oer corporate presentation september 2015 q2 · corporate presentation september 2015 energy...

TRANSCRIPT

CORPORATEPRESENTATION

September 2015

Energy Resources Inc.

Disclaimer

This presentation includes certain forward looking statements with respect to certain development projects, potential collaborative partnerships, results of operations and certain plans and objectives of the Company including, in particular and without limitation, the statements regarding potential sales revenues from projects, both current and under development, possible launch dates for new projects, ability to successfully integrate acquisitions or achieve production targets, and any revenue and profit guidance. By their very nature forward looking statements involve risk and uncertainty that could cause actual results and developments to differ materially from those expressed or implied. The significant risks related to the Company’s business which could cause the Company’s actual results and developments to differ materially from those forward looking statements are discussed in the Company’s annual report and other filings. All forward looking statements in this presentation are based on information known to the Company on the date hereof. The Company will not publicly update or revise any forward looking statements, whether as a result of new information, future events or otherwise, other than is required by law.

Past performance is no guide to future performance and persons needing advice should consult an independent financial adviser. All estimates of reserves and resources are classified in line with NI 51-101 regulations and Canadian Oil & Gas Evaluation Handbook standards. All estimates are from

stIndependent Reserves Evaluator Report having an effective date of 31 December 2014. BOEs [or McfGEs, or other applicable units of equivalency] may be misleading, particularly if used in isolation. A BOE conversion ratio of 6 Mcf: 1 bbl [or an McfGE conversion ratio of 1 bbl: 6 Mcf] is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

The estimates of reserves and future net revenue for individual properties may not reflect the same confidence level as estimates of reserves and future net revenue for all properties, due to the effects of aggregation.

Reserves: Reserves are volumes of hydrocarbons and associated substances estimated to be commercially recoverable from known accumulations from a given date forward by established technology under specified economic conditions and government regulations. Specified economic conditions may be current economic conditions in the case of constant price and un-inflated cost forecasts (as required by many financial regulatory authorities) or they may be reasonably anticipated economic

conditions in the case of escalated price and inflated cost forecasts.

Possible Reserves: Possible reserves are quantities of recoverable hydrocarbons estimated on the basis of engineering and geological data that are less complete and less conclusive than the data used in estimates of probable reserves. Possible reserves are less certain to be recovered than proved or probable reserves which means for purposes of reserves classification there is a 10% probability that more than these reserves will be recovered, i.e. there is a 90% probability that less than these reserves will be recovered. This category includes those reserves that may be recovered by an enhanced recovery scheme that is not in operation and where there is reasonable doubt as to its chance of success.

Proved Reserves: Proved reserves are those reserves that can be estimated with a high degree of certainty on the basis of an analysis of drilling, geological, geophysical and engineering data. A high degree of certainty generally means, for the purposes of reserve classification, that it is likely that the actual remaining quantities recovered will exceed the estimated proved reserves and there is a 90% confidence that at least these reserves will be produced, i.e. there is only a 10% probability that less than these reserves will be recovered. In general reserves are considered proved only if supported by actual production or formation testing. In certain instances proved reserves may be assigned on the basis of log and/or core analysis if analogous reservoirs are known to be economically productive. Proved reserves are also assigned for enhanced recovery processes which have been demonstrated to be economically and technically successful in the reservoir either by pilot testing or by analogy to installed projects in analogous reservoirs.

Probable Reserves: Probable reserves are quantities of recoverable hydrocarbons estimated on the basis of engineering and geological data that are similar to those used for proved reserves but that lack, for various reasons, the certainty required to classify the reserves are proved. Probable reserves are less certain to be recovered than proved reserves; which means, for purposes of reserves classification, that there is 50% probability that more than the Proved plus Probable Additional reserves will actually be recovered. These include reserves that would be recoverable if a more efficient recovery mechanism develops than was assumed in estimating proved reserves; reserves that depend on successful work-over or mechanical changes for recovery; reserves that require infill drilling and reserves from an enhanced recovery process which has yet to be established and pilot tested but appears to have favorable conditions

OER

This presentation does not constitute an invitation to underwrite, subscribe for, or otherwise acquire or dispose of any Oando Energy Resources Inc (the “Company”) shares or other securities.

2

3

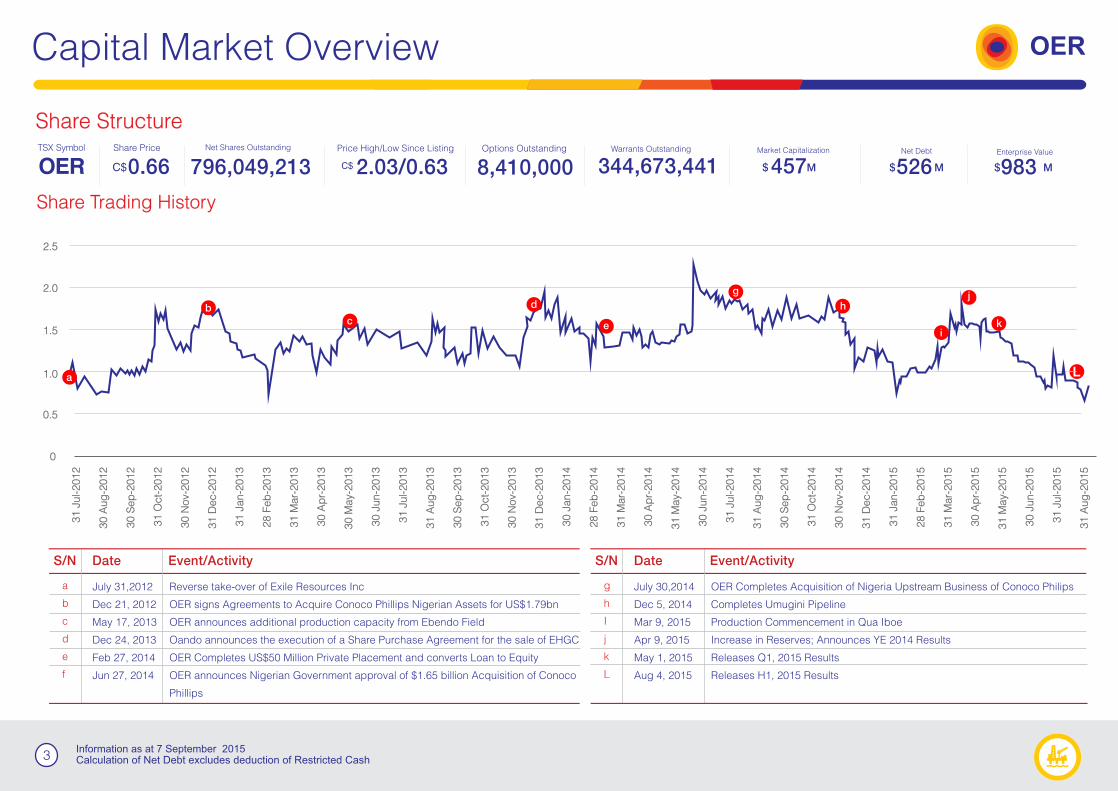

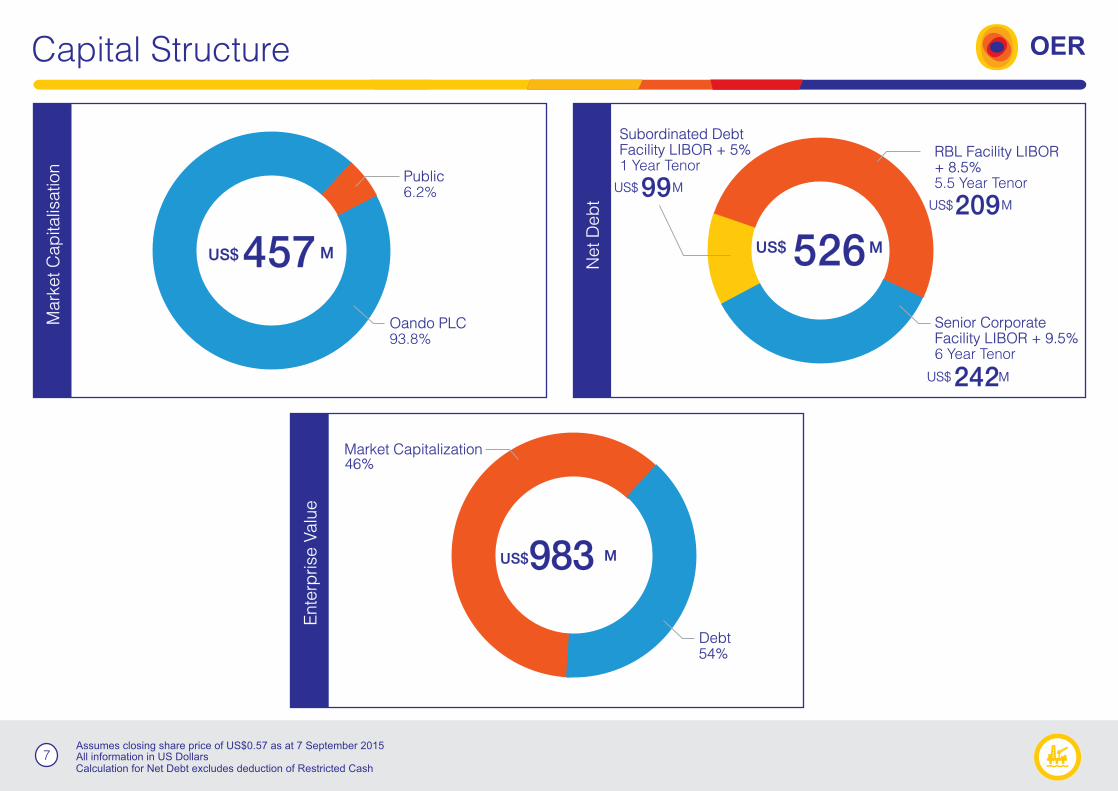

Share Structure

9830.66 2.03/0.63 344,673,4418,410,000Enterprise ValueMarket Capitalization Net Debt

457$ 526$ MM $ M

Capital Market Overview

Information as at 7 September 2015

OER

Share Trading History

796,049,213

Calculation of Net Debt excludes deduction of Restricted Cash

Date Event/ActivityS/N

Reverse take-over of Exile Resources Inc

OER signs Agreements to Acquire Conoco Phillips Nigerian Assets for US$1.79bn

OER announces additional production capacity from Ebendo Field

Oando announces the execution of a Share Purchase Agreement for the sale of EHGC

OER Completes US$50 Million Private Placement and converts Loan to Equity

OER announces Nigerian Government approval of $1.65 billion Acquisition of Conoco

