omnichannel reality check

TRANSCRIPT

0 Copyright 2015 FUJITSU

Human Centric Innovation

in Action

Fujitsu Forum 2015

18th – 19th November

1 Copyright 2015 FUJITSU

Omni-Channel Reality Check

Richard Clarke Vice President, Global Retail

Nick Mayes Principal Analyst, Pierre Audoin Consultants (PAC)

2 Copyright 2015 FUJITSU

Agenda

Key Messages

Fujitsu in Global Retail

Retail Disruptors and the Connected Store

Omni-Channel Research Findings – PAC

Q&A

3 Copyright 2015 FUJITSU

Key Messages

4 Copyright 2015 FUJITSU

Key Messages

Markets developing at different rates and no textbook solution roadmap

Physical store is not going away but will be an investment focus

Not just a front office play, plenty of heavy lifting in the back office to deliver results

5 Copyright 2015 FUJITSU

Fujitsu in Retail – at a glance

Revenue

$1.7bn

Solutions

Retail R&D/Innovation

>$45m

Years

>35

Global Retail Team

8,000

Countries

52 Analytics

Omni-channel Self Service

ICT Services

Customers

>500

PoS

6 Copyright 2015 FUJITSU

Connected Retail – our Mission

Globally Delivered

Retail Innovation

Connected Enterprise

STRATEGY CAPABILITY OUTCOME

Retail products, software, and services

Fujitsu IP and Japanese technology

Omni-channel, self-service, mobile

30+ years innovating in retail

Infrastructure, applications, networks

Integrated store solutions

Connecting front and back office

Multi-vendor management

Global solutions, local features

Global expertise, local delivery

Global Solution and Delivery Centers DIFFERENTIATED CUSTOMER EXPERIENCE

7 Copyright 2015 FUJITSU

Who we work with globally

EMEA Japan & Asia Americas

Oceania

8 Copyright 2015 FUJITSU

Case Studies

Large Fashion Retailer

End to end retail IT services in 800 UK and some 300 global stores; Fujitsu provides store IT support and maintenance including PoS application; service desk, desktop and payments

Fujitsu developed Total Managed Store – seamless and repeatable catalogue-based solutions and services stack

RFID solution – shipping, packaging, inventory and PoS in 150 stores in Japan

Front office transformation – 1700 stores in France and 10 other countries; self checkout, hybrid self service, scan and pay

Omni-channel retailing – 1450 stores in US/Canada; pos, mobile and omni-channel enablement;

9 Copyright 2015 FUJITSU

Retail industry disruptors

1. Physical and on line stores will merge

2. Smartphone will be the “shop in your hand”

3. Retailers will sell services and ship products

4. Personalisation will be the new normal

5. Retail will be global

6. Cost models will change

7. IT will no longer own IT

10 Copyright 2015 FUJITSU

Connected Store…the next big thing

‘Connected Store’ will be the next big thing in retail – it is about

connecting up online and offline worlds to redefine the ‘store’,

transform the shopping experience and improve retail operations.

Online Mobile Store

Connected Store Tomorrow Retailing Today

Transactional, in and out, experience

Easy Ordering (click ‘n’ collect) growing but still limited

Limited connection between ‘online’ and ‘offline’ shopping

o Online = speed, availability and personalisation on line

o Offline = anonymous/functional transaction with limited availability

Retailer, not customer, in control – stock, space, payment, fulfilment

Fixed, not mobile, shopping processes and environment

In store experience variable (queuing, customer recognition, service levels)

Omni channel transformation

11 Copyright 2015 FUJITSU

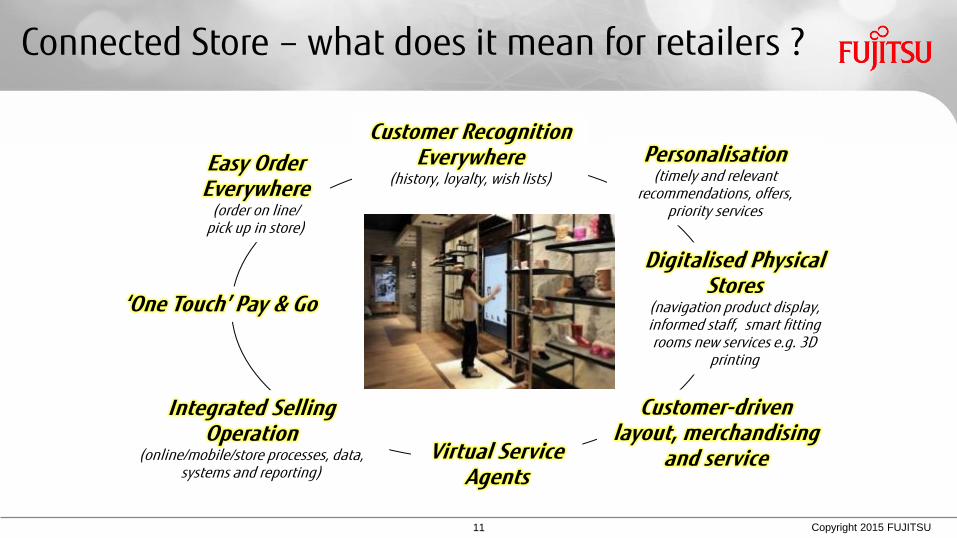

Connected Store – what does it mean for retailers ?

Customer Recognition Everywhere

(history, loyalty, wish lists)

Personalisation (timely and relevant

recommendations, offers, priority services

Virtual Service Agents

‘One Touch’ Pay & Go

Integrated Selling Operation

(online/mobile/store processes, data, systems and reporting)

Customer-driven layout, merchandising

and service

Easy Order Everywhere

(order on line/ pick up in store)

Digitalised Physical Stores

(navigation product display, informed staff, smart fitting rooms new services e.g. 3D

printing

12 Copyright 2015 FUJITSU

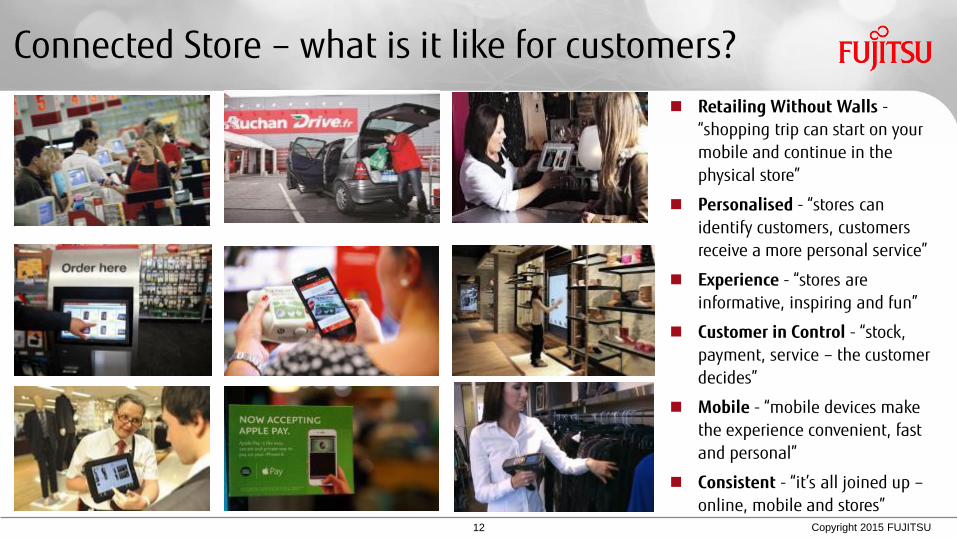

Connected Store – what is it like for customers?

Retailing Without Walls -“shopping trip can start on your mobile and continue in the physical store”

Personalised - “stores can

identify customers, customers receive a more personal service”

Experience - “stores are informative, inspiring and fun”

Customer in Control - “stock, payment, service – the customer decides”

Mobile - “mobile devices make the experience convenient, fast

and personal”

Consistent - “it’s all joined up – online, mobile and stores”

