national bureau of economic research … · building social capital through microfinance benjamin...

TRANSCRIPT

NBER WORKING PAPER SERIES

BUILDING SOCIAL CAPITAL THROUGH MICROFINANCE

Benjamin FeigenbergErica M. FieldRohini Pande

Working Paper 16018http://www.nber.org/papers/w16018

NATIONAL BUREAU OF ECONOMIC RESEARCH1050 Massachusetts Avenue

Cambridge, MA 02138May 2010

We thank Emmerich Davies, Sean Lewis Faupel, Sitaram Mukherjee and Anup Roy for superb fieldwork and research assistance, Alexandra Cirone and Gabe Scheffler for editorial assistance and VillageWelfare Society and Center for Micro-Finance for hosting this study, Theresa Chen, Annie Duflo,Nachiket Mor and Justin Oliver for enabling this work and ICICI, Exxon Mobil Educating Womenand Girls Initiative (administered through WAPP/CID at Harvard) and the Dubai Initiative for financialsupport. We also thank Attila Ambrus, Abhijit Banerjee, Tim Besley, Amitabh Chandra, Esther Duflo,Raquel Fernandez, Dominic Leggett, Muriel Niederle, Aloysius Sioux, Jesse Shapiro, Anil Somaniand numerous seminar participants for helpful comments. The views expressed herein are those ofthe authors and do not necessarily reflect the views of the National Bureau of Economic Research.

NBER working papers are circulated for discussion and comment purposes. They have not been peer-reviewed or been subject to the review by the NBER Board of Directors that accompanies officialNBER publications.

© 2010 by Benjamin Feigenberg, Erica M. Field, and Rohini Pande. All rights reserved. Short sectionsof text, not to exceed two paragraphs, may be quoted without explicit permission provided that fullcredit, including © notice, is given to the source.

Building Social Capital Through MicroFinanceBenjamin Feigenberg, Erica M. Field, and Rohini PandeNBER Working Paper No. 16018May 2010JEL No. C81,C93,O12,O16

ABSTRACT

A number of development assistance programs promote community interaction as a means of buildingsocial capital. Yet, despite strong theoretical underpinnings, the role of repeat interactions in sustainingcooperation has proven difficult to identify empirically. We provide the first experimental evidenceon the economic returns to social interaction in the context of microfinance. Random variation in thefrequency of mandatory meetings across first-time borrower groups generates exogenous and persistentchanges in clients' social ties. We show that the resulting increases in social interaction among clientsmore than a year later are associated with improvements in informal risk-sharing and reductions indefault. A second field experiment among a subset of clients provides direct evidence that more frequentinteraction increases economic cooperation among clients. Our results indicate that group lendingis successful in achieving low rates of default without collateral not only because it harnesses existingsocial capital, as has been emphasized in the literature, but also because it builds new social capitalamong participants.

Benjamin FeigenbergDepartment of EconomicsMITCambridge, [email protected]

Erica M. FieldDepartment of EconomicsHarvard UniversityM30 Littauer CenterCambridge, MA 02138and [email protected]

Rohini PandeKennedy School of GovernmentHarvard University79 JFK StreetCambridge, MA 02138and [email protected]

1 Introduction

Social capital, famously defined by Putnam (1993) as “features of social organization, such as trust,

norms and networks, that can improve the efficiency of society by facilitating coordinated actions,”

is thought to be particularly valuable in low-income countries where formal insurance is largely

unavailable and institutions for contract enforcement are weak.1 Since economic theory suggests

that repeated interactions among individuals can help build and maintain social capital (see, for

instance, Kreps et al., 1982), encouraging interaction could be an effective tool for development

policy. Indeed, numerous development assistance programs have introduced policies designed to

promote social contact among community members under the assumption that there are significant

economic returns to regular interaction. But can simply inducing people to interact more often

actually increase economic cooperation?

While a large body of research finds a positive correlation between social interaction and

cooperative outcomes, rigorous empirical evidence on this subject remains limited, largely due to

the difficulty of accounting for endogenous social ties (Manski, 1993, 2000). For instance, if more

cooperative individuals or societies are characterized by stronger or denser social networks, we

cannot assign a causal interpretation either to the positive association between community-level

social ties and public goods provision or to the higher levels of cooperation observed among friends

as compared to strangers in laboratory public goods games.2 In short, without randomly varying

social distance, it is difficult to validate the basic model of returns to repeated interaction and even

harder to determine whether small changes in social interaction can produce tangible returns.

This paper undertakes precisely this exercise in the context of a development program that

1Consistent with this idea, Guiso et al. (2004) demonstrate that residents in high social capital regions engage inmore sophisticated financial transactions, and Knack and Keefer (1997) show that a country’s level of trust correlatespositively with its growth rate.

2The public good provision and community ties literature includes Costa and Kahn (2003); Alesina and Ferrara(2002); DiPasquale and Glaeser (1999); Miguel et al. (2005); Olken (2009), while examples of laboratory gamesinclude Glaeser et al. (2000); Carter and Castillo (2004); Do et al. (2009); Karlan (2005); Ligon and Schecter (2008).Another shortcoming in the community ties and public goods literature is the use of survey-generated measures ofpropensity to cooperate, which are often inconsistent with incentivized trust measures generated by laboratory games(Glaeser et al., 2000).

2

emphasizes group interaction – microfinance. In the typical “Grameen Bank”-style microfinance

program, clients meet weekly in groups to make loan payments. In addition to facilitating debt

collection, these meetings encourage regular interaction among members of highly localized commu-

nities.3 To evaluate the economic returns to increased social contact that result from participation

in group lending, we randomly assigned first-time borrower groups of a microfinance institution

(MFI) in India to meet either once per week (weekly groups) or once per month (monthly groups).4

We show that mandated differences in meeting frequency over a ten-month period generated

persistent differences in individuals’ knowledge of and social contact with group members: Five

months into the loan cycle, clients in weekly groups were 90% more likely to have visited other

group members in their homes, and more than a year after their loan cycle ended they were 40%

more likely to attend social events together and visited one another 19% more often outside of

loan meetings. These gains were concentrated among clients who did not know each other well

before joining the MFI but had the ability to sustain social contact either through extended family

networks or geographic proximity.

Furthermore, reducing social distance had significant economic returns. Clients required to

meet more frequently in the experimental loan cycle were 19% more likely to report financial trans-

fers with people outside of their immediate family and 29% more likely to say that they would ask

another (former) group member for help in the event of a health emergency. They were also four

times less likely to default on their subsequent loan (during which all clients met at the same fre-

quency, irrespective of whether they had earlier been in weekly or monthly groups). While in theory

it is possible that more frequent repayment directly influenced default via long-run differences in

financial discipline, several pieces of evidence indicate that social ties were the central channel of

influence. Perhaps most striking, the reduction in default among weekly clients depended heavily

3In an anthropological study of Grameen Bank clients, Larance (2001) describes the social aspects of weeklyactivities such as “walking across the village to attend the center meeting, sitting in conversation with a diverse setof women, handling money for the group and receiving personal address.”

4In a similar spirit, Humphreys et al. (2009) randomize community development programs and show that theyencourage prosocial behavior. However, they are unable to identify the influence of social interactions, per se.

3

on those group characteristics – fraction of extended family members and close neighbors in the

group – that predicted differences in social capital formation. Importantly, these characteristics do

not directly influence default.

Not only do these results imply that development programs can readily generate economically

valuable social capital, but they provide an alternative explanation for the success of the classic

group lending model in achieving low rates of default without the use of collateral. Although joint

liability is almost universally emphasized as the key to mitigating default risk in group lending,

our results show that improvements in informal risk-sharing arrangements that develop among

clients in individual-liability lending groups significantly improve repayment rates. Further, recent

experimental evidence suggests that joint liability has little impact on default (Karlan and Gine,

2009). Our results also provide a rationale for the current trend among MFIs of maintaining

repayment in group meetings despite the transition from group to individual liability contracts

(Karlan and Gine, 2009).

To gather direct evidence on economic cooperation among clients and disentangle mechanisms

through which repeat interaction improves cooperation, we designed and implemented a second

field experiment (roughly sixteen months after the group meeting experiment ended). This lottery

experiment provided a unique opportunity to elicit clients’ willingness to share risk with group

members in a setting that did not trigger subjects’ awareness of being participants in an experiment.5

Each client entered a separate lottery in which she started with a 1 in 11 chance of winning a Rs.

200 ( $5) promotional coupon. She was offered the opportunity to give out additional lottery

tickets to any number of members of her first MFI group, reducing her individual probability of

winning but increasing the probability that someone from the group would win. Since ticket-giving

increases her expected payoff if and only if group members could be trusted to share their winnings

an individual’s willingness to give tickets captures the “resource potential” of her MFI network.

5Subjects’ awareness of being scrutinized has been shown to influence laboratory measures of pro-social behavior.In a recent overview of this literature, Levitt and List (2009) argue that individuals’ pro-social behavior in framedor artifactual experiments is likely to depend on the nature and degree of others’ scrutiny, the context in which adecision is embedded and the selection of participants, which significantly limits the generalizability of these results.

4

To distinguish insurance motivations for sharing from unconditional altruism, we varied the

form of lottery prize, randomly assigning each client to a lottery in which the prize was either one

Rs. 200 voucher or four Rs. 50 vouchers. Assuming the more easily divisible prize is perceived

as more conducive to sharing by the winner, a client will be more likely to give tickets to group

members when the prize is divisible if she is motivated at least in part by risk-sharing considerations

but no more likely if she is motivated only by selfless altruism.6 Consistent with this, we find that,

relative to a monthly client, a client who had been in a weekly group was 67% more likely to enter

a group member into the lottery when the prize was divisible but no more likely when it was not.

Further, in line with our earlier results we find that increased ticket-giving by weekly clients is

driven by increased giving to close neighbors and extended family.

Why do more frequent meetings facilitate risk-sharing? We exploit a unique feature of our

experimental setting to evaluate the importance of learning about fellow group members types

(level of impatience, trustworthiness, etc.), which implies only short-term benefits of more frequent

interaction, versus the possibility that regular interaction indefinitely improved risk-sharing capacity

by increasing clients’ effective discount factors or ability to implement punishment and reward

schemes that mitigate opportunistic behavior. At the time of the lottery, a subset of participants

were on a subsequent loan cycle in which their group had been re-randomized into weekly or

monthly repayment schedules. This provides experimental variation in the frequency of mandatory

interactions between group members at two points: once when they are new to each other and once

when they have been interacting regularly for almost two years. Clients randomly assigned to meet

frequently in both loan cycles give significantly more tickets than clients required to interact at a

high frequency only in the beginning. We interpret this as evidence that, in addition to any learning

effects that hasten the formation of reciprocal arrangements, higher meeting frequency also helps

6Similar variations of dictator or trust games have been used to parse out motives for giving in laboratoryexperiments. See for instance Ligon and Schecter (2008); Do et al. (2009); Carter and Castillo (2003). Perhapsclosest to our approach is Gneezy et al. (2000), who use a sequence of trust games with varying constraints on theamount that can be repaid in the second round to show that individuals contribute more when large repayments arefeasible.

5

sustain cooperation by reducing the costs or increasing the benefits of coordinating actions.

Our findings compliment existing work on microfinance, which has identified a role for social

connections in reducing default risk (Besley and Coate, 1995; Ghatak and Guinnane, 1999; Karlan,

2005).7 Our contributions are to generate and use random variation in social ties to establish

a causal effect of social interaction on cooperation that we cannot safely conclude from previous

studies (given the possibility of selection into social networks), and, in doing so, to demonstrate that

small changes in program design (here, the structure of the loan contract) can have a significant

effect on social capital. With respect to microfinance, our findings illustrate that the most popular

form of group lending not only harnesses social capital through joint liability contracts but actually

builds social capital among group members by encouraging regular social contact.

The rest of this paper is structured as follows: Section 2 describes the study setting and

experimental design. Section 3 documents the implications of meeting frequency for clients’ social

and financial behavior. Section 4 uses our second field experiment to disentangle channels through

which increases in social interaction increased economic cooperation, and Section 5 concludes.

2 Setting and Experimental Design

Our partner MFI, Village Welfare Society (VWS), started operations in the Indian state of West

Bengal in 1982. At the start of our field experiments, it had roughly 6.75 million dollars in outstand-

ing loans to over 56,000 female clients. According to the baseline survey, over 70% of households

in our sample owned a micro-enterprise, 30% report significant health shocks in the twelve months

prior to taking out a loan, and less than 40% had a savings account or formal insurance, suggesting

potentially significant returns to informal risk-sharing among group members.

Like most MFIs, VWS loan groups typically consist of clients from a single neighborhood,

which implies that members live in close proximity and are acquainted prior to joining. However,

7For instance, MFI clients in Peru who are more trustworthy in a trust game are less likely to default, andgroup-level default is lower in groups where clients have stronger social connections (Karlan, 2005, 2007).

6

while 67% of group members in our sample knew one another at group formation, most described

their relationship with other group members as neighbors (51%), acquaintances (6%), or strangers

(27%), rather than friends (7%) or family (9%).

