national research flagships water for a healthy country ... · gbe global business environment ghd...

TRANSCRIPT

UNCHARTED WATERSInfluences on the Australian urban water sector

Water for a Healthy Country

N AT I O N A L R E S E A R C H

FLAGSHIPS

UNCHARTED WATERSInfluences on the Australian urban water sector

ISBN: 0 643 09248 X

The Water for a Healthy Country National Research Flagship is a research partnershipbetween CSIRO, state and Australian governments, private and public industry and otherresearch providers.

The Flagship was established in 2003 as part of the CSIRO National Research FlagshipInitiative.

The work contained in this report is a collaboration between Nosco Consulting and the Waterfor a Healthy Country Flagship.

© Commonwealth of Australia 2005 All rights reserved.

This work is copyright. Apart from any use as permitted under the Copyright Act 1968, nopart may be reproduced by any process without prior written permission from theCommonwealth.

Citation: Nosco Consulting 2005, Uncharted Waters: Influences on the Australian urbanwater sector. CSIRO: Water for a Healthy Country National Research Flagship, Canberra.

DISCLAIMER

This report has been produced by Nosco Consulting for CSIRO Water for a Healthy Country.

While all due care and attention has been taken to establish the accuracy of the materialpublished, CSIRO and the authors—Nosco Consulting—disclaim liability for any loss whichmay arise from any person acting in reliance upon the contents of this document.

For further information contact:

Ph: 02 6246 4565

Fax: 02 6246 4564

<www.csiro.au>

July 2005

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

iii

Contents

ACKNOWLEDGMENTS .............................................................................................................. v

ABBREVIATIONS ....................................................................................................................... vi

EXECUTIVE SUMMARY ........................................................................................................... vii

Uncharted waters ........................................................................................................................................................................................................... viii

Key influencers ................................................................................................................................................................................................................. viii

1. INTRODUCTION...................................................................................................................... 1

1.1 Aim ............................................................................................................................................................................................................................................ 1

1.2 Approach to developing the paper ...................................................................................................................................................... 1

1.3 Structure ............................................................................................................................................................................................................................. 2

1.4 The seven key influencers ............................................................................................................................................................................2

2. GLOBALISATION AND LIBERALISATION ............................................................................ 4

2.1 A well-connected world .....................................................................................................................................................................................4

2.2 Global trends ................................................................................................................................................................................................................ 5

2.3 Urban water industry global liberalisation and competition ................................................................................... 6

But what if …? ........................................................................................................................................................................................................................ 7

3. PEOPLE AND INSTITUTIONS ................................................................................................ 9

3.1 Cultural values ............................................................................................................................................................................................................ 9

3.2 Governance ................................................................................................................................................................................................................ 10

3.3 Urban water sector institutional liberalisation .................................................................................................................... 11

But what if …? .................................................................................................................................................................................................................... 13

4. POPULATION ........................................................................................................................ 14

4.1 Population size and growth ..................................................................................................................................................................... 15

4.2 Skilled workforce .................................................................................................................................................................................................. 16

But what if…? ...................................................................................................................................................................................................................... 17

5. CLIMATE & ENVIROMENTAL CHANGE .............................................................................. 18

5.1 The environmental trends .......................................................................................................................................................................... 18

5.2 Water use and its environmental impact ................................................................................................................................. 18

iv

5.3 Variability in annual rainfall ...................................................................................................................................................................... 19

5.4 Global warming and sea-level rise ................................................................................................................................................. 19

5.5 Australia’s climate change ........................................................................................................................................................................ 20

But what if …? .................................................................................................................................................................................................................... 21

6. ENERGY AND GREENHOUSE GAS .................................................................................... 22

6.1 Australia’s greenhouse gas emissions ...................................................................................................................................... 22

6.2 Energy supply and price ............................................................................................................................................................................. 22

But what if …? .................................................................................................................................................................................................................... 25

7. SCIENCE AND TECHNOLOGY ............................................................................................ 26

7.1 New technology ..................................................................................................................................................................................................... 26

7.2 Water management – what is possible ..................................................................................................................................... 27

But what if …? .................................................................................................................................................................................................................... 29

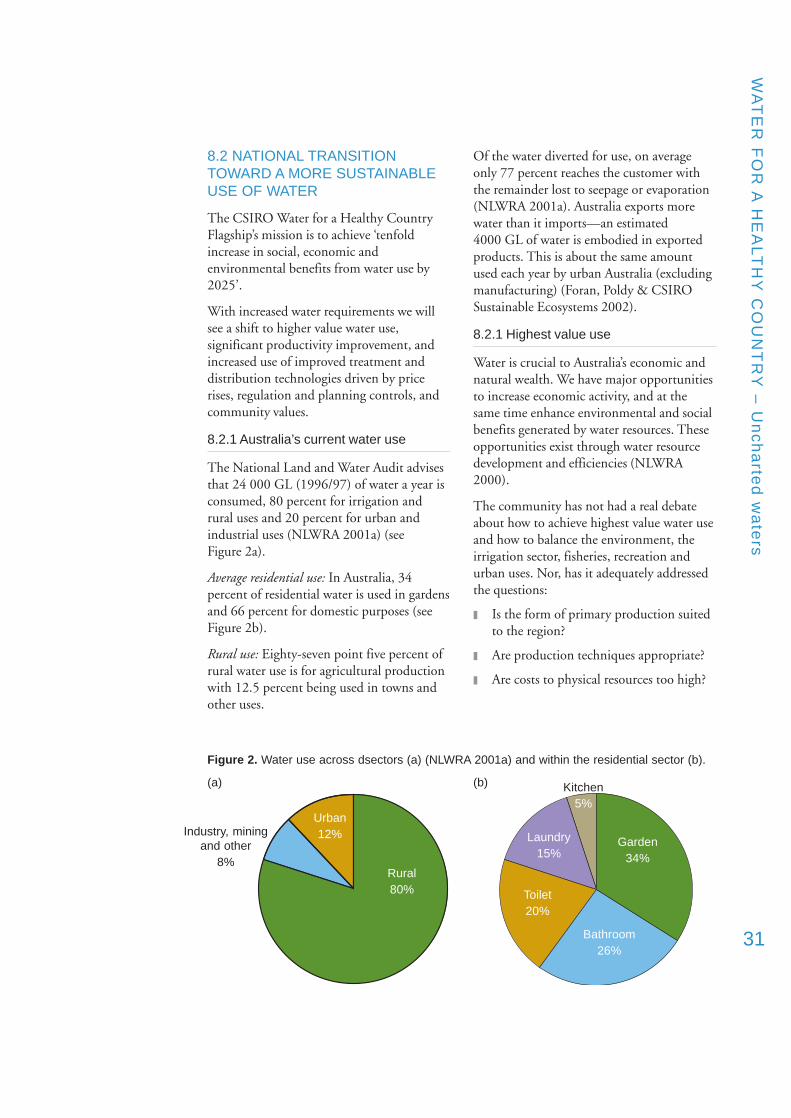

8. WATER USE AND MANAGEMENT ...................................................................................... 30

8.1 Availability and reliability of supply ................................................................................................................................................. 30

8.2 National transition toward a more sustainable use of water ............................................................................. 21

8.3 Water services infrastructure ................................................................................................................................................................ 34

But what if …? .................................................................................................................................................................................................................... 34

9. CONCLUSION ....................................................................................................................... 36

Key influencers ................................................................................................................................................................................................................. 36

APPENDIX A SCENARIOS ....................................................................................................... 39

Shell Global Scenarios ............................................................................................................................................................................................ 39

Sydney Water Corporation ................................................................................................................................................................................. 40

Aspire Australia 2025 ................................................................................................................................................................................................ 41

Water and Sustainable Development, Global Scenarios 2000 – 2050 .......................................................... 41

Watercourse – Navigating Your Utility’s Future .......................................................................................................................... 43

REFERENCES .......................................................................................................................... 44

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

v

We acknowledge CSIRO staff includingNick Abel, Stewart Burn, Steven Cork,Colin Creighton, Chris Davies, Tony Flimer,Barney Foran, Bruce Lee, Ted Lefroy,Shiroma Maheepala, Scott Maves, GraceMitchell, Craig Roy, Brian Ryan, GeoffSyme, John Wright and Mike Young fortheir input and advice.

Other advisors include:

❚ Kevin Goss, Murray Daring BasinCommission

❚ Ross Young, Water Services Associationof Australia (WSAA)

❚ Dr Tony Preistly, CRC Water Qualityand Treatment

❚ Dr Judi Hansen, Sydney WaterCorporation

❚ Dr Cynthia Mitchell, Institute ForSustainable Futures

We acknowledge Carol Howe and Roel Plantfor their direction and editing of this report.

Special thanks to Sydney Water Corporation,Curtin University and Intelligence ScanningNetwork for sharing their scenario planningexperiences and scanning information onurban water management.

