nomura securities international, inc., new york · 2012-05-23 · 1-212-667-9316 wisdom of crowds /...

TRANSCRIPT

STRICTLY PRIVATE AND CONFIDENTIAL

© Nomura

This commentary has been prepared by a Nomura

equities desk strategist and is NOT a product of

the Research Department. For additional

information concerning the role of trading desk

strategists, please see the important conflicts

disclosures beginning at page 42 of this report.

Nomura Securities International, Inc., New York

April 30, 2012

Quantitative Strategy

Joseph J. Mezrich

1-212-667-9316

Wisdom of crowds / Madness of crowds

Quantitative Desk Commentary

– Active management and the hunt for alpha

– Correlation and growth of systemic risk

– Changes over the past decade – a sampling

– Wisdom of crowds or madness of crowds?

The hunt for alpha: Paradigm in motion

Joseph Mezrich, 212.667.9316,

Equity fund flow –

passive funds grow, while active funds shrink

Note: Shows cumulative fund flow into US-equity funds, active funds, passive funds and ETFs. Period of analysis is from April 2003 through March 2012.

Source: Nomura Securities International, Inc, EPFR.

2

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400

Ap

r-0

3

Oct

-03

Ap

r-0

4

Oct

-04

Ap

r-0

5

Oct

-05

Ap

r-0

6

Oct

-06

Ap

r-0

7

Oct

-07

Ap

r-0

8

Oct

-08

Ap

r-0

9

Oct

-09

Ap

r-1

0

Oct

-10

Ap

r-1

1

Oct

-11

Ap

r-1

2

Cu

mu

lati

ve f

un

d f

low

(b

illio

n $

)US-equity fund flow: active vs. passive

US-equity funds

Active funds

Passive funds

Joseph Mezrich, 212.667.9316,

Wisdom of crowds or Madness of crowds?

What’s New? Why is this happening?

Cash equities

Fundamental Indexation

Min variance investing

Risk parity investing

Diversity weighting

Etc…

Many alternatives to traditional cap weighted benchmark

ETF’s/ ETN’s

SPLV (low vol)

PBP (BuyWrite)

IYR (real estate)

SH (short S&P500)

Risk on (ONN)/Risk off (OFF)

Etc …

Pick a theme or alternative beta to invest in

3

Joseph Mezrich, 212.667.9316,

The struggle for alpha

Note: Top chart shows cumulative average excess return (relative to the benchmark) in large-cap core funds based on quantitative methodologies (dark blue line) and large-cap core funds based on

fundamental methodologies (light blue line). Bottom chart shows excess return by year (relative to the benchmark) in large-cap core funds based on quantitative methodologies (dark blue bar) and large-cap

core funds based on fundamental methodologies (light blue bar).Red bar is the spread of excess returns between quant funds and fundamental funds. Currently, there are 20 funds in the quant core universe

and 44 funds in the fundamental core universe. Period of analysis is from January 2003 through 14 May 2012.

Source: Nomura Securities International, Inc, Russell, S&P, Bloomberg.

Quant vs. Fundamental Quant vs. Fundamental by year

4

-2

0

2

4

6

8

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Cu

mu

lati

ve e

xce

ss r

etu

rn (%

)

Quant vs. Fundamental

Dec 2010

Quant+50 bp in YTD

Fundamental +50 bp in YTD

Quant core funds

Fundamental core funds Dec 2011

Quant+153 bp in 2011

Fundamental -327 bp in 2011

-6

-4

-2

0

2

4

6

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Ex

cess

re

turn

(%)

Quant vs. Fundamental by year

Quant

Fundamental

Spread (Quant - Fundamental)

Joseph Mezrich, 212.667.9316,

Stock correlation collapses from record high

& bounces

Note: Shows 21-day stock correlation within sector, where the averages of all pair-wise stock correlations are calculated within GICS 10 sectors in Russell 1000

universe using 21-day total returns, and these correlations are averaged over all GICS 10 sectors. Period of analysis is from 5 January1987 through 11 May 2012.

Source: Nomura Securities International, Inc, Russell, IDC.

5

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.91

98

7

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

21-day stock correlation within sector in Russell 1000

Black Monday

Now

Greek debtLehmanbankrupcy

Gulf War

WorldComAsian financial crisis

LTCM

Sep 12011

Apr 182012

Joseph Mezrich, 212.667.9316,

Which correlation is more relevant for performance?

6

-0.1

-0.05

0

0.05

0.1

0.15

0.2

0.25

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

absolute factor return correlation (LHS) factor return correlation (RHS)

Note: Average pairwise 21-day correlation of factor returns using 22 representative factor returns shown in blue. Average pairwise 21-

day correlation of factor return magnitudes shown in red. Period of analysis is from 2 January 1987 through 22 March 2012.

Source: Nomura Securities International, Inc., S&P, Russell, I/B/E/S, Compustat, IDC.

Joseph Mezrich, 212.667.9316,

Factor magnitude correlation reflects diversity

shown by PCA analysis

7

Note: Shows weight of first principal component based on 21-day PCA using 22 representative factor returns (dark blue line) together with 21-day pair-wise absolute

factor correlation based on 22 representative factor returns in Russell 1000 universe (light blue line). Period of analysis is from 30 April 1993 through 11 May 2012.

