nj webfile nj telefile nj elf · 4 2002 nj charitable funds continued line 53 - new jersey —...

TRANSCRIPT

2002 Form NJ-1040 3

continued

In most cases, if you were a full-year New Jersey resident in 2002 and you filed a New Jersey resident incometax return in 2001, there’s an NJ FastFile option for you. There are no limitations on the amount of income youcan have, and you can file your homestead rebate application electronically, too. You’ll get your refund fasterwith NJ FastFile, and you can choose direct deposit for either your refund or homestead rebate check, or both.

Check the chart below to see which NJ FastFile option is best for you, then visit www.njfastfile.com or call1-800-323-4400.

NJ WebFile NJ TeleFile NJ ELFHow To File By computer…

Visit www.njfastfile.com and linkto our secure Web site to prepareyour return. Nothing to buy and nofiling fees.

By phone…Call 1-888-235-FILE (3453)toll-free

By computer…Use tax software you purchase orhave a tax preparer file your return.(You must file both Federal andState income tax returns.)

FilingStatus

Any filing status(must be same as last year)

Any filing status except“Married, filing separate return”(must be same as last year)

Any filing status

PersonalExemptions/Dependents

Exemption for Self ....................YesExemption for Spouse ...............YesAge 65 or Older ........................YesBlind or Disabled ......................YesDependent Children ..................YesOther Dependents......................YesDependents

Attending Colleges ...............Yes

Exemption for Self ....................YesExemption for Spouse ...............YesAge 65 or Older..........................NoBlind or Disabled .......................NoDependent Children...................YesOther Dependents.......................NoDependents*

Attending Colleges ...............Yes(*Only dependent children)

Exemption for Self ................... YesExemption for Spouse .............. YesAge 65 or Older........................ YesBlind or Disabled ..................... YesDependent Children.................. YesOther Dependents ..................... YesDependents

Attending Colleges .............. Yes

IncomeSources

Limited to:Wages; interest; dividends; netgains or income from disposition ofproperty; pensions and annuities;IRA withdrawals; gamblingwinnings; rents, royalties, patents,and copyrights; other income

Note: Number of transactions ineach category also limited.

Limited to:Wages, interest ($2,500 or less),and dividends ($2,500 or less)

All sources of income

Deductions All deductions you are eligible for Property tax deduction only All deductions you are eligible for

Credits All credits you are eligible to claim(including credit for taxes paid toother jurisdictions)

Limited to property tax credit, NJearned income tax credit, excessUI/HC/WD or disability insurancecontributions

All credits you are eligible to claim(including credit for taxes paid toother jurisdictions)

Payments All payment types includingwithholdings, estimated taxpayments, credit from last year’sreturn, payment made withextension application

Limited to withholdings on W-2s All payment types includingwithholdings, estimated taxpayments, credit from last year’sreturn, payment made withextension application

HomesteadRebate

All eligible homeowners andtenants

All eligible homeowners andtenants

All eligible homeowners andtenants

2002 NJ Charitable Funds4

continued

Line 53 - New Jersey — Endangered Wildlife FundHelp keep NJ’s wildlife in our future! Over 60 endangered and threatened species struggle for survival in NJ,the most densely populated state in the nation – and each day brings them closer to extinction. You can help ourbiologists stem the tide of species and habitat loss. Contributions from compassionate people like you go towardconservation, research, restoration, and education – real dollars that help the Endangered & Nongame SpeciesProgram protect imperiled animals such as the bald eagle, bobcat, and bog turtle, plus over 400 other nongamespecies in NJ. We receive no state-dedicated funding and rely on your support, so this year please “Check Off for Wildlife.” Thank you!

Please visit www.NJFishandWildlife.com/ensphome.htm for more info. For a free subscription to our newsletter, please write to ConserveWildlife News, ENSP, PO Box 400, Trenton, NJ 08625, call 609-984-6012, or e-mail [email protected]

Line 54 - New Jersey — Children’s Trust Fund…………… to prevent child abuseHelp protect New Jersey’s children! Every year thousands of children in New Jersey are neglected and abused.The Children’s Trust Fund works in all 21 counties to help prevent these terrible tragedies by supporting:

• home visiting programs for parents of newborns• respite care for children with special needs and their families• parent education and support groups.

We rely on your support. Every dollar you contribute goes directly to communities throughout New Jersey toprevent child abuse and neglect. Help children in New Jersey have a safe and healthy childhood - Support the Children’s Trust Fund.Want more information? Contact: Children’s Trust Fund, PO Box 711, Trenton, NJ 08625-0711Phone: 609-633-3992 Web: http://www.state.nj.us/humanservices/njcap.html

Line 55 - New Jersey — Vietnam Veterans’ Memorial Fund

“To Remember, To Heal, To Honor”

Your support honors 1,556 New Jerseyans whose names are engraved on the Memorialand helps us teach future generations about this unique time in our nation’s history at theVietnam Era Educational Center.

For more information, write: New Jersey Vietnam Veterans’ Memorial, PO Box 648,Holmdel, NJ 07733 or call: 1-800-648-8387. Visit us on the Web at http://www.njvvmf.org.

Line 56 - New Jersey — Breast Cancer Research Fund

YOUR STATE TAX REFUND TODAY HELPS OUR DAUGHTERS TOMORROW

Join the fight against breast cancer and help New Jersey based researchers find a cure nowso our daughters won’t have to fight this disease in the future. 100% of your donationsupports research relating to the prevention, screening, treatment, and cure of breast cancer.For further information, please contact: The New Jersey Commission on Cancer Research,PO Box 360, 28 West State Street, Rm 505, Trenton, NJ 08625-0360, Phone: 609-633-6552.Web: www.state.nj.us/health

Line 57 - New Jersey — U.S.S. New Jersey Educational Museum FundBATTLESHIP NEW JERSEYNew Jersey’s namesake Battleship would appreciate your continued support. Your contribution will be used to support theworld-class Educational Museum as a tribute to Veterans of all of the Armed Forces.

For more information contact:Battleship New Jersey Foundation, Inc.1715 Hwy 35, Middletown, NJ 07748Phone: 732-671-6488 Web: http://www.battleshipnj.org E-mail: [email protected]

2002 NJ Charitable Funds 5

continued

Line 58 - New Jersey — Other Designated Contribution01 - Drug Abuse Education Fund - THE EPIDEMIC OF DRUG ABUSE NEEDSYOUR HELP! Your contribution helps New Jersey children receive valuable education from highlytrained uniformed law enforcement officers throughout the State in providing drug abuse educationprograms. Research has shown that the more resistance education children receive, the more likely theywill be drug free. The monies raised will help maintain K-6 curricula and increase program activity toMiddle School and High School students as well as parents.

For more information contact D.A.R.E. New Jersey at 292 Prospect Plains Rd., Cranbury, NJ 08512or call 1-800 DARENJ1. Web address: http://www/darenj.org.

Line 58 - New Jersey — Other Designated Contribution02 - Korean Veterans’ Memorial Fund“To Honor, To Educate, To Recognize, To Commemorate”

Your support to the Korean War Memorial in Atlantic City honors all the New Jerseyans whoserved and especially the more than 827 soldiers who died during the Forgotten War. We needto inform future generations of the past so that no one ever forgets these men and women.Your contribution will be used to maintain this place of honor.

For more information, write: Korean War Memorial, c/o Dept. of Military and Veterans Affairs, PO Box 340, Eggert Crossing Road,Trenton, NJ 08625-0340. Phone: 609-530-7049. http://www.state.nj.us/military/korea/

Line 58 - New Jersey — Other Designated Contribution03 - Organ and Tissue Donor Awareness Education FundMore than 2,300 critically ill New Jerseyans from all walks of life — parents, children, siblings,grandparents — are waiting for life-saving organ transplants. Each day 17 people on waiting listswill die due to the lack of donated organs. But you have the power to donate life. Just one organand tissue donor can save up to 8 lives and enhance the health of 75 others. Your support will helpraise awareness of this drastic need for organ and tissue donors. Begin today by checking off line58 to help fund organ and tissue donor education awareness in New Jersey.For more information, call 1-800-SHARE-NJ or visit www.sharenj.org

Line 58 - New Jersey — Other Designated Contribution04 - NJ-AIDS Services Fund

New Jersey currently ranks fifth in the country in total cases of HIV infection with anestimated 50,000 people living with HIV/AIDS. Your donation will be used for prevention,education, treatment and research.

For more information write to: New Jersey AIDS Services Fund, c/o Positive Connection,1514 Palisade Avenue, Union City, NJ 07087, or call 1-973-485-6596.

Line 58 - New Jersey — Other Designated Contribution05 - Literacy Volunteers of America – New Jersey Fund“Literacy is the key to personal freedom.”

Millions of adults in New Jersey cannot read, write, or speak English well enough to successfully complete everydaytasks. Since 1979, Literacy Volunteers of America - New Jersey (LVA-NJ) has been providing leadership training,technical assistance, and management support to our network of local affiliates. These programs in turn offerpersonalized, one-to-one tutoring to adults at the lowest levels of literacy. We constantly strive to enhance andexpand our efforts so that more and more adults may know the joy of reading and the freedom that it brings.

For more information call 908-203-4582 or visit http://members.aol.com/lvanj

Contributions - continued

2002 Form NJ-1040 13

continued

FILING INFORMATION

♦ Your filing status and gross income determine whether you have to file a tax return.♦ Age is not a factor in determining whether a person must file. Even minors (including

students) and senior citizens must file if they meet the income filing requirements.♦ Gross income means taxable income after exclusions but before personal exemptions are

subtracted. It does not include nontaxable benefits. See page 23 to find out which typesof income are not taxable.

♦ Members of the Armed Forces see page 15 for additional information.

Use the following chart to determine whether you must file a tax return. This chart is a guide only and may notcover every situation. If you need assistance, contact the Division’s Customer Service Center (609-292-6400).

Who Must FileYou must file a New Jersey income tax return if–Your residency status is: your filing status is:

and your gross incomewas more than:

Full-Year Resident — File Form NJ-1040(Resident Return) as a full-year resident if:♦ New Jersey was your domicile (permanent legal residence) for the

entire year;

SingleMarried, filing separate return

$10,000(from all sources)

or

♦ New Jersey was not your domicile, but you maintained a permanent*home in New Jersey for the entire year and you spent more than 183days in New Jersey. (If you are a member of the Armed Forcesstationed here and New Jersey is not your domicile, you are not aresident under this definition.)

Married, filing joint returnHead of householdQualifying widow(er)

$20,000(from all sources)

Part-Year Resident — File Form NJ-1040(Resident Return) as a part-year resident if:You met the definition of resident for only part of the year.

SingleMarried, filing separate return

$10,000 from all sources(for the entire year)

NOTE: Both part-year resident (Form NJ-1040) and part-yearnonresident (Form NJ-1040NR) returns may have to be filedwhen a part-year resident receives income from New Jerseysources during the period of nonresidence.

Married, filing joint returnHead of householdQualifying widow(er)

$20,000 from all sources(for the entire year)

Nonresident — File Form NJ-1040NR(Nonresident Return) as a nonresident if:New Jersey was not your domicile, and you spent 183 days or less here;

or

SingleMarried, filing separate return

$10,000(from all sources)

New Jersey was not your domicile, you spent more than 183 days here,but you did not maintain a permanent* home here. Married, filing joint return

Head of householdQualifying widow(er)

$20,000(from all sources)

You may also be considered a nonresident for New Jersey incometax purposes if you were domiciled in New Jersey and you met allthree of the following conditions for the entire year:

♦ You did not maintain a permanent home in New Jersey; and♦ You did maintain a permanent home outside of New Jersey; and♦ You did not spend more than 30 days in New Jersey.

* A home (whether inside or outside of New Jersey) is not permanent if it is maintained only during a temporary or limited period forthe accomplishment of a particular purpose. Likewise, a home used only for vacations is not a permanent home.

Also File a Return if:♦ You had New Jersey income tax withheld from your wages and are due a refund.♦ You paid New Jersey estimated taxes for 2002 and are due a refund.♦ You are eligible for a New Jersey earned income tax credit and are due a refund.

2002 Form NJ-104014

continued

Other Filing InformationDomicile. A domicile is any place you re-gard as your permanent home—the placeto which you intend to return after a pe-riod of absence (as on vacation abroad,business assignment, educational leave,etc.). A person has only one domicile, al-though he or she may have more than oneplace to live. Once established, your dom-icile continues until you move to a newlocation with the intent to establish yourpermanent home there and to abandonyour New Jersey domicile. Moving to anew location, even for a long time, doesnot change your domicile if you intend toreturn to New Jersey.

A place of abode, whether inside or out-side of New Jersey is not permanent if itis maintained only during a temporarystay for the accomplishment of a particu-lar purpose (e.g., temporary job assign-ment). If New Jersey is your domicile,you will be considered a resident for NewJersey tax purposes unless you meet allthree conditions for nonresident status(see “Who Must File” on page 13). Like-wise, if New Jersey is not your domicile,you will only be considered a New Jerseyresident if you maintain a permanenthome and spend more than 183 days here.

Guidelines for Part-YearResidentsFiling Requirements. Any person whobecame a resident of this State or movedout of this State during the year is subjectto New Jersey income tax for that portionof the income received while a resident ofNew Jersey. Part-year residents mustfile a resident return and prorate allexemptions, deductions, and credits, aswell as the pension and other retire-ment income exclusions, to reflect theperiod covered by the return. A personwho receives income from a New Jerseysource while a nonresident must file aNew Jersey nonresident return.

If you were a New Jersey resident foronly part of the taxable year, you are sub-ject to the tax if your income for the entireyear exceeds $20,000 ($10,000 if filingstatus is single or married, filing separatereturn), even though the income reported

for your period of residence was belowthese thresholds. If the income receivedduring the entire year was $20,000 or less($10,000 if filing status is single or mar-ried, filing separate return), you must en-close a copy of your Federal income taxreturn or a statement to that effect if youdid not file a Federal return.

NOTE: If you derived any income from NewJersey sources during your period of non-residence, it may also be necessary to file aNew Jersey nonresident return. Anywithholdings should be allocated betweenthe resident and nonresident returns. Formore information, see Form NJ-1040NR,New Jersey nonresident return andinstructions.

Line 14 - Wages. You must determinefrom each W-2 you receive the portion ofyour “State wages, tips, etc.” that you

earned while you were a New Jersey resi-dent. If your W-2 indicates only wagesearned while you were a New Jersey resi-dent, use the amount from the “Statewages, tips, etc.” box. If your employerdid not separate your resident and non-resident wages on the W-2, you must pro-rate the “State wages, tips, etc.” amountfor the period of time you lived in NewJersey. Add the amounts reportable forthe period of New Jersey residency andplace the total on Line 14.

Do not include any W-2(s) where the totalW-2 income was derived from out-of-State sources during your period of non-residence.

Other Income. For interest, dividends,pensions, and other income, include onyour return only those amounts receivedwhile a resident of New Jersey. Part-year

AVOIDING COMMON MISTAKESCheck the following items to avoid delays in processing returns and refunds.

� Use the correct form. Form NJ-1040 should be used by part-year residents aswell as full-year residents. Use only a 2002 return for the 2002 tax year.

� Read the instruction booklet before completing the return.� File only original forms. The State is unable to scan photocopies of tax returns.� Use only blue or black ink when completing forms.

� Enter all numbers within the red boxes. Do not use dollar signs or dashes.� You may not report a loss on Form NJ-1040. Make no entry on lines where the

amount to be reported is zero or less, except for Line 41, Use Tax Due. If no usetax is owed, enter “0.00” on Line 41.

� Make no entry on unused lines.

� When rounding, enter zeros after the decimal point for cents.� Check name, address, social security number, and county/municipality code

for accuracy when using the label or writing information on the return.� Enter last name first when writing information on the tax return. This require-

ment differs from the Federal return.

� Fill in only one oval for your filing status.� Use “State wages” figure(s) from your W-2(s), not Federal wages figure(s). If

you received wages from sources outside New Jersey, this figure may need to beadjusted to reflect New Jersey tax law.