Acknowledgments

vi

Abbreviations

AGO Australian Greenhouse Office

BCA Business Council of Australia

CoAg Council of Australian Governments

GBE Global Business Environment

GHD Gutteridge, Haskins & Davey

NGO non-government organisation

NIC National Intelligence Council

NLWRA National Land and Water Resources Audit

OECD Organization for Economic Co-Operation and Development

SARS severe acute respiratory syndrome

UK United Kingdom

UN United Nations

UNESCO United Nations Educational, Scientific and Cultural Organisation

US United States

WSAA Water Services Association of Australia

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

vii

Developing sustainable water managementoptions requires thinking about the future,thinking about:

❚ how community needs and industryoperating conditions may change;

❚ the best strategies for catching theopportunities and managing the threats;and

❚ where to invest.

This is particularly important since untilrecently the water sector has been relativelyinsulated from many of the dramatic changesoccurring in other sectors within theAustralian community.

Stakeholders in the water sector are nowmaking decisions that have long-termimpacts in increasingly volatile conditions.

We view the future as one of opportunitiesthat bring uncertainty and challenges forurban water management.

We are in the midst of a worldwide,revolutionary change, with an uncertainoutcome. Part of the uncertainty has to donot just with events but with humanattitudes and reactions towards those events.People can react with hope and seize theopportunities … or they can react with fearand try and erect barriers to liberalisationto protect what they value.

GBE 2002

Most importantly, we recognise that theurban water sector is an integral part of thewider Australian community, and thereforeinterconnected with the global community.

POSSIBLE FUTURES

We face an infinite number of possiblefutures. This paper is a snapshot, asummation building on the work that othershave done. It discusses the key influencers—the ‘big ticket items’—that are likely to shapeurban water management over the next 20years. These influencers will impact on howsystems work and will cause importantevents and trends to occur.

Selection of the influencers and their specificfactors is based on:

❚ a review of scenarios undertaken by arange of organisations;

❚ a literature search, scanning 20-year plansundertaken by the states/territories andauthorities for the water sector; and

❚ input from researchers and peopledirectly involved in the water and alliedsectors.

Selection was made in the realisation of aneed to look outside the industry itself andpick up those big picture events that maychange the water sector’s present direction.

The purpose of this paper is to provide abasis for scenario planning, a collaborativeprocess, that involves a high level ofstakeholder engagement. It aims to stimulatedebate among urban water managers anddecision makers on the nature of the worldin 2024 and how it will effect planning.

Scenario development provides a mechanismto explore the interaction of the influencersand how they may roll out over time. Toillustrate how this can take shape a selectionof scenarios have been included in AppendixA: scenarios.

Executive summary

SCENARIO PLANNING

Scenarios are not a prediction about the future but tools for thinkingabout the future. Unlike forecasts which impose patterns extrapolatedfrom the present they explore wider possibilities. Scenarios are notprophecies. They incorporate a spectrum of ideas to create coherentand credible alternative stories about the future. Scenario planningis a tool designed to assist us to challenge assumptions, focus on keyuncertainties, understand the key influencers, and test strategies andplans. Scenarios are not about selecting the right ‘forecast’ but aboutaccepting uncertainties and making it part of our thinking.

viii

This paper also includes a series of ‘What if…’ pictures of possible futures that may bedriven by a particular influencer. You areencouraged to develop your own views ofhow the influencers and their interactionsmay create a different future. You are alsoencouraged to consider whether there areother influencers that will cause majordiscontinuities.

All decisions are taken against an uncertainfuture. These decisions can be difficult, as weare often trapped by the values andexperiences that influence our views on whatthe future may be like. Water authoritiesboth public and private, regulators, andgovernments need to choose those strategiesthat are of the most benefit even in differentfutures. This can be made easier by assessingthe options against possible scenarios.

UNCHARTED WATERS

By 2024 the urban water sector will havebeen shaped by significant events. How thoseevents shape the future will be determined bythe Australian community’s social values andits system of governance. These factors willalso be influenced by events.

It will be a bumpy ride to 2024, with manytwists and turns, and there are no road maps.Globalisation, liberalisation and informationtechnology, will make the journey one ofbreakneck speed.

❚ The global community will need to dealwith significant climate andenvironmental changes. These changeswill dominate initiatives in both urbanwater and energy sectors.

❚ Science and new technologies will offerus new choices and opportunitiesespecially in the areas of biotechnologyand information technology.

❚ We will face more pressure to change ourinstitutions and by 2024 the shape ofgovernment and business, and the waythey operate will be quite different.

❚ Australians will be older and there will bemore of us. We can speculate how thismay influence our values and willingnessto engage in the new world.

KEY INFLUENCERS

The seven key influencers for the urbanwater sector look at different possibledevelopments, and consequently new risksand opportunities that the water sectormight face. They have been identified as:

❚ globalisation and liberalisation;

❚ people and institutions;

❚ population;

❚ climate and environmental change;

❚ energy and greenhouse gas;

❚ science and technology; and

❚ water use and management.

These influencers emphasise the‘uncertainties’ rather that the predeterminedelements.

Influencer 1 – Globalisation andliberalisation

The primary shapers of Australia’s future—globalisation, liberalisation and the uptake ofnew technology—are unstoppable. We willbe more interdependent on the globalcommunity, and will experience a period ofrapid change and uncertainty.

Water sector: In 20 years the water sector’soperating environment will be founded onglobal events. Industry direction willincreasingly be determined from ‘outside’ by,for example, non-government organisations,commercial interests or the US. The waterindustry will need to be globally competitiveand adaptable.

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

ix

Influencer 2 – People and institutions

The relative importance of all the changeinfluencers will be determined by thecommunity’s willingness to embrace changeand government structures, together with theway in which they interact.

Water sector: If the Australian Governmentpursues market liberalisation, as a result ofthe Council of Australian Governments(CoAG) reforms and internationalcompetition, can the sector make thenecessary changes to its systems and culture?The risks are:

❚ the entry of global competitors and the‘cherry picking’ of services;

❚ elimination of cross subsidies; and

❚ stranding of assets.

There may be opportunities to re-position orconverge to form multi-utilities, or theindustry may move towards multipleparticipants with a distributed infrastructurenetwork.

Influencer 3 – Population

Australia’s population will increase and age.At the same time, populations in theunderdeveloped countries will grow fasterand be younger. The combination ofpopulation growth and urbanisation willfoster instability in neighbouring countries.Australia is at risk of a ‘brain drain’ withyoung people moving oversees.

Water sector: There is likely to be a growthand change in demand for urban waterservices, particularly along the east coast. Theindustry is likely to suffer a shortfall of skillsduring a period of rapid change.

Influencer 4 – Climate and environmentalchange

Exact impacts of global warming areuncertain—Australia is likely to be hotterand dryer, with more extreme weatherconditions.

Water sector: There will be an increaseddemand for water, reduced yields andincreased variability.

Influencer 5 – Energy and greenhousegas emissions

Australia will have sufficient energy to meetdemands for population and economicgrowth. However, environmentalconsiderations will dominate the energysector’s initiatives. Advances are being madeto increase efficiency in energy production,and to develop sustainable alternative energysources. We could become a hydrogensociety.

Water sector: The water sector is likely toexperience some increases in prices forenergy, but prices may become volatile. Theindustry will be accountable for itsgreenhouse gas emissions.

Influencer 6 – Science and technology

The next 20 years will see a further spread ofinformation technology and the applicationof new bio-technologies. Nano-technology,sensor technologies and bio-markers offer anextraordinary range of applications andbenefits.

Water sector: The use of bio-technology toinfluence landscape-scale ecological process,improved efficiencies in water use,breakthroughs in membrane technology,solutions for local retention of stormwaterand sewage disposal, will create new ways ofdelivering water services.

