oman - worldwide-tax-guide-oman 2012 pkf

DESCRIPTION

ÂTRANSCRIPT

OmanTax Guide

2012

PKF Worldwide Tax Guide 2012I

foreword

A country’s tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed?

Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. This handy reference guide provides clients and professional practitioners with comprehensive tax and business information for 100 countries throughout the world.

As you will appreciate, the production of the WWTG is a huge team effort and I would like to thank all tax experts within PFK member firms who gave up their time to contribute the vital information on their country’s taxes that forms the heart of this publication. I would also like thank Richard Jones, PKF (UK) LLP, Kevin Reilly, PKF Witt Mares, and Kaarji Vaughan, PKF Melbourne for co-ordinating and checking the entries from countries within their regions.

The WWTG continues to expand each year reflecting both the growth of the PKF network and the strength of the tax capability offered by member firms throughout the world.

I hope that the combination of the WWTG and assistance from your local PKF member firm will provide you with the advice you need to make the right decisions for your international business.

Jon HillsPKF (UK) LLPChairman, PKF International Tax Committee [email protected]

PKF Worldwide Tax Guide 2012 II

important disclaimer

This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication.

This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication.

The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication.

Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances.

PKF International is a network of legally independent member firms administered by PKF International Limited (PKFI). Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions on the part of any individual member firm or firms.

PKF Worldwide Tax Guide 2012III

preface

The PKF Worldwide Tax Guide 2012 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of 100 of the world’s most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current as of 30 September 2011, while also noting imminent changes where necessary.

On a country-by-country basis, each summary addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country’s personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments.

While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice.

In addition to the printed version of the WWTG, individual country taxation guides are available in PDF format which can be downloaded from the PKF website at www.pkf.com

PKF INTERNATIONAL LIMITEDAPRIL 2012

©PKF INTERNATIONAL LIMITEDALL RIGHTS RESERVEDUSE APPROVED WITH ATTRIBUTION

PKF Worldwide Tax Guide 2012 IV

about pKf international limited

PKF International Limited (PKFI) administers the PKF network of legally independent member firms. There are around 300 member firms and correspondents in 440 locations in around 125 countries providing accounting and business advisory services. PKFI member firms employ around 2,200 partners and more than 21,400 staff.

PKFI is the 10th largest global accountancy network and its member firms have $2.6 billion aggregate fee income (year end June 2011). The network is a member of the Forum of Firms, an organisation dedicated to consistent and high quality standards of financial reporting and auditing practices worldwide.

Services provided by member firms include:

Assurance & AdvisoryCorporate FinanceFinancial PlanningForensic AccountingHotel ConsultancyInsolvency – Corporate & PersonalIT ConsultancyManagement ConsultancyTaxation

PKF member firms are organised into five geographical regions covering Africa; Latin America; Asia Pacific; Europe, the Middle East & India (EMEI); and North America & the Caribbean. Each region elects representatives to the board of PKF International Limited which administers the network. While the member firms remain separate and independent, international tax, corporate finance, professional standards, audit, hotel consultancy, insolvency and business development committees work together to improve quality standards, develop initiatives and share knowledge and best practice cross the network.

Please visit www.pkf.com for more information.

PKF Worldwide Tax Guide 2012V

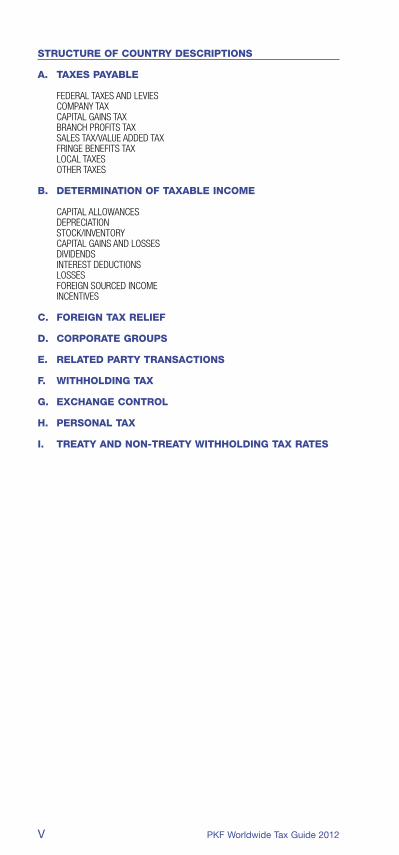

structure of country descriptions

a. taXes payable

FEDERAL TAXES AND LEVIES COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX SALES TAX/VALUE ADDED TAX FRINGE BENEFITS TAX LOCAL TAXES OTHER TAXES

b. determination of taXable income

CAPITAL ALLOWANCES DEPRECIATION STOCK/INVENTORY CAPITAL GAINS AND LOSSES DIVIDENDS INTEREST DEDUCTIONS LOSSES FOREIGN SOURCED INCOME INCENTIVES

c. foreiGn taX relief

d. corporate Groups

e. related party transactions

f. witHHoldinG taX

G. eXcHanGe control

H. personal taX

i. treaty and non-treaty witHHoldinG taX rates

PKF Worldwide Tax Guide 2012 VI

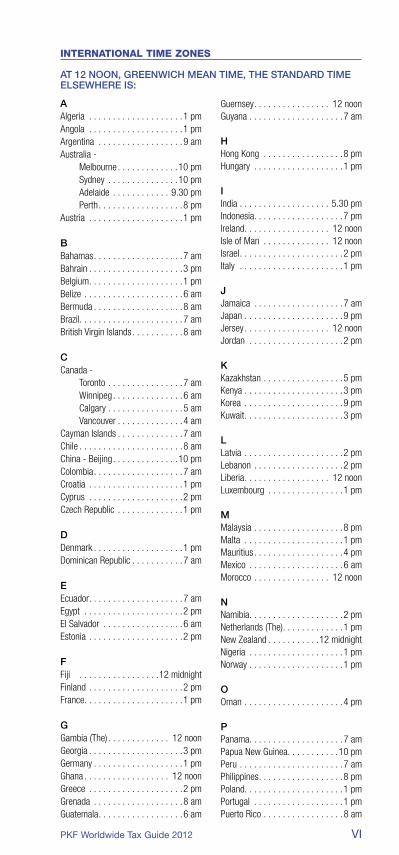

AAlgeria . . . . . . . . . . . . . . . . . . . .1 pmAngola . . . . . . . . . . . . . . . . . . . .1 pmArgentina . . . . . . . . . . . . . . . . . .9 amAustralia - Melbourne . . . . . . . . . . . . .10 pm Sydney . . . . . . . . . . . . . . .10 pm Adelaide . . . . . . . . . . . . 9.30 pm Perth . . . . . . . . . . . . . . . . . .8 pmAustria . . . . . . . . . . . . . . . . . . . .1 pm

BBahamas . . . . . . . . . . . . . . . . . . .7 amBahrain . . . . . . . . . . . . . . . . . . . .3 pmBelgium . . . . . . . . . . . . . . . . . . . .1 pmBelize . . . . . . . . . . . . . . . . . . . . .6 amBermuda . . . . . . . . . . . . . . . . . . .8 amBrazil. . . . . . . . . . . . . . . . . . . . . .7 amBritish Virgin Islands . . . . . . . . . . .8 am

CCanada - Toronto . . . . . . . . . . . . . . . .7 am Winnipeg . . . . . . . . . . . . . . .6 am Calgary . . . . . . . . . . . . . . . .5 am Vancouver . . . . . . . . . . . . . .4 amCayman Islands . . . . . . . . . . . . . .7 amChile . . . . . . . . . . . . . . . . . . . . . .8 amChina - Beijing . . . . . . . . . . . . . .10 pmColombia . . . . . . . . . . . . . . . . . . .7 amCroatia . . . . . . . . . . . . . . . . . . . .1 pmCyprus . . . . . . . . . . . . . . . . . . . .2 pmCzech Republic . . . . . . . . . . . . . .1 pm

DDenmark . . . . . . . . . . . . . . . . . . .1 pmDominican Republic . . . . . . . . . . .7 am

EEcuador . . . . . . . . . . . . . . . . . . . .7 amEgypt . . . . . . . . . . . . . . . . . . . . .2 pmEl Salvador . . . . . . . . . . . . . . . . .6 amEstonia . . . . . . . . . . . . . . . . . . . .2 pm

FFiji . . . . . . . . . . . . . . . . .12 midnightFinland . . . . . . . . . . . . . . . . . . . .2 pmFrance. . . . . . . . . . . . . . . . . . . . .1 pm

GGambia (The) . . . . . . . . . . . . . 12 noonGeorgia . . . . . . . . . . . . . . . . . . . .3 pmGermany . . . . . . . . . . . . . . . . . . .1 pmGhana . . . . . . . . . . . . . . . . . . 12 noonGreece . . . . . . . . . . . . . . . . . . . .2 pmGrenada . . . . . . . . . . . . . . . . . . .8 amGuatemala . . . . . . . . . . . . . . . . . .6 am

Guernsey . . . . . . . . . . . . . . . . 12 noonGuyana . . . . . . . . . . . . . . . . . . . .7 am

HHong Kong . . . . . . . . . . . . . . . . .8 pmHungary . . . . . . . . . . . . . . . . . . .1 pm

IIndia . . . . . . . . . . . . . . . . . . . 5.30 pmIndonesia. . . . . . . . . . . . . . . . . . .7 pmIreland . . . . . . . . . . . . . . . . . . 12 noonIsle of Man . . . . . . . . . . . . . . 12 noonIsrael . . . . . . . . . . . . . . . . . . . . . .2 pmItaly . . . . . . . . . . . . . . . . . . . . . .1 pm

JJamaica . . . . . . . . . . . . . . . . . . .7 amJapan . . . . . . . . . . . . . . . . . . . . .9 pmJersey . . . . . . . . . . . . . . . . . . 12 noonJordan . . . . . . . . . . . . . . . . . . . .2 pm

KKazakhstan . . . . . . . . . . . . . . . . .5 pmKenya . . . . . . . . . . . . . . . . . . . . .3 pmKorea . . . . . . . . . . . . . . . . . . . . .9 pmKuwait . . . . . . . . . . . . . . . . . . . . .3 pm

LLatvia . . . . . . . . . . . . . . . . . . . . .2 pmLebanon . . . . . . . . . . . . . . . . . . .2 pmLiberia . . . . . . . . . . . . . . . . . . 12 noonLuxembourg . . . . . . . . . . . . . . . .1 pm

MMalaysia . . . . . . . . . . . . . . . . . . .8 pmMalta . . . . . . . . . . . . . . . . . . . . .1 pmMauritius . . . . . . . . . . . . . . . . . . .4 pmMexico . . . . . . . . . . . . . . . . . . . .6 amMorocco . . . . . . . . . . . . . . . . 12 noon

NNamibia. . . . . . . . . . . . . . . . . . . .2 pmNetherlands (The) . . . . . . . . . . . . .1 pmNew Zealand . . . . . . . . . . .12 midnightNigeria . . . . . . . . . . . . . . . . . . . .1 pmNorway . . . . . . . . . . . . . . . . . . . .1 pm

OOman . . . . . . . . . . . . . . . . . . . . .4 pm

PPanama. . . . . . . . . . . . . . . . . . . .7 amPapua New Guinea. . . . . . . . . . .10 pmPeru . . . . . . . . . . . . . . . . . . . . . .7 amPhilippines . . . . . . . . . . . . . . . . . .8 pmPoland. . . . . . . . . . . . . . . . . . . . .1 pmPortugal . . . . . . . . . . . . . . . . . . .1 pmPuerto Rico . . . . . . . . . . . . . . . . .8 am

international time Zones

AT 12 NOON, GREENwICH MEAN TIME, THE sTANDARD TIME ELsEwHERE Is:

PKF Worldwide Tax Guide 2012VII

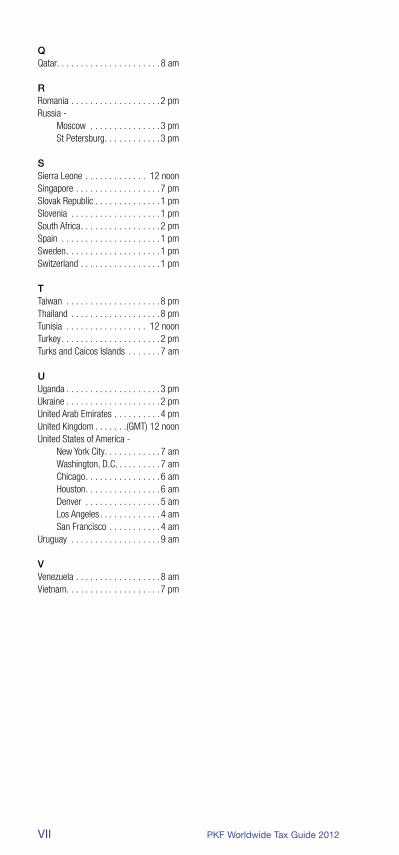

QQatar. . . . . . . . . . . . . . . . . . . . . .8 am

RRomania . . . . . . . . . . . . . . . . . . .2 pmRussia - Moscow . . . . . . . . . . . . . . .3 pm St Petersburg . . . . . . . . . . . .3 pm

sSierra Leone . . . . . . . . . . . . . 12 noonSingapore . . . . . . . . . . . . . . . . . .7 pmSlovak Republic . . . . . . . . . . . . . .1 pmSlovenia . . . . . . . . . . . . . . . . . . .1 pmSouth Africa . . . . . . . . . . . . . . . . .2 pmSpain . . . . . . . . . . . . . . . . . . . . .1 pmSweden . . . . . . . . . . . . . . . . . . . .1 pmSwitzerland . . . . . . . . . . . . . . . . .1 pm

TTaiwan . . . . . . . . . . . . . . . . . . . .8 pmThailand . . . . . . . . . . . . . . . . . . .8 pmTunisia . . . . . . . . . . . . . . . . . 12 noonTurkey . . . . . . . . . . . . . . . . . . . . .2 pmTurks and Caicos Islands . . . . . . .7 am

UUganda . . . . . . . . . . . . . . . . . . . .3 pmUkraine . . . . . . . . . . . . . . . . . . . .2 pmUnited Arab Emirates . . . . . . . . . .4 pmUnited Kingdom . . . . . . .(GMT) 12 noonUnited States of America - New York City . . . . . . . . . . . .7 am Washington, D.C. . . . . . . . . .7 am Chicago . . . . . . . . . . . . . . . .6 am Houston . . . . . . . . . . . . . . . .6 am Denver . . . . . . . . . . . . . . . .5 am Los Angeles . . . . . . . . . . . . .4 am San Francisco . . . . . . . . . . .4 amUruguay . . . . . . . . . . . . . . . . . . .9 am

VVenezuela . . . . . . . . . . . . . . . . . .8 amVietnam . . . . . . . . . . . . . . . . . . . .7 pm

PKF Worldwide Tax Guide 2012 1

Oman

oman

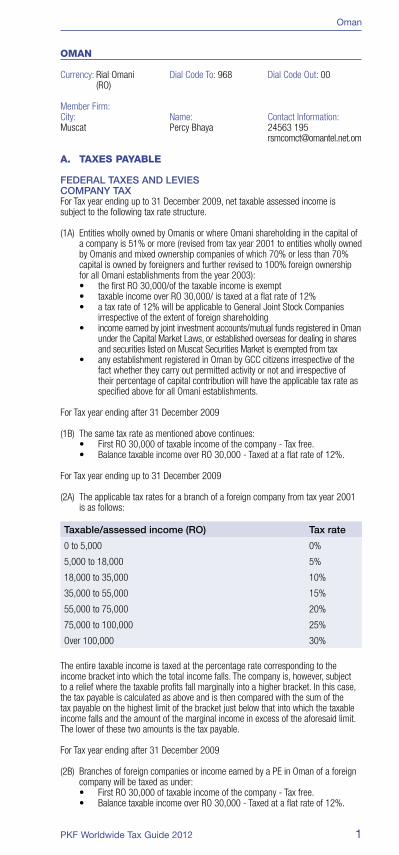

Currency: Rial Omani Dial Code To: 968 Dial Code Out: 00 (RO)

Member Firm:City: Name: Contact Information:Muscat Percy Bhaya 24563 195 [email protected]

a. taXes payable

FEDERAL TAxEs AND LEVIEsCOMPANy TAxFor Tax year ending up to 31 December 2009, net taxable assessed income is subject to the following tax rate structure.

(1A) Entities wholly owned by Omanis or where Omani shareholding in the capital of a company is 51% or more (revised from tax year 2001 to entities wholly owned by Omanis and mixed ownership companies of which 70% or less than 70% capital is owned by foreigners and further revised to 100% foreign ownership for all Omani establishments from the year 2003):

• thefirstRO30,000/ofthetaxableincomeisexempt • taxableincomeoverRO30,000/istaxedataflatrateof12% • ataxrateof12%willbeapplicabletoGeneralJointStockCompanies

irrespective of the extent of foreign shareholding • incomeearnedbyjointinvestmentaccounts/mutualfundsregisteredinOman

under the Capital Market Laws, or established overseas for dealing in shares and securities listed on Muscat Securities Market is exempted from tax

• anyestablishmentregisteredinOmanbyGCCcitizensirrespectiveofthefact whether they carry out permitted activity or not and irrespective of their percentage of capital contribution will have the applicable tax rate as specified above for all Omani establishments.

For Tax year ending after 31 December 2009

(1B) The same tax rate as mentioned above continues: • FirstRO30,000oftaxableincomeofthecompany-Taxfree. • BalancetaxableincomeoverRO30,000-Taxedataflatrateof12%.

For Tax year ending up to 31 December 2009

(2A) The applicable tax rates for a branch of a foreign company from tax year 2001 is as follows:

Taxable/assessed income (RO) Tax rate

0 to 5,000 0%

5,000 to 18,000 5%

18,000 to 35,000 10%

35,000 to 55,000 15%

55,000 to 75,000 20%

75,000 to 100,000 25%

Over 100,000 30%

The entire taxable income is taxed at the percentage rate corresponding to the income bracket into which the total income falls. The company is, however, subject to a relief where the taxable profits fall marginally into a higher bracket. In this case, the tax payable is calculated as above and is then compared with the sum of the tax payable on the highest limit of the bracket just below that into which the taxable income falls and the amount of the marginal income in excess of the aforesaid limit. The lower of these two amounts is the tax payable.

For Tax year ending after 31 December 2009

(2B) Branches of foreign companies or income earned by a PE in Oman of a foreign company will be taxed as under:

• FirstRO30,000oftaxableincomeofthecompany-Taxfree. • BalancetaxableincomeoverRO30,000-Taxedataflatrateof12%.

PKF Worldwide Tax Guide 20122

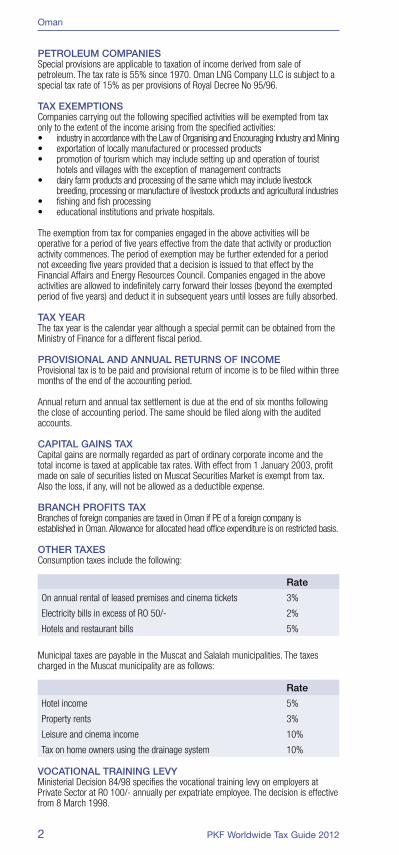

PETROLEUM COMPANIEsSpecial provisions are applicable to taxation of income derived from sale of petroleum. The tax rate is 55% since 1970. Oman LNG Company LLC is subject to a special tax rate of 15% as per provisions of Royal Decree No 95/96.

TAx ExEMPTIONsCompanies carrying out the following specified activities will be exempted from tax only to the extent of the income arising from the specified activities:• industryinaccordancewiththeLawofOrganisingandEncouragingIndustryandMining• exportationoflocallymanufacturedorprocessedproducts• promotionoftourismwhichmayincludesettingupandoperationoftourist

hotels and villages with the exception of management contracts• dairyfarmproductsandprocessingofthesamewhichmayincludelivestock

breeding, processing or manufacture of livestock products and agricultural industries• fishingandfishprocessing• educationalinstitutionsandprivatehospitals.

