oilvoice magazine | december 2013

DESCRIPTION

Edition 21 of the OilVoice Magazine.TRANSCRIPT

Edition twenty one – December 2013

Cover image by Enrico Strocchi

LNG heading east

Iran nuclear disaster for overpriced oil

Shale Gas - A case of what we know and what we don't know

1 OilVoice Magazine | DECEMBER 2013

Issue 21 – December 2013

OilVoice Acorn House 381 Midsummer Blvd Milton Keynes MK9 3HP Tel: +44 208 123 2237 Email: [email protected] Skype: oilvoicetalk Editor James Allen Email: [email protected] Director of Sales Terry O'Donnell Email: [email protected] Chief Executive Officer Adam Marmaras Email: [email protected] Social Network

Google+

Linked In

Read on your iPad You can open PDF documents, such as a PDF attached to an email, with iBooks.

Cover image by Enrico Strocchi

www.flickr.com/photos/strocchi

Adam Marmaras

Chief Executive Officer

Welcome to the 21st edition of the

OilVoice Magazine.

This month we have great articles from Angus Warren, Ola Nisja, Andrew McKillop, Gail Tverberg, Kurt Cobb, Keith Schaefer, Euan Mearns and Graham Shorr.

This is the last edition of 2013 and it has been a year of change for OilVoice. We've tried to focus on two main areas. Firstly the quality of our content. There are plenty of sites out there that contain only press releases, but we wanted to differentiate ourselves with opinion and commentary from the best authors in the business. New writers join our line up all the time, and we expect 2014 to be even better. If you have something to say, then please get in touch.

The second area we focussed on was recruitment. It's been hard work but we now have over 2000 active oil and gas jobs on the site, and new candidate growth is running at 20% month on month. A jobs board takes a while to 'bed in' an attract quality candidates, and we are well on the way. Hope you enjoy this edition, and have a great Christmas and New Year. Adam and the OilVoice Team

2 OilVoice Magazine | DECEMBER 2013

Contents

Featured Authors Biographies of this months featured authors 3 Why companies avoid new oil and gas technology by Angus Warren 5 Oil and gas disputes heat up as the market cools down by Ola Nisja and Jonathan Kjerschow 11 Iran nuclear disaster for overpriced oil by Andrew McKillop 13 Holistic Security in Oil & Gas - How to stay safe in a dangerous world by Angus Warren 17 What's ahead? Lower oil prices, despite higher extraction costs by Gail Tverberg 21 Shale Gas - A case of what we know and what we don't know by Angus Warren 33 Will the real International Energy Agency please stand up? by Kurt Cobb 35 A simple new fracking technique that could revolutionize the oil sector by Keith Schaefer 39 LNG heading east by Euan Mearns 41 U.S. reign as top global energy producer will be short lived by Graham Shorr 49 Why the U.S. government should allow LNG exports by Angus Warren 50

3 OilVoice Magazine | DECEMBER 2013

Featured Authors

Andrew McKillop

AMK CONSULT

Andrew MacKillop is an energy and natural resource sector professional with over 30 years’ experience in more than 12 countries.

Angus Warren

Warren Business Consulting

Angus is an oil and gas consultant who brings integrity, creativity and a track record of getting results to capturing your organization’s opportunities and resolving its unique issues.

Kurt Cobb

Resource Insights

Kurt Cobb is an author, speaker, and columnist focusing on energy and the environment. He is a regular contributor to the Energy Voices section of The Christian Science Monitor and author of the peak-oil-themed novel Prelude.

Ola Nisja

Wikborg Rein

Ola Ø. Nisja is a Partner at Wikborg Rein's Oslo office and he is part of the firm's Contract Law and Construction practice. He has substantial experience in litigation and dispute resolution and is admitted to the Supreme Court.

Keith Schaefer

Oil & Gas Investments Bulletin

Keith Schaefer, editor and publisher of the Oil & Gas Investments Bulletin.

4 OilVoice Magazine | DECEMBER 2013

Gail Tverberg

Our Finite World

Gail the Actuary’s real name is Gail Tverberg. She has an M. S. from the University of Illinois, Chicago in Mathematics, and is a Fellow of the Casualty Actuarial Society and a Member of the American Academy of Actuaries.

Euan Mearns

Energy Matters

Euan Mearns has B.Sc. and Ph.D. degrees in geology.

Graham Shorr

SaveOnEnergy

Graham Shorr is a Copywriter for SaveOnEnergy.com. When he’s not posting on his sustainability blog, he freelances in the energy field. He expertise lies in policy and investment of traditional and modern energy production.

5 OilVoice Magazine | DECEMBER 2013

Why companies avoid new oil and gas technology

Written by Angus Warren from Warren Business Consulting

Oil and Gas Technology: A huge impact historically, but little current appetite Throughout its history the oil and gas industry has been propelled forward by innovation and technology. Technology has dramatically altered the way in which oil and gas resources are discovered, developed, and produced. Technology has improved the performance of oil products, reduced environmental impact and advanced safety performance. It has also helped us to consume precious natural resources much more efficiently. Over the years there have been many technological breakthroughs and thousands of incremental advances. For example, oil recovery has increased from less than 10 per cent of oil in place in the early history of the industry, to in excess of 70 per cent in some fields today. And yet the R&D spend of oil and gas operating companies is small relative other sectors and there is some evidence that it is decreasing. In the global top 1000 companies by R&D spend, the top 25 contains no oil and gas companies, according to research by the U.K. government:

6 OilVoice Magazine | DECEMBER 2013

When R&D is expressed as a percentage of sales or operating profits, the picture looks even worse for oil and gas operating companies:

U.K. Government 2010 R&D Score Board

U.K. Government 2010 R&D Score Board Not only are oil and gas spending less on R&D, they are also less inclined to adopt technologies developed by others. There is little rigorous data and analysis to back

7 OilVoice Magazine | DECEMBER 2013

this assertion up. But there is plenty of anecdotal evidence. Just ask any budding entrepreneur with a new widget that promises increased productivity in the oil field. Even seasoned business developers in the large oil services companies will acknowledge that sales of new technology to operating companies are quite a challenge. How technology fell out of favour R&D spend by oil and gas operators appears to have fallen victim to the general outsourcing initiative which started in the 1980s. At this time companies began to scrutinise activities carried out within the firm and decided that in the 'buy versus build' decision, it was mostly better to buy new technology from the market place. This meant that service companies were called upon to fill the gap by increasing their R&D activities. Today, much technological innovation in the industry is generated by service companies and technology start-ups. National oil companies and governments have also played a role. Service companies file many more patents annually than the operators. Service companies will often acquire start-up technology companies early in the deployment phase of a new product or service. These start-up companies drive much of the innovation in the industry. What's driving oil company attitiudes to technology? So, why do oil and gas operators shy away from new technology so much more than other players in the industry and companies in other sectors? The answer is likely to come in several forms: Driven by investors: There is much greater transparency when investing in new technology in the retail, entertainment, telecoms and healthcare sectors. The new technology is all around us and clear to see. However, there is little mainstream media attention given to the impact of technology on natural resource companies. This may colour investors' perceptions. Slow Adopters: In oil and gas we are notoriously slow adopters of new technology. Operating companies may therefore take the view that commercialising technology in the oil and gas is too costly and time consuming. They may be right. Consider these 2 examples:

The world's first 3D seismic survey was undertaken by ExxonMobil in 1967, but it was not until the mid-1980s that the technology became truly mainstream.

Horizontal drilling began in the USA in the mid-1970s, but it wasn't until the 1980s that steerable motors that could be controlled from the surface were introduced - that allowed the real growth in horizontal drilling to take place between 1990 and 2000.

