nq magazine, august 2015

DESCRIPTION

NQ is an online magazine for newly qualified accountants and those in the final stages of their qualification. It's packed full of careers advice, industry news and topical features on the state of the accountancy industry across the globe. A must-read for aspiring accountants everywhere.TRANSCRIPT

THE VOICE OF ALL NQs

CAN YOU TRUST CORPORATE

REPORTS?Companies are

increasingly using the word ‘trust’ in annual

reports. Why?

TIME MANAGEMENT

How you can better manage that invaluable resource

– your time

Contact usemail:

[email protected]: @pqmagazine

facebook: pqmagazine.comcall: 020 7216 6444

August 2015

ETHNIC MINORITY ACCOUNTANTS IN THE WORKPLACE

Page 8

CORPORATE SECURITY

HOW ACCOUNTANTS COMPROMISE THE DIGITAL SECURITY OF THE

FIRMS THEY WORK FOR P20

P16

P18

P14

Institute of Directors demands UK bosses to go beyond ‘tick-box’ excercises when it

comes to corporate governance

IoD BRANDISHES

RED CARDTAX

SIMPLIFICATION

Key principles that will make

the UK’s tax system more

simplePage 12

ALL THE NEWS YOU NEED

and a whole lot more Pages 4 and 7

hays.co.uk/nq

SECRETS TO SUCCESSTOP INTERVIEW TIPS

As a newly-qualifed accountant, the next

important step in your career will be making

sure that you present the very best version

of yourself when it comes to meeting

prospective employers.

Our expert consultants in Accountancy and Finance have

created a list of tips and advice to help you prepare your CV.

THE RIGHT STRUCTURE

It’s important to assemble your CV using the most relevant

information in the appropriate order. Start with your contact

details, and then your eligibility to work in the UK. Include a

personal and skill summary followed by your work experience,

ensuring you start with the most recent frst. You should then

detail your education, training and qualifcations, leaving your

hobbies and references until last.

CONTENT IS KEY

Start by researching the company you are applying for and

tailoring your CV accordingly, you should match your skills and

experiences to refect their brand values. Most importantly make

sure you are showcasing all your key skills and achievements

in an honest fashion. Ensure you read the job description and

understand what is required of you to fulfl the role. You can refer

to the job description in your CV, tailoring your experience and

knowledge to suit the role. If you aren’t applying for a specifc

role, review similar job descriptions online and tailor your CV to

these. This is a good way to see what further skills or experience

you may need.

ATTENTION TO DETAIL

Your CV should be clean and well laid out using a professional

font such as Arial, 10pt. Start each bullet point with a verb

such as ‘created’ or ‘increased’, and it may also help to include

technical terminology in your CV so that the employer knows

you understand the industry. Spelling and punctuation must

be perfect, after you have proofread the text give it to a friend

to check for any errors. Finally, use an email account with a

professional tone, for example [email protected] instead of

To fnd out more about jobs on ofer visit us online,

or for help with planning your career contact Jane Knight

on 020 3465 0012 or email [email protected]

Join the ‘Hays Accountancy and Finance UK’

Facebook community today.

Hays Accountancy & Finance UK

AF-13284 NQ Magazine - 27 07 2015.indd 1 17/07/2015 15:20

COMMENT

Who do you trust?Trust you are enjoying the summer. One thing we can all trust is that the weather in the UK can’t be trusted! Now look what I have done – both CIMA and Robert Philips will be on my case for my over-use of the word ‘trust’. It appears that, over the past 10 years, this particular

word has become the corporate buzzword in annual reports (see page 16). But, as Phillips points out, trust and trustworthiness is not something companies can control – it is an outcome.

The National Association of Pension Funds (NAPF) is also on the corporate reporting case (page 17). It has a problem with the way companies report on ‘their greatest asset’ – its people! It wants to know more – about the composition of the workforce, its stability, its skills-set and its motivation and engagement.

We had a wry smile at research that showed nearly one in three accountants aren’t sure if their firm had an IT policy. One in 10 have even altered their computer settings, including compromising firewalls, to get what they want (page 21). Now we know we have all been hacked but some accountants’ behaviour at work seems the equivalent of leaving the front door permanently open. The worry has to be just how much breaches of security are now costing to put right. The average cost of the most severe online security transgression for big business now starts at £1.46m. That has doubled in one year.

Finally, we felt we needed to share the new research from Pearn Kandola about ethnic diversity in the accountancy profession. With 52% of ethnic minority accountants feeling discriminated against the solution is not as straight-forward as you may have thought (see page 8). Political correctness is a problem, as is black, Asian and minority ethnic (Bame) candidates unconsciously deselecting themselves from certain roles and organisations.

I trust you’ll enjoy this issue of NQ!

Graham Hambly, Editor ([email protected])

EDITOR’S COMMENTS

NUMBER CRUNCHING

of executives felt their management risk processes were not ‘mature’ P4

70%

Percentage of ethnic minority accountants

who feel discriminated against in the workplace P8

52%

cost to a hedge fund of a recent ‘Friday afternoon fraud’ P20

£740,000

the number of times the word ‘trust’

appeared in the annual reports of the FTSE 100 P16

317

the amount of time you

need to set aside to prioritise tasks for the following day P18

15 minutes

the total membership of the ACCA. It has 455,000 registered students, too P7

178,000

4 NQ Magazine August 2015

NEWS

Enhancing the conceptual underpinning of reportingThe International Accounting Standards Board (IASB) has

issued an exposure draft on proposed changes to the Conceptual Framework.

The ‘enhancements’ include a new chapter on measurement that describes appropriate measurement bases (historic cost and current value, including fair value) and the factors to consider when selecting a measurement basis.

The draft confirms that the statement of profit and loss is the primary source of

information about a company’s performance, adding guidance on when income and expenses can be reported outside the statement of profit and loss, in ‘other comprehensive income’ (OCI).

