obamacare presentation 2014 v3

DESCRIPTION

ÂTRANSCRIPT

FOLLOW PRESENTATION ON TWITTER

@churchtaxcredit www.obamacarefacts.com www.kff.com

ACA FROM THREE PERSPECTIVES

TAX PREPARER TAXPAYER

PROVIDER

WHAT IS OBAMACARE??

NANCY PELOSI SAID:

2011 UNITED STATES-KOREA FREE TRADE AGREEMENT IMPLEMENTATION ACT

• TITLE V— • OFFSETS SEC. 501. INCREASE IN PENALTY ON PAID

PREPARERS WHO FAIL TO COMPLY WITH EARNED INCOME TAX CREDIT DUE DILIGENCE REQUIREMENTS.

• (a) In General.--Section 6695(g) of the Internal Revenue Code of <<NOTE: 26 USC 6695.>> 1986 is amended by striking ``$100'' and inserting ``$500''.

• (b) Effective Date.--The amendment made by this section shall apply to returns required to be filed after December 31, 2011.

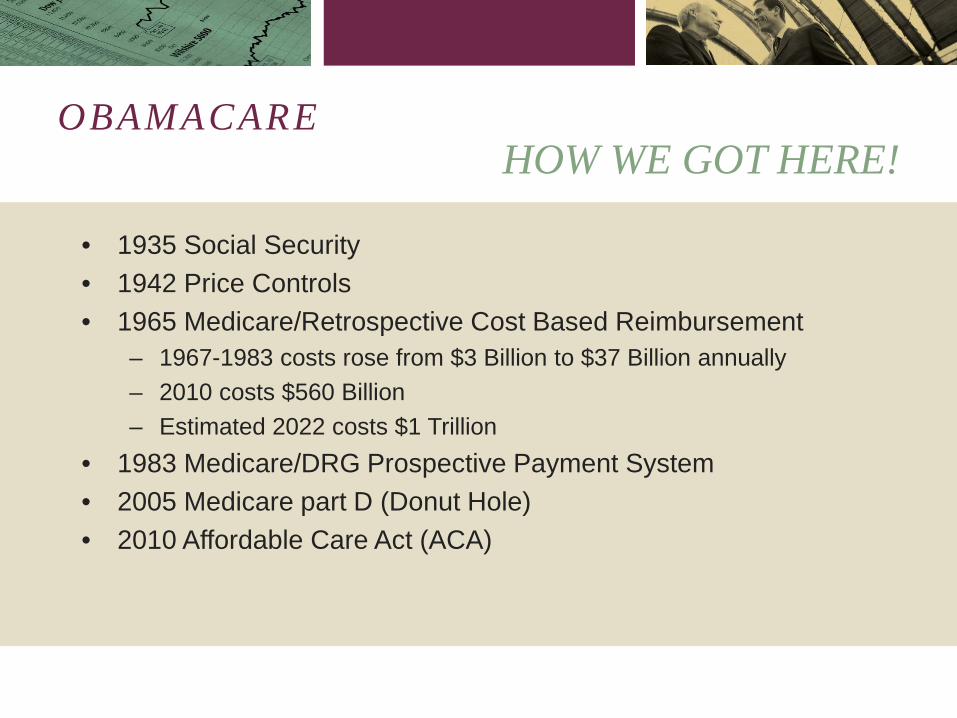

OBAMACARE HOW WE GOT HERE!

• 1935 Social Security • 1942 Price Controls • 1965 Medicare/Retrospective Cost Based Reimbursement

– 1967-1983 costs rose from $3 Billion to $37 Billion annually – 2010 costs $560 Billion – Estimated 2022 costs $1 Trillion

• 1983 Medicare/DRG Prospective Payment System • 2005 Medicare part D (Donut Hole) • 2010 Affordable Care Act (ACA)

OBAMACARE FACTS AFFORDABLE CARE ACT (ACA)

Signed into law to reform the health care industry by President Obama on March 23, 2010 and upheld by the Supreme Court on June 28, 2012 • Expands the affordability, quality, and availability of private and public health insurance through consumer protections, regulations, subsidies, taxes, insurance exchanges, and other reforms • Does not replace private insurance, Medicare or Medicaid

WHAT’S NEW WITH OBAMACARE? TIMELINE OF SORTS

2014 2018 2020 Pre-existing conditions can not be denied.

40% tax would be imposed on insurance companies providing “Cadillac” health plans valued at more than $10,200 for individual and $27,500 for families

“Donut Hole” Medicare RX benefit gap ends. Seniors continue to pay the 25% of drug costs until they reach the threshold for Medicare catastrophic coverage, when their copays drop to 5% Fines begin if you don’t have

coverage.

Higher rates allowed on basis of residence, family size & tobacco use

Current law: Donut Hole is when Medicare stops coverage of drugs after a plan spends $2,830 on RX. It starts to pay again after an individual exceeds $4,550 out of pocket. Gap is $1,720

Full Time defined as 30 hours per week

All group plans must be certified and provide a required minimum benefits

Medicaid expanded to cover up to 138% of poverty line ($29,300 for a family of 4)

HIGHLIGHTS OF THE ACA

• Expand healthcare coverage to 32 Million uninsured Americans

• Slow down the rising cost of healthcare • Requires Essential Health Benefits in

insurance plans • Closes the Medicare part D gap (Donut Hole) • Expands Medicaid coverage

MOST RECENT COURT CASE D.C. CIRCUIT COURT OF APPEALS

• To be heard May 8, 2014 • US Constitution Origination clause – all bills raising revenue shall

originate in the House of Representatives; but the Senate may propose or concur with amendments as on other bills,

• Matt Sissel and the Pacific Legal Foundation • In 2012 the Supreme Court calls the penalty a TAX • October 2009 the House passed a bill to modify a tax credit for

members of the armed forces and other federal employees who were first time home buyers

• The bill had NOTHING to do with healthcare

MOST RECENT COURT CASE D.C. CIRCUIT COURT OF APPEALS

• Two months later the bill was “amended” by the Senate. • The Senate renamed it and erased its contents completely. • Guess what they replaced it with? • That’s right…the contents of the ACA. • Case law establishes that the amendment must be “germane to

the subject matter of the House bill”. • Keep an eye on this!!

• “An origination question for the ACA” – George Will May 4, 2014

BASICS OF OBAMACARE

1. No discrimination based on gender 2. Insurance companies can not take away insurance because people

get sick 3. Insurance companies have to justify increases in cost 4. All Americans can purchase or be provided insurance based on their

income and employment 5. Americans can not be denied coverage based on pre-existing

conditions 6. No co-pays for key medical expenses 7. No annual or lifetime limits 8. Small businesses will receive tax credits for providing insurance 9. Young adults stay on their parents plan until there are 26

10 ESSENTIAL HEALTH BENEFITS

1) Ambulatory services 2) Emergency services 3) Hospitalization 4) Maternity and newborn care 5) Mental health and substance abuse 6) Prescription drugs 7) Rehab services and devices 8) Laboratory services 9) Preventative and wellness services 10) Pediatric services including oral and vision care

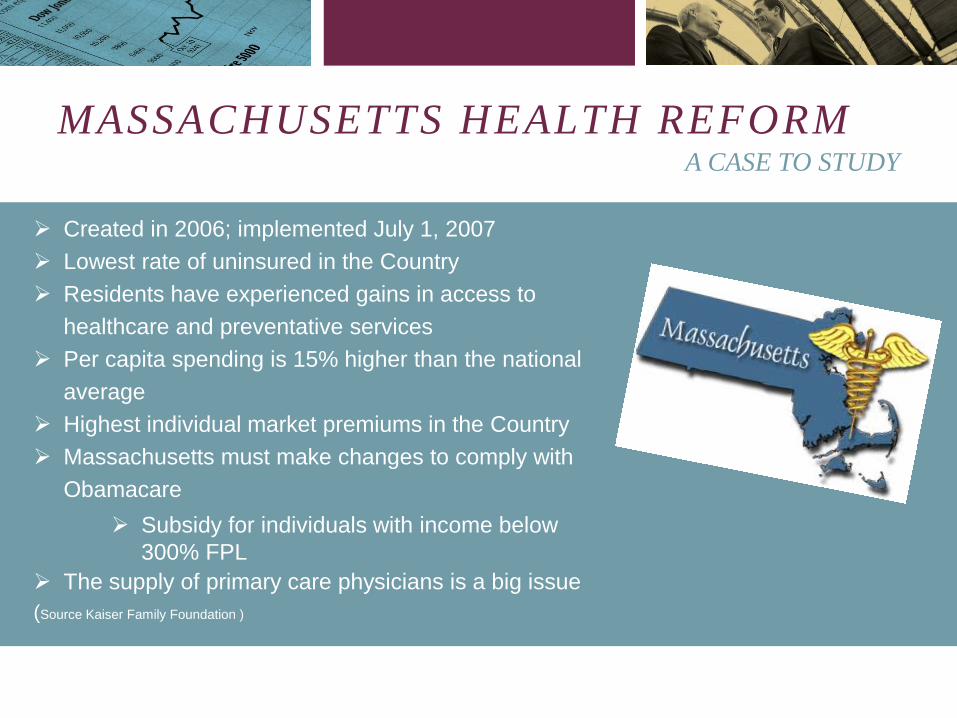

MASSACHUSETTS HEALTH REFORM

Created in 2006; implemented July 1, 2007 Lowest rate of uninsured in the Country Residents have experienced gains in access to

healthcare and preventative services Per capita spending is 15% higher than the national

average Highest individual market premiums in the Country Massachusetts must make changes to comply with

Obamacare Subsidy for individuals with income below

300% FPL The supply of primary care physicians is a big issue (Source Kaiser Family Foundation )

A CASE TO STUDY

OBAMACARE NEW KEY TAXES /BREAKS IN THE AFFORDABLE CARE ACT

• Individual Mandate (new tax) – Every individual must have coverage, get an exemption or pay a per

month fee • Employer Mandate (new tax)

– In 2015 large employers must insure full time employees or pay a per employee fee

• Additional Individual Taxes • Advanced Premium Tax Credits

– low-to-middle income Americans are eligible for a tax credit which reduce the upfront cost of premiums on health insurance purchased through an exchange

• Small Business Tax Credits – Small businesses may be eligible for tax credits of up to 50% of their cost

of employee premiums through the Small Business Health Options Program

WHAT IS THE INDIVIDUAL MANDATE?

• Requires all citizens and legal residents to have health coverage in 2014

• Health coverage includes: – Medicare – Tricare – Veterans Health Program – Employer offered health plans – Medicaid or the CHIP – Grandfathered health plan – Bronze level or better purchased on your own

INDIVIDUAL MANDATE MANDATE DOES NOT APPLY TO:

• Mandate does not apply to: – Religious objectors from religious sects – You are uninsured for less than three months – You have a hardship exemption – Undocumented immigrants – You are a member of a recognized health care sharing

ministry – Incarcerated – American Indians and Alaskan Natives – Those with Income below tax filing threshold – Lowest cost plan exceeds 8.0% of your income

INDIVIDUAL MANDATE EXEMPTIONS HARDSHIP EXEMPTIONS – THIS IS ANYONE!!!

• You were homeless • You were evicted in the last 6 months or are facing eviction or foreclosure • You received a shut off notice from a utility company • You recently experienced the death of a close family member • You experienced a disaster that caused substantial damage to property • You filed for bankruptcy in the last 6 months • You had medical expenses you couldn’t pay in the last 24 months • You recently experienced domestic violence • You experienced an increase in expenses due to caring for an aging family

member • Your individual insurance plan was cancelled and you believe other

Marketplace plans are unaffordable • You experienced another hardship in obtaining health insurance • www.healthcare.gov/exemptions

TAX PREPARER TIP • More info will come out

regarding these hardship exemptions as we get closer to the filing season.