Phillips

July 31,2012

Dec 21, 2012

May 17, 2013

Dec 24, 2013

Feb 27, 2014

Jun 27, 2014

a

b

c

d

e

f

Date Event/ActivityS/N

OER Completes Acquisition of Nigeria Upstream Business of Conoco Philips

Completes Umugini Pipeline

Production Commencement in Qua Iboe

Increase in Reserves; Announces YE 2014 Results

Releases Q1, 2015 Results

Releases H1, 2015 Results

July 30,2014

Dec 5, 2014

Mar 9, 2015

Apr 9, 2015

May 1, 2015

Aug 4, 2015

g

h

I

j

k

L

L

31 J

ul-2012

30 A

ug

-2012

30 S

ep

-2012

31 O

ct-

2012

30 N

ov-

2012

31 D

ec-2

012

31 J

an-2

013

28 F

eb

-2013

31 M

ar-

2013

30 A

pr-

2013

30 M

ay-

2013

30 J

un-2

013

31 J

ul-2013

31 A

ug

-2013

30 S

ep

-2013

31 O

ct-

2013

30 N

ov-

2013

31 D

ec-2

013

30 J

an-2

014

28 F

eb

-2014

31 M

ar-

2014

30 A

pr-

2014

31 M

ay-

2014

30 J

un-2

014

31 J

ul-2014

31 A

ug

-2014

30 S

ep

-2014

31 O

ct-

2014

30 N

ov-

2014

31 D

ec-2

014

31 J

an-2

015

28 F

eb

-2015

31 M

ar-

2015

30 A

pr-

2015

31 M

ay-

2015

30 J

un-2

015

31 J

ul-2015

31 A

ug

-2015

db

a

0.5

0

1.0

1.5

2.0

2.5

c e

g

h

i

j

k

4

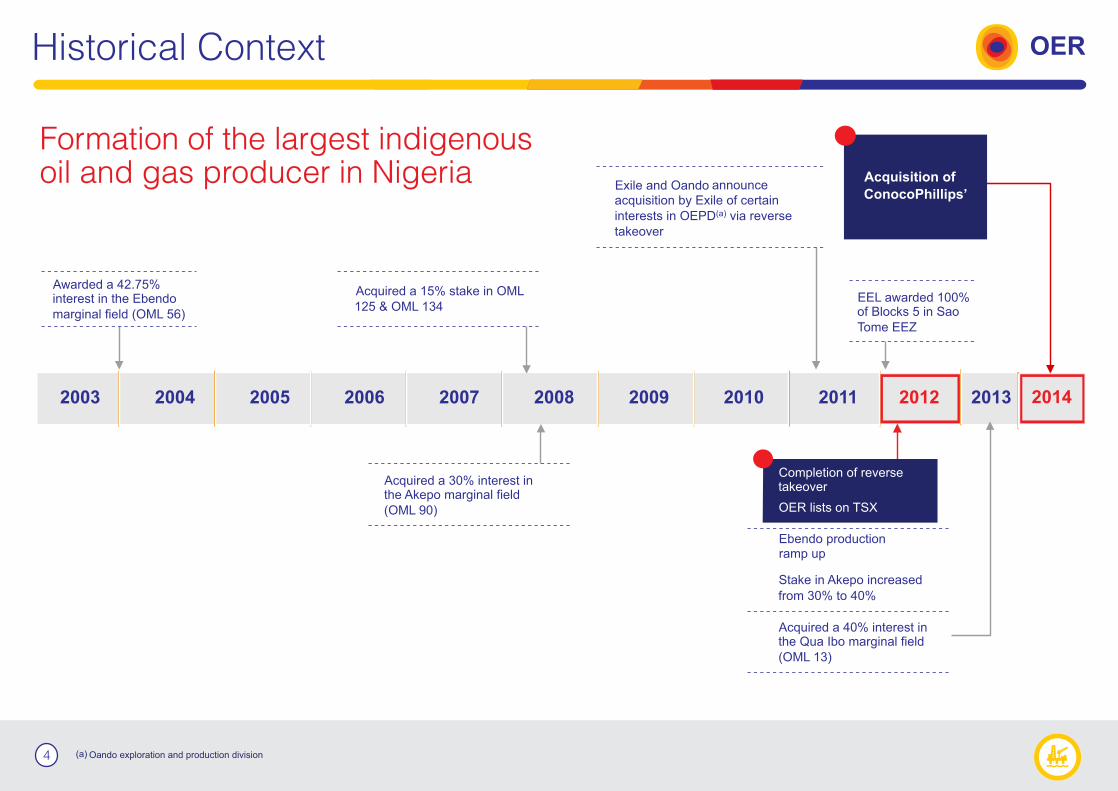

Historical Context

Ebendo productionramp up

OER

Formation of the largest indigenous oil and gas producer in Nigeria

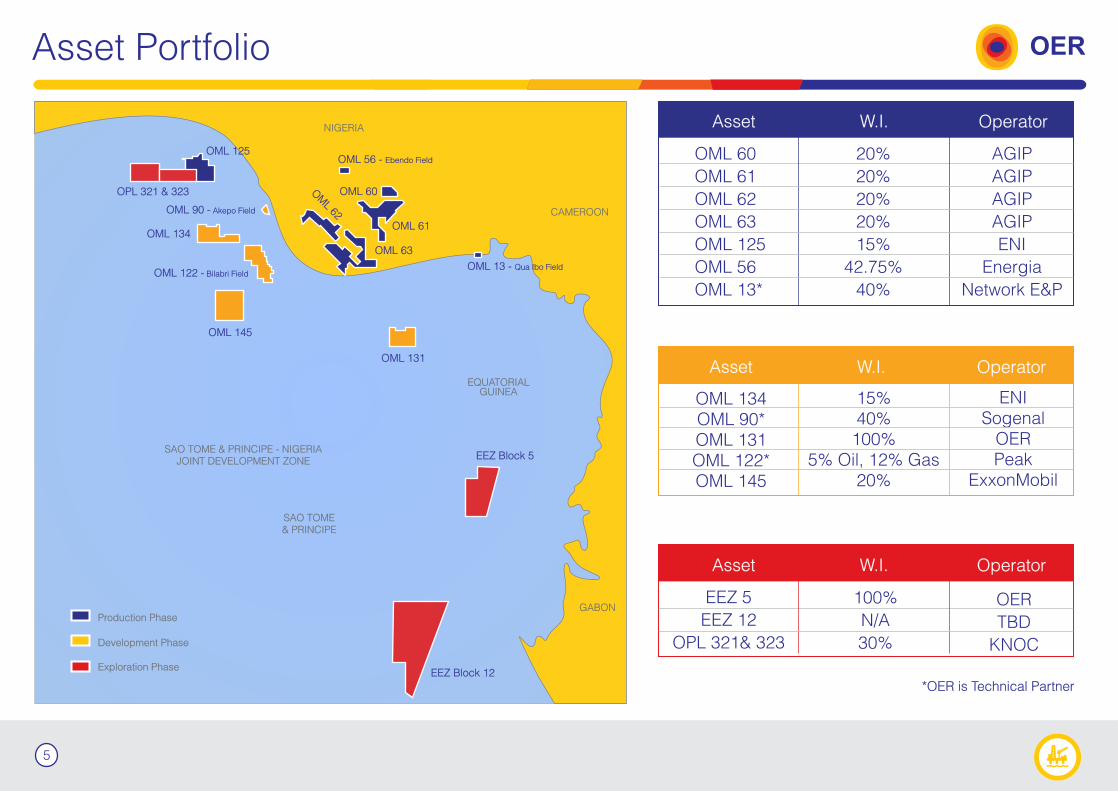

Asset Portfolio OER

5

OML 60

OML 61

OML 62

OML 63

OML 125

OML 56

OML 13*

20%

20%

20%

20%

15%

42.75%

40%

AGIP

AGIP

AGIP

AGIP

ENI

Energia

Network E&P

Asset W.I. Operator

OML 134OML 90*OML 131OML 122*OML 145

15%40%100%

5% Oil, 12% Gas20%

ENISogenal

OERPeak

ExxonMobil

Asset W.I. Operator

EEZ 5

EEZ 12

OPL 321& 323

100%

N/A

30%

OER

TBD

KNOC

Asset W.I. Operator

OML 125

NIGERIA

OPL 321 & 323

OML 134

OML 122 - Bilabri Field

OML 90 - Akepo Field

OML 56 - Ebendo Field

CAMEROON

EQUATORIALGUINEA

EEZ Block 5

SAO TOME& PRINCIPE

Production Phase

Development Phase

Exploration Phase

SAO TOME & PRINCIPE - NIGERIAJOINT DEVELOPMENT ZONE

GABON

EEZ Block 12

OML 145

OML 131

OM

L 62

OML 60

OML 61

OML 63

OML 13 - Qua Ibo Field

*OER is Technical Partner

6

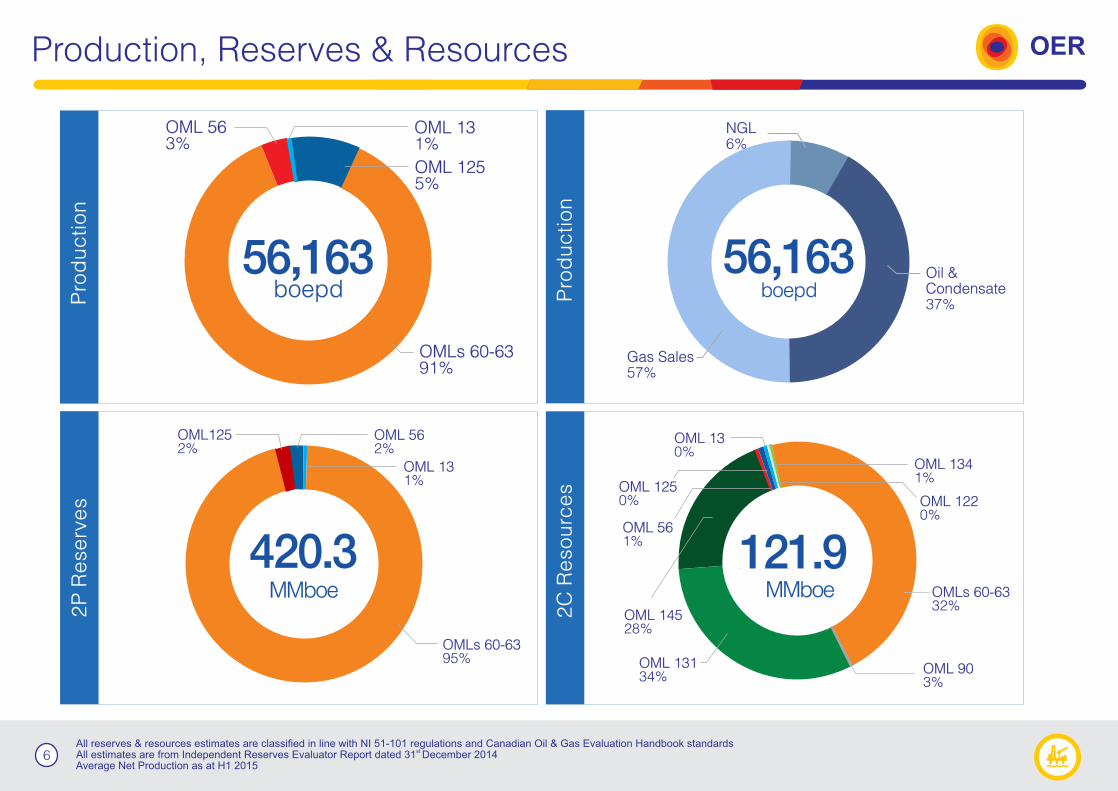

Production, Reserves & Resources

All reserves & resources estimates are classified in line with NI 51-101 regulations and Canadian Oil & Gas Evaluation Handbook standards stAll estimates are from Independent Reserves Evaluator Report dated 31 December 2014

Average Net Production as at H1 2015

OER2

P R

ese

rve

s

2C

Re

so

urc

es

Pro

du

ctio

n

OMLs 60-6332%

OML 145 28%

121.9MMboe

OML 131 34%

OML 13 0%

OML 134 1%

OML 122 0%

OML 56 1%

OML 125 0%

56,163

OML 56 3%

boepd

OML 125 5%

OMLs 60-6391%

420.3MMboe

OML 562%

OMLs 60-6395%

OML1252%

OML 131%

OML 13 1%

Pro

du

ctio

n

Oil & Condensate37%

NGL6%

Gas Sales57%

56,163boepd

OML 903%

7

Capital Structure

Assumes closing share price of US$0.57 as at 7 September 2015All information in US Dollars

OERM

ark

et C

ap

italis

ation

Oando PLC 93.8%

Public 6.2%

US$ M

Net D

eb

t

526

Subordinated DebtFacility LIBOR + 5%1 Year Tenor

RBL Facility LIBOR + 8.5% 5.5 Year Tenor

US$ M

Ente

rprise

Valu

e

Debt54%

Market Capitalization46%

US$

Senior CorporateFacility LIBOR + 9.5% 6 Year Tenor

M

Calculation for Net Debt excludes deduction of Restricted Cash

457

983

209US$ M

242US$ M

99US$ M

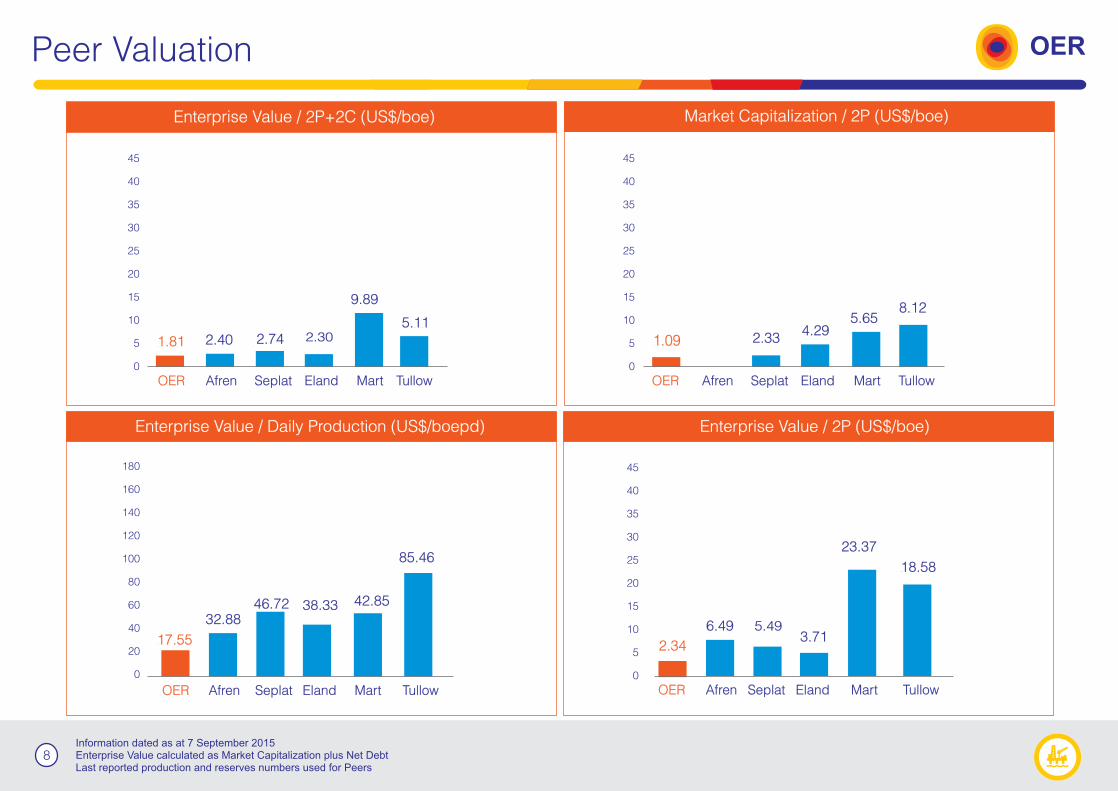

8Information dated as at 7 September 2015Enterprise Value calculated as Market Capitalization plus Net DebtLast reported production and reserves numbers used for Peers