Source: Nomura Securities International, Inc., S&P, Russell, I/B/E/S, Compustat, IDC.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0

10

20

30

40

50

60

70

80

901

99

3

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Factor m

agnitu

de

corre

lation

We

igh

t o

f 1

st p

rin

cip

al c

om

po

ne

nt

(%)

Weight of 1st principal component based on 21-day PCA

21-day factor magnitude correlation

Joseph Mezrich, 212.667.9316,

Book/Price & 1-Year Price Momentum

Correlation with Default Risk

8

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8M

ar-9

3

Oct

-93

May

-94

Dec

-94

Jul-9

5

Feb-

96

Sep-

96

Apr-

97

Nov

-97

Jun-

98

Jan-

99

Aug-

99

Mar

-00

Oct

-00

May

-01

Dec

-01

Jul-0

2

Feb-

03

Sep-

03

Apr-

04

Nov

-04

Jun-

05

Jan-

06

Aug-

06

Mar

-07

Oct

-07

May

-08

Dec

-08

Jul-0

9

Feb-

10

Sep-

10

Apr-

11

Nov

-11

Corr

elat

ion

wit

h D

efau

lt Ri

sk

1 Year Price Momentum Book/Price

Is this a picture of diversification?

Note: Chart shows cross sectional correlation between default risk and 1-year price momentum and B/P. As of Dec 31 2011 Universe is Russell 1000.

Source: Nomura Securities International, Inc., Compustat, I/B/E/S, IDC, Russell.

Joseph Mezrich, 212.667.9316,

-0.7

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0

0.1

0.21

98

3

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Ran

k C

orr

ela

tio

n

B/P-Momentum

9

Book/Price & 1-Year Price Momentum

Cross sectional correlation

Is this a picture of diversification?

Note: Chart shows cross sectional correlation between B/P and 1-year price momentum and B/P. Universe is Russell 1000. The latest data is as of 30 April 2012.

Source: Nomura Securities International, Inc., Compustat, I/B/E/S, IDC, Russell.

Joseph Mezrich, 212.667.9316,

Stock correlation and factor magnitude correlation –

different paths

Note: Light blue line shows 21-day stock correlation within sector, where the averages of all pair-wise stock correlations are calculated within GICS 10 sectors in

Russell 1000 universe using 21-day total returns and these correlations are averaged over all GICS 10 sectors. Dark blue line shows the average of 21-day pair-wise

absolute factor correlation based on 22 representative factor returns in Russell 1000 universe. Period of analysis is from 30 April 1993 through 11 May 2012.

Source: Nomura Securities International, Inc, Russell, S&P, Bloomberg.

10

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

21-d

ay c

orr

ela

tio

nFactor magnitude correlation vs. Stock correlation

21-day stock correlation within sectors

21-day factor magnitude correlation

Joseph Mezrich, 212.667.9316,

Quant performance depends on factor correlation

Note: Shows average 12-month rolling excess return of quant core funds relative to their benchmarks (dark blue line) together with the average of one-year

(252-day) pair-wise absolute factor correlation based on 22 representative factor returns in Russell 1000 universe (light blue line). Thinner lines are 12-

month moving average of each line. Currently, there are 20 funds in the quant core universe. Period of analysis is from January 2000 through 14 May 2012.

Source: Nomura Securities International, Inc, Bloomberg, Compustat, I/B/E/S, Russell, S&P and IDC.

11

0.15

0.25

0.35

0.45

0.55

0.65

-4

-3

-2

-1

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Factor m

agnitu

de

corre

lation

base

d o

n o

ne

year (%

)

On

e-y

ear

ro

llin

g al

ph

a o

f q

uan

t co

re f

un

ds

(%)

Quant fund alpha and factor magnitude correlation

One-year rolling alpha of quant core funds

One-year factor magnitude correlation

Joseph Mezrich, 212.667.9316,

Fundamental performance was once much better

Note: Shows 6-month rolling excess return of fundamental core funds (dark blue line). Last data points are as of 14 May 2012.

Source: Nomura Securities International, Inc, Bloomberg, Compustat, IDC, Russell.

12

-4

-3

-2

-1

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

6-m

on

th a

lph

a o

f fu

nd

amen

tal

fun

ds

(%)

Alpha of fundamental funds

6-month alpha of fundamental core funds

Joseph Mezrich, 212.667.9316,

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

-4

-2

0

2

4

6

8

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

6-m

on

th sto

ck corre

lation

with

in se

ctor

6-m

on

th a

lph

a o

f fu

nd

amen

tal

fun

ds

(%)

Alpha of fundamental funds and stock correlation

6-month alpha of Fundamental funds

6-month Stock correlation

Something changed

Fundamental performance depends on stock correlation

Note: Shows 6-month rolling excess return of fundamental core funds (dark blue line) and 126-day pair-wise stock correlation within sector in Russell

1000 (light blue line). Last data points are as of 14 May 2012.

Source: Nomura Securities International, Inc, Bloomberg, Compustat, IDC, Russell.

13

Joseph Mezrich, 212.667.9316,

Stock correlation

and the growth of systemic risk

14

Joseph Mezrich, 212.667.9316,

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Black Monday

Asian financial crisis

Lehmanbankrupcy

Now

Chinainflationconcern

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Japan earthquake

Lehmanbankruptcy

Black Monday

Now

Gulf War

Yamaichi bankruptcy

Quick rise of Yen rate

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Black Monday

Now

Greek debtLehmanbankrupcy

Gulf War

WorldComAsian financial crisis

LTCM

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Black Monday

Soviet coup Lehmanbankrupcy

Greek debt

Now

Stock correlation around the globe and the trend of

increasing stock correlation

Note: Shows 21-day stock correlation within sector, where the averages of all pair-wise stock correlations are calculated using 21-day total returns within

the 10 GICS sectors in the Russell 1000 (US), MSCI Europe (Europe) and MSCI Asia Pacific ex Japan (Asia) and within the 10 QUICK sectors in the

TOPIX 500 (Japan), and these correlations are averaged over all 10 sectors. Period of analysis is from 2 January1987 through 11 May 2012.