x

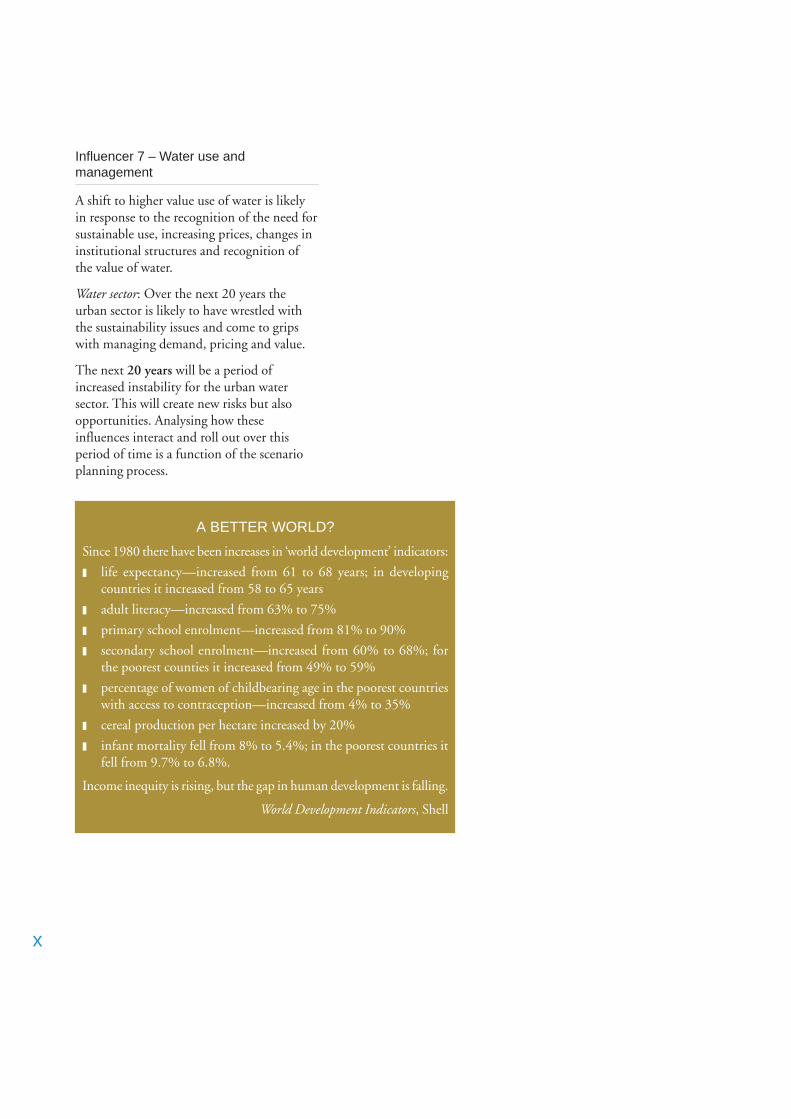

Influencer 7 – Water use andmanagement

A shift to higher value use of water is likelyin response to the recognition of the need forsustainable use, increasing prices, changes ininstitutional structures and recognition ofthe value of water.

Water sector: Over the next 20 years theurban sector is likely to have wrestled withthe sustainability issues and come to gripswith managing demand, pricing and value.

The next 20 years will be a period ofincreased instability for the urban watersector. This will create new risks but alsoopportunities. Analysing how theseinfluences interact and roll out over thisperiod of time is a function of the scenarioplanning process.

A BETTER WORLD?

Since 1980 there have been increases in ‘world development’ indicators:

❚ life expectancy—increased from 61 to 68 years; in developingcountries it increased from 58 to 65 years

❚ adult literacy—increased from 63% to 75%

❚ primary school enrolment—increased from 81% to 90%

❚ secondary school enrolment—increased from 60% to 68%; forthe poorest counties it increased from 49% to 59%

❚ percentage of women of childbearing age in the poorest countrieswith access to contraception—increased from 4% to 35%

❚ cereal production per hectare increased by 20%

❚ infant mortality fell from 8% to 5.4%; in the poorest countries itfell from 9.7% to 6.8%.

Income inequity is rising, but the gap in human development is falling.

World Development Indicators, Shell

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

1

1. Introduction

1.1 AIM

We all need to plan for the future. The urbanwater sector faces many uncertainties andpossible different futures—it may betransformed by issues that are bothconceivable and inconceivable at this presentpoint in time. Water authorities, businesses,regulators and governments need to selectstrategies that can create benefits even in verydifferent futures.

The aim of this discussion paper is tostimulate debate among urban watermanagers and decision makers on the natureof the world in 2024 and how it will effectplanning.

It identifies the influencers—the processesthat have a high influence on how systemswork, and that cause important events andtrends to occur. Almost all processes are bothinfluenced and influence other processes.They are the forces that will shape theenvironment. Those that will persist and canbe forecasted, and how change may occur isunknown.

1.2 APPROACH TO DEVELOPINGTHE PAPER

We face an infinite number of possiblefutures. This paper is a snapshot, asummation building on the work that othershave done. Selection of the influencers andtheir specific factors included in this paperemerged from:

❚ a review of scenarios undertaken by anumber of water and other organisations(national and international);

❚ a review of studies on trends;

❚ literature research;

❚ scanning of 20-year plans undertaken bythe states/territories and authorities forthe water sector; and

❚ input from researchers and peopledirectly involved in the water and alliedsectors.

Selection of the influencers was made in thecontext of a recognition of a need to lookoutside the water sector and pick up thosebig picture events that may change theindustry’s view of the direction of the sector.Trends and predetermined events that arewell understood by the water industry andhave been already been incorporated in theirlong-range plans were not included.

From the outset, the research sought toidentify:

❚ those issues about the future that couldturn the water sector upside down;

❚ what is making people feel enthusiasticand optimistic; and

❚ what is keeping them awake at night.

This paper discusses the key influencers or ‘big ticket items’ that are likely to shape urbanwater management over the next 20 years.

2

The selection was also made with the viewthat it is more productive to focus on asmaller range of key influencers.

Some of the predicted key influencers arealso based on trends that have an importantdegree of uncertainty. In contrast,judgements about the environment, climate,governance, and community attitudesrepresent a distillation of views of expertsfrom inside and outside CSIRO. These arematters for speculation as they arecontingent on the decisions that societies andgovernments will make.

Scenario planning is a collaborative processand one that involves a high level ofstakeholder engagement. The purpose of thispaper is to provide a basis for that process. Itis suggested that next steps towardsdeveloping scenarios should be:

1. agreement through consensus on theselection of the factors grouped withininfluencers;

2. development of exploratory firstgeneration scenarios to give insight intothe system, to identify predeterminedelements, and to understand theconnection between various forces andevents influencing the system;

3. detailed research (with a focus on gaininginsights) on some of the influencers andtheir uncertainties to gain a betterunderstanding of the forces that willeventually compel an outcome and theirinterplay; and

4. next generation scenarios or constructionof decision scenarios so that decisionmakers question their own views ofreality.

1.3 STRUCTURE

The structure of this paper is based on theseven-key influencers, with a section for eachinfluencer. Each section explores the ‘bigticket items’ the main factors that relate tothe influencers, and asks questions abouthow these factors may change the urbanwater sector or its strategies.

Hypothetical ‘What if …’ pictures ofpossible futures that may be driven by aparticular influencer are included at the endof each section. Readers are encouraged todevelop their own views of how theinfluencers and their interactions may createa different future. They are also encouragedto consider whether other influencers orfactors may cause major discontinuities.

Appendix A Scenarios provides summaries ofsome scenarios to illustrate how the variousinfluencers could play out in the future.

1.4 THE KEY INFLUENCERS

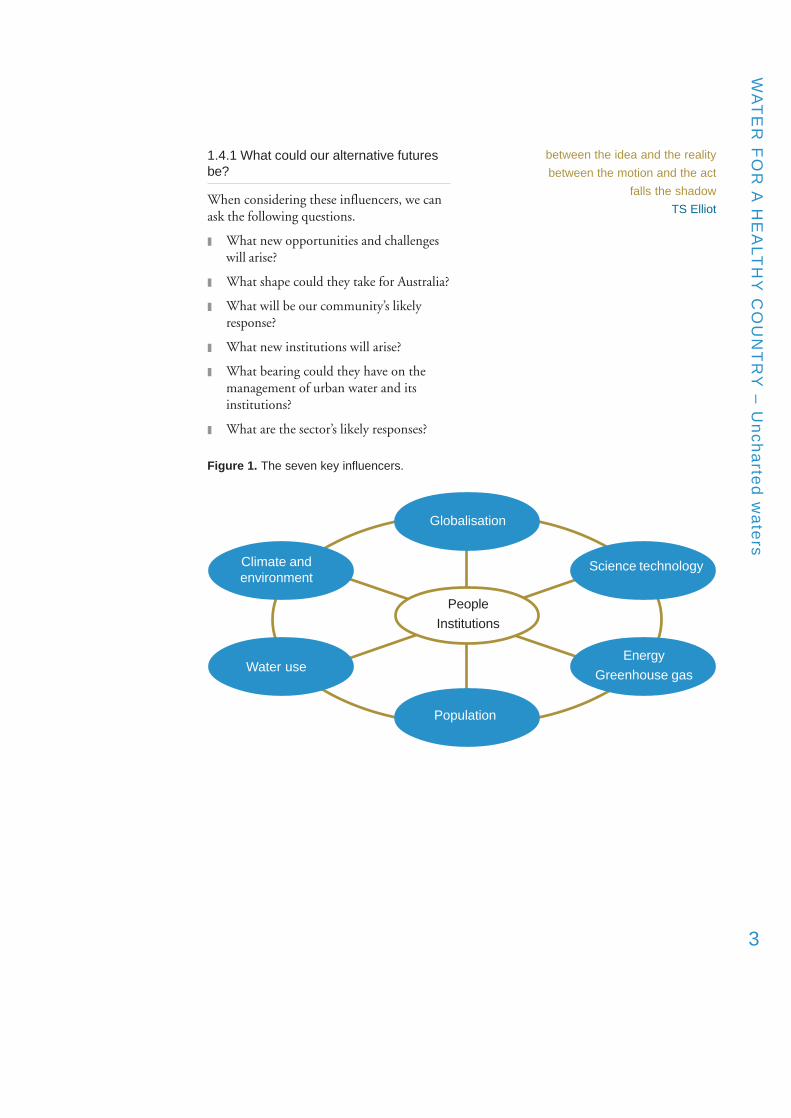

By 2024, water management in Australia islikely to be shaped by seven main influencers(see Figure 1):

❚ globalisation and liberalisation;

❚ people and institutions;

❚ population;

❚ climate and environmental change;

❚ science and technology;

❚ energy; and

❚ water use and management.