The basic loan group works as follows: After clients are screened and groups approved by

loan officers, members choose a group leader in whose home the loan officer will conduct weekly

repayment meetings for the duration of the loan cycle. The first two meetings are for group nurturing

and training, and loan repayment starts in the third week. During each meeting clients take an

oath promising to make regular repayment, after which the loan officer collects payment from each

member individually and marks passbooks.8 Loan cycles last for forty four weeks and all clients must

attend meetings for at least twenty weeks, after which point they may repay the remaining balance

in a single installment. In our sample the median weekly group met thirty seven times during a

single loan cycle and the average meeting length was twenty-five minutes (excluding waiting time).

For the experiment, between April and September 2006 we recruited one hundred new ten-

member borrower groups of first-time clients from neighborhoods in the catchment areas of three

VWS branches.9 At the time of recruitment, clients were told that repayment schedules would be

determined by lottery. Before loan disbursal, we randomly assigned thirty groups to the standard

weekly repayment schedule and seventy groups to a monthly repayment schedule.10 Each client

received a Rs. 4000 ( $100) loan, a reasonably large amount given that the average client had

assets worth $250 at baseline. Clients assigned to the weekly schedule were required to repay their

loans through 44 weekly installments of Rs. 100 starting two weeks after loan disbursal, and those

assigned to the monthly schedule in eleven Rs. 400 installments starting one month after loan

8A client’s repayment behavior is, thus, observable to other group members, although, in practice most clientssocialize while awaiting their turn. While a client can repay at a branch this occurred very rarely. However, once amajority of clients in a group have repaid their loan, VWS asks remaining clients to repay at the branch office.

9Loan officers aimed to form ten-member groups. In practice, group size ranged between eight and thirteenmembers, with 77% of the groups consisting of ten members.

10We originally intended to have two monthly repayment treatment arms: One that met weekly and one that metmonthly. In practice, weekly meetings among clients required to repay monthly broke down almost immediately,and clients ended up meeting on a monthly basis for most of their loan cycle. On average the weekly-monthly andmonthly-monthly groups ended up meeting 10.13 and 10 times.

7

disbursal. No client dropped out after her repayment schedule was announced.

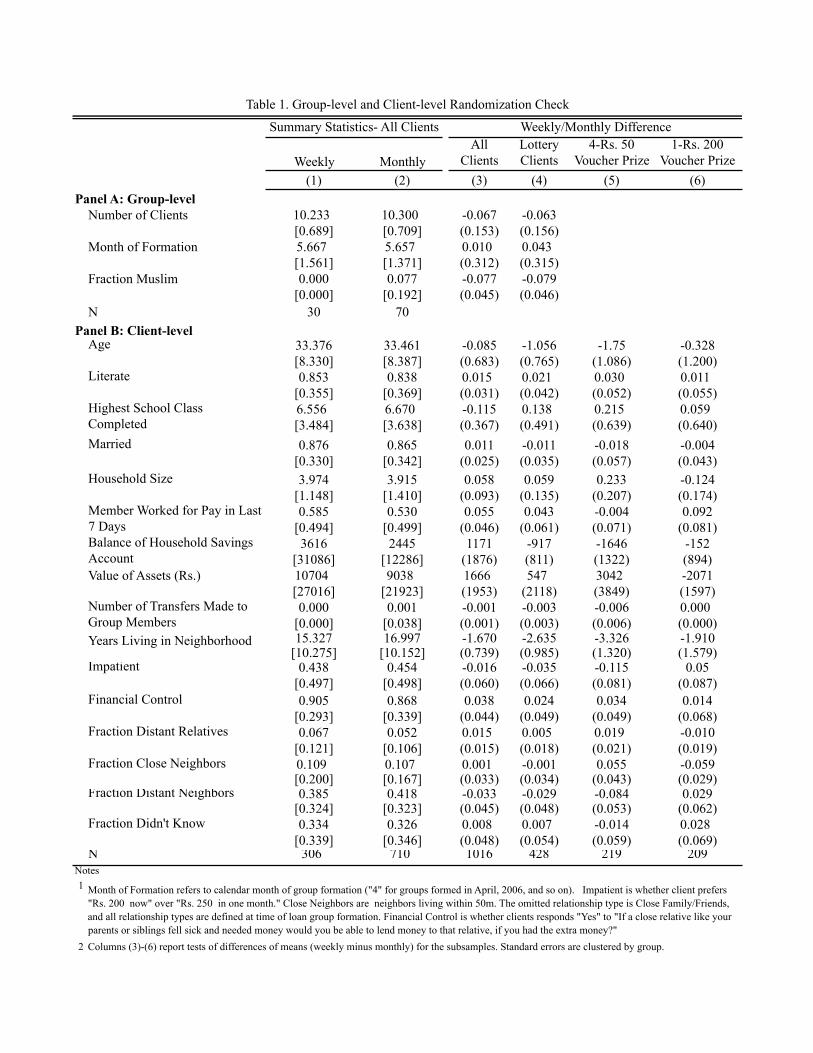

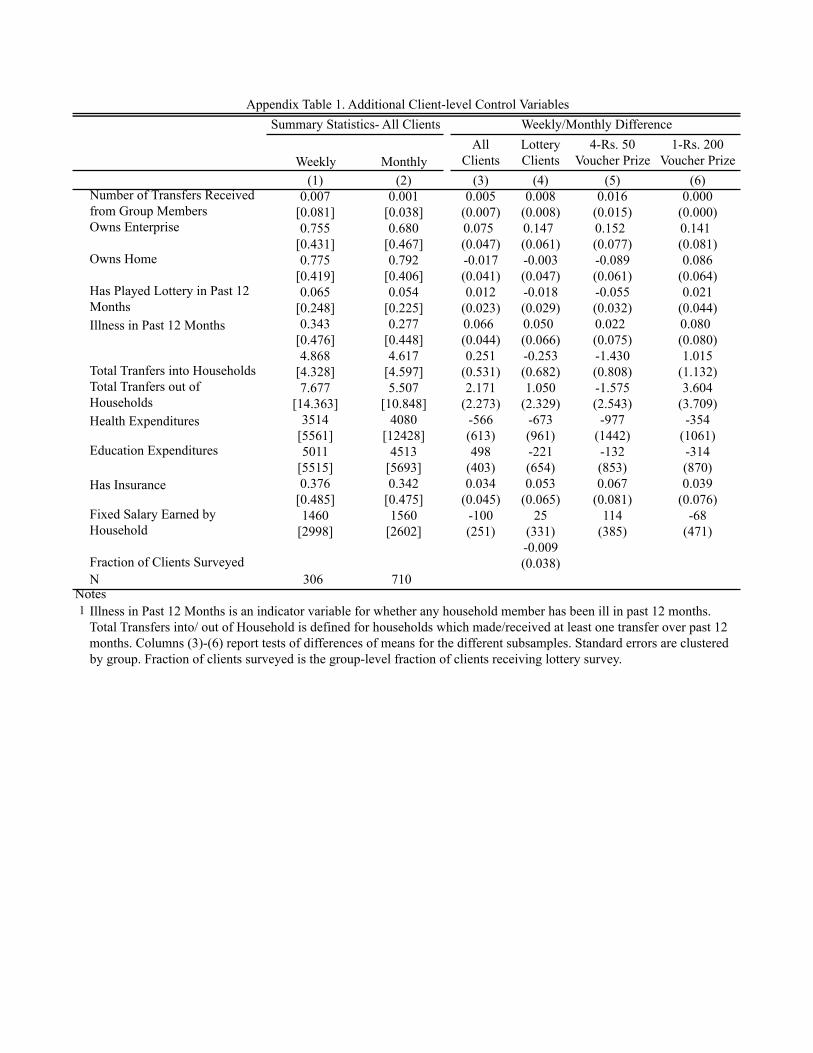

Between group formation and loan disbursement, we administered a baseline survey to 1016

of the 1026 clients. Table 1 and Appendix Table 1 provide a randomization check based on these

data. On average, monthly and weekly clients look similar at baseline across a wide range of

observable characteristics. No baseline characteristics out of 30 are significantly different at a 5%

level, and only two differences are statistically significant at the 10% level: whether a client is

Muslim and the number of years she has lived in her neighborhood. While monthly clients have

been in their neighborhoods for slightly longer, the difference is relatively small and is not associated

with differences in degree of social ties. For instance, they were no more likely to describe another

group member as family or friend (Table 1, Panel B). We have also verified that the results are

robust to excluding groups with Muslim clients. However, because of these differences, throughout

we report regressions with the controls listed in Table 1 and discuss any cases in which our results

are sensitive to the inclusion of controls.

3 Effect of Meeting Frequency on Client Behavior

To gauge the effect of meeting frequency on social capital formation, our study tracks clients for two

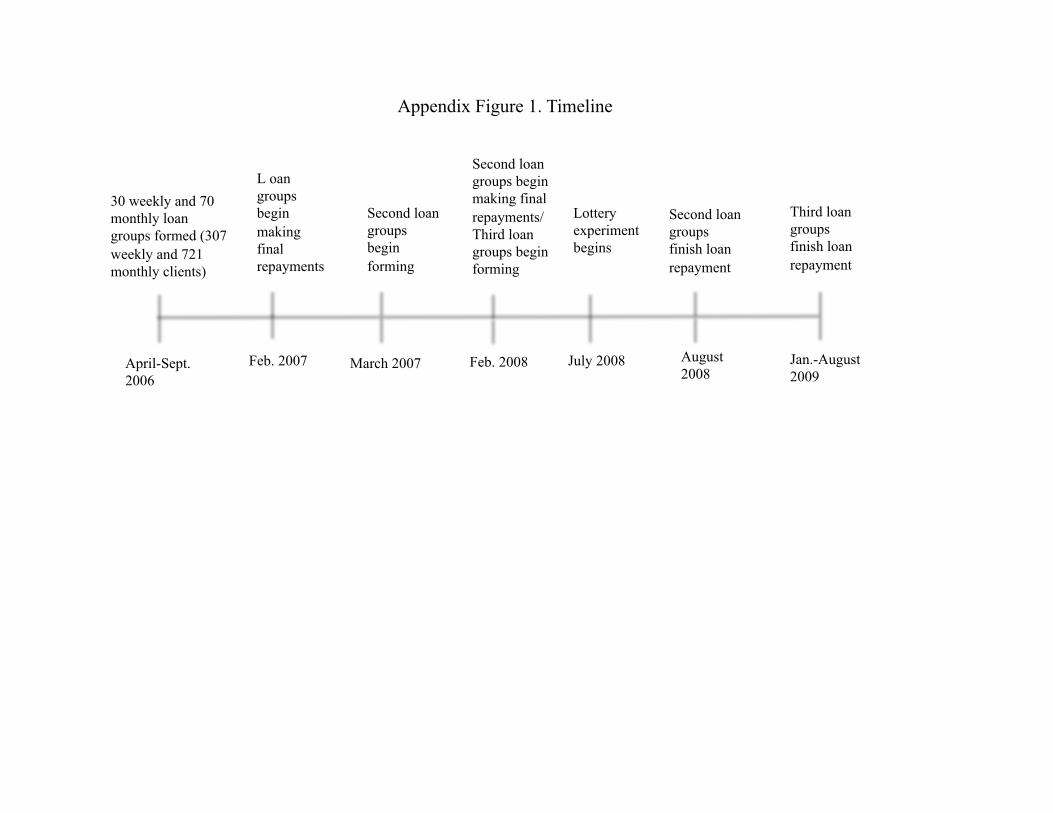

and a half loan cycles (roughly 100 weeks) beginning in April 2006. Appendix Figure 1 provides a

detailed timeline.

3.1 Social Capital Effects

We first measure short-run changes in group members’ social contact outside of repayment meetings

during the course of the experiment. To capture this, at the end of each meeting loan officers asked

clients four questions about their knowledge of and interactions outside of meetings with other

group members. Since data were collected in a relatively public setting, to maintain a degree of

anonymity clients were asked to aggregate their interactions across group members.

8

To capture the breadth of client interactions outside of meetings, each client was asked whether

all group members had visited her at home and whether she had visited all other group members in

their homes.11 For both outcomes, we construct an indicator that equals one if the client responded

in the affirmative at any group meeting. To capture clients’ knowledge of group members, each

client was asked if she knew the names of her group members’ husbands and children and whether

any of her group members had relatives visit in the last thirty days. For the first measure, we

again construct an indicator that equals one if the client responded in the affirmative at any group

meeting, and for the second we average across all responses for a client. To avoid inferences based

on selected outcomes, we report effects for a “social contact index” which averages across these four

outcomes (Kling et al., 2007).12 Since clients often repay early but never before the sixth month, we

restrict the analysis to data from the first five months of the loan cycle.13 To balance observations

across weekly and monthly clients, we randomly choose one meeting per month for weekly clients.