Source: Nomura Securities International, Inc., Russell, MSCI, IDC, S&P, Exshare

US Japan

Europe Asia

15

Joseph Mezrich, 212.667.9316,

Stock Correlation, now a product of sector correlation?

Note: Shows the average of within-sector stock correlation (top panel) and the average correlation

among 10 GICS sectors (middle panel). Bottom panel is the overlay of the top and bottom panels.

The panel on the right shows the spread between sector correlation and stock correlation. Universe

is Russell 1000.. Data from March 31, 1987 through May 15, 2012

Source: Nomura Securities International, Inc., Compustat, I/B/E/S, IDC, Russell.

28

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Average correlation of stocks within sectors

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Average correlation of sectors Average correlation of stocks within sectors

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9Average correlation of sectors

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Spread between Sector Correlation and Stock Correlation

Joseph Mezrich, 212.667.9316,

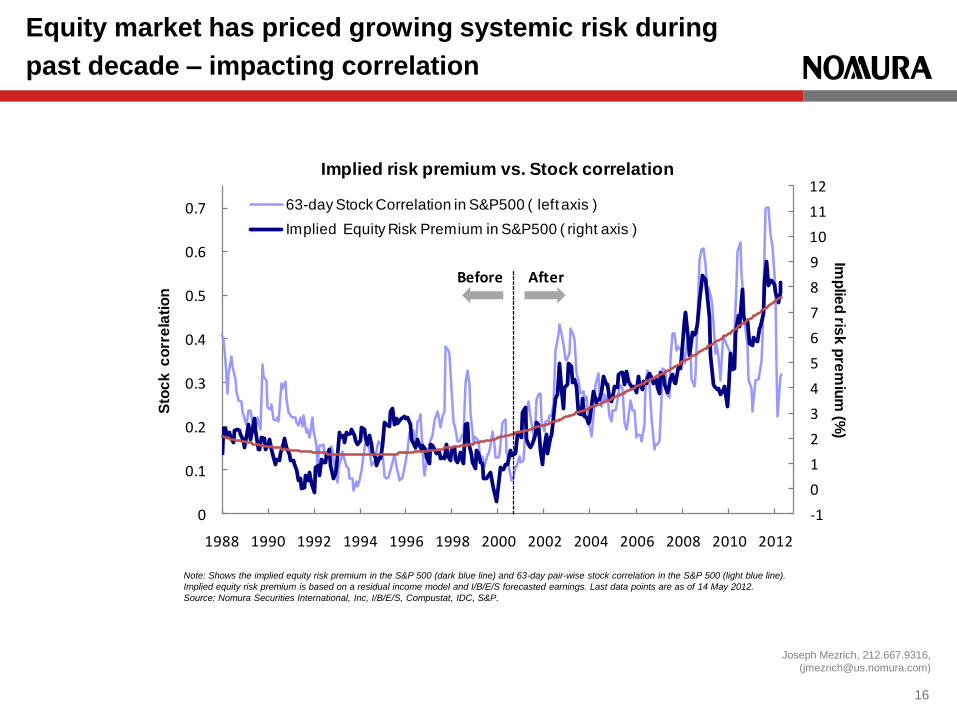

Equity market has priced growing systemic risk during

past decade – impacting correlation

Note: Shows the implied equity risk premium in the S&P 500 (dark blue line) and 63-day pair-wise stock correlation in the S&P 500 (light blue line).

Implied equity risk premium is based on a residual income model and I/B/E/S forecasted earnings. Last data points are as of 14 May 2012.

Source: Nomura Securities International, Inc, I/B/E/S, Compustat, IDC, S&P.

16

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Imp

lied

risk

pre

miu

m (%

)

Sto

ck

co

rre

lati

on

63-day Stock Correlation in S&P500 ( left axis )

Implied Equity Risk Premium in S&P500 ( right axis )

AfterBefore

Implied risk premium vs. Stock correlation

Joseph Mezrich, 212.667.9316,

Equity market has priced growing systemic risk during

past decade – impacting correlation

Note: Top chart shows the implied equity risk premium in the S&P 500 (dark blue line) and 63-day pair-wise stock correlation in the S&P 500 (light blue

line), while bottom chart shows the implied equity risk premium (dark blue line) and VIX (implied volatility in one-month S&P 500 options, light blue line).

Implied equity risk premium is based on a residual income model and I/B/E/S forecasted earnings. Last data points are as of 14 May 2012.

Source: Nomura Securities International, Inc, I/B/E/S, Compustat, IDC, S&P. 17

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Imp

lied

risk

pre

miu

m (%

)

Sto

ck

co

rre

lati

on

63-day Stock Correlation in S&P500 ( left axis )

Implied Equity Risk Premium in S&P500 ( right axis )

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

0

10

20

30

40

50

60

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Imp

lied

risk

pre

miu

m (%

)

Imp

lie

d

vo

lati

lity

(%

)

Implied Volatility in one-month S&P500 option ( VIX, left axis )

Implied Equity Risk Premium in S&P500 ( right axis )

AfterBefore

Implied risk premium vs. Stock correlation

Implied risk premium vs. Implied volatility

Joseph Mezrich, 212.667.9316,

Disconnect – Stocks vs. bonds & macro

17

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

4

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Imp

lied

10

-year in

flation

rate (%

)

23

26

29

32

35

38

41

44

47

50

53

56

59

62

65

-7-6-5-4-3-2-10123456789

101112131415

2004 2005 2006 2007 2008 2009 2010 2011 2012

ISM M

anu

facturin

g PM

I Ind

ex

Imp

lied

lon

g-te

rm e

arn

ings

gro

wth

rat

e (

%)

Implied long-term earnings growth rate

ISM Manufacturing PMI Composite Index

Average long-term earnings growthsince World War II ( 7.1% )

Implied 10-year inflation rate

Implied earnings growth, implied inflation and ISM Manufacturing PMI

Note: Shows the implied long-term earnings growth (LTG) of S&P500 (dark blue line) and implied 10-year inflation rate (light blue line).