These influencers are interdependent and areplausible drivers. They are as much aboutopportunities that, if captured, willtransform the water sector, as about over-the-horizon problems.

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

3

1.4.1 What could our alternative futuresbe?

When considering these influencers, we canask the following questions.

❚ What new opportunities and challengeswill arise?

❚ What shape could they take for Australia?

❚ What will be our community’s likelyresponse?

❚ What new institutions will arise?

❚ What bearing could they have on themanagement of urban water and itsinstitutions?

❚ What are the sector’s likely responses?

between the idea and the reality

between the motion and the act

falls the shadow

TS Elliot

Figure 1. The seven key influencers.

Globalisation

Climate andenvironment

Water use

Population

Energy

Greenhouse gas

Science technology

People

Institutions

4

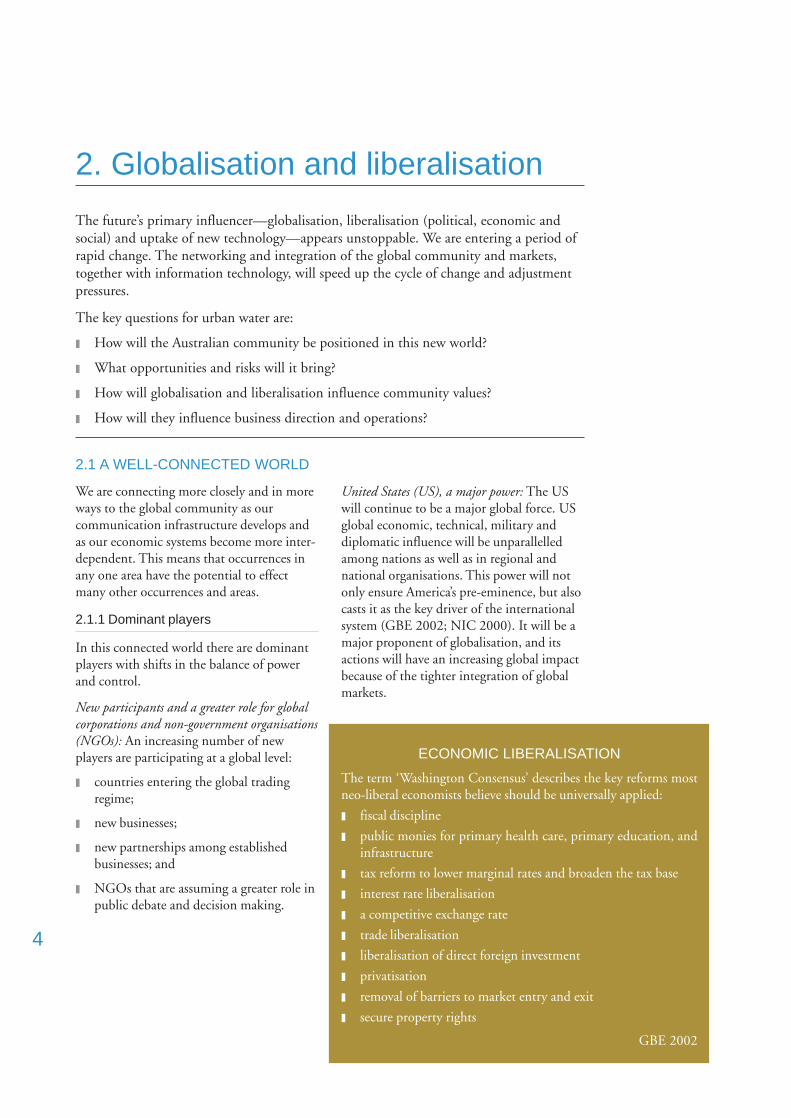

The future’s primary influencer—globalisation, liberalisation (political, economic andsocial) and uptake of new technology—appears unstoppable. We are entering a period ofrapid change. The networking and integration of the global community and markets,together with information technology, will speed up the cycle of change and adjustmentpressures.

The key questions for urban water are:

❚ How will the Australian community be positioned in this new world?

❚ What opportunities and risks will it bring?

❚ How will globalisation and liberalisation influence community values?

❚ How will they influence business direction and operations?

United States (US), a major power: The USwill continue to be a major global force. USglobal economic, technical, military anddiplomatic influence will be unparallelledamong nations as well as in regional andnational organisations. This power will notonly ensure America’s pre-eminence, but alsocasts it as the key driver of the internationalsystem (GBE 2002; NIC 2000). It will be amajor proponent of globalisation, and itsactions will have an increasing global impactbecause of the tighter integration of globalmarkets.

2. Globalisation and liberalisation

ECONOMIC LIBERALISATION

The term ‘Washington Consensus’ describes the key reforms mostneo-liberal economists believe should be universally applied:

❚ fiscal discipline

❚ public monies for primary health care, primary education, andinfrastructure

❚ tax reform to lower marginal rates and broaden the tax base

❚ interest rate liberalisation

❚ a competitive exchange rate

❚ trade liberalisation

❚ liberalisation of direct foreign investment

❚ privatisation

❚ removal of barriers to market entry and exit

❚ secure property rights

GBE 2002

2.1 A WELL-CONNECTED WORLD

We are connecting more closely and in moreways to the global community as ourcommunication infrastructure develops andas our economic systems become more inter-dependent. This means that occurrences inany one area have the potential to effectmany other occurrences and areas.

2.1.1 Dominant players

In this connected world there are dominantplayers with shifts in the balance of powerand control.

New participants and a greater role for globalcorporations and non-government organisations(NGOs): An increasing number of newplayers are participating at a global level:

❚ countries entering the global tradingregime;

❚ new businesses;

❚ new partnerships among establishedbusinesses; and

❚ NGOs that are assuming a greater role inpublic debate and decision making.

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

5

South-east Asia’s growth and stability:Emerging Asia will be the fastest growingregion, led by China and India, whoseeconomies already comprise roughly one-sixth of global GDP (NIC 2000). Howstable is our region? Potentially it providesunimaginable economic growthopportunities, and the stability and nature ofthe relationships will be of great importance.

Governments: Governments will have lesscontrol over flows of information,technology, migrants, arms and financialtransactions, whether licit or illicit acrosstheir borders. The quality of governancenationally and internationally willsubstantially determine how well states andsocieties cope with the global forces (NIC2000).

2.1.2 Pandemic disease

A well-connected world will further opentrade and increase movement of people.Global cooperation has shown to be effectivein controlling outbreaks of disease such assevere acute respiratory syndrome (SARS),although an increase in movement of peoplewas part of the reason for the threat andcould also introduce new pests and diseasesto humans, livestock and plants to Australia.In developing countries, the exposure ofpeople to ecosystems previously isolated fromhumans, together with human cohabitationwith stock and captive wild animals, increasethe risk of new diseases.

2.2 GLOBAL TRENDS

Possibly the most significant anticipatedtrends for the urban water sector are waterscarcity and economic growth.

MILLENNIUM DEVELOPMENT GOALS

Goal 7 Target 9: Integrate the principles of sustainable development into country policiesand programs and reverse the loss of environmental resources.

Goal 7 Target 10: By 2015 to halve the proportion of people without sustainable access tosafe drinking water and basic sanitation.

UN Millennium Project 2005

At least 1.1 billion people lack access to safewater, and 2.4 billion lack access to basicsanitation, a silent humanitarian crisis thateach day takes thousand of lives, robs thepoor of their health, thwarts progress towardgender equality, and hamstrings economicdevelopment, particularly in Africa and Asia.

UN Millennium Project 2004

Water scarcity: Globally, the withdrawal ofwater supplies is projected to increase by atleast 50 percent by 2025 (UN 2004). By2015, nearly half of the world’s population,will live in water-stressed countries (i.e. nomore than 1.7 ML of water per person peryear) mostly in Africa, the Middle East,South Asia, and Northern China (NIC2000). The United Nations advised:

... faced with inertia at the leadership levelthe global water crisis will reachunprecedented levels in years ahead withgrowing per capita scarcity of water inmany parts of the developing world …water resources will steadily decline becauseof growth, pollution and expected climatechange.

UNESCO 2003

Economic growth: It is predicted that overallthe global economy will return to the highgrowth levels of the 1960s and early 1970s.Political pressures for higher living standards,improved economic policies, rising foreigntrade and investment, diffusion ofinformation technologies, and anincreasingly dynamic private sector will drivethis change. Brakes on the economy, such asa substantial financial crisis or prolonged

6

disruption of energy supplies, may undo thisprojection. Regions, countries and groupsleft behind will face stagnation, politicalinstability and cultural alienation. The gulfbetween the haves and have-nots will widen.This will foster political, ethnic, ideologicaland religious extremism, along with theviolence that often accompanies it (NIC2000).

2.3 URBAN WATER INDUSTRYGLOBAL LIBERALISATION ANDCOMPETITION

The water sector is actively involved in theglobalisation and liberalisation processes.Over the past two decades, there has been adramatic growth in the privatisation of waterinfrastructure. By 2000 an estimated 93countries had privatised water or wastewaterservices, or were in the process of doing so.This included countries in North and LatinAmerica, the Caribbean, Europe, Africa, andthe Middle and Far East (Friend et al.2003b).

The focus of major international watercompanies is expansion and growth. This isdriven by the investment appeal of the waterindustry with its positive profit performance,and the need for infrastructure developmentin many third world countries (Friend et al.2003b).

The industry provides significant profits tothe three key players in the world marketnamely Vivendi Universal, Suez and RWE.Each is among the top 100 corporations.Their revenues are estimated to grow by tenpercent per year...

Friend et al. 2003b

There is a growth in alliances andinvolvement in public-private partnership.Competitiveness and acquisitions are alsofeatures. As an example, it appears that E.Onand RWL are aggressively competing forleader status in Germany. In the UnitedKingdom (UK), it is evident that watercompanies are responding to the regulatedwater industry with a growing interest innon-regulated ventures. Multi-utilities areemerging (Friend et al. 2003b).

Within this context there will be increasingexternal pressure on Australia to pursue theCoAG water reforms, creating opportunitiesfor new market entrants.

In 2003, profitability was a problem for 50percent of major Australian water companiesdespite increased revenues for most. Theongoing drought is unlikely to help asreduced water supply and restrictions impacton revenue (Friend et al. 2003b). This canmake them vulnerable in the longer term.

Increased liberalisation and competitionmeans that organisations not only need toimplement best practice, but also need tooperate in a strategic and commercialmanner to sustain profitability and marketshare. Those that cannot adapt quickly will‘go under’.

How many of you believe that you will be bought, sold, merged or affiliated with a public orprivate organisation within the next 15 years? You realize up until three months ago there werefour mega firms, each with a goal of owning or controlling 30 percent of the world’s water andwaste water infrastructure within one or two decades? Now there are only three. One bought upthe fourth.

Steve Gordon AWWA President, AWWA Mainstream, July 1999

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

7

Australia’s international position

Australia becomes a world leading nation:What if Australia’s international statusincreases and it becomes the second mostpowerful nation (after the US). This isachieved through its agility in adapting toglobal events, speed in applying newtechnology and its ‘national competitiveness’(its dynamic institutions, state-of-the-artenvironmental management practices androbust physical infrastructure). In additionAustralia leverages its other strengths—excellence in education, science andtechnology, cultural diversity, and abundant‘clean’ natural resources. It sets the globalenvironmental and water managementagenda, and provides technologicalleadership.

Australia hands over its sovereignty: Imaginethat Australia becomes the fifty-first state ofthe United States or, because of itsgeographical position and high proportion ofAsian born residents (following an increase inimmigration), Australia becomes a memberof a powerful Asian federation. Thefederation controls trade, security,international policy, and environmentalsustainability.

Australia disconnects from the world: What ifAustralia withdraws from the globalcommunity as a ‘revolt’ against the externallyimposed rate and direction of change. As thegap between the ‘haves and have-nots’widens, with few benefiting from the globalconnections. Australians attempt to re-createthe ‘good old days’. We retreat within ourborders, restricting the movement of people,produce, finance and communications.Government is concerned about losingcontrol and centralises its decision making.Australia fails to adapt and keep up. Oureconomic wealth falls.

The world disconnects from Australia. Imaginethat relationships between nations breaksdown. War spreads beyond the Middle Eastand splits the community into two opposingsides, creating a ‘Korea-type relationship’ ona global scale. Trade and communicationsbetween the sides cease. Countries try tocheck US dominance. The US assumes a lessbenign control of power, pursuing theirinterests at the expense of all.

BUT WHAT IF …?

Imagine alternative futures where:

❚ Australia becomes a world-leading nation;

❚ Australia hands over its sovereignty;

❚ Australia disconnects from the rest of the world;

❚ the rest of the world disconnects from Australia;

❚ international scarcity of potable water results in the creation of an internationaltrading market;

❚ the Australian water sector becomes a world leader; or

❚ the water sector operates in a hostile environment.

8

The water sector

International scarcity of potable water: What ifwater scarcity results in the creation of aninternational trading market with watertraded as either a bulk commodity orembodied in high input products such as riceor milk. The value of the traded goods wouldreflect their embodied water content.Demand for irrigation would increase withan increase in the production of the highwater content produce.

Australian water sector becomes a world leader:Imagine that the Australian water industrydevelops a leading position in sustainable,integrated water management, energy useand infrastructure design. The sustainabledelivery of low cost, reliable water underpinsAustralia’s economic and social growth. Thewater industry too enters the internationalmarket making a significant contribution toAustralia’s wealth.

Water sector operates in a hostile environment:Imagine that with rising internationalconflict Australia becomes more vulnerableto terrorism requiring additional defenceexpenditure. Funding for capital investment,science and technology becomes scarce.There is a decline in water quality andconcerns about its security, and servicesbecome unreliable.

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

9

3. People and institutions

Australia’s people and institutions will shape its future. They will determine the relativeimportance of the influencers through their capacity and willingness to embrace change,together with the way in which they interact.

Can Australia’s national culture and current system of government and public policydevelopment seize the opportunities and cope with the challenges ahead? If not, areAustralians capable of making fundamental changes that will work to both culture andstructure (Wayne Goss cited in BCA 2004)?

The key questions for urban water are:

❚ What will the community expect of water institutions and services?

❚ How far will governments pursue the reform agenda?

❚ How will stakeholders respond?

❚ What business enterprises will enter the marketplace?

3.1.1 How do we view water and theenvironment—as commodities or associal goods?

Water is not ‘respected’ or valued by theAustralian community generally. While waterand the environment are regarded asimportant, will policy be more pragmaticthan idealistic? Or, will the impendinginternational water scarcity or globalwarming change our views on itsmanagement and use?

Since a considerable amount of urban wateris used for recreational purposes, such asgardening and community parks, there is aview that water demand needs to beconsidered a social issue.

Water should be treated as a social andcultural good, and not primarily as aneconomic commodity. This presents adifferent view from decisions taken atseveral international forums in the 1990s,

The rate of change is so rapid it is just about the only certainty remaining; that there will bechange and there will be further change ... as Islam is demonstrating, human beings aren’talways happy with change and may revolt against it, even preferring a lower standard of livingfor the certainty of not changing any more. Change is exhausting.

Pru Goward Federal Sex Discrimination Commissioner

3.1 CULTURAL VALUES

How will people respond to future opportunitiesor challenges?

Most Australians have an optimistic outlookon our capacity to respond to challenges. Butare we looking through rose coloured glasses?

... people often do not act in the rational,self interested way they are ‘supposed to’ ineconomic theory ... People have a way ofupsetting the status quo, especially if theyact together under the force of deeply heldvalues galvanised by a new ideal or by newcircumstances – or when they feelthreatened.

GBE 2002

10

in which water was judged to be aneconomic commodity, reflecting a shifttowards market-based policies that reflectthe true cost of water, reduced subsidies andpossibly engage the private sector in watersupplies.

United Nations 2003

There is a view that water should flow to thehigher value use. However, tension existsbetween the demand for irrigation, forenvironmental flows and for urban supply.Increasingly urban and environmental usemay be considered to have the ‘higher value’.What would be the implications be forprimary producers? Alternatively, howwilling will the community be to embracefurther restrictions or changes in waterquality?

3.2 GOVERNANCE

The willingness and capacity of governmentsand its institutions to undertake a concertedeffort to sort out longer-term problems is akey influencer.

Do Australians accept that their future willbe profoundly influenced by factors such asour ageing population, globalisation,security issues and the strength of oureconomy? .Of course we have to addunpredictable events such as the worldexperiencing SARS and the September 11manifestation of asymmetric warfare.Australia cannot prevent such events. Thequestion is what will be the quality ofresponse from our system of governance andpolitics? The answer comes back to theleadership of the Australian nation—notonly political but also business, media andthe community?

Wayne Goss cited in BCA 2004

3.2.1 Institutional and structural changefatigue

Australia’s structural reform over the last 30years has covered almost every aspect ofeconomic activity. Key areas of reforminclude the labour market, tariff reductions,the exchange rate and financial sector,corporate governance, taxation, nationalcompetition policy, the public sector, andframeworks for monetary and fiscal policy(BCA 2004).

The reform dividend is evident in the highrates of productivity and economic growthachieved, especially relative to experiences ofmany other countries. This success wasneither guaranteed nor was it a result of luck.

A considerable amount of reform remains tobe undertaken, and new issues arecontinually arising.

However, there is an increasing level ofreform fatigue in the community, andevidence of some leaders stepping back fromfurther reform. While some Australianswelcome reform relief, ultimately Australia’sfuture will be diminished if it steps back.