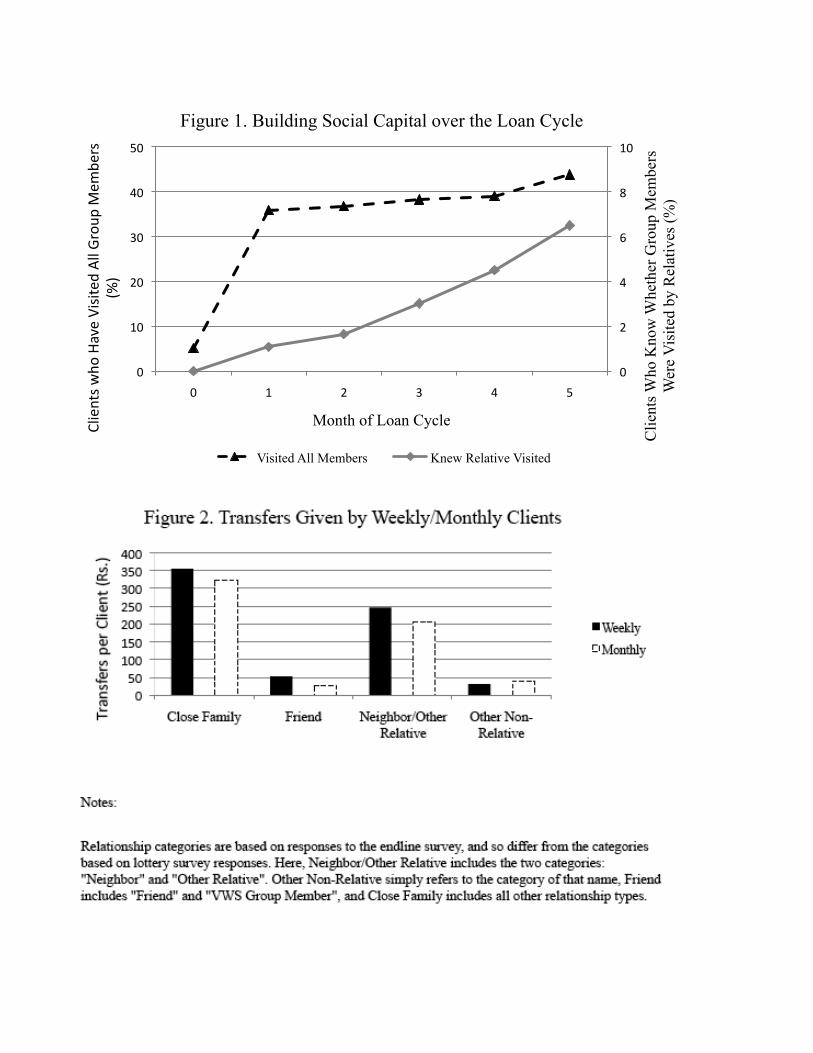

Figure 1 shows that the fraction of clients who had visited all group members in their homes

rose sharply in the first month and then increased gradually over the next five months to nearly 45%,

and the fraction of clients who knew whether their group members had been visited by relatives

increased steadily from 0% to 7%. We observe similar patterns for fraction of clients visited by all

group members and knowledge of the names of family members of other group clients (unreported).

These patterns are consistent with a “dose response” to mandatory meetings, in which case weekly

groups should end up with higher levels of social contact. To test this, we aggregate social contact

data to the group level – since client responses may have been influenced by being asked in a group

setting – and estimate for group g:

yg = β1Wg +Xgγ1 + αg + εg (1)

11Repayment meetings always occur at the group leader’s house.12The index is the equally weighted average of the four variables, with each variable normalized by subtracting

the mean for monthly clients and dividing by the standard deviation for these clients.13Due to delays in implementing the group meeting survey, 1.9% of clients (20 clients) lack eight weeks of data,

4.8% (49 clients) lack data for 6 weeks, and 7.8% (80 clients) lack four weeks of data.

9

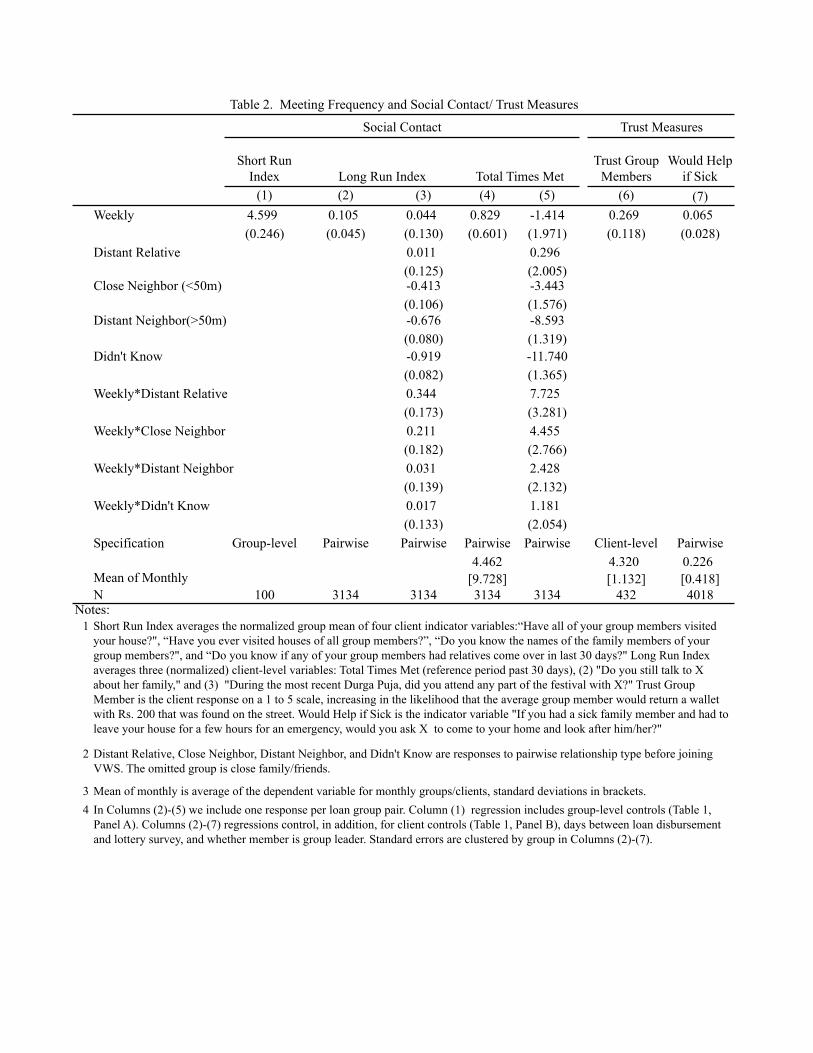

where yg is the social capital index, Wg is an indicator for weekly group, αg is a loan officer fixed

effect, and Xg is the set of group-level controls in Table 1. Regression results, presented in column

(1) of Table 2, indicate that moving from monthly to weekly repayment leads to a four standard

deviation increase in social contact outside of meetings.14

To examine whether changes in social contact persisted beyond the experiment and measure

individual social interactions in a more controlled setting, we visited a random sample of 432 clients

an average of 16 months after they had repaid their loan and collected survey data on the client’s

perceptions of the trustworthiness of her previous (first loan cycle) group members and her current

contact with these members.15 For consistency with short-run data collected during loan meetings,

our first long-run contact measure is the number of times over the last thirty days the client had

visited with a previous group member in either person’s home. The next two outcomes measure

the strength of social contact – whether the client still talks to the group member about family and

whether they celebrated the main Bengali festival (Durga Puja) together during the previous year.

Since we have roughly nine observations per client (all other group members), our analysis

sample contains 4018 pairwise observations. In order to avoid double-counting, in cases in which

we interviewed both members of a pair, we randomly drop one observation when the outcome is

social contact (which cannot vary, in the absence of measurement error, within a pair) and keep all

observations for outcomes that can differ within a pair. For member i matched with group member

m in group g we estimate

ygmi = β1Wg +Xgγ1 +Xiγ2 + δ1Di + δ2li + αg + εgmi (2)

where overlapping variables are defined as in equation (1), Di controls for number of days between

loan disbursement and survey, and li controls for being the group leader. Additional controls, listed

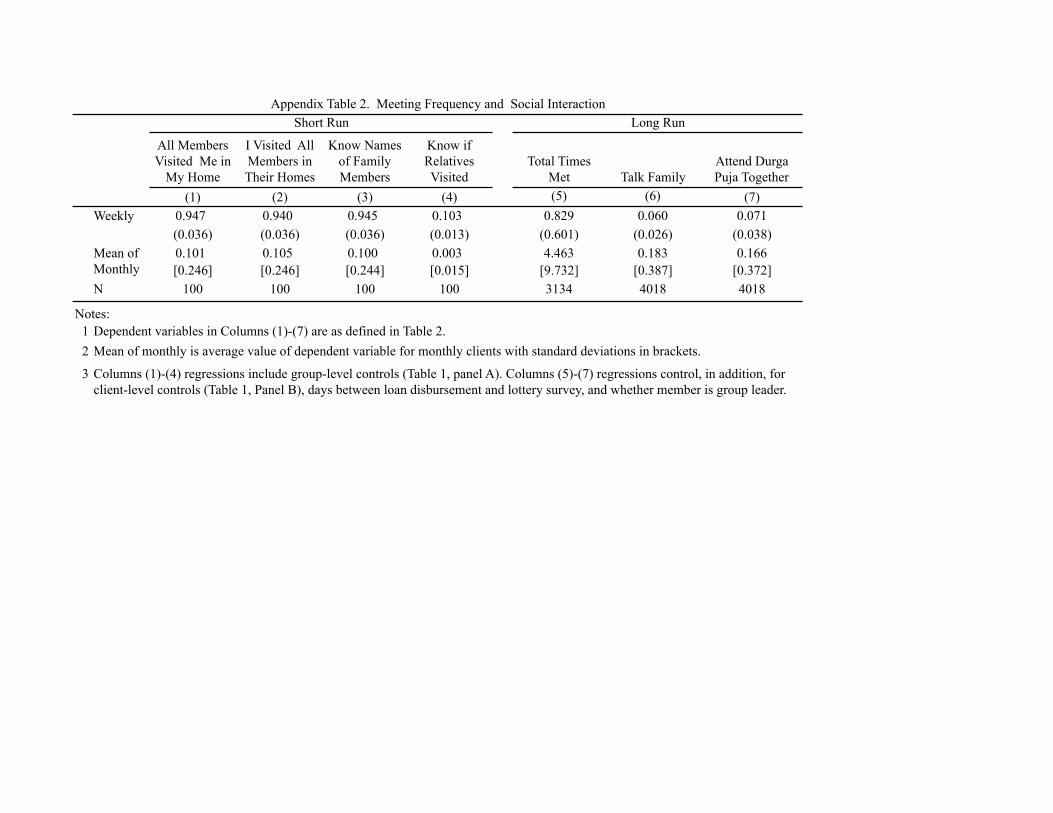

14In Appendix Table 2, we report the differences for each of the index components (for ease of interpretation weconsider the non-normalized group outcomes). In each case, the magnitude of the effect is strikingly large. All resultsare robust to excluding controls.

15The client also provided information on her relationship with each group member prior to joining VWS.

10

in Table 1, are defined at the group- and individual- level (Xg and Xi respectively). Standard errors

are clustered by group.

According to the estimates in column (2) of Table 2, more than a year after graduating

from their first loan cycle, clients who met weekly remain significantly more likely to interact than

their monthly counterparts: Moving from a monthly to a weekly schedule leads to a 0.11 standard

deviation increase in long-run social contact between clients. The effect is similar in magnitude

but statistically insignificant without controls. Furthermore, all of the individual index components

indicate greater social contact among weekly clients and two out of three are statistically significant

(Appendix Table 2). In sum, higher levels of friendship among weekly clients persisted long after

mandatory meetings ended.

Next, we examine how long-run changes in social contact varied across five categories of

baseline social distance: (i) immediate family members and friends; (ii) relatives more than once

removed (distant relatives); (iii) neighbors living within a block (close neighbors); (iv) neighbors

living more than a block away (far neighbors); and (v) strangers.16 Column (3) reveals that increases

in long-run social contact that accrue to weekly groups are concentrated among client pairs who

are distant relatives and close neighbors. Reassuringly, we do not observe a change in social contact

among immediate relatives (the omitted group), and not surprisingly, we also observe no significant

change among clients with few means of sustaining a social connection outside of group meetings

(those who were unknown prior to joining VWS or distant neighbors). These results are robust to

the exclusion of controls.

Looking directly at the component of the index that measures repeat interaction – number

of times the pair visited each other at home in the last thirty days – we observe that the average

weekly client pair meets 19% more often than their monthly counterpart, but the estimate is very

noisy (column (4)). However, when weekly is interacted with categories of initial social distance,

we observe large and significant increases in meeting frequency where changes in social ties are

16Distances were measured using GPS coordinates collected at baseline. We define a city block as living within a50-meter radius, which is half of the distance used to define city blocks in developed countries.

11

most heavily concentrated - among distant family and close neighbors. Among weekly clients, close

neighbors see each other just as often as friends and family members once removed while in monthly

groups they see each other 27% less often.

The last two columns consider trust-based measures of social capital. The outcome in column

(6) is a client’s perception of her average group member’s trustworthiness.17 More than a year after

repaying the loan, those who were on a weekly schedule rank average group member trustworthiness

0.27 points higher (on a 1-5 scale) and the difference is statistically significant with or without

controls.18 In column (7), the outcome variable is the client’s response to a hypothetical question on

whether she believes that a particular group member would help her in the event of illness. Weekly

clients are six percentage points more likely to report that a group member would provide assistance

in such an emergency (29%), which is statistically significant with but not without controls.