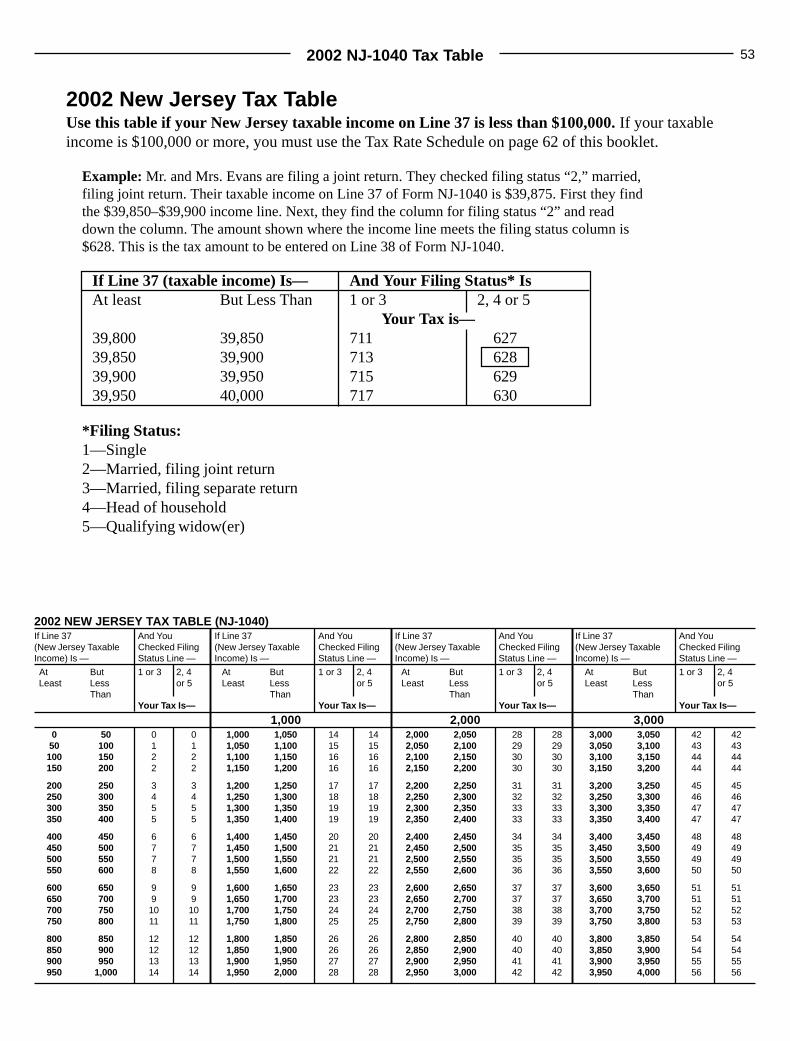

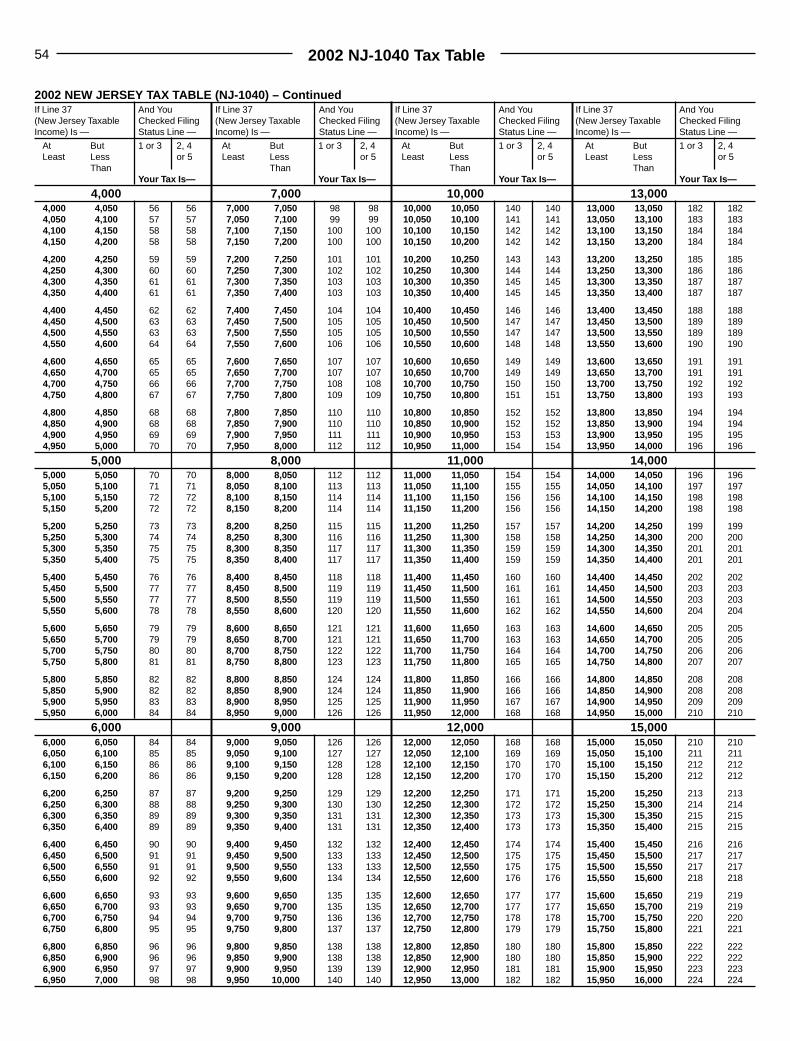

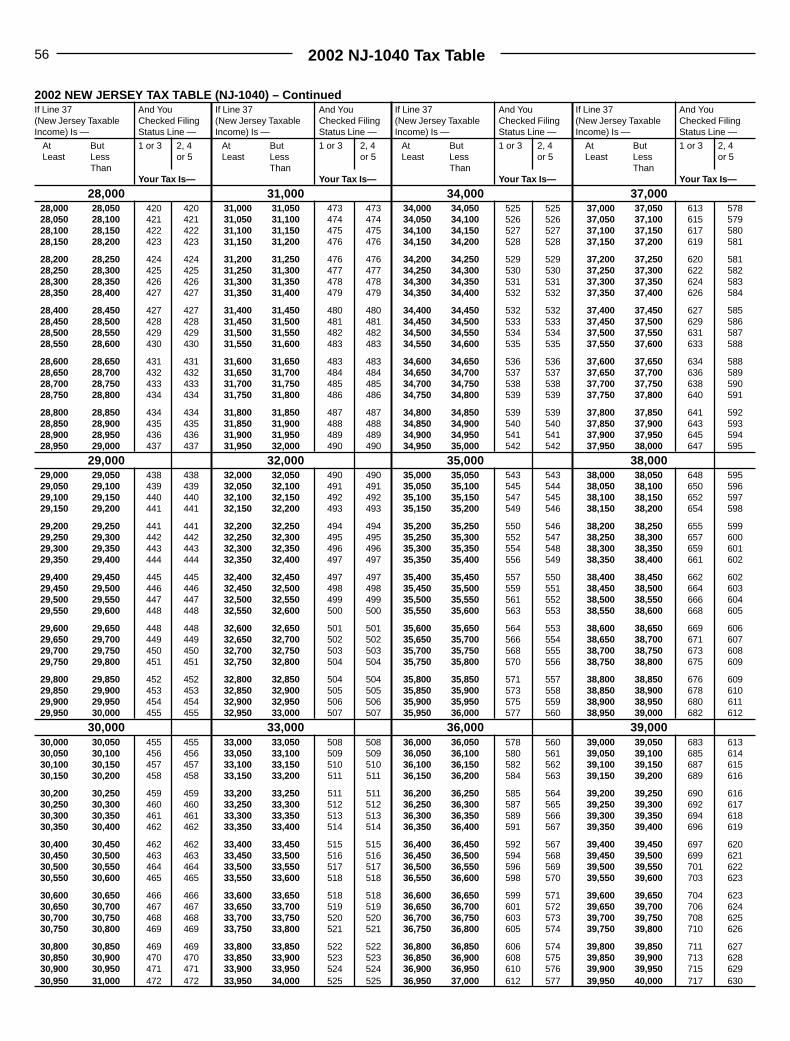

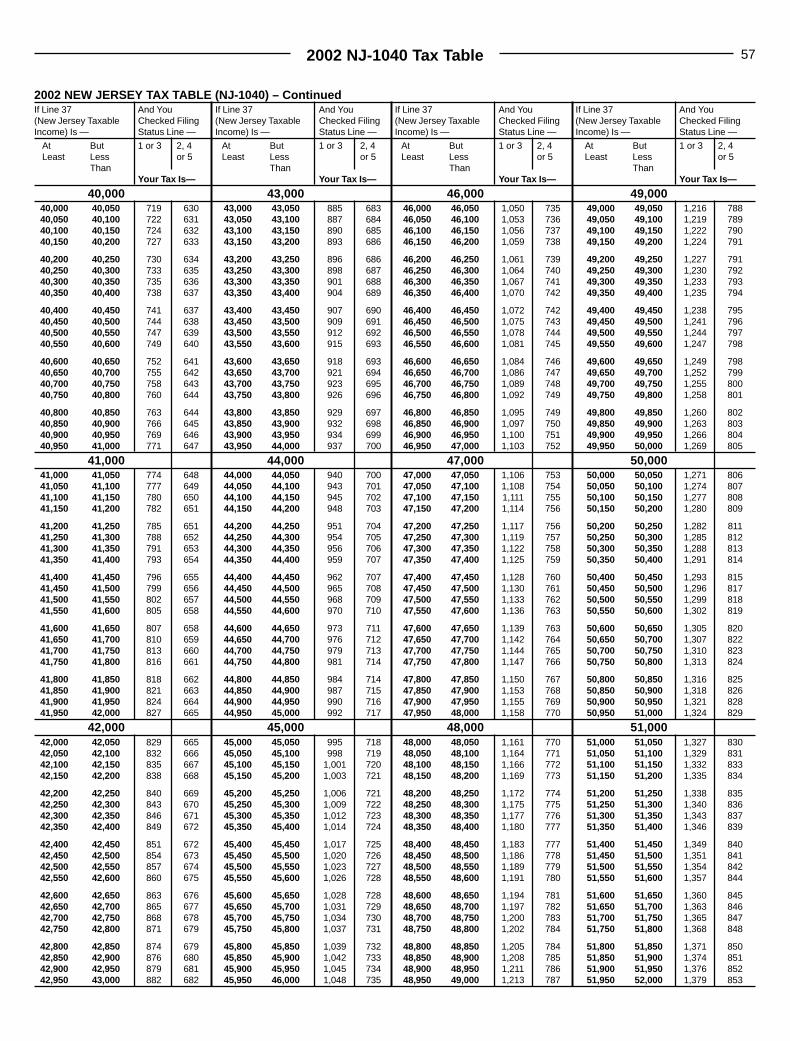

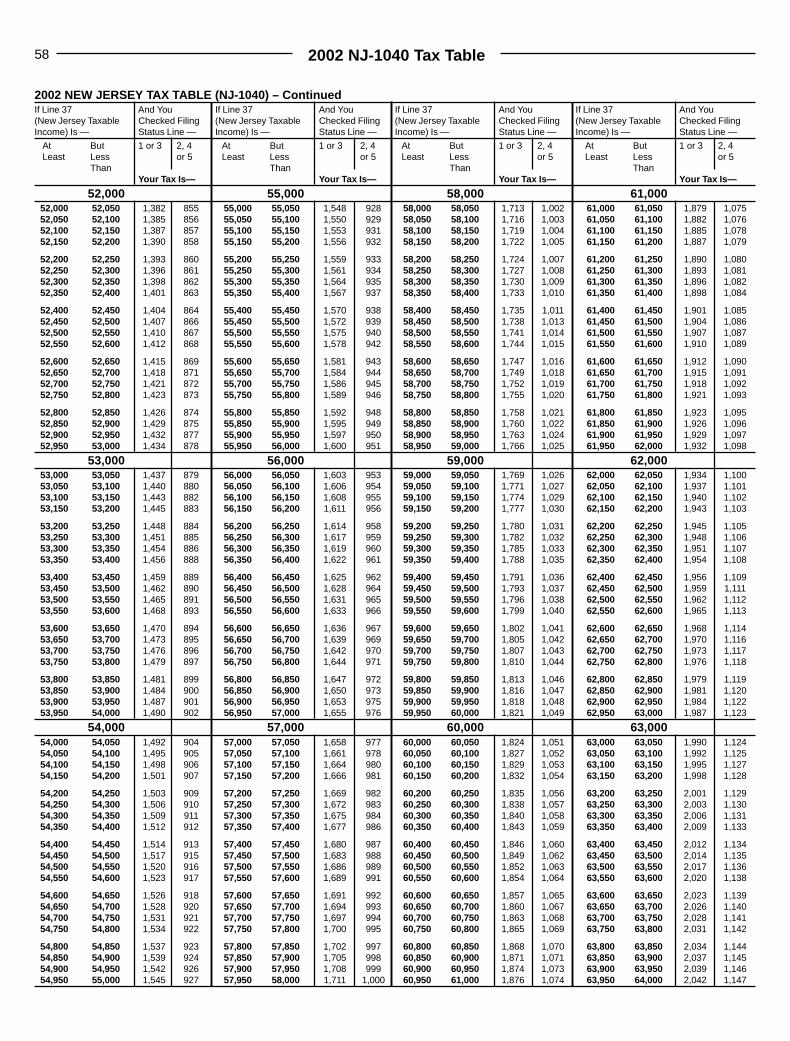

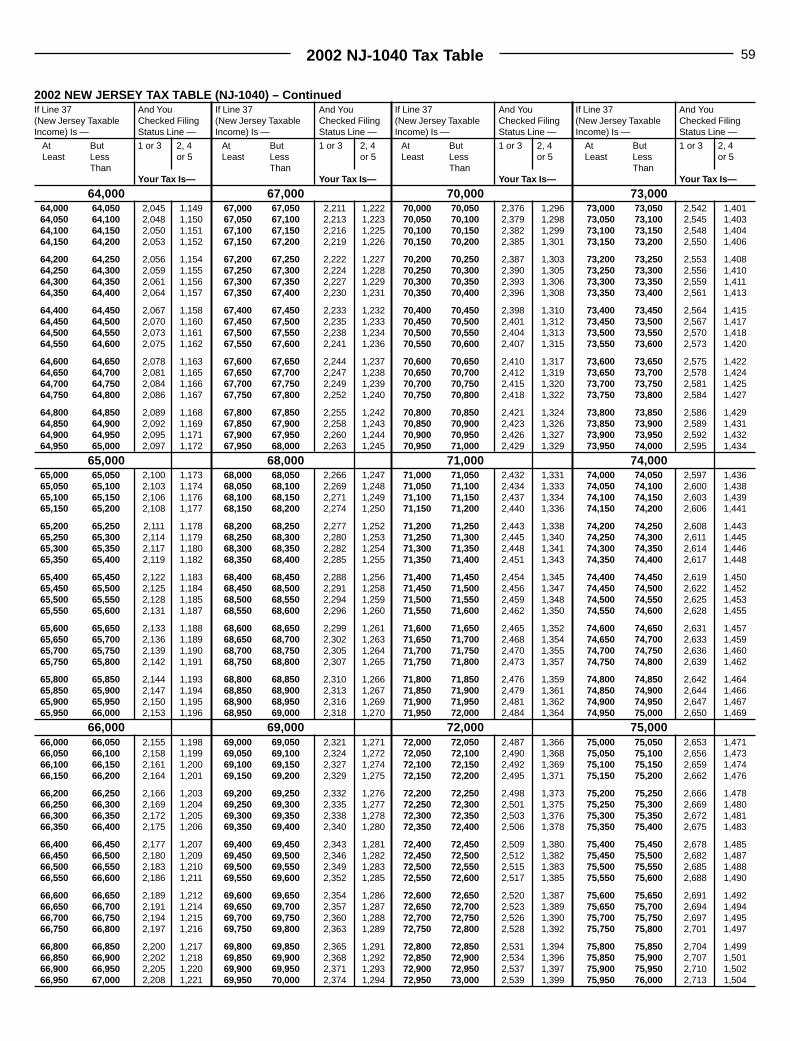

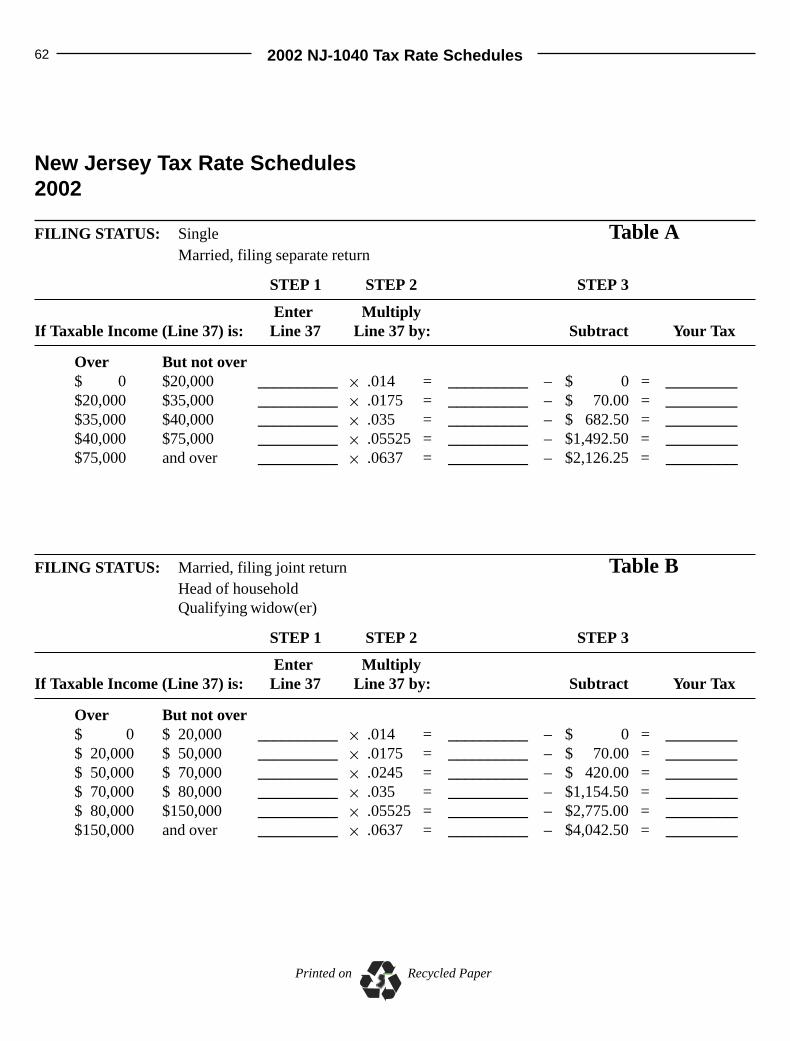

� Locate the correct column for your filing status in the Tax Table when calcu-lating your New Jersey tax liability on Line 38.

� Request a refund by completing Line 60.� Check your math.� Sign and date your return. Both spouses must sign a joint return.

� Keep a copy of your return and all supporting documents or schedules.� Changes or mistakes to your original return may be corrected by filing an

amended return. See page 19.

2002 Form NJ-1040 15

continued

resident partners and, in general, S corpo-ration shareholders must prorate the en-tity’s income based on the number of daysin the entity’s fiscal year that you were aresident divided by 365 (366 for leapyears). Partners and shareholders shouldrequest Tax Topic Bulletin GIT-9P, In-come from Partnerships, or GIT-9S,Income from S Corporations for instruc-tions on reporting distributive share ofpartnership income and net pro rata shareof S corporation income.

Line 19b - Pension Exclusion. If youqualify for the pension exclusion, proratethe exclusion by the number of monthsyou were a New Jersey resident. For thiscalculation 15 days or more is a month.

Line 28 - Other Retirement IncomeExclusion. Do not complete Worksheet Dfor the Other Retirement Income Exclu-sion (on page 32). Instead, total theearned income (wages, net profits frombusiness, partnership income, and S cor-poration income) you received for the en-tire year to determine whether or not youqualify for the exclusion.

Line 30c - Exemptions. Your total ex-emptions (Line 30c) must be proratedbased upon the number of months youwere a New Jersey resident. For this cal-culation 15 days or more is a month.

Lines 30a&b Mos. NJ Resident

12 = Line 30c×

Lines 31, 32, and 33 - Deductions. Youmay deduct medical expenses, qualifiedArcher medical savings account (MSA)contributions, health insurance costs ofthe self-employed, alimony and separatemaintenance payments, and qualifiedconservation contributions based on theactual amounts paid for the period of timeyou lived in New Jersey. Use WorksheetE on page 33 to determine the medical ex-pense deduction.

Line 36 - Property Tax Deduction. Youmay also be eligible to claim a deductionfor property taxes you paid, or rent con-stituting property taxes (18% of rent dueand paid) during your period of residency.When you do the calculation to determinewhether the deduction or credit is betterfor you, prorate the minimum tax benefit

of $50 ($25 if filing status is married, fil-ing separate return and you maintain thesame residence as your spouse) based onthe number of months you occupied yourNew Jersey residence. For this calculation15 days or more is a month. Use this pro-rated figure instead of the $50 figure ($25if filing status is married, filing separatereturn and you maintain the same resi-dence as your spouse) at Line 8, Sched-ule 1 or Line 5, Worksheet F.

Line 44 - Property Tax Credit. Youmust prorate the amount of any propertytax credit on Line 44 based on the numberof months you occupied your qualifiedNew Jersey residence. For this calculation15 days or more is a month.

