october 2007 do not cite or distribute without permission of nhs chicago

DESCRIPTION

Lessons from the Front Lines Counselor Perspectives on Default Interventions Homeownership Preservation Initiative (HOPI). October 2007 Do not cite or distribute without permission of NHS Chicago. Goals. Track perceptions of counselors on the “front lines” - PowerPoint PPT PresentationTRANSCRIPT

Lessons from the Front LinesCounselor Perspectives on Default

InterventionsHomeownership Preservation Initiative (HOPI)

October 2007

Do not cite or distribute without permission of NHS Chicago

Goals

• Track perceptions of counselors on the “front lines”

• Look for positive changes in borrower-servicer relationships

• How much progress are we making, collectively?

Survey of Default Counselors

Source: NHS Default Counselor Survey 2007

• Emailed to 400 counseling professionals in May & October 2007 – approximately 1/3 response rate

May: 139 responses – 113 practicing counselorsOct: 78 responses – 61 practicing counselors

• In total served 25,000 clients last 12 months

• 30% work at organizations with >5 “default counselors”

• 82% provide counseling directly– remainder oversee staff conducting counseling

Which best describes changes in demand for default counseling services in the last 6 months?

0%

10%

20%

30%

40%

50%

60%

Decreasedmore than50%

Decreasedby 10-50%

No change

Increasedby 10-50%

Increasedby 51-100%

Increasedby 101-200% ormore

Source: NHS Default Counselor Surveys 2007

Demand is accelerating.

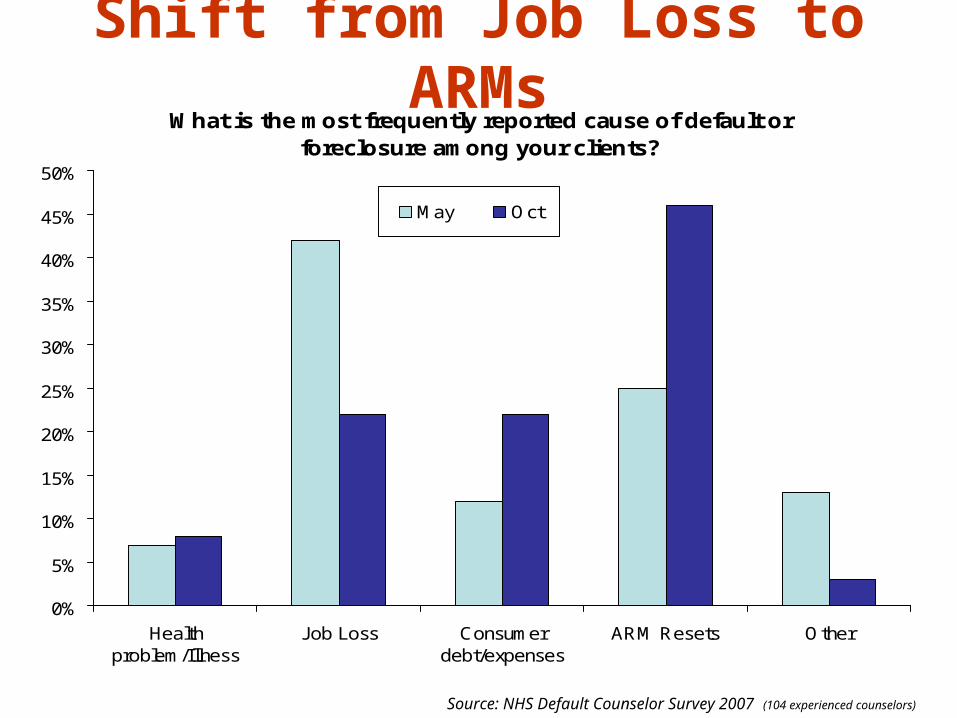

Shift from Job Loss to ARMsWhat is the most frequently reported cause of default or

foreclosure among your clients?

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Healthproblem/Illness

Job Loss Consumerdebt/expenses

ARM Resets Other

May Oct

Source: NHS Default Counselor Survey 2007 (104 experienced counselors)

Counselor Evaluation: Major Problems

Source: NHS Default Counselor Surveys 2007

What share of borrowers that you have seen involve fraud, loans that the borrower could never have afforded or 'exploding ARMs'?