3.2 Returns to Social Capital

According to the previous section, forcing people to meet more often for 6-10 months leads to

persistent increases in social ties. But do these social ties yield economic returns or simply change

patterns of friendship? Survey responses to a hypothetical scenario suggest that weekly clients are

also more willing to provide informal insurance to fellow group members (Table 2, column (7)), but

do informal risk-sharing arrangements develop in practice?

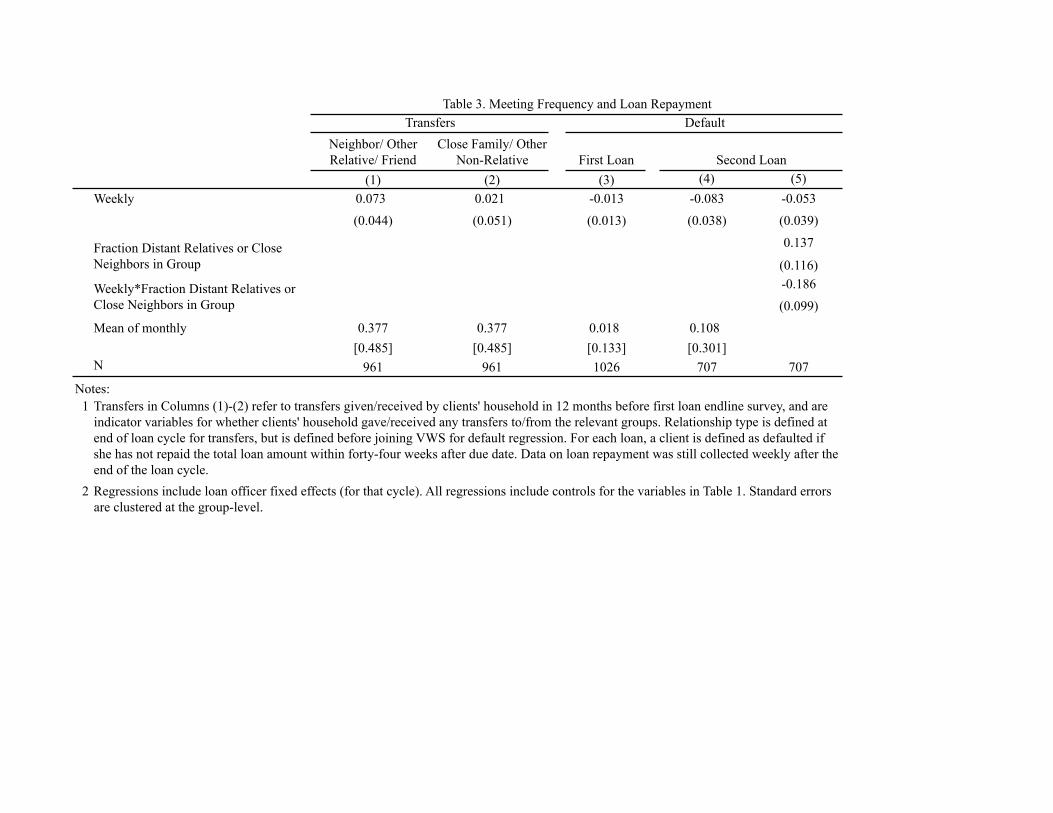

To test whether weekly meetings are associated with improvements in informal insurance, we

consider two measures of vulnerability to shocks: financial transfers between individuals other than

immediate family and loan default. At the end of the first loan cycle clients were administered a

survey that asked about the number and amount of transfers to and from individuals of fourteen

17Our regression specification is the individual level equivalent of equation (1).18The client was described the following scenario: “Imagine a person walking down the street sees someone in

front of him/her drop their wallet. Upon inspection, she finds that the wallet contains Rs 200 and the owner’s nameand phone number. The finder must decide whether to keep it or return it to its owner.” She was asked to rank thelikelihood that the finder would return the wallet if she was her average group member on a 1-5 scale described asfollows: “1-Would not return the money. 2- Unless someone knows she has got the wallet, would not return it. 3-Aslikely to return as not. 4- Will return, but might take up to a week. 5- Will return immediately.”

12

different relationship categories over the past year. Figure 2 shows the average transfers given by

a client by type of relationship. Overall, weekly clients give more transfers to all categories of

individuals except non-relatives who are neither friends nor neighbors, a category that is unlikely to

include members of a client’s loan group. Among client pairs in the two categories where gains in

social ties are concentrated - friends (at endline), neighbors and other relatives - , total transfers are

28% higher among weekly clients. Since the majority of clients report no transfers, for regression

estimates we consider the binary outcome of whether the client reports any transfers to or from

individuals inside or outside of her immediate family rather than amount of transfer.

To measure default, we use VWS transactions data to track client repayment behavior during

both the experimental and the subsequent loan cycle. At the end of our loan experiment, 69% of

clients took out a second loan with VWS, and the rate did not differ across monthly and weekly

clients. On average, the second loan was 35% larger than the first, and all clients repaid on a

fortnightly schedule.19 We consider a client in default on either loan if she failed to repay in full 44

weeks after the loan was due (roughly the length of an additional loan cycle).20

For both outcomes, we estimate OLS regressions of the form:

ygi = β1Wg +Xgγ1 +Xiγ2 + αg + εgi (3)

where variables and indices are defined as in Equation (2).

The results are presented in Table 3. Column (1) reveals that weekly clients are 19% more

likely to report transfers outside the family at the end of the experiment, and the difference is

significant at the 10% level. Furthermore, these transfers do not appear to displace transfers within

the immediate family or to individuals outside of the neighborhood (column (2)), suggesting a net

gain in informal insurance.

Since improvements in risk-sharing have implications for default rates, the next three columns

19Clients in the second loan cycle were subject to experimental variation in the timing of first repayment, but itwas independent of their first loan repayment schedule. See Appendix 7.3 for details.

20Results are very similar if we vary the time period over which default is defined.

13

look at default in the experimental and subsequent loan cycles. Column (3) shows that frequent

meetings are not associated with lower default in the first loan cycle. An important caveat is that

default is extremely low for first-time borrowers (1.8%), presumably due to the fact that, following

standard MFI practice, first loan sizes are below client demand for credit and “carrying capacity.”

However, once clients have graduated to larger loans, differences in default emerge despite the fact

that all clients have by that point converged to the same meeting frequency (fortnightly). Clients

assigned to monthly meetings for their first loan are four times more likely to default on their

second loan relative to clients assigned to weekly meetings for their first loan, and the difference is

statistically significant (column (4)).

Next we examine whether default reductions were concentrated among weekly clients most

likely to experience gains in social contact. The point estimates in column (5) indicate that this is the

case: There is a large and significant effect of weekly meeting on default only among clients with a

sufficient number of close neighbors and/or distant relatives in their group. This is reassuring since it

provides evidence that default patterns are not driven by the direct effect of meeting frequency. That

is, if the main channel of influence were the meeting itself (e.g. the oath, loan officer indoctrination,

ability to repay in small installments), we would not expect default rates to differ systematically

by features of group composition that do not directly predict default. We interpret the findings in

Table 3 as prima facie evidence that meeting more frequently helped clients build stronger social

ties and then leverage these social ties to deal with shocks (and maintain repayment).

The findings in Table 3 compliment Table 2 results in two ways: First, changes in social

contact that occur as a result of meeting regularly in loan groups have real economic returns and

therefore correspond to economically meaningful changes in social capital. Second, these measurable

returns to new relationships do not appear to be crowding out equally valuable relationships with

people outside of the loan group, as evidenced by lower overall vulnerability to shocks. Hence, we

can conclude that our intervention caused a net gain in social capital.

14

4 The Lottery: Disentangling Channels of Influence

A shortcoming of our survey data is that we cannot directly observe instances of risk-sharing

between group members, only aggregate outcomes (total transfers and default). Hence, to gather

direct evidence on the effect of group meetings on economic cooperation and evaluate the potential

channels of influence, we conducted a field experiment in the form of a promotional lottery more

than a year after clients completed their first loan cycle (average final repayment and survey dates

were April 2007 and July 2008, respectively). Our experiment, a variant of laboratory dictator and

trust games (Forsythe et al., 1994; Berg et al., 1995), was designed to elicit willingness to form

risk-sharing arrangements in a field setting.21

4.1 Design

We drew a random sample of 450 clients and successfully contacted 432 spread across 98 groups,

yielding a final sample of 129 weekly and 321 monthly clients (see Appendix for details). Table

1 provides a randomization check using group-level (Panel A) and client-level (Panel B) variables.

Column (4) shows that the lottery sample is representative of the experimental population, and

columns (5) and (6) examine the balance of voucher randomization (described below) on multiple

characteristics. As before, the two characteristics which are unbalanced remain fraction Muslim

and years in the neighborhood. The weekly clients in the Rs. 200 voucher randomization also

have slightly fewer closer neighbors (compared to monthly counterparts). We continue to report

regressions with the full set of controls and report any instances where the results vary with controls.

The protocol was as follows: Surveyors approached each selected client in her house and

invited her to enter a promotional lottery for the new VWS retail store.22 The lottery prize was gift

vouchers worth Rs. 200 ($5) redeemable at the store (see Appendix for the surveyor script). Aside

21In the dictator game, the experimenter asks an individual (sender) to divide a fixed amount of money betweenherself and another individual (receiver). In the trust game, the money transfer is typically tripled by the experimenterand the receiver is explicitly asked how much she wishes to send back to the sender.

22Importantly, the lottery protocol was conducted before the Table 4 survey data were collected.

15

from banking, VWS undertakes many community interventions and conducts regular promotional

activities in an effort to attract and retain clients. For this reason, our intervention is likely to seem

natural in this setting.

The client was informed that, in addition to her, the lottery included ten clients from different

VWS branches, which she was therefore unlikely to know. If she agreed to enter the draw (all clients

agreed), then she was given the opportunity to enter any number of other members from her first

VWS group into the same draw. Any group member she entered into the lottery would receive a

lottery ticket delivered to her house and be told whom it was from. She was told that the other ten

participants would not be given the opportunity to add individuals to the lottery.

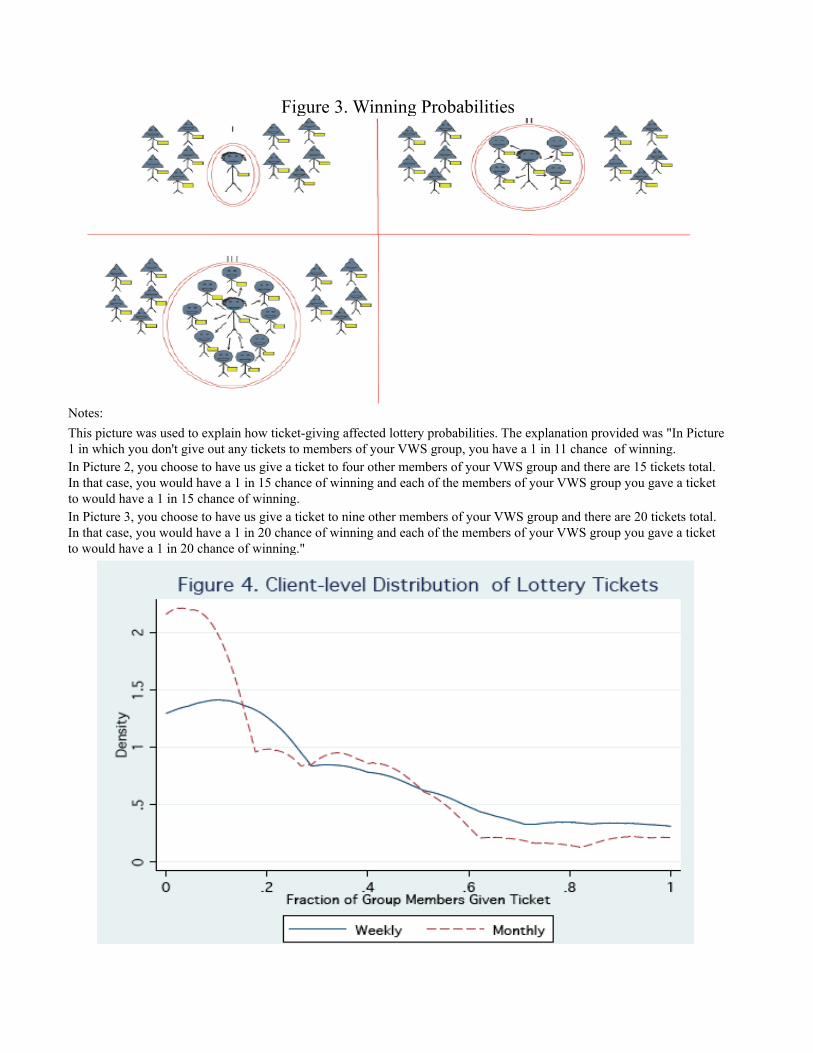

To clarify how ticket-giving influenced her odds of winning, the client was shown detailed

payoff matrices (see Figure 3). Enumerators explained that she could potentially increase the

number of lottery participants from 11 to as many as 20, thereby increasing the fraction of group

members in the draw from 9% to up to 50% while decreasing her individual probability of winning

from 9% to as low as 5%.