HEALTH INSURANCE PREMIUM TAX CREDIT

• Makes premiums affordable for individuals and families with lower income

• Available to individuals and families up to 400% of FPL (federal poverty level)

• Insured must apply through an exchange

TAX PREPARER TIP • Changes in your client’s

income can cause large subsidy re-payments at tax time. Warn your clients!!

2013 FEDERAL POVERTY LEVELS

FPL Annual Income – Individual

Annual Income – Family (3)

100% 11,496 19,536 133% 15,288 25,980 138% 15,864 26,952 200% 22,980 39,060 300% 34,476 58,596 400% 45,960 78,120

PREMIUM TAX CREDITS

Income Level Premium as a % of Income 100% to 133% FPL 2% of income 133%-150% 3-4% of income 150%-200% 4-6.3% of income 200%-250% 6.3-8.05% of income 250%-300% 8.05-9.5% of income 300%-400% 9.5% of income

You must go through the marketplace to receive the subsidies.

THE PENALTIES INDIVIDUAL SHARED RESPONSIBILITY FEE

• 2014 the greater of $95 per adult and $47.50 per child ($285 max per family) or 1% of family income

• 2015 the greater of $325 per adult and $162.50 per child ($975 max per family) or 2% of family income

• 2016 the greater of $695 per adult and $347.50 per child ($2,085 max per family) or 2.5% of family income

• 2017 – inflation adjusted

TAX PREPARER TIP • The penalty cannot be collected

through a lien or garnishment. It can only be a reduction of a tax refund. But beware, penalties and interest will accrue and my bet is the collection method will change in the future.

INDIVIDUAL MANDATE FOR TAX PREPARERS

1. If a taxpayers income situation changes, the premium tax credit may be overstated

2. The penalty is calculated on your MAGI (AGI with certain deductions added back)

3. The penalty is calculated in 1/12 for partial years lacking coverage 4. Anyone with a “gap” in coverage for three months or less is exempt

from the tax penalty 5. The penalty is paid on your income tax return at the end of the year 6. Health insurance plans will provide “proof of coverage” 7. The total penalty cannot exceed the national average for the annual

premiums for a bronze plan

TAX PREPARER TIP • Roughly calculate this FIRST!

Then make sure the taxpayer is reporting this on his/her return and not looking for another preparer who might not know the law.

CALCULATING THE PENALTY THIS IS EASY!!!

• Family of five. • Only insured the last three months of the year through a new

employer. • Income of $20,000 the last three months. $5,000 of unemployment

the first nine months. • Do not meet any of the exemptions. • Penalty Calculation for 2014: The greater of: the lesser of: $95 X 2 Adults + $47.50 X 3 children or $285 max or 1% of $25,000 = $250 So, $285 X 75% (9 months of no coverage) = $214

CALCULATING THE PENALTY THIS IS NOT!!!

• Single father of three with no insurance marries, • Single mother of two who was insured (but her children were not) in

California before she moved to Alabama to get married and start her new job that included insurance for the family after her 60 day probation period.

• On October 1 her new company announces that they will no longer provide insurance for families.

• Their combined AGI is $125,000 • She had $3500 in moving expenses, they both have $7500 in student

loan interest • One child works at McDonalds after school and made $8200. • His dad moved in with them in August due to poor health.

TAX PREPARER TIP • We need to bill for this

service. You could spend up to an hour or more properly calculating this penalty.

SIGNING UP THROUGH THE MARKETPLACE

• Alabama does not have a state exchange – chose to use the Federal marketplace

• Use the website www.healthcare.gov to sign up • Only three counties have more than one insurance company offering

insurance. Madison, Shelby, and Jefferson have BCBS and Humana • United Healthcare offers a plan off the exchange • Call 1-800-318-2596 • Open enrollment was from 10/1/2013 – 3/31/14 however extended to

4/15/14 • Enrollment for Medicaid is anytime • Next enrollment period begins 11/15/14 • Small business can apply for SHOP coverage anytime all year

MY INSURANCE THROUGH THE MARKETPLACE

• We are in our mid fifties • Self employed

PLAN Monthly

Premium Deductible Covered

after Ded Bronze 683 6,350 60% Silver 900 2,000 70% Gold 1,093 1,500 80% Platinum 1,318 100 90%

SIGNING UP THROUGH THE MARKETPLACE

• Special enrollment period for: – Getting married – Having or adopting a child – Moving to a new area with different health plan options – Losing other health coverage – Change in income or marital status for premium credit changes – Becoming a citizen

TAX PREPARER TIP • Move to Georgia, Mississippi,

Tennessee, or Florida and get a plan ASAP.