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Fraud Payments NeverAffordable

300+ BPS ARM Resets

May Oct

Most Common Outcomes Observed by Counselors

How common is each outcome for borrowers in default that you counsel?% Very Common

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Repaymentplan

Loanmodification

Foreclosureauction

Current withforeclosureprevention

loan

Forbearance Sale of home Refinance Current withown funds

May Oct

Source: NHS Default Counselor Surveys 2007

++ - -

Ratings of 22 Subprime Servicers

Source: NHS Default Counselor Surveys 2007

• Rate each institution's loss mitigation department based on your experience in the last 6 (six) months.

• 1-4 scale: 1: Very good to work with2: Fairly good to work with3: Fairly difficult to work with4: Very difficult to work with

• Average: 2.5 – between fairly good-difficult– No changes from May to October – but more variation for each lender

• Range 1.0 to 3.7 - experiences uneven– Key finding: Within institutions counselors have varied experiences.

» Even the ‘best’ have issues/problems as identified by counselors

How helpful is it in creating loan workouts to have a designated contact?

Extremely helpful

53%

Very helpful24%

Somewhat helpful

18%

Not at all helpful

1%

Somewhat unhelpful

4% Reduces time on hold, making call backs, etc by 15.4 minutes per client.

Saves counselor serving 100 clients 3.2 days in client service time per year.

Source: NHS Default Counselor Surveys 2007

Treatment of Counselors Improving

Source: NHS Default Counselor Surveys 2007

Best describes how you think the "typical" loss mitigation staff person feels about you when you are working with them on behalf of a client?

0%

10%

20%

30%

40%

50%

60%

They value myservices as a

fellow professional

They tolerate myrole but arerespectful

They barelytolerate my role

and not respectful

They are openlyhostile and

frustrated I aminvolved

May Oct

Flexible Options Are Being Used Enough?How often will any servicer or lender perform the following with your clients?

0%

10%

20%

30%

40%

50%

60%

70%

80%

Change an ARM intoa fixed rate loan

Reduce/write-downthe principal balance

Waive fees andaccrued interest

permanently

SometimesRarelyNever

Source: NHS Default Counselor Surveys 2007

Borrowers View Servicers PoorlyWhich best describes how borrowers in default view their

lender/servicer, in general?

Intimidated38%

Frustrated45%

Borrowers have no opinion

3%Angry13%

Positive 1%

Source: NHS Default Counselor Surveys 2007

Counselors: Recent Servicer EffortsWhich best describes changes you have observed among lenders/servicers working

with borrowers in default in the last six (6) months?

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Much morerestrictive/harder to

work with

Somewhat morerestrictive/harder to

work with

No change Somewhat moreresponsive

Much moreresponsive

May Oct

Source: NHS Default Counselor Surveys 2007

Sign of improvement

Why do borrowers fail to contact their lender when they have trouble making payments?

Don't know lenders can provide options 53%

Too depressed/stressed 26%

Think they can get by on their own 12%

Lenders mistreat them (write in) 10%

Most counselors wrote about multiple problems.

Consistent with borrower surveys and interviews

Source: NHS Default Counselors Surveys 2007

Expectation for demand for nonprofit foreclosure services over the next year?

Demand will increase a lot

71%

Demand will increase a little13%

Demand will decrease a lot

14%

Demand will stay the same1%

Demand will decrease a little1%

Source: NHS Default Counselor Surveys 2007

Counselor Feedback• “problems are becoming overwhelming for the counselors as

well…we need to work better together”

• “lenders need to realize we can play a ‘broker’ like role because we may have real relationships with people and more accurate information”

• “immediately patch us through to the decision makers rather than wasting our time”

• “create a better system for accepting authorization forms. A 24 hour delay, in many cases, is too long”

• “need to bypass the gorillas in collections”

• “create special processes/products if a nonprofit is involved—like we did on originations”

Looking Forward: More Work to Be Done

• Some evidence counseling-lending relationship getting better; more modifications being made

But housing values and surge in demand are challenges

• Improve connections between counselors & lenders Increasing need for services

• Expand use of modification strategies Disseminate innovations more evenly across institutions

• Borrowers need to better understand options & overcome emotional responses

Do not cite or distribute without permission of NHSpolicylabconsulting.com

produced by: