northwest farm credit services 2013 annual report

DESCRIPTION

2013 Annual ReportTRANSCRIPT

2 0 1 3 A N N U A L R E P O R T

Preparing the NextGeneration of Leadership

Visit us at: northwestfcs.comYou may receive multiple copies of the annual report due to system changes and the need to send annual financial information to every stockholder of record.

PATRONAGE PAID($ in millions)

2009 2010 2011 2012 2013

26.0

36.0

53.3 55.258.1

Karen SchottBoard Chair

Bar Four RanchBroadview, Montana

The Schott family raises winter wheat, spring wheat, peas and also managesa lease pasture operation.

Investments in youth education, industry associations, sponsorships and our Rural Community Grant Program are making a profound difference in the communities where we live and work.

We would like to extend our gratitude to Bruce Nelson and Drew Eggers as they retire from the board of directors after 15 and 13 years respectively. Their leadership, expe-rience and considerable expertise in many areas has been invaluable in overseeing Northwest FCS’ strategy and performance. We wish Bruce, Drew and their families the very best and we look forward to welcoming two new directors in March.

On behalf of the Northwest FCS Board, we appreciate the confidence our customer-owners have placed in this association. We also want to recognize our 180 Local Advi-sory Committee members, 640 employees and our senior leadership team for a job well done.

2013 was another successful year for the association. We posted record net income that provided strong growth in capital, allowing Northwest FCS to strengthen its financial capacity to serve our customers. The association also paid $58.1 million in cash patronage to our customer-owners across the Northwest.

Those of us in agriculture have experienced a strong run the past several years during a time when many areas of the economy have struggled. But, we all know good times never last forever. The board and management team are carefully monitoring trends and economic indicators to ensure we are well po-sitioned and continue to build organizational capacity to support Northwest agriculture for generations to come.

To complement the business side of our mission, Northwest FCS continues to put the company’s talent and resources back into our rural communities. We believe strong communities foster strong businesses.

On Behalf of the Board

2

Pictured left to right:

Dave Nisbet Bay Center, Washington

Drew Eggers Meridian, Idaho

John Helle Dillon, Montana

Shawn Walters New Dale, Idaho

2013 Board of Directors

Kevin Riel Yakima, Washington

Julie Shiflett Spokane, Washington

Mark Gehring Salem, Oregon

Jim Farmer Nyssa, Oregon

Rick Barnes Callahan, California

Herb Karst Sunburst, Montana

Christy Burmeister-Smith Newman Lake, Washington

Bruce Nelson Spokane, Washington

Karen Schott Chair - Broadview, Montana

Dave Hedlin Vice Chair - Mt. Vernon, Washington

PATRONAGE PAID($ in millions)

2009 2010 2011 2012 2013

26.0

36.0

53.3 55.258.1

Karen SchottBoard Chair

Bar Four RanchBroadview, Montana

The Schott family raises winter wheat, spring wheat, peas and also managesa lease pasture operation.

Investments in youth education, industry associations, sponsorships and our Rural Community Grant Program are making a profound difference in the communities where we live and work.

We would like to extend our gratitude to Bruce Nelson and Drew Eggers as they retire from the board of directors after 15 and 13 years respectively. Their leadership, expe-rience and considerable expertise in many areas has been invaluable in overseeing Northwest FCS’ strategy and performance. We wish Bruce, Drew and their families the very best and we look forward to welcoming two new directors in March.

On behalf of the Northwest FCS Board, we appreciate the confidence our customer-owners have placed in this association. We also want to recognize our 180 Local Advi-sory Committee members, 640 employees and our senior leadership team for a job well done.

2013 was another successful year for the association. We posted record net income that provided strong growth in capital, allowing Northwest FCS to strengthen its financial capacity to serve our customers. The association also paid $58.1 million in cash patronage to our customer-owners across the Northwest.

Those of us in agriculture have experienced a strong run the past several years during a time when many areas of the economy have struggled. But, we all know good times never last forever. The board and management team are carefully monitoring trends and economic indicators to ensure we are well po-sitioned and continue to build organizational capacity to support Northwest agriculture for generations to come.

To complement the business side of our mission, Northwest FCS continues to put the company’s talent and resources back into our rural communities. We believe strong communities foster strong businesses.

On Behalf of the Board

2

Pictured left to right:

Dave Nisbet Bay Center, Washington

Drew Eggers Meridian, Idaho

John Helle Dillon, Montana

Shawn Walters New Dale, Idaho

2013 Board of Directors

Kevin Riel Yakima, Washington

Julie Shiflett Spokane, Washington

Mark Gehring Salem, Oregon

Jim Farmer Nyssa, Oregon

Rick Barnes Callahan, California

Herb Karst Sunburst, Montana

Christy Burmeister-Smith Newman Lake, Washington

Bruce Nelson Spokane, Washington

Karen Schott Chair - Broadview, Montana

Dave Hedlin Vice Chair - Mt. Vernon, Washington

Insights from the CEOadvisors. By “trusted advisors” we mean knowledgeable staff who take time to understand our customers’ businesses and get to know their families and other key players in their operation and industry. Customers tell us their trusted advisors are a valued resource to help them grow and transition their businesses to the next generation.

Securing affordable financing is one of the biggest challenges faced by the next generation in agriculture, forestry and fisheries. Helping these

young and beginning producers start and grow their own businesses is an integral part of our cooperative mission. During 2013, the number of customers financed by our AgVision program increased signifi-cantly. We’ve added additional staff to work with and mentor these producers to make sound management decisions, thereby strengthening the foundation for the future of our industry.

Our Business Management Center programs help the next generation to improve and refine their financial and management skills.

In 2013 we launched our new RateWise program that rewards young and beginning producers for continuing their management education with interest rate reductions on new loans. We call it, “Learn and earn.”

Human Resource CapacityThe strength of our business has always been defined by the quality of our people and our performance-driven culture. We know the quality of our people differentiates this organization and will serve as the cornerstone of our success. For us to be successful, our employees must reflect the diversity of the communities and cultures in which we operate. That means we must attract, retain and motivate people from many backgrounds and perspectives. Over the past three years we have increased our staffing levels, and on average, we’ve hired 27 trainees per

year to ensure we continually bring new talent into the organization, build bench strength for the future and address ongoing succession needs. Investments in these trainees are substantial and include individual mentoring from our more experienced employees.

During 2013 we partnered with the Gallup research company to help us better understand and improve our level of employee engagement. Gallup defines engagement as an employees' involvement with, commitment to and satisfaction with work. Our initial results were very strong and we will continue to build on our strengths going forward.

I’m continually inspired by stories from employees who are reaching out to support worthy causes in their com-munities. They donate their time, talents and financial resources to care for our military veterans, secure food for local food banks or race to find a cure for cancer, just to name a few. To support their generosity we’re now providing three days of paid time off each year to continue this heart-felt work.

Operations Capacity2013 was a very productive year for operations and technology improvements. To top the list of accomplish-ments, we successfully converted our loan accounting system from one that was outdated to a new, more powerful system that is used by several Farm Credit associations. We save significant dollars by partnering with others. With the loan accounting conversion behind us, we’re now turning our attention to enhance customer and staff-related technologies in 2014.

We must make it easier for customers to do business with us electronically. Over the next two years we will develop customized web access to allow each customer to indi-vidualize their Northwest FCS access and banking information. We will also enhance the suite of online banking tools we offer.

Financial CapacityIncreasing our financial capacity means we build an organization that can handle future customer needs, make investments back into the business and pay an appropriate return

in the form of patronage to our customer-owners. Plus, the organization must have the financial capacity to withstand increasing volatility.

Improving the association’s credit quality has been a major focus area the past several years following the economic downturn in 2008-2009 when several industries faced historically hard times. We’ve worked closely with many of these customers as they’ve executed recovery plans to reposition their operations. We believe this even-handed and measured approach has reinforced our value proposition and deepened our long-term customer

relationships. In 2013 we significantly improved credit quality. Financial resources previously used to fund allowances for credit losses can now be used for more productive investments. Our capital grew to $1.8 billion, up 12.2 percent from $1.6 billion in 2012. A strong capital base provides for future loan growth and helps us withstand unforeseen future downturns.