The exemption from tax for companies engaged in the above activities will be operative for a period of five years effective from the date that activity or production activity commences. The period of exemption may be further extended for a period not exceeding five years provided that a decision is issued to that effect by the Financial Affairs and Energy Resources Council. Companies engaged in the above activities are allowed to indefinitely carry forward their losses (beyond the exempted period of five years) and deduct it in subsequent years until losses are fully absorbed.

TAx yEARThe tax year is the calendar year although a special permit can be obtained from the Ministry of Finance for a different fiscal period.

PROVIsIONAL AND ANNUAL RETURNs OF INCOMEProvisional tax is to be paid and provisional return of income is to be filed within three months of the end of the accounting period.

Annual return and annual tax settlement is due at the end of six months following the close of accounting period. The same should be filed along with the audited accounts.

CAPITAL GAINs TAxCapital gains are normally regarded as part of ordinary corporate income and the total income is taxed at applicable tax rates. With effect from 1 January 2003, profit made on sale of securities listed on Muscat Securities Market is exempt from tax. Also the loss, if any, will not be allowed as a deductible expense.

BRANCH PROFITs TAxBranches of foreign companies are taxed in Oman if PE of a foreign company is established in Oman. Allowance for allocated head office expenditure is on restricted basis.

OTHER TAxEsConsumption taxes include the following:

Rate

On annual rental of leased premises and cinema tickets 3%

Electricity bills in excess of RO 50/- 2%

Hotels and restaurant bills 5%

Municipal taxes are payable in the Muscat and Salalah municipalities. The taxes charged in the Muscat municipality are as follows:

Rate

Hotel income 5%

Property rents 3%

Leisure and cinema income 10%

Tax on home owners using the drainage system 10%

VOCATIONAL TRAINING LEVyMinisterial Decision 84/98 specifies the vocational training levy on employers at Private Sector at R0 100/- annually per expatriate employee. The decision is effective from 8 March 1998.

Oman

PKF Worldwide Tax Guide 2012 3

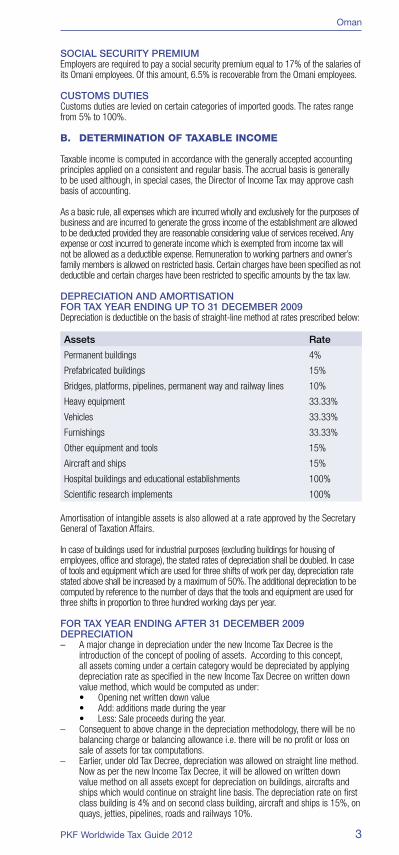

sOCIAL sECURITy PREMIUMEmployers are required to pay a social security premium equal to 17% of the salaries of its Omani employees. Of this amount, 6.5% is recoverable from the Omani employees.

CUsTOMs DUTIEsCustoms duties are levied on certain categories of imported goods. The rates range from 5% to 100%.

b. determination of taXable income

Taxable income is computed in accordance with the generally accepted accounting principles applied on a consistent and regular basis. The accrual basis is generally to be used although, in special cases, the Director of Income Tax may approve cash basis of accounting.

As a basic rule, all expenses which are incurred wholly and exclusively for the purposes of business and are incurred to generate the gross income of the establishment are allowed to be deducted provided they are reasonable considering value of services received. Any expense or cost incurred to generate income which is exempted from income tax will not be allowed as a deductible expense. Remuneration to working partners and owner’s family members is allowed on restricted basis. Certain charges have been specified as not deductible and certain charges have been restricted to specific amounts by the tax law.

