysis

Industry

characteristics

Competitive

position of the

issuer

Financial position

of the issuer

Operational

efficiency

Management

efficiency

Commitment to

new projects

Funding policies

of the issuer

Economic &

Industry risk

Business risk

(competitor‟s

assignment)

Instrument

terms

Management

assessment

Financial risk

Past Years‟

Rating

Methodology

Past Years‟

Financial Data

Competitive

position of the

company

Forecast of the

future

performance

Analysis of

company‟s

financial position

and ability to

generate cash

123

5.7.1 CRISIL Rating Methodology: CRISIL assesses all the factors that

could affect credit worthiness of the borrowing company and then assigns

rating to debt instruments. The key factors, considered for rating

assessment are:

Business Analysis: Every relevant piece of information concerning the

business is evaluated by assessing industrial risk, market position of the

company within industry, operating efficiency and legal position.

Financial Analysis: Under financial analysis, all relevant aspects

connected with the business and financial position of the company are

assessed. The profitability, solvency and liquidity ratios are taken into

consideration. Thus, CRISIL considers Growth rate of PAT, PAT/OI,

PBIT/Net Worth, Earnings on Capital Employed, PBDITA/TI, Current

Ratio, Quick Ratio, Debt to Equity Ratio, Interest Coverage Ratio, Pre-tax

Coverage Ratio, Earnings on Assets to Capital Employed, etc.

Management Evaluation: Judgment of management performance based

on past operating and financial results, planning and control system of

management, depths of managerial talents are considered.

Regulatory and Competitive Environment: CRISIL evaluates structure

and regulatory framework of financial system in which it works.

Fundamental Analysis: It covers aspects on liquidity management

(capital structure), asset quality, economic as well as industrial analysis

of that particular entity to take the rating decision accordingly.

5.7.2 ICRA Rating Methodology: While assigning ratings ICRA considers

all relevant factors that have a bearing on the future cash generation of the

issuer. A detailed analysis of the past financial statements is made and

estimates of future earnings under various scenarios are drawn up, over the

tenure of the instrument being rated. The other factors considered are:

Industry Characteristics: Industrial features are evaluated by ICRA by

taking into account various success factors, demand and supply position,

structure of industry and Government policies related to that particular

entity.

124

Competitive Position: The competitive position of the issuer is

evaluated by considering various factors including nature and basis of

competition, competitive advantage through marketing and distribution,

strength, weaknesses and opportunities available to the issuer in

comparison to the competitors.

Financial Risk Analysis: Under this, ICRA considers various accounting

policies, debt servicing track record, cash flow position, profitability

position and capital structure of the issuer. The ratios considered

specifically for the purpose include: Profit after Tax /Total Income, Profit

Before Depreciation Interest and Tax/Total Income, Earnings Before

Depreciation Interest and Tax/ Interest and Fixed Charges, Return on

Capital Employed, Return on Net Worth, Total Debt/ Net Worth, Current

Ratio, Quick Ratio, Cash Accrual Ratio and so on.

Operational Efficiency: Operational efficiency of the company is

assessed by evaluating the price or cost advantage availability, cost and

quality of raw material, availability of labour and labour relations

prevalent in the organization.

Management Quality: The quality of the management is evaluated by

observing the goals and philosophies of the management, and its

strategies and abilities to overcome adverse situations.

Commitment to New Projects: ICRA also evaluates the company‟s

commitment to new projects by estimating its progress in the initial

stages and from past performance on similar projects.

Funding Policies of the Issuer: The funding policies of the issuer are

also evaluated to get the deep knowledge of the sources of funds of the

issuer company and the uses to which these funds have been put into.

5.7.3 CARE Rating Methodology: CARE also takes into account various

quantitative as well as qualitative factors while assigning rating which

include:

Economy and Industry Risk: The factors assessed by CARE include the

effect of economic cycle on industry, business cycles, tariff structure,

125

basis of competition, environmental as well as political factors concerning

the issuer‟s business.

Business Risks (Competitor's Assessment): Factors considered under

this are size of company and market share, supply of raw material and

marketing arrangements, bargaining power of issuers, suppliers as well

as customers, and location advantages and disadvantages available to

the business of the issuer.

Financial Risk: It includes analysis of financial management, capital

structure, cash flow adequacy and profitability as well as liquidity

position of the company. The financial risk is evaluated by CARE by

considering various ratios including, Growth in total Income, Profit after

Tax/Total Income, Profit before Depreciation Interest and Tax/ Total

Income, Return on Capital Employed, Return on Net Worth, Debt-Equity

Ratio, Interest Coverage Ratio, Overall Gearing Ratio, Current Ratio,

Quick Ratio and Average Collection Period.