Looking ForwardLooking forward, our greatest challenge and opportu-nity will be increasing our human resource capacity. We know strong teams with great people outperform individuals. As our customers successfully transition their businesses to the next generation, we are also

developing our employees with an eye to the future. Promising young people are being mentored by our wise, experienced leaders. New technologies are being implemented to help our employees build fresh, new skills to better serve our customers. We will continue to build a purpose-driven culture – the foundation for any successful business – that inspires our people to grow and reach their full potential as we position to serve agriculture for generations to come.

2009 2010 2011 2012 2013

1.21.3

1.4

1.6

1.8

C APITAL($ in billions) 236.9

2009 2010 2011 2012 2013

106.1

150.1 159.2

187.3

NET INCOMEAFTER TAXES($ in millions)

As a cooperative, our goal is to provide value to you as a customer and an owner. As our customer, we strive to provide products at prices that are competitive, earning your trust through our knowledge of your business, the dedication and quality of our staff, and even-handedness through the inevitable cycles in agriculture. As an owner, we aim to provide you a meaningful return of value in the form of patronage dividends. In 2013 we returned $58.1 million in patronage to our customer-owners.

Your cooperative earned a record $236.9 million in 2013, up 26.5 percent from $187.3 million in 2012. A combination of factors contributed to our financial results, with credit quality improvement being the single largest factor. Producers continued to experience strong prices for most commodities, resulting in strong levels of net income. This year we saw many customers pay down or pay off debt, which limited our growth to a degree. We’ve been pleased to see our customers’ financial capacity continue to strengthen in these high income years for agriculture.

Building CapacityStrategy is about making choices, building competitive advantage and planning for the future. Strategy is not set through one initiative or one big deal. Rather, we build it by making sound decisions and enhancing capacity. We continued to build our organizational capacity during 2013 by concentrating on four key areas in our business plan – our customers, our people, operations, and our financial strength. In each of these vital areas, we made significant gains to build a business that will sustain itself during the inevitable cycles we’ll face in the future.

Customer CapacityThis year we placed a greater emphasis on developing our staff as trusted

3 4

“Customers tell us their trusted

advisors are a valued resource

to help them grow and

transition their business to

the next generation.”

Phil DiPofiPresident and CEO

NorthwestFarm Credit ServicesSpokane, Washington

Northwest FCS isthe leading financial cooperative in the Northwest with 45 branches and 640 employees in Idaho, Montana, Oregon, Washington and Alaska.

Insights from the CEOadvisors. By “trusted advisors” we mean knowledgeable staff who take time to understand our customers’ businesses and get to know their families and other key players in their operation and industry. Customers tell us their trusted advisors are a valued resource to help them grow and transition their businesses to the next generation.

Securing affordable financing is one of the biggest challenges faced by the next generation in agriculture, forestry and fisheries. Helping these

young and beginning producers start and grow their own businesses is an integral part of our cooperative mission. During 2013, the number of customers financed by our AgVision program increased signifi-cantly. We’ve added additional staff to work with and mentor these producers to make sound management decisions, thereby strengthening the foundation for the future of our industry.

Our Business Management Center programs help the next generation to improve and refine their financial and management skills.

In 2013 we launched our new RateWise program that rewards young and beginning producers for continuing their management education with interest rate reductions on new loans. We call it, “Learn and earn.”

Human Resource CapacityThe strength of our business has always been defined by the quality of our people and our performance-driven culture. We know the quality of our people differentiates this organization and will serve as the cornerstone of our success. For us to be successful, our employees must reflect the diversity of the communities and cultures in which we operate. That means we must attract, retain and motivate people from many backgrounds and perspectives. Over the past three years we have increased our staffing levels, and on average, we’ve hired 27 trainees per

year to ensure we continually bring new talent into the organization, build bench strength for the future and address ongoing succession needs. Investments in these trainees are substantial and include individual mentoring from our more experienced employees.

During 2013 we partnered with the Gallup research company to help us better understand and improve our level of employee engagement. Gallup defines engagement as an employees' involvement with, commitment to and satisfaction with work. Our initial results were very strong and we will continue to build on our strengths going forward.

I’m continually inspired by stories from employees who are reaching out to support worthy causes in their com-munities. They donate their time, talents and financial resources to care for our military veterans, secure food for local food banks or race to find a cure for cancer, just to name a few. To support their generosity we’re now providing three days of paid time off each year to continue this heart-felt work.

Operations Capacity2013 was a very productive year for operations and technology improvements. To top the list of accomplish-ments, we successfully converted our loan accounting system from one that was outdated to a new, more powerful system that is used by several Farm Credit associations. We save significant dollars by partnering with others. With the loan accounting conversion behind us, we’re now turning our attention to enhance customer and staff-related technologies in 2014.

We must make it easier for customers to do business with us electronically. Over the next two years we will develop customized web access to allow each customer to indi-vidualize their Northwest FCS access and banking information. We will also enhance the suite of online banking tools we offer.

Financial CapacityIncreasing our financial capacity means we build an organization that can handle future customer needs, make investments back into the business and pay an appropriate return

in the form of patronage to our customer-owners. Plus, the organization must have the financial capacity to withstand increasing volatility.

Improving the association’s credit quality has been a major focus area the past several years following the economic downturn in 2008-2009 when several industries faced historically hard times. We’ve worked closely with many of these customers as they’ve executed recovery plans to reposition their operations. We believe this even-handed and measured approach has reinforced our value proposition and deepened our long-term customer

relationships. In 2013 we significantly improved credit quality. Financial resources previously used to fund allowances for credit losses can now be used for more productive investments. Our capital grew to $1.8 billion, up 12.2 percent from $1.6 billion in 2012. A strong capital base provides for future loan growth and helps us withstand unforeseen future downturns.

Looking ForwardLooking forward, our greatest challenge and opportu-nity will be increasing our human resource capacity. We know strong teams with great people outperform individuals. As our customers successfully transition their businesses to the next generation, we are also

developing our employees with an eye to the future. Promising young people are being mentored by our wise, experienced leaders. New technologies are being implemented to help our employees build fresh, new skills to better serve our customers. We will continue to build a purpose-driven culture – the foundation for any successful business – that inspires our people to grow and reach their full potential as we position to serve agriculture for generations to come.

2009 2010 2011 2012 2013

1.21.3

1.4

1.6

1.8

C APITAL($ in billions) 236.9

2009 2010 2011 2012 2013

106.1

150.1 159.2

187.3

NET INCOMEAFTER TAXES($ in millions)

As a cooperative, our goal is to provide value to you as a customer and an owner. As our customer, we strive to provide products at prices that are competitive, earning your trust through our knowledge of your business, the dedication and quality of our staff, and even-handedness through the inevitable cycles in agriculture. As an owner, we aim to provide you a meaningful return of value in the form of patronage dividends. In 2013 we returned $58.1 million in patronage to our customer-owners.

Your cooperative earned a record $236.9 million in 2013, up 26.5 percent from $187.3 million in 2012. A combination of factors contributed to our financial results, with credit quality improvement being the single largest factor. Producers continued to experience strong prices for most commodities, resulting in strong levels of net income. This year we saw many customers pay down or pay off debt, which limited our growth to a degree. We’ve been pleased to see our customers’ financial capacity continue to strengthen in these high income years for agriculture.

Building CapacityStrategy is about making choices, building competitive advantage and planning for the future. Strategy is not set through one initiative or one big deal. Rather, we build it by making sound decisions and enhancing capacity. We continued to build our organizational capacity during 2013 by concentrating on four key areas in our business plan – our customers, our people, operations, and our financial strength. In each of these vital areas, we made significant gains to build a business that will sustain itself during the inevitable cycles we’ll face in the future.

