ncr real estate report h2 2017 presentation

TRANSCRIPT

NCRRESIDENTIAL & OFFICEJULY TO DECEMBER 2017

2

RESIDENTIAL RECAP H1 2017

Launches were at a new low in

H1 2017 with only 4,800 units

Sales registered a drop of 26% YoY

Unsold inventory of 180,370 units

remained a concern

Impact of RERA & GST

compliance

Low sales velocity

High unsold inventory

3

1,72,571

1,10,751 1,00,259 99,407

79,577

63,458

26,734

11,726

2010 2011 2012 2013 2014 2015 2016 2017

Launches

Launches at an all-time low

since 2010

56% drop YoY

No. o

f units

4

34,577

45,000

29,458

34,000

17,462

9,273

4,800 6,926

H1 2014 H2 2014 H1 2015 H2 2015 H1 2016 H2 2016 H1 2017 H2 2017

25% drop YoY

Half-yearly launches

RERA and GST compliance

magnified in the first half of 2017

No. o

f units

5

H2 2016 H2 2017

<2.5 mn 2% 68%

2.5-5 mn 14% 10%

5-7.5 mn 35% 16%

7.5-10 mn 33% 0%

10-20 mn 4% 4%

>20 11% 2%

Ticket sizes that saw

maximum change in H2 2017

Share of launches in less than

INR 5 mn bracket increased

to 78% from 16% YoY

6

1,17,559

93,986

79,178 74,966

48,630 48,800

40,005 37,653

2010 2011 2012 2013 2014 2015 2016 2017

Sales

Sales at an all time low

since 2010, a staggering

68% fall

No. o

f units

7

64,097

40,433

44,979

29,690

20,630 23,800

20,465

H2 2010 H2 2011 H2 2012 H2 2013 H2 2014 H2 2015 H2 2016 H2 2017

Half-yearly salesN

o. o

f units

Sales volume in H2 2017 up

from demonetisation-hit H2

2016, albeit way below 2010

Affordable housing

options and deep

discounts have

helped trickle sales

in Gurugram

GURUGRAMFARIDABAD

GREATER

NOIDA

NOIDA

GHAZIABAD

DELHI

7,853 units

171% YoY

23 units

-54% YoY

23 units

-54% YoY2,885 units

-26% YoY

6,218 units

-8% YoY

3,363 units

11% YoY

133 units

-55% YoY

Quarterly break-up of sales

Micro-marketQ4 2016 sales

(units)

Q4 2017 sales

(units)

YoY

change

Delhi 15 8 -45%

Faridabad 157 47 -70%

Ghaziabad 1,953 1,010 -48%

Greater Noida 2,653 2,176 -18%

Gurugram 958 2,749 187%

Noida 1,030 1,174 14%

NCR 6,765 7,163 6%

Considering all discounts in the

form of stamp duty waivers,

rental schemes, foreign trips,

customised payment plans, the

effective discount has been in

the range of

10-15%

Price change

10

2,780

3,370

3,970

4,330 4,444 4,578 4,250

4,165

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Q4 2010 Q4 2011 Q4 2012 Q4 2013 Q4 2014 Q4 2015 Q4 2016 Q4 2017

-2%YoY

70

80

90

100

110

120

130

140

Residential prices decline by

2% compared to an inflation

growth of 5.5% in 2017

Price divergence widens

11

CPI

NCR

12

NCR is nearly touching the

Knight Frank Affordability

Benchmark* of

4.5

(*house price to income ratio)