A client belonging to a ten-member group made nine pair-wise choices. Similar to trust and

dictator games, a member who received a ticket was not required to share her winnings. In the

absence of any sharing arrangements, the Nash outcome is to not give any tickets. Ticket-giving

increases a client’s expected payoff only if she trusts the recipient to share lottery earnings.

While alternative sharing arrangements are feasible, for expositional ease, we consider the

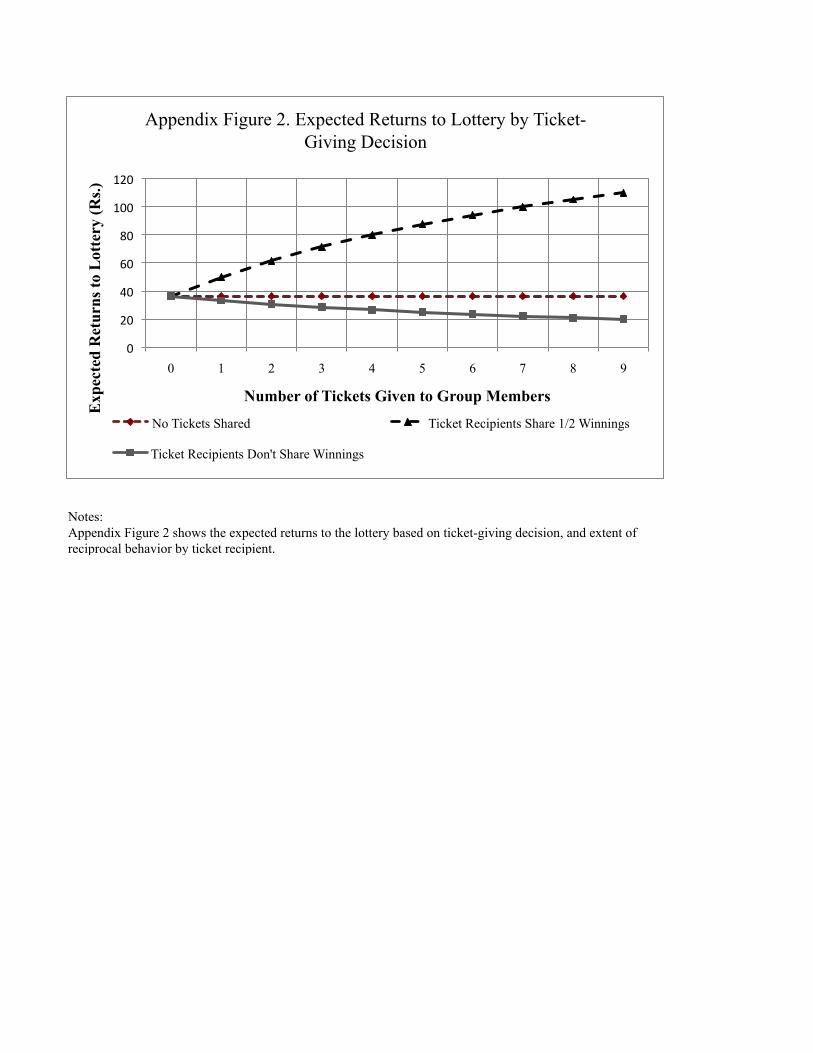

simple case of pairwise cooperation when the client (or sender) gives a single group member (receiver)

a ticket. For this pair, expected joint earnings increase since their joint chances of winning the lottery

rise from 9% to 17%. There are mutual gains from cooperation (if the receiver shares half of her

earnings, the sender’s expected lottery earnings rise from Rs.18 to 25 and the receiver’s expected

earnings rise from Rs.0 to 8.3), but costs to the sender if the receiver does not plan to share earnings

with her (in which case the sender’s expected lottery earnings fall since her individual probability

of winning the lottery declines from 9% to 8% as the pool of lottery entrants rises to twelve).

Appendix Figure 2 illustrates how ticket-giving changes a client’s expected payoff. The top

16

line shows her expected payoff when the receiver shares half her winnings with the client, and the

bottom line shows the reduction in her payoff if no receiver shares. The figure also illustrates a key

difference between our lottery and the trust game: Pairwise returns in the lottery depend on total

tickets given. If the sender trusts all other group members equally then she would give equally to

all group members. However, if trust of group members varies, then recognition of this externality

will further constrain ticket-giving to less trusted group members.23

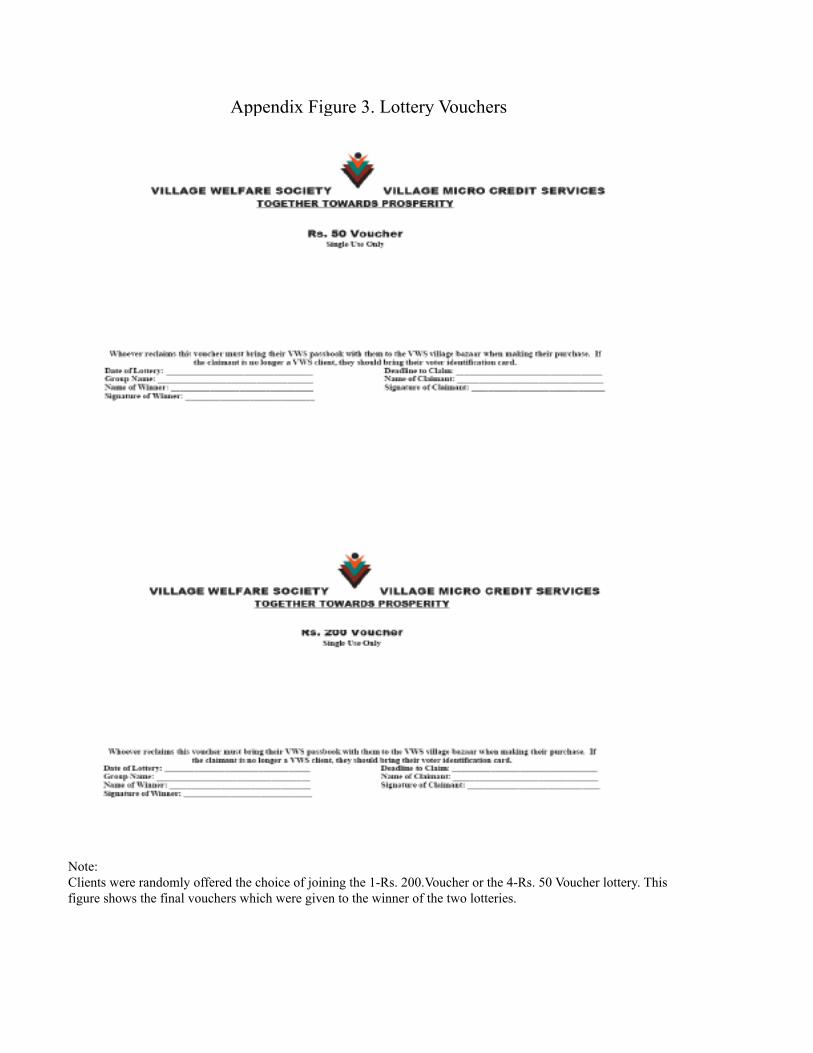

Finally, to isolate cooperative from purely altruistic motives for giving tickets, our experiment

varied the divisibility of the lottery prize. For a randomly chosen half of participants, the lottery

prize was one Rs. 200 voucher, while for the other half it consisted of four Rs. 50 vouchers.

Appendix Figure 3 provides pictures of these vouchers. A voucher could only be redeemed by one

client and all vouchers expired within two weeks.

4.2 Predictions

Stronger social ties should positively impact pro-social behavior. Hence,

Prediction 1 Higher meeting frequency in the first loan cycle will increase ticket-giving.

Ticket-giving could increase for two broad reasons. First, in a setting in which clients lack

access to explicit binding contracts, an increase in the frequency of interaction can enable a pair of

clients to devise and implement punishment and reward strategies that sustain reciprocal economic

arrangements, including informal insurance schemes (Karlan et al., 2009; Besley and Coate, 1995;

Ambrus et al., 2010). Alternatively, more frequent meetings may increase a client’s unconditional

altruism towards other group members. To distinguish between these two possibilities, we exploit

random variation in the divisibility of the lottery prize and make use of baseline heterogeneity across

clients in self-reported financial autonomy to make transfers, both of which should influence the

ticket-giver’s expectations of reciprocal ties. Neither a more divisible lottery prize nor the receiver’s

ability to make transfers should induce greater ticket-giving unless the sender cares about the ease

23It is also the case that, in our game, sender’s action and payoffs are stochastically related which also differentiatesit from the classic trust game.

17

of reciprocal transfers. Hence,

Prediction 2 If the primary channel is (unconditional) altruism, then the incidence of ticket-giving

will be independent of perceived ability of the receiver to reciprocate.

Meeting more frequently during the initial loan cycle can encourage reciprocal arrangements

between client pairs in multiple ways. Under certain circumstances more frequent meeting may

increase the scope of cooperation by improving clients’ ability to monitor other members’ actions.

Consider the case in which members can influence their income through hidden actions. If different

actions by members at time t imply different initial conditions for the income generation process

between t and t + ∆ (where ∆ is the time period between two meetings), observing income (at

meetings) provides a public signal of a member’s action (Costa, 2007).24 Hence, higher frequency

of meeting can improve monitoring in the sense of increased precision of the public signals.

Meeting more often can also change individuals’ effective discount factor. In a repeated

game framework, the suitable use of punishment strategies (e.g. grim trigger strategy) can sustain

cooperation among sufficiently patient individuals (Fudenberg and Maskin, 1986); for application

to informal insurance see Coate and Ravallion (1993)). Here, a higher frequency of meeting can be

modeled as reducing the period length between each repetition of the stage game. With perfect

monitoring, this is equivalent to raising the effective discount factor of pair members, which makes

it more likely that relatively impatient members can sustain cooperation. The positive returns to

mandating more frequent meeting will persist as long as meetings continue to reduce the expected

duration between repeat interactions. Hence,

Prediction 3 Increases in ticket-giving among weekly clients will be concentrated among those who

are relatively impatient only if the channel is improved reciprocal sharing arrangements.

An alternative channel through which repeat interaction at the start of a relationship can

facilitate reciprocity is by hastening learning about other group members’ ability and willingness

to cooperate. Such a learning-based story by itself would imply that returns to mandating frequent

24If actions do not differentiate initial conditions, higher frequency signals may not increase the reliability ofinformation extracted from public signals (D. Abreu and Pearce, 1991; Fudenberg and Levine, 2009).

18

interaction will diminish over time. To evaluate the importance of learning about types in explaining

our results, we exploit the following fact: At the time of our lottery, a subset of clients were on

a subsequent loan cycle in which they had been re-randomized onto weekly or monthly schedules.

This allows us to test the following prediction:

Prediction 4 If the primary channel is learning, the effect of more frequent interaction will be

significantly lower in future loan cycles.

4.3 Results

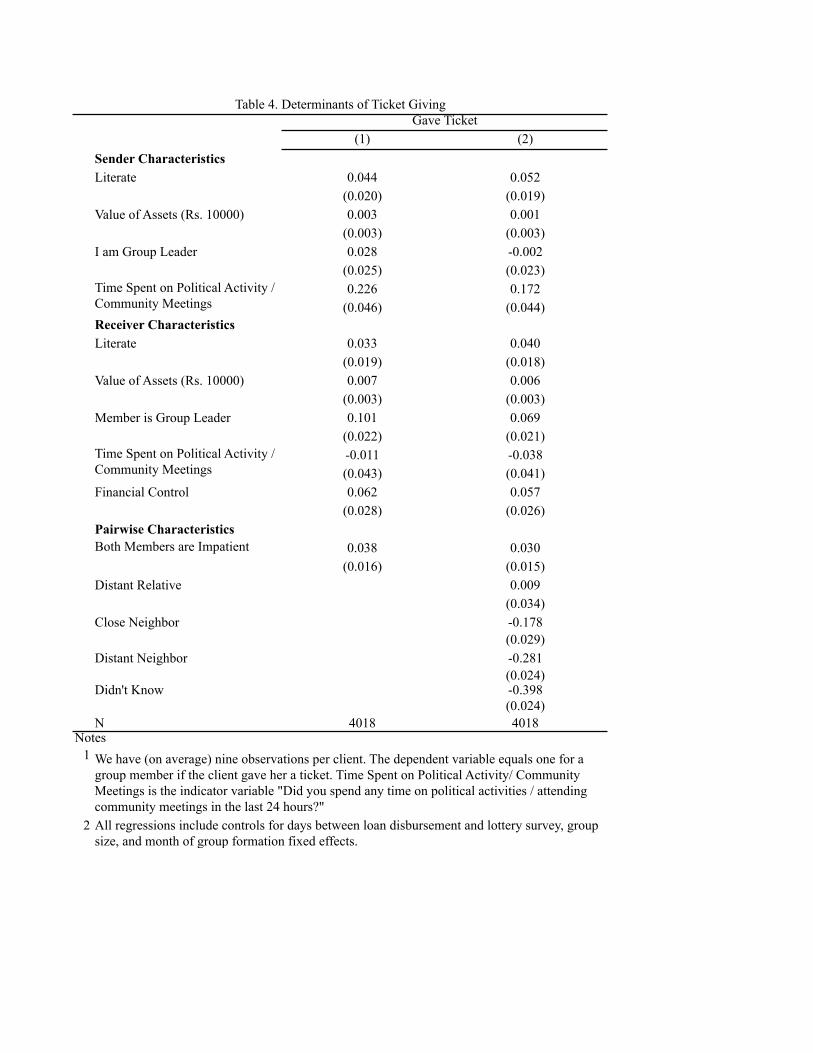

4.3.1 Determinants of Ticket-Giving

Our primary outcome of interest is ticket-giving. For each member of a client’s first loan group, we

recorded whether the participant entered her into the lottery. In total, 57% of participants gave

at least one ticket, which is very similar to individual propensity to give in dictator games (Levitt

and List, 2009). To see how individual and pairwise characteristics, including meeting frequency,

predict ticket-giving by lottery client i in group g, we pool our sample of weekly and monthly lottery

clients and estimate:

ygmi = Xiγ1 +Ximγ2 +Xmγ3 + φg + αg + εgmi (4)

where ygmi denotes whether client i gave group-member m a ticket. We are interested in the

influence of sender characteristics (Xi), receiver characteristics (Xm), and pairwise characteristics

(Xim). All regressions include loan officer (αg) and month of group formation (φg) fixed effects.