Implied LTG (from FY1 to FY5) is derived by inputting expected equity risk premium in Duke University’s CFO survey, based on a residual

income model. Equity risk premium since March 2012 is estimated by linear model using VIX and previous month’s risk premium. Implied

inflation rate is calculated by subtracting the real yield of the inflation- linked maturity from the yield of the closest nominal Treasury maturity.

Last data points are as of 14 May2012.

Source: Nomura Securities International, Inc, Graham and Harvey (2012), I/B/E/S, S&P, Compustat, IDC, Bloomberg.

Joseph Mezrich, 212.667.9316,

Factor failure –

Momentum & revisions meet reg FD

18

Joseph Mezrich, 212.667.9316,

Momentum worked consistently for sixty years,

and then …

Note: Cumulative monthly factor returns to 12-month momentum (decile spreads) since 1940. The portfolios are constructed monthly using NYSE prior (2-12) return decile

breakpoints. Universe is all NYSE, AMEX, and NASDAQ stocks. Analysis based on data from January 1940 to December 2009. Transaction costs not considered.

Source: Kenneth R. French’s website (http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html, Nomura Securities International Inc.

0

200

400

600

800

1,000

1,200

1,400

1940

1943

1946

1949

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

Cum

ula

tive

m

onth

ly r

etu

rns (

%)

1 Year Momentum since 1940

19

Joseph Mezrich, 212.667.9316,

0

20

40

60

80

100

120

140

160

1980

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Cu

mu

lati

ve

mo

nth

ly r

etu

rns,

%

Revision long alpha

Revision short alpha

0

50

100

150

200

250

300

1980

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Cu

mu

lati

ve

mo

nth

ly r

etu

rns,

% Revision

Is price momentum permanently damaged?

Note: Based on analyst up down revisions (number of FY1 I/B/E/S up estimates minus number of down estimates divided by total number of estimates). Top panel shows long-side

alpha (blue line, return of the highest-ranked decile minus the return of the market, Russell 1000) and short-side alpha (red line, market return minus the lowest-ranked decile return).

Bottom panel shows the factor return of up down revisions (long-side alpha plus short alpha), excluding transaction costs. Universe is Russell 1000. Last data as of 2/28/2010.

Source: Nomura Securities International Inc., Compustat, I/B/E/S, Russell, and IDC.

Impact of estimate revisions diminished due to Reg FD

1 year price momentum factor return Estimate revisions factor return

0

50

100

150

200

250

1978

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Cu

mu

lati

ve

mo

nth

ly r

etu

rns,

%

1 year PM long alpha

1 year PM short alpha

0

50

100

150

200

250

300

350

400

1978

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Cu

mu

lati

ve

mo

nth

ly r

etu

rns,

%

1 Year Price Momentum

20

Joseph Mezrich, 212.667.9316,

-50

0

50

100

150

200

250

300

350

-50

0

50

100

150

200

250

300

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

1 y

r P

M:

Cu

mu

lati

ve

Mo

nth

ly R

etu

rns

, %

Re

vis

ion

: C

um

ula

tiv

e M

on

thly

Re

turn

s,

%

Revision

1yrPM

10/2000 when Reg FD was implemented

The world changed around 2000

Note: Shows returns to analyst up down revisions (blue line, number of FY1 I/B/E/S up estimates minus down estimates divided

by total number of estimates) and returns to one-year price momentum (red line, last twelve months’ returns minus last month’s),

excluding transaction cost. Universe is Russell 1000. Last data as of 2/28/2010. Transaction costs are not considered.

Source: Nomura Securities International Inc., Russell, IDC.

The momentum-revisions coupling conundrum

21

Joseph Mezrich, 212.667.9316,

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

0.71

98

4

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Ran

k C

orr

ela

tio

n

Rank Correlation between B/P(predicted LTG) and Beta

B/P and Beta

Predicted LT growth and Beta

Regime shift in market risk of B/P and

predicted LT growth

Note: Shows a history of rank correlation between B/P and beta (dark blue line) and rank correlation between predicted long-term earnings growth and beta

(light blue line). Universe is Russell 1000. Period of analysis is from November 1983 through April 2012.

Source: Nomura Securities International Inc., Compustat, I/B/E/S, Russell, and IDC.

24

Joseph Mezrich, 212.667.9316,

-4

-3

-2

-1

0

1

2

3

4

5

6

7

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

Z-sc

ore

d d

isp

ers

ion

in

val

ue

fac

tor

Dispersion in value factors

Sales/Price Predicted E/P

EBITDA/EV Dividend Yield

E/P B/P

Spread in value factor dispersion – out of sync

over the past decade

Note: Shows de-trended and normalized dispersion of value factors (predicted E/P, E/P, B/P, dividend yield, Sales/Price, and EBITDA/EV) across the Russell 1000 stocks.

The dispersion of value factors is calculated by Median Absolute Deviation (MAD) / Median. Period of analysis is from January 1982 through December 2011.

Source: Nomura Securities International, Inc, Russell, Compustat, I/B/E/S, IDC.