IASB chair Hans Hoogervorst said that a solid Conceptual Framework is essential because

it shapes the decisions the IASB takes when developing standards. He said the two particularly important areas of the proposals are “ the clarification of the key role of profit or loss as an indicator of a company’s financial performance, and the chapter that describes the information provided by historical cost and current value measurements”.

The FRC has welcomed the draft. It said the framework will have a central role in the development of IFRS’s and so have a profound influence on financial reporting in the UK, Europe and globally.

Businesses are putting themselves in danger by neglecting or avoiding formal risk management processes, according to a new study by CIMA and North Carolina State University.

The report’s authors found that 70% of executives felt their management processes were not ‘mature’. And just 40% are satisfied with the reporting of information about top risk exposures to senior management.

CIMA’s Gillian Lees felt that, almost 10 years on from the global crash triggered by poor understanding of risk, it is depressing to see how little has changed. She suggested this is equivalent to not bothering to lock your house after a burglary. Lees explained: “Identifying possible threats to a business is essential for securing the firm’s future. Adapting to future risks and changes can give a company a competitive advantage. Failing to do either means sleepwalking towards disaster.”So what do companies need to do:● Organisations need to develop formal risk management structures that are integrated with their strategies. This will mean they are better informed to identify their most pressing risks.● There needs to be a clear way for risk management information to be passed upwards to those leading the strategies of the business. This will increase the businesses’ agility and ability to navigate the challenges and impact.● Boards need to establish risk management committees or have a board director responsible for this area to ensure they are adequately informed about key strategic risk information.

Sleeping walking to disaster

¢ Your free data serviceCompanies House has launched a public beta search service allowing users to access all of its digital data free of charge. This gives access to over 170m digital records on both companies and their directors, including company overviews, financial accounts, current and resigned officers and company filings.

New features are planned to become available in the coming months. These include officer searching, disqualified directors, dissolved companies and overseas data.

¢ Scrap quarterly updatesThe scrapping of quarterly updates would help the City adopt longer-term thinking, says Legal & General’s Mark Zinkula. He said there were other ways of staying in touch with shareholders and believes reporting to the stock

market twice a year through interim and full-year results would be a more effective use of everyone’s time!

¢ Call us RSMBaker Tilly is to adopt RSM as its brand name. Managing Partner Laurence Large said that although the name was changing the firm will continue to maintain the core essence and legacy of the Baker Tilly brand. The change becomes effective from 26 October 2015.

¢ ACCA and IIA join forcesACCA has agreed with the IIA (the Institute of Internal Auditors) to develop their Certified Internal Auditor (CIA) Challenge exam so it can be made available to members in November 2015. The deal will provide ACCA members with the opportunity to become CIA certified through the customised exam.

IN BRIEF

Hans Hoogervorst

Finance ManagerMedia & Advertising

To £55,000

•CIMA/ACCA/ACAQualified•LookingforanambitiousanddrivenFinanceManagertoimplementchangesandmakeanimpactonthefinanceteam.

•Developingandmanagingthecurrentteambychallengingandimprovingontheircurrentprocesses.

•Excitingplacetoworkwhereemployeesareencouragedtodevelopandimproveupontheirskillsetsatalltimes.

•Responsibilitiesincludeowningandmanagingeachperiodendtimetable,toensurealltasksarecompletedbyspecifieddeadlines.

•Ensurethatallbalancesheetreconciliationsareunderstood,completedandreviewedeachperiod.

•GuaranteethatSarbanesOxleyrequirementsarecompliedwithandthatallinternalcontrolsandprocessesaredocumented,centrallystoredandproperlycarriedout.

•ThisrolesupportstheCommercialFinanceteambypartneringwiththewiderbusinesstoensuretheyhavetherightsupportandtraining.

Commercial Finance AnalystLogistics

To £55,000 + Benefits

•CIMA/ACCA/ACAQualified•AdvancedExcelskills(pivottables,linkingspreadsheets&lookuptables).

•Rolerequiresstrongpresentationskillsandacommercialoutlook.

•TheCommercialFinanceAnalystwillactasabusinesspartnertokeystakeholderswithinkeybusinessunits.

•Responsibleforfinancialevaluationofnewcontracts,pricinganddecisionmakingsupportforthemajoraccountsacrosstheorganisation.

•Furtherresponsibilitiesincludeprovidingannualprofitabilityanalysisforkeyaccounts,implementingkeyperformancemetricstodriveprofitability.

•Identifyingcustomerspecificprofitabilitydrivers,managingandimplementingproactiveprofitimprovementplans.

•Businesspartneringwithaccountmanagementoncontractnegotiations,supportingthecreation&improvementprocesses.

Switch to a brighter future!

www.walkerdendle.co.uk T: +44 (0)20 8408 9999 E: [email protected]

7NQ Magazine August 2015

NEWS

Landmark changes for small businessThe Financial Reporting Council (FRC) has issued a suite of changes it is hoping will simplify accounting standards for micro-entities and small businesses in the UK.

The changes are largely being made in response to the implementation of a new EU Accounting Directive, and include:● A new standard FRS 105 ‘The Financial Reporting Standard applicable to the Micro-entities Regime’.● New Section 1A ‘Small Entities’ for FRS 102.● Other changes necessary for continued compliance with company law.

All the main changes are effective for accounting periods beginning on or after 1 January 2016, with early application permitted for accounting periods beginning on or after 1 January 2015.

In September 2015, the FRC is expected to issue revised editions of FRS 100 ‘Application of Financial Reporting Requirements’, FRS 101 ’Reduced Disclosure Framework’ and FRS 102 ‘The Financial Reporting Standard applicable in the UK and RoI’. These will reflect the changes announced in July.