8 OilVoice Magazine | DECEMBER 2013

Risk Aversion: In recent years' oil and gas companies have been driven to technically and politically more challenging parts of the world in the quest for new resources. At the same time there has been significant industry inflation and government take has been on the rise. Operators have become increasingly risk averse as they take on new projects that are more expensive and offer lower returns. In many ways, new technology is 'a risk too far'. Lacking Capabilities: The oil company strategy to outsource technology development to the services sector has resulted in a significant reduction in the number of people they have that understand technology and the R&D process. This has proven to be a barrier to the rapid introduction of new technologies to these companies. First Mover Disadvantage: Operating companies are generally reluctant to be the first to apply an unfamiliar technology, preferring others to take the initial risk. This can lead to a lengthy commercialisation process and delays in achieving economic gains for successful new technologies. However, commercialisation works much better if the operator has been involved in the development process. When operators are intimately familiar with the technology under development they are much better at estimating its risk reward characteristics. Short Termism: Operating companies are generally more willing to take geological or political risk than technical risk and this seems to be strongly influenced by investor expectations. Many new technologies will offer significant benefits over the long term. However, most new technologies also introduce short term downside risk, such as disruptions to drilling or production. In this scenario, short term corporate targets will almost always win the day. Similarly, which executive will take the short term risk to the performance of his unit, for the long term benefit of the whole company? Cost and Integration: The capital cost of introducing even the simplest new technology can be prohibitive, once all design, manufacturing, installation, operation and maintenance activities are accounted for. Even a small, new widget will be a part of a much bigger system, and often system integration issues make the oil and gas operator reluctant to adopt it. The 'Believers': some still investing in oil and gas technology All this said, there are a number of companies taking a strategic view of technology and investing in select new technologies. Strategic investors in oil and gas technology include Chevron, Shell, Energy Technology Ventures, a joint venture between GE, NRG, and ConocoPhillips, Statoil Ventures, and KPC Ventures. The last too are especially noteworthy, because they are divisions of national oil companies. And a recent report by Bain, the management consulting firm, noted that many NOCs seek to nurture entrepreneurship and foster globally competitive businesses in energy-related sectors in their home country. Many times this will involve start-ups which are developing new technologies.

9 OilVoice Magazine | DECEMBER 2013

Chevron has invested in firms such as Ampersand Ventures, Element Partners, EnerTech Capital, Nth Power, and RockPort Capital Partners. KPC Ventures backs Braemar Energy Ventures, Chrysalix, Emerald Technology Ventures, Conduit Ventures, Nth Power, and EnerTech Capital. Baker Hughes, Nalco, and Weatherford sponsor the Oil & Gas Innovation Center, and the Surge Accelerator serves as a Houston-based incubator for energy start-ups. Despite the general lack of industry appetite for new technology, there are believers who see the potential for breakthrough and are backing this belief with resources. Oil and Gas Operators Still have a Major Role to Play New technology development requires firstly an understanding of the problem to be solved and the benefits of resolution; secondly, knowledge of the underlying science and engineering of the proposed solution; and lastly, the capability to commercialise new products through development, finance and marketing. Therefore, the oil and gas operating companies have the leading role to play, and in many ways are the natural custodians of new technology.

View more quality content from Warren Business Consulting

G E O S O L U T I O N S

Sweet marks the spotNew life and deeper potential from an established basin

Over the past 150 years, California’s Ventura

Basin has been one of the world’s most

productive regions, yielding nearly 4 billion

barrels of oil.

Coinciding with the shale boom and the

subsequent search for sweet spots in the

Monterey Shale, as well as recent multi-

hundred-million barrel discoveries in the

nearby San Joaquin Basin, explorationists

have grown intrigued by the untapped

hydrocarbon potential in a basin presumed to

be past its prime. However, since most of the

area is densely populated, environmentally

sensitive and topographically challenging, ground-based seismic acquisition is impractical — not to mention expensive.

NEOS GeoSolutions conducted a 1,300 square mile survey that combined all available geological, geophysical, geochemical

and petrophysical datasets. This information, obtained from the public domain, third-party sources and NEOS’s own

archives, was combined with newly acquired gravity, magnetic and hyperspectral data, and then simultaneously integrated

and interpreted using a Multi-measurement Interpretation (MMI) methodology.

NEOS acquired Bouguer gravity data to delineate deep basin architecture and basin-scale structural features. The data

showed an outline of the basin at different depths, sediment thickness variations, and shelves, platforms and ridges, all

characteristics that coincided with known and prospective fields in the basin. The application of high-pass filtering helped

to highlight the basin’s changing boundaries and sediment thicknesses, both of which varied with depth.

Magnetic acquisition, with reduced-to-pole (RTP) analysis, showed three distinct areas of magnetic susceptibility that

correlated with regional, deep-seated fault and fracture networks. In the Ventura Basin, nearly 90% of known production

can be correlated with proximity to these fault and fracture systems.

With the acquisition of hyperspectral data, NEOS mapped existing hydrocarbon seeps on the surface. The data were then

verified and cross-calibrated by ground teams, and traced back into the subsurface along potential migration pathways

such as lineaments and fault planes.

All newly acquired data were then combined with existing information, including well logs, geologic maps and production

histories. Using proprietary software, NEOS applied predictive analytics to identify relevant anomalies that correlated with

known fields at specific reservoir intervals of interest. The result was a comprehensive, geostatistically supported snapshot

of the entire region identifying highly prospective areas for both oil and gas exploration.

To learn more about this project or others in the Unlock the Potential series, visit: www.ThePotentialUnlocked.com

A comprehensive, geostatistical assessment of prospectivity for Ventura County, California. Hot colors indicate high probability of oil; black dots indicate existing wells.

UNLOCK THE POTENTIAL IN YOUR FIELD | #3 IN A SERIES DECEMBER 2013

OilVoice

KEY TECHNOLOGIES:

MAGNETIC

GRAVITY

HYPERSPECTRAL

PREDICTIVE ANALYTICS

AREA: Ventura Basin, California

CUSTOMER: Large Independent

FOCUS: Regional Mapping

TYPE: Conventional

KEY INTERPRETIVE PRODUCTS:

≥ Basement topography

≥ 2D structural and lithological cross sections

≥ Maps of lineaments and fault networks

≥ Horizon-specific prospectivity maps

CUSTOMER BENEFITS:

Provides a relatively fast, cost-effective

subsurface prospectivity map beneath

urbanized, environmentally sensitive

or topographically challenging areas

without having to contend with

permits or access restrictions.

HIGHLIGHTS

CALIFORNIA

VENTURA BASIN

11 OilVoice Magazine | DECEMBER 2013

Oil and gas disputes heat up as the market cools down

Written by Ola Nisja and Jonathan Kjerschow from Wikborg Rein

Recent whispers coming out of the Norwegian offshore community have hinted that oil and gas companies putting off projects, and stabilisation of investment levels, are signs of a market that could be cooling down. Some analysts have even gone so far as to predict that oil prices could be taking a dive due to significant international shale oil production increases. With high oil prices driving the investment in offshore oil and gas exploration and production, it could be argued that there are a number of uncertainties in the market. And with 'uncertainty' generally comes conflict. In such a climate, parties are less prone to pay their way out of disputes, as maximizing returns on existing projects is commercially vital. From a legal perspective this implies disputes going further and more cases going to litigation. However, a great number of these disputes can be avoided or resolved at an earlier stage with mutually acceptable outcomes. Disputes typically arise when a contractor claims that an instruction from a company imposes obligations beyond an original contract's scope of work. On NCS work, the Norwegian standard forms are comprehensive and lay down detailed formal provisions as to how variations should be handled. Although most contractors and suppliers involved in deliveries to Norwegian Continental Shelf projects are familiar with these local standard forms, there are some key differences which should be highlighted for those unfamiliar with the legal process. These include strict rules on variation orders, the remedies available in certain situations of hardship, and the Norwegian background rules which will fill-in any contractual 'gaps'. The Devil is in the detail The detailed regulation of the NCS standard form contracts can come as a surprise to contractors more familiar with the FIDIC rules which have a less stringent regime. A characteristic of the Norwegian standard form is the importance of following procedure in order to avoid losing legal positions. The NCS Standard Form procedure has been developed over many years, and is meant to create greater contractual certainty and more order for NCS projects. However, the issuing of VORs and an increase in claims and counterclaims has the potential to shake-up the status quo. For oil and gas contractors and owners, these will be interesting times.

12 OilVoice Magazine | DECEMBER 2013

Pragmatism comes with legal risks With an increase of international players working in the Norwegian Continental Shelf supply industry, new challenges are arising. We have seen that cultural differences between Norwegian and overseas operators have resulted in different approaches and views as to the importance of contract details and the importance of NCS requirements. This clearly becomes an issue if one of the parties has a more informal approach to business than the other. In a number of cases, this has involved one part bringing a less confrontational style than most NCS contractors are used to, and a perceived disregard for formal procedure. It seems non-Norwegian contractors are used to a level of contractual 'pragmatism' which is not often seen on the NCS. Naturally, bringing a new approach into a mature market can be a risky practice. If a disagreement turns into a full legal dispute, the 'pragmatic' supplier might very well be confronted with a claim that a variation order request was presented too late. For a 'pragmatic' owner, a relaxed approach might result in the loss of rights (and legal position). Hire specialists and keep them involved With the above scenarios in mind, the obvious conclusion is that contracts and the procedural system should be followed strictly. On the NCS, contract managers are often instrumental in securing and enforcing compliance with the agreed contracts. Engaging contract managers may turn out to be a particularly good business investment when markets slow down, as a decreasing intake of orders tends to increase the propensity to claim additional payment based on (alleged) variations. However, a common operational mistake is that these managers are not sufficiently involved in the project on a day to day basis. Contract managers are often only involved in specific cases when things have gone wrong, or when a conflict is developing. This often prevents them from seeing the project as a whole and reduces the chances of a early resolution to a problem. Hiring experienced contract managers and implementing day-to-day routines to encourage the flow of information in the organisation to the people who need to know, are positive measures to counter this risk. Increasingly difficult markets may lead to tougher positions on contract management. It is important that companies working on the NCS seek specialist advice as early as possible in the project timeline, not just when negotiating the final settlement. This may prove to be a cost-effective form of project insurance, and could save your company a significant amount of money if a dispute starts to escalate.

View more quality content from Wikborg Rein

13 OilVoice Magazine | DECEMBER 2013

Iran nuclear disaster for overpriced oil

Written by Andrew McKillop from AMK CONSULT

IRAN NUCLEAR - ISRAEL NUCLEAR Alongside Gulf state leaderships and their official news outlets, Israel's Benyamin Netanyahu reacted with fury to the Iran nuclear sanctions-unwinding deal made in Geneva, 24 November. He fulminated: "What was concluded in Geneva last night is not a historic agreement, it's a historic mistake," adding "It's not made the world a safer place. Like the agreement with North Korea in 2005, this agreement has made the world a much more dangerous place". Not so much nuclear, but unclear was what Israel and Saudi Arabia intend to do next. Their loyal sherpah at the Geneva talkfest, France's foreign minister Laurent Fabius threw in the towel on trying to get a blanket rejection of Iranian offers, in his tireless attempts to scupper the deal. France has major arms selling contracts with the Wahabite Kingdom, an Islamic feudal theocracy where females persons are not even allowed to drive a car. Protecting the Wahabites from nuclear Iran is a noble quest. France also has legacy guilt for its World War II treatment of Jews, by its Vichy regime which collaborated throughout the war as a servile pawn of the Nazis, and France casts itself as a kneejerk glove puppet ally for Israeli aggression in the Middle East. However and despite that, the talks in Geneva had enough momentum to result in a concrete deal. Sanctions relief under the agreement is estimated by US officials as likely to provide Tehran about $6 to $7 billion in badly needed foreign-exchange earnings during the next six months, which the accord says will be a trial period. If Tehran does not hold to its commitments, the White House said in a press release, new and more powerful sanctions, as well as existing sanction will be imposed or reintroduced to cripple Iran. In the short-term, analysts estimate, Tehran may quickly obtain about $4 billion, through unfrozen earnings from oil sales previously trapped in overseas bank accounts by the sanctions and not remitted to Iran. To allay the predicted outburst of criticism in both the US Senate and Congress from the friends of Israel or the enemies of Iran, the White House made it plain that the US intends to go on hurting Iran. Its press release said the country would still lose around $25 billion in oil revenues during the six-month confidence-building phase and about $15 billion of its oil revenues will remain frozen in banks outside of Iran at the end of the trial period. SPINNING CENTRIFUGES AND KEEPING OIL HIGH The U.S. and its European partners in the historic deal will also suspend bans on

14 OilVoice Magazine | DECEMBER 2013

trade in petrochemicals, precious metals, automobiles and airplane spare parts, and further extend previously existing, but small humanitarian relief operations, and student funding exemptions for Iranians abroad. More important for the global economy, the White House press release brags that sanctions affecting crude oil sales have cut Iran's oil sales from 2.5 million barrels per day (Mbd) in early 2012 to 1 Mbd today, 'causing an estimate earnings loss of more than $80 billion since January 2012 that Iran will never be able to recoup'. The press release also says the EU will maintain its own ban on crude oil from Iran, and Iranian oil sales in Europe will be capped at about 1 Mbd, resulting in continuing lost oil revenues estimated at about 3 billion euros ($4 billion) per month, throughout the trial phase. The White House, in its long detailed press release on the Geneva agreement, anticipates and makes a clear attempt to head off criticism that the deal is too lenient, which among its five partners at the talks were most intense from the French. For weeks in France its government-owned TV channels and its government-owned radio stations have drummed the 'message' that military force, that is bombing Iran, is the only option. The harsh and shrill propaganda coming from the French government recurringly focused the role of Iran's centrifuges and its Arak heavy water reactor 'able to produce a bomb within 18 months'. France's large recent arms sales contracts with Riyadh, and what the Wahabite Kingdom expects in return were never mentioned. Also missing from French glove puppet media accounts of French hawk policy on Iran, the goal of keeping oil prices high was absent ! For China, Russia and Germany, the +1 player in the 5 + 1 sextet negotiating with Iran in Geneva, the deal was a lot simpler. They hailed the November 24 deal as a pure and simple breakthrough. While Russia, the equal-rank largest oil producer in the world with Saudi Arabia, may lose from an expected decline in world oil prices, other members of the sextet, except France, openly welcomed the outlook for Iranian oil to flow more freely. French President Francois Hollande in an e-mail statement from his office, November 24, was forced to claim that he: 'Welcomed the conclusion of the Geneva negotiations on Iran's nuclear program', also asserting for his national audience that it was France's tough stance that had nailed the Iranian snake. He said: 'The accord that was reached respects the demands imposed by France on.....uranium storage and enrichment, suspension of new facilities, and international control". To be sure Hollande quickly went on to say he wanted to 'normalize relations' with Iran, after wanting to bomb it, if only to get France a place in the queue for oil contracts, that analysts concluded would rapidly grow. 'Wall Street Journal', 25 November, reported that several European companies had already announced, by Sunday evening, that they were preparing to resume operations in Iran. SELLING THE DEAL The US White House in its own way hailed the November 24 agreement with Iran, giving a huge list of technical details on how the agreement will 'go on hurting Iran's nuclear program'. Its long and uber-arrogant press release focused many of the technical subjects, and it parried the expected criticism from the Paris-Riyadh-Jerusalem axis that Iran would soon be able to crank up its oil sales - hurting Riyadh if not Paris and Jerusalem.

15 OilVoice Magazine | DECEMBER 2013

Iran's centrifuges must turn slower and less, the agreement even limits the number of centrifuge rotors, cages and bearings Iran will be able to produce and possess! Iran must also cease all reprocessing of nuclear wastes inside the country - and hand the job, and the lucrative contracts for spent fuel transport and reprocessing to the very short list of countries able to do it. France, UK, USA, Russia, China. Business as usual. One carefully unpublished, but certain goal of the Iran nuclear negotiations circus is to maintain high oil prices, to the delight of Goldman Sachs, US shale oil producers, Saudi Arabia and its Gulf state friends - and major oil companies including France's Total Oil SA. Few if no other interest groups directly profit from overpriced oil. To what extent oil prices can be held at present overpriced highs is however uncertain. Market reaction and response in coming days and weeks will tell us. To be sure the real linkage of overpriced oil - and centrifuges spinning overground or underground in Iran - is almost zero. But the use of oil sanctions against Iran makes the relation ultra clear. Iran has to choose between national atomic kudos, and selling oil. The financial and revenue links exist, but the Geneva accord was very careful to not spell out the rate at which Iran will rejoin the 'community of oil exporters' , because the faster Iran does this, the faster oil prices will drop. Inside Iran, although given little or no coverage by western media, the same argument has raged - national kudos versus importing food, machinery, spare parts and general merchandise on the back of oil revenues. In Tehran, Sunday evening, car drivers honked their horns and flashed their lights because ordinary Iranians saw the Geneva deal as a breakthrough. They celebrated the deal as a political victory for President Hasan Rouhani and a step towards relieving Iran's failing economy. Not only outside Iran, but also inside, the nuclear program is criticised as a major waste of national funds - not a stepping stone to proudly possessing atomic weapons like those produced and owned by Israel and those owned and produced by Pakistan - for immediate supply to Saudi Arabia whenever the Wahabite Kingdom opens its petrodollar-fattened chequebook. ANTIQUE MILITARY AND CIVIL NUCLEAR According to France's president Hollande, reacting to the collapse of his foreign minister's attempts to keep Iran bombing on the agenda, by scuppering any deal in Geneva, the Iranian heavy water reactor in Arak was the red line in the sand. Stopping this HW reactor, for the French political class and its glove puppet media was tantamount to stopping the claimed and supposed Iranian nuclear weapons program dead in its tracks. French consumers of pap media were invited and told to believe that Iranian possession of a heavy water reactor signalled the same thing as the 1980s Pakistani atom bomb program of Abdul Qadr 'Bombs R Us' Khan, facilitated and enabled by the Canadian-supplied CANDU heavy water and depleted uranium (HW and DU) 137 megawatt KANUPP reactor - which was supplied, in fact almost given to Pakistan in 1964. Iranians, French were supposed to imagine, live in a timewarp making them totally unable to develop their own HW DU reactor technology, and assuming firstly that they wanted to 'brew' bomb grade plutonium from depleted