Wayne Goss cited in BCA 2004

3.2.2 Quality of Australia’s institutions

Countries with competent governance willreshape traditional government structures tobetter engage a more complex andinterconnected world. States with ineffectiveand incompetent governance will not onlyfail to benefit from globalisation but in someinstances will spawn conflicts at home andabroad, ensuring an even wider gap betweenregional winners and losers than exist today(GBE 2002).

Effective governance will increasingly bedetermined by:

❚ the ability and agility to formpartnerships to exploit increasedinformation flow;

❚ new technologies;

❚ migration; and

❚ the influence of non-state actors (GBE2002).

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

11

Responsibilities of semi-autonomousgovernment agencies will increasinglyintersect because of the transnational natureof priorities and requirements forinterdisciplinary policy responses.

3.2.3 Capacity of Australia’s institutions

Governance of democracies can only becomemore difficult.

Globalisation will increase transparency ofgovernment decision making …complicating the traditional deliberativeprocesses of democracies. Social decisions aremediated by institutions that were designedfor a slower, more methodical approach tosolving problems, and these problems wereassumed to come one by one.

The short-term nature of electoral cycles,inevitably bestows upon governments ashort-term outlook, now strongly reinforcedby the media’s rapid news cycle andcommunity expectations that problems canbe fixed immediately. Prevention forexample is not sexy in politics.

Goward 2003

Can the three tiers of government worktogether for the benefit of the nation? Willinefficiencies and duplication betweengovernments threaten Australia’s capacity forgrowth and social well being?

Many of Australia’s current environmentalproblem, have as acutely exacerbatingfeatures the overlapping responsibilities ofLocal, State and Federal Governments.Land clearing deteriorating condition of theMurray–Daring Basin are good examples ofproblems that cry out for the resolution ofoverlapping responsibilities for services andthe uncoordinated approaches to regulationand standards setting.

Michael Rae cited in BCA 2004

Environmental problems, especially waterallocation and greenhouse gas emissions areadressed on a piecemeal basis. Thegovernments each put money into water andenergy-related issues without a coordinatedeffort to sort out the longer-term problems.

3.2.4 Regulation and control

People want the efficiencies that marketliberalisation brings. They also wantappropriate government regulation. Many ofthe traditional approaches to regulating theeconomy and institutions will becomeincreasingly difficult to preform. The rate ofchange and its unpredictability in a globaleconomy requires a new way of ‘running theshop’, with new rules to manage theunwanted consequences of change.

3.3 URBAN WATER SECTORINSTITUTIONAL LIBERALISATION

In 1994, CoAG recognised the need forwater management reform and agreed toimplement a reform framework (ReformFramework). Still in its early days, the focushas been on getting the Reform Frameworkinto place and cost reductions. Most of thereal implications of these reforms are yet tobe played out. Far reaching changes arepredicted for the urban water sector forexample:

Pricing of services: Full cost pricing of allwater and wastewater services (including aprovision for environmental cost), as well asan unwinding of cross-subsidies (e.g.customers could pay different prices basedon their specific service delivery costs, timeof use and water quality) may be introduced.

Consumers will have come to terms with thefact that the days of cheap subsidised waterare coming to a close.

Prof Alan Fels, Chairman AustralianCompetition Commission

12

Marketisation of the sector: It is anticipatedthat:

❚ there will be new entrants under the ‘newaccess regime’ with competitors accessingexisting facilities;

❚ customers may have a choice of serviceproviders;

❚ full privatisation may occur;

❚ a further carving-up of businesses basedperhaps on geography, integrating thewater cycle elements, or infrastructurewill occur.

Increasingly water authorities may not wantto retain control of all aspects of watermanagement or may want to expand theirportfolios (e.g. they may re-positionthemselves as public health authorities).

Competition in other infrastructureindustries is driving convergence towards theprovision of multi-utility services.

In whichever direction the sector goes, it islikely that there be more providers, anincreased sophistication and a simplificationof the business.

Innovation and technical change:Liberalisation creates opportunities forinnovation and technical change—oldconstraints may be freed to create morediverse ways to deliver customer services.Changes in water delivery are expected and itis speculated that there will be greater localcontrol, management and service delivery toreduce risks and costs, and improvesustainability.

It is clear that whatever the water industrydoes, there will be rapid change with a movetoward a very different approach to servicedelivery. The Reform Framework will createnew dynamics for policy makers andregulators and will increase business risk and,in particular, the risks of assets beingstranded and the ‘cherry picking ofcustomers’.

While significant progress has been made,the Reform Framework is unlikely to meet itsimplementation target date of 2005. Ruralwater management reform is especiallylagging.

In Services Sydney Pty Ltd’s application to the National CompetitionCouncil for a recommendation to declare Sydney WaterCorporation’s transmission of sewage services and a service forconnection of new truck main service, it proposes to:

❚ establish a new state-of-the-art water reclamation plant; and

❚ construct water conduits to return tertiary treated water for otheruses.

The company will compete for customers principally on the basisthat its effluent treatment would be more environmentally friendlythan the ocean outfall system used by Sydney Water. Its pricingstructure is expected to be similar.

<www.ncc.gov.au>

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

13

Australia’s response to change

No change: Imagine if Australia’s governmentshave not been able to embrace the changeand where we are unable to achieveagreement on problems or the way forward,different levels of government are blamingeach other (BCA 2004). There is a lack oftrust between the people and governmentand social unrest. Short-term attitudesflourish with no concerted effort bygovernment to pursue long-termopportunities or sort out the longer-termproblems.

Australia’s institutions change: What ifAustralia has a stronger and more centralisednational government; state/territorygovernments are abolished? Alternatively,Western Australia and Queensland cede fromthe Australian federation.

Water sector

A MacWater takes over the Australian urbanwater market: An international watercompany experiences flat profits in itsprimary market and decides to expand intoother enterprises. ‘MacWater’ diversifies intoland development. A major breakthrough inwater treatment technology allows MacWaterto offer a better and cheaper service, withfranchised management of development sites

including local water service provision. Itsreal competitive advantage is its leadership incustomer knowledge, managing theenvironmental impact of its operations andcost efficiency. It is very successful andeventually takes over the urban waterindustry. Governments subsequently have avery small role in the delivery of essentialservices and the industry becomes self-regulating.

International market dominated by oligopolies:Globally the entire water market is corneredby a few mega-corporations, which colludeand act as aggressive oligopolies excludingnew entrants, and manipulating supply andprices. Australia’s water utilities adopt a ‘headin the sand’ approach. A corporation entersthe Australian market ‘cherry picking’ theservices it provides. The expensive lessprofitable services are left in the publicdomain. Their costs climb or the authoritiesbecome unviable, as their fixed overheadcosts are covered by a smaller customer base.Governments are forced to heavily subsidisethe water industry to ensure equity and basicservice provision to all citizens. Thecorporation subsequently provides small localtreatment plants, further stranding the largercentralised infrastructure system.

BUT WHAT IF …?

Imagine alternative futures where:

❚ no change occurs;

❚ Australia’s institutions change;

❚ a MacWater takes over the Australian urban water market; or

❚ the international market is dominated by oligopolies.

14

Australia’s future will be shaped by changes to local and global populations. Populationchanges:

❚ trigger changes to social values and community needs;

❚ trigger demand for goods, services and resources; and

❚ have environmental impacts.

Our demographic profile relative to those of our neighbours influences our relationships,and has economic and social implications.

The Australian Bureau of Statistics advised that:

The growth of the world’s human populations and its increasing demand for limited globalresources is a key issue for citizens and governments throughout the world. This is coupledwith evidence that many of the life support systems that make-up our natural environmentis being degraded by human activity and continued population growth will add to thepressure experienced by these systems.

ABS 2001

The key questions for urban water are:

❚ How can we provide for urban growth and meet higher environmental and publichealth standards?

❚ How will businesses manage a skills shortage at a time when they need to draw upon asolid skills and knowledge base to meet the challenges?

4. POPULATION

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

15

4.1 POPULATION SIZE ANDGROWTH

The world’s demographic balance ischanging: in the future there will be morepeople and in the developed countries thosepeople will be older.

4.1.1 Global population

Global population will increase from today’s6.4 billion to 7.8 billion in 2024 (U.S.Census Bureau 2004). Ninety-five percent ofthe increase will be in developingcountries—mainly in rapidly expandingurban areas—where political systems arebrittle. The combination of populationgrowth and urbanisation will fosterinstability (NIC 2000).

In developed countries, growth seems to havesettled at virtually zero. According to theUnited Nations 2003 projections, theaverage fertility rate in the more developedcountries is 1.6 (Australia’s is 1.7), while therate in the less developed countries is 2.9, theworld average is 2.7 (ABS 2003b).

4.1.2 Australia’s population

Population growth: Concerns have beenexpressed about the optimal population size.Estimates of Australia’s carrying capacity varyconsiderably, ranging from hundreds ofmillions to less than the current number ofpeople (ABS 2001). This issue remainsunresolved.

Australia’s June 2002 population of 19.7million is projected to grow to between 22.3to 24.6 million by June 2021. Fertility andmigration have the greatest impact on thisgrowth. Immigration is a more significantdriver as large changes in birth rates wouldbe needed to impact on total births (ABS2003b).