OBAMACARE AND SMALL BUSINESS SMALL EMPLOYER HEALTH PREMIUM CREDIT

• Three conditions must be met – FTE’s under 25 – Avg. wage per employee under $50K – Employer pays at least 50% of a premium for a QHP for at least one

employee • 2010-2013

– 35% credit, 25% for not-for-profits • 2014-2015

– 50% credit, 35% for not-for-profits • 2014, the health insurance must be purchased through the Small

Business Health Option Program (SHOP)

www.churchtaxcredit.com

EMPLOYER MANDATE

Small businesses with more than 100 FTEs and avg. annual wages of more than $250,000 must provide health coverage to full time employees in 2015 Starting in 2016, employers with 50-99 FTEs will have to ensure their fulltime workforce FTE = 30 hours per week Coverage must provide minimum benefits (Bronze level) Will hired veterans be included in the count?

THE PENALTIES

• The annual fee is $2K per full time employee if insurance isn’t offered

• The first 30 full time employees are exempt from the penalty • If one full time employee receives the premium tax credit

because insurance offered is subpar the employer must pay the lessor of $3K for each employee receiving the credit or $750 for each of their full time employees

• The fee is calculated per month and due annually • The fee is NOT tax deductible

EMPLOYER SHARED RESPONSIBILITY PAYMENT

TAX PREPARER TIP • Employers on the bubble can

avoid the penalty by having less than 30 full time (more than 30 hours per week) employees. Everyone else is less than 30 hours per week.

NEW REQUIREMENTS FOR REPORTING

Beginning 2015: 1. You must file an annual return reporting whether and what

health insurance you offered your employees 2. If you provide self-insured health coverage, you must file an

annual plan reporting certain information for each employee you cover

3. You are required to report the value of health insurance coverage you provided to each employee on his/her W-2 (box 12 code DD)

4. You must complete a form 1099 for all vendors. REPEALED • Vendors who receive $600 or more in payments

TAX PREPARER TIP • Taxpayers should bring to you

a report of the months that they were insured.

THE TAXPAYER PERSPECTIVE

2.3% TAX ON MEDICAL DEVICE MANUFACTUERS

10% TAX ON INDOOR TANNING SERVICES

BC/BS TAX HIKE TAX ON BRAND NAMED DRUGS EXCISE TAX FOR CHARITABLE

HOSPITALS WHO FAIL TO COMPLY WITH OBAMACARE REQUIREMENTS

TAXES THAT WILL NOT AFFECT THE AVERAGE INDIVIDUAL

THE TAXPAYER PERSPECTIVE

TAX ON HEALTH INSURERS TAX ON BRAND NAME DRUGS $500K EXECUTIVE COMPENSATION

LIMIT FOR HEALTH INSURANCE EXECUTIVES

TAXES THAT WILL NOT AFFECT THE AVERAGE INDIVIDUAL

NEW TAXES ON INDIVIDUALS

MEDICARE TAX ON INVESTMENT INCOME 3.8% MEDICARE PART A TAX INCREASE OF .9% 40% EXCISE TAX ON HIGH END PREMIUM HEALTH

INSURANCE PLANS (BEGINS 2018) ANNUAL $63 FEE LEVIED BY ACA ON ALL PLANS MEDICINE CABINET TAX ADDITIONAL TAX ON HSA/MSA DISTRIBUTIONS FOR NON