Management Assessment: CARE makes complete assessment of the

background and history of the issuer, corporate strategy adopted,

philosophy and quality of management and the strength of management

capabilities under stress.

Terms of Instrument: Rating also depends on such factors as maturity

of instrument, nature of security (whether secured or unsecured),

repayment terms, coupon rates, etc. So, CARE also considers all these

things before the assignment of rating.

5.7.4 FITCH Rating Methodology: FITCH rating analysis involves the

assessment of the following:

Past Years’ Rating Methodology: While assigning ratings FITCH takes

into account last few years‟ rating methodology on the basis of which

rating was done.

Past Years’ Financial Data: The ratios considered by FITCH while

evaluating the past years‟ financial data include, Profit Before

Depreciation Interest and Tax/ Total Income, Profit after Tax/Total

Income, Return on Capital Employed, Return on Net Worth, Operating

126

Profit/ Profit after Tax, Working Capital Turnover Ratio, Average

Collection Period, Debt-Equity Ratio, Interest Coverage Ratio, Current

Ratio and Quick Ratio.

Forecast of Future Performance: It means how much the business will

be able to earn in future which will be helpful in repayment of principal

amount borrowed and interest thereof.

Comparison of Company’s Performance with the Competitors: Under

this the agency compares the performance of the company being rated

with that of the competitors in the field to properly assess the relative

standing of the company.

Analysis of Company’s Ability to Generate Cash from Operations:

The Company‟s ability to generate cash in future is also assessed by the

agency to find out the relative capability of the business to repay its

obligations in time.

5.8 RATING SYMBOLS

A credit rating compresses an enormous amount of diverse

information into a single rating symbol. Rating symbols are symbolic

expression of an issuer‟s ability to respond to adverse changes in

circumstances and economic conditions. Rating symbols are indicators of

the opinion/assessment of credit rating agency regarding credit quality or

grade of the debt obligations or instruments. Rating symbols group together

similar entities in terms of their relative capacity of timely servicing of

obligations as per terms of contract. The suffixes plus (+) or minus (-) are

added to the symbols to indicate the relative position of the instrument

within the group covered by the symbol. Currently, rating agencies have

standardized rating nomenclatures for long-term ratings, short-term

instruments, medium-term ratings, corporate/issuer credit rating, claims

paying ability of insurance companies, IPO grading, etc. The comparative

analysis of the symbols used by various credit rating agencies is shown in

Tables 5.4a to 5.4j.