16 OilVoice Magazine | DECEMBER 2013

uranium source material, like Pakistan did. And like India did well before Pakistan, in 1974. The technology is antique. Nuclear weapons have moved on since the 1960s and 1970s. One uber-simple example is DU munitions and military ordnance, which need no centrifuges or plutonium or enriched uranium. Another is 'quick and dirty' low cost nuclear weapons only using nuclear waste, the most irradiated and chemically toxic possible. No bang, but plenty of damage for the buck. Nothing in the White House press release of November 24, 2013 would suggest we are talking about 40 or 50-year-old technology, well known by at least two or even three generations of nuclear and military scientists, worldwide. Pakistan's 'heavy water route' atom bombs date from the 1980s. In 1945, in southern Germany, Nobel prize physicist Werner Heisenberg was still trying to produce a Nazi atom bomb using the HW DU reactor route when Allied soldiers stormed his secret bunker lab! It was bombed out by the Allies using regular-type explosives. The Nazis lost the war. Atom bombs are antique tech. The Iranian nuclear sanctions show or circus endured so long that it was upstaged and sidelined by reality. Since the time that US-initiated and US-funded nuclear technology started being developed by Iran - from 1955 - the world has had two massive nuclear disasters, Chernobyl and Fukushima. For nuclear lobby diehards, of course, this does not destroy the pride, prestige and satisfaction that possessing nuclear power bestows, but the sheer costs of nuclear power are getting to be known - and not enjoyed. For Iran's mollahs, perhaps, scaling back the country's national nuclear program might be a big loss of face, but nuclear power, and weapons are a gadget for the elite whether it concerns poor or rich countries.

View more quality content from AMK CONSULT

17 OilVoice Magazine | DECEMBER 2013

Holistic Security in Oil & Gas - How to stay safe in a dangerous world

Written by Angus Warren from Warren Business Consulting

The following true story is retold by Tony Ling* of LPD Risk: 'Brian Wellcome's job was just to get the stuff out of the ground. Yes, he was in charge, but someone else would look after the politics: the locals, guerrillas - whatever. Some security guy had said something to him once, but he knew they always exaggerated. Anyway it was now all to late - just guns, screaming and death. He knew he was going to die. But when Brian's well site was attacked he was not killed; he was far too valuable as a hostage. He was released after nine months captivity and the payment of a considerable ransom. The irony in all this was that it had all been so preventable. An independent enquiry ordered by the Board revealed that far from being a long planned terrorist attack, Brian's capture had been a result of village revenge and guerrilla opportunity. The Company had upset its neighbours. A week before Brian's kidnapping a distressed pregnant woman and her husband had come to his fenced rig site asking for help from the clinic only to be turned away by the guard who came from a different tribe with a long running feud with the surrounding people. Brian had then refused to meet a deputation from the village. The woman died in childbirth but the baby son lived. The son was raised to think only of revenge and hatred of the foreigners who had stolen his land and his mother. He became a guerrilla leader and scourge of the oil industry. The evening before the attack on the rig the talk in the village was still about this rebuff; the hatred oIraq 01f the company was palpable. There happened to be a stranger passing through this previously peaceful village. He immediately saw an opportunity for political gain and offered revenge that was immediately accepted. It took him no more than a few hours to gather a dozen well armed comrades from the hills to attack Brian's rig-site. The guerrillas were able to capitalise on their popularity and quickly took over the area, the Army moved in to counter them and the company never operated there again'. What does this story teach us? In short, Brian's company had failed to engage the

18 OilVoice Magazine | DECEMBER 2013

local community as stakeholders. In our dangerous world security must be managed holistically to ensure operations, or a project, can work securely and peacefully; no company can afford neighbours as enemy. A holistic approach manages security risks under four pillars:

1. Working with host government security agencies: this benefits security but, if the company is not careful, it can also bring liability and risk to its reputation. 2. Physical protection: the old way of looking at security, but still important. 3. Ownership: security, like safety, is everyone's responsibility. 4. Working with the community: the term 'community' embraces the whole of civil society, national and international, but it is a company's local community in the area of operations that is usually the most crucial to their security.

In this article I will focus on the last pillar, working with the local community. As Brian and his company learnt, lose the support of your local community and you can lose the operation. Here are the main areas to focus on:

The security team should work with your company's social and community function: increasingly companies are combining security with other functions working to ensure a peaceful environment. Understand local political dynamics: this is particularly critical where there is a tribal, religious or cultural clash between the local community and the host country government. The security of the community is important to the security of the project: in many areas these are inseparable. Community based security: this is increasingly seen as both cheaper and more effective than relying on the traditional 'guard force' concept, particularly when the guards come from another tribe. In short community support comes when local people feel that they gain more than they lose from the operation's presence. There is no better way of achieving this than providing employment. Manage the impact of outsiders: the security risk to local people is increased by the presence of an extraction operation because immigrants, including criminals, are attracted by the new opportunities. Often the host government does not have the will or resources to deal with this so the company may have to become involved (within the terms laid down in the Voluntary Principles on Security and Human Rights). Consult: in order to facilitate the required peaceful environment companies should develop a consultation process to engage locals. Invest in the community: ensure 'sustainable local benefits' for communities and equitable distribution of royalties. Don't invest in infrastructure such as a school or clinic without resources such as teachers or medicines to maintain it. Help: focus on resolving the problems that communities themselves are concerned about.

19 OilVoice Magazine | DECEMBER 2013

Dialogue: engage in genuine dialogue with communities and listen to their concerns and deal with them. But never make promises to the community that you cannot deliver. Gain consent: ensure that consent is provided according to international good practice (such as the UN-REDD Programme Guidelines on Free, Prior and Informed Consent) and that communities have access to independent technical experts, such as water engineers. Do not polarize: do not contribute to the 'divide and rule' approach of separating indigenous communities or other groups or networks by polarizing them into 'pro' and 'anti' an extraction operation. Joint ventures: A company should consider developing a joint venture with the community so that it is directly involved with the development of the project. Human rights: implement a robust mechanism to deal with allegations of human rights abuse.

*The author is Tony Ling, Chairman of LPD Group, a company that provides risk management services to a range of clients in hostile and unstable environments. This story was first told as part of Tony Ling's long article in 'Risk and Energy Infrastructure Cross-?Border Dimensions', Global Law and Business, August 2011.

View more quality content from Warren Business Consulting

Globe Getech ’ s flagship global new ventures platform.

Regional Reports Focussed assessments of exploration risks and opportunities.

Commissions Bespoke projects utilising clients’ proprietary data.

Data Unrivalled global gravity and magnetic coverage.