The basic patterns in the data are broadly consistent with findings in the trust and dictator

game literatures. Column (1) of Table 4 shows that educated clients are more likely to give and

receive tickets. Richer respondents, those who state in baseline that they can make transfers outside

of their household (financial control), and the group leader receive more tickets. In contrast, re-

spondents who participate in community and political events are more likely to give but not receive

tickets. Finally, ticket-giving is higher when both members are impatient.25 In column (2), we

25We measure baseline impatience with a series of questions where the client chooses between Rs. 200 today versus

19

distinguish between pairs on the basis of initial social distance. As expected, ticket-giving falls with

social distance: Neighbors are much less likely to receive a ticket than friends or family members,

and group members that were previously unknown rarely receive tickets (the unconstrained means

across these three categories are roughly 25%, 53%, and 11%).

4.3.2 Initial Meeting Frequency and Ticket-Giving

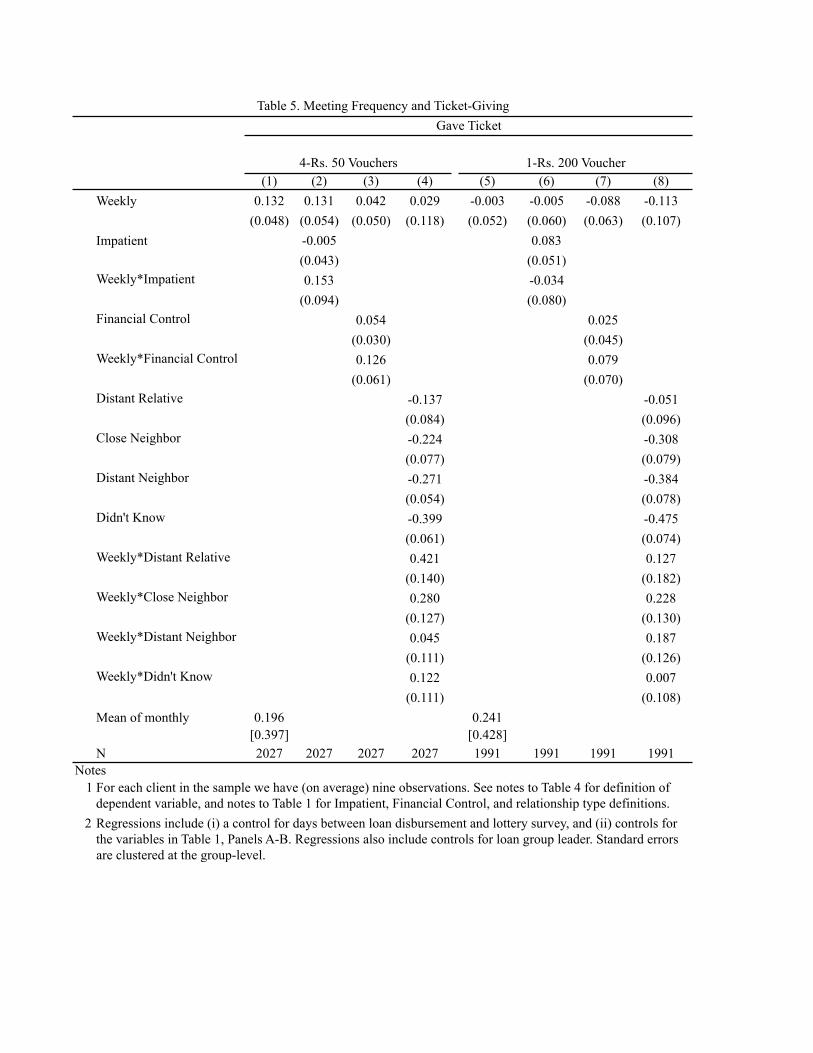

Next we examine whether ticket-giving behavior varied systematically with initial meeting fre-

quency. Figure 4 shows the distribution of tickets for weekly and monthly clients (in percentage

terms to account for group size differences). After zero tickets, the fraction of group members that

receives tickets declines gradually and then levels out after 60%. Weekly clients are substantially

less likely to give no tickets and more likely to give tickets to more than half of their group.

In Table 5 we provide regression results of the form given by equation (2). Columns (1) - (4)

present results for clients offered the divisible lottery prize while columns (5) - (8) show results for

clients randomized to the lottery with the less divisible prize. A comparison of columns (1) and

(5) shows that, relative to her monthly counterpart, a client in a weekly group is significantly more

likely to give a ticket to a group member if and only if the lottery prize is divisible. Weekly clients in

the divisible randomization are 67% more likely to give tickets than monthly clients, whereas there

is almost no difference between monthly and weekly clients when the prize comes in the form of one

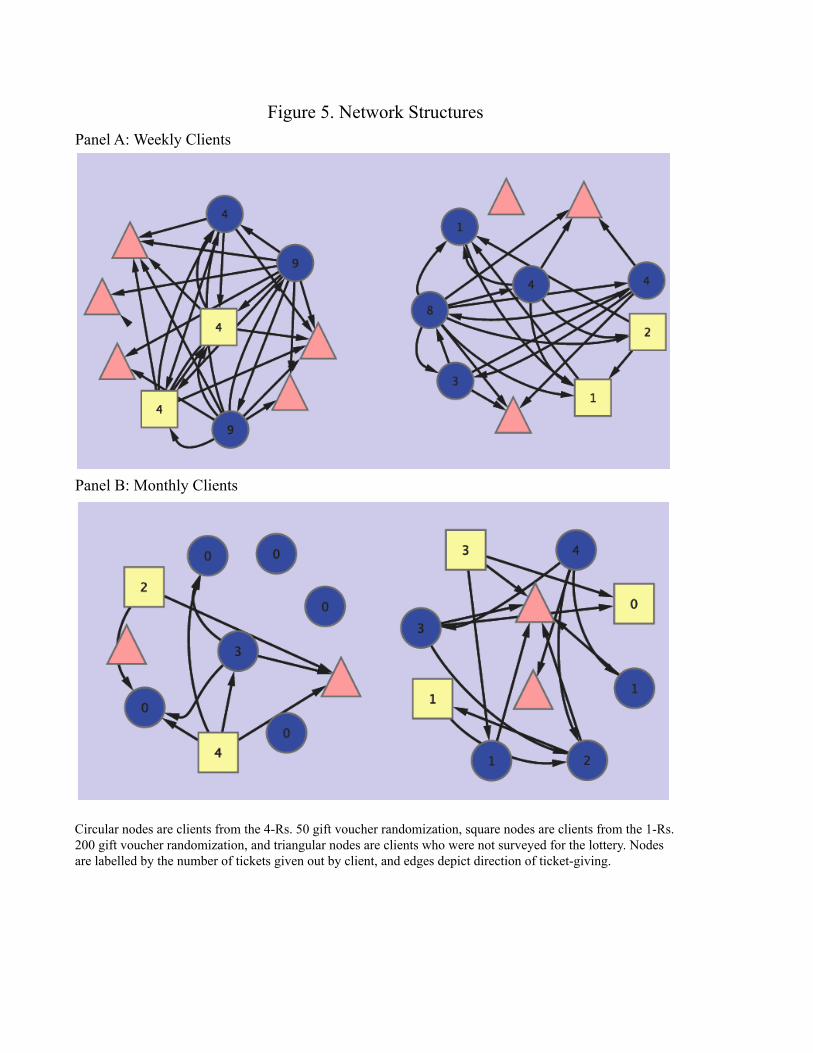

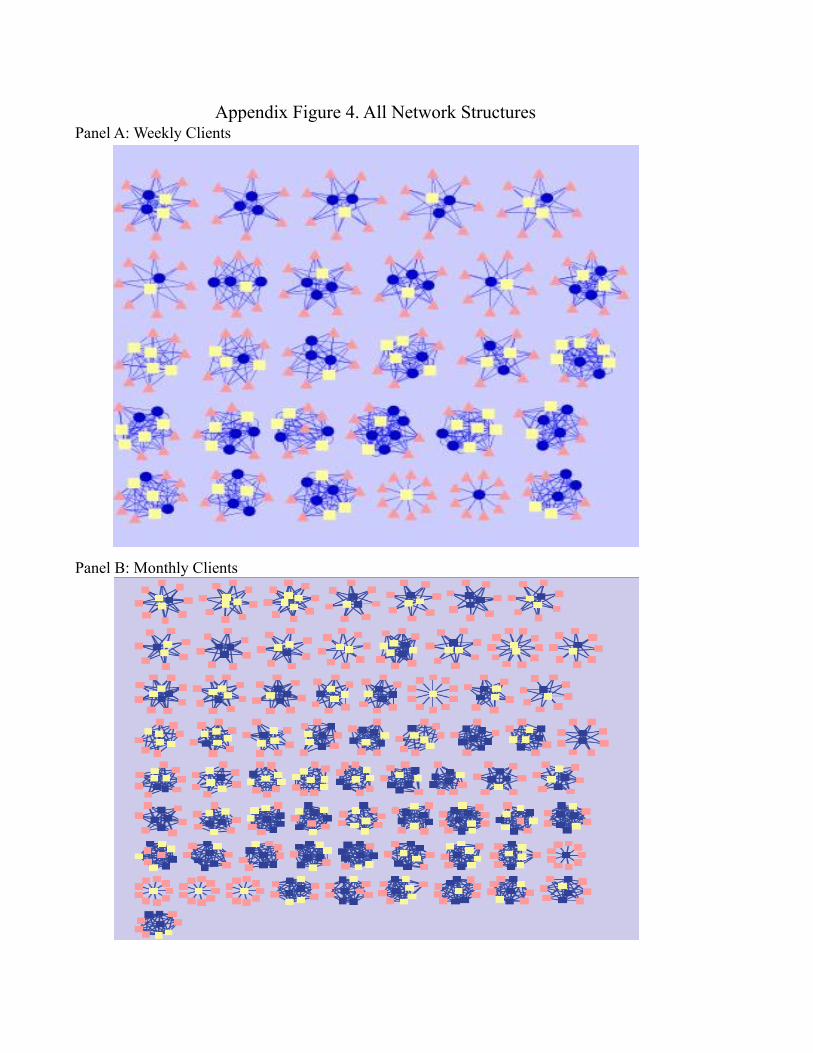

large voucher.26 Figure 5 shows four loan group networks that highlight the empirical ticket-giving

patterns found in the data (the full set of ticket-giving networks are shown in Appendix Figure 4).

Weekly clients’ higher propensity to give tickets is reflected in the higher relative connectedness of

the weekly networks in the divisible (i.e., circular nodes) but not the indivisible (i.e., square nodes)

gift voucher randomization. Significantly higher ticket-giving among weekly clients when the lottery

prize is easily divisible suggests that more frequent meetings increased ticket-giving by increasing

between Rs. 210 and Rs. 250 in a month.26In the pooled sample, the estimate of the coefficient on the interaction between weekly and divisible prize is

similar in magnitude but statistically insignificant, with a t-statistic of 1.54.

20

expectations of reciprocity.27 If frequent meetings had only increased unconditional altruism, then

ticket-giving would be independent of voucher divisibility.