DEPRECIATION AND AMORTIsATIONFOR TAx yEAR ENDING UP TO 31 DECEMBER 2009Depreciation is deductible on the basis of straight-line method at rates prescribed below:

Assets Rate

Permanent buildings 4%

Prefabricated buildings 15%

Bridges, platforms, pipelines, permanent way and railway lines 10%

Heavy equipment 33.33%

Vehicles 33.33%

Furnishings 33.33%

Other equipment and tools 15%

Aircraft and ships 15%

Hospital buildings and educational establishments 100%

Scientific research implements 100%

Amortisation of intangible assets is also allowed at a rate approved by the Secretary General of Taxation Affairs.

In case of buildings used for industrial purposes (excluding buildings for housing of employees, office and storage), the stated rates of depreciation shall be doubled. In case of tools and equipment which are used for three shifts of work per day, depreciation rate stated above shall be increased by a maximum of 50%. The additional depreciation to be computed by reference to the number of days that the tools and equipment are used for three shifts in proportion to three hundred working days per year.

FOR TAx yEAR ENDING AFTER 31 DECEMBER 2009DEPRECIATION– A major change in depreciation under the new Income Tax Decree is the

introduction of the concept of pooling of assets. According to this concept, all assets coming under a certain category would be depreciated by applying depreciation rate as specified in the new Income Tax Decree on written down value method, which would be computed as under:

• Openingnetwrittendownvalue • Add:additionsmadeduringtheyear • Less:Saleproceedsduringtheyear.– Consequent to above change in the depreciation methodology, there will be no

balancing charge or balancing allowance i.e. there will be no profit or loss on sale of assets for tax computations.

– Earlier, under old Tax Decree, depreciation was allowed on straight line method. Now as per the new Income Tax Decree, it will be allowed on written down value method on all assets except for depreciation on buildings, aircrafts and ships which would continue on straight line basis. The depreciation rate on first class building is 4% and on second class building, aircraft and ships is 15%, on quays, jetties, pipelines, roads and railways 10%.

Oman

PKF Worldwide Tax Guide 20124

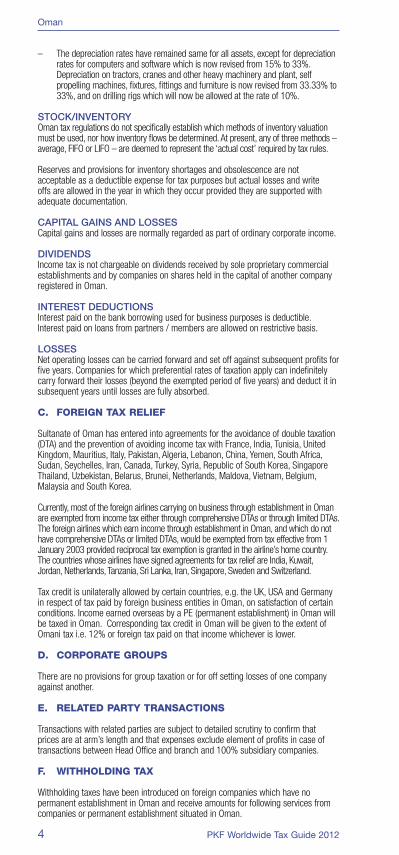

– The depreciation rates have remained same for all assets, except for depreciation rates for computers and software which is now revised from 15% to 33%. Depreciation on tractors, cranes and other heavy machinery and plant, self propelling machines, fixtures, fittings and furniture is now revised from 33.33% to 33%, and on drilling rigs which will now be allowed at the rate of 10%.

sTOCK/INVENTORyOman tax regulations do not specifically establish which methods of inventory valuation must be used, nor how inventory flows be determined. At present, any of three methods – average, FIFO or LIFO – are deemed to represent the ‘actual cost’ required by tax rules.

Reserves and provisions for inventory shortages and obsolescence are not acceptable as a deductible expense for tax purposes but actual losses and write offs are allowed in the year in which they occur provided they are supported with adequate documentation.

CAPITAL GAINs AND LOssEsCapital gains and losses are normally regarded as part of ordinary corporate income.

DIVIDENDsIncome tax is not chargeable on dividends received by sole proprietary commercial establishments and by companies on shares held in the capital of another company registered in Oman.

INTEREsT DEDUCTIONsInterest paid on the bank borrowing used for business purposes is deductible. Interest paid on loans from partners / members are allowed on restrictive basis.