127

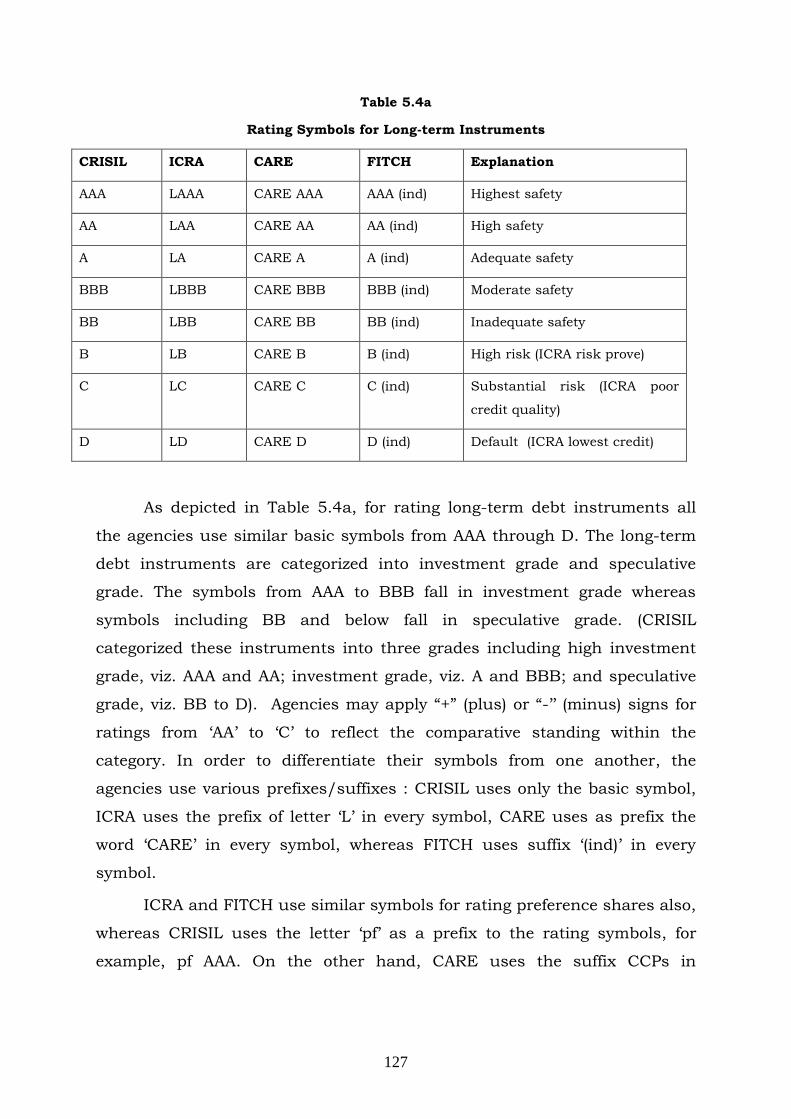

Table 5.4a

Rating Symbols for Long-term Instruments

CRISIL ICRA CARE FITCH Explanation

AAA LAAA CARE AAA AAA (ind) Highest safety

AA LAA CARE AA AA (ind) High safety

A LA CARE A A (ind) Adequate safety

BBB LBBB CARE BBB BBB (ind) Moderate safety

BB LBB CARE BB BB (ind) Inadequate safety

B LB CARE B B (ind) High risk (ICRA risk prove)

C LC CARE C C (ind) Substantial risk (ICRA poor

credit quality)

D LD CARE D D (ind) Default (ICRA lowest credit)

As depicted in Table 5.4a, for rating long-term debt instruments all

the agencies use similar basic symbols from AAA through D. The long-term

debt instruments are categorized into investment grade and speculative

grade. The symbols from AAA to BBB fall in investment grade whereas

symbols including BB and below fall in speculative grade. (CRISIL

categorized these instruments into three grades including high investment

grade, viz. AAA and AA; investment grade, viz. A and BBB; and speculative

grade, viz. BB to D). Agencies may apply “+” (plus) or “-‟‟ (minus) signs for

ratings from „AA‟ to „C‟ to reflect the comparative standing within the

category. In order to differentiate their symbols from one another, the

agencies use various prefixes/suffixes : CRISIL uses only the basic symbol,

ICRA uses the prefix of letter „L‟ in every symbol, CARE uses as prefix the

word „CARE‟ in every symbol, whereas FITCH uses suffix „(ind)‟ in every

symbol.

ICRA and FITCH use similar symbols for rating preference shares also,

whereas CRISIL uses the letter „pf‟ as a prefix to the rating symbols, for

example, pf AAA. On the other hand, CARE uses the suffix CCPs in

128

parentheses along with the symbol given above for rating cumulative

convertible preference shares, for example, CARE AAA (CCPs).

Table 5.4b

Rating Symbols for Medium-term Instruments

CRISIL ICRA CARE FITCH Explanation

FAAA MAAA CARE AAA (FD)/(CD) tAAA (ind) Highest safety

FAA MAA CARE AA(FD)/(CD) tAA (ind) High safety

FA MA CARE A(FD)/(CD) tA(ind) Adequate safety

-- -- CARE BBB(FD)/(CD) -- Sufficient safety(CARE only)

-- -- CARE BB(FD)/(CD) -- Inadequate safety(CARE only)

FB MB CARE B(FD)/(CD) tB (ind) Inadequate safety(CARE

susceptible to default)

FC MC CARE C(FD)/(CD) tC (ind) High risk

FD MD CARE D(FD)/(CD) tD (ind) Default

Table 5.4b highlights that for rating medium-term instruments, the

basic symbols used by CRISIL, ICRA and FITCH are AAA, AA, A, B C and D,

whereas CARE‟s symbols range through AAA, AA, A, BBB, BB, B, C and D.

The letter „F‟ is prefixed by CRISIL for rating fixed deposits of companies

whereas for rating certificates of deposit, CRISIL uses the similar symbols as

used by it for rating short-term instruments, i.e., ranging through P1 to P5.

The letter „M‟ is used by ICRA as a prefix for rating medium-term

instruments. CARE uses as prefix the word „CARE‟ and the word „FD‟ and

„CD‟ in parentheses as a suffix for rating fixed deposits and certificates of

deposit respectively. FITCH uses the letter „t‟ as a prefix and „(ind)‟ as a

suffix for rating all medium-term instruments.

As is evident from Table 5.4c, for rating short-term instruments the

basic parameter in the form of a five-point scale ranging from 1 to 5 is

similar for all the agencies but different prefixes are used by all the agencies

under study as CRISIL uses letter „P‟, ICRA uses the letter „A‟, CARE uses

PR, and FITCH uses the suffix „(ind)‟.