QUALIFIED MEDICAL EXPENSES FSA SPENDING ACCOUNT CAP MEDICAL ITEMIZED DEDUCTIONS ON SCHEDULE A

GOING FROM 7.5% TO 10% WAIVED FOR 65 YO+ IN 2013-2016

ADDITIONAL MEDICARE TAX

Applies to wages and self-employment income – NOT used for Medicare – Tax is 0.9% – Married, filing jointly $250,000 – Single, HOH, qualifying widow(er) $200,000 – Employer is required to withhold for wages over $200,000 – For higher earning MFJ, an adjustment to withholding or estimated

taxes may be necessary

TAX PREPARER TIP • If you have MFJ clients in this

income range it’s probably their withholding will not be enough. Resolve with quarterly payments or a change to the W-4

FLEXIBLE SPENDING ACCOUNT CAP

Formally, Pre-tax funds used for medical expenses – Includes contact lenses, children’s braces, OTC drugs – Special needs children tuition was eligible – No cap – No carryover

New, Pre-Tax funds used for medical expenses

– Can not be used for OTC drugs – New Cap = $2500 – $500 carryover

HSA – HEALTH SPENDING ACCOUNT

• Like an IRA • Non-Medical withdrawals incur a 20% penalty • Contributions can be up to $3300 for individual or $6550 for family • 55 and older may add $1000 catch up • Min. annual health insurance deductible $1250/Single or

$2500/Family • Max. out of pocket $6350/Single or $12,700/Family • Can withdraw excess at age 65 • Tax free earnings if used for medical expenses • Rolls over year after year • www.hsacenter.com

TAX PREPARER TIP • Educate yourself and talk to

clients about how an HSA can replace an FSA and save them money. Find a good Financial Planner to set up the accounts for your clients.

MEDICAL LOSS RATIO (MLR) WILL THEY GIVE IT BACK?

• ACA REQUIRES 80-85% OF PREMIUMS BE SPENT ON HEALTHCARE SERVICES AND HEALTHCARE QUALITY IMPROVEMENTS

• REFUNDED PREMIUMS MAY BE TAXABLE – Refunded premiums reduce the insurance companies’ taxable income – The reduction year and/or an estimated reserve have yet to be

addressed – If the taxpayer did not claim a health insurance deduction on their

1040, it is not taxable – If the taxpayer deducted health insurance on their schedule A or as a

SEHI, then they must claim the refund as income – It’s unlikely the taxpayer will receive a form 1099-MISC – As a tax preparer, we should ask and report!

TAX PREPARER TIP • Be sure to ask your clients

if they received a payment from their insurance company. It may be taxable.

SCHEDULE A MEDICAL DEDUCTION THRESHOLD INCREASE

• Increased from 7.5% to 10% • Waived for 65+ year olds for 2013-2016 • With higher ACA deductibles more and more

people will have medical expenses on their Schedule A

• This “increased tax” will affect a lot of people

DEFINING THE NIIT

A 3.8% net investment income tax went into effect starting in 2013 for individuals, estates, and trusts that have investment income above certain threshold amounts.

NET INVESTMENT INCOME TAX

NET INVESTMENT INCOME TAX

Filing Status Threshold Married, filing jointly $250,000 Married, filing separately $125,000 Single $200,000 Head of Household $200,000 Qualifying Widow(er) $250,000

TAXPAYERS THAT MAKE MORE THAN $200,000-$250.000

MAGI Thresholds for the NIIT

TAX PREPARER TIP • For taxpayers close to the limit, the focus is to

maintain consistency of income from year to year. Spikes in income (a bonus, IRA withdrawals, large capital gains) can trigger the NIIT for income like rents, interest, dividends, and other investment income.

• Consider an installment sale strategy for the sale of business property.

NIIT

A. Interest B. Dividends C. Capital Gains D. Rental Income E. Royalty Income F. Non Qualified Annuities G. Income from businesses involved in trading securities H. Income from a passive business I. Gains from the sale of stocks, bonds, and mutual funds J. Capital Gain distributions from mutual funds K. Gains from the sale of investment real estate L. Gains from the sale of interests in partnerships and S Corps

WHAT IS INCLUDED IN THE NIIT?