�

Line 46 - New Jersey�������Earned Income TaxCredit. If you were a New

Jersey resident for only part of the taxableyear, and your gross income for the entireyear from all sources was $20,000 or less,you may qualify for a New Jersey earnedincome tax credit if you meet the othereligibility requirements. The amount ofyour credit must be prorated based uponthe number of months you were a NewJersey resident. For this calculation 15days or more is a month.

For more information, request Tax TopicBulletin GIT-6, Part-Year Residents.

Guidelines for MilitaryPersonnelResidents. A member of the ArmedForces whose home of record (domicile)is New Jersey when entering the serviceremains a resident of New Jersey for in-come tax purposes, and must file a resi-dent return even if assigned to duty inanother state or country, unless he or shequalifies for nonresident status (see charton page 13). If you are a New Jersey resi-dent, you are subject to tax on all yourincome, including your military pay, re-gardless of where it is earned, unless theincome is specifically exempt from taxunder New Jersey law. Mustering-outpayments, subsistence and housing al-lowances are exempt.

�

Military pensions are ex-�������empt from New Jerseygross income tax, regard-

less of your age or disability status. SeePensions, Annuities, IRA Withdrawals,and Exclusion on page 27.

A member of the Armed Forces whosehome of record is New Jersey and who isstationed outside the State (whether livingin barracks, billets, apartment, or house)

Part-Year Residents - continued

TAXPAYERS’ BILL OF RIGHTSThe New Jersey Taxpayers’ Bill of Rights simplifies tax administration and en-sures that all taxpayers—individuals and businesses alike—are better informedand receive fair and equitable treatment during the tax collection process. High-lights of the Taxpayers’ Bill of Rights include:Service—♦ Division must respond to taxpayers’ questions within a reasonable time period.♦ Notices of taxes and penalties due must clearly identify the purpose of the no-

tice and must contain information about appeal procedures.Appeals—♦ Time to appeal to the Tax Court is generally 90 days.

Interest on Refunds—♦ Interest is paid at the prime rate on refunds for all taxes when the Division

takes more than six months to send you a refund.♦ You may request that your overpayment of this year’s tax be credited towards

next year’s tax liability, however, interest will not be paid on overpaymentsthat are credited forward.

For more information on the rights and obligations of both taxpayers and theDivision of Taxation under the Taxpayers’ Bill of Rights, request our publicationANJ-1, New Jersey Taxpayers’ Bill of Rights.

2002 Form NJ-104016

continued

and does not intend to remain outsideNew Jersey, continues to be a resident andmust file a resident return and report alltaxable income. However, if a service-person pays for and maintains facilitiessuch as an apartment or a home outside ofNew Jersey, either by out-of-pocket pay-ments or forfeiture of quarters allowance,such facilities will constitute a permanenthome outside of New Jersey. In this case,the serviceperson is not considered a NewJersey resident for tax purposes.

Nonresidents. A member of the ArmedForces whose home of record (domicile)is outside of New Jersey does not becomea New Jersey resident when assigned toduty in this State. A nonresident service-person’s military pay is not subject toNew Jersey income tax and he or she isnot required to file a New Jersey returnunless he or she has received income fromNew Jersey sources other than militarypay. Mustering-out payments, subsistenceand housing allowances are also exempt.A nonresident serviceperson who has in-come from New Jersey sources such as acivilian job in off-duty hours, income orgain from property located in New Jersey,or income from a business, trade, or pro-fession carried on in this State must file aNew Jersey nonresident return, FormNJ-1040NR.

If your permanent home (domicile) wasNew Jersey when you entered the mili-tary, but you have changed your state ofdomicile or you satisfy the conditions fornonresident status (see chart on page 13),then your military pay is not subject toNew Jersey income tax. File FormDD-2058-1 or DD-2058-2 with your fi-nance officer to stop future withholding ofNew Jersey income tax. If New Jersey in-come tax was erroneously withheld fromyour military pay, you must file a nonresi-dent return (Form NJ-1040NR) to obtaina refund of the tax withheld. For more in-formation, see the nonresident returninstructions.

Spouses of Military Personnel. Spouses(of military personnel) who were notdomiciled in New Jersey when they mar-ried the military spouse are not consid-ered residents of New Jersey if:

♦ The principal reason for moving tothis State was the transfer of the mili-tary spouse; and

♦ It is their intention to leave New Jerseywhen the military spouse is transferredor leaves the service.

New Jersey law requires that a couple’sfiling status for New Jersey gross incometax purposes be the same as for Federalincome tax purposes. A married couplefiling a joint Federal return must file ajoint return in New Jersey. The only ex-ception to this rule is when one spouse isa New Jersey resident and the other is anonresident for the entire year. In thiscase, the resident may file a separate re-turn and use the married, filing separatetax rates, unless both spouses agree to filejointly as residents. If a joint resident re-turn is filed, their joint income will betaxed as if both spouses were residents.

For more information, request Tax TopicBulletin GIT-7, Military Personnel.

�

Extensions. A person on�������active duty with the ArmedForces of the United States

who may not be able to file timely be-cause of distance, injury, or hospitaliza-tion as a result of this service, will auto-matically receive a three-month extensionby enclosing an explanation with the re-turn when filed.

New Jersey allows an extension to file anincome tax return for members of theArmed Forces serving in an area whichhas been declared a “combat zone” by ex-ecutive order of the President of theUnited States or a “qualified hazardousduty area” by Federal statute. Once youleave the combat zone or qualified haz-ardous duty area, you have 180 days tofile your tax return. Enclose a statementwith your return to explain the reason forthe extension.

In addition, if you are hospitalized outsideof the State of New Jersey as a result ofinjuries you received while serving in acombat zone or qualified hazardous dutyarea, you have 180 days from the timeyou leave the hospital or you leave thecombat zone or hazardous duty area,

whichever is later. Enclose a statement ofexplanation with your return when you file.

No interest or penalties will be assessedduring a valid extension for service in acombat zone or qualified hazardous dutyarea. This extension is also granted to ataxpayer’s spouse who files a joint return.

Death Related to Duty. When a memberof the Armed Forces serving in a combatzone or qualified hazardous duty area diesas a result of wounds, disease, or injuryreceived there, no income tax is due forthe taxable year the death occurred, nor forany earlier years served in the zone or area.

When to FileGenerally, your New Jersey income taxreturn is due when your Federal incometax return is due. For calendar year filers,the 2002 New Jersey income tax return isdue by April 15, 2003. Fiscal year filersmust file their New Jersey income tax re-turn by the 15th day of the fourth monthfollowing the close of the fiscal year.

Postmark Date. All New Jersey incometax returns postmarked on or before thedue date of the return are considered tobe filed on time. Tax returns postmarkedafter the due date are considered to befiled late. When a return is postmarkedafter the due date, the filing date for thatreturn is the date the return was receivedby the Division, not the postmark date ofthe return. Interest on unpaid liabilities isassessed from the due date of the return.

ExtensionsExtensions of time are granted only to fileyour New Jersey resident income tax re-turn. There are no extensions of time topay tax due. Penalties and interest areimposed whenever tax is paid after theoriginal due date.

Four-Month ExtensionYou may receive a four-month extensionof time to file your New Jersey residentincome tax return if at least 80% of thetax liability computed on your FormNJ-1040 when filed is paid in the form ofwithholdings, estimated, or other pay-ments by the original due date, and

Military Personnel - continued

2002 Form NJ-1040 17

continued

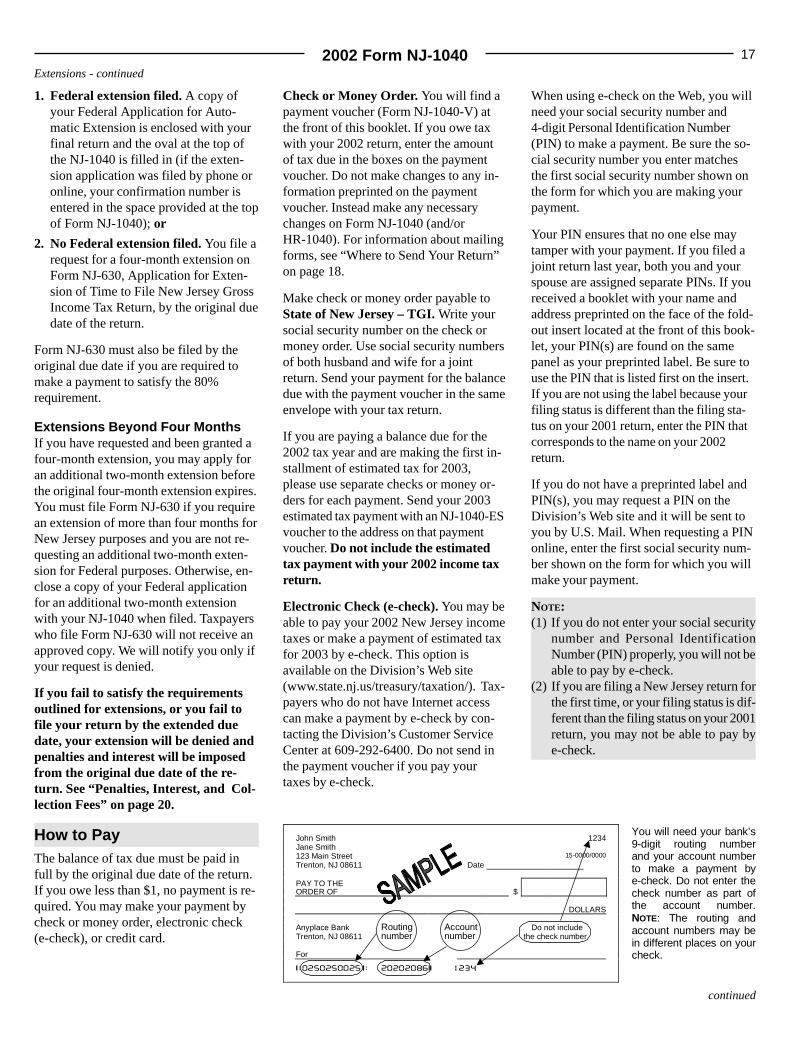

John Smith 1234Jane Smith123 Main Street 15-0000/0000

Trenton, NJ 08611 Date

PAY TO THEORDER OF $

DOLLARS

Anyplace Bank Routing Account Do not includeTrenton, NJ 08611 number number the check number

For

� ������������� � ���������� ����

You will need your bank’s9-digit routing numberand your account numberto make a payment bye-check. Do not enter thecheck number as part ofthe account number.NOTE: The routing andaccount numbers may bein different places on yourcheck.

1. Federal extension filed. A copy ofyour Federal Application for Auto-matic Extension is enclosed with yourfinal return and the oval at the top ofthe NJ-1040 is filled in (if the exten-sion application was filed by phone oronline, your confirmation number isentered in the space provided at the topof Form NJ-1040); or

2. No Federal extension filed. You file arequest for a four-month extension onForm NJ-630, Application for Exten-sion of Time to File New Jersey GrossIncome Tax Return, by the original duedate of the return.

Form NJ-630 must also be filed by theoriginal due date if you are required tomake a payment to satisfy the 80%requirement.

Extensions Beyond Four MonthsIf you have requested and been granted afour-month extension, you may apply foran additional two-month extension beforethe original four-month extension expires.You must file Form NJ-630 if you requirean extension of more than four months forNew Jersey purposes and you are not re-questing an additional two-month exten-sion for Federal purposes. Otherwise, en-close a copy of your Federal applicationfor an additional two-month extensionwith your NJ-1040 when filed. Taxpayerswho file Form NJ-630 will not receive anapproved copy. We will notify you only ifyour request is denied.

If you fail to satisfy the requirementsoutlined for extensions, or you fail tofile your return by the extended duedate, your extension will be denied andpenalties and interest will be imposedfrom the original due date of the re-turn. See “Penalties, Interest, and Col-lection Fees” on page 20.

How to PayThe balance of tax due must be paid infull by the original due date of the return.If you owe less than $1, no payment is re-quired. You may make your payment bycheck or money order, electronic check(e-check), or credit card.

Check or Money Order. You will find apayment voucher (Form NJ-1040-V) atthe front of this booklet. If you owe taxwith your 2002 return, enter the amountof tax due in the boxes on the paymentvoucher. Do not make changes to any in-formation preprinted on the paymentvoucher. Instead make any necessarychanges on Form NJ-1040 (and/orHR-1040). For information about mailingforms, see “Where to Send Your Return”on page 18.

Make check or money order payable toState of New Jersey – TGI. Write yoursocial security number on the check ormoney order. Use social security numbersof both husband and wife for a jointreturn. Send your payment for the balancedue with the payment voucher in the sameenvelope with your tax return.