Customer CapacityThis year we placed a greater emphasis on developing our staff as trusted

3 4

“Customers tell us their trusted

advisors are a valued resource

to help them grow and

transition their business to

the next generation.”

Phil DiPofiPresident and CEO

NorthwestFarm Credit ServicesSpokane, Washington

Northwest FCS isthe leading financial cooperative in the Northwest with 45 branches and 640 employees in Idaho, Montana, Oregon, Washington and Alaska.

6

Today, about 60 percent of farmers in this country are 55 years or older. For every one farmer and rancher under the age of 25, five

others are 75 or older. Getting young people involved in agriculture is critical to meeting the growing demand for food.

Fortunately, agriculture has been a bright spot in an otherwise weak economy and more young people are showing an interest.

Yet, it’s never easy to transition to the next generation, particularly for family-owned, capital intensive businesses. Young people

with passion need to be prepared to manage and lead. Economically, the business model has to perpetuate long-term growth.

If Northwest FCS customers are an indication of the future, agriculture is in good hands.

Experts predict a growing world population that will require 70 percentmore food production by 2050 – just 36 years away.

Generational Transitions – Building for the Future

6

Today, about 60 percent of farmers in this country are 55 years or older. For every one farmer and rancher under the age of 25, five

others are 75 or older. Getting young people involved in agriculture is critical to meeting the growing demand for food.

Fortunately, agriculture has been a bright spot in an otherwise weak economy and more young people are showing an interest.

Yet, it’s never easy to transition to the next generation, particularly for family-owned, capital intensive businesses. Young people

with passion need to be prepared to manage and lead. Economically, the business model has to perpetuate long-term growth.

If Northwest FCS customers are an indication of the future, agriculture is in good hands.

Experts predict a growing world population that will require 70 percentmore food production by 2050 – just 36 years away.

Generational Transitions – Building for the Future

Creating an On-Ramp into the Businessour foreman. These guys are natural leaders with respect from their peers. Now they look for solutions together before they call me. Our goal is to develop a team with the field expertise to support Adam and Hannah going forward.

Today Adam is leading our weekly manager meetings, keeping track of assignments and holding people accountable. Hannah handles payroll, food safety and accounting. I can still use my

horticulture experience to help during the spring but they really won’t need me at harvest. Ultimately my goal is to become nonessential and contribute more than I cost.

What would I tell others about succes-sion planning? Prepare, take your time and think it through. I envisioned the transition as being a tranquil period where everything would stay the same. But no, things get more complex. The company we’re transitioning today isn’t the same company we started transitioning two years ago. The business doesn’t stand still. We don’t always have clearly defined roles and

boundaries for people to operate within. But, I think we’re dynamic and adapting as we go.

Hannah and Adam have youth, energy and passion on their side. Adam learns better by doing versus being told what to do. He reminds me a lot of myself years ago. He’s confident and willing to try new things. That’s how Sharon and I started out. Now we’re working together to build a company that will thrive without us.

“Succession won’t happen

unless I make it happen. The

next generation can just be

workers or we can begin to

think like business owners.”

– Adam Poush

Top middle: Chuck and Northwest FCS Relationship Manager Alan Kirpes

Left: Sharon, Chuck and Alan Kirpes

Far right: Hannah and Adam Poush

Middle: Chuck and Sharon

Bottom middle: Adam, Hannah, Sharon and Chuck

Chuck PodlichOwner

Cider Works FarmsOrondo, Washington

Manages a 300-acre orchard with cider production facility, country market and fruit stand.

My wife Sharon and I are �rst generation fruit growers. We moved to Washington 35 years ago from the East Coast where I studied horticulture. People said if you want to get into the orchard business you either marry it or inherit it. But, we’re both a little headstrong. We found another way in by starting with nothing and adding a little bit here and there. We could make mistakes without a lot to lose back then. It’s much di�erent today with the size and scope of our business.

Sharon and I always thought we’d sell the business when we were tired of it. We didn’t think any of our four daughters would want to come back. But, in 2009 we started working on a succession plan when Hannah, 27, and her husband Adam, 29, wanted to leave their Portland-based careers for an on-ramp into the business. It didn’t take long to feel honored that we created a business someone wants to continue.

Adam grew up in Portland. He didn’t know anything about trees when he came here in 2012. I’m a horticulturist, so I don’t think it’s fair to expect Adam to be my direct replacement. But he’s a good business man. The �rst year Adam learned everything he could about our cider press and retail business. He’s managing those employees on a year-round basis now. Sometimes I think it’s a little tough for Sharon to let go of the retail business she built and I feel the same way on the orchard side.

In the �eld we’ve added a mid-level management team to work with

7

“I frequently bounce ideas offour Northwest FCS relationship

manager when it comes toexpansion. As a trusted advisor

Alan offers a valuable perspective that keeps me grounded in reality,

yet honors my dreams.”– Chuck Podlich

Creating an On-Ramp into the Businessour foreman. These guys are natural leaders with respect from their peers. Now they look for solutions together before they call me. Our goal is to develop a team with the field expertise to support Adam and Hannah going forward.

Today Adam is leading our weekly manager meetings, keeping track of assignments and holding people accountable. Hannah handles payroll, food safety and accounting. I can still use my

horticulture experience to help during the spring but they really won’t need me at harvest. Ultimately my goal is to become nonessential and contribute more than I cost.

What would I tell others about succes-sion planning? Prepare, take your time and think it through. I envisioned the transition as being a tranquil period where everything would stay the same. But no, things get more complex. The company we’re transitioning today isn’t the same company we started transitioning two years ago. The business doesn’t stand still. We don’t always have clearly defined roles and

boundaries for people to operate within. But, I think we’re dynamic and adapting as we go.

Hannah and Adam have youth, energy and passion on their side. Adam learns better by doing versus being told what to do. He reminds me a lot of myself years ago. He’s confident and willing to try new things. That’s how Sharon and I started out. Now we’re working together to build a company that will thrive without us.

“Succession won’t happen

unless I make it happen. The

next generation can just be

workers or we can begin to

think like business owners.”

– Adam Poush

Top middle: Chuck and Northwest FCS Relationship Manager Alan Kirpes

Left: Sharon, Chuck and Alan Kirpes

Far right: Hannah and Adam Poush

Middle: Chuck and Sharon

Bottom middle: Adam, Hannah, Sharon and Chuck

Chuck PodlichOwner

Cider Works FarmsOrondo, Washington

Manages a 300-acre orchard with cider production facility, country market and fruit stand.

My wife Sharon and I are �rst generation fruit growers. We moved to Washington 35 years ago from the East Coast where I studied horticulture. People said if you want to get into the orchard business you either marry it or inherit it. But, we’re both a little headstrong. We found another way in by starting with nothing and adding a little bit here and there. We could make mistakes without a lot to lose back then. It’s much di�erent today with the size and scope of our business.

Sharon and I always thought we’d sell the business when we were tired of it. We didn’t think any of our four daughters would want to come back. But, in 2009 we started working on a succession plan when Hannah, 27, and her husband Adam, 29, wanted to leave their Portland-based careers for an on-ramp into the business. It didn’t take long to feel honored that we created a business someone wants to continue.

Adam grew up in Portland. He didn’t know anything about trees when he came here in 2012. I’m a horticulturist, so I don’t think it’s fair to expect Adam to be my direct replacement. But he’s a good business man. The �rst year Adam learned everything he could about our cider press and retail business. He’s managing those employees on a year-round basis now. Sometimes I think it’s a little tough for Sharon to let go of the retail business she built and I feel the same way on the orchard side.