Baker Tilly’s Danielle Stewart said these were ‘landmark changes’ and will have the effect of cutting red tape for any small company in the UK that chooses to take up the exemptions.

She went on: “While some accountants may mourn the withdrawal of the current accounting standard for smaller entities, the new replacement standard will allow around 1.5m of the UK’s smallest companies to benefit from far simpler reporting requirements.”

Perhaps the most significant impact of this new regime arises, Stewart felt, because the upper turnover threshold for small companies has been raised from £6.5m to £10.2m.

It will also be the first time under UK GAAP that small companies will not have to include a cash flow statement in their accounts.

Diversity mattersA ground-breaking study of the top 10,000 executives in Britain’s most important firms reveals a deep ‘diversity deficit’ that could put UK companies at a serious disadvantage in both domestic and global markets.

The research, from recruitment firm Green Park, shows that while some

sectors of the economy are more gender and ethno-culturally diverse than others, the glass ceiling remains completely intact in all types of business.

Strikingly, professional and support services appears to be relatively non-diverse on every measure.

Report authors Trevor Philips and Professor Richard Webber explain that, broadly speaking, companies that are successful at promoting women to senior positions are not doing the same for minorities, and vice versa. Philips suggests the consensus is that the business elite is simply too narrow in its outlook, too prone to the ‘herd mentality’ and just not switched on enough to the modern world.

ACCA records record numbersThe ACCA looks just two short years away from breaking the 200,000-member barrier.

Latest figures for the year show an increase of more than 5% in member numbers, as 11,530 new members pushed the membership total to 178,000.

Student numbers are also up, but by only 3%. The ACCA recorded 455,000 students, of which 397,000 are studying for the ACCA qualification in 2014-15. This is an increase of over 12,000 on the previous year.

ACCA CEO Helen Brand said that demand for professional, ethical accountants is on the rise right across the world. Its research also found that 89% of learning providers who teach more than one professional accountancy qualification would recommend ACCA to prospective students is very welcome news.

¢ Shares for staffAccountants Price Bailey has made history by offering its 300 employees a stake in the firm. Each employee with more than one year’s service, irrespective of grade, will receive 25,000 shares in the firm at a value of around £250.

¢ Bank on an appBritain’s first digital-only bank has been given a banking licence. It’s called Atom Bank and will open for business later this year. Atom will only be available though an app via smartphones and tablets.

¢ New job for DeaneAccountant Julie Deane, famed for launching her Cambridge Satchel Company with just £600, has a new role. She has been asked to carry out an independent review for the government of self-employment in the UK, looking at the challenges faced by those who work for themselves.

¢ Madam PresidentCIMA has elected Myriam Madden (pictured) as its 82nd President. Madden is only the second woman to be elected to the office. She has worked for HBOS, Hewlett Packard, the Scottish Arts Council and the NHS, to name but a few!

IN BRIEF

Trevor Philips

Danielle Stewart

8 NQ Magazine August 2015

THE WORKPLACE

A black and white issue?Some 52% of ethnic minority accountants feel discriminated against at work, according to research. NQ went along to a seminar hosted by analysts Pearn Kandola, where the issue was discussed

A ccountancy once had a very poor record for attracting and employing Bame (black,

Asian and minority ethnic) candidates. Things have undoubtedly improved: from the 1960s to the 1980s the profession was almost exclusively white, with the senior roles occupied by men and a large gender pay differential. But, prompted by various race equality acts, by 2001 the percentage of Bame students studying for an accountancy degree was 28.9; by 2013 this figure was 43.5. But there’s another statistic

the organisation has no relatable role models; the candidate has no friends or family members working in the sector; they are not aware of the benefits of working in the sector; they perceive it is harder to “make it” than it is for their white candidates.

Added to that, recent studies have found that recruiters discriminate against candidates with foreign-sounding names or against women, when sifting through applications for roles.

So discrimination

to counter that: the percentage of Bame students studying at the Russell Group of universities is just 24%; for Oxbridge that percentage is just 0.2% (black students). Given that the major accountancy firms tend to recruit from Oxbridge and the Russell Group, there is still clearly a problem of access.

Interestingly, candidates unconsciously ‘deselect’ themselves for applying for certain roles with certain organisations, said Pearn Kandola’s Professor Binna Kandola. This could be for a number of reasons:

9NQ Magazine August 2015

THE WORKPLACE

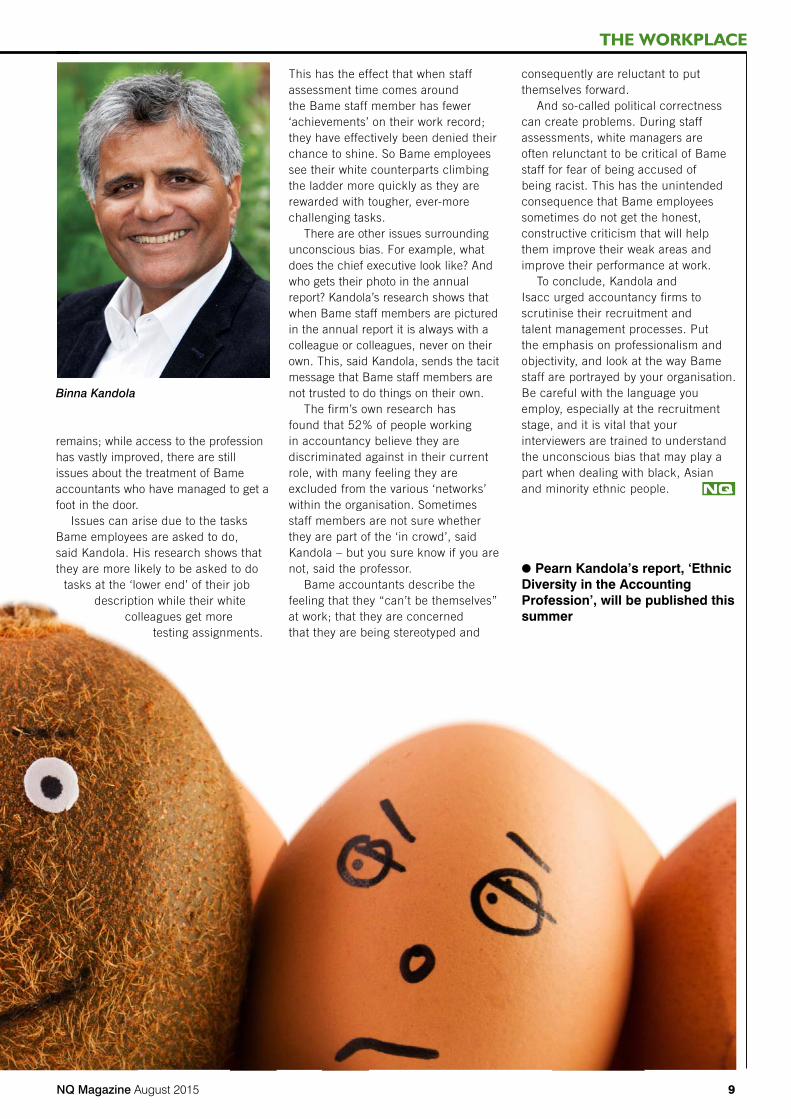

remains; while access to the profession has vastly improved, there are still issues about the treatment of Bame accountants who have managed to get a foot in the door.

Issues can arise due to the tasks Bame employees are asked to do, said Kandola. His research shows that they are more likely to be asked to do

tasks at the ‘lower end’ of their job description while their white

colleagues get more testing assignments.

This has the effect that when staff assessment time comes around the Bame staff member has fewer ‘achievements’ on their work record; they have effectively been denied their chance to shine. So Bame employees see their white counterparts climbing the ladder more quickly as they are rewarded with tougher, ever-more challenging tasks.

There are other issues surrounding unconscious bias. For example, what does the chief executive look like? And who gets their photo in the annual report? Kandola’s research shows that when Bame staff members are pictured in the annual report it is always with a colleague or colleagues, never on their own. This, said Kandola, sends the tacit message that Bame staff members are not trusted to do things on their own.

The firm’s own research has found that 52% of people working in accountancy believe they are discriminated against in their current role, with many feeling they are excluded from the various ‘networks’ within the organisation. Sometimes staff members are not sure whether they are part of the ‘in crowd’, said Kandola – but you sure know if you are not, said the professor.

Bame accountants describe the feeling that they “can’t be themselves” at work; that they are concerned that they are being stereotyped and

consequently are reluctant to put themselves forward.

And so-called political correctness can create problems. During staff assessments, white managers are often relunctant to be critical of Bame staff for fear of being accused of being racist. This has the unintended consequence that Bame employees sometimes do not get the honest, constructive criticism that will help them improve their weak areas and improve their performance at work.

To conclude, Kandola and Isacc urged accountancy firms to scrutinise their recruitment and talent management processes. Put the emphasis on professionalism and objectivity, and look at the way Bame staff are portrayed by your organisation. Be careful with the language you employ, especially at the recruitment stage, and it is vital that your interviewers are trained to understand the unconscious bias that may play a part when dealing with black, Asian and minority ethnic people.

● Pearn Kandola’s report, ‘Ethnic Diversity in the Accounting Profession’, will be published this summer

NQ

Binna Kandola

10 NQ Magazine August 2015

ETHICAL DILEMMA

Objective test How should you handle the audit of a client fi rm in which, due to unforeseen circumstances, your fi rm of accountants has a fi nancial interest?

Outline of the case

You are a partner in a three-partner firm of accountants. The firm generates fees in the region of £1.4 million a year. Within your portfolio of clients is Company A, which has been very successful since it first came to your firm five years ago. It now has an annual turnover in excess of £15 million.

Company A generates annually recurring fees for the practice of about £50,000, of which £35,000 is in respect of audit work and £15,000 relates to routine tax calculations and preparation of the corporation tax return. Your firm has a separate tax department, which performs the tax compliance work for Company A.

The company’s financial year end is December. Last year the audit work started in June, and the audit report was finally signed in August. By the end of August the tax return had been submitted to the taxation authority, and the firm’s invoice had been issued to Company A.

In September, a significant customer of Company A went into receivership, and Company A suffered a large bad debt. The directors approached you immediately, and were very open about the company’s short-term cash flow problem. Therefore you agreed that payment of the firm’s invoice of £50,000 could be spread over 10 months, commencing in October.

Company A also needs the support of its bank and, in December, it was negotiating a modest increase in its overdraft facility. It is now early March, and the bank has requested audited financial statements by the end of the month. The audit is well under way, and you have promised the directors of Company A that the bank will have the audited accounts on time.

The planning of the audit was performed by the audit senior and reviewed by the audit manager for the assignment (in whom you have a great deal of confidence). Due to pressure of work, you did not review the audit plan in detail before the audit team

commenced the year end audit work, and so you decide to review and sign off that section of the audit file now.

You note that the audit manager has correctly identified going concern as the area of the audit attracting greatest risk. However, at the time of planning the audit, the manager was unaware of the credit agreement reached with regard to the payment of last year’s fees. You check your firm’s records, and determine that Company A still owes the firm £25,000.