Ageing population: Over the next 20 yearsageing and retiring baby boomers presents achallenge. The additional pressure on the taxand welfare systems will be supported byfewer taxpayers and this will slow downeconomic growth. In 2002, 13 percent of thepopulation was aged 65 years and over; by2021, it is projected that they will represent19 to 20 percent (ABS 2003b). The elderlydependency ratio increased from 18 percentto 19 percent between 1954 and 1981, thento 21 percent by 1996. By 2031 it may reach31 percent. The net effect of a likely lifeexpectancy increase of over the next 10 yearswould be further increases in the proportionof over-sixty–fives.

Where we will live: There will be an overallmovement of the population to the coast andcities. Predictions are for a coastalcommunity that spreads along most ofeastern Australia. The drift will have asignificant impact on our capacity to managewater, infrastructure investment andenvironmental sustainability.

Further concentrations in capital cities willbe due to larger growth rates relative to therest of their state/territory. Melbourne islikely to increase by 19 percent to 4.2million in 2021 (estimated range is between4.1 and 4.3 million); Sydney by 18 percentto 4.9 million in 2021 (estimated range isbetween 4.7 and 5.1 million); Brisbane by35 percent to 2.3 million (estimated range isbetween 2.1 and 2.5 million). Brisbane andthe Gold Coast will merge into a newmegacity. They will remain Australia’s threemost populous cities (ABS 2003b).

How we will live: Households numbers areset to increase sharply, with a decline in thenumber of people per household. In 1947,the average Australian household size was 3.8persons. From 1981 to 1996 the number fellfrom 2.92 to 2.72. It is expected there willbe 2.3 persons per household in 2021. The

16

smaller households result from an ageingpopulation, family breakdown, smallerfamilies and lifestyle choices. It is forecastthat 500 000 new homes will be built inSydney over the next 20 to 30 years(Executive Intelligence). The percentage ofmulti-unit dwellings has increased.

Population make-up: Australian has one ofthe worlds’ most diverse populations: in2001, 23 percent were born overseas (ABS2003b), compared to, for example, 8 percentin both the US and New Zealand.Increasingly, Australians are dispersing andliving elsewhere in the world on a temporaryor permanent basis (1.7 percent of thepopulation in 2001).

Our population diversity and its connectionwith the global community increases ouradaptability and capacity to innovate.

4.2 SKILLED WORKFORCE

A critical assumption is that Australia will beable to draw on a pool of skills to support itstransition and growth. However, this may beunrealistic due to the combination of thebaby boomers retiring and a brain drain.

Baby boomers retire: Australia’s workforce hasa disproportionably high number of peopleclose to retirement, and fewer youngerworkers. In the next few decades a shortfallin the number of young people entering theworkforce could limit industry’s ability toconduct business and lead to higher wages.

European and Japanese populations are alsorapidly ageing, requiring more than 110million new workers by 2015 to maintainthe current working population to retireesdependency ratios (GBE 2002).

Brain drain: Increasingly, young Australiansare seeking opportunities overseas.

A key issue … is where we will come out interms of net brain gain or drain – that is,will Australia be able to attract more skilledindividuals on a relatively permanent basisthan we lose? Australia’s capacity tocontinue to benefit from ‘brain gain’ will bedetermined not only by domesticcircumstances—including the availabilityof competitive employment opportunitiesand policies to support skilled migrationand return of ex-patriots—but also by theequivalent circumstances globally. Australiais already facing competition for skilledlabour from other developed countries. Thiswill intensify as population ageingadvances. At the same time, permanent andlong-term departures by young, skilledAustralians have trended up (BCA 2004).

Melinda Cilento cited in BCA 2004

Water industry: A shortage of people enteringand remaining in the water treatmentindustry—in design, construction andmanagement—could lead to significantproblems in 10 to 20 years (GHD 2004).

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

17More than 6 million new settlers have arrived in Australia since theend of World War II.

ABS 2004c

BUT WHAT IF…?

Imagine alternative futures where:

❚ we experience a rising tide of refugees; or

❚ our population decreases.

An overwhelming population increase

A rising tide of refugees: Imagine if legal andillegal refugees cause a significant increase inour population due to:

❚ population pressures from growth in theleast developed countries that are leastable to support it—unless a significantimprovement in these countries’economic prospects occurs, it is likelyoutward migration will grow;

❚ regional instability due to high populationgrowth, urbanisation and a wideningdisparity of wealth;

❚ natural disasters (e.g. 30 of the world’slargest cities lie near coasts: a metre rise inthe oceans … would put an estimated300 million people directly at risk[Linden cited in Hawken, Lovins &Hunter Lovins 2000]);

❚ relative economic position—our relativelystrong economic fortune creates strongpull factors;

❚ a shift in Australia’s social or economicvalues where immigration policies that arebased on views on appropriate numbers,an obligation to accept refugees and theneed to control inflow, could change asviews change; movement of people couldalso be deregulated in the same way thatwe are seeing economic and politicalliberalisation; or

❚ loss of border control, where Australia losesits ability to control the inflow of illegalmigrants.

East coast growths:The current populationincrease is occurring mainly on the east coastof Australia. What if water authorities areunable to meet the demand for waterservices: demand exceeds available supplyand our ability to dispose of the effluent andthe capacity of infrastructure.

Population decrease

Population decrease: Imagine if a realpopulation decrease occurs as it becomesevident that Australia has exceeded itshuman carrying capacity or, a pandemicdisease dramatically reduces our populationand immigration inflow. The water industry’scosts increase dramatically and revenueraising capacity falls as:

❚ in anticipation of a population increase,industry has over-invested in capitalinfrastructure, with significant under-utilisation and high operating costs;

❚ more resources are allocated forenvironmental sustainability and toundertake remedial work; or

❚ the population’s increased dependencyratios limits the industry’s capacity togenerate the required revenue.

18

5. Climate and enviromental change

We are at a new moment in human history. For the first time, we are widely aware thatour day-to-day decisions have the power to destroy our own habitat. Water is integrallylinked to the environment’s health. Water is vital to the survival of ecosystems, and inturn ecosystems help regulate the quality and quantity of water (Rosegrant, Cai & Cline2002).

For much of Australia, climate change predictions forecast that with rising temperatures,there will be an increased demand for water, reduced yields and increasing yieldvariability.

The key questions for urban water are:

❚ What provisions can be made to manage reduced yield in general, and increased yieldvariability, combined with population and economic growth?

❚ What will be done to mitigate the risks arising from climate change andenvironmental degradation?

❚ How significant are those risks?

We learn geology the day after the earthquake.

Ralph Waldo Emerson

5.2 WATER USE AND ITSENVIRONMENTAL IMPACT

Approximately 73 percent of water used inAustralia (~24 000 GL) is supplied by rivers,21 percent by groundwater aquifers, and theremaining 9 percent by harvest of overlandflows. Surface water predominates in allstates and territories except Western Australiaand the Northern Territory (NLWRA2001a).

The National Land and Water ResourcesAudit showed that, in 2002, twenty-sixpercent of the 325 surface watermanagement areas units were either close toor already overused when compared withsustainable flow regime requirements. Theseaccount for 55 percent of total water use inAustralia. Thirty-one percent of the 538ground water management units are alsofully or over-allocated (NLWRA 2001b).

5.1 THE ENVIRONMENTALTRENDS

Contemporary (global) environmentalproblems will persist and in many instancesgrow over the next 15 years. Withincreasingly intensive land use, significantdegradation of arable land will continue aswill the loss of tropical forests. Given thepromising global economic outlookgreenhouse gas emissions will increasesubstantially. The depletion of tropicalforests, other specie-rich habitats, such aswetlands and coral reefs, will exacerbate thehistorically large losses of biological speciesnow occurring.

NIC 2000

Australia’s arable land and fresh water are alsopredicted to continue to decline both inquantity and quality as is our biodiversity(Michael Rae cited in BCA 2004).