129

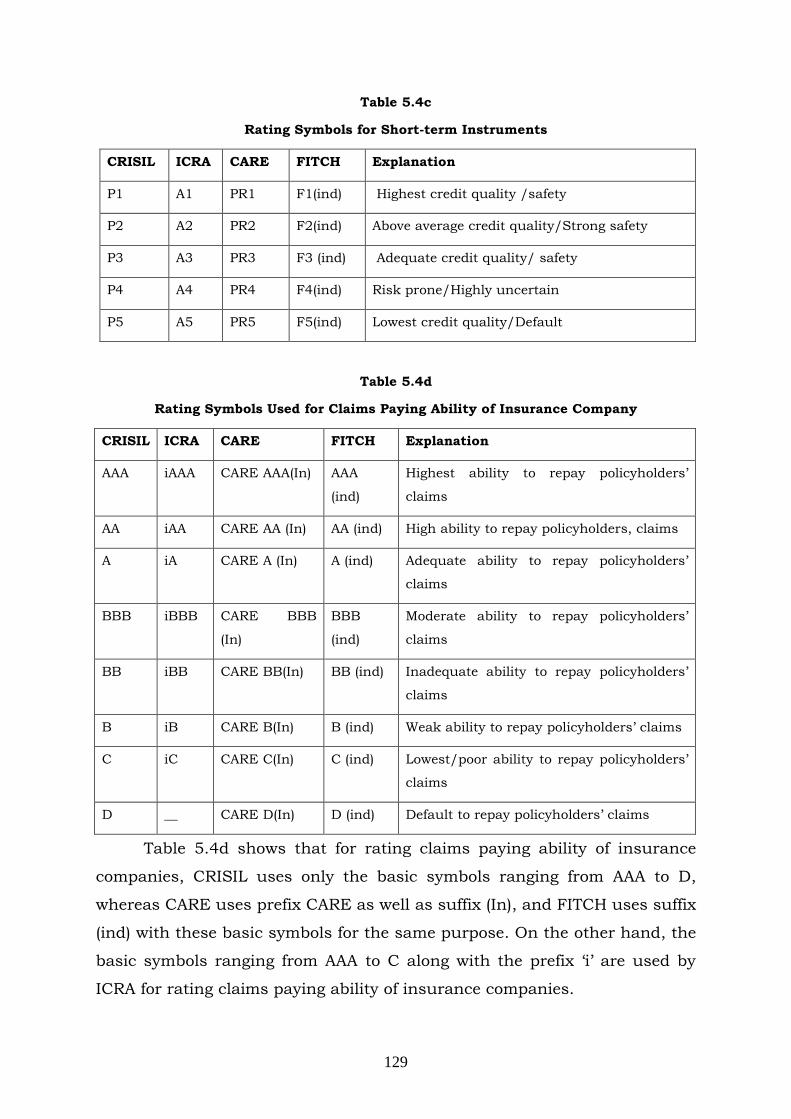

Table 5.4c

Rating Symbols for Short-term Instruments

CRISIL ICRA CARE FITCH Explanation

P1 A1 PR1 F1(ind) Highest credit quality /safety

P2 A2 PR2 F2(ind) Above average credit quality/Strong safety

P3 A3 PR3 F3 (ind) Adequate credit quality/ safety

P4 A4 PR4 F4(ind) Risk prone/Highly uncertain

P5 A5 PR5 F5(ind) Lowest credit quality/Default

Table 5.4d

Rating Symbols Used for Claims Paying Ability of Insurance Company

CRISIL ICRA CARE FITCH Explanation

AAA iAAA CARE AAA(In) AAA

(ind)

Highest ability to repay policyholders‟

claims

AA iAA CARE AA (In) AA (ind) High ability to repay policyholders, claims

A iA CARE A (In) A (ind) Adequate ability to repay policyholders‟

claims

BBB iBBB CARE BBB

(In)

BBB

(ind)

Moderate ability to repay policyholders‟

claims

BB iBB CARE BB(In) BB (ind) Inadequate ability to repay policyholders‟

claims

B iB CARE B(In) B (ind) Weak ability to repay policyholders‟ claims

C iC CARE C(In) C (ind) Lowest/poor ability to repay policyholders‟

claims

D __ CARE D(In) D (ind) Default to repay policyholders‟ claims

Table 5.4d shows that for rating claims paying ability of insurance

companies, CRISIL uses only the basic symbols ranging from AAA to D,

whereas CARE uses prefix CARE as well as suffix (In), and FITCH uses suffix

(ind) with these basic symbols for the same purpose. On the other hand, the

basic symbols ranging from AAA to C along with the prefix „i‟ are used by

ICRA for rating claims paying ability of insurance companies.