Peer Valuation OER

Enterprise Value / Daily Production (US$/boepd)

OER Afren Seplat Eland Mart Tullow

180

160

140

120

100

80

60

40

20

0

Enterprise Value / 2P (US$/boe)

Market Capitalization / 2P (US$/boe)

OER Afren Seplat Eland Mart Tullow

45

40

35

30

25

20

15

10

5

0

Enterprise Value / 2P+2C (US$/boe)

OER Afren Seplat Eland Mart Tullow

45

40

35

30

25

20

15

10

5

0

OER Afren Seplat Eland Mart Tullow

45

40

35

30

25

20

15

10

5

0

1.81 2.40 2.74 2.30

9.89

5.11

1.09 2.334.29

5.658.12

17.55

32.8846.72 38.33 42.85

85.46

2.34

6.49 5.493.71

23.37

18.58

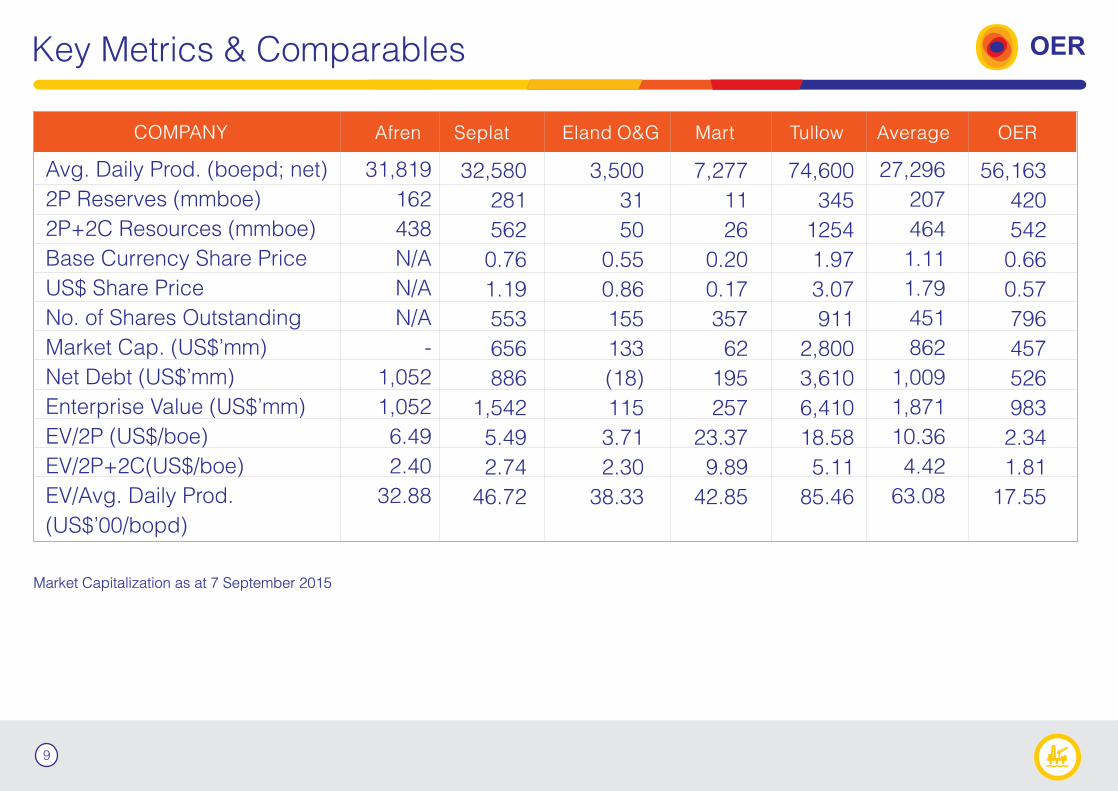

Key Metrics & Comparables

Market Capitalization as at 7 September 2015

OER

9

Avg. Daily Prod. (boepd; net)

2P Reserves (mmboe)

2P+2C Resources (mmboe)

Base Currency Share Price

US$ Share Price

No. of Shares Outstanding

Market Cap. (US$’mm)

Net Debt (US$’mm)

Enterprise Value (US$’mm)

EV/2P (US$/boe)

EV/2P+2C(US$/boe)

EV/Avg. Daily Prod.

(US$’00/bopd)

COMPANY Afren Seplat Eland O&G Mart Tullow Average OER

31,819

162

438

N/A

N/A

N/A

-

1,052

1,052

6.49

2.40

32.88

32,580

281

562

0.76

1.19

553

656

886

1,542

5.49

2.74

46.72

3,500

31

50

0.55

0.86

155

133

(18)

115

3.71

2.30

38.33

7,277

11

26

0.20

0.17

357

62

195

257

23.37

9.89

42.85

74,600

345

1254

1.97

3.07

911

2,800

3,610

6,410

18.58

5.11

85.46

27,296

207

464

1.11

1.79

451

862

1,009

1,871

10.36

4.42

63.08

56,163

420

542

0.66

0.57

796

457

526

983

2.34

1.81

17.55

Exploration & Production Growth Strategy OER

GROWTHSTRATEGY

Competitive Advantage

Indigenous status and capacityPresence in local communities, local partnerships and relationshipsCapital raising capabilities, through TSX listing

Value Drivers

De-risk existing resources portfolio and bring both existing and new assets on-streamCreate sole-risk opportunities within NAOC JVAcquisition of proven reserves and near term producing assetsReduce crude oil theft by improved surveillance and securityIncrease protable production through eld exploitation & improved reservoir management

Identication, access & acquisition of opportunities in the O&G Industry

Marginal eld programmesIOCs divestment plansGovernment bid roundsM&A activity

Disciplined approach to capitalstructure & valuation

Financial disciplineBalance sheet restructuringDebt reductionLower risk

Growing Reserves & Resources

10

11

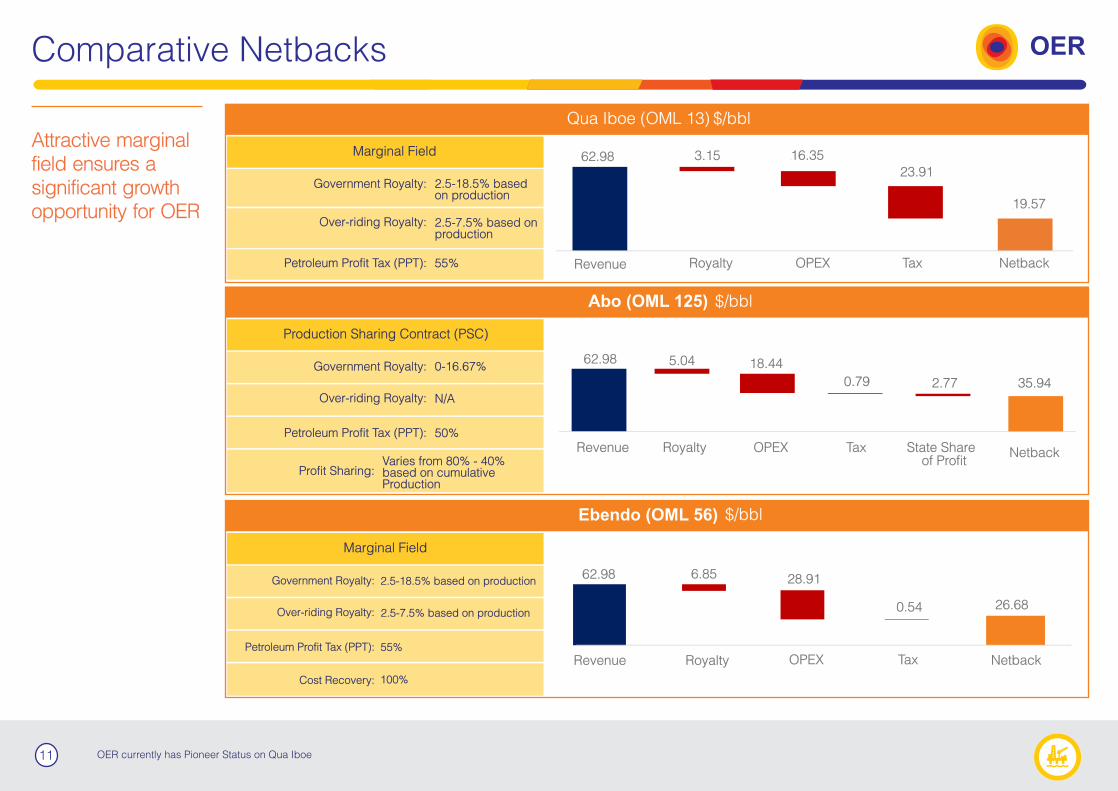

Comparative Netbacks OER

Attractive marginal field ensures a significant growth opportunity for OER

$/bbl

$/bbl

Production Sharing Contract (PSC)

Government Royalty:

Over-riding Royalty:

Petroleum Profit Tax (PPT):

Profit Sharing:

0-16.67%

N/A

50%

Varies from 80% - 40%based on cumulative Production

Marginal Field

Government Royalty:

Over-riding Royalty:

Petroleum Profit Tax (PPT):

Cost Recovery:

2.5-18.5% based on production

55%

100%

2.5-7.5% based on production

$/bbl

Marginal Field

Government Royalty:

Over-riding Royalty:

Petroleum Profit Tax (PPT):

2.5-18.5% basedon production

2.5-7.5% based on production

55%

Qua Iboe (OML 13)

62.98 5.04 18.44

0.79 2.77

Revenue Royalty OPEX Tax State Shareof Profit

62.98 6.85 28.91

0.54

Revenue Royalty OPEX Tax

62.98

Revenue Royalty OPEX Netback

35.94

Netback

26.68

Tax

3.15 16.3523.91

19.57

Netback

OER currently has Pioneer Status on Qua Iboe

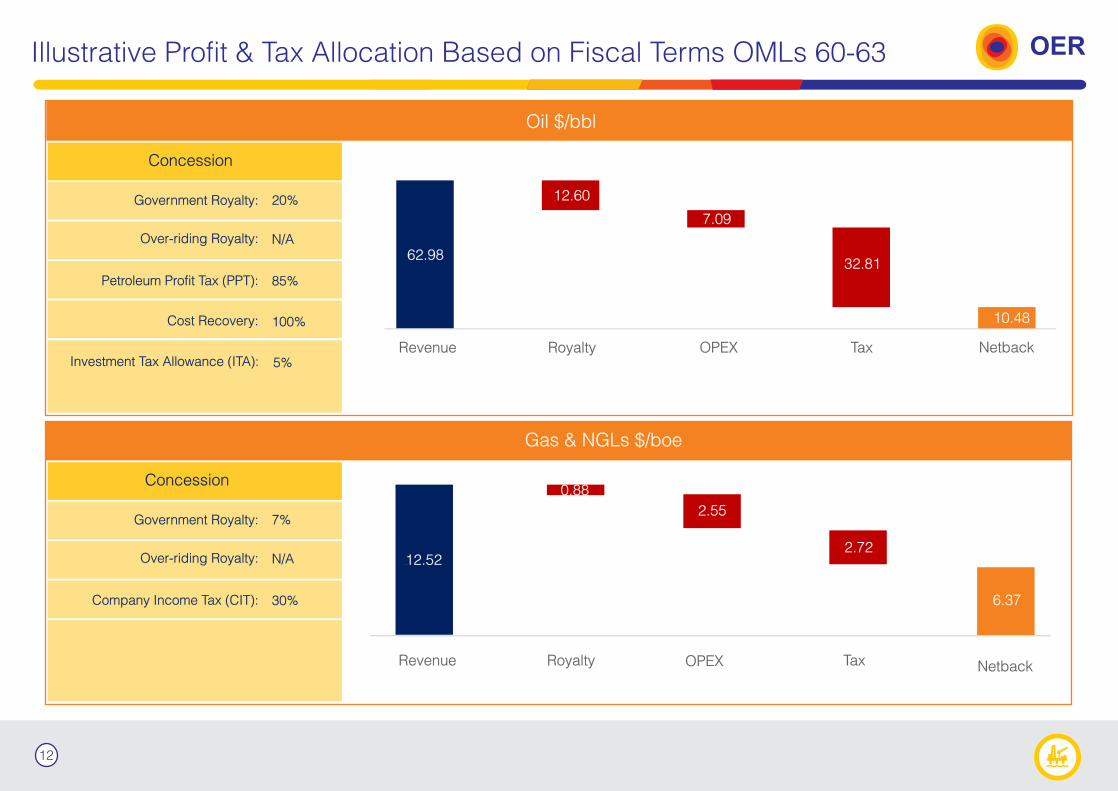

Illustrative Profit & Tax Allocation Based on Fiscal Terms OMLs 60-63 OER

12

Gas & NGLs $/boe

Oil $/bbl

Concession

Government Royalty:

Over-riding Royalty:

Petroleum Profit Tax (PPT):

Cost Recovery:

Investment Tax Allowance (ITA):

20%

N/A

85%

100%

5%

Concession

Government Royalty:

Over-riding Royalty:

Company Income Tax (CIT):

7%

N/A

30%

62.98

12.60

7.09

32.81

Revenue Royalty OPEX Tax Netback

12.52

0.88

2.55

2.72

6.37

Revenue Royalty OPEX Tax Netback

10.48

13

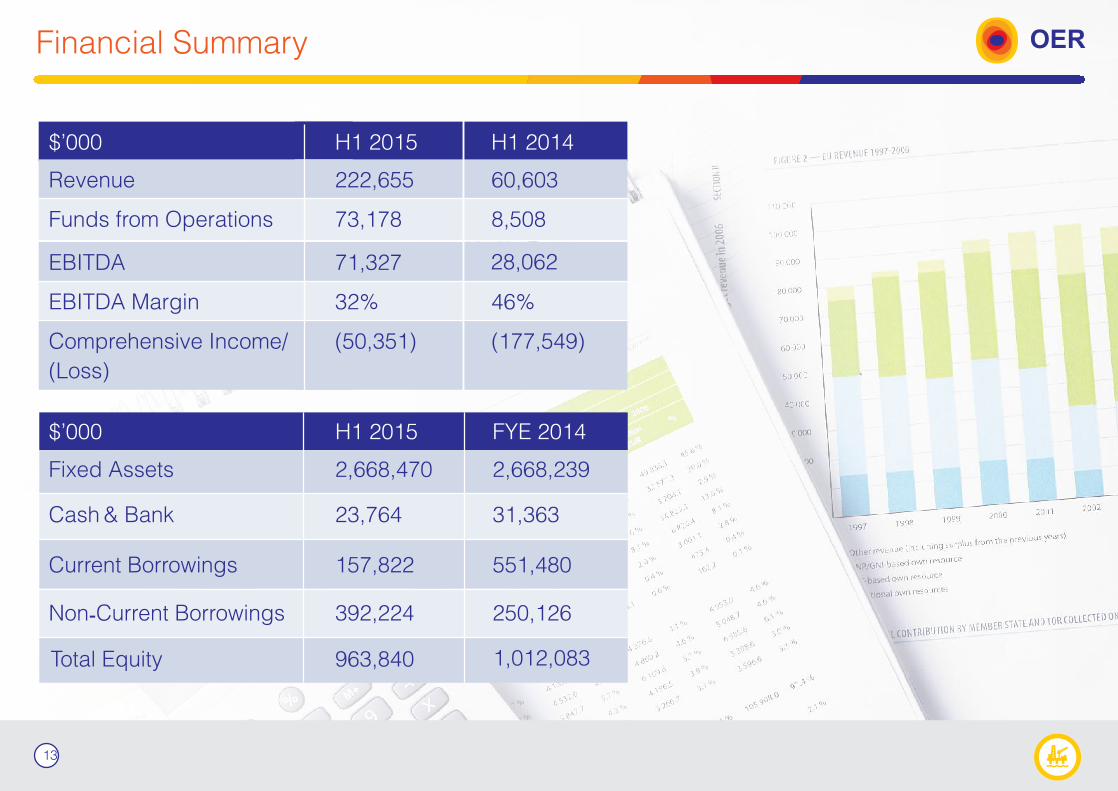

Financial Summary OER

$’000 H1 2015 H1 2014

Revenue 222,655 60,603

Funds from Operations 73,178 8,508

EBITDA 71,327 28,062

EBITDA Margin 32% 46%

Comprehensive Income/

(Loss)

(50,351) (177,549)

$’000 H1 2015 FYE 2014

Fixed Assets 2,668,470 2,668,239

Cash & Bank 23,764 31,363

Current Borrowings 157,822 551,480

Non-Current Borrowings 392,224 250,126

Total Equity 963,840 1,012,083

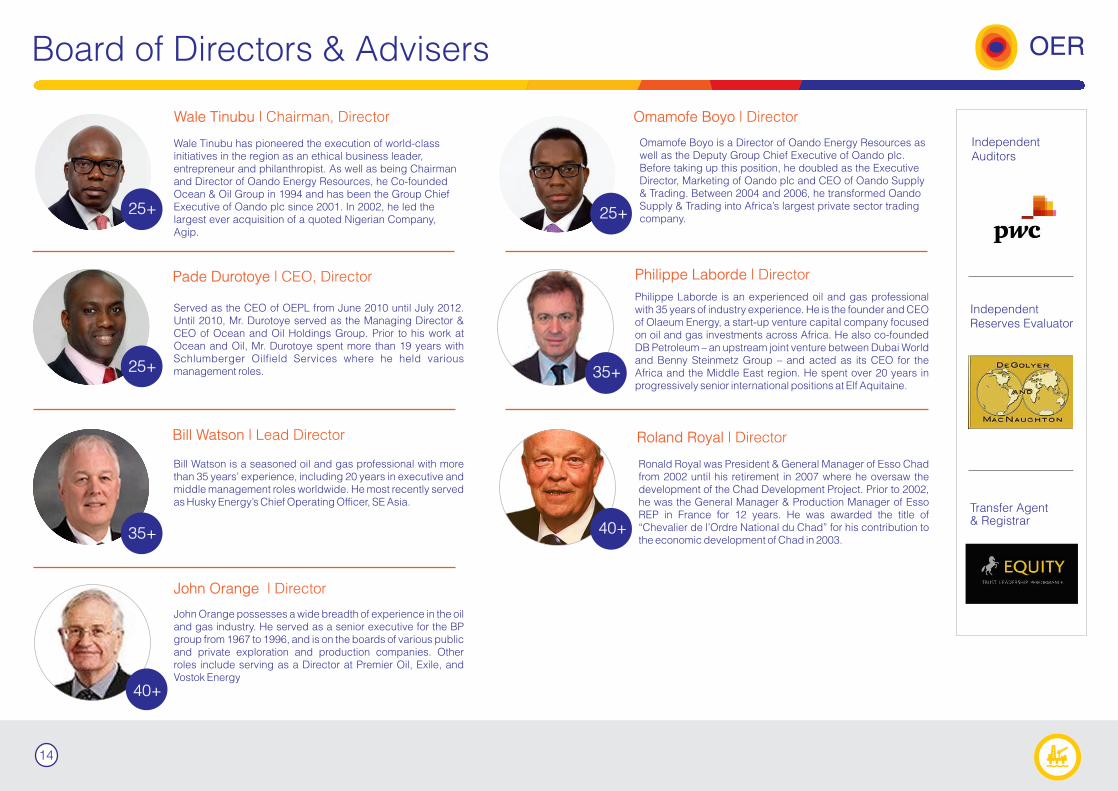

Omamofe Boyo is a Director of Oando Energy Resources as well as the Deputy Group Chief Executive of Oando plc. Before taking up this position, he doubled as the Executive Director, Marketing of Oando plc and CEO of Oando Supply & Trading. Between 2004 and 2006, he transformed Oando Supply & Trading into Africa’s largest private sector trading company.

Board of Directors & Advisers OER

Independent Auditors

Transfer Agent & Registrar

Independent Reserves Evaluator

Bill Watson | Lead Director

Wale Tinubu | Chairman, Director Omamofe Boyo | Director

John Orange | Director

Wale Tinubu has pioneered the execution of world-class initiatives in the region as an ethical business leader, entrepreneur and philanthropist. As well as being Chairman and Director of Oando Energy Resources, he Co-founded Ocean & Oil Group in 1994 and has been the Group Chief Executive of Oando plc since 2001. In 2002, he led the largest ever acquisition of a quoted Nigerian Company, Agip.

Bill Watson is a seasoned oil and gas professional with more than 35 years’ experience, including 20 years in executive and middle management roles worldwide. He most recently served as Husky Energy’s Chief Operating Officer, SE Asia.

John Orange possesses a wide breadth of experience in the oil and gas industry. He served as a senior executive for the BP group from 1967 to 1996, and is on the boards of various public and private exploration and production companies. Other roles include serving as a Director at Premier Oil, Exile, and Vostok Energy

25+ 25+

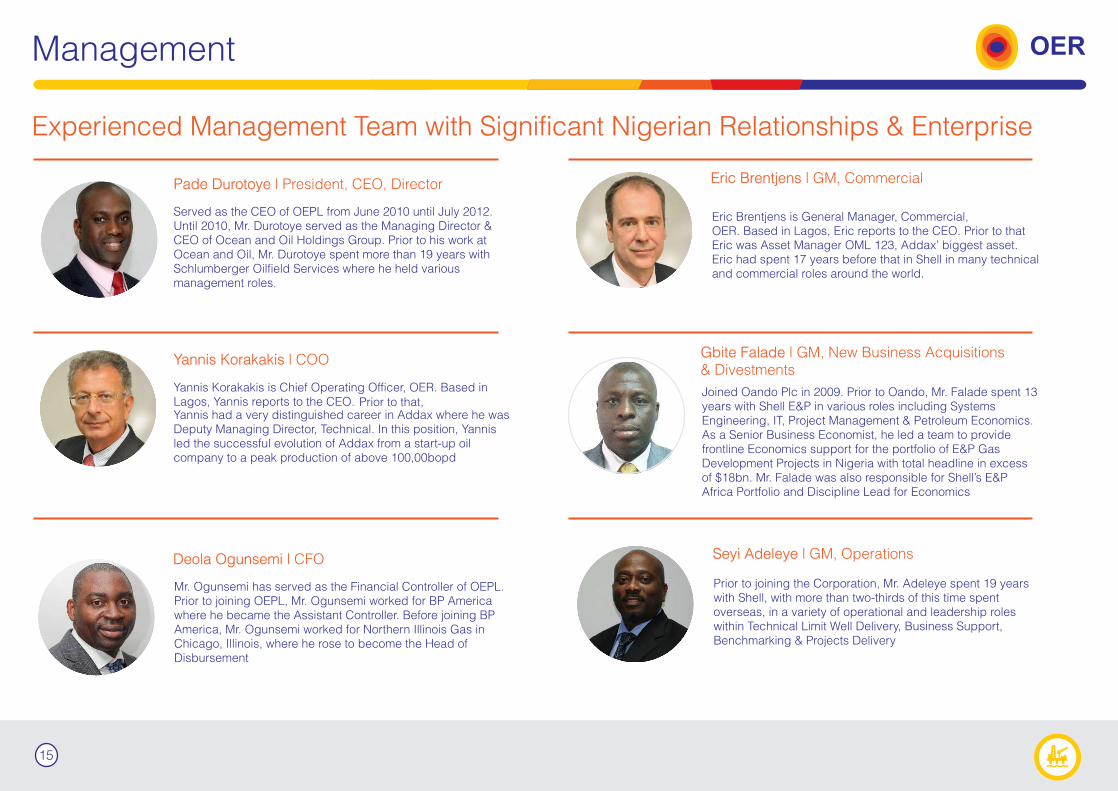

Pade Durotoye | CEO, Director

Served as the CEO of OEPL from June 2010 until July 2012. Until 2010, Mr. Durotoye served as the Managing Director & CEO of Ocean and Oil Holdings Group. Prior to his work at Ocean and Oil, Mr. Durotoye spent more than 19 years with Schlumberger Oilfield Services where he held various management roles.25+

35+

40+

Philippe Laborde | Director

Philippe Laborde is an experienced oil and gas professional with 35 years of industry experience. He is the founder and CEO of Olaeum Energy, a start-up venture capital company focused on oil and gas investments across Africa. He also co-founded DB Petroleum – an upstream joint venture between Dubai World and Benny Steinmetz Group – and acted as its CEO for the Africa and the Middle East region. He spent over 20 years in progressively senior international positions at Elf Aquitaine.

35+

Roland Royal | Director

Ronald Royal was President & General Manager of Esso Chad from 2002 until his retirement in 2007 where he oversaw the development of the Chad Development Project. Prior to 2002, he was the General Manager & Production Manager of Esso REP in France for 12 years. He was awarded the title of “Chevalier de l’Ordre National du Chad” for his contribution to the economic development of Chad in 2003.

40+

14

Management

Gbite Falade | GM, New Business Acquisitions & Divestments

Yannis Korakakis | COO

Pade Durotoye | President, CEO, Director

Deola Ogunsemi | CFO Seyi Adeleye | GM, Operations

Eric Brentjens | GM, Commercial

OER

Experienced Management Team with Significant Nigerian Relationships & Enterprise

Served as the CEO of OEPL from June 2010 until July 2012. Until 2010, Mr. Durotoye served as the Managing Director & CEO of Ocean and Oil Holdings Group. Prior to his work at Ocean and Oil, Mr. Durotoye spent more than 19 years with Schlumberger Oilfield Services where he held various management roles.

Yannis Korakakis is Chief Operating Officer, OER. Based in Lagos, Yannis reports to the CEO. Prior to that, Yannis had a very distinguished career in Addax where he was Deputy Managing Director, Technical. In this position, Yannis led the successful evolution of Addax from a start-up oil company to a peak production of above 100,00bopd

Joined Oando Plc in 2009. Prior to Oando, Mr. Falade spent 13 years with Shell E&P in various roles including Systems Engineering, IT, Project Management & Petroleum Economics. As a Senior Business Economist, he led a team to provide frontline Economics support for the portfolio of E&P Gas Development Projects in Nigeria with total headline in excess of $18bn. Mr. Falade was also responsible for Shell’s E&P Africa Portfolio and Discipline Lead for Economics

Mr. Ogunsemi has served as the Financial Controller of OEPL. Prior to joining OEPL, Mr. Ogunsemi worked for BP America where he became the Assistant Controller. Before joining BP America, Mr. Ogunsemi worked for Northern Illinois Gas in Chicago, Illinois, where he rose to become the Head of Disbursement

Prior to joining the Corporation, Mr. Adeleye spent 19 years with Shell, with more than two-thirds of this time spent overseas, in a variety of operational and leadership roles within Technical Limit Well Delivery, Business Support, Benchmarking & Projects Delivery

Eric Brentjens is General Manager, Commercial, OER. Based in Lagos, Eric reports to the CEO. Prior to thatEric was Asset Manager OML 123, Addax’ biggest asset. Eric had spent 17 years before that in Shell in many technical and commercial roles around the world.

15

16

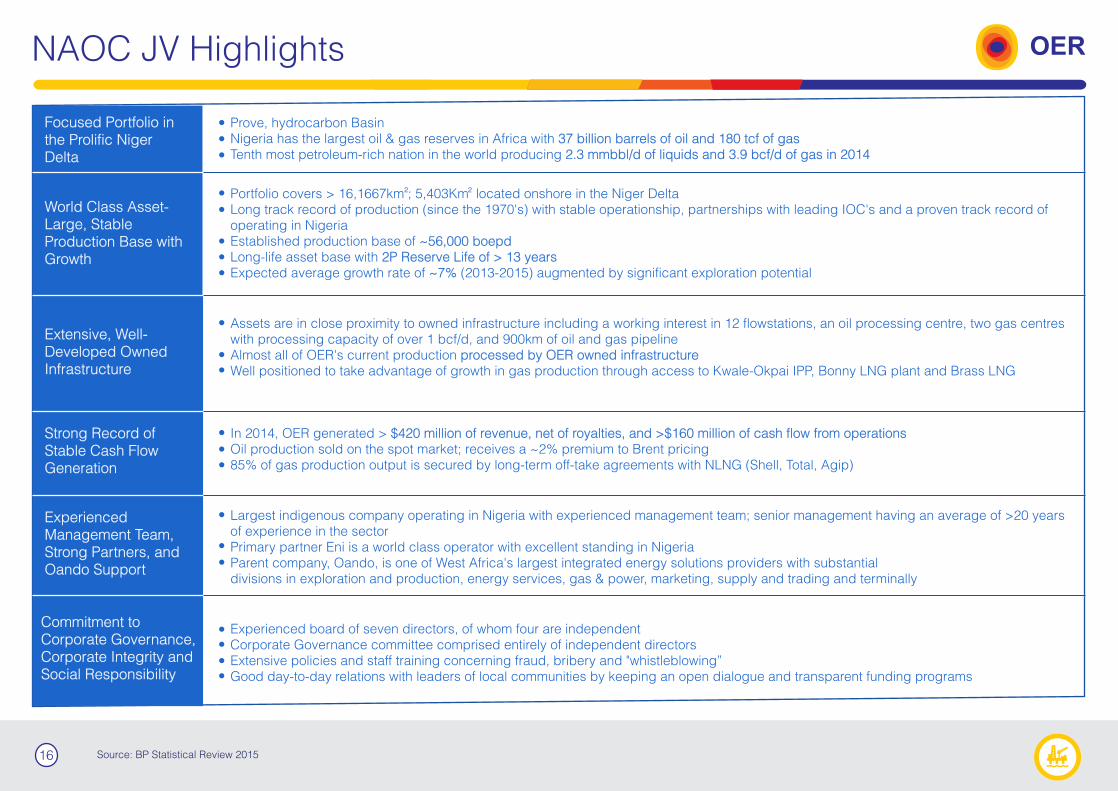

NAOC JV Highlights OER

Focused Portfolio in the Prolific Niger Delta

World Class Asset-Large, Stable Production Base with Growth

Extensive, Well-Developed Owned Infrastructure

Strong Record of Stable Cash Flow Generation

Experienced Management Team, Strong Partners, and Oando Support

Commitment to Corporate Governance, Corporate Integrity and Social Responsibility

Prove, hydrocarbon BasinNigeria has the largest oil & gas reserves in Africa with 37 billion barrels of oil and 180 tcf of gasTenth most petroleum-rich nation in the world producing 2.3 mmbbl/d of liquids and 3.9 bcf/d of gas in 2014

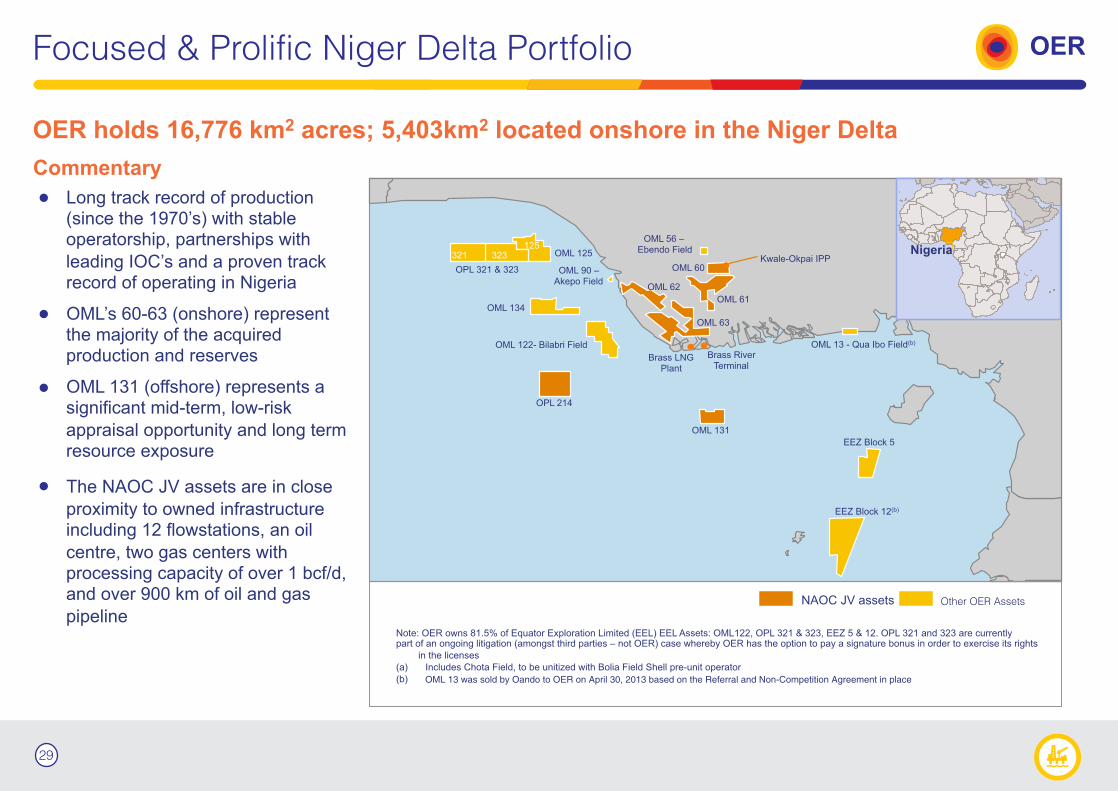

Portfolio covers > 16,1667km ; 5,403Km located onshore in the Niger DeltaLong track record of production (since the 1970's) with stable operationship, partnerships with leading IOC's and a proven track record of operating in NigeriaEstablished production base of ~56,000 boepdLong-life asset base with 2P Reserve Life of > 13 yearsExpected average growth rate of (2013-2015) augmented by significant exploration potential~7%

Assets are in close proximity to owned infrastructure including a working interest in 12 flowstations, an oil processing centre, two gas centres with processing capacity of over 1 bcf/d, and 900km of oil and gas pipelineAlmost all of OER's current production processed by OER owned infrastructure Well positioned to take advantage of growth in gas production through access to Kwale-Okpai IPP, Bonny LNG plant and Brass LNG

In 2014, OER generated > $420 million of revenue, net of royalties, and >$160 million of cash flow from operationsOil production sold on the spot market; receives a ~2% premium to Brent pricing85% of gas production output is secured by long-term off-take agreements with NLNG (Shell, Total, Agip)

Largest indigenous company operating in Nigeria with experienced management team; senior management having an average of >20 years of experience in the sectorPrimary partner Eni is a world class operator with excellent standing in Nigeria Parent company, Oando, is one of West Africa's largest integrated energy solutions providers with substantial divisions in exploration and production, energy services, gas & power, marketing, supply and trading and terminally

Experienced board of seven directors, of whom four are independent Corporate Governance committee comprised entirely of independent directorsExtensive policies and staff training concerning fraud, bribery and "whistleblowing”Good day-to-day relations with leaders of local communities by keeping an open dialogue and transparent funding programs

22

Source: BP Statistical Review 2015

All Reserves & Resources estimates are classified in line with NI 51-101 regulations and Canadian Oil & Gas Evaluation Handbook standards.

All estimates are from Independent ReservesEvaluator report dated 31st December 2014

Appendix

17

The Nigerian Operating Environment

18

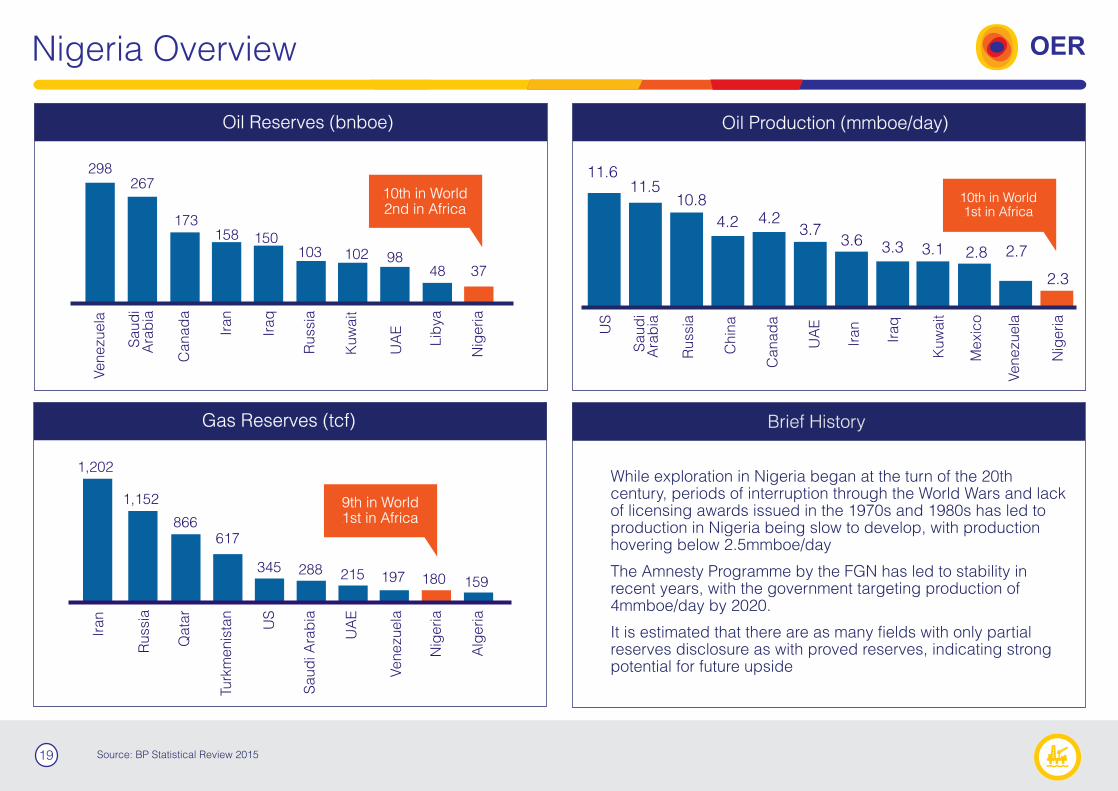

While exploration in Nigeria began at the turn of the 20th century, periods of interruption through the World Wars and lack of licensing awards issued in the 1970s and 1980s has led to production in Nigeria being slow to develop, with production hovering below 2.5mmboe/day

The Amnesty Programme by the FGN has led to stability in recent years, with the government targeting production of 4mmboe/day by 2020.

It is estimated that there are as many fields with only partial reserves disclosure as with proved reserves, indicating strong potential for future upside

298267

173158 150

103 102 9848 37

10th in World2nd in Africa

Oil Reserves (bnboe)

Gas Reserves (tcf)

1,202

1,152

866617

345 288 215 197 180 159

11.611.5

10.8

4.2 4.23.7

3.6 3.3 2.8 2.7

2.3

Venezu

ela

Saud

iA

rab

ia

Canad

a

Iran

Iraq

Russ

ia

Kuw

ait

UA

E

Lib

ya

Nig

eria

3.1

Brief History

Russ

ia

Iran

Qata

r

Turk

menis

tan

US

Saud

i Ara

bia

UA

E

Venezu

ela

Nig

eria

Alg

eria

Oil Production (mmboe/day)

Russ

ia

Saud

iA

rab

ia

US

Iran

Chin

a

Canad

a

UA

E

Mexi

co

Kuw

ait

Iraq

Venezu

ela

Nig

eria

10th in World1st in Africa

9th in World1st in Africa

Nigeria Overview OER

19 Source: BP Statistical Review 2015

20

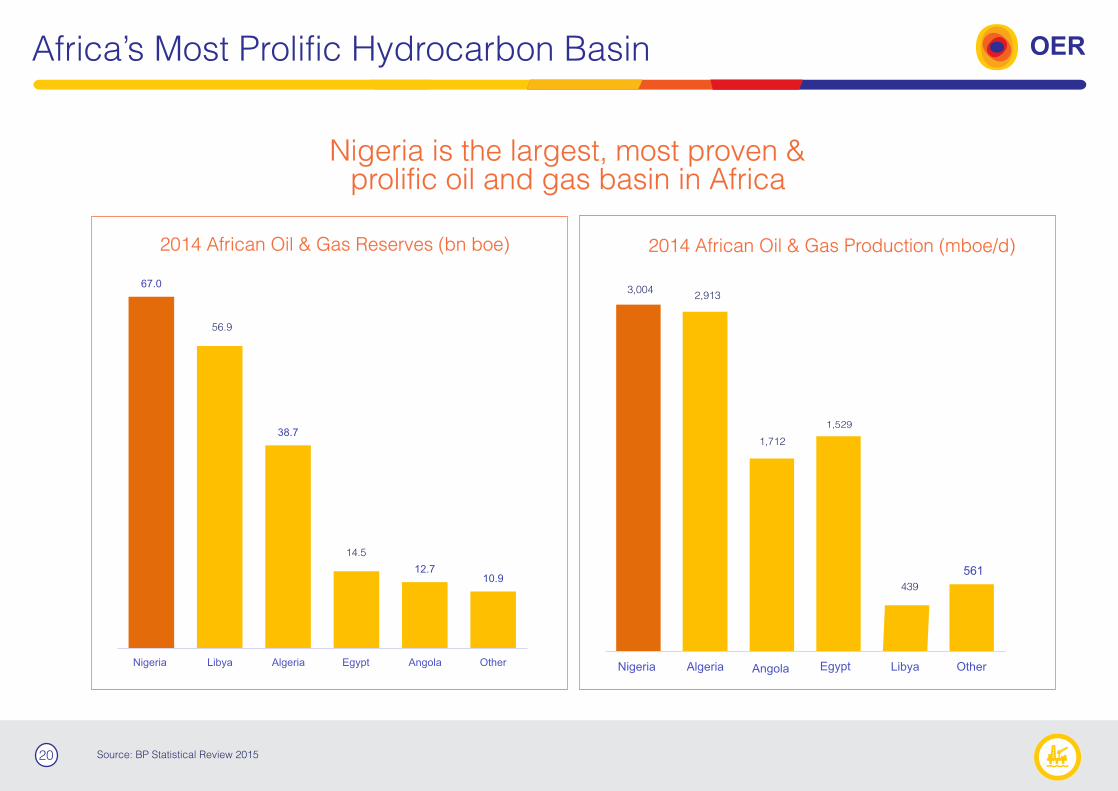

Nigeria is the largest, most proven &prolific oil and gas basin in Africa

Africa’s Most Prolific Hydrocarbon Basin OER

Source: BP Statistical Review 2015

2014 African Oil & Gas Production (mboe/d)2014 African Oil & Gas Reserves (bn boe)

56.9

14.5

3,0042,913

1,712

1,529

439

Nigerian Regional Geology OER

21

Source: Company Information

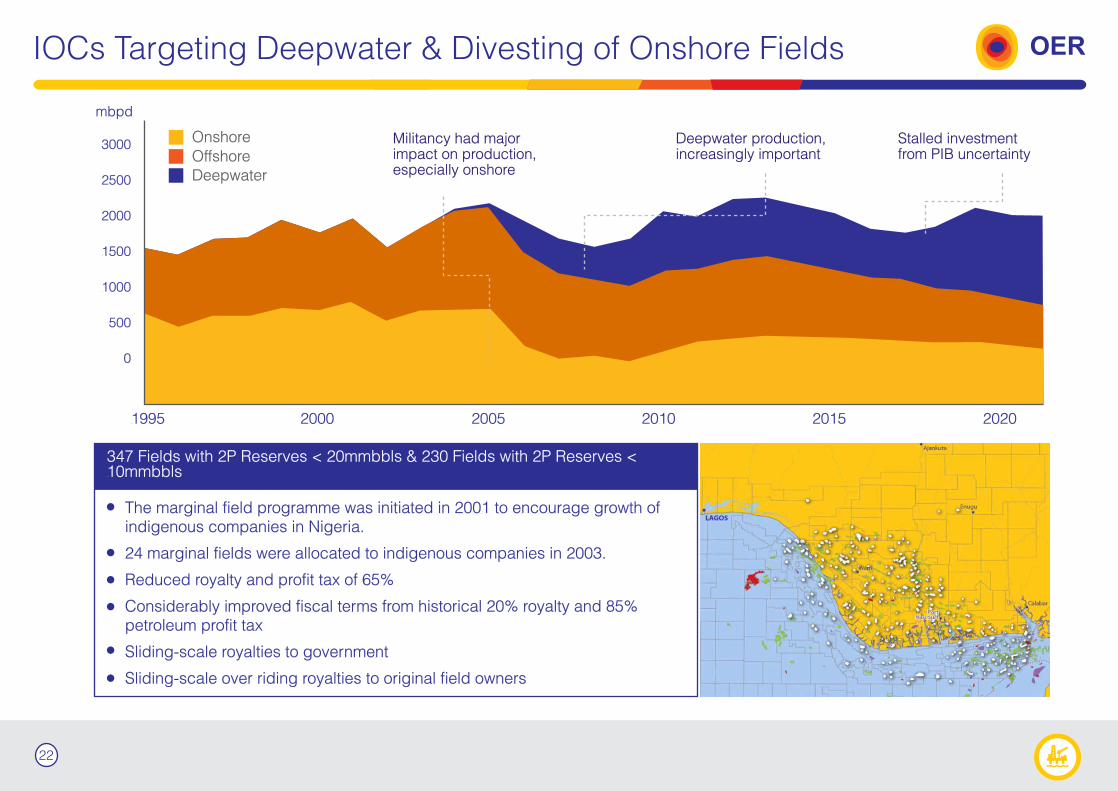

IOCs Targeting Deepwater & Divesting of Onshore Fields

3000

2500

2000

1500

1000

500

0

1995 2000 2005 2010 2015 2020

Militancy had major impact on production, especially onshore

Deepwater production, increasingly important

Stalled investment from PIB uncertainty

The marginal field programme was initiated in 2001 to encourage growth of indigenous companies in Nigeria.

24 marginal fields were allocated to indigenous companies in 2003.

Reduced royalty and profit tax of 65%

Considerably improved fiscal terms from historical 20% royalty and 85% petroleum profit tax

Sliding-scale royalties to government

Sliding-scale over riding royalties to original field owners

Onshore

OffshoreDeepwater

347 Fields with 2P Reserves < 20mmbbls & 230 Fields with 2P Reserves < 10mmbbls

mbpd

OER

22

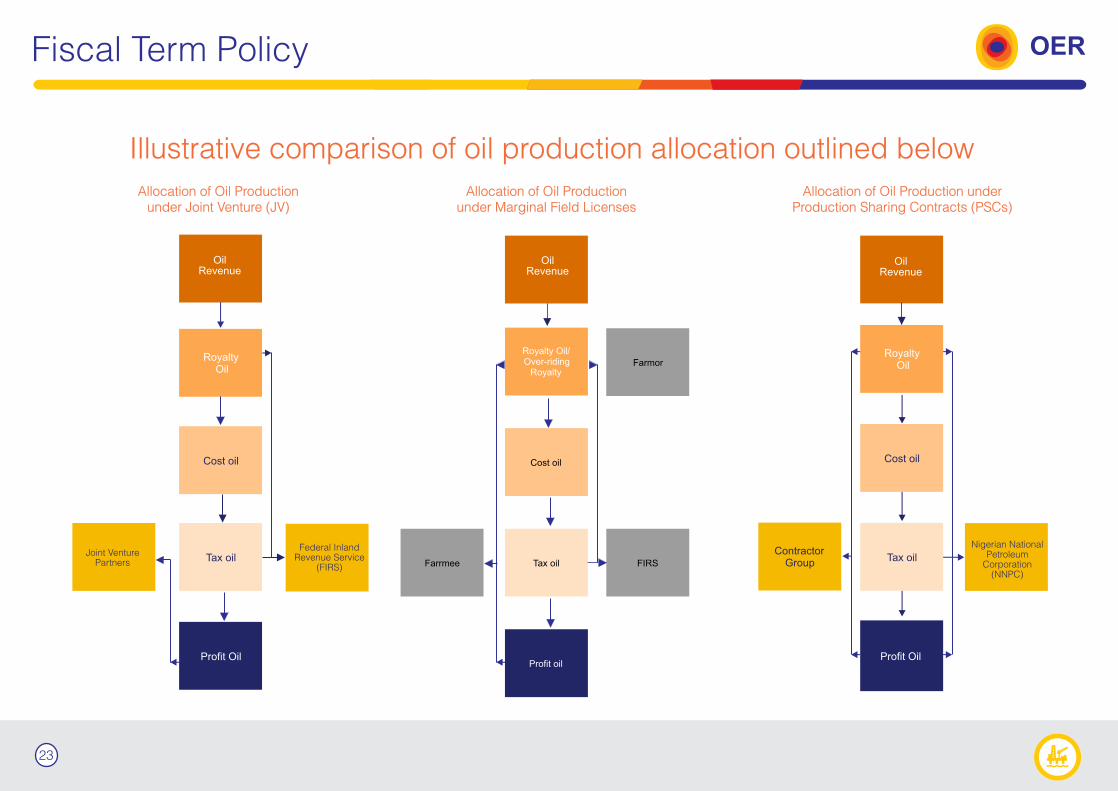

Illustrative comparison of oil production allocation outlined below

Fiscal Term Policy OER

Allocation of Oil Production under Joint Venture (JV)

Allocation of Oil Production under Marginal Field Licenses

Allocation of Oil Production under Production Sharing Contracts (PSCs)

Oil Revenue

Oil Revenue

Oil Revenue

Federal InlandRevenue Service

(FIRS)

Nigerian NationalPetroleum

Corporation(NNPC)

Joint VenturePartners

23

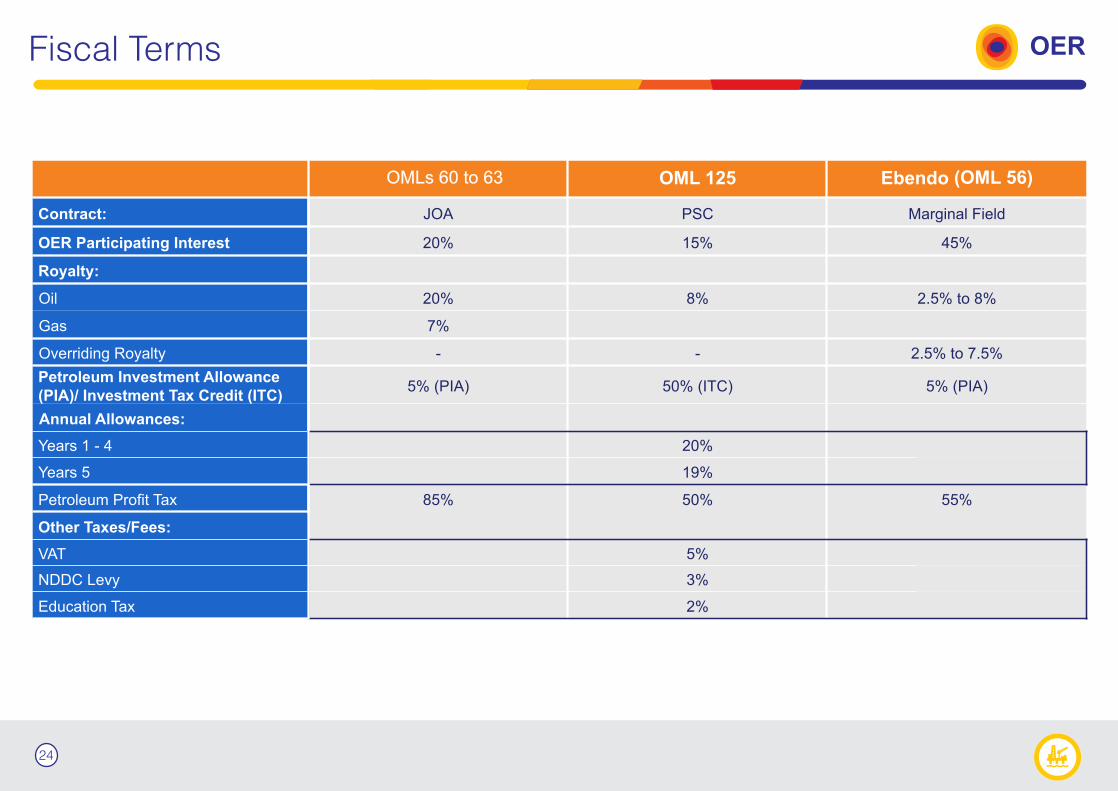

Fiscal Terms OER

24

OMLs 60 to 63

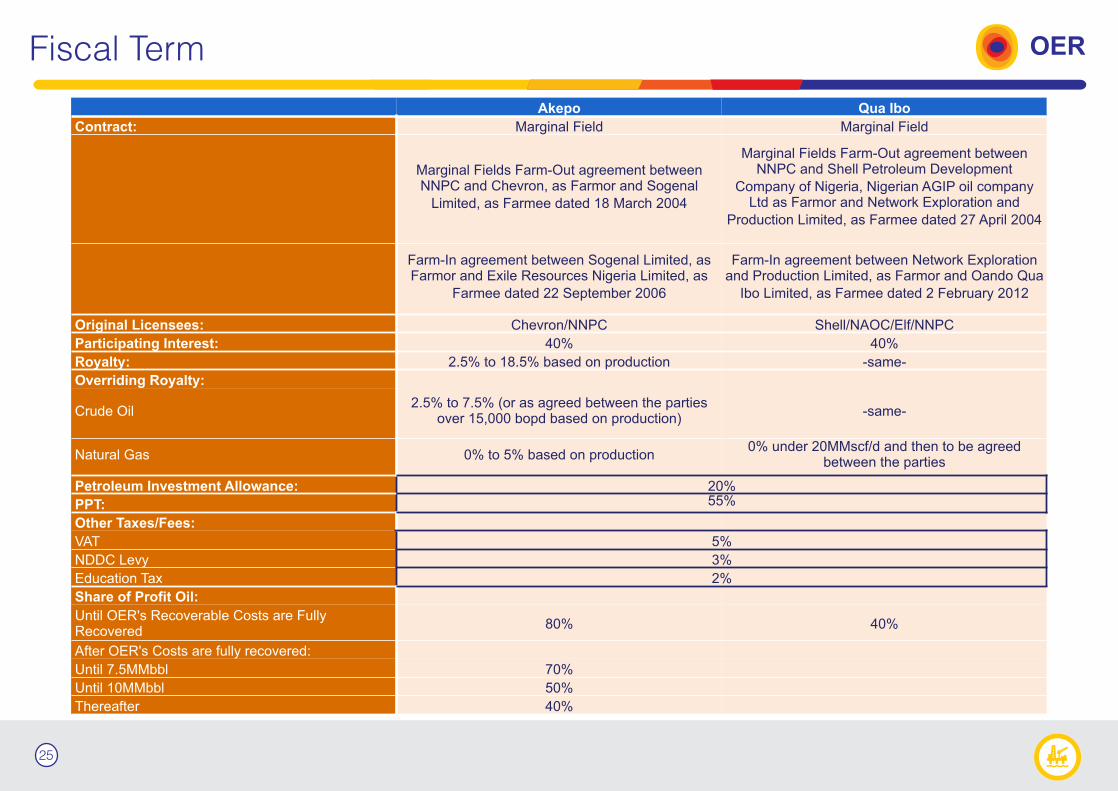

Fiscal Term OER

25

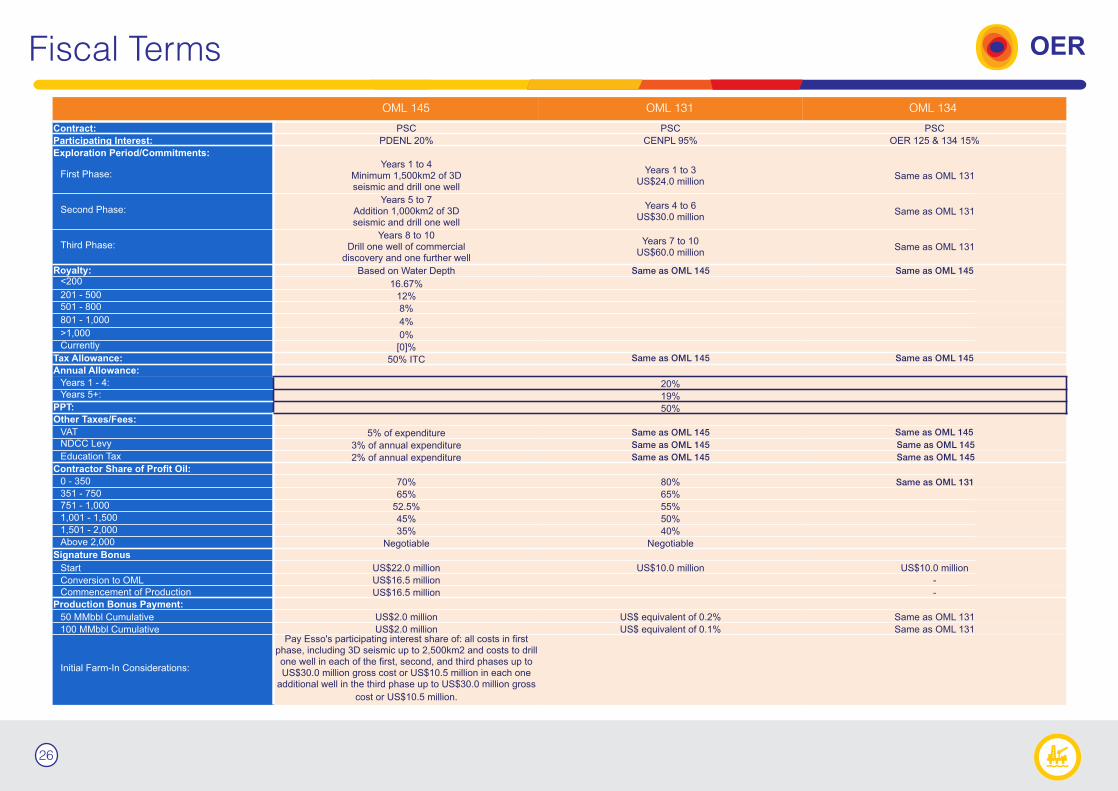

Fiscal Terms OER

OML 145 OML 131 OML 134

Same as OML 145

Same as OML 145

Same as OML 145

Same as OML 145

Same as OML 145

Same as OML 145

Same as OML 145

Same as OML 145

Same as OML 145

Same as OML 145

26

Same as OML 131

27

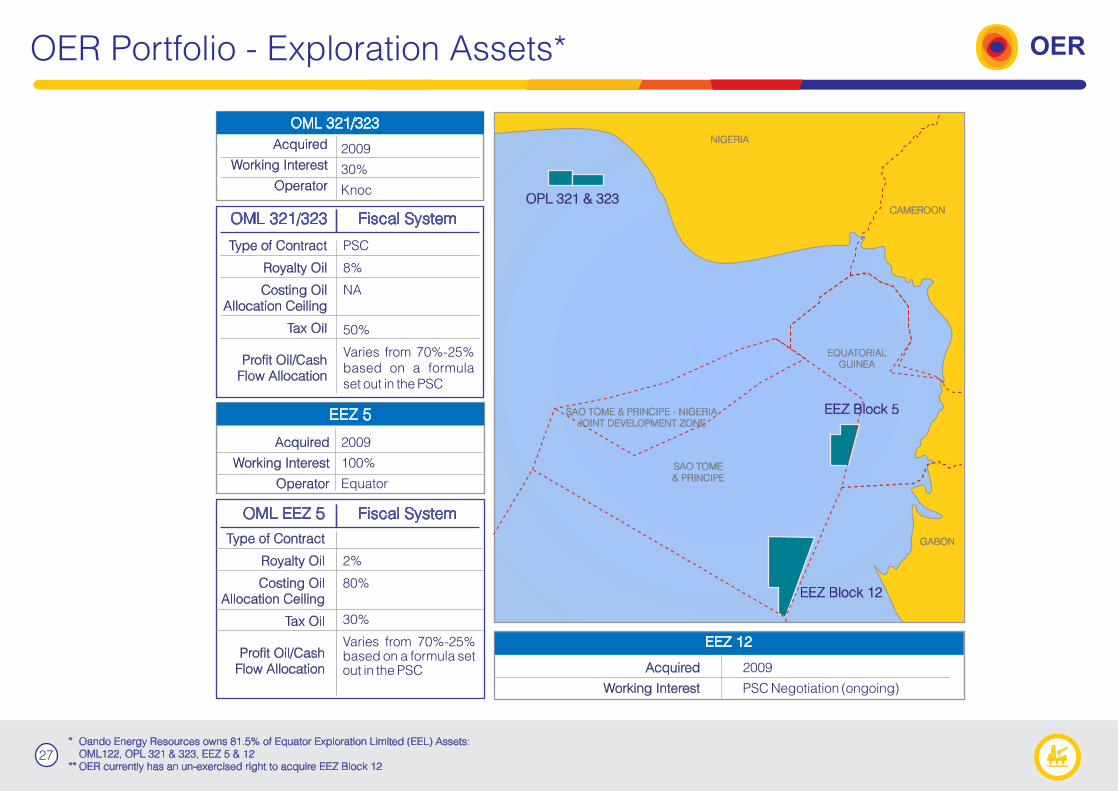

OER Portfolio - Exploration Assets* OER

28

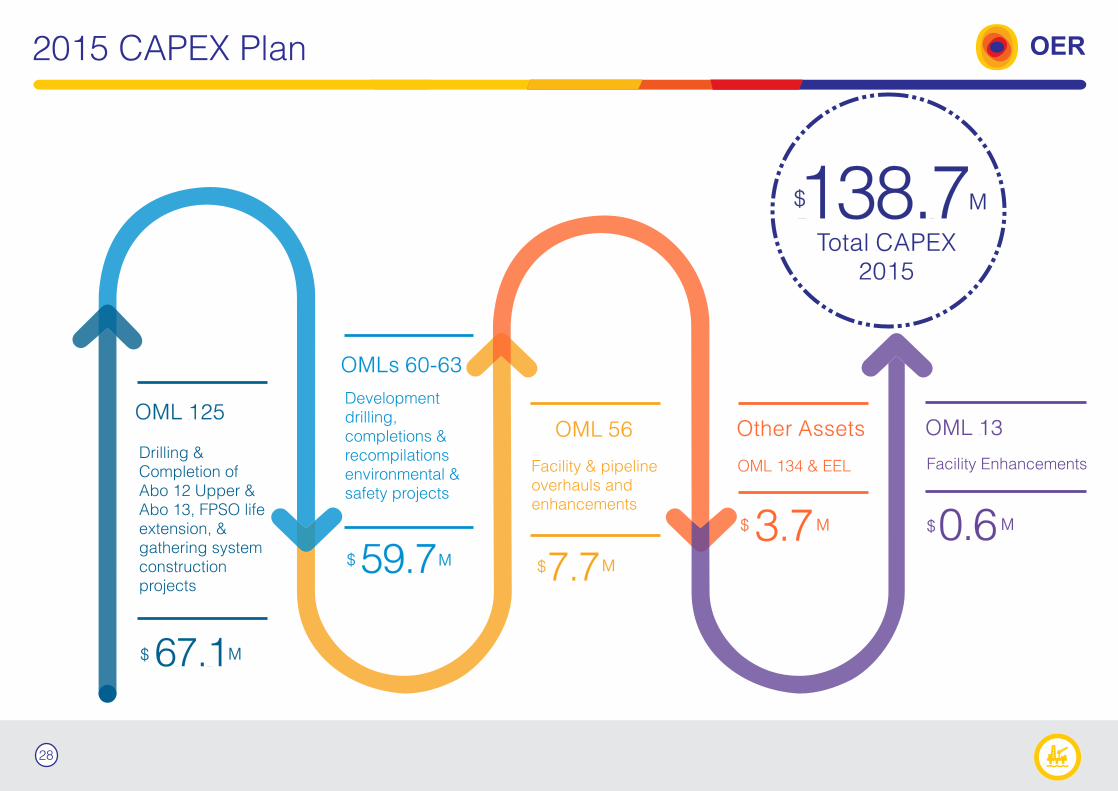

2015 CAPEX Plan OER

Drilling & Completion of Abo 12 Upper & Abo 13, FPSO life extension, & gathering system construction projects

OML 125

138.7M

Total CAPEX 2015

$

67.1M$

Development drilling, completions & recompilations environmental & safety projects

OML 56

59.7

Facility & pipeline overhauls and enhancements

OMLs 60-63

7.7$M$ M

Facility Enhancements

OML 13

0.6$ M

OML 134 & EEL

Other Assets

3.7$ M

Focused & Prolific Niger Delta Portfolio OER

OML 13 was sold by Oando to OER on April 30, 2013 based on the Referral and Non-Competition Agreement in place

29

Other OER Assets

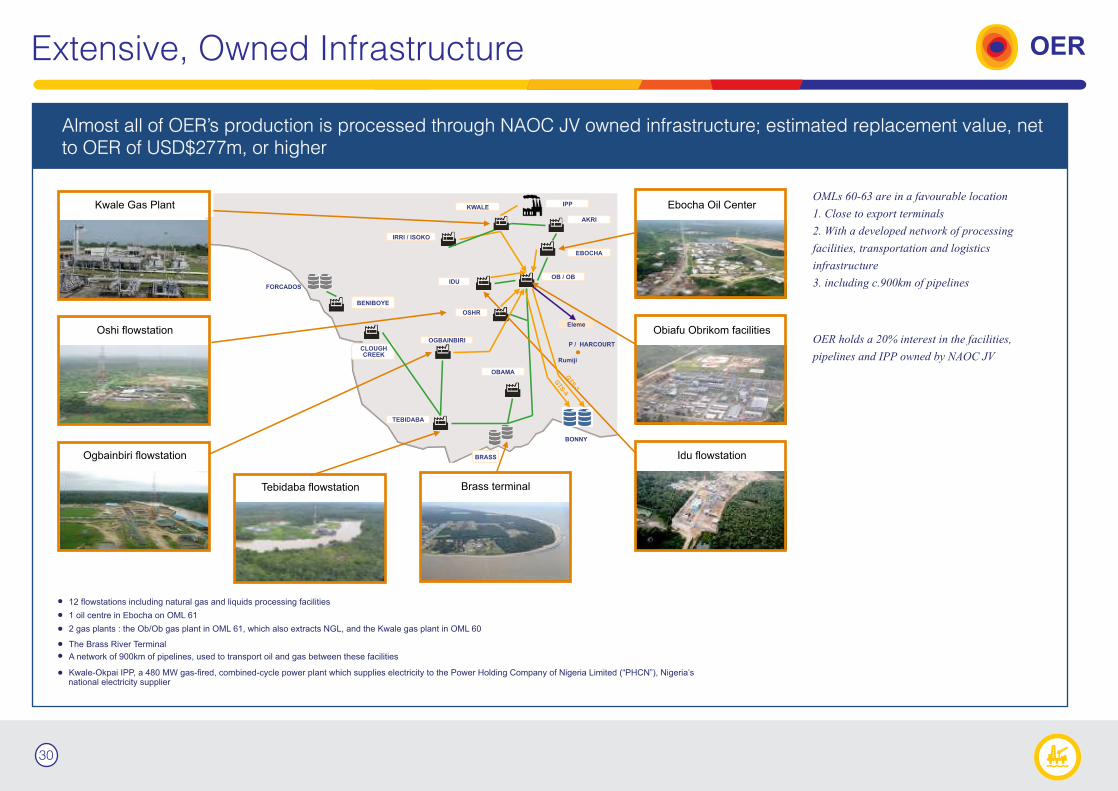

Extensive, Owned Infrastructure OER

Almost all of OER’s production is processed through NAOC JV owned infrastructure; estimated replacement value, net to OER of USD$277m, or higher