For further information contact Getech:Getech, Leeds, UK +44 113 322 2200 Getech, Houston, US +1 713 979 [email protected] www.getech.com

Leaders in the world of natural resource location

21 OilVoice Magazine | DECEMBER 2013

What's ahead? Lower oil prices, despite higher extraction costs

Written by Gail Tverberg from Our Finite World

Nearly everyone believes that oil prices will trend higher and higher, allowing increasing amounts of oil to be extracted. This belief is based on the observation that the cost of extraction is trending higher and higher. If we are to continue to have oil, we will need to pay the ever-higher cost of extraction. Either that, or we will have to pay the high cost of some type of substitute, if one can be found. Perhaps such a substitute will be a bit less expensive than oil, but costs are still likely to be high, since substitutes to date are higher-priced than oil. Even though this is conventional reasoning based on experience with many substances, it doesn’t work with oil. Part of the reasoning is right, though. It is indeed true that the cost of extracting oil is trending upward. We extracted the easy to extract oil, and thus “cheap” to extract oil, first and have been forced to move on to extracting oil that is much more expensive to extract. For example, extracting oil using fracking is expensive. So is extracting Brazil’s off-shore oil from under the salt layer. There are also rising indirect costs of production. Middle Eastern oil exporting nations need high tax revenue in order to keep their populations pacified with programs that provide desalinated water, food, housing and other benefits. This can be done only through high taxes on oil exports. The need for these high taxes acts to increase the sales prices required by these countries–often over $100 barrel (Arab Petroleum Investment House 2013). Even though the cost of extracting oil is increasing, the feedback loops that occur when oil prices actually do rise are such that oil prices tend to quickly fall back, if they actually do rise. We know this intuitively–in oil importing nations, deep recessions have been associated with big oil price spikes, such as occurred in the 1970s and in 2008. Economist James Hamilton has shown that 10 out of 11 US recessions since World War II were associated with oil price spikes (Hamilton 2011). Hamilton also showed that the effects of the oil price spike were sufficient to cause the recession of that began in late 2007 (Hamilton 2009). In this post, I will explore the reasons for these adverse feedback loops. I have discussed many of these issues previously in an academic paper I wrote that was published in the journal Energy, called “Oil Supply Limits and the Continuing Financial Crisis” (available here or here).

22 OilVoice Magazine | DECEMBER 2013

If I am indeed right about the path of oil prices being down, rather than up, the long-term direction of the economy is quite different from what most are imagining. Oil companies will find new production increasingly unprofitable, and will distribute funds back to shareholders, rather than invest them in unprofitable operations. In fact, some oil companies are already reporting lower profits (Straus and Reed 2013). Some oil companies will go bankrupt. As an example, the number two oil company in Brazil, OGX, recently filed for bankruptcy, because it could not profitably find and extract Brazil’s off-shore oil (Lorenzi and Blout 2013). Oil companies will increasingly find that the huge amount of debt that they must amass in the hope of producing profits sometime in the future is not really sustainable. The Houston Chronicle reports that an E&Y survey of Oil and Gas Companies indicates that the percentage of companies that expect to decrease debt to capital ratios jumped to 48% in October 2013 from 31% a year ago (Eaton 2013). If companies with huge debt loads cut back production to the amount that their cash flow will sustain, oil extraction can be expected to fall–just as it can be expected to fall if oil and gas companies go bankrupt or give back investment funds to shareholders. The downward path in oil production is likely to be steep, if oil prices do indeed drop. The economy depends on oil for many major functions, including most transportation, agriculture, and construction. Increasingly expensive to extract oil is a sign of diminishing returns. As we utilize more resources for extracting oil (oil, steel, water, human labor, capital, etc.), there will be fewer resources to invest in the rest of the economy, reducing its ability to grow. This lack of economic growth feeds back as low demand, bringing down the prices of commodities, including oil. It is because of this feedback loop that I believe that the path of oil prices is generally lower. This path is the opposite of what a naive reading of “supply and demand” curves from economics textbooks would suggest, and the opposite of what we need if the economy is to continue on its current path. Adverse Feedback 1: Wages stagnate as oil prices rise, tending to slow economic growth. Suppose we calculate average US wages over time, by dividing “Total Wages” by “Total Population,” (everyone, not just those working) and bring this amount to the current cost level using the CPI-Urban inflation adjustment. On this basis, US wages flattened as oil prices rose, both in the 1970s and in the 2000s. The average inflation-adjusted wage is 2% lower in 2012 ($22,040) than it was in 2004 ($22,475), even though labor productivity rose by an average of 1.7% per year during 2005-2012, according to the US Bureau of Labor Statistics. Between 1973 and 1982, average inflation-adjusted wages decreased from $17,294 to $16,265 (or 6%), even though productivity reportedly grew by an average of 1.1% per year during this period.

23 OilVoice Magazine | DECEMBER 2013

Figure 1. Average US wages compared to oil price, both in 2012$. US Wages are from Bureau of Labor Statistics Table 2.1, adjusted to 2012 using CPI-Urban inflation. Oil prices are Brent equivalent in 2012$, from BP’s 2013 Statistical Review of World Energy. To see one reason why wages might flatten, consider the situation of a manufacturer or other company shipping goods. The cost of goods, with shipping, would rise simply because of the cost of oil used in transport. Companies using oil more extensively in producing their products would need to raise prices even more, if their profits are to remain unchanged. If these companies simply pass the higher cost of oil on to consumers, they likely will sell fewer of their products, since some consumers will not be able to afford the products at the new higher price. To “fix” the problem of selling fewer goods, companies would likely lay off workers, to reflect the smaller quantity of goods sold–one reason for the drop in wages paid to workers shown on Figure 1. (Note that Figure 1 will reflect reduced wages, whether it results from fewer people working or lower wages of those working.) Another approach businesses might use to deal with the problem of rising costs due to higher oil prices would be to reduce costs other than oil, to try to keep the total cost of the product from rising. Wages are a big piece of a business’s total costs, so finding a way to keep wages down would be helpful. One such approach would be a wage freeze, or a cut in wages. Another would be to outsource production to a lower cost country. A third way would be to use increased automation. Any of these approaches would reduce wages paid in the United States. The latter two approaches would tend to have the greatest impact on the lowest paid workers. Thus, we would expect increasing wage disparity, together with the flattening or falling wages, as companies try to hold the cost of goods and services down, despite rising oil prices. The revenue received by businesses and governments ultimately comes from consumers. If the wages of lower-paid consumers flattens, these lower wages can

24 OilVoice Magazine | DECEMBER 2013

be expected to reduce economic growth, because with lower wages, these workers will have less income to buy discretionary goods and services. The higher-paid workers may have more income, but this won’t necessarily feed back into the economy well–it may inflate stock market prices, but not feed back as spending on goods and services, necessary for growth. There is even a feedback with respect to debt. The portion of the population with falling inflation-adjusted wages will find it harder to borrow, making it more difficult to buy big-ticket items such as cars and houses. Adverse Feedback 2: Consumers cut back on discretionary spending because of the higher cost of food and oil, leading to more layoffs and recession. Clearly, based on Figure 1, consumers cannot expect wage increases to match oil price increases. Even workers who work in the oil industry cannot expect wage increases equal to the increase in the price of oil, because part of the increase in cost comes from the need for more workers per barrel of oil. For example, it is more labor-intensive to extract oil from a large number of small wells, each of which require fracking, than it is to extract oil from a few larger wells, none of which require fracking. One cost that tends to increase with the cost of oil is the cost of food (Figure 2). The cost of food and the cost of commuting are necessities for most workers. They will cut down on discretionary expenditures, if necessary, to make certain these costs are covered.

Figure 2. FAO Food Price Index versus Brent spot oil price, based on US Energy Information Agency. *2013 is partial year. If wages are inadequate, workers will cut back in such area as restaurant meals, vacation travel, and charitable contributions, leading to even more problems with a

25 OilVoice Magazine | DECEMBER 2013

lack of jobs in these and other discretionary sectors. It might be noted that even countries that export oil can encounter difficulties as oil prices rise. These countries need a way to get the extra revenue from selling high-priced oil over to the many residents who must buy higher-priced food, but do not benefit from the wages paid to oil workers. It is not a coincidence that the Arab Spring uprisings took place in several oil exporting nations in early 2011, when food prices peaked on Figure 2. Adverse Feedback 3: Higher oil and food prices together with stagnating wages lead to cutbacks in spending for new cars and new homes, falling prices for new homes, defaults on home and car loans, and banks in need of bailouts. Purchasing more-expensive homes and new cars are types of discretionary spending. If consumers find their incomes are squeezed by high oil prices, they will cut back on expenditures such as these as well, leading to layoffs in the home construction and auto manufacturing industries. Such cutbacks can also result in bankruptcies of auto and home builders. If people buy fewer move-up homes, the price of resale homes will tend to fall. This in turn makes defaults on mortgages more likely. Layoffs will also tend to make defaults on mortgages more likely, as well as missed payments on auto loans.