130

Table 5.4e

Rating Symbols Used for Mutual Funds Grading

CRISIL ICRA CARE FITCH Explanation

AAAf mfAAA CARE AAAf AAA (ind) Minimal credit risk

AAf mfAA CARE AAf AA (ind) Very low credit risk

Af mfA CARE Af A (ind) Low credit risk

BBBf mfBBB CARE BBBf BBB (ind) Moderate credit risk

BBf mfBB CARE BBf BB (ind) High credit risk

Bf mfB CARE Bf B (ind) Very high credit risk

Cf mfC CARE Cf C (ind) Extremely higher credit risk

It is clear from Table 5.4e that for grading of mutual funds, along with

basic symbols ranging from AAA through C, CRISIL uses suffix „f‟, ICRA uses

prefix „mf‟, CARE uses prefix CARE as well as suffix „f‟, whereas FITCH uses

suffix (ind) for the purpose.

Table 5.4f mentions that for rating the issuers, CRISIL again uses the

basic symbols ranging from AAA to C. ICRA uses the prefix „Ir‟; CARE

prefixes the word „CARE‟ and suffixes (Is) to the basic symbol; and FITCH

uses the suffix (ind). It is also evident from the table that the basic symbols

used by CARE range from AAA to D.

131

Table 5.4f

Rating Symbols Used for Issuer Credit Rating

CRISIL ICRA CARE FITCH Explanation

AAA IrAAA CARE AAA(Is) AAA(ind) Extremely strong capacity to

meet financial commitments

AA IrAA CARE AA(Is) AA(ind) Very strong capacity to meet

financial commitments

A IrA CARE A(Is) A(ind) Strong capacity to meet

financial commitments

BBB IrBBB CARE BBB(Is) BBB(ind) Adequate capacity to meet

financial commitments

BB IrBB CARE BB(Is) BB(ind) Inadequate capacity to meet

financial commitments

B IrB CARE B(Is) B(ind) Risk-prone capacity to meet

financial commitments

CCC/C

C/C

IrC CARE C(Is) CCC(ind)/CC(in

d)/C(ind)

Lowest capacity to meet

financial commitments

__ __ CARE D(Is) __ Likely to default

Table 5.4g

IPO Grading Symbols

CRISIL ICRA CARE FITCH Explanation

5/5 IPO Grade 5 CARE IPO Grade 5 FITCH IPO

Grade 5(ind)

Strong Fundamentals of the

issuers concerned

4/5 IPO Grade 4 CARE IPO Grade 4 FITCH IPO

Grade 4(ind)

Above average fundamentals

of the issuers concerned

3/5 IPO Grade 3 CARE IPO Grade 3 FITCH IPO

Grade 3(ind)

Average fundamentals of the

issuers concerned

2/5 IPO Grade 2 CARE IPO Grade 2 FITCH IPO

Grade 2(ind)

Below average fundamentals

of the issuers concerned

1/5 IPO Grade 1 CARE IPO Grade 1 FITCH IPO

Grade 1(ind)

Poor fundamentals of the

issuers concerned

132

Table 5.4g reveals that the IPO grades are assigned on a five-point

scale ranging from 5 to 1. CRISIL uses the numerical symbol ranging from

5/5 (denoted as five on five) to 1/5 (denoted as one on five). ICRA‟s 5-point

IPO grade ranges from „IPO Grade 5‟ to „IPO Grade 1‟, whereas CARE uses

the prefix of word „CARE‟ with each symbol used by ICRA. Moreover, FITCH

also uses the similar symbols as used by ICRA but with slight modification

as it uses word „FITCH‟ as prefix and „(ind)‟ as suffix to each grade.

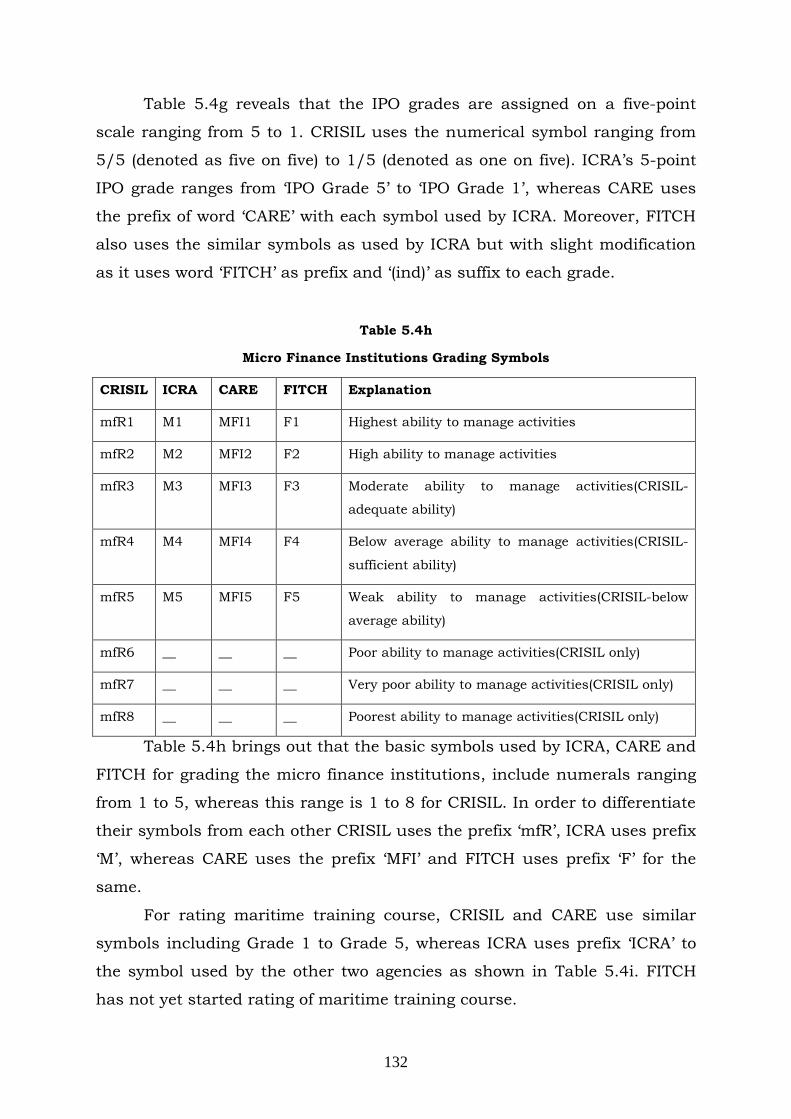

Table 5.4h

Micro Finance Institutions Grading Symbols

CRISIL ICRA CARE FITCH Explanation

mfR1 M1 MFI1 F1 Highest ability to manage activities

mfR2 M2 MFI2 F2 High ability to manage activities

mfR3 M3 MFI3 F3 Moderate ability to manage activities(CRISIL-

adequate ability)

mfR4 M4 MFI4 F4 Below average ability to manage activities(CRISIL-

sufficient ability)

mfR5 M5 MFI5 F5 Weak ability to manage activities(CRISIL-below

average ability)

mfR6 __ __ __ Poor ability to manage activities(CRISIL only)

mfR7 __ __ __ Very poor ability to manage activities(CRISIL only)

mfR8 __ __ __ Poorest ability to manage activities(CRISIL only)

Table 5.4h brings out that the basic symbols used by ICRA, CARE and

FITCH for grading the micro finance institutions, include numerals ranging

from 1 to 5, whereas this range is 1 to 8 for CRISIL. In order to differentiate

their symbols from each other CRISIL uses the prefix „mfR‟, ICRA uses prefix

„M‟, whereas CARE uses the prefix „MFI‟ and FITCH uses prefix „F‟ for the

same.

For rating maritime training course, CRISIL and CARE use similar

symbols including Grade 1 to Grade 5, whereas ICRA uses prefix „ICRA‟ to

the symbol used by the other two agencies as shown in Table 5.4i. FITCH

has not yet started rating of maritime training course.