© PAC 2015

Omnichannel Retail in Europe Strategies, Challenges & Measuring Success

© PAC

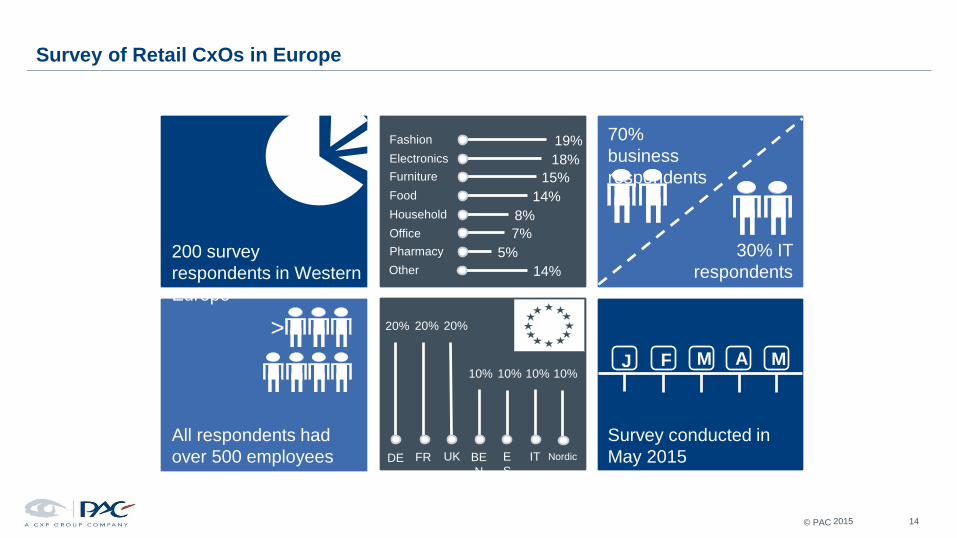

Survey of Retail CxOs in Europe

14 2015

200 survey

respondents in Western

Europe

70%

business

respondents

30% IT

respondents

FR

Survey conducted in

May 2015

All respondents had

over 500 employees

Fashion 19%

DE UK

> 20% 20% 20%

10%

Nordic E

S

J F M A M 10% 10% 10%

IT BE

N

Electronics 18% Furniture 15%

Food 14%

Household 8%

7%

Pharmacy 5%

Office

Other 14%

© PAC

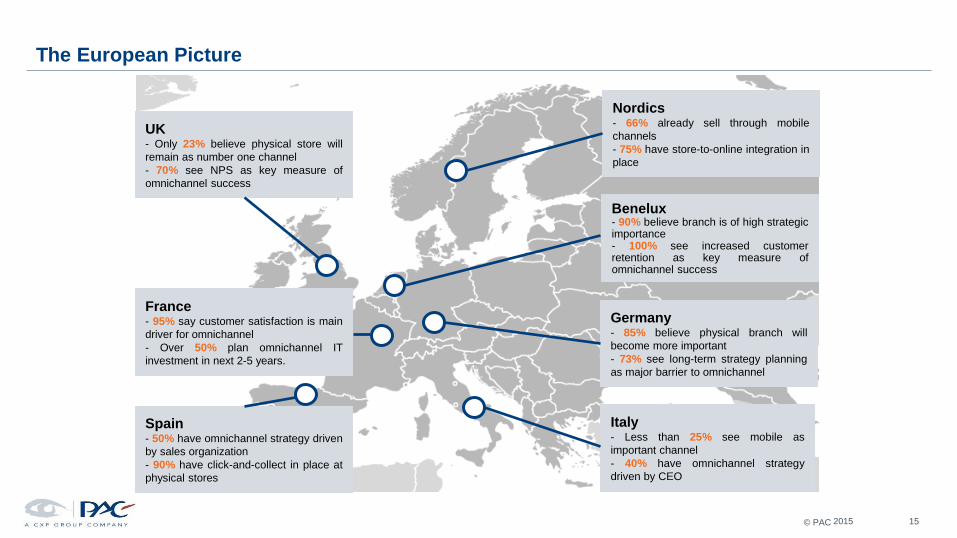

The European Picture

2015 15

UK - Only 23% believe physical store will

remain as number one channel

- 70% see NPS as key measure of

omnichannel success

Nordics - 66% already sell through mobile

channels

- 75% have store-to-online integration in

place

Spain - 50% have omnichannel strategy driven

by sales organization

- 90% have click-and-collect in place at

physical stores

Italy - Less than 25% see mobile as

important channel

- 40% have omnichannel strategy

driven by CEO

France - 95% say customer satisfaction is main

driver for omnichannel

- Over 50% plan omnichannel IT

investment in next 2-5 years.