25

Joseph Mezrich, 212.667.9316,

-0.4 -0.2 0 0.2 0.4

Predicted LT GrowthBeta

5 Year EPS Growth1 Year Price Momentum

CapEx/SalesUp to Down Revisions

1 Year Dividend GrowthPEG

Market Cap (Small - Large)Analyst Coverage

ROEEstimate Dispersion

1 Mon. Price ReversalE/P

Debt/EquityDividend Yield

Share BuybacksPredicted E/P

Earnings Quality (Accruals)EBITDA/EV

B/P

(i) 1985 - 1999

-0.4 -0.2 0 0.2 0.4

Predicted LT GrowthBeta

CapEx/Sales5 Year EPS Growth

Default RiskMarket Cap (Small - Large)

Analyst CoverageEstimate Dispersion

1 Mon. Price ReversalPEG

1 Year Dividend GrowthB/P

Up to Down Revisions1 Year Price Momentum

Dividend YieldEarnings Quality (Accruals)

Debt/EquityEBITDA/EV

Share BuybacksPredicted E/P

E/PROE

(ii) 2000 - 2005

-0.4 -0.2 0 0.2 0.4

B/PDefault RiskDebt/Equity

Estimate DispersionMarket Cap (Small - Large)Earnings Quality (Accruals)

BetaDividend Yield

EBITDA/EVPEG

1 Mon. Price ReversalPredicted E/P

Analyst CoverageCapEx/Sales

Predicted LT GrowthShare Buybacks

E/P5 Year EPS Growth

1 Year Dividend GrowthUp to Down Revisions

1 Year Price MomentumROE

(iii) 2006 - 2010

-0.4 -0.2 0 0.2 0.4

Default RiskBeta

Estimate DispersionMarket Cap (Small - Large)

B/PPEG

1 Year Dividend GrowthPredicted E/P

1 Mon. Price ReversalDebt/Equity

Predicted LT GrowthEarnings Quality (Accruals)

EBITDA/EVAnalyst Coverage

CapEx/SalesE/P

1 Year Price MomentumDividend Yield

Up to Down RevisionsShare Buybacks

ROE5 Year EPS Growth

(iv) 2011

Value

Growth

Value

Growth

Risk

Risk

Value vs. Growth were main drivers B/P migrated away from drivers

Value and Risk got mixed Risk dominated factor efficacies

First principal component loadings: paradigm shift

in “value vs. growth” over time

Note: Shows loadings of first principal component based on the performances of 22 representative factors for different periods: (i) January 1985 to December 1999,

(ii) January 2000 to December 2005, (iii) January 2006 to December 2010, and (iv) January 2011 to December 2011. For reasons of long-term data availability, the

analysis in the period (i) omits the default risk factor from our 22 representative factor (see Appendix B for factor definitions). Only period (iv), January 2011 to

December 2011, is based on daily factor performances, while other periods are based on monthly factor performances. Universe is Russell 1000.

Source: Nomura Securities International, Inc., Compustat, I/B/E/S, IDC, Russell. 26

Joseph Mezrich, 212.667.9316,

Factor Correlation with beta and default risk

Note: Shows factor score rank correlations with beta and default risk, as of December 31 2011. Yellow highlights indicate ten factors

with highest rank correlations, while blue highlights indicate ten factors with lowest rank correlations. Universe is Russell 1000.

Source: Nomura Securities International, Inc., Compustat, I/B/E/S, IDC, Russell.

Rank Correlation with Beta Rank Correlation with Default Risk

January 2012 January 2012

Beta 0.60

Default Risk 0.60

B/P 0.18 0.50

EPS Variability 0.49 0.50

EBITDA/Price 0.15 0.48

Estimate Dispersion 0.22 0.45

Sales/Price 0.18 0.40

Predicted E/P 0.21 0.39

EBITDA/EV 0.19 0.39

PEG 0.43 0.37

PEGY 0.38 0.36

Rank Correlation with Beta Rank Correlation with Default Risk

January 2012 January 2012

Gross Margin -0.12 -0.28

Dividend Payout Ratio -0.31 -0.30

5 Year EPS Growth -0.18 -0.33

ROE -0.08 -0.34

EBIT/WCPPE -0.16 -0.34

5 Year Dividend Growth -0.23 -0.35

Stable Growth -0.29 -0.41

ROIC -0.12 -0.41

ROA -0.12 -0.49

1 Year Price Momentum -0.31 -0.56

29

Joseph Mezrich, 212.667.9316,

Unintended bets - Risk off/Risk on/Risk Irrelevant

Note: Shows f actor returns against factors’ score rank correlation with default risk and beta. Universe is Russell 1000.

Source: Nomura Securities International, Inc., Compustat, I/B/E/S, IDC, Russell.

-15

-10

-5

0

5

10

-0.8 -0.6 -0.4 -0.2 0.0 0.2 0.4 0.6 0.8

Fact

or R

etur

n (%

)

Rank Correlation with Default Risk

Factor Return vs Correlation with Default Risk

-15

-10

-5

0

5

10

-0.4 -0.2 0.0 0.2 0.4 0.6 0.8

Fact

or R

etur

n (%

)

Rank Correlation with Beta

Factor Return vs Correlation with beta

Risk –on (Oct 2011)

-10

-5

0

5

10

15

20

-0.6 -0.4 -0.2 0.0 0.2 0.4 0.6 0.8

Fact

or R

etur

n (%

)

Rank Correlation with Default Risk

Factor Return vs Correlation with Default Risk

-10

-5

0

5

10

15

20

-0.4 -0.2 0.0 0.2 0.4 0.6 0.8

Fact

or R

etur

n (%

)Rank Correlation with Beta

Factor Return vs Correlation with beta

Risk – irrelevant(Oct 2005)

-6

-4

-2

0

2

4

-0.3 -0.2 -0.1 0.0 0.1 0.2 0.3 0.4

Fact

or

Ret

urn

(%)

Rank Correlation with Default Risk

Factor Return vs Correlation with Default Risk

-6

-4

-2

0

2

4

-0.4 -0.3 -0.2 -0.1 0.0 0.1 0.2 0.3 0.4 0.5

Fact

or

Ret

urn

(%)

Rank Correlation with Beta

Factor Return vs Correlation with beta

30

Joseph Mezrich, 212.667.9316,

Unintended bets - default (credit) risk has entered the room

Note: Shows R-squared of the regression of 52 factors (sector neutral) monthly return against their score rank correlation with

beta(blue line), and the default risk (red line) Period of analysis is January 1985 through Februrary 2012. Universe is Russell 1000.