133

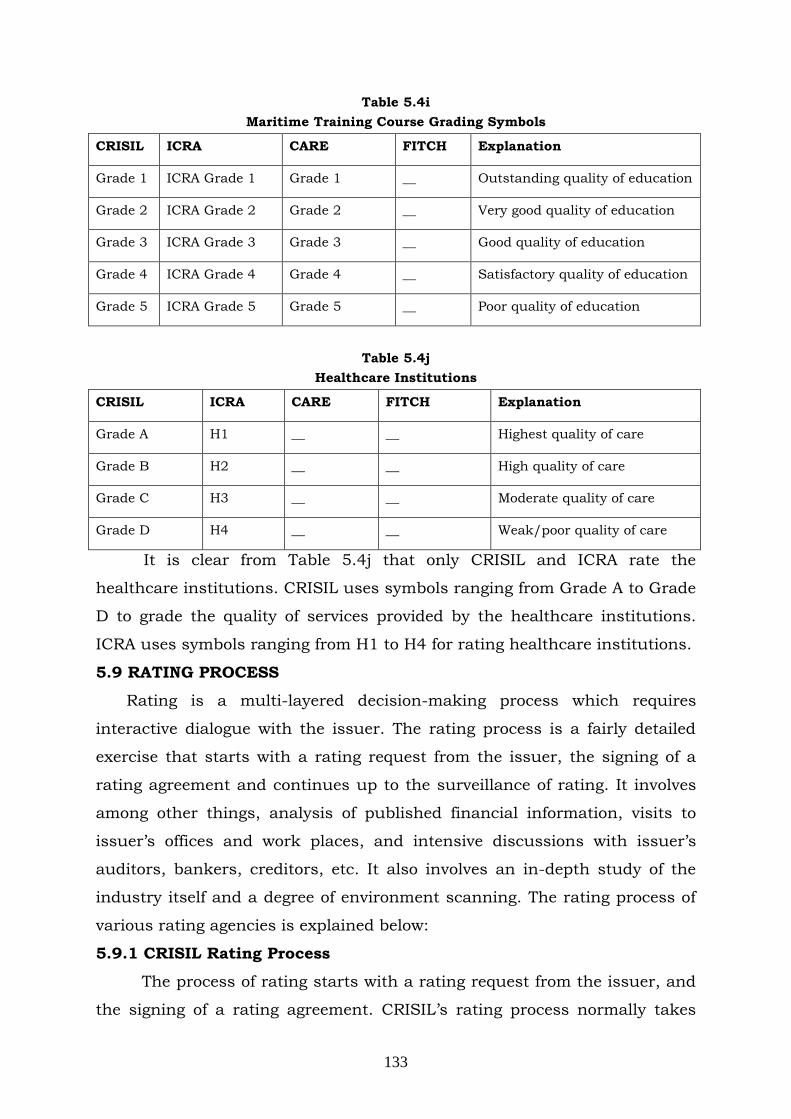

Table 5.4i

Maritime Training Course Grading Symbols

CRISIL ICRA CARE FITCH Explanation

Grade 1 ICRA Grade 1 Grade 1 __ Outstanding quality of education

Grade 2 ICRA Grade 2 Grade 2 __ Very good quality of education

Grade 3 ICRA Grade 3 Grade 3 __ Good quality of education

Grade 4 ICRA Grade 4 Grade 4 __ Satisfactory quality of education

Grade 5 ICRA Grade 5 Grade 5 __ Poor quality of education

Table 5.4j

Healthcare Institutions

CRISIL ICRA CARE FITCH Explanation

Grade A H1 __ __ Highest quality of care

Grade B H2 __ __ High quality of care

Grade C H3 __ __ Moderate quality of care

Grade D H4 __ __ Weak/poor quality of care

It is clear from Table 5.4j that only CRISIL and ICRA rate the

healthcare institutions. CRISIL uses symbols ranging from Grade A to Grade

D to grade the quality of services provided by the healthcare institutions.

ICRA uses symbols ranging from H1 to H4 for rating healthcare institutions.

5.9 RATING PROCESS

Rating is a multi-layered decision-making process which requires

interactive dialogue with the issuer. The rating process is a fairly detailed

exercise that starts with a rating request from the issuer, the signing of a

rating agreement and continues up to the surveillance of rating. It involves

among other things, analysis of published financial information, visits to

issuer‟s offices and work places, and intensive discussions with issuer‟s

auditors, bankers, creditors, etc. It also involves an in-depth study of the

industry itself and a degree of environment scanning. The rating process of

various rating agencies is explained below:

5.9.1 CRISIL Rating Process

The process of rating starts with a rating request from the issuer, and

the signing of a rating agreement. CRISIL‟s rating process normally takes

134

three to four weeks. However, rating can be arrived at shorter timeframes, to

meet urgent requirements. The CRISIL rating process includes the following

steps:

1. Request for Rating: The rating process starts with the issuer‟s request

for rating. Then the rating agreement is signed between the client and the

rating agency. The rating agency assigns a rating team for the purpose,

and the client provides the relevant information to the rating team along

with the rating fees.

2. Analysis of Information: The rating team conducts the preliminary

analysis of the information provided by the client. The team also

conducts the site visits for the purpose of analysis.

3. Meeting: Then the meetings between the rating team and management of

the issuer are conducted and the rating team does the final analysis of

the information after clarification of any doubts in the management

meeting.

4. Assignment of Rating: The rating team presents its analysis to the

rating committee which assigns the rating to the given instrument and

communicates the same to the issuer. The rating is then accepted by the

issuer or the issuer may appeal the rating agency to further refine the

rating.

5. Dissemination of Rating: In case the rating is accepted by the issuer it

is disseminated to CRISIL's subscriber base, and to the local and

international news media. Rating information is also updated on line on

the website of rating agency.

6. Continuous Surveillance: All ratings are kept under continuous

surveillance throughout its validity by the rating agency.

5.9.2 ICRA Rating Process

The Rating involves assessment of a number of qualitative factors

with a view to estimating the future earnings of the issuer. This requires

extensive interactions with the issuer‟s management, specifically on subjects

relating to plans, outlook, competitive position, and funding policies. Thus,

the following steps are included in the ICRA rating process:

135

1. Formal Request for Rating: ICRA‟s rating process is initiated on receipt

of a formal request (or mandate) from the prospective issuer.

2. Setting of Rating Team and Analysis of Information: A Rating team,

which usually consists of two analysts with the expertise and skills

required to evaluate the business of the issuer, is involved with the

Rating assignment. An issuer is provided a list of information

requirements and the broad framework for discussions. Then the Rating

team analyzes that information.

3. Interaction with the Management of the Issuer: Then there are

extensive interactions between Rating Team and the issuer‟s

management, specifically on subjects relating to plans, outlook,

competitive position, and funding policies. In some cases where the

agency finds it necessary, the site visits may be done by the rating team

for proper analysis of information.

4. Preparation of Rating Report: After completing the analysis, a Rating

Report is prepared by the Rating Team, which is then presented to the

ICRA Rating Committee. A presentation on the issuer‟s business and

management is also made by the Rating Team.

5. Assignment of Rating: The Rating Committee which is the final

authority for assigning Ratings assigns the rating. The assigned Rating,

along with the key issues, is communicated to the issuer‟s top

management for acceptance. Non-accepted Ratings are not disclosed and

complete confidentiality is maintained on them unless such disclosure is

required under any laws/regulations.

6. Review of Ratings: If the issuer does not find the Rating acceptable, it

has a right to appeal for a review. Such reviews are usually taken up if

the issuer provides certain fresh inputs. During a review, the issuer‟s

response is presented to the Rating Committee. If the inputs and/or fresh

clarifications so warrant, the Rating Committee would revise the initial

Rating decision.

7. Mandatory Surveillance: As part of a mandatory surveillance process,

ICRA monitors all accepted Ratings over the tenure of the Rated

instruments. The Ratings are generally reviewed once every year, unless

136

the circumstances of the case warrant an earlier review. The Rating

outstanding may be retained or revised (that is, upgraded or downgraded)

on surveillance.

5.9.3 CARE Rating Process

CARE rating process largely depends on the flow of information from

client. Rating decisions are made by rating committee. The CARE rating

process includes the following steps:

1. Request for Rating and Assignment of Rating Team: The client

requests the agency for rating and after signing of agreement between

both a rating team is assigned for the purpose by the rating agency.

2. Analysis of Information: The client is required to submit information

and detailed schedules and proper analysis of that information is done by

the agency.

3. Interaction with the Client: After the analysis of data by the rating

team, the team interacts with the client, and the client responds to the

queries raised by the team and provides the additional data as required

by the team. Further, the team undertakes the site visits and analyzes

the additional data submitted by the client.

4. Assignment of Rating: The internal committee of rating agency reviews

the analysis and then the Rating committee assigns rating to the client.

The rating so assigned is communicated to the client. The client may

then accept the rating or it may ask for review of rating in which case the

client has to furnish additional information for the purpose.

5. Publishing of Rating: In case the client accepts the rating then the

rating agency will give the notification about such rating in the press,

otherwise CARE will not publish the rating.

6. Review of Rating: Each rating is then reviewed formally at least once a

year when the analyst of rating agency meets the issuer‟s management.

5.9.4 FITCH Rating Process

The FITCH rating process includes the following steps:

137

1. Rating Agreement Signed: The rating agreement is signed between the

rating agency and the entity wanting to get its instrument rated.

2. Review of Publicly Available Information: FITCH‟s analysis and rating

decisions are based on information received from sources known to it and

believed by FITCH to be relevant to the analysis and rating decision. This

includes publicly available information on the issuer, such as company

financial and operational statistics, reports filed with regulatory agencies,

and industry and economic reports. In addition, the rating process may

incorporate data and insight gathered by analysts in the course of their

interaction with other entities across their sector of expertise.

3. Questions Sent to Issuer: In addition to review of publicly available

information the rating agency needs to ask certain special questions from

the issuer in order to get out the information (that is not available

otherwise) about the instrument. The issuers are required to reply within

the stipulated period and that too before the management meeting.

4. Management Meeting: After having received the replies from the issuers,

the rating agency conducts the meeting with the management to discuss

the relevance of information collected about particular instrument.