2017

52010

6

Unwinding of inventory levels,

QTS running in close ranges

due to slow sales velocity

Unsold inventory declines

13% YoY

Analysis of unsold inventory and QTS

13

1,6

7,0

00

1,9

1,3

70

1,9

5,8

28

2,0

6,0

28

2,0

0,3

98

1,9

2,7

58

1,8

0,3

70

1,6

6,8

31

9.0

12.0

15.0

17.0 17.3 17.418

17.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

- 5

0,0

00

1,0

0,0

00

1,5

0,0

00

2,0

0,0

00

2,5

0,0

00

H1 2014 H2 2014 H1 2015 H2 2015 H1 2016 H2 2016 H1 2017 H2 2017

QT

S

Un

so

ld In

ven

tory

Unsold inventory QTS

FARIDABAD

GREATER

NOIDA

GHAZIABAD

DELHI

QTS – 18 I Age - 14

Unsold inventory – 1,399 units

QTS – 17 I Age - 16

Unsold inventory –

44,793 units

QTS - 19 I Age - 19

Unsold inventory – 27,344 units

QTS - 17 I Age - 20

Unsold inventory – 62,952

units

QTS – 19 I Age - 19

Unsold inventory –

24,825 unitstsNOIDA

QTS - 47 I Age – 17

Unsold inventory –

5,518 units

GURUGRAM

Aging unsold inventory

remains a concern,

highest in India

Overall NCR levels

Unsold units: 166,831

QTS: 17

Age: 18

Age and QTS in quarters

KEY FINDINGS

15

01 03

02 04

Launches down by 93% from

peak in 2010

NCR sees a price correction

for the second time since

2016

Down 2% YoY in 2017

Unsold inventory down

by 13% YoY

Slow sales velocity has had little impact on QTS despite steep fall in new launches

Sales in 2017 dropped

by 6% YoY

• H2 2017 better by 21% from demonetisation-hit H2 2016 on account of base effect

• 17% lower than average H2 sales between 2013-15

• H2 2017 sees a drop of 25% YoY

• 2017 saw 56% fewer launches YoY

16

Transactions held steady

Vacancy level surged to 18% in

H1 2017; DLF CyberCity and Golf

Course Road were at single digit

vacancy

OFFICERECAP H1 2017

17

7.0

8.1

11.5

4.64.1

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2013 2014 2015 2016 2017

New completions

New completions hit a

five-year low

Mn

. S

q. ft.

Project delays hit the office market

as well

Though H2 2017 show an uptick in

new completions, not being in key

locations is a deterrent for

occupiers

18

4.0 4.1

5.5

6.0

2.8

1.8 1.8

2.3

H1 2014 H2 2014 H1 2015 H2 2015 H1 2016 H2 2016 H1 2017 H2 2017

Half-yearly new completions

New completions have been

patchy since 2016

Mn

. S

q. ft.

19

6.60

7.60

7.397.29

6.50

2013 2014 2015 2016 2017

11%YoY

Transactions

Traditionally a robust office

market, NCR records a

sharp fall in 2017

Mn

. S

q. ft.