In columns (2) and (6), we examine whether ticket-giving is sensitive to a client’s subjective

discount rate. If expectations of reciprocal transfers sustain ticket-giving, ticket-giving should only

be observed among sufficiently patient client pairs, and more frequent interaction can potentially

allow relatively impatient pairs to sustain cooperation. To investigate this, we create a dummy that

equals one if both members of a pair prefer Rs. 200 today to Rs. 250 in a month. In column (2),

we observe that weekly meetings make it more likely that impatient pairs engage in ticket-giving:

the coefficient estimate on the interaction between weekly and impatience is large and statistically

significant. Again, this relationship is only present for clients assigned to the divisible lottery prize,

consistent with the fact that ticket-giving is no greater for weekly clients when the prize is less

divisible. This pattern suggests that risk-sharing concerns underlie increased ticket-giving among

weekly clients, since impatience should not influence unconditionally altruistic behavior.28

In columns (3) and (7), we examine whether ticket giving is sensitive to the level of financial

control exercised by the receiver. In total, 89% of clients responded affirmatively to the baseline

survey question, “If a close relative like your parents or siblings fell sick and needed money, would

you be able to lend money to that relative, if you had the extra money?” If risk-sharing motivates

the higher level of ticket-giving observed in the divisible voucher case, and assuming that this

characteristic is to some extent observable to other members, we would expect a client to avoid

giving tickets to those who are unable to reciprocate. In line with this, we see that marginal ticket-

giving is concentrated among the set of potential receivers who report that they have the financial

independence to make transfers outside of the household.

Finally, in columns (4) and (8), we examine whether the weekly effect differs by initial social

27Anecdotal evidence from conversations with clients also suggested that they believed multiple vouchers increasedthe likelihood that those they gave tickets to would share any future winnings.

28We hypothesize that the net positive effect of pairwise impatience on ticket giving among weekly clients resultsfrom impatient clients likely having smaller social networks before the start of the loan cycle, and consequentlyhaving higher demand for risk-sharing arrangements.

21

distance. The coefficient estimates on the interaction terms indicate that increased ticket-giving

by weekly clients is driven by increased giving to close neighbors and distant family. The fact that

increased ticket-giving by weekly clients is concentrated among the categories of pairs in which we

also observe a significant effect on social contact (Table 2) is consistent with our interpretation

that higher long-run social contact increased propensity to form risk-sharing arrangements. The

fact that moving from a monthly to a weekly repayment schedule did not influence ticket-giving

to close family and friends provides an important placebo check: For immediate family members

or old friends, repayment schedules should not influence learning or monitoring since these pairs

presumably know each other well and see each other often outside of meetings. Also consistent with

this is the fact that ticket-giving is no higher among weekly relative to monthly clients who report

that they never see one another: Both sets of clients give tickets to roughly 15% of group members

whom they have not seen at all in the past 30 days.29

The fact that we observe no difference among monthly clients’ ticket-giving across the two

voucher categories, along with the fact that for monthly clients ticket-giving is independent of

impatience and ability to reciprocate, suggests that either ticket-giving among these members is not

primarily motivated by reciprocity, or that only marginal risk-sharing arrangements are sensitive to

small barriers to trust such as prize divisibility. A few empirical patterns support this interpretation:

First, 61% of tickets given by monthly clients do not appear to be reciprocal arrangements, based

on the fact that they are given either to individuals they have not seen in the last 30 days at the

time of the lottery or from whom they claim they would not ask for help in case of emergency, or

to immediate family members. Second, survey data indicate that monthly meetings did not lead

to long-run changes in social capital, indicating an absence of relatively new informal risk-sharing

arrangements among monthly clients. For instance, monthly group members are no more likely to

report giving or receiving transfers to individuals outside of the immediate family between baseline

and follow-up (unreported).

To examine whether ticket-giving was associated with reciprocal transfers, six months after

29Authors’ tabulations.

22

the lottery, we surveyed 39 of the 47 clients who received a ticket from a group member and won that

lottery.30. Although we do not observe explicit voucher-sharing (the winners always redeemed their

vouchers as opposed to giving them away), nearly all clients (85%) remembered who gave them

their ticket, and a quarter reported greater willingness to share post-lottery. We also observe a

significant difference across weekly and monthly clients, consistent with higher rates of risk-sharing

relative to altruism among ticket-givers – 7/23 (30.4%) of weekly clients but only 1/16 (6.3%) of

monthly clients report such willingness.31

4.3.3 Hastening versus Sustaining Cooperation

As explained in Section 4.2, more frequent interaction may help sustain cooperative arrangements

indefinitely, or it may simply hasten the formation of cooperative arrangements through more rapid

learning about client types. One basic piece of evidence against the learning story is that, at the

time of the lottery, the majority (69%) of clients have been in loan groups together for almost two

years, by which point types should arguably be revealed even among those who only met monthly

for the first several months (during the experiment).

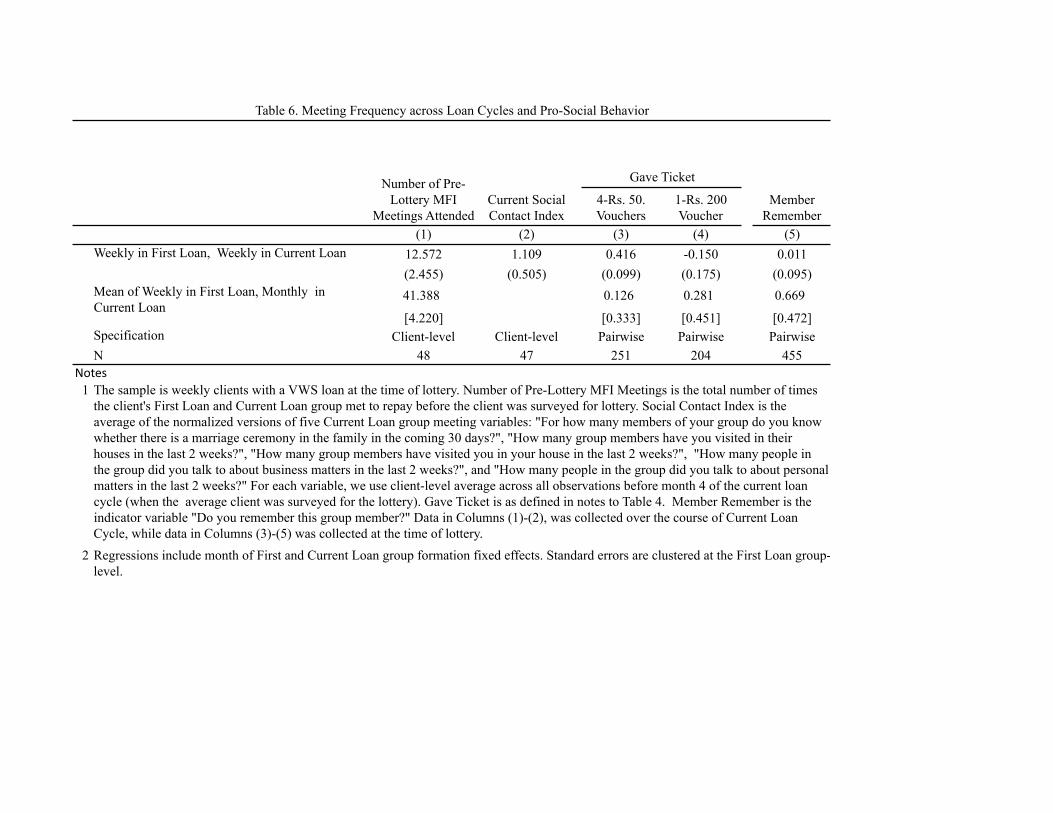

To further disentangle these two channels, we exploit experimental variation in meeting fre-

quency at two different points in time. At the time of our lottery, roughly a third of the clients (137

out of 432) were on a subsequent VWS loan cycle in which groups were re-randomized into weekly

and monthly meetings (see Appendix Figure 1). VWS has a preference for keeping client groups

together across cycles, but group members are replaced when there is drop out. On average, 60%

of current group members were also in the first loan group.

We consider the sub-sample of 48 third loan cycle clients who had been on the weekly schedule

in the first intervention and examine whether current meeting frequency influences current levels of

30Among this subset of ”indirect” lottery winners, 25 were in weekly and 22 were in monthly groups.31The specific question was, “If your friend asked to borrow money or goods from you in the future, do you think

you are more, less, or equally likely to share with her than you were before the lottery?” In terms of actual sharing,the most commonly shared goods (post-lottery) were food and sarees. In two cases, winners reported lending moneyto the group member who had given them the ticket.

23

cooperation. This allows us to observe whether forcing clients who already know each other well to

continue interacting regularly further increases cooperation. If so, then it is likely that, in addition

to any short-run learning effects that hasten cooperation between members, meeting frequency has

persistent benefits via monitoring or discount rate channels.

For this subset of clients, we use pairwise data on ticket-giving to estimate

ygmi = β1Wcg + δ1φg + δ2Dg + αg + εgmi (5)

where W cg is an indicator variable for the client being on a weekly repayment schedule in the current

loan cycle. The other variables are defined as in equations (1) and (2). Given the reduced sample

size we report regressions without controls (we observe similar but noisier estimates with controls).

Columns (1) and (2) of Table 6 show that clients in loan groups that were randomly assigned

to the weekly schedule in both the first and current loan cycle (“weekly-weekly”) currently see one

another significantly more often both at MFI meetings and outside of meetings than clients initially

on the weekly schedule but later assigned to the monthly schedule (“weekly-monthly”).32

Correspondingly, a weekly-weekly client is 29% more likely to engage in pro-social behavior

than a weekly-monthly client when the prize is easily divisible (column 3). As before, we find

no evidence of increased giving for the indivisible voucher option (column 4). We interpret the

difference for weekly-weekly clients in column (3) as evidence that repeated interactions among

loan group members helps sustain cooperative arrangements in the long run.

While the period over which learning about other clients can occur is uncertain, it is important

to note that, by the time of the survey, clients in this subsample had been interacting regularly

for 2.5 loan cycles during which time they saw each other weekly for at least six months and every

other week for at least six months more. Consistent with this, we see no difference across weekly-

32In column (1), the dependent variable is the number of required MFI meetings across the first and currentintervention (at the time of the survey). At the time of the lottery, a weekly-monthly client had met, on average,41 times, while a weekly-weekly client had met roughly 30% more often. Further, the likelihood of a client havinggroup members from the first loan in her current group is independent of repayment frequency (unreported).

24

weekly and weekly-monthly clients’ in the propensity to remember the names of their first loan

group members at the time of survey (column 5).

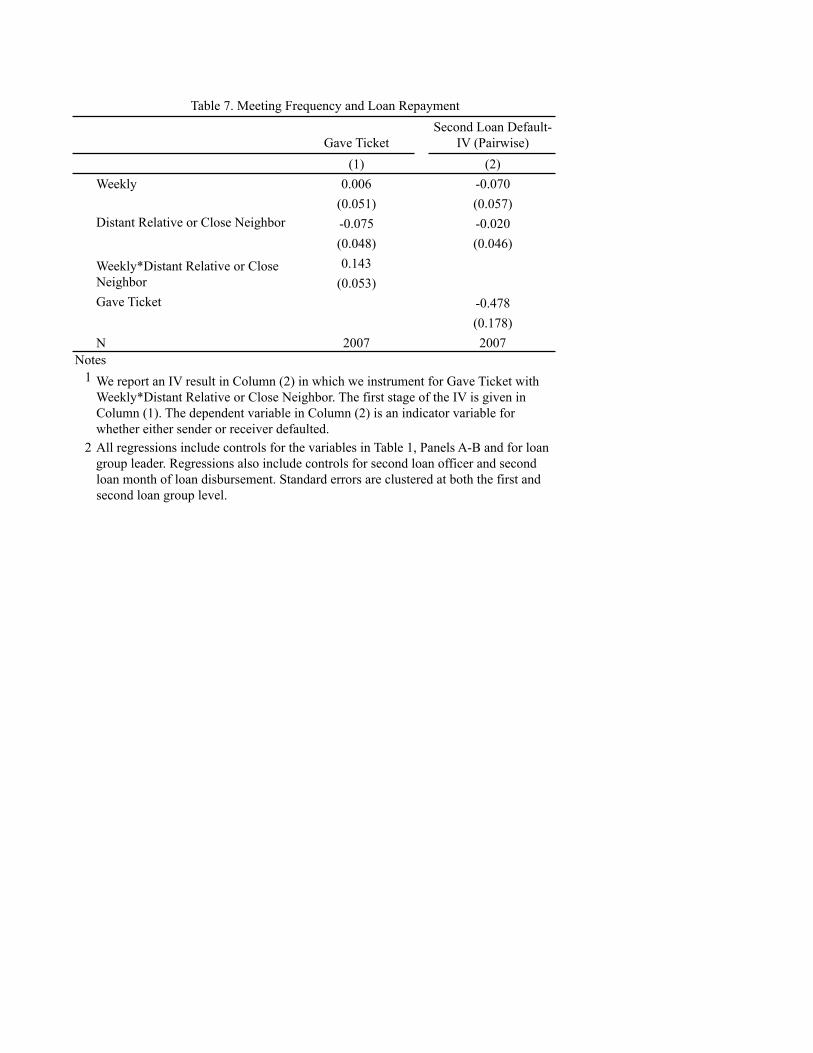

4.4 Social Capital and Default

The above evidence suggests that ticket-giving between clients reflects reciprocal economic ties.