OER holds a 20% interest in the facilities, pipelines and IPP owned by NAOC JV

OMLs 60-63 are in a favourable location1. Close to export terminals2. With a developed network of processing facilities, transportation and logistics infrastructure3. including c.900km of pipelines

30

Indigenous Advantage OER

31

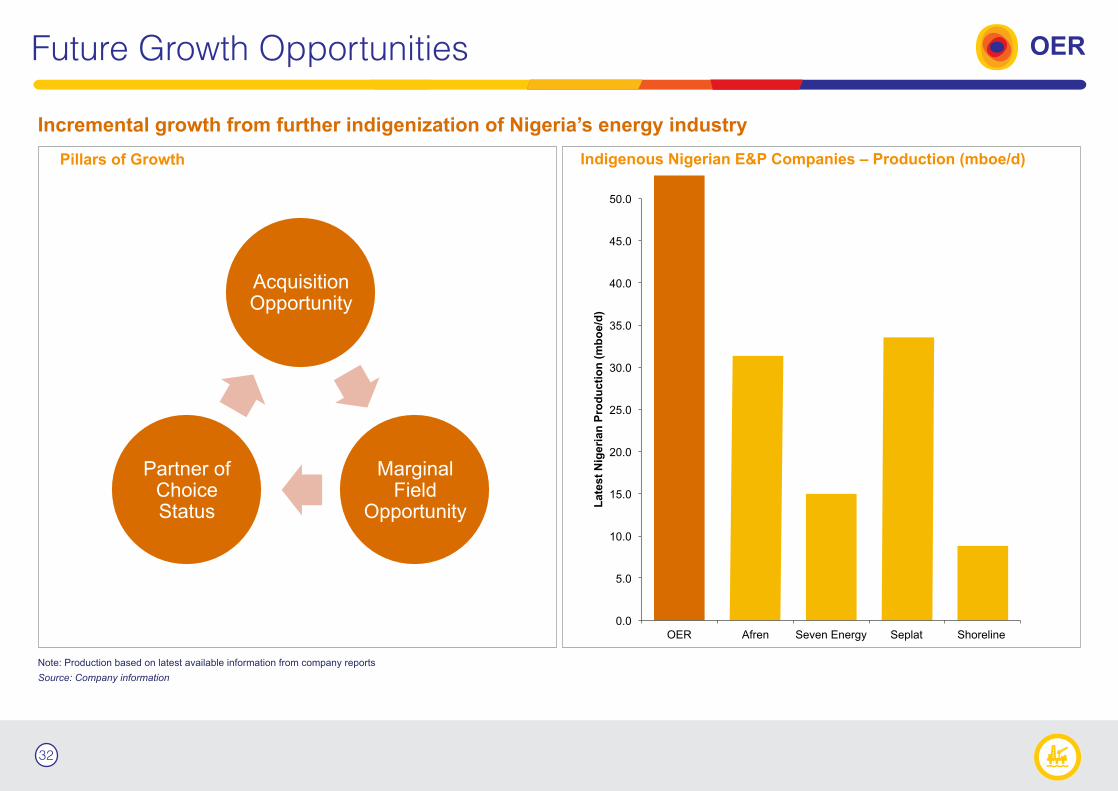

Future Growth Opportunities OER

32

Operating Environment - NAOC JV OER

33

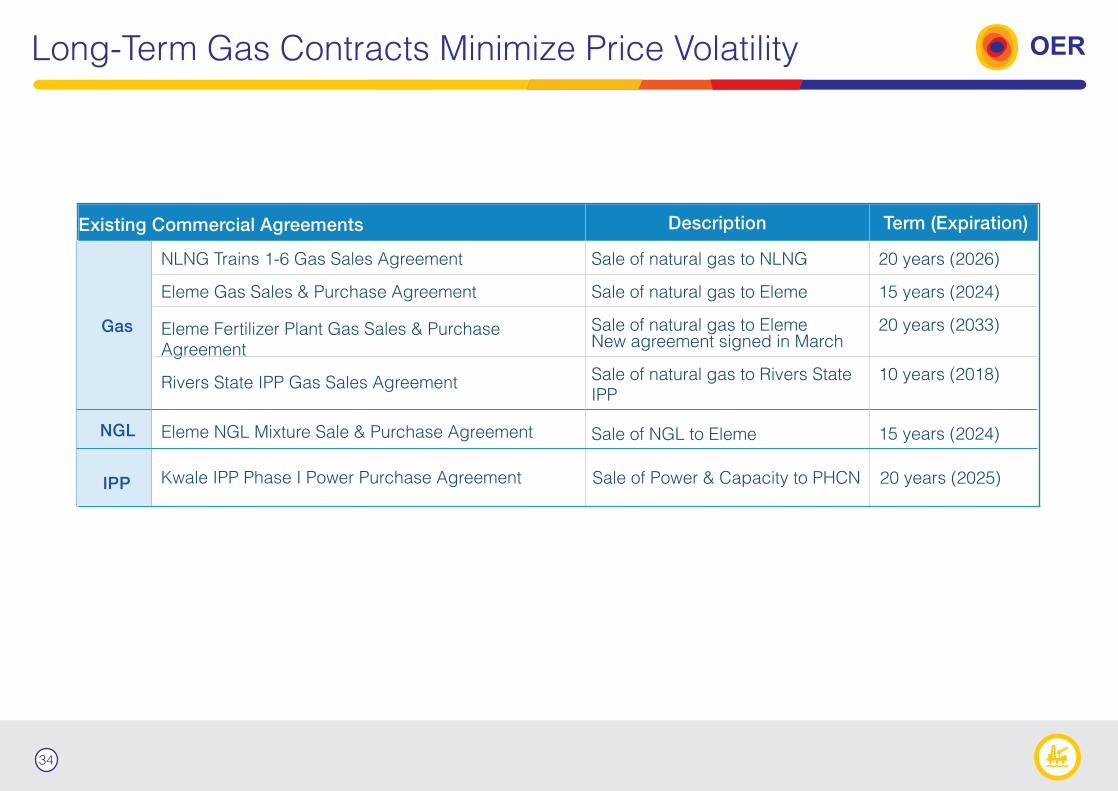

Long-Term Gas Contracts Minimize Price Volatility OER

Existing Commercial Agreements Description Term (Expiration)

NLNG Trains 1-6 Gas Sales Agreement

Eleme Gas Sales & Purchase Agreement

Eleme Fertilizer Plant Gas Sales & Purchase Agreement

Rivers State IPP Gas Sales Agreement

Eleme NGL Mixture Sale & Purchase Agreement

Kwale IPP Phase I Power Purchase Agreement

Gas

NGL

IPP

Sale of natural gas to NLNG

Sale of natural gas to Eleme

Sale of natural gas to ElemeNew agreement signed in March

Sale of natural gas to Rivers State IPP

Sale of NGL to Eleme

Sale of Power & Capacity to PHCN

20 years (2026)

15 years (2024)

20 years (2033)

10 years (2018)

15 years (2024)

20 years (2025)

34

Contact OER

Contact Details

Energy Resources

Head, Corporate Development & Investor Relations

+234 (1) [email protected]

Tokunboh Akindele

35