Figure 3. S&P Case-Shiller 20-City Home Price Index, using seasonally adjusted three month average data. April 2006 is the peak month. Data is latest shown on website as of November 2013. Most people do not associate the drop in US home prices with the rise in oil prices, but the latest rise in oil prices began as early as 2003 and 2004 (see Figure 2), and the drop in home prices began in 2006. Some of the earliest drops in home prices

26 OilVoice Magazine | DECEMBER 2013

occurred in the most distant suburbs, where oil prices played the biggest role. Banks increasingly found themselves in financial trouble, as defaults on mortgages and other loans grew. These defaults are often blamed on bad underwriting. While bad underwriting may have played a role (and may also have helped prevent the US from falling into recession even earlier, when oil prices began rising), the falling prices of homes created part of the default problem, as did job layoffs associated with higher oil prices. All of these feedbacks led to a need for more government involvement–lower interest rates to try to hold the economy together, get spending back up, and raise home prices. Adverse Feedback 4: Cutbacks in consumer debt combined with flat wages appear to have led to the decline in spending that precipitated the July 2008 drop in oil prices. Consumer debt still remains depressed. Oil prices started falling in July 2008, and did not hit bottom until the winter of 2008 (Figure 4).

Figure 4. West Texas Intermediate Monthly Average Spot Price, based on us Energy Information Administration data. What could have precipitated such a fall? Many people consider the bankruptcy of Lehman Brothers on September 15, 2008 to be pivotal in the financial crisis of 2008, but the drop in oil prices started months earlier. What could have precipitated such a steep drop in oil prices? It seems to me that the real underlying cause was a mismatch between what goods cost (such as high food and oil prices) and the amount consumers had available for spending. There are two basic sources of consumer spending–wages and increases in debt. If consumer debt suddenly starts decreasing, rather than increasing,

27 OilVoice Magazine | DECEMBER 2013

consumer spending can be expected to fall (especially if wages are not rising). In fact, consumer debt did start falling at precisely the time that oil prices crashed. Mortgage debt started falling in the third quarter of 2008, reflecting a combination of falling home prices and mortgage defaults. As noted previously, both of these were indirectly related to high oil prices.

Figure 5. US Home Mortgage Debt, based on Federal Reserve Z.1 data. Other consumer debt fell at the same time. Revolving credit (primarily credit card debt) hit a peak in July 2008, and began to fall (Figure 6).

Figure 6. US Revolving Credit outstanding (primarily credit card debt), based on Federal Reserve G.19 Report.

28 OilVoice Magazine | DECEMBER 2013

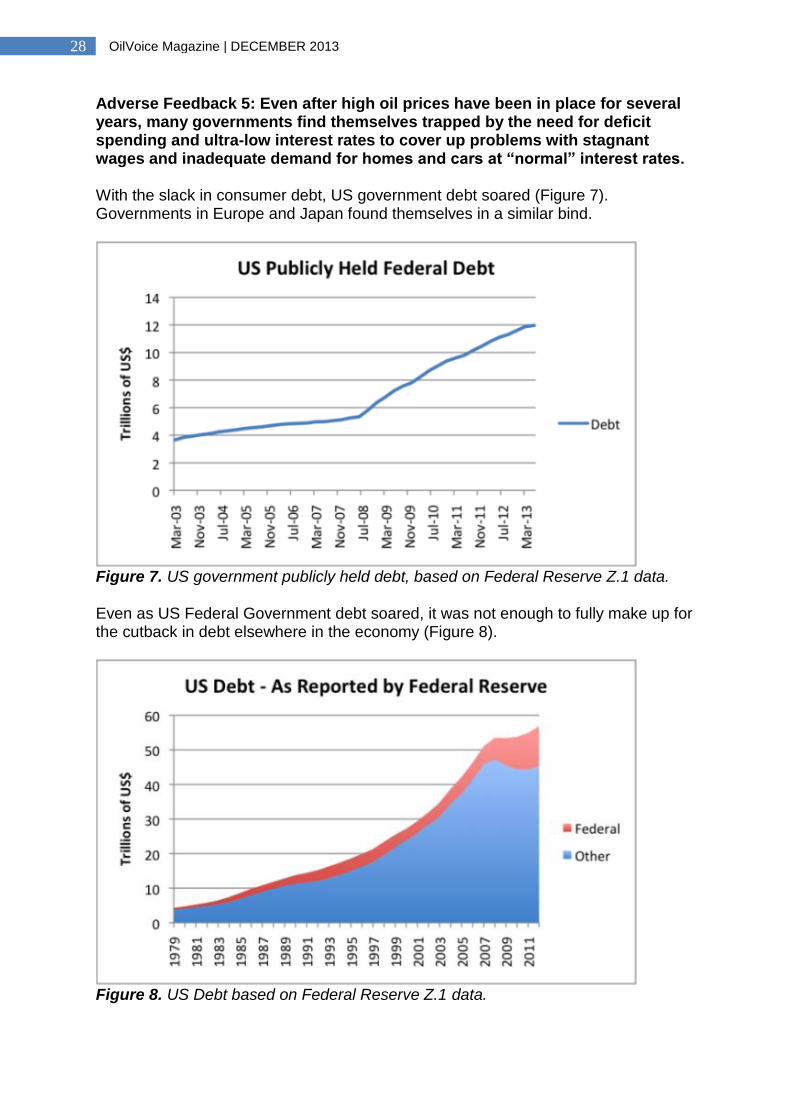

Adverse Feedback 5: Even after high oil prices have been in place for several years, many governments find themselves trapped by the need for deficit spending and ultra-low interest rates to cover up problems with stagnant wages and inadequate demand for homes and cars at “normal” interest rates. With the slack in consumer debt, US government debt soared (Figure 7). Governments in Europe and Japan found themselves in a similar bind.

Figure 7. US government publicly held debt, based on Federal Reserve Z.1 data. Even as US Federal Government debt soared, it was not enough to fully make up for the cutback in debt elsewhere in the economy (Figure 8).

Figure 8. US Debt based on Federal Reserve Z.1 data.

29 OilVoice Magazine | DECEMBER 2013

How do governments get themselves caught in such a bind? Businesses can to a significant extent overcome their problems with high oil prices by laying off workers and finding lower cost methods of production. Individuals, however, find that the wage problems persist as long as oil prices remain high and businesses have the option of replacing their services with lower cost workers elsewhere. Globalization definitely makes this problem worse. When workers have job problems, governments find themselves in the unfortunate position of trying to fix the situation by providing more unemployment benefits, food stamps, and disability benefits. Governments also find themselves with lagging tax revenue, because businesses increasingly are located in offshore tax havens, and workers’ incomes are lagging. Adverse Feedback 6: Rising prices of oil have contributed to long term inflation. If oil prices start falling, this tends to create the opposite problem–deflation. Once oil price deflation starts, it may lead to a self-reinforcing debt default cycle. Not all inflation is related to higher energy prices, but some of it is. This is one reason the US government sometimes gives an inflation estimate “excluding volatile food and energy prices.” Inflation over the years appears to be one way that a small amount of diminishing returns has fed into the economy. The concern a person has is that deflation will tend to lead to debt defaults. Clearly lower oil and gas prices mean that oil and gas businesses will become less profitable, and loans in this area will tend to default. But loans related to other types of commodities may tend to default as well. There will also tend to be layoffs in these industries, and in surrounding communities. Also, with deflation, the low interest rate policies of governments no longer have the stimulating impact that they would have without deflation. So governments will have to concoct negative interest rate plans, and see if they can make these work, to take the place of current plans. One question is how effective today’s Quantitative Easing and ultra-low interest rate programs have been. We know that they have tended to blow bubbles in asset prices, such as stock market prices. But are ultra-low interest rates part of what allowed oil prices to re-inflate after the July 2008 drop? Certainly, they have helped hold up auto and home sales, and have supported oil drilling operations that rely heavily on debt. To some extent, the current system appears to be held together with duct tape. It looks like it could fall apart on its own, or it could fall apart as governments try to reduce their deficits by higher taxes and lower spending (See Figure 7). Adding deflation to the combination would seem to be another way of making the current approach for covering up our problems even more vulnerable to collapse. The frightening thing is that there is already some evidence that oil prices (and commodity prices in general) are starting to trend downward. The chart I showed in Figure 4 showed West Texas Intermediate (WTI) oil prices–a price that is often

30 OilVoice Magazine | DECEMBER 2013

quoted in the US. On Figure 9, I show WTI oil prices alongside Brent, another oil benchmark. Brent reflects world oil prices to a greater extent than WTI price does. It seems to be showing a recent downward trend in world oil prices. To the extent that this downward trend in prices feeds back into inflation rates and makes Quantitative Easing work less well, this downward trend becomes a potential problem. Its effect would tend to offset the stimulating effect on economies that lower oil prices would normally have.