If you are paying a balance due for the2002 tax year and are making the first in-stallment of estimated tax for 2003,please use separate checks or money or-ders for each payment. Send your 2003estimated tax payment with an NJ-1040-ESvoucher to the address on that paymentvoucher. Do not include the estimatedtax payment with your 2002 income taxreturn.

Electronic Check (e-check). You may beable to pay your 2002 New Jersey incometaxes or make a payment of estimated taxfor 2003 by e-check. This option isavailable on the Division’s Web site(www.state.nj.us/treasury/taxation/). Tax-payers who do not have Internet accesscan make a payment by e-check by con-tacting the Division’s Customer ServiceCenter at 609-292-6400. Do not send inthe payment voucher if you pay yourtaxes by e-check.

When using e-check on the Web, you willneed your social security number and4-digit Personal Identification Number(PIN) to make a payment. Be sure the so-cial security number you enter matchesthe first social security number shown onthe form for which you are making yourpayment.

Your PIN ensures that no one else maytamper with your payment. If you filed ajoint return last year, both you and yourspouse are assigned separate PINs. If youreceived a booklet with your name andaddress preprinted on the face of the fold-out insert located at the front of this book-let, your PIN(s) are found on the samepanel as your preprinted label. Be sure touse the PIN that is listed first on the insert.If you are not using the label because yourfiling status is different than the filing sta-tus on your 2001 return, enter the PIN thatcorresponds to the name on your 2002return.

If you do not have a preprinted label andPIN(s), you may request a PIN on theDivision’s Web site and it will be sent toyou by U.S. Mail. When requesting a PINonline, enter the first social security num-ber shown on the form for which you willmake your payment.

NOTE:(1) If you do not enter your social security

number and Personal IdentificationNumber (PIN) properly, you will not beable to pay by e-check.

(2) If you are filing a New Jersey return forthe first time, or your filing status is dif-ferent than the filing status on your 2001return, you may not be able to pay bye-check.

Extensions - continued

2002 Form NJ-104018

continued

Credit Card. You may pay your 2002New Jersey income taxes or make a pay-ment of estimated tax for 2003 by creditcard. Pay by phone (1-800-2PAYTAX,toll-free) or directly over the Internet(www.officialpayments.com) and use aVisa, American Express, MasterCard, orDiscover/Novus credit card. Do not sendin the payment voucher if you pay yourtaxes by credit card.

There is a convenience fee of 2.5% paiddirectly to Official Payments Corporationbased on the amount of your tax payment.

Time Limit for Assessing AdditionalTaxes. The Division of Taxation has threeyears from the date you filed your incometax return or the original due date of thereturn, whichever is later, to send you abill for additional taxes you owe. There isno time limit if you did not file your tax

return, or if you filed a false or fraudulentreturn with the intent to evade tax. Thetime limit may be extended if:

♦ You amended or the IRS adjusted yourFederal taxable income or your Federalearned income credit;

♦ You amended your New Jersey taxableincome;

♦ You entered into a written agreementwith the Division extending the time tomake an assessment;

♦ You omit more than 25% of your grossincome on your New Jersey income taxreturn; or

♦ An erroneous refund is made as a resultof fraud or misrepresentation by thetaxpayer.

Where to Send Your ReturnYour packet contains a large envelope.Use the large envelope to mail yourNJ-1040 and HR-1040 along with relatedenclosures, payment voucher, and checkor money order for any tax due. On theflap of the large envelope you will findpreprinted address labels with differentaddresses for different categories of re-turns. To ensure your return is mailedproperly:

1. Remove all labels along perforationsfrom envelope flap; and

2. Choose the correct label for your return.

Mail Returns Requesting a Refund (orwith No Tax Due) with or withoutHomestead Rebate Applications to:

STATE OF NEW JERSEY

DIVISION OF TAXATION

REVENUE PROCESSING CENTER

PO BOX 555TRENTON NJ 08647-0555

Mail Returns Indicating Tax DueTogether with Payment Voucherand Check or Money Order to:

STATE OF NEW JERSEY

DIVISION OF TAXATION

REVENUE PROCESSING CENTER

PO BOX 111TRENTON NJ 08645-0111

Mail Homestead Rebate ApplicationsFiled Without Income Tax Returns to:

STATE OF NEW JERSEY

DIVISION OF TAXATION

REVENUE PROCESSING CENTER

PO BOX 197TRENTON NJ 08646-0197

3. Moisten and affix only the correctlabel on the front of the large returnenvelope.

Do not staple, paper clip, or tape yourcheck or money order to the voucher.

RefundsA return must be filed to claim a refundfor overpayment of tax. If the refund is $1or less, you must enclose a statement spe-cifically requesting it.

Time Period for Refunds. You havethree years from the date the return wasfiled or two years from the time tax waspaid, whichever was later, to claim a re-fund. If you and the Division agree inwriting to extend the period of assess-ment, the period for filing a refund claimwill also be extended.

Interest Paid on Refunds. If the Divisiontakes more than six months to send youyour income tax refund, you have a rightto receive interest on that refund. Interestat the prime rate, compounded annually,will be paid from the later of:

♦ the date the refund claim was filed;♦ the date the tax was paid; or♦ the due date of the return.

No interest will be paid when an over-payment is credited to the next year’s taxliability or on an overpayment or portionof an overpayment which consists of aNew Jersey earned income tax credit.

New Jersey law requires that any moneyowed to the State of New Jersey, any ofits agencies, or the Internal RevenueService be deducted from your refund orcredit before it is issued. Homestead re-bates may also be affected. These debtsinclude among other things money owedfor past due taxes, child support dueunder a court order, school loans, andIRS levies. If the Division applies yourrefund, credit, or rebate to any of thesedebts, you will be notified through themail.

How to Pay - continued

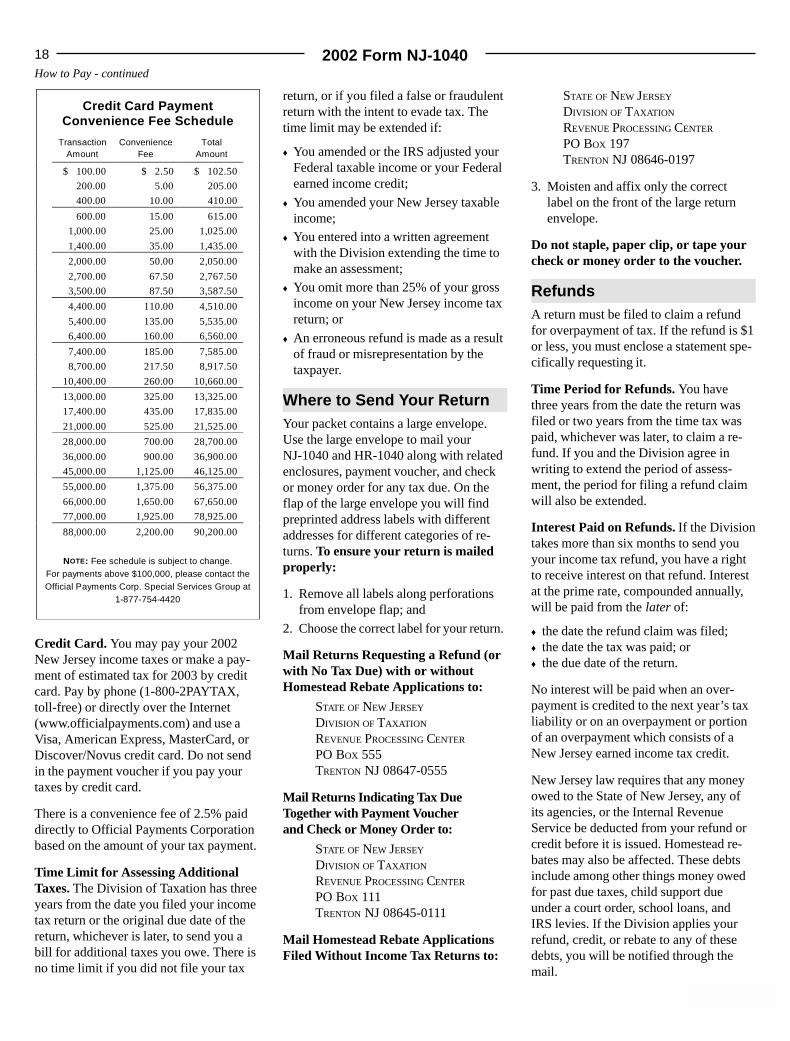

Credit Card PaymentConvenience Fee Schedule

TransactionAmount

ConvenienceFee

TotalAmount

$ 100.00 $ 2.50 $ 102.50

200.00 5.00 205.00

400.00 10.00 410.00

600.00 15.00 615.00

1,000.00 25.00 1,025.00

1,400.00 35.00 1,435.00

2,000.00 50.00 2,050.00

2,700.00 67.50 2,767.50

3,500.00 87.50 3,587.50

4,400.00 110.00 4,510.00

5,400.00 135.00 5,535.00

6,400.00 160.00 6,560.00

7,400.00 185.00 7,585.00

8,700.00 217.50 8,917.50

10,400.00 260.00 10,660.00

13,000.00 325.00 13,325.00

17,400.00 435.00 17,835.00

21,000.00 525.00 21,525.00

28,000.00 700.00 28,700.00

36,000.00 900.00 36,900.00

45,000.00 1,125.00 46,125.00

55,000.00 1,375.00 56,375.00

66,000.00 1,650.00 67,650.00

77,000.00 1,925.00 78,925.00

88,000.00 2,200.00 90,200.00

NOTE: Fee schedule is subject to change.For payments above $100,000, please contact theOfficial Payments Corp. Special Services Group at

1-877-754-4420

2002 Form NJ-1040 19

continued

Deceased TaxpayersIf a person received income in 2002 butdied before filing a return, the New Jerseyincome tax return should be filed by thesurviving spouse, executor, or admin-istrator. Use the same filing status thatwas used on the final Federal income taxreturn. Print “Deceased” and the date ofdeath above the decedent’s name. Do notprorate exemptions or deductions unlessthe decedent was a part-year resident. Thedue date for filing is the same as for Fed-eral purposes. In the area where you signthe return write “Filing as SurvivingSpouse,” if appropriate. A personal repre-sentative filing the return must sign in hisor her official capacity. Any refund checkwill be issued to the decedent’s survivingspouse or estate.

Income in Respect of a Decedent. If youhad the right to receive income that thedeceased person would have received hadhe or she lived, and the income was notincluded on the decedent’s final return,you must report the income on your ownreturn when you receive it. The income orgain is included on Line 25, as “Other”income.

Estates and TrustsFiling Requirements for Estates andTrusts. The fiduciary of an estate or trustmay be required to file a New Jerseygross income tax return for that estate ortrust. The return for an estate or trustmust be filed on a New Jersey FiduciaryReturn, Form NJ-1041. The fiduciarymust also provide each beneficiary with acopy of the Federal Schedule K-1 whichshows the beneficiary’s share of the estateor trust income.

Revocable grantor trusts are required tofile a New Jersey Fiduciary Return, FormNJ-1041, where there is sufficient nexuswith this State and the statutory filing re-quirement is met. For further information,see the Fiduciary return, Form NJ-1041,instructions.

Filing Requirements for Beneficiaries.You must report the items of income orgain you receive as a beneficiary of an es-tate or trust on Line 25, “Other” income.Interest, dividends, capital gains, business

or partnership income, etc. as listed on theFederal K-1 form(s) you received must beadjusted to reflect New Jersey tax law andthen netted together before inclusion onthe “Other” income line. Enclose a copyof the Federal K-1(s) with your return.

If the income from a grantor trust is re-portable by or taxable to the grantor forFederal income tax purposes, it is alsotaxable to the grantor for New Jerseygross income tax purposes. See instruc-tions for Line 25 on page 31 for reportingrequirements.

PartnershipsA partnership is not subject to gross in-come tax. Individual partners are subjectto tax on the income they earned from thepartnership under the Federal InternalRevenue Code and the New Jersey GrossIncome Tax Act. See page 30 for informa-tion on reporting income from a partner-ship. Every partnership having a NewJersey resident partner or income fromNew Jersey sources must file a New Jer-sey Partnership Return, Form NJ-1065,with the New Jersey Division of Taxationby the 15th day of the fourth month fol-lowing the close of the partnership’s tax-able year. For more information onpartnership filing, request Form NJ-1065and instructions.

Estimated TaxEstimated tax means the amount whichyou estimate to be your income tax for thetaxable year after subtracting payments,withholdings, and other credits.