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

19

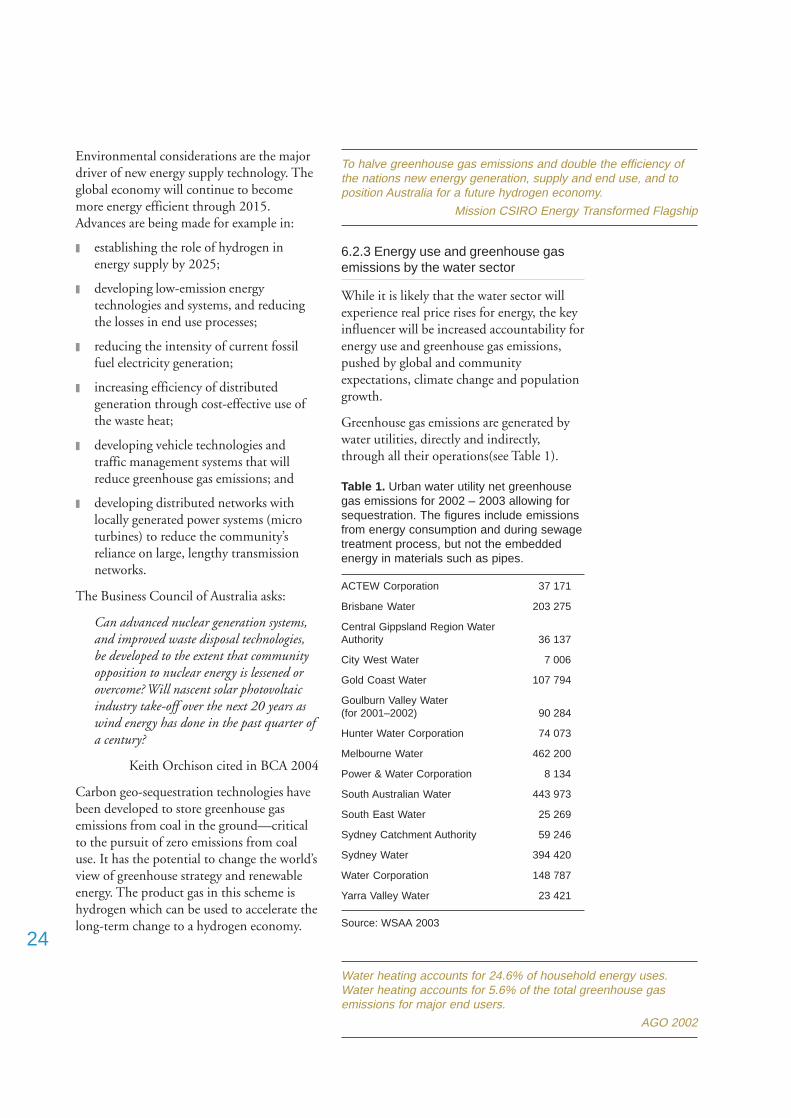

Water quality data are limited with onlybetween 67 and 75 out of Australia’s 246river basins (about 28 percent) able to beassessed for any of the key variables—turbidity, nutrients or salinity. Sixty-fivebasins had major exceedances of guidelines(NLWRA 2000).

5.3 VARIABILITY IN ANNUALRAINFALL

In all parts of Australia there is greatvariability in annual rainfall:

❚ along the east coast it can vary by a factorof two or three to one betweenconsecutive years; and

❚ in arid areas annual rainfall inconsecutive years can vary by a factor of10 or higher.

Also, both long- and short-term cycles of wetand dry weather can be identified and thesecan be Australia wide or regional. Long-termweather cycles of 40–50 years have beenidentified (GHD 2004). These can have asignificant impact on the reliability ofexisting supplies.

Many of Australia’s rivers have highlyvariable flows. Droughts and floods arecommon, and hence rivers and groundwaterresources have been developed extensively forirrigated agriculture and domestic watersupplies.

The variable climate and water cycle flowssuggest that the use of the system to supportthe service needs of the community and theeconomy also needs to vary. The movetowards integrated water cycle managementwill require sensitivity to this volatility.Further, if we learn to live with climatevariability we will be better equipped to dealwith climate change.

5.4 GLOBAL WARMING AND SEA-LEVEL RISE

For many, global warming looms as one ofthe planet’s biggest threats. Over the past 20years researchers have gathered evidence thatburning fossil fuel is causing temperatures torise. The exact pace of global warming, aswell as mankind’s contribution, is uncertain(Cline 2004).

Rising temperatures can cause considerableharm depending on how big the future risesare and how quickly they happen, and theimpacts on regional environments.

Predictions are that the Earth’s averagetemperature is likely to rise by 1.4 to 5.8oCby the year 2100 relative to 1990, a warmingrate of 0.1 to 0.5oC per decade. With thiswill be a rise in sea level of 9 to 88 cm by2100, or 0.8 to 8.0 cm per decade (CSIRO2001b).

Given the promising global economicoutlook, greenhouse gas emissions willincrease substantially. But the pressures onthe environment as a result of economicgrowth will decrease as a result of less energy-intensive economic development,technological advances and the shift towardsless polluting fuels such as natural gas (NIC2000).

There are many uncertainties. Forecasts ongreenhouse gas emissions are subject to:

❚ population growth;

❚ technological change;

❚ social and political behaviour; and

❚ the validity of the climate modelling.

The climates too are influenced by thenormal climatic cycles and otherunpredictable factors such as solar radiationand chaotic variations in the climate system.

Many people’s intuition that weather is shifting and is becomingmore volatile is confirmed by meteorological measurements.Spring in the Northern Hemisphere is coming a week earlier: thealtitude at which the atmosphere chills to freezing is rising bynearly 15 feet a year; glaciers are retreating almost everywhere.

20

5.5 AUSTRALIA’S CLIMATECHANGE

Australia’s temperature, rainfall patterns andavailability of water will change relative to1990.

Rising temperatures: By 2030, Australia’sannual average temperatures will probably bebetween 0.4 and 2.0oC higher, with slightlyless warming in some coastal areas andTasmania, and greater warming in the north-west. The greatest amount of warming willoccur in spring; the least amount will be inwinter. In the north-west, the greatestpotential warming will be in summer. Theseincreases may lead to large changes inoccurrence of extremely hot or cold days(CSIRO 2001a).

Changes to average rainfall, rainfall patternand intensity of rainfall events: Average annualrainfall could increase or decrease. Changesvary from -10 percent to +10 percent by2030 and -35 percent to +35 percent by2070, relative to 1990. Decreases will bemost pronounced in winter and spring.There will be a bias towards decreases in thesouth-west, parts of the south-east andQueensland. Some inland and eastern coastalareas may become wetter in summer, andsome inland areas may become wetter inautumn (CSIRO 2001a).

Where average rainfall increases we couldhave more extremely wet years, and where itdecreases, more dry spells. An increase inextreme daily rainfall leading to morefrequent heavy rainfall events and flooding, islikely (CSIRO 2001b).

It will be drier, as higher temperaturesincrease evaporation, and this will tend to begreater where there is a correspondingdecrease in rainfall (CSIRO 2001b).

5.5.1 Implications of a climate change

Climate change will have social, economicand ecological impacts. All our naturalecosystems are vulnerable. Water resources,cities and towns, the energy sector andindustry are likely to be sensitive to climatechange, although the net effects are difficultto predict (CSIRO 2001a). The likelyimplications for urban water include watershortages, extreme weather events andenvironmental impacts.

Water shortage: Shortages are likely to occurparticularly in winter-rain–fed systemsalready under stress. This will lead to asharpening of competition between differentwater users, especially where large diversionsfrom river systems are made for industry andirrigation. The trends will be:

❚ increased water stress with increases instream flow in northern Australia anddecreases for southern Australia;

❚ warmer conditions, accompanied byrainfall decrease in key agriculturalregions particularly in winter and spring;and

❚ a decrease in water available forirrigation, domestic and industrial uses;environmental flows; and crop andpasture growth.

Extreme weather events: More frequentextreme events such as bushfires, floods,storms and drought are likely to occur.

Environmental impacts: A substantialreduction in biodiversity is likely to occur asmany natural systems will have difficultyadapting to climate changes. The range oftropical diseases, disease vectors and toxicalgal blooms are likely to be expanded(CSIRO 2001a).

If the world’s nations wanted to stabilise the atmosphere in itspresent disrupted state, they would need to cut CO2 emissionsimmediately by about three-fifths.

Hawken, Lovins & Hunter Lovins 2000

WA

TE

R F

OR

A H

EA

LT

HY

CO

UN

TR

Y –

Un

ch

arte

d w

ate

rs

21

5.5.2 Community response to climatechange

Planning and adaptation strategies can helpto minimise the adverse impacts andoptimise benefits. However, climate changeis not well understood and is poorly acceptedby decision makers and the public.

Global warming will challenge theinternational community as indications ofa warming climate … occur. The KyotoProtocol on Climate Change, whichmandates emission reductions targets fordeveloped countries, is unlikely to come inforce soon or without substantialmodification. Even in the absence of aformal treaty, however, some incrementalprogress will be made in reducing thegrowth in greenhouse gas emissions.

Cline 2004

Economist and columnist Robert JSamuelson in Newsweek expressed the viewthat:

It would be political suicide to do anythingserious about [climate] … So shrewdpoliticians are learning to dance around thedilemma’ … Without a breakthrough inalternative energy – nuclear or something –no one knows how to lower emissionsadequately without crushing the econom …

Samuelson cited in Hawken, Lovins &Hunter Lovins 2000

A contrary view is that:

Samuelson, like many business people,believes climate protection is costly becausethe best publicised (though not the mostbroadly accepted) economic computermodels say it is. …those models find carbonabatement costly because that’s what theyassume. The menu of climate-protectingopportunities is so large that over-time, theycan overtake and even surpass the pace ofeconomic growth… These steady long-termimprovements are profitable and alreadyunderway.

Hawken, Lovins & Hunter Lovins 2000

BUT WHAT IF …?

Imagine alternative futures where:

❚ large and sudden climatic changes occur;

❚ environmental decline triggers extinction; or

❚ existing production patterns intensify.