Further, the strength of these ties is influenced by group composition and meeting frequency during

the lottery client’s first loan cycle. Based on these patterns, we can directly estimate the effect of

these ties on default risk using an instrumental variables (IV) approach in which random assignment

to a weekly group in the first loan cycle and having a distant relative or neighbor as a group member

is used as an instrument for ticket-giving. The second stage equation is:

yim = γ1tim + γ2pim + β1Wg + δ1φg + δ2Dg + αg + εgmi (6)

where tim is an indicator variable that equals one if either member of the pair gave a ticket and

pim is an indicator variable that equals one if the members are either close neighbors or distant

relatives. The other variables are as defined in equation (5).

The first stage equation takes the form

tim = ρ1pim + ρ2Wg + ρ3pim ×Wg + ρ4φg + ρ5Dg + αg + εgmi. (7)

The excluded instrument is the interaction between the weekly indicator (for first loan cycle) and

the pair being distant relatives or close neighbors.

The first stage estimates are reported in column (1) of Table 7. Client pairs consisting of

distant relatives or close neighbors are 14% more likely to engage in ticket-giving if they were

randomly assigned to a weekly group in their first loan cycle. The 2SLS estimates are reported

in column (2). The likelihood that at least one member of the pair defaults in the second loan

cycle is roughly 50% lower and statistically significant if the pair enjoy reciprocal economic ties, as

25

evidenced by ticket-giving in the lottery.33

The validity of the IV estimate depends on the assumption that meeting frequency influenced

default rates only through the development of social ties. Since our experiment varied both the

frequency of client interaction and the frequency with which they made loan payments and interacted

with the loan officer, the central concern is that meeting frequency also influenced clients’ financial

habits. In that case, simply comparing the behavior of weekly and monthly clients does not allow

us to disentangle the effect of social capital from the effect of repayment schedules on default.

For instance, repayment frequency could have influenced client income through long-run changes

in savings behavior if clients assigned to repay weekly on their first loan developed better savings

habits that lasted into subsequent loan cycles.34

For this reason, we do not use assignment to weekly groups as the instrument but rather the

differential impact of being in a weekly group for clients of a specific relationship type – those who

are reasonably close but not extremely so in terms of geography or familial ties. As there is no

obvious reason why the importance of fiscal discipline or, more generally, loan officer indoctrination

should depend on this particular group characteristic, the pattern suggests that social capital is

the central channel of influence. It is also important to keep in mind that both ticket-giving and

default are measured when clients are no longer on their initial repayment schedule. Hence, it is not

the case that, at the time of the lottery, clients in the monthly treatment are struggling to make

larger payments, which could explain their reluctance to give tickets. Perhaps most importantly,

alternative channels of influence such as financial habits cannot account for the fact that ticket-

giving within weekly clients is sensitive to voucher divisibility, which was randomly assigned.

33The results are very similar in magnitude and statistically significant if we estimate these regressions at the clientrather than the pair level.

34While possible that income varied across repayment schedules through small interest rate differences (weeklyclients faced slightly higher implicit interest rates since they had to repay faster); however, such differences are verysmall and yield opposite predictions to what we find (weekly clients are more generous and default less).

26

4.5 The Costs of Building Social Capital

The evidence in Table 7 implies significant benefits to MFIs from building social capital. However,

these benefits do not come free given non-trivial transactions costs of meeting four times as often.

For clients, we estimate that weekly meetings entail approximately two additional hours per month,

or 15 hours over the course of an average loan cycle. Meanwhile, banks could cut transactions costs

per client by nearly three-fourths - or reach nearly four times as many clients for the same cost -

by moving from a weekly to a monthly schedule.

In terms of benefits default data for the second loan cycle shows that the average client who

was on monthly repayment during her initial loan cycle defaults on Rs. 150 more than the average

client previously on a weekly repayment schedule, which is almost the same as the bank’s additional

transaction cost per client of meeting weekly.35 Hence, a conservative back-of-the-envelope calcu-

lation suggests that weekly meetings may be cost-effective for a MFI, which explains why MFIs

persist with high frequency repayment schedules despite the higher transactions costs.

Evaluating the social planner’s problem is less straightforward since the costs and benefits to

clients of meeting weekly are difficult to calculate. The total cost to clients of regular repayment

is likely to exceed the simple time cost of meeting attendance given the additional financial burden

of making regular installments, and the total benefits of increases in social capital are likely to

exceed the reduction in default risk. While these tradeoffs are difficult to observe, given the wealth

of benefits from improved informal insurance and potential externalities from social capital such

as information transfers between clients, it is likely that clients are also better off on a weekly

schedule.36

35We estimate that loan officers spend an additional 1.5 hours per month per group, which amounts to 3.75% oftheir monthly wage for every 10 customers, or Rs. 150. Given that a loan cycle is ten months and contains tenmembers, this implies an average cost per client of roughly Rs. 150.

36While there is one potentially important negative externality that we also do not observe – crowd out of otherforms of social capital enjoyed by the client – as argued in Section 3.2, the reduction in client default arguablycaptures the net effect of meeting frequency on social capital inside and outside of loan groups.

27

5 Conclusions

A widely held belief across social scientists in many disciplines is that social interactions encourage

norms of reciprocity and trust. In fact, participation in groups is often used to measure an indi-

vidual’s or community’s degree of economic cooperation (see, for instance, Narayan and Pritchett,

1999; Alesina and Ferrara, 2002). However, while the notion is theoretically well-grounded, it is

not clear from previous work whether the correlation between social distance and trust reflects the

causal effect of interaction on economic cooperation. Using field experiments, we provide rigor-

ous evidence that repeat interactions can in practice facilitate cooperative behavior by enabling

individuals to sustain reciprocal economic ties.

Further, our results demonstrate that development programs can increase social ties and

enhance social capital among members of a highly localized community in a strikingly short amount

of time. In our study, close neighbors from similar socio-economic backgrounds got to know each

other well enough to cooperate with only the outside stimulus of micro-finance meetings. While

many authors have suggested a link between social capital and MFI default rates, ours is the first

study to provide rigorous evidence on the role of microfinance in building social capital.

Our findings support the idea that complementarities in social capital acquisition creates the

possibility of multiple equilibria (Glaeser et al., 2002). This, in turn, suggests potentially large gains

from policies which facilitate interaction and help coordinate social capital investments, especially

in low income countries where formal risk-sharing arrangements remain limited. By broadening and

strengthening social networks the group-based lending model used by MFIs may provide an impor-

tant impetus for the economic development of poor communities and the empowerment of women.

While we cannot expect all communities to respond equally to such stimuli, our findings are likely

to be most readily applicable to the fast-growing urban and peri-urban areas of cities in developing

countries (such as Kolkata) where microfinance is spreading the most rapidly. Understanding how

other development programs or public policies can be designed to enhance the social infrastructure

of poor communities is a promising area of future research.

28

References

Alesina, A. and E. L. Ferrara (2002). Who Trusts Others? Journal of Public Economics 85 (2),

207–234.

Ambrus, A., M. Mobius, and A. Szeidl (2010). Consumption Risk-sharing in Social Networks .

mimeo.

Berg, J., J. Dickhaut, and K. McCabe (1995). Trust, Reciprocity and Social History. Games and

Economic Behavior 10, 122–142.

Besley, T. and S. Coate (1995). Group Lending, Repayment Incentives and Social Collateral. Journal

of Development Economics 46 (1), 1–18.

Carter, M. and M. Castillo (2003). Does It Take More than Markets to Get Ahead? An Experimental

Approach to Social Capital in South Africa. Agricultural and Applied Economics Staff Paper

Series, Paper No. 448, University of Wisconsin.

Carter, M. and M. Castillo (2004). Morals, Markets and Mutual Insurance: Using Economic

Experiments to Study Recovery from Hurricane Mitch. In C. Barrett (Ed.), Exploring the Moral

Dimensions of Economic Behavior. Routledge.

Coate, S. and M. Ravallion (1993). Reciprocity without Commitment: Characterization and Per-

formance of Informal Risk-Sharing. Journal of Development Economics 40 (1), 1–24.

Costa, A. O. (2007). Frequent Monitoring in Repeated Games under Brownian Uncertainty. Mimeo,

Universidad Carlos III de Madrid.

Costa, D. and M. Kahn (2003). Understanding the Decline in American Social Capital, 1953-1998.

Kyklos 56 (1), 17–46.

D. Abreu, P. M. and D. Pearce (1991). Information and Timing in Repeated Partnerships. Econo-

metrica 59.

29

DiPasquale, D. and E. Glaeser (1999). Incentives and Social Capital: Are Homeowners Better

Citizens? Journal of Urban Economics 45 (2), 354–384.

Do, Q.-A., S. Leider, M. Mobius, and T. Rosenblat (2009). Directed Altruism and Enforced Reci-

procity in Social Networks. Quarterly Journal of Economics, forthcoming 124 (4).

Forsythe, R., J. Horowitz, N.Savin, and M. Sefton (1994). Fairness in Simple Bargaining Games.

Games and Economic Behavior 6, 347–69.

Fudenberg, D. and D. Levine (2009). Repeated Games with Frequent Signals. Quarterly Journal

of Economics 124, 233–265.

Fudenberg, D. and E. Maskin (1986). Folk Theorem for Repeated Games with Discounting or with

Incomplete Information. Econometrica 54, 533–554.

Ghatak, M. and T. W. Guinnane (1999). The Economics of Lending with Joint Liability: Theory

and Practice. Journal of Development Economics 60 (1), 195–228.

Glaeser, E., D. Laibson, and B. Sacerdote (2002). An Economic Approach to Social Capital.

Economic Journal 112 (483), 437–458.

Glaeser, E., D. Laibson, J. Scheinkman, and C. Soutter (2000). Measuring Trust. Quarterly Journal

of Economics 115 (3), 811–846.

Gneezy, U., W.Guth, and F. Verboven (2000). Presents or Investments? An Experimental Analysis.

Journal of Economic Psychology 21 (5), 481–493.

Guiso, L., P. Sapienza, and L. Zingales (2004). The Role of Social Capital in Financial Development.

American Economic Review 94 (3), 526–556.

Humphreys, N., J. Fearon, and J. Weinstein (2009). Can Development Aid Contribute to Social

Cohesion After Civil War? American Economic Review 99 (2), 287–291.

30

Karlan, D. (2005). Using Experimental Economics to Measure Social Capital and Predict Real

Financial Decisions. American Economic Review 95 (5), 1688–1699.

Karlan, D. (2007). Social Connections and Group Banking. Economic Journal 117 (517), F52–F84,

02.

Karlan, D. and X. Gine (2009). Group versus Individual Liability: Long Term Evidence from

Philippine Microcredit Lending Groups. Working Paper.

Karlan, D., M. Mobius, T. Rosenblat, and A. Szeidl (2009). Trust and Social Collateral. Quarterly

Journal of Economics 124, 1307–1361.

Kling, J., J. Liebman, and L. Katz (2007). Experimental Analysis of Neighborhood Effects. Econo-

metrica 75, 83–119.

Knack, S. and P. Keefer (1997). Does Social Capital Have an Economic Payoff? A Cross-Country

Investigation. Quarterly Journal of Economics 112 (4), 1251–1288.

Kreps, D., P. Milgrom, J. Roberts, and R. Wilson (1982). Rational Cooperation in the Finitely

Repeated Prisoner’s Dilemma. Journal of Economic Theory 27, 245–52.

Larance, L. (2001). Fostering Social Capital Through NGO Design: Grameen Bank Membership in

Bangladesh. International Social Work 44.

Levitt, S. D. and J. A. List (2009). What Do Laboratory Experiments Measuring Social Preferences

Reveal About the Real World? Journal of Economic Perspectives 21 (2), 153–174.

Ligon, E. and L. Schecter (2008). The Value of Social Networks in Rural Paraguay. University of

Wisconsin Working Paper.

Manski, C. (1993). Identification of Endogenous Social Effects: The Reflection Problem. Review of

Economic Studies 60 (3), 531–542.

31

Manski, C. (2000). Economic Analysis of Social Interactions. Journal of Economic Perspec-

tives 14 (3), 115–136.

Miguel, E., P. Gertler, and David (2005). Does Social Capital Promote Industrialization? Evidence

from a Rapid Industrializer. Review of Economics and Statistics 87 (4), 754–762.

Narayan, D. and L. Pritchett (1999). Cents and Sociability: Household Income and Social Capital

in Rural Tanzania. Economic Development and Cultural Change 47 (4), 871–97.

Olken, B. (2009). Do Television and Radio Destroy Social Capital? Evidence from Indonesian

Villages. American Economic Journal: Applied Economics, forthcoming.

Putnam, R. (1993). Making Democracy Work: Civic Traditions in Modern Italy. Princeton, NJ:

Princeton University Press.

6 Appendix

6.1 VWS Protocol

Group Formation: The loan officer surveys the demographic make-up of a potential neighborhood.

If appropriate, then s/he conducts a meeting to inform potential clients about the VWS loan product

and invites them to a five-day Continuous Group Training (CGT) program. The program runs an

hour each day, and introduces clients to the benefits and responsibilities associated with the loan

product. Each potential loan group is assigned a separate CGT program. At the end of the CGT,

the loan officer forms women who were considered sufficiently informed and interested into a group,

identifies (with group members) a group leader and offers each member of the group a loan.37