norazita marina abdul aziz

TRANSCRIPT

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 178

RECLAIMING THE ACCOUNTS: AN UNDERSTANDING FROM ISLAMIC

PRINCIPLES AND VALUES

Norazita Marina Abdul Aziz

Centre of General Studies,

Universiti Utara Malaysia (UUM)

06010 Sintok, Kedah

Email address: [email protected]

Abstract

Islamic accounting is essential by providing a basis on the Islamic debts and the

justice in the life of the hereafter, which can be referred to Al-Quran, Prophet

Sayings (Al-Hadith) or Ijma’ and Qiyas. The limitation in the Western accounting

has influenced the development of the Islamic Shariah framework in Islamic

Accounting. Since adherence to Shariah Islamiah is a form of worship, the Islamic

accounting framework is thus an act of worship in fulfilling obligations to Allah

(God), society and self as well as achieving Al-Falah (rewards in this world and

hereafter). The paper examines the applicability by revisiting the MASB's Islamic

Accounting project, where it was discontinued in the year 2009 based on a few

reasons stated by MASB. Thus, the paper discusses a holistic view of the underlying

values and principles of the Shari’ah Islami’iah (Islamic teachings) and its

application to the IPA, is defined as an assurance function that seeks to establish

socioeconomic justice through its formalised procedures, routines, objective

measurement, control and reporting in accordance with Shari’ah Islami’iah

principles. In line with this, the Islamic moral values and ethical conduct of an

individual is essential in delineating the relationship of between man and Allah; man

and another man; and lastly man and nature (through the conception of

hablunminnallah, hablunminnas). The ontological position is founded from the

Tawhidic position, which underpins the concept of Oneness of the God.

Keywords: Islamic accounting; Islamic accounting values and principles

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 179

INTRODUCTION

Interestingly, the basic of Islamic debts and justice in the life of the hereafter can be

reflected from the Al-Quran. The understanding of the Al-Quran translation can be

delineated in the following verses in the Al-Quran.

“O you who have believed, when you contract a debt for a specified

term, write it down. And let a scribe write [it] between you in justice.

Let no scribe refuse to write as Allah has taught him. So let him write

and let the one who has the obligation dictate.” (al-Baqarah, 2:282)

“And We place the scales of justice for the Day of Resurrection, so no

soul will be treated unjustly at all. And if there is [even] the weight of

a mustard seed, We will bring it forth. And sufficient are We as

accountant.” (al-Anbiya’, 21:47)

Islamic accounting has becoming an important issue in deliberating and applying the

International Financial Reporting Standards (IFRS) and International Accounting

Standards (IAS) for the Islamic transactions. The Islamic accounting research focus

on the Islamic teachings, law and values in deliberating the Islamic accounting

(Gambling and Karim, 1991; Gambling and Karim, 1986; Haniffa, 2002; Haniffa and

Hudaib, 2004; Lewis, 2001, 2006).

Financial reporting from an Islamic perspective is a process through which

appropriate information is communicated to users and assisted them to assess

whether an entity is operating within the Shariah boundary and fulfilling its

responsibilities to society and the environment, and for users to make decisions that

would persuade the entity to fulfil or to continue to fulfil those responsibilities

(Hameed, 2001; Hamid, Craig, and Clarke, 1993; Haniffa, 2002; Lewis, 2006).

Interestingly, the Islamic transactions have to exclude these elements, which are (i)

elements of interest (riba), (ii) uncertainty (gharar), (iii) gambling (masyir) and (iv)

prohibition of certain goods (such as alcohol and pork) (Lewis, 2010).

Islamic accounting will become an interesting area to be discussed and researched

due to the complexity of business transactions in the modern world (Lewis, 2010). In

the globalisation market, the area of Islamic accounting will provide a broader and

new platform for research to be conducted especially concerning on the applicability

in setting up a new Islamic accounting standards in Malaysia, which is derived

through a Shariah teachings and law. Additionally, it provides an avenue for

undertaking research related to the harmonisation of Islamic accounting standards in

the Islamic countries.

In Malaysia, Islamic accounting standards are regulated by the Malaysian

Accounting Standard Board (MASB). In 2009, they stopped the development of the

Islamic accounting standards in Malaysia as they believe that the values and

principles in Islam is similar to that is being proposed by International Standard

Board (IAS) (MASB, 2011). The MASB will refer to the Shariah Supervisory Board

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 180

and specialist in the area should they encounter any discrepancies pertaining to the

Shariah Compliant (MASB, 2011).

The paper is essential in developing the context and boundaries in the application of

Islamic accounting standards in Malaysia and in the global setting. The in-depth

analysis on the review of the literature will provide an extension to the

epistemological analysis for the Islamic accounting philosophy and assist the

government policy setters in making decision pertaining to Islamic transactions.

Thus, the paper addresses the development of Islamic accounting standards in

Malaysia by specifically identify the historical background of Islamic accounting in

Malaysia and examine the applicability of the adoption of conventional accounting

standard to the Islamic accounting perspectives. The next section elaborates on the

review of literature in Islamic accounting, which is essential in setting up the concept

and boundaries related to the ontological positions in Islamic foundations.

REVIEW OF PREVIOUS RESEARCH

Research on Islamic accounting perspective has becoming an interesting and

debatable area in the recent years (Baydoun and Willett, 2000; Gambling and Karim,

1991; Gambling and Karim, 1986; Haniffa, 2002; Haniffa and Hudaib, 2004; Lewis,

2001, 2006, 2010; Zurina and Nurazalia, 2013). There has been an increasing

emphasis related to the Islamic banking mainly on the applicability of the

conventional accounting principles for the Islamic institutions (Baydoun and Willett,

2000; Gambling and Karim, 1991; Gambling and Karim, 1986; Zurina and

Nurazalia, 2013), economic consequences, the need for separate accounting

standards for Islamic banks, the formulisation of standards Islamic corporate reports,

the historical account of the development of Islamic accounting and the requirements

in the appointment of Muslim accountants in the Middle Ages.

Two early contributions to the Islamic accounting literature, Gambling and Karim

(1986) and Tomkins and Karim (1987), are influenced by the emerging literature on

social accounting, particularly Gambling’s (1974) Societal Accounting. The authors

claim accounting and business ideas and methods developed in a Western

environment influenced by Judeo-Christian ethical notions would not necessarily

operate effectively in a Muslim environment. They emphasise the need for Islamic

accounting to be grounded in Shariah Law. They identify a duty for organizations to

be accountable to the Muslim community (the ummah) and discuss factors, which

they consider likely to influence Muslim users’ needs relating to financial reporting.

Interestingly, the basic of Islamic debts and justice in the life of the hereafter can be

reflected from the Al-Quran. The understanding of the Al-Quran translation can be

delineated in the following verses in the Al-Quran.

“And We place the scales of justice for the Day of Resurrection, so no

soul will be treated unjustly at all. And if there is [even] the weight of

a mustard seed, We will bring it forth. And sufficient are We as

accountant.” (al-Anbiya’, 21:47)

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 181

The conventional accounting is developed under the premise of utilitarianism that

holds the actions in producing greatest amount of goods for a number of people in

the society (Neu, 1992), which leads to greediness (Haniffa, 2002). This rationality

deviates from Islamic perspective and need to be revisited so that it aligns with the

Islamic teachings.

From the limitation of conventional accounting, the Shariah Islamiah is proposed as

the foundation in building a theoretical framework for Islamic perspective

accounting. Since adherence to Shariah Islamiah is a form of worship, the role of

Islamic perspective accounting is thus an act of worship in fulfilling obligations to

Allah (God), society and self as well as achieving Al-Falah (rewards in this world

and hereafter).

Thus, the paper delineates a holistic view of the underlying values and principles of

the Shariah Islamiah (Islamic teachings) and its application to the Islamic

perspective of accounting, which can be define an assurance function to seek in

establishing socioeconomic justice through its formalised procedures, routines,

objective measurement, control and reporting in accordance with Shariah Islamiah

principles.

Therefore, the paper investigates the fundamental principles and values of Islamic

business ethics, the implications of these principles for Islamic accounting based on

Islamic teachings and law.

RESEARCH METHODOLOGY

The study is conducted based on interpretive position1 by undertaking library search

and documentary review in addressing the research questions. The research is

conducted by interpreting the meaning of language and texts, which can be in a form

of reports, articles and manuscripts. The interpretive inquiry employs in order to

provide an understanding of the knowledge in addressing the research questions.

The paper inductively employed qualitative research methodology in contextualising

the Islamic accounting in Malaysia. The Islamic philosophical underpinnings are

based on the contextualisation of the Islamic values and principle, which can be

identified within the Islamic Shariah Framework that evolved from the research

findings. A thematic analysis is conducted to create appropriate themes from various

documentary reviews, which addressed the field of inquiry.

The ontological positions discusses in this paper stem within the contemplation based

on Islamic position, which can be highlighted through the understanding of social

relations among Muslim through the understanding that human relations consists

intangible relations that uniquely relate to the submission of Allah, the one God

(Quran, 51:56)

1 Called qualitative research in some disciplines, it is conducted from an experience-near perspective

in that the researcher does not start with concepts determined a priori but rather seeks to allow these to

emerge from encounters in "the field" (which we define here broadly, to encompass both traditional

in-country fieldwork, domestic and overseas, and textual-archival research).

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 182

Thus, the paper adopts qualitative research to revisit the underpinning principles and

values and discuss the appropriateness of MASB’s action to embed the conventional

principles and values in the Malaysian Financial Reporting Standards (MFRS).

THE ISLAMIC DIVINE LAW FOR ONE’S ACCOUNT

As a comprehensive religion, Islam provides a nature of the relationship between the

Creator and His creations, the nature of the relation between humanity and the

universe, humans’ relations with their own society, different societies and humanity

as a whole (Haniffa, 2002). With related to human, which is considered part of the

“hablumninallah, hablunminannas”, the notion that humans are accountable to God

for their actions and omissions is a central tenet of Islam (Askary and Clarke, 1997;

Haniffa, 2002). Islam reckons all activities of one’s life as being in effect an act of

worship as long as they are within the bounds of conscience, goodness and honesty

(Haniffa, 2002; Lewis, 2010).

There are opinions to exclude religious consideration from the research philosophical

foundations. The novice researcher may find it is irrelevant to consider the religious

thoughts in applying it to financial reporting – an area that they may view as

unrelated to matters of faith.

However, in Islamic thought, there must be comprehensive governance of man’s life

to preserve his innate purity from being corrupted by earthly desires. Hence, all

aspects of life, whether ibadah (relating to worship) or muamalat (relating to

mankind and its environment), must be governed by the teachings of Al-Quran and

As-Sunnah.

Islam provides a nature of the relationship between the Creator and His creations, the

nature of the relation between humanity and the universe, humans’ relations with

their own society, different societies and humanity as a whole, and the relationship

between humans and their souls. Islam reckons all activities of one’s life as being in

effect an act of worship as long as they are within the bounds of conscience,

goodness and honesty (Kotb, 1970, p. 9).

Two early contributions to the Islamic accounting literature, Gambling and Karim

(1986) and Tomkins and Karim (1987), are influenced by the emerging literature on

social accounting, particularly Gambling’s (1974) Societal Accounting. The authors

claim accounting and business ideas and methods developed in a Western

environment influenced by Judeo-Christian ethical notions would not necessarily

operate effectively in a Muslim environment. They emphasise the need for Islamic

accounting to be grounded in Sharia. They identify a duty for organizations to be

accountable to the Muslim community (the ummah) and discuss factors, which they

consider likely to influence Muslim users’ needs relating to financial reporting. This

is an important platform that conform the significance of the study to be undertaken.

In the particular case of financial reporting, proponents of financial reporting from an

Islamic perspective cite Quranic verses such as the following as the basis for

subjecting it to Islamic religious considerations:

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 183

“O ye who believe! When ye deal with each other in transactions

involving future obligations in a fixed period of time, reduce them to

writing; let a scribe write down faithfully as between the parties; let

not the scribe refuse to write; as Allah has taught him, so let him write

...” (al-Baqarah, 2:282)

With the conviction that the recording of financial transactions is a divine

commandment, the field of study known as ‘Islamic accounting’ was created.

Besides this philosophical fundamental queries on Islamic accounting literature,

there are two key elements that are prohibited, which is stated in the Quran that is the

prohibition of riba, sometimes interpreted as usury but more usually as all forms of

interest, and the fundamental duty of all Muslims to pay the religious levy zakat

(Gambling and Karim, 1991).

With related to human, which is considered part of the hablumninallah,

hablunminannas, the notion that humans are accountable to God for their actions

and omissions is a central tenet of Islam. To clarify this, Askary and Clarke (1997)

review words related to accounting that are mentioned in the Qur’an. The word

hisab (account, reckoning) and its derivatives appear more than eighty times in

different verses of the Qur’an. Judgement in the Hereafter is described in terms of

weighing one’s good and evil deeds in a balance, with the good and evil deeds

being recorded in books or registers.

The theme of accountability to God is pursued further by Alam (1998), and

particularly by Lewis (2001), who discusses two important ethical concepts for

Islamic accounting: God’s absolute ownership of all resources and humanity’s role

as God’s representative (khalifa) on earth, granted stewardship of God’s

possession. These concepts support the contemporary idea of sustainability.

It can be seen that Shari’ah Islami’iah is based on two basic sources: the Qur’an

(the word of Allah) and the Hadith (sayings, approvals and actions of the Prophet

Muhammad, peace be upon him (pbuh) during his lifetime). The third source is

Ijma’, a consensus of Muslim scholars and is applied only in the absence of an

explicit answer to the issue in question. The final source is Qiyas, which is

represented in the analogical deductions from the other three sources for

contemporary issues that are not directly mentioned in those sources but have similar

characteristics as those that existed in the past. Once any decision is made by either

Ijma’ or Qiyas, it becomes mandatory and cannot be overruled by future generations

(Zaid, 2000).

Thus, the study proposed to developed an Islamic Accounting theoretical framework

that is based on the Tawhidic position based on the Al-Quran, Sunnah and Ijma’

Qiyas, which covers the Islamic accounting philosophical stances, values and

principles.

The paper will explore the fundamental principles and values of Islamic business

ethics, the implications of these principles for Islamic accounting, and social and

economic responsibility.

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 184

OVERVIEW OF MASB

However, in Malaysia, Malaysian Accounting Standards Board (MASB) is

established under the Financial Reporting Act 1997 (the Act) as an independent

authority to develop and issue accounting and financial reporting standards in

Malaysia. They monitor and provide the standards issued by the MASB legal

authority.

Interestingly, The MASB states they are not aware of any MASB accounting

requirement that violates Shariah. Nevertheless, in the extremely rare circumstances

where there is a Shariah prohibition to a requirement in an MASB approved

accounting standard, that requirement need not be complied with, and MASB will

undertake to issue alternative guidance. This can be seen from the statement release

by MASB in addressing the issues related to the requisition of Islamic accounting

standards in Malaysia.

“We are not aware of any MASB accounting requirement that violates

Shariah. However, in the extremely rare circumstances where there is

a Shariah prohibition to a requirement in an MASB approved

accounting standard, that requirement need not be complied with, and

MASB will undertake to issue alternative guidance.” (Statement

release by MASB)

MASB’s action is inconsistent with the Accounting and Auditing Organization for

Islamic Financial Institutions (AAOIFI). To elaborate, AAOIFI sets accounting,

auditing, governance, ethics and Shariah standards for Islamic financial institutions.

While it is a pioneer in Islamic standard-setting, the MASB is concerned that its

accounting standards may not have been developed based on a conceptual framework

similar to the MASB approved accounting standards. Thus, the MASB has not

approved AAOIFI financial accounting standards for use by entities under its

purview.

If for some reason, there is a matter that is not dealt with by MASB approved

accounting standards, but for which guidance may be found in an AAOIFI financial

accounting standard, an entity may consider the AAOIFI requirement, provided that

it is in accordance with the requirements of Financial Reporting Standards (FRS) 108

on the selection and application of accounting policies.

In general, this would mean that an entity may not apply AAOIFI recognition and

measurement requirements that depart from MASB requirements. However, the

inclusion of additional disclosures required under AAOIFI standards, if appropriate,

may be acceptable.

The inconsistencies emerged between the MASB and AAOIFI, leads to the

discrepancies in Islamic accounting choices and the underpinnings of Islamic

philosophical foundations in setting out the global standards for Islamic transactions.

The irregularities on the adoption of Islamic accounting standards between MASB

and AAOIFI will lead to the failure in harmonising Islamic accounting standards in

the Islamic countries globally.

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 185

Since, MASB claims the Islamic Accounting Standards pronouncement in

unnecessary (MASB, 2011), it is important the study to revisit what has been done

by the MASB in promoting the Islamic accounting principles and values in the

Malaysian Financial Reporting Standards (MFRS). MASB Islamic accounting

pronouncements provide guidance on how the MASB approved accounting standards

are to be applied to Islamic transactions and events. However, MASB do not in any

way validate an entity’s activities as being Shariah compliant.

Therefore, in providing improvement to the problem, the proposal will identify

Islamic accounting context within the Islamic accounting standards setter in

Malaysia, i.e. MASB. The proposal will highlight the Islamic accounting philosophy,

values and principles in order to have a clear direction in the formulation and

construction of the “true” Islamic accounting that can be used worldwide that

delineate from the Islamic fundamental foundation. The detail of the research

objectives and questions is delineated in the following section.

MALAYSIA ACCOUNTING STANDARDS BOARD (MASB)

In Malaysia, Malaysian Accounting Standards Board (MASB) is established under

the Financial Reporting Act 1997 (the Act) as an independent authority to develop

and issue accounting and financial reporting standards in Malaysia. They monitor

and provide the standards issued by the MASB legal authority.

Interestingly, The MASB states they are not aware of any MASB accounting

requirement that violates Shariah. However, in the extremely rare circumstances

where there is a Shariah prohibition to a requirement in an MASB approved

accounting standard, that requirement need not be complied with, and MASB will

undertake to issue alternative guidance.

For example, MASB claims that FRS 108, Accounting Policies, Changes in

Accounting Estimates and Errors, and SOP i-1 provide guidance on the selection and

application of accounting policies in the absence of a MASB approved accounting

standard that applies to a transaction, other event or condition.

MASB utilizes the principles stated in the IFRS and IAS, which management shall

use its judgement in developing and applying an accounting policy that results in

information that is:

i relevant to the economic decision-making needs of users; and

ii reliable, in that the financial statements:

iii represent faithfully the financial position, financial performance and cash

flows of the entity;

iv reflect the economic substance of transactions, other events and conditions,

and not merely the legal form;

v are neutral, i.e. free from bias;

vi are prudent; and

vii are complete in all material respects.

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 186

In making the judgement described, management shall refer to, and consider the

applicability of, the following sources in descending order:

i the requirements and guidance in Standards and Interpretations dealing with

similar and related issues; and

ii the definitions, recognition criteria and measurement concepts for assets,

liabilities, income and expenses in the Framework.

MASB believes that the management may also consider the most recent

pronouncements of other standard-setting bodies that use a similar conceptual

framework to develop accounting standards, other accounting literature and accepted

industry practices, to the extent that these do not conflict with the sources described

above.

MASB claims the Islamic Accounting Standards pronouncement in unnecessary

(MASB, 2009). MASB Islamic accounting pronouncements provide guidance on

how the MASB approved accounting standards are to be applied to Islamic

transactions and events. MASB do not in any way validate an entity’s activities as

being Shariah-compliant.

This indication is detrimental especially when it comes to the explanation and

elaboration concerning the Islamic accounting philosophical stances especially

related to the uniqueness of the Islamic values and principles.

Thus, this proposal will highlight the Islamic accounting philosophy, values and

principles in order to have a clear direction in the formulation of the “true” Islamic

accounting that can be used worldwide that delineate from the Islamic fundamental

foundation.

THE AAOIFI GUIDELINES VS MASB

The Accounting and Auditing Organization for Islamic Financial Institutions

(AAOIFI) sets accounting, auditing, governance, ethics and Shariah standards for

Islamic financial institutions. While it is a pioneer in Islamic standard-setting, the

MASB is concerned that its accounting standards may not have been developed

based on a conceptual framework similar to the MASB approved accounting

standards. Thus, the MASB has not approved AAOIFI financial accounting

standards for use by entities under its purview.

If for some reason, there is a matter that is not dealt with by MASB approved

accounting standards, but for which guidance may be found in an AAOIFI financial

accounting standard, an entity may consider the AAOIFI requirement, provided that

it is in accordance with the requirements of FRS 108 on the selection and application

of accounting policies.

In general, this would mean that an entity may not apply AAOIFI recognition and

measurement requirements that depart from MASB requirements. However, the

inclusion of additional disclosures required under AAOIFI standards, if appropriate,

may be acceptable.

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 187

WHAT COULD HAPPEN IF THE PROBLEM IS NOT ADDRESSED?

Mixture of principles and the ontological and epistemological position will have the

elements that related to the social norms and actions and not directly relate to the

divine law of human conduct and ethical concepts for developing the politic,

economy and social (Haniffa, 2002). Research philosophy need to be based on

Islamic values and principles in deriving to the Islamic conceptual Framework for

the formulation and construction of Islamic accounting standards, which is not

embedded the social norms.

In Islam, the rights and obligations of individuals and organizations with respect to

others are clearly defined by religion, and are neither imposed by secular law that is

exposed to change, nor subject to personal views.

“And how many a city rebelled against the Commandments of its Lord

and His Messengers then we took a severe account from it, and gave it

a horrible punishment.” (al-Thalaq, 65:8)

From an Islamic standpoint, this is considered to make Islam a stronger and more

effective basis for ethical values.

Despite the presence of many schools of thought in Islam, there is agreement on

basic matters of principle (Hamid et. al, 1993, p. 136). The Islamic accountability

considers an organisation to be accountable to God (Allah) and to the communities in

which they operate and have a duty of truthful within the society they engaged in. In

addition, the social responsibilities of an individual within the Islamic context are

derived from the words of God (contained in the Al-Quran); and the good deeds and

sayings (the Sunnah) of the Prophet Muhammad pbuh (peace and blessings be upon

him) (Haniffa, 2002; Lewis, 2006).

Responsibilities of members of society to each other are well defined, do not change

over time and are not affected by different theoretical frameworks. Islam claims to be

a religion relevant for all times and places. In addition, in the Islamic context, the

social responsibilities of individuals that are derived from the word of God

(contained in the Qur’an) and from his prophet Mohammed’s deeds and sayings (the

Sunah) apply in the construction of social engagement in the NGO. The discussion

on Islamic accountability can be seen in a wider perspective that it involves the one’s

relationship with Allah and to other human beings, where Islam considers work to be

part of the worship of God (Haniffa, 2002; Haniffa and Hudaib, 2004).

The relationship to Allah can be considered through the “hisab”, which brings a

universal sense of one’s obligation to Allah and to other mankind. In this viewpoint,

every Muslim has an “account” to Allah, in “recording” all good and bad deeds,

which will continue until the death. And, for Allah, the accounts for all his servants

will be delivered to the mankind on the day of judgement.

“To Allah belongs whatever is in the heaven and whatever is in the

earth; and if you disclose whatever is in your heart or keep it hidden,

Allah will call you to account for it; then He will forgive whomsoever

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 188

He pleases and punish whomsoever He pleases, and Allah is potent

over everything.” (al-Baqarah, 2:284)

The deliberation on the relationship with Allah is stated by Lewis (2006) as the

concept of accountability in Islam is derived from the concept of Tauhid (the unity of

Allah). The concept of the unity of Allah implies total submission to Allah’s will and

following the religious requirement in all aspects of life (Maali, Casson and Napier,

2003). Baydoun and Willett (2000) said that the concept of the unity of Allah gives

rise to different and broader concept of accountability that implied by the Western

models. The verse below reinforces the notion that everyone is accountable to Allah

on the day of judgement for their actions during their lives.

“Allah takes careful account of everything” (Al-Nisa’, 4:86)

Therefore, this theoretical foundation of this paper is based on the Islamic

accountability, which stems the relationship of human and Allah and the relationship

of human to other mankind. By referring to this notion, I believe the paper will cover

the ultimate relationship of ABIM where it involves the relationship of the ABIM’s

members with the Allah that is based on moral imperatives and values in oneself and

the relationship with other community at large.

“Undoubtedly, in the creation of heavens and earth and in the mutual

alternation of night and day, there are signs for men of understanding.

Who remember Allah standing and sitting and lying on their sides, and

contemplate in the creation of heavens and earth; (saying) "O our

Lord! You have not made it in vain, hallowed be You, You save us from

the torment of the Hell.” (Ali Imran, 3:190-191)

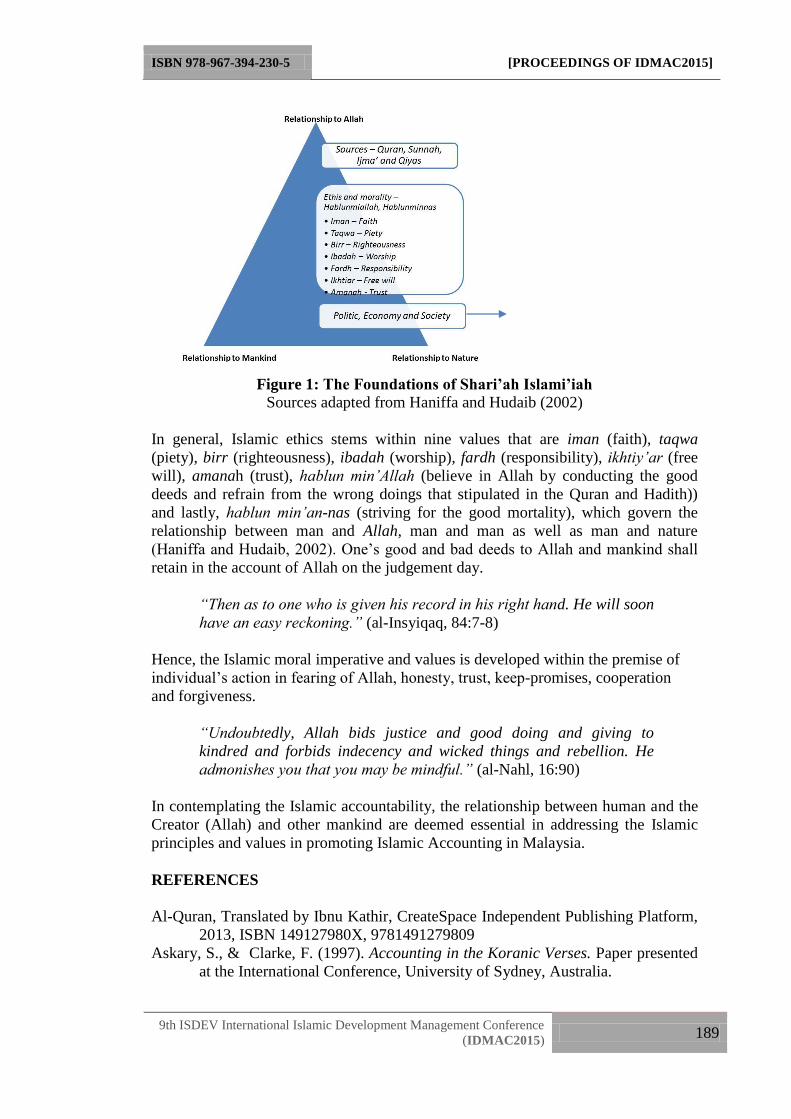

From this notion, the paper proposes the important elements that need to be

comprehend in the MASB for proposing specific Islamic Accounting Standards. The

Shariah Islamiah Framework, as summarised in Figure 1, can be referred to as a basis

in addressing the one’s account from the Islamic fundamental position for its

principles and values.

POLITICS:

Syura – Consultation

Khilafa – Succession

Bay’a – Obedience

ECONOMICS:

Zakat – Religious levy

Halal – Lawful means

Nizam – Order

I’tidal – Moderation

Islah – Noble

SOCIETY:

Ummah – Community

Maslahah – Public interest

Dar al-darar – Prevention of

harmful activities

Raf al-haraf – Removal of

hardship in society

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 189

Figure 1: The Foundations of Shari’ah Islami’iah

Sources adapted from Haniffa and Hudaib (2002)

In general, Islamic ethics stems within nine values that are iman (faith), taqwa

(piety), birr (righteousness), ibadah (worship), fardh (responsibility), ikhtiy’ar (free

will), amanah (trust), hablun min’Allah (believe in Allah by conducting the good

deeds and refrain from the wrong doings that stipulated in the Quran and Hadith))

and lastly, hablun min’an-nas (striving for the good mortality), which govern the

relationship between man and Allah, man and man as well as man and nature

(Haniffa and Hudaib, 2002). One’s good and bad deeds to Allah and mankind shall

retain in the account of Allah on the judgement day.

“Then as to one who is given his record in his right hand. He will soon

have an easy reckoning.” (al-Insyiqaq, 84:7-8)

Hence, the Islamic moral imperative and values is developed within the premise of

individual’s action in fearing of Allah, honesty, trust, keep-promises, cooperation

and forgiveness.

“Undoubtedly, Allah bids justice and good doing and giving to

kindred and forbids indecency and wicked things and rebellion. He

admonishes you that you may be mindful.” (al-Nahl, 16:90)

In contemplating the Islamic accountability, the relationship between human and the

Creator (Allah) and other mankind are deemed essential in addressing the Islamic

principles and values in promoting Islamic Accounting in Malaysia.

REFERENCES

Al-Quran, Translated by Ibnu Kathir, CreateSpace Independent Publishing Platform,

2013, ISBN 149127980X, 9781491279809

Askary, S., & Clarke, F. (1997). Accounting in the Koranic Verses. Paper presented

at the International Conference, University of Sydney, Australia.

ISBN 978-967-394-230-5 [PROCEEDINGS OF IDMAC2015]

9th ISDEV International Islamic Development Management Conference

(IDMAC2015) 190

Baydoun, N., and Willett, R. (2000). Islamic corporate reports. ABACUS, 36(1), 71-

90.

Gambling, T., & Karim, R. A. (1991). Business and Accounting Ethics in Islam.

London Mansell.

Gambling, T. E., & Karim, R. A. (1986). Islam and 'social accounting'. Journal of

Business Finance and Accounting, 13(1), 39-50.

Hameed, S. (2001, 10 - 12 October). Islamic accounting - accounting for the new

millenium? Paper presented at the Asia Pacific Conference 1, Kota Bahru,

Kelantan, Malaysia.

Hamid, S., Craig, R., & Clarke, F. (1993). Religion: A confounding cultural element

in the international harmonisation of accounting? ABACUS, 29(2), 131-148.

Haniffa, R. (2002). Social responsibility disclosure: an Islamic perspective.

Indonesian Management and Accounting Journal 1(2).

Haniffa, R., & Hudaib, M. (2004, 15-17 June). Disclosure practices of Islamic

financial institutions: an exploratory study. Paper presented at the

Accounting, Commerce and Finance: The Islamic Perspective International

Conference V, Brisbane, Australia.

Kotb, S. (1970). Social justice in Islam / [by] Sayed Kotb. Translated from the

Arabic by John B. Hardie. : New York : Octagon Books, 1970 [c1953]

Lewis, M. K. (2001). Islam and accounting

Lewis, M. K. (2006, April 10-12). Accountability and Islam. Paper presented at the

Fourth International Conference on Accounting and Finance in Transitions,

Adelaide.

Lewis, M. K. (2010). Accentuating the positive: governance of Islamic investment

funds. Journal of Islamic Accounting and Business Research 1(1), 42-59.

MASB. (2011). Accounting for Islamic Financial Transactions and Entities In A. W.

G. o. I. Finance (Ed.), December 2011.

Neu, D. (1992). The social contsruction of positive choices. Accounting,

Organisation and Society 17(3/4), 223-237.

Zurina, S., & Nurazalia, Z. (2013). doption of international financial reporting

standards and international accounting standards in Islamic financial

institutions from the practitioners' viewpoint. Middle East Journal of

Scientific Research 13 (Research in Contemporary Islamic Finance and

Wealth Management, 13, 42-49.