Benelux - 90% believe branch is of high strategic importance - 100% see increased customer retention as key measure of omnichannel success

Germany - 85% believe physical branch will

become more important

- 73% see long-term strategy planning

as major barrier to omnichannel

© PAC

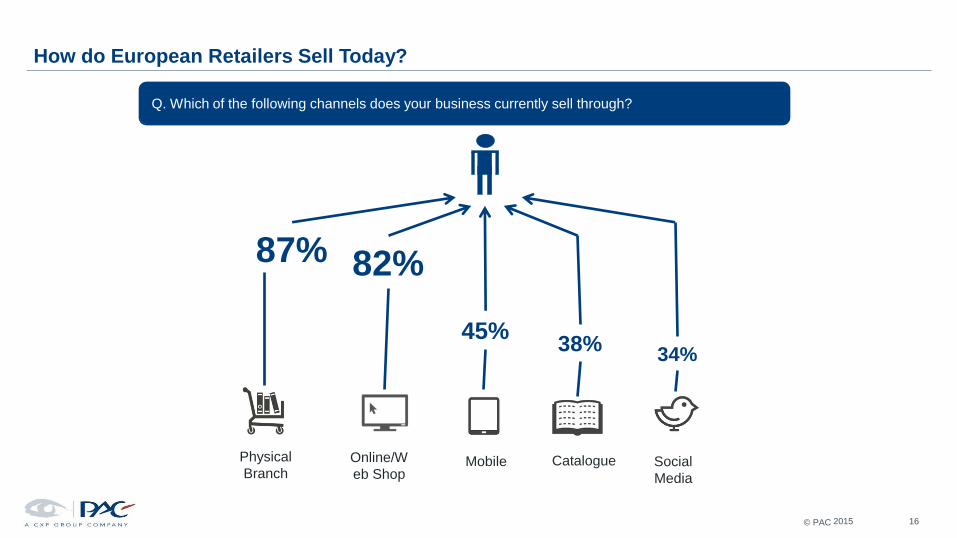

How do European Retailers Sell Today?

16 2015

Physical

Branch Online/W

eb Shop Mobile Catalogue Social

Media

87% 82%

45% 38%

34%

Q. Which of the following channels does your business currently sell through?

© PAC

Physical

Branch

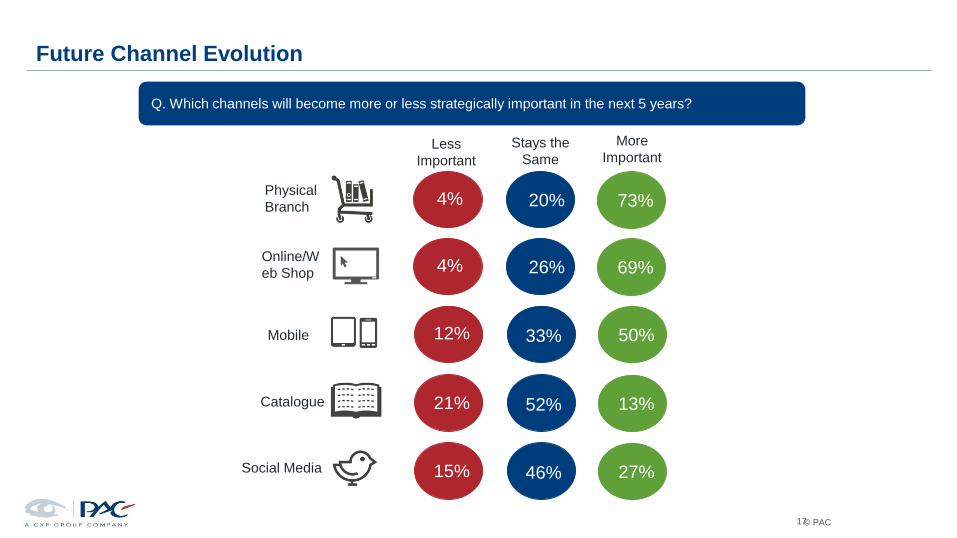

Future Channel Evolution

Online/W

eb Shop

Mobile

Catalogue

Social Media

Less

Important

Stays the

Same

More

Important

73% 20% 4%

69% 26% 4%

50%

13%

27%

33% 12%

52% 21%

46% 15%

17

Q. Which channels will become more or less strategically important in the next 5 years?

© PAC

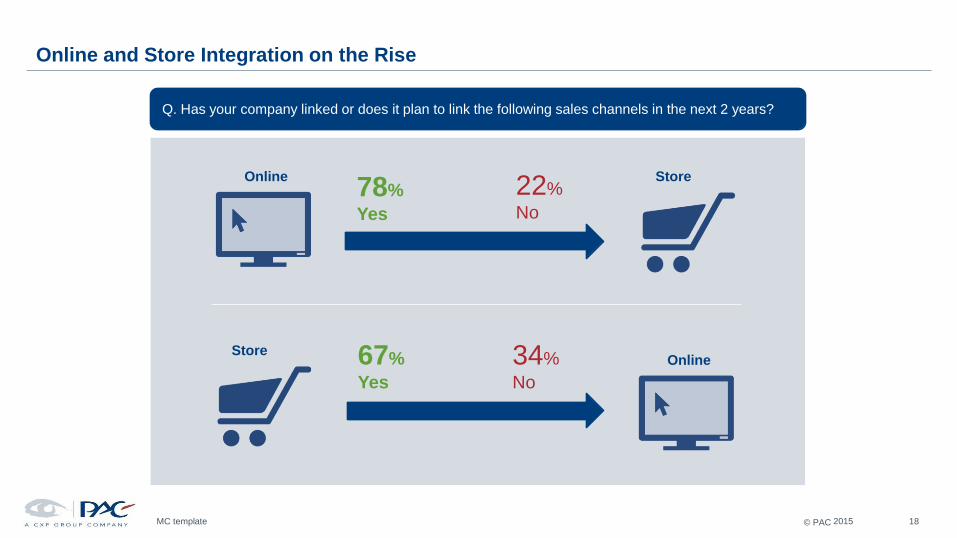

Online and Store Integration on the Rise

MC template 18 2015

78% Yes

22%

No

67%

Yes

34%

No

Online

Store

Store

Online

Q. Has your company linked or does it plan to link the following sales channels in the next 2 years?

© PAC

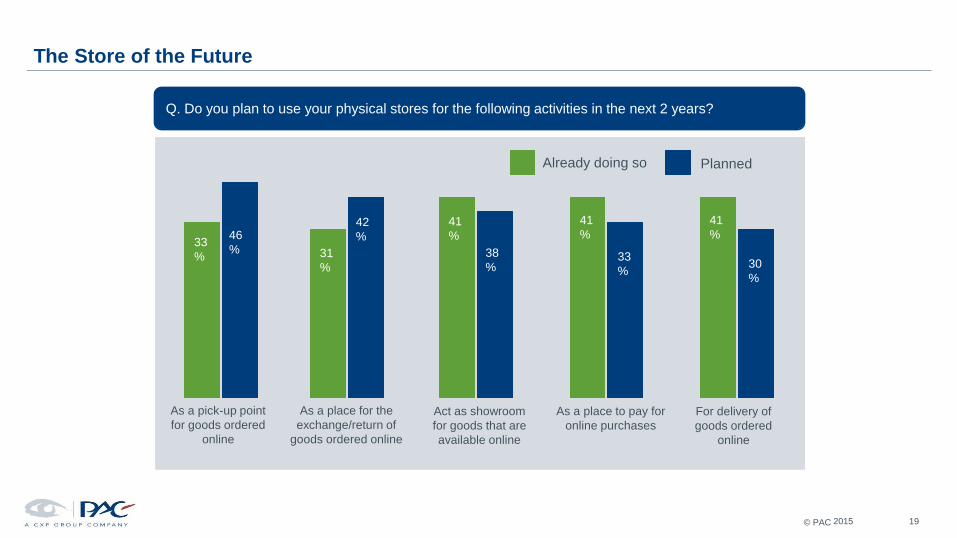

The Store of the Future

19 2015

Q. Do you plan to use your physical stores for the following activities in the next 2 years?

As a pick-up point

for goods ordered

online

As a place for the

exchange/return of

goods ordered online

Act as showroom

for goods that are

available online

As a place to pay for

online purchases

For delivery of

goods ordered

online

Already doing so Planned

33

%

46

% 31

%

42

%

41

%

38

%

41

%

33

%

41

%

30

%

© PAC