Key fundamental principles

Integrity: There was a flaw in the planning of the audit, which was not noticed by the audit manager before the audit work commenced. Is it possible to ignore the flaw and yet act with integrity, given that the flaw was unintentional? Objectivity: Can you reach an objective audit conclusion in view of your wish for Company A to continue trading and settle its outstanding fees to your firm? Professional competence: You need to bear in mind any ethical standards for auditors relevant to the country in which you practice. Professional behaviour: Regardless of the actual impact of the outstanding debt on your objectivity, if the bank (or a hypothetical, objective, well-informed third party) knew of the outstanding fees, what impact would it have on your firm’s reputation?

Considerations

Identify relevant facts: Through a combination of circumstances, your firm is under pressure to complete an audit assignment while it has a financial interest in the client. The debt of Company A to your firm was not as a result of an investment decision, but a pragmatic

11NQ Magazine August 2015

ETHICAL DILEMMA

solution to a problem being faced by an honest client. Nevertheless, your firm has a clear interest in the client’s ongoing existence, and would not want the audit opinion to jeopardise the repayment of the debt. Identify affected parties: Potentially, the affected parties are you and your firm, Company A, the bank and any stakeholders in Company A who will refer to your firm’s audit opinion. Who should be involved in the resolution: You may involve the audit manager in discussions, although he can do nothing to make your opinion more objective. He can only provide advice (as can your professional body). You should certainly involve your partners, and consider who else you may involve who is free from any personal interest in Company A.

Possible course of action

You need to ensure that the audit opinion is reached objectively, but also that a reasonable and informed third party would conclude that objectivity has been adequately safeguarded. Any discussion with the audit manager and the audit senior, who performed the planning initially, should have the objective of amending the firm’s planning procedures to ensure that outstanding fees are always considered in the future.

The bank will probably have reviewed Company A’s debtors and creditors at various times and may, at any time, question how your firm could retain objectivity. You may wish to pre-empt such a question by disclosing to the bank (with the consent of your client) the safeguards you have put in place.

In any event, you should discuss those safeguards with the directors of Company A, as there will be costs associated with the safeguards, and it would appear reasonable to pass these costs on to the client.

The appropriate safeguards will depend on the

significance of the threat presented by the outstanding fees of £25,000. This will depend on many factors, including the personal circumstances of you and your partners. In the context of the firm, the debt of £25,000 represents less than 2% of the firm’s annual income. However, the annual fee income from the client (£50,000) equates to 3.6% of the firm’s income and, when the invoice is raised for the current audit, the outstanding debt will be significant.

You must minimise the threat to objectivity brought about by the firm’s interest in Company A continuing to trade. A possible solution may be to obtain directors’ guarantees in respect of the outstanding fees and the invoice that is soon to be raised. Provided the directors are in a position to provide such guarantees, this would have a commercial benefit as well as an ethical one. It will almost certainly be necessary to obtain legal advice before entering into such an agreement.

However, even if this possible course of action is pursued, it may not be sufficient to reduce the threat to objectivity to an insignificant level. This may only be achieved by introducing an independent auditor to review your firm’s audit work before the audit report is signed.

This should be someone who is independent of the firm and therefore unsympathetic to the firm’s interests. It may be advisable to engage a consultancy company to perform the review, and to discuss with your client how the additional costs will be met.

You should keep your partners informed of the issue, and the safeguards you intend to implement, throughout the resolution process.

You should document, in detail, the steps that you take in resolving your dilemma, in case your ethical judgement is challenged in the future.

● This article is taken from a series of Ethical Dilemmas Case Studies, published by the CCAB.See http://www.ccab.org.uk/reports.php

NQ

???

12 NQ Magazine August 2015

TAX

Don’t make it complicated

13NQ Magazine August 2015

TAX

their own views on areas of the code. But do let us know what you think is the most complex area of the system and we will give it a rating if we haven’t already!”

● The OTS’s paper on avoiding complexity can be found here: https://www.gov.uk/government/publications/how-to-avoid-complexity-in-the-tax-system

● The OTS’s complexity index can be found here: https://www.gov.uk/government/publications/offi ce-of-tax-simplifi cation-complexity-index

NQ

K ey principles for avoiding complexity in the tax system have been set out by the

Office of Tax Simplification (OTS). An OTS paper identifies four key principles for ensuring new and amended measures are as simple as possible.

Separately, the OTS has also published a revised version of its complexity index. The index provides a way of assessing the relative complexity of areas of the tax system. John Whiting, Tax Director of the Office of Tax Simplification, said: “The OTS’s brief is to develop recommendations for simplifying the tax system. Naturally, we see a lot of complexity – and we have had a general project running for some time on analysing complexity. The aim is to show what causes complexity – and so develop ways of avoiding it.

“We have drawn together the lessons we have learned over the period of the OTS’s work to date and set out what we see as the key principles of how to avoid complexity. They’re framed with tax policymakers in mind, but we hope that they will be of interest to all those involved with the tax system – and we hope they might provoke some debate.”

The complexity principles come out of the OTS’s work on specific areas of the tax system and identify the common themes and problems that affect very different areas of taxation.

The OTS found that change was the most significant factor in creating complexity. A stable but complex tax system becomes simpler as people become familiar with it.

The paper goes on to identify four principles politicians and policymakers are urged to consider to avoid adding unnecessary complexity. These are:● Ensure the proposed tax measure

meets the policy aims.● Focus the measure carefully.● Design the measure to meet the aim.● Maintain the measure properly.

The aim of the OTS’s complexity index is to judge the complexity of a

particular tax or set of rules. It is based on 10 factors, including the number of exemptions and reliefs, the number of pages of legislation, the complexity of HMRC guidance and the number of taxpayers affected.

It will be used to help the OTS identify future projects and for monitoring changes in complexity of different areas of tax.

Whiting said: “We can’t have a simple tax system – life is complex and the tax system will reflect that – but we can have a simpler tax system. The aim of our complexity index is to help identify the areas most in need of simplification. We use a range of factors to assess complexity which we think give a good representative result, though we accept that people will have

It is easy to avoid complexity in the tax system – don’t keep changing it! So says the Offi ce for Tax Simplifi cation, which also offers some other useful advice

THE OTS PRINCIPLES FOR AVOIDING COMPLEXITY ARE:

✔ Ensure the proposed tax measure meets the policy aims

● Should it be a tax measure in the first place? Would grants or further regulation be better?

● Will the benefit outweigh the disruption and transitional issues?

● Consider the likely impact on taxpayers, their advisers and HMRC.

✔ Focus the measure carefully

● Talk to the people affected by the legislation and try to see it from their point of view.

● Resist pleas by special interest groups for exceptions that cannot be proven to be really necessary.

● Consider the ability of the target group to understand the measure (e.g. pensioners) or claim it (e.g. small business).

✔ Design the measure to meet the aim

● Consider the administration in greater depth. What forms and guidance will be needed?

● Is there existing legislation that can be used? Better to use or build on what is there rather than start again.

● Stand back: does the new measure really do the job or has it become too involved?

✔ Maintain the measure properly

● Keep rules up-to-date with the changing circumstances.● Establish a process to assess and challenge provisions to

ensure they remain relevant.

John Whiting

14 NQ Magazine August 2015

CORPORATE GOVERNANCE

Hear no evil… former FIFA president Sepp Blatter

IoD brandishes the red card

15NQ Magazine August 2015

CORPORATE GOVERNANCE

NQ

The Institute of Directors (IoD) wants UK bosses to go beyond a ‘tick-box exercise’ when it comes to corporate governance

Whether it’s a multi-million-pound accounting error at Britain’s largest

supermarket chain, shareholder revolts over hefty pay-outs for FTSE executives or corruption at FIFA, the body that oversees world football, it’s never been more obvious that corporate governance matters. Unfortunately, the UK’s current approach to identifying what makes for good governance is flawed, according to new IoD report, The Great Governance Debate – Towards a Good Governance Index for Listed Companies.

Ken Olisa, Chairman of the advisory panel for the report, warned that it was wrong to rely on regulators, whose focus is inevitably on compliance, to improve governance at the UK’s biggest companies: “Identifying symptoms of governance failures, and then drawing up check lists to eradicate them, leaves us in the position of always fighting the last battle. The financial crisis was not caused by a lack of rules, it was caused by behaviour that was clearly egregious to any outside observer. Unfortunately, the UK seems to have learned little since the crisis, sticking to a prescriptive set of attributes aimed at creating the ‘cardboard cut-out’ perfect company.

At least the ‘comply-or-explain’ principle recognises that businesses’ circumstances are different, he said. But there is a need to go one step further and accept that even if all listed companies were 100% compliant with the corporate governance code this would not prevent future scandals, failures or collapses. A false sense of security created by compliance is no security at all.

One of the key findings of this new research is that no single factor dictates whether a company is well run, whether that’s the number of non-executives on a board or how often the auditor is changed. It is simply not correct for a company to say that because they have ticked certain boxes they show good governance.

Olisa believes now is the time for some bold thinking on how we define and measure governance, including the recognition that it is essentially an organic process involving the interaction of groups of people.

The IoD intends to lead the way in creating a better way of looking at governance that gives investors, employees and the wider public

greater confidence in the transparency and accountability of our biggest companies.

Its report takes a fresh look at what board practices actually matter, and for the first time combines external perceptions of whether a company is well-run with the objective factors normally used to judge good governance.

Simon Walker, Director General of the IoD, explained the motivation behind the report: “The reputation of corporate Britain took an almighty kicking during the financial crisis, and several years later is still on its knees. Any attempt to restore public faith in business must start with good corporate governance, but focusing solely on how companies report compliance with a framework, while not looking at underlying behaviour, will simply not do the job. This report challenges previous ways of measuring the governance of big companies, and kicks off a new debate on how firms can improve their transparency, accountability and performance.”

The IoD, in association with Cass Business School, has set itself the task of creating a robust index that does not encourage box-ticking and will stay reliable as the economy and business change over time. The panel overseeing the project looked at instrumental governance factors including business performance, audit arrangements, directors’ pay and shareholder relations, and undertook a survey of business people’s perceptions of the UK’s biggest companies.

In a new approach, the panel then combined this information in an attempt to achieve a more impartial and deeper understanding of the governance of these companies. This is an important step towards creating an index of listed companies, which will aid investors and directors in their decision-making.

16 NQ Magazine August 2015

CORPORATE REPORTING

Who do we trust? So why are companies increasingly using the word ‘trust’ in their annual reports?

Companies’ use of the word ‘trust’ has risen by a factor of eight in the past decade, indicating

an increasing corporate obsession with trustworthiness, according to a study by CIMA and Robert Phillips, author of ‘Trust me, PR is dead’. They argue that, sadly, the focus on trust is not always backed up by corporate action. “Trust often spoken is trust rarely earned,” says Phillips.

An analysis of the use of ‘trust’ – when referring to the concept, not the legal structure – in annual reports of FTSE 100 companies over the past decade found that the word was mentioned just 38 times in 2005, but has climbed steadily since, appearing on 317 occasions in 2014.

Tony Manwaring, CIMA’s executive director of external affairs, said: “The concept of ‘trust’ has always been misused by companies, but the past 10 years has seen it achieve staggering growth as a corporate buzzword.

“This is bizarre, because trust is not something companies can directly control – it is an outcome. It does not work as a message. Endlessly repeat the word ‘trust’ if you want, but it will not make people trust you.”

Likewise, the phrase “building trust” appeared just once in a single 2005 annual report; in 2013 it was mentioned 18 times.

Robert Phillips said: “I would happily retire the t-word from the English language for a decade or two, allowing us time to refl ect on what it really means to be trusted or trustworthy. It has been used and abused to the point of exhaustion. This is where so many leaders immediately fail. They think that by speaking endless words of trust or, in Ed Miliband’s case,

carving those words in stone, somehow we will trust them. We won’t.”

Phillips argues that to be more trusted, companies need to create “public value” as well as shareholder value, and focus on profi t optimisation rather than profi t maximisation. He cites banking, arguing that if a bank was to make radical changes, including copying the John Lewis Partnership employee ownership model, cutting out extravagant bonuses and levying a small charge to its retail banking customers rather than claiming to offer ‘free banking’ it would begin to earn genuine consumer trust, “and quickly address the challenge of being socially useless”.

He said: “If a fi rm wishes to become trustworthy, the answer does not lie with crafting narratives, managing messages or meaningless platitudes. We need actions, not words.” NQ

17NQ Magazine August 2015

CORPORATE REPORTING

Workforce-size hole in corporate reportingThe National Association of Pension Funds (NAPF) has published a new discussion paper highlighting the lack of reporting by companies on how they manage their workforce

D espite the familiar corporate mantra of “our people are our greatest asset”, and the widely accepted view that human capital is one of the four pillars of

capital that underpins corporate and economic growth (the others being physical, social and intellectual capital), most companies still fail to report on it in any meaningful way.

The report underlines the role of pension funds in the UK economy as long-term investors with a clear interest in promoting the long-term success of the companies in which they invest; but points out that NAPF members still often struggle to find any clear or consistent reporting with respect to an investee company’s workforce. While there has been significant evolution in recent years of corporate reporting on governance and environmental matters, the workforce remains notable by absence in company reports.

Joanne Segars, Chief Executive of NAPF, said: “We often hear much talk of the ‘productivity puzzle’ and how this can be solved to bolster the economic recovery, yet one of the key factors in driving growth – both corporate and economic – does not appear to be deemed sufficiently material for companies to measure or report. That factor is the people who constitute a company’s workforce, sometimes called its human capital.

“Companies often tell us they would report on this if investors asked them to – and too few investors make that request. But, on the other hand, investors say they would

place greater emphasis on this issue if more meaningful information were available. The NAPF wants to kick-start a discussion to resolve this conundrum. In the spirit of what gets measured gets managed and what gets reported gets done, we have identified four areas where there should be better disclosure and we will be encouraging investors, analysts, companies and policy makers to explore this agenda further.”

The four areas the NAPF suggests as areas to be developed in corporate reporting are:● The composition of the workforce.● The stability of the workforce.● The skills and capability of the workforce.● The motivation and engagement of the workforce.

The NAPF will host a series of roundtable discussions in the second half of this year to bring together investors, analysts, companies, standard setters and policy makers to develop expectations further. The conclusions of these discussions will also be incorporated into the NAPF’s Corporate Governance Policy & Voting Guidelines. NAPF will also provide an assessment of the progress made in this area in its 2016 Annual AGM Report.

● A full copy of the NAPF paper, Where is the workforce in corporate reporting? can be found at http://tinyurl.com/qjpfdaz.

Where is the workforce in corporate reporting?June 2015ww.napf.co.uk

NQ

18 NQ Magazine August 2015

Make more time for yourself

time management

E veryone recognises that sinking feeling you get when time is running away with you. Perhaps it’s already lunchtime and you’ve been too busy to drink

your morning coffee, or maybe you’ve been given a task with an incredibly tight deadline and are struggling to juggle it with existing work pressures.

Time management is an essential skill to master and could be the solution to your problems whether you are working on a project or starting a new role. You will always have to juggle different tasks and manage distractions, but understanding the difference between what’s important and what’s urgent and prioritising accordingly, can prevent your work snowballing out of control.

It’s not just life in the office that can be improved if you’re using your time effectively, your home life can benefit too. Ineffective time management can lead to stress and longer working hours, which can negatively affect your work/life balance and the quality of time you have out of work. Compromised wellbeing, tiredness and lack of motivation can then impact on your performance in the workplace, resulting in a vicious cycle. Mastering time management can go a long way to prevent this.

Taking control of your time can appear a daunting task at first, but it can be easily broken into easy steps – ironically you will need to invest some of your time to be successful. The first step is to learn that urgent is time related, importance is value related, but most people respond to urgency rather than importance. Whilst they can coincide, they’re not the same and a key point of time management is to deal with important tasks before they become urgent, as it is easier to do important tasks well when they’re not urgent.

Managing your time is an important skill, but it’s one that is well worth developing, says Nicki Cresswell

Once you know what you need to do first, you can plan how you will spend your day. Set aside at least 10 to 15 minutes every morning and split your day into sections. Allow adequate time to complete all urgent and important tasks in the morning, leaving a short gap between each one to deal with emails, conversations and unexpected tasks. Once you have allotted time for all your urgent tasks, you can think about how long you’ll need for all of your important activities and other tasks. The most effective time to make a list is at the end of the day before. Set aside 15 minutes to prioritise your tasks for the following day. This will enable you to have maximum focus and clarity at the start of the day.

Good communication is key for good time management. If it becomes clear when you’re planning your day that you won’t have time to complete something, raise this as soon as possible with your manager, or work out where you can gain some more time. Can you cut 15 minutes off another task? Could you re-prioritise your current workload? Ask those around you if they have any materials or input that could cut down the use of your time. If possible, delegate the task to another person who has more capacity, either to your manager, a colleague or an assistant.

Ensuring clear communication also limits mixed messages or unclear distractions. This saves you repeating conversations or having unexpected extra work to do. If you’re ever unclear about what you’ve been asked to do, make sure you clarify straight away rather than diving in not knowing what is expected of you.

Incorporating these practices into your day can help you be more productive but less busy.