NIIT

A. Wages B. Unemployment compensation C. Operating income from a non-passive business D. Social Security benefits E. Alimony F. Tax exempt interest G. Distributions from certain qualified plans (401A; 403B; 457B;

traditional IRA)

WHAT IS NOT INCLUDED IN THE NIIT?

HOW DOES THE 3.8% SURTAX WORK? MARRIED COUPLE WITH INCOME OVER $250K

TAX PREPARER TIP Have your clients: • Investment in tax exempt bonds • Minimize dividends-invest for capital appreciation • Increase participation to make passive gains non-passive • Convert passive income to salary (be careful with the 0.9%

Medicare tax) • Strategically take capital losses • Convert to ROTHs in low income years • Maximize above the line deductions like HSA, SEP, and traditional

IRAs.

OBAMACARE MEDICAID EXPANSION

• Original law called for expansion in every state – Supreme court ruling allowed states to opt out

• Expanded Medicaid plan would expand coverage to citizens at 138% of FPL

• Alabama has opted out creating a coverage gap • Different studies project different results for Alabama

ESTIMATED INCOME FROM NEW TAXES OVER NEXT 10 YEARS

Tax Estimated Income (Billions) NIIT $123 Medicare Payroll Tax $86 Individual Employer Mandate $65 Tax on Health Insurers $60.1 Excise Tax on Cadillac Plans $32 Biofuel Tax $23.6 Medical Device Manufacturing $20 Schedule A Medical Deduction $15.2 Tanning Tax $2.7

HOSPITALS AND PHYSICIANS HOW DO THEY GET PAID?

• Medicare is prospective. Paid based on the patient’s DRG (diagnosis related group).

• Medicaid pays based on a per diem. Usually less than $1000 per day.

• BCBS pays based on a per diem. $1500 to $2500 per day.

• A small percentage of insurance companies percent of charges.

• Self pay is usually no pay.

ISSUES PROVIDERS WILL FACE

Improving Quality Cost to track quality Follow up with discharged patients Denied charges

Inpatient Value Based Purchasing Program ACA’s main pay for performance quality

improvement mechanism Re-admission Penalties

Hospital Re-Admission Reduction Program

• Penalizes hospitals with high 30-day re-admission rates

• Penalty of Medicare reimbursement

• 2013 max. penalty is 1% • 2014 max. penalty is 2% • 2015 max. penalty is 3%

•2013 – 2/3 of hospitals were penalized

ISSUES PROVIDERS WILL FACE

AKA Reimbursement Adjustment Based on Quality • Large practices are subject in 2015 • Small practices are subject in 2017

PHYSICIAN VALUE BASED PAYMENT MODIFIER PROGRAM

ISSUES PROVIDERS WILL FACE

Electronic Health Record (EHR) Meaningful Use

We will continue to face issues in meeting stage 1-3 requirements and incurring a large expense to do so.

ELECTRONIC HEALTH RECORD

ISSUES PROVIDERS WILL FACE

Deductibles are rising! This creates more collection efforts, increased staff, less reimbursement and higher bad debt. Patients will begin to ration their own care due to out of pocket costs. Less Reimbursement = Less Everything Where do you cut costs?

- FTEs - Benefits - Raises - Other cuts…

RISING DEDUCTIBLES

ISSUES PROVIDERS WILL FACE

The focus must be on the patient as a whole rather than an episode of care. How do we do that? Who do we partner with? How much will it cost in the early years? Community Hospitals will begin to eliminate services that become unprofitable example: OB services Hospitals and Physicians must start working together!

COOPERATION CRITICAL

ISSUES PROVIDERS WILL FACE

• 2% Medicare DRG payment reduction • Sequestration • Medicare disproportionate share cuts

• 25% is still paid as it was historically • 75% will fund a pool to be distributed based on

Medicare and Medicaid inpatient days • Pool has been reduced $546 million

Are we moving toward alternate forms of payment including pay for performance, bundled payments, capitation, or even a single payor system???

QUESTIONS?

Richard Byerly, CPA

Byerly & Associates 120 S Ross St

Auburn, AL 36830 334-740-7037

[email protected] www.byerlycpa.com

www.churchtaxcredit.com