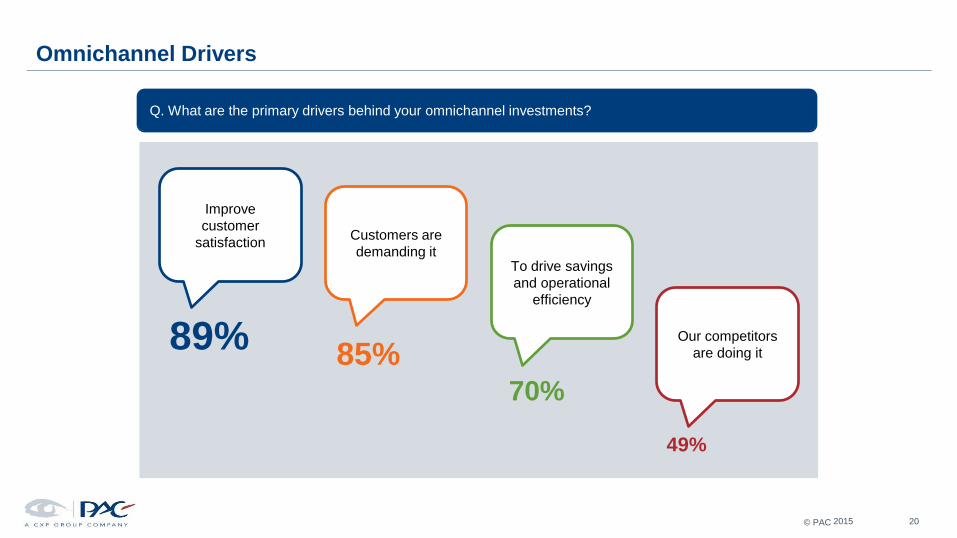

Omnichannel Drivers

20 2015

Customers are

demanding it

85%

Improve

customer

satisfaction

89%

To drive savings

and operational

efficiency

70%

Our competitors

are doing it

49%

Q. What are the primary drivers behind your omnichannel investments?

© PAC

Measuring Omni-Channel Success

21 2015

86%

Increased

Customer

Retention

Q. How do you measure the success of your omni-channel strategy?

Increased

New

Customer

Acquisition

Increase in

Net Promoter

Score

Reduction in

Customer

Effort Increase in

Brand Reach

84%

66%

73% 67%

© PAC

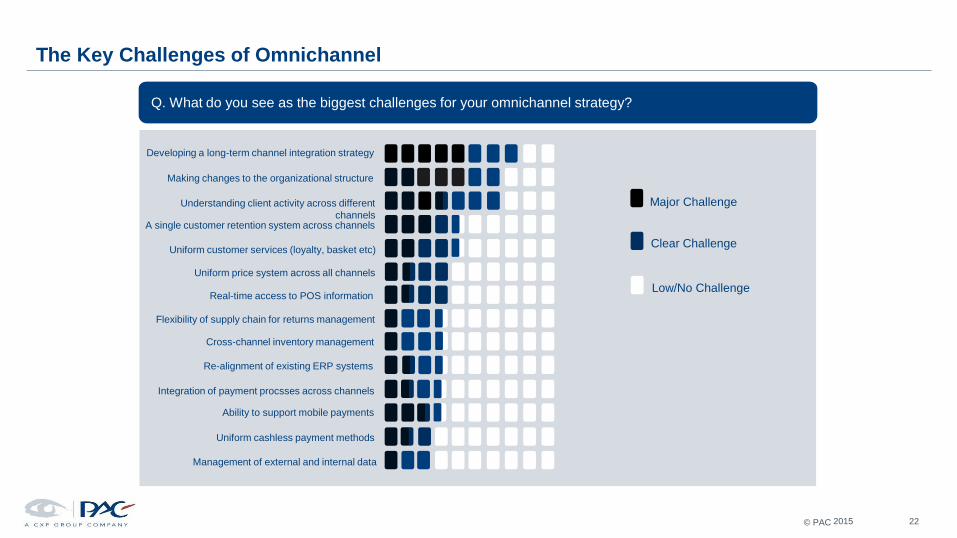

The Key Challenges of Omnichannel

22 2015

Major Challenge

Clear Challenge

Developing a long-term channel integration strategy

Making changes to the organizational structure

Integration of payment procsses across channels

Understanding client activity across different

channels

Real-time access to POS information

Uniform cashless payment methods

A single customer retention system across channels

Ability to support mobile payments

Cross-channel inventory management

Re-alignment of existing ERP systems

Low/No Challenge

Flexibility of supply chain for returns management

Management of external and internal data

Uniform price system across all channels

Uniform customer services (loyalty, basket etc)

Q. What do you see as the biggest challenges for your omnichannel strategy?

© PAC

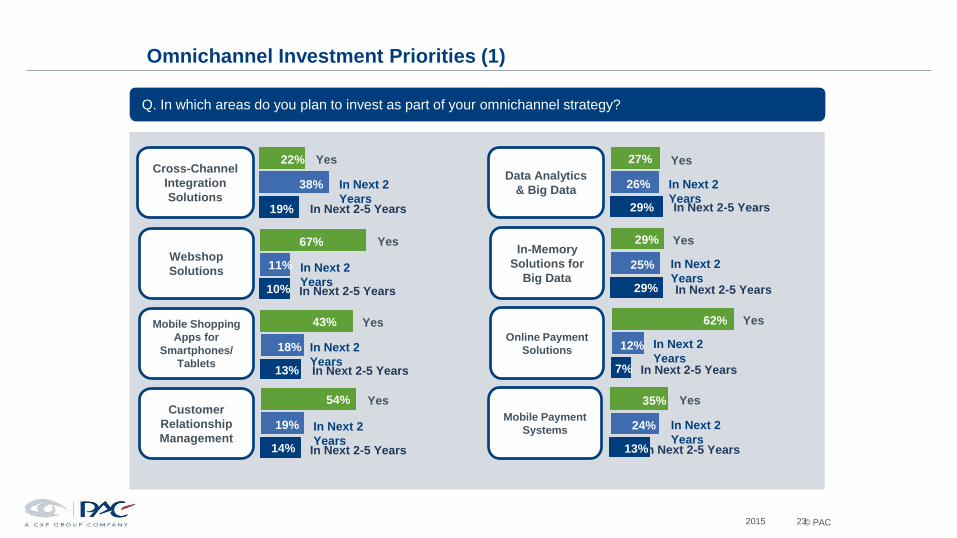

Omnichannel Investment Priorities (1)

23 2015

In Next 2

Years In Next 2-5 Years

Yes Cross-Channel

Integration

Solutions

Q. In which areas do you plan to invest as part of your omnichannel strategy?

Webshop

Solutions

Mobile Shopping

Apps for

Smartphones/

Tablets

Customer

Relationship

Management

Data Analytics

& Big Data

In-Memory

Solutions for

Big Data

Online Payment

Solutions

In Next 2

Years In Next 2-5 Years

Yes

In Next 2

Years In Next 2-5 Years

Yes

In Next 2

Years In Next 2-5 Years

Yes

In Next 2

Years In Next 2-5 Years

Yes

In Next 2

Years In Next 2-5 Years

Yes

In Next 2

Years In Next 2-5 Years

Yes

22%

38%

19%

67%

11%

10%

43%

18%

13%

54%

19%

14%

27%

26%

29%

29%

25%

29%

62%

12%

7%

Mobile Payment

Systems In Next 2

Years In Next 2-5 Years

Yes 35%

24%

13%

© PAC

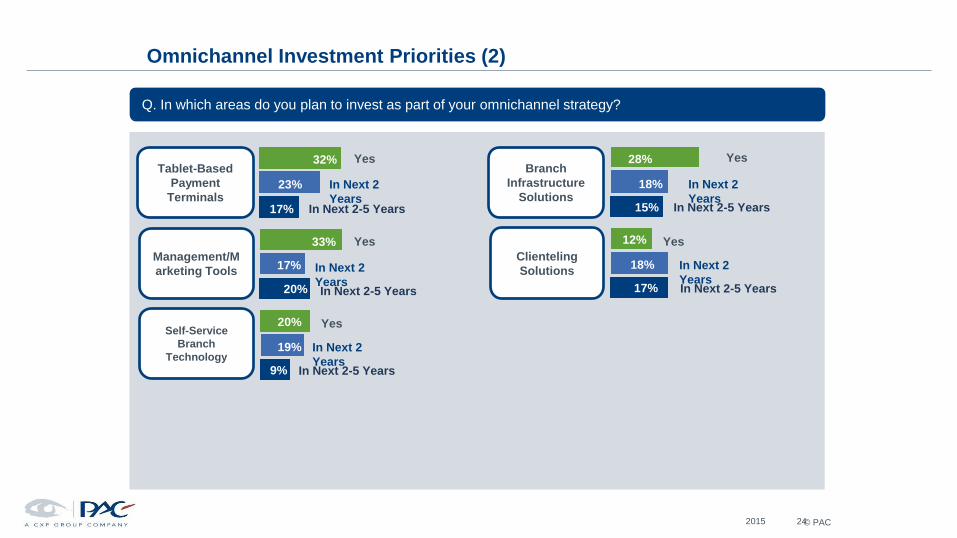

Omnichannel Investment Priorities (2)

24 2015

In Next 2

Years In Next 2-5 Years

Yes Tablet-Based

Payment

Terminals

Q. In which areas do you plan to invest as part of your omnichannel strategy?

Management/M

arketing Tools

Self-Service

Branch

Technology

Branch

Infrastructure

Solutions

Clienteling

Solutions In Next 2

Years In Next 2-5 Years

Yes

In Next 2

Years In Next 2-5 Years

Yes

In Next 2

Years In Next 2-5 Years

Yes

In Next 2

Years In Next 2-5 Years

Yes

32%

23%

17%

33%

17%

20%

20%

19%

9%

28%

18%

15%

12%

18%

17%

© PAC

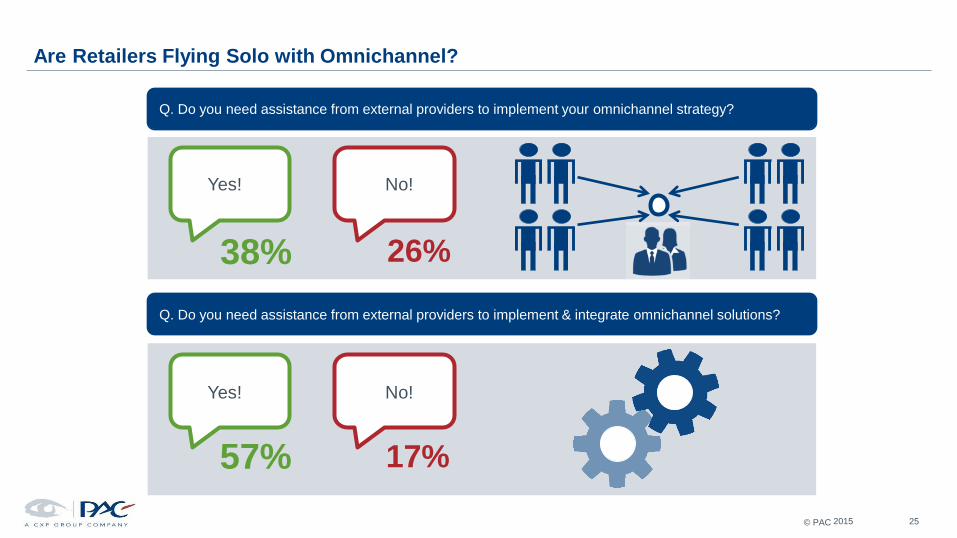

Are Retailers Flying Solo with Omnichannel?

25 2015

Q. Do you need assistance from external providers to implement your omnichannel strategy?

No! Yes!

38% 26%

Q. Do you need assistance from external providers to implement & integrate omnichannel solutions?

57% 17%

No! Yes!

© PAC

Contact

Founded in 1976, Pierre Audoin Consultants (PAC) is part of CXP Group, the leading independent European

research and consulting firm for the software, IT services and digital transformation industry.

CXP Group offers its customers comprehensive support services for the evaluation, selection and optimization of

their software solutions and for the evaluation and selection of IT services providers, and accompanies them in

optimizing their sourcing and investment strategies. As such, CXP Group supports ICT decision makers in their

digital transformation journey.

Further, CXP Group assists software and IT services providers in optimizing their strategies and go-to-market

approaches with quantitative and qualitative analyses as well as consulting services. Public organizations and

institutions equally base the development of their IT policies on our reports.

Capitalizing on 40 years of experience, based in 8 countries (with 17 offices worldwide) and with 140 employees,

CXP Group provides its expertise every year to more than 1,500 ICT decision makers and the operational divisions

of large enterprises as well as mid-market companies and their providers. CXP Group consists of three branches:

Le CXP, BARC (Business Application Research Center) and Pierre Audoin Consultants (PAC).

For more information please visit: www.pac-online.com

PAC’s latest news: www.pac-online.com/blog

Follow us on Twitter: @PAC_Consultants

Nick Mayes

Principal Analyst

+44 (0)20 7553 3968

2015 Omnichannel Retail in Europe - Strategies, Challenges & Measuring Success

27 Copyright 2015 FUJITSU

Key Messages

28 Copyright 2015 FUJITSU

Key Messages

Markets developing at different rates and no textbook solution roadmap

Physical store is not going away but will be an investment focus

Not just a front office play, plenty of heavy lifting in the back office to deliver results

29 Copyright 2015 FUJITSU

Omni-Channel Reality Check

Richard Clarke Vice President, Global Retail

Nick Mayes Principal Analyst, Pierre Audoin Consultants (PAC)

30 Copyright 2015 FUJITSU