19NQ Magazine August 2015

time management

1 Work out what you need to achieve before you start a task: Thinking through exactly what the result will be will guide how you get there, ensuring you stay focused and eliminate unnecessary ground work

2 Advise your colleagues that you’re busy: Making it clear that you’re concentrating on a specific, urgent task can cut down the number of distractions

3 Make time for emails and calls in between tasks: Don’t stop what you’re doing to flick through your emails. Commit to getting a certain amount of work done, and check your emails when you’re finished – consider whether they need responding to now or can wait until later in the day. You can also use your out of office to let people know when you’ll be able to respond

4 Use any spare time carefully: If you finish something earlier than expected, use the extra time productively. Can you make a list so you know where to start the next morning, or track down that piece of information you’ve been looking for?

5 Complete short tasks quickly: If you need to send a brief email or make a quick call, do it before you start a big task. Things that take under two minutes can be addressed immediately in-between bigger tasks, allowing them to be crossed off the to-do list

Managing your time well will make you more efficient and more productive, as well as allowing you to feel more in control of your work. There are bound to be times when demands appear overwhelming, but by prioritising your work you can ensure you make the most of the time available to you, achieving the best results you can.

● Nicki Cresswell is Wellbeing Training Coordinator at CABA

NQ

20 NQ Magazine August 2015

SECURITY

Beware the cyber attack

21NQ Magazine August 2015

SECURITY

So while the majority of accountants are security conscious about IT on the home front they have a different attitude at work!

And this comes at a price. The average cost of the most severe online security breaches for big business now starts at £1.46m. That is double the cost of the year before (£600,000).

The Information Security Breaches Survey 2015 shows the rising costs of malicious software attacks and staff-related breaches and illustrates the need to take action.

For small and medium sized businesses the most severe breaches cost can now reach as much as £310,800, up from £115,000 in 2014.

The good news is more firms are taking action to tackle the cyber threat, with one-third of organisations now using the government’s ‘Ten Steps to Cyber Security’ guidance (www.gov.uk/government/publications/10-steps-to-cyber-security-advice-sheets). Nearly half (49%) of all organisation have also achieved a ‘Cyber Essentials’ badge to protect themselves from common internet threats (www.cyberstreetwise.com/cyberessentials).

The survey showed 90% of large organisations reported they had suffered an information security breach, while 74% of SMEs reported the same. Worryingly, for companies with more than 500 employees the average cost of the most severe breaches is now £1.46m – £3.14m.

Attacks from ‘outsiders’ have also become a greater threat for both small and large businesses.

PwC’s Cyber Security Director, Andrew Miller, said that breaches are becoming increasingly sophisticated, often involving internal staff to amplify their effect.

It seems we all need to grow up when it comes to our attitudes to cyber security. If we don’t there is going to be an even bigger cost in the future.

NQ

D id you know there is a thing called ‘Friday afternoon fraud’? Apparently, the

fraudsters understand that by Friday afternoon most of us are looking to be in the pub or going home, and this makes us vulnerable.

The conmen are looking to catch people when they are feeling fatigued and more likely to make that one mistake that lets them in.

One hedge fund recently admitted it had lost £740,000 in such a sting. The CFO of Fortelus Capital, Thomas Meston, was tricked into giving away passwords and account details.

The fund is now suing Meston because the person he gave the details to at 6pm on that fateful Friday afternoon was not an employee of their bank, Coutts.

Earlier this year, the Solicitors Regulation Authority also issued a warning after it revealed it was receiving four reports a month from firms being tricked into giving bank details to fraudsters on Friday afternoons.

Fraud is everywhere, it appears we can trust no one. HMRC was also forced to issue a warning in early July as new stats showed that nearly 51,000 ‘phishing’ emails had been reported between April and July last year – double the number for the same periods in 2013.

Some of these scam messages claim to be from a ‘Tax Credit Office Agent’ offering a tax refund, or include a link to a fake version of the gov.uk website. Again, people are often asked to provide bank details or other sensitive information.

Last year HMRC worked with other agencies to shut down 8,877 of these scam websites – a 500% increase year-on-year. The message is: stay vigilant.

But let’s be realistic – we have all been hacked! Almost everyone in the western world has had their personal details stolen by digital fraudsters,

Security is a major issue for companies. And apparently there is one group you really need to be aware of – the accountants!

according to the man portrayed by Leonardo Di Caprio in the film ‘Catch Me If You Can’.

Frank Abagnale (we met him recently) works for the FBI and pointed to one well-known incident where the names, dates of birth, children’s details and social security numbers of 80 million Americans were stolen from Anthem insurance. This is not a lone story.

The problem is that hackers sit on the stolen information for months, even years, before using it.

Now what about accountants? Did you know that in a recent survey it was discovered that over one-third of UK accountants knowingly flout their own companies’ IT policy, opening a cyber-gateway to fraud?

New research by Lifeline IT reveals that one of the biggest threats of cyber-attacks, harmful viruses and fraud for accountancy firms actually comes from within their own workforce, who often ignore IT guidelines.

Only 42% of the thousands of accountants surveyed knew their firm’s IT policy, while nearly one-third said they weren’t even sure if there was one, and a quarter admitted there wasn’t one in place.

Almost two in 10 of the accountants owned up to visiting ‘restricted’ websites and going on social media, while 13% downloaded non-work related items such as YouTube clips and 10% circulated prohibited material including emoticons.

More seriously, an alarming one in 10 said they had altered their computer settings, including removing firewalls, to gain greater access to the internet; 2% have even opened quarantined or spam emails.

Interestingly, when it comes to using their own personal IT equipment over two-thirds claimed to be ‘really careful’ about security, with more than 60% saying they regularly updated anti-virus software and firewalls.

I need to findpqjobs.co.uk now!

PQ jobs pqjobs.co.uk

Your jobs boardnew pqjobs house ad 26/9/11 13:52 Page 1