LOssEsNet operating losses can be carried forward and set off against subsequent profits for five years. Companies for which preferential rates of taxation apply can indefinitely carry forward their losses (beyond the exempted period of five years) and deduct it in subsequent years until losses are fully absorbed.

c. foreiGn taX relief

Sultanate of Oman has entered into agreements for the avoidance of double taxation (DTA) and the prevention of avoiding income tax with France, India, Tunisia, United Kingdom, Mauritius, Italy, Pakistan, Algeria, Lebanon, China, Yemen, South Africa, Sudan, Seychelles, Iran, Canada, Turkey, Syria, Republic of South Korea, Singapore Thailand, Uzbekistan, Belarus, Brunei, Netherlands, Maldova, Vietnam, Belgium, Malaysia and South Korea.

Currently, most of the foreign airlines carrying on business through establishment in Oman are exempted from income tax either through comprehensive DTAs or through limited DTAs. The foreign airlines which earn income through establishment in Oman, and which do not have comprehensive DTAs or limited DTAs, would be exempted from tax effective from 1 January 2003 provided reciprocal tax exemption is granted in the airline’s home country. The countries whose airlines have signed agreements for tax relief are India, Kuwait, Jordan, Netherlands, Tanzania, Sri Lanka, Iran, Singapore, Sweden and Switzerland.

Tax credit is unilaterally allowed by certain countries, e.g. the UK, USA and Germany in respect of tax paid by foreign business entities in Oman, on satisfaction of certain conditions. Income earned overseas by a PE (permanent establishment) in Oman will be taxed in Oman. Corresponding tax credit in Oman will be given to the extent of Omani tax i.e. 12% or foreign tax paid on that income whichever is lower.

d. corporate Groups

There are no provisions for group taxation or for off setting losses of one company against another.

e. related party transactions

Transactions with related parties are subject to detailed scrutiny to confirm that prices are at arm’s length and that expenses exclude element of profits in case of transactions between Head Office and branch and 100% subsidiary companies.

f. witHHoldinG taX

Withholding taxes have been introduced on foreign companies which have no permanent establishment in Oman and receive amounts for following services from companies or permanent establishment situated in Oman.

Oman

PKF Worldwide Tax Guide 2012 5

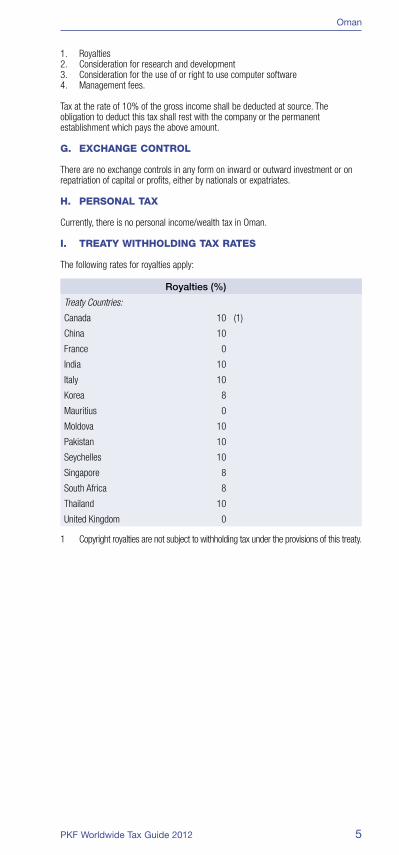

1. Royalties2. Consideration for research and development3. Consideration for the use of or right to use computer software4. Management fees.

Tax at the rate of 10% of the gross income shall be deducted at source. The obligation to deduct this tax shall rest with the company or the permanent establishment which pays the above amount.

G. eXcHanGe control

There are no exchange controls in any form on inward or outward investment or on repatriation of capital or profits, either by nationals or expatriates.

H. personal taX

Currently, there is no personal income/wealth tax in Oman.

i. treaty witHHoldinG taX rates

The following rates for royalties apply:

Royalties (%)

Treaty Countries:

Canada 10 (1)

China 10

France 0

India 10

Italy 10

Korea 8

Mauritius 0

Moldova 10

Pakistan 10

Seychelles 10

Singapore 8

South Africa 8

Thailand 10

United Kingdom 0

1 Copyright royalties are not subject to withholding tax under the provisions of this treaty.

Oman

PKF Worldwide Tax Guide 2012 565

www.pkf.com$100