�

You are required to make�������estimated tax paymentsusing Form NJ-1040-ES

when your estimated tax exceeds $400.Instructions for computing the estimatedtax and making the payments are includedwith the form. Review the amount of yourNew Jersey gross income tax on your ex-pected gross income (after deductions andcredits) to determine if you need to makeestimated tax payments for 2003.

To avoid having to make estimated tax pay-ments, you may ask your employer to with-hold an additional amount from your wages

by completing Form NJ-W4. Failure to filea Declaration of Estimated Tax or pay all orpart of an underpayment will result in inter-est charges on the underpayment.

Underpayment of Estimated Tax. If youfailed to make all of the required esti-mated tax payments as described above,you should request Form NJ-2210, Un-derpayment of Estimated Tax by Individ-uals, Estates or Trusts. Complete FormNJ-2210 to determine if interest is dueand if so, calculate the amount. If youcomplete and enclose Form NJ-2210 withyour return, fill in the oval below Line 45.

Amended ReturnsIf you received an additional tax state-ment (W-2 or 1099) after your return wasfiled, or you discovered that you madeany error or omission on your return, filean amended New Jersey resident return,Form NJ-1040X.

Changes in Your Federal Income Taxor Federal Earned Income Credit. Ifyou receive a notice from the InternalRevenue Service that they changed yourreported income, and that change alteredyour New Jersey taxable income, or if youreceive a notice that your Federal earnedincome credit has been changed, and thatchange alters your New Jersey earned in-come tax credit, you must notify the Divi-sion of the change in writing within 90days. File an amended tax return and payany additional tax due.

If you file an amended Federal returnwhich changes your New Jersey taxableincome or your Federal earned incomecredit, you must file an amended New Jer-sey resident return, Form NJ-1040X,within 90 days.

Accounting MethodUse the same accounting method for NewJersey gross income tax that you used forFederal income tax purposes. Incomemust be recognized and reported in thesame period as it is recognized and re-ported for Federal income tax purposes.

2002 Form NJ-104020

continued

Rounding Off to WholeDollarsWhen completing your return and the ac-companying schedules, you may show themoney items in whole dollars. If you haveto add two or more items to figure thetotal to enter on a line, include cents whenadding the items and round off only thetotal. When entering the rounded total onthe line, eliminate any amount under 50cents and increase any amount 50 cents ormore to the next higher dollar. If you doround off, do so for all amounts. Whenrounding, enter zeros after the decimalpoint for cents.

Penalties, Interest, andCollection FeesPenalty and interest should be includedwith the payment of any tax due.

Late Filing Penalty5% per month (or fraction of a month) upto a maximum of 25% of the outstandingtax liability when a return is filed after thedue date or extended due date. Also, apenalty of $100 for each month the returnis late may be imposed.

Late Payment Penalty5% of the outstanding tax balance may beimposed.

Interest3% above the prime rate for every monthor fraction of a month the tax is unpaid,compounded annually. At the end of eachcalendar year, any tax, penalties, and in-terest remaining due (unpaid) will becomepart of the balance on which interest ischarged.

Collection FeesIn addition, if your tax bill is sent to ourcollection agency, a referral cost recoveryfee of 10% of the tax due may be addedto your liability. If a certificate of debt isissued for your outstanding liability, a feefor the cost of collection of tax may alsobe imposed.

SignaturesSign and date your return in blue or blackink. Both husband and wife must sign ajoint return. If you are filing a HomesteadRebate Application (Form HR-1040) withyour tax return, it is not necessary to signthe rebate application. However, if youare filing only Form HR-1040, the appli-cation must be signed and dated in ink.The signature(s) on the form you file mustbe original; photocopied signatures arenot acceptable. A return without theproper signatures cannot be processedand will be returned to you. This causesunnecessary processing delays and mayresult in penalties for late filing or a delayor denial of your homestead rebate.

Don’t Need Forms Mailed to You NextYear? Taxpayers who pay someone elseto prepare their returns probably do notuse the income tax return booklets mailedto them each year. If you do not need abooklet mailed to you next year, fill in theoval below the signature line. Telling usthat you do not need a booklet next yearwill help us reduce printing and mailingcosts.

�

Preparer Authorization.�������Because of the strict provi-sions of confidentiality,

Division of Taxation personnel may notdiscuss your return or enclosures withanyone other than you without your writ-ten authorization. If, for any reason, youwant a Division of Taxation representa-tive to discuss your tax return with the in-dividual who signed your return as your“Paid Tax Preparer,” we must have yourpermission to do so. To authorize the Di-vision of Taxation to discuss your returnand enclosures with your “Paid Tax Pre-parer,” fill in the oval above the preparer’ssignature line.

Tax Preparers. Anyone who prepares areturn for a fee must sign the return as a“Paid Preparer” and enter his or her socialsecurity number or Federal preparer taxidentification number. Include the com-pany or corporation name and Federalidentification number, if applicable. A taxpreparer who fails to sign the return orprovide a tax identification number may

incur a $25 penalty for each omission.Someone who prepares your return butdoes not charge you should not sign yourreturn.

Keeping Tax RecordsKeep copies of your tax returns and thesupporting documentation of income, ageand/or disability, deductions, and creditsuntil the statute of limitations has expiredfor each return. Generally, this is threeyears after the filing date or two yearsfrom the date the tax was paid, whicheveris later.

Privacy Act NotificationThe Federal Privacy Act of 1974 requiresan agency requesting information from in-dividuals to inform them why the requestis being made and how the information isbeing used.

Your social security number is used pri-marily to account for and give credit fortax payments. The Division of Taxationalso uses social security numbers in theadministration and enforcement of all taxlaws for which it is responsible. In addi-tion, the Division of Taxation is requiredby law to forward an annual list to theAdministrative Office of the Courts con-taining the names, addresses, and socialsecurity numbers of individuals who file aNew Jersey resident tax return or home-stead rebate application. This list will beused to avoid duplication of names onjury lists.

Federal/State Tax AgreementThe New Jersey Division of Taxation andthe Internal Revenue Service have enteredinto a Federal/State Agreement to ex-change income tax information in order toverify the accuracy and consistency of in-formation reported on Federal and NewJersey income tax returns.

Fraudulent ReturnAny person who deliberately fails to file areturn, files a fraudulent return, or at-tempts to evade the tax in any mannermay be liable for a penalty up to $7,500or imprisonment for a term between threeand five years or both.

2002 Form NJ-1040 Line by Line Instructions 21

continued

Name and AddressPlace the peel-off label at the front of thisbooklet in the name and address section atthe top of the return. Do not use the labelif any of the information is incorrect. Ifyour label contains inaccurate informationor you do not have a label, print or typeyour name (last name first), complete ad-dress, and zip code in the spaces pro-vided. Also include your spouse’s name iffiling jointly. Your refund and next year’sform will be sent to the address youprovide.

If your legal residence and the address onthe return differ, enclose a statement ofexplanation to avoid a delay in processing.

Social Security Number

�

Your social security�������number(s) is not printedon your name and address

label. You must enter your social secu-rity number(s) in the space provided onthe return, one digit in each box. If yourfiling status is married, filing joint return,remember to report both spouses’ num-bers in the order in which the names arelisted on the return.

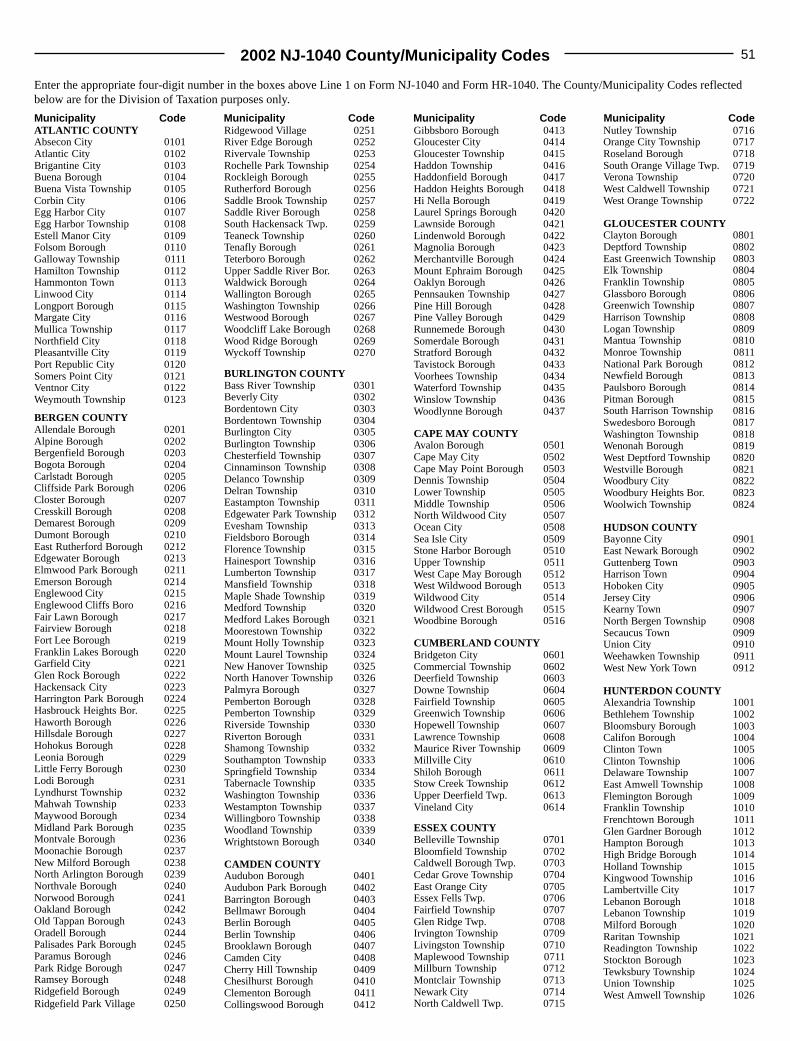

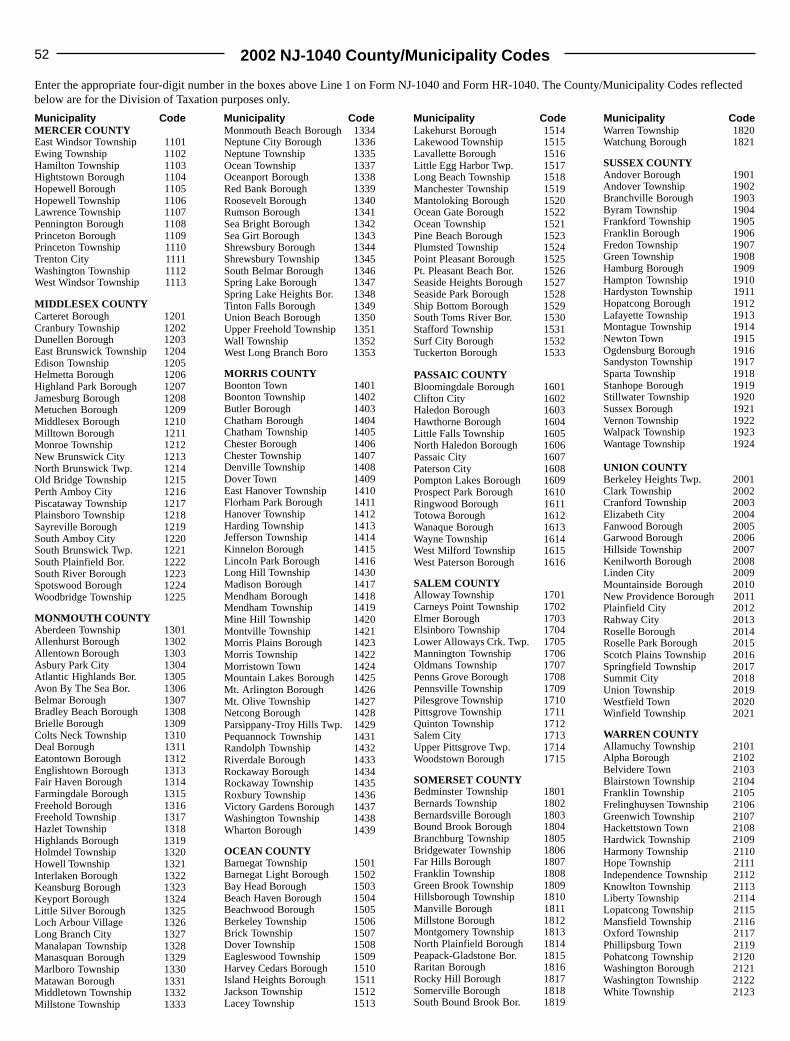

County/Municipality CodeCheck the county/municipality code onyour label (see example below). Do notuse the label if any of the information isincorrect. If your label contains inaccu-rate information or you do not have alabel, enter your four-digit code, one digitin each box, from the table on page 51. Ifyour municipality is not listed, enter thecode for the municipality where you payyour property taxes. This code identifiesthe county and municipality of your cur-rent residence. The county and municipal-ity codes in these instructions are forDivision of Taxation purposes only.