Source: Nomura Securities International, Inc., Compustat, I/B/E/S, IDC, Russell.

31

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

R-s

qu

ared

market risk

default risk

Joseph Mezrich, 212.667.9316,

Price momentum, default risk and beta

Note: Shows monthly cumulative returns of factors one-year price momentum (blue line), default risk (high-low, red line) and beta (high-low,

green line). Universe is Russell 1000. Period of analysis is from March 1993 through December 2011. Transaction costs are not considered.

Source: Nomura Securities International, Inc., Compustat, I/B/E/S, IDC, Russell. 34

-100

-50

0

50

100

150

200

Ma

r-9

3

No

v-9

3

Jul-

94

Ma

r-9

5

No

v-9

5

Jul-

96

Ma

r-9

7

No

v-9

7

Jul-

98

Ma

r-9

9

No

v-9

9

Jul-

00

Ma

r-0

1

No

v-0

1

Jul-

02

Ma

r-0

3

No

v-0

3

Jul-

04

Ma

r-0

5

No

v-0

5

Jul-

06

Ma

r-0

7

No

v-0

7

Jul-

08

Ma

r-0

9

No

v-0

9

Jul-

10

Ma

r-1

1

No

v-1

1

Cu

mu

lati

ve

Mo

nth

ly F

act

or

Re

turn

s, % 1 Year Price Momentum

high default - low default

Beta

July 2007

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Ma

r-9

3

No

v-9

3

Jul-

94

Ma

r-9

5

No

v-9

5

Jul-

96

Ma

r-9

7

No

v-9

7

Jul-

98

Ma

r-9

9

No

v-9

9

Jul-

00

Ma

r-0

1

No

v-0

1

Jul-

02

Ma

r-0

3

No

v-0

3

Jul-

04

Ma

r-0

5

No

v-0

5

Jul-

06

Ma

r-0

7

No

v-0

7

Jul-

08

Ma

r-0

9

No

v-0

9

Jul-

10

Ma

r-1

1

No

v-1

1

Co

rre

lati

on

of m

om

en

tum

wit

h D

efa

ult

R

isk

and

Be

ta

Momentum with Default Risk Momentum with Beta

1

2

Joseph Mezrich, 212.667.9316,

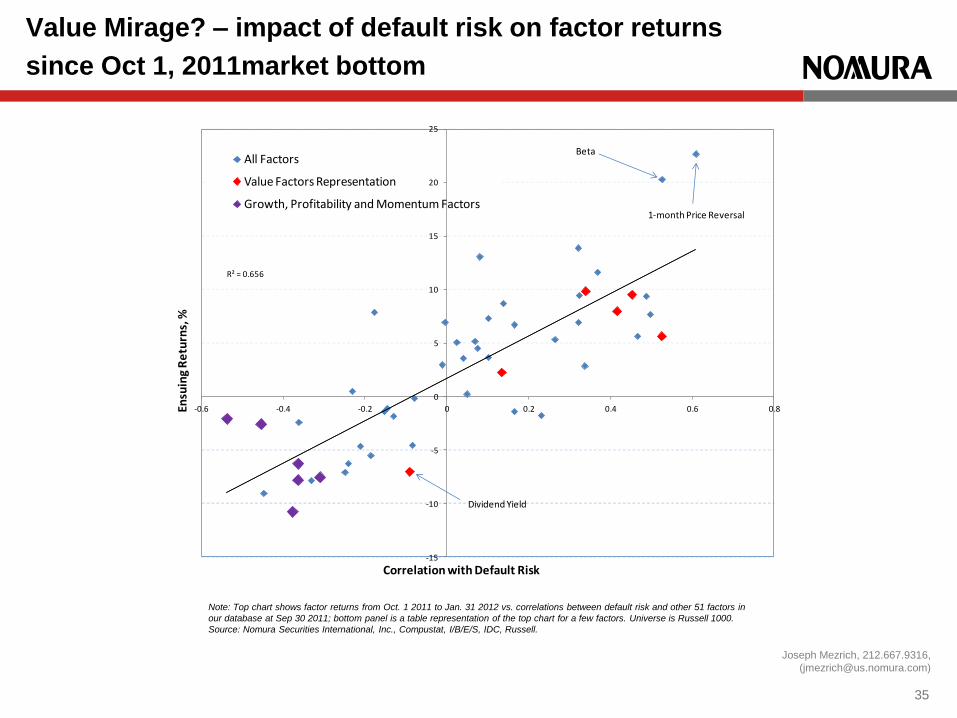

Value Mirage? – impact of default risk on factor returns

since Oct 1, 2011market bottom

Note: Top chart shows factor returns from Oct. 1 2011 to Jan. 31 2012 vs. correlations between default risk and other 51 factors in

our database at Sep 30 2011; bottom panel is a table representation of the top chart for a few factors. Universe is Russell 1000.

Source: Nomura Securities International, Inc., Compustat, I/B/E/S, IDC, Russell.