20

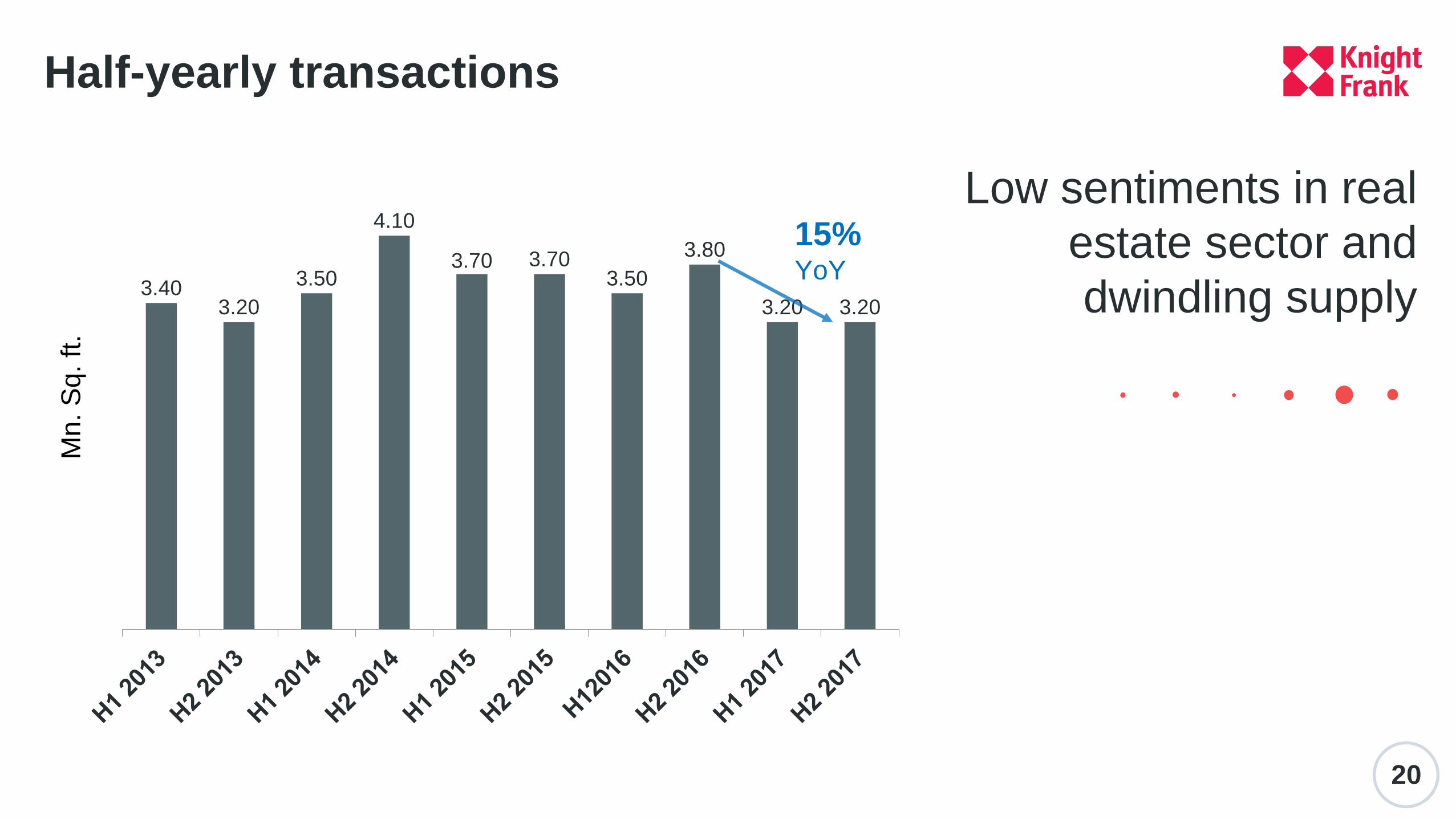

Half-yearly transactions

Low sentiments in real

estate sector and

dwindling supply3.403.20

3.50

4.10

3.70 3.703.50

3.80

3.20 3.20

Mn

. S

q. ft.