************************************************************X X X X X X X X X X X X X X X X X X X X X X X X X XSMIT 1111SMITH JOHN & JANE123 MAIN STREET County/Municipality CodeTRENTON, NJ 08611

123123123900

Filing Status (Lines 1 - 5)Generally, you must use the same filingstatus on your New Jersey return as youdo for Federal income tax purposes. Indi-cate the appropriate filing status. Fill inonly one oval.

If spouses file a joint Federal income taxreturn, they must also file a joint New Jer-sey income tax return. If spouses fileseparate Federal returns, separate Statereturns must also be filed. If your filingstatus is married, filing separate return, besure to enter the social security number ofyour spouse in the boxes provided at thetop of the tax return.

If you meet the requirements to file ashead of household for Federal income taxpurposes, you may file as head of house-hold for New Jersey. Certain married in-dividuals living apart may file as head ofhousehold for New Jersey if they meet therequirements to file as head of householdfor Federal purposes.

If during the entire taxable year onespouse was a resident and the other a non-resident, the resident spouse may file aseparate New Jersey return. The residentspouse computes income and exemptionsas if a Federal married, filing separate re-turn had been filed. You have the optionof filing a joint return, but remember,joint income would be taxed as if bothspouses were residents.

For more information on filing status,order Tax Topic Bulletin GIT-4, FilingStatus.

Exemptions - Personal(Lines 6 - 8)The exemptions claimed on Lines 6, 7,and 8 apply only to you and your spouse.The exemptions for age and disability arenot available for dependents. If your filingstatus is married, filing separate return,you generally do not fill in the spouseoval on Lines 6, 7, or 8.

Line 6 - Regular ExemptionsAs a taxpayer you may claim a personalexemption for yourself, even if you are aminor who is claimed as a dependent on

your parents’ return. For your conven-ience, “Yourself” is already filled in. Ifyou are filing a joint return, fill in thespouse oval as well. Add the number ofovals filled in and enter the result in thered box on Line 6.

Line 7 - Age 65 or OlderIf either you or your spouse were 65 yearsof age or older at the end of the tax year,you (and your spouse if qualified) are eli-gible for an additional exemption. Youmust enclose proof of age such as a copyof a birth certificate, driver’s license, orchurch records with your return the firsttime you claim the exemption. Fill in theappropriate oval(s). Add the number ofovals filled in and enter the result in thered box on Line 7.

Line 8 - Blind or DisabledIf either you or your spouse were blind ordisabled at the end of the tax year, you(and your spouse if qualified) are eligiblefor an additional exemption. “Disabled”means total and permanent inability toengage in any substantial gainful activitybecause of any physical or mental impair-ment, including blindness. You must en-close a copy of the doctor’s certificate orother medical records with your returnthe first time you claim the exemption.This information need not be submittedeach year providing there is no change inyour condition. Fill in the appropriateoval(s). Add the number of ovals filled inand enter the result in the red box on Line8.

Exemptions - Dependency(Lines 9 - 11)The exemptions claimed on Lines 9, 10,and 11 apply only to dependents. The ex-emption for dependents attending collegesis not available to you, the taxpayer, oryour spouse.

Line 9 - Dependent ChildrenYou may claim an exemption for each de-pendent child who qualifies as your de-pendent for Federal income tax purposes.Enter the number of your dependent chil-dren in the red box on Line 9.

2002 Form NJ-1040 Line by Line Instructions22

continued

Line 10 - Other DependentsYou may claim an exemption for eachother dependent who qualifies as your de-pendent for Federal income tax purposes.Enter the number of your other depen-dents in the red box on Line 10.

Line 11 - DependentsAttending CollegesYou may claim an additional exemptionfor each dependent under age 22 who is afull-time student at an accredited collegeor postsecondary institution for whomyou paid one-half or more of the tuitionand maintenance costs. Financial aid re-ceived by the student is not calculatedinto your cost when totaling one-half ofyour dependent’s tuition and maintenance.However, the money earned by studentsin College Work Study Programs is in-come and is taken into account. Remem-ber, to claim this additional exemption,each dependent must have alreadybeen claimed on Line 9 or 10.

Requirements♦ Student must be under 22 years of

age for the entire tax year.

♦ Student must attend full-time. “Full-time” is determined by the institution.

♦ Student must spend at least some partof each of five calendar months of thetax year at school.

♦ The educational institution must main-tain a regular faculty and curriculumand have a body of students inattendance.

Enter the number of exemptions for yourqualified dependents attending colleges inthe red box on Line 11.

Line 12 - TotalsAdd Lines 6, 7, 8, and 11 and enter thetotal in the red box on Line 12a. AddLines 9 and 10 and enter that total in thered box on Line 12b.

Residency Status (Line 13)If you were a New Jersey resident foronly part of the taxable year, list themonth, day, and year your residencybegan and the month, day, and year itended. All months should be listed astwo-digit numbers with the digits 01 forJanuary, 02 for February, 03 for March,etc. Place the correct number for the be-ginning and ending months directly in theboxes containing the red letter “M,” onedigit in each box.

The days of the months should be listedas two-digit numbers beginning with thedigits 01 for the first day of the month andending with the digits 31 for the last dayof the month. Place the correct numberfor the beginning and ending dates di-rectly in the boxes containing the red let-ter “D,” one digit in each box.

For calendar year filers the year should beentered as 02 and the numbers placed di-rectly in the boxes containing the red let-ter “Y,” one digit in each box. Fiscal yearfilers should enter the appropriate year inthe “Y” boxes.

Gubernatorial Elections FundThe Gubernatorial Elections Fund, fi-nanced by taxpayer designated $1 con-tributions, provides partial publicfinancing to qualified candidates for theoffice of Governor of New Jersey. Withits contribution and expenditure limits,the Gubernatorial Public Financing Pro-gram has since 1977 assisted 56 candi-dates to conduct their campaigns freefrom the improper influence of excessivecampaign contributions. Operation of theprogram has also permitted candidates oflimited financial means to run for electionto the State’s highest office. As a condi-tion of their receipt of public financing,candidates must agree to participate intwo debates which provide the public withan opportunity to hear the views of eachcandidate. For more information on theGubernatorial Public Financing Program,contact the New Jersey Election Law En-forcement Commission at 609-292-8700or write to:

Gross Income includes the following:♦ Wages and other compensation♦ Interest and dividends♦ Earnings on nonqualified withdrawals from qualified state tuition program ac-

counts, including the New Jersey Better Educational Savings Trust Program(NJBEST) accounts

♦ Net profits from business, trade, or profession♦ Net gains or income from sale or disposition of property♦ Pensions, annuities, and IRA withdrawals♦ Net distributive share of partnership income♦ Net pro rata share of S corporation income♦ Net rental, royalty, and copyright income♦ Net gambling winnings♦ Alimony♦ Estate and trust income♦ Income in respect of a decedent♦ Prizes and awards, including scholarships and fellowships (unless they satisfy the

conditions on page 31)♦ Value of residence provided by employer♦ Fees for services rendered, including jury duty

New Jersey gross income also includes the following which are not subject toFederal income tax:♦ Interest from obligations of states and their political subdivisions, other than New

Jersey and its political subdivisions♦ Income earned by a resident from foreign employment♦ Certain contributions to pensions and tax-deferred annuities♦ Employee contributions to Federal Thrift Savings Funds, 403(b), 457, SEP, or any

other type of retirement plan other than 401(k) Plans

2002 Form NJ-1040 Line by Line Instructions 23

continued

Exempt IncomeDo not include the following income when deciding if you must file a return. Theseitems should not appear anywhere on your form except for tax-exempt interest, whichis reported on Line 15b.

♦ Federal Social Security♦ Railroad Retirement (Tier 1 and Tier 2)♦ United States military pensions and survivor’s benefit payments♦ Life insurance proceeds received because of a person’s death♦ Employee’s death benefits♦ Permanent and total disability, including VA benefits♦ Temporary disability received from the State of New Jersey or as third party

sick pay♦ Worker’s Compensation♦ Gifts and inheritances♦ Qualifying scholarships or fellowship grants♦ New Jersey Lottery winnings♦ Unemployment Compensation♦ Interest and capital gains from: (a) Obligations of the State of New Jersey or any of

its political subdivisions; or (b) Direct Federal obligations exempt under law, suchas U.S. Savings Bonds and Treasury Bills, Notes, and Bonds (see Line 15b)

♦ Distributions paid by mutual funds to the extent the distributions are attributable tointerest earned on Federal obligations

♦ Certain distributions from “New Jersey Qualified Investment Funds”(see Line 15b)

♦ Earnings on qualified withdrawals from qualified state tuition program accounts,including the New Jersey Better Educational Savings Trust Program (NJBEST)accounts

♦ Employer and employee contributions to 401(k) Salary Reduction Plans (but notFederal Thrift Savings Funds)

♦ Some benefits received from certain employer-provided cafeteria plans (but notsalary reduction or premium conversion plans). Request Division TechnicalBulletin TB-39

♦ Contributions to and distributions from Archer MSAs if they are excluded forFederal income tax purposes

♦ Direct payments and benefits received under homeless persons assistanceprograms

♦ Homestead rebates♦ NJ SAVER rebates♦ Property tax reimbursements♦ Income tax refunds (New Jersey, Federal, and other jurisdictions)♦ New Jersey earned income tax credit payments♦ Welfare♦ Child support♦ Amounts paid as reparations or restitution to Nazi Holocaust victims♦ Assistance from a charitable organization, whether in the form of cash or property

NJ ELECTION LAW ENFORCEMENT COMMISSION

PO BOX 185TRENTON NJ 08625-0185

Lists of contributors to gubernatorial can-didates may be viewed on the ElectionLaw Enforcement Commission Web siteat: www.elec.state.nj.us.

Participation in the $1 income tax check-off protects the continuity and integrity ofthe Gubernatorial Elections Fund by pro-viding that funds will be reserved for fu-ture gubernatorial elections therebydeterring the use of needed funding forother purposes. If you want to designate$1 to go to help candidates for governor

pay campaign expenses, fill in the “Yes”oval in the Gubernatorial Elections Fundsection of the return. If you are filing ajoint return, your spouse may also desig-nate $1 to this fund. Filling in the “Yes”oval will not in any way increase yourtax liability or reduce your refund.

Income (Lines 14 - 25)Gross income means all income you re-ceived in the form of money, goods, prop-erty, and services unless specificallyexempt by law. As a New Jersey residentyou must report all taxable income youreceive, whether from New Jersey or not,on your return.

�Important! A net loss in�������any category of incomecannot be reported as

such on Form NJ-1040. A loss withinone category of income may be appliedagainst other income within the samecategory. However, a net loss in onecategory of income cannot be appliedagainst income or gains in another. Inthe case of a net loss in any category,make no entry on the correspondingline. No carryback or carryover oflosses is allowed under New Jersey law.

If you have income that is taxed both byNew Jersey and by another jurisdictionoutside of New Jersey, you may be eli-gible for a credit against your New Jerseyincome tax. See instructions for Sched-ule A, Credit for Income or Wage TaxesPaid to Other Jurisdiction, on page 40.

Line 14 - Wages, Salaries,Tips, etc.Enter the total amount you received dur-ing the taxable year from wages, salaries,tips, fees, commissions, bonuses, andother payments received for services per-formed as an employee. Include all pay-ments you received whether in cash,benefits, or property.