35

R² = 0.656

-15

-10

-5

0

5

10

15

20

25

-0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8Ensu

ing

Re

turn

s, %

Correlation with Default Risk

All Factors

Value Factors Representation

Growth, Profitability and Momentum Factors

Beta

1-month Price Reversal

Dividend Yield

Joseph Mezrich, 212.667.9316,

36

Impact of default risk on factor returns

between Oct 1, 2011 and March 31, 2012

R² = 0.4761

-15

-10

-5

0

5

10

15

20

25

30

-0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8

Ensu

ing

Retu

rns,

%

Correlation with Default Risk

All Factors

Value Factors Representation

Growth, Profitability and Momentum Factors

Beta

1-month Price Reversal

Dividend Yield

Value

Factors Correlation (9/30/2011) Returns (10/1/2011 - 3/31/2012)

B/P 0.53 4.55

SALES/PRICE 0.45 7.60

PREDICTED E/P 0.42 4.44

EBITDA/EV 0.34 2.04

E/P 0.13 -0.54

DIVIDEND YIELD -0.09 -10.12

Growth, Profitability

and Momentum Correlation (9/30/2011) Returns (10/1/2011 - 1/19/2012)

5 Year EPS Growth -0.38 -11.18

5 Year Dividend Growth -0.36 -10.14

ROE -0.36 -7.27

ROIC -0.45 -2.79

ROA -0.54 -3.63

1 Year Price Momentum -0.31 -5.43

Note: Top chart shows factor returns from Oct. 1 2011 to March. 31 2012 vs. correlations between default risk and other 51 factors in

our database at Sep 30 2011; bottom panel is a table representation of the top chart for a few factors. Universe is Russell 1000.

Source: Nomura Securities International, Inc., Compustat, I/B/E/S, IDC, Russell.

Joseph Mezrich, 212.667.9316,

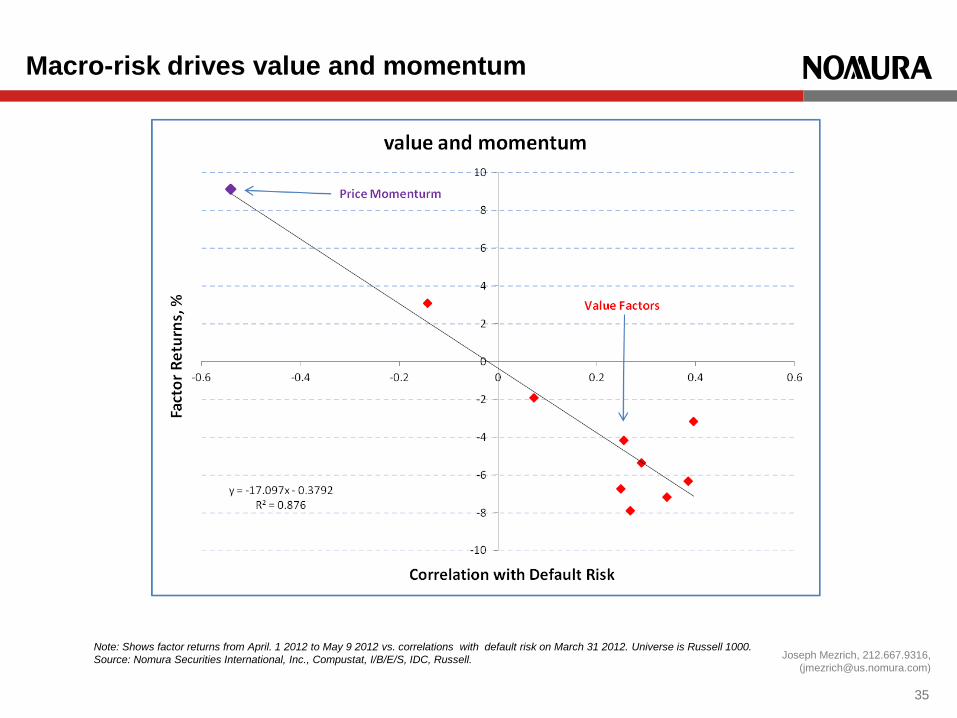

Macro-risk drives value and momentum

Note: Shows factor returns from April. 1 2012 to May 9 2012 vs. correlations with default risk on March 31 2012. Universe is Russell 1000.

Source: Nomura Securities International, Inc., Compustat, I/B/E/S, IDC, Russell.

35

Joseph Mezrich, 212.667.9316,

Where do changes of the past decade leave investors?

The hunt for alpha: Paradigm in motion

37

Joseph Mezrich, 212.667.9316,

Crossing correlation trends –

rising for stocks, flat for factors

Note: Light blue line shows 21-day stock correlation within sector, where the averages of all pair-wise stock correlations are calculated within GICS 10 sectors in

Russell 1000 universe using 21-day total returns and these correlations are averaged over all GICS 10 sectors. Dark blue line shows the average of all pair-wise

absolute factor correlation among 22 representative factor returns in Russell 1000 universe. Period of analysis is from 2 January 1991 through 11 May 2012.

Source: Nomura Securities International, Inc, Russell, S&P, Bloomberg.

38

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.81

99

1

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

21

-day

co

rre

lati

on

Factor magnitude correlation vs. Stock correlation

21-day factor magnitude correlation21-day stock correlation

?

Joseph Mezrich, 212.667.9316,

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

21

-day

co

rre

lati

on

Factor magnitude correlation vs. Stock correlation

21-day factor magnitude correlation21-day stock correlation

Crossing correlation trends –

rising for stocks, flat for factors

39

Note: Light blue line shows 252-day (one-year) stock correlation within sector, where the averages of all pair-wise stock correlations are calculated within GICS 10 sectors in

Russell 1000 universe using 252-day total returns and these correlations are averaged over all GICS 10 sectors. Dark blue line shows the average of all pair-wise absolute

factor correlation using 252-day factor returns of 22 representative factors in Russell 1000 universe. Period of analysis is from 2 January 1991 through 11 May 2012.