In the �eld we’ve added a mid-level management team to work with

7

“I frequently bounce ideas offour Northwest FCS relationship

manager when it comes toexpansion. As a trusted advisor

Alan offers a valuable perspective that keeps me grounded in reality,

yet honors my dreams.”– Chuck Podlich

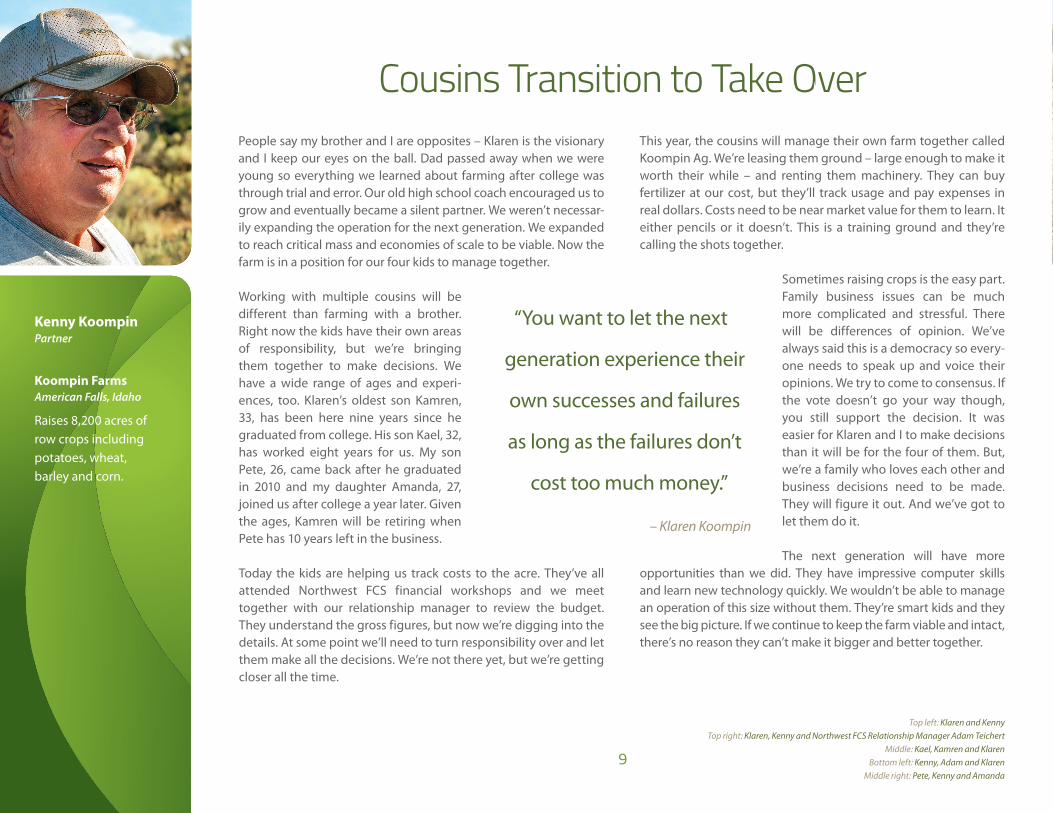

Cousins Transition to Take OverThis year, the cousins will manage their own farm together called Koompin Ag. We’re leasing them ground – large enough to make it worth their while – and renting them machinery. They can buy fertilizer at our cost, but they’ll track usage and pay expenses in real dollars. Costs need to be near market value for them to learn. It either pencils or it doesn’t. This is a training ground and they’re calling the shots together.

Sometimes raising crops is the easy part. Family business issues can be much more complicated and stressful. There will be differences of opinion. We’ve always said this is a democracy so every-one needs to speak up and voice their opinions. We try to come to consensus. If the vote doesn’t go your way though, you still support the decision. It was easier for Klaren and I to make decisions than it will be for the four of them. But, we’re a family who loves each other and business decisions need to be made. They will figure it out. And we’ve got to let them do it.

The next generation will have more opportunities than we did. They have impressive computer skills and learn new technology quickly. We wouldn’t be able to manage an operation of this size without them. They’re smart kids and they see the big picture. If we continue to keep the farm viable and intact, there’s no reason they can’t make it bigger and better together.

“You want to let the next

generation experience their

own successes and failures

as long as the failures don’t

cost too much money.”

– Klaren Koompin

Top left: Klaren and Kenny

Top right: Klaren, Kenny and Northwest FCS Relationship Manager Adam Teichert

Middle: Kael, Kamren and Klaren

Bottom left: Kenny, Adam and Klaren

Middle right: Pete, Kenny and Amanda

Kenny KoompinPartner

Koompin FarmsAmerican Falls, Idaho

Raises 8,200 acres of row crops including potatoes, wheat, barley and corn.

People say my brother and I are opposites – Klaren is the visionary and I keep our eyes on the ball. Dad passed away when we were young so everything we learned about farming after college was through trial and error. Our old high school coach encouraged us to grow and eventually became a silent partner. We weren’t necessar-ily expanding the operation for the next generation. We expanded to reach critical mass and economies of scale to be viable. Now the farm is in a position for our four kids to manage together.

Working with multiple cousins will be different than farming with a brother. Right now the kids have their own areas of responsibility, but we’re bringing them together to make decisions. We have a wide range of ages and experi-ences, too. Klaren’s oldest son Kamren, 33, has been here nine years since he graduated from college. His son Kael, 32, has worked eight years for us. My son Pete, 26, came back after he graduated in 2010 and my daughter Amanda, 27, joined us after college a year later. Given the ages, Kamren will be retiring when Pete has 10 years left in the business.

Today the kids are helping us track costs to the acre. They’ve all attended Northwest FCS financial workshops and we meet together with our relationship manager to review the budget. They understand the gross figures, but now we’re digging into the details. At some point we’ll need to turn responsibility over and let them make all the decisions. We’re not there yet, but we’re getting closer all the time.

“To be a viable business long term, you need a

competitive lender who shares your vision.”

– Klaren Koompin

9

Cousins Transition to Take OverThis year, the cousins will manage their own farm together called Koompin Ag. We’re leasing them ground – large enough to make it worth their while – and renting them machinery. They can buy fertilizer at our cost, but they’ll track usage and pay expenses in real dollars. Costs need to be near market value for them to learn. It either pencils or it doesn’t. This is a training ground and they’re calling the shots together.

Sometimes raising crops is the easy part. Family business issues can be much more complicated and stressful. There will be differences of opinion. We’ve always said this is a democracy so every-one needs to speak up and voice their opinions. We try to come to consensus. If the vote doesn’t go your way though, you still support the decision. It was easier for Klaren and I to make decisions than it will be for the four of them. But, we’re a family who loves each other and business decisions need to be made. They will figure it out. And we’ve got to let them do it.

The next generation will have more opportunities than we did. They have impressive computer skills and learn new technology quickly. We wouldn’t be able to manage an operation of this size without them. They’re smart kids and they see the big picture. If we continue to keep the farm viable and intact, there’s no reason they can’t make it bigger and better together.

“You want to let the next

generation experience their

own successes and failures

as long as the failures don’t

cost too much money.”

– Klaren Koompin

Top left: Klaren and Kenny

Top right: Klaren, Kenny and Northwest FCS Relationship Manager Adam Teichert

Middle: Kael, Kamren and Klaren

Bottom left: Kenny, Adam and Klaren

Middle right: Pete, Kenny and Amanda

Kenny KoompinPartner

Koompin FarmsAmerican Falls, Idaho

Raises 8,200 acres of row crops including potatoes, wheat, barley and corn.

People say my brother and I are opposites – Klaren is the visionary and I keep our eyes on the ball. Dad passed away when we were young so everything we learned about farming after college was through trial and error. Our old high school coach encouraged us to grow and eventually became a silent partner. We weren’t necessar-ily expanding the operation for the next generation. We expanded to reach critical mass and economies of scale to be viable. Now the farm is in a position for our four kids to manage together.

Working with multiple cousins will be different than farming with a brother. Right now the kids have their own areas of responsibility, but we’re bringing them together to make decisions. We have a wide range of ages and experi-ences, too. Klaren’s oldest son Kamren, 33, has been here nine years since he graduated from college. His son Kael, 32, has worked eight years for us. My son Pete, 26, came back after he graduated in 2010 and my daughter Amanda, 27, joined us after college a year later. Given the ages, Kamren will be retiring when Pete has 10 years left in the business.

Today the kids are helping us track costs to the acre. They’ve all attended Northwest FCS financial workshops and we meet together with our relationship manager to review the budget. They understand the gross figures, but now we’re digging into the details. At some point we’ll need to turn responsibility over and let them make all the decisions. We’re not there yet, but we’re getting closer all the time.

“To be a viable business long term, you need a

competitive lender who shares your vision.”

– Klaren Koompin

9

Carrying the Legacy Forwardsister Sue Loband played an absolutely vital role as his personal representative, getting the business and related assets transitioned to Curt’s children while giving them space to grow into their roles. Outside professionals Curt worked with and trusted helped us navigate complicated tax and legal issues.

Initially, Matt, Angie and Mandi found themselves in roles that weren’t clearly defined or always comfortable. We started working

with a facilitator from Northwest FCS six months after Curt passed away and the planning process was a significant help to us. The family came together to create a unified vision for the business. We talked about strengths, weaknesses, their roles and where the family wanted to take the business going forward. The siblings are very loyal to each other, but there are honest differences of opinion too. We needed an outside facilitator to help them learn to communicate as partners, to ask tough questions and hold us all accountable to answer them.

I’m grateful for how much this family wanted to communicate and work together. Matt has really grown into his leadership role as general manager. He has a plan and is encouraging others while holding them accountable. Angie is a tremendous asset on the HR side, sharing her passion for people and relationships. Together they’ve earned the loyalty and respect of everyone who works here. Mandi isn’t involved in the day-to-day operations, but she has an important voice at the ownership table. These were the well-laid plans Curt Maberry made. He would be so pleased to see how his kids have grown as they care for the legacy he built.

“A strategic plan is only

as good as the paper it’s

written on unless someone

puts it into action.”

– Matt Maberry

Curt Maberry started working on a transition plan in 2005. He was 58 with two kids on the farm, Matt, 25 and Angie, 28. Oldest daughter Mandi, 30, was close to home pursuing her art career. Curt was expanding the crop side of the business and increasing production in the processing plant. His vision was to create a sustainable operation. None of us ever imagined he would pass away so suddenly just two years later.

Today Curt’s legacy lives on, reflected in the business he built, the relationships he made and the family he treasured. Curt loved sports, which influenced his management style. He always had an organized plan. He coached his employees, particularly his kids, to plan ahead and ex-ecute. Instead of telling people what to do he always asked them what the priorities were. He wanted everyone to think for themselves before he gave direction. His coaching management style made the transition easier when everyone stepped up quickly to contribute to the team.

Growing up, Matt, Angie and Mandi shared rich experiences working on and around the farm. Curt was intentional about putting them in different positions to learn the business. Matt and Angie were involved in the numbers early on, putting budgets together for the departments they worked in. Curt insisted on having regular business meetings to help them understand the financial cycles our industry goes through.

One of the most important things Curt did in estate planning was selecting the right people to put in places of responsibility. Curt’s

11

Top left: Northwest FCS Credit Officer Corrine Reynolds and Tom

Top right: Matt, Angie and Mandi

Middle: Matt, Angie, Mandi and Tom

Bottom left: Angie and Mandi

Bottom right: Angie and Matt

Tom VanBerkumBusiness Manager

Tom joined Curt Maberry Farm in 2005 after working for their public accounting firm.

Curt Maberry FarmLynden, Washington

Grows and processes nearly 1,000 acres of strawberries, red raspberries and blueberries.

“Northwest FCS provides

resources beyond just funding

loans. The business planning

services are truly valued

and appreciated.”

– Angie Maberry

Carrying the Legacy Forwardsister Sue Loband played an absolutely vital role as his personal representative, getting the business and related assets transitioned to Curt’s children while giving them space to grow into their roles. Outside professionals Curt worked with and trusted helped us navigate complicated tax and legal issues.

Initially, Matt, Angie and Mandi found themselves in roles that weren’t clearly defined or always comfortable. We started working

with a facilitator from Northwest FCS six months after Curt passed away and the planning process was a significant help to us. The family came together to create a unified vision for the business. We talked about strengths, weaknesses, their roles and where the family wanted to take the business going forward. The siblings are very loyal to each other, but there are honest differences of opinion too. We needed an outside facilitator to help them learn to communicate as partners, to ask tough questions and hold us all accountable to answer them.

I’m grateful for how much this family wanted to communicate and work together. Matt has really grown into his leadership role as general manager. He has a plan and is encouraging others while holding them accountable. Angie is a tremendous asset on the HR side, sharing her passion for people and relationships. Together they’ve earned the loyalty and respect of everyone who works here. Mandi isn’t involved in the day-to-day operations, but she has an important voice at the ownership table. These were the well-laid plans Curt Maberry made. He would be so pleased to see how his kids have grown as they care for the legacy he built.

“A strategic plan is only

as good as the paper it’s

written on unless someone

puts it into action.”

– Matt Maberry

Curt Maberry started working on a transition plan in 2005. He was 58 with two kids on the farm, Matt, 25 and Angie, 28. Oldest daughter Mandi, 30, was close to home pursuing her art career. Curt was expanding the crop side of the business and increasing production in the processing plant. His vision was to create a sustainable operation. None of us ever imagined he would pass away so suddenly just two years later.

Today Curt’s legacy lives on, reflected in the business he built, the relationships he made and the family he treasured. Curt loved sports, which influenced his management style. He always had an organized plan. He coached his employees, particularly his kids, to plan ahead and ex-ecute. Instead of telling people what to do he always asked them what the priorities were. He wanted everyone to think for themselves before he gave direction. His coaching management style made the transition easier when everyone stepped up quickly to contribute to the team.

Growing up, Matt, Angie and Mandi shared rich experiences working on and around the farm. Curt was intentional about putting them in different positions to learn the business. Matt and Angie were involved in the numbers early on, putting budgets together for the departments they worked in. Curt insisted on having regular business meetings to help them understand the financial cycles our industry goes through.

One of the most important things Curt did in estate planning was selecting the right people to put in places of responsibility. Curt’s

11

Top left: Northwest FCS Credit Officer Corrine Reynolds and Tom

Top right: Matt, Angie and Mandi

Middle: Matt, Angie, Mandi and Tom

Bottom left: Angie and Mandi

Bottom right: Angie and Matt

Tom VanBerkumBusiness Manager

Tom joined Curt Maberry Farm in 2005 after working for their public accounting firm.

Curt Maberry FarmLynden, Washington

Grows and processes nearly 1,000 acres of strawberries, red raspberries and blueberries.

“Northwest FCS provides

resources beyond just funding

loans. The business planning

services are truly valued

and appreciated.”

– Angie Maberry

Our Brand PromiseNorthwest Farm Credit Services is your

trusted source for financial solutions.

No other lender understands the agriculture,

food and fiber industries better and is more

committed to their future and that of

rural America.

2013 NORTHWEST FARM CREDIT SERVICES, ACA Annual Report to Stockholders

1

N O R T H W E S T F A R M C R E D I T S E R V I C E S , A C A

REPORT OF MANAGEMENT The financial statements of Northwest Farm Credit Services, ACA and its wholly owned subsidiaries

(Northwest FCS) are prepared by management, who is responsible for their integrity and

objectivity, including amounts necessarily based on judgments and estimates. The financial

statements have been prepared in conformity with accounting principles generally accepted in the

United States of America, and, in the opinion of management, fairly present the financial condition

of Northwest FCS. Other financial information included in the 2013 Annual Report to Stockholders

is consistent with that in the financial statements.

To meet its responsibility for reliable financial information, management depends on Northwest

FCS’ accounting and internal control systems, which have been designed to provide reasonable,

but not absolute, assurances that assets are safeguarded and transactions are properly authorized

and recorded. The systems have been designed to recognize the cost must be related to the

benefits derived. To monitor compliance, the Internal Audit staff performs audits of the accounting

records, reviews accounting systems and internal controls, and recommends improvements as

appropriate. The financial statements are audited by PricewaterhouseCoopers LLP, independent

auditors, who, as part of the audit process, also conduct an audit of internal controls to obtain a

sufficient understanding of the internal control structure in order to establish a basis for reliance

thereon in determining the nature, extent, and timing of procedures applied to the audit of the

financial statements. Northwest FCS is also examined by the Farm Credit Administration.

The Chief Executive Officer, as delegated by the Northwest FCS Board of Directors, has overall

responsibility for Northwest FCS’ system of internal controls and financial reporting. The Board has

delegated significant responsibility to the Audit Committee, which is comprised entirely of directors

who are independent of Northwest FCS’ management. The Audit Committee meets periodically

with management, the independent auditors, and the internal auditors to ensure they are carrying

out their responsibilities. The Audit Committee is also responsible for performing an oversight role

by reviewing and monitoring the financial, accounting, and auditing procedures of Northwest FCS

in addition to reviewing Northwest FCS’ financial reports. The independent auditors and the

internal auditors have full and free access to the Audit Committee, with or without the presence of

management, to discuss the adequacy of the internal control structure for financial reporting and

any other matters they believe should be brought to the attention of the committee.

The undersigned certify that they have reviewed the 2013 Annual Report to Stockholders and it

has been prepared in accordance with all applicable statutory or regulatory requirements and the

information contained herein is true, accurate, and complete to the best of our knowledge and

belief.

Phil DiPofi

President and CEO

February 28, 2014

Tom Nakano

EVP-Chief Administrative and

Financial Officer

February 28, 2014

Karen Schott

Chair of the Board

February 28, 2014

2

N O R T H W E S T F A R M C R E D I T S E R V I C E S , A C A

MANAGEMENT’S ANNUAL REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING Management of Northwest FCS is responsible for establishing and maintaining adequate internal

control over financial reporting for Northwest FCS’ consolidated financial statements. For purposes

of this report “internal control over financial reporting” is defined as a process designed by or

under the supervision of Northwest FCS’ principal executives and principal financial officers, or

persons performing similar functions, and effected by its board of directors, management and

other personnel, to provide reasonable assurance regarding the reliability of financial reporting

information and the preparation of the consolidated financial statements for external purposes in

accordance with accounting principles generally accepted in the United States of America and

includes those policies and procedures that: (1) pertain to the maintenance of records that in

reasonable detail accurately and fairly reflect the transactions and dispositions of the assets of

Northwest FCS, (2) provide reasonable assurance that transactions are recorded as necessary to

permit preparation of financial information, and that receipts and expenditures are being made

only in accordance with authorizations of management and directors of Northwest FCS, and (3)

provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition,

use or disposition of Northwest FCS’ assets that could have a material effect on its consolidated

financial statements.

Northwest FCS’ management has completed an assessment of the effectiveness of internal control

over financial reporting as of December 31, 2013. In making the assessment, management used

the framework in Internal Control—Integrated Framework, promulgated by the Committee of

Sponsoring Organizations of the Treadway Commission, commonly referred to as the “COSO”

criteria.

Based on the assessment performed, Northwest FCS concluded that as of December 31, 2013, the

internal control over financial reporting was effective. Additionally, based on this assessment,

Northwest FCS determined there were no material weaknesses in the internal control over financial

reporting as of December 31, 2013. There were no material changes in the internal control over

financial reporting during the year ended December 31, 2013.

Northwest FCS’ independent auditors, PricewaterhouseCoopers LLP, who audit Northwest FCS’

consolidated financial statements, have issued a report on the effectiveness of internal control over

financial reporting. See Report of Independent Auditors.

Phil DiPofi

President and CEO

February 28, 2014

Tom Nakano

EVP-Chief Administrative and

Financial Officer

February 28, 2014

Karen Schott

Chair of the Board

February 28, 2014

3

N O R T H W E S T F A R M C R E D I T S E R V I C E S , A C A

REPORT OF AUDIT COMMITTEE The Audit Committee is composed of seven members of the Northwest FCS Board of Directors. In

2013, the Audit Committee met five times in person and participated in four conference calls. The

Audit Committee oversees the scope of Northwest FCS’ internal audit program, the independence

of the outside auditors, the adequacy of Northwest FCS’ system of internal controls and procedures

and the adequacy of management’s action with respect to recommendations arising from those

auditing activities. In addition, the Audit Committee approved the appointment of

PricewaterhouseCoopers LLP (PwC) as our independent auditors for 2013. The Audit Committee’s

responsibilities are described more fully in the Internal Controls Policy and the Audit Committee

Operating Statement.

Management is responsible for internal controls and the preparation of the financial statements in

accordance with accounting principles generally accepted in the United States of America. PwC is

responsible for performing an independent audit of the financial statements in accordance with

generally accepted auditing standards in the United States of America and for issuing its report

based on the audit. The Audit Committee’s responsibilities include monitoring and overseeing these

processes.

In this context, the Audit Committee reviewed and discussed the audited financial statements for

the year ended December 31, 2013, with management. The Audit Committee also reviewed with

PwC the matters required to be discussed by Statement on Auditing Standards No. 114, as

amended (Communication with Audit Committees), PwC and the internal auditors directly provided

reports on significant matters to the Audit Committee.

The Audit Committee received the written disclosures and the letter from PwC in accordance with

Independence Standards Board Standard No. 1 (Independence Discussion with Audit Committees)

and discussed with PwC its independence. The Audit Committee requires prior approval of all non-

audit services provided by PwC. In 2013, PwC was engaged for a training related non-audit

service. The Audit Committee has discussed with management and PwC such other matters and

received such assurances from them as the Audit Committee deemed appropriate.

Based on the foregoing review and discussions, and relying thereon, the Audit Committee

recommended the Northwest FCS Board of Directors include the audited financial statements in the

annual report as of and for the year ended December 31, 2013.

Christy Burmeister-Smith

Chair of the Audit Committee

February 28, 2014

Drew Eggers

Jim Farmer

Mark Gehring

Dave Hedlin

John Helle

Shawn Walters

4

N O R T H W E S T F A R M C R E D I T S E R V I C E S , A C A

FIVE-YEAR SUMMARY OF SELECTED FINANCIAL DATA

5

N O R T H W E S T F A R M C R E D I T S E R V I C E S , A C A

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS The following discussion summarizes the financial position and results of operations of Northwest

Farm Credit Services, an Agricultural Credit Association, and its wholly-owned subsidiaries

(collectively referred to as Northwest FCS) for the year ended December 31, 2013. The

commentary should be read in conjunction with the accompanying Consolidated Financial

Statements and Notes. The Consolidated Financial Statements were prepared under the oversight

of the Audit Committee.

Our quarterly and annual reports to shareholders may be obtained free of charge on our website,

www.northwestfcs.com or upon request at Northwest Farm Credit Services, ACA, P.O. Box 2515,

Spokane, Washington 99220-2515 or by telephone at (509) 340-5300 or toll free (800) 743-2125.

Dollar amounts are in thousands unless otherwise stated.

Forward-Looking Statements Certain statements contained in this report that are not historical facts are forward-looking

statements within the meaning of the Private Securities Litigation Reform Act. Our actual results

may differ materially from those included in the forward-looking statements that relate to plans,

projections, expectations, and intentions. Forward-looking statements are typically identified by

words such as “believe,” “expect,” “anticipate,” “intend,” “estimate,” “plan,” “project,” “may,”

“will,” “should,” “would,” “could” or similar expressions. Although we believe the information

expressed or implied in such forward-looking statements is reasonable, no assurance can be given

that such projections and expectations will be realized or the extent to which a particular plan,

projection, or expectation may be realized. These forward-looking statements are based on current

knowledge and are subject to various risks and uncertainties, including, but not limited to:

fluctuations in the agricultural, energy, international and leasing industry sectors; weather,

disease, and other adverse climatic or biological conditions that impact agricultural productivity and

income; United States and global economic conditions; sovereign or regulatory actions; the level of

interest rates; changes in assumptions underlying the valuations of financial instruments; changes

in estimates underlying the allowance for credit losses; economic conditions and credit

performance of the loan portfolio, growth and seasonal factors; tax reform; the effect of banking

and financial services reforms; possible amendments to, and interpretations of, risk-based capital

guidelines and reporting instructions; the ability of states to adopt more extensive consumer

privacy protections through legislation or regulation; the resolution of legal proceedings and

related matters; and nonperformance by counterparties to derivative positions.

Business Overview

Farm Credit System Structure and Mission

As of January 1, 2014 we are one of 78 associations in the Farm Credit System (System), which

was created by Congress in 1916 and has served agricultural producers for more than 95 years.

The System’s mission is to provide sound and dependable credit to American farmers, ranchers,

and producers or harvesters of aquatic products and farm-related businesses through a member-

owned cooperative system. This is done by making loans and providing financial services. Through

its commitment and dedication to agriculture, the System continues to have the largest portfolio of

agricultural loans of any lender in the United States. The Farm Credit Administration (FCA) is the

System’s independent safety and soundness federal regulator and was established to supervise,

examine and regulate System institutions.

Our Structure and Focus

As a cooperative, we are owned by the members we serve. The territory we serve extends across

a diverse agricultural region consisting primarily of Washington, Idaho, Oregon, Montana and

Alaska. We make long-term real estate mortgage loans to farmers, ranchers, rural residents, and

agribusinesses and production and intermediate-term loans for agricultural production or operating

purposes. Additionally, we provide related services to our customers, such as credit life insurance,

multi-peril crop and crop hail insurance and business management services. Our success begins

with our extensive agricultural experience and knowledge of the market and is dependent on the

level of satisfaction we provide our customers.

As part of the System, we obtain the funding for our lending and operations from CoBank, ACB

(CoBank), which is one of the four Farm Credit System Banks. CoBank is a cooperative of which we

are a member. CoBank, its related associations, and AgVantis Inc. (AgVantis) a technology service

corporation, are referred to as the District. Effective January 1, 2012, U.S. AgBank, FCB merged

with CoBank, FCB, a wholly owned subsidiary of CoBank. The merger did not impact the financial

position or presentation of financial information for Northwest FCS.

6

We, along with the customers’ investment in our association are materially affected by CoBank’s

financial condition and results of operations. The CoBank quarterly and annual reports are

available free of charge by accessing CoBank’s website, www.cobank.com, or may be obtained at

no charge by contacting us. Annual reports are available within 75 days after year end and

quarterly reports are available within 40 days after the calendar quarter end.

2013 Financial Highlights The year ended December 31, 2013 reflected strong financial performance. Record earnings and a

strong capital position allowed us to declare a cash patronage distribution of $58.1 million

representing a return of approximately 75 basis points for the majority of our eligible customers

based on their average 2013 loan balances. Other highlights include:

Net income for the year was $236,889, up 26.5 percent from 2012. The increase in net

income is driven mainly by significantly improved credit quality which resulted in credit loss

reversals of $34,677 as compared to a provision for credit losses recorded in 2012 of

$30,490.

Capital levels remained strong and well in excess of regulatory minimums. As of December

31, 2013, our members’ equity totaled approximately $1.8 billion, and our members’ equity as

a percentage of total assets was 18.3 percent.

Our loan portfolio volume increased modestly in 2013, with an ending gross loan and accrued

interest balance of $9.2 billion. During the same period our nonaccrual loan volume

significantly declined by $83,690, a decrease of 49.2 percent.

Commodity Review and Outlook The following highlights the general health of agricultural commodities with the greatest

concentrations in our loan portfolio.

Dairy: After enduring negative profit margins for much of the year, dairy producers closed 2013

with strong profit margins fueled by rising milk prices, falling corn prices, and historically high U.S.

dairy exports. Milk prices are expected to remain strong in 2014, but could be pressured by

increased competition in global export markets. Milk production in New Zealand and the European

Union is expected to increase. Although lower feed costs are expected to support dairy producers’

profit margins, prices for soybean meal, alfalfa, and other feed ingredients remain high relative to

declines in corn prices.

Forest Products: Volatility in pricing and demand continues in the forest products industry.

Competition between domestic mills and export buyers is driving log prices higher. In areas of the

Northwest, log prices exceed levels associated with the height of the housing boom. In the lumber

and panel markets, mills have experienced periods of strong price increases followed by steep

downward corrections. This volatility complicates management decisions, particularly in an

environment of rising log costs. U.S. fiber consumption is expected to grow in 2014, driven

primarily by increases in housing starts. However, price volatility is expected to continue, fueled by

changes in supply chain inventory levels and mill capacity utilization.

Cattle and Livestock: The principal commodity we finance in this sector is beef cattle. Cattle

markets continue to strengthen. Prices for feeder and fed cattle are at record levels. Falling feed

prices are the most significant variable supporting feeder cattle prices. With improved profit

margins, feedlots are bidding up prices in order to secure inventory. Tight supplies will continue to

support cattle prices for the foreseeable future. Global and domestic beef demand is strong,

further supporting prices. However, continued beef price increases may challenge consumer

demand.

Fruit and Tree Nuts: The principal commodity we finance in this sector is apples. The outlook for

the Northwest apple industry is tempered from last season. For the 2013-2014 crop season, the

second largest crop in Northwest history is matched with a rebound in the North American apple

crop. Increased supplies are weighing on markets. Northwest apples are experiencing high cullage

due to internal condition issues. Affected fruit is not acceptable in the fresh market, which is

impacting returns for both growers and packers. Apple prices, while generally profitable, have

been pressured lower. Prices are expected to firm in the first quarter of 2014 and stay strong

through the marketing season.

Grains: The principal commodity we finance in this sector is wheat. Northwest wheat producers

face a changing marketplace entering 2014. Wheat market fundamentals are bearish, pressured by

rising global stocks and weak cross-market support from corn. Although U.S. wheat production

was down in the 2013-2014 crop season, worldwide wheat stocks rose. Stronger near-term prices

are unlikely without a supply disruption. Lower corn prices are generally pressuring grain prices,

and ample corn supplies are reducing the amount of wheat used as feed. Profitability for wheat

producers will be challenged in 2014 given falling prices. However, strong profits in recent years

have bolstered wheat producers’ ability to bear downside risk.

7

Potatoes: Northwest fresh potato prices have improved considerably from the prior year. Lower

potato production in the United States and the Northwest is supporting the market. Fall frosts

negatively impacted the storability of potatoes in some areas. Where storage issues are not a

concern, producers are delaying open market potato sales, anticipating stronger prices later in the

season. Overall, potato growers are expected to be profitable for their 2013 crop.

For more information on our industries served visit the Northwest FCS Knowledge Center at

www.northwestfcs.com.

Loan Portfolio Total loans and accrued interest outstanding were $9.2 billion at December 31, 2013, an increase

of $162,398, or 1.8 percent from the December 31, 2012 balance of $9.1 billion. During 2012, total

loans and accrued interest increased $525,859 million or 6.2 percent, from $8.5 billion at

December 31, 2011.

In 2013, the modest growth in the portfolio is a result of strong customer liquidity and less

dependence on operating funding. In 2012, our growth came primarily from existing customer

expansion in land and capital improvements.

Loans and accrued interest by type are presented in the following table:

Loan concentrations by state are presented in the following table:

Gross loans, impaired loans and related accrued interest, where appropriate, are presented in the

following table:

Total impaired loans and interest decreased $93,010, or 41.6 percent, during the year ended

December 31, 2013 as compared to December 31, 2012. The majority of this decrease was related

to nonaccrual loans, which decreased $83,690 or 49.2 percent, as compared with December 31,

2012. The following table reflects activity within the nonaccrual loan portfolio:

As of December 31, 2013, nonaccrual loans that were current as to principal and interest

installments totaled $77,785 representing 89.9 percent of the nonaccrual loan portfolio compared

to $125,206 representing 73.5 percent of the nonaccrual loan portfolio at December 31, 2012, and

8

$178,550 representing 73.4 percent of the nonaccrual loan portfolio at December 31, 2011.

Additional loan information is in Note 3 to the Consolidated Financial Statements.

Allowance for Credit Losses The allowance for credit losses is comprised of the allowance for loan losses (ALL) and the reserve

for unfunded lending commitments. The allowance for credit losses is our best estimate of the

amount of probable losses inherent in our loan portfolio at the balance sheet date. The allowance

for credit losses is determined based on a periodic evaluation of the loan portfolio and unfunded

lending commitments, which generally considers types of loans, credit quality, specific industry

conditions, general economic and political conditions, and changes in the character, composition,

and performance of the portfolio, among other factors. The allowance for credit losses is calculated

based on a historical loss model that takes into consideration various risk characteristics of our

loan portfolio. We evaluate the reasonableness of this model and determine whether adjustments

to the allowance are appropriate to reflect the risks inherent in the portfolio.

Individual loans are evaluated based on the borrower’s overall financial condition, resources, and

payment history; the prospects for support from any financially responsible guarantor; and, if

appropriate, the estimated net realizable value of any collateral. The allowance for loan losses

attributable to these loans is established by a process that estimates the probable loss inherent in

the loans, taking into account various historical and projected factors, internal risk ratings,

regulatory oversight, geographic location, industry and other factors.

We maintain a reserve on unfunded commitments. The reserve reflects our best estimate of losses

inherent in lending commitments made to customers but not yet disbursed. Factors such as the

likelihood of disbursements and the likelihood of losses given disbursement are utilized in

determining this reserve. This reserve is reported within Other liabilities on the Consolidated

Balance Sheet and totaled $15,000 at December 31, 2013 and $12,000 at December 31, 2012 and

2011.

The ALL reserves at December 31, 2013, 2012, and 2011 totaled $97,000, $128,000, and

$126,500, respectively. Specific loan loss reserves at December 31, 2013, 2012, and 2011 totaled

$16,405, $47,971, and $31,679, respectively. For each of these respective years, the specific

reserve was primarily comprised of those relationships within the agricultural sectors which were

impacted by volatility in commodity and input prices, such as dairy, as well as those industries,

such as nursery, that were impacted by the overall downturn in the U.S. economy.

Coverage of the ALL, as a percentage of certain key loan categories, is presented in the following

table:

Results of Operations Our net income for the year ended December 31, 2013, was $236,889, compared to $187,255 for

2012 and $159,156 for 2011. The following table provides detail of changes in the components of

our net income:

Net Interest Income: Net interest income was $3,816 lower in 2013 compared to 2012

primarily due to a decrease in loan spread caused in part by greater prepayment expense,

competitive pressures and an increase in the average loan volume in lower spread lines of

business. Net interest income was $6,472 higher in 2012 compared to 2011 primarily due to an

increase in average loan volume, increased income from nonaccrual loans and a decrease in the

cost of funds. The cost of funds was impacted by the composition of the balance sheet and the

amount of equity available to fund loan volume. These items were partially offset by a decrease in

loan spread caused in part by greater prepayment expense, competitive pressures, and lower

interest rates.

9

Influences on net interest income from changes in effective rates on, and volume of, interest-

earning assets and interest-bearing liabilities between the years ended December 31, 2013, and

2012, and between the years ended December 31, 2012 and 2011, are presented in the following

table:

Information regarding the average daily balances and average rates earned and paid on our

portfolio are presented in the following table:

Reversal of/Provision for credit losses: In 2013, credit quality improved significantly as

shown by the reduction in nonaccrual loans. Additionally, net recoveries of $6,677 were recorded

in 2013. Both of these resulted in a credit loss reversal in 2013. In the prior two years, our charge-

offs, nonaccrual loans, and adverse loans were higher than historical averages, and resulted in

larger provisions for credit losses. Charge-offs net of recoveries totaled $28,990 and $26,841 in

2012 and 2011, respectively, and were concentrated in the dairy and nursery sectors.

Noninterest income: The decrease in noninterest income of $10,225 in 2013 when compared to

2012 was primarily due to a $11,238 refund received in 2012 from the Farm Credit System

Insurance Corporation (Insurance Corporation) related to the Farm Credit Insurance Fund

(Insurance Fund). As described in Note 1 to the Consolidated Financial Statements when the

Insurance Fund exceeds the statutory 2 percent secure base amount, the Insurance Corporation

evaluates the insurance premium assessment rate for Farm Credit System banks and may refund

excess amounts. The Insurance Fund ended 2011 above the secure base amount, and

consequently in the second quarter of 2012, the Insurance Corporation distributed to Farm Credit

entities the excess amount. No similar refunds were received in 2013 or 2011. These refunds are

recorded in Other income on the Consolidated Statement of Income. Financially related services

decreased $2,155, or 13.8 percent as compared to 2012 related mainly to $2,147 received in 2012

from profit sharing with insurance companies. Similar profit sharing with insurance companies was

not recognized in 2013 or 2011.

Operating expense: In 2013, operating expenses increased by $5,121 when compared to 2012.

Factors causing higher operating expenses when compared to the previous year were increased

Insurance Fund premiums of $3,190, related to the assessment rate increasing, purchased services

of $2,626, and salaries and benefits of $2,612. Purchased services increased primarily due to

technology services we purchase from Financial Partners, Inc. as well as costs associated with

contract labor for a new loan accounting system. Salaries and benefits were higher than in the

previous year due to normal annual salary increases and incentive expenses related to 2013

performance. These increases were partially offset by a decrease in occupancy and equipment

expense associated with certain assets that were fully depreciated in the prior year. Additionally,

the reversal of a portion of the contingent liability recorded previously related to revenue taxes

resulted in a reduction of operating expenses in 2013 of $1,638.

Operating expenses increased by $9,000 in 2012 compared to 2011. The change is related mainly

to salaries and benefits which increased $10,620 as compared to the prior year. Salaries and

benefits include normal annual salary increases, increased incentive and defined benefit plan

expenses. This increase was partially offset by a decrease in other operating expense of $2,008

when compared to 2011. This decrease is attributed to higher deferred loan origination costs and a

decline in credit enhancement premiums as compared to the prior year. Other operating expense

also included an additional $1,000 related to a previously existing contingent liability related to

revenue taxes. Decreases in operating expenses were in occupancy and equipment and insurance

fund premiums.

Provision for income taxes: Income tax expense was $2,468 lower than in the previous year.

The effective tax rate was 2.9 percent for the year ended December 31, 2013 as compared to 4.8

percent for 2012. Contributing to the reduction was the reversal of the $1,000 uncertain tax

10

position recorded in the prior year as the uncertainty related to the state tax position has been

resolved. The remaining reduction in taxes is primarily related to a reduction in the income from

non-patronage sourced business in our taxable entity as compared to the prior year. The tax

expense in 2012 increased $3,143 as compared to 2011. Contributing to the increase was a $1,000

uncertain tax position recorded in the year ended December 31, 2012 referred to above. The

remaining increase in the provision for tax expense in 2012 as compared to 2011 was primarily

related to non-patronage sourced income from our taxable entity.

Liquidity and Funding Sources The primary source of our liquidity and funding is a direct loan from CoBank which is reported as

Note payable to CoBank, ACB on the Consolidated Balance Sheet. As described in Note 7 to the

Consolidated Financial Statements, this direct loan is governed by a General Financing Agreement

(GFA) and is collateralized by a pledge of substantially all of our assets and is also subject to

regulatory borrowing limits. The GFA includes financial and credit metrics that if not maintained

can result in increases to our funding costs. The GFA also requires us to comply with FCA

regulations regarding liquidity. To meet this requirement, we are allocated a share of CoBank’s

liquid assets. We are currently in compliance with the GFA and do not foresee issues with

obtaining funding or maintaining liquidity.