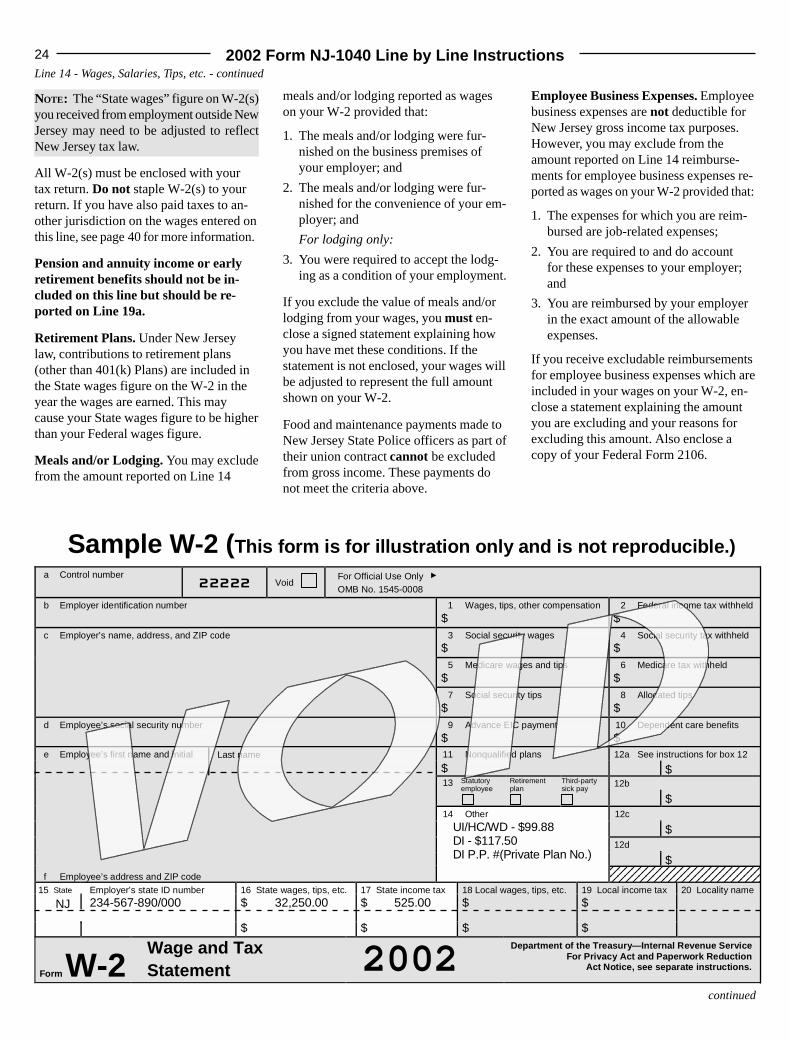

Enter the total of State wages, salaries,tips, etc. from all employment both insideand outside New Jersey. Be sure to takethe figure(s) from the “State wages”box on your W-2(s). See sample W-2 onpage 24.

Gubernatorial Elections Fund - continued

2002 Form NJ-1040 Line by Line Instructions24

continued

Line 14 - Wages, Salaries, Tips, etc. - continued

NOTE: The “State wages” figure on W-2(s)you received from employment outside NewJersey may need to be adjusted to reflectNew Jersey tax law.

All W-2(s) must be enclosed with yourtax return. Do not staple W-2(s) to yourreturn. If you have also paid taxes to an-other jurisdiction on the wages entered onthis line, see page 40 for more information.

Pension and annuity income or earlyretirement benefits should not be in-cluded on this line but should be re-ported on Line 19a.

Retirement Plans. Under New Jerseylaw, contributions to retirement plans(other than 401(k) Plans) are included inthe State wages figure on the W-2 in theyear the wages are earned. This maycause your State wages figure to be higherthan your Federal wages figure.

Meals and/or Lodging. You may excludefrom the amount reported on Line 14

meals and/or lodging reported as wageson your W-2 provided that:

1. The meals and/or lodging were fur-nished on the business premises ofyour employer; and

2. The meals and/or lodging were fur-nished for the convenience of your em-ployer; and

For lodging only:

3. You were required to accept the lodg-ing as a condition of your employment.

If you exclude the value of meals and/orlodging from your wages, you must en-close a signed statement explaining howyou have met these conditions. If thestatement is not enclosed, your wages willbe adjusted to represent the full amountshown on your W-2.

Food and maintenance payments made toNew Jersey State Police officers as part oftheir union contract cannot be excludedfrom gross income. These payments donot meet the criteria above.

Employee Business Expenses. Employeebusiness expenses are not deductible forNew Jersey gross income tax purposes.However, you may exclude from theamount reported on Line 14 reimburse-ments for employee business expenses re-ported as wages on your W-2 provided that:

1. The expenses for which you are reim-bursed are job-related expenses;

2. You are required to and do accountfor these expenses to your employer;and

3. You are reimbursed by your employerin the exact amount of the allowableexpenses.

If you receive excludable reimbursementsfor employee business expenses which areincluded in your wages on your W-2, en-close a statement explaining the amountyou are excluding and your reasons forexcluding this amount. Also enclose acopy of your Federal Form 2106.

123456789012345678901231234567890123456789012312345678901234567890123

Sample W-2 (This form is for illustration only and is not reproducible.)a Control number

��������� VoidFor Official Use Only �OMB No. 1545-0008

b Employer identification number 1 Wages, tips, other compensation

$2 Federal income tax withheld

$c Employer’s name, address, and ZIP code 3 Social security wages

$4 Social security tax withheld

$5 Medicare wages and tips

$6 Medicare tax withheld

$7 Social security tips

$8 Allocated tips

$d Employee’s social security number 9 Advance EIC payment

$10 Dependent care benefits

$12a See instructions for box 12e Employee’s first name and initial Last name 11 Nonqualified plans

$ $12bStatutory13

employeeRetirementplan

Third-partysick pay

$12c

$12d

$f Employee’s address and ZIP code

14 Other

UI/HC/WD - $99.88DI - $117.50DI P.P. #(Private Plan No.)

15 State

NJEmployer’s state ID number

234-567-890/00016 State wages, tips, etc.

$ 32,250.0017 State income tax

$ 525.0018 Local wages, tips, etc.

$19 Local income tax

$20 Locality name

$ $ $ $

Form W-2Wage and TaxStatement 2002

Department of the Treasury—Internal Revenue ServiceFor Privacy Act and Paperwork Reduction

Act Notice, see separate instructions.

2002 Form NJ-1040 Line by Line Instructions 25

continued

Commuter Transportation Benefits.Certain amounts you receive from youremployer up to $1,200 for using an alter-native means of commuting (such as pub-lic transportation, carpools, vanpools,etc.) may be excluded from your New Jer-sey gross income. Commuter transporta-tion benefits may not be excluded fromgross income unless your employer pro-vides those benefits in addition to yourregular compensation.

If the commuter transportation benefitsyou received exceed the maximum ex-cludable amount, the excess amount istaxable and is included in your gross in-come. Your W-2 form will show both thetaxable and nontaxable benefit amounts.The taxable benefits are included in the“State wages” figure on your W-2, whilethe nontaxable benefits are not.

An employee who receives money to-wards commuter transportation benefitsmust provide his/her employer with suit-able proof (receipts, ticket stubs, etc.) toshow that the employer-provided moneywas used for an alternative means ofcommuting.

Federal Statutory Employees. If you areconsidered a “statutory employee” forFederal income tax purposes, you may notdeduct your business expenses unless youare self-employed or an independent con-tractor under New Jersey law. The Fed-eral label of “statutory employee” has nomeaning for New Jersey gross income taxpurposes. Business expenses may only bededucted from the business income of aself-employed individual. See the instruc-tions for Line 17 (Net Profits fromBusiness).

Moving Expenses. Moving expenses arenot deductible for New Jersey gross in-come tax purposes. However, you mayexclude from the amount reported onLine 14 reimbursements for the followingmoving expenses if the Federal require-ments to claim moving expenses were metand the expenses were included in wageson your W-2.

1. The cost of moving your householdgoods and personal effects from theold home to the new home.

2. The actual expenses incurred by youfor traveling, meals, and lodging whenmoving you and your family from yourold residence to your new residence.

Reimbursements for any other moving ex-pense may not be excluded from income.

If you receive excludable reimbursementsfor moving expenses which are includedin your wages on your W-2, enclose astatement explaining the amount you areexcluding and your reasons for excludingthis amount. Also enclose a copy of yourFederal Form 3903.

Compensation for Injuries or Sickness.Certain amounts received for personal in-juries or sickness are not subject to tax.You may exclude from the amount re-ported on Line 14 such amounts includedas wages on your W-2 provided that:

1. The payments must be compensationfor wage loss which results from ab-sence due to injury or sickness of theemployee; and

2. The payments must be due and payableunder an enforceable contractual obli-gation under the plan; and

3. The payments must not relate to sickleave wage continuation, the taking ofwhich is largely discretionary and thepayments are made regardless of thereason for absence from work.

If such payments are included in the Statewage figure on your W-2, you must fileForm NJ-2440 with your New Jersey re-turn to exclude them.

Line 15a - Taxable InterestIncomeReport all of your taxable interest fromsources both inside and outside of NewJersey on Line 15a. New Jersey taxableinterest income includes interest from thefollowing:

♦ Banks♦ Savings and loan associations♦ Credit unions♦ Savings accounts♦ Earnings on nonqualified withdrawals

from qualified state tuition programaccounts, including the New Jersey

Better Educational Savings Trust Pro-gram (NJBEST) accounts

♦ Distributions from Coverdell educationsavings accounts (ESAs), but only theearnings portion

♦ Checking accounts♦ Bonds and notes♦ Certificates of deposit♦ Ginnie Maes♦ Fannie Maes♦ Freddie Macs♦ Repurchase agreements♦ Life insurance dividends♦ Obligations of states and their political

subdivisions, other than New Jersey♦ Any other interest not specifically

exempt

Interest received by your sole proprietor-ship is reportable as net profits from busi-ness on Line 17. Your portion of interestearned and received by a partnership, anestate or trust or, in general, an S corpo-ration is reportable as distributive share ofpartnership income on Line 20, net in-come from estates or trusts on Line 25, ornet pro rata share of S corporation incomeon Line 21. For detailed information re-garding the reporting of partnership or Scorporation income, request Tax TopicBulletin GIT-9P, Income From Partner-ships, or GIT-9S, Income From S Corpo-rations. For information regarding grantortrusts, see the reporting instructions forLine 25 on page 31. Interest paid ordeemed to have been paid to you by apartnership or an S corporation and re-portable to you on Form 1099 must be in-cluded on Line 15a.

Forfeiture Penalty for Early With-drawal. If you incur a penalty by with-drawing a time deposit early, you maysubtract the amount of the penalty fromyour interest income.

If your taxable interest income onLine 15a is more than $1,500, enclose acopy of Schedule B, Federal Form 1040,or Schedule 1, Federal Form 1040A.

Line 15b - Tax-ExemptInterest IncomeReport all of your tax-exempt interest, aswell as exempt interest dividends from aNew Jersey Qualified Investment Fund,

Line 14 - Wages, Salaries, Tips, etc. - continued

2002 Form NJ-1040 Line by Line Instructions26

continued

on Line 15b. If Line 15b is more than$10,000, you must include an itemizedschedule detailing the amount receivedfrom each source. New Jersey tax-exempt interest income includes interestfrom:

♦ Obligations of the State of New Jerseyor any of its political subdivisions

♦ Direct Federal obligations such as U.S.Savings Bonds and Treasury Bills,Notes, and Bonds

♦ Earnings on qualified withdrawalsfrom qualified state tuition programaccounts, including the New JerseyBetter Educational Savings Trust Pro-gram (NJBEST) accounts

♦ Sallie Maes♦ CATS♦ TIGRs♦ Certain distributions from “New Jersey

Qualified Investment Funds”♦ Distributions paid by mutual funds to

the extent the distributions are attrib-utable to interest earned on Federalobligations

New Jersey Qualified InvestmentFunds. A New Jersey Qualified Invest-ment Fund is a regulated investment com-pany in which at least 80% of the fund’sinvestments (other than cash or receiv-ables) are obligations issued either di-rectly by the Federal government or theState of New Jersey or any of its politicalsubdivisions. The Fund must certify suchstatus with the Division of Taxationannually.

If you received a distribution from aqualified investment fund, you may ex-clude from your income only the portionof the distribution which comes fromqualified exempt obligations. Althoughexcluded from income, the tax-exemptportion is reported on Line 15b. The tax-able portion of the distribution, if any, isreported as dividends on Line 16. By Feb-ruary 15, shareholders should be notifiedby the New Jersey qualified investmentfund of the portion of their distributionthat may be excluded from income. Con-tact your broker to determine whetheryour fund qualifies.

Do not report interest earned on yourIRA(s) on Line 15b, Tax-Exempt Inter-

Line 15b - Tax-Exempt Interest Income - continued

duce the basis of the stock or investmentand are not taxable until your investmentis fully recovered.

Insurance Premiums. Dividends re-ceived from insurance companies are nottaxable unless the dividends received ex-ceed the premiums paid. Any interestfrom accumulated insurance dividends istaxable and must be reported on Line 15a.

Line 17 - Net Profits FromBusinessReport the net profits from your business,trade, or profession on Line 17. To deter-mine your New Jersey profit (or loss),first complete a Federal Schedule C (orSchedule C-EZ or Schedule F). To com-ply with New Jersey income tax law,make the following adjustments to yourFederal Schedule C (or Schedule C-EZ orSchedule F):

1. Add any amount you deducted fortaxes based on income.