15%YoY

21

21.0%

20.0%

21.0%

18.0%

16.0%

15.0%

16.0%

17.0%

18.0%

19.0%

20.0%

21.0%

22.0%

2013 2014 2015 2016 2017

Vacancy

Vacancy levels have

come down as a result

of limited supply

12 month change

Limited supply

exerts pressure on

rentals in select

office areas CBD DELHI

INR 214-350/sq ft/month

2%

NOIDA

INR 44-70/sq ft/month

5%

SBD DELHI

INR 93-163/sq ft/month

6%

FARIDABAD

INR 45-55/sq ft/month

0%

INR 110-165/sq ft/month

5%

GURGAON ZONE C

INR 25-35/sq ft/month

0%

INR 71-134/sq ft/month

5%

GURGAON ZONE A

GURGAON ZONE B

23

Industry H2 2017 H2 2016

BANKING, FINANCIAL

SERVICES &

INSURANCE8% 6%

IT/ITES 28% 15%

MANUFACTURING 28% 23%

OTHER SERVICES 36% 56%

Other services sector takes up 56%

from the overall transaction pie, a

highest since 2015

Share of technology

sector at only 15% in

2017 – the lowest ever

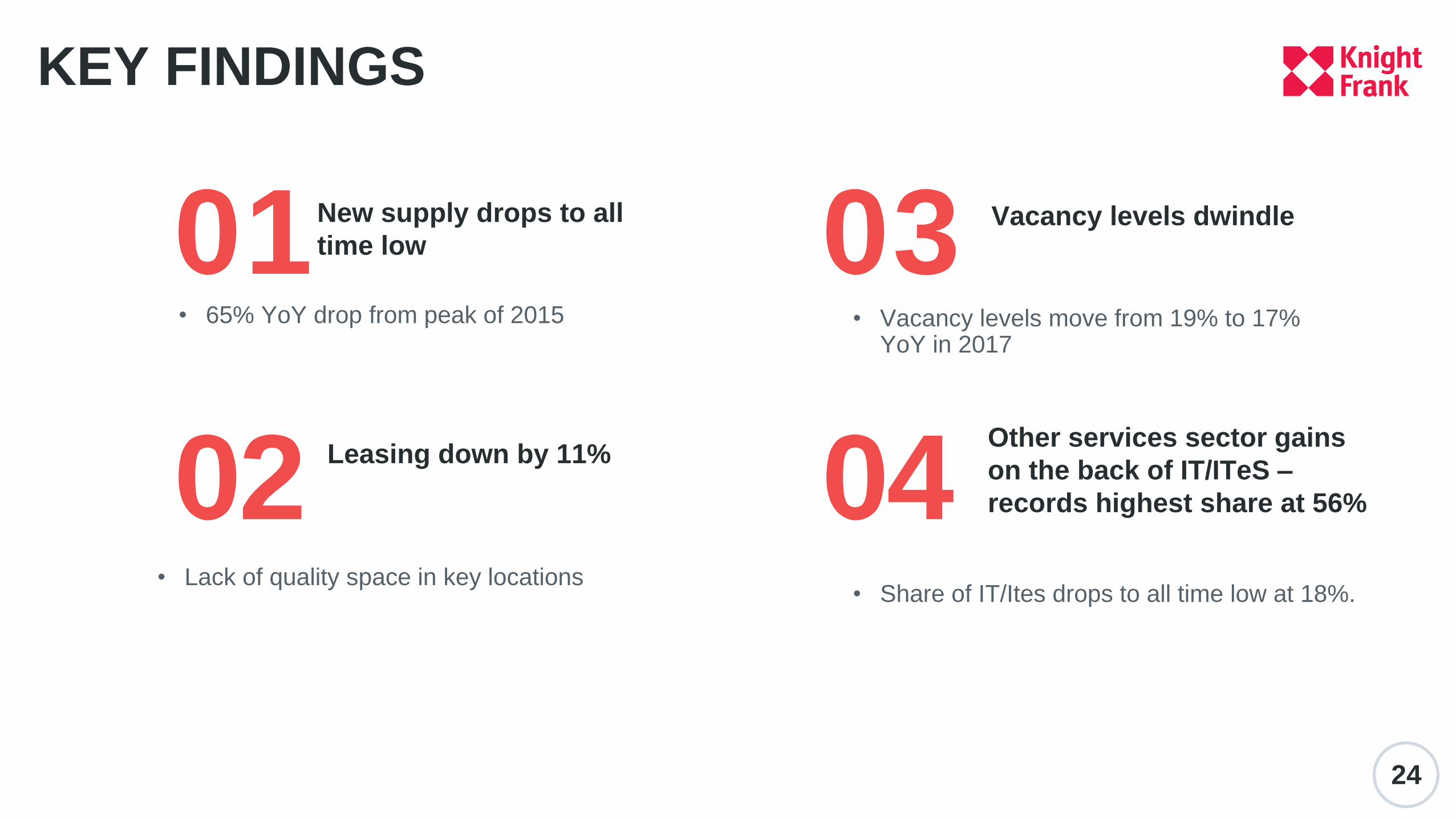

KEY FINDINGS

01 03

02 04

24

New supply drops to all

time low

• 65% YoY drop from peak of 2015

Vacancy levels dwindle

• Vacancy levels move from 19% to 17% YoY in 2017

Other services sector gains

on the back of IT/ITeS –

records highest share at 56%

• Share of IT/Ites drops to all time low at 18%.

Leasing down by 11%

• Lack of quality space in key locations

NCRRESIDENTIAL & OFFICE

In residential segment, NCR sees a price

correction for the second time since 2016

In office market, share of technology sector at

only 15% in 2017 – the lowest ever