Figure 9. Brent oil price compared to West Texas Intermediate oil price, based on EIA monthly average spot prices. Conclusion Oil and other fossil fuels are unusual materials. Historically, their value to society has been far higher than their cost of extraction. It is the difference between the value to society and their cost of extraction that has helped economies around the world grow. Now, as the cost of oil extraction rises, we see this difference shrinking. As this difference shrinks, the ability of economies to grow is eroding, especially for those countries that depend most heavily on oil–Japan, Europe, and the United States. It should not be surprising if the growth of these countries slows as oil prices rise. The trend toward globalization can only make this trend worse, because it gives businesses an opportunity to lower wage costs by outsourcing part of their production to lower-cost countries (that use less oil!). When costs are reduced in this manner, businesses are also able get the “benefit” of more lax pollution laws overseas. We saw in Figure 9 that global oil prices seem already to be trending downward, as growth in countries such as China, Brazil, and India is faltering. At the same time, oil from easy to extract locations is depleting, and oil companies have no choice but move on locations where more resources of all kinds are required, leading to diminishing returns and ever-higher cost of extraction. The way I view our

31 OilVoice Magazine | DECEMBER 2013

predicament is shown in Figure 10.

Figure 10. Our Oil Price Predicament. Over time, if we want to maintain constant oil consumption, the price consumers can afford tends to fall, while the price required by oil producers in order to earn a profit tends to rise. Over time, in order to maintain constant oil production, the price consumers can afford tends to fall, because governments need to “take back” the huge deficit spending they are using now to prop up the system. At the same time, prices required by producers tend to rise, as the mix of oil production moves to more difficult locations. While in theory oil prices could spike again because of rising demand of the less developed countries, it is hard to see how this price spike could be sustained. We would likely run into the same problems we had before, with more layoffs and plus credit contraction leading to a cutback in demand in the US, the European Union, and Japan. These users represent a big enough share of the total that their drop in demand would tend to bring world prices back down. The problem this time, though, is that governments seem to be getting close to being “out of ammunition,” in trying to fight what is really diminishing returns of one of the major drivers of our economy. I don’t know exactly how things might play out, but experience with prior civilizations suggests that “collapse” might be a reasonable description of the outcome.

View more quality content from Our Finite World

33 OilVoice Magazine | DECEMBER 2013

Shale Gas - A case of what we know and what we don't know

Written by Angus Warren from Warren Business Consulting

With headlines ranging from claims that shale is the world's source of cheap gas, to those that say that fracking is the ultimate evil, you would had to be living on another planet to not have seen or read something about shale gas in the last few years. This blog by Leigh Bolton*, principal of Holmwood Consulting, challenges us to take a balanced view of shale gas: The barrage of 'print' on shale gas has been coupled with any number of industry conferences claiming to give the only answer to shale gas developments. All this has, however, probably confused rather than helped. In an effort to bring clarity, here are my top ten 'knows' and 'don't knows' on shale gas. So, what do we actually know? Firstly, we know that shale has been known by geologists for a very, very long time but no-one did very much because there was an abundance of cheap conventional gas wells for companies to develop - why do something technologically difficult and expensive when there are easy fields to develop? Secondly, there is a huge amount of shale rock around the world and it exists in almost every country, with China having probably 50% more than the USA, for example. However, we need to be careful here as we need to distinguish between large shale gas resources (what we think is present) and much smaller reserves (what we think we can technically and commercially recover). Thirdly, shale developments are a resource play as the natural gas is located everywhere throughout the shale rock formation and not accumulated in trapped reservoirs like 'conventional' plays. These shale rocks are the source rock for the conventional reservoirs. They lie at sufficiently deep levels (more than 1000m) that their organic matter has been converted into gas (rather than oil). However, we come back to those geological favourites of porosity and permeability. A large proportion of the shale gas remains trapped in the shale, since it is virtually impermeable. The gas is therefore well dispersed and held within this very dense shale rock in pores of only about 1 micron/ 1/1000 mm size. Fourthly, because of this micro-pore and no permeability situation, we are forced to

34 OilVoice Magazine | DECEMBER 2013

use horizontal drilling (to reach the maximum bed area) and hydraulic fracking (to fracture the shale rock locally and allow gas to migrate into the well) techniques. 'Fracking' has caused enormous news with misleading videos posted on the web, some (now discredited) reports on environmental effects, plus the usual 'rent a mob' protests. It is perhaps interesting to note that the oil industry has used fracking for many, many years without comment - it was only when it was further developed for shale gas development in the USA that it became headline news. Fifthly, there is no doubt that the path-finding shale developments in the USA completely changed the USA's natural gas market, moving the country to self-sufficiency and driving natural gas prices to new lows. There have been some unexpected results however in that the gas sales price has been driven so low that a number of shale gas developers have plugged their gas wells and are now producing shale oil from elsewhere in the formation or are looking to export their shale gas production as LNG to world markets in order to make sufficient returns. Additionally, there are now moves in the heartland of the Barnett shale (the first US shale field to be developed) to ban fracking inside city limits - people have made their money and are now reverting to the old NIMBY actions. Sixthly, developments in the USA are no panacea for anyone else. The USA has had a history of wildcat drilling over many years, with many service drilling companies and rigs, and thereby already knew much of the geology of the country. There was also abundant water for the fracking process. So, what do we not know? Seventhly, most countries in the world outside the USA have little knowledge of the shale geology and will need to spend probably 5 years or more just drilling to see what's there. Outside the US there has been little culture of wildcat drilling. This is the case in Europe's flagship shale gas country, Poland, where sensible production levels will not be achieved for several years yet. In China, for example, they are in the very early stages of shale development and water limitations in many areas will limit or negate any production. Eighthly, there are still concerns about subsurface movements (mini-earthquakes) and potential environmental issues. As an industry shale gas production is in its infancy and we do not have enough data to argue coherently that all is well and we are, quite frankly, doing a pretty poor job of explaining shale gas to communities. There will always be 'antis' but I am talking about the man in the street here. Ninthly, there are more and more articles and comments appearing that the US 'shale gale' might not last as rapid well production decline and other economic factors come to light. Industry observers are now using words like 'a stop gap in the market to bridge to something else' - worrying for others if the reference country and benchmark might be wobbling. Tenthly, and lastly, there is always the great unknown - we don't know what we don't know. This is just as true for shale gas as it is for the whole of the oil and gas industry.

35 OilVoice Magazine | DECEMBER 2013

So, this is a very personal view of the shale gas world. I have been accused of pessimism by some advocates and pragmatism by others in the market. I have tried not to let emotion cloud this short blog and will close by asking: 'Do we need shale gas?' The answer is, 'Definitely yes, but as a piece of the gas supply puzzle and not as the single answer to the world's gas or energy needs.' And, as additional food for thought, shale gas is described as a 'game changer' but the potential of extracting gas from methane hydrates would be a much bigger 'disruptive technology' to the energy industry. *Leigh Bolton is the principal of Holmwood Consulting Limited. a leading independent gas, LNG and power consultancy.

View more quality content from Warren Business Consulting

Will the real International Energy Agency please stand up?