Source: Nomura Securities International, Inc., S&P, Russell, I/B/E/S, Compustat, IDC.

.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

On

e-y

ear

co

rre

lati

on

Factor magnitude correlation vs. Stock correlation

One-year stock correlation

One-year factor magnitude correlation

Joseph Mezrich, 212.667.9316,

Factor premium vs. stock alpha

A diversification opportunity?

40

Note: Shows one-year rolling excess return (relative to the benchmark) in large-cap core funds based on quantitative methodologies (dark blue line) and

large-cap core funds based on fundamental methodologies (light blue line). Currently, there are 20 funds in the quant core universe and 44 funds in the

fundamental core universe. Period of analysis is from January 2003 through 11 May 2012.

Source: Nomura Securities International, Inc., Bloomberg, S&P, Russell.

-4

-3

-2

-1

0

1

2

3

4

5

6

7

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

On

e-y

ear

ro

llin

g al

ph

a o

f co

re f

un

ds

(%)

Fundamental fund alpha vs. Quant fund alpha

One-year rolling alpha of fundamental core funds

One-year rolling alpha of quant core funds

Conclusion

– Wisdom of crowds or madness of crowds?

Joseph Mezrich, 212.667.9316,

Disclaimer

News and statistical data are aggregated from Bloomberg and other public sources including local newswires and are provided for informational purposes only.

This market commentary has been prepared by individual sales or trading personnel of Nomura Securities, International, Inc. ("Nomura" or the “Firm”). The opinions and comments contained herein

represent the views and observations of individual sales or trading personnel and are not a product of Nomura's Research Department. This market commentary (including any summaries and trading

calls) represents short-term ideas designed to take advantage of the most recent market fluctuations, which are subject to change without notice, and may differ from, or be inconsistent with the views of

Nomura research analysts or other sales and trading personnel within the Firm. The trading calls, in particular, are based on the observations by the Firm’s trading and sales personnel of various market

and trading data, including, but not limited to, trading volumes, oversold/undersold indicators and other technical information, market color, published news stories and Nomura research. More

information, however, is available upon request. Please contact your Nomura sales coverage person for more information on the items covered in this market commentary.

This material has been prepared or distributed by sales and trading personnel of Nomura Securities International, Inc. (“Nomura”) and is not a product of a Nomura research department.

This material is (1) for your information only; (2) not to be construed as an offer to sell or a solicitation of an offer to buy any security mentioned herein; and (3) based upon information that we consider

reliable, but we do not represent that it is accurate or complete, and it should not be relied upon as such. Opinions expressed are current opinions as of the date appearing on this material only and the

information, including the opinions contained herein, are subject to change without notice.

Complete copies of any research report referenced, summarized or excerpted in this message and related disclosures are available on the Nomura research website which can be accessed through the

link below. These reports may contain dated information and are sent for historical purposes only. They should not be relied upon in substitution for the exercise of independent judgment, are intended

for your use only and may not be transmitted to other parties.

Nothing herein shall form the basis of or be relied on in connection with any contract or commitment whatsoever. Neither Nomura nor any other person accepts any liability whatsoever for any loss

(howsoever arising and whether direct or consequential) from any use of the information contained herein or otherwise arising in connection herewith.

Nomura Research Website (http://www.nomuranow.com/research/globalresearchportallogin/login.aspx?ReturnUrl=research/globalresearchportal/Default.aspx)

Derivative investments require investors to assess several characteristics and risk factors that may not be present in other types of transactions. You should consider the specific return and risk profile

of a particular derivative investment before effecting, or agreeing to effect, any transaction. In reaching a determination as to the appropriateness of any proposed transaction, clients should undertake a

thorough independent review of the legal, regulatory, credit, tax, accounting and economic consequences of such action. The information presented has been obtained from or based upon sources

believed by the trader or sales person to be reliable, but none of Nomura or its employees, the trader or sales person represents or warrant its accuracy or completeness and is not responsible for losses

or damages arising out of errors, omissions or changes in market factors.

We do not provide legal, accounting or tax advice. In compliance with Internal Revenue Service Circular 230, we hereby notify you that any discussion of tax matters set forth herein was written in

connection with the promotion or marketing of the matters described herein and was not intended or written to be used, and cannot be used by any person, for the purposes of avoiding tax-related

penalties under federal, state or local tax law. Each person should seek legal, accounting and tax advice based on its particular circumstances from independent advisors.

Nomura and its affiliates may from time to time perform investment banking or other services (including acting as advisor, manager or lender) for or solicit investment banking or other business from,

companies mentioned herein. Nomura and its affiliates may make a market or deal as principal in the securities mentioned in this document or in options, futures, or other derivatives based thereon. In

addition, Nomura and its affiliates, shareholders, directors, officers and/or employees may from time to time have long or short positions in such securities or in options, futures, or other derivative

instruments based thereon.

No part of this material may be (i) copied, photocopied, or duplicated in any form, by any means, or (ii) redistributed without our prior express consent. Further information on any of the securities

mentioned herein may be obtained upon request. If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-

free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents

of this publication, which may arise as a result of electronic transmission. If verification is required, please request a hard-copy version.

Nomura Securities International, Inc. is a member of FINRA (http://www.finra.org/index.htm) and SIPC(http://www.sipc.org/).

This commentary has been prepared by a desk strategist and is NOT a product of the Research Department.

42

Nomura Securities International, Inc., New York

Quantitative Desk Strategies

This commentary has been prepared by a Nomura equities desk

strategist and is NOT a product of the Research Department.

STRICTLY PRIVATE AND CONFIDENTIAL

43