Written by Kurt Cobb from Resource Insights

It was as if the International Energy Agency were appearing on the old American television game show To Tell the Truth last week as it offered a third contradictory forecast in the space of a year. You may recall that on To Tell the Truth the host would begin by reading a statement from a person with an unusual story or profession. Then, a celebrity panel would question three contestants who claimed to be that person. Afterwards, the panelists would vote on whom they believed was the real person. Finally, the host would say, "Will the real [name of person] please stand up?" (Some episodes are still available

36 OilVoice Magazine | DECEMBER 2013

here on YouTube.) The difference is that the contestants on To Tell the Truth would try to tell similar, plausible stories so as to stump the panel. In the non-game-show world of energy forecasting, the IEA--a consortium of 28 countries, all net oil importers except for Canada and Norway--plays all three contestants and does not even attempt to be consistent. So, it's possible that the agency is just a collective mental case with multiple personality disorder. However, one has to allow for the fact that the IEA is not just one person or one voice. Still, if the agency were a single person, what it has released over the last year as official pronouncements would likely have a psychiatrist reaching for the DSM-IV (Diagnostic and Statistical Manual of Mental Disorders, Fourth Edition). Last November in its 2012 World Energy Outlook (WEO), the agency noted rising U.S. oil production and even predicted that the United States would become energy self-sufficient by 2035 (a doubtful call, in my view). It also noted that growing oil demand in the Asia has more than outweighed declines in European and U.S. consumption, keeping upward pressure on prices. It said that growth in Iraq's oil exports was not a sure thing. While the 2012 WEO is really a rather optimistic document on supply, it did not paint an especially rosy picture, indicating that obtaining the supplies of oil necessary to meet projected demand was not a foregone conclusion. Then, only six months later came the agency's so-called Medium-Term Oil Market Report which read like an ad for the North American oil and gas industry. The agency touted a "supply shock" in oil from American tight oil fields unleashed by a new kind of hydraulic fracturing--a shock that would send "ripples throughout the world." Unlike six months earlier, worldwide supply was supposed to take flight on the wings of fracking. This enthusiasm didn't last long. In its latest report, the just-issued 2013 World Energy Outlook, the agency sounded like a group of Gloomy Guses noting that "Brent crude oil has averaged $110 per barrel in real terms since 2011, a sustained period of high oil prices that is without parallel in oil market history." The report goes on to say, "The capacity of technologies to unlock new types of resources, such as light tight oil (LTO) and ultra-deepwater fields, and to improve recovery rates in existing fields is pushing up estimates of the amount of oil that remains to be produced. But this does not mean that the world is on the cusp of a new era of oil abundance." The most recent forecast calls for rising oil prices in real terms through 2035. This is in part because the agency expects that "no country replicates the level of success with LTO" that we are seeing in the United States today. What's really happening here? Is the IEA getting better at seeing the future? Not really. What's happening is that the IEA is being asked to do something which it cannot possibly do: accurately predict oil supplies 22 years into the future. So, given this impossible task, the agency responds by following current trends (and industry hype) and then extrapolating them.

37 OilVoice Magazine | DECEMBER 2013

Now that the IEA has had a chance to re-examine the industry's claims in light of more experience with tight oil development, it is backing off its previous assessment in its Medium-Term Oil Market Report from May. Fatih Birol, chief economist for the IEA, told the Financial Times that he would now characterize rising oil production in the United States as "a surge, rather than a revolution." He expects OPEC to become dominant once again in oil markets early in the next decade. The Financial Times characterized the report as predicting an oil supply crunch. But, will the IEA have a change of heart once again? It might, depending on what it hears from industry sources and what it chooses to believe. But, the takeaway from the last year of IEA projections is not that the agency is suffering some sort of breakdown, but that it has been given an impossible task that in the volatile world of oil supplies has it casting about for a coherent story. In short, it is trying to tell the truth without knowing the truth for the simple reason that in this case the truth cannot known. That has made it a poor contestant in its own real-life episode of To Tell the Truth stretched out over the past year. It is a fool's errand to try to predict the future of world energy supplies. But, it is even more foolish to base our public policy, business and personal decisions on such predictions. P. S. There is a minor acknowledgement that such forecasts are exercises in futility in a disclaimer at the end of the 2013 World Energy Outlook summary. The disclaimer reads: "The IEA makes no representation or warranty, express or implied, in respect of the publication’s contents (including its completeness or accuracy) and shall not be responsible for any use of, or reliance on, the publication." This is standard boilerplate, I know. But, it is not the kind of language that inspires confidence.

View more quality content from Resource Insights

Upcoming Events and

Training Courses

Reserve your place at FindingPetroleum.com

Events

Finding opportunities in the Middle East ...to be avoided or too good to turn down? London, 12 Dec 2013 Oil in North West Europe ...will independence of supply just be a mirage? London, 23 Jan 2014 Advances in Seismic Technology ...seismic technology powers on! London, 06 Feb 2014 Leading edge exploration in Africa ...invest in Africa! London, 26 Mar 2014 Global Hotspots ...are we at a nodal point? London, 22 Apr 2014

Training Courses

An introduction to shale gas (& oil) for non-geoscientists London, 12 Feb 2014 £500 per place Play Fairway Analysis London, 12 Mar 2014 £500 per place Introduction to Oil and Gas Exploration and Production London, 08 Apr 2014 £500 per place

39 OilVoice Magazine | DECEMBER 2013

A simple new fracking technique that could revolutionize the oil sector

Written by Keith Schaefer from Oil & Gas Investments Bulletin

I want to tell you about a new development in fracking that’s getting some press down in the US. This is actually pretty simple, but if I’m correct in interpreting this, it would be quite important in the global oil patch. From what I can tell, EOG Resources is increasing IP rates in the Bakken simply by changing the way they frack—from long skinny fracks into formations, into wide short ones that stay much closer to the well bore. And–this is the important part—they say first-year decline rates are going down a lot, and total oil recovered is going up a lot. In doing the shorter, wider fracks, they use a lot more sand and water to create more rock face/surface to liberate more oil from the stock. One of the other companies to evidently first use this method is Whiting (WLL-NYSE), and this slide comes from their powerpoint that visually shows what I’m trying to say:

“In the next five years, everybody is going to be doing this,” says author Michael Filloon, who wrote about this very simple new fracking strategy recently at www.SeekingAlpha.com. It was the first story I’ve seen anywhere on this issue. “I think it will work in every play in the US,” he adds.

40 OilVoice Magazine | DECEMBER 2013

Filloon got onto the story after noticing EOG was handily beating quarterly expectations (they sure have a great stock chart!) and yet there was no conclusive talk from management on the quarterly conference calls to explain why. So Filloon went online into the North Dakota public data on EOG’s wells and plotted the data himself, working backward to figure out IP rates and decline rates. It was great investigative reporting. (You should all follow Michael at SeekingAlpha!) His story—link below—is a little technical, but the charts he uses shows the depletion rates for wells getting lower—meaning the high initial production doesn’t fall off a cliff like the industry has become used to. There aren’t a lot of data points yet, and they are almost all from EOG, (though supported by the Whiting presentation above which came out at a JP Morgan conference recently) but they point to larger IP rates and lower declines using a wider, shallower frack that uses a lot more sand (called proppant, as it props open the frack pores) and water. Here’s the story: http://seekingalpha.com/article/1755982-bakken-update-frac-sand-pricing-could-go-parabolic-as-eog-resources-well-design-revolutionizes-unconventional-oil-production EOG is showing some BIG jumps in the EUR of their Bakken wells in their powerpoint. EUR stands for Estimated Ultimate Recovery—how much oil they actually expect to get out of their wells.”Some of these wells have EURs of two million barrels of oil equivalent–that’s unheard of,” says Filloon. At the same time, EOG is showing that well costs are coming down. If it’s all true…what does this mean? Well, the data is suggesting this could greatly reduce the initial hyperbolic decline in tight oil in North America. In other words, these wells would produce stronger for longer out of the gate, and recover a lot more oil than before. That would be big—NO, it would be huge. That speaks directly to my recent story, which showed cash flows are expanding perboe for producers now—so they can weather a drop in the oil price and likely have steady cash flow. It almost sounds too good to be true, except the Bakken stocks and frack sand stocks took off at the same time in mid-August. Interesting. It should mean more production per well, more oil. More supply should mean lower oil prices. That’s good for refiners, but of course gasoline prices will fall too—but likely not as much as it’s allowed to be exported.

41 OilVoice Magazine | DECEMBER 2013